VWAP-RSI Scalper FINAL v1Description

This script implements a robust, battle-tested intraday scalping strategy designed for prop firm challenges, funded trader programs, and serious futures scalpers.

It combines VWAP, RSI, EMA trend, and ATR-based risk management to capture high-probability mean reversion and momentum moves during the most liquid hours of the trading day.

Core Logic

RSI (Relative Strength Index):

Trades are triggered when the RSI is either oversold or overbought using a short lookback (default: 3). This ensures only the strongest intraday reversals or exhaustion moves are considered.

VWAP Filter:

Longs are only taken above VWAP, shorts only below VWAP, aligning trades with the session’s dominant bias.

EMA Filter:

Additional trend quality filter—longs require price above EMA, shorts below EMA.

Session Control:

Only trades between user-defined session hours (default: US cash session), eliminating overnight/illiquid action.

ATR-based Dynamic Stops & Targets:

Every trade uses a stop loss at 1x ATR and a take profit at 2x ATR for a positive risk/reward ratio.

Max Trades Per Day:

Prevents overtrading and controls risk exposure (default: 3).

Performance (Sample Backtest)

Profit Factor: 1.37+ (prop-firm quality)

Drawdown: <1% (very conservative risk)

Win Rate: 37–48% (RR > 1, so high edge)

Consistency: Smooth, steady equity curve over hundreds of trades.

Best For:

ES/NQ/CL/GC intraday traders

Prop firm evaluation challenges (Tradeify, Topstep, Apex, etc.)

Anyone needing robust, no-nonsense systematic edge for futures or indices.

How to Use & Tune

Apply to 3min, 5min, or 15min charts of liquid futures or indices.

Change parameters in the settings panel to suit your asset, volatility, or session hours.

Use “Strategy Tester” to validate P&L, win rate, and drawdown.

How to Optimize

Raise/lower RSI length or bands to make signals more/less frequent.

Adjust stop/target multiples for your preferred risk/reward profile.

Change session hours to match your broker or market.

Disclaimer

This is not financial advice. Use on a demo or sim account first. Results will vary by market, slippage, and execution speed. Past performance does not guarantee future results.

If you find this useful, please give it a like, follow for more strategies, and comment your results or questions!

Good luck and safe trading!

Cari dalam skrip untuk "scalping"

Options Strategy V2.0📈 Options Strategy V2.0 – Intraday Reversal-Resilient Momentum System

Overview:

This strategy is designed specifically for intraday SPY, TSLA, MSFT, etc. options trading (0DTE or 1DTE), using high-probability signals derived from a confluence of technical indicators: EMA crossovers, RSI thresholds, ATR-based risk control, and volume spikes. The strategy aims to capture strong directional moves while avoiding overtrading, thanks to a built-in cooldown logic and optional time/session filters.

⚙️ Core Concept

The strategy executes trades only in the direction of the prevailing trend, determined by short- and long-term Exponential Moving Averages (EMA). Entry signals are generated when the Relative Strength Index (RSI) confirms momentum in the direction of the trend, and volume spikes suggest institutional activity.

To increase adaptability and user control, it includes a highly customizable parameter set for both long and short entries independently.

📌 Key Features

✅ Trend-Following Logic

Long entries are only allowed when EMA(short) > EMA(long)

Short entries are only allowed when EMA(short) < EMA(long)

✅ RSI Confirmation

Long: Requires RSI crossover above a configurable threshold

Short: Requires RSI crossunder below a configurable threshold

Optional rejection filters: Entry blocked above/below specific RSI extremes

✅ Volume Spike Filter

Confirms institutional participation by comparing current volume to an average multiplied by a user-defined factor.

✅ ATR-Based Risk Management

Both Stop Loss (SL) and Take Profit (TP) are dynamically calculated using ATR × a multiplier.

TP/SL ratio is fully configurable.

✅ Cooldown Control

After every trade, the system waits for a set number of bars before allowing new entries.

This prevents overtrading and increases signal quality.

Optionally, cooldown is ignored for reversal trades, ensuring the system can react immediately to a confirmed trend change.

✅ Candle Body Filter (Noise Control)

Avoids trades on candles with too small bodies relative to wicks (often noise or indecision candles).

✅ VWAP Confirmation (Optional)

Ensures price is trading above VWAP for long entries, or below for short entries.

✅ Time & Session Filters

Trades only during regular market hours (09:30–16:00 EST).

No-trade zone (e.g., 14:15–15:45 EST) to avoid low-liquidity traps or late-day whipsaws.

✅ End-of-Day Auto Close

All open positions are force-closed at 15:55 EST, protecting against overnight risk (especially relevant for 0DTE options).

📊 Visual Aids

EMA plots show trend direction

VWAP line provides real-time mean-reversion context

Stop Loss and Take Profit lines appear dynamically with each trade

Alerts notify of entry signals and exit triggers

🔧 Customization Panel

Nearly every element of the strategy can be tailored:

EMA lengths (short and long, for both sides)

RSI thresholds and length

ATR length, SL multiplier, and TP/SL ratio

Volume spike sensitivity

Minimum EMA distance filter

Candle body ratio filter

Session restrictions

Cooldown logic (duration + reversal exception)

This makes the strategy extremely versatile, allowing both conservative and aggressive configurations depending on the trader’s profile and the market context.

📌 Example Use Case: SPY Options (0DTE or 1DTE)

This system was designed and tested specifically for SPY and other intraday options trading, where:

Delta is around 0.50 or higher

Trades are short-lived (often 1–5 candles)

You aim to trade 1–3 signals per day, filtering out weak entries

🚫 Important Notes

It is not a scalping strategy; it relies on confirmed breakouts with trend support

No pyramiding or re-entries without cooldown to preserve risk integrity

Should be used with real-time alerts and manual broker execution

📈 Alerts Included

📈 Long Entry Signal

📉 Short Entry Signal

⚠️ Auto-closed all positions at 15:55 EST

✅ Proven Settings – Real Trades + Backtest Results

The current version of the strategy includes the optimal settings I’ve arrived at through extensive backtesting, as well as 3 months of real trading with consistent profitability. These results reflect real-world execution under live market conditions using 0DTE SPY options, with disciplined trade management and risk control.

🧠 Final Thoughts

Options Strategy V2.0 is a robust, highly tunable intraday strategy that blends momentum, trend-following, and volume confirmation. It is ideal for disciplined traders focused on SPY or other 0DTE/1DTE options, and it includes guardrails to reduce false signals and improve execution timing.

Perfect for those who seek precision, flexibility, and risk-defined setups—not blind automation.

Game Theory Trading StrategyGame Theory Trading Strategy: Explanation and Working Logic

This Pine Script (version 5) code implements a trading strategy named "Game Theory Trading Strategy" in TradingView. Unlike the previous indicator, this is a full-fledged strategy with automated entry/exit rules, risk management, and backtesting capabilities. It uses Game Theory principles to analyze market behavior, focusing on herd behavior, institutional flows, liquidity traps, and Nash equilibrium to generate buy (long) and sell (short) signals. Below, I'll explain the strategy's purpose, working logic, key components, and usage tips in detail.

1. General Description

Purpose: The strategy identifies high-probability trading opportunities by combining Game Theory concepts (herd behavior, contrarian signals, Nash equilibrium) with technical analysis (RSI, volume, momentum). It aims to exploit market inefficiencies caused by retail herd behavior, institutional flows, and liquidity traps. The strategy is designed for automated trading with defined risk management (stop-loss/take-profit) and position sizing based on market conditions.

Key Features:

Herd Behavior Detection: Identifies retail panic buying/selling using RSI and volume spikes.

Liquidity Traps: Detects stop-loss hunting zones where price breaks recent highs/lows but reverses.

Institutional Flow Analysis: Tracks high-volume institutional activity via Accumulation/Distribution and volume spikes.

Nash Equilibrium: Uses statistical price bands to assess whether the market is in equilibrium or deviated (overbought/oversold).

Risk Management: Configurable stop-loss (SL) and take-profit (TP) percentages, dynamic position sizing based on Game Theory (minimax principle).

Visualization: Displays Nash bands, signals, background colors, and two tables (Game Theory status and backtest results).

Backtesting: Tracks performance metrics like win rate, profit factor, max drawdown, and Sharpe ratio.

Strategy Settings:

Initial capital: $10,000.

Pyramiding: Up to 3 positions.

Position size: 10% of equity (default_qty_value=10).

Configurable inputs for RSI, volume, liquidity, institutional flow, Nash equilibrium, and risk management.

Warning: This is a strategy, not just an indicator. It executes trades automatically in TradingView's Strategy Tester. Always backtest thoroughly and use proper risk management before live trading.

2. Working Logic (Step by Step)

The strategy processes each bar (candle) to generate signals, manage positions, and update performance metrics. Here's how it works:

a. Input Parameters

The inputs are grouped for clarity:

Herd Behavior (🐑):

RSI Period (14): For overbought/oversold detection.

Volume MA Period (20): To calculate average volume for spike detection.

Herd Threshold (2.0): Volume multiplier for detecting herd activity.

Liquidity Analysis (💧):

Liquidity Lookback (50): Bars to check for recent highs/lows.

Liquidity Sensitivity (1.5): Volume multiplier for trap detection.

Institutional Flow (🏦):

Institutional Volume Multiplier (2.5): For detecting large volume spikes.

Institutional MA Period (21): For Accumulation/Distribution smoothing.

Nash Equilibrium (⚖️):

Nash Period (100): For calculating price mean and standard deviation.

Nash Deviation (0.02): Multiplier for equilibrium bands.

Risk Management (🛡️):

Use Stop-Loss (true): Enables SL at 2% below/above entry price.

Use Take-Profit (true): Enables TP at 5% above/below entry price.

b. Herd Behavior Detection

RSI (14): Checks for extreme conditions:

Overbought: RSI > 70 (potential herd buying).

Oversold: RSI < 30 (potential herd selling).

Volume Spike: Volume > SMA(20) x 2.0 (herd_threshold).

Momentum: Price change over 10 bars (close - close ) compared to its SMA(20).

Herd Signals:

Herd Buying: RSI > 70 + volume spike + positive momentum = Retail buying frenzy (red background).

Herd Selling: RSI < 30 + volume spike + negative momentum = Retail selling panic (green background).

c. Liquidity Trap Detection

Recent Highs/Lows: Calculated over 50 bars (liquidity_lookback).

Psychological Levels: Nearest round numbers (e.g., $100, $110) as potential stop-loss zones.

Trap Conditions:

Up Trap: Price breaks recent high, closes below it, with a volume spike (volume > SMA x 1.5).

Down Trap: Price breaks recent low, closes above it, with a volume spike.

Visualization: Traps are marked with small red/green crosses above/below bars.

d. Institutional Flow Analysis

Volume Check: Volume > SMA(20) x 2.5 (inst_volume_mult) = Institutional activity.

Accumulation/Distribution (AD):

Formula: ((close - low) - (high - close)) / (high - low) * volume, cumulated over time.

Smoothed with SMA(21) (inst_ma_length).

Accumulation: AD > MA + high volume = Institutions buying.

Distribution: AD < MA + high volume = Institutions selling.

Smart Money Index: (close - open) / (high - low) * volume, smoothed with SMA(20). Positive = Smart money buying.

e. Nash Equilibrium

Calculation:

Price mean: SMA(100) (nash_period).

Standard deviation: stdev(100).

Upper Nash: Mean + StdDev x 0.02 (nash_deviation).

Lower Nash: Mean - StdDev x 0.02.

Conditions:

Near Equilibrium: Price between upper and lower Nash bands (stable market).

Above Nash: Price > upper band (overbought, sell potential).

Below Nash: Price < lower band (oversold, buy potential).

Visualization: Orange line (mean), red/green lines (upper/lower bands).

f. Game Theory Signals

The strategy generates three types of signals, combined into long/short triggers:

Contrarian Signals:

Buy: Herd selling + (accumulation or down trap) = Go against retail panic.

Sell: Herd buying + (distribution or up trap).

Momentum Signals:

Buy: Below Nash + positive smart money + no herd buying.

Sell: Above Nash + negative smart money + no herd selling.

Nash Reversion Signals:

Buy: Below Nash + rising close (close > close ) + volume > MA.

Sell: Above Nash + falling close + volume > MA.

Final Signals:

Long Signal: Contrarian buy OR momentum buy OR Nash reversion buy.

Short Signal: Contrarian sell OR momentum sell OR Nash reversion sell.

g. Position Management

Position Sizing (Minimax Principle):

Default: 1.0 (10% of equity).

In Nash equilibrium: Reduced to 0.5 (conservative).

During institutional volume: Increased to 1.5 (aggressive).

Entries:

Long: If long_signal is true and no existing long position (strategy.position_size <= 0).

Short: If short_signal is true and no existing short position (strategy.position_size >= 0).

Exits:

Stop-Loss: If use_sl=true, set at 2% below/above entry price.

Take-Profit: If use_tp=true, set at 5% above/below entry price.

Pyramiding: Up to 3 concurrent positions allowed.

h. Visualization

Nash Bands: Orange (mean), red (upper), green (lower).

Background Colors:

Herd buying: Red (90% transparency).

Herd selling: Green.

Institutional volume: Blue.

Signals:

Contrarian buy/sell: Green/red triangles below/above bars.

Liquidity traps: Red/green crosses above/below bars.

Tables:

Game Theory Table (Top-Right):

Herd Behavior: Buying frenzy, selling panic, or normal.

Institutional Flow: Accumulation, distribution, or neutral.

Nash Equilibrium: In equilibrium, above, or below.

Liquidity Status: Trap detected or safe.

Position Suggestion: Long (green), Short (red), or Wait (gray).

Backtest Table (Bottom-Right):

Total Trades: Number of closed trades.

Win Rate: Percentage of winning trades.

Net Profit/Loss: In USD, colored green/red.

Profit Factor: Gross profit / gross loss.

Max Drawdown: Peak-to-trough equity drop (%).

Win/Loss Trades: Number of winning/losing trades.

Risk/Reward Ratio: Simplified Sharpe ratio (returns / drawdown).

Avg Win/Loss Ratio: Average win per trade / average loss per trade.

Last Update: Current time.

i. Backtesting Metrics

Tracks:

Total trades, winning/losing trades.

Win rate (%).

Net profit ($).

Profit factor (gross profit / gross loss).

Max drawdown (%).

Simplified Sharpe ratio (returns / drawdown).

Average win/loss ratio.

Updates metrics on each closed trade.

Displays a label on the last bar with backtest period, total trades, win rate, and net profit.

j. Alerts

No explicit alertconditions defined, but you can add them for long_signal and short_signal (e.g., alertcondition(long_signal, "GT Long Entry", "Long Signal Detected!")).

Use TradingView's alert system with Strategy Tester outputs.

3. Usage Tips

Timeframe: Best for H1-D1 timeframes. Shorter frames (M1-M15) may produce noisy signals.

Settings:

Risk Management: Adjust sl_percent (e.g., 1% for volatile markets) and tp_percent (e.g., 3% for scalping).

Herd Threshold: Increase to 2.5 for stricter herd detection in choppy markets.

Liquidity Lookback: Reduce to 20 for faster markets (e.g., crypto).

Nash Period: Increase to 200 for longer-term analysis.

Backtesting:

Use TradingView's Strategy Tester to evaluate performance.

Check win rate (>50%), profit factor (>1.5), and max drawdown (<20%) for viability.

Test on different assets/timeframes to ensure robustness.

Live Trading:

Start with a demo account.

Combine with other indicators (e.g., EMAs, support/resistance) for confirmation.

Monitor liquidity traps and institutional flow for context.

Risk Management:

Always use SL/TP to limit losses.

Adjust position_size for risk tolerance (e.g., 5% of equity for conservative trading).

Avoid over-leveraging (pyramiding=3 can amplify risk).

Troubleshooting:

If no trades are executed, check signal conditions (e.g., lower herd_threshold or liquidity_sensitivity).

Ensure sufficient historical data for Nash and liquidity calculations.

If tables overlap, adjust position.top_right/bottom_right coordinates.

4. Key Differences from the Previous Indicator

Indicator vs. Strategy: The previous code was an indicator (VP + Game Theory Integrated Strategy) focused on visualization and alerts. This is a strategy with automated entries/exits and backtesting.

Volume Profile: Absent in this strategy, making it lighter but less focused on high-volume zones.

Wick Analysis: Not included here, unlike the previous indicator's heavy reliance on wick patterns.

Backtesting: This strategy includes detailed performance metrics and a backtest table, absent in the indicator.

Simpler Signals: Focuses on Game Theory signals (contrarian, momentum, Nash reversion) without the "Power/Ultra Power" hierarchy.

Risk Management: Explicit SL/TP and dynamic position sizing, not present in the indicator.

5. Conclusion

The "Game Theory Trading Strategy" is a sophisticated system leveraging herd behavior, institutional flows, liquidity traps, and Nash equilibrium to trade market inefficiencies. It’s designed for traders who understand Game Theory principles and want automated execution with robust risk management. However, it requires thorough backtesting and parameter optimization for specific markets (e.g., forex, crypto, stocks). The backtest table and visual aids make it easy to monitor performance, but always combine with other analysis tools and proper capital management.

If you need help with backtesting, adding alerts, or optimizing parameters, let me know!

BTC 1m Chop Top/Bottom Reversal (Stable Entries)Strategy Description: BTC 5m Chop Top/Bottom Reversal (Stable Entries)

This strategy is engineered to capture precise reversal points during Bitcoin’s choppy or sideways price action on the 5-minute timeframe. It identifies short-term tops and bottoms using a confluence of volatility bands, momentum indicators, and price structure, optimized for high-probability scalping and intraday reversals.

Core Logic:

Volatility Filter: Uses an EMA with ATR bands to define overextended price zones.

Momentum Divergence: Confirms reversals using RSI and MACD histogram shifts.

Price Action Filter: Requires candle confirmation in the direction of the trade.

Locked Signal Logic: Prevents repaints and disappearing trades by confirming signals only once per bar.

Trade Parameters:

Short Entry: Above upper band + overbought RSI + weakening MACD + bearish candle

Long Entry: Below lower band + oversold RSI + strengthening MACD + bullish candle

Take Profit: ±0.75%

Stop Loss: ±0.4%

This setup is tuned for traders using tight risk control and leverage, where execution precision and minimal drawdown tolerance are critical.

TPC Strategy XAUUSD - M5 with Fixed SL/TPThis script implements a trend-following strategy for XAUUSD on the 5-minute chart, using 200 EMA and 21 EMA to filter direction. Entries are triggered based on RSI, MACD crossovers, and price action alignment. It includes fixed Stop Loss (15 pips) and Take Profit (22.5 pips) with visual SL/TP lines, BUY/SELL labels, and alert conditions for automated notifications. Designed for intraday scalping and low-risk entries during trending conditions.

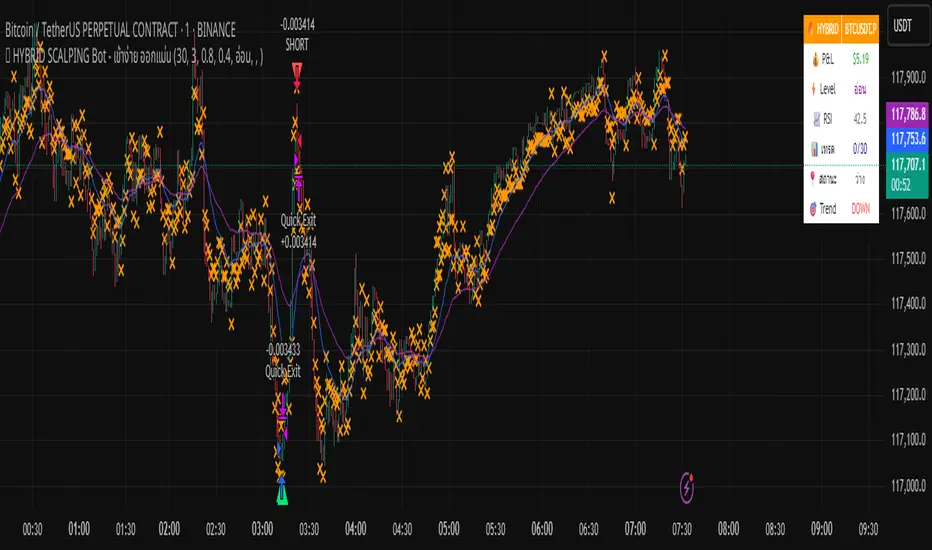

🔥 HYBRID SCALPING Bot - เข้าง่าย ออกแม่นA tool bot that helps analyze charts accurately, focusing on profits.

30M Scalping Strategy with Debug LogsWhat’s changed

Spot‑only: all short logic removed—only long entries and exits are generated.

Logging: uses log.info() to send entry/exit details (timestamp, price, ATR, RSI) to the Pine Logs console.

Clean & concise: core scalp logic (EMAs, RSI, MACD, volume, ATR SL/TP) remains intact.

EMA 20 and Anchored VWAP with Typical PriceIntraday scalping using EMA 20 and VWAP along with targets and Stoploss

Auto Intelligence Selective Moving Average(AI/MA)# 🤖 Auto Intelligence Moving Average Strategy (AI/MA)

**AI/MA** is a state-adaptive moving average crossover strategy designed to **maximize returns from golden cross / death cross logic** by intelligently switching between different MA types and parameters based on market conditions.

---

## 🎯 Objective

To build a moving average crossover strategy that:

- **Adapts dynamically** to market regimes (trend vs range, rising vs falling)

- **Switches intelligently** between SMA, EMA, RMA, and HMA

- **Maximizes cumulative return** under realistic backtesting

---

## 🧪 materials amd methods

- **MA Types Considered**: SMA, EMA, RMA, HMA

- **Parameter Ranges**: Periods from 5 to 40

- **Market Conditions Classification**:

- Based on the slope of a central SMA(20) line

- And the relative position of price to the central line

- Resulting in 4 regimes: A (Bull), B (Pullback), C (Rebound), D (Bear)

- **Optimization Dataset**:

- **Bybit BTCUSDT.P**

- **1-hour candles**

- **2024 full-year**

- **Search Process**:

- **Random search**: 200 parameter combinations

- Evaluated by:

- `Cumulative PnL`

- `Sharpe Ratio`

- `Max Drawdown`

- `R² of linear regression on cumulative PnL`

- **Implementation**:

- Optimization performed in **Python (Pandas + Matplotlib + Optuna-like logic)**

- Final parameters ported to **Pine Script (v5)** for TradingView backtesting

---

## 📈 Performance Highlights (on optimization set)

| Timeframe | Return (%) | Notes |

|-----------|------------|----------------------------|

| 6H | +1731% | Strongest performance |

| 1D | +1691% | Excellent trend capture |

| 12H | +1438% | Balance of trend/range |

| 5min | +27.3% | Even survives scalping |

| 1min | +9.34% | Robust against noise |

- Leverage: 100x

- Position size: 100%

- Fees: 0.055%

- Margin calls: **none** 🎯

---

## 🛠 Technology Stack

- `Python` for data handling and optimization

- `Pine Script v5` for implementation and visualization

- Fully state-aware strategy, modular and extendable

---

## ✨ Final Words

This strategy is **not curve-fitted**, **not over-parameterized**, and has been validated across multiple timeframes. If you're a fan of dynamic, intelligent technical systems, feel free to use and expand it.

💡 The future of simple-yet-smart trading begins here.

Buy Dip Multiple Positions🎯 Objective

This strategy aims to capture aggressive dip-buying opportunities during volume-confirmed price reversals in short term downtrending markets. It is optimized for multi-entry precision, adaptive stop management, and real-time trade monitoring.

It allows traders to execute multiple long entries and dynamically trail stops to maximize gains while capping risk. Designed with modular inputs, this strategy is ideal for intraday momentum scalping and swing trading alike.

🔧 How It Operates

The strategy triggers buy entries when three conditions align:

Reversal Candle: Current close < prior low × 0.998

Volume Confirmation: Current volume exceeds average of prior 2 bars × 1.2

Price Surge Threshold: Current close below user-defined % of close from N bars ago

Once a reversal candle is confirmed, the strategy:

Calculates position size based on user-defined risk parameters

Allows up to a max number of simultaneous trades

Trailing Stop kicks in 2 bars after entry, climbing by a user-defined % each bar

Exit occurs when price hits either the trailing stop or target price

🛠️ Inputs

Users can customize all major aspects of the strategy:

Max Simultaneous Trades: Default 20

Trailing Stop Increase per Bar (%): Default 1%

Initial Stop (% of Reversal Low): Default 85%

Target Price (% Above Reversal Low): Default 60%

Price Surge Threshold (% of Past Close): Default 89%

Surge Lookback Bars: Default 14

Show Active Trade Dot: Toggle to display green trade status dot

📊 Visual Overlays

The chart displays the following:

Marker Description

🟢 Green Dot Active trade (toggleable)

🔴 Red Dot Max trades reached

📈 Trailing Stop Applied internally but not plotted (can be added)

📊 Metrics Plots of win rate, winning/losing trade counts

📎 Notes

Strategy uses strategy.cash allocation logic

Entry size adapts to account equity and risk per trade

All parameters are accessible via the settings panel

Built entirely in Pine Script v5

This strategy balances flexibility and precision, giving traders control over entry timing, capital allocation, and stop behavior. Ideal for those looking to automate dip-buy setups with tactical overlays and visual alerts.

Holy GrailThis is a long-only educational strategy that simulates what happens if you keep adding to a position during pullbacks and only exit when the asset hits a new All-Time High (ATH). It is intended for learning purposes only — not for live trading.

🧠 How it works:

The strategy identifies pullbacks using a simple moving average (MA).

When price dips below the MA, it begins monitoring for the first green candle (close > open).

That green candle signals a potential bottom, so it adds to the position.

If price goes lower, it waits for the next green candle and adds again.

The exit happens after ATH — it sells on each red candle (close < open) once a new ATH is reached.

You can adjust:

MA length (defines what’s considered a pullback)

Initial buy % (how much to pre-fill before signals start)

Buy % per signal (after pullback green candle)

Exit % per red candle after ATH

📊 Intended assets & timeframes:

This strategy is designed for broad market indices and long-term appreciating assets, such as:

SPY, NASDAQ, DAX, FTSE

Use it only on 1D or higher timeframes — it’s not meant for scalping or short-term trading.

⚠️ Important Limitations:

Long-only: The script does not short. It assumes the asset will eventually recover to a new ATH.

Not for all assets: It won't work on assets that may never recover (e.g., single stocks or speculative tokens).

Slow capital deployment: Entries happen gradually and may take a long time to close.

Not optimized for returns: Buy & hold can outperform this strategy.

No slippage, fees, or funding costs included.

This is not a performance strategy. It’s a teaching tool to show that:

High win rate ≠ high profitability

Patience can be deceiving

Many signals = long capital lock-in

🎓 Why it exists:

The purpose of this strategy is to demonstrate market psychology and risk overconfidence. Traders often chase strategies with high win rates without considering holding time, drawdowns, or opportunity cost.

This script helps visualize that phenomenon.

Long/Short/Exit/Risk management Strategy # LongShortExit Strategy Documentation

## Overview

The LongShortExit strategy is a versatile trading system for TradingView that provides complete control over entry, exit, and risk management parameters. It features a sophisticated framework for managing long and short positions with customizable profit targets, stop-loss mechanisms, partial profit-taking, and trailing stops. The strategy can be enhanced with continuous position signals for visual feedback on the current trading state.

## Key Features

### General Settings

- **Trading Direction**: Choose to trade long positions only, short positions only, or both.

- **Max Trades Per Day**: Limit the number of trades per day to prevent overtrading.

- **Bars Between Trades**: Enforce a minimum number of bars between consecutive trades.

### Session Management

- **Session Control**: Restrict trading to specific times of the day.

- **Time Zone**: Specify the time zone for session calculations.

- **Expiration**: Optionally set a date when the strategy should stop executing.

### Contract Settings

- **Contract Type**: Select from common futures contracts (MNQ, MES, NQ, ES) or custom values.

- **Point Value**: Define the dollar value per point movement.

- **Tick Size**: Set the minimum price movement for accurate calculations.

### Visual Signals

- **Continuous Position Signals**: Implement 0 to 1 visual signals to track position states.

- **Signal Plotting**: Customize color and appearance of position signals.

- **Clear Visual Feedback**: Instantly see when entry conditions are triggered.

### Risk Management

#### Stop Loss and Take Profit

- **Risk Type**: Choose between percentage-based, ATR-based, or points-based risk management.

- **Percentage Mode**: Set SL/TP as a percentage of entry price.

- **ATR Mode**: Set SL/TP as a multiple of the Average True Range.

- **Points Mode**: Set SL/TP as a fixed number of points from entry.

#### Advanced Exit Features

- **Break-Even**: Automatically move stop-loss to break-even after reaching specified profit threshold.

- **Trailing Stop**: Implement a trailing stop-loss that follows price movement at a defined distance.

- **Partial Profit Taking**: Take partial profits at predetermined price levels:

- Set first partial exit point and percentage of position to close

- Set second partial exit point and percentage of position to close

- **Time-Based Exit**: Automatically exit a position after a specified number of bars.

#### Win/Loss Streak Management

- **Streak Cutoff**: Automatically pause trading after a series of consecutive wins or losses.

- **Daily Reset**: Option to reset streak counters at the start of each day.

### Entry Conditions

- **Source and Value**: Define the exact price source and value that triggers entries.

- **Equals Condition**: Entry signals occur when the source exactly matches the specified value.

### Performance Analytics

- **Real-Time Stats**: Track important performance metrics like win rate, P&L, and largest wins/losses.

- **Visual Feedback**: On-chart markers for entries, exits, and important events.

### External Integration

- **Webhook Support**: Compatible with TradingView's webhook alerts for automated trading.

- **Cross-Platform**: Connect to external trading systems and notification platforms.

- **Custom Order Execution**: Implement advanced order flows through external services.

## How to Use

### Setup Instructions

1. Add the script to your TradingView chart.

2. Configure the general settings based on your trading preferences.

3. Set session trading hours if you only want to trade specific times.

4. Select your contract specifications or customize for your instrument.

5. Configure risk parameters:

- Choose your preferred risk management approach

- Set appropriate stop-loss and take-profit levels

- Enable advanced features like break-even, trailing stops, or partial profit taking as needed

6. Define entry conditions:

- Select the price source (such as close, open, high, or an indicator)

- Set the specific value that should trigger entries

### Entry Condition Examples

- **Example 1**: To enter when price closes exactly at a whole number:

- Long Source: close

- Long Value: 4200 (for instance, to enter when price closes exactly at 4200)

- **Example 2**: To enter when an indicator reaches a specific value:

- Long Source: ta.rsi(close, 14)

- Long Value: 30 (triggers when RSI equals exactly 30)

### Best Practices

1. **Always backtest thoroughly** before using in live trading.

2. **Start with conservative risk settings**:

- Small position sizes

- Reasonable stop-loss distances

- Limited trades per day

3. **Monitor and adjust**:

- Use the performance table to track results

- Adjust parameters based on how the strategy performs

4. **Consider market volatility**:

- Use ATR-based stops during volatile periods

- Use fixed points during stable markets

## Continuous Position Signals Implementation

The LongShortExit strategy can be enhanced with continuous position signals to provide visual feedback about the current position state. These signals can help you track when the strategy is in a long or short position.

### Adding Continuous Position Signals

Add the following code to implement continuous position signals (0 to 1):

```pine

// Continuous position signals (0 to 1)

var float longSignal = 0.0

var float shortSignal = 0.0

// Update position signals based on your indicator's conditions

longSignal := longCondition ? 1.0 : 0.0

shortSignal := shortCondition ? 1.0 : 0.0

// Plot continuous signals

plot(longSignal, title="Long Signal", color=#00FF00, linewidth=2, transp=0, style=plot.style_line)

plot(shortSignal, title="Short Signal", color=#FF0000, linewidth=2, transp=0, style=plot.style_line)

```

### Benefits of Continuous Position Signals

- Provides clear visual feedback of current position state (long/short)

- Signal values stay consistent (0 or 1) until condition changes

- Can be used for additional calculations or alert conditions

- Makes it easier to track when entry conditions are triggered

### Using with Custom Indicators

You can adapt the continuous position signals to work with any custom indicator by replacing the condition with your indicator's logic:

```pine

// Example with moving average crossover

longSignal := fastMA > slowMA ? 1.0 : 0.0

shortSignal := fastMA < slowMA ? 1.0 : 0.0

```

## Webhook Integration

The LongShortExit strategy is fully compatible with TradingView's webhook alerts, allowing you to connect your strategy to external trading platforms, brokers, or custom applications for automated trading execution.

### Setting Up Webhooks

1. Create an alert on your chart with the LongShortExit strategy

2. Enable the "Webhook URL" option in the alert dialog

3. Enter your webhook endpoint URL (from your broker or custom trading system)

4. Customize the alert message with relevant information using TradingView variables

### Webhook Message Format Example

```json

{

"strategy": "LongShortExit",

"action": "{{strategy.order.action}}",

"price": "{{strategy.order.price}}",

"quantity": "{{strategy.position_size}}",

"time": "{{time}}",

"ticker": "{{ticker}}",

"position_size": "{{strategy.position_size}}",

"position_value": "{{strategy.position_value}}",

"order_id": "{{strategy.order.id}}",

"order_comment": "{{strategy.order.comment}}"

}

```

### TradingView Alert Condition Examples

For effective webhook automation, set up these alert conditions:

#### Entry Alert

```

{{strategy.position_size}} != {{strategy.position_size}}

```

#### Exit Alert

```

{{strategy.position_size}} < {{strategy.position_size}} or {{strategy.position_size}} > {{strategy.position_size}}

```

#### Partial Take Profit Alert

```

strategy.order.comment contains "Partial TP"

```

### Benefits of Webhook Integration

- **Automated Trading**: Execute trades automatically through supported brokers

- **Cross-Platform**: Connect to custom trading bots and applications

- **Real-Time Notifications**: Receive trade signals on external platforms

- **Data Collection**: Log trade data for further analysis

- **Custom Order Management**: Implement advanced order types not available in TradingView

### Compatible External Applications

- Trading bots and algorithmic trading software

- Custom order execution systems

- Discord, Telegram, or Slack notification systems

- Trade journaling applications

- Risk management platforms

### Implementation Recommendations

- Test webhook delivery using a free service like webhook.site before connecting to your actual trading system

- Include authentication tokens or API keys in your webhook URL or payload when required by your external service

- Consider implementing confirmation mechanisms to verify trade execution

- Log all webhook activities for troubleshooting and performance tracking

## Strategy Customization Tips

### For Scalping

- Set smaller profit targets (1-3 points)

- Use tighter stop-losses

- Enable break-even feature after small profit

- Set higher max trades per day

### For Day Trading

- Use moderate profit targets

- Implement partial profit taking

- Enable trailing stops

- Set reasonable session trading hours

### For Swing Trading

- Use longer-term charts

- Set wider stops (ATR-based often works well)

- Use higher profit targets

- Disable daily streak reset

## Common Troubleshooting

### Low Win Rate

- Consider widening stop-losses

- Verify that entry conditions aren't triggering too frequently

- Check if the equals condition is too restrictive; consider small tolerances

### Missing Obvious Trades

- The equals condition is extremely precise. Price must exactly match the specified value.

- Consider using floating-point precision for more reliable triggers

### Frequent Stop-Outs

- Try ATR-based stops instead of fixed points

- Increase the stop-loss distance

- Enable break-even feature to protect profits

## Important Notes

- The exact equals condition is strict and may result in fewer trade signals compared to other conditions.

- For instruments with decimal prices, exact equality might be rare. Consider the precision of your value.

- Break-even and trailing stop calculations are based on points, not percentage.

- Partial take-profit levels are defined in points distance from entry.

- The continuous position signals (0 to 1) provide valuable visual feedback but don't affect the strategy's trading logic directly.

- When implementing continuous signals, ensure they're aligned with the actual entry conditions used by the strategy.

---

*This strategy is for educational and informational purposes only. Always test thoroughly before using with real funds.*

Anomalous Holonomy Field Theory🌌 Anomalous Holonomy Field Theory (AHFT) - Revolutionary Quantum Market Analysis

Where Theoretical Physics Meets Trading Reality

A Groundbreaking Synthesis of Differential Geometry, Quantum Field Theory, and Market Dynamics

🔬 THEORETICAL FOUNDATION - THE MATHEMATICS OF MARKET REALITY

The Anomalous Holonomy Field Theory represents an unprecedented fusion of advanced mathematical physics with practical market analysis. This isn't merely another indicator repackaging old concepts - it's a fundamentally new lens through which to view and understand market structure .

1. HOLONOMY GROUPS (Differential Geometry)

In differential geometry, holonomy measures how vectors change when parallel transported around closed loops in curved space. Applied to markets:

Mathematical Formula:

H = P exp(∮_C A_μ dx^μ)

Where:

P = Path ordering operator

A_μ = Market connection (price-volume gauge field)

C = Closed price path

Market Implementation:

The holonomy calculation measures how price "remembers" its journey through market space. When price returns to a previous level, the holonomy captures what has changed in the market's internal geometry. This reveals:

Hidden curvature in the market manifold

Topological obstructions to arbitrage

Geometric phase accumulated during price cycles

2. ANOMALY DETECTION (Quantum Field Theory)

Drawing from the Adler-Bell-Jackiw anomaly in quantum field theory:

Mathematical Formula:

∂_μ j^μ = (e²/16π²)F_μν F̃^μν

Where:

j^μ = Market current (order flow)

F_μν = Field strength tensor (volatility structure)

F̃^μν = Dual field strength

Market Application:

Anomalies represent symmetry breaking in market structure - moments when normal patterns fail and extraordinary opportunities arise. The system detects:

Spontaneous symmetry breaking (trend reversals)

Vacuum fluctuations (volatility clusters)

Non-perturbative effects (market crashes/melt-ups)

3. GAUGE THEORY (Theoretical Physics)

Markets exhibit gauge invariance - the fundamental physics remains unchanged under certain transformations:

Mathematical Formula:

A'_μ = A_μ + ∂_μΛ

This ensures our signals are gauge-invariant observables , immune to arbitrary market "coordinate changes" like gaps or reference point shifts.

4. TOPOLOGICAL DATA ANALYSIS

Using persistent homology and Morse theory:

Mathematical Formula:

β_k = dim(H_k(X))

Where β_k are the Betti numbers describing topological features that persist across scales.

🎯 REVOLUTIONARY SIGNAL CONFIGURATION

Signal Sensitivity (0.5-12.0, default 2.5)

Controls the responsiveness of holonomy field calculations to market conditions. This parameter directly affects the threshold for detecting quantum phase transitions in price action.

Optimization by Timeframe:

Scalping (1-5min): 1.5-3.0 for rapid signal generation

Day Trading (15min-1H): 2.5-5.0 for balanced sensitivity

Swing Trading (4H-1D): 5.0-8.0 for high-quality signals only

Score Amplifier (10-200, default 50)

Scales the raw holonomy field strength to produce meaningful signal values. Higher values amplify weak signals in low-volatility environments.

Signal Confirmation Toggle

When enabled, enforces additional technical filters (EMA and RSI alignment) to reduce false positives. Essential for conservative strategies.

Minimum Bars Between Signals (1-20, default 5)

Prevents overtrading by enforcing quantum decoherence time between signals. Higher values reduce whipsaws in choppy markets.

👑 ELITE EXECUTION SYSTEM

Execution Modes:

Conservative Mode:

Stricter signal criteria

Higher quality thresholds

Ideal for stable market conditions

Adaptive Mode:

Self-adjusting parameters

Balances signal frequency with quality

Recommended for most traders

Aggressive Mode:

Maximum signal sensitivity

Captures rapid market moves

Best for experienced traders in volatile conditions

Dynamic Position Sizing:

When enabled, the system scales position size based on:

Holonomy field strength

Current volatility regime

Recent performance metrics

Advanced Exit Management:

Implements trailing stops based on ATR and signal strength, with mode-specific multipliers for optimal profit capture.

🧠 ADAPTIVE INTELLIGENCE ENGINE

Self-Learning System:

The strategy analyzes recent trade outcomes and adjusts:

Risk multipliers based on win/loss ratios

Signal weights according to performance

Market regime detection for environmental adaptation

Learning Speed (0.05-0.3):

Controls adaptation rate. Higher values = faster learning but potentially unstable. Lower values = stable but slower adaptation.

Performance Window (20-100 trades):

Number of recent trades analyzed for adaptation. Longer windows provide stability, shorter windows increase responsiveness.

🎨 REVOLUTIONARY VISUAL SYSTEM

1. Holonomy Field Visualization

What it shows: Multi-layer quantum field bands representing market resonance zones

How to interpret:

Blue/Purple bands = Primary holonomy field (strongest resonance)

Band width = Field strength and volatility

Price within bands = Normal quantum state

Price breaking bands = Quantum phase transition

Trading application: Trade reversals at band extremes, breakouts on band violations with strong signals.

2. Quantum Portals

What they show: Entry signals with recursive depth patterns indicating momentum strength

How to interpret:

Upward triangles with portals = Long entry signals

Downward triangles with portals = Short entry signals

Portal depth = Signal strength and expected momentum

Color intensity = Probability of success

Trading application: Enter on portal appearance, with size proportional to portal depth.

3. Field Resonance Bands

What they show: Fibonacci-based harmonic price zones where quantum resonance occurs

How to interpret:

Dotted circles = Minor resonance levels

Solid circles = Major resonance levels

Color coding = Resonance strength

Trading application: Use as dynamic support/resistance, expect reactions at resonance zones.

4. Anomaly Detection Grid

What it shows: Fractal-based support/resistance with anomaly strength calculations

How to interpret:

Triple-layer lines = Major fractal levels with high anomaly probability

Labels show: Period (H8-H55), Price, and Anomaly strength (φ)

⚡ symbol = Extreme anomaly detected

● symbol = Strong anomaly

○ symbol = Normal conditions

Trading application: Expect major moves when price approaches high anomaly levels. Use for precise entry/exit timing.

5. Phase Space Flow

What it shows: Background heatmap revealing market topology and energy

How to interpret:

Dark background = Low market energy, range-bound

Purple glow = Building energy, trend developing

Bright intensity = High energy, strong directional move

Trading application: Trade aggressively in bright phases, reduce activity in dark phases.

📊 PROFESSIONAL DASHBOARD METRICS

Holonomy Field Strength (-100 to +100)

What it measures: The Wilson loop integral around price paths

>70: Strong positive curvature (bullish vortex)

<-70: Strong negative curvature (bearish collapse)

Near 0: Flat connection (range-bound)

Anomaly Level (0-100%)

What it measures: Quantum vacuum expectation deviation

>70%: Major anomaly (phase transition imminent)

30-70%: Moderate anomaly (elevated volatility)

<30%: Normal quantum fluctuations

Quantum State (-1, 0, +1)

What it measures: Market wave function collapse

+1: Bullish eigenstate |↑⟩

0: Superposition (uncertain)

-1: Bearish eigenstate |↓⟩

Signal Quality Ratings

LEGENDARY: All quantum fields aligned, maximum probability

EXCEPTIONAL: Strong holonomy with anomaly confirmation

STRONG: Good field strength, moderate anomaly

MODERATE: Decent signals, some uncertainty

WEAK: Minimal edge, high quantum noise

Performance Metrics

Win Rate: Rolling performance with emoji indicators

Daily P&L: Real-time profit tracking

Adaptive Risk: Current risk multiplier status

Market Regime: Bull/Bear classification

🏆 WHY THIS CHANGES EVERYTHING

Traditional technical analysis operates on 100-year-old principles - moving averages, support/resistance, and pattern recognition. These work because many traders use them, creating self-fulfilling prophecies.

AHFT transcends this limitation by analyzing markets through the lens of fundamental physics:

Markets have geometry - The holonomy calculations reveal this hidden structure

Price has memory - The geometric phase captures path-dependent effects

Anomalies are predictable - Quantum field theory identifies symmetry breaking

Everything is connected - Gauge theory unifies disparate market phenomena

This isn't just a new indicator - it's a new way of thinking about markets . Just as Einstein's relativity revolutionized physics beyond Newton's mechanics, AHFT revolutionizes technical analysis beyond traditional methods.

🔧 OPTIMAL SETTINGS FOR MNQ 10-MINUTE

For the Micro E-mini Nasdaq-100 on 10-minute timeframe:

Signal Sensitivity: 2.5-3.5

Score Amplifier: 50-70

Execution Mode: Adaptive

Min Bars Between: 3-5

Theme: Quantum Nebula or Dark Matter

💭 THE JOURNEY - FROM IMPOSSIBLE THEORY TO TRADING REALITY

Creating AHFT was a mathematical odyssey that pushed the boundaries of what's possible in Pine Script. The journey began with a seemingly impossible question: Could the profound mathematical structures of theoretical physics be translated into practical trading tools?

The Theoretical Challenge:

Months were spent diving deep into differential geometry textbooks, studying the works of Chern, Simons, and Witten. The mathematics of holonomy groups and gauge theory had never been applied to financial markets. Translating abstract mathematical concepts like parallel transport and fiber bundles into discrete price calculations required novel approaches and countless failed attempts.

The Computational Nightmare:

Pine Script wasn't designed for quantum field theory calculations. Implementing the Wilson loop integral, managing complex array structures for anomaly detection, and maintaining computational efficiency while calculating geometric phases pushed the language to its limits. There were moments when the entire project seemed impossible - the script would timeout, produce nonsensical results, or simply refuse to compile.

The Breakthrough Moments:

After countless sleepless nights and thousands of lines of code, breakthrough came through elegant simplifications. The realization that market anomalies follow patterns similar to quantum vacuum fluctuations led to the revolutionary anomaly detection system. The discovery that price paths exhibit holonomic memory unlocked the geometric phase calculations.

The Visual Revolution:

Creating visualizations that could represent 4-dimensional quantum fields on a 2D chart required innovative approaches. The multi-layer holonomy field, recursive quantum portals, and phase space flow representations went through dozens of iterations before achieving the perfect balance of beauty and functionality.

The Balancing Act:

Perhaps the greatest challenge was maintaining mathematical rigor while ensuring practical trading utility. Every formula had to be both theoretically sound and computationally efficient. Every visual had to be both aesthetically pleasing and information-rich.

The result is more than a strategy - it's a synthesis of pure mathematics and market reality that reveals the hidden order within apparent chaos.

📚 INTEGRATED DOCUMENTATION

Once applied to your chart, AHFT includes comprehensive tooltips on every input parameter. The source code contains detailed explanations of the mathematical theory, practical applications, and optimization guidelines. This published description provides the overview - the indicator itself is a complete educational resource.

⚠️ RISK DISCLAIMER

While AHFT employs advanced mathematical models derived from theoretical physics, markets remain inherently unpredictable. No mathematical model, regardless of sophistication, can guarantee future results. This strategy uses realistic commission ($0.62 per contract) and slippage (1 tick) in all calculations. Past performance does not guarantee future results. Always use appropriate risk management and never risk more than you can afford to lose.

🌟 CONCLUSION

The Anomalous Holonomy Field Theory represents a quantum leap in technical analysis - literally. By applying the profound insights of differential geometry, quantum field theory, and gauge theory to market analysis, AHFT reveals structure and opportunities invisible to traditional methods.

From the holonomy calculations that capture market memory to the anomaly detection that identifies phase transitions, from the adaptive intelligence that learns and evolves to the stunning visualizations that make the invisible visible, every component works in mathematical harmony.

This is more than a trading strategy. It's a new lens through which to view market reality.

Trade with the precision of physics. Trade with the power of mathematics. Trade with AHFT.

I hope this serves as a good replacement for Quantum Edge Pro - Adaptive AI until I'm able to fix it.

— Dskyz, Trade with insight. Trade with anticipation.

NY Opening Range Breakout - MA StopCore Concept

This strategy trades breakouts from the New York opening range (9:30-9:45 AM NY time) on intraday timeframes, designed for scalping and day trading.

Setup Requirements

Timeframe: Works on any timeframe under 15 minutes (1m, 2m, 3m, 5m, 10m)

Session: New York market hours

Range Period: 9:30-9:45 AM NY time (15-minute opening range)

Entry Rules

Long Entries:

Wait for a candle to close above the opening range high

Enter long on the next candle (before 12:00 PM NY time)

Must be above moving average if using MA-based take profit

Short Entries:

Wait for a candle to close below the opening range low

Enter short on the next candle (before 12:00 PM NY time)

Must be below moving average if using MA-based take profit

Risk Management

Stop Loss:

Long trades: Opening range low

Short trades: Opening range high

Take Profit Options:

Fixed Risk Reward: 1.5x the range size (customizable ratio)

Moving Average: Exit when price crosses back through MA

Both: Whichever comes first

Key Features

Trade Direction Options:

Long Only

Short Only

Both directions

Moving Average Filter:

Prevents entries that would immediately hit stop loss

Uses EMA/SMA/WMA/VWMA with customizable length

Acts as dynamic support/resistance

Time Restrictions:

No entries after 12:00 PM NY time (customizable cutoff)

One trade per direction per day

Daily reset of all variables

Visual Elements

Red/green lines showing opening range

Purple line for moving average

Entry and breakout signals with shapes

Take profit and stop loss levels plotted

Information table with current status

Strategy Logic Flow

Morning: Capture 9:30-9:45 range high/low

Wait: Monitor for breakout (previous candle close outside range)

Filter: Check MA condition if using MA-based exits

Enter: Trade on next candle after breakout

Manage: Exit at fixed TP, MA cross, or stop loss

Reset: Start fresh next trading day

This is a momentum-based breakout strategy that capitalizes on early market volatility while using the opening range as natural support/resistance levels.

SOXL Trend Surge v3.0.2 – Profit-Only RunnerSOXL Trend Surge v3.0.2 – Profit-Only Runner

This is a trend-following strategy built for leveraged ETFs like SOXL, designed to ride high-momentum waves with minimal interference. Unlike most short-term scalping scripts, this model allows trades to develop over multiple days to even several months, capitalizing on the full power of extended directional moves — all without using a stop-loss.

🔍 How It Works

Entry Logic:

Price is above the 200 EMA (long-term trend confirmation)

Supertrend is bullish (momentum confirmation)

ATR is rising (volatility expansion)

Volume is above its 20-bar average (liquidity filter)

Price is outside a small buffer zone from the 200 EMA (to avoid whipsaws)

Trades are restricted to market hours only (9 AM to 2 PM EST)

Cooldown of 15 bars after each exit to prevent overtrading

Exit Strategy:

Takes partial profit at +2× ATR if held for at least 2 bars

Rides the remaining position with a trailing stop at 1.5× ATR

No hard stop-loss — giving space for volatile pullbacks

⚙️ Strategy Settings

Initial Capital: $500

Risk per Trade: 100% of equity (fully allocated per entry)

Commission: 0.1%

Slippage: 1 tick

Recalculate after order is filled

Fill orders on bar close

Timeframe Optimized For: 45-minute chart

These parameters simulate an aggressive, high-volatility trading model meant for forward-testing compounding potential under realistic trading costs.

✅ What Makes This Unique

No stop-loss = fewer premature exits

Partial profit-taking helps lock in early wins

Trailing logic gives room to ride large multi-week moves

Uses strict filters (volume, ATR, EMA bias) to enter only during high-probability windows

Ideal for leveraged ETF swing or position traders looking to hold longer than the typical intraday or 2–3 day strategies

⚠️ Important Note

This is a high-risk, high-reward strategy meant for educational and testing purposes. Without a stop-loss, trades can experience deep drawdowns that may take weeks or even months to recover. Always test thoroughly and adjust position sizing to suit your risk tolerance. Past results do not guarantee future returns. Backtest range: May 8, 2020 – May 23, 2025

LANZ Strategy 3.0 [Backtest]🔷 LANZ Strategy 3.0 — Asian Range Fibonacci Scalping Strategy

LANZ Strategy 3.0 is a precision-engineered backtesting tool tailored for intraday traders who rely on the Asian session range to determine directional bias. This strategy implements dynamic Fibonacci projections and strict time-window validation to simulate a clean and disciplined trading environment.

🧠 Core Components:

Asian Range Bias Definition: Direction is established between 01:15–02:15 a.m. NY time based on the candle’s close in relation to the midpoint of the Asian session range (18:00–01:15 NY).

Limit Order Execution: Only one trade is placed daily, using a limit order at the Asian range high (for sells) or low (for buys), between 01:15–08:00 a.m. NY.

Fibonacci-Based TP/SL:

Original Mode: TP = 2.25x range, SL = 0.75x range.

Optimized Mode: TP = 1.95x range, SL = 0.65x range.

No Trade After 08:00 NY: If the limit order is not executed before 08:00 a.m. NY, it is canceled.

Fallback Logic at 02:15 NY: If the market direction misaligns with the setup at 02:15 a.m., the system re-evaluates and can re-issue the order.

End-of-Day Closure: All positions are closed at 15:45 NY if still open.

📊 Backtest-Ready Design:

Entries and exits are executed using strategy.entry() and strategy.exit() functions.

Position size is fixed via capital risk allocation ($100 per trade by default).

Only one position can be active at a time, ensuring controlled risk.

📝 Notes:

This strategy is ideal for assets sensitive to the Asian/London session overlap, such as Forex pairs and indices.

Easily switch between Fibonacci versions using a single dropdown input.

Fully deterministic: all entries are based on pre-defined conditions and time constraints.

👤 Credits:

Strategy developed by rau_u_lanz using Pine Script v6. Built for traders who favor clean sessions, directional clarity, and consistent execution using time-based logic and Fibonacci projections.

REVELATIONS (VoVix - PoC) REVELATIONS (VoVix - POC): True Regime Detection Before the Move

Let’s not sugarcoat it: Most strategies on TradingView are recycled—RSI, MACD, OBV, CCI, Stochastics. They all lag. No matter how many overlays you stack, every one of these “standard” indicators fires after the move is underway. The retail crowd almost always gets in late. That’s never been enough for my team, for DAFE, or for anyone who’s traded enough to know the real edge vanishes by the time the masses react.

How is this different?

REVELATIONS (VoVix - POC) was engineered from raw principle, structured to detect pre-move regime change—before standard technicals even light up. We built, tested, and refined VoVix to answer one hard question:

What if you could see the spike before the trend?

Here’s what sets this system apart, line-by-line:

o True volatility-of-volatility mathematics: It’s not just "ATR of ATR" or noise smoothing. VoVix uses normalized, multi-timeframe v-vol spikes, instantly detecting orderbook stress and "outlier" market events—before the chart shows them as trends.

o Purist regime clustering: Every trade is enabled only during coordinated, multi-filter regime stress. No more signals in meaningless chop.

o Nonlinear entry logic: No trade is ever sent just for a “good enough” condition. Every entry fires only if every requirement is aligned—local extremes, super-spike threshold, regime index, higher timeframe, all must trigger in sync.

o Adaptive position size: Your contracts scale up with event strength. Tiny size during nominal moves, max leverage during true regime breaks—never guesswork, never static exposure.

o All exits governed by regime decay logic: Trades are closed not just on price targets but at the precise moment the market regime exhausts—the hardest part of systemic trading, now solved.

How this destroys the lag:

Standard indicators (RSI, MACD, OBV, CCI, and even most “momentum” overlays) simply tell you what already happened. VoVix triggers as price structure transitions—anyone running these generic scripts will trade behind the move while VoVix gets in as stress emerges. Real alpha comes from anticipation, not confirmation.

The visuals only show what matters:

Top right, you get a live, live quant dashboard—regime index, current position size, real-time performance (Sharpe, Sortino, win rate, and wins). Bottom right: a VoVix "engine bar" that adapts live with regime stress. Everything you see is a direct function of logic driving this edge—no cosmetics, no fake momentum.

Inputs/Signals—explained carefully for clarity:

o ATR Fast Length & ATR Slow Length:

These are the heart of VoVix’s regime sensing. Fast ATR reacts to sharp volatility; Slow ATR is stability baseline. Lower Fast = reacts to every twitch; higher Slow = requires more persistent, “real” regime shifts.

Tip: If you want more signals or faster markets, lower ATR Fast. To eliminate noise, raise ATR Slow.

o ATR StdDev Window: Smoothing for volatility-of-volatility normalization. Lower = more jumpy, higher = only the cleanest spikes trigger.

Tip: Shorten for “jumpy” assets, raise for indices/futures.

o Base Spike Threshold: Think of this as your “minimum event strength.” If the current move isn’t volatile enough (normalized), no signal.

Tip: Higher = only biggest moves matter. Lower for more signals but more potential noise.

o Super Spike Multiplier: The “are you sure?” test—entry only when the current spike is this multiple above local average.

Tip: Raise for ultra-selective/swing-trading; lower for more active style.

Regime & MultiTF:

o Regime Window (Bars):

How many bars to scan for regime cluster “events.” Short for turbo markets, long for big swings/trends only.

o Regime Event Count: Only trade when this many spikes occur within the Regime Window—filters for real stress, not isolated ticks.

Tip: Raise to only ever trade during true breakouts/crashes.

o Local Window for Extremes:

How many bars to check that a spike is a local max.

Tip: Raise to demand only true, “clearest” local regime events; lower for early triggers.

o HTF Confirm:

Higher timeframe regime confirmation (like 45m on an intraday chart). Ensures any event you act on is visible in the broader context.

Tip: Use higher timeframes for only major moves; lower for scalping or fast regimes.

Adaptive Sizing:

o Max Contracts (Adaptive): The largest size your system will ever scale to, even on extreme event.

Tip: Lower for small accounts/conservative risk; raise on big accounts or when you're willing to go big only on outlier events.

o Min Contracts (Adaptive): The “toe-in-the-water.” Smallest possible trade.

Tip: Set as low as your broker/exchange allows for safety, or higher if you want to always have meaningful skin in the game.

Trade Management:

o Stop %: Tightness of your stop-loss relative to entry. Lower for tighter/safer, higher for more breathing room at cost of greater drawdown.

o Take Profit %: How much you'll hold out for on a win. Lower = more scalps. Higher = only run with the best.

o Decay Exit Sensitivity Buffer: Regime index must dip this far below the trading threshold before you exit for “regime decay.”

Tip: 0 = exit as soon as stress fails, higher = exits only on stronger confirmation regime is over.

o Bars Decay Must Persist to Exit: How long must decay be present before system closes—set higher to avoid quick fades and whipsaws.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Tip: Set to 1 for instant regime exit; raise for extra confirmation (less whipsaw risk, exits held longer).

________________________________________

Bottom line: Tune the sensitivity, selectivity, and risk of REVELATIONS by these inputs. Raise thresholds and windows for only the best, most powerful signals (institutional style); lower for activity (scalpers, fast cryptos, signals in constant motion). Sizing is always adaptive—never static or martingale. Exits are always based on both price and regime health. Every input is there for your control, not to sell “complexity.” Use with discipline, and make it your own.

This strategy is not just a technical achievement: It’s a statement about trading smarter, not just more.

* I went back through the code to make sure no the strategy would not suffer from repainting, forward looking, or any frowned upon loopholes.

Disclaimer:

Trading is risky and carries the risk of substantial loss. Do not use funds you aren’t prepared to lose. This is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

Expect more: We’ll keep pushing the standard, keep evolving the bar until “quant” actually means something in the public code space.

Use with clarity, use with discipline, and always trade your edge.

— Dskyz , for DAFE Trading Systems

Bober XM v2.0# ₿ober XM v2.0 Trading Bot Documentation

**Developer's Note**: While our previous Bot 1.3.1 was removed due to guideline violations, this setback only fueled our determination to create something even better. Rising from this challenge, Bober XM 2.0 emerges not just as an update, but as a complete reimagining with multi-timeframe analysis, enhanced filters, and superior adaptability. This adversity pushed us to innovate further and deliver a strategy that's smarter, more agile, and more powerful than ever before. Challenges create opportunity - welcome to Cryptobeat's finest work yet.

## !!!!You need to tune it for your own pair and timeframe and retune it periodicaly!!!!!

## Overview

The ₿ober XM v2.0 is an advanced dual-channel trading bot with multi-timeframe analysis capabilities. It integrates multiple technical indicators, customizable risk management, and advanced order execution via webhook for automated trading. The bot's distinctive feature is its separate channel systems for long and short positions, allowing for asymmetric trade strategies that adapt to different market conditions across multiple timeframes.

### Key Features

- **Multi-Timeframe Analysis**: Analyze price data across multiple timeframes simultaneously

- **Dual Channel System**: Separate parameter sets for long and short positions

- **Advanced Entry Filters**: RSI, Volatility, Volume, Bollinger Bands, and KEMAD filters

- **Machine Learning Moving Average**: Adaptive prediction-based channels

- **Multiple Entry Strategies**: Breakout, Pullback, and Mean Reversion modes

- **Risk Management**: Customizable stop-loss, take-profit, and trailing stop settings

- **Webhook Integration**: Compatible with external trading bots and platforms

### Strategy Components

| Component | Description |

|---------|-------------|

| **Dual Channel Trading** | Uses either Keltner Channels or Machine Learning Moving Average (MLMA) with separate settings for long and short positions |

| **MLMA Implementation** | Machine learning algorithm that predicts future price movements and creates adaptive bands |

| **Pivot Point SuperTrend** | Trend identification and confirmation system based on pivot points |

| **Three Entry Strategies** | Choose between Breakout, Pullback, or Mean Reversion approaches |

| **Advanced Filter System** | Multiple customizable filters with multi-timeframe support to avoid false signals |

| **Custom Exit Logic** | Exits based on OBV crossover of its moving average combined with pivot trend changes |

### Note for Novice Users

This is a fully featured real trading bot and can be tweaked for any ticker — SOL is just an example. It follows this structure:

1. **Indicator** – gives the initial signal

2. **Entry strategy** – decides when to open a trade

3. **Exit strategy** – defines when to close it

4. **Trend confirmation** – ensures the trade follows the market direction

5. **Filters** – cuts out noise and avoids weak setups

6. **Risk management** – controls losses and protects your capital

To tune it for a different pair, you'll need to start from scratch:

1. Select the timeframe (candle size)

2. Turn off all filters and trend entry/exit confirmations

3. Choose a channel type, channel source and entry strategy

4. Adjust risk parameters

5. Tune long and short settings for the channel

6. Fine-tune the Pivot Point Supertrend and Main Exit condition OBV

This will generate a lot of signals and activity on the chart. Your next task is to find the right combination of filters and settings to reduce noise and tune it for profitability.

### Default Strategy values

Default values are tuned for: Symbol BITGET:SOLUSDT.P 5min candle

Filters are off by default: Try to play with it to understand how it works

## Configuration Guide

### General Settings

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Long Positions** | Enable or disable long trades | Enabled |

| **Short Positions** | Enable or disable short trades | Enabled |

| **Risk/Reward Area** | Visual display of stop-loss and take-profit zones | Enabled |

| **Long Entry Source** | Price data used for long entry signals | hl2 (High+Low/2) |

| **Short Entry Source** | Price data used for short entry signals | hl2 (High+Low/2) |

The bot allows you to trade long positions, short positions, or both simultaneously. Each direction has its own set of parameters, allowing for fine-tuned strategies that recognize the asymmetric nature of market movements.

### Multi-Timeframe Settings

1. **Enable Multi-Timeframe Analysis**: Toggle 'Enable Multi-Timeframe Analysis' in the Multi-Timeframe Settings section

2. **Configure Timeframes**: Set appropriate higher timeframes based on your trading style:

- Timeframe 1: Default is now 15 minutes (intraday confirmation)

- Timeframe 2: Default is 4 hours (trend direction)

3. **Select Sources per Indicator**: For each indicator (RSI, KEMAD, Volume, etc.), choose:

- The desired timeframe (current, mtf1, or mtf2)

- The appropriate price type (open, high, low, close, hl2, hlc3, ohlc4)

### Entry Strategies

- **Breakout**: Enter when price breaks above/below the channel

- **Pullback**: Enter when price pulls back to the channel

- **Mean Reversion**: Enter when price is extended from the channel

You can enable different strategies for long and short positions.

### Core Components

### Risk Management

- **Position Size**: Control risk with percentage-based position sizing

- **Stop Loss Options**:

- Fixed: Set a specific price or percentage from entry

- ATR-based: Dynamic stop-loss based on market volatility

- Swing: Uses recent swing high/low points

- **Take Profit**: Multiple targets with percentage allocation

- **Trailing Stop**: Dynamic stop that follows price movement

## Advanced Usage Strategies

### Moving Average Type Selection Guide

- **SMA**: More stable in choppy markets, good for higher timeframes

- **EMA/WMA**: More responsive to recent price changes, better for entry signals

- **VWMA**: Adds volume weighting for stronger trends, use with Volume filter

- **HMA**: Balance between responsiveness and noise reduction, good for volatile markets

### Multi-Timeframe Strategy Approaches

- **Trend Confirmation**: Use higher timeframe RSI (mtf2) for overall trend, current timeframe for entries

- **Entry Precision**: Use KEMAD on current timeframe with volume filter on mtf1

- **False Signal Reduction**: Apply RSI filter on mtf1 with strict KEMAD settings

### Market Condition Optimization

| Market Condition | Recommended Settings |

|------------------|----------------------|

| **Trending** | Use Breakout strategy with KEMAD filter on higher timeframe |

| **Ranging** | Use Mean Reversion with strict RSI filter (mtf1) |

| **Volatile** | Increase ATR multipliers, use HMA for moving averages |

| **Low Volatility** | Decrease noise parameters, use pullback strategy |

## Webhook Integration

The strategy features a professional webhook system that allows direct connectivity to your exchange or trading platform of choice through third-party services like 3commas, Alertatron, or Autoview.

The webhook payload includes all necessary parameters for automated execution:

- Entry price and direction

- Stop loss and take profit levels

- Position size

- Custom identifier for webhook routing

## Performance Optimization Tips

1. **Start with Defaults**: Begin with the default settings for your timeframe before customizing

2. **Adjust One Component at a Time**: Make incremental changes and test the impact

3. **Match MA Types to Market Conditions**: Use appropriate moving average types based on the Market Condition Optimization table

4. **Timeframe Synergy**: Create logical relationships between timeframes (e.g., 5min chart with 15min and 4h higher timeframes)

5. **Periodic Retuning**: Markets evolve - regularly review and adjust parameters

## Common Setups

### Crypto Trend-Following

- MLMA with EMA or HMA

- Higher RSI thresholds (75/25)

- KEMAD filter on mtf1

- Breakout entry strategy

### Stock Swing Trading

- MLMA with SMA for stability

- Volume filter with higher threshold

- KEMAD with increased filter order

- Pullback entry strategy

### Forex Scalping

- MLMA with WMA and lower noise parameter

- RSI filter on current timeframe

- Use highest timeframe for trend direction only

- Mean Reversion strategy

## Webhook Configuration

- **Benefits**:

- Automated trade execution without manual intervention

- Immediate response to market conditions

- Consistent execution of your strategy

- **Implementation Notes**:

- Requires proper webhook configuration on your exchange or platform

- Test thoroughly with small position sizes before full deployment

- Consider latency between signal generation and execution

### Backtesting Period

Define a specific historical period to evaluate the bot's performance:

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Start Date** | Beginning of backtest period | January 1, 2025 |

| **End Date** | End of backtest period | December 31, 2026 |

- **Best Practice**: Test across different market conditions (bull markets, bear markets, sideways markets)

- **Limitation**: Past performance doesn't guarantee future results

## Entry and Exit Strategies

### Dual-Channel System

A key innovation of the Bober XM is its dual-channel approach: