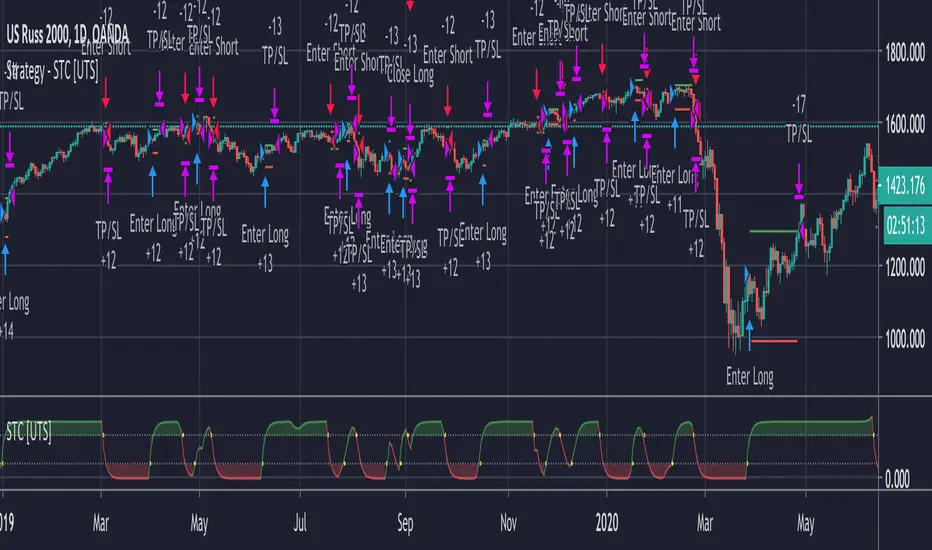

Strategy - Uber STC - Schaff Trend Cycle [UTS]Backtesting of Uber STC - Schaff Trend Cycle

Backtest with focus win/loss profitability.

Formula: profitability = win / (win+loss)

Default equity 100k USD

Default 2% Risk per trade

Default currency USD

Define backtest interval precisely by month, year, day

LONG and SHORT positions

Visualize SL and TP on chart

ATR (len: 14, smooth: SMA)

ATR based Stop-Loss, if hit trade will be closed and considered as loss

ATR based Take-Profit, if hit trade will be closed and considered as win

On TP or SL hit the trade is closed and marked as win/loss

Cari dalam skrip untuk "profit"

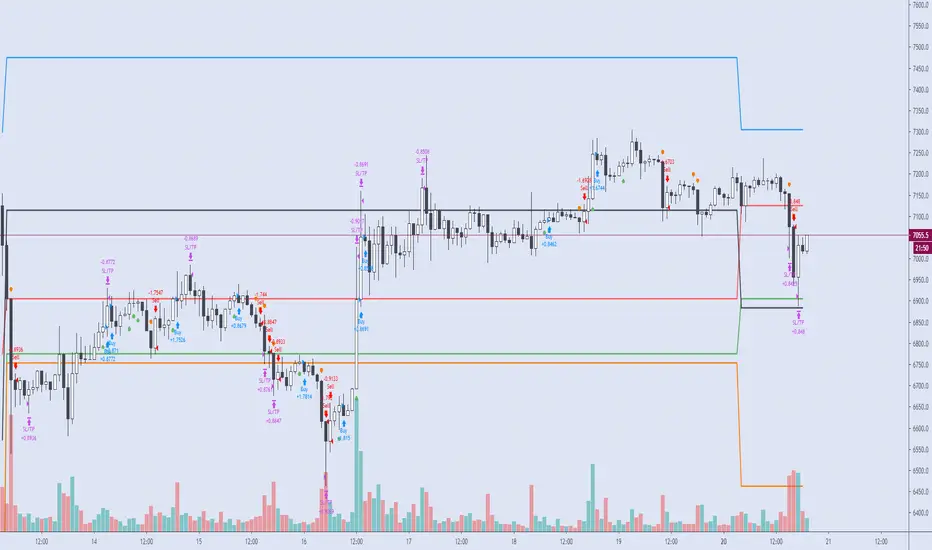

Support/ Resistance with H1 ATR - strategy mainline versionThis script using ATR (average true range) with source hl2 for create Support/ Resistance line

The color meaning:

- Green = Support line

- Red = Resistance line

Signal:

- If close price breakout Resistance line -> LONG signal will been active.

- If close price breakout Support line -> SHORT signal will been active.

Input setting:

Recommended default setting.

- Factor: amplitude for create Support/ Resistance line.

- Length: length of ATR.

- Offset: number of bar for check sideway or choppy market.

- Take profit: if you want test close position by profit.

- Stop loss: should not be missed.

- Open Position with Stop-Market type:

+ Open LONG position with high price and type Stop-Market.

+ Open SHORT position with low price and type Stop-Market.

Strategy setting:

Recommended default setting if you trade on Binance Futures or change Comission if you trade on another exchange.

Best backtest if:

- Max drawdown less than 10%.

- Min backtest time: 6 month.

- Avg profit: 10%/ month when no leverage is used.

Alert version:

1 - Select create new alert

2 - Condition:

+ eb BUY -> LONG signal

+ eb BUY close -> close LONG position

+ eb SELL -> SHORT signal

+ eb SELL close -> close SHORT position

3 - Option: recommended using only. Because the signal will be more accurate if the price close breakout successfully.

+ Always put stop loss position to avoid PUMP/ DUMP market.

// Note: alert version not free, send for me a private message on TradingView to get price and gain access.

Recommended:

- Using in M30, M45, H1 timeframe with default setting.

- Symbol: BTC

- Exchange: Binance Futures

- Order size: 10% wallet balance, maximum 25% wallet balance.

- Leverage: X2-X5, maximum X10.

---> I using 10% wallet balance and X2 only.

Strategy - Backtest Uber WAE - Waddah Attar Explosion [UTS]Backtest of WAE - Waddah Attar Explosion

Backtest with focus win/loss profitability.

Formula: profitability = win / (win+loss)

Default equity 100k USD

Default 2% Risk per trade

Default currency USD

Define backtest interval precisely by month, year, day

LONG and SHORT positions

Visualize SL and TP on chart

ATR (len: 14, smooth: SMA)

ATR based Stop-Loss, if hit trade will be closed and considered as loss

ATR based Take-Profit, if hit trade will be closed and considered as win

On TP or SL hit the trade is closed and marked as win/loss

Strategy - Backtest Uber Kuskus Starlight [UTS]Backtest of Uber Kuskus Starlight

Backtest with focus win/loss profitability.

Formula: profitability = win / (win+loss)

Default equity 100k USD

Default 2% Risk per trade

Default currency USD

Define backtest interval precisely by month, year, day

LONG and SHORT positions

Visualize SL and TP on chart

ATR (len: 14, smooth: SMA)

ATR based Stop-Loss, if hit trade will be closed and considered as loss

ATR based Take-Profit, if hit trade will be closed and considered as win

On TP or SL hit the trade is closed and marked as win/loss

The MATRIX: Ultimate Crypto Position StrategyHi all,

We are cryptocurrency miners and 'hodlers’ since 2013, with unwavering confidence in the technology behind it. We’d always thought that it would be a life-changing êvent. And we were right. We went from “broke” to making shit loads of money and all the way back to bitter nothing. If you are lucky, you probably haven’t experienced what if feels to be high on cash and then fall very deep low, but let me reassure you, it is a nasty feeling.

Then we wondered, what the hell did we do wrong? Or better say, what didn’t we do right! The answer was dead simple: We had no experience in trading, we were overwhelmed by emotions and we didn't use any trading strategy. Hence, we were doomed to fail from the beginning.

In order to build an all-in-one profitable trading strategy, we had to start from zero. The one thing we learned is that your goal for financial gain cannot be achieved without discipline and consistency. Our prime focus was to absorb as much info as possible regarding trading and coding by doing an extensive self-study, which consequentially took us to the next level.

One of the secrets to being successful from a trading perspective is to have an indefatigable and undying thirst for information and knowledge. As Bruce Lee once said: “Learning is never cumulative; it is a movement of knowing which has no beginning nor end”. So, we adapted what was useful, rejected what was useless, and added our own preferences based on our mindset. We were totally committed to be the best. Our goal was never to lose money again! Of course, this is an illusion, as no single strategy is correct all of the time.

Therefore, the final trading strategy was based on the following key elements:

• The avoidance of risk is more important than absolute profit. Do not anticipate and do not move without market confirmation. Being a little late in your trade is your indication if you are right or wrong.

• Offering simplicity and practicality, for those that do not have the time to trade 24/7.

• Believe in analysis and not in forecasting. Trading is a skill for those who are smart and gambling for those who are not.

In conclusion, we are absolutely thrilled to finally release this trading strategy after one year of extensive back testing and optimization. The script was supposed to be for personal use only, but because Tradingview has helped us a lot in this process, we want to share it with all of you and give something back to this amazing community. If you learned something new today and found value, please give us a like to show your support! We’d really appreciate it.

***The script is invite-only, message us to get script access***

-------------------------------------------------------------------------------------------------

The MATRIX: Ultimate Crypto Position Strategy should be used as follows:

• The trading strategy was designed and optimized for trading cryptocurrencies only ; furthermore it works best on established high market cap cryptocurrencies that have a clear trend such as:

BTCUSD

ETHUSD

LTCUSD

XRMUSD

EOSUSD

ADAUSD

DASHUSD

ETCUSD

• The trading strategy is based on swing/position methodology. The script must therefore be used on daily timeframe candles only (1D) .

• Use USD trading pairs only (e.g. use ETHUSD instead of the ETHBTC) since the individual trend is captured more effectively and therefore gives better results.

-------------------------------------------------------------------------------------------------

The MATRIX:Ultimate Crypto Position Strategy is based on the following indicators:

• Ichimoku Cloud ; acts as the leading indicator.

• Volume ; without strong volume , a market move is not valid.

• MACD and Vortex ; both being used as confirmation indicators.

• Choppiness index ; avoids trading in choppy markets.

• Bullish/ Bearish Regular Divergences in combination with RSI to spot tops and bottoms.

• Simple and Exponential Moving Averages ; prêvents trading against the trend.

The trading strategy is easy to use, trend based and without repainting, meaning once a signal has been made it is permanent and that no future data is used in the decision making. It detects the trend and filters out market noise based on more than 10 technical indicators. ONLY when all indicators align with each other the algorithm prints a BUY or SELL signal. The trading strategy provides high probability trading signals and minimizes risk! This script aims to capture the profit from longer term trending moves and by doing so filters out non-substantial trends and avoids the associated risks with these trades.

-------------------------------------------------------------------------------------------------

The MATRIX: Ultimate Crypto Position Strategy has the following features:

• Automatically generated Buy / Sell alerts in the form of a label.

• NO Repaint once candle is closed.

• SAFEGUARD ; custom built-in security prevẹnts trading when the price is out of equilibrium.

• Customizable Display for the Ichimoku cloud indicator display.

-------------------------------------------------------------------------------------------------

Below are the backtest results. Keep in mind that this strategy is quite conservative resulting in few long positions. These results are therefore no guarantee for the future.

Back test results: (only Long trades, signal to signal, order size: 100% of equity, commision fee 0.1%, period: start of chart)

Exchange-----Asset---------Timeframe---Percent Profitable----Profit Factor-----Total Trades----Max Drawdown---Average bars in trade-----Net Profit

Coinbase-----BTC/USD---------1D----------------100----------------N/A------------------10---------------0.00---------------------54-------------------6183.6

Coinbase-----ETH/USD---------1D----------------100----------------N/A------------------7----------------0.00---------------------46-------------------11673.0

Coinbase-----LTC/USD---------1D-----------------100---------------N/A-------------------7----------------0.00---------------------46------------------4727.0

Bínance------EOS/USD---------1D-----------------100---------------N/A-------------------3----------------0.00---------------------34------------------42.8

Bínance------ADA/USD---------1D-----------------100---------------N/A-------------------2----------------0.00---------------------40------------------118.4

Coinbase-----XTZ/USD---------1D-----------------100---------------N/A-------------------1----------------0.00---------------------36------------------34.4

Bínance------BNB/USD---------1D-----------------66.7--------------10.8-------------------6---------------24.22--------------------38------------------1488.8

Bínance------ETC/USD---------1D-----------------100---------------N/A-------------------2----------------0.00---------------------33------------------94.9

Bínance------XMR/USD---------1D-----------------100---------------N/A-------------------3----------------0.00---------------------43------------------74.2

Bínance------ICX/USD----------1D-----------------100---------------N/A-------------------2----------------0.00---------------------29------------------215.3

-------------------------------------------------------------------------------------------------

Reminder: Use this trading strategy at your own risk and trade responsibly. We are not responsible for any financial loss using this strategy.

***The script is invite-only, message us to get script access***

888 BOT #backtest█ 888 BOT #backtest

This is an Expert Advisor 'EA' or Automated trading script for ‘longs’ and ‘shorts’, which uses only a Take Profit or, in the worst case, a Stop Loss to close the trade.

It's a much improved version of the previous ‘Repanocha’. It doesn`t use 'Trailing Stop' or 'security()' functions (although using a security function doesn`t mean that the script repaints) and all signals are confirmed, therefore the script doesn`t repaint in alert mode and is accurate in backtest mode.

Apart from the previous indicators, some more and other functions have been added for Stop-Loss, re-entry and leverage.

It uses 8 indicators, (many of you already know what they are, but in case there is someone new), these are the following:

1. Jurik Moving Average

It's a moving average created by Mark Jurik for professionals which eliminates the 'lag' or delay of the signal. It's better than other moving averages like EMA, DEMA, AMA or T3.

There are two ways to decrease noise using JMA. Increasing the 'LENGTH' parameter will cause JMA to move more slowly and therefore reduce noise at the expense of adding 'lag'

The 'JMA LENGTH', 'PHASE' and 'POWER' parameters offer a way to select the optimal balance between 'lag' and over boost.

Green: Bullish, Red: Bearish.

2. Range filter

Created by Donovan Wall, its function is to filter or eliminate noise and to better determine the price trend in the short term.

First, a uniform average price range 'SAMPLING PERIOD' is calculated for the filter base and multiplied by a specific quantity 'RANGE MULTIPLIER'.

The filter is then calculated by adjusting price movements that do not exceed the specified range.

Finally, the target ranges are plotted to show the prices that will trigger the filter movement.

Green: Bullish, Red: Bearish.

3. Average Directional Index (ADX Classic) and (ADX Masanakamura)

It's an indicator designed by Welles Wilder to measure the strength and direction of the market trend. The price movement is strong when the ADX has a positive slope and is above a certain minimum level 'ADX THRESHOLD' and for a given period 'ADX LENGTH'.

The green color of the bars indicates that the trend is bullish and that the ADX is above the level established by the threshold.

The red color of the bars indicates that the trend is down and that the ADX is above the threshold level.

The orange color of the bars indicates that the price is not strong and will surely lateralize.

You can choose between the classic option and the one created by a certain 'Masanakamura'. The main difference between the two is that in the first it uses RMA () and in the second SMA () in its calculation.

4. Parabolic SAR

This indicator, also created by Welles Wilder, places points that help define a trend. The Parabolic SAR can follow the price above or below, the peculiarity that it offers is that when the price touches the indicator, it jumps to the other side of the price (if the Parabolic SAR was below the price it jumps up and vice versa) to a distance predetermined by the indicator. At this time the indicator continues to follow the price, reducing the distance with each candle until it is finally touched again by the price and the process starts again. This procedure explains the name of the indicator: the Parabolic SAR follows the price generating a characteristic parabolic shape, when the price touches it, stops and turns (SAR is the acronym for 'stop and reverse'), giving rise to a new cycle. When the points are below the price, the trend is up, while the points above the price indicate a downward trend.

5. RSI with Volume

This indicator was created by LazyBear from the popular RSI.

The RSI is an oscillator-type indicator used in technical analysis and also created by Welles Wilder that shows the strength of the price by comparing individual movements up or down in successive closing prices.

LazyBear added a volume parameter that makes it more accurate to the market movement.

A good way to use RSI is by considering the 50 'RSI CENTER LINE' centerline. When the oscillator is above, the trend is bullish and when it is below, the trend is bearish.

6. Moving Average Convergence Divergence (MACD) and (MAC-Z)

It was created by Gerald Appel. Subsequently, the histogram was added to anticipate the crossing of MA. Broadly speaking, we can say that the MACD is an oscillator consisting of two moving averages that rotate around the zero line. The MACD line is the difference between a short moving average 'MACD FAST MA LENGTH' and a long moving average 'MACD SLOW MA LENGTH'. It's an indicator that allows us to have a reference on the trend of the asset on which it is operating, thus generating market entry and exit signals.

We can talk about a bull market when the MACD histogram is above the zero line, along with the signal line, while we are talking about a bear market when the MACD histogram is below the zero line.

There is the option of using the MAC-Z indicator created by LazyBear, which according to its author is more effective, by using the parameter VWAP (volume weighted average price) 'Z-VWAP LENGTH' together with a standard deviation 'STDEV LENGTH' in its calculation.

7. Volume Condition

Volume indicates the number of participants in this war between bulls and bears, the more volume the more likely the price will move in favor of the trend. A low trading volume indicates a lower number of participants and interest in the instrument in question. Low volumes may reveal weakness behind a price movement.

With this condition, those signals whose volume is less than the volume SMA for a period 'SMA VOLUME LENGTH' multiplied by a factor 'VOLUME FACTOR' are filtered. In addition, it determines the leverage used, the more volume, the more participants, the more probability that the price will move in our favor, that is, we can use more leverage. The leverage in this script is determined by how many times the volume is above the SMA line.

The maximum leverage is 8.

8. Bollinger Bands

This indicator was created by John Bollinger and consists of three bands that are drawn superimposed on the price evolution graph.

The central band is a moving average, normally a simple moving average calculated with 20 periods is used. ('BB LENGTH' Number of periods of the moving average)

The upper band is calculated by adding the value of the simple moving average X times the standard deviation of the moving average. ('BB MULTIPLIER' Number of times the standard deviation of the moving average)

The lower band is calculated by subtracting the simple moving average X times the standard deviation of the moving average.

the band between the upper and lower bands contains, statistically, almost 90% of the possible price variations, which means that any movement of the price outside the bands has special relevance.

In practical terms, Bollinger bands behave as if they were an elastic band so that, if the price touches them, it has a high probability of bouncing.

Sometimes, after the entry order is filled, the price is returned to the opposite side. If price touch the Bollinger band in the same previous conditions, another order is filled in the same direction of the position to improve the average entry price, (% MINIMUM BETTER PRICE ': Minimum price for the re-entry to be executed and that is better than the price of the previous position in a given %) in this way we give the trade a chance that the Take Profit is executed before. The downside is that the position is doubled in size. 'ACTIVATE DIVIDE TP': Divide the size of the TP in half. More probability of the trade closing but less profit.

█ STOP LOSS and RISK MANAGEMENT.

A good risk management is what can make your equity go up or be liquidated.

The % risk is the percentage of our capital that we are willing to lose by operation. This is recommended to be between 1-5%.

% Risk: (% Stop Loss x % Equity per trade x Leverage) / 100

First the strategy is calculated with Stop Loss, then the risk per operation is determined and from there, the amount per operation is calculated and not vice versa.

In this script you can use a normal Stop Loss or one according to the ATR. Also activate the option to trigger it earlier if the risk percentage is reached. '% RISK ALLOWED'

'STOP LOSS CONFIRMED': The Stop Loss is only activated if the closing of the previous bar is in the loss limit condition. It's useful to prevent the SL from triggering when they do a ‘pump’ to sweep Stops and then return the price to the previous state.

█ BACKTEST

The objective of the Backtest is to evaluate the effectiveness of our strategy. A good Backtest is determined by some parameters such as:

- RECOVERY FACTOR: It consists of dividing the 'net profit' by the 'drawdown’. An excellent trading system has a recovery factor of 10 or more; that is, it generates 10 times more net profit than drawdown.

- PROFIT FACTOR: The ‘Profit Factor’ is another popular measure of system performance. It's as simple as dividing what win trades earn by what loser trades lose. If the strategy is profitable then by definition the 'Profit Factor' is going to be greater than 1. Strategies that are not profitable produce profit factors less than one. A good system has a profit factor of 2 or more. The good thing about the ‘Profit Factor’ is that it tells us what we are going to earn for each dollar we lose. A profit factor of 2.5 tells us that for every dollar we lose operating we will earn 2.5.

- SHARPE: (Return system - Return without risk) / Deviation of returns.

When the variations of gains and losses are very high, the deviation is very high and that leads to a very poor ‘Sharpe’ ratio. If the operations are very close to the average (little deviation) the result is a fairly high 'Sharpe' ratio. If a strategy has a 'Sharpe' ratio greater than 1 it is a good strategy. If it has a 'Sharpe' ratio greater than 2, it is excellent. If it has a ‘Sharpe’ ratio less than 1 then we don't know if it is good or bad, we have to look at other parameters.

- MATHEMATICAL EXPECTATION: (% winning trades X average profit) + (% losing trades X average loss).

To earn money with a Trading system, it is not necessary to win all the operations, what is really important is the final result of the operation. A Trading system has to have positive mathematical expectation as is the case with this script: ME = (0.87 x 30.74$) - (0.13 x 56.16$) = (26.74 - 7.30) = 19.44$ > 0

The game of roulette, for example, has negative mathematical expectation for the player, it can have positive winning streaks, but in the long term, if you continue playing you will end up losing, and casinos know this very well.

PARAMETERS

'BACKTEST DAYS': Number of days back of historical data for the calculation of the Backtest.

'ENTRY TYPE': For '% EQUITY' if you have $ 10,000 of capital and select 7.5%, for example, your entry would be $ 750 without leverage. If you select CONTRACTS for the 'BTCUSDT' pair, for example, it would be the amount in 'Bitcoins' and if you select 'CASH' it would be the amount in $ dollars.

'QUANTITY (LEVERAGE 1X)': The amount for an entry with X1 leverage according to the previous section.

'MAXIMUM LEVERAGE': It's the maximum allowed multiplier of the quantity entered in the previous section according to the volume condition.

The settings are for Bitcoin at Binance Futures (BTC: USDTPERP) in 30 minutes.

For other pairs and other timeframes, the settings have to be adjusted again. And within a month, the settings will be different because we all know the market and the trend are changing.

█ 888 BOT (SPANISH)

Este es un Expert Advisor 'EA' o script de trading automatizado para ‘longs’ y ‘shorts’, el cual, utiliza solo un Take Profit o, en el peor de los casos, un Stop Loss para cerrar el trade.

Es una versión muy mejorada del anterior ‘Repanocha’. No utiliza ‘Trailing Stop’, ni funciones ‘security()’ (aunque usar una función security no significa que el script repinte) y todas las señales son confirmadas, por consiguiente, el script no repinta en modo alertas y es preciso en en el modo backtest.

Aparte de los anteriores indicadores se han añadido algunos más y otras funciones para Stop-Loss, de re-entrada y apalancamiento.

Utiliza 8 indicadores, (muchos ya sabéis sobradamente lo que son, pero por si hay alguien nuevo), son los siguientes:

1. Jurik Moving Average

Es una media móvil creada por Mark Jurik para profesionales la cual elimina el ‘lag’ o retardo de la señal. Es mejor que otras medias móviles como la EMA, DEMA, AMA o T3.

Hay dos formas de disminuir el ruido utilizando JMA. El aumento del parámetro 'LENGTH' hará que JMA se mueva más lentamente y, por lo tanto, reducirá el ruido a expensas de añadir ‘lag’

Los parámetros 'JMA LENGTH', 'PHASE' y 'POWER' ofrecen una forma de seleccionar el equilibrio óptimo entre ‘lag’ y sobre impulso.

Verde : Alcista, Rojo: Bajista.

2. Range filter

Creado por Donovan Wall, su función es la de filtrar o eliminar el ruido y poder determinar mejor la tendencia del precio a corto plazo.

Primero, se calcula un rango de precio promedio uniforme 'SAMPLING PERIOD' para la base del filtro y se multiplica por una cantidad específica 'RANGE MULTIPLIER'.

A continuación, el filtro se calcula ajustando los movimientos de precios que no exceden el rango especificado.

Por último, los rangos objetivo se trazan para mostrar los precios que activarán el movimiento del filtro.

Verde : Alcista, Rojo: Bajista.

3. Average Directional Index (ADX Classic) y (ADX Masanakamura)

Es un indicador diseñado por Welles Wilder para medir la fuerza y dirección de la tendencia del mercado. El movimiento del precio tiene fuerza cuando el ADX tiene pendiente positiva y está por encima de cierto nivel mínimo 'ADX THRESHOLD' y para un periodo dado 'ADX LENGTH'.

El color verde de las barras indica que la tendencia es alcista y que el ADX está por encima del nivel establecido por el threshold.

El color Rojo de las barras indica que la tendencia es bajista y que el ADX está por encima del nivel de threshold.

El color naranja de las barras indica que el precio no tiene fuerza y seguramente lateralizará.

Se puede elegir entre la opción clásica y la creada por un tal 'Masanakamura'. La diferencia principal entre los dos es que en el primero utiliza RMA() y en el segundo SMA() en su cálculo.

4. Parabolic SAR

Este indicador, creado también por Welles Wilder, coloca puntos que ayudan a definir una tendencia. El Parabolic SAR puede seguir al precio por encima o por debajo, la particularidad que ofrece es que cuando el precio toca al indicador, este salta al otro lado del precio (si el Parabolic SAR estaba por debajo del precio salta arriba y viceversa) a una distancia predeterminada por el indicador. En este momento el indicador vuelve a seguir al precio, reduciendo la distancia con cada vela hasta que finalmente es tocado otra vez por el precio y se vuelve a iniciar el proceso. Este procedimiento explica el nombre del indicador: el Parabolic SAR va siguiendo al precio generando una característica forma parabólica, cuando el precio lo toca, se para y da la vuelta (SAR son las siglas en inglés de ‘stop and reverse’), dando lugar a un nuevo ciclo. Cuando los puntos están por debajo del precio, la tendencia es alcista, mientras que los puntos por encima del precio indica una tendencia bajista.

5. RSI with Volume

Este indicador lo creo un tal LazyBear de TV a partir del popular RSI.

El RSI es un indicador tipo oscilador utilizado en análisis técnico y creado también por Welles Wilder que muestra la fuerza del precio mediante la comparación de los movimientos individuales al alza o a la baja de los sucesivos precios de cierre.

LazyBear le añadió un parámetro de volumen que lo hace más preciso al movimiento del mercado.

Una buena forma de usar el RSI es teniendo en cuenta la línea central de 50 'RSI CENTER LINE'. Cuando el oscilador está por encima, la tendencia es alcista y cuando está por debajo la tendencia es bajista.

6. Moving Average Convergence Divergence (MACD) y (MAC-Z)

Fue creado por Gerald Appel. Posteriormente se añadió el histograma para anticipar el cruce de medias. A grandes rasgos podemos decir que el MACD es un oscilador consistente en dos medias móviles que van girando en torno a la línea de cero. La línea del MACD no es más que la diferencia entre una media móvil corta 'MACD FAST MA LENGTH' y una media móvil larga 'MACD SLOW MA LENGTH'. Es un indicador que nos permite tener una referencia sobre la tendencia del activo sobre el cual se está operando, generando de este modo señales de entrada y salida del mercado.

Podemos hablar de mercado alcista cuando el histograma del MACD se sitúe por encima de la línea cero, junto con la línea de señal, mientras que hablaremos de mercado bajista cuando el histograma MACD se situará por debajo de la línea cero.

Está la opción de utilizar el indicador MAC-Z creado por LazyBear que según su autor es más eficaz, por utilizar el parámetro VWAP (precio medio ponderado por volumen) 'Z-VWAP LENGTH' junto con una desviación standard 'STDEV LENGTH' en su cálculo.

7. Volume Condition

El volumen indica el número de participantes en esta guerra entre toros y osos, cuanto más volumen más probabilidad de que se mueva el precio a favor de la tendencia. Un volumen bajo de negociación indica un menor número de participantes e interés por el instrumento en cuestión. Los bajos volúmenes pueden revelar debilidad detrás de un movimiento de precios.

Con esta condición se filtran aquellas señales cuyo volumen es inferior a la SMA de volumen para un periodo 'SMA VOLUME LENGTH' multiplicado por un factor 'VOLUME FACTOR'. Además, determina el apalancamiento utilizado, a más volumen, más participantes, más probabilidad de que se mueva el precio a nuestro favor, es decir, podemos utilizar más apalancamiento. El apalancamiento en este script lo determina las veces que está el volumen por encima de la línea de la SMA.

El apalancamiento máximo es de 8.

8. Bollinger Bands

Este indicador fue creado por John Bollinger y consiste en tres bandas que se dibujan superpuestas al gráfico de evolución del precio.

La banda central es una media móvil, normalmente se emplea una media móvil simple calculada con 20 períodos. ('BB LENGTH' Número de periodos de la media móvil)

La banda superior se calcula sumando al valor de la media móvil simple X veces la desviación típica de la media móvil. ('BB MULTIPLIER' Número de veces la desviación típica de la media móvil)

La banda inferior de calcula restando a la media móvil simple X veces la desviación típica de la media móvil.

la franja comprendida entre las bandas superior e inferior contiene, estadísticamente, casi un 90% de las posibles variaciones del precio, lo que significa que cualquier movimiento del precio fuera de las bandas tiene especial relevancia.

En términos prácticos, las bandas de Bollinger se comporta como si de una banda elástica se tratara de manera que, si el precio las toca, éste tiene mucha probabilidad de rebotar.

En ocasiones, después de rellenarse la orden de entrada, el precio se devuelve hacia el lado contrario. Si toca la banda de Bollinger se rellena otra orden en la misma dirección de la posición para mejorar el precio medio de entrada, (% MINIMUM BETTER PRICE': Precio mínimo para que se ejecute la re-entrada y que sea mejor que el precio de la posición anterior en un % dado) de esta manera damos una oportunidad al trade de que el Take Profit se ejecute antes. La desventaja es que se dobla el tamaño de la posición. 'ACTIVATE DIVIDE TP': Divide el tamaño del TP a la mitad. Más probabilidad de que se cierre el trade pero menos ganancias.

█ STOP LOSS y RISK MANAGEMENT.

Una buena gestión de las pérdidas o gestión del riesgo es lo que puede hacer que tu cuenta suba o se liquide en poco tiempo.

El % de riesgo es el porcentaje de nuestro capital que estamos dispuestos a perder por operación. Este se aconseja que debe estar comprendido entre un 1-5%.

% Risk = (% Stop Loss x % Equity per trade x Leverage) / 100

Primero se calcula la estrategia con Stop Loss, después se determina el riesgo por operación y a partir de ahí se calcula el monto por operación y no al revés.

En este script puedes usar un Stop Loss normal o uno según el ATR. También activar la opción de que salte antes si se alcanza el porcentaje de riesgo. '% RISK ALLOWED'

'STOP LOSS CONFIRMED': Solamente se activa el Stop Loss si el cierre de la barra anterior se encuentra en la condición de límite de pérdidas. Es útil para evitar que se dispare el SL cuando hacen un ‘pump’ para barrer Stops y luego se devuelve el precio a la normalidad.

█ BACKTEST

El objetivo del Backtest es evaluar la eficacia de nuestra estrategia. Un buen Backtest lo determinan algunos parámetros como son:

- RECOVERY FACTOR: Consiste en dividir el ‘beneficio neto’ entre el ‘drawdown’. Un excelente sistema de trading tiene un recovery factor de 10 o más; es decir, genera 10 veces más beneficio neto que drawdown.

- PROFIT FACTOR: El ‘Profit Factor’ es otra medida popular del rendimiento de un sistema. Es algo tan simple como dividir lo que ganan las operaciones con ganancias entre lo que pierden las operaciones con pérdidas. Si la estrategia es rentable entonces por definición el ‘Profit Factor’ va a ser mayor que 1. Las estrategias que no son rentables producen factores de beneficio menores que uno. Un buen sistema tiene un profit factor de 2 o más. Lo bueno del ‘Profit Factor’ es que nos dice lo que vamos a ganar por cada dolar que perdemos. Un profit factor de 2.5 nos dice que por cada dolar que perdamos operando vamos a ganar 2.5.

- SHARPE: (Retorno sistema – Retorno sin riesgo) / Desviación de los retornos.

Cuando las variaciones de ganancias y pérdidas son muy altas, la desviación es muy elevada y eso conlleva un ratio de ‘Sharpe’ muy pobre. Si las operaciones están muy cerca de la media (poca desviación) el resultado es un ratio de ‘Sharpe’ bastante elevado. Si una estrategia tiene un ratio de ‘Sharpe’ mayor que 1 es una buena estrategia. Si tiene un ratio de ‘Sharpe’ mayor que 2, es excelente. Si tiene un ratio de ‘Sharpe’ menor que 1 entonces no sabemos si es buena o mala, hay que mirar otros parámetros.

- MATHEMATICAL EXPECTATION:(% operaciones ganadoras X ganancia media) + (% operaciones perdedoras X pérdida media).

Para ganar dinero con un sistema de Trading, no es necesario ganar todas las operaciones, lo verdaderamente importante es el resultado final de la operativa. Un sistema de Trading tiene que tener esperanza matemática positiva como es el caso de este script.

El juego de la ruleta, por ejemplo, tiene esperanza matemática negativa para el jugador, puede tener rachas positivas de ganancias, pero a la larga, si se sigue jugando se acabará perdiendo, y esto los casinos lo saben muy bien.

PARAMETROS

'BACKTEST DAYS': Número de días atrás de datos históricos para el calculo del Backtest.

'ENTRY TYPE': Para % EQUITY si tienes 10000$ de capital y seleccionas 7.5% tu entrada sería de 750$ sin apalancamiento. Si seleccionas CONTRACTS para el par BTCUSDT sería la cantidad en Bitcoins y si seleccionas CASH sería la cantidad en dólares.

'QUANTITY (LEVERAGE 1X)': La cantidad para una entrada con apalancamiento X! según el apartado anterior.

'MAXIMUM LEVERAGE': Es el máximo multiplicador permitido de la cantidad introducida en el apartado anterior según la condición de volumen.

Los settings son para Bitcoin en Binance Futures (BTC:USDTPERP) en 30 minutos.

Para otro pares y otras temporalidades se tienen que ajustar las opciones de nuevo. Además para dentro de un mes, los ajustes serán otros distintos ya que el mercado y la tendencia es cambiante.

MARUSIA TRADING STRATEGIES [VCRYPTO]Description of MARUSIA TRADING STRATEGIES

«MARUSIA» is a compilation of several strategies.

You may choose the one which best suits your trading habit from options menu.

The strategies are based on indicator’s and bar’s closing level analysis on different timeframes.

At the time being there are 3 types of strategies for BTC on 1H and 3H tf.

+++ BTC 1H 90% Success +++ (Beginner)

Instrument - BTC, timeframe – 1H, exchange – Bitmex.

The advantage of the strategy is a high quantity of profitable trades (90% at the time of publishing).

The Trading View backtest results from 2019:

+ 303% net profit

+ 90% profitable trades

+ 6% drawback

+++ BTC 1H Mega Scalper +++ (Intermediate)

Instrument - BTC, timeframe – 1H, exchange – Bitmex.

The advantage of the strategy is more frequent trades with a good probability of success.

The Trading View backtest results from 2019:

+ 792% net profit

+ 64% profitable trades

+ 5% drawback

+++ BTC 3H Mega Scalper +++ (Expert)

Instrument - BTC, timeframe – 3H, exchange – Bitmex.

The advantage of the strategy is more frequent trades with a good probability of success.

The Trading View backtest results from 2018:

+ 1637% net profit

+ 79% profitable trades

+ 4,4% drawback

HOW TO USE

1. Choose the strategy from the strategy’s option menu on the chart. Pay attention to the instrument and timeframe you are using the selected strategy for.

2. Wait until you see green (above bar) or orange (below bar) label. To receive an alert when these labels (or signals) appear on the chart use ALERT INDICATOR for this strategy.

3. On the opening of the next bar enter the position if the label on the previous bar hasn’t disappeared. Green – for Buy, orange – for Sell. In this case you will see Buy/Sell signal on the chart.

4. Putting TRAILING STOPS

4.1. You should put a trailing stop when the price moves to profit up or down for 1% from your entry. For example, if you are long at 7255 USD and price moves up to 7328 USD (7255*1.01), put trailing stop with a trailing value 0,4% of your entry price, which is 29 USD (7255*0.004).

4.2. Every time when there is a long or short position, you may see a green info label with entry price, trail stop activation level and trail value. You may use this information instead of making a calculation by yourself. Only if your entry is the same as in the label.

5. Position closing maybe by reaching your trailing stop (in this case you may reenter the position on the next bar, if there is a signal label as per step 2 on the bar where your trailing stop is triggered) or when there is a signal for opposite direction.

6. If the signals appear differently than described as above, just refresh the website of Trading View. This happens because mostly take profits are shown only after the current bar is closed.

• The Buy/Sell signal label may move up or down on the bar with price’s movement. Don’t worry it doesn’t mean that your entry is changing.

• The lines on the chart are weekly price levels – the price levels of the previous week –

Green – open, Red – close, Blue – high, Brown – low, Black – hl2 (average of high and low). You may use them as support and resistance levels.

***

+ Trading View backtest results

+No repaint

+ Several strategies to choose which suits your trading habit

+Free testing

+Support with a call

Pm to get access to the strategy.

____________________________________________________________________________

Описание к стратегии "MARUSIA TRADING STRATEGIES "

Сборник нескольких стратегий серии "Marusia"

Выбор конкретной стратегии осуществляется из удобного меню

Основа наших стратегий - совмещение индикаторного анализа и анализа уровня закрытия свечей на разных временных интервалах (анализ уровней).

+++ BTC 1H 90% Success +++ (Beginner)

Стратегия работает на инструменте Bitcoin (BTC) по котировкам биржи BITMEX на 1 часовом таймфрейме (1H).

Основное преимущество данной стратегии - супервысокая успешность сделок (более 90% на момент публикации).

Данная стратегия представляет собой гибрид среднесрочных стратегий по частоте сделок (с 2019 по 12.04.2020 - 204 сделки, в среднем одна сделка раз в 2 дня) и элемент высокочастотных (скальп) стратегий - необходимо выставление использование скользящего стоп-приказа (trailing stop-loss), расчетные данные по которому появляются прямо на экране при открытии сделки.

Статистика по данной стратегии, подтвержденная бэктестом в Trading View

С 2019 года до момента публикации стратегии бектест показывает следующие данные:

+ 303% чистой прибыли

+ 90% успешных сделок

+ 6% макс. единовременная просадка

+++ BTC 1H Mega Scalper +++ (Intermediate)

Стратегия работает на инструменте Bitcoin (BTC) по котировкам биржи BITMEX на 1 часовом таймфрейме (1H)

Основное преимущество данной стратегии - высокочастотные сделки с хорошей вероятностью успеха.

С 2019 года до момента публикации стратегии бектест Trading View показывает следующие данные:

+ 792% чистой прибыли

+ 64% успешных сделок

+ 5% макс. единовременная просадка

+++ BTC 3H Mega Scalper +++ (Expert)

Стратегия работает на инструменте Bitcoin (BTC) по котировкам биржи BITMEX на 3 часовом таймфрейме (3H)

Основное преимущество данной стратегии - высокочастотные сделки с хорошей вероятностью успеха

С 2019 года до момента публикации стратегии бектест Trading View показывает следующие данные:

+ 1637% чистой прибыли

+ 79% успешных сделок

+ 4,4% макс. единовременная просадка

***

Инструкиция по использованию:

1. Вы открываете график с включенной стратегией. Обратите внимание на инструмент и таймфрейм стратегии.

2. Ожидаете появления на графике зеленого (снизу) или оранжевого (сверху) флажка.

Для получения уведомления появления значков (сигналов) используйте АЛЕРТНЫЙ ИНДИКАТОР для данной стратегии.

3. На открытии следующей свечи входите в сделку, если флажек из п.2 остался и не пропал (зеленый флажек - покупка, оранжевый - продажа)

4. Выставление trailing stop-loss

4.1 Trailing stop-loss выставляется, когда цена прошла 1% в профит от цены выхода в сделку (например: покупка 7255 и когда цена будет 7328 (7255*1,01) выставляется плавающий стоп-лосс (trailing stop-loss) в размере 0,4% от цены входа "29" (7255*0,004).

4.2. Как только будет закрыта свеча, на которой Вы вошли в сделку - вы увидете значения из п.4.1 на экране рядом с графиком (вы можете их использовать без самостоятельного расчета, но тогда есть риск, что если цена на свече входа достигнет значения из п. 4.1 - то сделка закроется, а вы это увидите только на следующей свече, когда значение цены может быть менее выгодное)

5. Выход из сделки осуществляется либо по trailing stop-loss (тогда вы можете перезайти в сделку на открытии следующей свечи, если на свече, на которой произошло закрытие по trailing stop-loss появились флажки из п.2), либо по появлению противоположного флажка, тогда вход в сделку, в соответствии с п. 2 и 3

7. Если Вы увидели, что сигналы отличаются от написанного в данной инструкции - просто обновите страницу с Trading View в браузере и все встанет на свои места.

* На свече захода в сделку сигнал "buy/sell" может "плавать" по свече, но если Вы выполнили п.1-3 Вам неочем беспокоиться. Не обращайте на него внимание.

***

Основные отличия от стратегий наших коллег:

+ Результаты бэктеста в платформе Trading View – прозрачная статистика по сделкам, которую вы можете посмотреть самостоятельно

+ Построен на принципах non-repaint basis – сигналы не исчезают (при правильном соблюдении инструкции по использованию)

+ Каждая стратегия серии построена на своем уникальном принципе - вы можете выбрать для себя оптимальный набор стратегий

+ Бесплатный тестовый период

+ Поддержка с возможностью организации телефонного звонка

Для предоставления доступа к данной стратегии - пожалуйста пишите в личные сообщения. Мы быстро с Вами свяжемся.

VITALIY ETHEREUM 3H STRATEGY [VCRYPTO]DESCRIPTION OF VITALIY ETH 3H STRATEGY

This strategy is made for trading ETHEREUM ( ETH ) using data from BITMEX exchange on 3 hour timeframe.

There is also a special indicator for the strategy to receive alerts on your tradingview platform which is very handful to enter the market as soon as there is a buy/sell signal.

Strategy is based on Pine script v.4 and it uses several indicators and oscillators to generate a buy/sell signal for ETH .

There is no repaint, which means that a signal will not disappear when price goes in wrong direction. I.e when a signal is generated, it

will be listed in trade history after bar's close and wont be changed.

And this is one of the advantages of the strategy over other 90% strategies.

The profitability curve of the strategy also has a stable growth, which means that the strategy is profitable at any phase the market,

not only at any particalar moment.

The strategy is a SWING strategy, which means that a signal for opening a position (buy or sell) at the same time closes previous position.

Because of its specificity the strategy doesn’t have take profit/stop loss options and it is not recommended to use leverage.

Your risc is limited by time interval from opening one position and opening another one when the price reverses.

The strategy has a backtest statistics on TradingView. 2018 – 141%, 2019 – 171%, until Apr. 6th, 2020 – 103%, from 2018 till Apr. 6th, 2020 - 417% of net profit

Max drawdown (the sum of non-profitable trades until receiving a profitable trade) during a year not more than 12.44%.

The strategy is published for testing and will be free to use during this period of time.

To get access to the strategy after testing finishes write in comments and pm me.

______________________________________________________________________________________________________________________

ОПИСАНИЕ VITALIY ETH 3H STRATEGY

Стратегия работает на инструменте Ethereum (ETH) по котировкам биржи BITMEX на 3 часовом таймфрейме (3H), а также имеет удобные алерты для сигналов на покупку/продажу.

Это позволит Вам заниматься своими делами, не следя за тем, что происходит на рынке, но в нужное время совершить сделку, получив предупреждение на телефон / компьютер.

Стратегия построена на последней версии Pine Script, в ее основе лежит совокупность множества индикаторов и правил, которые в определенный момент дают сигнал на покупку или продажу ETH. Стратегия основана на "non-repaint" базисе, таким образом, если стратегия показала вход в сделку (по итогу закрытия свечи) - то данная сделка так и остается без изменений и записывается в историю сделок. Это выгодно отличает данную стратегию от 90% таковых в Trading View и дает уверенность, что появившийся сигнал на сделку не исчезнет в случае, если рынок пойдет в противоположную сторону. Данный фактор означает, что статистика по данной стратегии не будет "нарисована", как в большинстве других стратегий. Также, не маловажным фактором является поступательная кривая доходности, что означает, что стратегия будет зарабатывать на всех фазах рынка, а не только в определенный момент времени.

Данная стратегия относится к сегменту SWING стратегий, когда один сигнал является одновременно закрытием одной сделки и открытием противоположной.

В связи со спецификой стратегии она не использует стоп-ордера, поэтому предполагает торговлю строго без плечей. Если вы хотите снизить риск по данной стратегии, то можете заходить в сделки пониженным объемом средств.

Ваш риск ограничен временным интервалом от момента, как цена пошла в противоположную сторону, до момента пока стратегия не дала сигнал на перекладку в новую сделку.

Статистика, подтвержденная бэктестом в Trading View, за последние пару лет: 2018 - 141%, 2019 - 171%, на 06.04.2020 - 103%, с 2018 по 06.04.2020 - 417%. Это данные по Чистой прибыли на вложенный капитал. Максимальная просадка ("Max drawdown" по данным Trading View) за период с 2018 по 06.04.2020 не превысила 12,44%

Для предоставления доступа к данной стратегии - пожалуйста пишите в комментариях запрос с копией в личные сообщения. Мы быстро с Вами свяжемся.

Underworld Hunter Backtesting AlgorhitmThis strategy is built to prove the profitability of my Underworld Hunter indicator . It tests two different strategies. I won't be going into the calculation again since it is part of the original script. I just made a few adjustments.

First one is clearly visual. It plots slimmer twin-coloured lines now and has a different colour for every extreme level. Second is less obvious - I switched Relative Strength Index for Commodity Channel Index.

Extreme levels are as follows: green 100 -► 120, yellow 120 -► 140, orange 140 -► 160, red 160 -► 180 and purple above 180, I will have a special separate algorithm for testing optimal CCI levels someday, in this script, these values are only meant to help you with manual operations and do not influence results of the strategy in any way.

#Trending strategy

The trending strategy opens a position whenever the price leaves the bands and holds it until two consecutive bars are closed within the bands. The picture shows one winning position that hasn't yet been resulted. It also shows a few fakeouts. For this strategy, you want to keep the length below 110, the deviation should be below 2 and you probably want to play lower timeframes.

#Within the bands

The second strategy is pretty much the opposite. It opens a position when the price reaches outer bands and holds it until two consecutive bars are closed within the bands and current bar closes below previous bars low in case of long. It is working on hourly timeframes and you need higher length and deviation to succeed. The picture shows a few positions on EURUSD. Each of them is profitable but would be much higher if you closed it manually when it was time. You need to enable this strategy, which automatically disables the other one.

When using my script, you need to bear in mind that the first strategy doesn't detect optimal levels to close the price. A trend is often followed by a less volatile and boring correction which causes bands to shrink and lower your profits if you don't close manually as it will take longer till bands are reached.

On the other hand, second script literally has no stop-loss. As long as the price is outside the range, it will never close which will cause major drawdowns, unless you control the trade manually. CCI is here to help you with both.

I also recommend combining this with Market Profile (on TW, there is only Volume Profile, which can be used in a similar way) and trading day theory (trending with multiple distributions, trending day, normal day, a variation on a normal day, non-trending day or neutral day). Always keep in mind that it is up to traders to be profitable, indicators can support a good trader, but they will not fix a bad one.

XPloRR S&P500 Stock Market Crash Detection Strategy v2XPloRR S&P500 Stock Market Crash Detection Strategy v2

Long-Term Trailing-Stop strategy detecting S&P500 Stock Market Crashes/Corrections and showing Volatility as warning signal for upcoming crashes

Detecting or avoiding stock market crashes seems to be the 'Holy Grail' of strategies.

Since none of the strategies that I tested can beat the long term Buy&Hold strategy, the purpose was to detect a stock market crash on the S&P500 and step out in time to minimize losses and beat the Buy&Hold strategy. So beat the Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

With the default parameters the strategy generates 10262% profit (starting at 01/01/1962 until release date), with 10 closed trades, 100% profitable, while the Buy&Hold strategy only generates 3633% profit, so this strategy beats the Buy&Hold strategy by 2.82 times !

Also the strategy detects all major S&P500 stock market crashes and corrections since 1962 depending on the Trailing Stop Smoothness parameter, and steps out in time to cut losses and steps in again after the bottom has been reached. The 5 major crashes/corrections of 1987, 1990, 2001, 2008 and 2010 were successfully detected with the default parameters.

The script was first released on November 03 2019 and detected the Corona Crash on March 04 2020 with a Volatility crash-alert and a Sell crash-alert.

I have also created an Alerter Study Script based on the engine of this script, which generates Buy, Sell and Volatility signals.

If you are interested in this Alerter version script, please drop me a mail.

The script shows a lot of graphical information:

the Close value is shown in light-green. When the Close value is temporarily lower than the Buy value, the Close value is shown in light-red. This way it is possible to evaluate the virtual losses during the current trade.

the Trailing Stop value is shown in dark-green. When the Sell value is lower than the Buy value, the last color of the trade will be red (best viewed when zoomed)

the EMA and SMA values for both Buy and Sell signals are shown as colored graphs

the Buy signals are labeled in blue and the Sell signals are labeled in purple

the Volatility is shown below in green and red. The Alert Threshold (red) is default set to 2 (see Volatility Threshold parameter below)

How to use this Strategy?

Select the SPX (S&P500) graph and add this script to the graph.

Look in the strategy tester overview to optimize the values Percent Profitable and Net Profit (using the strategy settings icon, you can increase/decrease the parameters), then keep using these parameters for future Buy/Sell signals on the S&P500.

More trades don't necessarily generate more overall profit. It is important to detect only the major crashes and avoid closing trades on the smaller corrections. Bearing the smaller corrections generates a higher profit.

Watch out for the Volatility Alerts generated at the bottom (red). The Threshold can by changed by the Volatility Threshold parameter (default=2% ATR). In almost all crashes/corrections there is an alert ahead of the crash.

Although the signal doesn't predict the exact timing of the crash/correction, it is a clear warning signal that bearish times are ahead!

The correction in December 2018 was not a major crash but there was already a red Volatility warning alert. If the Volatility Alert repeats the next weeks/months, chances are higher that a bigger crash or correction is near. As can be seen in the graphic, the deeper the crash is, the higher and wider the red Volatility signal goes. So keep an eye on the red flag!

Here are the parameters:

Fast MA Buy: buy trigger when Fast MA Buy crosses over the Slow MA Buy value (use values between 10-20)

Slow MA Buy: buy trigger when Fast MA Buy crosses over the Slow MA Buy value (use values between 21-50)

Minimum Buy Strength: minimum upward trend value of the Fast MA Buy value (directional coefficient)(use values between 10-100)

Fast MA Sell: sell trigger when Fast MA Sell crosses under the Slow MA Sell value (use values between 10-20)

Slow MA Sell: sell trigger when Fast MA Sell crosses under the Slow MA Sell value (use values between 21-50)

Minimum Sell Strength: minimum downward trend value of the Fast MA Sell value (directional coefficient)(use values between 10-100)

Trailing Stop ATR: trailing stop % distance from the smoothed Close value (use values between 2-20)

Trailing Stop Smoothness: MA value for smoothing out the Trailing Stop close value

Buy On Start Date: force Buy on start date even without Buy signal (default: true)

Sell On End Date: force Sell on end date even without Sell signal (default: true)

Volatility EMA Period: MA value of the Volatility value (default 15)

Volatility Threshold: Threshold value to change volatility graph to red (default 2)

Volatility Graph Scaler: Scaling of the volatility graph (default 5)

Important : optimizing and using these parameters is no guarantee for future winning trades!

Super Algorithm Strategy (Joy Bangla)This is the strategy tester for the

Below are the performance results

Starting with $10,000

Net Profit: 88%

66% profitable trades

34% losing trades. Do look at the losing trades. If one did careful moment management, some of those may end up profitable as well.

4.158 Profit factor.

16.1% drawdown. I would go a bit more and say if I am using this, my risk management should ensure for a stop loss of 20%.

66 bars on average (aka it holds for a long time. So, one needs to look into the funding factor in money management)

Sharpe Ratio: 0.291

Only 7 trades done (with 6 closed) in 2 and a half years. So this absolutely reduces noise as much as possible.

In short, if I had $10000 of BTC beginning of 2018, I would be having $18,878 worth of btc right now.

With 4x leverage, this could be a huge potential.

For info on gaining access see the ⬇ link below ⬇ in our signature field & direct message me. I have a busy schedule at my own workplace. Trading is my hobby. Hence, please be kind to me if I am late in replying.

Cracking Cryptocurrency - Bottom Feeder Strategy TesterBottom Feeder - Strategy Tester

The Bottom Feeder is designed to algorithmically detect significantly oversold conditions in price that represent profitable buying opportunities. Combining this with it’s unique Stop and Target System, the Bottom Feeder is designed to return consistent return with minimal draw down. Whether used as a Market Bottom Detector or as a system for executing safe, profitable mean reversion trades, the Bottom Feeder is a powerful tool in any trader’s arsenal.

Bottom Feeder was designed to be used on BTCUSD, however it is also effective on other USD/USDT pairs. One will have to check the individual pair they wish to trade with the Strategy Tester to simulate performance.

Strategy displayed is from 2018-2021 on **Conservative Mode** with Percent of Equity (30%) enabled.

Options

Let’s go through the input options one by one, so that you are able to comfortably navigate all that this indicator has to offer. The link below will display a picture of the layout of the settings for your convenience.

For the sake of simplicity, let’s note now that all settings marked **Conservative Mode** will not work in Aggressive Mode.

Mode : Determines how aggressively Bottom Feeder generates a buy signal. In Conservative Mode, trades can only be opened once per candle and the stop and target will update as new signals appear. In Aggressive Mode, a separate trade is opened each time Bottom Feeder signals, which may be multiple times within one Daily candle.

Position Sizing Strategy : Determines what Risk Management system you will deploy when trading Bottom Feeder. Your options are “Percent of Equity” and “Distance to Stop Loss”. If Percent of Equity is selected, a trade size will be equal to a percentage of your equity, pursuant to the value in the ‘Percent of Equity’ box. If Distance to Stop Loss is selected, then your Position Size will be determined based off the distance to your stop loss and the value in the ‘Risk Percentage’ box.

Percent Of Equity : Determines what percentage of your equity will be allocated to each trade when ‘Position Sizing Strategy’ is enabled.

Risk Percentage : Determines the size of each trade if ‘Distance to Stop Loss’ strategy is enabled. This value reflects what percent of your account you will lose per trade if the trade hits your stop loss.

Plot Target and Stop Loss : Toggles on/off the visualized take profit and stop losses on the chart.

**Conservative Mode** TP Multiplier : This is an input box, it requires a float value. That is, it can accept either a whole number integer or a number with a decimal. This number will determine your Take Profit target. It will take whatever number is entered into this box and multiply the Average True Range against it to determine your Take Profit.

**Conservative Mode** SL Multiplier : See above - this will modify your Stop Loss Value.

**Conservative Mode** Average or Median True Range : This is a drop-down option, the two options are Average True Range or Median True Range. If Average True Range is selected, then this indicator will use the Average True Range calculation, that is, the average of a historical set of True Range values to determine the Average True Range value for Target and Stop Loss calculation. If Median True Range is selected, it will not take an average and will instead take the Median value of your historical look back period.

**Conservative Mode** True Range Length : This is an input that requires an integer. This will represent your historical lookback period for Average/Median True Range calculation.

**Conservative Mode** True Range Smoothing : This is a drop-down with the following options: Exponential Moving Average ( EMA ), Simple Moving Average ( SMA ), Weighted Moving Average ( WMA ), Relative Moving Average (RMA). This will determine the smoothing type for calculating the Average True Range if it is selected. Note: if Median True Range is selected above, this option will not have any effect as there is no smoothing for a Median value.

**Conservative Mode** Custom True Range Value? : This is a true/false option that is false by default. If enabled, it will override the Average/Median True Range calculation in favor of a users custom True Range value to be input below.

**Conservative Mode** Custom True Range Value : This is an input box that requires a float value. If Custom True Range is enabled this is where a user will input their desired custom True Range value for Target and Stop Loss calculation.

From Month/Day/Year to Month/Day/Year : This sets the Time Frame of your backtest for the Bottom Feeder Strategy. It will run FROM the date selected TO the date selected.

Stop and Target Description

Because Bottom Feeder is designed only to scalp the various market bottoms that can appear over time in the market and not to identify trends or to trade ranges, it’s imperative that the indicator notify us not just to when to enter our trades, but when to exit! In the service of that, CC Bottom Feeder has a built in Stop and Target system that tracks and displays the stop loss and take profit levels of each individual open trade, whether in Aggressive or Conservative Mode.

Conservative Mode Targeting: In Conservative Mode, Bottom Feeder signals are aggregated into a compound trade. The signal will appear as a green label pointing up below a candle, and will appear upon a candle close. If Bottom Feeder then generates another signal the stop loss and target price will be updated. The process will continue until the aggregated trade completes in either direction. On a trade with multiple signals, a larger position is slowly entered into upon each buy signal.

Aggressive Mode Targeting: In Aggressive Mode, Bottom Feeder signals are individually displayed as they are generated, regardless of how many signals are generated on any single candle. If Bottom Feeder continues to signal, each individual open trade will have their own stop loss and target that will be displayed on the chart until the individual trade completes in either direction. As opposed to a large compound position, aggressive mode represents a higher number of independent signals with their own stop and target levels.

Stop losses and targets are designed to be hard, not soft. That is, they are intended to be stop market orders, not mental stop losses. If price wicks through the target or stop, it will activate.

Strategy - Backtest Uber SSL Channel / SSL Indicator [UTS]Backtesting of Uber SSL Channel / SSL Indicator

Backtest with focus win/loss profitability. Formula: profitability = win / (win+loss)

Do not put too much weight on trade PNL as the value is not necessary correct.

For example: on SL or TP hit an open position is marked as to be closed but executed on the open a new candle, thus leads to incorrect PNL.

Default equity 50k

Default 2% Risk per trade

Default currency USD

Define backtest interval precisely by month, year, day

ATR (len: 14, smooth: SMA)

ATR based Stop-Loss, if hit trade will be closed and considered as loss

ATR based Take-Profit, if hit trade will be closed and considered as win

If TP or SL is hit trade is closed and of course considered as win/loss

---

DM me / Tip (see Signature) or Subscribe for access

Strategy - Backtest Uber ASH - Absolute Strength Histogram [UTS]Backtesting of Uber ASH - Absolute Strength Histogram

Backtest with focus win/loss profitability. Formula: profitability = win / (win+loss)

Do not put too much weight on trade PNL as the value is not necessary correct.

For example: on SL or TP hit an open position is marked as to be closed but executed on the open a new candle, thus leads to incorrect PNL.

Default equity 50k

Default 2% Risk per trade

Default currency USD

Define backtest interval precisely by month, year, day

ATR (len: 14, smooth: SMA)

ATR based Stop-Loss, if hit trade will be closed and considered as loss

ATR based Take-Profit, if hit trade will be closed and considered as win

If TP or SL is hit trade is closed and of course considered as win/loss

---

DM me / Tip (see Signature) or Subscribe for access

CS Trading Bot Strategy - Crypto EditionWhat is this strategy about?

The CS Trading Bot Strategy is for researching the most lucrative Crypto assets to be selected for in the corresponding Study (that actually generates alerts/signals).

The Strategy is very profitable for a vast amount of Crypto assets and the algorithm behind is not overfitted.

How to use it?

As a rule of thumb, the best time-frames are the 4h, 3h, 2h and 1h (sometimes 30M and 45M).

For many high profile/volume assets such as BTC, ETH and XRP the Daily is very profitable, as well. Weekly and Monthly time-frames should be avoided.

It is not recommended to apply this strategy to new assets with only a few weeks of history. I recommend a history of at least 6 months and 5 trades in the Strategy stats.

In the Strategy settings, you can adjust the time-span to see how the Strategy performs in certain conditions like bear-markets (see for example 4H on BTCUSDT from Jan 2018 - March 2019).

What to look for on researching?

If you are researching, make sure to look for these metrics in the Strategy overview:

Linear equity growth (especially over a larger period of time)

Low drawdown

Profitability above 50%

Average gain per trade of 5%

A satisfying profit for your selected time-span

Min. 5 trades, better 10

Min. 6 Months time-span

As a head-start, I suggest to research on the following assets, so you get a feeling about what to look for based on the list above:

POLONIEX:BTCUSDT

POLONIEX:ETHUSDT

POLONIEX:XRPUSDT

Why Poloniex? Because it has a long history for these assets...

Once you determined your favorite assets, you are ready to add the corresponding Study and within, set alerts for them.

Here the Webhooks are very interesting as you can forward your signals to your own trading bot or simply wait until my trading bot is available (currently in development)

Since I develop myself, rest assured it will be available soon. Look out for comments below as soon as it is available!

The bot is a commercial package including:

This Strategy for finding the best assets

The Study for setting alerts based on the best assets (webhooks, emails, popups, etc)

Access to our automated trading bot (separate download, as soon as available)

How to access?

If you are interested to get access to the complete package, please don't hesitate to send me a private message for a quote.

The amount of concurrent users using the package (=licenses) is limited to max. 500 a month (more we cannot manually handle has Tradingview has no automation for this yet).

Access to the bot package is based on a monthly basis. If you get access, you will asked in person at the end of the month if you want to continue or not.

PD Crypto Performer PRO (Backtest)Description:

This is the backtesting version of the PD Crypto Performer Pro (Alert) . You can choose to backtest either one of the two strategies included, a trend-identifying swing strategy and a low risk scalping strategy. Both strategies assume the same capital amount invested ($10,000) each trade. You can also see how your capital grows over time by enabling the reinvesting proceeds option. For details, please check out this tutorial .

The backtesting results could be easily improved in live trading by utilizing the “Take Profit” signals and following the recommended methods of use below.

To assist the decision-making process, the code currently references BTCUSD. As a result, it is only suitable for crypto traders. However, we are working on the stock and forex versions, and the Performer will have these compatibilities soon.

Most importantly, our signals DO NOT REPAINT !

Recommended Use:

- Time Frame: 1HR

- Asset: Large cap crypto assets.

For lower risk tolerance, we recommend using the indicator on ETHUSD. For maximizing profits, we recommend using the indicator on BCHUSD.

- Always set stop loss according to your own risk tolerance

- Take profits along the way. Check out this video tutorial for when to reenter after our take profit signals.

Recommended Use for Advanced Traders:

- Position sizing:

Larger position if the 1HR signal is in the same direction compared to the 4HR trend.

Smaller position if the 1HR signal is in the opposite direction compared to the 4HR trend.

- Better entry/exit points:

Track the 1HR signal for the asset you are trading on other exchanges along with the BTCUSD 1HR signal. Sometimes, the signals from different exchanges occur with a 1-2 hour difference. You could use these earlier signals along with a lower time frame (eg. 15min) entry confirmation from your own exchange for better entry / exit points.

- Use “Take Profit” signals for counter trend scalps. Recover at the reentering opportunities . This works best with candlestick pattern confirmations.

Never use this if you suspect a flag / inverted flag pattern is forming.

Go to www.phi-deltalytics.com and sign up for a FREE trial today!

Let us know if you have any questions or recommendations. We are here for your success!

Disclaimer:

It should not be assumed that the methods, techniques, or indicators presented will be profitable or that they will not result in losses. Past results are not necessarily indicative of future results. This is not a solicitation of any order to buy or sell.

JackTrendChaser V3Hi everyone! I am so thrilled to announce this!

>> LIMITED TIME OFFER, read below! <<

My name is Jack and I have been trading trends using TA on Forex for 10 years now and have within the past two years been trading Bitcoin and other cryptocurrencies.

I am a part time trader and developer. On a daily basis I work as a software developer creating various algorythms for big data usage - such as machine learning etc. and I have found a passion in creating scripts to predict major trend moves. Which is why I would like to share this script (strategy) with you all!

Looking at the stats it looks amazing! 100% profitability - who doesn't want that?! But that doesn't mean it cannot be improved - I am daily looking into how I can improve this to become even more profitable.

Currently the script have been tested with BTC and ETH:

BTC = 100% profitability and 9 trades since 2016

ETH = 83% profitability and 6 trades since 2016 with a drawdown of $5.

Now - 9 and 6 trades since 2016 isn't many trades but it suites my way of trading perfectly! I aim for the major trends and try to hit the pullbacks as soon as possible.

You can use this script alone or with other complimenting indicators. I like to draw some support and resistance levels for even further verification.

TRIAL OFFER:

Everyone is offered a 15 days trail.

Let me know in the comments if you would like a trail. Please do not PM me for trails.

>> LIMITED TIME OFFER <<

Since this is my first script to publish on TradingView I am offering the FIRST 10 traders a LIFETIME access to the script for a very small price! After that everyone else will be able to buy acces for 1m, 6m, 1y or lifetime (but at a higher price).

So how do you become one of the first 10?! Simpel - just PM me for the details.

I will update this post when the first 10 has been chosen.

>> OBS: I might be away from TradingView up to 24hours at a time because of my job - but don't panic! I will keep track of every message and get back to everyone as soon as possible!

Best regards

Jack

QuantCat 15M Trend Strategy [Crypto]**NOTE: IF YOU DO NOT OWN TRADINGVIEW PRO YOUR STRATEGIES WILL TAKE DATA FROM A SMALLER SAMPLE SIZE, AND THUS GIVE LESS ACCURATE BACKTESTING RESULTS TO THE ONES WE SHOW (LINKS WITH STEP 3) AND OPTIMISED OUR STRATEGIES WITH**

QuantCat 15M Crypto Trend Strategy

This strategy will allow you to absolutely smash the Crypto/USD pairs. We have optimised this strategy to work best for the Crypto/USD pairs on the 15 minute time frame. There are 4 pairs that we optimised the strategy to work for. There are a few main steps are as follows to use the strategy in it's most efficient manner-

1. Pyramiding orders needs to be set to 2 for maximum efficiency of the strategy due to aggressive and conservative entries, recommended % of equity per trade = 10-50%.

2. 15 Minute time frame needs to be applied (obvious, we know).

3. Pairs we used to optimise and backtest the strategy should ideally be used when using the strategy-

BTC/USD - prntscr.com

LTC/USD - prntscr.com

BCH/USD - prntscr.com

ETH/BTC - prntscr.com

XRP/BTC - prntscr.com

LTC/BTC - prntscr.com

We have a list of Visual and Technical features that are implemented into our strategy to make sure it is easy to use, consistent and giving it the highest chance of being profitable.

Visual Features

Colored candles- a visual to notification of an entry.

Stop-loss line- a horizontal red line to show the user where the stop-loss has been placed. Our testing proved a horizontal stop was more profitable than implementation of a trailing.

Price Bands- a dynamic price band to show the direction of the trend and support zones.

Technical Features

Trend Confirmation- Our algorithm fires entries only on trend confirmation and looks to trade the move for as long as it can, while also filtering out any false entries.

Aggressive and Conservative Entries- Two different types of entries have been incorporated in the strategy to maximise profit.

If you have discord alerts access, be sure to watch out in the discord for entries!

QuantCat 15M Crypto Trend StrategyQuantCat 15M Crypto Trend Strategy

This strategy will allow you to absolutely smash the Crypto/USD pairs. We have optimised this strategy to work best for the Crypto/USD pairs on the 15 minute time frame. There are 4 pairs that we optimised the strategy to work for. There are a few main steps are as follows to use the strategy in it's most efficient manner-

1. Pyramiding orders needs to be set to 2 for maximum efficiency of the strategy.

2. 15 Minute timeframe needs to be applied (obvious, we know)

3. Pairs we used to optimise and backtest the strategy should ideally be used when using the strategy-

BTC/USD

ETH/USD

LTC/USD

BCH/USD

We have a list of Visual and Technical features that are implemented into our strategy to make sure it is easy to use, consistent and giving it the highest chance of being profitable.

Visual Features

Colored candles- a visual to notification of an entry.

Stop-loss line- a horizontal red line to show the user where the stop-loss has been placed. Our testing proved a horizontal stop was more profitable than implementation of a trailing.

Price Bands- a dynamic price band to show the direction of the trend and support zones.

Technical Features

Trend Confirmation- Our algorithm fires entries only on trend confirmation and looks to trade the move for as long as it can, while also filtering out any false entries.

Aggressive and Conservative Entries- Two different types of entries have been incorporated in the strategy to maximise profit.

If you have discord alerts access, be sure to watch out in the discord for entries!

BitcoinNinjas Ninja Signals Buy/Sell Alert Trading Strategy v3.0Bitcoin Ninjas 'Ninja Signals' Buy/Sell Alerts & Backtesting TradingView Script v3.0

(for Cryptocurrencies, Forex, GunBot, ProfitTrailer, automatic trading software, and more)

This is version 3 of our popular Ninja Signals trading script, which is similar to version 2, but with a new hard-coded calibration (resolution) setting that automatically matches candle size (period) to ensure that no repainting occurs regardless of the number or type of indicators and filters traders apply when configuring the script.

'Ninja Signals' v3.0 (SCRIPT)

'Ninja Signals' v3.0 (STRATEGY)

'Ninja Signals' v2.0 (SCRIPT)

'Ninja Signals' v2.0 (STRATEGY)

'Ninja Signals' v1.0 (SCRIPT)

'Ninja Signals' v1.0 (STRATEGY)

-Allows users to easily set automated buy and sell alerts on TradingView for use with automatic and manual trading of cryptocurrencies, Forex securities, and more (alerts are compatible with automatic trading software such as GunBot, ProfitTrailer, and more).

-Synthesizes many powerful indicators [e.g. Relative Strength Index (RSI), stochastic RSI, Money Flow Index (MFI), Moving Average Convergence Divergence (MACD), etc.) into one super script to generate very precise buy and sell signals in almost any market condition.

-Buy arrows (blue) and sell arrows (red) can be changed or hidden for ease of viewing.

-No lag EMA trendline featuring trend-reversal color-coding (white uptrend, black downtrend).

-Adjustable ‘calibration’ setting allows users to customize the script to work for any currency or security available through TradingView, on any exchange, simply by adjusting a number.