MACD-V with Volatility Normalisation [DCD]MACD-V with Volatility Normalisation

This indicator is a modified version of the traditional MACD, designed to account for market volatility by normalizing the MACD line using the Average True Range (ATR). It provides a more adaptive approach to identifying momentum shifts and potential trend reversals. This indicator was developed by Alex Spiroglou in this paper:

Spiroglou, Alex, MACD-V: Volatility Normalised Momentum (May 3, 2022).

Features:

Volatility Normalization: The MACD line is adjusted using ATR to standardize its values across different market conditions.

Customizable Parameters: Users can adjust the MACD fast length, slow length, signal line smoothing, and ATR length to suit their trading style.

Histogram Visualization: The histogram highlights the difference between the MACD and signal lines, with customizable colors for positive and negative momentum.

Crossover Signals: Green and red dots indicate bullish and bearish crossovers between the MACD and signal lines.

Background Highlighting: The chart background changes to green when the MACD is above 0 and red when it is below 0, providing a clear visual cue for bullish and bearish conditions.

Horizontal Levels: Dotted horizontal lines are plotted at key levels for better visualization of MACD values.

How to Use:

Look for crossovers between the MACD and signal lines to identify potential buy or sell signals.

Use the histogram to gauge the strength of momentum.

Pay attention to the background color for quick identification of bullish (green) or bearish (red) conditions.

This indicator is ideal for traders who want a more dynamic MACD that adapts to market volatility. Customize the settings to align with your trading strategy and timeframe.

Cari dalam skrip untuk "momentum"

Relative Directional Index (RDI)🔍 Overview

The Relative Directional Index (RDI) is a hybrid tool that fuses the Average Directional and the Relative Strength Indices (ADX and RSI) into a single, highly visual interface. While the former captures trend strength, the latter reveals momentum shifts and potential exhaustion. Together, they can confirm trend structure, anticipate reversals, and sharpen the timing entries and exits.

📌 Why Combine ADX with RSI?

Most indicators focus on either trend-following (like ADX) or momentum detection (like RSI)—but rarely both. Each comes with trade-offs:

- ADX alone confirms trend strength but ignores momentum.

- RSI alone signals overbought/oversold, but lacks trend context.

The RDI resolves this by integrating both, offering:

- Smarter filters for trend entries

- Early warnings of momentum breakdowns

- More confident signal validation

🧠 Design Note: Fibonacci Harmony

All default values—5, 13, 21—are Fibonacci numbers. This is intentional, as these values reflect the natural rhythm of market cycles, and promote harmonic calibration between price action and indicator logic.

🔥 Key Features

✅ ADX Histogram

- Green bars = trend gaining strength

- Red bars = trend weakening

- Adjustable transparency for visual tuning

✅ ADX Line (Orange)

- Measures trend strength over time

- Rising = accelerating trend

- Falling = trend may be fading

✅ RSI Line (Lemon Yellow)

- Captures momentum surges and slowdowns

- Above 50 = bullish control

- Below 50 = bearish pressure

✅ Trend Strength Squares

- Bright green = strong uptrend

- Bright red = strong downtrend

- Faded colors = range-bound or indecisive

✅ ADX/RSI Crossover Markers

- Yellow square = RSI crosses above ADX → momentum building

- Orange square = ADX crosses above RSI → trend still dominant

✅ Customizable Reference Lines

- Yellow (50) = strong trend threshold

- Red (30) = weak trend zone

- Green (70) = overextended, potential exhaustion

_______________________________________________________

🎯 How to Trade with the RDI

The RDI helps traders identify momentum-supported trends, catch early reversals, and avoid false signals during consolidation.

✅ Trend Confirmation Entries

🔼 Bullish → Enter long on pullbacks or resistance breakouts

- ADX rising above 30

- RSI above 50

- Green trend square visible

🔽 Bearish → Enter short on breakdowns or failed retests

- ADX rising

- RSI below 50

- Red trend square visible

🧯 Exit if RSI crosses back against trend direction or ADX flattens

🚨 Reversal Setups Using Divergence

📈 Bullish Divergence → Long entry after confirmation (e.g. engulfing bar, volume spike)

- Price prints lower low

- RSI prints higher low

- Green triangle

📉 Bearish Divergence → Short entry on breakdown

- Price prints higher high

- RSI prints lower high

- Red triangle

Tip: Stronger if ADX is declining (fading trend strength)

🔂 Breakout Detection via Cross Markers

- Yellow square = RSI > ADX → breakout brewing

- Orange square = ADX > RSI → trend continuation likely

⏸️ Avoid Choppy Markets

- RSI between 45–55

- Faded trend squares

- Flat ADX below 20–30

🧠 Pro Tips

- Combine RDI with VWAPs, moving averages and/or pitchforks

- Watch for alignment between trend and momentum

- Use divergence markers as confirmation, not stand-alone triggers

_______________________________________________________

⚠️ Hidden Divergence (Optional)

The RDI includes optional hidden divergence detection. These signals suggest trend continuation but are off by default. Use with discretion—best in established trends, not sideways markets.

🙈 Hidden Bullish

- Price prints higher low

- RSI prints lower low

🙈 Hidden Bearish

- Price prints lower high

- RSI prints higher high

Momentum Cycle Oscillator (MCO)1. Concept and Inspiration

The Momentum Cycle Oscillator (MCO) is a unique indicator designed to combine volatility and momentum into a unified tool for identifying market cycles. Traditional indicators often isolate either momentum (e.g., RSI) or volatility (e.g., Bollinger Bands), but the MCO bridges the gap by synthesizing these dimensions into one oscillating signal. By measuring price acceleration (momentum) and range consistency (volatility), the MCO aims to detect when a price cycle is shifting from contraction to expansion or vice versa, signaling potential trend reversals or continuations. Its zero-centered design provides a clear demarcation between bullish and bearish cycles.

2. Mathematical Structure

The MCO is built on two foundational components: the volatility factor and the momentum factor. The volatility factor quantifies the price range over a defined period, highlighting market consistency and expansion. Meanwhile, the momentum factor assesses the rate of change in smoothed closing prices, revealing directional acceleration. These two factors are multiplied to create the raw MCO value, which is further smoothed to reduce noise and improve readability. The resulting oscillator fluctuates around zero, with positive values indicating upward cycles and negative values signaling downward cycles.

3. Practical Applications

The MCO excels in identifying cycle turning points, where the market transitions from a bearish phase to a bullish phase or vice versa. Traders can use the zero line as a reference: a crossover from below to above zero suggests a potential buy signal, while a crossover from above to below zero indicates a sell signal. The MCO’s unique blend of volatility and momentum also helps detect shifts in trend strength, making it valuable in both trending and ranging markets. Its histogram visualization further aids traders by emphasizing the magnitude and direction of market momentum.

4. Innovative Features

What sets the MCO apart is its ability to adapt dynamically to market conditions. By fusing two dimensions of market behavior—volatility and momentum—it provides a holistic view of price action. Unlike traditional indicators that rely heavily on recursion (e.g., EMA), the MCO’s straightforward calculation reduces lag, ensuring timely signals. Furthermore, its use of normalized components allows it to function effectively across diverse assets and timeframes without extensive parameter tuning. This makes it particularly versatile for both intraday traders and long-term investors.

5. Limitations and Potential

While the MCO is robust, it is not immune to challenges. In highly choppy or low-volume markets, the indicator may generate false signals, as volatility and momentum can be erratic. Additionally, its performance depends on proper parameter calibration, with periods requiring adjustment to align with the asset’s behavior. However, its creative approach to combining volatility and momentum offers immense potential for refinement and customization. With proper backtesting and optimization, the MCO could become a staple tool for traders seeking a comprehensive yet simple way to interpret market cycles.

Pip hunter 1-Minute Scalping Strategy [manesisnet]NOTE: This is my first attempt to write an indicator using pine script and it's not recommended for serious trading, just use it for your own research or feel free to create your own versions based on the below.

Overview: The "1-Minute Scalping Strategy" is a custom TradingView indicator designed for short-term traders looking to capitalize on quick price movements in the 1-minute timeframe. This strategy combines moving averages and the Relative Strength Index (RSI) to generate buy and sell signals while filtering out potential false entries by confirming trends on a higher timeframe.

How It Works:

Moving Averages:

The indicator uses two Simple Moving Averages (SMAs):

A fast SMA (5-period) for short-term price movements.

A slow SMA (20-period) to identify the overall trend.

Buy signals are generated when the fast SMA crosses above the slow SMA, indicating bullish momentum.

Sell signals occur when the fast SMA crosses below the slow SMA, indicating bearish momentum.

Higher Time Frame Confirmation:

To enhance the accuracy of the signals, the strategy checks the trend on a higher timeframe (default is 5 minutes).

A buy signal is only valid if the current price is above the higher timeframe SMA, confirming that the overall trend is bullish.

A sell signal is only valid if the current price is below the higher timeframe SMA, confirming a bearish trend.

This confirmation helps avoid false breakouts and ensures that trades are aligned with the prevailing market direction.

Relative Strength Index (RSI):

The RSI is used to assess market momentum and potential reversal points.

The indicator calculates a 14-period RSI to identify overbought and oversold conditions.

For buy signals, the RSI must be below 60 (indicating the market is not overbought).

For sell signals, the RSI must be above 40 (indicating the market is not oversold).

This helps to filter out trades that might occur during extreme market conditions.

Visual Representation:

The fast SMA (5-period) is plotted in blue, the slow SMA (20-period) in red, and the higher timeframe SMA in orange.

Buy signals are indicated with a green label below the bar, while sell signals are indicated with a red label above the bar.

This visual representation allows traders to quickly identify potential entry points.

Alerts:

The script includes alert conditions for buy and sell signals, enabling traders to receive notifications when the conditions for entering trades are met.

RSI Slope Filtered Signals [UAlgo]The "RSI Slope Filtered Signals " is a technical analysis tool designed to enhance the accuracy of RSI (Relative Strength Index) signals by incorporating slope analysis. This indicator not only considers the RSI value but also analyzes the slope of the RSI over a specified number of bars, providing a more refined signal that accounts for the momentum and trend strength. By utilizing both positive and negative slope arrays, the indicator dynamically adjusts its thresholds, ensuring that signals are responsive to changing market conditions. This tool is particularly useful for traders looking to identify overbought and oversold conditions with a higher degree of precision, filtering out noise and providing clear visual cues for potential market reversals.

🔶 Key Features

Dynamic Slope Analysis: Measures the slope of RSI over a customizable number of bars, offering insights into the momentum and trend direction.

Adaptive Thresholds: Uses historical slope data to calculate dynamic thresholds, adjusting signal sensitivity based on market conditions.

Normalized Slope Calculation: Normalizes the slope values to provide a consistent measure across different market conditions, making the indicator more versatile.

Clear Signal Visualization: The indicator plots both positive and negative normalized slopes with color gradients, visually representing the strength of the trend.

Overbought and Oversold Signals: Plots overbought and oversold signals directly on the chart when the calculated value reaches the user-specified threshold, helping traders identify potential reversal points.

Customizable Settings: Allows users to adjust the RSI length, slope measurement bars, and lookback periods, providing flexibility to tailor the indicator to different trading strategies.

🔶 Interpreting the Indicator

The "RSI Slope Filtered Signals " indicator is designed to be easy to interpret. Here's how you can use it:

Normalized Slope: The indicator plots the normalized slope of the RSI, with values above zero indicating positive momentum and values below zero indicating negative momentum. A higher positive slope suggests a strong upward trend, while a deeper negative slope indicates a strong downward trend.

Reversal Signals: The indicator plots several horizontal lines at different thresholds (+3, +2, +1, 0, -1, -2, -3). These levels are used to gauge the strength of the momentum based on the normalized slope. For example, a normalized slope crossing above the +2 threshold may indicate a strong bullish trend, while crossing below the -2 threshold may suggest a strong bearish trend. These thresholds help in understanding the intensity of the current trend and provide context for interpreting the indicator's signals.

This indicator generates overbought and oversold signals not solely based on the RSI entering extreme levels (above 70 for overbought and below 30 for oversold), but also by considering the behavior of the normalized slope relative to specific thresholds. Specifically, the Overbought Signal (🔽) is triggered when the RSI is above 70 and the normalized slope from the previous bar is greater than or equal to the upper threshold, with the current slope being lower than the previous slope, indicating a potential bearish reversal as momentum may be slowing down.

Similarly, the Oversold Signal (🔼) is generated when the RSI is below 30 and the normalized slope from the previous bar is less than or equal to the lower threshold, with the current slope being higher than the previous slope, signaling a potential bullish reversal as the downward momentum may be weakening.

Area Plots: The indicator also plots the positive and negative slopes as filled areas, providing a quick visual cue for the strength and direction of the trend. Green areas represent positive slopes (upward momentum), while red areas represent negative slopes (downward momentum).

By combining these elements, the "RSI Slope Filtered Signals " provides a comprehensive view of the market's momentum, helping traders make more informed decisions by filtering out false signals and focusing on the significant trends.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Trade Scanner Pro [MarketSignalsPro]

█ OVERVIEW

Trade Scanner Pro is a trade signal generator based on my trend following momentum reversal system. It identifies a pullback and then confirms momentum exhaustion which produces a signal appearing as a set of suggested orders (horizontal lines) on the chart. The goal is to help traders capitalize on price momentum while simplifying decision making and offering a way to gauge expectations. It can be used for any market, any time frame and configured for counter trend signals also.

█ CONCEPT

While markets are highly random, especially on smaller time frames, trends do exist.

Trade Scanner Pro offers a visually structured way to align the user

with price momentum that is relevant to the trend. It accomplishes this by incorporating a unique mix of standard technical formulas to identify a pullback followed by a momentum reversal. The process occurs in 3 steps:

1 — Identifying the trend of the current time frame.

2 — Evaluating the retrace in terms of how far it moves away from the typical price.

3 — Confirming price exhaustion by recognizing a reversal in price momentum.

Once the criteria are met, a signal appears as a blue horizontal line. This is the entry price suggestion (see label). Stop and take profit orders are also calculated simultaneously. These appear as a red line and green line respectively with price labels. The stop and take profit orders are based upon an average of previous price ranges and will be relative to the price action on the chosen time frame. The initial reward/risk ratio is set to 1.5:1, and can be changed in the settings menu.

This system can also be adjusted to cater to the experience level of the trader. For example, more advanced traders can select “counter trend” mode which will only show signals on the opposite side of the trend. A trailing stop can be activated to help stay in a trade after reaching the profit level. There is also a “heads up” mode which colors the candles orange which means a signal is more likely to appear over the next couple of candles. More on these features in the next section.

For best results, time frames of 1 minute and above should be considered. The smaller the time frame, the more signals, but also more noise and stop outs. Knowing your

market and the most active time of day is especially important for smaller time frames.

█ FEATURES

The following features can be found in the settings menu of Trade Scanner Pro.

Show Trend:

The initial setting is “on”. This shows the trend label on the upper right corner of the screen. Trend can be either bullish or bearish. At times there will be a “conflict” label that appears below the trend label. Conflict means the trend MAY be in the process of changing. This occurs when price persists against the prevailing trend for a prolonged amount of time.

Counter Trend:

When selected will ignore signals on the side of the trend and show counter trend signals only. If the “heads up” feature is selected, orange candles will only appear for potential counter trend signals.

Trailing Stop:

When selected, a trailing stop order suggestion (orange line) will appear beginning from the stop loss price (red line) after a few closed candles. The trailing stop line will follow the price upon each new close of the candles until it is touched. This serves as a point of reference to capture larger market movements and skew reward/risk favorably over time.

Heads Up:

When selected will paint orange candles when there is a greater chance a signal will appear. For example, in trend mode it will only evaluate signals on the side of the trend. In counter trend mode it will evaluate counter trend signals only. For advanced users, this “pre signal” can offer potential opportunities to enter a trade before the signal appears.

Reward Ratio:

This is the reward part of the reward/risk formula used to establish the take profit suggestion on the chart. Initially it is set at 1.5 which produces a line on the chart at a 1.5:1 ratio. The user can change this setting to better align with their expectations. For example, if a larger market movement is anticipated, 2 can be entered into the input field and will generate a take profit line 2X farther than the stop loss line (2:1 reward/risk).

█ LIMITATIONS

Markets are HIGHLY random, especially on smaller time frames. No system that is based on public domain formulas can be expected to be HIGHLY accurate. It is reasonable to expect a 50% win rate more often than not. Profitability in such systems depends on the reward/risk rather than win rate.

This is a system based on price momentum which means MOMENTUM must be present for best results especially on very short time frames.

While this system helps to reduce the burden of analysis, the user should have some basic familiarity with technical analysis. Basic knowledge can help to better determine a quality signal over noise.

█ RAMBLINGS

The stop loss orders MUST be respected otherwise the user puts their entire account at risk. Signals can appear at price locations where larger magnitude risk is extremely high. Respecting the stop loss suggestions can help to mitigate this risk.

For best results set up notifications to receive a message on your desktop, smart phone or tablet rather than sitting in front of a computer screen waiting for a signal to appear. Keep in mind a 1 minute chart in a single market can produce 5 or 6 signals throughout the entire daily session and NOT all will be profitable. A 1 hour time frame may produce 1 or 2 throughout the day. The larger the time frame the lower frequency of signals.

█ THANKS

Special thanks to Cryptosnagger for

helping me translate my concept into a pine script reality.

Momentum Madness (AKA: Moms Mad)The "Momentum Madness" indicator is a customizable technical analysis tool designed for TradingView. It aims to help traders assess price momentum and make informed trading decisions. Below is a description of how this indicator works:

Indicator Title and Settings:

The indicator is titled "Momentum Madness" with a short title "Moms Mad."

Users can customize various settings to tailor the indicator to their preferences.

Input Parameters:

Traders can set the lengths (periods) for four different momentum calculations (len1, len2, len3, len4).

They can specify a lookback period for trend direction determination.

Users can choose from three smoothing types (RMA, SMA, EMA) and set the smoothing length (smoothLength).

The indicator offers options to adjust momentum calculations based on volume (useVolumeWeight), RSI (useRSIAdjustment), and MACD (useMACDAdjustment).

If the trend filter is enabled (useTrendFilter), the indicator considers whether the price is above the 200-period SMA.

Traders can incorporate Bollinger Bands adjustments (useBBAdjustment) and set the Bollinger Bands length (bbLength).

A volatility adjustment can be applied (useVolatilityAdjustment), using the Average True Range (ATR) with a specified length (atrLength).

Smoothing Function:

The indicator offers three smoothing options: RMA, SMA, and EMA, allowing users to select their preferred method for smoothing price data.

Momentum Calculations:

The indicator calculates four different momentum values (mom1, mom2, mom3, mom4) by subtracting the current price from historical prices based on the specified lengths.

Enhancement Features:

Users can enhance momentum calculations through volume weighting, RSI adjustment, MACD adjustment, trend filtering, Bollinger Bands adjustment, and volatility adjustment, depending on their preferences.

Trend Direction Detection:

The indicator identifies the trend direction based on the comparison of the current momentum (mom4Smooth) with a momentum value from a specified lookback period. It determines whether the trend is bullish (green), bearish (red), or neutral (no change).

Plots:

The indicator visualizes the four smoothed momentum values (mom1Smooth, mom2Smooth, mom3Smooth, mom4Smooth) as separate plots on the chart, each with its own customizable color.

A zero line is displayed for reference (yellow).

The average momentum (averageMomentumSmooth) is plotted and can be customized with its own color.

The "Momentum 4" plot dynamically changes color based on trend direction (green for bullish, red for bearish).

Fill:

The indicator fills the area between the "Momentum 4" plot and the zero line with a customizable color to highlight bullish or bearish momentum.

Look for crossover events by studying the chart and understanding what they all mean. Happy trading :)

Momentum RSIThis RSI is used to determine price Momentum and Overbought or Oversold Market conditions. When the RSI is between 50% and 70% price is considered to have upward momentum. When The RSI is between 50% and 30% price is considered to have downward momentum. When the RSI is between 40% and 60% price is considered to have no directional momentum and is considered to be in consolidation. When the RSI is above 70% price is to be considered Overbought. When the RSI is bellow 30% price is to be considered Oversold

EGX Monitor Dashboard By Biscuits_Trading_Solutionsلوحة مراقبة البورصة المصرية من Biscuits_Trading_Solutions

نظرة عامة:

لوحة مراقبة البورصة المصرية هي أداة تحليل فني شاملة مصممة لتوفير نظرة فورية وواضحة على صحة السوق. تجمع الأداة مؤشرات رئيسية مختارة بعناية لتناسب السوق المصري لتوفر عليك عبء إضافة عدد كبير من المؤشرات في وقت واحد على الشاشة - بما في ذلك متوسطات متحركة، MACD، RSI، ADX، ATR، وتحليل متقدم لحجم التداول (دلتا) - في جدول واحد وسهل القراءة على الرسم البياني. مثالية للمتداولين الذين يحتاجون لتقييم الاتجاه، الزخم، وديناميكيات الحجم في لمحة دون تشويش الشاشة.

English Version is below ⬇️⬇️

المميزات الرئيسية:

* لوحة متابعة للمتوسطات المتحركة: تتابع وتلون وضع السعر بالنسبة لـ 6 متوسطات متحركة رئيسية (200 بسيط، 100 بسيط/آسي، 50 بسيط، 20 آسي، 9 آسي).

* تحليل متقدم لـ MACD: تعرض قيمة هِستوجرام MACD، حالة التقاطع بين MACD وخط الإشارة، وتكشف عن انحرافات صعودية محتملة (Bullish Divergence).

* مقاييس الزخم: تتضمن قراءات RSI و ADX، مع تلوينها للإشارة إلى مناطق الشراء المفرط والبيع المفرط وقوة الاتجاه.

تحليل متطور للحجم:

*دلتا الحجم/السيولة (الفارق بين حجم الشراء وحجم البيع).

* الحجم مقارنة بمتوسطه المتحرك لـ 20 و 50 فترة (لمقارنته بفترة متوسطة 20 شمعة وطويلة 50 شمعة)

* دلتا الحجم مقارنة بمتوسطها المتحرك لـ 20 و 50 فترة لقياس ضغط البيع والشراء.

عرض مرئي نظيف : جميع البيانات معروضة في جدول شبه شفاف يمكن وضعه في أي مكان على الرسم البياني. يتم أيضًا رسم المتوسطات المتحركة بخفة للاستدلال البصري.

مدخلات قابلة للتخصيص : جميع أطوال المؤشرات، المضاعفات، وموضع الجدول قابلة للتعديل كليًا من الإعدادات.

إزاحة الشمعة : تسمح لك بمشاهدة قراءات المؤشر من عدد محدد من الشمعات السابقة، مما يفيد في تحليل الظروف السابقة.

طريقة الاستخدام:

* تقييم الاتجاه: انظر إلى جدول المتوسطات المتحركة. وجود عدة خلايا خضراء (السعر فوق المتوسط) يشير إلى اتجاه صاعد قوي، بينما يشير اللون الأحمر إلى اتجاه هابط.

* تأكيد الزخم: تحقق من مؤشر RSI (شراء مفرط >70، بيع مفرط <30) و ADX (اتجاه قوي >25) لفهم سياق الزخم.

*تأكيد الحجم: استخدم أعمدة الحجم لتأكيد الحركات. حركة السعر المصحوبة بحجم "أعلى من المتوسط" ودلتا "صعودي" تكون أكثر أهمية.

إشارات الدخول/الخروج:

* انحراف MACD الصعودي يمكن أن يشير إلى انعكاس محتمل.

* وجود "نعم" لـ "MACD > Sig" يؤكد الزخم الصعودي.

* قيم ATR المرتفعة تشير إلى زيادة التقلب، وغالبًا ما ترافق الاتجاهات القوية أو اختراقات المستويات.

الإعدادات:

ما عليك سوى إضافة المؤشر إلى الرسم البياني الخاص بك. ستظهر اللوحة تلقائيًا. يمكنك ضبط جميع المعاملات (أطوال المتوسطات المتحركة، إعدادات الحجم، مكان الجدول) في تبويب "الإدخالات" في نافذة المؤشر لتناسب أسلوب تداولك.

إخلاء مسؤولية: جميع الإشارات التي تظهر ليست دعوة للبيع والشراء، هذا المحتوى تعليمي يساعدك على قراءة الشاشة بشكل أفضل، وقرارك الاستثماري يعود لك وحدك.

---

EGX Monitor Dashboard By Biscuits_Trading_Solutions

Overview :

The EGX Monitor Dashboard is a comprehensive technical analysis tool designed to provide a clear and immediate overview of the market's health. It consolidates key indicators, carefully selected for the Egyptian market, saving you the burden of adding a large number of indicators to your screen at once —including moving averages, MACD, RSI, ADX, ATR, and advanced volume delta analysis—into a single, easy-to-read table on your chart. Perfect for traders who need to assess trend, momentum, and volume dynamics at a glance without cluttering their screen.

Key Features :

* Moving Average Dashboard: Tracks and color-codes the price position relative to 6 key moving averages (200 SMA, 100 SMA/EMA, 50 SMA, 20 EMA, 9 EMA).

* Advanced MACD Analysis: Displays the MACD histogram value, the MACD vs. Signal line crossover state, and detects potential bullish divergences.

* Momentum Gauges: Includes RSI and ADX readings, color-coded for overbought/oversold and trend strength conditions.

Advanced Volume/Liquidity Analysis:

* Volume Delta (the difference between buying and selling volume).

* Volume compared to its 20 and 50-period moving averages (for medium-term 20-bar and long-term 50-bar comparisons).

* Volume Delta compared to its 20 and 50-period moving averages to measure buying/selling pressure.

Clean Visualization: All data is presented in a semi-transparent table that can be positioned anywhere on the chart. The moving averages are also plotted lightly for visual reference.

Customizable Inputs: All indicator lengths, multipliers, and the table position are fully adjustable in the settings.

Bar Offset: Allows you to view the indicator readings from a specific number of bars back, useful for analyzing past conditions.

How to Use:

* Trend Assessment: Look at the MA table. A cluster of green "Bullish" cells (price above MA) indicates a strong uptrend, while red indicates a downtrend.

* Momentum Confirmation: Check the RSI (overbought >70, oversold <30) and ADX (strong trend >25) for momentum context.

* Volume Confirmation: Use the volume columns to confirm moves. A price move with "Above Avg" volume and "Bullish" Delta is more significant.

Entry/Exit Clues:

* A "Bullish" MACD divergence can signal a potential reversal.

* A "Yes" for "MACD > Sig" confirms bullish momentum.

* High ATR values indicate increased volatility, often accompanying strong trends or breakouts.

Configuration:

Simply add the indicator to your chart. The dashboard will appear automatically. You can adjust all parameters (MA lengths, volume settings, table position) in the indicator's "Inputs" tab to suit your trading style.

Disclaimer: All signals that appear are not an invitation to buy or sell. This content is educational and is intended to help you read the screen better. Your investment decision is yours alone.

Maple Trend Maximizer – AI-Powered Trend & Entry IndicatorOverview:

Maple Trend Maximizer is an AI-inspired market analysis tool that identifies trend direction, highlights high-probability entry zones, and visually guides you through market momentum. Designed for traders seeking smart, data-driven signals, it combines trend alignment with proprietary AI-style calculations for precise timing.

Key Features:

AI Trend Detection:

Automatically identifies bullish and bearish trends using advanced smoothing and trend alignment techniques.

Momentum & Signal Lines:

Dynamic lines indicate market strength and potential turning points.

Colors change to highlight high-probability entry zones.

Entry Signals:

Optional visual markers suggest precise entries when trend direction and momentum align.

Configurable to reduce noise and focus on strong setups.

Multi-Timeframe Flexibility:

Works on intraday charts or higher timeframes for swing and position trading.

Customizable Settings:

Adjustable smoothing, trend sensitivity, and signal display options.

Lets you fine-tune the indicator to your trading style.

Benefits:

Quickly identifies market direction and optimal entries.

Provides clear, visually intuitive signals.

Can be used standalone or integrated into a larger strategy system.

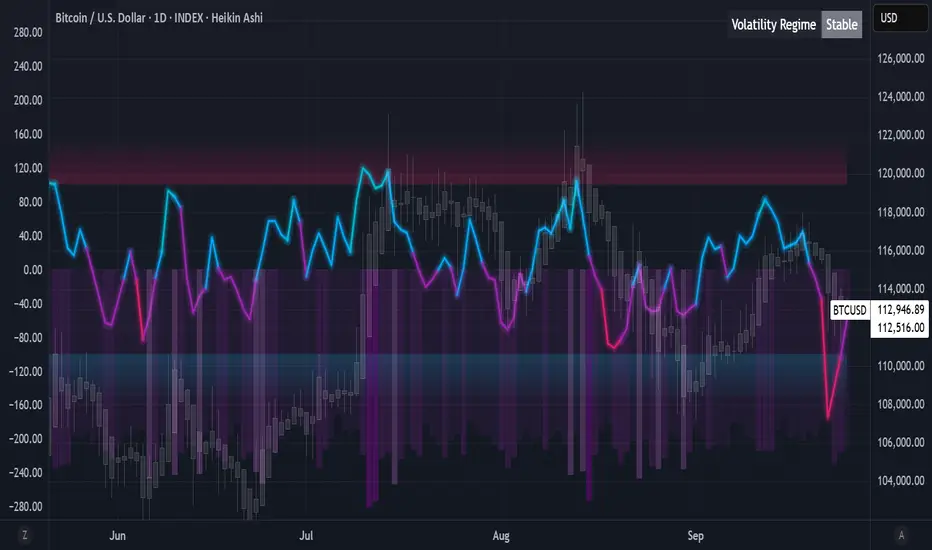

Algorithmic Value Oscillator [CRYPTIK1]Algorithmic Value Oscillator

Introduction: What is the AVO? Welcome to the Algorithmic Value Oscillator (AVO), a powerful, modern momentum indicator that reframes the classic "overbought" and "oversold" concept. Instead of relying on a fixed lookback period like a standard RSI, the AVO measures the current price relative to a significant, higher-timeframe Value Zone .

This gives you a more contextual and structural understanding of price. The core question it answers is not just "Is the price moving up or down quickly?" but rather, " Where is the current price in relation to its recently established area of value? "

This allows traders to identify true "premium" (overbought) and "discount" (oversold) levels with greater accuracy, all presented with a clean, futuristic aesthetic designed for the modern trader.

The Core Concept: Price vs. Value The market is constantly trying to find equilibrium. The AVO is built on the principle that the high and low of a significant prior period (like the previous day or week) create a powerful area of perceived value.

The Value Zone: The range between the high and low of the selected higher timeframe.

Premium Territory (Distribution Zone): When the oscillator moves into the glowing pink/purple zone above +100, it is trading at a premium.

Discount Territory (Accumulation Zone): When the oscillator moves into the glowing teal/blue zone below -100, it is trading at a discount.

Key Features

1. Glowing Gradient Oscillator: The main oscillator line is a dynamic visual guide to momentum.

The line changes color smoothly from light blue to neon teal as bullish momentum increases.

It shifts from hot pink to bright purple as bearish momentum increases.

Multiple transparent layers create a professional "glow" effect, making the trend easy to see at a glance.

2. Dynamic Volatility Histogram: This histogram at the bottom of the indicator is a custom volatility meter. It has been engineered to be adaptive, ensuring that the visual differences between high and low volatility are always clear and dramatic, no matter your zoom level. It uses a multi-color gradient to visualize the intensity of market volatility.

3. Volatility Regime Dashboard: This simple on-screen table analyzes the histogram and provides a clear, one-word summary of the current market state: Compressing, Stable, or Expanding.

How to Use the AVO: Trading Strategies

1. Reversion Trading This is the most direct way to use the indicator.

Look for Buys: When the AVO line drops into the teal "Accumulation Zone" (below -100), the price is trading at a discount. Watch for the oscillator to form a bottom and start turning up as a signal that buying pressure is returning.

Look for Sells: When the AVO line moves into the pink "Distribution Zone" (above +100), the price is trading at a premium. Watch for the oscillator to form a peak and start turning down as a signal that selling pressure is increasing.

2. Best Practices & Settings

Timeframe Synergy: The AVO is most effective when your chart timeframe is lower than your selected "Value Zone Source." For example, if you trade on the 1-hour chart, set your Value Zone to "Previous Day."

Confirmation is Key: This indicator provides powerful context, but it should not be used in isolation. Always combine its readings with your primary analysis, such as market structure and support/resistance levels.

Rainbow Trend [Mc]1. Momentum-Based Foundation

This indicator measures the velocity and strength of price changes.

Rising momentum indicates that price movement (upward or downward) has strength behind it.

When momentum weakens or reverses, it often signals a potential trend reversal.

2. Long-Term Time Frame

Unlike traditional indicators like RSI or Stochastic, which use shorter lookback periods (e.g., 14 days), this indicator uses a much longer period, such as 50 to 200 days.

This extended range helps smooth out volatility and provides a clearer view of the primary trend.

3. Multicolored Gradient Lines

The indicator displays multi-layered colored curves, often with a rainbow-like gradient.

Red or pink areas indicate strong selling pressure or peak momentum in an uptrend.

Green or bright green dots often suggest recovery or bottoming momentum.

Orange or yellow colors indicate neutral or transition zones, awaiting trend confirmation.

4. Horizontal Levels (Overbought/Oversold Zones)

The chart includes reference levels such as +160, 0, -40, and -120 (as shown in the image).

These levels help identify when momentum is reaching overbought or oversold conditions.

Reversals often begin near the upper or lower extremes of these zones.

5. Reversal Signal Markers

Red dots at the top indicate extreme bullish momentum and potential topping zones.

Green dots at the bottom suggest oversold conditions and potential bullish reversals.

GKD-C Composite RSI [Loxx]Giga Kaleidoscope GKD-C Composite RSI is a Confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ What is the Composite RSI?

The Composite Relative Strength Index (Composite RSI) is a sophisticated adaptation of the traditional Relative Strength Index (RSI). This advanced indicator combines the benefits of smoothing techniques with the relative strength index to offer a more detailed perspective of market conditions. To fully comprehend the scope of Composite RSI, it's crucial to first understand the traditional RSI and its limitations.

The Relative Strength Index (RSI) is a widely used momentum oscillator that gauges the speed and change of price movements. Developed by J. Welles Wilder, the RSI is a scale from 0 to 100, with high and low levels typically set at 70 and 30, respectively. When the RSI climbs above 70, the asset is often considered overbought, suggesting a potential price decrease. Conversely, when the RSI falls below 30, the asset is deemed oversold, indicating a potential price increase.

While the RSI is beneficial in various market conditions, it is not without its limitations. One of the main criticisms of the traditional RSI is that it can produce false signals during trending markets. This is primarily due to the fact that the RSI only considers a single timeframe and does not account for volatility in the market.

The Composite RSI aims to address these limitations. This advanced indicator uses smoothing techniques and depth analysis to provide a more nuanced view of the market. As the provided pseudocode suggests, the Composite RSI calculates the Relative Strength (RS) over a given period and a certain depth, incorporating the average upward and downward changes in the price.

By using the Composite RSI, traders can better interpret market conditions and make more informed decisions. Its application of smoothing techniques helps to filter out market noise and reduce the likelihood of false signals. Furthermore, by considering multiple periods (the depth), the Composite RSI provides a more comprehensive view of market momentum.

While the traditional RSI remains a valuable tool in technical analysis, the Composite RSI offers a more nuanced and comprehensive approach to assessing market conditions. By incorporating smoothing techniques and depth analysis, the Composite RSI provides a more reliable and robust measure of market momentum, enhancing the decision-making process for traders and investors alike.

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v2.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data to A backtest module wherein the various components of the GKD system are combined to create a trading signal.

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Full GKD Backtest

Baseline: Hull Moving Average

Volatility/Volume: Hurst Exponent

Confirmation 1: Composite RSI

Confirmation 2: uf2018 as shown

Continuation: Vortex

Exit: Rex Oscillator

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD system.

█ Giga Kaleidoscope Modularized Trading System Signals

Standard Entry

1. GKD-C Confirmation gives signal

2. Baseline agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

1-Candle Standard Entry

1a. GKD-C Confirmation gives signal

2a. Baseline agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Baseline Entry

1. GKD-B Basline gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

7. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

1-Candle Baseline Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Volatility/Volume Entry

1. GKD-V Volatility/Volume gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Volatility/Volume Entry

1a. GKD-V Volatility/Volume gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSVVC Bars Back' prior

Next Candle

1b. Price retraced

2b. Volatility/Volume agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Baseline agrees

Confirmation 2 Entry

1. GKD-C Confirmation 2 gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Volatility/Volume agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Confirmation 2 Entry

1a. GKD-C Confirmation 2 gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSC2C Bars Back' prior

Next Candle

1b. Price retraced

2b. Confirmation 2 agrees

3b. Confirmation 1 agrees

4b. Volatility/Volume agrees

5b. Baseline agrees

PullBack Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price is beyond 1.0x Volatility of Baseline

Next Candle

1b. Price inside Goldie Locks Zone Minimum

2b. Price inside Goldie Locks Zone Maximum

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Continuation Entry

1. Standard Entry, 1-Candle Standard Entry, Baseline Entry, 1-Candle Baseline Entry, Volatility/Volume Entry, 1-Candle Volatility/Volume Entry, Confirmation 2 Entry, 1-Candle Confirmation 2 Entry, or Pullback entry triggered previously

2. Baseline hasn't crossed since entry signal trigger

4. Confirmation 1 agrees

5. Baseline agrees

6. Confirmation 2 agrees

█ Connecting to Backtests

All GKD indicators are chained indicators meaning you export the value of the indicators to specialized backtest to create your GKD trading system. Each indicator contains a proprietary signal generation algorithm that only work with GKD backtests. You can find these backtests using the links below.

GKD-BT Giga Confirmation Stack Backtest:

GKD-BT Giga Stacks Backtest:

GKD-BT Full Giga Kaleidoscope Backtest:

GKD-BT Solo Confirmation Super Complex Backtest:

GKD-BT Solo Confirmation Complex Backtest:

GKD-BT Solo Confirmation Simple Backtest:

Momentum-Adjusted Volatility Ratio (MAVR)The Momentum-Adjusted Volatility Ratio (MAVR) indicator is designed to help you understand the strength of price movements relative to the market's volatility. It combines the concepts of rate of change (ROC) and average true range (ATR) and then calculates their ratio, which is then smoothed using an exponential moving average (EMA). Here's a general guide on how to use the MAVR indicator:

Identify the trend: Look for the overall direction of the EMA of the MAVR. When the EMA is above the zero line, it indicates that the momentum is positive and the trend is generally bullish. Conversely, when the EMA is below the zero line, it indicates that the momentum is negative, and the trend is generally bearish.

Assess momentum strength: Pay attention to the distance between the EMA of the MAVR and the zero line. A larger distance indicates a stronger momentum, while a smaller distance suggests weaker momentum. If the EMA of the MAVR moves further away from the zero line, it indicates that the price movement is becoming more robust relative to the market's volatility.

Look for potential entry and exit signals: When the EMA of the MAVR crosses the zero line, it could provide a potential trading signal. For instance, a cross from below to above the zero line may indicate a potential buying opportunity, while a cross from above to below the zero line may signal a potential selling opportunity. Keep in mind that the MAVR indicator should not be used in isolation, and it's essential to combine it with other technical analysis tools and risk management techniques.

Monitor for divergences: Sometimes, the price and the EMA of the MAVR can show divergences. For example, if the price makes a higher high while the EMA of the MAVR makes a lower high, it could signal a bearish divergence, suggesting a potential trend reversal. Similarly, if the price makes a lower low while the EMA of the MAVR makes a higher low, it could indicate a bullish divergence, suggesting a possible trend reversal.

Remember that no indicator is perfect, and the MAVR should be used in conjunction with other technical analysis tools and a solid trading strategy to increase the chances of success. Always use proper risk management techniques to protect your capital.

BullBarbies MoRoll v1.0If you like the TTM Squeeze histogram, this may be your favorite new indicator.

5 customizable timeframe MACD-based oscillators are programmed to give you a heads-up when momentum is rolling over and changing to a new direction by using lower timeframes as a "heads-up" of a potential change. Designed to be used on the 5 minute chart, but can be adapted for higher timeframes as well. Not recommended for charts under 5 minutes. Settings default to those recommended for a 5 in chart: 5, 4, 3, 2, & 1 min oscillators. If using on a higher timeframe, consider starting with the current timeframe and stepping each down from there. Lower timeframe oscillators will begin to roll first. Most multi-timeframe indicators keep watch for conditions on higher timeframes, this one is designed to give you a leg-up in seeing what's happening underneath the price action and squeezes by taking a peak at lower timeframes. Designed to be faster to help you make intra-day day trading decisions.

When all 5 indicators are in color agreement (all red or all green), this indicates strong directional momentum. To catch a shift in momentum, watch for colors to begin shifting red to green or green to red. When you can catch these shifts at support and resistance, it can make for a higher probability trade than trading just support and resistance. The more oscillators in agreement, the more confidence you can have that you are on the right side of the trade.

Pay attention to relative distance from the zero line as well. A trend day will have oscillators spending most of their time to one side or the other of the zero line. Oscillators change colors at the zero line for visual aid. Extremely high or low readings can indicate oversold or overbought conditions.

When the lines are a tangled mess of red and green, this indicates choppy conditions when many daytraders like to avoid.

Works well paired with the TTM squeeze for a more detailed look at your current timeframe.

This indicator has several features:

* 5 Timeframe oscillators that display as lines

* A zero line to show relative distance from the midpoint

* 4 color settings: rising above/below zero; falling above/below zero

I built this indicator because I love using the TTM Squeeze histogram on multiple timeframes to aid in predicting the loss and gain of momentum, but do not want to dedicate the monitor space to 5 charts just for the squeeze histogram. Plotting the histogram as lines allows the display of multiple timeframes. It has become standard on my intraday trading charts.

WVF - OscillatorAnother attempt on making use of CM-Williams-Vix-Fix-Finds-Market-Bottoms from Chris Moody - which is arguably one of the best indicator available on pine and tradingview platform. Every time I revisit this, I get new ideas on applying this method.

I have slightly altered formula to

highest(source)-source/highest(source)

from the original formula

highest(close)-low/highest(close)

Process is simple:

Calculate WVF for OHLC values separately

Calculate momentum on each of the WVF values based on distance from moving average

Plot the candles based on OHLC momentum.

Candle color depends on whether close, open and previous close. If close is higher than open and previous close, we get green coloured candles. If close is lower than previous close and open then we get red coloured candles. In all other cases, we will have silver candles.

High/Low bands are calculated based on median of highest and lowest values of VixFix. We also plot median of close which can be used in some cases.

How to use this to find market bottom. Look for one of the below conditions:

First red candle above high band - which signals momentum of vix fix is about to fall.

First red candle above median line - can be used only if upward momentum of wvf candles are trending well.

Crossunder of wvf candles under high band.

Possible exit scenarios

Green WVF candle formed above WVF high line

Entry is taken on first red candle above median line - but, candles turned green before WVF crossing under median line - may signal our thesis is wrong and price may drop further.

Some examples.

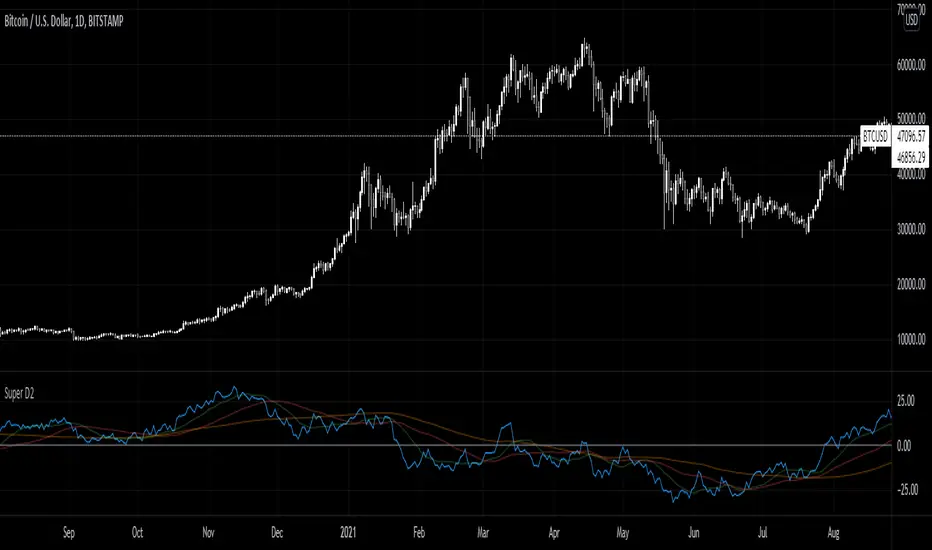

Super D2Momentum Indicator based on previous candle structure over past 40 periods

- Blue is momentum score

- Green = 15 ema

- Red = 50 sma

- orange = 100 sma

The indicator looks at the previous candles differences between open, close, high, and low to determine momentum. A high close relative to open or low indicates very strong momentum for example.

MDX Free Version (MA)This is a free version of the MDX Crypto trading "bot". Note that this indicator and the MDX version are based on simple code available on trading view or via google search.

This indicator is using two exponential moving averages. One average is set over 21 bars (fast) and the other is set over 55 bars (slow). When the plots intersect it represents a change in momentum. MDX refers to this as a confirmation.

Also shown on the chart is the "Super Trend" indicator. This is the red and green line with inflection points highlighted by a red or green arrow. These points are changes in uptrends and downtrends. MDX refers to this as a "long buy" when green, and a "short sell" when red. Commonly these are buy/sell signals. When a buysignal (green arrow) occurs followed by a change in momentum toward a downtrend, MDX refers to this as a "confirmed buy". When a sell signal (red arrow) occurs followed by a change in momentum toward a downtrend, MDX refers to this as a "confirmed sell". This can been seen more clearly on the MDS Crypto Free Version (PA) indicator which is also available. This uses the same information as the MA indicator, but formatted for the candle chart.

Usage:

Caution this indicator is not reliable on its own, especially on low time scales. When looking back in time this indicator will almost always show a "confirmed buy" before a large increase in price, but on many occasions you can have a "confirmed buy" which is followed by a dump in price, that will not trigger sell signal in time.

Vol%MAThis study finds buying/selling opportunities on the basis of candlestick and volume percentage changes, prequalified by momentum.

Candlestick percentage changes that are equal to or greater the desired percentage with the momentum range are marked by blue diamonds.

Volume percentage changes that are equal to or greater the desired percentage with the momentum range are marked by red circles.

When candlestick and volume percentage changes aligned with user configurations are under momentum, a buy signal is triggered with BUY ASSET and a black triangle is placed at the bottom of the chart.

When candlestick and volume percentage changes aligned with user configurations are above momentum, a sell signal is triggered with SELL ASSET and a black triangle is placed at the top of the chart.

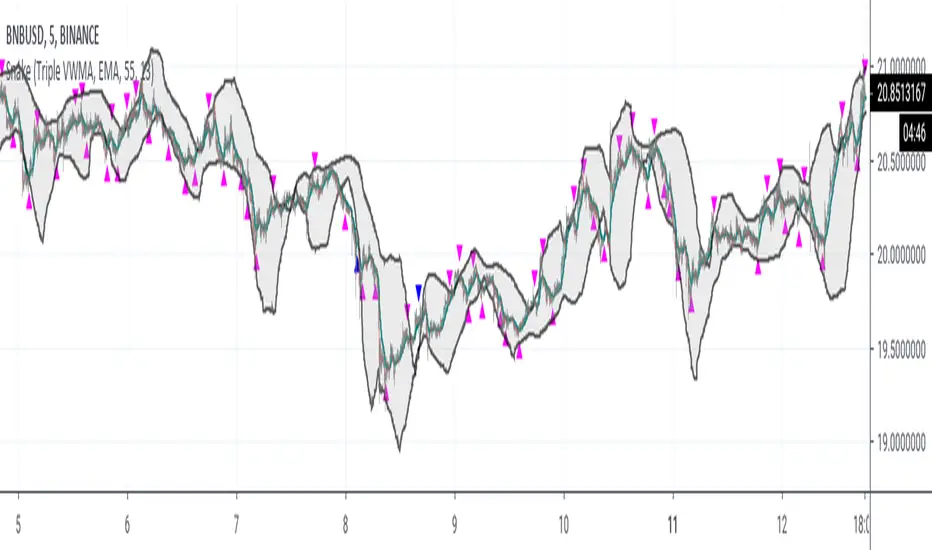

SnakeWhile moving averages are a good way to visualize price action, they are, in general, very poor indicators to trade against. Usually, the lowest prices occur before the cross over of multiple moving averages, while the best profits occur just before the crossunders of the moving averages.

This study captures the buy signals before the cross overs and sells just prior to the cross unders, when prices are lowest and highest respectively.

This is accomplished by treating the moving average as a "snake", specifically looking for the "head" of the snake to turn upwards when buying is most opportunistic. Note the the body must still be trending downward.

For selling, the "snake's head" must be turning down while the body is trending up.

This script uses blue arrows, pointing up, at the bottom, to indicate a buy signal, sending an alert of BUY ASSET.

Blue arrows, point down, at the top, represent sell signals with an alert of SELL ASSET.

The gray bar or strip is momentum. The snake's head must be above momentum for a sell, and below for a buy. This study does NOT work well with stable coins.

The longer the momentum, the more likely weak signals will be weeded out, but also presents less opportunities for buys.

The longer the length of the snake, the more likely cascading down turns will be ignored, but requires a longer trend to identify buy signals.

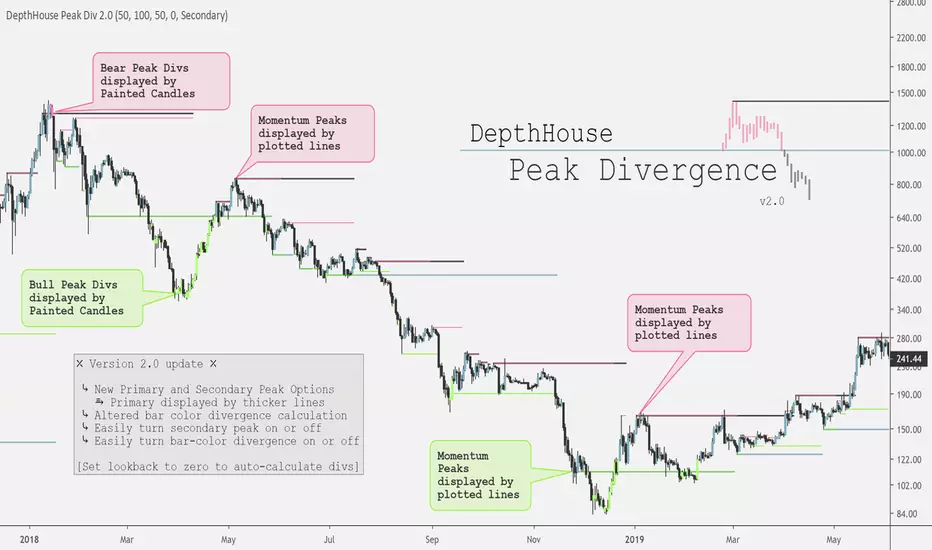

DepthHouse - Peak DivergenceDepthHouse - Peak Divergence indicator uses the same linear regression calculation as my Peak Momentum Oscillator to help determine and plot peak momentum points.

These peak levels are then plotted by either red or green lines above or below the candle.

Red lines represent a peak in bear momentum while green represents peaks in bull momentum.

These levels are then used to determine momentum divergence in the displayed market.

If divergence is present the bars colors will change represent either bull or bear div.

Important Notes:

If the price crosses a peak line and the bar color does not change; it means momentum has increased/decreased with the price and the divergence has been canceled.

If divergence is present, and then the following candle is not colored then momentum has increased to cancel the previously present divergence.

By default, the look-back period is set to zero , which automatically calculates the distance for the peak levels to look-back. However this number can be set to whatever look-back period you would like.

At time of release this indicator is in its early stages. So please leave feedback on how it can be improved!

RSI Regime: Continuation vs Reversal Indicator Description: RSI Regime (Continuation vs. Reversal)

This indicator uses the standard Relative Strength Index (RSI) to analyze market momentum and categorize it into three "regimes." Its primary goal is to help you determine if an overbought (OB) or oversold (OS) signal is likely to be a continuation of the current trend or a reversal point.

It also identifies "Fast Trend Starts," which are exceptionally fast and powerful moves from one extreme to the other.

Core Features & How to Read It

1. The Three RSI Regimes (Background Color) The script calculates a moving average (SMA) of the RSI to determine the dominant medium-term momentum. This is shown as the background color:

Bull Regime (Green Background): The RSI's average is high (e.g., above 55). The market is in a clear uptrend.

Bear Regime (Red Background): The RSI's average is low (e.g., below 45). The market is in a clear downtrend.

Range Regime (Orange Background): The RSI's average is in the middle. The market is consolidating or undecided.

2. Overbought (OB) & Oversold (OS) Signals

When the RSI line crosses into the overbought (e.g., >70) or oversold (e.g., <30) zones, the indicator generates one of two types of signals:

A) Continuation Signals (Small Triangles: ►)

These signals suggest an OB/OS reading is just a "pause" and the main trend will likely continue.

Orange ► (at the top): Appears when RSI becomes overbought while the market is already in a Bull Regime. This suggests the uptrend is strong, and this OB signal may not lead to a big drop.

Teal ► (at the bottom): Appears when RSI becomes oversold while the market is already in a Bear Regime. This suggests the downtrend is strong, and this OS signal may not lead to a big bounce.

(Note: An optional Price EMA filter can be enabled to make these signals more strict.)

B) Reversal Signals (Small Labels: "OS→>50" / "OB→<50")

These labels appear after an OB/OS signal to confirm that a reversal has actually occurred.

"OS→>50 Reversal" (Aqua Label): Appears if the RSI becomes oversold and then recovers back above the 50 midline within a set number of bars. This confirms the oversold dip was a reversal point.

"OB→<50 Reversal" (Orange Label): Appears if the RSI becomes overbought and then falls back below the 50 midline within a set number of bars. This confirms the overbought peak was a reversal point.

3. "Fast Trend Starts" (Large Labels)

This is a unique feature that identifies the fastest percentile of market moves. It measures how many bars it takes for the RSI to go from one extreme to the other and flags when a move is in the top 5% (default) of all historical moves.

"Long Pullbacks (Fast OS→BullRange)" (Large Green Label): This powerful signal appears when the RSI moves from oversold (<30) all the way up to the bull range (>60) exceptionally fast. It identifies a very strong, fast, and decisive bounce that could signal the start of a new uptrend.

"Short Pumps (Fast OB→BearRange)" (Large Red Label): This appears when the RSI moves from overbought (>70) all the way down to the bear range (<40) exceptionally fast. It identifies a very sharp, fast rejection or "pump-and-dump" that could signal the start of a new downtrend.

Key User Inputs

RSI Length (14): The lookback period for the main RSI calculation.

OB (70) / OS (30): The standard overbought and oversold levels.

Bull/Bear Range Threshold (60/40): These are the levels used to confirm the "Fast Trend Starts." They are separate from the OB/OS levels.

RSI Regime SMA Length (21): The lookback period for the moving average that determines the background regime.

Use Price EMA filter (true): If checked, the small "Continuation" triangles will only appear if the price is also above (for bulls) or below (for bears) its own 50-period EMA.

Fastest X% duration (5.0): This sets the percentile for the "Fast Trend Start" labels. 5.0 means it only flags moves that are in the fastest 5% of all recorded moves.

GMO The GMO is a multi-component confluence oscillator that helps traders visualise when several momentum and trend conditions align.

It blends an EMA trend filter, RSI bias, MACD histogram direction, and Stochastic RSI crossovers, with the option to add Fibonacci retracement proximity for additional confidence.

When multiple conditions agree, combined visual markers (triangle + emoji) appear above or below price, and background shading reflects bullish or bearish momentum. Supporting plots display MACD histogram bars, RSI, Stochastic RSI lines, and the chosen Fibonacci level, allowing quick confirmation at a glance.

This tool is best used as part of a broader confluence-based strategy and should be paired with independent analysis and risk management.