Candle StrategyThis strategy is based candle count number also strategy analysis -

Rules for buy-

1) choose Candle Number(Ex.-47) For Trade

2) Trade Sell if price is above high of day 1st candle that mean direction is upside

3) We are taking stop loss on lowest low of candle since day first candle to trade no.

4) close Trade at last bar of the day

5) Trader Can Choose Trade Direction From input

Rules for Sell-

1) Choose Candle Number(Ex.-47) For Trade

2) Trade Sell if price is below low of day 1st candle that mean direction is downside

3) We are taking stop loss on highest of candle since day first candle to trade no.

4) close Trade at last bar of the day

5) Trader Can Choose Trade Direction From input

Note - this strategy can be also use for static to understand which candle will make low/high of the day high chance Example in bank nifty 5 minutes chart candle no 47 have highest trade

opportunity appear on long side ...this data is small based on 5000 previous bar ...

Disclaimer: market involves significant risks, including complete possible loss of funds. Consequently trading is not suitable for all investors and traders. By increasing leverage risk increases as well.With the demo account you can test any trading strategies you wish in a risk-free environment. Please bear in mind that the results of the transactions of the practice account are virtual, and do not reflect any real profit or loss or a real trading environment, whereas market conditions may affect both the quotation and execution

Cari dalam skrip untuk "profitable"

ATR StopThe "ATR Stop" indicator is designed to provide traders with insights into potential stop levels based on Average True Range (ATR) calculations specifically tailored for profitable (green candles) and unprofitable (red candles) price movements. This tool aims to assist traders in identifying potential stop levels that adjust dynamically based on the volatility of distinct market conditions.

The indicator functions by calculating two types of ATR: one for profitable movements and the other for unprofitable movements. The Average True Range is calculated separately for green and red candles, allowing users to assess potential stop levels more accurately based on the nature of price movements.

Key features of the "ATR Stop" indicator include:

Custom ATR Calculation: It calculates the ATR for profitable (green) and unprofitable (red) movements separately, considering only specific candle types based on their closing price relative to their opening price.

Dynamic Multiplier: Users can adjust the multiplier to fine-tune the sensitivity of the ATR-based stop levels, accommodating different risk preferences and market conditions.

Clear Visualization: The indicator plots the ATR levels for profitable (green) and unprofitable (red) movements one candle ahead on the chart, providing a visual representation of potential stop levels.

To use the indicator effectively, traders can adjust the ATR length and multiplier parameters based on their trading strategies and risk management preferences. By considering distinct price movements, this tool can assist in setting more informed stop levels in varying market conditions.

Please note that while the "ATR Stop" indicator can be a valuable addition to a trader's toolbox, it should be used in conjunction with other technical analysis tools and risk management strategies to make well-informed trading decisions.

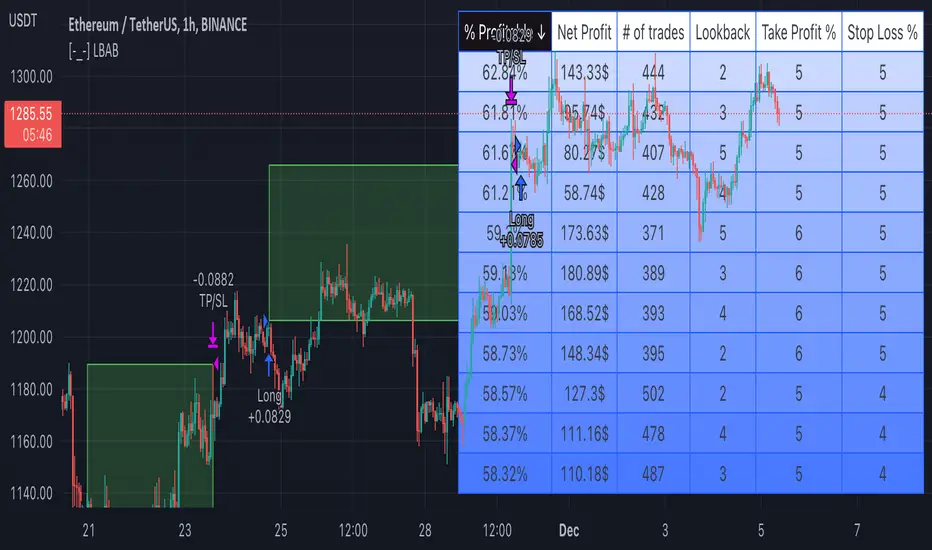

[-_-] Level Breakout, Auto Backtesting StrategyDescription:

A Long only strategy based on breakout from a certain level formed by High price. It has auto-backtesting capabilities (you set ranges for the three main parameters: Lookback, TP and SL; the strategy then goes through different combinations of those parameters and displays a table with results that you can sort by Percentage of profitable trades AND/OR Net profit AND/OR Number of trades). So you can, for example, sort only by Net profit to find combination of parameters that gives highest net profit, or sort by Net profit and Percentage profitable to find a combination of parameters that gives the best balance between profitability and profit. The auto-backtesting also takes into account the commission which is set in % in the inputs (make sure to set the same value in properties of the strategy so that auto-backtesting and real backtesting results match).

NOTE: auto-backtesting only find the best combinations and displays them in a table, you will then need to manually set the Lookback, TP and SL inputs for real backtesting to match.

Parameters:

- Lookback -> # of bars for filtering signals; recommended range from 2 to 5

- TP (%) -> take profit; recommended range from 5 to 10

- SL (%) -> stop loss; recommended range from 1 to 5

- Commission (%) -> commission per trade

- Min/Max Lookback -> lookback range for auto-backtesting

- Min/Max TP -> take profit range for auto-backtesting

- Min/Max SL -> stop loss range for auto-backtesting

- Percentage profitable -> sort by percentage of profitable trades

- Net profit -> sort by net profit

- Number of trades -> sort by number of trades

SAR+RSI+EMAs SignalsNOTE:

Indicator based strategies may expire and begin to work again. There are various ways to check the expiration of these strategies but I suggest equity curve trading (EC trading) as the best one.

Please check every single indicator based strategy to see if it’s still profitable or it has been expired to avoid losses.

Principles:

I personally believe every profitable indicator-based setup need 3 factors. Actually I analyze indicator-based set up in this way!

1- Trend detector: a tool that detect the “trend”.

2- Oscillators (Discount finder): a tool that detects “discounts” in the direction of the trend.

3- Stimulus: A tool that indicates the Initiation of a movement.

There may be profitable strategies that do not use all three, because other factors are strong enough to lead us to profit, but they are rare and sometimes they hide the other forgotten factor in the main two ones.

Elements:

(Since most of traders here, are familiar with these famous indicators I will not take your time to write about their uses and formula)

SAR: As a Trend detector, regarding position of close and SAR

EMA 7 and EMA 21: As trend detectors, regarding position of EMA 7 as fast “moving average” and EMA 21 as slow one. Also we need another confirmation for trend regarding EMA 7 and closing price of the signal candle.

RSI: In this strategy RSI is used both as a discount finder and a stimulus.

For RSI being over/under 50, regarding the trend, a possible discount may have been occurred. Imagine these conditions: close>EMA7, EMA7>EMA21, close>SAR and simultaneously RSI being under 50 is really a sign of powerful uptrend which it’s RSI decreasing might be a sign of corrective move, which will be following a bullish impulsive move.

The other use of RSI is to stimulate a buy signal by “crossing” over 50 or 30 (50 as balanced point of momentum and 30 as a sign of ending an oversold) or stimulate a sell signal by “crossing” under 50 or 70 (50 as balanced point of momentum and 70 as a sign of ending an overbought).

Entry point: you can use one of the followings.

1- Open of the next candle

2- EMA 7

3- Open of the signal candle

(Totally optional but “open of the next candle” is suggested by me.)

SL: Use one of the followings.

1- SAR or some pips (regarding ATR Or your experience of this trading instrument’s fluctuations in this time frame) below the SAR

2- Fixed amount (regarding ATR Or your experience of this trading instrument’s fluctuations in this time frame)

3- Use EMA21 as dynamic SL (if a candle far enough from the initiative candle close over (for sell) below ( for buy)

Again number 1 is suggested by me.

TP: Use one of the followings.

1- Use static levels or zones of support and resistance as TP.

2- Use dynamic levels for instance band of BB or moving averages (Moving the SL is possible).

3- Use fixed R to R

And I believe static zones of support and resistance work better.

Examples:

I indicate a buy signal on the chart!

Using local level as TP worked just good.

Using EMA was better in this case.

And using a riskier level or a fixed R to R is obvious in the chart!

Since in the range markets, this strategy may not work well and at the same time, TP to SL might be too small to be worth the risk, I prefer to use levels to filter range market conditions!

I convert all those circumstances to a simple buy and sell signs on the chart!

EMA21 and SAR are still visible because it is possible that traders use them for their TP and SL.

This is how it look without EMA21 and SAR!

Another screenshot of this strategy!

I also add a check box to filter signals by another trend detector. MATD created by me to help traders detect trend!

As it’s visible, some profitable signals filtered too, but using a longer-term trend detector as an additional one, alongside the double EMAs is very useful for this strategy.

The other box “use high&low instead of close for fast EMA” makes the “EMA7 and close” trend detector an easygoing one!

Almost everything is editable here!

*** I did not invent this strategy, you can find it for free on net ***

I'll change it to a "strategy" instead of an indicator if reader like to!

Webhook Starter Kit [HullBuster]

Introduction

This is an open source strategy which provides a framework for webhook enabled projects. It is designed to work out-of-the-box on any instrument triggering on an intraday bar interval. This is a full featured script with an emphasis on actual trading at a brokerage through the TradingView alert mechanism and without requiring browser plugins.

The source code is written in a self documenting style with clearly defined sections. The sections “communicate” with each other through state variables making it easy for the strategy to evolve and improve. This is an excellent place for Pine Language beginners to start their strategy building journey. The script exhibits many Pine Language features which will certainly ad power to your script building abilities.

This script employs a basic trend follow strategy utilizing a forward pyramiding technique. Trend detection is implemented through the use of two higher time frame series. The market entry setup is a Simple Moving Average crossover. Positions exit by passing through conditional take profit logic. The script creates ten indicators including a Zscore oscillator to measure support and resistance levels. The indicator parameters are exposed through 47 strategy inputs segregated into seven sections. All of the inputs are equipped with detailed tool tips to help you get started.

To improve the transition from simulation to execution, strategy.entry and strategy.exit calls show enhanced message text with embedded keywords that are combined with the TradingView placeholders at alert time. Thereby, enabling a single JSON message to generate multiple execution events. This is genius stuff from the Pine Language development team. Really excellent work!

This document provides a sample alert message that can be applied to this script with relatively little modification. Without altering the code, the strategy inputs can alter the behavior to generate thousands of orders or simply a few dozen. It can be applied to crypto, stocks or forex instruments. A good way to look at this script is as a webhook lab that can aid in the development of your own endpoint processor, impress your co-workers and have hours of fun.

By no means is a webhook required or even necessary to benefit from this script. The setups, exits, trend detection, pyramids and DCA algorithms can be easily replaced with more sophisticated versions. The modular design of the script logic allows you to incrementally learn and advance this script into a functional trading system that you can be proud of.

Design

This is a trend following strategy that enters long above the trend line and short below. There are five trend lines that are visible by default but can be turned off in Section 7. Identified, in frequency order, as follows:

1. - EMA in the chart time frame. Intended to track price pressure. Configured in Section 3.

2. - ALMA in the higher time frame specified in Section 2 Signal Line Period.

3. - Linear Regression in the higher time frame specified in Section 2 Signal Line Period.

4. - Linear Regression in the higher time frame specified in Section 2 Signal Line Period.

5. - DEMA in the higher time frame specified in Section 2 Trend Line Period.

The Blue, Green and Orange lines are signal lines are on the same time frame. The time frame selected should be at least five times greater than the chart time frame. The Purple line represents the trend line for which prices above the line suggest a rising market and prices below a falling market. The time frame selected for the trend should be at least five times greater than the signal lines.

Three oscillators are created as follows:

1. Stochastic - In the chart time frame. Used to enter forward pyramids.

2. Stochastic - In the Trend period. Used to detect exit conditions.

3. Zscore - In the Signal period. Used to detect exit conditions.

The Stochastics are configured identically other than the time frame. The period is set in Section 2.

Two Simple Moving Averages provide the trade entry conditions in the form of a crossover. Crossing up is a long entry and down is a short. This is in fact the same setup you get when you select a basic strategy from the Pine editor. The crossovers are configured in Section 3. You can see where the crosses are occurring by enabling Show Entry Regions in Section 7.

The script has the capacity for pyramids and DCA. Forward pyramids are enabled by setting the Pyramid properties tab with a non zero value. In this case add on trades will enter the market on dips above the position open price. This process will continue until the trade exits. Downward pyramids are available in Crypto and Range mode only. In this case add on trades are placed below the entry price in the drawdown space until the stop is hit. To enable downward pyramids set the Pyramid Minimum Span In Section 1 to a non zero value.

This implementation of Dollar Cost Averaging (DCA) triggers off consecutive losses. Each loss in a run increments a sequence number. The position size is increased as a multiple of this sequence. When the position eventually closes at a profit the sequence is reset. DCA is enabled by setting the Maximum DCA Increments In Section 1 to a non zero value.

It should be noted that the pyramid and DCA features are implemented using a rudimentary design and as such do not perform with the precision of my invite only scripts. They are intended as a feature to stress test your webhook endpoint. As is, you will need to buttress the logic for it to be part of an automated trading system. It is for this reason that I did not apply a Martingale algorithm to this pyramid implementation. But, hey, it’s an open source script so there is plenty of room for learning and your own experimentation.

How does it work

The overall behavior of the script is governed by the Trading Mode selection in Section 1. It is the very first input so you should think about what behavior you intend for this strategy at the onset of the configuration. As previously discussed, this script is designed to be a trend follower. The trend being defined as where the purple line is predominately heading. In BiDir mode, SMA crossovers above the purple line will open long positions and crosses below the line will open short. If pyramiding is enabled add on trades will accumulate on dips above the entry price. The value applied to the Minimum Profit input in Section 1 establishes the threshold for a profitable exit. This is not a hard number exit. The conditional exit logic must be satisfied in order to permit the trade to close. This is where the effort put into the indicator calibration is realized. There are four ways the trade can exit at a profit:

1. Natural exit. When the blue line crosses the green line the trade will close. For a long position the blue line must cross under the green line (downward). For a short the blue must cross over the green (upward).

2. Alma / Linear Regression event. The distance the blue line is from the green and the relative speed the cross is experiencing determines this event. The activation thresholds are set in Section 6 and relies on the period and length set in Section 2. A long position will exit on an upward thrust which exceeds the activation threshold. A short will exit on a downward thrust.

3. Exponential event. The distance the yellow line is from the blue and the relative speed the cross is experiencing determines this event. The activation thresholds are set in Section 3 and relies on the period and length set in the same section.

4. Stochastic event. The purple line stochastic is used to measure overbought and over sold levels with regard to position exits. Signal line positions combined with a reading over 80 signals a long profit exit. Similarly, readings below 20 signal a short profit exit.

Another, optional, way to exit a position is by Bale Out. You can enable this feature in Section 1. This is a handy way to reduce the risk when carrying a large pyramid stack. Instead of waiting for the entire position to recover we exit early (bale out) as soon as the profit value has doubled.

There are lots of ways to implement a bale out but the method I used here provides a succinct example. Feel free to improve on it if you like. To see where the Bale Outs occur, enable Show Bale Outs in Section 7. Red labels are rendered below each exit point on the chart.

There are seven selectable Trading Modes available from the drop down in Section 1:

1. Long - Uses the strategy.risk.allow_entry_in to execute long only trades. You will still see shorts on the chart.

2. Short - Uses the strategy.risk.allow_entry_in to execute short only trades. You will still see long trades on the chart.

3. BiDir - This mode is for margin trading with a stop. If a long position was initiated above the trend line and the price has now fallen below the trend, the position will be reversed after the stop is hit. Forward pyramiding is available in this mode if you set the Pyramiding value in the Properties tab. DCA can also be activated.

4. Flip Flop - This is a bidirectional trading mode that automatically reverses on a trend line crossover. This is distinctively different from BiDir since you will get a reversal even without a stop which is advantageous in non-margin trading.

5. Crypto - This mode is for crypto trading where you are buying the coins outright. In this case you likely want to accumulate coins on a crash. Especially, when all the news outlets are talking about the end of Bitcoin and you see nice deep valleys on the chart. Certainly, under these conditions, the market will be well below the purple line. No margin so you can’t go short. Downward pyramids are enabled for Crypto mode when two conditions are met. First the Pyramiding value in the Properties tab must be non zero. Second the Pyramid Minimum Span in Section 1 must be non zero.

6. Range - This is a counter trend trading mode. Longs are entered below the purple trend line and shorts above. Useful when you want to test your webhook in a market where the trend line is bisecting the signal line series. Remember that this strategy is a trend follower. It’s going to get chopped out in a range bound market. By turning on the Range mode you will at least see profitable trades while stuck in the range. However, when the market eventually picks a direction, this mode will sustain losses. This range trading mode is a rudimentary implementation that will need a lot of improvement if you want to create a reliable switch hitter (trend/range combo).

7. No Trade. Useful when setting up the trend lines and the entry and exit is not important.

Once in the trade, long or short, the script tests the exit condition on every bar. If not a profitable exit then it checks if a pyramid is required. As mentioned earlier, the entry setups are quite primitive. Although they can easily be replaced by more sophisticated algorithms, what I really wanted to show is the diminished role of the position entry in the overall life of the trade. Professional traders spend much more time on the management of the trade beyond the market entry. While your trade entry is important, you can get in almost anywhere and still land a profitable exit.

If DCA is enabled, the size of the position will increase in response to consecutive losses. The number of times the position can increase is limited by the number set in Maximum DCA Increments of Section 1. Once the position breaks the losing streak the trade size will return the default quantity set in the Properties tab. It should be noted that the Initial Capital amount set in the Properties tab does not affect the simulation in the same way as a real account. In reality, running out of money will certainly halt trading. In fact, your account would be frozen long before the last penny was committed to a trade. On the other hand, TradingView will keep running the simulation until the current bar even if your funds have been technically depleted.

Entry and exit use the strategy.entry and strategy.exit calls respectfully. The alert_message parameter has special keywords that the endpoint expects to properly calculate position size and message sequence. The alert message will embed these keywords in the JSON object through the {{strategy.order.alert_message}} placeholder. You should use whatever keywords are expected from the endpoint you intend to webhook in to.

Webhook Integration

The TradingView alerts dialog provides a way to connect your script to an external system which could actually execute your trade. This is a fantastic feature that enables you to separate the data feed and technical analysis from the execution and reporting systems. Using this feature it is possible to create a fully automated trading system entirely on the cloud. Of course, there is some work to get it all going in a reliable fashion. Being a strategy type script place holders such as {{strategy.position_size}} can be embedded in the alert message text. There are more than 10 variables which can write internal script values into the message for delivery to the specified endpoint.

Entry and exit use the strategy.entry and strategy.exit calls respectfully. The alert_message parameter has special keywords that my endpoint expects to properly calculate position size and message sequence. The alert message will embed these keywords in the JSON object through the {{strategy.order.alert_message}} placeholder. You should use whatever keywords are expected from the endpoint you intend to webhook in to.

Here is an excerpt of the fields I use in my webhook signal:

"broker_id": "kraken",

"account_id": "XXX XXXX XXXX XXXX",

"symbol_id": "XMRUSD",

"action": "{{strategy.order.action}}",

"strategy": "{{strategy.order.id}}",

"lots": "{{strategy.order.contracts}}",

"price": "{{strategy.order.price}}",

"comment": "{{strategy.order.alert_message}}",

"timestamp": "{{time}}"

Though TradingView does a great job in dispatching your alert this feature does come with a few idiosyncrasies. Namely, a single transaction call in your script may cause multiple transmissions to the endpoint. If you are using placeholders each message describes part of the transaction sequence. A good example is closing a pyramid stack. Although the script makes a single strategy.close() call, the endpoint actually receives a close message for each pyramid trade. The broker, on the other hand, only requires a single close. The incongruity of this situation is exacerbated by the possibility of messages being received out of sequence. Depending on the type of order designated in the message, a close or a reversal. This could have a disastrous effect on your live account. This broker simulator has no idea what is actually going on at your real account. Its just doing the job of running the simulation and sending out the computed results. If your TradingView simulation falls out of alignment with the actual trading account lots of really bad things could happen. Like your script thinks your are currently long but the account is actually short. Reversals from this point forward will always be wrong with no one the wiser. Human intervention will be required to restore congruence. But how does anyone find out this is occurring? In closed systems engineering this is known as entropy. In practice your webhook logic should be robust enough to detect these conditions. Be generous with the placeholder usage and give the webhook code plenty of information to compare states. Both issuer and receiver. Don’t blindly commit incoming signals without verifying system integrity.

Setup

The following steps provide a very brief set of instructions that will get you started on your first configuration. After you’ve gone through the process a couple of times, you won’t need these anymore. It’s really a simple script after all. I have several example configurations that I used to create the performance charts shown. I can share them with you if you like. Of course, if you’ve modified the code then these steps are probably obsolete.

There are 47 inputs divided into seven sections. For the most part, the configuration process is designed to flow from top to bottom. Handy, tool tips are available on every field to help get you through the initial setup.

Step 1. Input the Base Currency and Order Size in the Properties tab. Set the Pyramiding value to zero.

Step 2. Select the Trading Mode you intend to test with from the drop down in Section 1. I usually select No Trade until I’ve setup all of the trend lines, profit and stop levels.

Step 3. Put in your Minimum Profit and Stop Loss in the first section. This is in pips or currency basis points (chart right side scale). Remember that the profit is taken as a conditional exit not a fixed limit. The actual profit taken will almost always be greater than the amount specified. The stop loss, on the other hand, is indeed a hard number which is executed by the TradingView broker simulator when the threshold is breached.

Step 4. Apply the appropriate value to the Tick Scalar field in Section 1. This value is used to remove the pipette from the price. You can enable the Summary Report in Section 7 to see the TradingView minimum tick size of the current chart.

Step 5. Apply the appropriate Price Normalizer value in Section 1. This value is used to normalize the instrument price for differential calculations. Basically, we want to increase the magnitude to significant digits to make the numbers more meaningful in comparisons. Though I have used many normalization techniques, I have always found this method to provide a simple and lightweight solution for less demanding applications. Most of the time the default value will be sufficient. The Tick Scalar and Price Normalizer value work together within a single calculation so changing either will affect all delta result values.

Step 6. Turn on the trend line plots in Section 7. Then configure Section 2. Try to get the plots to show you what’s really happening not what you want to happen. The most important is the purple trend line. Select an interval and length that seem to identify where prices tend to go during non-consolidation periods. Remember that a natural exit is when the blue crosses the green line.

Step 7. Enable Show Event Regions in Section 7. Then adjust Section 6. Blue background fills are spikes and red fills are plunging prices. These measurements should be hard to come by so you should see relatively few fills on the chart if you’ve set this up as intended. Section 6 includes the Zscore oscillator the state of which combines with the signal lines to detect statistically significant price movement. The Zscore is a zero based calculation with positive and negative magnitude readings. You want to input a reasonably large number slightly below the maximum amplitude seen on the chart. Both rise and fall inputs are entered as a positive real number. You can easily use my code to create a separate indicator if you want to see it in action. The default value is sufficient for most configurations.

Step 8. Turn off Show Event Regions and enable Show Entry Regions in Section 7. Then adjust Section 3. This section contains two parts. The entry setup crossovers and EMA events. Adjust the crossovers first. That is the Fast Cross Length and Slow Cross Length. The frequency of your trades will be shown as blue and red fills. There should be a lot. Then turn off Show Event Regions and enable Display EMA Peaks. Adjust all the fields that have the word EMA. This is actually the yellow line on the chart. The blue and red fills should show much less than the crossovers but more than event fills shown in Step 7.

Step 9. Change the Trading Mode to BiDir if you selected No Trades previously. Look on the chart and see where the trades are occurring. Make adjustments to the Minimum Profit and Stop Offset in Section 1 if necessary. Wider profits and stops reduce the trade frequency.

Step 10. Go to Section 4 and 5 and make fine tuning adjustments to the long and short side.

Example Settings

To reproduce the performance shown on the chart please use the following configuration: (Bitcoin on the Kraken exchange)

1. Select XBTUSD Kraken as the chart symbol.

2. On the properties tab set the Order Size to: 0.01 Bitcoin

3. On the properties tab set the Pyramiding to: 12

4. In Section 1: Select “Crypto” for the Trading Model

5. In Section 1: Input 2000 for the Minimum Profit

6. In Section 1: Input 0 for the Stop Offset (No Stop)

7. In Section 1: Input 10 for the Tick Scalar

8. In Section 1: Input 1000 for the Price Normalizer

9. In Section 1: Input 2000 for the Pyramid Minimum Span

10. In Section 1: Check mark the Position Bale Out

11. In Section 2: Input 60 for the Signal Line Period

12. In Section 2: Input 1440 for the Trend Line Period

13. In Section 2: Input 5 for the Fast Alma Length

14. In Section 2: Input 22 for the Fast LinReg Length

15. In Section 2: Input 100 for the Slow LinReg Length

16. In Section 2: Input 90 for the Trend Line Length

17. In Section 2: Input 14 Stochastic Length

18. In Section 3: Input 9 Fast Cross Length

19. In Section 3: Input 24 Slow Cross Length

20. In Section 3: Input 8 Fast EMA Length

21. In Section 3: Input 10 Fast EMA Rise NetChg

22. In Section 3: Input 1 Fast EMA Rise ROC

23. In Section 3: Input 10 Fast EMA Fall NetChg

24. In Section 3: Input 1 Fast EMA Fall ROC

25. In Section 4: Check mark the Long Natural Exit

26. In Section 4: Check mark the Long Signal Exit

27. In Section 4: Check mark the Long Price Event Exit

28. In Section 4: Check mark the Long Stochastic Exit

29. In Section 5: Check mark the Short Natural Exit

30. In Section 5: Check mark the Short Signal Exit

31. In Section 5: Check mark the Short Price Event Exit

32. In Section 5: Check mark the Short Stochastic Exit

33. In Section 6: Input 120 Rise Event NetChg

34. In Section 6: Input 1 Rise Event ROC

35. In Section 6: Input 5 Min Above Zero ZScore

36. In Section 6: Input 120 Fall Event NetChg

37. In Section 6: Input 1 Fall Event ROC

38. In Section 6: Input 5 Min Below Zero ZScore

In this configuration we are trading in long only mode and have enabled downward pyramiding. The purple trend line is based on the day (1440) period. The length is set at 90 days so it’s going to take a while for the trend line to alter course should this symbol decide to node dive for a prolonged amount of time. Your trades will still go long under those circumstances. Since downward accumulation is enabled, your position size will grow on the way down.

The performance example is Bitcoin so we assume the trader is buying coins outright. That being the case we don’t need a stop since we will never receive a margin call. New buy signals will be generated when the price exceeds the magnitude and speed defined by the Event Net Change and Rate of Change.

Feel free to PM me with any questions related to this script. Thank you and happy trading!

CFTC RULE 4.41

These results are based on simulated or hypothetical performance results that have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Also, because these trades have not actually been executed, these results may have under-or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated or hypothetical trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to these being shown.

BEST Trailing Stop StrategyHello traders

Here we go again.... with the second strategy snippet.

Reminder: the first snipper was a Trailing Profit strategy script

What's on the menu?

A trailing stop is designed to protect gains by enabling a trade to remain open and continue to profit as long as the price is moving in the investor's favor.

The order closes the trade if the price changes direction by a specified percentage or dollar amount.

Trigger me I'm famous

I developed many trading strategies in my career and often I've been asked to trigger a trailing-stop once a certain % move has been made.

On the screenshot below, the SL trigger is plotted in maroon.

Once the price goes past that level for the first time, I'll start trailing the trailing stop level.

In other words, when we see a price makes an interesting move in percentage value - we decide to trail the stop for at least not losing any more

All the BEST

Dave

Parabolic SARThis is a redesign of the built-in Parabolic SAR indicator. I added a proper input system, an option to highlight initial points for both lines and an option to choose points width. So, customize it as you want.

Parabolic SAR was originally developed by J. Welles Wilder and described in his book "New Concepts in Technical Trading Systems" (1978). It is a trend-following indicator that can be used as a trailing stop loss.

To know which settings for PSAR are the most profitable on your instrument and timeframe you can use this tool

Profitable Parabolic SAR

Buy The Dip - Does It Work?Buying the dip has become a meme in crypto, but does it actually work?

Using this script you can find out.

The dip is defined here as the average true range multiplied by a number of your choosing (dipness input) and subtracted from the low.

When price crosses under the dip level, a long is initiated. The long is then closed using a timestop (default value 20 bars), no fancy exits here.

A general rule for buying the dip should be to be more passive in a bull market and aggressive in a bear market.

Same goes for all counter trend trading.

Heres a few other examples of dip buying statistics using the H4 timeframe:

50% profitable, 1.692 Profit Factor

BINANCE:PIVXBTC

56.52% profitable, 1.254 Profit Factor

BINANCE:KMDBTC

27.27% Profitable, 0.257 Profit Factor... yikes!

BINANCE:BTSBTC

73.33% Profitable, 13.627 Profit Factor... o.O

BINANCE:MANABTC

Engulfing pullbackThis Indicator searching for pullback on input Moving Average with Engulfing candle

Rules for indicator :-

Buy Signal -

1) search for pullback on ma if price above ma and come back and touches ma

2)after pullback on ma searching for bullish engulfing pattern on next candle

3)if pullback on previous candle and bullish engulfing for buy signal form

Sell Signal -

1) search for pullback on ma if price below ma and come back touches ma

2)after pullback on ma searching for bearish engulfing pattern on next candle

3)if pullback on previous candle and bearish engulfing for buy signal form

Disclaimer -Traders can use this script as a starting point for further customization or as a reference for developing their own trading strategies. It's important to note that past performance is not indicative of future results, and thorough testing and validation are recommended before deploying any trading strategy.

Lorentzian Classification Strategy Based in the model of Machine learning: Lorentzian Classification by @jdehorty, you will be able to get into trending moves and get interesting entries in the market with this strategy. I also put some new features for better backtesting results!

Backtesting context: 2022-07-19 to 2023-04-14 of US500 1H by PEPPERSTONE. Commissions: 0.03% for each entry, 0.03% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 3 indicators are used:

Machine learning: Lorentzian Classification by @jdehorty

One Ema of 200 periods for identifying the trend

Supertrend indicator as a filter for some exits

Atr stop loss from Gatherio

Trade conditions:

For longs:

Close price is above 200 Ema

Lorentzian Classification indicates a buying signal

This gives us our long signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 1:1 and take profit of 3:1 where half position will be closed. This will be showed as buy.

The other half will be closed when the model indicates a selling signal or Supertrend indicator gives a bearish signal. This will be showed as cl buy.

For shorts:

Close price is under 200 Ema

Lorentzian Classification indicates a selling signal

This gives us our short signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 1:1 and take profit of 3:1 where half position will be closed. This will be showed as sell.

The other half will be closed when the model indicates a buying signal or Supertrend indicator gives a bullish signal. This will be showed as cl sell.

Risk management

To calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss or last swing for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss or last swing is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

> In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

> You can also choose a fixed amount, so you will have to activate fixed amount in risk management for trades and set the fixed amount for backtesting.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, a table of some stats from backtesting, etc.

You will find the settings for risk management at the end of the script if you want to change something or trying new values for other assets for backtesting.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital

I also added a function for backtesting if you had added or withdrawn money frequently:

Adding money: You can choose how often you want to add money (Monthly, yearly, daily or weekly). Then a fixed amount of money and activate or deactivate this function

Withdraw money: You can choose if you want to withdraw a fixed amount or a percentage of earnings. Then you can choose a fixed amount of money, the period of time and activate or deactivate this function. Also, the percentage of earnings if you choosed this option.

Some other assets where strategy has worked

BTCUSD 4H, 1D

ETHUSD 4H, 1D

BNBUSD 4H

SPX 1D

BANKNIFTY 4H, 15 min

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!. If you have problems loading the script reduce max bars back number in general settings

Strategies for trending markets use to have more looses than wins and it takes a long time to get profits, so do not forget to be patient and consistent !

Please, visit the post from @jdehorty called Machine Learning: Lorentzian Classification for a better understanding of his script!

Any support and boosts will be well received. If you have any question, do not doubt to ask!

Investments/swing trading strategy for different assetsStop worrying about catching the lowest price, it's almost impossible!: with this trend-following strategy and protection from bearish phases, you will know how to enter the market properly to obtain benefits in the long term.

Backtesting context: 1899-11-01 to 2023-02-16 of SPX by Tvc. Commissions: 0.05% for each entry, 0.05% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 5 indicators are used:

One Ema of 200 periods

Atr Stop loss indicator from Gatherio

Squeeze momentum indicator from LazyBear

Moving average convergence/divergence or Macd

Relative strength index or Rsi

Trade conditions:

There are three type of entries, one of them depends if we want to trade against a bearish trend or not.

---If we keep Against trend option deactivated, the rules for two type of entries are:---

First type of entry:

With the next rules, we will be able to entry in a pull back situation:

Squeeze momentum is under 0 line (red)

Close is above 200 Ema and close is higher than the past close

Histogram from macd is under 0 line and is higher than the past one

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

For closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Second type of entry:

With the next rules, we will not lose a possible bullish movement:

Close is above 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entry, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

---If we keep Against trend option activated, the rules are the same as the ones above, but with one more type of entry. This is more useful in weekly timeframes, but could also be used in daily time frame:---

Third type of entry:

Close is under 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entries, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Risk management

For calculating the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

If you activate break even using rsi, when rsi crosses under overbought zone break even will be activated. This can work in some assets.

---Important: In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Some assets and timeframes where the strategy has also worked:

BTCUSD : 4H, 1D, W

SPX (US500) : 4H, 1D, W

GOLD : 1D, W

SILVER : 1D, W

ETHUSD : 4H, 1D

DXY : 1D

AAPL : 4H, 1D, W

AMZN : 4H, 1D, W

META : 4H, 1D, W

(and others stocks)

BANKNIFTY : 4H, 1D, W

DAX : 1D, W

RUT : 1D, W

HSI : 1D, W

NI225 : 1D, W

USDCOP : 1D, W

Buy/Sell on the levelsThis script is generally

My describe is:

There are a lot of levels we would like to buy some crypto.

When the price has crossed the level-line - we buy, but only if we have the permission in array(2)

When we have bought the crypto - we lose the permission for buy for now(till we will sell it on the next higher level)

When we sell some crypto(on the buying level + 1) we have the permission again.

There also are 2 protect indicators. We can buy if these indicators both green only(super trend and PIVOT )

Jun 12

Release Notes: Hello there,

Uncomment this section before use for real trade:

if array.get(price_to_sellBue, i) >= open and array.get(price_to_sellBue, i) <= close// and

//direction < 0 and permission_for_buy != 0

Here is my script.

In general - this is incredible simple script to use and understand.

First of all You can see this script working with only long orders, it means we going to get money if crypto grows only. Short orders we need to close the position on time.

In this script we buy crypto and sell with step 1% upper.

You can simply change the step by changing the price arrays.

Please note, if You want to see where the levels of this script is You Have to copy the next my indicator called LEVEL 1%

In general - if the price has across the price-level we buy some crypto and loose permission for buying for this level till we sell some crypto. There is ''count_of_orders" array field with value 2. When we bought some crypto the value turns to 0. 0 means not allowed to by on this level!!! The script buy if the bar is green only(last tick).

The script check every level(those we can see in "price_to_sellBue" array).

If the price across one of them - full script runs. After buying(if it possible) we check is there any crypto for sell on the level.

We check all levels below actual level( of actual level - ''i'' than we check all levels from 0 to i-1).

If there is any order that has value 0 in count of orders and index <= i-1 - we count it to var SELL amount and in the end of loop sell all of it.

Pay attention - it sells only if price across the level with red bar AND HAS ORDERS TO SELL WHICH WAS BOUGHT BELOW!!!

In Strategy tester it shows not-profitables orders sometimes, because if You have old Long position - it sells it first. First in - first out.

If the price goes down for a long time and You sell after 5 buys You sell the first of it with the highest value.

There is 2 protection from horrible buying in this strategy. The first one - Supertrend. If the supertrend is red - there is no permission for buy.

The second one - something between PIVOT and supertrend but with switcher.

If the price across last minimum - switcher is red - no permission for buy and the actual price becomes last minimum . The last maximum calculated for last 100 bars.

When the price across last maximum - switcher is green, we can buy. The last minimum calculation for last 100 bars, last maximum is actual price.

This two protections will save You from buying if price get crash down.

Enjoy my script.

Should You need the code or explanation, You have any ideas how to improve this crypt, contact me.

Vladyslav.

Jun 12

Release Notes: Here has been uncommented the protection for buy in case of price get down.

5 hours ago

Release Notes: Changed rages up to actual price to make it work

Amazing Crossover System - 100+ pips per day!I got the main concept for this system on another site. While I have made one important change, I must stress that the heart of this system was created by someone else! We must give credit where credit is due!

Y'all know baby pips. @ForexPhantom published about this system and did both back and forward test around 10 years ago.

I found it on the sit and now I put it to code to see how it performs. I assume 10 points spread for every trade. I use Renesource or AxiTrader to get the low spreads.

There are 2 mods, the single trades and constant trading on the direction.

Main concept

Indicators

5 EMA -- YELLOW

10 EMA -- RED

RSI (10 - Apply to Median Price: HL/2) -- One level at 50.

TIME FRAME

1 Hour Only (very important!)

PAIRS

Virtually any pair seems to work as this is strictly technical analysis.

I recommend sticking to the main currencies and avoiding cross currencies (just his preference).

WHEN TO ENTER A TRADE

Enter LONG when the Yellow EMA crosses the Red EMA from underneath.

RSI must be approaching 50 from the BOTTOM and cross 50 to warrant entry.

Enter SHORT when the Yellow EMA crosses the Red EMA from the top.

RSI must be approaching 50 from the TOP and cross 50 to warrant entry.

I've attached a picture which demonstrates all these conditions.

That's it!

f.bpcdn.co

FADE GIGA CANDLE STRAT# 🔥 FADE GIGA CANDLE STRATEGY

## Overview

The **Fade Giga Candle Strategy** is a contrarian trading indicator designed to identify extreme price movements (called "Giga Candles") and predict mean reversion opportunities. This strategy is specifically optimized for Polymarket's 15-minute crypto prediction markets (BTC, ETH, SOL, XRP) but can be applied to any timeframe.

**Core Concept:** When price makes an unusually large move with extreme RSI and high volume, it often reverses in the next period. This indicator detects those moments and signals to "fade" (bet against) the move.

---

## 📊 What Does It Do?

### Signal Generation

- **FADE BEARISH (📉)**: Detects massive green candles → Predicts price will go DOWN next

- **FADE BULLISH (📈)**: Detects massive red candles → Predicts price will go UP next

### Real-Time Stats

- Win Rate tracking

- Total Return calculation

- Expected Value (EV) analysis

- Breakeven threshold display (57.14% for 75% win / 100% loss structure)

### Visual Alerts

- Chart labels showing predictions

- Background highlighting on signal candles

- Stats table in top-right corner

- RSI indicator with overbought/oversold zones

---

## ⚙️ How It Works

### 1. Giga Candle Detection

The indicator analyzes the last 500 candles and identifies "Giga Candles" based on:

- **Body Size Percentile** (default 93rd): Only the top 7% largest candles qualify

- **Minimum Body %** (default 0.5%): Filters out noise on small moves

### 2. Confirmation Filters

Before generating a signal, the indicator checks:

**RSI Filter (Optional)**

- RSI must be ≥70 (overbought) OR ≤30 (oversold)

- Indicates price is at an extreme level

**Volume Filter (Optional)**

- Current volume must be ≥1.5x the 20-period average

- Confirms the move has conviction

### 3. Fade Logic

```

IF Giga Green Candle + RSI Extreme + High Volume

→ FADE BEARISH (predict DOWN)

IF Giga Red Candle + RSI Extreme + High Volume

→ FADE BULLISH (predict UP)

```

---

## 🎛️ Settings & Parameters

### Giga Candle Detection

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| **Giga Candle Percentile** | 93.0 | 80-99 | Top X% of candles by body size. 93 = only top 7% qualify as "giga" |

| **Min Body % (Safety)** | 0.5 | 0.1-2.0 | Minimum body size as % of price. Prevents false signals on low volatility |

### RSI Filter

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| **Use RSI Filter** | ON | ON/OFF | Require RSI to be extreme before signaling |

| **RSI Length** | 14 | 5-50 | Period for RSI calculation |

| **RSI Overbought** | 70 | 60-85 | Threshold for overbought condition |

| **RSI Oversold** | 30 | 15-40 | Threshold for oversold condition |

### Volume Filter

| Parameter | Default | Range | Description |

|-----------|---------|-------|-------------|

| **Use Volume Filter** | ON | ON/OFF | Require high volume before signaling |

| **Volume SMA Length** | 20 | 10-50 | Period for average volume calculation |

| **Volume Multiplier** | 1.5 | 1.0-3.0 | Current volume must be X times the average |

### Display Options

- **Show Signal Labels**: Display prediction labels on chart

- **Highlight Signal Candles**: Background color on signal bars

- **Show Stats Table**: Performance statistics in top-right

- **Enable Alerts**: Push notifications when signals occur

---

## 🚀 How to Use

### For Polymarket Trading (Recommended)

1. **Set timeframe to 15 minutes** (matches Polymarket market duration)

2. **Apply to BTC, ETH, SOL, or XRP charts**

3. **Wait for signal:**

- 📉 FADE BEARISH → Buy "DOWN" on Polymarket

- 📈 FADE BULLISH → Buy "UP" on Polymarket

4. **Hold until market resolves** (15 minutes)

5. **Track your performance** using the stats table

### For Regular Trading

1. Use on any liquid crypto market

2. When signal appears, consider entering a mean-reversion trade

3. Set stop-loss at 100% of entry (built into expected value calculation)

4. Take profit at 75% gain (matches the 57.14% breakeven math)

### Understanding the Stats Table

**Win Rate**: Your prediction accuracy percentage

- **Target: >57.14%** (breakeven for 75% win / 100% loss structure)

- Green if profitable, red if unprofitable

**Expected Value (EV)**: Average % return per trade

- **Positive EV** = Strategy is profitable long-term

- **Negative EV** = Strategy is losing long-term

- Formula: `(WinRate% × 75) - (LossRate% × 100)`

**Total Return**: Cumulative % gain/loss across all signals

---

## 📈 Interpretation Guide

### Strong Signals

✅ Large giga candle (top 3-5%)

✅ RSI >75 or <25 (very extreme)

✅ Volume >2x average

✅ Signal appears after sustained trend

✅ Win rate >60% in recent trades

### Weak Signals (Consider Skipping)

⚠️ Borderline giga candle (barely above threshold)

⚠️ RSI only slightly extreme (71 or 29)

⚠️ Volume just meets minimum (1.5x)

⚠️ Signal appears during choppy/sideways market

⚠️ Win rate <50% in recent trades

---

## 💡 Pro Tips

### 1. Timeframe Matters

- **15-min**: Best for Polymarket, captures intraday exhaustion

- **1-hour**: Better for swing trading

- **5-min**: Too noisy, not recommended

### 2. Market Context

- Works best in **trending markets** that overextend

- Less effective in **tight ranges** (consolidation)

- Avoid during **low liquidity** hours (weekends, holidays)

### 3. Filter Tuning

**More Aggressive (More Signals)**

- Lower Giga Percentile (90th)

- Disable RSI filter

- Lower volume multiplier (1.2x)

**More Conservative (Fewer, Higher Quality)**

- Raise Giga Percentile (95th)

- Tighter RSI thresholds (75/25)

- Higher volume multiplier (2.0x)

### 4. Bankroll Management

- **Never bet >5% of capital** on a single signal

- Maintain 20+ bet bankroll minimum

- Use Kelly Criterion: `Bet% = (WinRate - LossRate) / 2`

- Example: 60% win rate → Bet ~10% of bankroll

### 5. Track Your Performance

- Monitor the stats table actively

- If win rate drops below 55% for 20+ trades, **stop trading**

- If EV goes negative, **reassess filters or market conditions**

- Keep a trading journal outside the indicator

---

## ⚠️ Risk Disclosure

### Important Warnings

1. **Past performance ≠ future results**: Backtested win rates may not hold in live trading

2. **Market conditions change**: Strategy may stop working if market dynamics shift

3. **Gambler's ruin risk**: Even profitable strategies can lose multiple trades in a row

4. **Polymarket specific**:

- Carries smart contract risk

- Subject to liquidity constraints

- Markets can resolve unexpectedly

5. **Not financial advice**: This is an educational tool, not a recommendation to trade

### Best Practices

- Start with **small position sizes** to test

- Track at least **50 signals** before evaluating performance

- Consider **paper trading** first (simulated trades)

- Never trade with money you can't afford to lose

- Understand the **57.14% breakeven** requirement

---

## 🔧 Troubleshooting

### "No signals appearing"

- Check if filters are too strict (try disabling RSI/Volume filters temporarily)

- Reduce Giga Percentile to 90th

- Ensure sufficient chart history loaded (>500 candles)

### "Too many signals"

- Increase Giga Percentile to 95th

- Enable both RSI and Volume filters

- Raise volume multiplier to 2.0x

### "Win rate seems low"

- Check if you're trading during low liquidity periods

- Verify you're using 15-min timeframe for Polymarket

- Consider market is in tight consolidation (strategy works best in trends)

---

## 📚 Technical Details

### Calculations

- **Body Size**: `|close - open|`

- **Body %**: `(bodySize / open) × 100`

- **Giga Threshold**: `percentile_nearest_rank(last 500 candles, 93rd)`

- **RSI**: Standard 14-period RSI

- **Volume Ratio**: `current_volume / SMA(volume, 20)`

### Performance Tracking

- Checks if previous signal was correct after 1 bar

- Win = +75% to total return

- Loss = -100% to total return

- Win Rate = `(correct_predictions / total_signals) × 100`

---

## 🎯 Ideal Use Cases

### ✅ Perfect For:

- Polymarket 15-minute crypto prediction markets

- Mean-reversion trading on liquid crypto pairs

- Contrarian traders who fade extremes

- Systematic traders who follow rules-based signals

### ❌ Not Ideal For:

- Trend-following strategies (this is contrarian)

- Low volatility assets (needs large moves)

- Illiquid markets (won't have "giga" candles)

- Sub-5-minute scalping (too much noise)

---

## 📞 Support & Updates

**Version**: 6.0

**Last Updated**: January 2025

**Compatible With**: TradingView Pine Script v6

### Feedback Welcome

If you find this indicator useful or have suggestions for improvement, please:

- ⭐ Leave a rating

- 💬 Comment with your results

- 🚀 Share your settings for different markets

**Good luck, and trade responsibly!** 🎯

---

## Quick Start Checklist

- Set timeframe to 15 minutes

- Load BTC, ETH, SOL, or XRP chart

- Verify stats table shows in top-right

- Enable alerts for signal notifications

- Start with paper trading to validate

- Track at least 20 signals before going live

- Never bet more than 5% of bankroll per trade

- Monitor win rate and stop if <55%

**Remember: The goal is >57.14% win rate for profitability!**

ORB Fusion🎯 CORE INNOVATION: INSTITUTIONAL ORB FRAMEWORK WITH FAILED BREAKOUT INTELLIGENCE

ORB Fusion represents a complete institutional-grade Opening Range Breakout system combining classic Market Profile concepts (Initial Balance, day type classification) with modern algorithmic breakout detection, failed breakout reversal logic, and comprehensive statistical tracking. Rather than simply drawing lines at opening range extremes, this system implements the full trading methodology used by professional floor traders and market makers—including the critical concept that failed breakouts are often higher-probability setups than successful breakouts .

The Opening Range Hypothesis:

The first 30-60 minutes of trading establishes the day's value area —the price range where the majority of participants agree on fair value. This range is formed during peak information flow (overnight news digestion, gap reactions, early institutional positioning). Breakouts from this range signal directional conviction; failures to hold breakouts signal trapped participants and create exploitable reversals.

Why Opening Range Matters:

1. Information Aggregation : Opening range reflects overnight news, pre-market sentiment, and early institutional orders. It's the market's initial "consensus" on value.

2. Liquidity Concentration : Stop losses cluster just outside opening range. Breakouts trigger these stops, creating momentum. Failed breakouts trap traders, forcing reversals.

3. Statistical Persistence : Markets exhibit range expansion tendency —when price accepts above/below opening range with volume, it often extends 1.0-2.0x the opening range size before mean reversion.

4. Institutional Behavior : Large players (market makers, institutions) use opening range as reference for the day's trading plan. They fade extremes in rotation days and follow breakouts in trend days.

Historical Context:

Opening Range Breakout methodology originated in commodity futures pits (1970s-80s) where floor traders noticed consistent patterns: the first 30-60 minutes established a "fair value zone," and directional moves occurred when this zone was violated with conviction. J. Peter Steidlmayer formalized this observation in Market Profile theory, introducing the "Initial Balance" concept—the first hour (two 30-minute periods) defining market structure.

📊 OPENING RANGE CONSTRUCTION

Four ORB Timeframe Options:

1. 5-Minute ORB (0930-0935 ET):

Captures immediate market direction during "opening drive"—the explosive first few minutes when overnight orders hit the tape.

Use Case:

• Scalping strategies

• High-frequency breakout trading

• Extremely liquid instruments (ES, NQ, SPY)

Characteristics:

• Very tight range (often 0.2-0.5% of price)

• Early breakouts common (7 of 10 days break within first hour)

• Higher false breakout rate (50-60%)

• Requires sub-minute chart monitoring

Psychology: Captures panic buyers/sellers reacting to overnight news. Range is small because sample size is minimal—only 5 minutes of price discovery. Early breakouts often fail because they're driven by retail FOMO rather than institutional conviction.

2. 15-Minute ORB (0930-0945 ET):

Balances responsiveness with statistical validity. Captures opening drive plus initial reaction to that drive.

Use Case:

• Day trading strategies

• Balanced scalping/swing hybrid

• Most liquid instruments

Characteristics:

• Moderate range (0.4-0.8% of price typically)

• Breakout rate ~60% of days

• False breakout rate ~40-45%

• Good balance of opportunity and reliability

Psychology: Includes opening panic AND the first retest/consolidation. Sophisticated traders (institutions, algos) start expressing directional bias. This is the "Goldilocks" timeframe—not too reactive, not too slow.

3. 30-Minute ORB (0930-1000 ET):

Classic ORB timeframe. Default for most professional implementations.

Use Case:

• Standard intraday trading

• Position sizing for full-day trades

• All liquid instruments (equities, indices, futures)

Characteristics:

• Substantial range (0.6-1.2% of price)

• Breakout rate ~55% of days

• False breakout rate ~35-40%

• Statistical sweet spot for extensions

Psychology: Full opening auction + first institutional repositioning complete. By 10:00 AM ET, headlines are digested, early stops are hit, and "real" directional players reveal themselves. This is when institutional programs typically finish their opening positioning.

Statistical Advantage: 30-minute ORB shows highest correlation with daily range. When price breaks and holds outside 30m ORB, probability of reaching 1.0x extension (doubling the opening range) exceeds 60% historically.

4. 60-Minute ORB (0930-1030 ET) - Initial Balance:

Steidlmayer's "Initial Balance"—the foundation of Market Profile theory.

Use Case:

• Swing trading entries

• Day type classification

• Low-frequency institutional setups

Characteristics:

• Wide range (0.8-1.5% of price)

• Breakout rate ~45% of days

• False breakout rate ~25-30% (lowest)

• Best for trend day identification

Psychology: Full first hour captures A-period (0930-1000) and B-period (1000-1030). By 10:30 AM ET, all early positioning is complete. Market has "voted" on value. Subsequent price action confirms (trend day) or rejects (rotation day) this value assessment.

Initial Balance Theory:

IB represents the market's accepted value area . When price extends significantly beyond IB (>1.5x IB range), it signals a Trend Day —strong directional conviction. When price remains within 1.0x IB, it signals a Rotation Day —mean reversion environment. This classification completely changes trading strategy.

🔬 LTF PRECISION TECHNOLOGY

The Chart Timeframe Problem:

Traditional ORB indicators calculate range using the chart's current timeframe. This creates critical inaccuracies:

Example:

• You're on a 5-minute chart

• ORB period is 30 minutes (0930-1000 ET)

• Indicator sees only 6 bars (30min ÷ 5min/bar = 6 bars)

• If any 5-minute bar has extreme wick, entire ORB is distorted

The Problem Amplifies:

• On 15-minute chart with 30-minute ORB: Only 2 bars sampled

• On 30-minute chart with 30-minute ORB: Only 1 bar sampled

• Opening spike or single large wick defines entire range (invalid)

Solution: Lower Timeframe (LTF) Precision:

ORB Fusion uses `request.security_lower_tf()` to sample 1-minute bars regardless of chart timeframe:

```

For 30-minute ORB on 15-minute chart:

- Traditional method: Uses 2 bars (15min × 2 = 30min)

- LTF Precision: Requests thirty 1-minute bars, calculates true high/low

```

Why This Matters:

Scenario: ES futures, 15-minute chart, 30-minute ORB

• Traditional ORB: High = 5850.00, Low = 5842.00 (range = 8 points)

• LTF Precision ORB: High = 5848.50, Low = 5843.25 (range = 5.25 points)

Difference: 2.75 points distortion from single 15-minute wick hitting 5850.00 at 9:31 AM then immediately reversing. LTF precision filters this out by seeing it was a fleeting wick, not a sustained high.

Impact on Extensions:

With inflated range (8 points vs 5.25 points):

• 1.5x extension projects +12 points instead of +7.875 points

• Difference: 4.125 points (nearly $200 per ES contract)

• Breakout signals trigger late; extension targets unreachable

Implementation:

```pinescript

getLtfHighLow() =>

float ha = request.security_lower_tf(syminfo.tickerid, "1", high)

float la = request.security_lower_tf(syminfo.tickerid, "1", low)

```

Function returns arrays of 1-minute high/low values, then finds true maximum and minimum across all samples.

When LTF Precision Activates:

Only when chart timeframe exceeds ORB session window:

• 5-minute chart + 30-minute ORB: LTF used (chart TF > session bars needed)

• 1-minute chart + 30-minute ORB: LTF not needed (direct sampling sufficient)

Recommendation: Always enable LTF Precision unless you're on 1-minute charts. The computational overhead is negligible, and accuracy improvement is substantial.

⚖️ INITIAL BALANCE (IB) FRAMEWORK

Steidlmayer's Market Profile Innovation:

J. Peter Steidlmayer developed Market Profile in the 1980s for the Chicago Board of Trade. His key insight: market structure is best understood through time-at-price (value area) rather than just price-over-time (traditional charts).

Initial Balance Definition:

IB is the price range established during the first hour of trading, subdivided into:

• A-Period : First 30 minutes (0930-1000 ET for US equities)

• B-Period : Second 30 minutes (1000-1030 ET)

A-Period vs B-Period Comparison:

The relationship between A and B periods forecasts the day:

B-Period Expansion (Bullish):

• B-period high > A-period high

• B-period low ≥ A-period low

• Interpretation: Buyers stepping in after opening assessed

• Implication: Bullish continuation likely

• Strategy: Buy pullbacks to A-period high (now support)

B-Period Expansion (Bearish):

• B-period low < A-period low

• B-period high ≤ A-period high

• Interpretation: Sellers stepping in after opening assessed

• Implication: Bearish continuation likely

• Strategy: Sell rallies to A-period low (now resistance)

B-Period Contraction:

• B-period stays within A-period range

• Interpretation: Market indecisive, digesting A-period information

• Implication: Rotation day likely, stay range-bound

• Strategy: Fade extremes, sell high/buy low within IB

IB Extensions:

Professional traders use IB as a ruler to project price targets:

Extension Levels:

• 0.5x IB : Initial probe outside value (minor target)

• 1.0x IB : Full extension (major target for normal days)

• 1.5x IB : Trend day threshold (classifies as trending)

• 2.0x IB : Strong trend day (rare, ~10-15% of days)

Calculation:

```

IB Range = IB High - IB Low

Bull Extension 1.0x = IB High + (IB Range × 1.0)

Bear Extension 1.0x = IB Low - (IB Range × 1.0)

```

Example:

ES futures:

• IB High: 5850.00

• IB Low: 5842.00

• IB Range: 8.00 points

Extensions:

• 1.0x Bull Target: 5850 + 8 = 5858.00

• 1.5x Bull Target: 5850 + 12 = 5862.00

• 2.0x Bull Target: 5850 + 16 = 5866.00

If price reaches 5862.00 (1.5x), day is classified as Trend Day —strategy shifts from mean reversion to trend following.

📈 DAY TYPE CLASSIFICATION SYSTEM

Four Day Types (Market Profile Framework):

1. TREND DAY:

Definition: Price extends ≥1.5x IB range in one direction and stays there.

Characteristics:

• Opens and never returns to IB

• Persistent directional movement

• Volume increases as day progresses (conviction building)

• News-driven or strong institutional flow

Frequency: ~20-25% of trading days

Trading Strategy:

• DO: Follow the trend, trail stops, let winners run

• DON'T: Fade extremes, take early profits

• Key: Add to position on pullbacks to previous extension level

• Risk: Getting chopped in false trend (see Failed Breakout section)

Example: FOMC decision, payroll report, earnings surprise—anything creating one-sided conviction.

2. NORMAL DAY:

Definition: Price extends 0.5-1.5x IB, tests both sides, returns to IB.

Characteristics:

• Two-sided trading

• Extensions occur but don't persist

• Volume balanced throughout day

• Most common day type

Frequency: ~45-50% of trading days

Trading Strategy:

• DO: Take profits at extension levels, expect reversals

• DON'T: Hold for massive moves

• Key: Treat each extension as a profit-taking opportunity

• Risk: Holding too long when momentum shifts

Example: Typical day with no major catalysts—market balancing supply and demand.

3. ROTATION DAY:

Definition: Price stays within IB all day, rotating between high and low.

Characteristics:

• Never accepts outside IB

• Multiple tests of IB high/low

• Decreasing volume (no conviction)

• Classic range-bound action

Frequency: ~25-30% of trading days

Trading Strategy:

• DO: Fade extremes (sell IB high, buy IB low)

• DON'T: Chase breakouts

• Key: Enter at extremes with tight stops just outside IB

• Risk: Breakout finally occurs after multiple failures

Example: [/b> Pre-holiday trading, summer doldrums, consolidation after big move.

4. DEVELOPING:

Definition: Day type not yet determined (early in session).

Usage: Classification before 12:00 PM ET when IB extension pattern unclear.

ORB Fusion's Classification Algorithm:

```pinescript

if close > ibHigh:

ibExtension = (close - ibHigh) / ibRange

direction = "BULLISH"

else if close < ibLow:

ibExtension = (ibLow - close) / ibRange

direction = "BEARISH"

if ibExtension >= 1.5:

dayType = "TREND DAY"

else if ibExtension >= 0.5:

dayType = "NORMAL DAY"

else if close within IB:

dayType = "ROTATION DAY"

```

Why Classification Matters:

Same setup (bullish ORB breakout) has opposite implications:

• Trend Day : Hold for 2.0x extension, trail stops aggressively

• Normal Day : Take profits at 1.0x extension, watch for reversal

• Rotation Day : Fade the breakout immediately (likely false)

Knowing day type prevents catastrophic errors like fading a trend day or holding through rotation.

🚀 BREAKOUT DETECTION & CONFIRMATION

Three Confirmation Methods:

1. Close Beyond Level (Recommended):

Logic: Candle must close above ORB high (bull) or below ORB low (bear).

Why:

• Filters out wicks (temporary liquidity grabs)

• Ensures sustained acceptance above/below range

• Reduces false breakout rate by ~20-30%

Example:

• ORB High: 5850.00

• Bar high touches 5850.50 (wick above)

• Bar closes at 5848.00 (inside range)

• Result: NO breakout signal

vs.

• Bar high touches 5850.50

• Bar closes at 5851.00 (outside range)

• Result: BREAKOUT signal confirmed

Trade-off: Slightly delayed entry (wait for close) but much higher reliability.

2. Wick Beyond Level:

Logic: [/b> Any touch of ORB high/low triggers breakout.

Why:

• Earliest possible entry

• Captures aggressive momentum moves

Risk:

• High false breakout rate (60-70%)

• Stop runs trigger signals

• Requires very tight stops (difficult to manage)

Use Case: Scalping with 1-2 point profit targets where any penetration = trade.

3. Body Beyond Level:

Logic: [/b> Candle body (close vs open) must be entirely outside range.

Why:

• Strictest confirmation