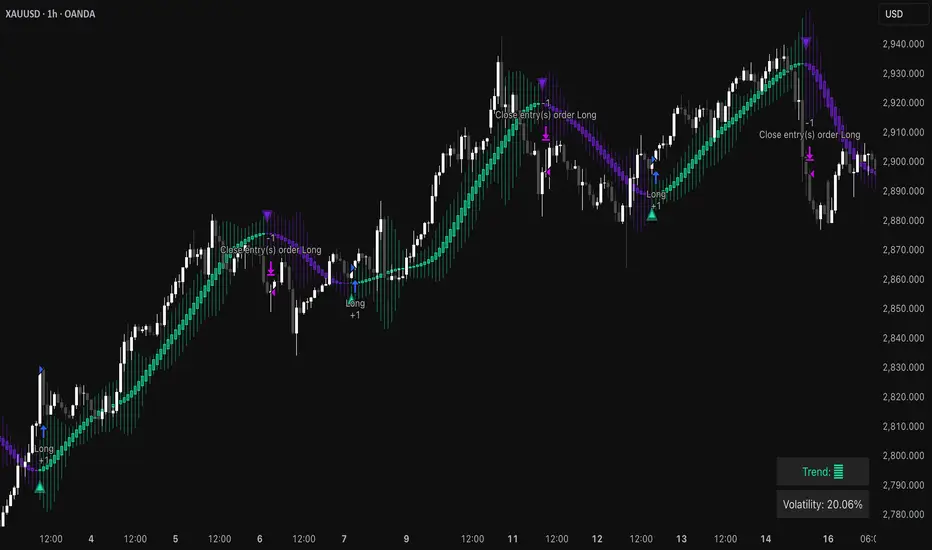

Triangular Hull Moving Average [BigBeluga X PineIndicators]This strategy is based on the original Triangular Hull Moving Average (THMA) + Volatility indicator by BigBeluga. Full credit for the concept and design goes to BigBeluga.

The strategy blends smoothed trend-following logic using a Triangular Hull Moving Average with dynamic volatility overlays, providing actionable trade signals with responsive visual feedback. It's designed for traders who want a non-lagging trend filter while also monitoring market volatility in real time.

How the Strategy Works

1. Triangular Hull Moving Average (THMA) Core

At its core, the strategy uses a Triangular Hull Moving Average (THMA) — a variation of the traditional Hull Moving Average with triple-smoothing logic:

It combines multiple weighted moving averages (WMAs) to create a faster and smoother trend line.

This reduces lag without compromising trend accuracy.

The THMA reacts more responsively to price movements than classic MAs.

THMA Formula:

thma(_src, _length) =>

ta.wma(ta.wma(_src,_length / 3) * 3 - ta.wma(_src, _length / 2) - ta.wma(_src, _length), _length)

This logic filters out short-term noise while still being sensitive to genuine trend shifts.

2. Volatility-Enhanced Candle Plotting

An optional volatility mode overlays the chart with custom candles that incorporate volatility bands:

Wicks expand and contract dynamically based on market volatility.

The volatility value is computed using a HMA of high-low range over a user-defined length.

The candle bodies reflect THMA values, while the wicks reflect the current volatility spread.

This feature allows traders to visually gauge the strength of price moves and anticipate possible breakouts or slowdowns.

3. Trend Reversal Signal Detection

The strategy identifies trend reversals when the THMA line crosses over/under its own past value:

A bullish signal is triggered when THMA crosses above its value from two bars ago.

A bearish signal is triggered when THMA crosses below its value from two bars ago.

These shifts are marked on the chart with triangle-shaped signals for clear visibility.

This logic helps detect momentum shifts early and enables reactive trade entries.

Trade Entry & Exit Logic

Trade Modes Supported

Users can choose between:

Only Long – Enters long trades only.

Only Short – Enters short trades only.

Long & Short – Enables both directions.

Entry Conditions

Long Entry:

Triggered when a bullish crossover is detected.

Active only if the strategy mode allows long trades.

Short Entry:

Triggered when a bearish crossover is detected.

Active only if the strategy mode allows short trades.

Exit Conditions

In Only Long mode, the strategy closes long positions when a bearish signal appears.

In Only Short mode, the strategy closes short positions when a bullish signal appears.

In Long & Short mode, the strategy does not auto-close positions — instead, it opens new positions on each confirmed signal.

Dashboard Visualization

In the bottom-right corner of the chart, a live dashboard displays:

The current trend direction (🢁 for bullish, 🢃 for bearish).

The current volatility level as a percentage.

This helps traders quickly assess market status and adjust their decisions accordingly.

Customization Options

THMA Length: Adjust how smooth or reactive the trend detection should be.

Volatility Toggle & Length: Enable or disable volatility visualization and set sensitivity.

Color Settings: Choose colors for up/down trend visualization.

Trade Direction Mode: Limit the strategy to long, short, or both types of trades.

Use Cases & Strategy Strengths

1. Trend Following

Use the THMA-based candles and triangle signals to enter with momentum. The indicator adapts quickly, reducing lag and improving trade timing.

2. Volatility Monitoring

Visualize the strength of the trend with volatility wicks. Use expanding bands to confirm breakouts and contracting ones to detect weakening moves.

3. Signal Confirmation

Combine this tool with other indicators or use the trend shift triangles as confirmations for manual entries.

Conclusion

The THMA + Volatility Strategy is a non-repainting trend-following system that integrates:

Triangular Hull MA for advanced trend detection.

Real-time volatility visualization.

Clear entry signals based on trend reversals.

Configurable trade direction settings.

It is ideal for traders who:

Prefer smoothed price analysis.

Want to follow trends with precision.

Value visual volatility feedback for breakout detection.

Full credit for the original concept and indicator goes to BigBeluga.

Cari dalam skrip untuk "momentum"

EMA Scoring Strategy## **📊 EMA Scoring Strategy for Trend Analysis**

This strategy is designed to **identify bullish trends** based on multiple **Exponential Moving Averages (EMAs)**. It assigns a **score** based on how the price and EMAs interact, and highlights strong bullish conditions when the score reaches **4 or above**.

---

## **🔹 Strategy Logic**

### 1️⃣ **Calculating EMAs**

- **EMA 21** → Short-term trend

- **EMA 50** → Mid-term trend

- **EMA 100** → Long-term trend

---

### 2️⃣ **Scoring System**

For each trading day, the strategy assigns **+1 or -1 points** based on the following conditions:

| Condition | Score |

|-----------|-------|

| If **Price > EMA 21** | +1 |

| If **Price > EMA 50** | +1 |

| If **Price > EMA 100** | +1 |

| If **EMA 21 > EMA 50** | +1 |

| If **EMA 50 > EMA 100** | +1 |

| If **EMA 21 > EMA 100** | +1 |

| If **Price < EMA 21** | -1 |

| If **Price < EMA 50** | -1 |

| If **Price < EMA 100** | -1 |

| If **EMA 21 < EMA 50** | -1 |

| If **EMA 50 < EMA 100** | -1 |

| If **EMA 21 < EMA 100** | -1 |

---

### 3️⃣ **Bullish Confirmation** (Score ≥ 4)

- The **score is calculated every day**.

- When the **score reaches 4 or above**, it confirms a strong **bullish trend**.

- A **green background** is applied to highlight such days.

- A **histogram** is plotted **only when the score is 4 or higher** to keep the chart clean.

- A **buy signal** is generated when the score **crosses above 4**.

---

## **🔹 Visualization & Alerts**

### ✅ **What You See on the Chart**

1. **EMA Lines (21, 50, 100)** 📈

2. **Green Background for Strong Bullish Days (Score ≥ 4)** ✅

3. **Histogram Showing Score (Only for 4 and above)** 📊

4. **Buy Signal When Score Crosses Above 4** 💰

### 🔔 **Alerts**

- **An alert is triggered** when the score crosses **above 4**, notifying the user about a bullish trend.

---

## **📌 How to Use This Strategy**

1. **Identify Strong Bullish Trends:** When the score is **4 or above**, it suggests that price momentum is strong.

2. **Enter Trades on Buy Signals:** When the score **crosses above 4**, it could be a good time to buy.

3. **Stay in the Trade While Score is 4+:** The green background confirms a **strong uptrend**.

4. **Exit When Score Drops Below 4:** This suggests weakening momentum.

---

## **🔹 Advantages of This Strategy**

✅ **Simple & Objective** - Uses clear rules for trend confirmation

✅ **Filters Out Noise** - Only highlights strong bullish conditions

✅ **Works on Any Market** - Can be applied to stocks, indices, crypto, etc.

✅ **Customizable** - You can tweak EMAs or score conditions as needed

---

## **🚀 Next Steps**

Would you like me to add **stop-loss conditions**, **sell signals**, or any **extra confirmations like RSI or volume**? 😃

Forex Hammer and Hanging Man StrategyThe strategy is based on two key candlestick chart patterns: Hammer and Hanging Man. These chart patterns are widely used in technical analysis to identify potential reversal points in the market. Their relevance in the Forex market, known for its high liquidity and volatile price movements, is particularly pronounced. Both patterns provide insights into market sentiment and trader psychology, which are critical in currency trading, where short-term volatility plays a significant role.

1. Hammer:

• Typically occurs after a downtrend.

• Signals a potential trend reversal to the upside.

• A Hammer has:

• A small body (close and open are close to each other).

• A long lower shadow, at least twice as long as the body.

• No or a very short upper shadow.

2. Hanging Man:

• Typically occurs after an uptrend.

• Signals a potential reversal to the downside.

• A Hanging Man has:

• A small body, similar to the Hammer.

• A long lower shadow, at least twice as long as the body.

• A small or no upper shadow.

These patterns are a manifestation of market psychology, specifically the tug-of-war between buyers and sellers. The Hammer reflects a situation where sellers tried to push the price down but were overpowered by buyers, while the Hanging Man shows that buyers failed to maintain the upward movement, and sellers could take control.

Relevance of Chart Patterns in Forex

In the Forex market, chart patterns are vital tools because they offer insights into price action and market sentiment. Since Forex trading often involves large volumes of trades, chart patterns like the Hammer and Hanging Man are important for recognizing potential shifts in market momentum. These patterns are a part of technical analysis, which aims to forecast future price movements based on historical data, relying on the psychology of market participants.

Scientific Literature on the Relevance of Candlestick Patterns

1. Behavioral Finance and Candlestick Patterns:

Research on behavioral finance supports the idea that candlestick patterns, such as the Hammer and Hanging Man, are relevant because they reflect shifts in trader psychology and sentiment. According to Lo, Mamaysky, and Wang (2000), patterns like these could be seen as representations of collective investor behavior, influenced by overreaction, optimism, or pessimism, and can often signal reversals in market trends.

2. Statistical Validation of Chart Patterns:

Studies by Brock, Lakonishok, and LeBaron (1992) explored the profitability of technical analysis strategies, including candlestick patterns, and found evidence that certain patterns, such as the Hammer, can have predictive value in financial markets. While their study primarily focused on stock markets, their findings are generally applicable to the Forex market as well.

3. Market Efficiency and Candlestick Patterns:

The efficient market hypothesis (EMH) posits that all available information is reflected in asset prices, but some studies suggest that markets may not always be perfectly efficient, allowing for profitable exploitation of certain chart patterns. For instance, Jegadeesh and Titman (1993) found that momentum strategies, which often rely on price patterns and trends, could generate significant returns, suggesting that patterns like the Hammer or Hanging Man may provide a slight edge, particularly in short-term Forex trading.

Testing the Strategy in Forex Using the Provided Script

The provided script allows traders to test and evaluate the Hammer and Hanging Man patterns in Forex trading by entering positions when these patterns appear and holding the position for a specified number of periods. This strategy can be tested to assess its performance across different currency pairs and timeframes.

1. Testing on Different Timeframes:

• The effectiveness of candlestick patterns can vary across different timeframes, as market dynamics change with the level of detail in each timeframe. Shorter timeframes may provide more frequent signals, but with higher noise, while longer timeframes may produce more reliable signals, but with fewer opportunities. This multi-timeframe analysis could be an area to explore to enhance the strategy’s robustness.

2. Exit Strategies:

• The script incorporates an exit strategy where positions are closed after holding them for a specified number of periods. This is useful for testing how long the reversal patterns typically take to play out and when the optimal exit occurs for maximum profitability. It can also help to adjust the exit logic based on real-time market behavior.

Conclusion

The Hammer and Hanging Man patterns are widely recognized in technical analysis as potential reversal signals, and their application in Forex trading is valuable due to the market’s high volatility and liquidity. This strategy leverages these candlestick patterns to enter and exit trades based on shifts in market sentiment and psychology. Testing and optimization, as offered by the script, can help refine the strategy and improve its effectiveness.

For further refinement, it could be valuable to consider combining candlestick patterns with other technical indicators or using multi-timeframe analysis to confirm patterns and increase the probability of successful trades.

References:

• Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of Technical Analysis: Computational Algorithms, Statistical Inference, and Empirical Implementation. The Journal of Finance, 55(4), 1705-1770.

• Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple Technical Trading Rules and the Stochastic Properties of Stock Returns. The Journal of Finance, 47(5), 1731-1764.

• Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

This provides a theoretical basis for the use of candlestick patterns in trading, supported by academic literature and research on market psychology and efficiency.

Tomas Ratio Strategy with Multi-Timeframe AnalysisHello,

I would like to present my new indicator I have compiled together inspired by Calmar Ratio which is a ratio that measures gains vs losers but with a little twist.

Basically the idea is that if HLC3 is above HLC3 (or previous one) it will count as a gain and it will calculate the percentage of winners in last 720 hourly bars and then apply 168 hour standard deviation to the weekly average daily gains.

The idea is that you're supposed to buy if the thick blue line goes up and not buy if it goes down (signalized by the signal line). I liked that idea a lot, but I wanted to add an option to fire open and close signals. I have also added a logic that it not open more trades in relation the purple line which shows confidence in buying.

As input I recommend only adjusting the amount of points required to fire a signal. Note that the lower amount you put, the more open trades it will allow (and vice versa)

Feel free to remove that limiter if you want to. It works without it as well, this script is meant for inexperienced eye.

I will also publish a indicator script with this limiter removed and alerts added for you to test this strategy if you so choose to.

Also, I have added that the trades will enter only if price is above 720 period EMA

Disclaimer

This strategy is for educational purposes only and should not be considered financial advice. Always backtest thoroughly and adjust parameters based on your trading style and market conditions.

Made in collaboration with ChatGPT.

Precision Trading Strategy: Golden EdgeThe PTS: Golden Edge strategy is designed for scalping Gold (XAU/USD) on lower timeframes, such as the 1-minute chart. It captures high-probability trade setups by aligning with strong trends and momentum, while filtering out low-quality trades during consolidation or low-volatility periods.

The strategy uses a combination of technical indicators to identify optimal entry points:

1. Exponential Moving Averages (EMAs): A fast EMA (3-period) and a slow EMA (33-period) are used to detect short-term trend reversals via crossover signals.

2. Hull Moving Average (HMA): A 66-period HMA acts as a higher-timeframe trend filter to ensure trades align with the overall market direction.

3. Relative Strength Index (RSI): A 12-period RSI identifies momentum. The strategy requires RSI > 55 for long trades and RSI < 45 for short trades, ensuring entries are backed by strong buying or selling pressure.

4. Average True Range (ATR): A 14-period ATR ensures trades occur only during volatile conditions, avoiding choppy or low-movement markets.

By combining these tools, the PTS: Golden Edge strategy creates a precise framework for scalping and offers a systematic approach to capitalize on Gold’s price movements efficiently.

Harmony Signal Flow By ArunThis Pine Script strategy, titled "Harmony Signal Flow By Arun," uses the Relative Strength Index (RSI) indicator to generate buy and sell signals based on custom thresholds. The script incorporates stop-loss and target management and restricts new trades until the previous position closes. Here's a detailed description:

Custom RSI Metric:

The strategy calculates a 5-period RSI based on the closing price, aiming for a more responsive measure of price momentum.

RSI thresholds are defined:

Lower threshold (30): Indicates oversold conditions, triggering a potential buy.

Upper threshold (70): Indicates overbought conditions, prompting a possible sell.

Entry Conditions:

Buy Signal: The strategy initiates a buy order when the RSI crosses above the lower threshold (30), indicating a shift from oversold conditions.

Sell Signal: A sell order is triggered when the RSI crosses below the upper threshold (70), suggesting an overbought reversal.

Only one order (buy or sell) can be active at a time, ensuring that a new trade begins only when there’s no existing position.

Stop-Loss and Target Management:

For each trade, stop-loss and target conditions are applied to manage risk and secure profits.

For Buy Positions:

Stop-loss is set 100 points below the entry price.

Target is set 150 points above the entry price.

For Sell Positions:

Stop-loss is set 100 points above the entry price.

Target is 150 points below the entry price.

The strategy closes the trade when either the stop-loss or target is met, marking the trade as "closed" and allowing a new trade entry.

Trade Sequencing:

A new trade (buy or sell) is only permitted after the previous position hits either its stop-loss or target, preventing overlapping trades and ensuring clear trade sequences.

This sequential approach enhances risk management by ensuring only one active position at any time.

End-of-Day Closure:

All open positions are closed automatically at 3:25 PM (Indian market time) to avoid overnight exposure, ensuring the strategy remains strictly intraday.

The flag for trade entry is reset at the end of each day, enabling fresh trades the next day.

Chart Indicators:

The script plots buy and sell signals directly on the chart with visible labels.

It also displays the custom RSI metric with horizontal lines for the lower and upper thresholds, providing visual cues for entry and exit points.

Summary

This strategy is a momentum-based intraday trading approach that uses the RSI for identifying potential reversals and manages trades through predefined stop-loss and target levels. By enforcing trade sequencing and closing positions at the end of the trading day, it prioritizes risk management and seeks to capitalize on short-term trends while avoiding overnight market risks.

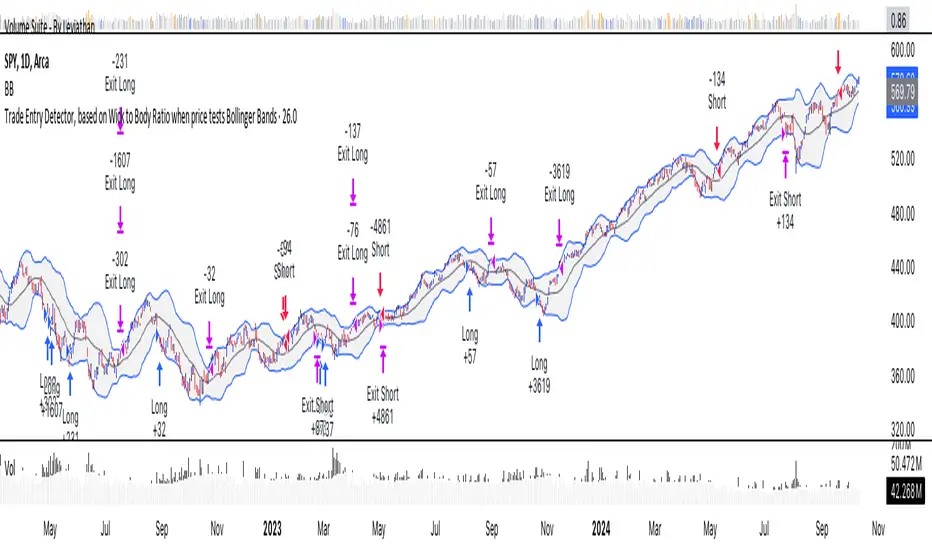

Trade Entry Detector, Wick to Body Ratio Trade Entry Detector: Wick-to-Body Ratio Strategy with Bollinger Bands

Overview

The Trade Entry Detector is a custom strategy for TradingView that leverages the Bollinger Bands and a unique wick-to-body ratio approach to capture precise entry opportunities. This indicator is designed for traders who want to pinpoint high-probability reversal points when price interacts with Bollinger Bands, all while offering flexible entry fill options.

The strategy performs primary analysis on the daily time frame, regardless of your current chart setting, allowing you to view daily Bollinger Band levels and entry signals even on lower time frames. This approach is suitable for swing traders and short-term traders looking to align intraday moves with higher time frame signals.

How the Strategy Works

1. Bollinger Band Analysis on the Daily Time Frame

Bollinger Bands are calculated using a 20-period simple moving average (SMA) and a standard deviation multiplier (default is 2). These bands dynamically expand and contract based on market volatility, making them ideal for identifying overbought and oversold conditions:

* Upper Band: Indicates potential overbought levels.

* Lower Band: Indicates potential oversold levels.

2. Wick-to-Body Ratio Condition

This strategy places significant emphasis on candle wicks relative to the candle body. Here’s why:

* A large upper wick relative to the body signals potential selling pressure after testing the upper Bollinger Band.

* A large lower wick relative to the body indicates buying support after testing the lower Bollinger Band.

* Ratio Threshold: You can set a minimum wick-to-body ratio (default is 1.0), meaning that the wick must be at least equal in size to the body. This ensures only candles with significant reversals are considered for entry.

3. Flexible Entry Timing

To adapt to various trading styles, the indicator allows you to choose the entry fill timing:

* Daily Close: Enter at the close of the daily candle.

* Daily Open: Enter at the open of the following daily candle.

* HOD (High of Day): Set entry at the daily high, for those who want confirmation of upward momentum.

* LOD (Low of Day): Set entry at the daily low, ideal for confirming downward movement.

4. Position Sizing and Risk Management

The strategy calculates position size based on a fixed risk percentage of your account balance (default is 1%). This approach dynamically adjusts position sizes based on stop-loss distance:

* Stop Loss: Placed at the nearest swing high (for shorts) or swing low (for longs).

* Take Profit: Exits are triggered when the price reaches the opposite Bollinger Band.

5. Order Expiration

Each pending order (long or short) expires after two days if unfilled, allowing for new setups on subsequent candles if conditions are met again.

Using the Trade Entry Detector

Step-by-Step Guide

1. Set the Primary Time Frame

The core calculations run on the daily time frame, but the strategy can be applied to intraday charts (e.g., 65-minute or 15-minute) for deeper insights.

2. Adjust Bollinger Band Settings

* Length: Default is 20, which determines the period for calculating the moving average.

* Standard Deviation Multiplier: Default is 2.0, which sets the width of the bands. Adjusting this can help you capture broader or tighter volatility ranges.

3. Define the Wick-to-Body Ratio

Set the minimum ratio between wick and body (default 1.0). Higher values filter out candles with less wick-to-body contrast, focusing on stronger rejection moves.

4. Choose Entry Fill Timing

Select your preferred fill condition:

* Daily Close: Confirms the trade at the end of the daily session.

* Daily Open: Executes the entry at the open of the next day.

* HOD/LOD: Uses the daily high or low as an additional confirmation for upward or downward moves.

5. Position Sizing and Risk Management

* Set your account balance and risk percentage. The strategy automatically calculates position sizes based on the stop distance to manage risk efficiently.

* Stop Loss and Take Profit points are automatically set based on swing highs/lows and opposing Bollinger Bands, respectively.

Practical Example

Let’s say SPY (S&P 500 ETF) tests the lower Bollinger Band on the daily time frame, with a lower wick that is twice the size of the body (meeting the 1.0 ratio threshold). Here’s how the strategy might proceed:

1. Signal: The lower wick on SPY suggests buying interest at the lower Bollinger Band.

2. Entry Fill Timing: If you’ve selected "Daily Open," the entry order will be placed at the next day's open price.

3. Stop Loss: Positioned at the nearest daily swing low to minimize risk.

4. Take Profit: If SPY price moves up and reaches the upper Bollinger Band, the position is automatically closed.

Indicator Features and Benefits

* Multi-Time Frame Compatibility: Perform daily analysis while tracking signals on any intraday chart.

* Automatic Position Sizing: Tailor risk per trade based on account balance and desired risk percentage.

* Flexible Entry Options: Choose from close, open, HOD, or LOD for optimal timing.

* Effective Trend Reversal Identification: Uses wick-to-body ratio and Bollinger Band interaction to pinpoint potential reversals.

* Dynamic Visualization: Bollinger Bands are displayed on your chosen time frame, allowing seamless intraday tracking.

Summary

The Trade Entry Detector provides a unique, data-driven way to spot reversal points with customizable entry options. By combining Bollinger Bands with wick-to-body ratio conditions, it identifies potential trade setups where price has tested extremes and shown reversal signals. With its flexible entry timing, risk management features, and multi-time frame compatibility, this indicator is ideal for traders looking to blend daily market context with shorter-term execution.

Tips for Usage:

* For swing trading, consider the Daily Open or Close entry options.

* For momentum entries, HOD or LOD may offer better alignment with the direction of the wick.

* Backtest on different assets to find optimal Bollinger Band and wick-to-body settings for your market.

Use this indicator to enhance your understanding of price behavior at key levels and improve the precision of your entry points. Happy trading!

Trend Signals with TP & SL [UAlgo] StrategyThe "Trend Signals with TP & SL Strategy" is a trading strategy designed to capture trend continuation signals while incorporating sophisticated risk management techniques. This strategy is tailored for traders who wish to capitalize on trending market conditions with precise entry and exit points, automatically calculating Take Profit (TP) and Stop Loss (SL) levels based on either Average True Range (ATR) or percentage values. The strategy aims to enhance trade management by preventing multiple simultaneous positions and dynamically adapting to changing market conditions.

This strategy is highly configurable, allowing traders to adjust sensitivity, the ATR calculation method, and the cloud moving average length. Additionally, the strategy can display buy and sell signals directly on the chart, along with visual representation of entry points, stop losses, and take profits. It also features a cloud-based trend analysis using a MACD-driven color fill that indicates the strength and direction of the trend.

🔶 Key Features

Configurable Trend Continuation Signals:

Source Selection: The strategy uses the midpoint of the high-low range as the default source, but it is adjustable.

Sensitivity: The sensitivity of the trend signals can be adjusted using a multiplier, ranging from 0.5 to 5.

ATR Calculation: The strategy allows users to choose between two ATR calculation methods for better adaptability to different market conditions.

Cloud Moving Average: Traders can adjust the cloud moving average length, which is used in conjunction with MACD to provide a visual trend indication.

Take Profit & Stop Loss Management:

ATR-Based or Percent-Based: The strategy offers flexibility in setting TP and SL levels, allowing traders to choose between ATR-based multipliers or fixed percentage values.

Dynamic Adjustment: TP and SL levels are dynamically adjusted according to the selected method, ensuring trades are managed based on real-time market conditions.

Prevention of Multiple Positions:

Single Position Control: To reduce risk and enhance strategy reliability, the strategy includes an option to prevent multiple positions from being opened simultaneously.

Visual Trade Indicators:

Buy/Sell Signals: Clearly displays buy and sell signals on the chart for easy interpretation.

Entry, SL, and TP Lines: Draws lines for entry price, stop loss, and take profit directly on the chart, helping traders to monitor trades visually.

Trend Cloud: A color-filled cloud based on MACD and the cloud moving average provides a visual cue of the trend’s direction and strength.

Performance Summary Table:

In-Chart Statistics: A table in the top right of the chart displays key performance metrics, including total trades, wins, losses, and win rate percentage, offering a quick overview of the strategy’s effectiveness.

🔶 Interpreting the Indicator

Trend Signals: The strategy identifies trend continuation signals based on price action relative to an ATR-based threshold. A buy signal is generated when the price crosses above a key level, indicating an uptrend. Conversely, a sell signal occurs when the price crosses below a level, signaling a downtrend.

Cloud Visualization: The cloud, derived from MACD and moving averages, changes color to reflect the current trend. A positive cloud in aqua suggests an uptrend, while a red cloud indicates a downtrend. The transparency of the cloud offers further nuance, with more solid colors denoting stronger trends.

Entry and Exit Management: Once a trend signal is generated, the strategy automatically sets TP and SL levels based on your chosen method (ATR or percentage). The stop loss and take profit lines will appear on the chart, showing where the strategy will exit the trade. If the price reaches either the SL or TP, the trade is closed, and the respective line is deleted from the chart.

Performance Metrics: The strategy’s performance is tracked in real-time with an in-chart table. This table provides essential information about the number of trades executed, the win/loss ratio, and the overall win rate. This information helps traders assess the strategy's effectiveness and make necessary adjustments.

This strategy is designed for those who seek to engage with trending markets, offering robust tools for entry, exit, and overall trade management. By understanding and leveraging these features, traders can potentially improve their trading outcomes and risk management.

🔷 Related Script

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

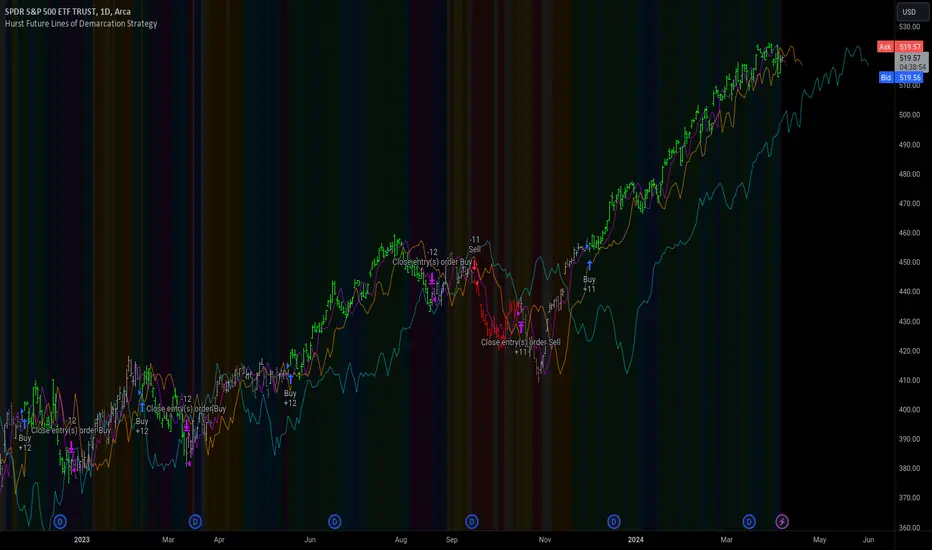

Hurst Future Lines of Demarcation StrategyJ. M. Hurst introduced a concept in technical analysis known as the Future Line of Demarcation (FLD), which serves as a forward-looking tool by incorporating a simple yet profound line into future projections on a financial chart. Specifically, the FLD is constructed by offsetting the price half a cycle ahead into the future on the time axis, relative to the Hurst Cycle of interest. For instance, in the context of a 40 Day Cycle, the FLD would be represented by shifting the current price data 20 days forward on the chart, offering an idea of future price movement anticipations.

The utility of FLDs extends into three critical areas of insight, which form the backbone of the FLD Trading Strategy:

A price crossing the FLD signifies the confirmation of either a peak or trough formation, indicating pivotal moments in price action.

Such crossings also help determine precise price targets for the upcoming peak or trough, aligned with the cycle of examination.

Additionally, the occurrence of a peak in the FLD itself signals a probable zone where the price might experience a trough, helping to anticipate of future price movements.

These insights by Hurst in his "Cycles Trading Course" during the 1970s, are instrumental for traders aiming to determine entry and exit points, and to forecast potential price movements within the market.

To use the FLD Trading Strategy, for example when focusing on the 40 Day Cycle, a trader should primarily concentrate on the interplay between three Hurst Cycles:

The 20 Day FLD (Signal) - Half the length of the Trade Cycle

The 40 Day FLD (Trade) - The Cycle you want to trade

The 80 Day FLD (Trend) - Twice the length of the Trade Cycle

Traders can gauge trend or consolidation by watching for two critical patterns:

Cascading patterns, characterized by several FLDs running parallel with a consistent separation, typically emerge during pronounced market trends, indicating strong directional momentum.

Consolidation patterns, on the other hand, occur when multiple FLDs intersect and navigate within the same price bandwidth, often reversing direction to traverse this range multiple times. This tangled scenario results in the formation of Pause Zones, areas where price momentum is likely to temporarily stall or where the emergence of a significant trend might be delayed.

This simple FLD indicator provides 3 FLDs with optional source input and smoothing, A-through-H FLD interaction background, adjustable “Close the Trade” triggers, and a simple strategy for backtesting it all.

The A-through-H FLD interactions are a framework designed to classify the different types of price movements as they intersect with or diverge from the Future Line of Demarcation (FLD). Each interaction (designated A through H by color) represents a specific phase or characteristic within the cycle, and understanding these can help traders anticipate future price movements and make informed decisions.

The adjustable “Close the Trade” triggers are for setting the crossover/under that determines the trade exits. The options include: Price, Signal FLD, Trade FLD, or Trend FLD. For example, a trader may want to exit trades only when price finally crosses the Trade FLD line.

Shoutouts & Credits for all the raw code, helpful information, ideas & collaboration, conversations together, introductions, indicator feedback, and genuine/selfless help:

🏆 @TerryPascoe

🏅 @Hpotter

👏 @parisboy

TrippleMACDCryptocurrency Scalping Strategy for 1m Timeframe

Introduction:

Welcome to our cutting-edge cryptocurrency scalping strategy tailored specifically for the 1-minute timeframe. By combining three MACD indicators with different parameters and averaging them, along with applying RSI, we've developed a highly effective strategy for maximizing profits in the cryptocurrency market. This strategy is designed for automated trading through our bot, which executes trades using hooks. All trades are calculated for long positions only, ensuring optimal performance in a fast-paced market.

Key Components:

MACD (Moving Average Convergence Divergence):

We've utilized three MACD indicators with varying parameters to capture different aspects of market momentum.

Averaging these MACD indicators helps smooth out noise and provides a more reliable signal for trading decisions.

RSI (Relative Strength Index):

RSI serves as a complementary indicator, providing insights into the strength of bullish trends.

By incorporating RSI, we enhance the accuracy of our entry and exit points, ensuring timely execution of trades.

Strategy Overview:

Long Position Entries:

Initiate long positions when all three MACD indicators signal bullish momentum and the RSI confirms bullish strength.

This combination of indicators increases the probability of successful trades, allowing us to capitalize on uptrends effectively.

Utilizing Linear Regression:

Linear regression is employed to identify consolidation phases in the market.

Recognizing consolidation periods helps us avoid trading during choppy price action, ensuring optimal performance.

Suitability for Grid Trading Bots:

Our strategy is well-suited for grid trading bots due to frequent price fluctuations and opportunities for grid activation.

The strategy's design accounts for price breakthroughs, which are advantageous for grid trading strategies.

Benefits of the Strategy:

Consistent Performance Across Cryptocurrencies:

Through rigorous testing on various cryptocurrency futures contracts, our strategy has demonstrated favorable results across different coins.

Its adaptability makes it a versatile tool for traders seeking consistent profits in the cryptocurrency market.

Integration of Advanced Techniques:

By integrating multiple indicators and employing linear regression, our strategy leverages advanced techniques to enhance trading performance.

This strategic approach ensures a comprehensive analysis of market conditions, leading to well-informed trading decisions.

Conclusion:

Our cryptocurrency scalping strategy offers a sophisticated yet user-friendly approach to trading in the fast-paced environment of the 1-minute timeframe. With its emphasis on automation, accuracy, and adaptability, our strategy empowers traders to navigate the complexities of the cryptocurrency market with confidence. Whether you're a seasoned trader or a novice investor, our strategy provides a reliable framework for achieving consistent profits and maximizing returns on your investment.

Bollinger Bands, RSI, and MA StrategyThe "Bollinger Bands, RSI and MA Strategy" is a trend-following strategy that combines the Bollinger Bands indicator, the Relative Strength Index (RSI), and a moving average (MA). It aims to identify potential entry and exit points in the market based on price volatility, momentum, and trend.

The strategy uses two Bollinger Bands with different standard deviations to create price channels. The default settings for the Bollinger Bands are a length of 20 periods and a standard deviation of 2.0. The upper and lower bands of the Bollinger Bands serve as dynamic resistance and support levels, respectively.

The RSI indicator is employed to gauge the strength of price momentum.

The strategy also incorporates a 50-period moving average (MA) to help identify the overall trend direction. When the price is above the MA, it suggests an uptrend, and when the price is below the MA, it suggests a downtrend.

The entry conditions for long trades are when the RSI is above the overbought level and there is no contraction in the Bollinger Bands. For short trades, the entry conditions are when the RSI is below the oversold level and there is no contraction in the Bollinger Bands.

The exit conditions for long trades are when the RSI drops below the overbought level or when the price closes below the 50-period MA.

For short trades, the exit conditions are when the RSI goes above the oversold level or when the price closes above the 50-period MA.

The strategy generates alerts for potential long and short entry signals, as well as for exit signals when the specified conditions are met. These alerts can be used to receive notifications or take further actions, such as placing trades manually or using automated trading systems.

It is important to note that this strategy serves as a starting point and should be thoroughly backtested and validated with historical data before applying it to live trading. Additionally, it is recommended to consider risk management techniques, including setting appropriate stop-loss and take-profit levels, to effectively manage trades.

FFT Strategy Bi-Directional Stop/Profit/Trailing + VMA + AroonThis strategy uses the Fast Fourier Transform inspired from the source code of @tbiktag for the Fast Fourier Transform & @lazybear for the VMA filter.

If you are not familiar with the Fast Fourier transform it is a variation of the Discrete Fourier Transform. Veritasium on youtube has a great video on it with a follow up recommendation from 3brown1blue. In short it will extract all the frequencies from a set of data. @tbiktag laid the groundwork for creating the indicator which will allow you to isolate only those signals which are the most relevant and remove the noise. I recommend having @tbiktag's FFT Transform indicator side by side with this to understand what my variation is doing by setting similar settings .

Using this idea, you can then optimize a strategy to the frequencies that are best. The main entry signal is when the FFT Signal crosses above or below the 0 line .

Included with this strategy is the ability to optionally bi-directionally set:

Stop Loss

Trailing Stop Loss

Take Profit

Trailing Take Profit

Entries are optionally further filtered by use of the VMA using the algorithm from LazyBear which allows you to adjust a variable moving average with 3 market trend detections. Green represents upwards momentum; Blue sideways trading and Red downwards momentum. The idea being to filter out buy or sell entries unless the market is moving in that direction, and this makes a big difference as you can see for yourself when you turn it off or on. Turning it off will change the color of the FFT signal to orange instead of the green, blue, red colors .

I have added 2 custom stop loss types as well for experimentation:

1. VMA Filter stop loss to exit the trade if the VMA detects a market trend direction change matching the rules you have set. I have set this to off by default, but it is there so you can see what affect it may have on other tickers. It can increase the profit factor but usually at a cost of net profit.

2. The Aroon Filter stop loss with different lengths for the short or long direction. For the Aroon strategy (which is a trend change detector) it is considered bullish if the upper line (green in my code) is above 70 and the lower line (red in my code) is below 30 and the opposite for the bearish case. With this in mind, I have set it to filter by default only the extreme ends (99 and 1) to increase profit factor and net profit but I encourage you to try different settings and see how it affects things. Turning this off yields much higher net profit but at the cost of the profit factor and drawdown . To disable this just uncheck the 'Use Aroon Filter Long' (or short) and it will also hide the aroon graphics and crosses on the plot.

I will be adding more features in an attempt to lower the drawdown on this strategy but I hope you enjoy what I have so far!

Volume and Moving average,will this model working in real-trade?i`ve recently made this script through few month,understand me if there are some incorrect grammar or something.

basically this script is based on moving average strategy and the bollinger bands

if the buy volume is bigger than sell volume,also buy volume is bigger then daily average volume than it`s defined current market is bullish and entered(of course there is some other conditions)

the exit condition is find the highest price after entered,keep refresh the highest price through time and then,if the current price is ?%lower then highest price,it will closed the position.

my question is this : 1 this model will working in real-trade?

2 why the winning rate is 100%?

- i`ve coded if the position margin over -10%,close the position this code isn`t work? or the other profit line is prevent that happened?

8 Day Extended Runs Inspired by Linda Bradford Raschke.

Strategy suited to the US T-note (ZN1!) with a t-test of 4.06.

The 5 day SMA is vital to Linda’s trend identification system. She’s done extensive testing and research using this indicator and has built models based on it. Linda used the 5 day SMA to determine that large outlier price moves happen in the direction of the trend in each market about 9-10 times per year. The powerful part about that number is that when the trend does persist, it can go on a long run, making this a trade with a high expected value.

Note: the current exit criteria is sell 10 days after entry, users should experiment with different stop placements.

MA Strength StrategyThis is based on Aligned Moving Average Index published earlier:

But, instead of scoring trend based on how many moving averages are aligned, we are considering upside score. Higher scores are assigned for slower moving averages and lower scores for faster moving averages to give more stress to long term trend.

Buy/Sell conditions are based on moving average crossover on the upside score sum of Loopback days.

This is a very rough idea which seems to have been working ok on long only trades. Can be further improved.

EXODUS EXODUS by (DAFE) Trading Systems

EXODUS is a sophisticated trading algorithm built by Dskyz (DAFE) Trading Systems for competitive and competition purposes, designed to identify high-probability trades with robust risk management. this strategy leverages a multi-signal voting system, combining three core components—SPR, VWMO, and VEI—alongside ADX, choppiness filters, and ATR-based volatility gates to ensure trades are taken only in favorable market conditions. the algo uses a take-profit to stop-loss ratio, dynamic position sizing, and a strict voting mechanism requiring all signals to align before entering a trade.

EXODUS was not overfitted for any specific symbol. instead, it uses a generic tuned setting, making it versatile across various markets. while it can trade futures, it’s not currently set up for it but has the potential to do more with further development. visuals are intentionally minimal due to its competition focus, prioritizing performance over aesthetics. a more visually stunning version may be released in the future with enhanced graphics.

The Unique Core Components Developed for EXODUS

SPR (Session Price Recalibration)

SPR measures momentum during regular trading hours (RTH, 0930-1600, America/New_York) to catch session-specific trends.

spr_lookback = input.int(15, "SPR Lookback") this sets how many bars back SPR looks to calculate momentum (default 15 bars). it compares the current session’s price-volume score to the score 15 bars ago to gauge momentum strength.

how it works: a longer lookback smooths out the signal, focusing on bigger trends. a shorter one makes SPR more sensitive to recent moves.

how to adjust: on a 1-hour chart, 15 bars is 15 hours (about 2 trading days). if you’re on a shorter timeframe like 5 minutes, 15 bars is just 75 minutes, so you might want to increase it to 50 or 100 to capture more meaningful trends. if you’re trading a choppy stock, a shorter lookback (like 5) can help catch quick moves, but it might give more false signals.

spr_threshold = input.float (0.7, "SPR Threshold")

this is the cutoff for SPR to vote for a trade (default 0.7). if SPR’s normalized value is above 0.7, it votes for a long; below -0.7, it votes for a short.

how it works: SPR normalizes its momentum score by ATR, so this threshold ensures only strong moves count. a higher threshold means fewer trades but higher conviction.

how to adjust: if you’re getting too few trades, lower it to 0.5 to let more signals through. if you’re seeing too many false entries, raise it to 1.0 for stricter filtering. test on your chart to find a balance.

spr_atr_length = input.int(21, "SPR ATR Length") this sets the ATR period (default 21 bars) used to normalize SPR’s momentum score. ATR measures volatility, so this makes SPR’s signal relative to market conditions.

how it works: a longer ATR period (like 21) smooths out volatility, making SPR less jumpy. a shorter one makes it more reactive.

how to adjust: if you’re trading a volatile stock like TSLA, a longer period (30 or 50) can help avoid noise. for a calmer stock, try 10 to make SPR more responsive. match this to your timeframe—shorter timeframes might need a shorter ATR.

rth_session = input.session("0930-1600","SPR: RTH Sess.") rth_timezone = "America/New_York" this defines the session SPR uses (0930-1600, New York time). SPR only calculates momentum during these hours to focus on RTH activity.

how it works: it ignores pre-market or after-hours noise, ensuring SPR captures the main market action.

how to adjust: if you trade a different session (like London hours, 0300-1200 EST), change the session to match. you can also adjust the timezone if you’re in a different region, like "Europe/London". just make sure your chart’s timezone aligns with this setting.

VWMO (Volume-Weighted Momentum Oscillator)

VWMO measures momentum weighted by volume to spot sustained, high-conviction moves.

vwmo_momlen = input.int(21, "VWMO Momentum Length") this sets how many bars back VWMO looks to calculate price momentum (default 21 bars). it takes the price change (close minus close 21 bars ago).

how it works: a longer period captures bigger trends, while a shorter one reacts to recent swings.

how to adjust: on a daily chart, 21 bars is about a month—good for trend trading. on a 5-minute chart, it’s just 105 minutes, so you might bump it to 50 or 100 for more meaningful moves. if you want faster signals, drop it to 10, but expect more noise.

vwmo_volback = input.int(30, "VWMO Volume Lookback") this sets the period for calculating average volume (default 30 bars). VWMO weights momentum by volume divided by this average.

how it works: it compares current volume to the average to see if a move has strong participation. a longer lookback smooths the average, while a shorter one makes it more sensitive.

how to adjust: for stocks with spiky volume (like NVDA on earnings), a longer lookback (50 or 100) avoids overreacting to one-off spikes. for steady volume stocks, try 20. match this to your timeframe—shorter timeframes might need a shorter lookback.

vwmo_smooth = input.int(9, "VWMO Smoothing")

this sets the SMA period to smooth VWMO’s raw momentum (default 9 bars).

how it works: smoothing reduces noise in the signal, making VWMO more reliable for voting. a longer smoothing period cuts more noise but adds lag.

how to adjust: if VWMO is too jumpy (lots of false votes), increase to 15. if it’s too slow and missing trades, drop to 5. test on your chart to see what keeps the signal clean but responsive.

vwmo_threshold = input.float(10, "VWMO Threshold") this is the cutoff for VWMO to vote for a trade (default 10). above 10, it votes for a long; below -10, a short.

how it works: it ensures only strong momentum signals count. a higher threshold means fewer but stronger trades.

how to adjust: if you want more trades, lower it to 5. if you’re getting too many weak signals, raise it to 15. this depends on your market—volatile stocks might need a higher threshold to filter noise.

VEI (Velocity Efficiency Index)

VEI measures market efficiency and velocity to filter out choppy moves and focus on strong trends.

vei_eflen = input.int(14, "VEI Efficiency Smoothing") this sets the EMA period for smoothing VEI’s efficiency calc (bar range / volume, default 14 bars).

how it works: efficiency is how much price moves per unit of volume. smoothing it with an EMA reduces noise, focusing on consistent efficiency. a longer period smooths more but adds lag.

how to adjust: for choppy markets, increase to 20 to filter out noise. for faster markets, drop to 10 for quicker signals. this should match your timeframe—shorter timeframes might need a shorter period.

vei_momlen = input.int(8, "VEI Momentum Length") this sets how many bars back VEI looks to calculate momentum in efficiency (default 8 bars).

how it works: it measures the change in smoothed efficiency over 8 bars, then adjusts for inertia (volume-to-range). a longer period captures bigger shifts, while a shorter one reacts faster.

how to adjust: if VEI is missing quick reversals, drop to 5. if it’s too noisy, raise to 12. test on your chart to see what catches the right moves without too many false signals.

vei_threshold = input.float(4.5, "VEI Threshold") this is the cutoff for VEI to vote for a trade (default 4.5). above 4.5, it votes for a long; below -4.5, a short.

how it works: it ensures only strong, efficient moves count. a higher threshold means fewer trades but higher quality.

how to adjust: if you’re not getting enough trades, lower to 3. if you’re seeing too many false entries, raise to 6. this depends on your market—fast stocks like NQ1 might need a lower threshold.

Features

Multi-Signal Voting: requires all three signals (SPR, VWMO, VEI) to align for a trade, ensuring high-probability setups.

Risk Management: uses ATR-based stops (2.1x) and take-profits (4.1x), with dynamic position sizing based on a risk percentage (default 0.4%).

Market Filters: ADX (default 27) ensures trending conditions, choppiness index (default 54.5) avoids sideways markets, and ATR expansion (default 1.12) confirms volatility.

Dashboard: provides real-time stats like SPR, VWMO, VEI values, net P/L, win rate, and streak, with a clean, functional design.

Visuals

EXODUS prioritizes performance over visuals, as it was built for competitive and competition purposes. entry/exit signals are marked with simple labels and shapes, and a basic heatmap highlights market regimes. a more visually stunning update may be released later, with enhanced graphics and overlays.

Usage

EXODUS is designed for stocks and ETFs but can be adapted for futures with adjustments. it performs best in trending markets with sufficient volatility, as confirmed by its generic tuning across symbols like TSLA, AMD, NVDA, and NQ1. adjust inputs like SPR threshold, VWMO smoothing, or VEI momentum length to suit specific assets or timeframes.

Setting I used: (Again, these are a generic setting, each security needs to be fine tuned)

SPR LB = 19 SPR TH = 0.5 SPR ATR L= 21 SPR RTH Sess: 9:30 – 16:00

VWMO L = 21 VWMO LB = 18 VWMO S = 6 VWMO T = 8

VEI ES = 14 VEI ML = 21 VEI T = 4

R % = 0.4

ATR L = 21 ATR M (S) =1.1 TP Multi = 2.1 ATR min mult = 0.8 ATR Expansion = 1.02

ADX L = 21 Min ADX = 25

Choppiness Index = 14 Chop. Max T = 55.5

Backtesting: TSLA

Frame: Jan 02, 2018, 08:00 — May 01, 2025, 09:00

Slippage: 3

Commission .01

Disclaimer

this strategy is for educational purposes. past performance is not indicative of future results. trading involves significant risk, and you should only trade with capital you can afford to lose. always backtest and validate any strategy before using it in live markets.

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

About the Author

Dskyz (DAFE) Trading Systems is dedicated to building high-performance trading algorithms. EXODUS is a product of rigorous research and development, aimed at delivering consistent, and data-driven trading solutions.

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Ichimoku by FarmerBTCLegal Disclaimer

This strategy, "Ichimoku by FarmerBTC," is provided for educational and informational purposes only. It does not constitute financial advice and should not be relied upon as such. Trading and investing involve substantial risk, including the potential for losing more than your initial investment. Past performance is not indicative of future results. Always consult with a qualified financial advisor before making trading or investment decisions. The author of this strategy is not responsible for any financial losses incurred through its use.

Overview

The "Ichimoku by FarmerBTC" strategy is a trend-following system built on the Ichimoku Cloud indicator, enhanced with volume analysis and a high-timeframe Simple Moving Average (HTF SMA) condition. It is designed to identify long-only trade opportunities and performs optimally on higher timeframes, such as the daily chart or above.

Core Components

1. Ichimoku Cloud

The Ichimoku Cloud is a comprehensive trend-following indicator that helps identify the overall market direction and momentum. It consists of:

Conversion Line (Tenkan-Sen): Measures short-term momentum.

Base Line (Kijun-Sen): Filters medium-term trends.

Leading Span A: The average of the Conversion and Base Lines, forming one cloud boundary.

Leading Span B: The midpoint of the highest high and lowest low over a longer period, forming the other cloud boundary.

Key Ichimoku Rules Applied:

The strategy identifies bullish trends when:

The price is above the cloud.

The cloud is bullish (Leading Span A > Leading Span B).

2. High-Timeframe Simple Moving Average (HTF SMA)

This condition ensures alignment with the broader trend:

Default SMA Length: 13 periods.

Default Timeframe: 1 day.

HTF SMA Rule:

Trades are allowed only when the price is above the HTF SMA, ensuring alignment with the larger trend.

3. Volume Analysis

The strategy uses volume to validate trade setups:

Volume MA: A 20-period moving average of volume is calculated.

Trades are allowed only when the current volume is at least 1.5x the Volume MA, indicating strong market participation.

Entry and Exit Rules

Entry Condition (Long Only):

Price above the Ichimoku Cloud: Confirms a bullish trend.

Bullish Cloud: Leading Span A > Leading Span B indicates upward momentum.

Price above the HTF SMA: Ensures alignment with the broader trend.

Volume exceeds threshold: Confirms strong market participation.

Exit Condition:

The strategy exits the position when the price moves below the Ichimoku Cloud, signaling a potential trend reversal.

Best Timeframes

This strategy is optimized for daily (1D) or higher timeframes (e.g., weekly 1W). Using it on lower timeframes may produce false signals due to increased noise in price and volume data.

Default Settings

Ichimoku Settings:

Conversion Line Period: 10

Base Line Period: 30

Lagging Span Period: 53

Displacement: 26

HTF SMA Settings:

SMA Length: 13

Timeframe: 1 Day

Volume Settings:

Volume MA Length: 20

Volume Multiplier: 1.5x

Visualization

Ichimoku Cloud:

Dynamic cloud coloring (green for bullish, red for bearish) helps identify the current trend.

HTF SMA:

A purple line overlays the chart, providing a clear representation of the high-timeframe trend.

Volume Panel:

An optional panel displays volume (blue histogram) and the Volume Moving Average (orange line) to analyze market participation.

Advantages of This Strategy

High Accuracy on Higher Timeframes:

Filtering trades using the Ichimoku Cloud, HTF SMA, and volume ensures robust trend alignment, reducing false signals.

Volume Confirmation:

Incorporates volume as a validation metric to enter trades only during strong market participation.

Easy Customization:

Parameters like Ichimoku periods, SMA length, timeframe, and volume thresholds can be adjusted to suit different assets or trading styles.

Limitations

Not Suitable for Low Timeframes:

Lower timeframes can produce excessive noise, leading to false signals.

Long-Only:

The strategy is designed only for bullish markets and does not support short trades.

Lagging Nature of Indicators:

Both the Ichimoku Cloud and SMA are lagging indicators, meaning they react to past price movements.

Conclusion

The "Ichimoku by FarmerBTC" strategy is an excellent tool for trend-following on daily or higher timeframes. Its combination of Ichimoku Cloud, high-timeframe SMA, and volume ensures a robust framework for identifying high-probability long trades in trending markets. However, users are advised to test the strategy thoroughly and manage their risk appropriately. Always consult with a financial professional before making trading decisions.

Ultimate Oscillator Trading StrategyThe Ultimate Oscillator Trading Strategy implemented in Pine Script™ is based on the Ultimate Oscillator (UO), a momentum indicator developed by Larry Williams in 1976. The UO is designed to measure price momentum over multiple timeframes, providing a more comprehensive view of market conditions by considering short-term, medium-term, and long-term trends simultaneously. This strategy applies the UO as a mean-reversion tool, seeking to capitalize on temporary deviations from the mean price level in the asset’s movement (Williams, 1976).

Strategy Overview:

Calculation of the Ultimate Oscillator (UO):

The UO combines price action over three different periods (short-term, medium-term, and long-term) to generate a weighted momentum measure. The default settings used in this strategy are:

Short-term: 6 periods (adjustable between 2 and 10).

Medium-term: 14 periods (adjustable between 6 and 14).

Long-term: 20 periods (adjustable between 10 and 20).

The UO is calculated as a weighted average of buying pressure and true range across these periods. The weights are designed to give more emphasis to short-term momentum, reflecting the short-term mean-reversion behavior observed in financial markets (Murphy, 1999).

Entry Conditions:

A long position is opened when the UO value falls below 30, indicating that the asset is potentially oversold. The value of 30 is a common threshold that suggests the price may have deviated significantly from its mean and could be due for a reversal, consistent with mean-reversion theory (Jegadeesh & Titman, 1993).

Exit Conditions:

The long position is closed when the current close price exceeds the previous day’s high. This rule captures the reversal and price recovery, providing a defined point to take profits.

The use of previous highs as exit points aligns with breakout and momentum strategies, as it indicates sufficient strength for a price recovery (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages two well-established phenomena in financial markets: momentum and mean-reversion. Momentum, identified in earlier studies like those by Jegadeesh and Titman (1993), describes the tendency of assets to continue in their direction of movement over short periods. Mean-reversion, as discussed by Poterba and Summers (1988), indicates that asset prices tend to revert to their mean over time after short-term deviations. This dual approach aims to buy assets when they are temporarily oversold and capitalize on their return to the mean.

Multi-timeframe Analysis:

The UO’s incorporation of multiple timeframes (short, medium, and long) provides a holistic view of momentum, unlike single-period oscillators such as the RSI. By combining data across different timeframes, the UO offers a more robust signal and reduces the risk of false entries often associated with single-period momentum indicators (Murphy, 1999).

Trading and Market Efficiency:

Studies in behavioral finance, such as those by Shiller (2003), show that short-term inefficiencies and behavioral biases can lead to overreactions in the market, resulting in price deviations. This strategy seeks to exploit these temporary inefficiencies, using the UO as a signal to identify potential entry points when the market sentiment may have overly pushed the price away from its average.

Strategy Performance:

Backtests of this strategy show promising results, with profit factors exceeding 2.5 when the default settings are optimized. These results are consistent with other studies on short-term trading strategies that capitalize on mean-reversion patterns (Jegadeesh & Titman, 1993). The use of a dynamic, multi-period indicator like the UO enhances the strategy’s adaptability, making it effective across different market conditions and timeframes.

Conclusion:

The Ultimate Oscillator Trading Strategy effectively combines momentum and mean-reversion principles to trade on temporary market inefficiencies. By utilizing multiple periods in its calculation, the UO provides a more reliable and comprehensive measure of momentum, reducing the likelihood of false signals and increasing the profitability of trades. This aligns with modern financial research, showing that strategies based on mean-reversion and multi-timeframe analysis can be effective in capturing short-term price movements.

References:

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Williams, L. (1976). Ultimate Oscillator. Market research and technical trading analysis.

Triple ThreatThis indicator provides buy and sell signals for Bitcoin based on confluence from well-known momentum, volatility, and trend indicators. It has successfully captured the major directional trends on Bitcoin's daily chart since 2018, and the settings are currently optimized for this chart in particular. This indicator implements RSI to gauge momentum, BBWP to gauge volatility, and an EMA to gauge trend. Maximum confluence signals are represented by horizontal bars in the indicator's pane, where the tallest green bar is a confirmed buy signal, and the tallest red bar is a confirmed sell signal. The shortest bar represents a momentum-only signal, and the second-shortest bar represents a volatility signal in confluence with the previously given momentum signal.

To track momentum, the RSI is plotted to the indicator plane against a moving average of the RSI. A momentum signal is generated when the RSI crosses over its moving average, retests/approaches the moving average, and then continues in the crossover direction (i.e., it fails to cross the moving average to the opposite side, creating a successful retest). The settings that affect this trigger are the "Crossover Threshold," which specifies how much the RSI should exceed the moving average to be considered a crossover, and the "Retest threshold," which specifies how closely the RSI should approach the moving average to be considered a retest. A momentum signal is ALSO generated if the RSI or its moving average exceed their counterpart by a certain threshold. For example, if the threshold was set at 10, a BUY signal would be generated when the RSI exceeds the moving average by 10, or a SELL signal would be generated when the moving average exceeds the RSI by 10. This threshold can be set using the "Instant Signal Threshold" setting. Either type of momentum signal will be plotted on the pane as the shortest horizontal bar, with its color indicating the signal's direction.

Volatility is primarily measured using the Bollinger Band Width Percentile (BBWP) indicator, which was created by The_Caretaker. BBWP plots the volatility of the asset's price, given by Bollinger Band width, relative to past volatility by assigning the volatility readings into percentiles. The indicator also includes a moving average of the BBWP itself, where a crossover to the upside represents expanding volatility and a crossover to the downside represents contracting volatility. This indicator is used to confirm a signal given by the momentum indicators - a momentum signal that is given during a period of expanding volatility has a greater likelihood of success. Therefore, when the BBWP crosses above its moving average by a given threshold, a previously triggered momentum signal is considered to be "confirmed." The threshold for this crossover can be set using the "BBWP Confirmation Threshold" setting. However, it is also relevant that periods of extreme volatility often accompany an extremity in price action (a "top" or "bottom"), in which case the BBWP is likely to contract after price reaches such an extremity. This phenomenon is captured by also using "extreme reads" on the momentum indicator to signal that there has already been enough volatility to confirm a momentum signal. If the RSI gives an "extreme read" before triggering a signal, the momentum signal is also considered to be confirmed. For example, if the RSI is above 80, breaks below 80, and then gives a SELL signal, this sell signal is considered to be confirmed without requiring the BBWP to crossover its moving average to the upside. The threshold that would confirm a SELL signal can be set with the "Overbought" setting, and the threshold that would confirm a BUY signal can be set with the "Oversold" setting. Whenever a volatility signal confirms a momentum signal, a medium-sized horizontal bar will be plotted on the pane in the same directional color as the momentum signal. Note that a momentum signal may trigger at the exact same time as the volatility signal which confirms it; in this case, only the medium-sized bar will be visible on the pane, but its direction can still be identified by its color.

Lastly, to reduce the likelihood of "false signals," a trend indicator is used to confirm the direction of the signal. This is typically an exponential moving average. If a confirmed volatility SELL signal is given, and the closing price is below the moving average, then the SELL signal is also confirmed by the trend. Likewise, if a confirmed volatility BUY signal is given, and the closing price is above the moving average, then the BUY signal is confirmed by the trend. The type and length of the moving average used to verify the trend can be set using the "Moving Average Type" and "Moving Average Length" settings found below the momentum/volatility settings. A trend signal is plotted on the pane as a tall horizontal bar, and is more deeply colored than the momentum and volatility signals.

For maximum confluence, it is recommended that the trend signal, given by the tallest bar, is the one that forms the basis of trades executed while using the Triple Threat indicator. It is possible to enter more aggressive trades with better entries by using only the volatility signal, given by the medium-sized bar, however this entails greater risk and should only be done in confluence with an additional trading strategy of your own discretion. Backtesting has shown that using the volatility signal alone underperforms using the volatility signal in confluence with the trend signal.

Please also be advised that the default setting are optimized for Bitcoin's daily chart only. The indicator is still applicable to other timeframes and asset classes, but the settings may need to be modified. I have a list of settings for other Bitcoin timeframes, and I would be happy to share them upon request.

I hope you can find this indicator to be of some use to your trading strategies. I'd be happy to hear any feedback from the community, so please don't hesitate to reach out. Stay safe, and happy trading.

SMH_DualMomentum (ROC + Volume Trend)SMH Dual Momentum (ROC + Volume Confirmation)

This indicator identifies high-quality bullish trends by combining price momentum (Rate of Change) with volume confirmation, and exits when momentum structurally fails.

Core Logic

BUY signal

Rate of Change (ROC) over N periods is above a positive threshold (strong upside momentum)

Current volume is above its moving average (rising market participation)

SELL signal

ROC crosses below zero, indicating loss of bullish momentum

Why It Works

ROC measures the speed and strength of price movement, filtering out weak or drifting trends

Volume confirmation ensures momentum is supported by real capital flow, reducing false breakouts

Momentum-based exit avoids prolonged drawdowns and capital stagnation

Key Advantages

Focuses on trend continuation, not prediction

Filters out low-quality price moves and range-bound markets

Captures long, high-conviction trends with relatively few trades

Simple, robust rules using only price and volume

Best Use Cases

Designed for trend-driven ETFs such as SMH (Semiconductors)

Suitable for swing to position trading on daily charts

Works best in markets with strong sector rotation and institutional participation

Notes

This is a trend-following momentum tool, not a mean-reversion indicator

No stop-loss is built in; risk management should be handled externally if required

Parameters can be adjusted to match different timeframes or assets

Supertrend + EMA + RSI Algo (Low Risk High Accuracy)This is a trend-following + momentum confirmation strategy designed to reduce false signals and control loss.

Supertrend (10,3) → Identifies overall market direction (Buy in uptrend, Sell in downtrend)

EMA 50 & EMA 200 → Confirms strong trend and avoids sideways market

Buy only when EMA 50 is above EMA 200

Sell only when EMA 50 is below EMA 200

RSI (14) → Confirms momentum

Buy when RSI > 55 (strong bullish momentum)

Sell when RSI < 45 (strong bearish momentum)

---

🔹 Entry Logic

BUY: Market is in uptrend + strong momentum

SELL: Market is in downtrend + strong bearish pressure

---

🔹 Risk Management (Most Important)

Stop Loss: Based on ATR (adapts to volatility)

Target: Fixed Risk-Reward ratio (example: 1 : 2.5)

This keeps loss small and profits larger

---

🔹 Best Use Case

Works best in trending markets

Ideal timeframes: 15m, 1h, 4h

Suitable for crypto futures & swing trading

Beginner-friendly if used with low leverage

Buy-Dip / Sell-Pullback Buy the Dip / Sell the Pullback – Trend-Following Strategy (EOD → Next Day Execution)

Overview

This is a trend-following futures strategy designed to participate in pullbacks within established trends, not to predict reversals.

It works on End-of-Day (EOD) confirmation and executes trades on the next trading session, making it suitable for positional and swing traders.

The strategy combines momentum, trend direction, volatility, and price location to filter for high-quality setups while avoiding overtrading.

🔍 Core Philosophy

Trade only in the direction of the prevailing trend

Buy dips in uptrends

Sell pullbacks in downtrends

Avoid chasing price after extended gaps

Use volatility-adjusted risk management (ATR-based SL & targets)

📊 Indicators Used

RSI (20)

Measures underlying momentum strength

Stochastic Oscillator (55, 34, 21)

Confirms pullback exhaustion within a trend

Supertrend (10, 2)

Defines primary trend direction

Bollinger Bands (20, 2)

Provides structural trend bias

ATR (5)

Used for:

Entry gap filter

Stop-loss

Profit target

Supertrend buffer

✅ Long (Buy) Setup – Evaluated at EOD

A long setup is generated when all of the following conditions are satisfied at the close of the trading day:

RSI(20) is above the bullish threshold (default: 48)

Stochastic %K is above %D (confirming pullback momentum)

Supertrend direction is bullish

Price is near or above Supertrend, allowing a volatility-adjusted buffer (ATR-based)

Price is above the Bollinger Band middle line

This combination ensures:

The market is trending up

Momentum supports continuation

The pullback is controlled, not a breakdown

❌ Short (Sell) Setup – Evaluated at EOD

A short setup is generated when:

RSI(20) is below the bearish threshold (default: 52)

Stochastic %K is below %D

Supertrend direction is bearish

Price is near or below Supertrend, with an ATR buffer

Price is below the Bollinger Band middle line

This filters for pullbacks within sustained downtrends.

⏰ Trade Execution Logic (Next Day Rule)

Once a setup is confirmed at EOD, a trade is attempted on the next trading session

To avoid chasing gaps:

Long trades are allowed only if price does not move more than a defined multiple of the previous day’s True Range

Short trades follow the same logic in reverse

This is implemented via limit orders, ensuring realistic backtesting and execution behavior

🛑 Risk Management

All exits are volatility-adjusted using ATR:

Stop-Loss:

1.1 × ATR(5) from entry price

Target:

2.2 × ATR(5) from entry price

This results in a risk–reward ratio of approximately 1:2

ATR is frozen at entry to avoid forward-looking bias.

🧠 Why This Strategy Works

Avoids low-quality trades during consolidation

Participates only when trend + momentum align

Prevents emotional gap-chasing