Dinkan Price Action Pro | Pure Price Action Toolkit🔸 Overview

Dinkan Price Action Pro is a pure price-action research toolkit that automatically detects and visualizes Order Blocks (OB), Fair Value Gaps (FVG), merged-candle hidden structures, liquidity zones (including HTF bias liquidity), and trendline & chart-pattern liquidity.

This indicator helps traders align with the Higher Time Frame (HTF) bias — the direction of the dominant institutional wave — and uncover hidden candlestick structures that normal timeframe charts never show.

⚙️ Core Features

✅ Automatic Order Block detection (bullish & bearish)

✅ Fair Value Gaps with real-time fill tracking

✅ Merged-Candle Engine — reveals hidden structures between standard timeframes

✅ Liquidity Zones — equal highs/lows, trendline liquidity & HTF liquidity pools

✅ HTF Bias Engine — detect directional bias across multiple timeframes

✅ Auto Trendlines & Chart Pattern Liquidity

🔍 How It Works (Step by Step)

🕯️ A. Merged Candle Engine (Hidden Structure)

1️⃣ Choose how many candles to merge (e.g., 3–5).

2️⃣ The script groups candles backward from the current bar in continuous sets.

3️⃣ Each merged candle forms using:

• Open = first candle’s open • Close = last candle’s close

• High = highest high • Low = lowest low

4️⃣ These new candles expose “hidden” structures between fixed timeframes — revealing true base-impulse patterns missed by normal charts.

🟩 B. Order Block Detection

Detects consolidation (base) followed by strong impulse.

Marks demand (green) and supply (red) zones automatically.

Strength calculated using impulse range (and volume, if available).

Older, mitigated OBs can be hidden for clarity.

🟦 C. Fair Value Gaps (FVG)

Automatically detects imbalances between consecutive candles.

Unfilled FVGs are highlighted; once filled, zones fade or gray out.

Works dynamically across merged and standard candles.

🟧 D. Liquidity Zones

Finds equal highs/lows, wick clusters, and structural liquidity.

Trendline liquidity and chart-pattern liquidity detected in real time.

Projects HTF liquidity zones from higher charts down to current timeframe.

🔺 E. HTF Bias Engine

Analyzes higher and medium timeframes (HTF/MTF) using CISD-style confirmation.

Bias auto-adjusts or can be manually selected.

🧭 Purpose: Identify the dominant institutional flow and trade in its direction.

⏰ Timeframe Alignment

Recommended structure:

HTF: 4H or 1D

MTF: 1H or 30M

LTF: 15M or 5M

Users may let the script auto-adjust or manually configure each timeframe combination.

📘 Inputs & Settings

🔹 OB sensitivity (Low / Medium / High)

🔹 Volume weighting toggle

🔹 HTF & MTF selection (Auto / Manual)

🔹 Multi-symbol mode

🔹 Visual toggles (OB, FVG, trendlines, merged candles, bias labels)

🔹 Alert toggles (zone touch, bias flip, hidden structure detection)

📊 How to Use — Workflow Example

1️⃣ Load the indicator on your chart.

2️⃣ Check the HTF Bias direction — trade only in that direction.

3️⃣ Identify nearby Order Blocks or FVGs inside HTF liquidity areas.

4️⃣ Watch the Merged Candle View to confirm hidden structures (base + impulse).

5️⃣ Wait for LTF confirmation (e.g., small structure break, wick rejection).

6️⃣ Place stop beyond the opposite OB edge; target next liquidity cluster.

🎯 This workflow aligns your lower-timeframe trades with the dominant higher-timeframe flow.

🧱 Repainting & Stability

Completed OBs and FVGs remain static — they do not repaint.

Real-time zones during candle formation can update until candle closes (standard behavior).

Merged candles are recalculated each bar; once a group closes, it remains fixed historically.

⚠️ Limitations

This is not a buy/sell signal generator.

Volume-weighted features require volume data.

Use responsible risk management and independent confirmation methods.

🔒 Invite-Only / Locked Code

The script is published as invite-only to protect proprietary implementations of:

The merged-candle engine

Liquidity and bias-detection heuristics

Invite-only publishing complies with TradingView rules.

All logic, purpose, and usage are fully described here for transparency.

🧩 Originality & Usefulness

This script is an original integrated system, not a simple mashup.

Each module is interconnected to provide a unified analytical process:

The Merged Candle Engine creates hybrid bars that expose hidden base–impulse patterns.

These merged bars feed into the Order Block and Fair Value Gap logic, refining zone accuracy.

The Liquidity Detector references those zones and merged bars to locate valid structural pools.

Finally, the HTF Bias Engine confirms directional context across multiple pairs and timeframes.

Together, these elements form a dynamic framework that interprets institutional footprints and structure flow — something no single indicator can achieve individually.

The combination produces new analytical value: a precise, adaptive HTF bias alignment and structure-based liquidity map in one visual system.

📜 Disclaimer

This tool is for educational and analytical use only.

It does not constitute financial advice.

Trading involves risk — always perform independent analysis and practice sound risk management.

Past performance does not guarantee future results.

Cari dalam skrip untuk "liquidity"

Smart Volume S/R Pro [The_lurker]مؤشر "Smart Volume S/R Pro " هو أداة تحليل فني متقدمة مصممة لمساعدة المتداولين في تحديد مستويات الدعم والمقاومة القوية بناءً على حجم التداول، مع إضافة ميزات تحليلية متطورة مثل تصفية الاتجاه ، مناطق الثقة ، تقييم القوة ، حساب احتمالية الاختراق ، قياس السيولة ، تحديد الأهداف السعرية ، ومستويات فيبوناتشي . وايضا تقديم تسميات (Labels) بجانب كل مستوى دعم ومقاومة، تحتوي على أرقام ومعلومات دقيقة تعكس حالة السوق. هذه التسميات ليست مجرد زينة، بل أدوات تحليلية تساعد المتداولين على اتخاذ قرارات مستنيرة بناءً على بيانات السوقيهدف هذا المؤشر إلى توفير رؤية شاملة للسوق .

الوظائف الرئيسية للمؤشر

1- تحديد مستويات الدعم والمقاومة بناءً على حجم التداول العالي

يقوم المؤشر بتحليل الأشرطة (Bars) السابقة (حتى 300 شريط افتراضيًا) لتحديد النقاط التي شهدت أعلى مستويات حجم التداول.

يرسم خطوط أفقية تمثل مستويات المقاومة (عند أعلى سعر في تلك الأشرطة) والدعم (عند أدنى سعر)، ويمكن للمستخدم اختيار عدد الخطوط المعروضة (من 1 إلى 6).

2- تصفية الاتجاه باستخدام مؤشر ADX

يستخدم المؤشر مؤشر الاتجاه المتوسط (ADX) لتقييم قوة الاتجاه في السوق.

عندما تكون قوة الاتجاه عالية (تتجاوز عتبة محددة، 25 افتراضيًا)، يقلل المؤشر عدد مستويات الدعم والمقاومة المعروضة للتركيز فقط على المستويات الأكثر أهمية.

3- مناطق الثقة الديناميكية

يضيف المؤشر مناطق حول مستويات الدعم والمقاومة بناءً على متوسط المدى الحقيقي (ATR)، مما يساعد المتداولين على تصور النطاقات التي قد يتفاعل فيها السعر مع هذه المستويات.

يمكن تعديل عرض هذه المناطق باستخدام مضاعف ATR.

4- تقييم قوة المستويات

يحسب المؤشر قوة كل مستوى بناءً على حجم التداول، عدد المرات التي تم اختبار المستوى فيها (Touch Count)، وقرب السعر الحالي من المستوى.

يتم عرض درجة القوة (من 0 إلى 100) بجانب كل مستوى إذا تم تفعيل هذه الخاصية.

5- احتمالية الاختراق

يقدّر المؤشر احتمالية اختراق كل مستوى بناءً على الزخم (ROC)، قوة المستوى، والمسافة بين السعر الحالي والمستوى.

يظهر الاحتمال كنسبة مئوية إذا تم تفعيل الخيار، مما يساعد المتداولين على توقع الحركات المحتملة.

6- تحليل السيولة التاريخية

يقيس المؤشر السيولة حول كل مستوى بناءً على حجم التداول في النطاقات القريبة منه.

يمكن عرض قيم السيولة في التسميات أو استخدامها لتعديل عرض الخطوط (الخطوط الأكثر سيولة تظهر أعرض).

7- الأهداف السعرية

عند تفعيل هذه الخاصية، يحسب المؤشر أهداف سعرية للاختراق (Breakout) والارتداد (Reversal) بناءً على الزخم وقوة المستوى وATR.

يمكن عرض هذه الأهداف كنصوص في التسميات أو كخطوط أفقية على الرسم البياني.

8- مستويات فيبوناتشي

يرسم المؤشر مستويات فيبوناتشي (0.0، 0.236، 0.382، 0.5، 0.618، 0.786، 1.0) بناءً على أعلى وأدنى سعر في فترة النظرة الخلفية.

يمكن للمستخدم اختيار أي من هذه المستويات لعرضها أو إخفائها.

9- تنبيه شامل للاختراق

يوفر المؤشر تنبيهًا واحدًا يشمل جميع المستويات، حيث يُطلق التنبيه عندما يخترق السعر أي مستوى دعم أو مقاومة مع رسالة توضح نوع الاختراق والمستوى المخترق.

كيفية عمل المؤشر

الخطوة الأولى: يحدد المؤشر الأشرطة ذات الحجم العالي خلال فترة النظرة الخلفية المحددة (Lookback Period).

الخطوة الثانية: يرسم مستويات الدعم والمقاومة بناءً على أعلى وأدنى الأسعار في تلك الأشرطة، مع مراعاة عدد الخطوط المختارة من المستخدم.

الخطوة الثالثة: يطبق مرشح الاتجاه (إذا كان مفعلاً) لتقليل عدد المستويات في حالة الاتجاه القوي.

الخطوة الرابعة: يضيف التحليلات الإضافية مثل القوة، السيولة، احتمالية الاختراق، والأهداف السعرية، ويرسم مناطق الثقة ومستويات فيبوناتشي حسب الإعدادات.

الخطوة الخامسة: يراقب السعر ويطلق تنبيهًا عند الاختراق.

الإعدادات القابلة للتخصيص

1- فترة النظرة الخلفية (Lookback Period): عدد الأشرطة التي يتم تحليلها (افتراضيًا 300).

2- عدد الخطوط (Number of Lines): من 1 إلى 6 مستويات دعم ومقاومة.

3- الألوان والأنماط: يمكن تغيير ألوان الخطوط وأنماطها (ممتلئة، متقطعة، منقطة).

4- التسميات: تفعيل/تعطيل التسميات، وحجمها، وموقعها، ولون النص.

5- مرشح الاتجاه: تفعيل/تعطيل ADX، وتعديل طوله وعتبته.

6- مناطق الثقة: تفعيل/تعطيل، وتعديل طول ATR ومضاعفه.

7- القوة واحتمالية الاختراق: تفعيل/تعطيل العرض، وتعديل طول ROC.

8- السيولة: تفعيل/تعطيل تأثير السيولة على عرض الخطوط وقيمها في التسميات.

9- الأهداف السعرية: تفعيل/تعطيل الأهداف وعرضها كخطوط.

10- فيبوناتشي: اختيار المستويات المعروضة ولون الخطوط.

فوائد المؤشر

دقة عالية: يعتمد على حجم التداول لتحديد المستويات، مما يجعله أكثر موثوقية من المستويات العشوائية.

مرونة: يوفر خيارات تخصيص واسعة تتيح للمتداولين تكييفه حسب استراتيجياتهم.

تحليل شامل: يجمع بين الدعم والمقاومة، الاتجاه، السيولة، والأهداف في أداة واحدة.

سهولة الاستخدام: التسميات والتنبيهات تجعل من السهل متابعة السوق دون تعقيد.

==================================================================================تسميات (Labels) بجانب كل مستوى دعم ومقاومة، تحتوي على أرقام ومعلومات دقيقة تعكس حالة السوق. هذه التسميات ليست مجرد زينة، بل أدوات تحليلية تساعد المتداولين على اتخاذ قرارات مستنيرة بناءً على بيانات السوق. في هذا الشرح، سنستعرض كل رقم أو قيمة تظهر في التسميات ومعناها العملي.

مكونات التسميات

التسميات تظهر بجانب كل مستوى دعم (Support) ومقاومة (Resistance) وتبدأ بحرف "S" للدعم أو "R" للمقاومة، تليها مجموعة من الأرقام والقيم التي يمكن تفعيلها أو تعطيلها حسب إعدادات المستخدم. إليك تفصيل كل عنصر:

1- عدد اللمسات (Touch Count)

الرمز: يظهر مباشرة بعد "S" أو "R" (مثال: "R: 5" أو "S: 3").

المعنى: يشير إلى عدد المرات التي اختبر فيها السعر هذا المستوى دون اختراقه.

الفائدة: كلما زاد عدد اللمسات، كلما كان المستوى أقوى وأكثر أهمية. على سبيل المثال، إذا كان "R: 5"، فهذا يعني أن السعر ارتد من هذا المستوى 5 مرات، مما يجعله مقاومة قوية محتملة.

2- قوة المستوى (Strength Rating)

الرمز: يظهر بين قوسين مربعين (مثال: " ").

المعنى: قيمة من 0 إلى 100 تعكس قوة المستوى بناءً على عوامل مثل حجم التداول، عدد اللمسات، وقرب السعر الحالي من المستوى.

الفائدة: القيم العالية (مثل 75 أو أكثر) تشير إلى مستوى قوي يصعب اختراقه، بينما القيم المنخفضة (مثل 30 أو أقل) تدل على ضعف المستوى وسهولة اختراقه. يمكن للمتداول استخدام هذا لتحديد المستويات الأكثر موثوقية.

3- احتمالية الاختراق (Breakout Probability)

الرمز: يبدأ بحرف "B" متبوعًا بنسبة مئوية (مثال: "B: 60%").

المعنى: نسبة من 0% إلى 100% تُظهر احتمالية اختراق السعر للمستوى بناءً على الزخم الحالي، قوة المستوى، والمسافة بين السعر والمستوى.

الفائدة: نسبة مرتفعة (مثل 60% أو أكثر) تعني أن السعر قد يخترق المستوى قريبًا، بينما النسب المنخفضة (مثل 20%) تشير إلى احتمال ارتداد السعر. هذا مفيد لتوقع الحركة التالية.

4- قيمة السيولة (Liquidity Value)

الرمز: يبدأ بحرف "L" متبوعًا برقم (مثال: "L: 1200").

المعنى: يمثل متوسط حجم التداول في النطاق القريب من المستوى، مما يعكس السيولة التاريخية حوله.

الفائدة: القيم العالية تدل على وجود سيولة كبيرة، مما يعني أن السعر قد يتفاعل بقوة مع هذا المستوى (إما بالارتداد أو الاختراق). القيم المنخفضة تشير إلى سيولة ضعيفة، مما قد يجعل المستوى أقل تأثيرًا.

5- الأهداف السعرية (Price Targets)

الرمز: يبدأ بـ "BT" (هدف الاختراق) و"RT" (هدف الارتداد) متبوعين بأرقام (مثال: "BT: 150.50 RT: 148.20").

المعنى:

BT (Breakout Target): السعر المحتمل الذي قد يصل إليه السعر بعد اختراق المستوى.

RT (Reversal Target): السعر المحتمل الذي قد يصل إليه السعر إذا ارتد من المستوى.

الفائدة: تساعد المتداولين في تحديد نقاط الخروج المحتملة بعد الاختراق أو الارتداد، مما يسهل وضع خطة تداول دقيقة.

أمثلة عملية

تسمية مقاومة: "R: 4 B: 25% L: 1500 BT: 155.00 RT: 152.00"

المستوى اختُبر 4 مرات، قوته 80 (قوي جدًا)، احتمالية الاختراق 25% (منخفضة، أي احتمال ارتداد أعلى)، السيولة 1500 (مرتفعة)، هدف الاختراق 155.00، هدف الارتداد 152.00.

الاستنتاج: المستوى قوي ومن المرجح أن يرتد السعر منه، لكن إذا اخترق، فقد يصل إلى 155.00.

تسمية دعم: "S: 2 B: 70% L: 800 BT: 145.00 RT: 147.50"

المستوى اختُبر مرتين، قوته 40 (متوسطة إلى ضعيفة)، احتمالية الاختراق 70% (مرتفعة)، السيولة 800 (متوسطة)، هدف الاختراق 145.00، هدف الارتداد 147.50.

الاستنتاج: المستوى ضعيف ومن المحتمل أن يخترقه السعر ليهبط إلى 145.00.

كيفية الاستفادة من التسميات

تحديد القوة والضعف: استخدم قوة المستوى (Strength) لمعرفة ما إذا كان المستوى موثوقًا للارتداد أو عرضة للاختراق.

توقع الحركة: انظر إلى احتمالية الاختراق (Breakout Probability) لتحديد ما إذا كنت ستنتظر اختراقًا أو ترتدًا.

إدارة المخاطر: استخدم الأهداف السعرية (BT وRT) لتحديد نقاط جني الأرباح أو وقف الخسارة.

تقييم السيولة: ركز على المستويات ذات السيولة العالية لأنها غالبًا تكون نقاط تحول رئيسية في السوق.

تأكيد التحليل: ادمج عدد اللمسات مع القوة والسيولة للحصول على صورة كاملة عن أهمية المستوى.

تخصيص التسميات

يمكن للمستخدم تفعيل أو تعطيل أي من هذه القيم (القوة، الاحتمالية، السيولة، الأهداف) من إعدادات المؤشر.

يمكن أيضًا تغيير حجم التسميات (صغير، عادي، كبير)، موقعها (يمين، يسار، أعلى، أسفل)، ولون النص لتناسب احتياجاتك.

التسميات في هذا المؤشر هي بمثابة لوحة تحكم صغيرة بجانب كل مستوى دعم ومقاومة، تقدم لك معلومات فورية عن قوته، احتمالية اختراقه، سيولته، وأهدافه السعرية. بفهم هذه الأرقام، يمكنك تحسين قراراتك في التداول، سواء كنت تبحث عن نقاط دخول، خروج، أو إدارة مخاطر. إذا كنت تريد أداة تجمع بين البساطة والعمق التحليلي .

تنويه:

المؤشر هو أداة مساعدة فقط ويجب استخدامه مع التحليل الفني والأساسي لتحقيق أفضل النتائج.

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView.

The Smart Volume S/R Pro indicator is an advanced technical analysis tool designed to help traders identify strong support and resistance levels based on trading volume, with the addition of advanced analytical features such as trend filtering, confidence zones, strength assessment, breakout probability calculation, liquidity measurement, price target identification, and Fibonacci levels. It also provides labels next to each support and resistance level, containing accurate numbers and information that reflect the market condition. These labels are not just decorations, but analytical tools that help traders make informed decisions based on market data. This indicator aims to provide a comprehensive view of the market.

Main functions of the indicator

1- Identifying support and resistance levels based on high trading volume

The indicator analyzes previous bars (up to 300 bars by default) to identify the points that witnessed the highest levels of trading volume.

It draws horizontal lines representing resistance levels (at the highest price in those bars) and support (at the lowest price), and the user can choose the number of lines displayed (from 1 to 6).

2- Filtering the trend using the ADX indicator

The indicator uses the Average Directional Index (ADX) to assess the strength of a trend in the market.

When the strength of the trend is high (exceeding a specified threshold, 25 by default), the indicator reduces the number of support and resistance levels displayed to focus only on the most important levels.

3- Dynamic Confidence Zones

The indicator adds zones around support and resistance levels based on the Average True Range (ATR), helping traders visualize the ranges in which the price may interact with these levels.

The width of these zones can be adjusted using the ATR multiplier.

4- Assessing the Strength of Levels

The indicator calculates the strength of each level based on trading volume, the number of times the level has been tested (Touch Count), and the proximity of the current price to the level.

A strength score (from 0 to 100) is displayed next to each level if this feature is enabled.

5- Breakout Probability

The indicator estimates the probability of breaking each level based on momentum (ROC), the strength of the level, and the distance between the current price and the level.

The probability is displayed as a percentage if the option is enabled, helping traders anticipate potential moves.

6- Historical Liquidity Analysis

The indicator measures liquidity around each level based on the trading volume in the ranges near it.

The liquidity values can be displayed in the labels or used to adjust the width of the lines (the most liquid lines appear wider).

7- Price Targets

When this feature is enabled, the indicator calculates price targets for breakout and reversal based on momentum, level strength and ATR.

These targets can be displayed as text in the labels or as horizontal lines on the chart.

8- Fibonacci Levels

The indicator plots Fibonacci levels (0.0, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0) based on the highest and lowest price in the lookback period.

The user can choose which of these levels to display or hide.

9- Comprehensive Breakout Alert

The indicator provides a single alert that includes all levels, where the alert is triggered when the price breaks any support or resistance level with a message explaining the type of breakout and the level broken.

How the indicator works

Step 1: The indicator identifies the bars with high volume during the specified Lookback Period.

Step 2: Draws support and resistance levels based on the highest and lowest prices in those bars, taking into account the number of lines selected by the user.

Step 3: Apply the trend filter (if enabled) to reduce the number of levels in case of a strong trend.

Step 4: Adds additional analyses such as strength, liquidity, breakout probability, and price targets, and draws confidence zones and Fibonacci levels according to the settings.

Step 5: Monitors the price and triggers an alert when the breakout occurs.

Customizable Settings

1- Lookback Period: Number of bars to analyze (default 300).

2- Number of Lines: From 1 to 6 support and resistance levels.

3- Colors and Styles: Line colors and styles can be changed (filled, dashed, dotted).

4- Labels: Enable/disable labels, their size, location, and text color.

5- Trend Filter: Enable/disable ADX, and modify its length and threshold.

6- Confidence Zones: Enable/disable, and modify the ATR length and multiplier.

7- Strength and Breakout Probability: Enable/disable the display, and modify the ROC length.

8- Liquidity: Enable/disable the effect of liquidity on the display of the lines and their values in the labels.

9- Price Targets: Enable/disable the targets and display them as lines.

10- Fibonacci: Choose the displayed levels and the color of the lines.

Indicator Benefits

High Accuracy: It relies on trading volume to determine the levels, which makes it more reliable than random levels.

Flexibility: It provides extensive customization options that allow traders to adapt it to their strategies.

Comprehensive Analysis: Combines support and resistance, trend, liquidity, and targets in one tool. Ease of Use: Labels and alerts make it easy to follow the market without complexity.

Labels next to each support and resistance level contain accurate numbers and information that reflect the market situation. These labels are not just decorations, but analytical tools that help traders make informed decisions based on market data. In this explanation, we will review each number or value that appears in the labels and their practical meaning.

Label Components

Labels appear next to each support and resistance level and begin with the letter "S" for support or "R" for resistance, followed by a set of numbers and values that can be enabled or disabled according to the user's settings. Here is a breakdown of each element:

1- Touch Count

Symbol: Appears immediately after "S" or "R" (example: "R: 5" or "S: 3").

Meaning: Indicates the number of times the price has tested this level without breaking it.

Benefit: The more touches, the stronger and more important the level. For example, if it is "R: 5", it means that the price has bounced off this level 5 times, making it a potentially strong resistance.

2- Strength Rating

Symbol: Appears between square brackets (example: " ").

Meaning: A value from 0 to 100 that reflects the strength of the level based on factors such as trading volume, number of touches, and proximity of the current price to the level.

Benefit: High values (such as 75 or more) indicate a strong level that is difficult to break, while low values (such as 30 or less) indicate a weak level that is easy to break. A trader can use this to determine the most reliable levels.

3- Breakout Probability

Symbol: Starts with the letter "B" followed by a percentage (example: "B: 60%").

Meaning: A percentage from 0% to 100% that shows the probability of the price breaking the level based on the current momentum, the strength of the level, and the distance between the price and the level.

Interest: A high percentage (such as 60% or more) means that the price may soon break through the level, while low percentages (such as 20%) indicate that the price may bounce. This is useful for anticipating the next move.

4- Liquidity Value

Symbol: Starts with the letter "L" followed by a number (example: "L: 1200").

Meaning: Represents the average trading volume in the range near the level, reflecting historical liquidity around it.

Interest: High values indicate high liquidity, meaning that the price may react strongly to this level (either by bouncing or breaking through). Low values indicate low liquidity, which may make the level less influential.

5- Price Targets

Symbol: Starts with "BT" (breakout target) and "RT" (rebound target) followed by numbers (example: "BT: 150.50 RT: 148.20").

Meaning:

BT (Breakout Target): The potential price that the price may reach after breaking the level.

RT (Reversal Target): The potential price that the price may reach if it rebounds from the level.

Utility: Helps traders identify potential exit points after a breakout or rebound, making it easier to develop an accurate trading plan.

Working examples

Resistance label: "R: 4 B: 25% L: 1500 BT: 155.00 RT: 152.00"

Level tested 4 times, strength 80 (very strong), probability of breakout 25% (low, i.e. higher probability of rebound), liquidity 1500 (high), breakout target 155.00, rebound target 152.00.

Conclusion: The level is strong and the price is likely to rebound from it, but if it breaks, it may reach 155.00.

Support Label: "S: 2 B: 70% L: 800 BT: 145.00 RT: 147.50"

Level tested twice, Strength 40 (medium to weak), Breakout Probability 70% (high), Liquidity 800 (medium), Breakout Target 145.00, Rebound Target 147.50.

Conclusion: The level is weak and the price is likely to break it to drop to 145.00.

How to use labels

Determine strength and weakness: Use the level's strength to see if the level is reliable for a bounce or vulnerable to a breakout.

Predict the move: Look at the Breakout Probability to determine whether to wait for a breakout or a bounce.

Risk Management: Use price targets (BT and RT) to set take profit or stop loss points.

Liquidity Evaluation: Focus on levels with high liquidity as they are often key turning points in the market.

Analysis Confirmation: Combine the number of touches with strength and liquidity to get a complete picture of the level’s importance.

Customize Labels

The user can enable or disable any of these values (strength, probability, liquidity, targets) from the indicator settings.

The size of the labels (small, normal, large), their position (right, left, top, bottom), and the color of the text can also be changed to suit your needs.

The labels in this indicator act as a small dashboard next to each support and resistance level, providing you with instant information about its strength, probability of breakout, liquidity, and price targets. By understanding these numbers, you can improve your trading decisions, whether you are looking for entry points, exit points, or risk management. If you want a tool that combines simplicity with analytical depth.

Disclaimer:

The indicator is an auxiliary tool only and should be used in conjunction with technical and fundamental analysis for best results.

Disclaimer

The information and posts are not intended to be, or constitute, any financial, investment, trading or other types of advice or recommendations provided or endorsed by TradingView.

OrderFlow [Adjustable] | FractalystWhat's the indicator's purpose and functionality?

This indicator is designed to assist traders in identifying real-time probabilities of buyside and sellside liquidity .

It allows for an adjustable pivot level , enabling traders to customize the level they want to use for their entries.

By doing so, traders can evaluate whether their chosen entry point would yield a positive expected value over a large sample size, optimizing their strategy for long-term profitability.

For advanced traders looking to enhance their analysis, the indicator supports the incorporation of up to 7 higher timeframe biases .

Additionally, the higher timeframe pivot level can be adjusted according to the trader's preferences,

Offering maximum adaptability to different strategies and needs, further helping to maximize positive EV.

EV=(P(Win)×R(Win))−(P(Loss)×R(Loss))

-----

What's the purpose of these levels? What are the underlying calculations?

1. Understanding Swing highs and Swing Lows

Swing High: A Swing High is formed when there is a high with 2 lower highs to the left and right.

Swing Low: A Swing Low is formed when there is a low with 2 higher lows to the left and right.

2. Understanding the purpose and the underlying calculations behind Buyside, Sellside and Pivot levels.

3. Identifying Discount and Premium Zones.

4. Importance of Risk-Reward in Premium and Discount Ranges

----

How does the script calculate probabilities?

The script calculates the probability of each liquidity level individually. Here's the breakdown:

1. Upon the formation of a new range, the script waits for the price to reach and tap into pivot level level. Status: "⏸" - Inactive

2. Once pivot level is tapped into, the pivot status becomes activated and it waits for either liquidity side to be hit. Status: "▶" - Active

3. If the buyside liquidity is hit, the script adds to the count of successful buyside liquidity occurrences. Similarly, if the sellside is tapped, it records successful sellside liquidity occurrences.

4. Finally, the number of successful occurrences for each side is divided by the overall count individually to calculate the range probabilities.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

----

What does the multi-timeframe functionality offer?

In the adjustable version of the orderflow indicator, you can incorporate up to 7 higher timeframe probabilities directly into the table.

This feature allows you to analyze the probabilities of buyside and sellside liquidity across multiple timeframes, without the need to manually switch between them.

By viewing these higher timeframe probabilities in one place, traders can spot larger market trends and refine their entries and exits with a better understanding of the overall market context.

This multi-timeframe functionality helps traders:

1. Simplify decision-making by offering a comprehensive view of multiple timeframes at once.

2. Identify confluence between timeframes, enhancing the confidence in trade setups.

3. Adapt strategies more effectively, as the higher timeframe pivot levels can be customized to meet individual preferences and goals.

----

What are the multi-timeframe underlying calculations?

The script uses the same calculations (mentioned above) and uses security function to request the data such as price levels, bar time, probabilities and booleans from the user-input timeframe.

----

How does the Indicator Identifies Positive Expected Values?

OrderFlow indicator instantly calculates whether a trade setup has the potential for positive expected value (EV) in the long run.

To determine a positive EV setup, the indicator uses the formula:

EV=(P(Win)×R(Win))−(P(Loss)×R(Loss))

where:

P(Win) is the probability of a winning trade.

R(Win) is the reward or return for a winning trade, determined by the current risk-to-reward ratio (RR).

P(Loss) is the probability of a losing trade.

R(Loss) is the loss incurred per losing trade, typically assumed to be -1.

By calculating these values based on historical data and the current trading setup, the indicator helps you understand whether your trade has a positive expected value over a large sample size.

----

How can I know that the setup I'm going to trade with has a postive EV?

If the indicator detects that the adjusted pivot and buy/sell side probabilities have generated positive expected value (EV) in historical data, the risk-to-reward (RR) label within the range box will be colored blue and red .

If the setup does not produce positive EV, the RR label will appear gray.

This indicates that even the risk-to-reward ratio is greater than 1:1, the setup is not likely to yield a positive EV because, according to historical data, the number of losses outweighs the number of wins relative to the RR gain per winning trade.

----

What is the confidence level in the indicator, and how is it determined?

The confidence level in the indicator reflects the reliability of the probabilities calculated based on historical data. It is determined by the sample size of the probabilities used in the calculations. A larger sample size generally increases the confidence level, indicating that the probabilities are more reliable and consistent with past performance.

----

How does the confidence level affect the risk-to-reward (RR) label?

The confidence level (★) is visually represented alongside the probability label. A higher confidence level indicates that the probabilities used to determine the RR label are based on a larger and more reliable sample size.

----

How can traders use the confidence level to make better trading decisions?

Traders can use the confidence level to gauge the reliability of the probabilities and expected value (EV) calculations provided by the indicator. A confidence level above 95% is considered statistically significant and indicates that the historical data supporting the probabilities is robust. This high confidence level suggests that the probabilities are reliable and that the indicator’s recommendations are more likely to be accurate.

In data science and statistics, a confidence level above 95% generally means that there is less than a 5% chance that the observed results are due to random variation. This threshold is widely accepted in research and industry as a marker of statistical significance. Studies such as those published in the Journal of Statistical Software and the American Statistical Association support this threshold, emphasizing that a confidence level above 95% provides a strong assurance of data reliability and validity.

Conversely, a confidence level below 95% indicates that the sample size may be insufficient and that the data might be less reliable . In such cases, traders should approach the indicator’s recommendations with caution and consider additional factors or further analysis before making trading decisions.

----

How does the sample size affect the confidence level, and how does it relate to my TradingView plan?

The sample size for calculating the confidence level is directly influenced by the amount of historical data available on your charts. A larger sample size typically leads to more reliable probabilities and higher confidence levels.

Here’s how the TradingView plans affect your data access:

Essential Plan

The Essential Plan provides basic data access with a limited amount of historical data. This can lead to smaller sample sizes and lower confidence levels, which may weaken the robustness of your probability calculations. Suitable for casual traders who do not require extensive historical analysis.

Plus Plan

The Plus Plan offers more historical data than the Essential Plan, allowing for larger sample sizes and more accurate confidence levels. This enhancement improves the reliability of indicator calculations. This plan is ideal for more active traders looking to refine their strategies with better data.

Premium Plan

The Premium Plan grants access to extensive historical data, enabling the largest sample sizes and the highest confidence levels. This plan provides the most reliable data for accurate calculations, with up to 20,000 historical bars available for analysis. It is designed for serious traders who need comprehensive data for in-depth market analysis.

PRO+ Plans

The PRO+ Plans offer the most extensive historical data, allowing for the largest sample sizes and the highest confidence levels. These plans are tailored for professional traders who require advanced features and significant historical data to support their trading strategies effectively.

For many traders, the Premium Plan offers a good balance of affordability and sufficient sample size for accurate confidence levels.

----

What is the HTF probability table and how does it work?

The HTF (Higher Time Frame) probability table is a feature that allows you to view buy and sellside probabilities and their status from timeframes higher than your current chart timeframe.

Here’s how it works:

Data Request : The table requests and retrieves data from user-defined higher timeframes (HTFs) that you select.

Probability Display: It displays the buy and sellside probabilities for each of these HTFs, providing insights into the likelihood of price movements based on higher timeframe data.

Detailed Tooltips: The table includes detailed tooltips for each timeframe, offering additional context and explanations to help you understand the data better.

----

What do the different colors in the HTF probability table indicate?

The colors in the HTF probability table provide visual cues about the expected value (EV) of trading setups based on higher timeframe probabilities:

Blue: Suggests that entering a long position from the HTF user-defined pivot point, targeting buyside liquidity, is likely to result in a positive expected value (EV) based on historical data and sample size.

Red: Indicates that entering a short position from the HTF user-defined pivot point, targeting sellside liquidity, is likely to result in a positive expected value (EV) based on historical data and sample size.

Gray: Shows that neither long nor short trades from the HTF user-defined pivot point are expected to generate positive EV, suggesting that trading these setups may not be favorable.

----

How to use the indicator effectively?

For Amateur Traders:

Start Simple: Begin by focusing on one timeframe at a time with the pivot level set to the default (50%). This helps you understand the basic functionality of the indicator.

Entry and Exit Strategy: Focus on entering trades at the pivot level while targeting the higher probability side for take profit and the lower probability side for stop loss.

Use simulation or paper trading to practice this strategy.

Adjustments: Once you have a solid understanding of how the indicator works, you can start adjusting the pivot level to other values that suit your strategy.

Ensure that the RR labels are colored (blue or red) to indicate positive EV setups before executing trades.

For Advanced Traders:

1. Select Higher Timeframe Bias: Choose a higher timeframe (HTF) as your main bias. Start with the default pivot level and ensure the confidence level is above 95% to validate the probabilities.

2. Align Lower Timeframes: Switch between lower timeframes to identify which ones align with your predefined HTF bias. This helps in synchronizing your trading decisions across different timeframes.

3. Set Entries with Current Pivot Level: Use the current pivot level for trade entries. Ensure the HTF status label is active, indicating that the probabilities are valid and in play.

4. Target HTF Liquidity Level: Aim for liquidity levels that correspond to the higher timeframe, as these levels are likely to offer better trading opportunities.

5. Adjust Pivot Levels: As you gain experience, adjust the pivot levels to further optimize your strategy for high EV. Fine-tune these levels based on the aggregated data from multiple timeframes.

6. Practice on Paper Trading: Test your strategies through paper trading to eliminate discretion and refine your approach without financial risk.

7. Focus on Trade Management: Ultimately, effective trade management is crucial. Concentrate on managing your trades well to ensure long-term success. By aiming for setups that produce positive EV, you can position yourself similarly to how a casino operates.

----

🎲 Becoming the House (Gaining Edge Over the Market):

In American roulette, the house has a 5.26% edge due to the 0 and 00. This means that while players have a 47.37% chance of winning on even-money bets, the true odds are 50%. The discrepancy between the true odds and the payout ensures that, statistically, the casino will win over time.

From the Trader's Perspective: In trading, you gain an edge by focusing on setups with positive expected value (EV). If you have a 55.48% chance of winning with a 1:1 risk-to-reward ratio, your setup has a higher probability of profitability than the losing side. By consistently targeting such setups and managing your trades effectively, you create a statistical advantage, similar to the casino’s edge.

----

🎰 Applying the Concept to Trading:

Just as casinos rely on their mathematical edge, you can achieve long-term success in trading by focusing on setups with positive EV. By ensuring that your probabilities and risk-to-reward (RR) ratios are in your favor, you create an edge similar to that of the house.

And by systematically targeting trades with favorable probabilities and managing your trades effectively, you improve your chances of profitability over the long run. Which is going to help you “become the house” in your trading, leveraging statistical advantages to enhance your overall performance.

----

What makes this indicator original?

Real-Time Probability Calculations: The indicator provides real-time calculations of buy and sell probabilities based on historical data, allowing traders to assess the likelihood of positive expected value (EV) setups instantly.

Adjustable Pivot Levels: It features an adjustable pivot level that traders can modify according to their preferences, enhancing the flexibility to align with different trading strategies.

Multi-Timeframe Integration: The indicator supports up to 7 higher timeframes, displaying their probabilities and biases in a single view, which helps traders make informed decisions without switching timeframes.

Confidence Levels: It includes confidence levels based on sample sizes, offering insights into the reliability of the probabilities. Traders can gauge the strength of the data before making trades.

Dynamic EV Labels: The indicator provides color-coded EV labels that change based on the validity of the setup. Blue indicates positive EV in a long bias, red indicates positive EV in a short bias and gray signals caution, making it easier for traders to identify high-quality setups.

HTF Probability Table: The HTF probability table displays buy and sell probabilities from user-defined higher timeframes, helping traders integrate broader market context into their decision-making process.

----

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

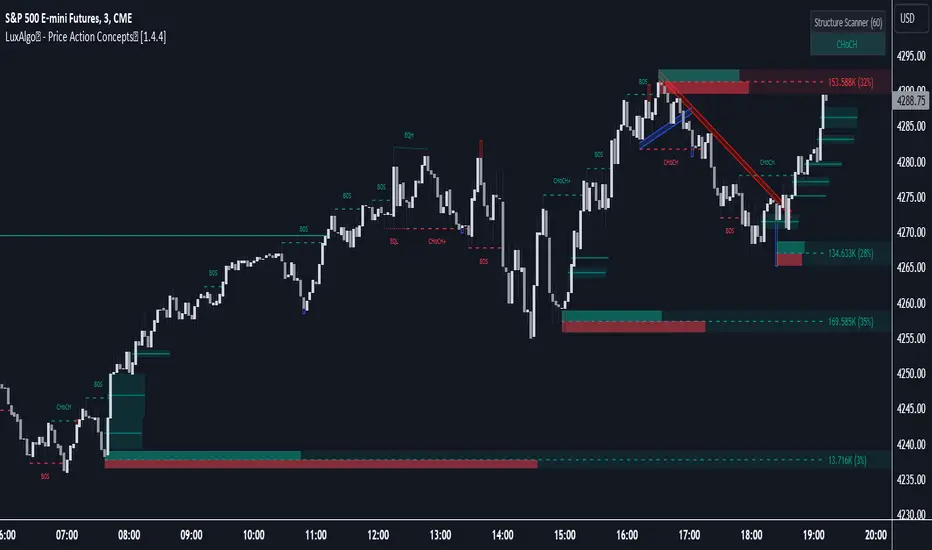

LuxAlgo® - Price Action Concepts™Price Action Concepts™ is a first of it's kind all-in-one indicator toolkit which includes various features specifically based on pure price action.

Order Blocks w/ volume data, real-time market structure (BOS, CHoCH, EQH/L) w/ 'CHoCH+' being a more confirmed reversal signal, a MTF dashboard, Trend Line Liquidity Zones (real-time), Chart Pattern Liquidity Zones, Liquidity Grabs, and much more detailed customization to get an edge trading price action automatically.

Many traders argue that trading price action is better than using technical indicators due to lag, complexity, and noisy charts. Popular ideas within the trading space that cater towards price action trading include "trading like the banks" or "Smart Money Concepts trading" (SMC), most prominently known within the forex community.

What differentiates price action trading from others forms of technical analysis is that it's main focus is on raw price data opposed to creating values or plots derived from price history.

Mostly all of the features within this script are generated purely from price action, more specifically; swing highs, swing lows, and market structure... which allows users to automate their analysis of price action for any market / timeframe.

🔶 FEATURES

This script includes many features based on Price Action; these are highlighted below:

Market structure (BOS, CHoCH, CHoCH+, EQH/L) (Internal & Swing) multi-timeframe

Volumetric Order Blocks & mitigation methods (bullish & bearish)

Liquidity Concepts

Trend Line Liquidity Zones

Chart Pattern Liquidity

Liquidity Grabs Feature

Imbalance Concepts MTF w/ multiple mitigation methods

Fair Value Gaps

Balanced Price Range

Activity Asymmetry

Strong/Weak Highs & Lows w/ volume percentages

Premium & Discount Zones included

Candle Coloring based on market structure

Previous Highs/Lows (Daily, Monday's, Weekly, Monthly, Quarterly)

Multi-Timeframe Dashboard (15m, 1h, 4h, 1d)

Built-in alert conditions & Any Alert() Function Call Conditions

Advanced Alerts Creator to create step-by-step alerts with various conditions

+ more (see changelog below for current features)

🔶 BASIC DEMONSTRATION

In the image above we can see a demonstration of the market structure labeling within this indicator. The automatic BOS & CHoCH labels on top of dashed lines give clear indications of breakouts & reversals within the internal market structure (short term price action). The "CHoCH+" label is also demonstrated as it triggers only if price has already made a new higher low, or lower high.

We can also see a solid line with a larger BOS label in the middle of the chart. This label demonstrates a break of structure taking into account the swing market structure (longer term price action). All of these labels are generated in real-time.

🔶 USAGE & EXAMPLES

In the image below we can see how a trade setup could be created using Order Blocks w/ volume metrics to find points of interest in the market, swing / internal market structure to get indications of longer & shorter term reversals, and trend line liquidity zones to find more likely impulses & breakouts within trends.

We can see in the next image below that price came down to the highest volume order block marked out previously as our point of interest for an entry used in confluence with the overall market structure being bullish (swing CHoCH). Due to price closing below the middle Order Block at (24.77%), we saw it was mitigated, and then price revisited liquidity above the Trend Line zone above, leading us to the first Order Block as a target.

You will notice the % values adjust as Order Blocks are touched & mitigated, aligning with the correct volume detected when the Order Block was established.

In the image below we can see more features from within Price Action Concepts™ indicator, including Chart Pattern Liquidity, Fair Value Gaps (one of many Imbalance Concepts), Liquidity Grabs, as well as the primary market structures & OBs.

By using multiple features as such, users can develop a greater interpretation of where liquidity rests in the market, which allows them to develop trading plans a lot easier. Liquidity Grabs are highlighted as blue/red boxes on the wicks during specific price action that indicates the market has made an impulse specifically to take out resting buy or sell side orders.

We can notice in the trade demonstrated below (hindsight example) how price often moves to the areas of the most liquidity, even if unexpected according to classical technical analysis performed by retail traders such as chart patterns. Wicks to take out orders above & potentially trap traders are much more noticeable with features such as these.

The Chart Patterns which can be detected include:

Ascending/Descending Wedges (Asc/Desc Wedge)

Ascending/Descending Broadening Wedges (Asc/Desc BW)

Ascending/Descending/Symmetrical Triangles (Asc/Desc/Sym Triangle)

Double Tops/Bottoms (Double Top/Double BTM)

Head & Shoulders (H&S)

Inverted Head & Shoulders (IH&S)

General support & resistance during undetected patterns

In the image below we can see more features from within the indicator, including Balanced Price Range (another imbalance method similar to FVG), Market Structure Candle Coloring, Accumulation & Distribution zones, Premium & Discount zones w/ a percentage on each zone, the MTF dashboard, as well as the Previous Daily Highs & Lows (one of many highs/lows) displayed on the chart automatically.

The colored candles use more specific market structure analysis, specifically allowing users to visualize when trends are considered "normal" or "strong". By utilizing other features alongside this market structure analysis, such as noticing price retesting the PDL level + the Equilibrium as resistance, a Balanced Price Range below price, the discount with a high 72% metric, and the MTF dashboard displaying an overall bearish structure...

...users can instantly gain a deeper interpretation of price action, make highly confluent trading plans while avoiding classical technical indicators, and use traditional retail trading concepts such as chart patterns / trend lines to their advantage in finding logical areas of liquidity & points of interest in the market.

The image below shows the previous chart zoomed in with 2 liquidity concepts re-enabled & used alongside a new range targeting the same Discount zone.

🔶 SETTINGS

Market Structure Internal: Allows the user to select which internal structures to display (BOS, CHoCH, or None).

Market Structure Swing: Allows the user to select which swing structures to display (BOS, CHoCH, or None).

MTF Scanner: See market structure on various timeframes & how many labels are active consecutively.

Equal Highs & Lows: Displays EQH / EQL labels on chart for detecting equal highs & lows.

Color Candles: Plots candles based on the internal & swing structures from within the indicator on the chart.

Order Blocks Internal: Enables Internal Order Blocks & allows the user to select how many most recent Internal Order Blocks appear on the chart as well as select a color.

Order Blocks Swing: Enables Swing Order Blocks & allows the user to select how many most recent Swing Order Blocks appear on the chart as well as select a color.

Mitigation Method: Allows the user to select how the script mitigates an Order Block (close, wick, or average).

Internal Buy/Sell Activity: Allows the user to display buy/sell activity within Order Blocks & decide their color.

Show Metrics: Allows the user to display volume % metrics within the Order Blocks.

Trend Line Liquidity Zones: Allows the user to display Trend Line Zones on the chart, select the number of Trend Lines visible, & their colors.

Chart Pattern Liquidity: Allows the user to display Chart Patterns on the chart, select the significance of the pattern detection, & their colors.

Liquidity Grabs: Allows the user to display Liquidity Grabs on the chart.

Imbalance Concepts: Allows the user to select the type of imbalances to display on the chart as well as the styling, mitigation method, & timeframe.

Auto FVG Threshold: Filter out non-significant fair value gaps.

Premium/ Discount Zones: Allows the user to display Premium, Discount , and Equilibrium zones on the chart

Accumulation / Distribution: Allows the user to display accumulation & distribution consolidation zones with an optional Consolidation Zig-Zag setting included.

Highs/Lows MTF: Displays previous highs & lows as levels on the chart for the previous Day, Monday, Week, Month, or quarter (3M).

General Styling: Provides styling options for market structure labels, market structure theme, and dashboard customization.

Any Alert() Function Call Conditions: Allows the user to select multiple conditions to use within 1 alert.

🔶 CONCLUSION

Price action trading is a widely respected method for its simplicity & realistic approach to understanding the market itself. Price Action Concepts™ is an extremely comprehensive product that opens the possibilities for any trader to automatically display useful metrics for trading price action with enhanced details in each. While this script is useful, it's critical to understand that past performance is not necessarily indicative of future results and there are many more factors that go into being a profitable trader.

🔶 HOW TO GET ACCESS

You can see the Author's instructions below to get instant access to this indicator & our premium suite.

SMC Pro+ ICT v4 Enhanced - FINAL🎯 SMC Pro+ ICT v4 Enhanced - Complete Smart Money Trading System📊 Professional All-in-One Indicator for Smart Money Concepts & ICT MethodologyThe SMC Pro+ ICT v4 Enhanced is a comprehensive trading system that combines Smart Money Concepts (SMC) with Inner Circle Trader (ICT) methodology. This indicator provides institutional-grade market structure analysis, liquidity mapping, and volume profiling in one powerful package.✨ CORE FEATURES🏗️ Advanced Market Structure Detection

MSS (Market Structure Shift) - Identifies major trend reversals with precision

BOS (Break of Structure) - Confirms trend continuation moves

CHoCH (Change of Character) - Detects internal structure shifts

Modern LuxAlgo-Style Lines - Clean, professional visualization

Dual Sensitivity System - External structure (major swings) + Internal structure (minor swings)

Customizable Labels - Tiny, Small, or Normal sizes

Structure Break Visualization - Clear break point markers

💎 Supply & Demand Zones (POI - Point of Interest)

Institutional Order Blocks - Where smart money enters/exits

ATR-Based Zone Sizing - Dynamically adjusted to market volatility

Smart Overlap Detection - Prevents cluttered charts

Historical Zone Tracking - Maintains up to 50 zones

POI Central Lines - Pinpoint entry/exit levels

Auto-Extension - Zones extend to current price

Auto-Cleanup - Removes broken zones automatically

📦 Fair Value Gap (FVG) Detection

Bullish & Bearish FVGs - Institutional inefficiencies

Consequent Encroachment (CE) - 50% fill levels

Auto-Delete Filled Gaps - Keeps charts clean

Customizable Lookback - 1-30 days of history

Color-Coded Zones - Easy visual identification

CE Line Styles - Dotted, Dashed, or Solid

🚀 Enhanced PVSRA Volume Analysis

This is one of the most powerful features:

200% Volume Candles - Extreme institutional activity (Lime/Red)

150% Volume Candles - High institutional interest (Blue/Fuchsia)

Volume Climax Detection - Major reversal signals with 2.5x+ volume

Exhaustion Signals - Identifies buying/selling exhaustion with high accuracy

Enhanced Volume Divergence - NEW! High-quality reversal detection

Price makes lower low, Volume makes higher low = Bullish Divergence

Price makes higher high, Volume makes lower high = Bearish Divergence

Strict trend context filtering for accuracy

Rising/Falling Volume Patterns - Momentum confirmation (allows 1 exception in 3 bars)

Volume Spread Analysis - Price range × Volume for true strength

Body/Wick Ratio Analysis - Candle structure quality

ATR Normalization - Adjusts for different market volatility

Volume Profile Indicators - 🔥 EXTREME, ⚡ VERY HIGH, 📈 HIGH, ✅ ABOVE AVG

💧 Advanced Liquidity System

Smart money targets these levels:

Weekly High/Low Liquidity - Major institutional targets

Daily High/Low Liquidity - Intraday key levels

4H Session Liquidity - Short-term targets

Distance Indicators - Shows % distance from current price

Strength Indicators - Identifies high-probability sweeps

Swept Level Detection - Tracks executed liquidity grabs

Customizable Line Styles - Width, length, offset controls

Color-Coded Levels - Easy visual hierarchy

🎯 Master Bias System

Data-driven directional bias with 9-factor scoring:

Bull/Bear Bias Calculation - 0-100% scoring system

Multi-Timeframe Analysis - Daily, 4H, 1H trend alignment

Kill Zone Integration - London (2-5 AM) & NY (8-11 AM) sessions

EMA Alignment Factor - Trend confirmation

Volume Confirmation - Adds 5% when volume supports direction

Range Filter Integration - Adds 10% for trending markets

Session Context - Above/below session midpoint scoring

Bias Strength Rating - STRONG (>75%), MODERATE (60-75%), WEAK (<60%)

Real-Time Updates - Dynamic recalculation

📈 Premium & Discount Zones

Fibonacci-based institutional pricing:

Extreme Premium - Above 78.6% (Overvalued)

Premium Zone - 61.8% - 78.6% (Expensive)

Equilibrium - 38.2% - 61.8% (Fair Value)

Discount Zone - 21.4% - 38.2% (Cheap)

Extreme Discount - Below 21.4% (Undervalued)

Visual Zone Boxes - Color-coded for instant recognition

200-500 Bar Lookback - Customizable range calculation

🔄 Range Filter

Advanced trend detection:

Smoothed Range Calculation - Eliminates noise

Dynamic Support/Resistance - Auto-adjusting levels

Upward/Downward Counters - Measures trend strength

Color-Coded Line - Green (uptrend), Red (downtrend), Orange (ranging)

Adjustable Period - 1-200 bars

Multiplier Control - Fine-tune sensitivity (0.1-10.0)

🌊 Liquidity Zones (Vector Zones)

PVSRA-based horizontal liquidity:

Above Price Zones - Resistance clusters

Below Price Zones - Support clusters

Maximum 500 Zones - Professional-grade capacity

Body/Wick Definition - Choose zone boundaries

Auto-Cleanup - Removes cleared zones

Color Override - Custom styling options

Transparency Control - 0-100% opacity

📊 EMA System

Triple EMA trend confirmation:

Fast EMA (9) - Green line - Immediate trend

Medium EMA (21) - Blue line - Short-term trend

Slow EMA (50) - Red line - Major trend

EMA Alignment Detection - Bull/Bear stack confirmation

Dashboard Integration - Status: 📈 BULL ALIGN, 📉 BEAR ALIGN, 🔀 MIXED

Adjustable Lengths - Customize all three EMAs (5-200)

🎯 IDM (Institutional Decision Maker) Levels

Key institutional price levels:

Latest IDM Detection - 20-bar pivot lookback

Extended Lines - Projects 50 bars into future

Customizable Styles - Solid, Dashed, or Dotted

Line Width Control - 1-5 pixels

Color Selection - Match your chart theme

Price Label - Shows exact level with tick precision

📱 Professional Dashboard

Real-time market intelligence panel:

🎯 SIGNAL - 🟢 LONG, 🔴 SHORT, ⏳ WAIT, 🛑 NO TRADE

🎲 BIAS - Bull/Bear with STRONG/MODERATE/WEAK rating

📊 BULL/BEAR Scores - 0-100% percentage display

💎 ZONE - Current premium/discount location

🕐 KZ - Kill Zone status (🇬🇧 LONDON/🇺🇸 NY/⏸️ OFF)

🏗️ STRUCT - Market structure status (BULLISH/BEARISH/NEUTRAL)

⚡ EVENT - Last structure event (MSS/BOS)

⚡ INT - Internal structure trend

🎯 IDM - Latest institutional level

📊 EMA - EMA alignment status

🔄 RF - Range Filter direction

📊 PVSRA - Volume status (🚀 CLIMAX/📈 RISING/📉 FALLING)

📅 MTF - Multi-timeframe alignment (✅ FULL/⚠️ PARTIAL/❌ CONFLICT)

💪 CONF - Confidence score (0-100%)

📊 VOL - Volume ratio (e.g., 1.8x average)

Advanced Metrics (Toggle On/Off):

📏 RSI - Value + Status (OVERBOUGHT/STRONG/NEUTRAL/WEAK/OVERSOLD)

📈 MACD - Value + Direction (BULL/BEAR)

🌪️ VOL - Volatility state (⚠️ EXTREME/🔥 HIGH/📊 NORMAL/😴 LOW)

🔊 VOL PROF - Volume profile ratio

⏱️ TF - Current timeframe

Dashboard Customization:

4 Positions - Top Left, Top Right, Bottom Left, Bottom Right

3 Sizes - Small, Normal, Large

2 Modes - Compact (MTF combined) or Full (separate rows)

Professional Design - Dark theme with color-coded cells

🎮 TRADING SIGNALS & SETUP SCORING🟢 LONG Setup Requirements (9-Factor Confidence Score)

MTF Alignment - Daily/4H/1H/Structure all bullish (+2 points for full, +1 for partial)

Volume Confirmation - Above 1.2x average (+1 point)

Structure Event - MSS or BOS bullish (+2 points)

EMA Alignment - 9 > 21 > 50 (+1 point)

Kill Zone Active - London/NY + Bull bias >75% (+2 points)

Bias Match - Master bias matches structure trend (+1 point)

Confidence Threshold - >60% minimum for signal

🔴 SHORT Setup Requirements

Same 9-factor system but inverted for bearish conditions.💪 Confidence Levels

75-100% - ⭐ HIGH CONFIDENCE (Strong setup, all factors aligned)

50-74% - ⚠️ MODERATE (Good setup, partial alignment)

0-49% - ❌ LOW CONFIDENCE (Wait for better setup)

🎯 Signal Output

🟢 LONG - Bull bias + Bullish structure + >60% confidence

🔴 SHORT - Bear bias + Bearish structure + >60% confidence

⏳ WAIT LONG - Bull bias but low confidence

⏳ WAIT SHORT - Bear bias but low confidence

🛑 NO TRADE - Neutral bias or conflicting signals

🔔 COMPREHENSIVE ALERT SYSTEM (12 Alerts)Structure Alerts

⚡ MSS Bullish - Major bullish reversal

⚡ MSS Bearish - Major bearish reversal

📈 BOS Bullish - Bullish continuation

📉 BOS Bearish - Bearish continuation

⚠️ CHoCH Bullish - Internal bullish shift

⚠️ CHoCH Bearish - Internal bearish shift

Bias & Confidence Alerts

🟢 Bias Shift Bull - Master bias turns bullish

🔴 Bias Shift Bear - Master bias turns bearish

⭐ High Confidence - Setup reaches 75%+ confidence

Volume Alerts (High Probability)

🚀 Volume Climax Buy - Extreme bullish volume spike

💥 Volume Climax Sell - Extreme bearish volume spike

⚠️ Selling Exhaustion - Potential bullish reversal

⚠️ Buying Exhaustion - Potential bearish reversal

📊 Bullish Volume Divergence - High-quality bullish reversal signal

📊 Bearish Volume Divergence - High-quality bearish reversal signal

🎨 EXTENSIVE CUSTOMIZATIONColors & Styling

✅ All colors customizable for every component

✅ Supply/Demand zone colors + outlines

✅ FVG colors (bullish/bearish)

✅ PVSRA candle colors (6 types)

✅ Liquidity level colors (Weekly/Daily/4H/Swept)

✅ Structure line colors

✅ Premium/Equilibrium/Discount zone colorsDisplay Controls

✅ Toggle each feature on/off independently

✅ Adjustable sensitivities (Structure: 5-30, Internal: 3-15)

✅ Label size controls (Tiny/Small/Normal)

✅ Line width adjustments (1-5 pixels)

✅ Transparency controls (0-100%)

✅ Extension lengths (20-100 bars)

✅ Lookback periods (50-500 bars)Volume Settings

✅ PVSRA symbol override (trade one asset, analyze another)

✅ Climax threshold (2.0-5.0x)

✅ Rising volume bar count (2-5 bars)

✅ Divergence filters (Strict/Lenient)

✅ Divergence minimum bars (10-30)

✅ Volume threshold multiplier (1.0-2.0x)Dashboard Settings

✅ Position (4 corners)

✅ Size (Small/Normal/Large)

✅ Compact/Full mode

✅ Show/Hide advanced metrics

✅ Show/Hide EMA status💡 BEST PRACTICES & USAGE TIPS⏰ Optimal Timeframes

Scalping - 1m, 5m (Use Kill Zones, Volume Climax, FVG)

Day Trading - 5m, 15m, 1H (Use Structure, Liquidity, Bias)

Swing Trading - 4H, Daily (Use MTF, Premium/Discount, Structure)

Position Trading - Daily, Weekly (Use major structure, liquidity)

🎯 Asset Classes

✅ Forex - All pairs (especially majors during Kill Zones)

✅ Crypto - BTC, ETH, altcoins (24/7 liquidity)

✅ Stocks - All stocks and indices (use session times)

✅ Commodities - Gold, Silver, Oil (high volume periods)

✅ Indices - S&P 500, NASDAQ, DAX, etc.🔥 High-Probability Setups

The Perfect Storm

MSS in direction of daily trend

Kill Zone active

Volume climax

Confidence >75%

Price in discount (long) or premium (short)

Volume Divergence Play

Enhanced volume divergence signal

CHoCH confirms direction change

Price near liquidity level

FVG forms for entry

Liquidity Sweep

Price sweeps weekly/daily high/low

Immediate rejection (selling/buying exhaustion)

Structure shift (MSS)

Volume confirmation

Structure Retest

BOS breaks structure

Price returns to POI/FVG

Volume confirms (>1.2x)

Kill Zone active

📊 Multi-Timeframe Analysis

Higher Timeframe - Identify trend & structure (Daily/4H)

Trading Timeframe - Find entries (15m/1H)

Lower Timeframe - Precise entries (1m/5m)

Look for MTF alignment - Dashboard shows ✅ FULL or ⚠️ PARTIAL

⚠️ Risk Management

Always use stop-loss (below/above recent structure)

Position size: 1-2% risk per trade

Target liquidity levels for take profit

Use supply/demand zones for SL placement

Watch for exhaustion signals near targets

Smart Money Decoded [GOLD]Title: Smart Money Decoded

Description:

Introduction

Smart Money Decoded is a comprehensive, institutional-grade visualization suite designed to simplify the complex world of Smart Money Concepts (SMC). While many indicators flood the chart with noise, this tool focuses on clarity, precision, and high-probability structure.

This script is built for traders who follow the "Inner Circle Trader" (ICT) methodologies but struggle to identify valid Zones, Displacement, and Liquidity Sweeps in real-time.

💎 Key Features & Logic

1. Refined Market Structure (BOS & CHoCH)

Instead of marking every minor pivot, this script uses a filtered Swing High/Low detection system.

HH/LL/LH/HL Labels: Only significant structure points are mapped.

BOS (Break of Structure): Marks trend continuations in the direction of the bias.

CHoCH (Change of Character): Marks potential trend reversals.

2. Advanced Order Blocks (with "Strict Mode")

Not all down-candles before an up-move are Order Blocks. This script separates the weak from the strong.

Standard OBs: Visualized with standard transparency.

⚡ SWEEP OBs (High Probability): Order Blocks that explicitly swept liquidity (Stop Hunt) before the reversal are highlighted with a thicker border, brighter color, and a ⚡ symbol. These are your high-probability "Turtle Soup" entries.

Strict Mode Toggle: In the settings, you can choose to hide all weak OBs and only see the ones that swept liquidity.

3. Dynamic Breaker Blocks

A true ICT Breaker is a failed Order Block that trapped liquidity.

This script automatically detects when a valid OB is mitigated (broken through) and projects it forward as a Breaker Block.

This ensures you are trading off valid flipped zones (Support becomes Resistance, Resistance becomes Support).

4. Fair Value Gaps (FVG)

Automatically detects Imbalances (Imbalance/Inefficiency).

Includes an ATR Filter to ignore tiny, insignificant gaps, keeping your chart clean.

Option to show the Consequent Encroachment (50% CE) level for precision entries.

5. Liquidity Zones (BSL / SSL)

Automatically plots Buy Side Liquidity (BSL) and Sell Side Liquidity (SSL) at key swing points.

Once price sweeps these levels, the zone is removed or marked as "Swept," helping you identify when the draw on liquidity has been met.

6. Institutional Data Panel

A dashboard in the top right corner displays:

Market Bias: Bullish/Bearish/Neutral based on structure.

Premium/Discount: Tells you if price is in the expensive (Premium) or cheap (Discount) part of the current dealing range.

Active Zones: Counts of current open arrays.

⚙️ How To Use This Indicator

Identify Bias: Look at the Structure Labels (HH/LL) and the Panel. Are we making Higher Highs?

Wait for the Trap: Look for a Liquidity Sweep (BSL/SSL taken) or a ⚡ Sweep OB.

Entry Confirmation: Watch for a return to a Fair Value Gap (FVG) or a retest of a Breaker Block (BRK).

Manage Risk: Use the visuals to place stops above/below invalidation points.

Customization:

Go to the settings to toggle "Strict Mode" for Order Blocks, change colors to match your theme, or adjust the lookback periods to fit your specific asset (Forex, Crypto, or Indices).

📚 Credits & Acknowledgments

This script is an educational tool based on the public teachings of Michael J. Huddleston (The Inner Circle Trader - ICT).

Concepts used: Order Blocks, Breakers, FVGs, Market Structure, Liquidity Pools.

Credit is fully given to ICT for originating these concepts and sharing them with the world.

⚠️ Disclaimer

This script is NOT affiliated with, endorsed by, or connected to Michael J. Huddleston (ICT) in any way. It is an independent coding project intended for educational purposes and visual assistance.

Trading involves substantial risk. This indicator does not guarantee profits. Always use proper risk management. Trust your analysis first, and use indicators as confluence.

#Smart Money Concepts, #SMC, #ICT,#Liquidity, #Market Structure, #Trend, #Price Action.

CandelaCharts - Turtle Soup Model📝 Overview

The ICT Turtle Soup Model indicator is a precision-engineered tool designed to identify high-probability reversal setups based on ICT’s renowned Turtle Soup strategy.

The Turtle Soup Model is a classic reversal setup that exploits false breakouts beyond previous swing highs or lows. It targets areas where retail traders are trapped into breakout trades, only for the price to reverse sharply in the opposite direction.

Price briefly breaks a previous high (for short setups) or low (for long setups), triggering stop orders and pulling in breakout traders. Once that liquidity is taken, smart money reverses price back inside the range, creating a high-probability fade setup.

📦 Features

Liquidity Levels: Projects forward-looking liquidity levels after a Turtle Soup model is formed, highlighting potential price targets. These projected zones act as magnet levels—areas where price is likely to reach based on the liquidity draw narrative. This allows traders to manage exits and partials with more precision.

Market Structure Shift (MSS): Confirms reversal strength by detecting a bullish or bearish MSS after a sweep. Acts as a secondary confirmation to filter out weak setups.

Custom TF Pairing: Choose your own combination of entry timeframe and context timeframe. For example, trade 5m setups inside a 1h HTF bias — perfect for aligning microstructure with macro intent.

HTF & LTF PD Arrays: Displays HTF PD Arrays (e.g., Fair Value Gaps, Inversion Fair Value Gaps) to serve as confluence zones.

History: Review and backtest past Turtle Soup setups directly on the chart. Toggle historical models on/off to study model behavior across different market conditions.

Killzone Filter: Limit signals to specific trading sessions or time blocks (e.g., New York AM, London, Asia, etc). Avoid signals in low-liquidity or choppy environments.

Standard Deviation: Calculates and projects four levels of standard deviation from the point of model confirmation. These zones help identify overextended moves, mean-reversion opportunities, and confluence with liquidity or PD arrays.

Dashboard: The dashboard displays the active model type, remaining time of the HTF candle, current bias, asset name, and date—providing real-time context and signal clarity at a glance.

⚙️ Settings

Core

Status: Filter models based on status

Bias: Controls what model type will be displayed, bullish or bearish

Fractal: Controls the timeframe pairing that will be used

High Probability Models: Detects and plots only the high-probability models

Sweeps

Sweep: Shows the sweep that forms a model

I-sweep: Controls the visibility of invalidated sweeps

D-purge: Plots the double purge sweeps

S-area: Highlights the sweep area

Liquidity

Liquidity: Displays the liquidity levels that belong to the model

MSS

MSS: Displays the Market Structure Shift for a model

History

History: Controls the number of past models displayed on the chart

Filters

Asia: Filter models based on Asia Killzone hours

London: Filter models based on London Killzone hours

NY AM: Filter models based on NY AM Killzone hours

NY Launch: Filter models based on NY Launch Killzone hours

NY PM: Filter models based on NY PM Killzone hours

Custom: Filter models based on user Custom hours

HTF

Candles: Controls the number of HTF candles that will be visible on the chart

Candles T: Displays the model’s third timeframe candle, which serves as a confirmation of directional bias

NY Open: Display True Day Open line

Offset: Controls the distance of HTF from the current chart

Space: Controls the space between HTF candles

Size: Controls the size of HTF candles

PD Array: Displays ICT PD Arrays

CE Line: Style the equilibrium line of PD Array

Border: Style the border of the PD Array

LTF

H/L Line: Displays on the LTF chart the High and Low of each HTF candle

O/C Line: Displays on the LTF chart the Open and Close of each HTF candle

PD Array: Displays ICT PD Arrays

CE Line: Style the equilibrium line of PD Array

Border: Style the border of the PD Array

Standard Deviation

StDev: Controls standard deviation of available levels

Labels: Controls the size of standard deviation levels

Lines: Controls the line widths and color of standard deviation levels

Dashboard

Panel: Display information about the current model

💡 Framework

The Turtle Soup Model is designed to detect and interpret false breakout patterns by analyzing key price action components, each playing a vital role in identifying liquidity traps and generating actionable reversal signals.

The model incorporates the following timeframe pairing:

15s - 5m - 15m

1m - 5m - 1H

2m - 15m - 2H

3m - 30m - 3H

5m - 60m - 4H

15m - 1H - 8H

30m - 3H - 12H

1H - 4H - 1D

4H - 1D - 1W

1D - 1W - 1M

1W - 1M - 6M

1M - 6M - 12M

Below are the key components that make up the model:

Sweep

D-purge

MSS

Liquidity

Standard Deviation

HTF & LTF PD Arrays

The Turtle Soup Model operates through a defined lifecycle that identifies its current state and determines the validity of a trade opportunity.

The model's lifecycle includes the following statuses:

Formation (grey)

Invalidation (red)

Pre-Invalidation (purple)

Success (green)

By incorporating the phases of Formation, Invalidation, and Success, traders can effectively manage risk, optimize position handling, and capitalize on the high-probability opportunities presented by the Turtle Soup Model.

⚡️ Showcase

Introducing the Turtle Soup Model — a powerful trading tool engineered to detect high-probability false breakout reversals. This indicator helps you pinpoint liquidity sweeps, confirm market structure shifts, and identify precise entry and exit points, enabling more confident, informed, and timely trading decisions.

LTF PD Array

LTF PD Arrays are essential for model formation—a valid Turtle Soup setup will only trigger if a qualifying LTF PD Array is present near the sweep zone.

HTF PD Array

HTF PD Arrays provide macro-level context and are used to validate the direction and strength of the potential reversal.

Timeframe Alignment

In the Turtle Soup trading model, timeframe alignment is an essential structural component. The model relies on multi-timeframe context to identify high-probability reversal setups based on failed breakouts.

High-Probability Model

A high-probability setup forms when key elements align: a Sweep, Market Structure Shift (MSS), LTF and HTF PD Arrays.

Killzone Filters

Filter Turtle Soup Models based on key market sessions: Asia, London, New York AM, New York Launch, and New York PM . This allows you to focus on high-liquidity periods where smart money activity is most likely to occur, improving both the quality and timing of your trade setups.

Unlock your trading edge with the Turtle Soup Model — your go-to tool for sharper insights, smarter decisions, and more confident execution in the markets.

🚨 Alerts

This script offers alert options for all model types. The alerts need to be set up manually from TradingView.

Bearish Model

A bearish model alert is triggered when a model forms, signaling a high sweep, MS,S and LTF PD Array.

Bullish Model

A bullish model alert is triggered when a model forms, signaling a low sweep, MSS and LTF PD Array.

⚠️ Disclaimer

These tools are exclusively available on the TradingView platform.

Our charting tools are intended solely for informational and educational purposes and should not be regarded as financial, investment, or trading advice. They are not designed to predict market movements or offer specific recommendations. Users should be aware that past performance is not indicative of future results and should not rely on these tools for financial decisions. By using these charting tools, the purchaser agrees that the seller and creator hold no responsibility for any decisions made based on information provided by the tools. The purchaser assumes full responsibility and liability for any actions taken and their consequences, including potential financial losses or investment outcomes that may result from the use of these products.

By purchasing, the customer acknowledges and accepts that neither the seller nor the creator is liable for any undesired outcomes stemming from the development, sale, or use of these products. Additionally, the purchaser agrees to indemnify the seller from any liability. If invited through the Friends and Family Program, the purchaser understands that any provided discount code applies only to the initial purchase of Candela's subscription. The purchaser is responsible for canceling or requesting cancellation of their subscription if they choose not to continue at the full retail price. In the event the purchaser no longer wishes to use the products, they must unsubscribe from the membership service, if applicable.

We do not offer reimbursements, refunds, or chargebacks. Once these Terms are accepted at the time of purchase, no reimbursements, refunds, or chargebacks will be issued under any circumstances.

By continuing to use these charting tools, the user confirms their understanding and acceptance of these Terms as outlined in this disclaimer.

CandelaCharts - Buyside & Sellside 📝 Overview

The Buyside & Sellside Liquidity Indicator is designed to identify and emphasize one of the foundational concepts within the ICT (Inner Circle Trader) trading methodology: liquidity levels.

This tool focuses on pinpointing key areas in the market where buy-side and sell-side liquidity is concentrated, providing traders with insights into potential price targets, reversal zones, and institutional order flow behavior.