Bollinger Bands And Aroon Scalping (by Coinrule)Many technical indicators can be profitable in certain market conditions while failing in others. No indicator is perfect alone.

All the best trading strategies involve multiple indicators and leverage the benefit of each of them. The following is an optimised strategy based on Bollinger Bands and the Aroon indicator.

The Bollinger Bands are among the most famous and widely used indicators. They can suggest when an asset is oversold or overbought in the short term, thus provide the best time for buying and selling it.

A strategy buying dips can work well during times of uptrend. Downtrends will result in a drawdown for the P&L of the strategy. The suggested approach minimises the drawdowns, ensuring that the system trades only when it's more likely to close the trade in profit.

The Setup

ENTRY

The price crosses below the basis line of the Bollinger Band indicator

The Aroon Indicator is above 90

EXIT

The price crosses below the upper Bollinger Band

The Aroon Indicator drops below 70

The Aroon Indicator plays a key role in this strategy. It acts as a confirmation that the asset is currently in an uptrend. On the other hand, it acts as a stop if market conditions deteriorate. The strategy uses an Aroon Indicator set to 288 periods to provide a longer-term view on market conditions, not being heavily dependent on short-term volatility.

The best time frame for this strategy based on our backtest is the 4-hr . The 1-hr can work well with three times more trades, on average. As trades increase, the profitability decreases. Yet again, this is the confirmation that trading more does not mean gaining more.

To make the results more realistic, the strategy assumes each order to trade 30% of the available capital. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Cari dalam skrip untuk "bollingerband"

Bollinger Band with RSI

Using combination bollinger band and RSI indicator as guide to predict price volatility and the best entry point. The strategy logic is pretty straightforward where we're interested with close price that touches the lower bollinger band ; there are only two scenarios that will happened after the price reaches the lower band; the price might rebound from the lower bollinger band or drop lower and continue downtrend. To confirm the price movement, we use a second indicator which is the RSI to further investigate the price trend. For example, if the price reaches the lower bollinger band but the RSI value is not in the oversold region, we can conclude that the price will go lower and continue downtrend. If the RSI value is in the oversold region, we can use this price area as our entry point.

Stop loss is necessary to avoid losing too much capital if the RSI value lingers too long in the oversold region.

Best take profit area is when the price rebound above the middle bollinger band area/upper bollinger band or when the RSI reaches overbought region; whichever comes first.

Long entry:

RSI < 30 & close price < lower bollinger band

Exit entry:

RSI > 70

Default stop loss: -25%

Triple ThreatThis indicator provides buy and sell signals for Bitcoin based on confluence from well-known momentum, volatility, and trend indicators. It has successfully captured the major directional trends on Bitcoin's daily chart since 2018, and the settings are currently optimized for this chart in particular. This indicator implements RSI to gauge momentum, BBWP to gauge volatility, and an EMA to gauge trend. Maximum confluence signals are represented by horizontal bars in the indicator's pane, where the tallest green bar is a confirmed buy signal, and the tallest red bar is a confirmed sell signal. The shortest bar represents a momentum-only signal, and the second-shortest bar represents a volatility signal in confluence with the previously given momentum signal.

To track momentum, the RSI is plotted to the indicator plane against a moving average of the RSI. A momentum signal is generated when the RSI crosses over its moving average, retests/approaches the moving average, and then continues in the crossover direction (i.e., it fails to cross the moving average to the opposite side, creating a successful retest). The settings that affect this trigger are the "Crossover Threshold," which specifies how much the RSI should exceed the moving average to be considered a crossover, and the "Retest threshold," which specifies how closely the RSI should approach the moving average to be considered a retest. A momentum signal is ALSO generated if the RSI or its moving average exceed their counterpart by a certain threshold. For example, if the threshold was set at 10, a BUY signal would be generated when the RSI exceeds the moving average by 10, or a SELL signal would be generated when the moving average exceeds the RSI by 10. This threshold can be set using the "Instant Signal Threshold" setting. Either type of momentum signal will be plotted on the pane as the shortest horizontal bar, with its color indicating the signal's direction.

Volatility is primarily measured using the Bollinger Band Width Percentile (BBWP) indicator, which was created by The_Caretaker. BBWP plots the volatility of the asset's price, given by Bollinger Band width, relative to past volatility by assigning the volatility readings into percentiles. The indicator also includes a moving average of the BBWP itself, where a crossover to the upside represents expanding volatility and a crossover to the downside represents contracting volatility. This indicator is used to confirm a signal given by the momentum indicators - a momentum signal that is given during a period of expanding volatility has a greater likelihood of success. Therefore, when the BBWP crosses above its moving average by a given threshold, a previously triggered momentum signal is considered to be "confirmed." The threshold for this crossover can be set using the "BBWP Confirmation Threshold" setting. However, it is also relevant that periods of extreme volatility often accompany an extremity in price action (a "top" or "bottom"), in which case the BBWP is likely to contract after price reaches such an extremity. This phenomenon is captured by also using "extreme reads" on the momentum indicator to signal that there has already been enough volatility to confirm a momentum signal. If the RSI gives an "extreme read" before triggering a signal, the momentum signal is also considered to be confirmed. For example, if the RSI is above 80, breaks below 80, and then gives a SELL signal, this sell signal is considered to be confirmed without requiring the BBWP to crossover its moving average to the upside. The threshold that would confirm a SELL signal can be set with the "Overbought" setting, and the threshold that would confirm a BUY signal can be set with the "Oversold" setting. Whenever a volatility signal confirms a momentum signal, a medium-sized horizontal bar will be plotted on the pane in the same directional color as the momentum signal. Note that a momentum signal may trigger at the exact same time as the volatility signal which confirms it; in this case, only the medium-sized bar will be visible on the pane, but its direction can still be identified by its color.

Lastly, to reduce the likelihood of "false signals," a trend indicator is used to confirm the direction of the signal. This is typically an exponential moving average. If a confirmed volatility SELL signal is given, and the closing price is below the moving average, then the SELL signal is also confirmed by the trend. Likewise, if a confirmed volatility BUY signal is given, and the closing price is above the moving average, then the BUY signal is confirmed by the trend. The type and length of the moving average used to verify the trend can be set using the "Moving Average Type" and "Moving Average Length" settings found below the momentum/volatility settings. A trend signal is plotted on the pane as a tall horizontal bar, and is more deeply colored than the momentum and volatility signals.

For maximum confluence, it is recommended that the trend signal, given by the tallest bar, is the one that forms the basis of trades executed while using the Triple Threat indicator. It is possible to enter more aggressive trades with better entries by using only the volatility signal, given by the medium-sized bar, however this entails greater risk and should only be done in confluence with an additional trading strategy of your own discretion. Backtesting has shown that using the volatility signal alone underperforms using the volatility signal in confluence with the trend signal.

Please also be advised that the default setting are optimized for Bitcoin's daily chart only. The indicator is still applicable to other timeframes and asset classes, but the settings may need to be modified. I have a list of settings for other Bitcoin timeframes, and I would be happy to share them upon request.

I hope you can find this indicator to be of some use to your trading strategies. I'd be happy to hear any feedback from the community, so please don't hesitate to reach out. Stay safe, and happy trading.

LPB MicroCycles StrategyWhat it is:

We use the Hodrick-Prescott filter applied to the closing price, and then take the outputted trendline and apply a custom vwap, the time frame of which is based on user input, not the default 1 day vwap . Then we go long if the value 2 bars ago is greater then one bar ago. We sell and color the bars and lines when the if the value of 2 bars ago is less than one bar ago.

Also included:

GUI for backtesting

ATR Based Stop Loss

How to use:

Go long when the indicators suggest it, and use the stop losses to reduce risk.

Best if paired with a volatility measurement (inside candles, average true range , bollingerband%B)

Custom Band Strategy1. Trend

if ema200 > ema30 Long entry only

else Short entry only

2. Custom Band

Upper band = sma(period) + max(close, period) * multiplier

Lower band = sma(period) - max(close, period) * multiplier

Multiplier can be either 1.3 or 1.1 depending on the trend.

(If trend is long, upper band's factor would be 1.3, lower band be 1.1)

2. Long entry condition

- Cross over the lower band and band width is greater than (close price)*2.2%(assume this band width as an expected ROE)

- Previous candle change rate((close-open)/open*100) is less than 3%.

3. Short entry condition

- Cross under the upper band and band width is greater than (close price)*2.2%

- Previous candle change rate is less than 3%.

4. Long/Short exit condition

- cross over/under the lower/upper band and roe is higher than 2%.

5. Stop/Target condition

- Target 10%, Stoploss 3%

- Previous candle change rate is higher than 3%.

Most variables can be set manually.

Test period changeable.

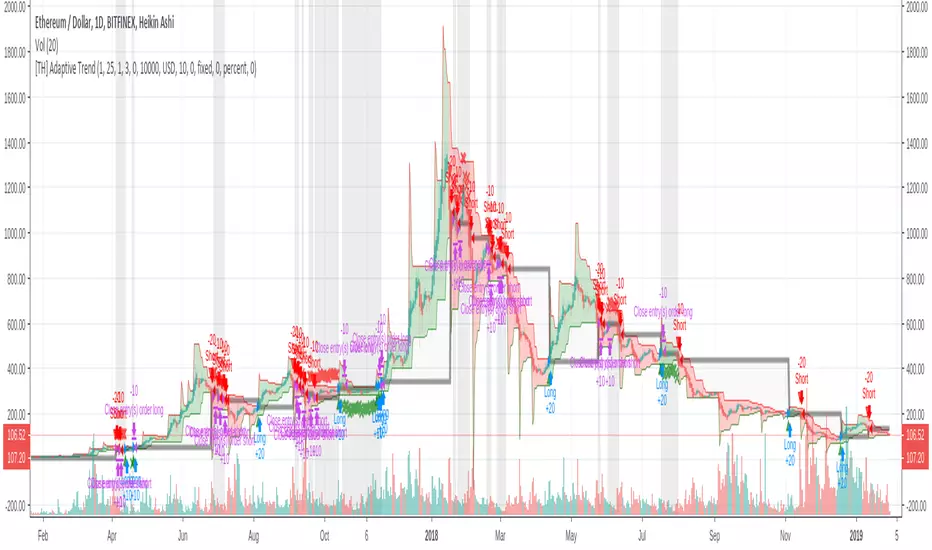

[TH] Adaptive Trend : StrategyAdaptive Trend : Strategy

*** It should be used with 'heikin ashi' chart ***

Super Trend

Basically, it is super trend strategy ( Rajandran R Supertrend )

- My idea is,

1. (scale) Factor of super trend is related with sensitivity of Up/Down trend change

2. Constant Factor cause failure of super trend strategy when market prices variance is low ( ie. high Factor ==> miss short trend )

3. By using variance measure ( like BollingerBand ) as a varying Factor, maybe we can catch short trend and long trend together

Loss Cut

The silver thick line is loss cut line & silver background means exit position status

I found that silver background is appear usually when price moves horizontally

1. It is set to open price of actual position entry ( heikin ashi chart's open price = loss cut line = (open + close)/2 )

2. If position is long

==> loss cut is executed when low price is lower than loss cut line

==> re-entry when low price is higher than loss cut line

3. If Position is short

==> loss cut is executed when high price is higher than loss cut line

==> re-entry when high price is lower than loss cut lin

ChannelBreakOutStrategyV2.1This is the basic strategy that uses the price breakout of BollingerBands.

Hazel nut BB Strategy, volume base- lite versionHazel nut BB Strategy, volume base — lite version

Having knowledge and information in financial markets is only useful when a trader operates with a well-defined trading strategy. Trading strategies assist in capital management, profit-taking, and reducing potential losses.

This strategy is built upon the core principle of supply and demand dynamics. Alongside this foundation, one of the widely used technical tools — the Bollinger Bands — is employed to structure a framework for profit management and risk control.

In this strategy, the interaction of these tools is explained in detail. A key point to note is that for calculating buy and sell volumes, a lower timeframe function is used. When applied with a tick-level resolution, this provides the most precise measurement of buyer/seller flows. However, this comes with a limitation of reduced historical depth. Users should be aware of this trade-off: if precise tick-level data is required, shorter timeframes should be considered to extend historical coverage .

The strategy offers multiple configuration options. Nevertheless, it should be treated strictly as a supportive tool rather than a standalone trading system. Decisions must integrate personal analysis and other instruments. For example, in highly volatile assets with narrow ranges, it is recommended to adjust profit-taking and stop-loss percentages to smaller values.

◉ Volume Settings

• Buyer and seller volume (up/down volume) are requested from a lower timeframe, with an option to override the automatic resolution.

• A global lookback period is applied to calculate moving averages and cumulative sums of buy/sell/delta volumes.

• Ratios of buyers/sellers to total volume are derived both on the current bar and across the lookback window.

◉ Bollinger Band

• Bands are computed using configurable moving averages (SMA, EMA, RMA, WMA, VWMA).

• Inputs allow control of length, standard deviation multiplier, and offset.

• The basis, upper, and lower bands are plotted, with a shaded background between them.

◉ Progress & Proximity

• Relative position of the price to the Bollinger basis is expressed as percentages (qPlus/qMinus).

• “Near band” conditions are triggered when price progress toward the upper or lower band exceeds a user-defined threshold (%).

• A signed score (sScore) represents how far the close has moved above or below the basis relative to band width.

◉ Info Table

• Optional compact table summarizing:

• - Upper/lower band margins

• - Buyer/seller volumes with moving averages

• - Delta and cumulative delta

• - Buyer/seller ratios per bar and across the window

• - Money flow values (buy/sell/delta × price) for bar-level and summed periods

• The table is neutral-colored and resizable for different chart layouts.

◉ Zone Event Gate

• Tracks entry into and exit from “near band” zones.

• Arming logic: a side is armed when price enters a band proximity zone.

• Trigger logic: on exit, a trade event is generated if cumulative buyer or seller volume dominates over a configurable window.

◉ Trading Logic

• Orders are placed only on zone-exit events, conditional on volume dominance.

• Position sizing is defined as a fixed percentage of strategy equity.

• Long entries occur when leaving the lower zone with buyer dominance; short entries occur when leaving the upper zone with seller dominance.

◉ Exit Rules

• Open positions are managed by a strict priority sequence:

• 1. Stop-loss (% of entry price)

• 2. Take-profit (% of entry price)

• 3. Opposite-side event (zone exit with dominance in the other direction)

• Stop-loss and take-profit levels are configurable

◉ Notes

• This lite version is intended to demonstrate the interaction of Bollinger Bands and volume-based dominance logic.

• It provides a framework to observe how price reacts at band boundaries under varying buy/sell pressure, and how zone exits can be systematically converted into entry/exit signals.

When configuring this strategy, it is essential to carefully review the settings within the Strategy Tester. Ensure that the chosen parameters and historical data options are correctly aligned with the intended use. Accurate back testing depends on applying proper configurations for historical reference. The figure below illustrates sample result and configuration type.

4H Bollinger Breakout StrategyThis strategy leverages Bollinger Bands on the 4-hour timeframe for long and short trades in trending or ranging markets. Entries trigger on BB breakouts with optional filters for volume, trend, and RSI. Exits occur on opposite BB crosses. Customizable for long-only, short-only, or indicator mode via code comments. Supports forex, stocks, or crypto with full equity allocation and 0.1% commission.

Length (Default: 20): Period for BB basis and std dev; shorter for sensitivity, longer for smoothing.

Basis MA Type (Default: SMA): Selects MA for middle band (SMA, EMA, etc.); EMA for faster response.

Source (Default: Close): Price input for calculations; use close for standard accuracy.

StdDev Multiplier (Default: 1.8): Band width control; higher for fewer signals, lower for more.

Offset (Default: 0): Shifts BB plots; typically unchanged.

Use Filters (Default: True): Applies volume, trend, RSI checks to filter signals.

Volume MA Length (Default: 20): For volume filter (long: >105% avg, short: >120%).

Trend MA Length (Default: 80): SMA for trend filter (long: above MA, short: below).

RSI Length (Default: 14): For short filter (entry if RSI <85).

Use Long/Short Signals (Defaults: True): Toggles directions; long entry on lower BB crossover, short on upper crossunder.

Visuals: BB plots (blue basis, red upper, green lower), orange trend MA, filled background.

Labels/Alerts: Green/red for long entry/exit, yellow/purple for short; alert conditions included.

Ahsan Tufail Precise MA Crossover Filter for Reliable SignalsIntroduction:

In the ever-evolving world of Forex trading, strategies that provide a competitive edge are highly sought after. The Moving Average (MA) crossover technique is a popular long-term approach, but its vulnerability to false signals can lead to potential losses. To overcome this challenge, we introduce a game-changing MA crossover filter designed to weed out false signals and unlock the full potential of this strategy. In this article, we delve into the mechanics of this filter, providing a comprehensive analysis of its components and how it enhances the accuracy of buy and sell signals.

The Power of the MA Crossover Filter:

The essence of our MA crossover filter lies in the integration of a specialized indicator that operates on a scale of 0 to 100. This ingenious indicator dynamically measures the distance between the middle Bollinger band and either the upper or lower Bollinger band. By analyzing the values of the last 504 candlesticks, it maps the range from 50 to 100 for the largest and smallest distances between the middle and upper Bollinger bands. Similarly, for values ranging from 0 to 50, it measures the distance between the middle and lower Bollinger bands.

Unveiling the Signal Execution Process:

The brilliance of this filter is revealed in its meticulous execution of buy and sell signals, which significantly reduces false crossovers. Let's explore the process step-by-step:

Buy Signal Precision:

To initiate a buy signal, the price must be positioned above the 200-period Simple Moving Average (SMA).

The filter validates the crossover by checking the indicator's value, ensuring it falls below the threshold of 25.

Sell Signal Accuracy:

For a sell signal, the price must be below the 200-period Simple Moving Average (SMA).

The filter confirms the crossover by verifying the indicator's value, which should exceed the threshold of 75.

This selective approach ensures that only high-confidence crossovers are considered, maximizing the potential for profitable trades.

Fine-Tuning the Filter for Optimal Performance:

While the MA crossover filter exhibits its prowess in GBPUSD and EURUSD currency pairs, it may require adjustments for other pairs. Currency pairs possess unique characteristics, and adapting the filter to specific behavior is crucial for its success.

To fine-tune the filter for alternative currency pairs, traders should conduct rigorous backtesting and analyze historical price data. By experimenting with indicator threshold values, traders can calibrate the filter to accurately match the dynamics of the target currency pair. This iterative process allows for customization, ultimately resulting in a finely-tuned filter that aligns with the unique behavior of the selected market.

Conclusion:

The MA crossover filter represents a paradigm shift in long-term Forex trading strategies. By intelligently filtering false signals, this precision tool unleashes the true potential of the MA crossover technique, elevating its profitability and enhancing overall trading performance. While no strategy guarantees absolute success, incorporating this filter empowers traders with a heightened level of confidence in their buy and sell signals. Embracing the power of this innovative filter can be a transformative step towards mastering Forex profits and staying ahead in the dynamic world of currency trading.

Shorting when Bollinger Band Above Price with RSI (by Coinrule)The Bollinger Bands are among the most famous and widely used indicators. A Bollinger Band is a technical analysis tool defined by a set of trendlines plotted two standard deviations (positively and negatively) away from a simple moving average ( SMA ) of a security's price, but which can be adjusted to user preferences. They can suggest when an asset is oversold or overbought in the short term, thus providing the best time for buying and selling it.

The relative strength index ( RSI ) is a momentum indicator used in technical analysis. RSI measures the speed and magnitude of a security's recent price changes to evaluate overvalued or undervalued conditions in the price of that security. The RSI can do more than point to overbought and oversold securities. It can also indicate securities primed for a trend reversal or corrective pullback in price. It can signal when to buy and sell. Traditionally, an RSI reading of 70 or above indicates an overbought situation. A reading of 30 or below indicates an oversold condition.

The short order is placed on assets that present strong momentum when it's more likely that it is about to reverse. The rule strategy places and closes the order when the following conditions are met:

ENTRY

The closing price is greater than the upper standard deviation of the Bollinger Bands

The RSI is less than 70.

EXIT

The trade is closed when the RSI is less than 70

The lower standard deviation of the Bollinger Band is less than the closing price.

This strategy was backtested from the beginning of 2022 to capture how this strategy would perform in a bear market.

The strategy assumes each order to trade 70% of the available capital to make the results more realistic. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange by volume.

Bollinger Band BreakoutThis strategy buys when price crosses above an upper Bollinger Band and sells when the lower band is breached. What makes this strategy different than others:

Long only with filtering for only showing strong tickers

Filter out trades below a moving average on both the current timeframe and a longer period timeframe to keep you out of bear markets

Optional ability to set a tighter initial stop level to increase exposure and decrease downside risk on freshly opened trades while you wait for the lower Bollinger Band trailing stop to catch up

Take entries/exits on wicks/stops or wait for candle closes before entry

Select which dates to backtest

Customize Bollinger Band parameters including the ability to have different values for the upper and lower band standard deviation

Bollinger Band strategy with split, limit, stopEntering a short position after breaking the upper Bollinger Band, entering a long position when entering after breaking the lower Bollinger Band

Provides templates for how to display position average price, stop loss, and profit price using the plot function on the chart, and how to buy splits

After entering the position, if the price crosses the mid-band line, the stop loss is adjusted to the mid-band line.

Bollinger Pair TradeNYSE:MA-1.6*NYSE:V

Revision: 1

Author: @ozdemirtrading

Revision 2 Considerations :

- Simplify and clean up plotting

Disclaimer: This strategy is currently working on the 5M chart. Change the length input to accommodate your needs.

For the backtesting of more than 3 months, you may need to upgrade your membership.

Description:

The general idea of the strategy is very straightforward: it takes positions according to the lower and upper Bollinger bands.

But I am mainly using this strategy for pair trading stocks. Do not forget that you will get better results if you trade with cointegrated pairs.

Bollinger band: Moving average & standard deviation are calculated based on 20 bars on the 1H chart (approx 240 bars on a 5m chart). X-day moving averages (20 days as default) are also used in the background in some of the exit strategy choices.

You can define position entry levels as the multipliers of standard deviation (for exp: mult2 as 2 * standard deviation).

There are 4 choices for the exit strategy:

SMA: Exit when touches simple moving average (SMA)

SKP: Skip SMA and do not stop if moving towards 20D SMA, and exit if it touches the other side of the band

SKPXDSMA: Skip SMA if moving towards 20D SMA, and exit if it touches 20D SMA

NoExit: Exit if it touches the upper & lower band only.

Options:

- Strategy hard stop: if trade loss reaches a point defined as a percent of the initial capital. Stop taking new positions. (not recommended for pair trade)

- Loss per trade: close position if the loss is at a defined level but keeps watching for new positions.

- Enable expected profit for trade (expected profit is calculated as the distance to SMA) (recommended for pair trade)

- Enable VIX threshold for the following options: (recommended for volatile periods)

- Stop trading if VIX for the previous day closes above the threshold

- Reverse active trade direction if VIX for the previous day is above the threshold

- Take reverse positions (assuming the Bollinger band is going to expand) for all trades

Backtesting:

Close positions after a defined interval: mark this if you want the close the final trade for backtesting purposes. Unmark it to get live signals.

Use custom interval: Backtest specific time periods.

Other Options:

- Use EMA: use an exponential moving average for the calculations instead of simple moving average

- Not against XDSMA: do not take a position against 20D SMA (if X is selected as 20) (recommended for pairs with a clear trend)

- Not in XDSMA 1 DEV: do not take a position in 20D SMA 1*standart deviation band (recommended if you need to decrease # of trades and increase profit for trade)

- Not in XDSMA 2 DEV: do not take a position in 20D SMA 2*standart deviation band

Session management:

- Not in session: Session start and end times can be defined here. If you do not want to trade in certain time intervals, mark that session.(helps to reduce slippage and get more realistic backtest results)

Ichimoku Cloud and Bollinger Bands (by Coinrule)The Ichimoku Cloud is a collection of technical indicators that show support and resistance levels, as well as momentum and trend direction. It does this by taking multiple averages and plotting them on a chart. It also uses these figures to compute a “cloud” that attempts to forecast where the price may find support or resistance in the future.

The Ichimoku Cloud was developed by Goichi Hosoda, a Japanese journalist, and published in the late 1960s. It provides more data points than the standard candlestick chart. While it seems complicated at first glance, those familiar with how to read the charts often find it easy to understand with well-defined trading signals.

The Ichimoku Cloud is composed of five lines or calculations, two of which comprise a cloud where the difference between the two lines is shaded in.

The lines include a nine-period average, a 26-period average, an average of those two averages, a 52-period average, and a lagging closing price line.

The cloud is a key part of the indicator. When the price is below the cloud, the trend is down. When the price is above the cloud, the trend is up.

The above trend signals are strengthened if the cloud is moving in the same direction as the price. For example, during an uptrend, the top of the cloud is moving up, or during a downtrend, the bottom of the cloud is moving down.

The Bollinger Bands are among the most famous and widely used indicators. A Bollinger Band is a technical analysis tool defined by a set of trendlines plotted two standard deviations (positively and negatively) away from a simple moving average ( SMA ) of a security's price, but which can be adjusted to user preferences. They can suggest when an asset is oversold or overbought in the short term, thus providing the best time for buying and selling it.

This strategy combines the Ichimoku Cloud with Bollinger Bands to better enter trades.

Long orders are placed when these basic signals are triggered.

Long Position:

Tenkan-Sen is above the Kijun-Sen

Chikou-Span is above the close of 26 bars ago

Close is above the Kumo Cloud

The closing price is greater than the upper standard deviation of the Bollinger Bands

Short Position:

Tenkan-Sen is below the Kijun-Sen

Chikou-Span is below the close of 26 bars ago

Close is below the Kumo Cloud

The upper standard deviation of the Bollinger Band is greater than the closing price

The script is backtested from 1 January 2022 and provides good returns.

The strategy assumes each order is using 30% of the available coins to make the results more realistic and to simulate you only ran this strategy on 30% of your holdings. A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

This script also works well on BTC 30m/1h, ETH 2h, MATIC 2h/30m, AVAX 1h/2h, SOL 45m timeframes

Bollinger Bands + EMA 9A 1 minute scalping strategy.

Uses Bollinger Bands (no basis line) and a 9 period EMA.

Waits for price to close below the lower Bollinger Band and the next candle to close bullish above the lower Bollinger Band but below the 9 Period EMA.

If all conditions are met, the script enters a long position with TP at the 9 Period EMA.

Best TradingView Strategy - For NASDAQ and DOW30 and other IndexThe script is totally based on momentum , volume and price. We have used :

1: Bollinger Band Squeezes to know when a breakout might happen.

2: Used Moving Averages(SMA and EMA) to know the direction.

3: The success Rate of this strategy is above 75% and if little price action is added it can easily surpass 90% success mark.

4: Do not worry about drawdowns , we have implemented trailing SL ,so you might see a little extra drawdown but in reality its pretty less.

5: I myself have tested this strategy for 41 days with a 250$ account and right now I have 2700$.

Bollinger Bands Fibonacci Ratios StrategyHello, everyone!

We have just released an innovative strategy for TradingView. It allows you to identify price pivot points and volatility.

This strategy is:

User-friendly

Configurable

Equipped with Bollinger Bands and smoothed ATR to measure volatility

Features

Thanks to the BB Fibo strategy, you can:

Trade stocks and commodities.

Identify price pivot points.

Choose any band for trading Long or Short positions.

Swap upper and lower bands applying Use Reverse Buy/Sell parameters.

Note! The upper bands are for the Long position. The lower bands are for the Short positions.

Parameters

We have equipped our strategy with more than 14 additional parameters. So, you can configure the EA according to your needs!

Inputs:

Length

Source: Open, High, Low, Close, HL2, HLC3, OHLC4

Offset

Fibonacci Ratio 1 — a Fibonacci factor for the 1st upper and lower indicator lines calculating.

Fibonacci Ratio 2 — a Fibonacci factor for the 2nd upper and lower indicator lines calculating.

Fibonacci Ratio 3 — a Fibonacci factor for the 3d upper and lower indicator lines calculating.

Use Reverse Buy — the strategy will use lower Bollinger bands instead of upper ones.

Fibonacci Buy — band selection for opening Long positions conditions.

Use Reverse Sell — the strategy will use upper Bollinger bands instead of lower ones.

Fibonacci Sell — band selection for opening Short positions conditions.

Style:

Basis — baseline color and style settings.

Upper 3 — the 3d upper line color and style.

Upper 2 — the 2nd upper line color and style.

Upper 1 — the 1st upper line color and style.

Lower 1 — the 1st lower line color and style.

Lower 2 — the 2nd lower line color and style.

Lower 3 — the 3d upper line color and style.

Background — the background color within the 3d upper and 3d lower indicator band.

Precision — the number of decimals for BB Fibo values.

Note! Try BB Fibo on your demo account first before going live.

Sideways Strategy DMI + Bollinger Bands (by Coinrule)Markets don’t always trade in a clear direction. At a closer look, most of the time, they move sideways. Relying on trend-following strategies all the time can thus lead to repeated false signals in such conditions.

However, before you can safely trade sideways, you have to identify the most suitable market conditions.

The main features of such strategies are:

Short-term trades, with quick entries and quick exits

Slightly contrarian and mean-reversionary

Require some indicator that tells you it’s a sideways market

This Sideways DMI + Bollinger Bands strategy incorporates such features to bring you a profitable alternative when the regular trend-following systems stop working.

ENTRY

1. The trading system requires confirmation for a sideways market from the Directional Movement Index (DMI) before you can start opening any trades. For this purpose, the strategy uses the absolute difference between positive and negative DMI, which must be lower than 20.

2. To pick the right moment to buy, the strategy looks at the Bollinger Bands (BB). It enters the trade when the price crosses over the lower BB.

EXIT

The strategy then exits when the move has been exhausted. Generally, in sideways markets, the price should revert lower. The position is closed when the price crosses back down below the upper BB.

The best time frame for this strategy based on our backtest is the 1-hr. Shorter timeframes can also work well on certain coins that are more volatile and trade sideways more often. However, as expected, these exhibit larger volatility in their returns. In general, this approach suits medium timeframes. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

You can execute this strategy on your favourite exchange at coinrule.com.

rj_temu_pair_tradea simple "temu" implementation of a pair trade

see robotjames.substack.com for details.

Oleg_Aryukov_StrategyTrader Oleg Aryukov's strategy, based on a variety of oscillators, allows him to try to catch reversals in cryptocurrencies.

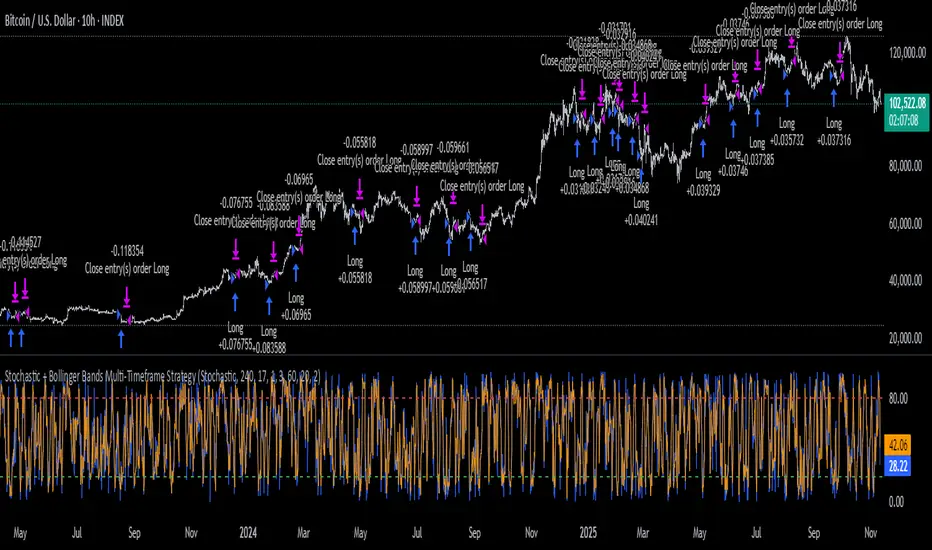

Stochastic + Bollinger Bands Multi-Timeframe StrategyThis strategy fuses the Stochastic Oscillator from the 4-hour timeframe with Bollinger Bands from the 1-hour timeframe, operating on a 10-hour chart to capture a unique volatility rhythm and temporal alignment discovered through observational alpha.

By blending momentum confirmation from the higher timeframe with short-term volatility extremes, the strategy leverages what some traders refer to as “rotating volatility” — a phenomenon where multi-timeframe oscillations sync to reveal hidden trade opportunities.

🧠 Strategy Logic

✅ Long Entry Condition:

Stochastic on the 4H timeframe:

%K crosses above %D

Both %K and %D are below 20 (oversold zone)

Bollinger Bands on the 1H timeframe:

Price crosses above the lower Bollinger Band, indicating a potential reversal

→ A long trade is opened when both momentum recovery and volatility reversion align.

✅ Long Exit Condition:

Stochastic on the 4H:

%K crosses below %D

Both %K and %D are above 80 (overbought zone)

Bollinger Bands on the 1H:

Price reaches or exceeds the upper Bollinger Band, suggesting exhaustion

→ The long trade is closed when either signal suggests a potential reversal or overextension.

🧬 Temporal Structure & Alpha

This strategy is deployed on a 10-hour chart — a non-standard timeframe that may align more effectively with multi-timeframe mean reversion dynamics.

This subtle adjustment exploits what some traders identify as “temporal drift” — the desynchronization of volatility across timeframes that creates hidden rhythm in price action.

→ For example, Stochastic on 4H (lookback 17) and Bollinger Bands on 1H (lookback 20) may periodically sync around 10H intervals, offering unique alpha windows.

📊 Indicator Components

🔹 Stochastic Oscillator (4H, Length 17)

Detects momentum reversals using %K and %D crossovers

Helps define overbought/oversold zones from a mid-term view

🔹 Bollinger Bands (1H, Length 20, ±2 StdDev)

Measures price volatility using standard deviation around a moving average

Entry occurs near lower band (support), exits near upper band (resistance)

🔹 Multi-Timeframe Logic

Uses request.security() to safely reference 4H and 1H indicators from a 10H chart

Avoids repainting by using closed higher-timeframe candles only

📈 Visualization

A plot selector input allows toggling between:

Stochastic Plot (%K & %D, with overbought/oversold levels)

Bollinger Bands Plot (Upper, Basis, Lower from 1H data)

This helps users visually confirm entry/exit triggers in real time.

🛠 Customization

Fully configurable Stochastic and BB settings

Timeframes are independently adjustable

Strategy settings like position sizing, slippage, and commission are editable

⚠️ Disclaimer

This strategy is intended for educational and informational purposes only.

It does not constitute financial advice or a recommendation to buy or sell any asset.

Market conditions vary, and past performance does not guarantee future results.

Always test any trading strategy in a simulated environment and consult a licensed financial advisor before making real-world investment decisions.

BB SPY Mean Reversion Investment StrategySummary

Mean reversion first, continuation second. This strategy targets equities and ETFs on daily timeframes. It waits for price to revert from a Bollinger location with candle and EMA agreement, then manages risk with ATR based exits. Uniqueness comes from two elements working together. One, an adaptive band multiplier driven by volatility of volatility that expands or contracts the envelope as conditions change. Two, a bias memory that re arms the same direction after any stop, target, or time exit until a true opposite signal appears. Add it to a clean chart, use the markers and levels, and select on bar close for conservative alerts. Shapes can move while the bar is open and settle on close.

Scope and intent

• Markets. Currently adapted for SPY, needs to be optimized for other assets

• Timeframes. Daily primary. Other frames are possible but not the default

• Default demo. SPY on daily

• Purpose. Trade mean reversion entries that can chain into a longer swing by splitting holds into ATR or time segments

Originality and usefulness

• Novelty. Adaptive band width from volatility of volatility plus a persistent bias array that keeps the original direction alive across sequential entries until an opposite setup is confirmed

• Failure modes mitigated. False starts in chop are reduced by candle color and EMA location. Missed continuation after a take profit or stop is addressed by the re arm engine. Oversized envelopes during quiet regimes are avoided by the adaptive multiplier

• Testability. Every module has Inputs and visible levels so users can see why a suggestion appears

• Portable yardstick. All risk and targets are expressed in ATR units

Method overview in plain language

The engine measures where price sits relative to Bollinger bands, confirms with candle color and EMA location, requires ADX for shorts(in our case long close since we use it currently as long only), and optionally requires a trend or mean reversion regime using band width percent rank and basis slope. Risk uses ATR for stop, target, and optional breakeven. A small array stores the last confirmed direction. While flat, the engine keeps a pending order in that direction. The array flips only when a true opposite setup appears.

Base measures

• Range basis. True Range smoothed over a user defined ATR Length

• Return basis. Not required

Components

• Bollinger envelope. SMA length and standard deviation multiplier. Entry is based on cross of close through the band with location bias

• Candle and EMA filter. Close relative to open and close relative to EMA align direction

• ADX gate for shorts. Requires minimum trend strength for short trades

• Adaptive multiplier. Band width scales using volatility of volatility so envelopes breathe with conditions

• Regime gate optional. Band width percent rank and basis slope identify trend or mean reversion regimes

• Risk manager. ATR stop, ATR target, optional breakeven, optional time exit

• Bias memory. Array stores last confirmed direction and re arms entries while flat

Fusion rule

Minimum satisfied gates count style. All required gates must be true. Optional gates are controlled in Inputs. Bias memory never overrides an opposite confirmed setup.

Signal rule

• Long setup when close crosses up through the lower band, the bar closes green, and close is above the long EMA

• Short setup when close crosses down through the upper band, the bar closes red, close is below the short EMA, and ADX is above the minimum

• While flat the model keeps a pending order in the stored direction until a true opposite setup appears

• IN LONG or IN SHORT describes states between entry and exit

What you will see on the chart

• Markers for Long and Short setups

• Exit markers from ATR or time rules

• Reference levels for entry, stop, and target

• Bollinger bands and optional adaptive bands

Inputs with guidance

Setup

• Signal timeframe. Uses the chart timeframe

• Invert direction optional. Flips long and short

Logic

• BB Length. Typical 10 to 50. Higher smooths more

• BB Mult. Typical 1.0 to 2.5. Higher widens entries

• EMA Length long. Typical 10 to 50

• EMA Length short. Typical 5 to 30

• ADX Minimum for short. Typical 15 to 35

Filters

• Regime Type. none or trend or mean reversion

• Rank Lookback. Typical 100 to 300

• Basis Slope Length and Threshold. Larger values reduce false trends

Risk

• ATR Length. Typical 10 to 21

• ATR Stop Mult. Typical 1.0 to 3.0

• ATR Take Profit Mult. Typical 2.0 to 5.0

• Breakeven Trigger R. Move stop to entry after the chosen multiple

• Time Exit. Minimum bars and extension when profit exceeds a fraction of ATR

Bias and rearm

• Bias flips kept. Array depth

• Keep rearm when flat. Maintain a pending order while flat

UI

• Show markers and levels. Clean defaults

Usage recipes

Alerts update in real time and can change while the bar forms. Select on bar close for conservative workflows.

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• If any higher timeframe calls are enabled, request.security uses lookahead off

• Commission 0.03 percent

• Slippage 3 ticks

• Default order size method Percent of equity with value 5

• Pyramiding 0

• Process orders on close On

• Bar magnifier Off

• Recalculate after order is filled Off

• Calc on every tick Off

Realism and responsible publication

No performance claims. Costs and fills vary by venue. Shapes can move intrabar and settle on close. Strategies use standard candles only.

Honest limitations and failure modes

High impact releases and thin liquidity can break assumptions. Gap heavy symbols may require larger ATR. Very quiet regimes can reduce contrast in the mean reversion signal. If stop and target can both be touched inside one bar, outcome follows the TradingView order model for that bar path.

Regimes with extreme one sided trend and very low volatility can reduce mean reversion edges. Results vary by symbol and venue. Past results never guarantee future outcomes.

Open source reuse and credits

None.

Backtest realism

Costs are realistic for liquid equities. Sizing does not exceed five percent per trade by default. Any departure should be justified by the user.

If you got any questions please le me know