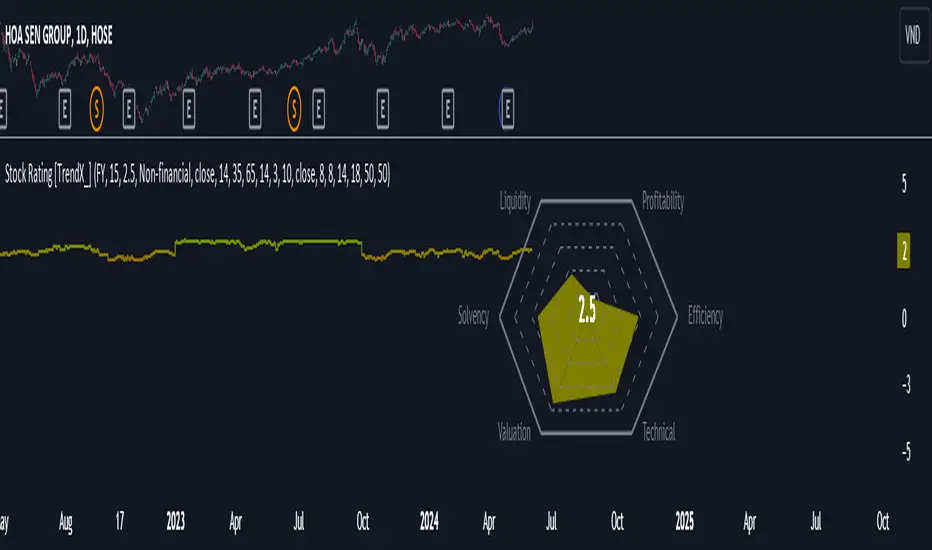

Stock Rating [TrendX_]# OVERVIEW

This Stock Rating indicator provides a thorough evaluation of a company (NON-FINANCIAL ONLY) ranging from 0 to 5. The rating is the average of six core financial metrics: efficiency, profitability, liquidity, solvency, valuation, and technical ratings. Each metric encompasses several financial measurements to ensure a robust and holistic evaluation of the stock.

## EFFICIENCY METRICS

1. Asset-to-Liability Ratio : Measures a company's ability to cover its liabilities with its assets.

2. Equity-to-Liability Ratio : Indicates the proportion of equity used to finance the company relative to liabilities.

3. Net Margin : Shows the percentage of revenue that translates into profit.

4. Operating Expense : Reflects the costs required for normal business operations.

5. Operating Expense Ratio : Compares operating expenses to total revenue.

6. Operating Profit Ratio : Measures operating profit as a percentage of revenue.

7. PE to Industry Relative PE/PB : Compares the company's PE ratio to the industry average.

## PROFITABILITY METRICS

1. ROA : Indicates how efficiently a company uses its assets to generate profit.

2. ROE : Measures profitability relative to shareholders' equity.

3. EBITDA : Reflects a company's operational profitability.

4. Free Cash Flow Margin : Shows the percentage of revenue that remains as free cash flow.

5. Revenue Growth : Measures the percentage increase in revenue over a period.

6. Gross Margin : Reflects the percentage of revenue exceeding the cost of goods sold.

7. Net Margin : Percentage of revenue that is net profit.

8. Operating Margin : Measures the percentage of revenue that is operating profit.

## LIQUIDITY METRICS

1. Current Ratio : Indicates the ability to cover short-term obligations with short-term assets.

2. Interest Coverage Ratio : Measures the ability to pay interest on outstanding debt.

3. Debt-to-EBITDA : Compares total debt to EBITDA.

4. Debt-to-Equity Ratio : Indicates the relative proportion of debt and equity financing.

## SOLVENCY METRICS

1. Altman Z-score : Predicts bankruptcy risk

2. Beneish M-score : Detects earnings manipulation.

3. Fulmer H-factor : Predicts business failure risk.

## VALUATION METRICS

1. Industry Relative PE/PB Comparison : Compares the company's PE and PB ratios to industry averages.

2. Momentum of PE, PB, and EV/EBITDA Multiples : Tracks the trends of PE, PB, and EV/EBITDA ratios over time.

## TECHNICAL METRICS

1. Relative Strength Index (RSI) : Measures the speed and change of price movements.

2. Supertrend : Trend-following indicator that identifies market trends.

3. Moving Average Golden-Cross : Occurs when a short-term MA crosses above mid-term and long-term MA which are determined by half-PI increment in smoothing period.

4. On-Balance Volume Golden-Cross : Measures cumulative buying and selling pressure.

Penunjuk Pine Script®