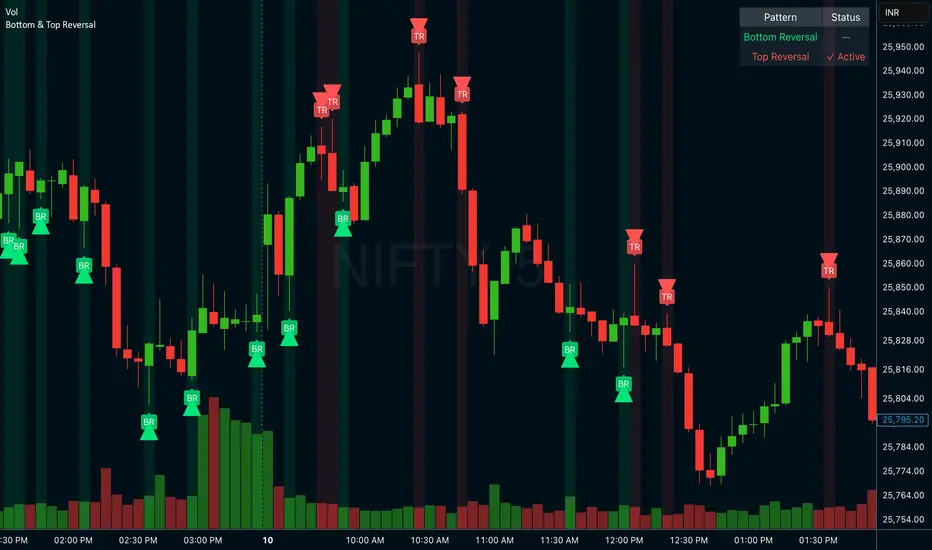

Bottom & Top ReversalBottom & Top Reversal

Bottom Reversal (Bullish):

Opens gap down but recovers strongly

Makes new low but closes above previous close

Lime green arrow + label

Top Reversal (Bearish):

Opens gap up but fails

Makes new high but closes below previous close

Red arrow + label

Extra features:

Status table showing active patterns

Toggle each pattern on/off

Background highlights

Alert system

Penunjuk Pine Script®