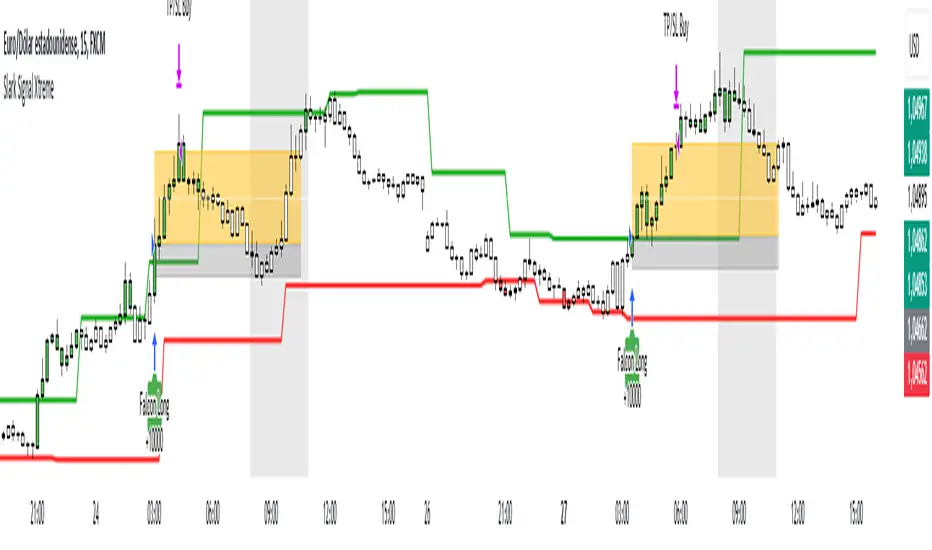

ThinkTech AI SignalsThink Tech AI Strategy

The Think Tech AI Strategy provides a structured approach to trading by integrating liquidity-based entries, ATR volatility thresholds, and dynamic risk management. This strategy generates buy and sell signals while automatically calculating take profit and stop loss levels, boasting a 64% win rate based on historical data.

Usage

The strategy can be used to identify key breakout and retest opportunities. Liquidity-based zones act as potential accumulation and distribution areas and may serve as future support or resistance levels. Buy and sell zones are identified using liquidity zones and ATR-based filters. Risk management is built-in, automatically calculating take profit and stop loss levels using ATR multipliers. Volume and trend filtering options help confirm directional bias using a 50 EMA and RSI filter. The strategy also allows for session-based trading, limiting trades to key market hours for higher probability setups.

Settings

The risk/reward ratio can be adjusted to define the desired stop loss and take profit calculations. The ATR length and threshold determine ATR-based breakout conditions for dynamic entries. Liquidity period settings allow for customized analysis of price structure for support and resistance zones. Additional trend and RSI filters can be enabled to refine trade signals based on moving averages and momentum conditions. A session filter is included to restrict trade signals to specific market hours.

Style

The strategy includes options to display liquidity lines, showing key support and resistance areas. The first 15-minute candle breakout zones can also be visualized to highlight critical market structure points. A win/loss statistics table is included to track trade performance directly on the chart.

This strategy is intended for descriptive analysis and should be used alongside other confluence factors. Optimize your trading process with Think Tech AI today!

Cari dalam skrip untuk "liquidity"

ICT Bread and Butter Sell-SetupICT Bread and Butter Sell-Setup – TradingView Strategy

Overview:

The ICT Bread and Butter Sell-Setup is an intraday trading strategy designed to capitalize on bearish market conditions. It follows institutional order flow and exploits liquidity patterns within key trading sessions—London, New York, and Asia—to identify high-probability short entries.

Key Components of the Strategy:

🔹 London Open Setup (2:00 AM – 8:20 AM NY Time)

The London session typically sets the initial directional move of the day.

A short-term high often forms before a downward push, establishing the daily high.

🔹 New York Open Kill Zone (8:20 AM – 10:00 AM NY Time)

The New York Judas Swing (a temporary rally above London’s high) creates an opportunity for short entries.

Traders fade this move, anticipating a sell-off targeting liquidity below previous lows.

🔹 London Close Buy Setup (10:30 AM – 1:00 PM NY Time)

If price reaches a higher timeframe discount array, a retracement higher is expected.

A bullish order block or failure swing signals a possible reversal.

The risk is set just below the day’s low, targeting a 20-30% retracement of the daily range.

🔹 Asia Open Sell Setup (7:00 PM – 2:00 AM NY Time)

If institutional order flow remains bearish, a short entry is taken around the 0-GMT Open.

Expect a 15-20 pip decline as the Asian range forms.

Strategy Rules:

📉 Short Entry Conditions:

✅ New York Judas Swing occurs (price moves above London’s high before reversing).

✅ Short entry is triggered when price closes below the open.

✅ Stop-loss is set 10 pips above the session high.

✅ Take-profit targets liquidity zones on higher timeframes.

📈 Long Entry (London Close Reversal):

✅ Price reaches a higher timeframe discount array between 10:30 AM – 1:00 PM NY Time.

✅ A bullish order block confirms the reversal.

✅ Stop-loss is set 10 pips below the day’s low.

✅ Take-profit targets 20-30% of the daily range retracement.

📉 Asia Open Sell Entry:

✅ Price trades slightly above the 0-GMT Open.

✅ Short entry is taken at resistance, targeting a quick 15-20 pip move.

Why Use This Strategy?

🚀 Institutional Order Flow Tracking – Aligns with smart money concepts.

📊 Precise Session Timing – Uses market structure across London, New York, and Asia.

🎯 High-Probability Entries – Focuses on liquidity grabs and engineered stop hunts.

📉 Optimized Risk Management – Defined stop-loss and take-profit levels.

This strategy is ideal for traders looking to trade with institutions, fade liquidity grabs, and capture high-probability short setups during the trading day. 📉🔥

CBC Strategy with Trend Confirmation & Separate Stop LossCBC Flip Strategy with Trend Confirmation and ATR-Based Targets

This strategy is based on the CBC Flip concept taught by MapleStax and inspired by the original CBC Flip indicator by AsiaRoo. It focuses on identifying potential reversals or trend continuation points using a combination of candlestick patterns (CBC Flips), trend filters, and a time-based entry window. This approach helps traders avoid false signals and increase trade accuracy.

What is a CBC Flip?

The CBC Flip is a candlestick-based pattern that identifies moments when the market is likely to change direction or strengthen its trend. It checks for a shift in price behavior between consecutive candles, signaling a bullish (upward) or bearish (downward) move.

However, not all flips are created equal! This strategy differentiates between Strong Flips and All Flips, allowing traders to choose between a more conservative or aggressive approach.

Strong Flips vs. All Flips

Strong Flips

A Strong Flip is a high-probability setup that occurs only after liquidity is swept from the previous candle’s high or low.

What is a liquidity sweep? This happens when the price briefly moves beyond the high or low of the previous candle, triggering stop-losses and trapping traders in the wrong direction. These sweeps often create fuel for the next move, making them powerful reversal signals.

Examples:

Long Setup: The price dips below the previous candle’s low (sweeping liquidity) and then closes higher, signaling a potential bullish move.

Short Setup: The price moves above the previous candle’s high and then closes lower, signaling a potential bearish move.

Why Use Strong Flips?

They provide fewer signals, but the accuracy is generally higher.

Ideal for trending markets where liquidity sweeps often mark key turning points.

All Flips

All Flips are less selective, offering both Strong Flips and additional signals without requiring a liquidity sweep.

This approach gives traders more frequent opportunities but comes with a higher risk of false signals, especially in sideways markets.

Examples:

Long Setup: A CBC flip occurs without sweeping the previous low, but the trend direction is confirmed (slow EMA is still above VWAP).

Short Setup: A CBC flip occurs without sweeping the previous high, but the trend is still bearish (slow EMA below VWAP).

Why Use All Flips?

Provides more frequent entries for active or aggressive traders.

Works well in trending markets but requires caution during consolidation periods.

How This Strategy Works

The strategy combines CBC Flips with multiple filters to ensure better trade quality:

Trend Confirmation: The slow EMA (20-period) must be positioned relative to the VWAP to confirm the overall trend direction.

Long Trades: Slow EMA must be above VWAP (upward trend).

Short Trades: Slow EMA must be below VWAP (downward trend).

Time-Based Filter: Traders can specify trading hours to limit entries to a particular time window, helping avoid low-volume or high-volatility periods.

Profit Target and Stop-Loss:

Profit Target: Defined as a multiple of the 14-period ATR (Average True Range). For example, if the ATR is 10 points and the profit target multiplier is set to 1.5, the strategy aims for a 15-point profit.

Stop-Loss: Uses a dynamic, candle-based stop-loss:

Long Trades: The trade closes if the market closes below the low of two candles ago.

Short Trades: The trade closes if the market closes above the high of two candles ago.

This approach adapts to recent price behavior and protects against unexpected reversals.

Customizable Settings

Strong Flips vs. All Flips: Choose between a more selective or aggressive entry style.

Profit Target Multiplier: Adjust the ATR multiplier to control the distance for profit targets.

Entry Time Range: Define specific trading hours for the strategy.

Indicators and Visuals

Fast EMA (10-Period) – Black Line

Slow EMA (20-Period) – Red Line

VWAP (Volume-Weighted Average Price) – Orange Line

Visual Labels:

▵ (Triangle Up) – Marks long entries (buy signals).

▿ (Triangle Down) – Marks short entries (sell signals).

Credits

CBC Flip Concept: Inspired by MapleStax, who teaches this concept.

Original Indicator: Developed by AsiaRoo, this strategy builds on the CBC Flip framework with additional features for improved trade management.

Risks and Disclaimer

This strategy is for educational purposes only and does not constitute financial advice.

Trading involves significant risk and may result in the loss of capital. Past performance does not guarantee future results. Use this strategy in a simulated environment before applying it to live trading.

TPS Short Strategy by Larry ConnersThe TPS Short strategy aims to capitalize on extreme overbought conditions in an ETF by employing a scaling-in approach when certain technical indicators signal potential reversals. The strategy is designed to short the ETF when it is deemed overextended, based on the Relative Strength Index (RSI) and moving averages.

Components:

200-Day Simple Moving Average (SMA):

Purpose: Acts as a long-term trend filter. The ETF must be below its 200-day SMA to be eligible for shorting.

Rationale: The 200-day SMA is widely used to gauge the long-term trend of a security. When the price is below this moving average, it is often considered to be in a downtrend (Tushar S. Chande & Stanley Kroll, "The New Technical Trader: Boost Your Profit by Plugging Into the Latest Indicators").

2-Period RSI:

Purpose: Measures the speed and change of price movements to identify overbought conditions.

Criteria: Short 10% of the position when the 2-period RSI is above 75 for two consecutive days.

Rationale: A high RSI value (above 75) indicates that the ETF may be overbought, which could precede a price reversal (J. Welles Wilder, "New Concepts in Technical Trading Systems").

Scaling-In Mechanism:

Purpose: Gradually increase the short position as the ETF price rises beyond previous entry points.

Scaling Strategy:

20% more when the price is higher than the first entry.

30% more when the price is higher than the second entry.

40% more when the price is higher than the third entry.

Rationale: This incremental approach allows for an increased position size in a worsening trend, potentially increasing profitability if the trend continues to align with the strategy’s premise (Marty Schwartz, "Pit Bull: Lessons from Wall Street's Champion Day Trader").

Exit Conditions:

Criteria: Close all positions when the 2-period RSI drops below 30 or the 10-day SMA crosses above the 30-day SMA.

Rationale: A low RSI value (below 30) suggests that the ETF may be oversold and could be poised for a rebound, while the SMA crossover indicates a potential change in the trend (Martin J. Pring, "Technical Analysis Explained").

Risks and Considerations:

Market Risk:

The strategy assumes that the ETF will continue to decline once shorted. However, markets can be unpredictable, and price movements might not align with the strategy's expectations, especially in a volatile market (Nassim Nicholas Taleb, "The Black Swan: The Impact of the Highly Improbable").

Scaling Risks:

Scaling into a position as the price increases may increase exposure to adverse price movements. This method can amplify losses if the market moves against the position significantly before any reversal occurs.

Liquidity Risk:

Depending on the ETF’s liquidity, executing large trades in increments might affect the price and increase trading costs. It is crucial to ensure that the ETF has sufficient liquidity to handle large trades without significant slippage (James Altucher, "Trade Like a Hedge Fund").

Execution Risk:

The strategy relies on timely execution of trades based on specific conditions. Delays or errors in order execution can impact performance, especially in fast-moving markets.

Technical Indicator Limitations:

Technical indicators like RSI and SMA are based on historical data and may not always predict future price movements accurately. They can sometimes produce false signals, leading to potential losses if used in isolation (John Murphy, "Technical Analysis of the Financial Markets").

Conclusion

The TPS Short strategy utilizes a combination of long-term trend filtering, overbought conditions, and incremental shorting to potentially profit from price reversals. While the strategy has a structured approach and leverages well-known technical indicators, it is essential to be aware of the inherent risks, including market volatility, liquidity issues, and potential limitations of technical indicators. As with any trading strategy, thorough backtesting and risk management are crucial to its successful implementation.

ALT Risk Metric StrategyHere's a professional write-up for your ALT Risk Strategy script:

ALT/BTC Risk Strategy - Multi-Crypto DCA with Bitcoin Correlation Analysis

Overview

This strategy uses Bitcoin correlation as a risk indicator to time entries and exits for altcoins. By analyzing how your chosen altcoin performs relative to Bitcoin, the strategy identifies optimal accumulation periods (when alt/BTC is oversold) and profit-taking opportunities (when alt/BTC is overbought). Perfect for traders who want to outperform Bitcoin by strategically timing altcoin positions.

Key Innovation: Why Alt/BTC Matters

Most traders focus solely on USD price, but Alt/BTC ratios reveal true altcoin strength:

When Alt/BTC is low → Altcoin is undervalued relative to Bitcoin (buy opportunity)

When Alt/BTC is high → Altcoin has outperformed Bitcoin (take profits)

This approach captures the rotation between BTC and alts that drives crypto cycles

Key Features

📊 Advanced Technical Analysis

RSI (60% weight): Primary momentum indicator on weekly timeframe

Long-term MA Deviation (35% weight): Measures distance from 150-period baseline

MACD (5% weight): Minor confirmation signal

EMA Smoothing: Filters noise while maintaining responsiveness

All calculations performed on Alt/BTC pairs for superior market timing

💰 3-Tier DCA System

Level 1 (Risk ≤ 70): Conservative entry, base allocation

Level 2 (Risk ≤ 50): Increased allocation, strong opportunity

Level 3 (Risk ≤ 30): Maximum allocation, extreme undervaluation

Continuous buying: Executes every bar while below threshold for true DCA behavior

Cumulative sizing: L3 triggers = L1 + L2 + L3 amounts combined

📈 Smart Profit Management

Sequential selling: Must complete L1 before L2, L2 before L3

Percentage-based exits: Sell portions of position, not fixed amounts

Auto-reset on re-entry: New buy signals reset sell progression

Prevents premature full exits during volatile conditions

🤖 3Commas Automation

Pre-configured JSON webhooks for Custom Signal Bots

Multi-exchange support: Binance, Coinbase, Kraken, Bitfinex, Bybit

Flexible quote currency: USD, USDT, or BUSD

Dynamic order sizing: Automatically adjusts to your tier thresholds

Full webhook documentation compliance

🎨 Multi-Asset Support

Pre-configured for popular altcoins:

ETH (Ethereum)

SOL (Solana)

ADA (Cardano)

LINK (Chainlink)

UNI (Uniswap)

XRP (Ripple)

DOGE

RENDER

Custom option for any other crypto

How It Works

Risk Metric Calculation (0-100 scale):

Fetches weekly Alt/BTC price data for stability

Calculates RSI, MACD, and deviation from 150-period MA

Normalizes MACD to 0-100 range using 500-bar lookback

Combines weighted components: (MACD × 0.05) + (RSI × 0.60) + (Deviation × 0.35)

Applies 5-period EMA smoothing for cleaner signals

Color-Coded Risk Zones:

Green (0-30): Extreme buying opportunity - Alt heavily oversold vs BTC

Lime/Yellow (30-70): Accumulation range - favorable risk/reward

Orange (70-85): Caution zone - consider taking initial profits

Red/Maroon (85-100+): Euphoria zone - aggressive profit-taking

Entry Logic:

Buys execute every candle when risk is below threshold

As risk decreases, position sizing automatically scales up

Example: If risk drops from 60→25, you'll be buying at L1 rate until it hits 50, then L2 rate, then L3 rate

Exit Logic:

Sells only trigger when in profit AND risk exceeds thresholds

Sequential execution ensures partial profit-taking

If new buy signal occurs before all sells complete, sell levels reset to L1

Configuration Guide

Choosing Your Altcoin:

Select crypto from dropdown (or use CUSTOM for unlisted coins)

Pick your exchange

Choose quote currency (USD, USDT, BUSD)

Risk Metric Tuning:

Long Term MA (default 150): Higher = more extreme signals, Lower = more frequent

RSI Length (default 10): Lower = more volatile, Higher = smoother

Smoothing (default 5): Increase for less noise, decrease for faster reaction

Buy Settings (Aggressive DCA Example):

L1 Threshold: 70 | Amount: $5

L2 Threshold: 50 | Amount: $6

L3 Threshold: 30 | Amount: $7

Total L3 buy = $18 per candle when deeply oversold

Sell Settings (Balanced Exit Example):

L1: 70 threshold, 25% position

L2: 85 threshold, 35% position

L3: 100 threshold, 40% position (final exit)

3Commas Setup

Bot Configuration:

Create Custom Signal Bot in 3Commas

Set trading pair to your altcoin/USD (e.g., ETH/USD, SOL/USDT)

Order size: Select "Send in webhook, quote" to use strategy's dollar amounts

Copy Bot UUID and Secret Token

Script Configuration:

Paste credentials into 3Commas section inputs

Check "Enable 3Commas Alerts"

Save and apply to chart

TradingView Alert:

Create Alert → Condition: "alert() function calls only"

Webhook URL: api.3commas.io

Enable "Webhook URL" checkbox

Expiration: Open-ended

Strategy Advantages

✅ Outperform Bitcoin: Designed specifically to beat BTC by timing alt rotations

✅ Capture Alt Seasons: Automatically accumulates when alts lag, sells when they pump

✅ Risk-Adjusted Sizing: Buys more when cheaper (better risk/reward)

✅ Emotional Discipline: Systematic approach removes fear and FOMO

✅ Multi-Asset: Run same strategy across multiple altcoins simultaneously

✅ Proven Indicators: Combines RSI, MACD, and MA deviation - battle-tested tools

Backtesting Insights

Optimal Timeframes:

Daily chart: Best for backtesting and signal generation

Weekly data is fetched internally regardless of display timeframe

Historical Performance Characteristics:

Accumulates heavily during bear markets and BTC dominance periods

Captures explosive altcoin rallies when BTC stagnates

Sequential selling preserves capital during extended downtrends

Works best on established altcoins with multi-year history

Risk Considerations:

Requires capital reserves for extended accumulation periods

Some altcoins may never recover if fundamentals deteriorate

Past correlation patterns may not predict future performance

Always size positions according to personal risk tolerance

Visual Interface

Indicator Panel Displays:

Dynamic color line: Green→Lime→Yellow→Orange→Red as risk increases

Horizontal threshold lines: Dashed lines mark your buy/sell levels

Entry/Exit labels: Green labels for buys, Orange/Red/Maroon for sells

Real-time risk value: Numerical display on price scale

Customization:

All threshold lines are adjustable via inputs

Color scheme clearly differentiates buy zones (green spectrum) from sell zones (red spectrum)

Line weights emphasize most extreme thresholds (L3 buy and L3 sell)

Strategy Philosophy

This strategy is built on the principle that altcoins move in cycles relative to Bitcoin. During Bitcoin rallies, alts often bleed against BTC (high sell, accumulate). When Bitcoin consolidates, alts pump (take profits). By measuring risk on the Alt/BTC chart instead of USD price, we time these rotations with precision.

The 3-tier system ensures you're always averaging in at better prices and scaling out at better prices, maximizing your Bitcoin-denominated returns.

Advanced Tips

Multi-Bot Strategy:

Run this on 5-10 different altcoins simultaneously to:

Diversify correlation risk

Capture whichever alt is pumping

Smooth equity curve through rotation

Pairing with BTC Strategy:

Use alongside the BTC DCA Risk Strategy for complete portfolio coverage:

BTC strategy for core holdings

ALT strategies for alpha generation

Rebalance between them based on BTC dominance

Threshold Calibration:

Check 2-3 years of historical data for your chosen alt

Note where risk metric sat during major bottoms (set buy thresholds)

Note where it peaked during euphoria (set sell thresholds)

Adjust for your risk tolerance and holding period

Credits

Strategy Development & 3Commas Integration: Claude AI (Anthropic)

Technical Analysis Framework: RSI, MACD, Moving Average theory

Implementation: pommesUNDwurst

Disclaimer

This strategy is for educational purposes only. Cryptocurrency trading involves substantial risk of loss. Altcoins are especially volatile and many fail completely. The strategy assumes liquid markets and reliable Alt/BTC price data. Always do your own research, understand the fundamentals of any asset you trade, and never risk more than you can afford to lose. Past performance does not guarantee future results. The authors are not financial advisors and assume no liability for trading decisions.

Additional Warning: Using leverage or trading illiquid altcoins amplifies risk significantly. This strategy is designed for spot trading of established cryptocurrencies with deep liquidity.

Tags: Altcoin, Alt/BTC, DCA, Risk Metric, Dollar Cost Averaging, 3Commas, ETH, SOL, Crypto Rotation, Bitcoin Correlation, Automated Trading, Alt Season

Feel free to modify any sections to better match your style or add specific backtesting results you've observed! 🚀Claude is AI and can make mistakes. Please double-check responses. Sonnet 4.5

XAUUSD 1m SMC Zones (BOS + Flexible TP Modes + Trailing Runner)//@version=6

strategy("XAUUSD 1m SMC Zones (BOS + Flexible TP Modes + Trailing Runner)",

overlay = true,

initial_capital = 10000,

pyramiding = 10,

process_orders_on_close = true)

//━━━━━━━━━━━━━━━━━━━

// 1. INPUTS

//━━━━━━━━━━━━━━━━━━━

// TP / SL

tp1Pips = input.int(10, "TP1 (pips)", minval = 1)

fixedSLpips = input.int(50, "Fixed SL (pips)", minval = 5)

runnerRR = input.float(3.0, "Runner RR (TP2 = SL * RR)", step = 0.1, minval = 1.0)

// Daily risk

maxDailyLossPct = input.float(5.0, "Max daily loss % (stop trading)", step = 0.5)

maxDailyProfitPct = input.float(20.0, "Max daily profit % (stop trading)", step = 1.0)

// HTF S/R (1H)

htfTF = input.string("60", "HTF timeframe (minutes) for S/R block")

// Profit strategy (Option C)

profitStrategy = input.string("Minimal Risk | Full BE after TP1", "Profit Strategy", options = )

// Runner stop mode (your option 4)

runnerStopMode = input.string( "BE only", "Runner Stop Mode", options = )

// ATR trail settings (only used if ATR mode selected)

atrTrailLen = input.int(14, "ATR Length (trail)", minval = 1)

atrTrailMult = input.float(1.0, "ATR Multiplier (trail)", step = 0.1, minval = 0.1)

// Pip size (for XAUUSD: 1 pip = 0.10 if tick = 0.01)

pipSize = syminfo.mintick * 10.0

tp1Points = tp1Pips * pipSize

slPoints = fixedSLpips * pipSize

baseQty = input.float (1.0, "Base order size" , step = 0.01, minval = 0.01)

//━━━━━━━━━━━━━━━━━━━

// 2. DAILY RISK MANAGEMENT

//━━━━━━━━━━━━━━━━━━━

isNewDay = ta.change(time("D")) != 0

var float dayStartEquity = na

var bool dailyStopped = false

equityNow = strategy.initial_capital + strategy.netprofit

if isNewDay or na(dayStartEquity)

dayStartEquity := equityNow

dailyStopped := false

dailyPnL = equityNow - dayStartEquity

dailyPnLPct = dayStartEquity != 0 ? (dailyPnL / dayStartEquity) * 100.0 : 0.0

if not dailyStopped

if dailyPnLPct <= -maxDailyLossPct

dailyStopped := true

if dailyPnLPct >= maxDailyProfitPct

dailyStopped := true

canTradeToday = not dailyStopped

//━━━━━━━━━━━━━━━━━━━

// 3. 1H S/R ZONES (for direction block)

//━━━━━━━━━━━━━━━━━━━

htOpen = request.security(syminfo.tickerid, htfTF, open)

htHigh = request.security(syminfo.tickerid, htfTF, high)

htLow = request.security(syminfo.tickerid, htfTF, low)

htClose = request.security(syminfo.tickerid, htfTF, close)

// Engulf logic on HTF

htBullPrev = htClose > htOpen

htBearPrev = htClose < htOpen

htBearEngulf = htClose < htOpen and htBullPrev and htOpen >= htClose and htClose <= htOpen

htBullEngulf = htClose > htOpen and htBearPrev and htOpen <= htClose and htClose >= htOpen

// Liquidity sweep on HTF previous candle

htSweepHigh = htHigh > ta.highest(htHigh, 5)

htSweepLow = htLow < ta.lowest(htLow, 5)

// Store last HTF zones

var float htResHigh = na

var float htResLow = na

var float htSupHigh = na

var float htSupLow = na

if htBearEngulf and htSweepHigh

htResHigh := htHigh

htResLow := htLow

if htBullEngulf and htSweepLow

htSupHigh := htHigh

htSupLow := htLow

// Are we inside HTF zones?

inHtfRes = not na(htResHigh) and close <= htResHigh and close >= htResLow

inHtfSup = not na(htSupLow) and close >= htSupLow and close <= htSupHigh

// Block direction against HTF zones

longBlockedByZone = inHtfRes // no buys in HTF resistance

shortBlockedByZone = inHtfSup // no sells in HTF support

//━━━━━━━━━━━━━━━━━━━

// 4. 1m LOCAL ZONES (LIQUIDITY SWEEP + ENGULF + QUALITY SCORE)

//━━━━━━━━━━━━━━━━━━━

// 1m engulf patterns

bullPrev1 = close > open

bearPrev1 = close < open

bearEngulfNow = close < open and bullPrev1 and open >= close and close <= open

bullEngulfNow = close > open and bearPrev1 and open <= close and close >= open

// Liquidity sweep by previous candle on 1m

sweepHighPrev = high > ta.highest(high, 5)

sweepLowPrev = low < ta.lowest(low, 5)

// Local zone storage (one active support + one active resistance)

// Quality score: 1 = engulf only, 2 = engulf + sweep (we only trade ≥2)

var float supLow = na

var float supHigh = na

var int supQ = 0

var bool supUsed = false

var float resLow = na

var float resHigh = na

var int resQ = 0

var bool resUsed = false

// New resistance zone: previous bullish candle -> bear engulf

if bearEngulfNow

resLow := low

resHigh := high

resQ := sweepHighPrev ? 2 : 1

resUsed := false

// New support zone: previous bearish candle -> bull engulf

if bullEngulfNow

supLow := low

supHigh := high

supQ := sweepLowPrev ? 2 : 1

supUsed := false

// Raw "inside zone" detection

inSupRaw = not na(supLow) and close >= supLow and close <= supHigh

inResRaw = not na(resHigh) and close <= resHigh and close >= resLow

// QUALITY FILTER: only trade zones with quality ≥ 2 (engulf + sweep)

highQualitySup = supQ >= 2

highQualityRes = resQ >= 2

inSupZone = inSupRaw and highQualitySup and not supUsed

inResZone = inResRaw and highQualityRes and not resUsed

// Plot zones

plot(supLow, "Sup Low", color = color.new(color.lime, 60), style = plot.style_linebr)

plot(supHigh, "Sup High", color = color.new(color.lime, 60), style = plot.style_linebr)

plot(resLow, "Res Low", color = color.new(color.red, 60), style = plot.style_linebr)

plot(resHigh, "Res High", color = color.new(color.red, 60), style = plot.style_linebr)

//━━━━━━━━━━━━━━━━━━━

// 5. MODERATE BOS (3-BAR FRACTAL STRUCTURE)

//━━━━━━━━━━━━━━━━━━━

// 3-bar swing highs/lows

swHigh = high > high and high > high

swLow = low < low and low < low

var float lastSwingHigh = na

var float lastSwingLow = na

if swHigh

lastSwingHigh := high

if swLow

lastSwingLow := low

// BOS conditions

bosUp = not na(lastSwingHigh) and close > lastSwingHigh

bosDown = not na(lastSwingLow) and close < lastSwingLow

// Zone “arming” and BOS validation

var bool supArmed = false

var bool resArmed = false

var bool supBosOK = false

var bool resBosOK = false

// Arm zones when first touched

if inSupZone

supArmed := true

if inResZone

resArmed := true

// BOS after arming → zone becomes valid for entries

if supArmed and bosUp

supBosOK := true

if resArmed and bosDown

resBosOK := true

// Reset BOS flags when new zones are created

if bullEngulfNow

supArmed := false

supBosOK := false

if bearEngulfNow

resArmed := false

resBosOK := false

//━━━━━━━━━━━━━━━━━━━

// 6. ENTRY CONDITIONS (ZONE + BOS + RISK STATE)

//━━━━━━━━━━━━━━━━━━━

flatOrShort = strategy.position_size <= 0

flatOrLong = strategy.position_size >= 0

longSignal = canTradeToday and not longBlockedByZone and inSupZone and supBosOK and flatOrShort

shortSignal = canTradeToday and not shortBlockedByZone and inResZone and resBosOK and flatOrLong

//━━━━━━━━━━━━━━━━━━━

// 7. ORDER LOGIC – TWO PROFIT STRATEGIES

//━━━━━━━━━━━━━━━━━━━

// Common metrics

atrTrail = ta.atr(atrTrailLen)

// MINIMAL MODE: single trade, BE after TP1, optional trailing

// HYBRID MODE: two trades (Scalp @ TP1, Runner @ TP2)

// Persistent tracking

var float longEntry = na

var float longTP1 = na

var float longTP2 = na

var float longSL = na

var bool longBE = false

var float longRunEntry = na

var float longRunTP1 = na

var float longRunTP2 = na

var float longRunSL = na

var bool longRunBE = false

var float shortEntry = na

var float shortTP1 = na

var float shortTP2 = na

var float shortSL = na

var bool shortBE = false

var float shortRunEntry = na

var float shortRunTP1 = na

var float shortRunTP2 = na

var float shortRunSL = na

var bool shortRunBE = false

isMinimal = profitStrategy == "Minimal Risk | Full BE after TP1"

isHybrid = profitStrategy == "Hybrid | Scalp TP + Runner TP"

//━━━━━━━━━━ LONG ENTRIES ━━━━━━━━━━

if longSignal

if isMinimal

longEntry := close

longSL := longEntry - slPoints

longTP1 := longEntry + tp1Points

longTP2 := longEntry + slPoints * runnerRR

longBE := false

strategy.entry("Long", strategy.long)

supUsed := true

supArmed := false

supBosOK := false

else if isHybrid

longRunEntry := close

longRunSL := longRunEntry - slPoints

longRunTP1 := longRunEntry + tp1Points

longRunTP2 := longRunEntry + slPoints * runnerRR

longRunBE := false

// Two separate entries, each 50% of baseQty (for backtest)

strategy.entry("LongScalp", strategy.long, qty = baseQty * 0.5)

strategy.entry("LongRun", strategy.long, qty = baseQty * 0.5)

supUsed := true

supArmed := false

supBosOK := false

//━━━━━━━━━━ SHORT ENTRIES ━━━━━━━━━━

if shortSignal

if isMinimal

shortEntry := close

shortSL := shortEntry + slPoints

shortTP1 := shortEntry - tp1Points

shortTP2 := shortEntry - slPoints * runnerRR

shortBE := false

strategy.entry("Short", strategy.short)

resUsed := true

resArmed := false

resBosOK := false

else if isHybrid

shortRunEntry := close

shortRunSL := shortRunEntry + slPoints

shortRunTP1 := shortRunEntry - tp1Points

shortRunTP2 := shortRunEntry - slPoints * runnerRR

shortRunBE := false

strategy.entry("ShortScalp", strategy.short, qty = baseQty * 50)

strategy.entry("ShortRun", strategy.short, qty = baseQty * 50)

resUsed := true

resArmed := false

resBosOK := false

//━━━━━━━━━━━━━━━━━━━

// 8. EXIT LOGIC – MINIMAL MODE

//━━━━━━━━━━━━━━━━━━━

// LONG – Minimal Risk: 1 trade, BE after TP1, runner to TP2

if isMinimal and strategy.position_size > 0 and not na(longEntry)

// Move to BE once TP1 is touched

if not longBE and high >= longTP1

longBE := true

// Base SL: BE or initial SL

float dynLongSL = longBE ? longEntry : longSL

// Optional trailing after BE

if longBE

if runnerStopMode == "Structure trail" and not na(lastSwingLow) and lastSwingLow > longEntry

dynLongSL := math.max(dynLongSL, lastSwingLow)

if runnerStopMode == "ATR trail"

trailSL = close - atrTrailMult * atrTrail

dynLongSL := math.max(dynLongSL, trailSL)

strategy.exit("Long Exit", "Long", stop = dynLongSL, limit = longTP2)

// SHORT – Minimal Risk: 1 trade, BE after TP1, runner to TP2

if isMinimal and strategy.position_size < 0 and not na(shortEntry)

if not shortBE and low <= shortTP1

shortBE := true

float dynShortSL = shortBE ? shortEntry : shortSL

if shortBE

if runnerStopMode == "Structure trail" and not na(lastSwingHigh) and lastSwingHigh < shortEntry

dynShortSL := math.min(dynShortSL, lastSwingHigh)

if runnerStopMode == "ATR trail"

trailSLs = close + atrTrailMult * atrTrail

dynShortSL := math.min(dynShortSL, trailSLs)

strategy.exit("Short Exit", "Short", stop = dynShortSL, limit = shortTP2)

//━━━━━━━━━━━━━━━━━━━

// 9. EXIT LOGIC – HYBRID MODE

//━━━━━━━━━━━━━━━━━━━

// LONG – Hybrid: Scalp + Runner

if isHybrid

// Scalp leg: full TP at TP1

if strategy.opentrades > 0

strategy.exit("LScalp TP", "LongScalp", stop = longRunSL, limit = longRunTP1)

// Runner leg

if strategy.position_size > 0 and not na(longRunEntry)

if not longRunBE and high >= longRunTP1

longRunBE := true

float dynLongRunSL = longRunBE ? longRunEntry : longRunSL

if longRunBE

if runnerStopMode == "Structure trail" and not na(lastSwingLow) and lastSwingLow > longRunEntry

dynLongRunSL := math.max(dynLongRunSL, lastSwingLow)

if runnerStopMode == "ATR trail"

trailRunSL = close - atrTrailMult * atrTrail

dynLongRunSL := math.max(dynLongRunSL, trailRunSL)

strategy.exit("LRun TP", "LongRun", stop = dynLongRunSL, limit = longRunTP2)

// SHORT – Hybrid: Scalp + Runner

if isHybrid

if strategy.opentrades > 0

strategy.exit("SScalp TP", "ShortScalp", stop = shortRunSL, limit = shortRunTP1)

if strategy.position_size < 0 and not na(shortRunEntry)

if not shortRunBE and low <= shortRunTP1

shortRunBE := true

float dynShortRunSL = shortRunBE ? shortRunEntry : shortRunSL

if shortRunBE

if runnerStopMode == "Structure trail" and not na(lastSwingHigh) and lastSwingHigh < shortRunEntry

dynShortRunSL := math.min(dynShortRunSL, lastSwingHigh)

if runnerStopMode == "ATR trail"

trailRunSLs = close + atrTrailMult * atrTrail

dynShortRunSL := math.min(dynShortRunSL, trailRunSLs)

strategy.exit("SRun TP", "ShortRun", stop = dynShortRunSL, limit = shortRunTP2)

//━━━━━━━━━━━━━━━━━━━

// 10. RESET STATE WHEN FLAT

//━━━━━━━━━━━━━━━━━━━

if strategy.position_size == 0

longEntry := na

shortEntry := na

longBE := false

shortBE := false

longRunEntry := na

shortRunEntry := na

longRunBE := false

shortRunBE := false

//━━━━━━━━━━━━━━━━━━━

// 11. VISUAL ENTRY MARKERS

//━━━━━━━━━━━━━━━━━━━

plotshape(longSignal, title = "Long Signal", style = shape.triangleup,

location = location.belowbar, color = color.lime, size = size.tiny, text = "L")

plotshape(shortSignal, title = "Short Signal", style = shape.triangledown,

location = location.abovebar, color = color.red, size = size.tiny, text = "S")

Gemini Wyckoff Trend SystemStrategy Name: Gemini Wyckoff-Trend System

1. Core Design Philosophy

This strategy fuses Wyckoff Theory (specifically the "Law of Effort vs. Result") with classic Trend Following principles. Its primary goal is not to catch every minor fluctuation, but to filter out 80% of market noise and fakeouts, ensuring that you only pull the trigger when "Smart Money" enters the market with genuine volume.

It operates on a strict "3-Dimension Verification" logic:

Trend (Context): Never trade against the macro trend.

Structure (Price Action): Identify accumulation zones and wait for the breakout.

Volume (Effort): Require massive volume confirmation to validate the move.

2. The 3-Filter System

Filter 1: The Trend Filter (EMA 200)

Rule: The strategy only looks for Long setups when the price is ABOVE the 200-period Exponential Moving Average (EMA).

Purpose: To strictly prevent "catching falling knives" or counter-trend trading during a bear market.

Filter 2: The Structure Filter (Donchian Channel)

Rule: The script automatically identifies the highest high of the past 20 bars to define the "Accumulation Box." A signal is only possible if the price closes above this resistance level.

Wyckoff Term: This represents "Jumping the Creek" (JTC)—signaling that price is leaving the trading range.

Filter 3: The Volume Filter (RVOL > 1.5)

Rule: The breakout bar must have a volume that is at least 1.5x higher than the average volume of the past 20 bars.

Purpose: To eliminate "Upthrusts" (Fake Breakouts). If price breaks out on low volume, the system ignores it.

3. Visual Guide

Once loaded, here is how to read the chart:

📉 Orange Line (EMA 200): The Bull/Bear divider. If price is below this line, stay in cash.

🌫️ Grey Zone: The "No-Trade Zone" (Accumulation/Consolidation). Do not trade while price is inside this box.

🟢 Lime Green Bar: The Entry Signal. This indicates a valid breakout confirmed by high volume (Smart Money entry).

🪜 Red Step Line: Your Trailing Stop (ATR-based). As long as you hold a position, watch this line. If price closes below it, exit immediately.

📊 Dashboard (Top Right): Monitors market "Heat." If RVOL is Green, volume is significant.

4. Best Practices

Ideal For: Traders who struggle with over-trading or FOMO. This script enforces patience and discipline.

Timeframe: Recommended for 4-Hour (4H) or Daily (1D) charts to catch major crypto trends (e.g., Bitcoin main waves).

Asset Class: Crypto, Stocks, or any asset with high volume liquidity.

5. Risk Warning

This strategy includes a built-in ATR Volatility Stop. The stop-loss level adjusts dynamically based on market volatility. Please adhere strictly to the stop-loss signals to protect your capital.

SmartMoneyConcept ProFlow StrategySmartMoneyConcept ProFlow is a complete SMC-based algo built for trending markets and clean volatility phases – especially on crypto pairs like BTC, ETH and perpetual futures.

It combines:

• Smart Money swing structure (BOS / CHoCH)

• Dynamic Support & Resistance levels

• Order Block–style gap detection

• Volatility normalization (ATR / Range / BBWidth)

• SuperTrend trend filter

• ATR & Volume-based exits, TP lock and session control

The goal: fewer random trades, more focused entries when structure + volatility + trend are in sync.

1. Core Idea

Smart Structure Levels (S/R)

– The strategy builds dynamic support/resistance using swing highs/lows.

– Breakouts above resistance or below support, with enough volatility (filter), become primary trade signals.

BOS / CHoCH Engine

– Tracks Break of Structure (BOS) and Change of Character (CHoCH).

– BOS up/down help define the current trend bias.

– CHoCH highlights potential reversals after a confirmed BOS in the opposite direction.

Order Block Gap Logic

– Detects displacement candles with gaps (based on ATR) to approximate OB-style “impulsive moves”.

– Bullish gaps can add confluence for long entries, bearish gaps for shorts.

Volatility-Aware Entries

– Uses normalized volatility (via ATR, Range or BBWidth).

– Filters out breakouts in dead, low-vol environments and focuses on moves with real expansion.

2. Trend & Risk Management Stack

SuperTrend Filter

– Optional “Only With SuperTrend Direction” to restrict entries to the current ST trend.

– ST flips can also force exits if you want to exit as soon as the main trend changes.

ATR-Based Stops & Trails

– ATR distance check to avoid ultra-tight stops that get chopped instantly.

– Three modes:

• StopOnly – classic fixed ATR stop.

• TrailOnly – trailing ATR-style stop.

• StopAndTrail – initial fixed stop that later trails with price.

Volume-Based Exits (Optional)

– Exit on extremely low volume (move losing participation).

– Or on opposite volume spikes (strong counter-pressure against your position).

– Or use Both for a more active volume management.

TP Lock Logic

– When unrealized profit reaches a chosen value, the position is closed and a “lock” can be applied.

– Use this lock to:

• block same-direction re-entries for that side, or

• allow them again depending on your preference.

3. Anti-Churn & Session Control

Anti-Churn Controls

– Minimum bars between entries.

– Cooldown after an ATR exit.

– Limit of max entries per bar.

Session Filter

– Restrict trading to a specific hourly window (e.g. main market session).

– Option to force close positions outside your active session.

– Handy for intraday traders who don’t want overnight or low-liquidity exposure.

4. SmartMoney Preset Modes

Preset Mode:

• EtherFlux – more flexible, for general breakout & volatility trading.

• SmartMoney – SMC-focused preset:

– Adjusted length, volatility filter and ATR settings.

– Option to disable exits from the strategy side (for manual risk control).

Switching presets automatically tunes multiple internal parameters so you don’t have to micromanage every input each time.

5. Visual Layer

This script has a complete visual suite to help you “read the tape”:

– Bar Colors by position and SuperTrend bias.

– Support / Resistance dots and lines (stepline style).

– Order Block markers (bullish / bearish gap labels).

– BOS / CHoCH labels to track structure shifts in real-time.

– Liquidation Zones (visual only)

• Approximate long and short liquidation areas based on assumed leverage.

• Shaded zones on the chart for quick liquidity map.

– Status Labels

• Session status (ACTIVE / OFF / DISABLED).

• Current position (LONG / SHORT / FLAT).

• TP Lock status (longs locked / shorts locked / no lock).

All visuals are designed for dark charts but also work on light themes with minor tweaks.

6. Quick Input Guide

• Levels Period & Volatility Filter – main structure sensitivity and breakout quality.

• Volatility Method – ATR / Range / BBWidth normalization for the vol filter.

• ATR Stop & Management – core risk rules: ATR multiplier, stop/trail mode, min ATR distance.

• SuperTrend Settings – trend bias and ST-flip exits.

• SmartMoney Preset – quick switch between EtherFlux and SmartMoney tuning.

• Volume Exits – low volume / opposite spike / both.

• Session Filter – hour-based trading window + optional forced flat outside session.

• Follow-Signal Mode – flip from long→short or short→long when signal reverses (signal-based rotation).

• TP Lock – secure profits at a fixed amount and optionally block same-direction re-entries.

• Liq Zones – visual only, for liquidity map (no direct trade logic).

How to Use (My Suggestion)

Start on 15m–4H charts for liquid pairs (BTC, ETH, majors).

Choose your preset:

– EtherFlux for more general breakout + vol trading.

– SmartMoney if you want stricter SMC behaviour.

Turn on SuperTrend + ATR stops for cleaner risk management.

Forward-test in replay / paper trading before using real capital.

Use the visual BOS/CHoCH + Liq Zones as context , not as blind signals.

Important

This is a backtest & research tool . It is not financial advice and does not guarantee profits. Always combine it with your own risk management, position sizing, and forward-testing before going live. Trading leveraged products and crypto can result in partial or full loss of capital.

RC - Crypto Scalper v3Cryptocurrency scalping strategy for perpetual futures with risk management and automation capabilities.

## Strategy Overview

This strategy identifies high-probability scalping opportunities in cryptocurrency perpetual futures markets using adaptive position sizing, dynamic stop losses, and intelligent exit management to maintain consistent risk-adjusted returns across varying market conditions.

## Technical Foundation

The strategy employs exponential moving averages for trend detection, Bollinger Bands for volatility measurement and mean reversion signals, RSI for momentum confirmation and overbought/oversold conditions, ATR for dynamic volatility-based stop placement, and VWAP for institutional price level identification. These technical indicators are combined with volume analysis and optional multi-timeframe confirmation to filter low-probability setups.

## Entry Methodology

The strategy identifies trading opportunities using three complementary approaches that can be enabled individually or in combination:

Momentum-Based Entries: Detects directional price movements aligned with short-term and intermediate-term trend indicators, with momentum oscillator confirmation to avoid entries at exhaustion points. Volume analysis provides additional confirmation of institutional participation.

Mean Reversion Entries: Identifies price extremes using statistical volatility bands combined with momentum divergence, targeting high-probability reversal zones in ranging market conditions. Entries require initial price structure confirmation to reduce false signals.

Institutional Flow Entries: Monitors volume-weighted price levels to identify areas where institutional orders are likely concentrated, entering on confirmed breaks of these key levels with supporting directional bias from trend indicators.

Each methodology uses distinct combinations of the technical indicators mentioned above, with specific parameter relationships and confirmation requirements that can be customized based on trader preference and market conditions.

## Exit Framework

Adaptive Stop Loss: Uses ATR-based stops (default 0.7x multiplier on 14-period ATR) that automatically adjust to current market volatility. Stop distance expands during volatile periods to avoid premature stops while tightening during consolidation to protect capital. Alternative percentage-based stops available for traders preferring fixed-distance risk management.

Trailing Profit System: Employs a dual-target exit approach combining fixed limit orders with dynamic trailing stops. The system activates trailing stops when positions reach profitable thresholds, allowing winning trades to capture extended moves while protecting accumulated gains. The high fixed limit (6R default) serves as a ceiling for exceptional moves while the trailing mechanism handles the majority of exits at optimal profit levels.

Time-Based Management: Implements maximum holding period constraints (50 bars default) to prevent capital from being trapped in directionless price action. This ensures consistent capital turnover and prevents the strategy from holding through extended consolidation periods.

Breakeven Protection: Automatically adjusts stop loss to entry price plus commission costs once trades reach predefined profit thresholds (0.7R default), eliminating downside risk on positions that have demonstrated directional follow-through.

## Risk Management

Position Sizing: Dynamic position sizing based on account equity percentage risk model (2% default). Calculates optimal position size based on entry price, stop distance, and account risk tolerance. Includes maximum position exposure caps and minimum position size thresholds to ensure practical trade execution.

Daily Loss Limits: Automatic trading suspension when intraday losses exceed configured threshold (5% of equity default). Prevents catastrophic drawdown days and removes emotional decision-making during adverse market conditions. Resets automatically at the start of each new trading day.

Leverage Controls: Comprehensive leverage monitoring with built-in liquidation protection for margined positions. Strategy calculates liquidation prices based on leverage settings and automatically closes positions approaching critical margin levels, preventing forced liquidations.

Exposure Management: Multiple layers of position size controls including maximum position value as percentage of equity (50% default), leverage-adjusted margin requirements, and minimum capital availability thresholds before opening new positions.

## Market Filters

Session-Based Filtering: Configurable trading windows for Asian (00:00-08:00 UTC), London (08:00-16:00 UTC), and New York (13:00-21:00 UTC) sessions. Allows traders to focus on specific market hours or avoid illiquid periods based on their asset and trading style.

Volatility Requirements: Minimum and maximum ATR percentage thresholds ensure strategy only operates within optimal volatility ranges. Prevents trading during both insufficient movement periods and extreme volatility events where execution quality deteriorates.

Trend Alignment: Optional higher timeframe trend filter ensures directional bias aligns with broader market structure, reducing counter-trend entries during strong directional moves.

Volume Confirmation: Configurable volume requirements for entry validation, ensuring sufficient market participation and reducing false signals during low-liquidity periods.

## Automation Support

Built-in webhook integration generates JSON payloads compatible with popular broker automation platforms. Alert system provides comprehensive notifications for all entry signals, exit executions, risk limit breaches, and daily trading status updates. Supports both automated and manual execution workflows.

## Settings Explanation

Initial Capital: $5,000

Selected as realistic starting point for retail traders entering crypto futures markets. Strategy scales proportionally - larger accounts show similar percentage returns with proportionally larger absolute gains and position sizes.

Risk Per Trade: 2%

Conservative default providing significant drawdown tolerance. With 51% historical win rate and positive expectancy, risking 2% per trade allows for extended losing streaks without account impairment. Adjustable from 0.5% (very conservative) to 5% (aggressive, experienced traders only).

Leverage: 10x

Standard cross-margin leverage for cryptocurrency perpetual futures. Combined with 2% risk setting and maximum 50% equity position size caps, actual exposure remains controlled despite leverage. Built-in liquidation protection provides additional safety layer.

Commission: 0.055%

Modeled on major exchange maker fee structures (Bybit, Binance Futures).

**Slippage: 50 ticks**

Ultra-conservative slippage assumption representing extreme worst-case execution scenarios. ETH perpetual tick size is $0.01, therefore 50 ticks equals $0.50 per side or $1.00 round trip slippage per trade.

Real-world slippage on 30-minute timeframe typically ranges from 2-5 ticks ($0.02-0.05 round trip) under normal conditions, with 10-20 ticks during highly volatile periods. The 50-tick setting assumes every single trade executes during extreme market stress conditions.

This ultra-conservative modeling approach means real-world trading performance under typical market conditions may exceed backtest results, as the strategy has been tested under punishing execution cost assumptions that represent worst-case scenarios rather than expected outcomes.

Stop Loss: ATR-based (0.7x multiplier)

Volatility-adaptive stops optimized for 30-minute cryptocurrency perpetuals. The 0.7x multiplier balances protection against premature stops due to normal market noise. Lower multipliers (0.5-0.6x) suitable for lower timeframes, higher multipliers (0.8-1.2x) for higher timeframes.

Take Profit: 6R (Risk:Reward)

High target designed to work in conjunction with trailing stop system rather than as primary exit mechanism. Historical analysis shows most profitable trades exit via trailing stops at lower multiples, with the 6R limit capturing occasional extended moves. This configuration allows the trailing stop system to operate optimally while providing upside capture on exceptional price runs.

Trailing Stop: Activates at 1R | Offset 0.5R

Trailing mechanism engages when position reaches 1:1 risk-reward, then maintains 0.5R distance from peak favourable price. This configuration allows profitable trades room to develop while protecting accumulated gains from reversals.

Maximum Holding Period: 50 bars

Automatic exit trigger after 50 bars (25 hours on 30-minute timeframe) prevents capital commitment to non-trending price action. Adjustable based on timeframe and trading style preferences.

## Backtest Performance

Test Period: November 2023 - November 2025 (2 years)

Asset: ETH/USDT Perpetual Futures

Timeframe: 30 minutes

Initial Capital: $5,000

Performance Metrics:

- Final Equity: $25,353.99

- Net Profit: $20,353.99

- Total Return: 407.08%

- Annualized Return: ~204%

- Total Trades: 2,549

- Winning Trades: 1,308 (51.28%)

- Losing Trades: 1,241 (48.72%)

- Profit Factor: 1.215

- Sharpe Ratio: 0.813

- Sortino Ratio: 6.428

- Maximum Drawdown: 11.53%

- Average Drawdown: <2%

Trade Statistics:

- Average Win: 1.15% per trade

- Average Loss: -0.98% per trade

- Win/Loss Ratio: 1.17:1

- Largest Win: 7.14%

- Largest Loss: -2.31%

- Average Trade Duration: ~8 hours

- Trades Per Month: ~106

Cost Analysis:

- Total Commission Paid: $21,277.06

- Commission as % of Gross Profit: 18.5%

- Modeled Slippage Impact: $2,549.00 (50 ticks per trade)

- Total Trading Costs: $23,826.06

- Net Profit After All Costs: $20,353.99

Risk-Adjusted Performance:

- Return/Max DD Ratio: 35.3

- Profit Per Trade: $7.98 average

- Risk of Ruin: <0.001% (with 2% risk, 51% win rate, 1.17 R:R)

## Bear Market Validation

To validate robustness across different market conditions, the strategy was additionally tested during the 2022 cryptocurrency bear market:

Test Period: May 2022 - November 2022 (7 months)

Market Conditions: ETH declined 57% (from ~$2,900 to ~$1,200)

Bear Market Results:

- Net Profit: $4,959.69

- Return: 99.19%

- Total Trades: 845

- Win Rate: 51.72%

- Maximum Drawdown: 18.54%

- Profit Factor: 1.235

- Outperformance vs Buy & Hold: +156.3%

The strategy demonstrated profitable performance during severe market decline, with short positions showing particular strength (54.1% win rate on shorts vs 49.4% on longs). This validates that the edge is not dependent on bullish market conditions and the multiple entry methodologies adapt naturally to different market environments.

## Recommended Usage

Optimal Timeframes:

- Primary: 30-minute (tested and optimized)

- Alternative: 1-hour (more selective, fewer trades)

- Not recommended: <15-minute (execution quality deteriorates)

Suitable Assets:

High-liquidity cryptocurrency perpetual futures recommended:

- BTC/USDT (>$2B daily volume)

- ETH/USDT (>$1B daily volume)

- SOL/USDT, AVAX/USDT (>$100M daily volume)

- Avoid low-liquidity pairs (<$50M daily volume)

Risk Configuration:

- Conservative: 1-1.5% per trade

- Moderate: 2-3% per trade (default: 2%)

- Aggressive: 3-5% per trade (requires discipline)

## Important Considerations

Backtesting vs Live Trading: Always paper trade first. Real-world results vary based on execution quality, broker-specific factors, network latency, and individual trade management decisions. Backtest performance represents historical simulation with ultra-conservative cost assumptions, not guaranteed future results.

Market Conditions: Strategy designed for liquid, actively-traded markets. Performance characteristics:

- Strong trends: Optimal (trailing stops capture extended moves)

- Ranging markets: Moderate (mean reversion component provides edge)

- Low volatility: Reduced (ATR filter prevents most entries)

- Extreme volatility: Protected (maximum volatility filter prevents entries)

Cost Impact: Commission represents approximately 18.5% of gross profit in backtests. The 50-tick slippage assumption is deliberately punitive - typical execution will likely be 5-10x better (2-10 ticks actual vs 50 ticks modeled), meaning real-world net results may significantly exceed backtest performance under normal market conditions.

Execution Quality: 30-minute timeframe provides sufficient time for order placement and management. Automated execution recommended for consistency. Manual execution requires discipline to follow signals without hesitation or second-guessing.

Starting Procedures:

1. Run backtest on your specific asset and timeframe

2. Paper trade for minimum 50 trades or 2 weeks

3. Start with minimum position sizes (0.5-1% risk)

4. Gradually scale to target risk levels as confidence builds

5. Monitor actual execution costs vs backtest assumptions

## Strategy Limitations

- Requires liquid markets; performance degrades significantly on low-volume pairs

- No built-in news event calendar; traders should manually avoid scheduled high-impact events

- Weekend/holiday trading may experience wider spreads and different price behaviour

- Does not model spread costs (assumes mid-price fills); add 1-2 ticks additional cost for market orders

- Performance during market structure changes (regime shifts) may differ from backtest period

- Requires consistent monitoring during active trading hours for optimal automated execution

- Slippage assumptions are deliberately extreme; actual slippage will typically be much lower

## Risk Disclosure

Cryptocurrency trading involves substantial risk of loss. Leverage amplifies both gains and losses. This strategy will experience losing streaks and drawdowns. The 11.53% maximum historical drawdown in bull market testing and 18.54% in bear market testing do not represent ceilings - larger drawdowns are possible and should be expected in live trading.

Past performance does not guarantee future results. Market conditions evolve, and historical edge may diminish or disappear. No strategy works in all market conditions. The strategy has been tested with extremely conservative slippage assumptions (50 ticks per trade) that significantly exceed typical execution costs; this provides a safety margin but does not eliminate risk.

Capital at Risk: Only trade with capital you can afford to lose completely. The strategy's positive historical performance across both bull and bear markets does not eliminate the possibility of significant losses or account impairment.

Not Financial Advice: This strategy is an educational tool, not investment advice. Users are solely responsible for their trading decisions, risk management, and outcomes. The developer assumes no liability for trading losses.

Leverage Warning: Trading with leverage can result in losses exceeding initial investment. Ensure you understand leverage mechanics and liquidation risks before using leveraged products.

## Technical Requirements

- TradingView Premium subscription (for strategy testing and alerts)

- Understanding of risk management principles

- Familiarity with perpetual futures mechanics

- Broker account supporting crypto perpetuals (if trading live)

- For automation: Webhook-compatible execution platform

## Version History

v3.0 - November 2025 (Initial Release)

- Multi-methodology entry system (Momentum, Mean Reversion, VWAP)

- Comprehensive risk management framework

- Adaptive exit system with trailing stops

- Session and volatility filtering

- Webhook automation support

- Validated across bull market (2024-25) and bear market (2022) periods

- Tested with ultra-conservative 50-tick slippage assumptions

Disclaimer: This strategy is provided "as-is" for educational purposes. Past performance does not indicate future results. All backtests conducted with 50-tick slippage (ultra-conservative assumptions). Actual trading costs typically significantly lower. Trade responsibly and at your own risk.

Stochastic Hash Strat [Hash Capital Research]# Stochastic Hash Strategy by Hash Capital Research

## 🎯 What Is This Strategy?

The **Stochastic Slow Strategy** is a momentum-based trading system that identifies oversold and overbought market conditions to capture mean-reversion opportunities. Think of it as a "buy low, sell high" approach with smart mathematical filters that remove emotion from your trading decisions.

Unlike fast-moving indicators that generate excessive noise, this strategy uses **smoothed stochastic oscillators** to identify only the highest-probability setups when momentum truly shifts.

---

## 💡 Why This Strategy Works

Most traders fail because they:

- **Chase prices** after big moves (buying high, selling low)

- **Overtrade** in choppy, directionless markets

- **Exit too early** or hold losses too long

This strategy solves all three problems:

1. **Entry Discipline**: Only trades when the stochastic oscillator crosses in extreme zones (oversold for longs, overbought for shorts)

2. **Cooldown Filter**: Prevents revenge trading by forcing a waiting period after each trade

3. **Fixed Risk/Reward**: Pre-defined stop-loss and take-profit levels ensure consistent risk management

**The Math Behind It**: The stochastic oscillator measures where the current price sits relative to its recent high-low range. When it's below 25, the market is oversold (time to buy). When above 70, it's overbought (time to sell). The crossover with its moving average confirms momentum is shifting.

---

## 📊 Best Markets & Timeframes

### ⭐ OPTIMAL PERFORMANCE:

**Crude Oil (WTI) - 12H Timeframe**

- **Why it works**: Oil markets have predictable volatility patterns and respect technical levels

**AAVE/USD - 4H to 12H Timeframe**

- **Why it works**: DeFi tokens exhibit strong momentum cycles with clear extremes

### ✅ Also Works Well On:

- **BTC/USD** (12H, Daily) - Lower frequency but high win rate

- **ETH/USD** (8H, 12H) - Balanced volatility and liquidity

- **Gold (XAU/USD)** (Daily) - Classic mean-reversion asset

- **EUR/USD** (4H, 8H) - Lower volatility, requires patience

### ❌ Avoid Using On:

- Timeframes below 4H (too much noise)

- Low-liquidity altcoins (wide spreads kill performance)

- Strongly trending markets without pullbacks (Bitcoin in 2021)

- News-driven instruments during major events

---

## 🎛️ Understanding The Settings

### Core Stochastic Parameters

**Stochastic Length (Default: 16)**

- Controls the lookback period for price comparison

- Lower = faster reactions, more signals (10-14 for volatile markets)

- Higher = smoother signals, fewer trades (16-21 for stable markets)

- **Pro tip**: Use 10 for crypto 4H, 16 for commodities 12H

**Overbought Level (Default: 70)**

- Threshold for short entries

- Lower values (65-70) = more trades, earlier entries

- Higher values (75-80) = fewer but higher-conviction trades

- **Sweet spot**: 70 works for most assets

**Oversold Level (Default: 25)**

- Threshold for long entries

- Higher values (25-30) = more trades, earlier entries

- Lower values (15-20) = fewer but stronger bounce setups

- **Sweet spot**: 20-25 depending on market conditions

**Smooth K & Smooth D (Default: 7 & 3)**

- Additional smoothing to filter out whipsaws

- K=7 makes the indicator slower and more reliable

- D=3 is the signal line that confirms the trend

- **Don't change these unless you know what you're doing**

---

### Risk Management

**Stop Loss % (Default: 2.2%)**

- Automatically exits losing trades

- Should be 1.5x to 2x your average market volatility

- Too tight = death by a thousand cuts

- Too wide = uncontrolled losses

- **Calibration**: Check ATR indicator and set SL slightly above it

**Take Profit % (Default: 7%)**

- Automatically exits winning trades

- Should be 2.5x to 3x your stop loss (reward-to-risk ratio)

- This default gives 7% / 2.2% = 3.18:1 R:R

- **The golden rule**: Never have R:R below 2:1

---

### Trade Filters

**Bar Cooldown Filter (Default: ON, 3 bars)**

- **What it does**: Forces you to wait X bars after closing a trade before entering a new one

- **Why it matters**: Prevents emotional revenge trading and overtrading in choppy markets

- **Settings guide**:

- 3 bars = Standard (good for most cases)

- 5-7 bars = Conservative (oil, slow-moving assets)

- 1-2 bars = Aggressive (only for experienced traders)

**Exit on Opposite Extreme (Default: ON)**

- Closes your long when stochastic hits overbought (and vice versa)

- Acts as an early profit-taking mechanism

- **Leave this ON** unless you're testing other exit strategies

**Divergence Filter (Default: OFF)**

- Looks for price/momentum divergences for additional confirmation

- **When to enable**: Trending markets where you want fewer but higher-quality trades

- **Keep OFF for**: Mean-reverting markets (oil, forex, most of the time)

---

## 🚀 Quick Start Guide

### Step 1: Set Up in TradingView

1. Open TradingView and navigate to your chart

2. Click "Pine Editor" at the bottom

3. Copy and paste the strategy code

4. Click "Add to Chart"

5. The strategy will appear in a separate pane below your price chart

### Step 2: Choose Your Market

**If you're trading Crude Oil:**

- Timeframe: 12H

- Keep all default settings

- Watch for signals during London/NY overlap (8am-11am EST)

**If you're trading AAVE or crypto:**

- Timeframe: 4H or 12H

- Consider these adjustments:

- Stochastic Length: 10-14 (faster)

- Oversold: 20 (more aggressive)

- Take Profit: 8-10% (higher targets)

### Step 3: Wait for Your First Signal

**LONG Entry** (Green circle appears):

- Stochastic crosses up below oversold level (25)

- Price likely near recent lows

- System places limit order at take profit and stop loss

**SHORT Entry** (Red circle appears):

- Stochastic crosses down above overbought level (70)

- Price likely near recent highs

- System places limit order at take profit and stop loss

**EXIT** (Orange circle):

- Position closes either at stop, target, or opposite extreme

- Cooldown period begins

### Step 4: Let It Run

The biggest mistake? **Interfering with the system.**

- Don't close trades early because you're scared

- Don't skip signals because you "have a feeling"

- Don't increase position size after a big win

- Don't revenge trade after a loss

**Follow the system or don't use it at all.**

---

### Important Risks:

1. **Drawdown Pain**: You WILL experience losing streaks of 5-7 trades. This is mathematically normal.

2. **Whipsaw Markets**: Choppy, range-bound conditions can trigger multiple small losses.

3. **Gap Risk**: Overnight gaps can cause your actual fill to be worse than the stop loss.

4. **Slippage**: Real execution prices differ from backtested prices (factor in 0.1-0.2% slippage).

---

## 🔧 Optimization Guide

### When to Adjust Settings:

**Market Volatility Increased?**

- Widen stop loss by 0.5-1%

- Increase take profit proportionally

- Consider increasing cooldown to 5-7 bars

**Getting Too Few Signals?**

- Decrease stochastic length to 10-12

- Increase oversold to 30, decrease overbought to 65

- Reduce cooldown to 2 bars

**Getting Too Many Losses?**

- Increase stochastic length to 18-21 (slower, smoother)

- Enable divergence filter

- Increase cooldown to 5+ bars

- Verify you're on the right timeframe

### A/B Testing Method:

1. **Run default settings for 50 trades** on your chosen market

2. Document: Win rate, profit factor, max drawdown, emotional tolerance

3. **Change ONE variable** (e.g., oversold from 25 to 20)

4. Run another 50 trades

5. Compare results

6. Keep the better version

**Never change multiple settings at once** or you won't know what worked.

---

## 📚 Educational Resources

### Key Concepts to Learn:

**Stochastic Oscillator**

- Developed by George Lane in the 1950s

- Measures momentum by comparing closing price to price range

- Formula: %K = (Close - Low) / (High - Low) × 100

- Similar to RSI but more sensitive to price movements

**Mean Reversion vs. Trend Following**

- This is a **mean reversion** strategy (price returns to average)

- Works best in ranging markets with defined support/resistance

- Fails in strong trending markets (2017 Bitcoin, 2020 Tech stocks)

- Complement with trend filters for better results

**Risk:Reward Ratio**

- The cornerstone of profitable trading

- Winning 40% of trades with 3:1 R:R = profitable

- Winning 60% of trades with 1:1 R:R = breakeven (after fees)

- **This strategy aims for 45% win rate with 2.5-3:1 R:R**

### Recommended Reading:

- *"Trading Systems and Methods"* by Perry Kaufman (Chapter on Oscillators)

- *"Mean Reversion Trading Systems"* by Howard Bandy

- *"The New Trading for a Living"* by Dr. Alexander Elder

---

## 🛠️ Troubleshooting

### "I'm not seeing any signals!"

**Check:**

- Is your timeframe 4H or higher?

- Is the stochastic actually reaching extreme levels (check if your asset is stuck in middle range)?

- Is cooldown still active from a previous trade?

- Are you on a low-liquidity pair?

**Solution**: Switch to a more volatile asset or lower the overbought/oversold thresholds.

---

### "The strategy keeps losing money!"

**Check:**

- What's your win rate? (Below 35% is concerning)

- What's your profit factor? (Below 0.8 means serious issues)

- Are you trading during major news events?

- Is the market in a strong trend?

**Solution**:

1. Verify you're using recommended markets/timeframes

2. Increase cooldown period to avoid choppy markets

3. Reduce position size to 5% while you diagnose

4. Consider switching to daily timeframe for less noise

---

### "My stop losses keep getting hit!"

**Check:**

- Is your stop loss tighter than the average ATR?

- Are you trading during high-volatility sessions?

- Is slippage eating into your buffer?

**Solution**:

1. Calculate the 14-period ATR

2. Set stop loss to 1.5x the ATR value

3. Avoid trading right after market open or major news

4. Factor in 0.2% slippage for crypto, 0.1% for oil

---

## 💪 Pro Tips from the Trenches

### Psychological Discipline

**The Three Deadly Sins:**

1. **Skipping signals** - "This one doesn't feel right"

2. **Early exits** - "I'll just take profit here to be safe"

3. **Revenge trading** - "I need to make back that loss NOW"

**The Solution:** Treat your strategy like a business system. Would McDonald's skip making fries because the cashier "doesn't feel like it today"? No. Systems work because of consistency.

---

### Position Management

**Scaling In/Out** (Advanced)

- Enter 50% position at signal

- Add 50% if stochastic reaches 10 (oversold) or 90 (overbought)

- Exit 50% at 1.5x take profit, let the rest run

**This is NOT for beginners.** Master the basic system first.

---

### Market Awareness

**Oil Traders:**

- OPEC meetings = volatility spikes (avoid or widen stops)

- US inventory reports (Wed 10:30am EST) = avoid trading 2 hours before/after

- Summer driving season = different patterns than winter

**Crypto Traders:**

- Monday-Tuesday = typically lower volatility (fewer signals)

- Thursday-Sunday = higher volatility (more signals)

- Avoid trading during exchange maintenance windows

---

## ⚖️ Legal Disclaimer

This trading strategy is provided for **educational purposes only**.

- Past performance does not guarantee future results

- Trading involves substantial risk of loss

- Only trade with capital you can afford to lose

- No one associated with this strategy is a licensed financial advisor

- You are solely responsible for your trading decisions

**By using this strategy, you acknowledge that you understand and accept these risks.**

---

## 🙏 Acknowledgments

Strategy development inspired by:

- George Lane's original Stochastic Oscillator work

- Modern quantitative trading research

- Community feedback from hundreds of backtests

Built with ❤️ for retail traders who want systematic, disciplined approaches to the markets.

---

**Good luck, stay disciplined, and trade the system, not your emotions.**

LeiRos PRO — Smart Entry & Target System⚡ Short Description

LeiRos PRO is more than an indicator.

It is an intelligent next-generation analytical tool designed to visualize the true trajectory of market movement.

It reveals the hidden mechanics of price — the attraction points where liquidity is collected and extremes are updated before reversal.

🟢 During bullish phases, the market often reaches for previous highs.

Green points of LeiRos PRO highlight the levels price is most likely to reach before completing the impulse.

⚪ In bearish phases, the market tends to sweep uncollected lows.

White points indicate where stop hunts and local reversals commonly occur.

Built upon the interaction of EMA20 / EMA50 / EMA200, volatility analysis and momentum strength,

LeiRos PRO doesn’t just mark levels — it displays realistic targets price is drawn to with high probability.

📈 The higher the timeframe, the clearer and more stable the picture becomes.

On H1 and above, the plotted points act as reference zones for those seeking structured, logical price behavior rather than noise.

💡 The main advantage of LeiRos PRO is clarity — it removes guessing.

You see where price tends to move and where impulses are likely to end.

This is not theory — it’s market behavior visualized.

📘 Full Description

LeiRos PRO is a proprietary analytical tool created to precisely visualize directional bias, target zones, and protective stop areas.

It combines trend structure, volatility, and price action logic — helping traders see the key areas where the market’s intent becomes clear.

📈 Core Features:

Automatic trend detection: analyzes direction using EMA20, EMA50, and EMA200 to define the dominant side of the market.

Target visualization (Take-Profit): marks potential liquidity-grab zones where price often completes its move.

Protective stop zones (Stop-Loss): highlights areas where logical stops can be placed based on current structure.

Adaptive to timeframe: higher timeframes provide cleaner and more reliable reference points, suitable for short-, medium-, and long-term analysis.

⚙️ Recommended Use:

As a visual analytical tool for confirming trade direction.

On lower TFs — for identifying intraday entry points and potential objectives.

On higher TFs (H1 and above) — for building overall market context and defining major targets.

Marked points are not entry signals,

but contextual reference zones showing potential areas of liquidity collection or impulse completion.

⚠️ Disclaimer:

LeiRos PRO is an analytical and visualization tool, not a trading signal or guarantee of results.

All trading decisions, entries, exits, and risk management remain solely the responsibility of the user.

✳️ Note: