Reversal & Breakout Strategy with ORB### Reversal & Breakout Strategy with ORB

This strategy combines three distinct trading approaches—reversals, trend breakouts, and opening range breakouts (ORB)—into a single, cohesive system. The goal is to capture high-probability setups across different market conditions, leveraging a mashup of technical indicators for confirmation and risk management. Below, I’ll explain why this combination works, how the components interact, and how to use it effectively.

#### Why the Mashup?

- **Reversals**: Identifies overextended moves using RSI (overbought/oversold) and SMA50 crosses, filtered by VWAP and SMA200 trend direction. This targets mean-reversion opportunities in trending markets.

- **Breakouts**: Uses EMA9/EMA20 crossovers with VWAP and SMA200 confirmation to catch momentum-driven trend continuations.

- **Opening Range Breakout (ORB)**: Detects early momentum by breaking the high/low of a user-defined opening range (default: 15 bars) with volume confirmation. This adds a time-based edge, ideal for intraday trading.

The synergy comes from blending these methods: reversals catch pullbacks, breakouts ride trends, and ORB exploits early volatility—all filtered by trend (SMA200) and anchored by VWAP for context.

#### How It Works

1. **Indicators**:

- **EMA9/EMA20**: Fast-moving averages for breakout signals.

- **SMA50**: Medium-term trend filter for reversals.

- **SMA200**: Long-term trend direction to align trades.

- **RSI (14)**: Measures overbought (>70) or oversold (<30) conditions.

- **VWAP**: Acts as a dynamic support/resistance level.

- **ATR (14)**: Sets stop-loss distance (default: 1.5x ATR).

- **Volume**: Confirms ORB breakouts (1.5x average volume of opening range).

2. **Entry Conditions**:

- **Long**: Triggers on reversal (SMA50 cross + RSI < 30 + below VWAP + uptrend), breakout (EMA9 > EMA20 + above VWAP + uptrend), or ORB (break above opening range high + volume).

- **Short**: Triggers on reversal (SMA50 cross + RSI > 70 + above VWAP + downtrend), breakout (EMA9 < EMA20 + below VWAP + downtrend), or ORB (break below opening range low + volume).

3. **Risk Management**:

- Risks 5% of equity per trade (based on the initial capital set in the strategy tester).

- Stop-loss: Based on lowest low/highest high over 7 bars ± 1.5x ATR.

- Targets: Two exits at 1:1 and 1:2 risk:reward (50% of position at each).

- Break-even: Stop moves to entry price after the first target is hit.

4. **Backtesting Settings**:

- Commission: Hardcoded at 0.1% per trade (realistic for most brokers).

- Slippage: Hardcoded at 2 ticks (realistic for most markets).

- Tested on datasets yielding 100+ trades (e.g., 2-min or 5-min charts over months).

#### How to Use It

- **Timeframe**: Works best on intraday (2-min, 5-min) or daily charts. Adjust `Opening Range Bars` (e.g., 15 bars = 30 min on 2-min chart) for your timeframe.

- **Settings**:

- Set your initial equity in the TradingView strategy tester’s "Properties" tab under "Initial Capital" (e.g., $10,000). The script automatically risks 5% of this equity per trade.

- Adjust `Stop Loss ATR Multiplier` or `Risk:Reward Targets` based on your risk tolerance.

- Note that commission (0.1%) and slippage (2 ticks) are fixed in the script for backtesting consistency.

- **Execution**: Enter on signal, monitor plotted stop (red) and targets (green/blue). The strategy supports pyramiding (up to 2 positions) for scaling into trends.

#### Backtesting Notes

Results are realistic with commission (0.1%) and slippage (2 ticks) included. For a sufficient sample, test on volatile instruments (e.g., stocks, forex) over 3-6 months on lower timeframes. The default 1.5x ATR stop may seem wide, but it’s justified to avoid premature exits in volatile markets—feel free to tweak it with justification. The script assumes an initial capital of $10,000 in the strategy tester for the 5% risk calculation (e.g., $500 risk per trade); adjust this in the "Properties" tab as needed.

This mashup isn’t just a random mix; it’s a deliberate fusion of complementary strategies, offering traders flexibility across market phases. Questions? Let me know!

Cari dalam skrip untuk "momentum"

DrNon Action Zone📈 Strategy Title:

DrNon Action Zone — EMA Cross with ATR Stop, % Take-Profit, Alerts & Date Range

⸻

🧠 Strategy Concept:

DrNon Action Zone is a long-only trend-following strategy that enters trades when momentum aligns with long-term trend confirmation. It uses:

• EMA Cross (Fast vs. Slow) to identify momentum shift

• Optional EMA Filter based on days to confirm that price is in a “trend zone”

• ATR-based trailing stop for adaptive risk management

• Percentage Take-Profit for reward targeting

• Date Range Filter for focused backtesting or event-based execution

It also includes alerts, visual signals, and full customization via inputs.

⸻

⚙️ Strategy Inputs Explained:

Input Name Description

Fast EMA Length Period of the short-term EMA used for crossover signals (default: 5)

Slow EMA Length Period of the long-term EMA used for crossover signals (default: 200)

ATR Period Period used to calculate the Average True Range (ATR)

ATR Multiplier Multiplies ATR value to calculate the trailing stop distance

Take-Profit % Percentage above entry price to exit the trade for profit

Use EMA Filter? If enabled, long entries require price to be above a customizable EMA filter

EMA Filter Days Number of days used for EMA filter (converted to bars based on chart timeframe)

Use Date Range? Enable or disable the date filter

Start Date / End Date Specify a custom range to apply the strategy

⸻

✅ Long Entry Conditions (The Action Zone):

A long trade is entered when:

1. EMA(Fast) crosses above EMA(Slow)

2. If EMA Filter is enabled, Close > EMA(Filter Days)

3. If Date Filter is enabled, current candle is within specified start and end dates

⸻

❌ Exit Conditions:

The strategy will close the position when either:

• Price drops to ATR-based trailing stop, OR

• Price reaches the Take-Profit % target

⸻

🛎️ Alerts:

Alert Name Trigger Condition

Long Entry Alert EMA cross and all filters passed (entry signal triggered)

Exit Alert Price hit ATR Stop or Take-Profit (exit signal triggered)

⸻

📊 Visual Elements:

• Yellow Line — Fast EMA

• Blue Line — Slow EMA

• Purple Line — EMA Filter (based on user-defined days)

• Red Line — ATR-based Trailing Stop

• Lime Line — Take-Profit Level

• Green Triangle — Long Entry Signal (on crossover)

⸻

🧪 Backtesting Tips:

• Adjust EMA Filter Days to simulate different trend conditions (e.g., 100d, 150d, 200d).

• Use ATR Multiplier to adapt the stop-loss to market volatility.

• Combine date filtering with known events (e.g., earnings, FOMC meetings).

• Test in multiple timeframes — 1H, 4H, or Daily for stronger signals.

Trend Hunter Scalping [Daddin Algo]Trend Hunter Scalping Strategy Description

This strategy is a comprehensive scalping system designed to capture high-frequency trading opportunities within short timeframes. It combines multiple technical indicators to assess trend direction, momentum, volatility, and volume dynamics. Importantly, all parameters are user-adjustable, allowing the strategy to be optimized for various market conditions and individual preferences.

Technical Indicators and Settings

EMA (Exponential Moving Average):

The EMA is calculated based on a user-defined period. Rather than being fixed (e.g., a 200-period EMA), the period is adjustable to suit different market conditions. The position of the price relative to the EMA helps confirm the overall trend.

RSI & RSIOver:

The Relative Strength Index (RSI) measures momentum and the speed of price changes. Entry signals are generated when the RSI crosses its moving average. Additionally, overbought and oversold thresholds (set by the user) add an extra layer of confirmation for the signals.

ADX:

The Average Directional Index (ADX) assesses the strength of the current trend. When the ADX is above a user-specified threshold, the signals are considered more reliable. This helps in filtering out signals during weak trending periods.

Bollinger Bands:

Bollinger Bands gauge market volatility. The settings—including the length and the multiplier—are adjustable, providing flexibility to accommodate tightening or expanding volatility conditions.

Parabolic SAR:

This indicator identifies dynamic support and resistance levels, confirming the trend direction and helping pinpoint potential entry and exit points.

Pivot Levels (Fibonacci):

Calculated from the previous period's high, low, and close, pivot points and Fibonacci levels indicate potential reversal points and serve as support and resistance levels. These levels provide context for setting trailing stops and managing risk.

Volume Filter:

A volume condition ensures that trading signals are only considered valid when the current volume exceeds a multiple of its short-term moving average. This filter is adjustable, helping to confirm the strength of the market move.

Daddin Line:

Derived from a short-term moving average of the closing prices with a user-defined offset, the Daddin Line acts as an additional confirmation tool. Its parameters can be customized to better align with specific trading environments.

Trading Logic and Management

Signal Direction and Entry:

The strategy can generate both long (buy) and short (sell) signals, or be limited to one direction based on user preference. Entry orders are executed when all the selected indicator conditions are met. Additionally, maximum consecutive trade limits are implemented to help control risk.

Exit & Take Profit:

Trades are exited automatically when a user-defined profit percentage is reached. This take-profit percentage is flexible, enabling adjustments to match different market conditions or trading goals.

Trailing Stop (Dynamic Stop Loss):

A trailing stop mechanism is implemented using Fibonacci pivot levels. Once a position is open, the stop loss is dynamically updated as the price moves favorably. This ensures that profits are protected while minimizing losses in case of a sudden reversal.

Additional Features and Backtesting

Time Filtering (Backtesting):

The strategy includes a date range filter for backtesting. Users can define the start and end dates to evaluate the strategy’s performance during specific market periods, making it easier to assess its historical effectiveness.

Customizable Parameters:

Every indicator and risk management setting is fully customizable. This adaptability allows traders to tailor the strategy to different assets, timeframes, and market environments, ensuring optimal performance across diverse trading scenarios.

Conclusion

The Trend Hunter Scalping strategy effectively integrates multiple technical indicators to validate trends and manage risks efficiently. Its highly flexible, user-adjustable parameters make it adaptable to varying market conditions, providing traders with a robust framework for capturing quick trading opportunities.This strategy is designed to optimize both entry and exit points while offering comprehensive risk management controls.

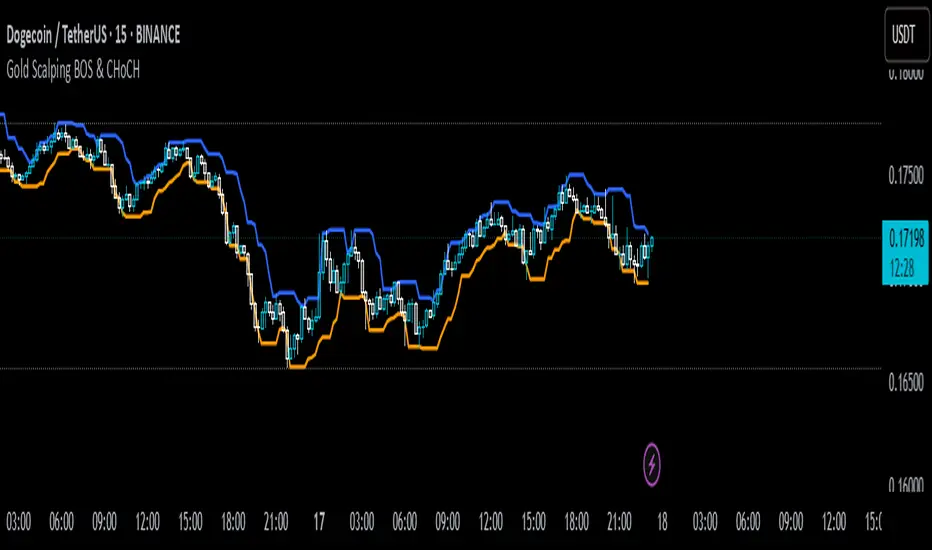

Gold Scalping BOS & CHoCHThis strategy is designed for scalping gold (XAU/USD) on the 3-minute timeframe, utilizing Break of Structure (BOS) and Change of Character (CHoCH) to identify high-probability trade setups. Unlike traditional SMA crossover strategies, this method focuses purely on price action and market structure shifts, allowing for early entries and better risk management.

Core Concepts:

Break of Structure (BOS) – Confirms a continuation of the trend when price breaks the last swing high (bullish) or last swing low (bearish).

Change of Character (CHoCH) – Detects possible trend reversals by identifying a shift in market momentum.

Dynamic Support & Resistance – Uses the last 10-bar highs and lows to determine adaptive stop-loss (SL) and take-profit (TP) levels.

Risk-to-Reward Ratio (1:2 RR) – Ensures trades are executed with a favorable risk/reward ratio.

Entry Conditions:

Buy Entry:

BOS (Bullish) confirmed (price breaks the previous swing high).

CHoCH (Bullish) confirms trend shift.

Price crosses back above the last swing low (confirmation of support).

Sell Entry:

BOS (Bearish) confirmed (price breaks the previous swing low).

CHoCH (Bearish) confirms trend shift.

Price crosses back below the last swing high (confirmation of resistance).

Exit Conditions:

Stop Loss (SL): Set at the most recent dynamic support (for buys) or resistance (for sells).

Take Profit (TP): 2x the risk (1:2 risk-reward ratio).

Advantages of This Strategy:

✅ No lagging indicators – Uses price action for real-time entries.

✅ High probability setups – Focuses only on strong structural breaks.

✅ Adaptive SL/TP – Uses real market structure instead of fixed values.

✅ Optimized for Scalping – Best suited for quick in-and-out trades.

Best Time to Trade:

🔹 London & New York Sessions (High volatility for gold).

Heiken Ashi Supertrend ATR-SL StrategyThis indicator combines Heikin Ashi candle pattern analysis with Supertrend to generate high-probability trading signals with built-in risk management. It identifies potential entries and exits based on specific Heikin Ashi candlestick formations while providing automated ATR-based stop loss management.

Trading Logic:

The system generates long signals when a green Heikin Ashi candle forms with no bottom wick (indicating strong bullish momentum). Short signals appear when a red Heikin Ashi candle forms with no top wick (showing strong bearish momentum). The absence of wicks on these candles signals a high-conviction market move in the respective direction.

Exit signals are triggered when:

1. An opposite pattern forms (red candle with no top wick exits longs; green candle with no bottom wick exits shorts)

2. The ATR-based stop loss is hit

3. The break-even stop is activated and then hit

Technical Approach:

- Select Heiken Ashi Canldes on your Trading View chart. Entried are based on HA prices.

- Supertrend and ATR-based stop losses use real price data (not HA values) for trend determination

- ATR-based stop losses automatically adjust to market volatility

- Break-even functionality moves the stop to entry price once price moves a specified ATR multiple in your favor

Risk Management:

- Default starting capital: 1000 units

- Default risk per trade: 10% of equity (customizable in strategy settings)

- Hard Stop Loss: Set ATR multiplier (default: 2.0) for automatic stop placement

- Break Even: Configure ATR threshold (default: 1.0) to activate break-even stops

- Appropriate position sizing relative to equity and stop distance

Customization Options:

- Supertrend Settings:

- Enable/disable Supertrend filtering (trade only in confirmed trend direction)

- Adjust Factor (default: 3.0) to change sensitivity

- Modify ATR Period (default: 10) to adapt to different timeframes

Visual Elements:

- Green triangles for long entries, blue triangles for short entries

- X-marks for exits and stop loss hits

- Color-coded position background (green for long, blue for short)

- Clearly visible stop loss lines (red for hard stop, white for break-even)

- Comprehensive position information label with entry price and stop details

Implementation Notes:

The indicator tracks positions internally and maintains state across bars to properly manage stop levels. All calculations use confirmed bars only, with no repainting or lookahead bias. The system is designed for swing trading on timeframes from 1-hour and above, where Heikin Ashi patterns tend to be more reliable.

This indicator is best suited for traders looking to combine the pattern recognition strengths of Heikin Ashi candles with the trend-following capabilities of Supertrend, all while maintaining disciplined risk management through automated stops.

Advanced Adaptive Grid Trading StrategyThis strategy employs an advanced grid trading approach that dynamically adapts to market conditions, including trend, volatility, and risk management considerations. The strategy aims to capitalize on price fluctuations in both rising (long) and falling (short) markets, as well as during sideways movements. It combines multiple indicators to determine the trend and automatically adjusts grid parameters for more efficient trading.

How it Works:

Trend Analysis:

Short, long, and super long Moving Averages (MA) to determine the trend direction.

RSI (Relative Strength Index) to identify overbought and oversold levels, and to confirm the trend.

MACD (Moving Average Convergence Divergence) to confirm momentum and trend direction.

Momentum indicator.

The strategy uses a weighted scoring system to assess trend strength (strong bullish, moderate bullish, strong bearish, moderate bearish, sideways).

Grid System:

The grid size (the distance between buy and sell levels) changes dynamically based on market volatility, using the ATR (Average True Range) indicator.

Grid density also adapts to the trend: in a strong trend, the grid is denser in the direction of the trend.

Grid levels are shifted depending on the trend direction (upwards in a bear market, downwards in a bull market).

Trading Logic:

The strategy opens long positions if the trend is bullish and the price reaches one of the lower grid levels.

It opens short positions if the trend is bearish and the price reaches one of the upper grid levels.

In a sideways market, it can open positions in both directions.

Risk Management:

Stop Loss for every position.

Take Profit for every position.

Trailing Stop Loss to protect profits.

Maximum daily loss limit.

Maximum number of positions limit.

Time-based exit (if the position is open for too long).

Risk-based position sizing (optional).

Input Options:

The strategy offers numerous settings that allow users to customize its operation:

Timeframe: The chart's timeframe (e.g., 1 minute, 5 minutes, 1 hour, 4 hours, 1 day, 1 week).

Base Grid Size (%): The base size of the grid, expressed as a percentage.

Max Positions: The maximum number of open positions allowed.

Use Volatility Grid: If enabled, the grid size changes dynamically based on the ATR indicator.

ATR Length: The period of the ATR indicator.

ATR Multiplier: The multiplier for the ATR to fine-tune the grid size.

RSI Length: The period of the RSI indicator.

RSI Overbought: The overbought level for the RSI.

RSI Oversold: The oversold level for the RSI.

Short MA Length: The period of the short moving average.

Long MA Length: The period of the long moving average.

Super Long MA Length: The period of the super long moving average.

MACD Fast Length: The fast period of the MACD.

MACD Slow Length: The slow period of the MACD.

MACD Signal Length: The period of the MACD signal line.

Stop Loss (%): The stop loss level, expressed as a percentage.

Take Profit (%): The take profit level, expressed as a percentage.

Use Trailing Stop: If enabled, the strategy uses a trailing stop loss.

Trailing Stop (%): The trailing stop loss level, expressed as a percentage.

Max Loss Per Day (%): The maximum daily loss, expressed as a percentage.

Time Based Exit: If enabled, the strategy exits the position after a certain amount of time.

Max Holding Period (hours): The maximum holding time in hours.

Use Risk Based Position: If enabled, the strategy calculates position size based on risk.

Risk Per Trade (%): The risk per trade, expressed as a percentage.

Max Leverage: The maximum leverage.

Important Notes:

This strategy does not guarantee profits. Cryptocurrency markets are volatile, and trading involves risk.

The strategy's effectiveness depends on market conditions and settings.

It is recommended to thoroughly backtest the strategy under various market conditions before using it live.

Past performance is not indicative of future results.

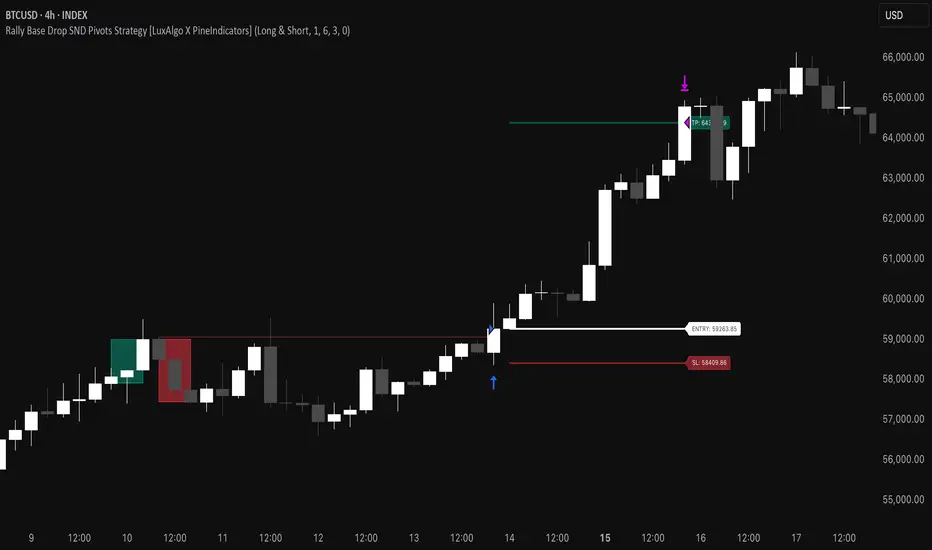

Rally Base Drop SND Pivots Strategy [LuxAlgo X PineIndicators]This strategy is based on the Rally Base Drop (RBD) SND Pivots indicator developed by LuxAlgo. Full credit for the concept and original indicator goes to LuxAlgo.

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand trading system that detects pivot points based on Rally, Base, and Drop (RBD) candles. This strategy automatically identifies key market structure levels, allowing traders to:

Identify pivot-based supply and demand (SND) zones.

Use fixed criteria for trend continuation or reversals.

Filter out market noise by requiring structured price formations.

Enter trades based on breakouts of key SND pivot levels.

How the Rally Base Drop SND Pivots Strategy Works

1. Pivot Point Detection Using RBD Candles

The strategy follows a rigid market structure methodology, where pivots are detected only when:

A Rally (R) consists of multiple consecutive bullish candles.

A Drop (D) consists of multiple consecutive bearish candles.

A Base (B) is identified as a transition between Rallies and Drops, acting as a pivot point.

The pivot level is confirmed when the formation is complete.

Unlike traditional fractal-based pivots, RBD Pivots enforce stricter structural rules, ensuring that each pivot:

Has a well-defined bullish or bearish price movement.

Reduces false signals caused by single-bar fluctuations.

Provides clear supply and demand levels based on structured price movements.

These pivot levels are drawn on the chart using color-coded boxes:

Green zones represent bullish pivot levels (Rally Base formations).

Red zones represent bearish pivot levels (Drop Base formations).

Once a pivot is confirmed, the high or low of the base candle is used as the reference level for future trades.

2. Trade Entry Conditions

The strategy allows traders to select from three trading modes:

Long Only – Only takes long trades when bullish pivot breakouts occur.

Short Only – Only takes short trades when bearish pivot breakouts occur.

Long & Short – Trades in both directions based on pivot breakouts.

Trade entry signals are triggered when price breaks through a confirmed pivot level:

Long Entry:

A bullish pivot level is formed.

Price breaks above the bullish pivot level.

The strategy enters a long position.

Short Entry:

A bearish pivot level is formed.

Price breaks below the bearish pivot level.

The strategy enters a short position.

The strategy includes an optional mode to reverse long and short conditions, allowing traders to experiment with contrarian entries.

3. Exit Conditions Using ATR-Based Risk Management

This strategy uses the Average True Range (ATR) to calculate dynamic stop-loss and take-profit levels:

Stop-Loss (SL): Placed 1 ATR below entry for long trades and 1 ATR above entry for short trades.

Take-Profit (TP): Set using a Risk-Reward Ratio (RR) multiplier (default = 6x ATR).

When a trade is opened:

The entry price is recorded.

ATR is calculated at the time of entry to determine stop-loss and take-profit levels.

Trades exit automatically when either SL or TP is reached.

If reverse conditions mode is enabled, stop-loss and take-profit placements are flipped.

Visualization & Dynamic Support/Resistance Levels

1. Pivot Boxes for Market Structure

Each pivot is marked with a colored box:

Green boxes indicate bullish demand zones.

Red boxes indicate bearish supply zones.

These boxes remain on the chart to act as dynamic support and resistance levels, helping traders identify key price reaction zones.

2. Horizontal Entry, Stop-Loss, and Take-Profit Lines

When a trade is active, the strategy plots:

White line → Entry price.

Red line → Stop-loss level.

Green line → Take-profit level.

Labels display the exact entry, SL, and TP values, updating dynamically as price moves.

Customization Options

This strategy offers multiple adjustable settings to optimize performance for different market conditions:

Trade Mode Selection → Choose between Long Only, Short Only, or Long & Short.

Pivot Length → Defines the number of required Rally & Drop candles for a pivot.

ATR Exit Multiplier → Adjusts stop-loss distance based on ATR.

Risk-Reward Ratio (RR) → Modifies take-profit level relative to risk.

Historical Lookback → Limits how far back pivot zones are displayed.

Color Settings → Customize pivot box colors for bullish and bearish setups.

Considerations & Limitations

Pivot Breakouts Do Not Guarantee Reversals. Some pivot breaks may lead to continuation moves instead of trend reversals.

Not Optimized for Low Volatility Conditions. This strategy works best in trending markets with strong momentum.

ATR-Based Stop-Loss & Take-Profit May Require Optimization. Different assets may require different ATR multipliers and RR settings.

Market Noise May Still Influence Pivots. While this method filters some noise, fake breakouts can still occur.

Conclusion

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand system that combines:

Pivot-based market structure analysis (using Rally, Base, and Drop candles).

Breakout-based trade entries at confirmed SND levels.

ATR-based dynamic risk management for stop-loss and take-profit calculation.

This strategy helps traders:

Identify high-probability supply and demand levels.

Trade based on structured market pivots.

Use a systematic approach to price action analysis.

Automatically manage risk with ATR-based exits.

The strict pivot detection rules and built-in breakout validation make this strategy ideal for traders looking to:

Trade based on market structure.

Use defined support & resistance levels.

Reduce noise compared to traditional fractals.

Implement a structured supply & demand trading model.

This strategy is fully customizable, allowing traders to adjust parameters to fit their market and trading style.

Full credit for the original concept and indicator goes to LuxAlgo.

Optimized Auto-Detect Strategy (MA, ATR, Trend, RSI) Overview

This script is designed for traders seeking a trend-following approach that adapts to different currency pairs (e.g., EURUSD, NZDUSD, XAUUSD). It combines moving average crossovers with ATR-based stops, optional trend filters, and RSI filters to help reduce false signals and capture larger moves.

Key Features

1. Auto-Detect Logic

- Automatically applies different moving average periods and ATR multipliers based on the symbol (e.g., XAUUSD, EURUSD, NZDUSD).

- Makes it easy to switch charts without manually adjusting parameters each time.

2. ATR-Based Stop

- Uses the Average True Range (ATR) to set dynamic stop-loss levels, adapting to each market’s volatility.

3. Optional Trend Filter

- Filters out trades if price is below the 200 SMA for longs (and above for shorts), aiming to avoid choppy, range-bound markets.

4. Optional RSI Filter

- Only enters long if RSI is above a certain threshold (e.g., 50), or short if below another threshold, reducing entries during low momentum.

5. Partial Exit & Trailing/Break-Even

- Locks in partial profit at a chosen R:R (e.g., 1:1), then either trails the remaining position or moves the stop to break-even.

- This helps capture additional gains if the trend extends beyond the initial target.

6. Customizable Parameters

- You can toggle on/off each filter (Trend, RSI) and adjust the ATR multiplier, MA periods, partial exit levels, etc.

- Allows easy optimization for different pairs or timeframes.

How to Use

1. Add to Chart: Click “Add to chart” in the Pine Editor.

2. Configure Inputs: In the script’s settings, toggle the filters you want (Trend Filter, RSI Filter, etc.) and set your desired ATR multiplier, RSI thresholds, partial exit ratio, etc.

3. Strategy Tester: Check the performance under the “Strategy Tester” tab. Adjust parameters if needed.

4. Realistic Settings: Consider adding spreads/commissions in the “Properties” tab for more accurate backtests, especially if you trade pairs with higher spreads (like XAUUSD).

Disclaimer

No Guarantee: This script does not guarantee profits. Markets are unpredictable, and results may vary with market conditions.

For Educational Purposes: Always do your own research and forward testing. Past performance does not indicate future results.

Strategy SuperTrend SDI WebhookThis Pine Script™ strategy is designed for automated trading in TradingView. It combines the SuperTrend indicator and Smoothed Directional Indicator (SDI) to generate buy and sell signals, with additional risk management features like stop loss, take profit, and trailing stop. The script also includes settings for leverage trading, equity-based position sizing, and webhook integration.

Key Features

1. Date-based Trade Execution

The strategy is active only between the start and end dates set by the user.

times ensures that trades occur only within this predefined time range.

2. Position Sizing and Leverage

Uses leverage trading to adjust position size dynamically based on initial equity.

The user can set leverage (leverage) and percentage of equity (usdprcnt).

The position size is calculated dynamically (initial_capital) based on account performance.

3. Take Profit, Stop Loss, and Trailing Stop

Take Profit (tp): Defines the target profit percentage.

Stop Loss (sl): Defines the maximum allowable loss per trade.

Trailing Stop (tr): Adjusts dynamically based on trade performance to lock in profits.

4. SuperTrend Indicator

SuperTrend (ta.supertrend) is used to determine the market trend.

If the price is above the SuperTrend line, it indicates an uptrend (bullish).

If the price is below the SuperTrend line, it signals a downtrend (bearish).

Plots visual indicators (green/red lines and circles) to show trend changes.

5. Smoothed Directional Indicator (SDI)

SDI helps to identify trend strength and momentum.

It calculates +DI (bullish strength) and -DI (bearish strength).

If +DI is higher than -DI, the market is considered bullish.

If -DI is higher than +DI, the market is considered bearish.

The background color changes based on the SDI signal.

6. Buy & Sell Conditions

Long Entry (Buy) Conditions:

SDI confirms an uptrend (+DI > -DI).

SuperTrend confirms an uptrend (price crosses above the SuperTrend line).

Short Entry (Sell) Conditions:

SDI confirms a downtrend (+DI < -DI).

SuperTrend confirms a downtrend (price crosses below the SuperTrend line).

Optionally, trades can be filtered using crossovers (occrs option).

7. Trade Execution and Exits

Market entries:

Long (strategy.entry("Long")) when conditions match.

Short (strategy.entry("Short")) when bearish conditions are met.

Trade exits:

Uses predefined take profit, stop loss, and trailing stop levels.

Positions are closed if the strategy is out of the valid time range.

Usage

Automated Trading Strategy:

Can be integrated with webhooks for automated execution on supported trading platforms.

Trend-Following Strategy:

Uses SuperTrend & SDI to identify trend direction and strength.

Risk-Managed Leverage Trading:

Supports position sizing, stop losses, and trailing stops.

Backtesting & Optimization:

Can be used for historical performance analysis before deploying live.

Conclusion

This strategy is suitable for traders who want to automate their trading using SuperTrend and SDI indicators. It incorporates risk management tools like stop loss, take profit, and trailing stop, making it adaptable for leverage trading. Traders can customize settings, conduct backtests, and integrate it with webhooks for real-time trade execution. 🚀

Important Note:

This script is provided for educational and template purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

Bollinger Bands by Abu ElyasBollinger Bands with Adjustable Stop Loss (Long-Only)

This strategy uses a Bollinger Band breakout approach to enter long positions and incorporates an adjustable stop loss for risk management.

Below is an overview of the logic, parameters, and usage instructions.

1. Bollinger Bands Logic

Basis (Middle Band): A moving average (type selectable by the user) of the chosen source, typically the closing price.

Upper Band: The basis plus a specified number of standard deviations (user-defined multiplier).

Lower Band: The basis minus the same number of standard deviations.

2. Entry Triggers

The strategy enters a long position when the close price rises above the upper Bollinger Band , suggesting a potential bullish breakout.

This logic is only applied within a user-specified date range (adjustable in the strategy’s inputs).

3. Exit Triggers

1. Bollinger Band Exit:

If the close price drops below the lower Bollinger Band , the strategy closes the position, indicating a loss of bullish momentum.

2. Stop Loss Exit:

A default 8% stop loss is set, which automatically exits the trade if the close falls 8% below the entry price.

This stop-loss percentage is adjustable from the strategy’s settings, allowing users to tailor risk based on their preferences.

3. Date Range:

If the current bar is outside of the specified start/end dates, the strategy will also exit any open positions.

4. Position Sizing & Other Settings

1- Position Size:

By default, the script uses 100% of account equity for each trade.

2- Commissions & Slippage:

Commission is set to 0%, and slippage is set to 3 ticks.

3- Timeframe Handling:

You can select a custom timeframe or leave it blank to use the chart’s timeframe.

5. Customization

1. Bollinger Bands Parameters:

Length of the moving average, type of moving average (SMA, EMA, etc.), and the standard deviation multiplier can be adjusted.

2. Stop Loss (%)

The default stop loss of 8% can be changed in the script’s input settings to any percentage you prefer.

3. Date Filter:

Modify the start/end dates to control the historical period over which the strategy executes trades.

6. Notes & Best Practices

1- No Short Trades:

This is a long‐only strategy. It will either be in a long position or flat (no open position).

2- Risk Management:

An 8% stop loss may or may not align with your personal risk tolerance. Always adjust according to market conditions and your own trading style.

3- Market Gaps & Volatility:

In highly volatile markets, slippage or gaps can cause the actual exit price to be worse than the intended stop-loss level.

4- Test Thoroughly:

Backtest on different timeframes and market conditions. No single strategy works in all scenarios.

7. Disclaimer

Educational Use Only: This script is for informational and illustrative purposes and should not be considered financial advice.

No Guarantee of Profit: Past performance does not guarantee future results. Trading involves substantial risk, and it is possible to lose more than your initial investment.

Consult a Professional: Always consult a qualified financial advisor before making investment decisions.

Use this script as a foundation and personalize it based on your trading style, tolerance for drawdowns, and market conditions.

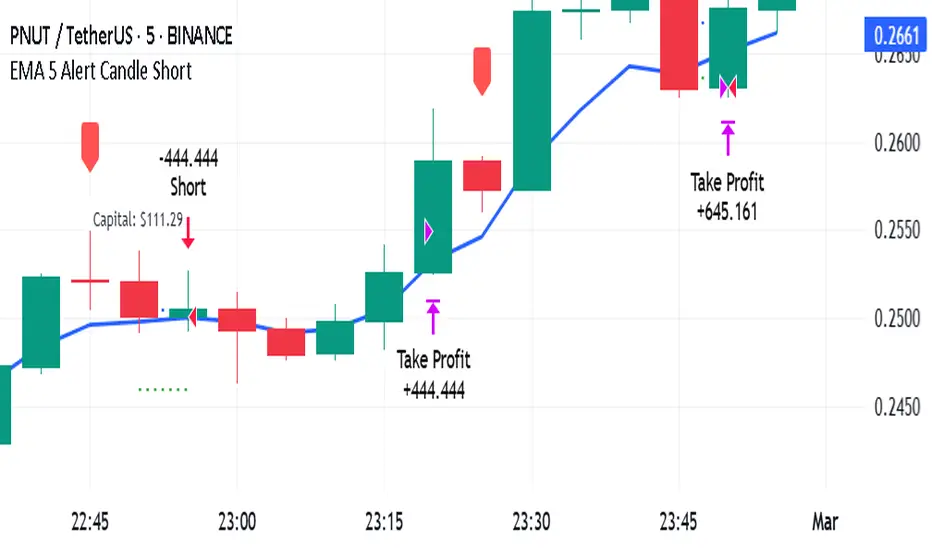

EMA 5 Alert Candle ShortThe 5 EMA (Exponential Moving Average) Strategy is a simple yet effective trading strategy that helps traders identify short-term trends and potential entry and exit points. This strategy is widely used in intraday and swing trading, particularly in forex, stocks, and crypto markets.

Components of the 5 EMA Strategy

5 EMA: A fast-moving average that reacts quickly to price movements.

15-minute or 1-hour timeframe (commonly used, but adaptable to other timeframes).

Candlestick Patterns: To confirm entry signals.

How the 5 EMA Strategy Works

Buy (Long) Setup:

Price Above the 5 EMA: The price should be trading above the 5 EMA.

Pullback to the 5 EMA: A minor retracement or consolidation near the 5 EMA.

Bullish Candlestick Confirmation: A bullish candle (e.g., engulfing or pin bar) forms near the 5 EMA.

Entry: Enter a long trade at the close of the bullish candle.

Stop Loss: Place below the recent swing low or 5-10 pips below the 5 EMA.

Take Profit: Aim for a risk-reward ratio of at least 1:2 or trail the stop using a higher EMA (e.g., 10 or 20 EMA).

Sell (Short) Setup:

Price Below the 5 EMA: The price should be trading below the 5 EMA.

Pullback to the 5 EMA: A small retracement towards the 5 EMA.

Bearish Candlestick Confirmation: A bearish candle (e.g., engulfing or pin bar) near the 5 EMA.

Entry: Enter a short trade at the close of the bearish candle.

Stop Loss: Place above the recent swing high or 5-10 pips above the 5 EMA.

Take Profit: Aim for a 1:2 risk-reward ratio or use a trailing stop.

Additional Filters for Better Accuracy

Higher Timeframe Confirmation: Check the trend on a higher timeframe (e.g., 1-hour or 4-hour).

Volume Confirmation: Enter trades when volume is increasing.

Avoid Sideways Market: Use the strategy only when the market is trending.

Advantages of the 5 EMA Strategy

✔️ Simple and easy to use.

✔️ Works well in trending markets.

✔️ Helps traders capture short-term momentum.

Disadvantages

❌ Less effective in choppy or sideways markets.

❌ Requires discipline in following stop-loss rules.

MH Strategy – Hull Moving Average-Based Trading StrategyThe MH Strategy is a TradingView strategy that leverages the Hull Moving Average (HullMA) to generate precise buy and sell signals. This strategy is designed to identify trend reversals and momentum shifts using a combination of weighted moving averages and HullMA-based calculations.

Key Features:

✅ Hull Moving Average-Based Signals – Uses a modified HullMA calculation to detect trend changes.

✅ Dynamic Support & Resistance – The strategy plots adaptive levels that act as dynamic entry and exit points.

✅ Trend-Based Entries & Exits – Generates long (buy) signals when the price moves above the calculated Hull retraction level and short (sell) signals when the price moves below it.

✅ Automated Trade Execution – Integrates with TradingView’s strategy function to open and close trades automatically based on signal conditions.

✅ Customizable Parameters – Allows users to adjust the HullMA period and price data source to optimize performance across different markets and timeframes.

How It Works:

HullMA Calculation: The strategy calculates a smoothed Hull Moving Average (HullMA) using a two-step weighted moving average method.

Trend Confirmation: The difference between the HullMA values helps determine trend direction and retraction levels.

Entry Conditions:

A buy signal is generated when the price is above the retraction level, and the previous price confirms the trend.

A sell signal is triggered when the price is below the retraction level with trend confirmation.

Exit Conditions:

The strategy closes long trades when the price drops below a threshold.

It closes short trades when the price rises above a set level.

Ideal Use Cases:

🔹 Swing & trend traders looking for momentum-based entries and exits.

🔹 Traders aiming for reduced lag compared to traditional moving averages.

🔹 Markets with strong price trends, such as forex, stocks, and crypto.

Try the MH Strategy and enhance your trading decisions with a refined HullMA-based trend detection system! 🚀

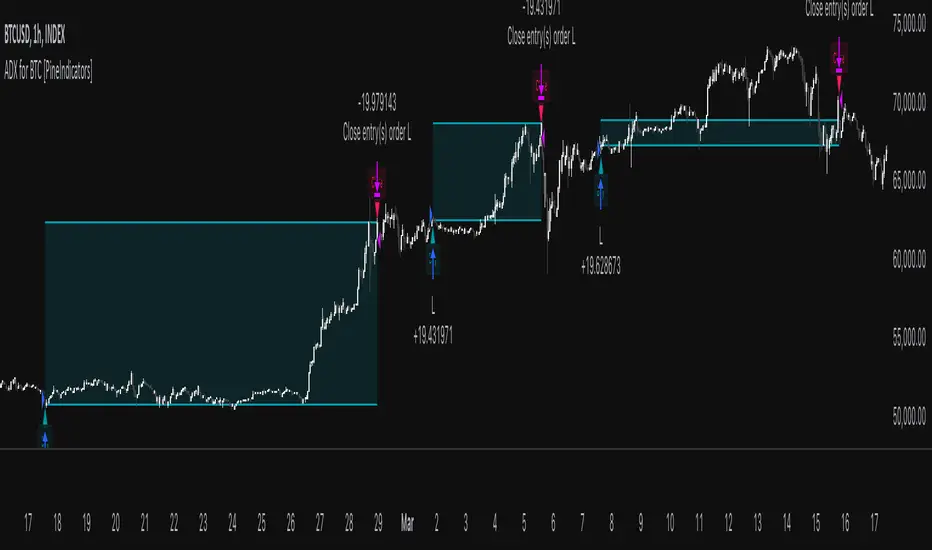

ADX for BTC [PineIndicators]The ADX Strategy for BTC is a trend-following system that uses the Average Directional Index (ADX) to determine market strength and momentum shifts. Designed for Bitcoin trading, this strategy applies a customizable ADX threshold to confirm trend signals and optionally filters entries using a Simple Moving Average (SMA). The system features automated entry and exit conditions, dynamic trade visualization, and built-in trade tracking for historical performance analysis.

⚙️ Core Strategy Components

1️⃣ Average Directional Index (ADX) Calculation

The ADX indicator measures trend strength without indicating direction. It is derived from the Positive Directional Movement (+DI) and Negative Directional Movement (-DI):

+DI (Positive Directional Index): Measures upward price movement.

-DI (Negative Directional Index): Measures downward price movement.

ADX Value: Higher values indicate stronger trends, regardless of direction.

This strategy uses a default ADX length of 14 to smooth out short-term fluctuations while detecting sustainable trends.

2️⃣ SMA Filter (Optional Trend Confirmation)

The strategy includes a 200-period SMA filter to validate trend direction before entering trades. If enabled:

✅ Long Entry is only allowed when price is above a long-term SMA multiplier (5x the standard SMA length).

✅ If disabled, the strategy only considers the ADX crossover threshold for trade entries.

This filter helps reduce entries in sideways or weak-trend conditions, improving signal reliability.

📌 Trade Logic & Conditions

🔹 Long Entry Conditions

A buy signal is triggered when:

✅ ADX crosses above the threshold (default = 14), indicating a strengthening trend.

✅ (If SMA filter is enabled) Price is above the long-term SMA multiplier.

🔻 Exit Conditions

A position is closed when:

✅ ADX crosses below the stop threshold (default = 45), signaling trend weakening.

By adjusting the entry and exit ADX levels, traders can fine-tune sensitivity to trend changes.

📏 Trade Visualization & Tracking

Trade Markers

"Buy" label (▲) appears when a long position is opened.

"Close" label (▼) appears when a position is exited.

Trade History Boxes

Green if a trade is profitable.

Red if a trade closes at a loss.

Trend Tracking Lines

Horizontal lines mark entry and exit prices.

A filled trade box visually represents trade duration and profitability.

These elements provide clear visual insights into trade execution and performance.

⚡ How to Use This Strategy

1️⃣ Apply the script to a BTC chart in TradingView.

2️⃣ Adjust ADX entry/exit levels based on trend sensitivity.

3️⃣ Enable or disable the SMA filter for trend confirmation.

4️⃣ Backtest performance to analyze historical trade execution.

5️⃣ Monitor trade markers and history boxes for real-time trend insights.

This strategy is designed for trend traders looking to capture high-momentum market conditions while filtering out weak trends.

Btc and Eth 5 min winnerWhat the Strategy Does

Finding the Trend (Like Watching the Bus Move): The strategy uses special tools called Hull Moving Averages (HMAs) to figure out if Bitcoin (BTC) Ethereum (ETH) prices are generally going up or down. It looks at short-term (5 minutes) and long-term (10 minutes) price movements to make sure the “bus” (the market) is moving strongly in one direction—up for buying, down for selling.

Spotting Good Times to Jump On (Buy or Sell Signals): It looks for two types of opportunities:

Pullbacks: When the price dips a little while still moving up (like the bus slowing down but not stopping), it’s a chance to buy.

Breakouts: When the price suddenly jumps higher after being stuck (like the bus speeding up), it’s another chance to buy. It does the opposite for selling when prices are dropping.

It also checks if there’s enough “passenger activity” (volume) and momentum (speed of price change) to make sure it’s a good move.

Avoiding Traffic Jams (Filters): The strategy uses tools like RSI (to check if the market’s too fast or too slow), volume (to see if enough people are trading), and ATR (to measure how wild the price swings are). It skips trades if things look too chaotic or if the trend isn’t strong enough.

Setting Safety Stops and Profit Targets: Once you’re on the “bus,” it sets rules to protect you:

Stop-Loss: If the price moves against you by a small amount (0.5% of the typical price swing), you jump off to avoid losing too much—think of it as getting off before the bus crashes.

Take-Profit: If the price moves in your favor by a small amount (1.0% of the typical swing), you cash out—imagine getting off at your stop with a profit.

Trailing Stop: If the price keeps moving your way, it adjusts your exit point to lock in more profit, like moving your stop closer as the bus keeps going.

Using Leverage (10x Boost): This strategy uses 10x leverage on Binance futures, meaning for every $1 you have, you trade like you have $10. This can make profits (or losses) 10 times bigger, so it’s risky but can be rewarding if you’re careful.

Why 5 Minutes and Bitcoin and Ethereum?

5-Minute Chart: This is like checking the bus every 5 minutes to make quick, small trades—perfect for fast, short profits.

Bitcoin Ethereum (BTC/USD)(ETH/USD): It’s the most popular and liquid crypto, so there’s lots of activity, making it easier to jump on and off without getting stuck.

Why It Aims for 90% Wins (But Be Realistic)

The goal is to win 9 out of 10 trades by being super picky about when to trade—only jumping on when the trend, momentum, and volume are all perfect. But in real trading, markets can be unpredictable, so 90% is very hard to achieve. Still, this strategy tries to be as accurate as possible by avoiding bad moves and focusing on strong trends.

Risks for a New Trader

Leverage: Trading with 10x leverage means small price moves can lead to big losses if you’re not careful. Start with a demo account (pretend money) on TradingView or Binance to practice.

Learning Curve: This strategy uses technical terms (like HMAs, RSI) and tools you’ll need to learn over time. Don’t rush—just practice and ask questions!

How to Use It

Go to TradingView, load this strategy on a 5-minute BTC/USD futures chart on Binance.

Watch the green triangles (buy signals) and red triangles (sell signals) on the chart—they tell you when to trade.

Use the stops and targets to manage your trades—don’t guess, let the strategy guide you.

Start small, learn from each trade, and don’t risk money you can’t afford to lose.

This is like learning to ride a bike—start slow, practice, and you’ll get better. If you have more questions or want simpler tips, feel free to ask! Trading can be fun and rewarding, but it takes patience and practice.

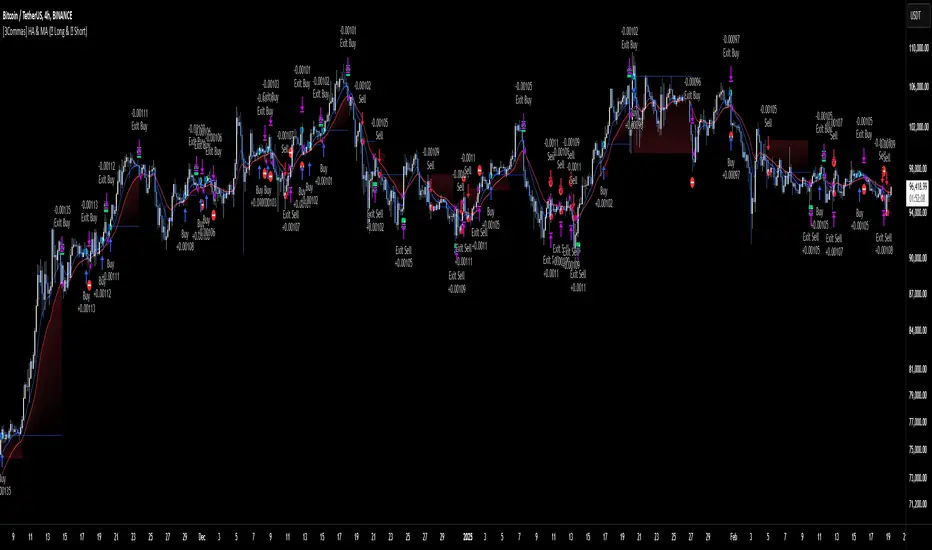

[3Commas] HA & MAHA & MA

🔷What it does: This tool is designed to test a trend-following strategy using Heikin Ashi candles and moving averages. It enters trades after pullbacks, aiming to let profits run once the risk-to-reward ratio reaches 1:1 while securing the position.

🔷Who is it for: It is ideal for traders looking to compare final results using fixed versus dynamic take profits by adjusting parameters and trade direction—a concept applicable to most trading strategies.

🔷How does it work: We use moving averages to define the market trend, then wait for opposite Heikin Ashi candles to form against it. Once these candles reverse in favor of the trend, we enter the trade, using the last swing created by the pullback as the stop loss. By applying the breakeven ratio, we protect the trade and let it run, using the slower moving average as a trailing stop.

A buy signal is generated when:

The previous candle is bearish (ha_bear ), indicating a pullback.

The fast moving average (ma1) is above the slow moving average (ma2), confirming an uptrend.

The current candle is bullish (ha_bull), showing trend continuation.

The Heikin Ashi close is above the fast moving average (ma1), reinforcing the bullish bias.

The real price close is above the open (close > open), ensuring bullish momentum in actual price data.

The signal is confirmed on the closed candle (barstate.isconfirmed) to avoid premature signals.

dir is undefined (na(dir)), preventing repeated signals in the same direction.

A sell signal is generated when:

The previous candle is bullish (ha_bull ), indicating a temporary upward move before a potential reversal.

The fast moving average (ma1) is below the slow moving average (ma2), confirming a downtrend.

The current candle is bearish (ha_bear), showing trend continuation to the downside.

The Heikin Ashi close is below the fast moving average (ma1), reinforcing bearish pressure.

The real price close is below the open (close < open), confirming bearish momentum in actual price data.

The signal is confirmed after the candle closes (barstate.isconfirmed), avoiding premature entries.

dir is undefined (na(dir)), preventing consecutive signals in the same direction.

In simple terms, this setup looks for trend continuation after a pullback, confirming entries with both Heikin Ashi and real price action, supported by moving average alignment to avoid false signals.

If the price reaches a 1:1 risk-to-reward ratio, the stop will be moved to the entry point. However, if the slow moving average surpasses this level, it will become the new exit point, acting as a trailing stop

🔷Why It’s Unique

Easily visualizes the benefits of using risk-to-reward ratios when trading instead of fixed percentages.

Provides a simple and straightforward approach to trading, embracing the "keep it simple" concept.

Offers clear visualization of DCA Bot entry and exit points based on user preferences.

Includes an option to review the message format before sending signals to bots, with compatibility for multi-pair and futures contract pairs.

🔷 Considerations Before Using the Indicator

⚠️Very important: The indicator must be used on charts with real price data, such as Japanese candlesticks, line charts, etc. Do not use it on Heikin Ashi charts, as this may lead to unrealistic results.

🔸Since this is a trend-following strategy, use it on timeframes above 4 hours, where market noise is reduced and trends are clearer. Also, carefully review the statistics before using it, focusing on pairs that tend to have long periods of well-defined trends.

🔸Disadvantages:

False Signals in Ranges: Consolidating markets can generate unreliable signals.

Lagging Indicator: Being based on moving averages, it may react late to sudden price movements.

🔸Advantages:

Trend Focused: Simplifies the identification of trending markets.

Noise Reduction: Uses Heikin Ashi candles to identify trend continuation after pullbacks.

Broad Applicability: Suitable for forex, crypto, stocks, and commodities.

🔸The strategy provides a systematic way to analyze markets but does not guarantee successful outcomes. Use it as an additional tool rather than relying solely on an automated system.

Trading results depend on various factors, including market conditions, trader discipline, and risk management. Past performance does not ensure future success, so always approach the market cautiously.

🔸Risk Management: Define stop-loss levels, position sizes, and profit targets before entering any trade. Be prepared for potential losses and ensure your approach aligns with your overall trading plan.

🔷 STRATEGY PROPERTIES

Symbol: BINANCE:BTCUSDT (Spot).

Timeframe: 4h.

Test Period: All historical data available.

Initial Capital: 10000 USDT.

Order Size per Trade: 1% of Capital, you can use a higher value e.g. 5%, be cautious that the Max Drawdown does not exceed 10%, as it would indicate a very risky trading approach.

Commission: Binance commission 0.1%, adjust according to the exchange being used, lower numbers will generate unrealistic results. By using low values e.g. 5%, it allows us to adapt over time and check the functioning of the strategy.

Slippage: 5 ticks, for pairs with low liquidity or very large orders, this number should be increased as the order may not be filled at the desired level.

Margin for Long and Short Positions: 100%.

Indicator Settings: Default Configuration.

MA1 Length: 9.

MA2 Length: 18.

MA Calculations: EMA.

Take Profit Ratio: Disable. Ratio 1:4.

Breakeven Ratio: Enable, Ratio 1:1.

Strategy: Long & Short.

🔷 STRATEGY RESULTS

⚠️Remember, past results do not guarantee future performance.

Net Profit: +324.88 USDT (+3.25%).

Max Drawdown: -81.18 USDT (-0.78%).

Total Closed Trades: 672.

Percent Profitable: 35.57%.

Profit Factor: 1.347.

Average Trade: +0.48 USDT (+0.48%).

Average # Bars in Trades: 13.

🔷 HOW TO USE

🔸 Adjust Settings:

The default values—MA1 (9) and MA2 (18) with EMA calculation—generally work well. However, you can increase these values, such as 20 and 40, to better identify stronger trends.

🔸 Choose a Symbol that Typically Trends:

Select an asset that tends to form clear trends. Keep in mind that the Strategy Tester results may show poor performance for certain assets, making them less suitable for sending signals to bots.

🔸 Experiment with Ratios:

Test different take profit and breakeven ratios to compare various scenarios—especially to observe how the strategy performs when only the trade is protected.

🔸This is an example of how protecting the trade works: once the price moves in favor of the position with a 1:1 risk-to-reward ratio, the stop loss is moved to the entry price. If the Slow MA surpasses this level, it will act as a trailing stop, aiming to follow the trend and maximize potential gains.

🔸In contrast, in this example, for the same trade, if we set a take profit at a 1:3 risk-to-reward ratio—which is generally considered a good risk-reward relationship—we can see how a significant portion of the upward move is left on the table.

🔸Results Review:

It is important to check the Max Drawdown. This value should ideally not exceed 10% of your capital. Consider adjusting the trade size to ensure this threshold is not surpassed.

Remember to include the correct values for commission and slippage according to the symbol and exchange where you are conducting the tests. Otherwise, the results will not be realistic.

If you are satisfied with the results, you may consider automating your trades. However, it is strongly recommended to use a small amount of capital or a demo account to test proper execution before committing real funds.

🔸Create alerts to trigger the DCA Bot:

Verify Messages: Ensure the message matches the one specified by the DCA Bot.

Multi-Pair Configuration: For multi-pair setups, enable the option to add the symbol in the correct format.

Signal Settings: Enable whether you want to receive long or short signals (Entry | TP | SL), copy and paste the the messages for the DCA Bots configured.

Alert Setup:

When creating an alert, set the condition to the indicator and choose "alert() function call only.

Enter any desired Alert Name.

Open the Notifications tab, enable Webhook URL, and paste the Webhook URL.

For more details, refer to the section: "How to use TradingView Custom Signals".

Finalize Alerts: Click Create, you're done! Alerts will now be sent automatically in the correct format.

🔷 INDICATOR SETTINGS

MA 1: Fast MA Length

MA 2: Slow MA Length

MA Calc: MA's Calculations (SMA,EMA, RMA,WMA)

TP Ratio: This is the take profit ratio relative to the stop loss, where the trade will be closed in profit.

BE Ratio: This is the breakeven ratio relative to the stop loss, where the stop loss will be updated to breakeven or if the MA2 is greater than this level.

Strategy: Order Type direction in which trades are executed.

Use Custom Test Period: When enabled signals only works in the selected time window. If disabled it will use all historical data available on the chart.

Test Start and End: Once the Custom Test Period is enabled, here you select the start and end date that you want to analyze.

Check Messages: Enable the table to review the messages to be sent to the bot.

Entry | TP | SL: Enable this options to send Buy Entry, Take Profit (TP), and Stop Loss (SL) signals.

Deal Entry and Deal Exit : Copy and paste the message for the deal start signal and close order at Market Price of the DCA Bot. This is the message that will be sent with the alert to the Bot, you must verify that it is the same as the bot so that it can process properly so that it executes and starts the trade.

DCA Bot Multi-Pair: You must activate it if you want to use the signals in a DCA Bot Multi-pair in the text box you must enter (using the correct format) the symbol in which you are creating the alert, you can check the format of each symbol when you create the bot.

👨🏻💻💭 We hope this tool helps enhance your trading. Your feedback is invaluable, so feel free to share any suggestions for improvements or new features you'd like to see implemented.

__

The information and publications within the 3Commas TradingView account are not meant to be and do not constitute financial, investment, trading, or other types of advice or recommendations supplied or endorsed by 3Commas and any of the parties acting on behalf of 3Commas, including its employees, contractors, ambassadors, etc.

Flux Charts - S&D Automation💎 GENERAL OVERVIEW

The MTF Supply & Demand Zones (S&D) Automation is a powerful and versatile tool designed to help traders rigorously test their trading strategies against historical market data. With various advanced settings, traders can fine-tune their strategies, assess performance, and identify key improvements before deploying in live trading environments. This tool offers a wide range of configurable settings, explained within this write-up.

Features of the new S&D Automation:

Step By Step : Configure your strategy step by step, which will allow you to have OR & AND logic in your strategies.

Highly Configurable : Offers multiple parameters for fine-tuning trade entry and exit conditions.

Multi-Timeframe Analysis : Allows traders to analyze multiple timeframes simultaneously for enhanced accuracy.

Provides advanced stop-loss, take-profit, and break-even settings.

Incorporates Supply & Demand Zone conditions, with settings like Sensitivity, Zone Invalidation, Minimum Zone Width & Minimum Zone Length settings for refined strategy execution.

🚩 UNIQUENESS

The S&D Automation stands out from conventional backtesting tools due to its unparalleled flexibility, precision, and advanced trading logic integration. Key factors that make it unique include:

✅ Comprehensive Strategy Customization – Unlike traditional backtesters that offer basic entry and exit conditions, S&D Automation provides a highly detailed parameter set, allowing traders to fine-tune their strategies with precision.

✅ Multi-Timeframe Supply & Demand Zones – This is the first-ever tool that allows traders to backtest Supply & Demand zones on multiple timeframes.

✅ Customizable Take-Profit Conditions – Offers various methods to set take-profit exits, including using core features from Supply & Demand Zones, and fixed exits like ATR, % change or price change, enabling traders to tailor their exit strategies to specific market behaviors.

✅ Customizable Stop-Loss Conditions – Provides several ways to set up stop losses, including using concepts from Supply & Demand Zones and trailing stops or fixed exits like ATR, % change or price change, allowing for dynamic risk management tailored to individual strategies.

✅ Integration of External Indicators – Allows the inclusion of other indicators or data sources from TradingView for creating strategy conditions, enabling traders to enhance their strategies with additional insights and data points.

By integrating these advanced features, S&D Automation ensures that traders can rigorously test and optimize their strategies with great accuracy and efficiency.

📌 HOW DOES IT WORK ?

The first setting you will want to set it the pyramiding setting. This setting controls the number of simultaneous trades in the same direction allowed in the strategy. For example, if you set it to 1, only one trade can be active in any time, and the second trade will not be entered unless the first one is exited. If it is set to 2, the script will handle both of them at the same time. Note that you should enter the same value to this pyramiding setting, and the pyramiding setting in the "Properties" tab of the script for this to work.

You can enable and set a backtesting window that will limit the entries to between the start date & end date.

Then, you can enter your desired settings for Supply & Demand Zones. You can also enable and set up to 3 timeframes, which you can use later on when customizing your strategies enter / exit conditions.

Entry Conditions

From the "Long Conditions" or the "Short Conditions" groups, you can set your position entry conditions. For settings like "initial capital" or "order size", you can open the "Properties" tab, where these are handled.

The S&D Automation can use the following conditions for entry conditions :

1. Demand Zone

Detection: Triggered when a Demand Zone forms or is detected

Retest: Triggered when price retests a Demand Zone. A retest is confirmed when a candle enters a Demand Zone and closes outside of it.

2nd Retest: Triggered when price retests a Demand Zone for the second time. A retest is confirmed when a candle enters a Demand Zone and closes outside of it.

3rd Retest: Triggered when price retests a Demand Zone for the third time. A retest is confirmed when a candle enters a Demand Zone and closes outside of it.

Retracement: Triggered when price touches a Demand Zone

Break: Triggered when a Demand Zone is invalidated by candle close or wick, depending on the user's input.

2. Supply Zone

Detection: Triggered when a Supply Zone forms or is detected

Retest: Triggered when price retests a Supply Zone. A retest is confirmed when a candle enters a Supply Zone and closes outside of it.

2nd Retest: Triggered when price retests a Supply Zone for the second time. A retest is confirmed when a candle enters a Supply Zone and closes outside of it.

3rd Retest: Triggered when price retests a Supply Zone for the third time. A retest is confirmed when a candle enters a Supply Zone and closes outside of it.

Retracement: Triggered when price touches a Supply Zone

Break: Triggered when a Supply Zone is invalidated by candle close or wick, depending on the user's input.

3. Any Zone

Detection: Triggered when any Supply or Demand Zone forms or is detected

Retest: Triggered when price retests any Supply or Demand Zone. A retest is confirmed when a candle enters any Supply or Demand Zone and closes outside of it.

2nd Retest: Triggered when price retests any Supply or Demand Zone for the second time. A retest is confirmed when a candle enters any Supply or Demand Zone and closes outside of it.

3rd Retest: Triggered when price retests any Supply or Demand Zone for the third time. A retest is confirmed when a candle enters any Supply or Demand Zone and closes outside of it.

Retracement: Triggered when price touches any Supply or Demand Zone

Break: Triggered when any Supply or Demand Zone is invalidated by candle close or wick, depending on the user's input.

🕒 TIMEFRAME CONDITIONS

The S&D Automation supports Multi-Timeframe (MTF) features, just like the Supply & Demand indicator. When setting an entry condition, you can also choose the timeframe.

To set up MTF conditions, navigate to the 'Timeframes' section in the settings, select your desired timeframes, and enable them. You can choose up to three timeframes.

Once you've selected your timeframes, you can use them in your strategy. When setting long and short entry/exit conditions, you can choose from Timeframe 1, Timeframe 2, or Timeframe 3.

External Conditions

Users can use external indicators on the chart to set entry conditions.

The second dropdown in the external condition settings allows you to choose a conditional operator to compare external outputs. Available options include:

Less Than or Equal To: <=

Less Than: <

Equal To: =

Greater Than: >

Greater Than or Equal To: >=

The position entry conditions work like this ;

Each side has 5 S&D Zone conditions and 1 Source condition. Each condition can be enabled or disabled using the checkbox on the left side of them.

The next selection is the alert type, which you can select between "Detection", "Retest", "Retracement" or "Break".

You can select which timeframe this condition should work on from Timeframe 1, 2, or 3. If you select "Any Timeframe", the condition will work for all timeframes.

Lastly select the step of this condition from 1 to 6.

The Source Condition

The last condition on each side is a source condition that is different from the others. Using this condition, you can create your own logic using other indicators' outputs on your chart. For example, suppose that you have an EMA indicator in your chart. You can have the source condition to something like "EMA > high".

The Step System

Each condition has a step number, and conditions are in topological order based on them.

The conditions are executed step by step. This means the condition with step 2 cannot be executed before the condition with step 1 is executed.

Conditions with the same step numbers have "OR" logic. This means that if you have 2 conditions with step 3, the condition with step 4 can trigger after only one of the step 3 conditions is executed.

➕ OTHER ENTRY FEATURES

The S&D Automation allows traders to choose when to execute trades and when not to execute trades.

1. Only Take Trades

This setting lets users specify the time period when their strategy can open or execute trades.

2. Don't Take Trades

This setting lets users specify time periods when their strategy can't open or execute trades.

↩️ EXIT CONDITIONS

1. Exit on Opposite Signal

When enabled, a long position will close when short entry conditions are met, and a short position will close when long entry conditions are met.

2. Exit on Session End

When enabled, positions will be closed at the end of the trading session.

📈 TAKE PROFIT CONDITIONS

There are several methods available for setting take profit exits and conditions.

1. Entry Condition TP

Users can use entry conditions as triggers for take-profit exits. This setting can be found under the long and short exit conditions.

2. Fixed TP

Users can set a fixed TP for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a TP exit when price reaches a specified level. For example, if you set the Price TP to 10 and buy NASDAQ:TSLA at $190, the trade will automatically exit when the price reaches $200 ($190 + $10).

Ticks: This method triggers a TP exit when price moves a specified number of ticks.

Percentage (%): This method triggers a TP exit when price moves a specified percentage.

ATR: This method triggers a TP exit based on a specified multiple of the Average True Range (ATR).

📉 STOP LOSS CONDITIONS

There are several methods available for setting stop-loss exits and conditions.

1. Entry Condition SL

Users can use entry conditions as triggers for stop-loss exits. This setting can be found under the long and short exit conditions.

2. Fixed SL

Users can set a fixed SL for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a SL exit when price reaches a specified level. For example, if you set the Price SL to 10 and buy NASDAQ:TSLA at $200, the trade will automatically exit when the price reaches $190 ($200 - $10).

Ticks: This method triggers a SL exit when price moves a specified number of ticks.

Percentage (%): This method triggers a SL exit when price moves a specified percentage.

ATR: This method triggers a SL exit based on a specified multiple of the Average True Range (ATR).

3. Trailing Stop

An explanation & example for the trailing stop feature is present on the write-up within the next section.

Exit conditions have the same logic of constructing conditions like the entry ones. You can construct a Take-Profit Condition & a Stop-Loss Condition. Note that the Take-Profit condition will only work if the position is in profit, regardless of if it's triggered or not. The same applies for the Stop-Loss condition, meaning that it will only work if the position is in loss.

You can also set a Fixed TP & Fixed SL based on the price movement after the position is entered. You have options like "Price", "Ticks", "%", or "Average True Range". For example, you can set a Fixed TP like "5%", and the position will be entered once it moves 5% up in a long position.

Trailing Stop

For the Fixed SL, you also have a "Trailing" stop option, for which you can set its activation level as well. The Trailing stop activation level and its value are expressed in ticks. Check this scenario for an example :

We have a ticker with a tick value of $1. Our Trailing Stop is set to 10 ticks, and the activation level is set to 30 ticks.

We buy 1 contract when the price is $100.

When the price becomes $110, we are in $10 (10 ticks) profit and the trailing stop is now activated.

The current price our stop's on is $110 - $30 (30 ticks), which is the level of $80.

The trailing stop will only move if the price moves up the highest high the price has been after we entered the position.

Let's suppose that price moves up $40 right after our trailing stop is activated. The price will now be $150, and our trailing stop will sit on $150 - $30 (30 ticks) = $120.

If the price is down the $120 level, our stop loss will be triggered.

There is also a "Hard SL" option designed for a backup stop-loss when trailing stops are enabled. You can enable & set this option and if the price goes down before our trailing stop even activates, the position will be exited.

You can also move stop-loss to the break-even (entry price of the position) after a certain profit is achieved using the last setting of the exit conditions. Note that for this to work, you must have a Fixed SL set-up.

➕ OTHER EXIT FEATURES

1. Move Stop Loss to Breakeven

This setting allows the strategy to automatically move the SL to Breakeven (BE) when the position is in profit by a certain amount. Users can choose between the following:

Price: This method moves the SL to BE when price reaches a specified level.

Ticks: This method moves the SL to BE when price moves a specified number of ticks.

Percentage (%): This method moves the SL to BE when price moves a specified percentage.

ATR: This method moves the SL to BE when price moves a specified multiple of the Average True Range (ATR).

Example Entry Scenario

To give an example , check this scenario; out conditions are :

LONG CONDITIONS

Demand Zone Detection, Step 1

Supply Zone Retest, Step 2

Demand Zone Break, Step 2

open > close, Step 3

First, the strategy needs to detect a Demand Zone Detection in order to start working.

After it's detected, now it's looking for either a Supply Zone Retest, or a Demand Zone Break to proceed to the next step, the reason for this is that they both have the same step number.

After one of them is detected, the strategy will consistently check candlesticks for the condition open > close. If a bullish candlestick occurs, a long position will be entered.

⏰ ALERTS

This indicator uses TradingView's strategy alert system. All entries and exits will be sent as an alert if configured. It's possible to further customize these alerts to your liking. For more information check TradingView's strategy alert customization page : www.tradingview.com

⚙️ SETTINGS

1. Backtesting Settings

Pyramiding: Controls the number of simultaneous trades allowed in the strategy. This setting must have the same value that is entered on the script's properties tab on the settings pane.

Enable Custom Backtesting Period: Restricts backtesting to a specific date range.

Start & End Time Configuration: Define precise start and end dates for historical analysis.

2. General Configuration

Detection Method: There are two detection methods you can choose from for identifying Supply & Demand Zones. Both methods aim to identify key areas where price is likely to react, but they do so using different approaches. Traders can choose the method that aligns with their trading style and time horizon.

Sensitivity: The Sensitivity setting allows traders to adjust how aggressively the script identifies supply and demand zones when using the Momentum Detection Method. This setting directly impacts the threshold for detecting zones when using the momentum detection method.

Zone Invalidation: The Zone Invalidation setting determines how supply and demand zones are invalidated.

Wick -> A zone is invalidated if a candle’s wick goes below a demand zone or above a supply zone.

Close -> A zone is invalidated if a candle closes below a demand zone or above a supply zone.

Zone Visibility Range: The Zone Visibility Range setting controls how far from the current price supply and demand zones are displayed on the chart. It helps traders focus on relevant zones while avoiding clutter from distant or less impactful areas.

Minimum Zone Width: The Minimum Zone Width setting defines the smallest size a supply or demand zone must have to be displayed on the chart. It uses the Average True Range (ATR) as a reference to ensure zones are proportionate to current market volatility.

Minimum Zone Length: The Minimum Zone Length setting determines the minimum number of bars a supply or demand zone must span to be displayed on the chart. This setting helps filter out short-lived or insignificant zones, ensuring only meaningful areas of supply or demand are highlighted.

3. Multi-Timeframe Analysis

Enable Up to Three Timeframes: Select and analyze trades across multiple timeframes.

4. Entry Conditions for Long & Short Trades

Multiple Conditions (1-6): Configure up to six independent conditions per trade direction.

Condition Types: Options include Detection, Retest, 2nd Retest, 3rd Retest, Retracement, and Break.

Timeframe Specification: Choose between "Any Timeframe", "Timeframe 1", "Timeframe 2", or "Timeframe 3".

Trade Execution Filters: Restrict trades within specific trading sessions.

5. Exit Conditions for Long & Short Trades

Exit on Opposite Signal: Automatically exit trades upon opposite trade conditions.

Exit on Session End: Closes all positions at the end of the trading session.

Multiple Take-Profit (TP) and Stop-Loss (SL) Configurations:

TP/SL based on % move, ATR, Ticks, or Fixed Price.

Hard SL option for additional risk control.

Move SL to BE (Break Even) after a certain profit threshold.

Volatility Arbitrage Spread Oscillator Model (VASOM)The Volatility Arbitrage Spread Oscillator Model (VASOM) is a systematic approach to capitalizing on price inefficiencies in the VIX futures term structure. By analyzing the differential between front-month and second-month VIX futures contracts, we employ a momentum-based oscillator (Relative Strength Index, RSI) to signal potential market reversion opportunities. Our research builds upon existing financial literature on volatility risk premia and contango/backwardation dynamics in the volatility markets (Zhang & Zhu, 2006; Alexander & Korovilas, 2012).

Volatility derivatives have become essential tools for managing risk and engaging in speculative trades (Whaley, 2009). The Chicago Board Options Exchange (CBOE) Volatility Index (VIX) measures the market’s expectation of 30-day forward-looking volatility derived from S&P 500 option prices (CBOE, 2018). Term structures in VIX futures often exhibit contango or backwardation, depending on macroeconomic and market conditions (Alexander & Korovilas, 2012).

This strategy seeks to exploit the spread between the front-month and second-month VIX futures as a proxy for term structure dynamics. The spread’s momentum, quantified by the RSI, serves as a signal for entry and exit points, aligning with empirical findings on mean reversion in volatility markets (Zhang & Zhu, 2006).

• Entry Signal: When RSI_t falls below the user-defined threshold (e.g., 30), indicating a potential undervaluation in the spread.

• Exit Signal: When RSI_t exceeds a threshold (e.g., 70), suggesting mean reversion has occurred.

Empirical Justification