Dobrusky Pressure CoreWhat it does & who it’s for

Dobrusky Pressure Core is a volume by time replacement for traders who care about which side actually controls each bar. Instead of just plotting total volume, it splits each bar into estimated buy vs sell pressure and overlays a custom, session-aware volume baseline. It’s built for discretionary traders who want more nuanced volume context for entries, breakouts, and pullbacks.

Core ideas

Buy/sell pressure split: Each bar’s volume is broken into estimated buying and selling pressure.

Dominant side highlighting: The dominant side (buy or sell) is always displayed starting from the bottom of the bar, so you can quickly see who “owned” that bar.

Median-based baseline: Uses the median of the last N bars (50 by default) to build a robust volume baseline that’s less sensitive to one-off spikes.

Session-aware behavior: Baseline is calculated from Regular Trading Hours (RTH) by default, with an option to include Extended Hours (ETH) and a control to force Regular data on higher timeframes.

Volume regimes: Three multipliers (1x, 1.5x, 2x by default) show normal, high, and extreme volume regions.

Flexible display: Baseline can be shown as lines or as columns behind the volume, with full color customization.

How the pressure logic works

For each bar, the script:

Adjusts the range for gaps relative to the prior close so the “true” traded range is more consistent.

Computes buy pressure as a proportion of the adjusted range from low to close.

Defines sell pressure as: total volume minus buy pressure.

Marks the bar as buy-dominant if buy pressure ≥ sell pressure, otherwise sell-dominant, and colors the dominant side from the bottom to at least the midpoint using the selected buy/sell colors.

In practice, this turns basic volume columns into bars where the internal split and dominant side are clearly visible, helping you judge whether aggressive buyers or sellers truly controlled the bar instead of just looking at the price action.

Volume baseline & session logic

The script builds a session-aware baseline from recent volume:

Baseline length: A rolling window (default 50 bars) is used to compute a median volume value instead of a simple moving average.

RTH-only by default: By default, the baseline is built from Regular Trading Hours bars only. During extended hours, the baseline effectively “freezes” at the last RTH-derived value unless you choose to include extended session data.

Extended mode: If you select Extended mode, the script builds separate rolling baselines for RTH and ETH trading, using the appropriate one depending on the current session.

Force Regular Above Timeframe: On timeframes equal to or higher than your chosen threshold, the baseline automatically uses Regular session data, even if Extended is selected.

Multipliers: Three adjustable multipliers (1x, 1.5x, 2x by default) create normal, high, and extreme volume bands for quick identification.

This lets you choose whether you want a pure RTH reference or a baseline that adapts to extended-session activity.

Example ways to use it

1. Replace standard volume bars

Add Dobrusky Pressure Core to your volume pane and hide the default volume if you prefer a clean look.

Use the colors and split to see at a glance whether buyers or sellers were dominant on each bar.

2. Pressure confirmation for entries

For longs (example concept; adapt to your own rules):

Require that the entry bar’s buy pressure is greater than the previous bar’s sell pressure , or

If the entry and prior bar are both buy-dominant, require that the entry bar has more buy pressure than the prior bar.

This helps avoid taking a long when buying pressure is clearly fading relative to what sellers recently showed. A mirrored idea can be used for short setups with sell pressure.

3. Context from baseline multipliers

Use ~1x baseline as “normal” volume.

Watch for bars at or above 1.5x baseline when you want to see increased participation.

Treat 2x baseline and above as “extreme” volume zones that may mark climactic or especially important bars.

In practice, the baseline and multipliers are best used as context and filters, not as rigid rules.

Settings overview

Display

- Show Volume Baseline: toggle the baseline and its levels on or off.

- Baseline Display: choose between Line or Bars for the baseline visualization.

Baseline Calculation

- Length: lookback for the median baseline (default 50, configurable).

- Baseline Session Data: choose Regular or Extended to control which session data feeds the baseline.

Session Controls

- Regular Session (Local to TZ): define your RTH window (e.g., 0930-1600).

- Session Time Zone: choose the time zone used for that window.

- Force Regular Above Timeframe: on higher timeframes, force the baseline to use Regular session data only.

Baseline Levels

- Show Level x Multiplier 1/2/3: toggle each volume regime level.

- Multiplier 1/2/3: define what you consider normal, high, and extreme volume (defaults: 1.0, 1.5, 2.0).

Colors

- Buy Volume / Sell Volume: choose colors for buy and sell pressure.

- Baseline Bars (Base / x2 / x3): colors when the baseline is drawn as columns.

- Baseline Line (Base / x2 / x3): colors when the baseline is drawn as lines.

Limitations & best practices

This is a decision-support and visualization tool, not a buy/sell signal generator.

Best suited to markets where volume data is meaningful (e.g., index futures, liquid equities, liquid crypto).

The usefulness of any volume-based metric depends on the underlying data feed and instrument structure.

Always combine pressure and baseline context with your own strategy, risk management, and testing.

Originality

Most volume tools either show total volume only or compare it to a simple moving average. Dobrusky Pressure Core combines:

An intrabar buy/sell pressure split based on a gap-adjusted price range.

A median-based, configurable baseline built from session-specific data.

Session-aware behavior that keeps the baseline focused on Regular hours by default, with the option to incorporate Extended hours and force Regular data on higher timeframes.

The goal is to give traders a richer, session-aware view of participation and pressure that standard volume bars and simple SMA overlays don’t provide, while keeping everything transparent and open-source so users can review and adapt the logic.

Cari dalam skrip untuk "bar"

Range Trading StrategyOVERVIEW

The Range Trading Strategy is a systematic trading approach that identifies price ranges

from higher timeframe candles or trading sessions, tracks pivot points, and generates

trading signals when range extremes are mitigated and confirmed by pivot levels.

CORE CONCEPT

The strategy is based on the principle that when a candle (or session) closes within the

range of the previous candle (or session), that previous candle becomes a "range" with

identifiable high and low extremes. When price breaks through these extremes, it creates

trading opportunities that are confirmed by pivot levels.

RANGE DETECTION MODES

1. HTF (Higher Timeframe) Mode:

Automatically selects a higher timeframe based on the current chart timeframe

Uses request.security() to fetch HTF candle data

Range is created when an HTF candle closes within the previous HTF candle's range

The previous HTF candle's high and low become the range extremes

2. Sessions Mode:

- Divides the trading day into 4 sessions (UTC):

* Session 1: 00:00 - 06:00 (6 hours)

* Session 2: 06:00 - 12:00 (6 hours)

* Session 3: 12:00 - 20:00 (8 hours)

* Session 4: 20:00 - 00:00 (4 hours, spans midnight)

- Tracks high, low, and close for each session

- Range is created when a session closes within the previous session's range

- The previous session's high and low become the range extremes

PIVOT DETECTION

Pivots are detected based on candle color changes (bullish/bearish transitions):

1. Pivot Low:

Created when a bullish candle appears after a bearish candle

Pivot low = minimum of the current candle's low and previous candle's low

The pivot bar is the actual bar where the low was formed (current or previous bar)

2. Pivot High:

Created when a bearish candle appears after a bullish candle

Pivot high = maximum of the current candle's high and previous candle's high

The pivot bar is the actual bar where the high was formed (current or previous bar)

IMPORTANT: There is always only ONE active pivot high and ONE active pivot low at any

given time. When a new pivot is created, it replaces the previous one.

RANGE CREATION

A range is created when:

(HTF Mode) An HTF candle closes within the previous HTF candle's range AND a new HTF

candle has just started

(Sessions Mode) A session closes within the previous session's range AND a new session

has just started

Or Range Can Be Created when the Extreme of Another Range Gets Mitigated and We Have a Pivot low Just Above the Range Low or Pivot High just Below the Range High

Range Properties:

rangeHigh: The high extreme of the range

rangeLow: The low extreme of the range

highStartTime: The timestamp when the range high was actually formed (found by looping

backwards through bars)

lowStartTime: The timestamp when the range low was actually formed (found by looping

backwards through bars)

highMitigated / lowMitigated: Flags tracking whether each extreme has been broken

isSpecial: Flag indicating if this is a "special range" (see Special Ranges section)

RANGE MITIGATION

A range extreme is considered "mitigated" when price interacts with it:

High is mitigated when: high >= rangeHigh (any interaction at or above the level)

Low is mitigated when: low <= rangeLow (any interaction at or below the level)

Mitigation can happen:

At the moment of range creation (if price is already beyond the extreme)

At any point after range creation when price touches the extreme

SIGNAL GENERATION

1. Pending Signals:

When a range extreme is mitigated, a pending signal is created:

a) BEARISH Pending Signal:

- Triggered when: rangeHigh is mitigated

- Confirmation Level: Current pivotLow

- Signal is confirmed when: close < pivotLow

- Stop Loss: Current pivotHigh (at time of confirmation)

- Entry: Short position

Signal Confirmation

b) BULLISH Pending Signal:

- Triggered when: rangeLow is mitigated

- Confirmation Level: Current pivotHigh

- Signal is confirmed when: close > pivotHigh

- Stop Loss: Current pivotLow (at time of confirmation)

- Entry: Long position

IMPORTANT: There is only ever ONE pending bearish signal and ONE pending bullish signal

at any given time. When a new pending signal is created, it replaces the previous one

of the same type.

2. Signal Confirmation:

- Bearish: Confirmed when price closes below the pivot low (confirmation level)

- Bullish: Confirmed when price closes above the pivot high (confirmation level)

- Upon confirmation, a trade is entered immediately

- The confirmation line is drawn from the pivot bar to the confirmation bar

TRADE EXECUTION

When a signal is confirmed:

1. Position Management:

- Any existing position in the opposite direction is closed first

- Then the new position is entered

2. Stop Loss:

- Bearish (Short): Stop at pivotHigh

- Bullish (Long): Stop at pivotLow

3. Take Profit:

- Calculated using Risk:Reward Ratio (default 2:1)

- Risk = Distance from entry to stop loss

- Target = Entry ± (Risk × R:R Ratio)

- Can be disabled with "Stop Loss Only" toggle

4. Trade Comments:

- "Range Bear" for short trades

- "Range Bull" for long trades

SPECIAL RANGES

Special ranges are created when:

- A range high is mitigated AND the current pivotHigh is below the range high

- A range low is mitigated AND the current pivotLow is above the range low

In these cases:

- The pivot value is stored in an array (storedPivotHighs or storedPivotLows)

- A "special range" is created with only ONE extreme:

* If pivotHigh < rangeHigh: Creates a range with rangeHigh = pivotLow, rangeLow = na

* If pivotLow > rangeLow: Creates a range with rangeLow = pivotHigh, rangeHigh = na

- Special ranges can generate signals just like normal ranges

- If a special range is mitigated on the creation bar or the next bar, it is removed

entirely without generating signals (prevents false signals)

Special Ranges

REVERSE ON STOP LOSS

When enabled, if a stop loss is hit, the strategy automatically opens a trade in the

opposite direction:

1. Long Stop Loss Hit:

- Detects when: position_size > 0 AND position_size <= 0 AND low <= longStopLoss

- Action: Opens a SHORT position

- Stop Loss: Current pivotHigh

- Trade Comment: "Reverse on Stop"

2. Short Stop Loss Hit:

- Detects when: position_size < 0 AND position_size >= 0 AND high >= shortStopLoss

- Action: Opens a LONG position

- Stop Loss: Current pivotLow

- Trade Comment: "Reverse on Stop"

The reverse trade uses the same R:R ratio and respects the "Stop Loss Only" setting.

VISUAL ELEMENTS

1. Range Lines:

- Drawn from the time when the extreme was formed to the mitigation point (or current

time if not mitigated)

- High lines: Blue (or mitigated color if mitigated)

- Low lines: Red (or mitigated color if mitigated)

- Style: SOLID

- Width: 1

2. Confirmation Lines:

- Drawn when a signal is confirmed

- Extends from the pivot bar to the confirmation bar

- Bearish: Red, solid line

- Bullish: Green, solid line

- Width: 1

- Can be toggled on/off

STRATEGY SETTINGS

1. Range Detection Mode:

- HTF: Uses higher timeframe candles

- Sessions: Uses trading session boundaries

2. Auto HTF:

- Automatically selects HTF based on current chart timeframe

- Can be disabled to use manual HTF selection

3. Risk:Reward Ratio:

- Default: 2.0 (2:1)

- Minimum: 0.5

- Step: 0.5

4. Stop Loss Only:

- When enabled: Trades only have stop loss (no take profit)

- Trades close on stop loss or when opposite signal confirms

5. Reverse on Stop Loss:

- When enabled: Hitting a stop loss opens opposite trade with stop at opposing pivot

6. Max Ranges to Display:

- Limits the number of ranges kept in memory

- Oldest ranges are purged when limit is exceeded

KEY FEATURES

1. Dynamic Pivot Tracking:

- Pivots update on every candle color change

- Always maintains one high and one low pivot

2. Range Lifecycle:

- Ranges are created when price closes within previous range

- Ranges are tracked until mitigated

- Mitigation creates pending signals

- Signals are confirmed by pivot levels

3. Signal Priority:

- Only one pending signal of each type at a time

- New signals replace old ones

- Confirmation happens on close of bar

4. Position Management:

- Closes opposite positions before entering new trades

- Tracks stop loss levels for reverse functionality

- Respects pyramiding = 1 (only one position per direction)

5. Time-Based Drawing:

- Uses time coordinates instead of bar indices for line drawing

- Prevents "too far from current bar" errors

- Lines can extend to any historical point

USAGE NOTES

- Best suited for trending and ranging markets

- Works on any timeframe, but HTF mode adapts automatically

- Sessions mode is ideal for intraday trading

- Pivot detection requires clear candle color changes

- Range detection requires price to close within previous range

- Signals are generated on bar close, not intra-bar

The strategy combines range identification, pivot tracking, and signal confirmation to

create a systematic approach to trading breakouts and reversals based on price structure, past performance does not in any way predict future performance

TheStrat: Failed 2 + 2 ConfirmationTheStrat: Failed-2 + 2 Confirmation (2-2 option)

This indicator spots a classic Strat “failed 2 → 2” sequence on consecutive bars, and fires alerts only when both conditions are met:

Failed-2 bar on the prior candle

Failed 2-Down (F2D): Took the prior low but closed green

Failed 2-Up (F2U): Took the prior high but closed red

By default this is strict (excludes outside bars/3’s). You can toggle to allow 3’s if you prefer a looser definition.

Current bar is a clean “2”

2U = broke prior high only; 2D = broke prior low only (excludes 3’s).

Optional: Require flip so the second bar must reverse direction (F2D→2U for longs, F2U→2D for shorts). Turn this off if you want any 2 after a Failed-2.

What gets plotted

Tiny markers on each Failed-2 as they occur (F2U/F2D).

A label when the combo confirms on the next bar:

Bullish: F2D→2U (or F2D→2 if flip is off) below the bar

Bearish: F2U→2D (or F2U→2) above the bar

Alerts (set from the “Add Alert” dialog)

Failed2 + 2 (Bull): Prior bar was F2D; current bar is a 2 (flip optional).

Failed2 + 2 (Bear): Prior bar was F2U; current bar is a 2 (flip optional).

Inputs

Colors for Failed-2 markers and combo labels

Require flip (on by default) → focuses on true 2-2 reversals

Count outside bars (3) as Failed-2? (off by default) → stricter = fewer, cleaner signals

How to trade it (typical Strat style)

Bullish combo (F2D→2U): Entry on break of the combo bar’s high; risk under its low (or under the prior bar).

Bearish combo (F2U→2D): Entry on break of the combo bar’s low; risk above its high.

First target = prior pivot (“magnitude”), then nearby pivots/BF levels. Improve odds by aligning with time-frame continuity (e.g., day/week in your direction).

Notes / Best practices

Uses barstate.isconfirmed → signals/labels are based on closed bars to avoid repaint.

If you see too many Failed-2 tags, keep outside-bar counting OFF (strict mode).

ALISH WEEK LABELS THE ALISH WEEK LABELS

Overview

This indicator programmatically delineates each trading week and encapsulates its realized price range in a live-updating, filled rectangle. A week is defined in America/Toronto time from Monday 00:00 to Friday 16:00. Weekly market open to market close, For every week, the script draws:

a vertical start line at the first bar of Monday 00:00,

a vertical end line at the first bar at/after Friday 16:00, and

a white, semi-transparent box whose top tracks the highest price and whose bottom tracks the lowest price observed between those two temporal boundaries.

The drawing is timeframe-agnostic (M1 → 1D): the box expands in real time while the week is open and freezes at the close boundary.

Time Reference and Session Boundaries

All scheduling decisions are computed with time functions called using the fixed timezone string "America/Toronto", ensuring correct behavior across DST transitions without relying on chart timezone. The start condition is met at the first bar where (dayofweek == Monday && hour == 0 && minute == 0); on higher timeframes where an exact 00:00 bar may not exist, a fallback checks for the first Monday bar using ta.change(dayofweek). The close condition is met on the first bar at or after Friday 16:00 (Toronto), which guarantees deterministic closure on intraday and higher timeframes.

State Model

The indicator maintains minimal persistent state using var globals:

week_open (bool): whether the current weekly session is active.

wk_hi / wk_lo (float): rolling extrema for the active week.

wk_box (box): the graphical rectangle spanning × .

wk_start_line and a transient wk_end_line (line): vertical delimiters at the week’s start and end.

Two dynamic arrays (boxes, vlines) store object handles to support bounded history and deterministic garbage collection.

Update Cycle (Per Bar)

On each bar the script executes the following pipeline:

Start Check: If no week is open and the start condition is satisfied, instantiate wk_box anchored at the current bar_index, prime wk_hi/wk_lo with the bar’s high/low, create the start line, and push both handles to their arrays.

Accrual (while week_open): Update wk_hi/wk_lo using math.max/min with current bar extremes. Propagate those values to the active wk_box via box.set_top/bottom and slide box.set_right to the current bar_index to keep the box flush with live price.

Close Check: If at/after Friday 16:00, finalize the week by freezing the right edge (box.set_right), drawing the end line, pushing its handle, and flipping week_open false.

Retention Pruning: Enforce a hard cap on historical elements by deleting the oldest objects when counts exceed configured limits.

Drawing Semantics

The range container is a filled white rectangle (bgcolor = color.new(color.white, 100 − opacity)), with a solid white border for clear contrast on dark or light themes. Start/end boundaries are full-height vertical white lines (y1=+1e10, y2=−1e10) to guarantee visibility across auto-scaled y-axes. This approach avoids reliance on price-dependent anchors for the lines and is robust to large volatility spikes.

Multi-Timeframe Behavior

Because session logic is driven by wall-clock time in the Toronto zone, the indicator remains consistent across chart resolutions. On coarse timeframes where an exact boundary bar might not exist, the script legally approximates by triggering on the first available bar within or immediately after the boundary (e.g., Friday 16:00 occurs between two 4-hour bars). The box therefore represents the true realized high/low of the bars present in that timeframe, which is the correct visual for that resolution.

Inputs and Defaults

Weeks to keep (show_weeks_back): integer, default 40. Controls retention of historical boxes/lines to avoid UI clutter and resource overhead.

Fill opacity (fill_opacity): integer 0–100, default 88. Controls how solid the white fill appears; border color is fixed pure white for crisp edges.

Time zone is intentionally fixed to "America/Toronto" to match the strategy definition and maintain consistent historical backtesting.

Performance and Limits

Objects are reused only within a week; upon closure, handles are stored and later purged when history limits are exceeded. The script sets generous but safe caps (max_boxes_count/max_lines_count) to accommodate 40 weeks while preserving Editor constraints. Per-bar work is O(1), and pruning loops are bounded by the configured history length, keeping runtime predictable on long histories.

Edge Cases and Guarantees

DST Transitions: Using a fixed IANA time zone ensures Friday 16:00 and Monday 00:00 boundaries shift correctly when DST changes in Toronto.

Weekend Gaps/Holidays: If the market lacks bars exactly at boundaries, the nearest subsequent bar triggers the start/close logic; range statistics still reflect observed prices.

Live vs Historical: During live sessions the box edge advances every bar; when replaying history or backtesting, the same rules apply deterministically.

Scope (Intentional Simplicity)

This tool is strictly a visual framing indicator. It does not compute labels, statistics, alerts, or extended S/R projections. Its single responsibility is to clearly present the week’s realized range in the Toronto session window so you can layer your own execution or analytics on top.

🚀 Ultimate Trading Tool + Strat Method🚀 Ultimate Trading Tool + Strat Method - Complete Breakdown

Let me give you a comprehensive overview of this powerful indicator!

🎯 What This Indicator Does:

This is a professional-grade, all-in-one trading system that combines two proven methodologies:

1️⃣ Technical Analysis System (Original)

Advanced trend detection using multiple EMAs

Momentum analysis with MACD

RSI multi-timeframe analysis

Volume surge detection

Automated trendline drawing

2️⃣ Strat Method (Pattern Recognition)

Inside bars, outside bars, directional bars

Classic patterns: 2-2, 1-2-2

Advanced patterns: 3-1-2, 2-1-2, F2→3

Timeframe continuity filters

📊 How It Generates Signals:

Technical Analysis Signals (Green/Red Triangles):

Buy Signal Triggers When:

✅ Price above EMA 21 & 50 (uptrend)

✅ MACD histogram rising (momentum)

✅ RSI between 30-70 (not overbought/oversold)

✅ Volume surge above 20-period average

✅ Price breaks above resistance trendline

Scoring System:

Trend alignment: +1 point

Momentum: +1 point

RSI favorable: +1 point

Trendline breakout: +2 points

Minimum score required based on sensitivity setting

Strat Method Signals (Blue/Orange Labels):

Pattern Recognition:

2-2 Setup: Down bar → Up bar (or reverse)

1-2-2 Setup: Inside bar → Down bar → Up bar

3-1-2 Setup: Outside bar → Inside bar → Up bar

2-1-2 Setup: Down bar → Inside bar → Up bar

F2→3 Setup: Failed directional bar becomes outside bar

Confirmation Required:

Must break previous bar's high (buy) or low (sell)

Optional timeframe continuity (daily & weekly aligned)

💰 Risk Management Features:

Dynamic Stop Loss & Take Profit:

ATR-Based: Adapts to market volatility

Stop Loss: Entry - (ATR × 1.5) by default

Take Profit: Entry + (ATR × 3.0) by default

Risk:Reward: Customizable 1:2 to 1:5 ratios

Visual Risk Zones:

Colored boxes show risk/reward area

Dark, bold lines for easy identification

Clear entry, stop, and target levels

🎨 What You See On Screen:

Main Signals:

🟢 Green Triangle "BUY" - Technical analysis long signal

🔴 Red Triangle "SELL" - Technical analysis short signal

🎯 Blue Label "STRAT" - Strat method long signal

🎯 Orange Label "STRAT" - Strat method short signal

Trendlines:

Green lines - Support trendlines (bullish)

Red lines - Resistance trendlines (bearish)

Automatically drawn from pivot points

Extended forward to predict future levels

Stop/Target Levels:

Bold crosses at stop loss levels (red color)

Bold crosses at take profit levels (green color)

Line width = 3 for maximum visibility

Trade Zones:

Light green boxes - Long trade risk/reward zone

Light red boxes - Short trade risk/reward zone

Shows potential profit vs risk visually

📊 Information Dashboard (Top Right):

Shows real-time market conditions:

Main Signal: Current technical signal status

Strat Method: Active Strat pattern

Trend: Bullish/Bearish/Neutral

Momentum: Strong/Weak based on MACD

Volume: High/Normal compared to average

TF Continuity: Daily/Weekly alignment

RSI: Current RSI value with color coding

Support/Resistance: Current trendline levels

🔔 Alert System:

Entry Alerts:

Technical Signals:

🚀 BUY SIGNAL TRIGGERED!

Type: Technical Analysis

Entry: 45.23

Stop: 43.87

Target: 48.95

```

**Strat Signals:**

```

🎯 STRAT BUY TRIGGER!

Pattern: 3-1-2

Entry: 45.23

Trigger Level: 44.56

Exit Alerts:

Target hit notifications

Stop loss hit warnings

Helps maintain discipline

⚙️ Customization Options:

Signal Settings:

Sensitivity: High/Medium/Low (controls how many signals)

Volume Filter: Require volume surge or not

Momentum Filter: Require momentum confirmation

Strat Settings:

TF Continuity: Require daily/weekly alignment

Pattern Selection: Enable/disable specific patterns

Confirmation Mode: Show only confirmed triggers

Risk Settings:

ATR Multiplier: Adjust stop/target distance

Risk:Reward: Set preferred ratio

Visual Elements: Show/hide any component

Visual Settings:

Colors: Customize all signal colors

Display Options: Toggle signals, levels, zones

Trendline Length: Adjust pivot detection period

🎯 Best Use Cases:

Day Trading:

Use low sensitivity setting

Enable all Strat patterns

Watch for high volume signals

Quick in/out trades

Swing Trading:

Use medium sensitivity

Require timeframe continuity

Focus on trendline breakouts

Hold for target levels

Position Trading:

Use high sensitivity (fewer signals)

Require strong momentum

Focus on weekly/daily alignment

Larger ATR multipliers

💡 Trading Strategy Tips:

High-Probability Setups:

Double Confirmation: Technical + Strat signal together

Trend Alignment: All timeframes agree

Volume Surge: Institutional participation

Trendline Break: Clear level breakout

Risk Management:

Always use stops - System provides them

Position sizing - Risk 1-2% per trade

Don't chase - Wait for signal confirmation

Take profits - System provides targets

What Makes Signals Strong:

✅ Both technical AND Strat signals fire together

✅ Timeframe continuity (daily & weekly aligned)

✅ Volume surge confirms institutional interest

✅ Multiple indicators align (trend + momentum + RSI)

✅ Clean trendline breakout with no resistance above (or support below)

⚠️ Common Mistakes to Avoid:

Don't ignore stops - System calculates them for a reason

Don't overtrade - Wait for quality setups

Don't disable volume filter - Unless you know what you're doing

Don't use max sensitivity - You'll get too many signals

Don't ignore timeframe continuity - It filters bad trades

🚀 Why This Indicator is Powerful:

Combines Multiple Edge Sources:

Technical analysis (trend, momentum, volume)

Pattern recognition (Strat method)

Risk management (dynamic stops/targets)

Market structure (trendlines, support/resistance)

Professional Features:

No repainting - signals are final when bar closes

Clear risk/reward before entry

Multiple confirmation layers

Adaptable to any market or timeframe

Beginner Friendly:

Clear visual signals

Automatic calculations

Built-in risk management

Comprehensive dashboard

This indicator essentially gives you everything a professional trader uses - trend analysis, momentum, patterns, volume, risk management - all in one clean package!

Any specific aspect you'd like me to explain in more detail? 🎯RetryClaude can make mistakes. Please double-check responses. Sonnet 4.5

Moving Averages PowerMoving Averages Power — Trend + Normalized Strength

Lightweight indicator that plots up to 15 SMAs (5 → 4320) and shows a compact table with each MA’s:

Slope % (per-bar)

Trend (Bullish/Bearish/Neutral)

Normalized “Strength” bars comparable across MA lengths and, optionally, across timeframes via ATR%

Not financial advice. For research/education only.

What it does

Plots 15 SMA lines on the price chart

Colors match trend: Bullish (green), Bearish (red), Neutral (gray)

Bottom-right table: MA, Slope %, Trend, Strength bars

Strength normalization modes:

None: raw |slope%|

Length: scales by length relative to a reference length

ATR%: scales by volatility (ATR as % of price)

Length+ATR%: combines both for better cross-timeframe comparability

How it works (concepts)

Slope % per bar: 100 × (MA − MA ) / MA

Normalization:

None: S = |slope%|

Length: S = |slope%| × (length / normRefLen)

ATR%: S = |slope%| / ATR%, where ATR% = 100 × ATR(atrLen) / close

Length+ATR%: S = (|slope%| × (length / normRefLen)) / ATR%

Bars: floor(S / strengthStep), clamped to Max bars (default 10)

Notes:

normRefLen (default 240) keeps Length scaling stable across very short and very long MAs

In ATR modes, Strength shows blank until there’s enough history for ATR

How to use

Add the indicator to your chart (Indicators → search this title → Add).

Open Settings:

Show/hide any of the 15 SMAs

Choose Strength normalization mode

Tune Strength step, Max bars, Reference length, and ATR Length

Read the table:

MA: period

Slope %: per-bar percent change of the MA

Trend: green (bullish), red (bearish), gray (neutral)

Strength: more bars = stronger trend under the chosen normalization

Inputs (quick reference)

Display:

15 toggles: Show SMA 5 … Show SMA 4320

Strength Settings:

Strength normalization: None | Length | ATR% | Length+ATR%

Strength step (normalized units): sensitivity of bar count

Max bars: clamp for the bar count (default 10)

Normalization reference length: baseline for Length scaling (default 240)

ATR Length (for ATR%): ATR lookback used for ATR%

Text:

Label font size, Table font size

Line + label colors

Bullish (slope > 0): green

Bearish (slope < 0): red

Neutral (otherwise): gray

The MA lines, end-of-series labels, and table trend cell use the same colors

Recommended presets (examples)

Intraday (e.g., BTCUSD, 1h):

Strength normalization: Length+ATR%

normRefLen: 240

Strength step: 0.02–0.05

Max bars: 10

ATR Length: 14

Daily (e.g., AAPL, 1D):

Strength normalization: Length

normRefLen: 240–480

Strength step: 0.01–0.03

Max bars: 10

Calibration tips

Bars often at max (pegged)?

Increase Strength step (e.g., 0.01 → 0.03 → 0.05)

Or increase normRefLen (e.g., 240 → 480 → 720)

Bars too few?

Decrease Strength step (e.g., 0.02 → 0.01 → 0.005)

Or decrease normRefLen (e.g., 240 → 120)

Cross-timeframe comparability:

Prefer Length+ATR%; start with Strength step ≈ 0.02–0.05 and tune

Limitations

SMA only (no EMA/WMA/etc.)

Per-bar slope is inherently timeframe-sensitive; use ATR% or Length+ATR% for better cross-timeframe comparisons

ATR modes require atrLen bars; Strength shows blank until ready

The longest SMA (4320) needs sufficient chart history

Troubleshooting

Strength always looks maxed:

You might be on Length mode with a very small step; increase Strength step and/or use Length+ATR%; review normRefLen

Strength blank cells:

In ATR modes, wait for enough history (atrLen) or switch to Length mode

Table bounds:

The script manages rows internally; if you customize periods, ensure the total rows fit the 4×16 table

Compatibility

Pine Script v6

Works on most symbols/timeframes with adequate history

If you find this useful, consider leaving feedback with your preferred defaults (symbol/timeframe) so I can provide better presets.

HTF Cross Breakout [CHE] HTF Cross Breakout — Detects higher timeframe close crossovers for breakout signals, anchors VWAP for trend validation, and flags continuations or traps with visual extensions for delta percent and stop levels.

Summary

This indicator spots moments when the current chart's close price crosses a higher timeframe close, marking potential breakouts only when the current bar shows directional strength. It anchors a volume-weighted average price line from the breakout point to track trend health, updating labels to show if the move continues or reverses into a trap. Extensions add a dotted line linking the breakout level to the current close with percent change display, plus a stop-loss marker at the VWAP end. Signals gain robustness from higher timeframe confirmation and anti-repainting options, reducing noise in live bars compared to simple crossover tools.

Motivation: Why this design?

Traders often face false breakouts from intrabar wiggles on lower timeframes, especially without higher timeframe alignment, leading to whipsaws in volatile sessions. This design uses higher timeframe close as a stable reference for crossover detection, combined with anchored volume weighting to gauge sustained momentum. It addresses these by enforcing bar confirmation and directional filters, providing clearer entry validation and risk points without overcomplicating the chart.

What’s different vs. standard approaches?

Reference baseline

Standard crossover indicators like moving average crosses operate solely on the chart timeframe, ignoring higher timeframe context and lacking volume anchoring.

Architecture differences

- Higher timeframe data pulls via security calls with optional repainting control for stability.

- Anchored VWAP resets at each signal, accumulating from the breakout bar only.

- Label dynamics update in real-time for continuation checks, with extensions for visual delta and stop computation.

- Event-driven line finalization prunes old elements after a set bar extension.

Practical effect

Charts show persistent lines and labels that extend live but finalize cleanly on new events, avoiding clutter. This matters for spotting trap reversals early via label color shifts, and extensions provide quick risk visuals without manual calculations, improving decision speed in trend trades.

How it works (technical)

The indicator first determines a higher timeframe based on user selection, pulling its close price securely. It checks for crossovers or crossunders of the current close against this higher close, but only triggers on confirmed bars with matching directional opens and closes. On a valid event, a horizontal line and label mark the higher close level, while a dashed VWAP line starts accumulating typical price times volume from that bar onward. During the active phase, the breakout line extends to the current bar, the label repositions and updates text based on whether the current close holds above or below the level for bulls or bears. A background tint warns if the close deviates adversely from the current VWAP. Extensions draw a vertical dotted line at the last bar between the breakout level and close, placing a midpoint label with percent difference; separately, a label at the VWAP end shows a computed stop price. Persistent variables track the active state and accumulators, resetting on new events after briefly extending old elements. Repaint risk from security calls is mitigated by confirmed bar gating or user opt-in.

Parameter Guide

Plateau Length (reserved for future, currently unused): Sets a length for potential plateau detection in extensions; default 3, minimum 1. Higher values would increase stability but are not active yet—leave at default to avoid tuning.

Line Width: Controls thickness of breakout, VWAP, and extension lines; default 2, range 1 to 5. Thicker lines improve visibility on busy charts but may obscure price action—use 1 for clean views, 3 or more for emphasis.

+Bars after next HTF event (finalize old, then delete): Extends old lines and labels by this many bars before deletion on new signals; default 20, minimum 0. Shorter extensions keep charts tidy but risk cutting visuals prematurely; longer aids review but builds clutter over time.

Evaluate label only on HTF close (prevents gray traps intrabar): When true, label updates wait for higher timeframe confirmation; default true. Enabling reduces intrabar flips for stabler signals, though it may delay feedback—disable for faster live trading at repaint cost.

Allow Repainting: Permits real-time security data without confirmation offset; default false. False ensures historical accuracy but lags live bars; true speeds updates but can repaint on HTF closes.

Timeframe Type: Chooses HTF method—Auto Timeframe (dynamic steps up), Multiplier (chart multiple), or Manual (fixed string); default Auto Timeframe. Auto adapts to chart scale for convenience; Multiplier suits custom scaling like 5 times current; Manual for precise like 1D on any chart.

Multiplier for Alternate Resolution: Scales chart timeframe when Multiplier type selected; default 5, minimum 1. Values near 1 mimic current resolution for subtle shifts; higher like 10 jumps to broader context, increasing signal rarity.

Manual Resolution: Direct timeframe string like 60 for 1H when Manual type; default 60. Match to trading horizon—shorter for swing, longer for positional—to balance frequency and reliability.

Show Extension 1: Toggles dotted line and delta percent label between breakout level and current close; default true. Disable to simplify for basic use, enable for precise momentum tracking.

Dotted Line Width: Thickness for Extension 1 line; default 2, range 1 to 5. Align with main Line Width for consistency.

Text Size: Size for delta percent label; options tiny, small, normal, large; default normal. Smaller reduces overlap on dense charts; larger aids glance reads.

Decimals for Δ%: Precision in percent change display; default 2, range 0 to 6. Fewer decimals speed reading; more suit low-volatility assets.

Positive Δ Color: Hue for upward percent changes; default lime. Choose contrasting for visibility.

Negative Δ Color: Hue for downward percent changes; default red. Pair with positive for quick polarity scan.

Dotted Line Color: Color for Extension 1 line; default gray. Neutral tones blend well; brighter for emphasis.

Background Transparency (0..100): Opacity for delta label background; default 90. Higher values fade for subtlety; lower solidifies for readability.

Show Extension 2: Toggles stop-loss label at VWAP end; default true. Turn off for entry focus only.

Stop Method: Percent from VWAP end or fixed ticks; options Percent, Ticks; default Percent. Percent scales with price levels; Ticks suits tick-based instruments.

Stop %: Distance as fraction of VWAP for Percent method; default 1.0, step 0.05, minimum 0.0. Tighter like 0.5 reduces risk but increases stops; wider like 2.0 allows breathing room.

Stop Ticks: Tick count offset for Ticks method; default 20, minimum 0. Adjust per asset volatility—fewer for tight control.

Price Decimals: Rounding for stop price text; default 4, range 0 to 10. Match syminfo.precision for clean display.

Text Size: Size for stop label; options tiny, small, normal, large; default normal. Scale to chart zoom.

Text Color: Foreground for stop text; default white. Ensure contrast with background.

Inherit VWAP Color (BG tint): Bases stop label background on VWAP hue; default true. True maintains theme; false allows custom black base.

BG Transparency (0..100): Opacity for stop label background; default 0. Zero for no tint; up to 100 for full fade.

Reading & Interpretation

Breakout lines appear green for bullish crosses or red for bearish, extending live until a new event finalizes them briefly then deletes. Labels start blank, updating to Bull Cont. or Bear Cont. in matching colors if holding the level, or gray Bull Trap/Bear Trap on reversal. VWAP dashes yellow for bulls, orange for bears, sloping with accumulated volume weight—deviations trigger faint red background warnings. Extension 1's dotted vertical shows at the last bar, with midpoint label green/red for positive/negative percent from breakout to close. Extension 2 places a left-aligned label at VWAP end with stop price and method note, tinted to VWAP for context.

Practical Workflows & Combinations

For trend following, enter long on green Bull Cont. labels above VWAP with higher highs confirmation, filtering via rising structure; short on red Bear Cont. below. Pair with volume surges or RSI above 50 for bulls to avoid traps. For exits, trail stops using the Extension 2 level, tightening on warnings or gray labels—aggressive on continuations, conservative post-trap. In multi-timeframe setups, use default Auto on 15m charts for 1H signals, scaling multiplier to 4 for daily context on hourly; test on forex/stocks where volume is reliable, avoiding low-liquidity assets.

Behavior, Constraints & Performance

Signals confirm on bar close with HTF gating when strict mode active, but live bars may update if repainting enabled—opt false for backtest fidelity, true for intraday speed. Security calls risk minor repaints on HTF closes, mitigated by confirmation offsets. Resources cap at 1000 bars back, 50 lines/labels total, with event prunes to stay under budgets—no loops, minimal arrays. Limits include VWAP lag in low-volume periods and dependency on accurate HTF data; gaps or holidays may skew anchors.

Sensible Defaults & Quick Tuning

Defaults suit 5m-1H charts on liquid assets: Auto HTF, no repaint, 1% stops. For choppy markets with excess signals, enable strict eval and bump multiplier to 10 for rarer triggers. If sluggish in trends, shorten extend bars to 10 and allow repainting for quicker visuals. On high-vol like crypto, widen stop % to 2.0 and use Ticks method; for stables like indices, tighten to 0.5% and keep Percent.

What this indicator is—and isn’t

This is a signal visualization layer for breakout confirmation and basic risk marking, best as a filter in discretionary setups. It isn’t a standalone system or predictive oracle—combine with price structure, news awareness, and sizing rules for real edges.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

BOCS Channel Scalper Indicator - Mean Reversion Alert System# BOCS Channel Scalper Indicator - Mean Reversion Alert System

## WHAT THIS INDICATOR DOES:

This is a mean reversion trading indicator that identifies consolidation channels through volatility analysis and generates alert signals when price enters entry zones near channel boundaries. **This indicator version is designed for manual trading with comprehensive alert functionality.** Unlike automated strategies, this tool sends notifications (via popup, email, SMS, or webhook) when trading opportunities occur, allowing you to manually review and execute trades. The system assumes price will revert to the channel mean, identifying scalp opportunities as price reaches extremes and preparing to bounce back toward center.

## INDICATOR VS STRATEGY - KEY DISTINCTION:

**This is an INDICATOR with alerts, not an automated strategy.** It does not execute trades automatically. Instead, it:

- Displays visual signals on your chart when entry conditions are met

- Sends customizable alerts to your device/email when opportunities arise

- Shows TP/SL levels for reference but does not place orders

- Requires you to manually enter and exit positions based on signals

- Works with all TradingView subscription levels (alerts included on all plans)

**For automated trading with backtesting**, use the strategy version. For manual control with notifications, use this indicator version.

## ALERT CAPABILITIES:

This indicator includes four distinct alert conditions that can be configured independently:

**1. New Channel Formation Alert**

- Triggers when a fresh BOCS channel is identified

- Message: "New BOCS channel formed - potential scalp setup ready"

- Use this to prepare for upcoming trading opportunities

**2. Long Scalp Entry Alert**

- Fires when price touches the long entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "LONG scalp signal at 24731.75 | TP: 24743.2 | SL: 24716.5"

**3. Short Scalp Entry Alert**

- Fires when price touches the short entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "SHORT scalp signal at 24747.50 | TP: 24735.0 | SL: 24762.75"

**4. Any Entry Signal Alert**

- Combined alert for both long and short entries

- Use this if you want a single alert stream for all opportunities

- Message: "BOCS Scalp Entry: at "

**Setting Up Alerts:**

1. Add indicator to chart and configure settings

2. Click the Alert (⏰) button in TradingView toolbar

3. Select "BOCS Channel Scalper" from condition dropdown

4. Choose desired alert type (Long, Short, Any, or Channel Formation)

5. Set "Once Per Bar Close" to avoid false signals during bar formation

6. Configure delivery method (popup, email, webhook for automation platforms)

7. Save alert - it will fire automatically when conditions are met

**Alert Message Placeholders:**

Alerts use TradingView's dynamic placeholder system:

- {{ticker}} = Symbol name (e.g., NQ1!)

- {{close}} = Current price at signal

- {{plot_1}} = Calculated take profit level

- {{plot_2}} = Calculated stop loss level

These placeholders populate automatically, creating detailed notification messages without manual configuration.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This indicator is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Indicator**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the indicator ideal for active day traders who want continuous alert opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased signal frequency also means higher potential commission costs and requires disciplined trade selection when acting on alerts.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The indicator normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The indicator uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The indicator tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The indicator uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. Visual markers (arrows and labels) appear on chart, and configured alerts fire immediately.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents alert spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long alert will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The indicator includes a multi-timeframe ATR filter to avoid alerts during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while viewing 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Alerts enabled

- If ATR < threshold: No alerts fire

This prevents notifications during dead zones where mean reversion is unreliable due to insufficient price movement. The ATR status is displayed in the info table with visual confirmation (✓ or ✗).

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. These levels are displayed as visual lines with labels and included in alert messages for reference when manually placing orders.

### Stop Loss Placement:

Stop losses are calculated just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. SL levels are displayed on chart and included in alert notifications as suggested stop placement.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

## INPUT PARAMETERS:

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long alert generation on/off

- **Enable Short Scalps**: Toggle short alert generation on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between alerts (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for alert enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time indicator status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Long Color**: Customize long signal color (default: darker green for readability)

- **Short Color**: Customize short signal color (default: red)

- **TP/SL Colors**: Customize take profit and stop loss line colors

- **Line Length**: Visual length of TP/SL reference lines (5-200 bars)

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short alerts

- **TP/SL reference lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing channel status, last signal, entry/TP/SL prices, risk/reward ratio, and ATR filter status

- **Visual confirmation** when alerts fire via on-chart markers synchronized with notifications

## HOW TO USE:

### For 1-3 Minute Scalping with Alerts (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars to reduce alert spam

- **Alert Setup**: Configure "Any Entry Signal" for combined long/short notifications

- **Execution**: When alert fires, verify chart visuals, then manually place limit order at entry zone with provided TP/SL levels

### For 5-15 Minute Day Trading with Alerts:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- **Alert Setup**: Configure separate "Long Scalp Entry" and "Short Scalp Entry" alerts if you trade directionally based on bias

- **Execution**: Review channel structure on alert, confirm ATR filter shows ✓, then enter manually

### For 30-60 Minute Swing Scalping with Alerts:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- **Alert Setup**: Use "New Channel Formation" to prepare for setups, then "Any Entry Signal" for execution alerts

- **Execution**: Larger timeframes allow more analysis time between alert and entry

### Webhook Integration for Semi-Automation:

- Configure alert webhook URL to connect with platforms like TradersPost, TradingView Paper Trading, or custom automation

- Alert message includes all necessary order parameters (direction, entry, TP, SL)

- Webhook receives structured data when signal fires

- External platform can auto-execute based on alert payload

- Still maintains manual oversight vs full strategy automation

## USAGE CONSIDERATIONS:

- **Manual Discipline Required**: Alerts provide opportunities but execution requires judgment. Not all alerts should be taken - consider market context, trend, and channel quality

- **Alert Timing**: Alerts fire on bar close by default. Ensure "Once Per Bar Close" is selected to avoid false signals during bar formation

- **Notification Delivery**: Mobile/email alerts may have 1-3 second delay. For immediate execution, use desktop popups or webhook automation

- **Cooldown Necessity**: Without cooldown, rapidly touching price action can generate excessive alerts. Start with 3-bar cooldown and adjust based on alert volume

- **ATR Filter Impact**: Enabling ATR filter dramatically reduces alert count but improves quality. Track filter status in info table to understand when you're receiving fewer alerts

- **Commission Awareness**: High alert frequency means high potential trade count. Calculate if your commission structure supports frequent scalping before acting on all alerts

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features are not included in this indicator version. Multi-timeframe ATR requires higher-tier TradingView subscription for request.security() functionality on timeframes below chart timeframe.

## KNOWN LIMITATIONS:

- **Indicator does not execute trades** - alerts are informational only; you must manually place all orders

- **Alert delivery depends on TradingView infrastructure** - delays or failures possible during platform issues

- **No position tracking** - indicator doesn't know if you're in a trade; you must manage open positions independently

- **TP/SL levels are reference only** - you must manually set these on your broker platform; they are not live orders

- **Immediate touch entry can generate many alerts** in choppy zones without adequate cooldown

- **Channel deletion at 10-tick breaks** may be too aggressive or lenient depending on instrument tick size

- **ATR filter from lower timeframes** requires TradingView Premium/Pro+ for request.security()

- **Mean reversion logic fails** in strong breakout scenarios - alerts will fire but trades may hit stops

- **No partial closing capability** - full position management is manual; you determine scaling out

- **Alerts do not account for gaps** or overnight price changes; morning alerts may be stale

## RISK DISCLOSURE:

Trading involves substantial risk of loss. This indicator provides signals for educational and informational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Mean reversion strategies can experience extended drawdowns during trending markets. Alerts are not guaranteed to be profitable and should be combined with your own analysis. Stop losses may not fill at intended levels during extreme volatility or gaps. Never trade with capital you cannot afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Always verify alerts against current market conditions before executing trades manually.

## ACKNOWLEDGMENT & CREDITS:

This indicator is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based alert generation, comprehensive alert condition system with customizable notifications, multi-timeframe ATR volatility filtering, cooldown period for alert management, dual TP methods (fixed points vs channel percentage), visual TP/SL reference lines, and real-time status monitoring table. This indicator version is specifically designed for manual traders who prefer alert-based decision making over automated execution.

Setup 9/13 Lite — Exhaustion & Reference LevelsWhat it is

A clean, lightweight tool that implements the classic 1–9 setup progression, to-13 exhaustion signal, and bar-#1 reference levels. Built for clarity with minimal chart clutter.

How it works

Setup (1–9):

• Buy side counts bars where Close < Close .

• Sell side counts bars where Close > Close .

• Counter resets on an opposite condition.

• On completion, a triangle marker appears (Buy 9 below bar, Sell 9 above bar).

Reference levels (from bar #1 of a completed setup):

• After a completed Buy setup, draw a horizontal line from the Low of bar #1.

• After a completed Sell setup, draw a horizontal line from the High of bar #1.

• Lines extend to the right and update on new completed setups.

Exhaustion (…to 13):

• Starts on the bar after a completed 9.

• Buy side: increments when Close ≤ Low (or < if “Strict” is on).

• Sell side: increments when Close ≥ High (or > if “Strict” is on).

• Stops when 13 is reached (single circle marker) or when a new opposite 9 appears.

Strict comparisons:

Toggle between strict (<, >) and non-strict (≤, ≥) rules for both parts.

Header panel:

A compact top-right table shows live Setup and Exhaustion counts.

Inputs

Show Setup (1–9)

Show Exhaustion (to 13)

Show reference levels (from bar #1)

Strict comparisons (< /> instead of ≤ / ≥)

Paint bars during Setup

Paint bars during Exhaustion

(Exhaustion tint overrides Setup tint when both are enabled.)

Visual guide

Green triangle below bar = Buy Setup 9

Red triangle above bar = Sell Setup 9

Green circle below bar = Buy Exhaustion 13

Red circle above bar = Sell Exhaustion 13

Green/Red horizontal line = Reference level from bar #1 of the last completed setup

Alerts

Buy Setup 9 completed

Sell Setup 9 completed

Buy Exhaustion reached 13

Sell Exhaustion reached 13

Tip: for fewer false pings, set alerts to “Once per bar close.”

Notes

Works on any symbol/timeframe; higher liquidity improves readings. These signals indicate potential exhaustion/context, not a standalone trading system—combine with trend filters, S/R, and risk management.

Disclaimer

Educational use only. Not financial advice.

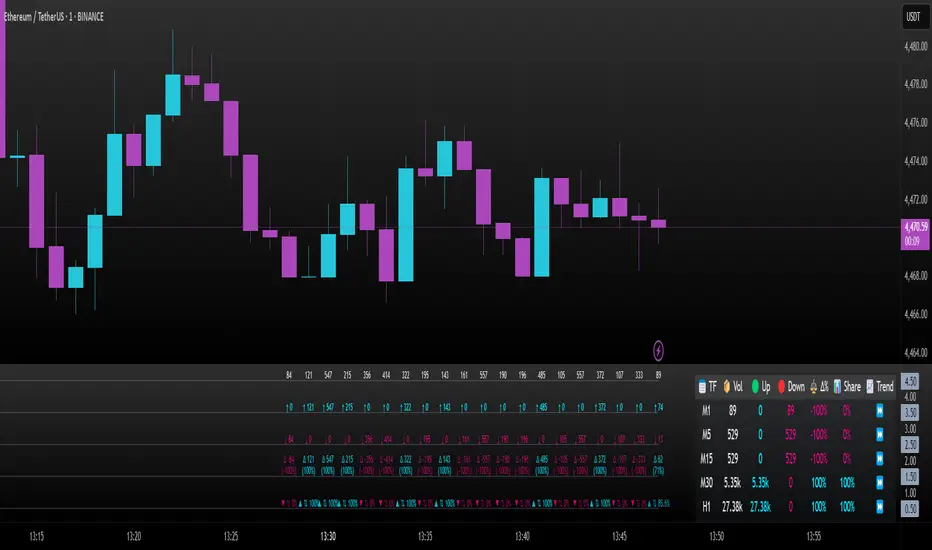

Intrabar Volume Delta — RealTime + History (Stocks/Crypto/Forex)Intrabar Volume Delta Grid — RealTime + History (Stocks/Crypto/Forex)

# Short Description

Shows intrabar Up/Down volume, Delta (absolute/relative) and UpShare% in a compact grid for both real-time and historical bars. Includes an MTF (M1…D1) dashboard, contextual coloring, density controls, and alerts on Δ and UpShare%. Smart historical splitting (“History Mode”) for Crypto/Futures/FX.

---

# What it does (Quick)

* **UpVol / DownVol / Δ / UpShare%** — visualizes order-flow inside each candle.

* **Real-time** — accumulates intrabar volume live by tick-direction.

* **History Mode** — splits Up/Down on closed bars via simple or range-aware logic.

* **MTF Dashboard** — one table view across M1, M5, M15, M30, H1, H4, D1 (Vol, Up/Down, Δ%, Share, Trend).

* **Contextual opacity** — stronger signals appear bolder.

* **Label density** — draw every N-th bar and limit to last X bars for performance.

* **Alerts** — thresholds for |Δ|, Δ%, and UpShare%.

---

# How it works (Real-Time vs History)

* **Real-time (open bar):** volume increments into **UpVolRT** or **DownVolRT** depending on last price move (↑ goes to Up, ↓ to Down). This approximates live order-flow even when full tick history isn’t available.

* **History (closed bars):**

* **None** — no split (Up/Down = 0/0). Safest for equities/indices with unreliable tick history.

* **Approx (Close vs Open)** — all volume goes to candle direction (green → Up 100%, red → Down 100%). Fast but yields many 0/100% bars.

* **Price Action Based** — splits by Close position within High-Low range; strength = |Close−mid|/(High−Low). Above mid → more Up; below mid → more Down. Falls back to direction if High==Low.

* **Auto** — **Stocks/Index → None**, **Crypto/Futures/FX → Approx**. If you see too many 0/100 bars, switch to **Price Action Based**.

---

# Rows & Meaning

* **Volume** — total bar volume (no split).

* **UpVol / DownVol** — directional intrabar volume.

* **Delta (Δ)** — UpVol − DownVol.

* **Absolute**: raw units

* **Relative (Δ%)**: Δ / (Up+Down) × 100

* **Both**: shows both formats

* **UpShare%** — UpVol / (Up+Down) × 100. >50% bullish, <50% bearish.

* Helpful icons: ▲ (>65%), ▼ (<35%).

---

# MTF Dashboard (🔧 Enable Dashboard)

A single table with **Vol, Up, Down, Δ%, Share, Trend (🔼/🔽/⏭️)** for selected timeframes (M1…D1). Great for a fast “panorama” read of flow alignment across horizons.

---

# Inputs (Grouped)

## Display

* Toggle rows: **Volume / Up / Down / Delta / UpShare**

* **Delta Display**: Absolute / Relative / Both

## Realtime & History

* **History Mode**: Auto / None / Approx / Price Action Based

* **Compact Numbers**: 1.2k, 1.25M, 3.4B…

## Theme & UI

* **Theme Mode**: Auto / Light / Dark

* **Row Spacing**: vertical spacing between rows

* **Top Row Y**: moves the whole grid vertically

* **Draw Guide Lines**: faint dotted guides

* **Text Size**: Tiny / Small / Normal / Large

## 🔧 Dashboard Settings

* **Enable Dashboard**

* **📏 Table Text Size**: Tiny…Huge

* **🦓 Zebra Rows**

* **🔲 Table Border**

## ⏰ Timeframes (for Dashboard)

* **M1…D1** toggles

## Contextual Coloring

* **Enable Contextual Coloring**: opacity by signal strength

* **Δ% cap / Share offset cap**: saturation caps

* **Min/Max transparency**: solid vs faint extremes

## Label Density & Size

* **Show every N-th bar**: draw labels only every Nth bar

* **Limit to last X bars**: keep labels only in the most recent X bars

## Colors

* Up / Down / Text / Guide

## Alerts

* **Delta Threshold (abs)** — |Δ| in volume units

* **UpShare > / <** — bullish/bearish thresholds

* **Enable Δ% Alert**, **Δ% > +**, **Δ% < −** — relative delta levels

---

# How to use (Quick Start)

1. Add the indicator to your chart (overlay=false → separate pane).

2. **History Mode**:

* Crypto/Futures/FX → keep **Auto** or switch to **Price Action Based** for richer history.

* Stocks/Index → prefer **None** or **Price Action Based** for safer splits.

3. **Label Density**: start with **Limit to last X bars = 30–150** and **Show every N-th bar = 2–4**.

4. **Contextual Coloring**: keep on to emphasize strong Δ% / Share moves.

5. **Dashboard**: enable and pick only the TFs you actually use.

6. **Alerts**: set thresholds (ideas below).

---

# Alerts (in TradingView)

Add alert → pick this indicator → choose any of:

* **Delta exceeds threshold** (|Δ| > X)

* **UpShare above threshold** (UpShare% > X)

* **UpShare below threshold** (UpShare% < X)

* **Relative Delta above +X%**

* **Relative Delta below −X%**

**Starter thresholds (tune per symbol & TF):**

* **Crypto M1/M5**: Δ% > +25…35 (bullish), Δ% < −25…−35 (bearish)

* **FX (tick volume)**: UpShare > 60–65% or < 40–35%

* **Stocks (liquid)**: set **Absolute Δ** by typical volume scale (e.g., 50k / 100k / 500k)

---

# Notes by Market Type

* **Crypto/Futures**: 24/7 and high liquidity — **Price Action Based** often gives nicer history splits than Approx.

* **Forex (FX)**: TradingView volume is typically **tick volume** (not true exchange volume). Treat Δ/Share as tick-based flow, still very useful intraday.

* **Stocks/Index**: historical tick detail can be limited. **None** or **Price Action Based** is a safer default. If you see too many 0/100% shares, switch away from Approx.

---

# “All Timeframes” accuracy

* Works on **any TF** (M1 → D1/W1).

* **Real-time accuracy** is strong for the open bar (live accumulation).

* **Historical accuracy** depends on your **History Mode** (None = safest, Approx = fastest/simplest, Price Action Based = more nuanced).

* The MTF dashboard uses `request.security` and therefore follows the same logic per TF.

---

# Trade Ideas (Use-Cases)

* **Scalping (M1–M5)**: a spike in Δ% + UpShare>65% + rising total Vol → momentum entries.

* **Intraday (M5–M30–H1)**: when multiple TFs show aligned Δ%/Share (e.g., M5 & M15 bullish), join the trend.

* **Swing (H4–D1)**: persistent Δ% > 0 and UpShare > 55–60% → structural accumulation bias.

---

# Advantages

* **True-feeling live flow** on the open bar.

* **Adaptable history** (three modes) to match data quality.

* **Clean visual layout** with guides, compact numbers, contextual opacity.

* **MTF snapshot** for quick bias read.

* **Performance controls** (last X bars, every N-th bar).

---

# Limitations & Care

* **FX uses tick volume** — interpret Δ/Share accordingly.

* **History Mode is an approximation** — confirm with trend/structure/liquidity context.

* **Illiquid symbols** can produce noisy or contradictory signals.

* **Too many labels** can slow charts → raise N, lower X, or disable guides.

---

# Best Practices (Checklist)

* Crypto/Futures: prefer **Price Action Based** for history.

* Stocks: **None** or **Price Action Based**; be cautious with **Approx**.

* FX: pair Δ% & UpShare% with session context (London/NY) and volatility.

* If labels overlap: tweak **Row Spacing** and **Text Size**.

* In the dashboard, keep only the TFs you actually act on.

* Alerts: start around **Δ% 25–35** for “punchy” moves, then refine per asset.

---

# FAQ

**1) Why do some closed bars show 0%/100% UpShare?**

You’re on **Approx** history mode. Switch to **Price Action Based** for smoother splits.

**2) Δ% looks strong but price doesn’t move — why?**

Δ% is an **order-flow** measure. Price also depends on liquidity pockets, sessions, news, higher-timeframe structure. Use confirmations.

**3) Performance slowdown — what to do?**

Lower **Limit to last X bars** (e.g., 30–100), increase **Show every N-th bar** (2–6), or disable **Draw Guide Lines**.

**4) Dashboard values don’t “match” the grid exactly?**

Dashboard is multi-TF via `request.security` and follows the history logic per TF. Differences are normal.

---

# Short “Store” Marketing Blurb

Intrabar Volume Delta Grid reveals the order-flow inside every candle (Up/Down, Δ, UpShare%) — live and on history. With smart history splitting, an MTF dashboard, contextual emphasis, and flexible alerts, it helps you spot momentum and bias across Crypto, Forex (tick volume), and Stocks. Tidy labels and compact numbers keep the panel readable and fast.

PumpC PAC & MAsPumpC – PAC & MAs (Open Source)

A complete Price Action Candles (PAC) toolkit combining classical price action patterns (Fair Value Gaps, Inside Bars, Hammers, Inverted Hammers, and Volume Imbalances) with a flexible Moving Averages (MAs) module and an advanced bar-coloring system.

This script highlights supply/demand inefficiencies and micro-patterns with forward-extending boxes, recolors zones when mitigated, qualifies patterns with a global High-Volume filter, and ships with ready-to-use alerts. It works across intraday through swing trading on any market (e.g., NASDAQ:QQQ , $CME:ES1!, FX:EURUSD , BITSTAMP:BTCUSD ).

This is an open-source script. The description is detailed so users understand what the script does, how it works, and how to use it. It makes no performance claims and does not provide trade advice.

Acknowledgment & Credits

This script originates from the structural and box-handling logic found in the Super OrderBlock / FVG / BoS Tools by makuchaku & eFe. Their pioneering framework provided the base methods for managing arrays of boxes, extending zones forward, and recoloring once mitigated.

Building on that foundation, I have substantially expanded and adapted the code to create a unified Price Action Candles toolkit . This includes Al Brooks–inspired PAC logic, additional patterns like Inside Bars, Hammers, Inverted Hammers, and the new Volume Imbalance module, along with strong-bar coloring, close-threshold detection, a flexible global High-Volume filter, and a multi-timeframe Moving Averages system.

What it does

Fair Value Gaps (FVG) : Detects 3-bar displacement gaps, plots forward-extending boxes, and optionally recolors them once mitigated.

Inside Bars (IB) : Highlights bars fully contained within the prior candle’s range, with optional high-volume filter.

Hammers (H) & Inverted Hammers (IH) : Identifies rejection candles using configurable body/upper/lower wick thresholds. High-volume qualification optional.

Volume Imbalances (VI) : Detects inter-body gaps where one candle’s body does not overlap the prior candle’s body. Boxes extend forward until wick-based mitigation occurs (only after the two-bar formation completes). Alerts available for creation and mitigation.

Mitigation Recolor : Each pattern can flip to a mitigated color once price trades back through its vertical zone.

Moving Averages (MAs) : Four configurable EMAs/SMAs, with per-MA timeframe, length, color, and clutter-free plotting rules.

Strong Bar Coloring : Highlights bullish/bearish engulfing reversals with different colors for high-volume vs low-volume cases.

Close Threshold Bars : Marks candles that close in the top or bottom portion of their range, even if the body is small. Helps spot continuation pressure before a full trend bar forms.

Alerts : Notifications available for FVG+, FVG−, IB, H, IH, VI creation, and VI mitigation.

Connection to Al Brooks’ PAC teachings

This script reflects Al Brooks’ Price Action Candle methodology. PAC patterns like Inside Bars, Hammers, and Inverted Hammers are not trade signals on their own—they gain meaning in context of trend, failed breakouts, and effort vs. result.