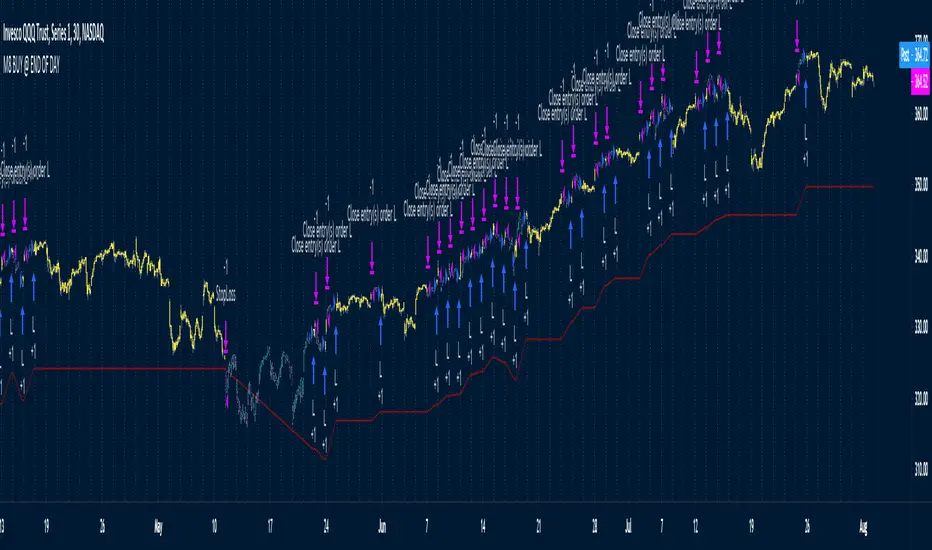

Heikin Ashi SupertrendAbout this Strategy

This supertrend strategy uses the Heikin Ashi candles to generate the supertrend but enters and exits trades using normal candle close prices. If you use the standard built in Supertrend indicator on Heikin Ashi candles, it will produce very unrealistic backtesting results because it uses the Heikin Ashi prices instead of the real prices. However, by signaling the supertrend reversals using Heikin Ashi while using standard candle close prices for the entries and exits, it corrects the backtesting errors and gives you a more realistic equity curve. You should set the chart to use standard candles and then hide them (the strategy creates the candles).

This strategy includes:

Plotting of Heikin Ashi candles

Heikin Ashi Supertrend

Long and Short Entry Signals

Move stop loss after trade is X% in profit

Profit Target

Stop Loss

Built in Alertatron automation

Alertatron Trade Automation Integration

For Alertatron integration, be sure to configure the strategy settings and "Enable Webhook Messages" before creating an alert with {{strategy.order.alert_message}} in the body of your alert message. Be sure to enable webhooks and point it to your Incoming Alertatron webhook URL.

Notes

While this strategy does pretty well during trending markets, It's worth noting that the Buy and Hold ROI is much better during peak times of the bull market

Not financial advice. Do not risk more than you can afford to lose.

Strategi Pine Script®