MKAST V2 (monthly)PLEASE READ THE ENTIRE POST BEFORE PURCHASING & USING THE MKAST Algorithm. Saves you and me some time in emails and messages. :)

This is the NEW MONTHLY ACCESS Version of the MKAST

The MKAST Buy Sell Algorithm is a very specific strategy, cut down to its roots and made perfect for the volatile crypto market.

Many Algorithms focus only on one aspect, one side, one specific rule.

As you know, this is not how life, the market or anything else works.

MKAST combines many different aspects at the same time, scans multiple other Algorithms and comes to a conclusion based on over 1350 lines of code.

It is based on Divergences, Elliott Waves , Ichimoku , MACD , MACD Histogram, RSI , Stoch , CCI , Momentum, OBV, DIOSC, VWMACD, CMF and multiple EMAs.

Every single aspect is weighted into the decision before giving out an indication.

Most buy/sell Algorithms FAIL because they try to apply the same strategy to every single chart, which

are as individual as humans.

To conquer this problem, MKAST has a wide range of settings and variables which can be easily

modified.

To make it a true strategy, MKAST has as well settings for Take Profit Points, Multiple Entries and Stop

Losses. Everything with an Alert Feature of course.

I know from experience that many people take one Algorithm and are simply too LAZY to add multiple Algorithms to make a rational choice.

The result of that is that they lose money, by following blatantly only one Algorithm.

MKAST has additional 9 Indicators, perfect for the crypto market, which can be turned on and off.

Manual

MKAST Signals Settings

“Show Signals?” - On/Off to show the Buy/Sell Signals.

“Aggressiveness” - Increase to make the signals less aggressive and decrease to make them more aggressive.

“Show Custom Signals?” - On/Off to show custom MKAST Signals as chosen in the settings below.

“Custom Buy/Sell Aggressiveness” - Choose a custom Aggressiveness for each buy and sell signal individually.

“TJ-Index Requirement For Buy/Sell” - If the TJ-Index is below the given number, it will show the signal in grey, this also applies for normal signals. Buy 0 and Sell 15 shows all signals in their original colour again.

“Don’t show signals that don’t meet index requirement?” - Checked, it will completely not show signals which would be “grey” as in the explanation above.

“Change Backgroundcolour if index is at 15 or 0?” - Checked, changes the colour of the chart if the index is at 15 or 0 points

MKAST Panel Settings

“Show Info Panel?” - Shows Info Panel on the chart.

“Move Info Panel UP by %” - Moves Info Panel up/down.

“Move Info Panel Left/Right ” - Moves Info Panel Left/Right.

“Show BitMEX Panel?” - Shows BitMEX Panel on the chart.

“Move BitMEX Panel by % ” - Moves BitMEX Panel up/down.

“Move BitMEX Panel Left/Right” - Moves BitMEX Panel Left/Right. “Signal Source” - Choose source of candle open/close for Equity calculation.

“Leverage Used?” - Select the used Leverage for your strategy and Equity calculation.

“Fees Per Trade in % ” - Deducts these fees after each trade from Equity calculation.

“Round Current Profit Price?” - Rounds the number on the Panel. “Trading Periods ” - Choose a trading Period which will be used to calculate Period Equity.

“Show separations of each Trading Period?” - Show separations on the chart of each Trading Period.

The very new feature on Tradingview and obviously now as well on MKAST are Information Panels.

I have chosen to add an Info Panel and a BitMEX Price Panel into MKAST, to make live and even

backtesting easier.

With only one blink of an eye the user is able to see ALL relevant information, without having to go

through various ways of checking and using other tools.

The Info Panel:

The first row shows the current profit. This is calculated since the signal initiation and the current candle close. Followed by a single number, which represents the current TJ-Index, removing the need of having to add the actual TJ-Index Oscillator on the chart.

The second row shows the current position and its status. This was added on request of many users wanting to know if their position is “about to change” or not. The status shows the users if the position is “endangered” or “okay”.

Followed by the “backtesting tool” already included inside the Panel. No need for complex oscillators with a hard reading for backtesting. With this one and simple panel, you see the Period Equity for the period chosen previously in the settings. This calculates all profits made inside that period and re-sets when the period ends. Right next to it, the Total Equity calculating ALL profits since the beginning of the chart.

Right below, you see the information about the last long and short position which have been open. This helps with the evaluation and documentation of the last trade.

The BitMEX Panel:

A convenient panel which shows all BitMEX contracts and their LIVE prices. The need for opening each chart goes away, the quality and experience of trading increases.

MKAST custom Signals are one of the notorious possibilities for ADVANCED strategies with MKAST.

Users who requested these features and use them frequently are the ones, having already a very unique trading strategy and they use these very custom signals as confluence or for multiple entry trades.

These custom signals and their settings can be mostly ignored by the majority of traders who are using this Algorithm.

The idea behind the grey signals has its roots in the idea of the TJ-Index. The TJ-Index being 15 Algorithms and conditions possible showing a bullish or bearish interpretation. The index counts the Algorithms which are showing a bullish interpretation.

Like that we can make sure that signals are shown in the original colour, are only those who have an additional confluence with the TJ-Index, not letting the user buy, if at least the majority is not bullish , and not letting the user sell, if at least the majority is bearish .

The custom buy and sell aggressiveness lets the user customise the MKAST algorithm even more.

Either the users wants to see how signals are changing on a different (slightly lower or higher) aggressiveness, being able to expect a change on their own settings. OR seeing that some signals of the same sort are a little out of place and is able to move these to a different aggressiveness, increasing the profitability even more.

Needless to say, custom signals are NOT a part of the Info Panel.

MKAST Label & Trendline Settings

“Show Labels?” - On/Off to show Labels above each signal, with the percentage gain or loss, calculated from the last signal to the new signal.

“Show Trendlines?” - On/Off to show automatic Trendlines following Gainzy Lines.

“Lookback Length” - Choose a length that the automatic trendiness use for calculation. Comparable to Aggressiveness.

“Wicks//Bodies” - Change between trendiness connecting from wick to wick or from body to body.

“Black lines// Coloured lines” - Change between simply black lines or changing colour lines.

“Filter Trendlines?” - On/Off to show all trendiness or just resistance decreasing and support increasing ones.

“Limit Extensions Of The Lines?” - This value increases by how much the trendiness are being extended. 0 = endless extension, otherwise 100 = maximum custom extension.MKAST Strategy “Take Profit 1” - On/Off to show TP1 points.

“Take Profit After %” - Set the percentage after which TP1 is active.

“Take Profit 2 ” - On/Off to show TP2 points.

“Take Profit 2 After %” - Set the percentage after which TP1 is

active.

“Take Profit 3” - On/Off to show TP3 points.

“Take Profit 3 After %” - Set the percentage after which TP1 is active.

“Second Entry” - On/Off to show Second Entry points.

“Second Entry After %” - Set the percentage after which Second Entry is active.

“Third Entry” - On/Off to show Third Entry points.

“Third Entry After %” - Set the percentage after which Third Entry is active.

“Stop Loss” - On/Off to show Stop Loss points.

“Stop Loss After %” - Set the percentage after which Stop Loss is active.

MKAST Strategy

To make the life of the MKAST user even easier, I have added all adjustable Take Profit Points, Multiple entry points and Stop Loss points.

I have never seen a sustainable and reliable trading strategy without TPs, Multiple entry and especially without a stop loss. Everything in the usual and fully customisable MKAST style.

Simply choose how many Take Profit points you would like to have and choose the percentage after which you would like to see the Take Profit point appear on the chart and notify you to take profits.

Are you a Trader who likes Multiple Entries? Also no problem with MKAST. Select how many additional entries you would like to have and after how many percent you would like them to appear on the chart and remind you of adding to the position.

What would a Strategy be without a Stop Loss? Same settings apply here as on the TPs and MEs .

All of the settings are able to take fractions of a number as well. This enables users to even use all of the strategy settings for scalping or FX pairs, where high leverage and the smallest of moves are used for trading.

Needless to say, all of these settings work on RENKO and Heikin Ashi as well. These might need adjustment, since the calculation is different, yet there is nothing standing in the way of it anymore.

Crypto Modified Indicators

“Show Divergences?” - On/Off to show Divergences on the Chart based on the data of 10 different Algorithms.

“Show Oversold/bought?” - On/Off to change the colour of the chart in Oversold/bought conditions.

“Oversold/bought value?” - Choose a value for which the chart is Oversold/bought.

“Show Fibonacci Levels?” - On/Off to show automatic Fibonacci Levels.

“Fibonacci Lookback Lenght” - This value states how many candles from right now are taken into account to paint the Fibonacci Levels.

“Fibonacci Custom Period” - Choose a custom Timeframe that should be used to paint the Fibonacci Levels.

“2nd-7th Fibonacci Level” - Enter a value for the Fibonacci Levels you would like to use and see on the chart.

“Plot 1.618 Level?” - On/Off for the Fibonacci extension level.

Crypto Modified Indicators

“Show Bands?” - On/Off to show the TJ-Bands on the chart.

“Bands Length” - Choose a value for the TJ-Bands Lenght

“Show Show EMA 1-3?” - On/Off to show the EMAs 1-3 on the chart.

“EMA Lenght 1-3” - Choose a value for the first to third EMA Lenght

“Show Ichimoku? ” - On/Off to show Ichimoku on the chart.

“Show Tenkin?” - On/Off to show Tenkin on the chart. “Tenkin” - Set the lenght of the Tenkin.

“Show Kijun?” - On/Off to show Kijun on the chart.

“Kijun” - Set the lenght of the Kijun.

“Show Senkou?” - On/Off to show the Senkou on the chart. “Senkou” - Set the lenght of the Senkou.

“Displacement” - Set the value of the Displacement.

“Show Chikou Span?” - On/Off to show the Chikou Span on the chart.

Crypto Custom Indicators

In the picture above, you see the first pair of Crypto Custom Indicators. The oversold and overbought conditions are highlighted.

Bullish and Bearish divergences are also plotted on the chart.

This is personally my favourite combination of Indicators and MKAST settings. It shows nicely

everything one needs to know and makes it easier to decide wether to follow a signal or not.

We here as well a perfect example of the Automatic Fibonacci Lines (Lookback 50, Timeframe 1D).

It shows all significant levels, which we can see being respected.

Orange = 23.6%, Green = 38.2%, Red = 50%, Yellow = 61.8%, Blue = 78.6%, White = 0%;100%

In this picture above, we observe the perfect ensemble of MKAST and an EMA strategy, especially modified for crypto markets.

Here, as by default, we have the EMAs at 21, 90 and 200. These have shown to be very significant moving support and resistance points in the crypto market.

In this picture above, I lowered the timeframe to show the highly significant levels of the Ichimoku . It has not the “usual values”. These here have been modified for the volatile crypto market and set as default.

An incredibly powerful tool for anyone who is ready to step up their trading game. It is a huge part of the MKAST back end and the strategy behind it.

MKAST Custom Alerts

1

MKAST without any doubt has Custom Alerts for all Signals that it is painting on the chart.

One can even choose to receive custom notifications for Take Profit points, Multiple Entry points and

the Stop Loss points.

The signals appear on the chart DURING the candle, not at the end of the candle. Therefore, the

alerts do this as well. These appear during the candle.

Here we can see all of the possible Alerts that can be chosen to be displayed. In total it is 14 different custom alerts, based on what the trader is looking for and how he is trading.

Personally, I have 10-15 coins that I trade the most and for these I have custom notifications, mostly though only the MKAST Buy/Sell and Stop Loss Signals.

To activate Alerts for MKAST,

1) Go to the “ALERT” icon on the top tool bar of your Tradingview.

2) Select “CONDITION” as “—MKAST—“

3) Then choose ONE condition from the list of conditions.

4) On “OPTIONS” you can set how many times it appears, I have “Once per Bar”.

4.1) If you want to make sure that the signal is truly there and not just a condition for a second during the candle, choose “ONCE PER BAR CLOSE”.

5) “Expiration Time” sets the time until the alert expires. PRO users have no expiration for alerts.

6) “Alert Actions” give you a row of choices what happens and how you want to be notified.

7) “Message” is the message that you receive inside the notification.

Thank you, Kong

Cari dalam skrip untuk "profit"

MKAST V2 (lifetime)PLEASE READ THE ENTIRE POST BEFORE PURCHASING & USING THE MKAST Algorithm. Saves you and me some time in emails and messages. :)

This is the NEW LIFETIME ACCESS Version of the MKAST

The MKAST Buy Sell Algorithm is a very specific strategy, cut down to its roots and made perfect for the volatile crypto market.

Many Algorithms focus only on one aspect, one side, one specific rule.

As you know, this is not how life, the market or anything else works.

MKAST combines many different aspects at the same time, scans multiple other Algorithms and comes to a conclusion based on over 1350 lines of code.

It is based on Divergences, Elliott Waves, Ichimoku, MACD, MACD Histogram, RSI, Stoch, CCI, Momentum, OBV, DIOSC, VWMACD, CMF and multiple EMAs.

Every single aspect is weighted into the decision before giving out an indication.

Most buy/sell Algorithms FAIL because they try to apply the same strategy to every single chart, which

are as individual as humans.

To conquer this problem, MKAST has a wide range of settings and variables which can be easily

modified.

To make it a true strategy, MKAST has as well settings for Take Profit Points, Multiple Entries and Stop

Losses. Everything with an Alert Feature of course.

I know from experience that many people take one Algorithm and are simply too LAZY to add multiple Algorithms to make a rational choice.

The result of that is that they lose money, by following blatantly only one Algorithm.

MKAST has additional 9 Indicators, perfect for the crypto market, which can be turned on and off.

Manual

MKAST Signals Settings

“Show Signals?” - On/Off to show the Buy/Sell Signals.

“Aggressiveness” - Increase to make the signals less aggressive and decrease to make them more aggressive.

“Show Custom Signals?” - On/Off to show custom MKAST Signals as chosen in the settings below.

“Custom Buy/Sell Aggressiveness” - Choose a custom Aggressiveness for each buy and sell signal individually.

“TJ-Index Requirement For Buy/Sell” - If the TJ-Index is below the given number, it will show the signal in grey, this also applies for normal signals. Buy 0 and Sell 15 shows all signals in their original colour again.

“Don’t show signals that don’t meet index requirement?” - Checked, it will completely not show signals which would be “grey” as in the explanation above.

“Change Backgroundcolour if index is at 15 or 0?” - Checked, changes the colour of the chart if the index is at 15 or 0 points

MKAST Panel Settings

“Show Info Panel?” - Shows Info Panel on the chart.

“Move Info Panel UP by %” - Moves Info Panel up/down.

“Move Info Panel Left/Right ” - Moves Info Panel Left/Right.

“Show BitMEX Panel?” - Shows BitMEX Panel on the chart.

“Move BitMEX Panel by % ” - Moves BitMEX Panel up/down.

“Move BitMEX Panel Left/Right” - Moves BitMEX Panel Left/Right. “Signal Source” - Choose source of candle open/close for Equity calculation.

“Leverage Used?” - Select the used Leverage for your strategy and Equity calculation.

“Fees Per Trade in % ” - Deducts these fees after each trade from Equity calculation.

“Round Current Profit Price?” - Rounds the number on the Panel. “Trading Periods ” - Choose a trading Period which will be used to calculate Period Equity.

“Show separations of each Trading Period?” - Show separations on the chart of each Trading Period.

The very new feature on Tradingview and obviously now as well on MKAST are Information Panels.

I have chosen to add an Info Panel and a BitMEX Price Panel into MKAST, to make live and even

backtesting easier.

With only one blink of an eye the user is able to see ALL relevant information, without having to go

through various ways of checking and using other tools.

The Info Panel:

The first row shows the current profit. This is calculated since the signal initiation and the current candle close. Followed by a single number, which represents the current TJ-Index, removing the need of having to add the actual TJ-Index Oscillator on the chart.

The second row shows the current position and its status. This was added on request of many users wanting to know if their position is “about to change” or not. The status shows the users if the position is “endangered” or “okay”.

Followed by the “backtesting tool” already included inside the Panel. No need for complex oscillators with a hard reading for backtesting. With this one and simple panel, you see the Period Equity for the period chosen previously in the settings. This calculates all profits made inside that period and re-sets when the period ends. Right next to it, the Total Equity calculating ALL profits since the beginning of the chart.

Right below, you see the information about the last long and short position which have been open. This helps with the evaluation and documentation of the last trade.

The BitMEX Panel:

A convenient panel which shows all BitMEX contracts and their LIVE prices. The need for opening each chart goes away, the quality and experience of trading increases.

MKAST custom Signals are one of the notorious possibilities for ADVANCED strategies with MKAST.

Users who requested these features and use them frequently are the ones, having already a very unique trading strategy and they use these very custom signals as confluence or for multiple entry trades.

These custom signals and their settings can be mostly ignored by the majority of traders who are using this Algorithm.

The idea behind the grey signals has its roots in the idea of the TJ-Index. The TJ-Index being 15 Algorithms and conditions possible showing a bullish or bearish interpretation. The index counts the Algorithms which are showing a bullish interpretation.

Like that we can make sure that signals are shown in the original colour, are only those who have an additional confluence with the TJ-Index, not letting the user buy, if at least the majority is not bullish, and not letting the user sell, if at least the majority is bearish.

The custom buy and sell aggressiveness lets the user customise the MKAST algorithm even more.

Either the users wants to see how signals are changing on a different (slightly lower or higher) aggressiveness, being able to expect a change on their own settings. OR seeing that some signals of the same sort are a little out of place and is able to move these to a different aggressiveness, increasing the profitability even more.

Needless to say, custom signals are NOT a part of the Info Panel.

MKAST Label & Trendline Settings

“Show Labels?” - On/Off to show Labels above each signal, with the percentage gain or loss, calculated from the last signal to the new signal.

“Show Trendlines?” - On/Off to show automatic Trendlines following Gainzy Lines.

“Lookback Length” - Choose a length that the automatic trendiness use for calculation. Comparable to Aggressiveness.

“Wicks//Bodies” - Change between trendiness connecting from wick to wick or from body to body.

“Black lines// Coloured lines” - Change between simply black lines or changing colour lines.

“Filter Trendlines?” - On/Off to show all trendiness or just resistance decreasing and support increasing ones.

“Limit Extensions Of The Lines?” - This value increases by how much the trendiness are being extended. 0 = endless extension, otherwise 100 = maximum custom extension.MKAST Strategy “Take Profit 1” - On/Off to show TP1 points.

“Take Profit After %” - Set the percentage after which TP1 is active.

“Take Profit 2 ” - On/Off to show TP2 points.

“Take Profit 2 After %” - Set the percentage after which TP1 is

active.

“Take Profit 3” - On/Off to show TP3 points.

“Take Profit 3 After %” - Set the percentage after which TP1 is active.

“Second Entry” - On/Off to show Second Entry points.

“Second Entry After %” - Set the percentage after which Second Entry is active.

“Third Entry” - On/Off to show Third Entry points.

“Third Entry After %” - Set the percentage after which Third Entry is active.

“Stop Loss” - On/Off to show Stop Loss points.

“Stop Loss After %” - Set the percentage after which Stop Loss is active.

MKAST Strategy

To make the life of the MKAST user even easier, I have added all adjustable Take Profit Points, Multiple entry points and Stop Loss points.

I have never seen a sustainable and reliable trading strategy without TPs, Multiple entry and especially without a stop loss. Everything in the usual and fully customisable MKAST style.

Simply choose how many Take Profit points you would like to have and choose the percentage after which you would like to see the Take Profit point appear on the chart and notify you to take profits.

Are you a Trader who likes Multiple Entries? Also no problem with MKAST. Select how many additional entries you would like to have and after how many percent you would like them to appear on the chart and remind you of adding to the position.

What would a Strategy be without a Stop Loss? Same settings apply here as on the TPs and MEs.

All of the settings are able to take fractions of a number as well. This enables users to even use all of the strategy settings for scalping or FX pairs, where high leverage and the smallest of moves are used for trading.

Needless to say, all of these settings work on RENKO and Heikin Ashi as well. These might need adjustment, since the calculation is different, yet there is nothing standing in the way of it anymore.

Crypto Modified Indicators

“Show Divergences?” - On/Off to show Divergences on the Chart based on the data of 10 different Algorithms.

“Show Oversold/bought?” - On/Off to change the colour of the chart in Oversold/bought conditions.

“Oversold/bought value?” - Choose a value for which the chart is Oversold/bought.

“Show Fibonacci Levels?” - On/Off to show automatic Fibonacci Levels.

“Fibonacci Lookback Lenght” - This value states how many candles from right now are taken into account to paint the Fibonacci Levels.

“Fibonacci Custom Period” - Choose a custom Timeframe that should be used to paint the Fibonacci Levels.

“2nd-7th Fibonacci Level” - Enter a value for the Fibonacci Levels you would like to use and see on the chart.

“Plot 1.618 Level?” - On/Off for the Fibonacci extension level.

Crypto Modified Indicators

“Show Bands?” - On/Off to show the TJ-Bands on the chart.

“Bands Length” - Choose a value for the TJ-Bands Lenght

“Show Show EMA 1-3?” - On/Off to show the EMAs 1-3 on the chart.

“EMA Lenght 1-3” - Choose a value for the first to third EMA Lenght

“Show Ichimoku? ” - On/Off to show Ichimoku on the chart.

“Show Tenkin?” - On/Off to show Tenkin on the chart. “Tenkin” - Set the lenght of the Tenkin.

“Show Kijun?” - On/Off to show Kijun on the chart.

“Kijun” - Set the lenght of the Kijun.

“Show Senkou?” - On/Off to show the Senkou on the chart. “Senkou” - Set the lenght of the Senkou.

“Displacement” - Set the value of the Displacement.

“Show Chikou Span?” - On/Off to show the Chikou Span on the chart.

Crypto Custom Indicators

In the picture above, you see the first pair of Crypto Custom Indicators. The oversold and overbought conditions are highlighted.

Bullish and Bearish divergences are also plotted on the chart.

This is personally my favourite combination of Indicators and MKAST settings. It shows nicely

everything one needs to know and makes it easier to decide wether to follow a signal or not.

We here as well a perfect example of the Automatic Fibonacci Lines (Lookback 50, Timeframe 1D).

It shows all significant levels, which we can see being respected.

Orange = 23.6%, Green = 38.2%, Red = 50%, Yellow = 61.8%, Blue = 78.6%, White = 0%;100%

In this picture above, we observe the perfect ensemble of MKAST and an EMA strategy, especially modified for crypto markets.

Here, as by default, we have the EMAs at 21, 90 and 200. These have shown to be very significant moving support and resistance points in the crypto market.

In this picture above, I lowered the timeframe to show the highly significant levels of the Ichimoku. It has not the “usual values”. These here have been modified for the volatile crypto market and set as default.

An incredibly powerful tool for anyone who is ready to step up their trading game. It is a huge part of the MKAST back end and the strategy behind it.

MKAST Custom Alerts

1

MKAST without any doubt has Custom Alerts for all Signals that it is painting on the chart.

One can even choose to receive custom notifications for Take Profit points, Multiple Entry points and

the Stop Loss points.

The signals appear on the chart DURING the candle, not at the end of the candle. Therefore, the

alerts do this as well. These appear during the candle.

Here we can see all of the possible Alerts that can be chosen to be displayed. In total it is 14 different custom alerts, based on what the trader is looking for and how he is trading.

Personally, I have 10-15 coins that I trade the most and for these I have custom notifications, mostly though only the MKAST Buy/Sell and Stop Loss Signals.

To activate Alerts for MKAST,

1) Go to the “ALERT” icon on the top tool bar of your Tradingview.

2) Select “CONDITION” as “—MKAST—“

3) Then choose ONE condition from the list of conditions.

4) On “OPTIONS” you can set how many times it appears, I have “Once per Bar”.

4.1) If you want to make sure that the signal is truly there and not just a condition for a second during the candle, choose “ONCE PER BAR CLOSE”.

5) “Expiration Time” sets the time until the alert expires. PRO users have no expiration for alerts.

6) “Alert Actions” give you a row of choices what happens and how you want to be notified.

7) “Message” is the message that you receive inside the notification.

Thank you, Kong

CryptoEngineering 🔥Isn’t It Time You Made Your Crypto Portfolio Great Again? 🔥

The falling knives, the heartbreaking crashes, the devastating feeling of watching a missed trade soar all the way to the moon.

The markets aren’t fair, which means you need a tool that gives you an edge. So,It is time to try EngineeringRobo.

The Engineeringrobo is a great ally in a crypto market - when the price moves the algorithm will automatically show Buy and Sell orders when there is a best opportunity to make a profit. It is a just SMART trading system script on TradingView that brings the easiest approach to trading with a high profitability rate.

I created EngineeringRobo to help you on your traders as a robo advisor , It will "not " trade on behalf of you on exchanges via API. It is not an AI robot,It is am ALGO Trading robot. You can use it on any trading markets (BIST, S&P 500,Commodities ,Forex, Crypto ) with any time frame!

My unique algorithm find profitable altcoins based on their Ichimoku, McGinley, MA, RSI, MACD, Stochastic, Volumes and Price Changes gives you BUY and SELL signals. The EngineeringRobo indicator displays two different signals for entry and exit on a coin to maximize its profitability on the chart. The signals can appear at any time during an open candle, but once closed the signal is final and wont change in the future.

One of the biggest advantages of algo trading is removing human emotion from the crypto markets,humans trading are susceptible to emotions that lead to irrational decisions.Robo doesn't have to think or feel good to make a trade. If conditions are met, it enters.When the trade goes the wrong way or hits a profit target, It exits. It doesn't get angry at the market or feel invincible after making a few good trades. The two emotions that lead to poor decisions that algo traders aren't susceptible to are fear,and greed.

That's why It makes money but most of you not!

What Are the Advantages of using it as a ROBO Advisor?

🔴Reduce your required screen-time

🔴Reduce anxiety over missing setups when you are busy

🔴Turn existing indicators into alerts (eg. Whenever RSI goes overbought)

🔴Find comfort in knowing that you have me on your side

To get the maximized results from @EngineeringRobo

Open tradingview

Decide the coin/BTC

Pick 1M

Draw the Support & Resistance lines

Change the 1W

Draw the lines - Support & Resistance

Find out Chart Patterns

Change to 3D/1D / 3H

Check Robo' signals

Set your orders

Enjoy your profits💰

***Even the best automated day trading software can trigger false trends.

In August 2012 by Knight Capital group;who lost over $440 million in just half an hour when their trading software went rogue in response to market conditions. That's why it is a Robo advisor not trading bot! Engineeringrobo is not a get-rich-quick scheme as well!

Disclaimer

Information on EngineeringRobo should not be seen as a recommendation to trade BIST, S&P 500,Commodities ,Forex, Crypto.

EngineeringRobo is not licensed nor authorized to provide advice on investing and related matters.

Information on the page is not, nor should it be seen as investment advice.Any trading decisions that you make are solely your responsibility. Clients without sufficient knowledge should seek individual advice from an authorized source.

Crypto and Forex trading entails significant risks and there is a chance that clients lose all of their invested money. Past performance is not a guarantee of future returns. Before trading with any of the Algos, clients should make sure they understand the risks.

EngineeringRobo nor its agents or partners are not registered and do not provide any services on the US territory.

***I have been trading since 2016 . Got my first bitcoin in 2013

cryptomars 1.0 Concussion trend alarm Description:

1. In the indicator, there is an orange signal that fluctuates linearly. It is a buy signal when it goes from bottom to top. When the signal line remains in the upper position, it indicates a multi-party trend.

2. When it goes from top to bottom, it indicates a sell signal. When the signal line remains below, it indicates a sales trend.

3. Depending on the time level, when the position of the signal line changes, determine whether the current candle is completed or not according to the time level of the chart you selected to determine the signal. For example, if you select a chart level of 5 meters, then when the signal line changes, for example, it will send a sell signal from top to bottom. At this time, please do not rush to sell. You should wait for this 5 meter candlestick to complete. When the candle is over and the next candle is started, if the signal line remains in the top-down form, the sell signal is normal and you can sell it.

Because the position of the signal appears, it is the location of the sale. During the completion of the candlestick , the signal may disappear after disappearing. We only have to wait for a while to get a more stable deal.

4. The alarm setting is very simple. There are two lines in the indicator. One is the orange signal line that fluctuates up and down, and the other is the fixed zero line of “zero”.

We set it in the alarm. When the signal line passes "zero" from the top, the short signal is sent only when the candle map is completed. When the signal line passes "zero" from "up" below, the signal is sent for a long time when the candlestick is completed.

One trick, the appearance of the signal, is that the price runs in one direction for a while, so it appears at or near the bottom. Because, when we have already made a profit in the transaction, we can make a profit in advance, and we do not need to wait for the opposite signal to stop the profit and reduce the risk of profit retracement.

Because in this market, the fluctuations are very large, and the people who compete are also very fierce. What we need to do is to make every transaction as possible, and we are all profitable. If we sell and find that the price is still rising, please don't feel sorry, don't consider eating all the profits.

6. When the signal appears, in most cases, even in the impact trend, it will still run a distance in the direction of the signal, that is, you will profit, so please close the position and make a profit in time. Otherwise, when the price volatility is too small, you miss the profit point, the price starts to run in the opposite direction, and you may change from profit to loss.

BITMEX's trailing stop loss is a great feature, please use it flexibly.

7, if it is a shock trend, please try not to trade.

8. We recommend that you turn on the “cryptomars 3.0” and “cryptomars 2.0” indicators. No matter who signs the trade first, you can trade, which can help you get more profit.

9. Remember, I hope this indicator will be your powerful assistant, but please don't rely on it completely. Learning more trading knowledge and skills is even more important. Therefore, when we consider the profitable position, you can use your trading skills, MACD , KDJ, etc. to assist and profit in a more suitable position.

cryptomars 2.0 short alarmDescription:

1. In the indicator, there is an orange signal that fluctuates linearly. It is a buy signal when it goes from bottom to top. When the signal line remains in the upper position, it indicates a multi-party trend.

2. When it goes from top to bottom, it indicates a sell signal. When the signal line remains below, it indicates a sales trend.

3. Depending on the time level, when the position of the signal line changes, determine whether the current candle is completed or not according to the time level of the chart you selected to determine the signal. For example, if you select a chart level of 5 meters, then when the signal line changes, for example, it will send a sell signal from top to bottom. At this time, please do not rush to sell. You should wait for this 5 meter candlestick to complete. When the candle is over and the next candle is started, if the signal line remains in the top-down form, the sell signal is normal and you can sell it.

Because the position of the signal appears, it is the location of the sale. During the completion of the candlestick , the signal may disappear after disappearing. We only have to wait for a while to get a more stable deal.

4. The alarm setting is very simple. There are two lines in the indicator. One is the orange signal line that fluctuates up and down, and the other is the fixed zero line of “zero”.

We set it in the alarm. When the signal line passes "zero" from the top, the short signal is sent only when the candle map is completed. When the signal line passes "zero" from "up" below, the signal is sent for a long time when the candlestick is completed.

One trick, the appearance of the signal, is that the price runs in one direction for a while, so it appears at or near the bottom. Because, when we have already made a profit in the transaction, we can make a profit in advance, and we do not need to wait for the opposite signal to stop the profit and reduce the risk of profit retracement.

Because in this market, the fluctuations are very large, and the people who compete are also very fierce. What we need to do is to make every transaction as possible, and we are all profitable. If we sell and find that the price is still rising, please don't feel sorry, don't consider eating all the profits.

6. When the signal appears, in most cases, even in the impact trend, it will still run a distance in the direction of the signal, that is, you will profit, so please close the position and make a profit in time. Otherwise, when the price volatility is too small, you miss the profit point, the price starts to run in the opposite direction, and you may change from profit to loss.

BITMEX's trailing stop loss is a great feature, please use it flexibly.

7, if it is a shock trend, please try not to trade.

8. We recommend that you turn on the “cryptomars 3.0” and “cryptomars 1.0” indicators. No matter who signs the trade first, you can trade, which can help you get more profit.

9. Remember, I hope this indicator will be your powerful assistant, but please don't rely on it completely. Learning more trading knowledge and skills is even more important. Therefore, when we consider the profitable position, you can use your trading skills, MACD , KDJ, etc. to assist and profit in a more suitable position.

cryptomars alarm 3.0

Description:

1. In the indicator, there is an orange signal that fluctuates linearly. It is a buy signal when it goes from bottom to top. When the signal line remains in the upper position, it indicates a multi-party trend.

2. When it goes from top to bottom, it indicates a sell signal. When the signal line remains below, it indicates a sales trend.

3. Depending on the time level, when the position of the signal line changes, determine whether the current candle is completed or not according to the time level of the chart you selected to determine the signal. For example, if you select a chart level of 5 meters, then when the signal line changes, for example, it will send a sell signal from top to bottom. At this time, please do not rush to sell. You should wait for this 5 meter candlestick to complete. When the candle is over and the next candle is started, if the signal line remains in the top-down form, the sell signal is normal and you can sell it.

Because the position of the signal appears, it is the location of the sale. During the completion of the candlestick , the signal may disappear after disappearing. We only have to wait for a while to get a more stable deal.

4. The alarm setting is very simple. There are two lines in the indicator. One is the orange signal line that fluctuates up and down, and the other is the fixed zero line of “zero”.

We set it in the alarm. When the signal line passes "zero" from the top, the short signal is sent only when the candle map is completed. When the signal line passes "zero" from "up" below, the signal is sent for a long time when the candlestick is completed.

One trick, the appearance of the signal, is that the price runs in one direction for a while, so it appears at or near the bottom. Because, when we have already made a profit in the transaction, we can make a profit in advance, and we do not need to wait for the opposite signal to stop the profit and reduce the risk of profit retracement.

Because in this market, the fluctuations are very large, and the people who compete are also very fierce. What we need to do is to make every transaction as possible, and we are all profitable. If we sell and find that the price is still rising, please don't feel sorry, don't consider eating all the profits.

6. When the signal appears, in most cases, even in the impact trend, it will still run a distance in the direction of the signal, that is, you will profit, so please close the position and make a profit in time. Otherwise, when the price volatility is too small, you miss the profit point, the price starts to run in the opposite direction, and you may change from profit to loss.

BITMEX's trailing stop loss is a great feature, please use it flexibly.

7, if it is a shock trend, please try not to trade.

8. We recommend that you turn on the “cryptomars 2.0” and “cryptomars 1.0” indicators. No matter who signs the trade first, you can trade, which can help you get more profit.

9. Remember, I hope this indicator will be your powerful assistant, but please don't rely on it completely. Learning more trading knowledge and skills is even more important. Therefore, when we consider the profitable position, you can use your trading skills, MACD , KDJ, etc. to assist and profit in a more suitable position.

Complete Trend Trading System [Fhenry0331]This system was designed for the beginner trader to make money swing trading. Your losses will be small and your gains will be mostly large. You will show consistent profit. Period.

The system works on any security you like to trade. I used GBPUSD as an example because of the up swing and down swing it had recently. I tried to put as much information of how the system works in the chart. Hope it helps and is not to cluttered.

I will reiterate how the system works here: Everything is based off of closed price.

Legend

Uptrend: Buy

Green bar: initial start of an uptrend or uptrend continuing. Place order above that bar. If the initial bar does not stray too far from the MVWAP , I will place orders above subsequent bars if no filled occurred.

If initial start of the trend is missed, I will wait for the pullback. A pullback is a close below the MVWAP, and a close above the EMA (Low), RSI is above 50. Orders are placed above the pullback bars with plotted char "B" and also plotted green triangle up. Again orders are placed above those bars. the bars do not notate automatic buys. Don't chase anything. You will miss the initial bar on something because of news or earnings and it rocket up. Just wait, it will pullback. If it doesn't, to hell with it, on to the next.

Take profits: In the indicator you will see "T." That notates to take some profits. It is a suggestion. I was always told to take profits into spikes, as well as you can never lose money if you take profits. Up to you if you want to scale out and take the suggested profits or not.

Exit Completely: In an uptrend, close your entire position on bars colored yellow or red. (Again, closed bars)

In uptrend bars colored orange and black, do nothing, they are just pullback bars. Look for the buy pullback signal, then follow pullback buy rules for an uptrend.

Downtrend: Short

Red bar: initial start of a downtrend or downtrend continuing. Place order below the bar. If the initial bar does not stray too far fro the MVWAP, place orders below subsequent bars.

If initial start on the downtrend is missed, wait for the pullback. A pullback is a close above the MVWAP, and close below the EMA(Low). RSI is below 50. Orders are placed below the pullback bars with the plotted char "S" and also plotted red triangle. Again those bars are not automatic shorts, orders are placed below them. Don't chase anything. Wait for price to come into your plan. The idea FOMO is the stupidest thing ever, how can you miss out on something when it is always there. The market is always there and something will come into your zone. Chill.

"T": same as in uptrend, suggestion to take some profits.

Exit Completely: In a downtrend, close your entire position on bars colored orange or green.

In downtrend you will see bars colored yellow and black, do nothing, they are pullback bars. Look for the pullback short signal and follow pullback short rules.

If you have any questions get at me. Take a look at it on what you trade. Flip it through different securities.

Best of luck in all you do.

P.S. You should not take a trade right before earnings. You should also exit a trade right before earnings.

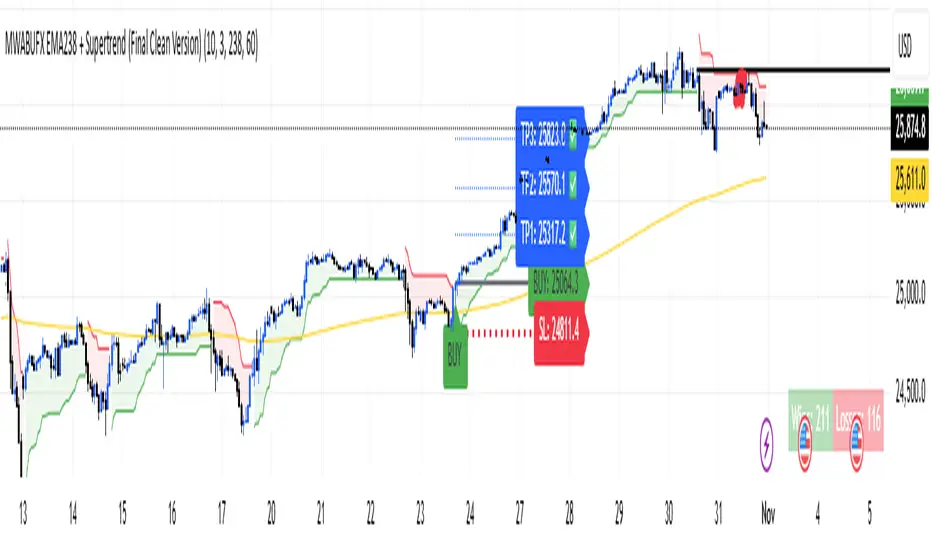

BMM V2.1 FINAL VERSION ⚙️ Optimized Trading Guide — MWABUFX 15-Minute Intraday Setup

🕒 Recommended Timeframe

✅ 15-Minute Chart (M15) — the most balanced and accurate for MWABUFX.

Why M15 Works Best:

Filters out small, noisy market movements found on 1m–5m charts.

Responds faster than 1H or 4H, perfect for daily profits.

Aligns well with market session volatility (London & New York).

Gives 2–5 high-probability trades per day depending on the pair.

Ideal for traders using PineConnector automation or manual execution.

🧭 How to Trade on 15-Minute

🟢 Buy Setup

EMA 238 is sloping upward and price is above it.

Supertrend flips green — wait for candle to close above the line.

Confirm trend direction on 1H timeframe (optional filter).

Enter trade at the close of the signal candle.

Stop-Loss: below recent swing low.

Take Profits:

TP1 → 1:1

TP2 → 1:2

TP3 → 1:3

Move SL to breakeven after TP1 is hit.

🔴 Sell Setup

EMA 238 is sloping downward and price is below it.

Supertrend flips red — wait for candle to close below the line.

Confirm 1H trend also bearish (optional).

Enter trade at the candle close.

Stop-Loss: above recent swing high.

Take Profits: TP1, TP2, TP3 as above.

🕐 Best Trading Hours (Kenya Time / GMT+3)

Session Time Ideal Pairs Notes

London Session 10:00 AM – 2:00 PM GBPUSD, EURUSD, Gold Cleanest 15-min trends

New York Session 3:30 PM – 7:00 PM US30, NAS100, XAUUSD, GBPUSD Strong volatility, high RR trades

Avoid After 8:30 PM — Market slows down, spreads widen

📌 If you must choose one — trade 15-minute charts during London–New York overlap (3:30 PM – 6:30 PM).

⚖️ Risk & Profit Strategy

Risk only 1–2% of balance per trade.

Focus on 1–3 solid setups per session — no overtrading.

Aim for minimum 1:2 reward-to-risk ratio.

Avoid entries when EMA 238 is flat (ranging market).

💡 Pro Tips

Use “Close of Candle” confirmation — avoid jumping in mid-bar.

Combine with session bias (e.g. buy Gold during bullish NY momentum).

Use alerts through PineConnector to catch trades instantly.

Don’t trade during major red news (NFP, CPI, FOMC).

Journal every trade — review TP/SL behavior to improve timing.

🏦 Institutional Smart Money Tracker_NEIL_BILLIONAIRE✅ INSTITUTIONAL SMART MONEY TRACKER V6 - COMPLETE

Here's what makes this institutional-grade and prevents wrong-direction trades:

🎯 CRITICAL ANTI-WRONG-DIRECTION FEATURES:

🏦 MASTER INSTITUTIONAL BIAS - Dashboard shows:

Strong Bullish (3-4 HTFs bullish) = ⚠️ ONLY TAKE LONG TRADES

Strong Bearish (3-4 HTFs bearish) = ⚠️ ONLY TAKE SHORT TRADES

Neutral = ⚠️ WAIT FOR CLEAR DIRECTION

🚨 BACKGROUND COLOR ALERTS:

Green tint = Strong bullish environment (safe to long)

Red tint = Strong bearish environment (safe to short)

Orange tint = DANGER ZONE - mixed signals, DON'T TRADE!

📊 MULTI-TIMEFRAME CONFIRMATION:

Analyzes 4 higher timeframes (15m, 1H, 4H, Daily by default)

Only generates signals when aligned with HTF trends

Shows trend strength for each timeframe

🎨 VISUAL ELEMENTS:

Green boxes = IDM bullish order blocks (demand zones)

Red boxes = IDM bearish order blocks (supply zones)

Blue/Orange boxes = EXT HTF order blocks

Aqua/Fuchsia boxes = Fair Value Gaps

Yellow boxes = Accumulation zones

Orange boxes = Distribution zones

⚠️ labels = Manipulation detected

💥 bubbles = High volume institutional activity

BOS/CHOCH labels = Market structure changes

🟢 LONG / 🔴 SHORT = Trade signals with full TP/SL levels

📋 DASHBOARD SHOWS:

Master institutional bias (color-coded)

Current timeframe trend + strength

4 HTF trends + strength levels

Market structure status

Volume analysis

Active trade with entry/SL/TP1/TP2/TP3

⚙️ EVERYTHING IS CUSTOMIZABLE:

Individual on/off toggles for all features

Colors, sizes, periods, thresholds

Dashboard position

HTF selections

Risk/reward ratios

🔔 8 BUILT-IN ALERTS:

Long signal

Short signal

Break of Structure

Change of Character

Manipulation detected

High volume spikes

Even when drunk/stoned, the massive dashboard + colored backgrounds make it IMPOSSIBLE to trade the wrong direction! 🎯

This is New Year's 2026 gift to fellow ♥ newbie traders, who are still learning to decode the market moves(♥just like me♥).

🏦 INSTITUTIONAL SMART MONEY TRACKER - COMPLETE TUTORIAL

📋 TABLE OF CONTENTS

Installation

Understanding the Dashboard

Visual Elements Guide

How to Read Signals

Trading Strategy

Settings Customization

Real Trading Examples

🚀 1. INSTALLATION {#installation}

Step 1: Copy the Code

Click on the artifact above and copy ALL the Pine Script code

Step 2: Open TradingView

Go to TradingView.com

Open any chart (BTC, ETH, stocks, forex, etc.)

Step 3: Open Pine Editor

Click "Pine Editor" at the bottom of the screen

Click "Open" → "New blank indicator"

Step 4: Paste & Save

Delete all existing code

Paste the copied indicator code

Click "Save" (give it a name like "Institutional SMT")

Click "Add to Chart"

Step 5: Initial Setup

The indicator will load with default settings

You'll see a dashboard in the top-right corner

Order blocks, FVGs, and zones will appear on the chart

📊 2. UNDERSTANDING THE DASHBOARD {#dashboard}

🏦 INSTITUTIONAL BIAS (TOP SECTION)

****** This is the MOST IMPORTANT section - it prevents wrong-direction trades!******

🟢 STRONG BULLISH = 3-4 higher timeframes bullish

→ ONLY TAKE LONG TRADES

🟡 BULLISH = 2 higher timeframes bullish

→ Prefer long trades, be cautious

🔴 STRONG BEARISH = 3-4 higher timeframes bearish

→ ONLY TAKE SHORT TRADES

🟠 BEARISH = 2 higher timeframes bearish

→ Prefer short trades, be cautious

⚪ NEUTRAL = Mixed signals

→ STAY OUT! Don't trade!

```

### **⚠️ WARNING MESSAGE**

- **"ONLY TAKE LONG TRADES"** = All HTFs aligned bullish

- **"ONLY TAKE SHORT TRADES"** = All HTFs aligned bearish

- **"WAIT FOR CLEAR DIRECTION"** = Don't trade yet!

### **CURRENT TIMEFRAME**

Shows your current chart's trend:

- **UP** = Bullish structure

- **DOWN** = Bearish structure

- **SIDE** = Sideways/choppy

**STRENGTH:**

- **STRONG** = ADX > 25 (trending market)

- **MEDIUM** = ADX 20-25 (moderate trend)

- **WEAK** = ADX < 20 (choppy/ranging)

### **HIGHER TIMEFRAMES (HTF)**

Displays 4 higher timeframes (default: 15m, 1H, 4H, Daily):

- **15m** = Short-term trend

- **1H** = Intraday trend

- **4H** = Swing trend

- **D** = Major trend

Each shows:

- Direction (UP/DOWN/SIDE)

- Strength (STRONG/MEDIUM/WEAK)

### **MARKET STRUCTURE**

- **BULLISH** = Higher highs and higher lows

- **BEARISH** = Lower highs and lower lows

- Shows last structure event (BOS/CHOCH)

### **VOLUME**

- **HIGH 💥** = Institutional activity detected

- **NORMAL** = Average volume

- Shows volume multiplier (e.g., "2.5x" = 2.5 times average)

### **ACTIVE SIGNAL**

- **🟢 LONG** = Active long trade with entry/SL/TP levels

- **🔴 SHORT** = Active short trade with entry/SL/TP levels

- **NO ACTIVE TRADE** = Waiting for setup

---

## 🎨 **3. VISUAL ELEMENTS GUIDE** {#visual-elements}

### **📦 ORDER BLOCKS**

**🟢 GREEN BOXES (Bullish IDM Order Blocks)**

- Last bearish candle before strong bullish move

- Demand zone where institutions bought

- Price often bounces here

- **Thicker border** = Unmitigated (not tested yet) → High probability zone

**🔴 RED BOXES (Bearish IDM Order Blocks)**

- Last bullish candle before strong bearish move

- Supply zone where institutions sold

- Price often rejects here

- **Thicker border** = Unmitigated (not tested yet) → High probability zone

**🔷 BLUE BOXES (EXT Bullish Order Blocks)**

- Higher timeframe demand zones

- Stronger support levels

- Dashed border = HTF zone

**🟠 ORANGE BOXES (EXT Bearish Order Blocks)**

- Higher timeframe supply zones

- Stronger resistance levels

- Dashed border = HTF zone

### **📊 FAIR VALUE GAPS (FVGs)**

**💠 AQUA BOXES (Bullish FVG)**

- Gap between price movement (inefficiency)

- Price tends to fill these gaps

- Buy zone when price returns

**💜 FUCHSIA BOXES (Bearish FVG)**

- Gap between price movement (inefficiency)

- Price tends to fill these gaps

- Sell zone when price returns

**🟡 YELLOW BOXES (Inverted FVG)**

- FVG that got filled and now acts as support/resistance

- Becomes a key level for future trades

### **⚡ BREAKER BLOCKS**

**BB Labels (Green/Red dotted lines)**

- Failed order blocks that flipped

- Was support, became resistance (or vice versa)

- Strong reversal zones

### **🎯 SMART MONEY ZONES**

**🟡 ACCUMULATION BOXES**

- Consolidation + increasing volume + bullish structure

- Institutions accumulating positions

- Expect bullish breakout

**🟠 DISTRIBUTION BOXES**

- Consolidation + increasing volume + bearish structure

- Institutions distributing/selling

- Expect bearish breakdown

**⚠️ MANIPULATION Labels**

- Large wicks + high volume

- Stop hunt detected

- Watch for reversal

### **💥 VOLUME BUBBLES**

- **Green bubble** = High volume bullish candle (institutional buying)

- **Red bubble** = High volume bearish candle (institutional selling)

- Shows volume multiplier (e.g., "3.2x")

### **📈 MARKET STRUCTURE**

**Small triangles:**

- 🔺 Green triangle below = Swing low

- 🔻 Red triangle above = Swing high

**BOS Labels (Green/Red)**

- Break of Structure

- Trend continuation signal

- **Green BOS** = Bullish continuation

- **Red BOS** = Bearish continuation

**CHOCH Labels (Blue/Orange)**

- Change of Character

- Potential trend reversal

- **Blue CHOCH** = Shift to bullish

- **Orange CHOCH** = Shift to bearish

### **⚠️ DIVERGENCE SIGNALS**

**🔼 BULL DIV (Green label below)**

- Price makes lower low, RSI makes higher low

- Bullish reversal signal

- Strong at oversold levels (RSI < 35)

**🔽 BEAR DIV (Red label above)**

- Price makes higher high, RSI makes lower high

- Bearish reversal signal

- Strong at overbought levels (RSI > 65)

### **🚨 BACKGROUND COLORS**

**Light Green Background**

- 3-4 HTFs bullish + strong trend

- Safe to take long trades

- High confidence environment

**Light Red Background**

- 3-4 HTFs bearish + strong trend

- Safe to take short trades

- High confidence environment

**Light Orange Background**

- Mixed signals across timeframes

- **DANGER ZONE - STAY OUT!**

- Wait for clarity

---

## 🎯 **4. HOW TO READ SIGNALS** {#signals}

### **🟢 LONG SIGNAL GENERATION**

Signal appears when ALL conditions met:

1. ✅ Market structure is bullish (uptrend)

2. ✅ Bullish order block formed

3. ✅ Price above last swing low

4. ✅ RSI < 65 (not overbought)

5. ✅ Volume > 1.2x average

**What You'll See:**

- **🟢 LONG** label at entry point

- Blue line = Entry price

- Red line = Stop loss

- Green dashed lines = TP1, TP2

- Green solid line = TP3 (final target)

**Dashboard Shows:**

- Entry price

- Stop loss level

- TP1 (40% target by default)

- TP2 (70% target by default)

- TP3 (100% target = 2:1 R:R by default)

### **🔴 SHORT SIGNAL GENERATION**

Signal appears when ALL conditions met:

1. ✅ Market structure is bearish (downtrend)

2. ✅ Bearish order block formed

3. ✅ Price below last swing high

4. ✅ RSI > 35 (not oversold)

5. ✅ Volume > 1.2x average

**What You'll See:**

- **🔴 SHORT** label at entry point

- Blue line = Entry price

- Red line = Stop loss

- Green dashed lines = TP1, TP2

- Green solid line = TP3 (final target)

---

## 📈 **5. TRADING STRATEGY** {#strategy}

### **🎓 THE GOLDEN RULES (FOLLOW THESE!)**

#### **Rule #1: MASTER BIAS IS LAW**

```

IF Dashboard shows "🟢 STRONG BULLISH":

✅ Take LONG trades ONLY

❌ Ignore all short signals

IF Dashboard shows "🔴 STRONG BEARISH":

✅ Take SHORT trades ONLY

❌ Ignore all long signals

IF Dashboard shows "⚪ NEUTRAL":

❌ DON'T TRADE

⏰ Wait for alignment

```

#### **Rule #2: Trade WITH Higher Timeframes**

- Check all 4 HTFs in dashboard

- Need at least 2-3 HTFs aligned

- More alignment = higher probability

#### **Rule #3: Use Order Blocks for Entry**

- Wait for price to return to unmitigated OB

- Enter when price touches thick-border box

- Best entries = HTF order block + Current TF order block overlap

#### **Rule #4: Confirm with Volume**

- Wait for 💥 volume bubble at entry

- High volume = institutional participation

- No volume = wait for confirmation

#### **Rule #5: Respect Market Structure**

- Don't fight BOS (continuation)

- Be cautious near CHOCH (reversal)

- Wait for structure to stabilize

### **📝 STEP-BY-STEP TRADING PROCESS**

#### **STEP 1: Check Dashboard**

```

1. Look at INSTITUTIONAL BIAS

- Green = Go long only

- Red = Go short only

- Orange/Gray = Stay out

2. Check HTF alignment

- Count how many HTFs aligned

- Need 2+ for good trades

- Need 3+ for best trades

3. Check current trend strength

- STRONG = good trending moves

- WEAK = choppy, reduce size

```

#### **STEP 2: Identify Key Zones**

```

1. Mark unmitigated order blocks (thick borders)

2. Note FVG zones (aqua/fuchsia boxes)

3. Watch for accumulation/distribution zones

4. Mark breaker blocks (dotted lines)

```

#### **STEP 3: Wait for Signal**

```

IF Bullish Bias:

✅ Wait for price to pull back to:

- Bullish order block (green box)

- Bullish FVG (aqua box)

- Support structure

✅ Wait for 🟢 LONG signal label

✅ Confirm with:

- Volume bubble (💥)

- BOS label (continuation)

- No bearish divergence

IF Bearish Bias:

✅ Wait for price to rally to:

- Bearish order block (red box)

- Bearish FVG (fuchsia box)

- Resistance structure

✅ Wait for 🔴 SHORT signal label

✅ Confirm with:

- Volume bubble (💥)

- BOS label (continuation)

- No bullish divergence

```

#### **STEP 4: Execute Trade**

```

1. Enter at signal (🟢 LONG or 🔴 SHORT label)

2. Set stop loss at red line

3. Set take profits:

- TP1 at first dashed green line (40%)

- TP2 at second dashed green line (70%)

- TP3 at solid green line (100%)

4. Trail stop loss after TP1 hit

```

#### **STEP 5: Manage Trade**

```

1. Move SL to breakeven after TP1 hit

2. Take partial profits at each TP level

3. Let remaining position run to TP3

4. Exit immediately if:

- Dashboard bias changes

- CHOCH appears (trend reversal)

- Manipulation label appears

```

### **💎 ADVANCED STRATEGIES**

#### **Strategy 1: Order Block Retest**

```

1. Wait for strong move (BOS)

2. Wait for pullback to unmitigated OB

3. Enter when price touches OB + signal appears

4. SL below OB (longs) or above OB (shorts)

5. Target next OB or swing point

```

#### **Strategy 2: FVG Fill**

```

1. Identify large FVG (aqua/fuchsia box)

2. Wait for price to return to FVG

3. Enter when price enters FVG + signal appears

4. SL beyond FVG

5. Target 50-100% FVG fill

```

#### **Strategy 3: Accumulation Breakout**

```

1. Wait for ACCUMULATION box to form

2. Wait for price to break out with volume

3. Enter on retest of breakout level

4. SL inside accumulation zone

5. Target measured move (height of box)

```

#### **Strategy 4: Manipulation Fade**

```

1. Wait for ⚠️ MANIPULATION label

2. Wait for price to reverse (wick rejection)

3. Enter opposite direction with signal

4. SL beyond manipulation wick

5. Target previous swing point

```

#### **Strategy 5: Divergence Reversal**

```

1. Wait for 🔼 BULL DIV or 🔽 BEAR DIV

2. Confirm with CHOCH (structure break)

3. Enter on OB retest after divergence

4. SL beyond divergence low/high

5. Target opposite side structure

```

---

## ⚙️ **6. SETTINGS CUSTOMIZATION** {#settings}

### **📦 ORDER BLOCKS**

```

🟢 Show IDM Order Blocks: ON/OFF

- Toggle immediate timeframe order blocks

- Customize colors (default: green/red 85% transparency)

🔷 Show EXT Order Blocks: ON/OFF

- Toggle higher timeframe order blocks

- Customize colors (default: blue/orange 90% transparency)

⚡ Show Breaker Blocks: ON/OFF

- Toggle failed order blocks

🎯 Highlight Unmitigated OBs: ON/OFF

- Makes untested blocks thicker (RECOMMENDED: ON)

→ Extend Order Blocks: ON/OFF

- Extends boxes to the right

Max OBs to Display: 1-50

- How many order blocks to show (default: 10)

```

### **📊 FAIR VALUE GAPS**

```

Show Fair Value Gaps: ON/OFF

Show Inverted FVGs: ON/OFF

Bullish FVG Color: Customize (default: aqua)

Bearish FVG Color: Customize (default: fuchsia)

Min FVG Size %: 0.01+

- Minimum gap size to display (default: 0.1%)

```

### **📈 MARKET STRUCTURE**

```

Show Market Structure: ON/OFF

- Swing highs/lows triangles

Mark BOS: ON/OFF

- Break of Structure labels

Mark CHOCH: ON/OFF

- Change of Character labels

Swing Detection Length: 3-50

- Sensitivity (default: 10)

- Lower = more swings

- Higher = major swings only

Label Size: tiny/small/normal

- Size of structure labels

```

### **🎯 SMART MONEY ZONES**

```

Show Accumulation Zones: ON/OFF

Show Distribution Zones: ON/OFF

Show Manipulation Zones: ON/OFF

Accumulation Detection Period: 10+

- Lookback period (default: 20)

Manipulation Wick Threshold: 1.0+

- Wick size multiplier (default: 1.5)

```

### **📊 VOLUME ANALYSIS**

```

Show Volume Analysis: ON/OFF

Show High Volume Bubbles: ON/OFF

Volume Threshold: 1.0+

- Multiplier for high volume (default: 2.0)

- 2.0 = 2x average volume

Volume MA Period: 5+

- Moving average length (default: 20)

```

### **⚠️ DIVERGENCES**

```

Show Divergences: ON/OFF

RSI Length: 5+

- RSI calculation period (default: 14)

Divergence Lookback: 3-20

- How far back to check (default: 5)

```

### **📋 DASHBOARD**

```

Show Main Dashboard: ON/OFF

- Toggle entire dashboard

Dashboard Position: 9 options

- top_left, top_center, top_right

- middle_left, middle_center, middle_right

- bottom_left, bottom_center, bottom_right

Show HTF Analysis: ON/OFF

- Toggle higher timeframe section

HTF 1: Any timeframe (default: 15)

HTF 2: Any timeframe (default: 60)

HTF 3: Any timeframe (default: 240)

HTF 4: Any timeframe (default: D)

```

### **🎯 TRADE SIGNALS**

```

Show Trade Signals: ON/OFF

- Toggle 🟢 LONG / 🔴 SHORT labels

Show Entry/SL/TP Levels: ON/OFF

- Toggle horizontal lines

Risk:Reward Ratio: 1.0+

- TP3 distance (default: 2.0 = 2:1 R:R)

TP1 % of Total Target: 10-100%

- First target (default: 40%)

TP2 % of Total Target: 10-100%

- Second target (default: 70%)

```

---

## 💡 **7. REAL TRADING EXAMPLES** {#examples}

### **📊 EXAMPLE 1: Perfect Long Setup**

```

SCENARIO: Bitcoin 5-minute chart

Dashboard shows:

✅ 🟢 STRONG BULLISH

✅ HTF1 (15m): UP - STRONG

✅ HTF2 (1H): UP - STRONG

✅ HTF3 (4H): UP - MEDIUM

✅ HTF4 (D): UP - STRONG

✅ Current TF: UP - STRONG

✅ Market Structure: BULLISH

✅ Volume: HIGH 💥

What happened:

1. Price pulled back to green order block (unmitigated)

2. 🟢 LONG signal appeared at $67,500

3. Volume bubble (💥 2.8x) confirmed entry

4. BOS label appeared (continuation)

Entry: $67,500

SL: $67,200 (below OB)

TP1: $67,800 (40%) ✅ Hit

TP2: $68,000 (70%) ✅ Hit

TP3: $68,300 (100%) ✅ Hit

Result: +1.2% profit, 2:1 R:R

```

### **📊 EXAMPLE 2: Perfect Short Setup**

```

SCENARIO: Ethereum 15-minute chart

Dashboard shows:

✅ 🔴 STRONG BEARISH

✅ HTF1 (15m): DOWN - STRONG

✅ HTF2 (1H): DOWN - MEDIUM

✅ HTF3 (4H): DOWN - STRONG

✅ HTF4 (D): DOWN - STRONG

✅ Current TF: DOWN - STRONG

✅ Market Structure: BEARISH

✅ Volume: HIGH 💥

What happened:

1. Price rallied to red order block (unmitigated)

2. 🔴 SHORT signal appeared at $3,520

3. Volume bubble (💥 3.1x) confirmed entry

4. BOS label appeared (bearish continuation)

5. 🔽 BEAR DIV appeared (extra confirmation)

Entry: $3,520

SL: $3,560 (above OB)

TP1: $3,496 (40%) ✅ Hit

TP2: $3,476 (70%) ✅ Hit

TP3: $3,440 (100%) ✅ Hit

Result: +2.3% profit, 2:1 R:R

```

### **📊 EXAMPLE 3: Avoided Bad Trade**

```

SCENARIO: SPY stock 1-hour chart

Dashboard shows:

❌ ⚪ NEUTRAL

❌ HTF1 (15m): UP

❌ HTF2 (1H): DOWN

❌ HTF3 (4H): SIDE

❌ HTF4 (D): UP

❌ Background: Light orange (danger)

What happened:

1. 🟢 LONG signal appeared at $450

2. BUT dashboard showed NEUTRAL

3. Warning: "⚠️ WAIT FOR CLEAR DIRECTION"

4. Ignored signal (followed rules)

5. Price dropped -1.5% shortly after

Result: Avoided -1.5% loss

Key lesson: Trust the dashboard over individual signals!

```

### **📊 EXAMPLE 4: FVG Retest Trade**

```

SCENARIO: Gold futures 30-minute chart

Dashboard shows:

✅ 🟢 BULLISH (2 HTFs aligned)

✅ Current TF: UP - MEDIUM

✅ Large aqua FVG box below price

What happened:

1. Price created large FVG gap

2. Price pulled back into FVG zone

3. 🟢 LONG signal at FVG midpoint $2,045

4. Volume bubble (💥 2.3x) at entry

5. FVG turned yellow (inverted = filled)

Entry: $2,045

SL: $2,040 (below FVG)

TP1: $2,053 (40%) ✅ Hit

TP2: $2,058 (70%) ✅ Hit

TP3: $2,065 (100%) ✅ Hit

Result: +1.0% profit

```

### **📊 EXAMPLE 5: Manipulation Fade**

```

SCENARIO: EUR/USD forex 5-minute chart

Dashboard shows:

✅ 🔴 BEARISH

✅ Current TF: DOWN - STRONG

What happened:

1. Price had large bullish wick

2. ⚠️ MANIPULATION label appeared

3. High volume at wick (stop hunt)

4. Price reversed quickly

5. 🔴 SHORT signal at 1.0895

Entry: 1.0895

SL: 1.0910 (above manipulation wick)

TP1: 1.0880 (40%) ✅ Hit

TP2: 1.0872 (70%) ✅ Hit

TP3: 1.0865 (100%) ✅ Hit

Result: +0.28% profit (30 pips)

```

---

## ⚠️ **8. COMMON MISTAKES TO AVOID**

### **❌ Mistake #1: Trading Against Dashboard**

```

WRONG: Dashboard shows 🔴 BEARISH, but you take a long

CORRECT: Only take shorts when bearish, only longs when bullish

```

### **❌ Mistake #2: Ignoring Higher Timeframes**

```

WRONG: Current 5m looks good, ignored that 1H/4H/D are opposite

CORRECT: Check all HTFs before entry, need 2+ aligned

```

### **❌ Mistake #3: Trading in Neutral Zones**

```

WRONG: Taking trades when dashboard shows ⚪ NEUTRAL

CORRECT: Wait for clear bias (green or red), skip mixed signals

```

### **❌ Mistake #4: No Volume Confirmation**

```

WRONG: Entering without 💥 volume bubble

CORRECT: Wait for high volume institutional participation

```

### **❌ Mistake #5: Ignoring Market Structure**

```

WRONG: Longing into strong bearish structure

CORRECT: Wait for CHOCH (structure change) before reversing

```

### **❌ Mistake #6: Over-Trading**

```

WRONG: Taking every signal that appears

CORRECT: Wait for best setups with all confirmations aligned

```

### **❌ Mistake #7: Moving Stop Loss**

```

WRONG: Moving SL farther away when trade goes against you

CORRECT: Respect original SL, let it hit if wrong

```

### **❌ Mistake #8: Not Taking Partial Profits**

```

WRONG: Holding full position hoping for TP3

CORRECT: Scale out at TP1 (40%), TP2 (70%), let TP3 run

```

---

## 🎯 **9. QUICK REFERENCE CHECKLIST**

### **✅ BEFORE TAKING ANY TRADE:**

```

□ Dashboard shows clear bias (🟢 or 🔴, NOT ⚪)

□ At least 2-3 HTFs aligned with trade direction

□ Current timeframe trend matches trade direction

□ Trend strength is MEDIUM or STRONG (not WEAK)

□ Signal label appeared (🟢 LONG or 🔴 SHORT)

□ Price at key level (OB, FVG, or structure)

□ Volume bubble (💥) confirms entry

□ No opposing divergence signal

□ No opposing CHOCH (reversal warning)

□ Clear entry, SL, and TP levels visible

□ Risk:Reward is favorable (2:1 minimum)

□ Position size calculated (risk max 1-2% account)

```

### **✅ DURING THE TRADE:**

```

□ Monitor dashboard for bias change

□ Watch for CHOCH (could signal reversal)

□ Look for manipulation labels (⚠️)

□ Take partial profits at each TP level

□ Move SL to breakeven after TP1 hit

□ Trail stop using order blocks

□ Exit if dashboard bias changes color

```

### **✅ AFTER THE TRADE:**

```

□ Journal the trade (setup, result, lessons)

□ Review what worked and what didn't

□ Check if you followed all rules

□ Adjust settings if needed

□ Wait for next quality setup

```

---

## 🎓 **10. PRO TIPS**

1. **Best Timeframes**:

- Scalping: 1m, 5m

- Day trading: 5m, 15m

- Swing trading: 1H, 4H

- Position trading: D, W

2. **Best Markets**:

- Crypto (BTC, ETH) = Very responsive

- Forex majors = Clean structure

- Stock indices (SPY, NQ) = Good volume

- Individual stocks = Works best on liquid names

3. **Best Times to Trade**:

- Crypto: 24/7 (best during US/EU hours)

- Forex: London/NY overlap (8am-12pm EST)

- Stocks: First 2 hours + last hour of session

4. **Risk Management**:

- Never risk more than 1-2% per trade

- Use proper position sizing

- Always set stop loss BEFORE entry

- Take profits at planned levels

5. **Optimization**:

- Start with default settings

- Adjust HTFs based on your trading style

- Experiment with swing length for your market

- Tune volume threshold for your asset

---

## 🆘 **11. TROUBLESHOOTING**

### **Problem: No signals appearing**

**Solution:**

- Check if "Show Trade Signals" is enabled

- Verify market has sufficient volatility

- Try lower timeframe (5m instead of 1H)

- Check if conditions are met (volume, structure, RSI)

### **Problem: Too many order blocks**

**Solution:**

- Reduce "Max OBs to Display" (try 5-8)

- Disable "Show EXT Order Blocks"

- Increase swing length to filter minor ones

### **Problem: Dashboard not showing**

**Solution:**

- Enable "Show Main Dashboard"

- Change dashboard position

- Refresh chart

- Check chart has enough data loaded

### **Problem: Signals opposite to dashboard**

**Solution:**

- **Always trust the dashboard over individual signals!**

- This is working as intended - ignore conflicting signals

- Dashboard prevents wrong-direction trades

### **Problem: Too much clutter on chart**

**Solution:**

- Disable FVGs if not using them

- Disable breaker blocks

- Reduce max order blocks

- Hide volume bubbles

- Disable divergences

- Keep only what you actively trade

---

## 🎯 **12. FINAL WORDS**

This indicator is designed to keep you on the RIGHT SIDE of institutional money. The #1 rule is:

> **"When in doubt, follow the dashboard. It's designed to prevent you from trading drunk, stoned, or just plain wrong!"**

### **Your Trading Mantra:**

```

🟢 GREEN DASHBOARD = ONLY LONGS

🔴 RED DASHBOARD = ONLY SHORTS

⚪ NEUTRAL/ORANGE = NO TRADES

Follow this, and you'll stay aligned with smart money!

Remember:

Quality > Quantity

Patience is profitable

The best trade is often no trade

Protect your capital first

Let winners run, cut losers fast

📞 NEED HELP?

If you have questions:

Review this tutorial section by section

Practice on demo account first

Start with larger timeframes (easier to read)

Paper trade until consistently profitable

Start small when going live

Good luck, and trade smart! 🚀📈

MACD Trading System - Professional V2# MACD Trading System - Professional V2

## Executive Summary

**MACD Pro V2** is an institutional-grade trading indicator combining classical MACD analysis with advanced risk management, multi-timeframe confirmation, and comprehensive performance metrics. Designed for both manual traders and algorithmic systems, this indicator provides actionable signals with built-in stop loss calculation, take profit targets, position sizing, and trailing stop logic.

This indicator is NOT just a signal generator—it's a complete trading system with risk/reward management, performance tracking, and market regime detection.

---

## Core Features

### 1. Advanced MACD Calculation

- **Customizable EMAs**: Fast (default 8), Slow (default 21), Signal (default 5)

- **Confirmed Signals**: Uses barstate.isconfirmed to prevent repainting

- **Zero-Line Position**: Shows MACD above/below zero for momentum context

### 2. Multi-Timeframe Analysis

- **4 Simultaneous Timeframes**: 4H, 1H, 15M, 5M analyzed in parallel

- **MTF Alignment Score**: 0-100% showing consensus across timeframes

- **Smart Requests**: Uses lookahead=barmerge.lookahead_off for accuracy

### 3. Market Regime Detection

Automatically identifies current market conditions:

- **TRENDING** - ADX > 25, strong directional movement

- **RANGING** - ADX < 20, choppy sideways movement

- **VOLATILE** - ATR > 1.5x average, high uncertainty

- **NORMAL** - Default market state

### 4. Integrated Risk Management

Complete position management system:

- **Stop Loss Calculation**: Automatic SL placement based on ATR × multiplier

- **Take Profit Targets**: Calculated using Risk:Reward ratio (default 2:1)

- **Position Sizing**: Scales position size based on account risk percentage

- **Trailing Stop**: Dynamically adjusts SL as price moves in your favor

- **Drawdown Monitoring**: Tracks maximum drawdown vs account

### 5. Advanced Signal Scoring

0-100 point system weighing:

- **MTF Alignment (35%)**: Multi-timeframe confirmation strength

- **Momentum (25%)**: RSI conditions + Divergence detection

- **Volume (20%)**: Volume profile and confirmation

- **Volatility (20%)**: Market regime adjustment

**Signal Classifications:**

- **STRONG (70+)**: High confidence, tight stops, optimal entry

- **MEDIUM (50-69)**: Valid signals, confirm with price action

- **WEAK (<50)**: Low conviction, skip or use tight risk management

### 6. Professional Performance Metrics

Real-time trading statistics:

- **Win Rate**: Percentage of winning trades

- **Max Drawdown**: Largest peak-to-trough decline

- **Sharpe Ratio**: Risk-adjusted returns (anualized)

- **Profit Factor**: Gross profit / Gross loss ratio

- **Consecutive Losses**: Psychological stress indicator

### 7. Advanced Filtering System

- **Divergence Detection**: Automatic bullish/bearish divergence identification

- **Support/Resistance**: Pivot-based dynamic S/R levels

- **Volume Confirmation**: Only takes signals with volume > 1.0x average

- **Session Filter**: Optional trading hours restriction