CM Indicator About Indicator:-

1) This is best Indicator for trend identification.

2) This is based on 42 EMA with Upper Band and Lower bands for trend identification.

3) This should be used for Line Bar chart only.

4) Line bar chart should be used at 1 hour for 15 line breaks.

How to Use:-

1) To go with trend is best use of this indicator.

2) This is for stocks and options not for index. Indicator used for Stocks at one hour and options for 10-15 minutes line break.

3) There will be 5% profitability defined for each entry, 3 entries with profit are best posible in same continuous trend 4 and 5th entry is in riskier zone in continuous trend.

4) Loss will only happen if there is trend reversal.

5) Loss could only be one trade of profit out of three profitable trades.

6) Back tested on 200 stocks and 100 options.

Cari dalam skrip untuk "profitable"

AltCoin & MemeCoin Index Correlation [Eddie_Bitcoin]🧠 Philosophy of the Strategy

The AltCoin & MemeCoin Index Correlation Strategy by Eddie_Bitcoin is a carefully engineered trend-following system built specifically for the highly volatile and sentiment-driven world of altcoins and memecoins.

This strategy recognizes that crypto markets—especially niche sectors like memecoins—are not only influenced by individual price action but also by the relative strength or weakness of their broader sector. Hence, it attempts to improve the reliability of trading signals by requiring alignment between a specific coin’s trend and its sector-wide index trend.

Rather than treating each crypto asset in isolation, this strategy dynamically incorporates real-time dominance metrics from custom indices (OTHERS.D and MEME.D) and combines them with local price action through dual exponential moving average (EMA) crossovers. Only when both the asset and its sector are moving in the same direction does it allow for trade entries—making it a confluence-based system rather than a single-signal strategy.

It supports risk-aware capital allocation, partial exits, configurable stop loss and take profit levels, and a scalable equity-compounding model.

✅ Why did I choose OTHERS.D and MEME.D as reference indices?

I selected OTHERS.D and MEME.D because they offer a sector-focused view of crypto market dynamics, especially relevant when trading altcoins and memecoins.

🔹 OTHERS.D tracks the market dominance of all cryptocurrencies outside the top 10 by market cap.

This excludes not only BTC and ETH, but also major stablecoins like USDT and USDC, making it a cleaner indicator of risk appetite across true altcoins.

🔹 This is particularly useful for detecting "Altcoin Season"—periods where capital rotates away from Bitcoin and flows into smaller-cap coins.

A rising OTHERS.D often signals the start of broader altcoin rallies.

🔹 MEME.D, on the other hand, captures the speculative behavior of memecoin segments, which are often driven by retail hype and social media activity.

It's perfect for timing momentum shifts in high-risk, high-reward tokens.

By using these indices, the strategy aligns entries with broader sector trends, filtering out noise and increasing the probability of catching true directional moves, especially in phases of capital rotation and altcoin risk-on behavior.

📐 How It Works — Core Logic and Execution Model

At its heart, this strategy employs dual EMA crossover detection—one pair for the asset being traded and one pair for the selected market index.

A trade is only executed when both EMA crossovers agree on the direction. For example:

Long Entry: Coin's fast EMA > slow EMA and Index's fast EMA > slow EMA

Short Entry: Coin's fast EMA < slow EMA and Index's fast EMA < slow EMA

You can disable the index filter and trade solely based on the asset’s trend just to make a comparison and see if improves a classic EMA crossover strategy.

Additionally, the strategy includes:

- Adaptive position sizing, based on fixed capital or current equity (compound mode)

- Take Profit and Stop Loss in percentage terms

- Smart partial exits when trend momentum fades

- Date filtering for precise backtesting over specific timeframes

- Real-time performance stats, equity tracking, and visual cues on chart

⚙️ Parameters & Customization

🔁 EMA Settings

Each EMA pair is customizable:

Coin Fast EMA: Default = 47

Coin Slow EMA: Default = 50

Index Fast EMA: Default = 47

Index Slow EMA: Default = 50

These control the sensitivity of the trend detection. A wider spread gives smoother, slower entries; a narrower spread makes it more responsive.

🧭 Index Reference

The correlation mechanism uses CryptoCap sector dominance indexes:

OTHERS.D: Dominance of all coins EXCLUDING Top 10 ones

MEME.D: Dominance of all Meme coins

These are dynamically calculated using:

OTHERS_D = OTHERS_cap / TOTAL_cap * 100

MEME_D = MEME_cap / TOTAL_cap * 100

You can select:

Reference Index: OTHERS.D or MEME.D

Or disable the index reference completely (Don't Use Index Reference)

💰 Position Sizing & Risk Management

Two capital allocation models are supported:

- Fixed % of initial capital (default)

- Compound profits, which scales positions as equity grows

Settings:

- Compound profits?: true/false

- % of equity: Between 1% and 200% (default = 10%)

This is critical for users who want to balance growth with risk.

🎯 Take Profit / Stop Loss

Customizable thresholds determine automatic exits:

- TakeProfit: Default = 99999 (disabled)

- StopLoss: Default = 5 (%)

These exits are percentage-based and operate off the entry price vs. current close.

📉 Trend Weakening Exit (Scale Out)

If the position is in profit but the trend weakens (e.g., EMA color signals trend loss), the strategy can partially close a configurable portion of the position:

- Scale Position on Weak Trend?: true/false

- Scaled Percentage: % to close (default = 65%)

This feature is useful for preserving profits without exiting completely.

📆 Date Filter

Useful for segmenting performance over specific timeframes (e.g., bull vs bear markets):

- Filter Date Range of Backtest: ON/OFF

- Start Date and End Date: Custom time range

OTHER PARAMETERS EXPLANATION (Strategy "Properties" Tab):

- Initial Capital is set to 100 USD

- Commission is set to 0.055% (The ones I have on Bybit)

- Slippage is set to 3 ticks

- Margin (short and long) are set to 0.001% to avoid "overspending" your initial capital allocation

📊 Visual Feedback and Debug Tools

📈 EMA Trend Visualization

The slow EMA line is dynamically color-coded to visually display the alignment between the asset trend and the index trend:

Lime: Coin and index both bullish

Teal: Only coin bullish

Maroon: Only index bullish

Red: Both bearish

This allows for immediate visual confirmation of current trend strength.

💬 Real-Time PnL Labels

When a trade closes, a label shows:

Previous trade return in % (first value is the effective PL)

Green background for profit, Red for losses.

📑 Summary Table Overlay

This table appears in a corner of the chart (user-defined) and shows live performance data including:

Trade direction (yellow long, purple short)

Emojis: 💚 for current profit, 😡 for current loss

Total number of trades

Win rate

Max drawdown

Duration in days

Current trade profit/loss (absolute and %)

Cumulative PnL (absolute and %)

APR (Annualized Percentage Return)

Each metric is color-coded:

Green for strong results

Yellow/orange for average

Red/maroon for poor performance

You can select where this appears:

Top Left

Top Right

Bottom Left

Bottom Right (default)

📚 Interpretation of Key Metrics

Equity Multiplier: How many times initial capital has grown (e.g., “1.75x”)

Net Profit: Total gains including open positions

Max Drawdown: Largest peak-to-valley drop in strategy equity

APR: Annualized return calculated based on equity growth and days elapsed

Win Rate: % of profitable trades

PnL %: Percentage profit on the most recent trade

🧠 Advanced Logic & Safety Features

🛑 “Don’t Re-Enter” Filter

If a trade is closed due to StopLoss without a confirmed reversal, the strategy avoids re-entering in that same direction until conditions improve. This prevents false reversals and repetitive losses in sideways markets.

🧷 Equity Protection

No new trades are initiated if equity falls below initial_capital / 30. This avoids overleveraging or continuing to trade when capital preservation is critical.

Keep in mind that past results in no way guarantee future performance.

Eddie Bitcoin

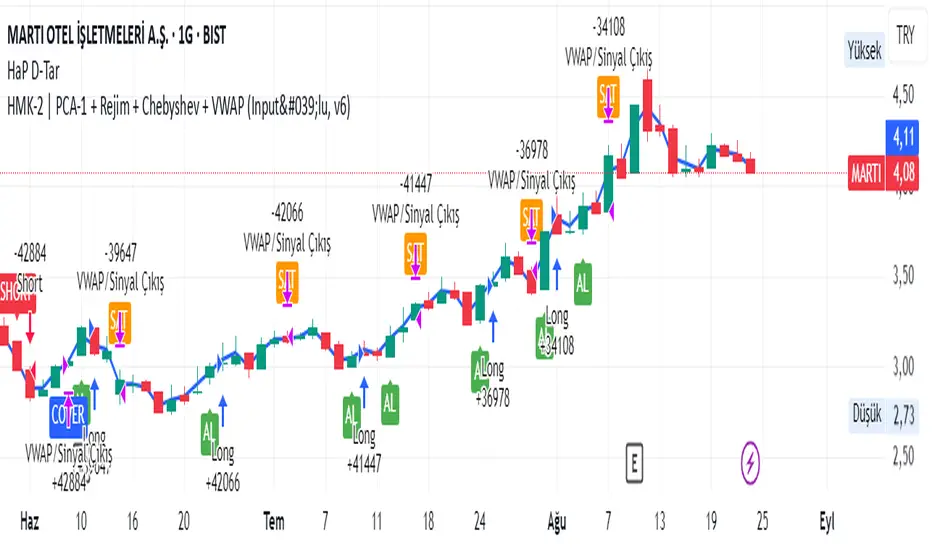

HMK-2 | PCA-1 + Rejim + Chebyshev + VWAP (Input'lu, v6)📌 HMK-2 | PCA-1 + Regime + Chebyshev + VWAP Strategy

1️⃣ Core Structure

Instead of relying on a single indicator, this system uses the Z-Score normalized average of three oscillators (RSI, MFI, ROC).

Signal (PCA-1):

RSI(14), MFI(14), ROC(5) → each is converted into a z-score.

Their average becomes the “composite signal,” our PCA-1 value.

Trend direction: If the Z-score EMA is rising → trend UP. If falling → trend DOWN.

2️⃣ Side Filters

Regime Filter (ADX + EMA)

ADX is calculated manually.

If ADX > 20 → trend exists → a 50-period EMA of this value smooths it.

This turns “trend regime” into a probability between 0–1.

Chebyshev Filter

A return series is checked against mean ± k*sigma bands.

If the return is within this band → valid signal. Extreme moves are filtered out.

VWAP Filter

Long trades: price must be above VWAP.

Short trades: price must be below VWAP.

Trades are only taken on the correct side of institutional cost averages.

3️⃣ Entry Conditions

Long:

PCA-1 signal crosses above threshold.

Trend Up + Regime OK + Chebyshev OK + Above VWAP.

Short:

PCA-1 signal crosses below threshold.

Trend Down + Regime OK + Chebyshev OK + Below VWAP.

4️⃣ Exit Mechanism

Main Exit: ATR-based stop/target.

Stop = entry price – ATR × (SL factor).

Take profit = entry price + ATR × (TP factor).

Additional Exit:

If price crosses to the opposite side of VWAP.

If PCA-1 signal crosses zero.

👉 Prevents trades from being locked, makes exits adaptive.

5️⃣ Labels / Visualization

AL / SHORT → entry points.

SAT / COVER → exit points.

VWAP line plotted in blue.

🧩 Strategy Features

Optimizable parameters:

Z-window (zWin)

Threshold

Chebyshev factor

ATR stop/target multipliers

This system works with:

Disciplined core (PCA-1 signal)

Triple protection (Regime + Chebyshev + VWAP)

Adaptive exits (ATR + VWAP/signal cross)

👉 Not a “single-indicator robot,” but a multi-filtered trade direction engine.

💡 Final Note

This is a base model of the system — open for further development.

I’ve shared the logic to give you a roadmap.

If you spot errors, fix them → that’s how you’ll improve it.

Don’t waste time asking me questions — refine and build it better yourselves.

Wishing you profitable trades. Stay well 🙏

Trapped Traders [ScorsoneEnterprises]This indicator identifies and visualizes trapped traders - market participants caught on the wrong side of price movements with significant volume imbalances. By analyzing volume delta at specific price levels, it reveals where traders are likely experiencing unrealized losses and may be forced to exit their positions.

The point of this tool is to identify where the liquidity in a trend may be.

var lowerTimeframe = switch

useCustomTimeframeInput => lowerTimeframeInput

timeframe.isseconds => "1S"

timeframe.isintraday => "1"

timeframe.isdaily => "5"

=> "60"

= ta.requestVolumeDelta(lowerTimeframe)

price_quantity = map.new()

is_red_candle = close < open

is_green_candle = close > open

for i=0 to lkb-1 by 1

current_vol = price_quantity.get(close)

new_vol = na(current_vol) ? lastVolume : current_vol + lastVolume

price_quantity.put(close, new_vol)

if is_green_candle and new_vol < 0

price_quantity.put(close, new_vol)

else if is_red_candle and new_vol > 0

price_quantity.put(close, new_vol)

We see in this snippet, the lastVolume variable is the most recent volume delta we can receive from the lower timeframe, we keep updating the price level we're keeping track of with that lastVolume from the lower timeframe.

This is the bulk of the concept as this level and size gives us the idea of how many traders were on the wrong side of the trend, and acting as liquidity for the profitable entries. The more, the stronger.

There are 3 ways to visualize this. A basic label, that will display the size and if positive or negative next to the bar, a gradient line that goes 10 bars to the future to be used as a support or resistance line that includes the quantity, and a bubble chart with the quantity. The larger the quantity, the bigger the bubble.

We see in this example on NYMEX:CL1! that there are lines plotted throughout this price action that price interacts with in meaningful way. There are consistently many levels for us.

Here on CME_MINI:ES1! we see the labels on the chart, and the size set to large. It is the same concept just another way to view it.

This chart of CME_MINI:RTY1! shows the bubble chart visualization. It is a way to view it that is pretty non invasive on the chart.

Every timeframe is supported including daily, weekly, and monthly.

The included settings are the display style, like mentioned above. If the user would like to see the volume numbers on the chart. The text size along with the transparency percentage. Following that is the settings for which lower timeframe to calculate the volume delta on. Finally, if you would like to see your inputs in the status line.

No indicator is 100% accurate, use "Trapped Traders" along with your own discretion.

FlowStateTrader FlowState Trader - Advanced Time-Filtered Strategy

## Overview

FlowState Trader is a sophisticated algorithmic trading strategy that combines precision entry signals with intelligent time-based filtering and adaptive risk management. Built for traders seeking to achieve their optimal performance state, FlowState identifies high-probability trading opportunities within user-defined time windows while employing dynamic trailing stops and partial position management.

## Core Strategy Philosophy

FlowState Trader operates on the principle that peak trading performance occurs when three elements align: **Focus** (precise entry signals), **Flow** (optimal time windows), and **State** (intelligent position management). This strategy excels at finding reversal opportunities at key support and resistance levels while filtering out suboptimal trading periods to keep traders in their optimal flow state.

## Key Features

### 🎯 Focus Entry System

**Support/Resistance Zone Trading**:

- Dynamic identification of key price levels using configurable lookback periods

- Entry signals triggered when price interacts with these critical zones

- Volume confirmation ensures genuine breakout/reversal momentum

- Trend filter alignment prevents counter-trend disasters

**Entry Conditions**:

- **Long Signals**: Price closes above support buffer, touches support level, with above-average volume

- **Short Signals**: Price closes below resistance buffer, touches resistance level, with above-average volume

- Optional trend filter using EMA or SMA for directional bias confirmation

### ⏰ FlowState Time Filtering System

**Comprehensive Time Controls**:

- **12-Hour Format Trading Windows**: User-friendly AM/PM time selection

- **Multi-Timezone Support**: UTC, EST, PST, CST with automatic conversion

- **Day-of-Week Filtering**: Trade only weekdays, weekends, or both

- **Lunch Hour Avoidance**: Automatically skips low-volume lunch periods (12-1 PM)

- **Visual Time Indicators**: Background coloring shows active/inactive trading periods

**Smart Time Features**:

- Handles overnight trading sessions seamlessly

- Prevents trades during historically poor performance periods

- Customizable trading hours for different market sessions

- Real-time trading window status in dashboard

### 🛡️ Adaptive Risk Management

**Multi-Level Take Profit System**:

- **TP1**: First profit target with optional partial position closure

- **TP2**: Final profit target for remaining position

- **Flexible Scaling**: Choose number of contracts to close at each level

**Dynamic Trailing Stop Technology**:

- **Three Operating Modes**:

- **Conservative**: Earlier activation, tighter trailing (protect profits)

- **Balanced**: Optimal risk/reward balance (recommended)

- **Aggressive**: Later activation, wider trailing (let winners run)

- **ATR-Based Calculations**: Adapts to current market volatility

- **Automatic Activation**: Engages when position reaches profitability threshold

### 📊 Intelligent Position Sizing

**Contract-Based Management**:

- Configurable entry quantity (1-1000 contracts)

- Partial close quantities for profit-taking

- Clear position tracking and P&L monitoring

- Real-time position status updates

### 🎨 Professional Visualization

**Enhanced Chart Elements**:

- **Entry Zone Highlighting**: Clear visual identification of trading opportunities

- **Dynamic Risk/Reward Lines**: Real-time TP and SL levels with price labels

- **Trailing Stop Visualization**: Live tracking of adaptive stop levels

- **Support/Resistance Lines**: Key level identification

- **Time Window Background**: Visual confirmation of active trading periods

**Dual Dashboard System**:

- **Strategy Dashboard**: Real-time position info, settings status, and current levels

- **Performance Scorecard**: Live P&L tracking, win rates, and trade statistics

- **Customizable Sizing**: Small, Medium, or Large display options

### ⚙️ Comprehensive Customization

**Core Strategy Settings**:

- **Lookback Period**: Support/resistance calculation period (5-100 bars)

- **ATR Configuration**: Period and multipliers for stops/targets

- **Reward-to-Risk Ratios**: Customizable profit target calculations

- **Trend Filter Options**: EMA/SMA selection with adjustable periods

**Time Filter Controls**:

- **Trading Hours**: Start/end times in 12-hour format

- **Timezone Selection**: Four major timezone options

- **Day Restrictions**: Weekend-only, weekday-only, or unrestricted

- **Session Management**: Lunch hour avoidance and custom periods

**Risk Management Options**:

- **Trailing Stop Modes**: Conservative/Balanced/Aggressive presets

- **Partial Close Settings**: Enable/disable with custom quantities

- **Alert System**: Comprehensive notifications for all trade events

### 📈 Performance Tracking

**Real-Time Metrics**:

- Net profit/loss calculation

- Win rate percentage

- Profit factor analysis

- Maximum drawdown tracking

- Total trade count and breakdown

- Current position P&L

**Trade Analytics**:

- Winner/loser ratio tracking

- Real-time performance scorecard

- Strategy effectiveness monitoring

- Risk-adjusted return metrics

### 🔔 Alert System

**Comprehensive Notifications**:

- Entry signal alerts with price and quantity

- Take profit level hits (TP1 and TP2)

- Stop loss activations

- Trailing stop engagements

- Position closure notifications

## Strategy Logic Deep Dive

### Entry Signal Generation

The strategy identifies high-probability reversal points by combining multiple confirmation factors:

1. **Price Action**: Looks for price interaction with key support/resistance levels

2. **Volume Confirmation**: Ensures sufficient market interest and liquidity

3. **Trend Alignment**: Optional filter prevents counter-trend positions

4. **Time Validation**: Only trades during user-defined optimal periods

5. **Zone Analysis**: Entry occurs within calculated buffer zones around key levels

### Risk Management Philosophy

FlowState Trader employs a three-tier risk management approach:

1. **Initial Protection**: ATR-based stop losses set at strategy entry

2. **Profit Preservation**: Trailing stops activate once position becomes profitable

3. **Scaled Exit**: Partial profit-taking allows for both security and potential

### Time-Based Edge

The time filtering system recognizes that not all trading hours are equal:

- Avoids low-volume, high-spread periods

- Focuses on optimal liquidity windows

- Prevents trading during news events (lunch hours)

- Allows customization for different market sessions

## Best Practices and Optimization

### Recommended Settings

**For Scalping (1-5 minute charts)**:

- Lookback Period: 10-20

- ATR Period: 14

- Trailing Stop: Conservative mode

- Time Filter: Major session hours only

**For Day Trading (15-60 minute charts)**:

- Lookback Period: 20-30

- ATR Period: 14-21

- Trailing Stop: Balanced mode

- Time Filter: Extended trading hours

**For Swing Trading (4H+ charts)**:

- Lookback Period: 30-50

- ATR Period: 21+

- Trailing Stop: Aggressive mode

- Time Filter: Disabled or very broad

### Market Compatibility

- **Forex**: Excellent for major pairs during active sessions

- **Stocks**: Ideal for liquid stocks during market hours

- **Futures**: Perfect for index and commodity futures

- **Crypto**: Effective on major cryptocurrencies (24/7 capability)

### Risk Considerations

- **Market Conditions**: Performance varies with volatility regimes

- **Timeframe Selection**: Lower timeframes require tighter risk management

- **Position Sizing**: Never risk more than 1-2% of account per trade

- **Backtesting**: Always test on historical data before live implementation

## Educational Value

FlowState serves as an excellent learning tool for:

- Understanding support/resistance trading

- Learning proper time-based filtering

- Mastering trailing stop techniques

- Developing systematic trading approaches

- Risk management best practices

## Disclaimer

This strategy is for educational and informational purposes only. Past performance does not guarantee future results. Trading involves substantial risk of loss and is not suitable for all investors. Users should thoroughly backtest the strategy and understand all risks before live trading. Always use proper position sizing and never risk more than you can afford to lose.

---

*FlowState Trader represents the evolution of systematic trading - combining classical technical analysis with modern risk management and intelligent time filtering to help traders achieve their optimal performance state through systematic, disciplined execution.*

Imbalance RSI Divergence Strategy# Imbalance RSI Divergence Strategy - User Guide

## What is This Strategy?

This strategy identifies **imbalance** zones in the market and combines them with **RSI divergence** to generate trading signals. It aims to capitalize on price gaps left by institutional investors and large volume movements.

### Main Settings

- **RSI Period (14)**: Period used for RSI calculation. Lower values = more sensitive, higher values = more stable signals.

- **ATR Period (10)**: Period for volatility measurement using Average True Range.

- **ATR Stop Loss Multiplier (2.0)**: How many ATR units to use for stop loss calculation.

- **Risk:Reward Ratio (4.0)**: Risk-reward ratio. 2.0 = 2 units of reward for 1 unit of risk.

- **Use RSI Divergence Filter (true)**: Enables/disables the RSI divergence filter.

### Imbalance Filters

- **Minimum Imbalance Size (ATR) (0.3)**: Minimum imbalance size in ATR units to filter out small imbalances.

- **Enable Lookback Limit (false)**: Activates historical lookback limitations.

- **Maximum Lookback Bars (300)**: Maximum number of bars to look back.

### Visual Settings

- **Show Imbalance Size**: Displays imbalance size in ATR units.

- **Show RSI Divergence Lines**: Shows/hides divergence lines.

- **Divergence Line Colors**: Colors for bullish/bearish divergence lines.

### Volatility-Based Adjustments

- **Low volatility markets**:

- Minimum Imbalance Size: 0.2-0.4 ATR

- ATR Stop Loss Multiplier: 1.5-2.0

- **High volatility markets**:

- Minimum Imbalance Size: 0.5-1.0 ATR

- ATR Stop Loss Multiplier: 2.5-3.5

### Risk Tolerance

- **Conservative approach**:

- Risk:Reward Ratio: 2.0-3.0

- RSI Divergence Filter: Enabled

- Minimum Imbalance Size: Higher (0.5+ ATR)

- **Aggressive approach**:

- Risk:Reward Ratio: 4.0-6.0

- Minimum Imbalance Size: Lower (0.2-0.3 ATR)

###Market Conditions

- **Trending markets**: Higher RSI Period (21-28)

- **Sideways markets**: Lower RSI Period (10-14)

- **Volatile markets**: Higher ATR Multiplier

## Recommended Testing Procedure

1. **Start with default settings** and backtest on 3-6 months of historical data

2. **Adjust RSI Period** to see which value produces better results

3. **Optimize ATR Multiplier** for stop loss levels

4. **Test different Risk:Reward ratios** comparatively

5. **Fine-tune Minimum Imbalance Size** to improve signal quality

## Important Considerations

- **False positive signals**: Imbalances may be less reliable during low volatility periods

- **Market openings**: First hours often produce more imbalances but can be riskier

- **News events**: Consider disabling strategy during major news releases

- **Backtesting**: Test across different market conditions (trending, sideways, volatile)

## Recommended Settings for Beginners

**Safe settings for new users:**

- RSI Period: 14

- ATR Period: 14

- ATR Stop Loss Multiplier: 2.5

- Risk:Reward Ratio: 3.0

- Minimum Imbalance Size: 0.5 ATR

- RSI Divergence Filter: Enabled

## Advanced Tips

### Signal Quality Improvement

- **Combine with market structure**: Look for imbalances near key support/resistance levels

- **Volume confirmation**: Higher volume during imbalance formation increases reliability

- **Multiple timeframe analysis**: Confirm signals on higher timeframes

### Risk Management

- **Position sizing**: Never risk more than 1-2% of account per trade

- **Maximum drawdown**: Set overall stop loss for the strategy

- **Market hours**: Consider avoiding low liquidity periods

### Performance Monitoring

- **Win rate**: Track percentage of profitable trades

- **Average R:R**: Monitor actual risk-reward achieved vs. target

- **Maximum consecutive losses**: Set alerts for strategy review

This strategy works best when combined with proper risk management and market analysis. Always backtest thoroughly before using real money and adjust parameters based on your specific market and trading style.

Order Blocks + Order-Flow ProxiesOrder Blocks + Order-Flow Proxies

This indicator combines structural analysis of order blocks with lightweight order-flow style proxies, providing a tool for chart annotation and contextual study. It is designed to help users visualize where significant structural shifts occur and how simple volume-based signals behave around those areas. The script does not guarantee profitable outcomes, nor does it issue financial advice. It is intended purely for research, learning, and discretionary use.

Conceptual Background

Order Blocks

An “order block” is a term often used to describe a zone on the chart where price left behind a significant reversal or imbalance before continuing strongly in the opposite direction. In practice, this can mean the last bullish or bearish candle before a strong breakout. Traders sometimes study these regions because they believe that unfilled resting orders may exist there, or simply because they mark important pivots in price structure. This indicator detects such moments by scanning for breaks of structure (BOS). When price pushes above or below recent swing levels with sufficient displacement, the script identifies the prior opposite candle as the potential order block.

Break of Structure

A break of structure in this context is defined when the closing price moves beyond the highest high or lowest low of a short lookback window. The script compares the magnitude of this break to an ATR-based displacement filter. This helps ensure that only meaningful moves are marked rather than small, random fluctuations.

Order-Flow Proxies

Traditional order flow analysis may use bid/ask data, footprint charts, or volume profiles. Because TradingView scripts cannot access true order-book data, this indicator instead uses proxy signals derived from standard chart data:

Delta (proxy): Estimated imbalance of buying vs. selling pressure, approximated using bar direction and volume.

Imbalance ratio: Normalizes delta by total volume, ranging between -1 and +1 in theory.

Cumulative Delta (CVD): Running sum of delta over time.

Effort vs. Result (EvR): A comparison between volume and actual bar movement, highlighting cases where large effort produced little result (or vice versa).

These are not real order-flow measurements, but rather simple mathematical constructs that mimic some of its logic.

How the Script Works

Detecting Break of Structure

The user specifies a swing length. When price closes above the recent high (for bullish BOS) or below the recent low (for bearish BOS), a potential shift is recorded.

To qualify, the breakout must exceed a displacement filter proportional to the ATR. This helps filter out weak moves.

Locating the Order Block Candle

Once a BOS is confirmed, the script looks back within a short window to find the last opposite-colored candle.

The high/low or open/close of that candle (depending on user settings) is marked as the potential order block zone.

Drawing and Maintaining Zones

Each order block is represented as a colored rectangle extending forward in time.

Bullish zones are teal by default, bearish zones are red.

Zones extend until invalidated (price closing or wicking beyond them, depending on user preference) or until a user-defined lifespan expires.

A pruning mechanism ensures that only the most recent set number of zones remain, preventing chart overload.

Monitoring Touches

The script checks whether the current bar’s range overlaps any existing order block.

If so, the “closest” zone is considered touched, and a label may appear on the chart.

Confirmation Filters

Touches can optionally be confirmed by order-flow proxies.

For a bullish confirmation, the following must align:

Imbalance ratio above threshold,

Delta EMA positive,

Effort vs. Result positive.

For a bearish confirmation, the opposite holds true.

Optionally, a higher-timeframe EMA slope filter can gate these confirmations. For example, a bullish confirmation may only be accepted if the higher-timeframe EMA is sloping upward.

Alerts

Users may create alerts based on conditions such as “bullish touch confirmed” or “bearish touch confirmed.”

Alerts can be gated to only fire after bar close, reducing intrabar noise.

Standard alertcondition calls are provided, and optional inline alert() calls can be enabled.

Inputs and Customization

Structure & OB

Swing length: Defines how many bars back to check for BOS.

ATR length & displacement factor: Adjust sensitivity for structural breaks.

Body vs. wick reference: Choose whether zones are based on candle bodies or full ranges.

Invalidation rule: Pick between wick breach or close beyond the level.

Lifespan (bars): Limit how long a zone remains active.

Max keep: Cap the number of zones stored to reduce clutter.

Order-Flow Proxies

Delta mode: Choose between “Close vs Previous Close” or “Body” for delta calculation.

EMA length: Smooths the delta/imbalance series.

Z-score lookback: Defines the averaging window for EvR.

Confirmation thresholds: Adjust the imbalance levels required for long/short confirmation.

Higher Timeframe Filter

Enable HTF gate: Optional filter requiring higher-timeframe EMA slope alignment.

HTF timeframe & EMA length: Configurable for context alignment.

Style

Colors and transparency for bullish and bearish zones.

Border color customization.

Alerts

Enable inline alerts: Optional direct calls to alert().

Alerts on bar close only: Helps avoid multiple firings during bar formation.

Practical Use

This tool is best seen as a way to annotate charts and to study how simple volume-derived signals behave near important structural levels. Some users may:

Observe whether order blocks line up with later price reactions.

Study how imbalance or cumulative delta conditions align with these zones.

Use it in a discretionary workflow to highlight areas of interest for deeper analysis.

Because the proxies are based only on candle OHLCV data, they are approximations. They cannot replace true depth-of-market analysis. Similarly, order block detection here is one specific algorithmic interpretation; other traders may define order blocks differently.

Limitations and Disclaimers

This indicator does not predict future price movement.

It does not access real order book or tick-by-tick data. All signals are derived from bar OHLCV.

Past performance of signals or zones does not guarantee future results.

The script is for educational and informational purposes only. It is not financial advice.

Users should test thoroughly, adjust parameters to their own instruments and timeframes, and use it in combination with broader analysis.

Summary

The Order Blocks + Order-Flow Proxies script is an experimental study tool that:

Detects potential order blocks using a displacement-filtered break of structure.

Marks these zones as boxes that persist until invalidation or expiry.

Provides lightweight order-flow-style proxies such as delta, imbalance, CVD, and effort vs. result.

Allows confirmation of zone touches through these proxies and optional higher-timeframe context.

Offers flexible customization, alerting, and chart-style options.

It is not a trading system by itself but rather a framework for studying price/volume behavior around structurally significant areas. With careful exploration, it can give users new ways to visualize market structure and to understand how simple flow-like measures behave in those contexts.

Indicator: Profitability by Day & Hour (stacked, non-overlay)What it does

This tool performs a simple seasonality study on the selected symbol. It measures historical returns and summarizes them in two horizontal heatmaps:

Hours table (top) — Columns 00–23 show the average return of each clock hour, plus sample size, win rate, volatility (SD), and a t-score.

Days table (middle) — Columns 1–7 correspond to Mon–Sun with the same metrics.

Summary (bottom) — Shows the most profitable day and hour in the history loaded on your chart.

Green cells indicate higher average returns; red cells indicate lower/negative averages. The layout is centered on the screen, with the hours table above the days table for quick scanning.

How it works (methodology)

Returns: by default the indicator uses log returns ln(Ct/Ct-1) (you can switch to simple % if you prefer).

Daily aggregation (no look-ahead): day statistics are computed from completed daily closes via a higher timeframe request. Yesterday’s daily close vs. the prior day is added to the appropriate weekday bucket, preventing repaint/forward bias.

Hourly aggregation (intraday only): hour statistics are computed bar-to-bar on the current intraday timeframe and accumulated by clock hour (00–23) of the symbol’s exchange timezone.

Metrics per bucket:

Mean: average return in that bucket.

n: number of observations.

Win%: share of positive returns.

SD: standard deviation of returns (volatility proxy).

t-score: mean / SD * sqrt(n) — a quick stability signal (not a hypothesis test).

The indicator does not rely on future data and does not repaint past values.

Reading the tables

Start with the Mean row in each table: it’s color-mapped (red → yellow → green).

Check n (sample size). A bright green cell with very low n is less meaningful than a mild green cell with large n.

Use Win% and SD to judge consistency and noise.

t-score is a compact “signal-to-noise × sample size” measure; higher absolute values suggest more stable effects.

Typical observations traders look for (purely illustrative): for some equity indices, the first hour after the cash open can dominate; for FX/crypto, certain late-US or early-Asia hours sometimes stand out. Always verify on your symbol and timeframe.

Market Clarity Pro Market Clarity Pro — See Key Zones, Trend & Volume Signals

Spot yesterday’s High (Supply) and Low (Demand) instantly — and know exactly where big buyers and sellers are likely waiting.

Red zones = strong selling pressure.

Green zones = strong buying pressure.

Plus, a built-in trend line keeps you trading in the right direction and away from sudden reversals.

You’ll also see:

🔴 Red arrow — not a sell signal, but a sign of heavy sellers stepping in, with volume confirmation and a candle breaking the previous one.

🔵 Blue arrow — not a buy signal, but a sign of strong buyers stepping in, with volume confirmation and a candle breaking the previous one.

These arrows highlight potential volume spikes and breakouts for confirmation only — you still confirm with the higher time frame for more market clarity.

Break above supply. Possible uptrend.

Break below demand. Possible downtrend.

📌 Before using this tool, watch the tutorial video to learn exactly how to apply it and how to spot profitable trades with confidence.

Kelly Position Size CalculatorThis position sizing calculator implements the Kelly Criterion, developed by John L. Kelly Jr. at Bell Laboratories in 1956, to determine mathematically optimal position sizes for maximizing long-term wealth growth. Unlike arbitrary position sizing methods, this tool provides a scientifically solution based on your strategy's actual performance statistics and incorporates modern refinements from over six decades of academic research.

The Kelly Criterion addresses a fundamental question in capital allocation: "What fraction of capital should be allocated to each opportunity to maximize growth while avoiding ruin?" This question has profound implications for financial markets, where traders and investors constantly face decisions about optimal capital allocation (Van Tharp, 2007).

Theoretical Foundation

The Kelly Criterion for binary outcomes is expressed as f* = (bp - q) / b, where f* represents the optimal fraction of capital to allocate, b denotes the risk-reward ratio, p indicates the probability of success, and q represents the probability of loss (Kelly, 1956). This formula maximizes the expected logarithm of wealth, ensuring maximum long-term growth rate while avoiding the risk of ruin.

The mathematical elegance of Kelly's approach lies in its derivation from information theory. Kelly's original work was motivated by Claude Shannon's information theory (Shannon, 1948), recognizing that maximizing the logarithm of wealth is equivalent to maximizing the rate of information transmission. This connection between information theory and wealth accumulation provides a deep theoretical foundation for optimal position sizing.

The logarithmic utility function underlying the Kelly Criterion naturally embodies several desirable properties for capital management. It exhibits decreasing marginal utility, penalizes large losses more severely than it rewards equivalent gains, and focuses on geometric rather than arithmetic mean returns, which is appropriate for compounding scenarios (Thorp, 2006).

Scientific Implementation

This calculator extends beyond basic Kelly implementation by incorporating state of the art refinements from academic research:

Parameter Uncertainty Adjustment: Following Michaud (1989), the implementation applies Bayesian shrinkage to account for parameter estimation error inherent in small sample sizes. The adjustment formula f_adjusted = f_kelly × confidence_factor + f_conservative × (1 - confidence_factor) addresses the overconfidence bias documented by Baker and McHale (2012), where the confidence factor increases with sample size and the conservative estimate equals 0.25 (quarter Kelly).

Sample Size Confidence: The reliability of Kelly calculations depends critically on sample size. Research by Browne and Whitt (1996) provides theoretical guidance on minimum sample requirements, suggesting that at least 30 independent observations are necessary for meaningful parameter estimates, with 100 or more trades providing reliable estimates for most trading strategies.

Universal Asset Compatibility: The calculator employs intelligent asset detection using TradingView's built-in symbol information, automatically adapting calculations for different asset classes without manual configuration.

ASSET SPECIFIC IMPLEMENTATION

Equity Markets: For stocks and ETFs, position sizing follows the calculation Shares = floor(Kelly Fraction × Account Size / Share Price). This straightforward approach reflects whole share constraints while accommodating fractional share trading capabilities.

Foreign Exchange Markets: Forex markets require lot-based calculations following Lot Size = Kelly Fraction × Account Size / (100,000 × Base Currency Value). The calculator automatically handles major currency pairs with appropriate pip value calculations, following industry standards described by Archer (2010).

Futures Markets: Futures position sizing accounts for leverage and margin requirements through Contracts = floor(Kelly Fraction × Account Size / Margin Requirement). The calculator estimates margin requirements as a percentage of contract notional value, with specific adjustments for micro-futures contracts that have smaller sizes and reduced margin requirements (Kaufman, 2013).

Index and Commodity Markets: These markets combine characteristics of both equity and futures markets. The calculator automatically detects whether instruments are cash-settled or futures-based, applying appropriate sizing methodologies with correct point value calculations.

Risk Management Integration

The calculator integrates sophisticated risk assessment through two primary modes:

Stop Loss Integration: When fixed stop-loss levels are defined, risk calculation follows Risk per Trade = Position Size × Stop Loss Distance. This ensures that the Kelly fraction accounts for actual risk exposure rather than theoretical maximum loss, with stop-loss distance measured in appropriate units for each asset class.

Strategy Drawdown Assessment: For discretionary exit strategies, risk estimation uses maximum historical drawdown through Risk per Trade = Position Value × (Maximum Drawdown / 100). This approach assumes that individual trade losses will not exceed the strategy's historical maximum drawdown, providing a reasonable estimate for strategies with well-defined risk characteristics.

Fractional Kelly Approaches

Pure Kelly sizing can produce substantial volatility, leading many practitioners to adopt fractional Kelly approaches. MacLean, Sanegre, Zhao, and Ziemba (2004) analyze the trade-offs between growth rate and volatility, demonstrating that half-Kelly typically reduces volatility by approximately 75% while sacrificing only 25% of the growth rate.

The calculator provides three primary Kelly modes to accommodate different risk preferences and experience levels. Full Kelly maximizes growth rate while accepting higher volatility, making it suitable for experienced practitioners with strong risk tolerance and robust capital bases. Half Kelly offers a balanced approach popular among professional traders, providing optimal risk-return balance by reducing volatility significantly while maintaining substantial growth potential. Quarter Kelly implements a conservative approach with low volatility, recommended for risk-averse traders or those new to Kelly methodology who prefer gradual introduction to optimal position sizing principles.

Empirical Validation and Performance

Extensive academic research supports the theoretical advantages of Kelly sizing. Hakansson and Ziemba (1995) provide a comprehensive review of Kelly applications in finance, documenting superior long-term performance across various market conditions and asset classes. Estrada (2008) analyzes Kelly performance in international equity markets, finding that Kelly-based strategies consistently outperform fixed position sizing approaches over extended periods across 19 developed markets over a 30-year period.

Several prominent investment firms have successfully implemented Kelly-based position sizing. Pabrai (2007) documents the application of Kelly principles at Berkshire Hathaway, noting Warren Buffett's concentrated portfolio approach aligns closely with Kelly optimal sizing for high-conviction investments. Quantitative hedge funds, including Renaissance Technologies and AQR, have incorporated Kelly-based risk management into their systematic trading strategies.

Practical Implementation Guidelines

Successful Kelly implementation requires systematic application with attention to several critical factors:

Parameter Estimation: Accurate parameter estimation represents the greatest challenge in practical Kelly implementation. Brown (1976) notes that small errors in probability estimates can lead to significant deviations from optimal performance. The calculator addresses this through Bayesian adjustments and confidence measures.

Sample Size Requirements: Users should begin with conservative fractional Kelly approaches until achieving sufficient historical data. Strategies with fewer than 30 trades may produce unreliable Kelly estimates, regardless of adjustments. Full confidence typically requires 100 or more independent trade observations.

Market Regime Considerations: Parameters that accurately describe historical performance may not reflect future market conditions. Ziemba (2003) recommends regular parameter updates and conservative adjustments when market conditions change significantly.

Professional Features and Customization

The calculator provides comprehensive customization options for professional applications:

Multiple Color Schemes: Eight professional color themes (Gold, EdgeTools, Behavioral, Quant, Ocean, Fire, Matrix, Arctic) with dark and light theme compatibility ensure optimal visibility across different trading environments.

Flexible Display Options: Adjustable table size and position accommodate various chart layouts and user preferences, while maintaining analytical depth and clarity.

Comprehensive Results: The results table presents essential information including asset specifications, strategy statistics, Kelly calculations, sample confidence measures, position values, risk assessments, and final position sizes in appropriate units for each asset class.

Limitations and Considerations

Like any analytical tool, the Kelly Criterion has important limitations that users must understand:

Stationarity Assumption: The Kelly Criterion assumes that historical strategy statistics represent future performance characteristics. Non-stationary market conditions may invalidate this assumption, as noted by Lo and MacKinlay (1999).

Independence Requirement: Each trade should be independent to avoid correlation effects. Many trading strategies exhibit serial correlation in returns, which can affect optimal position sizing and may require adjustments for portfolio applications.

Parameter Sensitivity: Kelly calculations are sensitive to parameter accuracy. Regular calibration and conservative approaches are essential when parameter uncertainty is high.

Transaction Costs: The implementation incorporates user-defined transaction costs but assumes these remain constant across different position sizes and market conditions, following Ziemba (2003).

Advanced Applications and Extensions

Multi-Asset Portfolio Considerations: While this calculator optimizes individual position sizes, portfolio-level applications require additional considerations for correlation effects and aggregate risk management. Simplified portfolio approaches include treating positions independently with correlation adjustments.

Behavioral Factors: Behavioral finance research reveals systematic biases that can interfere with Kelly implementation. Kahneman and Tversky (1979) document loss aversion, overconfidence, and other cognitive biases that lead traders to deviate from optimal strategies. Successful implementation requires disciplined adherence to calculated recommendations.

Time-Varying Parameters: Advanced implementations may incorporate time-varying parameter models that adjust Kelly recommendations based on changing market conditions, though these require sophisticated econometric techniques and substantial computational resources.

Comprehensive Usage Instructions and Practical Examples

Implementation begins with loading the calculator on your desired trading instrument's chart. The system automatically detects asset type across stocks, forex, futures, and cryptocurrency markets while extracting current price information. Navigation to the indicator settings allows input of your specific strategy parameters.

Strategy statistics configuration requires careful attention to several key metrics. The win rate should be calculated from your backtest results using the formula of winning trades divided by total trades multiplied by 100. Average win represents the sum of all profitable trades divided by the number of winning trades, while average loss calculates the sum of all losing trades divided by the number of losing trades, entered as a positive number. The total historical trades parameter requires the complete number of trades in your backtest, with a minimum of 30 trades recommended for basic functionality and 100 or more trades optimal for statistical reliability. Account size should reflect your available trading capital, specifically the risk capital allocated for trading rather than total net worth.

Risk management configuration adapts to your specific trading approach. The stop loss setting should be enabled if you employ fixed stop-loss exits, with the stop loss distance specified in appropriate units depending on the asset class. For stocks, this distance is measured in dollars, for forex in pips, and for futures in ticks. When stop losses are not used, the maximum strategy drawdown percentage from your backtest provides the risk assessment baseline. Kelly mode selection offers three primary approaches: Full Kelly for aggressive growth with higher volatility suitable for experienced practitioners, Half Kelly for balanced risk-return optimization popular among professional traders, and Quarter Kelly for conservative approaches with reduced volatility.

Display customization ensures optimal integration with your trading environment. Eight professional color themes provide optimization for different chart backgrounds and personal preferences. Table position selection allows optimal placement within your chart layout, while table size adjustment ensures readability across different screen resolutions and viewing preferences.

Detailed Practical Examples

Example 1: SPY Swing Trading Strategy

Consider a professionally developed swing trading strategy for SPY (S&P 500 ETF) with backtesting results spanning 166 total trades. The strategy achieved 110 winning trades, representing a 66.3% win rate, with an average winning trade of $2,200 and average losing trade of $862. The maximum drawdown reached 31.4% during the testing period, and the available trading capital amounts to $25,000. This strategy employs discretionary exits without fixed stop losses.

Implementation requires loading the calculator on the SPY daily chart and configuring the parameters accordingly. The win rate input receives 66.3, while average win and loss inputs receive 2200 and 862 respectively. Total historical trades input requires 166, with account size set to 25000. The stop loss function remains disabled due to the discretionary exit approach, with maximum strategy drawdown set to 31.4%. Half Kelly mode provides the optimal balance between growth and risk management for this application.

The calculator generates several key outputs for this scenario. The risk-reward ratio calculates automatically to 2.55, while the Kelly fraction reaches approximately 53% before scientific adjustments. Sample confidence achieves 100% given the 166 trades providing high statistical confidence. The recommended position settles at approximately 27% after Half Kelly and Bayesian adjustment factors. Position value reaches approximately $6,750, translating to 16 shares at a $420 SPY price. Risk per trade amounts to approximately $2,110, representing 31.4% of position value, with expected value per trade reaching approximately $1,466. This recommendation represents the mathematically optimal balance between growth potential and risk management for this specific strategy profile.

Example 2: EURUSD Day Trading with Stop Losses

A high-frequency EURUSD day trading strategy demonstrates different parameter requirements compared to swing trading approaches. This strategy encompasses 89 total trades with a 58% win rate, generating an average winning trade of $180 and average losing trade of $95. The maximum drawdown reached 12% during testing, with available capital of $10,000. The strategy employs fixed stop losses at 25 pips and take profit targets at 45 pips, providing clear risk-reward parameters.

Implementation begins with loading the calculator on the EURUSD 1-hour chart for appropriate timeframe alignment. Parameter configuration includes win rate at 58, average win at 180, and average loss at 95. Total historical trades input receives 89, with account size set to 10000. The stop loss function is enabled with distance set to 25 pips, reflecting the fixed exit strategy. Quarter Kelly mode provides conservative positioning due to the smaller sample size compared to the previous example.

Results demonstrate the impact of smaller sample sizes on Kelly calculations. The risk-reward ratio calculates to 1.89, while the Kelly fraction reaches approximately 32% before adjustments. Sample confidence achieves 89%, providing moderate statistical confidence given the 89 trades. The recommended position settles at approximately 7% after Quarter Kelly application and Bayesian shrinkage adjustment for the smaller sample. Position value amounts to approximately $700, translating to 0.07 standard lots. Risk per trade reaches approximately $175, calculated as 25 pips multiplied by lot size and pip value, with expected value per trade at approximately $49. This conservative position sizing reflects the smaller sample size, with position sizes expected to increase as trade count surpasses 100 and statistical confidence improves.

Example 3: ES1! Futures Systematic Strategy

Systematic futures trading presents unique considerations for Kelly criterion application, as demonstrated by an E-mini S&P 500 futures strategy encompassing 234 total trades. This systematic approach achieved a 45% win rate with an average winning trade of $1,850 and average losing trade of $720. The maximum drawdown reached 18% during the testing period, with available capital of $50,000. The strategy employs 15-tick stop losses with contract specifications of $50 per tick, providing precise risk control mechanisms.

Implementation involves loading the calculator on the ES1! 15-minute chart to align with the systematic trading timeframe. Parameter configuration includes win rate at 45, average win at 1850, and average loss at 720. Total historical trades receives 234, providing robust statistical foundation, with account size set to 50000. The stop loss function is enabled with distance set to 15 ticks, reflecting the systematic exit methodology. Half Kelly mode balances growth potential with appropriate risk management for futures trading.

Results illustrate how favorable risk-reward ratios can support meaningful position sizing despite lower win rates. The risk-reward ratio calculates to 2.57, while the Kelly fraction reaches approximately 16%, lower than previous examples due to the sub-50% win rate. Sample confidence achieves 100% given the 234 trades providing high statistical confidence. The recommended position settles at approximately 8% after Half Kelly adjustment. Estimated margin per contract amounts to approximately $2,500, resulting in a single contract allocation. Position value reaches approximately $2,500, with risk per trade at $750, calculated as 15 ticks multiplied by $50 per tick. Expected value per trade amounts to approximately $508. Despite the lower win rate, the favorable risk-reward ratio supports meaningful position sizing, with single contract allocation reflecting appropriate leverage management for futures trading.

Example 4: MES1! Micro-Futures for Smaller Accounts

Micro-futures contracts provide enhanced accessibility for smaller trading accounts while maintaining identical strategy characteristics. Using the same systematic strategy statistics from the previous example but with available capital of $15,000 and micro-futures specifications of $5 per tick with reduced margin requirements, the implementation demonstrates improved position sizing granularity.

Kelly calculations remain identical to the full-sized contract example, maintaining the same risk-reward dynamics and statistical foundations. However, estimated margin per contract reduces to approximately $250 for micro-contracts, enabling allocation of 4-5 micro-contracts. Position value reaches approximately $1,200, while risk per trade calculates to $75, derived from 15 ticks multiplied by $5 per tick. This granularity advantage provides better position size precision for smaller accounts, enabling more accurate Kelly implementation without requiring large capital commitments.

Example 5: Bitcoin Swing Trading

Cryptocurrency markets present unique challenges requiring modified Kelly application approaches. A Bitcoin swing trading strategy on BTCUSD encompasses 67 total trades with a 71% win rate, generating average winning trades of $3,200 and average losing trades of $1,400. Maximum drawdown reached 28% during testing, with available capital of $30,000. The strategy employs technical analysis for exits without fixed stop losses, relying on price action and momentum indicators.

Implementation requires conservative approaches due to cryptocurrency volatility characteristics. Quarter Kelly mode is recommended despite the high win rate to account for crypto market unpredictability. Expected position sizing remains reduced due to the limited sample size of 67 trades, requiring additional caution until statistical confidence improves. Regular parameter updates are strongly recommended due to cryptocurrency market evolution and changing volatility patterns that can significantly impact strategy performance characteristics.

Advanced Usage Scenarios

Portfolio position sizing requires sophisticated consideration when running multiple strategies simultaneously. Each strategy should have its Kelly fraction calculated independently to maintain mathematical integrity. However, correlation adjustments become necessary when strategies exhibit related performance patterns. Moderately correlated strategies should receive individual position size reductions of 10-20% to account for overlapping risk exposure. Aggregate portfolio risk monitoring ensures total exposure remains within acceptable limits across all active strategies. Professional practitioners often consider using lower fractional Kelly approaches, such as Quarter Kelly, when running multiple strategies simultaneously to provide additional safety margins.

Parameter sensitivity analysis forms a critical component of professional Kelly implementation. Regular validation procedures should include monthly parameter updates using rolling 100-trade windows to capture evolving market conditions while maintaining statistical relevance. Sensitivity testing involves varying win rates by ±5% and average win/loss ratios by ±10% to assess recommendation stability under different parameter assumptions. Out-of-sample validation reserves 20% of historical data for parameter verification, ensuring that optimization doesn't create curve-fitted results. Regime change detection monitors actual performance against expected metrics, triggering parameter reassessment when significant deviations occur.

Risk management integration requires professional overlay considerations beyond pure Kelly calculations. Daily loss limits should cease trading when daily losses exceed twice the calculated risk per trade, preventing emotional decision-making during adverse periods. Maximum position limits should never exceed 25% of account value in any single position regardless of Kelly recommendations, maintaining diversification principles. Correlation monitoring reduces position sizes when holding multiple correlated positions that move together during market stress. Volatility adjustments consider reducing position sizes during periods of elevated VIX above 25 for equity strategies, adapting to changing market conditions.

Troubleshooting and Optimization

Professional implementation often encounters specific challenges requiring systematic troubleshooting approaches. Zero position size displays typically result from insufficient capital for minimum position sizes, negative expected values, or extremely conservative Kelly calculations. Solutions include increasing account size, verifying strategy statistics for accuracy, considering Quarter Kelly mode for conservative approaches, or reassessing overall strategy viability when fundamental issues exist.

Extremely high Kelly fractions exceeding 50% usually indicate underlying problems with parameter estimation. Common causes include unrealistic win rates, inflated risk-reward ratios, or curve-fitted backtest results that don't reflect genuine trading conditions. Solutions require verifying backtest methodology, including all transaction costs in calculations, testing strategies on out-of-sample data, and using conservative fractional Kelly approaches until parameter reliability improves.

Low sample confidence below 50% reflects insufficient historical trades for reliable parameter estimation. This situation demands gathering additional trading data, using Quarter Kelly approaches until reaching 100 or more trades, applying extra conservatism in position sizing, and considering paper trading to build statistical foundations without capital risk.

Inconsistent results across similar strategies often stem from parameter estimation differences, market regime changes, or strategy degradation over time. Professional solutions include standardizing backtest methodology across all strategies, updating parameters regularly to reflect current conditions, and monitoring live performance against expectations to identify deteriorating strategies.

Position sizes that appear inappropriately large or small require careful validation against traditional risk management principles. Professional standards recommend never risking more than 2-3% per trade regardless of Kelly calculations. Calibration should begin with Quarter Kelly approaches, gradually increasing as comfort and confidence develop. Most institutional traders utilize 25-50% of full Kelly recommendations to balance growth with prudent risk management.

Market condition adjustments require dynamic approaches to Kelly implementation. Trending markets may support full Kelly recommendations when directional momentum provides favorable conditions. Ranging or volatile markets typically warrant reducing to Half or Quarter Kelly to account for increased uncertainty. High correlation periods demand reducing individual position sizes when multiple positions move together, concentrating risk exposure. News and event periods often justify temporary position size reductions during high-impact releases that can create unpredictable market movements.

Performance monitoring requires systematic protocols to ensure Kelly implementation remains effective over time. Weekly reviews should compare actual versus expected win rates and average win/loss ratios to identify parameter drift or strategy degradation. Position size efficiency and execution quality monitoring ensures that calculated recommendations translate effectively into actual trading results. Tracking correlation between calculated and realized risk helps identify discrepancies between theoretical and practical risk exposure.

Monthly calibration provides more comprehensive parameter assessment using the most recent 100 trades to maintain statistical relevance while capturing current market conditions. Kelly mode appropriateness requires reassessment based on recent market volatility and performance characteristics, potentially shifting between Full, Half, and Quarter Kelly approaches as conditions change. Transaction cost evaluation ensures that commission structures, spreads, and slippage estimates remain accurate and current.

Quarterly strategic reviews encompass comprehensive strategy performance analysis comparing long-term results against expectations and identifying trends in effectiveness. Market regime assessment evaluates parameter stability across different market conditions, determining whether strategy characteristics remain consistent or require fundamental adjustments. Strategic modifications to position sizing methodology may become necessary as markets evolve or trading approaches mature, ensuring that Kelly implementation continues supporting optimal capital allocation objectives.

Professional Applications

This calculator serves diverse professional applications across the financial industry. Quantitative hedge funds utilize the implementation for systematic position sizing within algorithmic trading frameworks, where mathematical precision and consistent application prove essential for institutional capital management. Professional discretionary traders benefit from optimized position management that removes emotional bias while maintaining flexibility for market-specific adjustments. Portfolio managers employ the calculator for developing risk-adjusted allocation strategies that enhance returns while maintaining prudent risk controls across diverse asset classes and investment strategies.

Individual traders seeking mathematical optimization of capital allocation find the calculator provides institutional-grade methodology previously available only to professional money managers. The Kelly Criterion establishes theoretical foundation for optimal capital allocation across both single strategies and multiple trading systems, offering significant advantages over arbitrary position sizing methods that rely on intuition or fixed percentage approaches. Professional implementation ensures consistent application of mathematically sound principles while adapting to changing market conditions and strategy performance characteristics.

Conclusion

The Kelly Criterion represents one of the few mathematically optimal solutions to fundamental investment problems. When properly understood and carefully implemented, it provides significant competitive advantage in financial markets. This calculator implements modern refinements to Kelly's original formula while maintaining accessibility for practical trading applications.

Success with Kelly requires ongoing learning, systematic application, and continuous refinement based on market feedback and evolving research. Users who master Kelly principles and implement them systematically can expect superior risk-adjusted returns and more consistent capital growth over extended periods.

The extensive academic literature provides rich resources for deeper study, while practical experience builds the intuition necessary for effective implementation. Regular parameter updates, conservative approaches with limited data, and disciplined adherence to calculated recommendations are essential for optimal results.

References

Archer, M. D. (2010). Getting Started in Currency Trading: Winning in Today's Forex Market (3rd ed.). John Wiley & Sons.

Baker, R. D., & McHale, I. G. (2012). An empirical Bayes approach to optimising betting strategies. Journal of the Royal Statistical Society: Series D (The Statistician), 61(1), 75-92.

Breiman, L. (1961). Optimal gambling systems for favorable games. In J. Neyman (Ed.), Proceedings of the Fourth Berkeley Symposium on Mathematical Statistics and Probability (pp. 65-78). University of California Press.

Brown, D. B. (1976). Optimal portfolio growth: Logarithmic utility and the Kelly criterion. In W. T. Ziemba & R. G. Vickson (Eds.), Stochastic Optimization Models in Finance (pp. 1-23). Academic Press.

Browne, S., & Whitt, W. (1996). Portfolio choice and the Bayesian Kelly criterion. Advances in Applied Probability, 28(4), 1145-1176.

Estrada, J. (2008). Geometric mean maximization: An overlooked portfolio approach? The Journal of Investing, 17(4), 134-147.

Hakansson, N. H., & Ziemba, W. T. (1995). Capital growth theory. In R. A. Jarrow, V. Maksimovic, & W. T. Ziemba (Eds.), Handbooks in Operations Research and Management Science (Vol. 9, pp. 65-86). Elsevier.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Kaufman, P. J. (2013). Trading Systems and Methods (5th ed.). John Wiley & Sons.

Kelly Jr, J. L. (1956). A new interpretation of information rate. Bell System Technical Journal, 35(4), 917-926.

Lo, A. W., & MacKinlay, A. C. (1999). A Non-Random Walk Down Wall Street. Princeton University Press.

MacLean, L. C., Sanegre, E. O., Zhao, Y., & Ziemba, W. T. (2004). Capital growth with security. Journal of Economic Dynamics and Control, 28(4), 937-954.

MacLean, L. C., Thorp, E. O., & Ziemba, W. T. (2011). The Kelly Capital Growth Investment Criterion: Theory and Practice. World Scientific.

Michaud, R. O. (1989). The Markowitz optimization enigma: Is 'optimized' optimal? Financial Analysts Journal, 45(1), 31-42.

Pabrai, M. (2007). The Dhandho Investor: The Low-Risk Value Method to High Returns. John Wiley & Sons.

Shannon, C. E. (1948). A mathematical theory of communication. Bell System Technical Journal, 27(3), 379-423.

Tharp, V. K. (2007). Trade Your Way to Financial Freedom (2nd ed.). McGraw-Hill.

Thorp, E. O. (2006). The Kelly criterion in blackjack sports betting, and the stock market. In L. C. MacLean, E. O. Thorp, & W. T. Ziemba (Eds.), The Kelly Capital Growth Investment Criterion: Theory and Practice (pp. 789-832). World Scientific.

Van Tharp, K. (2007). Trade Your Way to Financial Freedom (2nd ed.). McGraw-Hill Education.

Vince, R. (1992). The Mathematics of Money Management: Risk Analysis Techniques for Traders. John Wiley & Sons.

Vince, R., & Zhu, H. (2015). Optimal betting under parameter uncertainty. Journal of Statistical Planning and Inference, 161, 19-31.

Ziemba, W. T. (2003). The Stochastic Programming Approach to Asset, Liability, and Wealth Management. The Research Foundation of AIMR.

Further Reading

For comprehensive understanding of Kelly Criterion applications and advanced implementations:

MacLean, L. C., Thorp, E. O., & Ziemba, W. T. (2011). The Kelly Capital Growth Investment Criterion: Theory and Practice. World Scientific.

Vince, R. (1992). The Mathematics of Money Management: Risk Analysis Techniques for Traders. John Wiley & Sons.

Thorp, E. O. (2017). A Man for All Markets: From Las Vegas to Wall Street. Random House.

Cover, T. M., & Thomas, J. A. (2006). Elements of Information Theory (2nd ed.). John Wiley & Sons.

Ziemba, W. T., & Vickson, R. G. (Eds.). (2006). Stochastic Optimization Models in Finance. World Scientific.

Clean Multi-Indicator Alignment System

Overview

A sophisticated multi-indicator alignment system designed for 24/7 trading across all markets, with pure signal-based exits and no time restrictions. Perfect for futures, forex, and crypto markets that operate around the clock.

Key Features

🎯 Multi-Indicator Confluence System

EMA Cross Strategy: Fast EMA (5) and Slow EMA (10) for precise trend direction

VWAP Integration: Institution-level price positioning analysis

RSI Momentum: 7-period RSI for momentum confirmation and reversal detection

MACD Signals: Optimized 8/17/5 configuration for scalping responsiveness

Volume Confirmation: Customizable volume multiplier (default 1.6x) for signal validation

🚀 Advanced Entry Logic

Initial Full Alignment: Requires all 5 indicators + volume confirmation

Smart Continuation Entries: EMA9 pullback entries when trend momentum remains intact

Flexible Time Controls: Optional session filtering or 24/7 operation

🎪 Pure Signal-Based Exits

No Forced Closes: Positions exit only on technical signal reversals

Dual Exit Conditions: EMA9 breakdown + RSI flip OR MACD cross + EMA20 breakdown

Trend Following: Allows profitable trends to run their full course

Perfect for Swing Scalping: Ideal for multi-session position holding

📊 Visual Interface

Real-Time Status Dashboard: Live alignment monitoring for all indicators

Color-Coded Candles: Instant visual confirmation of entry/exit signals

Clean Chart Display: Toggle-able EMAs and VWAP with professional styling

Signal Differentiation: Clear labels for entries, X-crosses for exits

🔔 Alert System

Entry Notifications: Separate alerts for buy/sell signals

Exit Warnings: Technical breakdown alerts for position management

Mobile Ready: Push notifications to TradingView mobile app

Market Applications

Perfect For:

Gold Futures (GC): 24-hour precious metals trading

NASDAQ Futures (NQ): High-volatility index scalping

Forex Markets: Currency pairs with continuous operation

Crypto Trading: 24/7 cryptocurrency momentum plays

Energy Futures: Oil, gas, and commodity swing trades

Optimal Timeframes:

1-5 Minutes: Ultra-fast scalping during high volatility

5-15 Minutes: Balanced approach for most markets

15-30 Minutes: Swing scalping for trend following

🧠 Smart Position Management

Tracks implied position direction

Prevents conflicting signals

Allows trend continuation entries

State-aware exit logic

⚡ Scalping Optimized

Fast-reacting indicators with shorter periods

Volume-based confirmation reduces false signals

Clean entry/exit visualization

Minimal lag for time-sensitive trades

Configuration Options

All parameters fully customizable:

EMA Lengths: Adjustable from 1-30 periods

RSI Period: 1-14 range for different market conditions

MACD Settings: Fast (1-15), Slow (1-30), Signal (1-10)

Volume Confirmation: 0.5-5.0x multiplier range

Visual Preferences: Colors, displays, and table options

Risk Management Features

Clear visual exit signals prevent emotion-based decisions

Volume confirmation reduces false breakouts

Multi-indicator confluence improves signal quality

Optional time filtering for session-specific strategies

Best Use Cases

Futures Scalping: NQ, ES, GC during active sessions

Forex Swing Trading: Major pairs during overlap periods

Crypto Momentum: Bitcoin, Ethereum trend following

24/7 Automated Systems: Algorithmic trading implementation

Multi-Market Scanning: Portfolio-wide signal monitoring

Gemini Trend Following SystemStrategy Description: The Gemini Trend Following System

Core Philosophy

This is a long-term trend-following system designed for a position trader or a patient swing trader, not a day trader. The fundamental goal is to capture the majority of a stock's major, multi-month or even multi-year uptrend.

The core principle is: "Buy weakness in a confirmed uptrend, and sell only when the uptrend's structure is fundamentally broken."

It operates on the belief that it's more profitable to ride a durable trend than to chase short-term breakouts or worry about daily price fluctuations. It prioritizes staying in a winning trade over frequent trading.

The Three Pillars of the Strategy

The script's logic is built on three distinct pillars, processed in order:

1. The Regime Filter: "Is This Stock in a Healthy Uptrend?"

Before even considering a trade, the script acts as a strict gatekeeper. It will only "watch" a stock if it meets all the criteria of a healthy, long-term uptrend. This is the most important part of the strategy as it filters out weak or speculative stocks.

A stock passes this filter if:

The 50-day Simple Moving Average (SMA) is above the 200-day SMA. This is the classic definition of a "Golden Cross" state, indicating the medium-term trend is stronger than the long-term trend—a hallmark of a bull market for the stock.