Penunjuk Pine Script®

Cari dalam skrip untuk "bar"

The Last 5N Bars HLI made this script to watch the market on the timely manner.

Always set up per day and week.

- 1 hour chart 24, 4 hour chart 6, 15 min chart 96, etc

- Keep eyes on the similar bars on the same hour every day. As big players have regular working time every day.

- Labels ' position can show a trend

Penunjuk Pine Script®

Bollinger Bands Bar ColoringThis is a simple script that colors bars/candles based on where price is relative to the basis, and the upper and lower bands of the Bollinger Bands.

If price is above the basis, candles will be colored green, and if price is below the basis, candles will be colored red.

If price is outside of the bands on either side, the candles will be colored a darker shade of either color depending on if it is above or below.

I created this indicator because I like that at a glance I can have an idea of the bullishness or bearishness of price action based on the Bollinger Bands, without actually having the Bands overlayed on my charts.

It's also quite nice because I find that the areas where there is a shift in candle color (especially from green to red and vice versa) aid in identifying levels of support and resistance, and shifts in market structure.

I have another indicator that is a huge modification of the Bollinger Bands %B, which includes the candle coloring (and MAs), but this frees up space on my chart while still providing me with the primary information I'm looking for.

Penunjuk Pine Script®

Penunjuk Pine Script®

Penunjuk Pine Script®

Market Info Bar Charts - Was BoredSimple script in a form of a bar chart showing you some market information ;)

Penunjuk Pine Script®

Tick RenkoTick Renko, bars are formed on live chart.

note:there is a issue that creates artifacts while there is not enough history loaded.

Penunjuk Pine Script®

Combo Backtest 123 Percent change bar This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This histogram displays price or % change from previous bar.

WARNING:

- For purpose educate only

- This script to change bars colors.

Strategi Pine Script®

Combo Backtest 123 Reversal & N Bars Up This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Evaluates for n number of consecutive higher closes. Returns a value

of 1 when the condition is true or 0 when false.

WARNING:

- For purpose educate only

- This script to change bars colors.

Strategi Pine Script®

Combo Backtest 123 Reversal & N Bars Down This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Evaluates for n number of consecutive lower closes. Returns a value

of 1 when the condition is true or 0 when false.

WARNING:

- For purpose educate only

- This script to change bars colors.

Strategi Pine Script®

Penunjuk Pine Script®

Lyiness_Range-Bar-IdentificationRBI

The indicator shows you the range bar as a channel and automatically draws it on the chart. The indicator adapts automatically to each chart time.

Using the drawing tool, draw the channel from the 4-hour diagram into the chart and switch to the 15-minute diagram to see a breakout there.

this gives you the strongest resistance and the strongest support line in the chart

Penunjuk Pine Script®

low and high X Bars//This script finds High and Low X bars back. Simple pine script, can customize lookback period.

Penunjuk Pine Script®

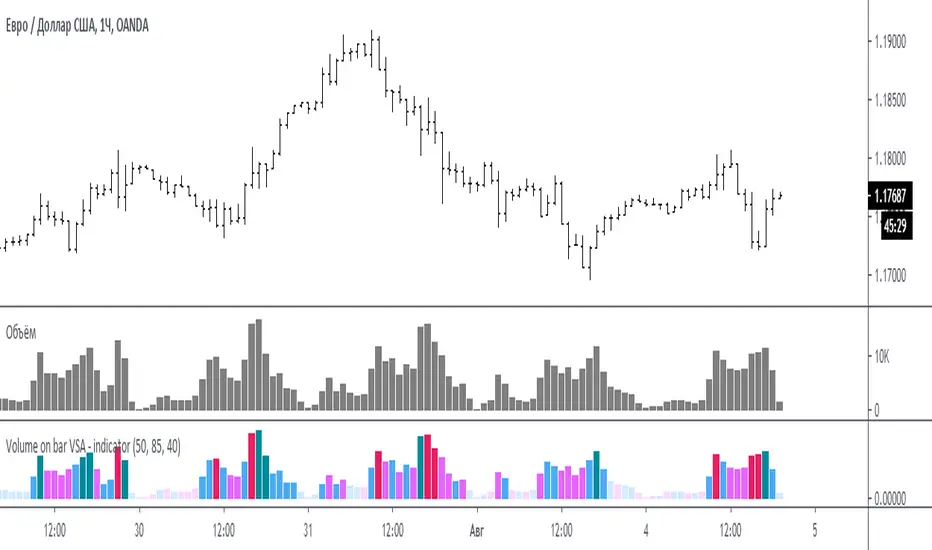

Volume on bar VSA - indicator V2Google translate.

This indicator compares the volume with its average value and tints it depending on whether the tail on the bar is bullish or bearish.

In the settings you can set (sensitivity) for tinting volumes of high and medium

Этот индикатор сравнивает объем со средним его значением и подкрашивает его в зависимости от того какой хвост на баре, бычий или медвежий.

В настройках можно задать (чувствительность) для подкрашивания объемов повышенных и средних

Penunjuk Pine Script®

Volume on bar VSA - indicatorЭтот индикатор сравнивает объем со средним его значением и подкрашивает его в зависимости от того какой хвост на баре, бычий или медвежий.

В настройках можно задать сигнальную линию (чувствительность) для подкрашивания объемов, если он превышает эту линию. (на графике красная линия)

Сигнальная линия задаётся в процентах от среднего объема за указанный период.

Серым цветом показан средний объем.

Google translate

This indicator compares the volume with its average value and tints it depending on which tail on the bar is bullish or bearish.

In the settings, you can set a signal line (sensitivity) for tinting volumes, if it exceeds this line. (red line on the chart)

The signal line is set as a percentage of the average volume for the specified period.

Gray indicates the average volume.

Penunjuk Pine Script®

ATR% The average true range / close price of previous barThe ATR% is an indicator to measure the increased volatility comparing with the past period.

1. Default is 14 bars, but we can switch to 21 or 7.

2. For the smoothing method, by default using simple moving average, but EMA, WMA and RMA is an option.

3. if over 1.5%, we consider the volatility increased significantly.

4. Combine ATR%, Stock screening (notional and volatility ) with 1-3 min chart, it's very easy to catch the sudden price movement for Japan Equities. hope you find it useful.

Penunjuk Pine Script®

Oscillator OB/OS BarsChoose between 3 different oscillators (RSI, MFI, and StochRSI) to show bars when the oscillator is oversold/overbought.

Green = oversold

Red = overbought

Orange = Bearish "Reversal"

Aqua = Bullish "Reversal"

I created this to help determine patterns with other stuff I'm building. Thought others may find it useful for the same purpose, not to trade based off of this.

Used those 3 oscillators cause their OB/OS levels are clear enough (though I put no effort into the stochrsi like I should've but welp)

enjoy zzzzzz

Penunjuk Pine Script®

EMA Bar ColoringHi,

This is a simple visualization because I wanted to use tradingview on the cellphone with less Lines and Easy to understand.

There are 4 moving averages for each level of the closing price, the color changes.

The Moving averages can be seen in the option tab.

Also the plot of the closing prices can also be seen.

It works better with bar charts.

Best Regards,

RERS

Penunjuk Pine Script®

Engulfing Signal Considering Three Bars BeforeIts a simple analysis using Candle Pattern Technique, Engulfing. The script will find the engulf candle by considering three bars before. For Bullish Engulfing it will be colored by yellow, and for Bearish will be white. I reccomend you for using this script in Daily Time Frame.

Enjoyyyy!!!

Penunjuk Pine Script®

How to detect last bar of day Simple way how to detect last bar of day and close all positions

UPD: day end can be different for yours because stocks market use another timezone

Penunjuk Pine Script®

Internal Bar Strength IndicatorThe Internal Bar Strength Indicator is pretty basic but very intuitive. Most stocks that close near their high of the day tend to fall the next day and stocks that close near their low tend to rise the next day. This indicator has very similar buy and sell signals as the RSI. Buy when the indicator rises above its signal or if the indicator is in the red zone and rises up outside of the red zone. Sell when the indicator falls below its signal or if the indicator is in the green zone and falls down outside of the green zone.

Let me know if you would like to see other indicators from me!

Penunjuk Pine Script®

GRAB or TrendStrength Bars with Highlights[Salty]GRAB or TrendStrength Bars with Propulsion Dots and Highlights for Squeeze Pro, CCI-Arrows, and SlowStoch

This indicator shows GRAB or TrendStrength candles and allows several moving averages to be displayed at the same time.

It has arrows and diamonds above or below the candles to show CCI values above 100 or below -100 with the arrow pointing in the direction of the momentum.

Diamonds indicate slightly weaker momentum than arrows, but still consider strong.

It has background coloring that is light green to show bullish trends and light red to show bearish trends that are derived from slow stochastics.

In general Darker colors are used for down moves and lighter colors are use to show up moves. Also, red indicates bearish, and green indicates bullish throughout.

It has yellow background to show squeezes with additional Squeeze Pro information shown at the bottom of the chart in the form of letters and momentum arrows.

L = Low compression squeeze, S = Normal Squeeze, and H = High Compression Squeeze.

It has a set of propulsion dots for each Moving Average. The trend is consider bullish when green colored dots print, and bearish when red dots print.

3 ATR Keltner channels are printed. The first two show the values used by the squeeze by default

2 Bolinger Bands are displayed based on the values used by the Squeeze by default.

1 VWAP line may be displayed.

TIP: overlaying the TICK symbol is great for confirming a bias where positive values are bullish and negative values are bearish.

Penunjuk Pine Script®

Highlight Last Bar of: D | W | M | Hour| H4 | MinutesSimple script highlighting a vertical line on the last bar of the Day/ Week/ Month/ Hour/ H4/ minute etc.

Helps maintain visibility of higher timeframes when on lower timeframes.

Quickly identify end of period levels.

Penunjuk Pine Script®