ryantrad3s session highs and lowsThis indicator allows you find London Session and Asia Session highs and lows without marking them yourself. This indicator can also help you find good draws on liquidity for the day and potential highs and lows you can target during that trading day. I recommend trading NQ and ES with this indicator because that's what I seen it work best with. The blue lines are London Session high and low and the red lines are Asia Session high and low. Hope this can save you time marking out your chart before market open.

Cari dalam skrip untuk "liquidity"

Smarter Money Concepts - MTF IFVGs [PhenLabs]📊 Smarter Money Concepts - MTF IFVG

Version: PineScript™ v6

📌 Description

This multi-timeframe indicator identifies Inverse Fair Value Gaps (IFVGs) and their inversions across simultaneous chart intervals, helping traders spot liquidity voids and potential reversal zones. By analyzing price action through the lens of institutional order flow patterns, it solves the problem of manual gap tracking across timeframes while incorporating volatility-adjusted parameters and psychological level analysis for higher-probability setups.

🚀 Points of Innovation

• Multi-Timeframe Engine - Simultaneous analysis of 3 higher timeframes

• Adaptive Parameters - Auto-adjusts to market volatility conditions

• Quality Scoring System - Ranks gaps using RVI strength and size metrics

• Inversion Tracking - Monitors failed gaps for counter-trend signals

• Render Optimization - Prevents chart clutter with smart gap management

🔧 Core Components

FVG Detection Logic: Identifies gaps using customizable price source (Close/Wick)

Inversion Tracker: Manages failed gaps and generates counter signals

Multi-Timeframe Engine: Processes 3 independent higher timeframe analyses

Dashboard System: Real-time display of active gaps across all timeframes

🔥 Key Features

• Volatility-adjusted gap size filters (ATR-based)

• Customizable timeframe confluence analysis

• Color-coded quality scoring

• Non-repainting inversion signals

• Mobile-optimized visual rendering

🎨 Visualization

• Colored Boxes: Translucent zones show active gaps (green/bullish, red/bearish)

• Midline Plot: Dashed gray line marks gap midpoint for price targets

• Inversion Markers: Intense colors show failed gaps (dark red/bullish failure, bright green/bearish failure)

• HTF Differentiation: Higher timeframe gaps shown in blue/teal hues

📖 Usage Guidelines

Multi-Timeframe Settings

• Higher Timeframe 1

Default: 30 | Range: Any > Chart TF | Controls primary confluence timeframe

• Show All Timeframes

Default: True | Toggles multi-TF gap displays

Gap Settings

• Source

Default: Close | Options: | Determines gap measurement method

• RVI Period

Default: 14 | Range: 1-50 | Sets momentum confirmation sensitivity

• RVI Value

Default 0.1 | 0 to see all IFVGs | Increase min RVI to see the most powerful IFVGs

✅ Best Use Cases

• Identifying confluence across timeframes

• Spotting institutional order blocks

• High-probability reversal trading

• Trend continuation confirmation

• Volatility breakout setups

⚠️ Limitations

• Repaints historical gap zones

• Requires understanding of FVG concepts

• Higher timeframe data latency

• Quality scores rely on RVI/ATR settings

💡 What Makes This Unique

First FVG indicator with true multi-timeframe processing

Adaptive parameters that auto-adjust to volatility

Quantifiable quality scoring system

Professional-grade dashboard with HTF tracking

🔬 How It Works

Gap Detection: Identifies FVGs using price relationships and RVI confirmation

Inversion Tracking: Monitors price breaches to flag failed gaps

Quality Assessment: Scores gaps based on size, momentum, and location

Adaptive Filtering: Adjusts parameters using ATR-based volatility analysis

Multi-TF Synthesis: Correlates gaps across user-selected timeframes

Visual Rendering: Displays only relevant, active gaps to prevent clutter

💡 Note:

Start with default settings and gradually adjust parameters after observing market interactions. Focus on gaps with quality scores above 7 that align with higher timeframe trends. Combine with price action at psychological levels for highest-probability setups. Remember that higher timeframe gaps generally carry more significance than current chart gaps.

MACD Liquidity Tracker SystemMACD Liquidity Tracker System

🔹 Enhanced MACD with candle coloring, entry markers, and customizable signal logic.

🧠 Features:

This tool combines a color-coded MACD histogram with signal-based candle colors and small shape markers (🔼🔽) for clear market momentum and entry visualization.

📊 Visuals:

MACD Histogram (Sub-panel):

4 dynamic colors to show momentum direction:

🔹 Bright Blue = MACD > 0 & rising (strong bullish)

🔹 Dark Blue = MACD > 0 & falling (weakening bullish)

🔹 Bright Magenta = MACD < 0 & falling (strong bearish)

🔹 Dark Magenta = MACD < 0 & rising (weakening bearish)

Price Candles (Main Chart):

🔹 Bright Blue = Active Long signal

🔹 Bright Magenta = Active Short signal

Entry Markers:

🔼 Blue triangle (below candle) = Start of Long

🔽 Magenta triangle (above candle) = Start of Short

⚙️ System Types (select in settings):

Normal:

🔹 Long = MACD > 0

🔹 Short = MACD < 0

Fast: (Based on histogram color)

🔹 Long = Bright Blue OR Dark Magenta

🔹 Short = Dark Blue OR Bright Magenta

Safe:

🔹 Long = Only Bright Blue

🔹 Short = All other colors

🔔 Alerts:

Alerts trigger only on the first bar of a new Long/Short signal.

Easy to set up using TradingView’s alert system.

📌 How to Use:

Add the indicator to your chart

Open settings and select a System Type

Adjust MACD parameters if needed

Use histogram color + candle color for momentum and signal confirmation

Set alerts for clean entries if desired

💡 Ideal for traders seeking visual clarity and flexible MACD-based strategies.

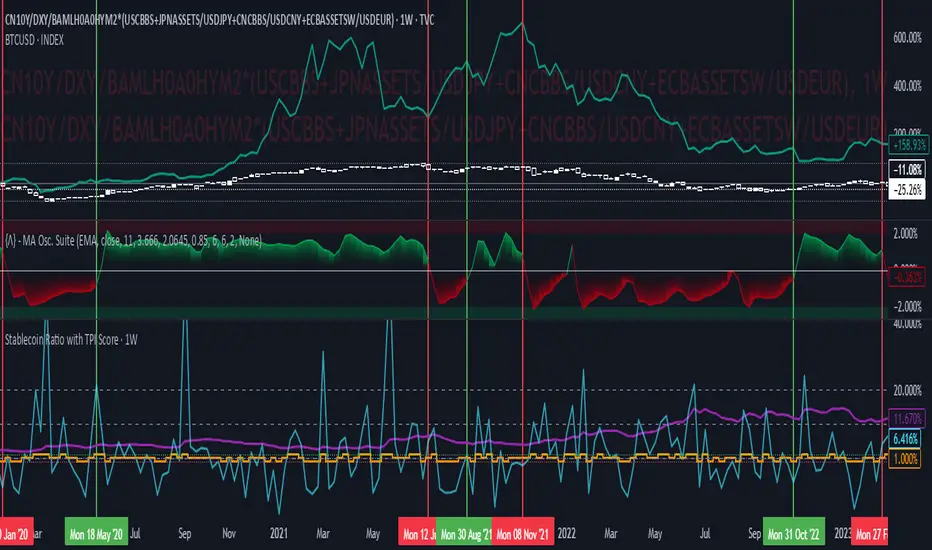

Stablecoin Ratio with TPI ScoreThe script measures the stablecoin ratio (total stablecoin market cap divided by total crypto market cap, times 100) and its weekly change. Stablecoins (e.g., USDT, USDC) are a key gateway for capital entering or exiting the crypto ecosystem.

A rising ratio suggests more capital is parked in stablecoins (potential buying power), while a falling ratio indicates capital leaving (selling or withdrawal).

In a macro analysis, this is critical—it reflects the availability of liquid funds that could fuel price movements.

In macroeconomics, liquidity is a driver of asset prices.

In crypto, stablecoins represent sidelined capital ready to deploy.

How does it work?

Stablecoin Ratio:

Formula: (total_stablecoin_mcap / total_crypto_mcap) * 100.

Example: If stablecoins = $235B and total market cap = $2.5T, ratio = 9.4%.

Plotted as a red line in the oscillator pane, showing the percentage of the market held in stablecoins.

Weekly Change:

Calculates the percentage change in the ratio from the previous week:

(current_ratio - previous_ratio) / previous_ratio * 100.

Example: Ratio goes from 9% to 10% = +11.11% change.

TPI Score Assignment:

+1 (Bullish): If the ratio increases by more than 5% week-over-week.

-1 (Bearish): If the ratio decreases by more than 5% week-over-week.

0 (Neutral): If the change is between -5% and +5%.

Plotted as orange step line bars in the oscillator pane, snapping to +1, 0, or -1.

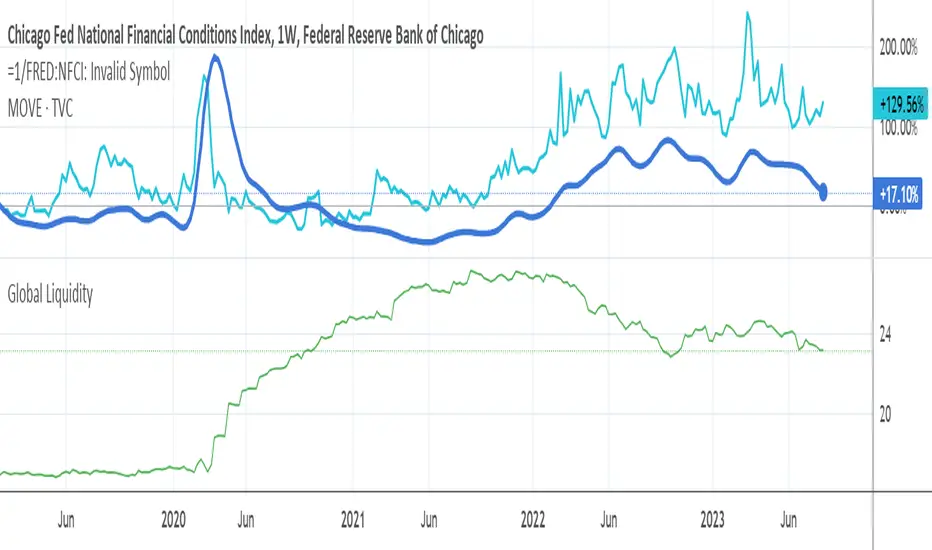

Global Liquidity Indicator in USDThis indicator aggregates the total central bank balance sheets and M2 money supply for the USA, Canada, China, European Union, Japan, and the UK, converting all values to USD and normalizing them to trillions for easy visualization. It plots three lines: Total Balance Sheet, Total M2, and Combined Total, providing a comprehensive view of global liquidity trends.

Key Features:

Dynamic Coloring: Customize line colors based on direction—green for upward trends, red for downward (or any colors you choose), with independent on/off toggles for each line.

Real-Time Currency Conversion: Uses live forex rates (e.g., USD/CNY, USD/EUR) for accurate USD conversions.

Pivot Liquidity Sweep + SignalsCore Functionalities:

Sweep Signals:

The indicator identifies sweeps of liquidity by detecting when price exceeds recent pivot highs (swing highs) or pivot lows (swing lows) and then reverses direction. It draws attention to these scenarios by labeling them on the chart.

For bullish sweep signals, the entry point is the closing price of the sweep candle, with the stop loss placed at the highest point between the sweep candle and the previous candle.

For bearish sweeps, the entry point is similarly identified, with the stop loss being the lowest price of the sweep candle and the candle before it. The profit target is dynamically set to the low or high of the closest valid pivot depending on the direction of the trade.

Rejection Signals:

Rejection signals are identified when price attempts to break a pivot high or low but fails, causing a rejection.

Bullish rejections involve price trying to break a pivot low but closing back above it, indicating potential for a bounce.

Bearish rejections follow a similar pattern, with price attempting to break a pivot high but failing to hold above it, signaling a potential bearish move.

High-Precision Intrabar Data:

The "Intrabar Precision" feature allows the indicator to use lower timeframe data to accurately plot sweeps and rejections, providing traders with precise entry and exit points.

The intrabar settings are particularly useful for traders looking for high-precision trades, such as scalpers who want to capture small yet consistent moves.

ATR and Percentage-Based Filters:

The indicator allows for customizable filters to ensure signals meet certain thresholds before being validated. Traders can use ATR (Average True Range) or percentage-based conditions to filter out low-quality signals, ensuring that the trades captured have enough volatility or price movement potential.

Dashboard:

The built-in dashboard provides a quick overview of trades executed using the indicator, displaying metrics such as the total number of sweep and rejection trades, their success rates, and total profit in points.

The dashboard is color-coded for easy reading and offers traders insights into the overall performance of their strategy, helping with ongoing evaluation and optimization.

Labeling and Alerts:

Every time a sweep or rejection signal is detected, the indicator automatically labels the chart to help traders quickly identify the trading opportunities.

Alerts are also generated for each trading signal, providing the trader with real-time notifications, which can be useful for those who are not constantly monitoring their charts.

Stop Loss and Target Adaptation:

The stop loss levels are adjusted dynamically based on the recent pivot points, and the target profit is derived from valid subsequent pivot levels to ensure realistic and efficient trade exits.

CRT Trades (turtle soup, A-M-D ranges with inside bars)CRT means Candle Range Theory. Every single candle is a range, on every single timeframe. Ranges may be either manipulated - turtle souped or broken - engulfed - closed above/below and retested.

CRT is usually presented as a 3 candle model. However it may consist of more than 3 candles due to inside bars. Inside bar is the candle where high is not higher then previous candle high and low is not lower then previous candle low.

First candle represents accumulation (may consist of more candles - inside bars), second candle represents manipulation (turtle soup) and third candle represents distribution. The abbreviation for that is A-M-D.

In accumulation the range with specific high and low is created. In manipulation (turtle soup) the high or low of the range is manipulated - liquidity taken and price should usually reverse back to the range. In distribution price is reversing back to the opposite side of the range. On higher timeframe it looks like manipulation candle wick is higher/lower than previous range high/low (may consist of 1 or more inside bar candles) but the body must not close above/below previous range high/low. Otherwise it is not manipulation (turtle soup) most likely and price should continue in direction of the candle close. Distribution candle should touch opposite side of range and it is mostly heavy and fast candle.

CRT model can be found on higher timeframe (e.g. 4h) and entries can be found on lower timeframe (e.g. 15m). You always use only lower timeframe on your chart because CRT model on the higher timeframe is shown on the lower one and also you can plan entries on the lower timeframe. You are able to change CRT model higher timeframe in the indicator settings.

There are two types of entries:

simple - wait for manipulation candle to close on higher timeframe (HTF) and then enter on lower timeframe (LTF) above open of the distribution candle on HTF if it is short or on LTF below open of the distribution candle on HTF if it is long. These entries can be done by market order.

advanced - wait for the break of previous range high/low and enter by limit order when price reverses back to the range and retraces to the order block or fair value gap created by the breaker candle.

Stop loss can be placed above/below of the top/bottom created by manipulation candle. First take profit should be placed in 1/2 of the accumulation range and second take profit should be placed at the opposite range of accumulation range.

It is possible to filter only particular accumulation (range) and manipulation (turtle soup) candles depending also on timezone set in the settings. For example on 4h CRT model if you fill input "indices" for section "range" like 1,2 and input "indices" for section "turtle soup" like 3,4 then you are awaiting the range to form during asia session and manipulation during london session if the timezone is somewhere around "UTC+2".

Dotted lines represent turtle soup of previous range and solid lines represent engulfing candle of the breaker candle on lower timeframe. When the engulfing is closed you can look for entries either by market order after closing or by limit order when the price retraces to order block (created by breaker candle) or fair value gap (created by engulfing).

Recommendations for combining lower (entries) and higher (crt model) timeframes:

1D CRT model => 1h entries,

4h CRT model => 15m entries,

1h CRT model => 5m entries,

15m CRT model => 1m entries.

Custom Opening Price Levels (PO3)This indicator is designed to assist the trader in identifying the Power of Three through the opens of the candles.

-------------------------

The PO3 is a concept introduced by ICT. First, you need to have a directional bias for the month or the specific candle in question. It should be of high time frame (HTF BIAS).

At the open of the specific candle, the market will generate interest in the direction opposite to the HTF BIAS, accumulating positions. It will then manipulate the positions of less informed traders to generate the necessary liquidity to fill informed operators positions.

Finally, positions are distributed in favor of the bias.

-------------------------

The PO3 is a phenomenon that repeats across all timeframes. This indicator is highly customizable and allows the user to choose from a range of timeframes: 3 months, 1 month, 1 week, 1 day, and 3 hours. The indicator displays the last 3 opens for the selected period.

-------------------------

The script is open-source, so feel free to add more timeframes or open levels if you have coding skills.

LDPM Crossover Scanner AddonThe LDPM Crossover Scanner is designed to be used in conjunction with the Liquidity Dependent Price Movement Algorithm and is included with LDPM access.

The LDPM Crossover Scanner displays the LDPM status for up to 10 equity's. When conditions are bearish, per LDPM, the equity will light up on the scanner; otherwise, the equity will not light up.

When used in aggregate, this becomes a particularly useful way to measure up-coming market moves (especially when the crossover scanner showcases equities with significant beta to the chart's underlying!).

Market Structure Volume Distribution [LuxAlgo]The Market Structure Volume Distribution tool allows traders to identify the strength behind breaks of market structure at defined price ranges to measure de correlation of forces between bulls and bears visually and easily.

🔶 USAGE

This tool has three main features: market structure highlighting, grid levels, and volume profile. Each feature is covered more in depth below:

🔹 Market Structure

The basic unit of market structure is a swing point, the period of the swing point is user-defined, so traders can identify longer-term market structures. Price breaking a prior swing point will confirm the occurrence of a market structure.

The tool will plot a line after a market structure is confirmed, by default the lines on bullish MS will be green (indicative of an uptrend), and red in case of bearish MS (indicative of a downtrend).

🔹 Grid Levels

The Grid visually divides the price range contained inside the tool execution window, into equal size rows, the number of rows is user-defined so users can divide the full price range up to 100 rows.

The main objective of this feature is to help identify the execution window and the limits of each row in the volume profile so traders can know in a simple look what BoMS belongs to each row.

There is however another use for the grid, by dividing the range into equal-sized parts, this feature provides automatic support and resistance levels as good as any other.

Grid provides a visual help to know what our execution window is and to associate MS with their rows in the profile. It can provide S/R levels too.

🔹 Volume Profile

The volume profile feature shows in a visually easy way the volume behind each MS aggregated by rows and divided into buy and sell volume to spot the differences in a simple look.

This tool allows users to spot the liquidity associated with the event of a market structure in a specific price range, allowing users to know which price areas where associated with the most trading activity during the occurrence of a market structutre.

🔶 SETTINGS

🔹 Data Gathering

Execute on all visible range: Activate this to use all visible bars on the calculations. This disables the use of the next parameter "Execute on the last N bars". Default false.

Execute on the last N bars: Use last N bars on the calculations. To use this parameter "Execute on all visible range" must be disabled. Values from 20 to 5000, default 500.

Pivot Length: How many bars will be used to confirm a pivot. The bigger this parameter is the fewer breaks of structure will detect. Values from 1, default 2

🔹 Profile

Profile Rows: Number of rows in the volume profile. Values from 2 to 100, default 10.

Profile Width: Maximum width of the volume profile. Values from 25 to 500, default 200.

Profile Mode: How the volume will be displayed on each row. "TOTAL VOLUME" will aggregate buy & sell volume per row, "BUY&SELL VOLUME" will separate the buy volume from the sell volume on each row. Default BUY&SELL VOLUME.

🔹 Style

Buy Color: This is the color for the buy volume on the profile when the "BUY&SELL VOLUME" mode is activated. Default green.

Sell Color: This is the color for the sell volume on the profile when the "BUY&SELL VOLUME" mode is activated. Default red.

Show dotted grid levels: Show dotted inner grid levels. Default true.

Smart Orderblocks / Supply and Demand (@JP7FX)

"Smart" Order Block Supply and Demand Indicator – a tool inspired by Smart Money Concepts and designed to complement your trading style.

It's not about perfection, but rather about enhancing your trading insights and catching things you might have missed.

Keep in mind that the structural representation here is subjective, just like many other indicators. It's more of a guide to help you navigate the market.

While it doesn't explicitly include Imbalance / FVG, you have the flexibility to use additional Imbalance /FVG indicators, including my own, to complement the insights drawn from Supply and Demand zones.

This indicator offers customisation options like trading ranges, allowing you to mark Killzones and tailor it to your preferences. Explore liquidity levels, 50% retracement lines, and personalize the colors and lines to match your unique chart setup.

Guide below on how the "Hidden" Zones are created!

Trade Safe :)

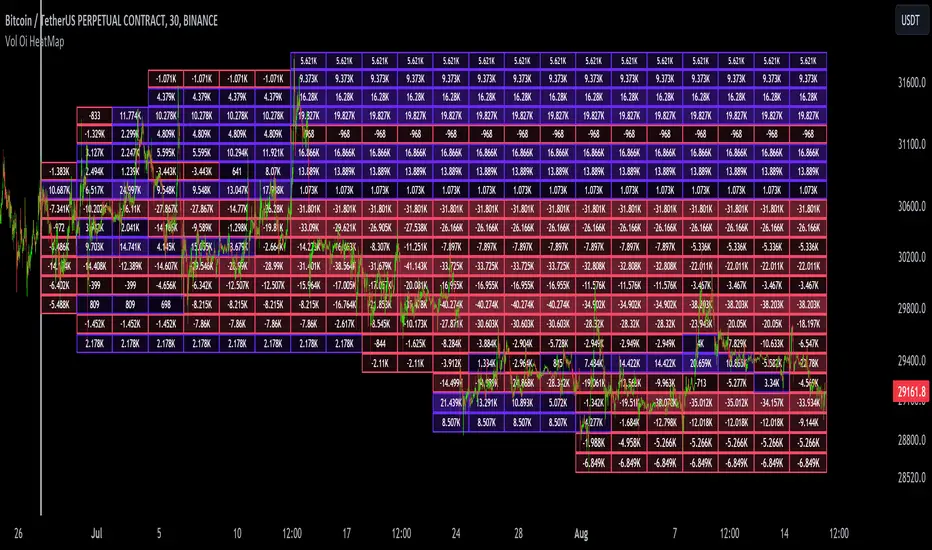

Dynamic Liquidity Map [Kioseff Trading]Hello!

Just a quick/fun project here: "Dynamic Heatmap".

This script draws a volume delta or open interest delta heatmap for the asset on your chart.

The adjective "Dynamic" is used for two reasons (:

1: Self-Adjusting Lower Timeframe Data

The script requests ~10 lower timeframe volume and open interest data sets.

When using the fixed range feature the script will, beginning at the start time, check the ~10 requested lower timeframes to see which of the lower timeframes has available data.

The script will always use the lowest timeframe available during the calculation period. As time continues, the script will continue to check if new lower timeframe data (lower than the currently used lowest timeframe) is available. This process repeats until bar time is close enough to the current time that 1-minute data can be retrieved.

The image above exemplifies the process.

Incrementally lower timeframe data will be used as it becomes available.

1: Fixed range capabilities

The script features a "fixed range" tool, where you can manually set a start time (or drag & drop a bar on the chart) to determine the interval the heatmap covers.

From the start date, the script will calculate the calculate the sub-intervals necessary to draw a rows x columns heatmap. Consequently, setting the start time further back will draw a heat map with larger rows x columns, whereas, a start time closer to the current bar time will draw a more "precise" heatmap with smaller rows x columns.

Additionally, the heatmap can be calculated using open interest data.

The image above shows the heatmap displaying open interest delta.

The image above shows alternative settings for the heatmap.

Delta values have been hidden alongside grid border colors. These settings can be replicated to achieve a more "traditional" feel for the heatmap.

Thanks for checking this out!

HTF Liquidity Dashboard [TFO]The purpose of this indicator is to server as a multi-symbol scanner that indicates when user-defined symbols have exceeded their previous Day/Week/Month highs and lows.

By default, the dashboard will use a compact view where the green ✔ means that price has swept and is currently exceeding the level of interest, the red ❌ implies that price swept the level but reversed back into the original range, and - indicates that the level hasn't been reached. However, the dashboard text can be toggled to show the numerical values of the highs and lows instead of these compact strings, as shown in the following image.

These levels may be shown and customized on the current chart as well via the Show Levels option. By default, levels from the selected timeframes will initially be plotted as black, and will change to red once traded through. Users can optionally increase the Session Limit parameter to show more than one previous high/low on their chart, for each selected timeframe.

Optionally, we can also plot labels to show when any of the user-defined symbols have exceeded their respective highs and lows, for any of the selected timeframes. Alerts can be created for these events as well; simply select the desired symbols and timeframes, create a new alert using this indicator, and you should be alerted when highs and lows are traded through. Note: if you encounter any issues with duplicate alerts, try deleting the alert, navigating to a lower timeframe such as the 1m, and making a new alert.

Nexus Blast Trading Strategy [Kaspricci]Nexus Blast Trading Strategy - Kaspricci

This indicator shows the different sessions during the day (London session, New York AM session, New York PM session and Asian session) by adding vertical lines and draws horizontal lines for the high and low during each session. Furthermore those lines turn red once the price has taken this high or low. Blue lines indicate liquidity not yet taken.

On top the indicator draws boxes of different color to indicate bullish and bearish Fair Value Gaps (FVG).

Happy to receive your feedback. Please leave a comment for bugs as well as ideas for improvement.

General Settings

Time Zone - used for marking sessions and end of day.

Sessions

Sessions - start and end time for each session based on set time zone

Number of Days back - for how many days in the past the startegy will draw strategy highs and lows. Theres is a maximum of 50 days defined.

FVG Settings

Threshold in Ticks - you can hide very small FVGs by increasing this threshold

FVG Colors - colors used for the bearish and bullish FVG box

This script is for educational purposes only! It is not meant to be a financial advice.

PS: The former strategy script was removed by TV, as it would violate several rules according to them.

Central Bank LiquidityCentral Bank Liquidity = Total value of the assets of all Federal Reserve Banks - Overnight Reverse Repurchase Agreements (RRP) - The Treasury General Account (TGA)

TradingView ticker arithmetic: FRED:WALCL-FRED:WTREGEN-FRED:RRPONTSYD

Market Structure and Liquidity IndicatorThis indicator tracks the market structure by identifying the highest high and lowest low. It then calculates the area of interest by taking the average of these levels. Additionally, it calculates liquidity by dividing the volume by the range between the highest high and lowest low.

Please note that this is a basic example, and you can modify and enhance it according to your specific requirements and trading strategy. Remember to thoroughly backtest and validate any trading strategy or indicator before using it in live trading.

Global LiquidityPlots the sum of the balance sheets of the world's major central banks - FED, ECB, BoE, PBoC, BOJ, India and Switzerland - in a currency of your choice. Defaults to USD.

Also shows FED net liquidity (balance sheet - tga - rrp) for comparison. Uses a configurable multiplier to make the two lines viewable on the same price scale.

Traders Reality Vector Candle ZonesVector Candle Zone indicator displays areas of unrecovered liquidity based on PVSRA with override option for the chart symbol.

Developed for TradersReality by infernixx with library conversion by peshocore

SPX and Federal Net Liquidity differenceScript for applying Federal Net Liquidity to the SPX post-2020 monetary policy. Original indicator from jlb05013 with adjustments to make it more readable and usable. When the indicator is above 250 the SPX is overbought and when it's below -250 the SPX is oversold.

It's not perfect, I'm just publishing because I didn't see it already out there.

Price Action All In One IndicatorIf you are the one who is "Price Action" style & does not want to use many indicators or complex indicators or you are an ICT (The Inner Circle Trader)

student or ICT charter, this simple beautiful All In One Indicator is right for you.

The indicator has the following functions.

TIME ZONE SETTING

The default timezone is New York Time GMT-4, if you leave the time zone setting blank, it will use the symbol timezone. Note that the trading time changes with one hour delay in winter. so if you just trade forex, and leave the time zone setting blank, TradingView will adjust the symbol timezone automatically for you or don't forget to change the timezone setting GMT-4 or GMT-5 depending on daylight saving time.

STATISTIC PANEL

You can choose which panel to show through settings.

Session Info Panel : pips info of ADR, Asian, London, and New York sessions.

Trend Panel : showing trend (up/down) of

5m/15m/1h/4h/D/W time frames (TF)

4MA (default values: SMA with lengths: 20–50–100–200)

Money Management Panel : in trading, money management is very important. Just put the % risk, & stop loss value below, the indicator will calculate a suitable size/amount for each trade.

Size by Lots: input stop loss in pips

Size by Units: input stop loss in % (of price)

(*)Units size is calculated by % stop loss & current bar close price. You have to determine a stop-loss price to convert to % stop loss by yourself.

TIME SEPARATORS

We can choose which time separators we want to display. The indicator has 5 options: Anchor Time/Day/Week/Month/Quarter. Of course, we can choose to show just one or all 5 of them.

With Anchor Time you can choose which time you want to draw a vertical line for better timing analysis. This can show up to 2 Anchor Time lines. The default values are 00:00 (New York Midnight Opening) and 08:30 (New York Session Opening). You also have an option to show the past lines or not.

About Day Separator, cause TradingView has supported Session Breaks in Setting but if you don't like to use it or when enabling, it distracts you, you can use mine. My favorite trading dates are Tuesday & Wednesday.

PRICE LEVELS

For intraday trading, the high/low/close of the previous day, the previous week, ADR (default period is 5) are very important key levels. You can choose which one you like to show for better analysis. Of course, you can change the color & style of the lines. This is also my favorite indicator.

This indicator also has an option to show up to 2 price lines at a specific time, you can choose the price type (high/low/close/open) that you want to display. The default time values are:

Specific Time 1: 0:00. (New York Midnight Opening Price)

Specific Time 2: 8:30 am. (New York Session Opening Price)

ACCUMULATION ZONE

The market tends to reprice the higher/lower to the old high/low or imbalance/fair value price to promote buy/sell stops or to provide smart money pricing for long/short entries. Typically, it redistributes quickly and you must learn to anticipate them at key levels intraday. Weak short/long holders will be squeezed in the retracement.

Except for the open price, the price changes continuously until the closing time, so the accumulation area can also be changed in real-time, but if you combine it with other information when analyzing, you can predict/determine whether the zone has been established or not with high probability. In short, price needs time to be accumulated, I usually don't pay attention to this daily zone till London open/close or New York sessions

Not only daily zone, but the indicator also supports higher timeframes accumulation zone from

SESSION & STD

There are 3 sessions: Asian, London, New York. The default values are below (New York Time).

Asian: 19:00 ~ 00:00

London Open (London KillZone): 01:00 ~ 05:00

New York Open (New York KillZone): 07:00 ~ 10:00

If you do not want to show the label, just leave the label values blank or change them to whatever you want.

This is one of my favorite functions. I use it on 15m, 30m, 1h TF for Forex intraday trading. My favorite trading sessions are London Open & New York Open.

You also can choose to show or not Standard Deviations (STD). The default values are set for Asian Range STD and max STD levels can be shown are 5. I use the following 3 types of STD (New York Time):

CBDR (Central Bank Deviations) STD: 14:00 ~ 20:00

Flout STD: 15:00 ~00:00

Asian Range STD: 19:00 ~ 00:00

LOOKBACK HIGH/LOW/MID

Can show high/low/mid of the data ranges on the daily/4h chart. The default values are:

- 20–40–60 days back from today for daily TF.

- 30–60–90 bars back from the latest bar for 4h TF.

The default anchor bar for calculating the lookback is the latest one but with:

- 4h TF: we can change the lookback from the 1st day of the week.

- Daily TF: we can change the lookback from the 1st day of the month.

The indicator also has options showing the high/low/mid (equilibrium level) lines for better analysis. Especially, on daily TF, we have the option that can show up to 4 lines (25% for each one) of the data range.

Of course, you can change the colors or the style of the high/low/mid lines.

The lookback can be shown on the lower TFs for better detection when the market structure is shifted.

MAGIC BARS

Fractal bar : The bar's color is changed when the divergence occurs between the price & RSI. You can change the RSI period (default value is 14) & RSI source. (open/high/low/close,…)

Imbalance bar or liquidity void or fair value gap - whatever you call it. This is my favorite indicator when trading on all TFs.You can choose to extend the last n imbalance bars if you like in the settings. I make sure I covered all cases of imbalance/fair value gap.

OLD HIGH/LOW

First, this function is not used as the common Support & Resistance that retail traders usually use, so I call it Old High/Low. I usually use it in 2 ways:

Detect the next buy/sell stops that Market Makers aim to manipulate.

Detect whether market structure shifted or not (Break of structure)

In settings you can:

Set the period to detect high/low levels, the default value is 10. My other favorite values are 6 & 2.

On a lower time frame, you might want to set it to a large number to remove noise.

On a higher time frame, a small number is enough, I think.

Choose the numbers of the last lines you want to show on your chart.

Of course, the style of lines can be changed easily.

TRENDLINES

A very simple trendline with default pivot left strength is 10.

By default, trendline uses high/low price but you have the "Using close price" option.

LINEAR REGRESSION CHANNEL

The Linear Regression Channel is a three-line technical indicator used to analyze the upper and lower limits of an existing trend. It is a statistical tool used to predict the future from past data and is used to determine trend direction or when prices may be overextended.

You can choose

To fill the background or not

To show inner/outer lines or not

To change the colors/line styles of upper zone, lower zone, upper lines, lower lines, midline

DIRECTION BOX

Working on all TFs, this looks like the same with lookback function but if you would like to display them in a box for easily focusing/comparing with other symbols or for detecting divergence in a specific period. The indicator also has a setting to show or hide lines connecting between lows or highs.

Another example of how I use High/Low connecting lines to detect divergence between S&P 500 and NASDAQ 100.

ZIG ZAG

Can show up to 2 ZigZag lines.

This is suitable for traders who have difficulty in detecting key levels (recent high/low) of the prices to confirm market structure or just for drawing Fibonacci easily at those levels.

MA (Moving Average)

I believe that this is one of the most used indicators for every trader. There are 5 types of MA to choose from: EMA, SMA, WMA, VWMA, SMMA(RMA).

This can show up to 4 MAs. You can choose the source (close/high/low,…) for each one. My favorite values are 34 & 89 EMA.

This indicator also supports MA Bands. You can select which MA you want to display the bands, and the "width" of the bands can be changed via the settings.

WATERMARK

It's just a simple function but I think it's very useful for those who want to add Copyright info to the chart, to prevent others from copying it.

Others/known issues/limitations

In forex or stock (things that are traded only on weekdays), TradingView's does not include the latest bars till Monday so the Day Separator cannot fill that space. Because TradingView deals with those bars as Sunday's ones so I set the color of Sunday the same as Friday for good UI/UX. On Crypto charts, the indicator shows without problems.

If you see "Internal server study error", please try closing the current TradingView tab in your browser and reopening it in a new tab. The error will disappear.

Because TradingView does not provide any detailed error information when such "general error" occurs. It's very difficult to detect which function is causing this error or is there something that caused TradingView "overloaded" through a long time running/loading on that tab? Honestly, I don't know exactly the cause, but in my experience, this error often occurs in the following cases:

When you have the TradingView Tab open for hours. In my case, I usually leave TradingView tab open overnight & when I come back the next day, this error might appear. (I'm a Mac user & I almost never shut down my Mac)

When you change settings too many times, especially settings of drawing objects like line width in a using session, it might cause this error.

So, after changing the setting or when you come back for the next trade, please save & close that TradingView tab, and then open a new one, everything will work fine.

You can see the images below that show I have tested my indicator from 1-minute time frame, enabled all functions, change every setting to max values & everything still works fine.

ICT Index Futures Session LinesICT Index Futures Session Lines

Description:

The script is based on one of ICT's concepts on trading Index Futures. The script lays out the daily range from an intraday basis.

Range:

00:00 - New York Midnight

08:30 – New York Open (News events come out)

12:00/13:00 - New York Lunch (No trade time period)

13:30 - (Algorithm)

16:30 - Close

* The open, high and low lines are plotted from 00:00 to 08:30

How To Use:

You will need to check the daily bias. Prior to 8:30 you are to look for previous swing points where liquidity may exist. During the open you want to see if a high or low is taken out, and then wait for an energetic break/displacement for a potential FVG/imbalance retracement entry.

Strategy is for LTF (1 to 15m)

Default time zone is set to America/New_York (UTC New York), so lines will be plotted correctly regardless of user’s local UTC chart setting.

Ticker SummaryTicker Summary provides at-a-glance summary information about a ticker near the current bar on the chart:

P/E ratio

Fwd P/E ratio

PEG ratio

Floating shares vs. total shares outstanding

% of trading volume that was short over the last 3 days

Average True Range (ATR) over last 14 days

There are a few less common items of information:

How many ATR multiples the ATR is extended over the last 10 bars. This gives an idea of how far the stock is currently extended.

"R-frequency", explained below.

An optional "ATR Reticule" is shown near the price. This is useful for traders that use ATR as a guideline for price targets and stop losses. On the left is the # of ATRs the stock is currently above the session open. On the right is the # of ATRs the stock is extended above the 10-bar moving average.

R-frequency: a measure of liquidity relevant to your own trading size. It is the frequency at which 1-R of your trading account is traded for a stock. Formula:

(1-R worth of shares) / (average dollar value traded per second), where:

"1-R worth of shares" is how many shares you would buy for a stop loss of -1 ATR, with max risk dollar value based on the Balance and Max Risk % indicator options.

"Average dollar value traded per second" is the 14-day average of (avg(high, low and close) * daily volume)

R-frequency of a second or less is very liquid. If the value is higher (for example, over 60 seconds) the stock is less liquid and you may have some trouble filling limit orders quickly.