90 Minute Cycles Full90-Minute Cycles Indicator for London and NY Sessions

This is a more streamlined version of the 90-minute cycle indicator by sunwoo101.

The 90-Minute Cycles Indicator is built to help traders easily follow and trade around key market cycles during the London and New York sessions. Marking important 90-minute intervals and highlighting the True Cycle Open Price provides clear visual cues to help you make more informed trading decisions.

Key Features:

90-Minute Cycles for London and NY: The indicator automatically draws vertical lines marking every 90-minute cycle for the London and NY sessions. These lines are great for timing your trades and spotting potential shifts in market momentum.

True Cycle Open Price: A horizontal line is drawn at the True Cycle Open Price, which stays visible throughout the session. This gives you a key reference point for price levels that tend to act as support or resistance.

Customizable Visuals: You can fully personalize the indicator’s appearance - adjusting the colors and line styles and even controlling when the lines appear - so it blends perfectly with your existing charts.

All Cycles Drawn from the Start: Unlike other indicators, this one draws all the 90-minute cycles right when the session begins, so you can see the full day’s potential market moves as soon as the first cycle starts.

What’s Different About This Indicator:

London Session Support: In addition to the NY session, you now have 90-minute cycles for the London session, complete with its own True Cycle Open Price.

Better Customization: You have more control over the visual aspects of the indicator, so it can be tailored to fit your specific charting preferences.

Complete Cycle Visibility: All cycles are drawn immediately when the session starts, providing a full view of the day’s key moments right from the opening.

How to Use:

This indicator is perfect for scalping and short-term trading. Whether trading Forex or Indices and following SMT concepts, the cycle timing can help you pinpoint the best times for entering and exiting trades. The True Cycle Open Price is a crucial level of support or resistance throughout the session, making it a key marker to watch.

Scalpers: Use the 90-minute cycle lines to time your trades with the market's rhythm.

Day Traders: This indicator tracks the London and NY sessions, making it an excellent tool for day trading strategies where timing is critical.

Multi-Session Support:

Whether you're trading the London or New York session, the indicator will automatically adjust to your time zone and align the cycles to the relevant session. This helps you stay on top of key market activity across major trading hubs without changing anything manually.

Cari dalam skrip untuk "session"

Timing - Fx MGKWhat You See:

Session Boxes:

As you observe, the larger purple box represents the Asian Session, spanning from around 22:00 to 06:00 UTC. You notice how it captures the overnight market activity.

The smaller, greyish box marks the London Session, from about 08:00 to 12:00 UTC. You can see how the price action changes during this session.

The New York Session is also indicated, with vertical lines possibly marking the open and close, helping you track movements as the U.S. markets come into play.

High and Low Levels:

Horizontal lines are drawn at the high and low of each session. You can use these as potential support or resistance levels, aiding in your decision-making process.

Vertical Lines:

These lines likely correspond to specific key times, such as session opens or closes. You can quickly identify the transition between sessions, which is crucial for your timing.

Color Coding:

Each session is color-coded, making it easier for you to distinguish between them at a glance. The purple, grey, and additional lines offer a clear visual distinction.

How You Use It:

This indicator is your go-to for understanding how different market sessions affect price action. You’ll use it to:

Recognize important price levels within each session.

Identify potential entry and exit points based on session highs and lows.

Observe how the market transitions from one session to another, giving you insight into the best times to trade.

Customization:

You have the flexibility to adjust the settings. You can change session times to suit your trading hours, modify colors to match your chart theme, and even choose which sessions to display or hide based on your focus.

This tool is designed to enhance your analysis, providing you with a structured view of market sessions. With this indicator, you’re well-equipped to navigate the global markets with greater precision and confidence.

Depth of Market (DOM) [LuxAlgo]The Depth Of Market (DOM) tool allows traders to look under the hood of any market, taking price and volume analysis to the next level. The following features are included: DOM, Time & Sales, Volume Profile, Depth of Market, Imbalances, Buying Pressure, and up to 24 key intraday levels (it really packs a punch).

As a disclaimer, this tool does not use tick data, it is a DOM reconstruction from the provided real-time time series data (price and volume). So the volume you see is from filled orders only, this tool does not show unfilled limit orders.

Traders can enable or disable any of the features at will to avoid being overwhelmed with too much information and to make the tool perform faster.

The features that have the biggest impact on performance are Historical Data Collection, Key Levels (POC & VWAP), Time & Sales, Profile, and Imbalances. Disable these features to improve the indicator computational performance.

🔶 DOM

This is the simplest form of the tool, a simple DOM or ladder that displays the following columns:

PRICE: Price level

BID: Total number of market sell orders filled or limit buy orders filled.

SELL: Sell market orders

BUY: Buy market orders

ASK: Total number of market buy orders filled or limit sell orders filled.

The DOM only collects historical data from the last 24 hours and real-time data.

Traders can select a reset period for the DOM with two options:

DAILY: Resets at the beginning of each trading day

SESSIONS: Resets twice, as DAILY and 15.5 hours later, to coincide with the start of the RTH session for US tickers.

The DOM has two main modes, it can display price levels as ticks or points. The default is automatic based on the current daily volatility, but traders can manually force one mode or the other if they wish.

For convenience, traders have the option to set the number of lines (price levels), and the size of the text and to display only real-time data.

By default, the top price is set to 0 so that the DOM automatically adjusts the price levels to be displayed, but traders can set the top price manually so that the tool displays only the desired price levels in a fixed manner.

🔹 Volume Profile

As additional features to the basic DOM, traders have access to the volume profile histogram and the total volume per price level.

This helps traders identify at a glance key price areas where volume is accumulating (high volume nodes) or areas where volume is lacking (low volume nodes) - these areas are important to some traders who base their decision-making process on them.

🔹 Imbalances

Other added features are imbalances and buying pressure:

Interlevel Imbalance: volume delta between two different price levels

Intralevel Imbalance: delta between buy and sell volume at the same price level

Buying Pressure Percent: percentage of buy volume compared to total volume

Imbalances can help traders identify areas of interest in the price for possible support or resistance.

🔹 Depth

Depth allows traders to see at a glance how much supply is above the current price level or how much demand is below the current price level.

Above the current price level shows the cumulative ask volume (filled sell limit orders) and below the current price level shows the cumulative bid volume (filled buy limit orders).

🔶 KEY LEVELS

The tool includes up to 24 different key intraday levels of particular relevance:

Previous Week Levels

PWH: Previous week high

PWL: Previous week low

PWM: Previous week middle

PWS: Previous week settlement (close)

Previous Day Levels

PDH: Previous day high

PDL: Previous day low

PDM: Previous day middle

PDS: Previous day settlement (close)

Current Day Levels

OPEN: Open of day (or session)

HOD: High of day (or session)

LOD: Low of day (or session)

MOD: Middle of day (or session)

Opening Range

ORH: Open range high

ORL: Open range low

Initial Balance

IBH: Initial balance high

IBL: Initial balance low

VWAP

+3SD: Volume weighted average price plus 3 standard deviations

+2SD: Volume weighted average price plus 2 standard deviations

+1SD: Volume weighted average price plus 1 standard deviation

VWAP: Volume weighted average price

-1SD: Volume weighted average price minus 1 standard deviation

-2SD: Volume weighted average price minus 2 standard deviations

-3SD: Volume weighted average price minus 3 standard deviations

POC: Point of control

Different traders look at different levels, the key levels shown here are objective and specific areas of interest that traders can act on, providing us with potential areas of support or resistance in the price.

🔶 TIME & SALES

The tool also features a full-time and sales panel with time, price, and size columns, a size filter, and the ability to set the timezone to display time in the trader's local time.

The information shown here is what feeds the DOM and it can be useful in several ways, for example in detecting absorption. If a large number of orders are coming into the market but the price is barely moving, this indicates that there is enough liquidity at these levels to absorb all these orders, so if these orders stop coming into the market, the price may turn around.

🔶 SETTINGS

Period: Select the anchoring period to start data collection, DAILY will anchor at the start of the trading day, and SESSIONS will start as DAILY and 15.5 hours later (RTH for US tickers).

Mode: Select between AUTO and MANUAL modes for displaying TICKS or POINTS, in AUTO mode the tool will automatically select TICKS for tickers with a daily average volatility below 5000 ticks and POINTS for the rest of the tickers.

Rows: Select the number of price levels to display

Text Size: Select the text size

🔹 DOM

DOM: Enable/Disable DOM display

Realtime only: Enable/Disable real-time data only, historical data will be collected if disabled

Top Price: Specify the price to be displayed on the top row, set to 0 to enable dynamic DOM

Max updates: Specify how many times the values on the SELL and BUY columns are accumulated until reset.

Profile/Depth size: Maximum size of the histograms on the PROFILE and DEPTH columns.

Profile: Enable/Disable Profile column. High impact on performance.

Volume: Enable/Disable Volume column. Total volume traded at price level.

Interlevel Imbalance: Enable/Disable Interlevel Imbalance column. Total volume delta between the current price level and the price level above. High impact on performance.

Depth: Enable/Disable Depth, showing the cumulative supply above the current price and the cumulative demand below. Impact on performance.

Intralevel Imbalance: Enable/Disable Intralevel Imbalance column. Delta between total buy volume and total sell volume. High impact on performance.

Buying Pressure Percent: Enable/Disable Buy Percent column. Percentage of total buy volume compared to total volume.

Imbalance Threshold %: Threshold for highlighting imbalances. Set to 90 to highlight the top 10% of interlevel imbalances and the top and bottom 10% of intra-level imbalances.

Crypto volume precision: Specify the number of decimals to display on the volume of crypto assets

🔹 Key Levels

Key Levels: Enable/Disable KEY column. Very high performance impact.

Previous Week: Enable/Disable High, Low, Middle, and Close of the previous trading week.

Previous Day: Enable/Disable High, Low, Middle, and Settlement of the previous trading day.

Current Day/Session: Enable/Disable Open, High, Low and Middle of the current period.

Open Range: Enable/Disable High and Low of the first candle of the period.

Initial Balance: Enable/Disable High and Low of the first hour of the period.

VWAP: Enable/Disable Volume-weighted average price of the period with 1, 2, and 3 standard deviations.

POC: Enable/Disable Point of Control (price level with the highest volume traded) of the period.

🔹 Time & Sales

Time & Sales: Enable/Disable time and sales panel.

Timezone offset (hours): Enter your time zone\'s offset (+ or −), including a decimal fraction if needed.

Order Size: Set order size filter. Orders smaller than the value are not displayed.

🔶 THANKS

Hi, I'm makit0 coder of this tool and proud member of the LuxAlgo Opensource team, it's an honor to be part of the LuxAlgo family doing something I love as it's writing opensource code and sharing it with the world. I'd like to thank all of you who use, comment on, and vote for all of our open-source tools, and all of you who give us your support.

And of course thanks to the PineCoders family for all the work in front of and behind the scenes that makes the PineScript community what it is, simply the best.

Peace, Love & PineScript!

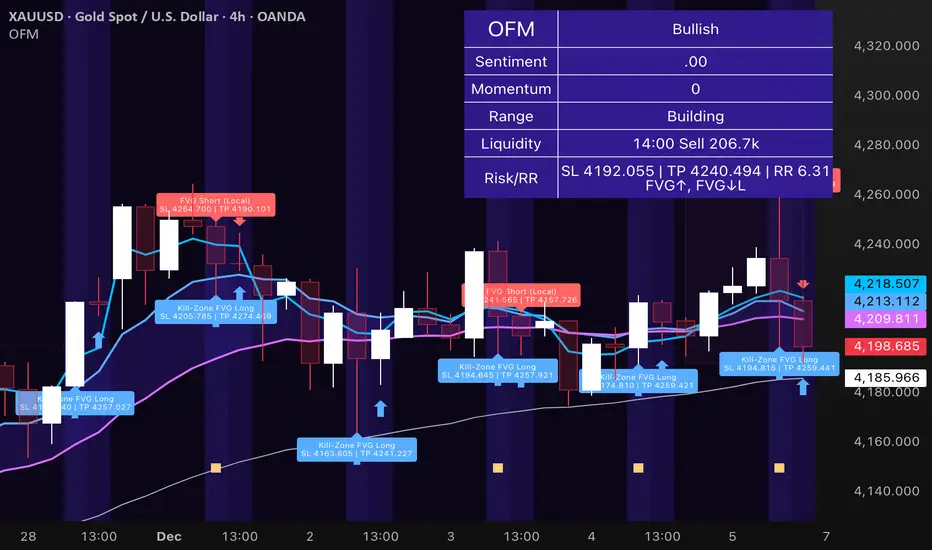

Obsidian Flux Matrix# Obsidian Flux Matrix | JackOfAllTrades

Made with my Senior Level AI Pine Script v6 coding bot for the community!

Narrative Overview

Obsidian Flux Matrix (OFM) is an open-source Pine Script v6 study that fuses social sentiment, higher timeframe trend bias, fair-value-gap detection, liquidity raids, VWAP gravitation, session profiling, and a diagnostic HUD. The layout keeps the obsidian palette so critical overlays stay readable without overwhelming a price chart.

Purpose & Scope

OFM focuses on actionable structure rather than marketing claims. It documents every driver that powers its confluence engine so reviewers understand what triggers each visual.

Core Analytical Pillars

1. Social Pulse Engine

Sentiment Webhook Feed: Accepts normalized scores (-1 to +1). Signals only arm when the EMA-smoothed value exceeds the `sentimentMin` input (0.35 by default).

Volume Confirmation: Requires local volume > 30-bar average × `volSpikeMult` (default 2.0) before sentiment flags.

EMA Cross Validation: Fast EMA 8 crossing above/below slow EMA 21 keeps momentum aligned with flow.

Momentum Alignment: Multi-timeframe momentum composite must agree (positive for longs, negative for shorts).

2. Peer Momentum Heatmap

Multi-Timeframe Blend: RSI + Stoch RSI fetched via request.security() on 1H/4H/1D by default.

Composite Scoring: Each timeframe votes +1/-1/0; totals are clamped between -3 and +3.

Intraday Readability: Configurable band thickness (1-5) so scalpers see context without losing space.

Dynamic Opacity: Stronger agreement boosts column opacity for quick bias checks.

3. Trend & Displacement Framework

Dual EMA Ribbon: Cyan/magenta ribbon highlights immediate posture.

HTF Bias: A higher-timeframe EMA (default 55 on 4H) sets macro direction.

Displacement Score: Body-to-ATR ratio (>1.4 default) detects impulses that seed FVGs or VWAP raids.

ATR Normalization: All thresholds float with volatility so the study adapts to assets and regimes.

4. Intelligent Fair Value Gap (FVG) System

Gap Detection: Three-candle logic (bullish: low > high ; bearish: high < low ) with ATR-sized minimums (0.15 × ATR default).

Overlap Prevention: Price-range checks stop redundant boxes.

Spacing Control: `fvgMinSpacing` (default 5) avoids stacking from the same impulse.

Storage Caps: Max three FVGs per side unless the user widens the limit.

Session Awareness: Kill zone filters keep taps focused on London/NY if desired.

Auto Cleanup: Boxes delete when price closes beyond their invalidation level.

5. VWAP Magnet + Liquidity Raid Engine

Session or Rolling VWAP: Toggle resets to match intraday or rolling preferences.

Equal High/Low Scanner: Looks back 20 bars by default for liquidity pools.

Displacement Filter: ATR multiplier ensures raids represent genuine liquidity sweeps.

Mean Reversion Focus: Signals fire when price displaces back toward VWAP following a raid.

6. Session Range Breakout System

Initial Balance Tracking: First N bars (15 default) define the session box.

Breakout Logic: Requires simultaneous liquidity spikes, nearby FVG activity, and supportive momentum.

Z-Score Volume Filter: >1.5σ by default to filter noisy moves.

7. Lifestyle Liquidity Scanner

Volume Z-Scores: 50-bar baseline highlights statistically significant spikes.

Smart Money Footprints: Bottom-of-chart squares color-code buy vs sell participation.

Panel Memory: HUD logs the last five raid timestamps, direction, and normalized size.

8. Risk Matrix & Diagnostic HUD

HUD Structure: Table in the top-right summarizes HTF bias, sentiment, momentum, range state, liquidity memory, and current risk references.

Signal Tags: Aggregates SPS, FVG, VWAP, Range, and Liquidity states into a compact string.

Risk Metrics: Swing-based stops (5-bar lookback) + ATR targets (1.5× default) keep risk transparent.

Signal Families & Alerts

Social Pulse (SPS): Volume-confirmed sentiment alignment; triangle markers with “SPS”.

Kill-Zone FVG: Session + HTF alignment + FVG tap; arrow markers plus SL/TP labels.

Local FVG: Captures local reversals when HTF bias has not flipped yet.

VWAP Raid: Equal-high/low raids that snap toward VWAP; “VWAP” label markers.

Range Breakout: Initial balance violations with liquidity and imbalance confirmation; circle markers.

Liquidity Spike: Z-score spikes ≥ threshold; square markers along the baseline.

Visual Design & Customization

Theme Palette: Primary background RGB (12,6,24). Accent shading RGB (26,10,48). Long accents RGB (88,174,255). Short accents RGB (219,109,255).

Stylized Candles: Optional overlay using theme colors.

Signal Toggles: Independently enable markers, heatmap, and diagnostics.

Label Spacing: Auto-spacing enforces ≥4-bar gaps to prevent text overlap.

Customization & Workflow Notes

Adjust ATR/FVG thresholds when volatility shifts.

Re-anchor sentiment to your webhook cadence; EMA smoothing (default 5) dampens noise.

Reposition the HUD by editing the `table.new` coordinates.

Use multiples of the chart timeframe for HTF requests to minimize load.

Session inputs accept exchange-local time; align them to your market.

Performance & Compliance

Pure Pine v6: Single-line statements, no `lookahead_on`.

Resource Safe: Arrays trimmed, boxes limited, `request.security` cached.

Repaint Awareness: Signals confirm on close; alerts mirror on-chart logic.

Runtime Safety: Arrays/loops guard against `na`.

Use Cases

Measure when social sentiment aligns with structure.

Plan ICT-style intraday rebalances around session-specific FVG taps.

Fade VWAP raids when displacement shows exhaustion.

Watch initial balance breaks backed by statistical volume.

Keep risk/target references anchored in ATR logic.

Signal Logic Snapshot

Social Pulse Long/Short: `sentimentEMA` gated by `sentimentMin`, `volSpike`, EMA 8/21 cross, and `momoComposite` sign agreement. Keeps hype tied to structural follow-through.

Kill-Zone FVG Long/Short: Requires session filter, HTF EMA bias alignment, and an active FVG tap (`bullFvgTap` / `bearFvgTap`). Labels include swing stops + ATR targets pulled from `swingLookback` and `liqTargetMultiple`.

Local FVG Long/Short: Uses `localBullish` / `localBearish` heuristics (EMA slope, displacement, sequential closes) to surface intraday reversals even when HTF bias has not flipped.

VWAP Raids: Detect equal-high/equal-low sweeps (`raidHigh`, `raidLow`) that revert toward `sessionVwap` or rolling VWAP when displacement exceeds `vwapAlertDisplace`.

Range Breakouts: Combine `rangeComplete`, breakout confirmation, liquidity spikes, and nearby FVG activity for statistically backed initial balance breaks.

Liquidity Spikes: Volume Z-score > `zScoreThreshold` logs direction, size, and timestamp for the HUD and optional review workflows.

Session Logic & VWAP Handling

Kill zone + NY session inputs use TradingView’s session strings; `f_inSession()` drives both visual shading and whether FVG taps are tradeable when `killZoneOnly` is true.

Session VWAP resets using cumulative price × volume sums that restart when the daily timestamp changes; rolling VWAP falls back to `ta.vwap(hlc3)` for instruments where daily resets are less relevant.

Initial balance box (`rangeBars` input) locks once complete, extends forward, and stays on chart to contextualize later liquidity raids or breakouts.

Parameter Reference

Trend: `emaFastLen`, `emaSlowLen`, `htfResolution`, `htfEmaLen`, `showEmaRibbon`, `showHtfBiasLine`.

Momentum: `tf1`, `tf2`, `tf3`, `rsiLen`, `stochLen`, `stochSmooth`, `heatmapHeight`.

Volume/Liquidity: `volLookback`, `volSpikeMult`, `zScoreLen`, `zScoreThreshold`, `equalLookback`.

VWAP & Sessions: `vwapMode`, `showVwapLine`, `vwapAlertDisplace`, `killSession`, `nySession`, `showSessionShade`, `rangeBars`.

FVG/Risk: `fvgMinTicks`, `fvgLookback`, `fvgMinSpacing`, `killZoneOnly`, `liqTargetMultiple`, `swingLookback`.

Visualization Toggles: `showSignalMarkers`, `showHeatmapBand`, `showInfoPanel`, `showStylizedCandles`.

Workflow Recipes

Kill-Zone Continuation: During the defined kill session, look for `killFvgLong` or `killFvgShort` arrows that line up with `sentimentValid` and positive `momoComposite`. Use the HUD’s risk readout to confirm SL/TP distances before entering.

VWAP Raid Fade: Outside kill zone, track `raidToVwapLong/Short`. Confirm the candle body exceeds the displacement multiplier, and price crosses back toward VWAP before considering reversions.

Range Break Monitor: After the initial balance locks, mark `rangeBreakLong/Short` circles only when the momentum band is >0 or <0 respectively and a fresh FVG box sits near price.

Liquidity Spike Review: When the HUD shows “Liquidity” timestamps, hover the plotted squares at chart bottom to see whether spikes were buy/sell oriented and if local FVGs formed immediately after.

Metadata

Author: officialjackofalltrades

Platform: TradingView (Pine Script v6)

Category: Sentiment + Liquidity Intelligence

Hope you Enjoy!

ICT Liquidity Sweep Asia/London 1 Trade per High & Low🧠 ICT Liquidity Sweep Asia/London — 1 Trade per High & Low

This strategy is inspired by the ICT (Inner Circle Trader) concepts of liquidity sweeps and market structure, focusing on the Asia and London sessions.

It automatically identifies liquidity grabs (sweeps) above or below key session highs/lows and enters trades with a fixed risk/reward ratio (RR).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚙️ Core Logic

-Asia Session: 8:00 PM – 11:59 PM (New York time)

-London Session: 2:00 AM – 5:00 AM (New York time)

-The script marks the Asia High/Low and London High/Low ranges for each day.

-When the market sweeps above a session high → potential Short setup

-When the market sweeps below a session low → potential Long setup

-A trade is triggered when the confirmation candle closes in the opposite direction of the sweep (bearish after a high sweep, bullish after a low sweep).

-Only one trade per sweep type (1 per High, 1 per Low) is allowed per session.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

📈 Risk Management

-Configurable Risk/Reward Target (default = 2:1)

-Configurable Position Size (number of contracts)

-Each trade uses a fixed Stop Loss (beyond the wick of the sweep) and a Take Profit calculated from the RR setting.

-All trades are automatically logged in the Strategy Tester with performance metrics.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

💡 Features

✅ Visual session highlighting (Asia = Aqua, London = Orange)

✅ Automatic liquidity line plotting (session highs/lows)

✅ Entry & exit labels (optional visual display)

✅ Customizable RR and contract size

✅ Works on any instrument (ideal for indices, futures, or forex)

✅ Compatible with all timeframes (optimized for 1M–15M)

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚠️ Notes

-Best used on New York time-based charts.

-Designed for educational and backtesting purposes — not financial advice.

-Use as a foundation for further optimization (e.g., SMT confirmation, FVG filter, or time-based restrictions).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

🧩 Recommended Use

Pair this with:

-ICT’s concepts like CISD (Change in State of Delivery) and FVGs (Fair Value Gaps)

-Higher timeframe liquidity maps

-Session bias or daily narrative filters

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

Author: jygirouard

Strategy Version: 1.3

Type: ICT Liquidity Sweep Automation

Timezone: America/New_York

Transformer Flux DashboardHere’s a practical guide to what your Transformer Flux Dashboard does and how to use it.

What it is

A compact, two-column trading dashboard + signal pack that blends trend, MACD, and OBV into one view (“Flux Score”) and adds session awareness (pre-sessions and main sessions in Eastern time). It’s designed for regular candles by default and avoids repaint by letting you confirm on bar close.

Core pieces it calculates

Moving Averages

Two MAs: Fast (HMA/EMA) and Slow (HMA/EMA).

You choose length, line width, color, and transparency.

Trend engine (Strict/Lenient)

Uses the relation between Fast/Slow MA and a debounced fast-MA slope filter (slope > ATR×buffer).

Strict: requires fast>slow and slow rising (or the inverse for down).

Lenient: fast>slow or slow rising (or the inverse).

A confirmation window (bars) must hold true before trend flips. That window can be auto-tuned by session (Asia/London/NY) or set globally.

OBV confirmation (optional)

OBV smoothed by SMA; needs to be rising/falling for N bars (also session-aware if you enable presets).

MACD

Standard MACD Fast/Slow/Signal; the dashboard shows Bull ▲, Bear ▼ or Flat based on line vs signal.

Flux Score (top row)

A composite, smoothed gauge from 0–100:

40% Trend, 30% MACD, 30% OBV → EMA(3) smoothed.

Labels: Bullish ≥ 70, Bearish ≤ 30, otherwise Neutral.

Summary line explains why (e.g., “MACD↑, OBV↑, Trend up”).

Sessions & zones (Eastern/NY time)

Recognizes Asia / London / New York main sessions and pre-sessions using your chart’s Eastern time.

Session label (top of chart): text is white; background auto-matches the current session color (or your manual color).

Zone backgrounds (optional): off by default; when on, default transparency ≈ 95% (very light), with separate colors for each session and pre-session. A toggle lets you draw pre-session on top or beneath main sessions.

Signals & markers

Two strength tiers: Strong (Trend + OBV + MACD aligned) and Weak (2 of the 3 agree).

To reduce clutter, markers only appear on direction shifts (from last visible direction to a new one), and you can enforce a minimum bar gap.

Marker style:

Default Icons with LabelUp/LabelDown (tiny).

Colors: strong long = bright white by default; others configurable.

Weak markers are slightly offset from price using ATR so they don’t overlap wicks.

Dashboard (2-column)

Left column = label, right column = value:

Flux Score: numeric + Bullish/Neutral/Bearish tag.

Summary: short reason of the score.

Trend: UP / DOWN / FLAT (cell tinted green/red/gray).

MACD: Bull ▲ / Bear ▼ / Flat (tinted).

Signal: last printed signal + bar age (fresh signals get a lighter tint).

MA: slow MA type/length and up/down arrow.

Sess: current session label (e.g., “Pre-London”, “New York”).

VIX / VXN (optional): shows current value.

Auto tint: based on calm/watch/elevated thresholds (you control levels and colors).

Manual tint: fixed BG color if you prefer consistency.

Params: “P”=trend bars, “O”=OBV bars, mode (Strict/Lenient), and “Candles”.

You can set a global Default Transparency for the dashboard cells.

Key settings to know

Confirm On Close: when on (default), trend/OBV/MACD states use the last confirmed bar; this avoids mid-bar flicker and reduces repaint risk.

Session presets: when enabled, the number of bars required for confirmations tightens/loosens per session (e.g., Asia uses more bars than NY).

Colors & Opacity:

MA lines have their own transparency (default 0 = fully opaque).

Dashboard cells use a single global transparency (default 40%).

Session zones default to very light (95%) and are off by default.

VIX/VXN cells can auto-color by regime or use a manual background.

Markers:

“Icons” vs “Ticks.” Default is Icons with tiny labels up/down.

“Shift only” display reduces noise; you can also set min bar spacing.

How to read it (quick workflow)

Flux Score row: a fast “risk-on/off” gauge.

≥70 with green Trend/MACD cells → higher-conviction long context.

≤30 with red Trend/MACD cells → higher-conviction short context.

Summary explains why the score is what it is.

Signal row: tells you the last official signal and how many bars ago it fired. Fresh signals tint lighter.

MA row: aligns your slow baseline; arrow helps spot slow-turns early.

Sess row + label: know which market is active; behavior and your confirmation bars adapt by session if presets are on.

VIX/VXN (if enabled): extra context for risk regime (values and color band).

Good practices & caveats

It’s confirmation-based to reduce false flips; you’ll get signals slightly later, by design.

All signals are informational; there’s no position management or stops in this build (we removed the stop visuals by request).

If you switch to exotic chart types or extreme resolutions, re-tune lengths and confirmation bars (and potentially disable session presets).

For scalping, consider reducing confirmation bars and OBV smoothing; for higher timeframes, increase them.

Quick customization ideas

Want faster flips? Lower confirmBars and obvBars, increase slope buffer a bit to retain quality.

Want fewer weak signals? Show only strong markers (toggle off weak via colors/visibility or increase min bar gap).

Prefer EMA stacking? Set both Fast/Slow to EMA.

Don’t care about OBV? Turn OBV confirm off; Trend + MACD will drive

SMT SwiftEdge PowerhouseSMT SwiftEdge Powerhouse: Precision Trading with Divergence, Liquidity Grabs, and OTE Zones

The SMT SwiftEdge Powerhouse is a powerful trading tool designed to help traders identify high-probability entry points during the most active market sessions—London and New York. By combining Smart Money Technique (SMT) Divergence, Liquidity Grabs, and Optimal Trade Entry (OTE) Zones, this script provides a unique and cohesive strategy for capturing market reversals with precision. Whether you're a scalper or a swing trader, this indicator offers clear visual signals to enhance your trading decisions on any timeframe.

What Does This Script Do?

This script integrates three key concepts to identify potential trading opportunities:

SMT Divergence:

SMT Divergence compares the price action of two correlated assets (e.g., Nasdaq and S&P 500 futures) to detect hidden market reversals. When one asset makes a higher high while the other makes a lower high (bearish divergence), or one makes a lower low while the other makes a higher low (bullish divergence), it signals a potential reversal. This technique leverages institutional "smart money" behavior to anticipate market shifts.

Liquidity Grabs:

Liquidity Grabs occur when price breaks above recent highs or below recent lows on higher timeframes (5m and 15m), often triggering stop-loss orders from retail traders. These breakouts are identified using pivot points and confirm institutional activity, setting the stage for a reversal. The script focuses on liquidity grabs during the London and New York sessions for maximum market activity.

Optimal Trade Entry (OTE) Zones:

OTE Zones are Fibonacci-based retracement areas (e.g., 61.8%) calculated after a liquidity grab. These zones highlight where price is likely to retrace before continuing in the direction of the reversal, offering a high-probability entry point. The script adjusts the width of these zones using the Average True Range (ATR) to adapt to market volatility.

By combining these components, the script identifies when institutional activity (liquidity grabs) aligns with market reversals (SMT divergence) and pinpoints precise entry points (OTE zones) during high-liquidity sessions.

Why Combine These Components?

The integration of SMT Divergence, Liquidity Grabs, and OTE Zones creates a robust trading system for several reasons:

Synergy of Institutional Signals: SMT Divergence and Liquidity Grabs both reflect "smart money" behavior—divergence shows hidden reversals, while liquidity grabs confirm institutional intent to trap retail traders. Together, they provide a strong foundation for identifying high-probability setups.

Session-Based Precision: Focusing on the London and New York sessions ensures signals occur during periods of high volatility and liquidity, increasing their reliability.

Precision Entries with OTE: After confirming a setup with divergence and liquidity grabs, OTE zones provide a clear entry area, reducing guesswork and improving trade accuracy.

Adaptability: The script works on any timeframe, with adjustable settings for signal sensitivity, session times, and Fibonacci levels, making it versatile for different trading styles.

This combination makes the script unique by aligning institutional insights with actionable entry points, tailored to the most active market hours.

How to Use the Script

Setup:

Add the script to your chart (works on any timeframe, e.g., 1m, 5m, 15m).

Configure the settings in the indicator's inputs:

Session Settings: Adjust the start/end times for London and New York sessions (default: London 8-11 UTC, New York 13-16 UTC). You can disable session restrictions if desired.

Asset Settings: Set the primary and secondary assets for SMT Divergence (default: NQ1! and ES1!). Ensure the assets are correlated.

Signal Settings: Adjust the lookback period, ATR period, and signal sensitivity (Low/Medium/High) to control the frequency of signals.

OTE Settings: Choose the Fibonacci level for OTE zones (default: 61.8%).

Visual Settings: Enable/disable OTE zones, SMT labels, and debug labels for troubleshooting.

Interpreting Signals:

Blue Circles: Indicate a liquidity grab (price breaking a 5m or 15m pivot high/low), marking the start of a potential setup.

Blue OTE Zones: Appear after a liquidity grab, showing the retracement area (e.g., 61.8% Fibonacci level) where price is likely to enter for a reversal trade. The label "OTE Trigger 5m/15m" confirms the direction (Short/Long) and session.

Green/Red Entry Boxes: Mark precise entry points when price enters the OTE zone and confirms the SMT Divergence. Green boxes indicate a long entry, red boxes a short entry.

Trading Example:

On a 1m chart, a blue circle appears when price breaks a 5m pivot high during the London session.

A blue OTE zone forms, showing a retracement area (e.g., 61.8% Fibonacci level) with the label "OTE Trigger 5m/15m (Short, London)".

Price retraces into the OTE zone, and a red "Short Entry" box appears, confirming a bearish SMT Divergence.

Enter a short trade at the red box, with a stop-loss above the OTE zone and a take-profit at the next support level.

Originality and Utility

The SMT SwiftEdge Powerhouse stands out by merging SMT Divergence, Liquidity Grabs, and OTE Zones into a single, session-focused indicator. Unlike traditional indicators that focus on one aspect of price action, this script combines institutional reversal signals with precise entry zones, tailored to the most active market hours. Its adaptability across timeframes, customizable settings, and clear visual cues make it a versatile tool for traders seeking to capitalize on smart money movements with confidence.

Tips for Best Results

Use on correlated assets like NQ1! (Nasdaq futures) and ES1! (S&P 500 futures) for accurate SMT Divergence.

Test on lower timeframes (1m, 5m) for scalping or higher timeframes (15m, 1H) for swing trading.

Adjust the "Signal Sensitivity" to "High" for more signals or "Low" for fewer, high-quality setups.

Enable "Show Debug Labels" if signals are not appearing as expected, to troubleshoot pivot points and liquidity grabs.

JJ Highlight Time Ranges with First 5 Minutes and LabelsTo effectively use this Pine Script as a day trader , here’s how the various elements can help you manage trades, track time sessions, and monitor price movements:

Key Components for a Day Trader:

1. First 5-Minute Highlight:

- Purpose: Day traders often rely on the first 5 minutes of the trading session to gauge market sentiment, watch for opening price gaps, or plan entries. This script draws a horizontal line at the high or low of the first 5 minutes, which can act as a key level for the rest of the day.

- How to Use: If the price breaks above or below the first 5-minute line, it can signal momentum. You might enter a long position if the price breaks above the first 5-minute high or a short if it breaks below the first 5-minute low.

2. Session Time Highlights:

- Morning Session (9:15–10:30 AM): The market often shows its strongest price action during the first hour of trading. This session is highlighted in yellow. You can use this highlight to focus on the most volatile period, as this is when large institutional moves tend to occur.

- Afternoon Session (12:30–2:55 PM): The blue highlight helps you track the mid-afternoon session, where liquidity may decrease, and price action can sometimes be choppier. Day traders should be more cautious during this period.

- How to Use: By highlighting these key times, you can:

- Focus on key breakouts during the morning session.

- Be more conservative in your trades during the afternoon, as market volatility may drop.

3. Dynamic Labels:

- Top/Bottom Positioning: The script places labels dynamically based on the selected position (Top or Bottom). This allows you to quickly glance at the session's start and identify where you are in terms of time.

- How to Use: Use these labels to remind yourself when major time segments (morning or afternoon) begin. You can adjust your trading strategy depending on the session, e.g., being more aggressive in the morning and more cautious in the afternoon.

Trading Strategy Suggestions:

1. Momentum Trades:

- After the first 5 minutes, use the high/low of that period to set up breakout trades.

- Long Entry: If the price breaks the high of the first 5 minutes (especially if there's a strong trend).

- Short Entry: If the price breaks the low of the first 5 minutes, signaling a potential downtrend.

2. Session-Based Strategy:

- Morning Session (9:15–10:30 AM):

- Look for strong breakout patterns such as support/resistance levels, moving average crossovers, or candlestick patterns (like engulfing candles or pin bars).

- This is a high liquidity period, making it ideal for executing quick trades.

- Afternoon Session (12:30–2:55 PM):

- The market tends to consolidate or show less volatility. Scalping and mean-reversion strategies work better here.

- Avoid chasing big moves unless you see a clear breakout in either direction.

3. Support and Resistance:

- The first 5-minute high/low often acts as a key support or resistance level for the rest of the day. If the price holds above or below this level, it’s an indication of trend continuation.

4. Breakout Confirmation:

- Look for breakouts from the highlighted session time ranges (e.g., 9:15 AM–10:30 AM or 12:30 PM–2:55 PM).

- If a breakout happens during a key time window, combine that with other technical indicators like volume spikes , RSI , or MACD for confirmation.

---

Example Day Trader Usage:

1. First 5 Minutes Strategy: After the market opens at 9:15 AM, watch the price action for the first 5 minutes. The high and low of these 5 minutes are critical levels. If the price breaks above the high of the first 5 minutes, it might indicate a strong bullish trend for the day. Conversely, breaking below the low may suggest bearish movement.

2. Morning Session: After the first 5 minutes, focus on the **9:15 AM–10:30 AM** window. During this time, look for breakout setups at key support/resistance levels, especially when paired with high volume or momentum indicators. This is when many institutions make large trades, so price action tends to be more volatile and predictable.

3. Afternoon Session: From 12:30 PM–2:55 PM, the market might experience lower volatility, making it ideal for scalping or range-bound strategies. You could look for reversals or fading strategies if the market becomes too quiet.

Conclusion:

As a day trader, you can use this script to:

- Track and react to key price levels during the first 5 minutes.

- Focus on high volatility in the morning session (9:15–10:30 AM) and **be cautious** during the afternoon.

- Use session-based timing to adjust your strategies based on the time of day.

BRT Cluster VolumeTitle and Purpose

BRT Cluster Volume is a powerful market analysis tool designed to identify key support and resistance levels, cluster volumes, and breakout signals. This script is highly beneficial for traders who aim to gain deeper insights into market trends and pinpoint zones of interest for buyers and sellers.

Key Features

1. Support and Resistance Levels:

- The script automatically detects chart extremums by analyzing a specified number of bars on the left and right to form levels. This approach effectively identifies local highs and lows.

- The uniqueness of this implementation lies in its dynamic data processing. For each extremum, the "channel width" is calculated, allowing insignificant levels to be filtered out based on a user-defined minimum width. This method eliminates noise and ensures focus on critical levels.

- Extremum lines can be extended to the right (when enabled), allowing traders to track current price movements relative to historical levels.

2. Cluster Volume:

- The cluster analysis is based on lower timeframe data, providing precise identification of key zones of market participant activity. The script dynamically requests close prices and volumes from lower timeframes, calculates the average volume, and identifies levels where volumes exceed a defined threshold.

- The visualization of cluster volumes is unique: volumes exceeding the threshold are displayed as candles with customizable colors and markers. These indicators help traders identify zones of significant interest.

- Cluster volume is only displayed when it interacts with support or resistance levels, ensuring that the visualization remains precise and relevant for market analysis.

3. Breakout Signals:

- The script evaluates "breakout strength" for each breakout of support or resistance levels by comparing the current price with the level. This helps filter false breakouts and focus on significant price movements.

- Traders can select the source for breakout signals (close price or high/low), offering flexibility for various trading styles and strategies.

- By incorporating the concept of "maximum breakout strength," the script highlights only meaningful breakouts, ignoring minor fluctuations.

4. Integration of Trading Sessions:

- Extremum levels for major trading sessions (Asia, Europe, USA) are identified and labeled on the chart. This allows traders to see when significant price levels were formed during the day.

- The script uses timestamps to automatically detect session times, ensuring accuracy and minimizing manual adjustments.

5. Dynamic Data Updates:

- The script dynamically updates support and resistance levels in real time as new data becomes available. This feature is crucial for traders working in fast-moving markets.

- Outdated information (such as obsolete levels) is automatically removed to keep the chart clean and focused on relevant data.

6. Visualization of Activity Zones:

- Trend direction is visualized using color-coded candles based on cluster volumes. For instance, candles with volumes exceeding the average are highlighted with specific colors, helping traders quickly identify areas of heightened activity.

- The unique aspect of this visualization is that cluster volumes appear only in zones where they interact with breakout levels, providing an intuitive and streamlined presentation of critical data.

Usage

- Support and Resistance: Adjust the "Left Bars" and "Right Bars" settings to determine extremums. Use the "Channel Min Width" setting to filter out insignificant levels.

- Cluster Volume: Customize the analysis period and volume threshold to identify high-activity zones. Enable breakout clusters to see how volumes interact with breakouts.

- Session Extremums: Highlight significant levels for Asia, Europe, and US trading sessions to gain insights into market dynamics across different time zones.

- Breakout Signals: Configure the breakout strength and source (close or high/low) for precise signal detection.

Parameter Details

1. Support & Resistance:

- `Left Bars` / `Right Bars`: Number of bars to consider for determining extremums.

- `# of Lines`: Maximum number of support/resistance lines to display.

- `Channel Min Width`: Minimum channel width to filter insignificant levels.

2. Breakout:

- `Show Breakouts`: Toggle breakout signal display.

- `Max breakout strength`: Maximum strength for valid breakouts.

- `Breakout source`: Data source for breakouts (close or high/low).

3. Cluster Volume:

- `Lookback`: Number of bars to analyze for cluster volumes.

- `Threshold`: Volume threshold (percentage above the average).

- `Cluster Volume Timeframe`: Timeframe for cluster volume analysis.

- `Breakout Cluster`: Display cluster volumes only for breakout-related zones.

4. Visual Settings:

- `Extend extremum lines to the right`: Extend support/resistance lines to the right.

- `Show ASIA/EU/US Session Extremums`: Display extremums for trading sessions.

Features and Benefits

- The script provides flexible parameter customization, allowing it to adapt to different trading styles and timeframes.

- The visualization is designed to be clean and intuitive, ensuring users can easily interpret the data.

- Suitable for all timeframes, making it ideal for both intraday and long-term market analysis.

Limitations

- The script is not suitable for analysis on non-standard chart types (e.g., Heikin Ashi, Renko, Kagi).

- To ensure accurate performance, realistic data for commission and slippage should be used.

Warnings

- The script relies on historical data for calculations, which may cause discrepancies in real-time conditions.

- Users should fully understand the functionality of cluster analysis and breakout signals before using the script in live trading.

This script combines advanced data processing logic, dynamic level adjustments, and unique visualization approaches, making it an indispensable tool for market analysis and trading decision-making.

ATR GOD Strategy by TradeSmart (PineConnector-compatible)This is a highly-customizable trading strategy made by TradeSmart, focusing mainly on ATR-based indicators and filters. The strategy is mainly intended for trading forex , and has been optimized using the Deep Backtest feature on the 2018.01.01 - 2023.06.01 interval on the EUR/USD (FXCM) 15M chart, with a Slippage value of 3, and a Commission set to 0.00004 USD per contract. The strategy is also made compatible with PineConnector , to provide an easy option to automate the strategy using a connection to MetaTrader. See tooltips for details on how to set up the bot, and check out our website for a detailed guide with images on how to automate the strategy.

The strategy was implemented using the following logic:

Entry strategy:

A total of 4 Supertrend values can be used to determine the entry logic. There is option to set up all 4 Supertrend parameters individually, as well as their potential to be used as an entry signal/or a trend filter. Long/Short entry signals will be determined based on the selected potential Supertrend entry signals, and filtered based on them being in an uptrend/downtrend (also available for setup). Please use the provided tooltips for each setup to see every detail.

Exit strategy:

4 different types of Stop Losses are available: ATR-based/Candle Low/High Based/Percentage Based/Pip Based. Additionally, Force exiting can also be applied, where there is option to set up 4 custom sessions, and exits will happen after the session has closed.

Parameters of every indicator used in the strategy can be tuned in the strategy settings as follows:

Plot settings:

Plot Signals: true by default, Show all Long and Short signals on the signal candle

Plot SL/TP lines: false by default, Checking this option will result in the TP and SL lines to be plotted on the chart.

Supertrend 1-4:

All the parameters of the Supertrends can be set up here, as well as their individual role in the entry logic.

Exit Strategy:

ATR Based Stop Loss: true by default

ATR Length (of the SL): 100 by default

ATR Smoothing (of the SL): RMA/SMMA by default

Candle Low/High Based Stop Loss: false by default, recent lowest or highest point (depending on long/short position) will be used to calculate stop loss value. Set 'Base Risk Multiplier' to 1 if you would like to use the calculated value as is. Setting it to a different value will count as an additional multiplier.

Candle Lookback (of the SL): 50 by default

Percentage Based Stop Loss: false by default, Set the stop loss to current price - % of current price (long) or price + % of current price (short).

Percentage (of the SL): 0.3 by default

Pip Based Stop Loss: Set the stop loss to current price - x pips (long) or price + x pips (short). Set 'Base Risk Multiplier' to 1 if you would like to use the calculated value as is. Setting it to a different value will count as an additional multiplier.

Pip (of the SL): 10 by default

Base Risk Multiplier: 4.5 by default, the stop loss will be placed at this risk level (meaning in case of ATR SL that the ATR value will be multiplied by this factor and the SL will be placed that value away from the entry level)

Risk to Reward Ratio: 1.5 by default, the take profit level will be placed such as this Risk/Reward ratio is met

Force Exiting:

4 total Force exit on custom session close options: none applied by default. If enabled, trades will close automatically after the set session is closed (on next candle's open).

Base Setups:

Allow Long Entries: true by default

Allow Short Entries: true by default

Order Size: 10 by default

Order Type: Capital Percentage by default, allows adjustment on how the position size is calculated: Cash: only the set cash amount will be used for each trade Contract(s): the adjusted number of contracts will be used for each trade Capital Percentage: a % of the current available capital will be used for each trade

ATR Limiter:

Use ATR Limiter: true by default, Only enter into any position (long/short) if ATR value is higher than the Low Boundary and lower than the High Boundary.

ATR Limiter Length: 50 by default

ATR Limiter Smoothing: RMA/SMMA by default

High Boundary: 1000 by default

Low Boundary: 0.0003 by default

MA based calculation: ATR value under MA by default, If not Unspecified, an MA is calculated with the ATR value as source. Only enter into position (long/short) if ATR value is higher/lower than the MA.

MA Type: RMA/SMMA by default

MA Length: 400 by default

Waddah Attar Filter:

Explosion/Deadzone relation: Not specified by default, Explosion over Deadzone: trades will only happen if the explosion line is over the deadzone line; Explosion under Deadzone: trades will only happen if the explosion line is under the deadzone line; Not specified: the opening of trades will not be based on the relation between the explosion and deadzone lines.

Limit trades based on trends: Not specified by default, Strong Trends: only enter long if the WA bar is colored green (there is an uptrend and the current bar is higher then the previous); only enter short if the WA bar is colored red (there is a downtrend and the current bar is higher then the previous); Soft Trends: only enter long if the WA bar is colored lime (there is an uptrend and the current bar is lower then the previous); only enter short if the WA bar is colored orange (there is a downtrend and the current bar is lower then the previous); All Trends: only enter long if the WA bar is colored green or lime (there is an uptrend); only enter short if the WA bar is colored red or orange (there is a downtrend); Not specified: the color of the WA bar (trend) is not relevant when considering entries.

WA bar value: Not specified by default, Over Explosion and Deadzone: only enter trades when the WA bar value is over the Explosion and Deadzone lines; Not specified: the relation between the explosion/deadzone lines to the value of the WA bar will not be used to filter opening trades.

Sensitivity: 150 by default

Fast MA Type: SMA by default

Fast MA Length: 10 by default

Slow MA Type: SMA

Slow MA Length: 20 by default

Channel MA Type: EMA by default

BB Channel Length: 20 by default

BB Stdev Multiplier: 2 by default

Trend Filter:

Use long trend filter 1: false by default, Only enter long if price is above Long MA.

Show long trend filter 1: false by default, Plot the selected MA on the chart.

TF1 - MA Type: EMA by default

TF1 - MA Length: 120 by default

TF1 - MA Source: close by default

Use short trend filter 1: false by default, Only enter long if price is above Long MA.

Show short trend filter 1: false by default, Plot the selected MA on the chart.

TF2 - MA Type: EMA by default

TF2 - MA Length: 120 by default

TF2 - MA Source: close by default

Volume Filter:

Only enter trades where volume is higher then the volume-based MA: true by default, a set type of MA will be calculated with the volume as source, and set length

MA Type: RMA/SMMA by default

MA Length: 200 by default

Date Range Limiter:

Limit Between Dates: false by default

Start Date: Jan 01 2023 00:00:00 by default

End Date: Jun 24 2023 00:00:00 by default

Session Limiter:

Show session plots: false by default, show market sessions on chart: Sidney (red), Tokyo (orange), London (yellow), New York (green)

Use session limiter: false by default, if enabled, trades will only happen in the ticked sessions below.

Sidney session: false by default, session between: 15:00 - 00:00 (EST)

Tokyo session: false by default, session between: 19:00 - 04:00 (EST)

London session: false by default, session between: 03:00 - 11:00 (EST)

New York session: false by default, session between: 08:00 - 17:00 (EST)

Trading Time:

Limit Trading Time: true by default, tick this together with the options below to enable limiting based on day and time

Valid Trading Days Global: 123567 by default, if the Limit Trading Time is on, trades will only happen on days that are present in this field. If any of the not global Valid Trading Days is used, this field will be neglected. Values represent days: Sunday (1), Monday (2), ..., Friday (6), Saturday(7) To trade on all days use: 123457

(1) Valid Trading Days: false, 123456 by default, values represent days: Sunday (1), Monday (2), ..., Friday (6), Saturday(7) The script will trade on days that are present in this field. Please make sure that this field and also (1) Valid Trading Hours Between is checked

(1) Valid Trading Hours Between: false, 1800-2000 by default, hours between which the trades can happen. The time is always in the exchange's timezone

All other options are also disabled by default

PineConnector Automation:

Use PineConnector Automation: false by default, In order for the connection to MetaTrader to work, you will need do perform prerequisite steps, you can follow our full guide at our website, or refer to the official PineConnector Documentation. To set up PineConnector Automation on the TradingView side, you will need to do the following:

1. Fill out the License ID field with your PineConnector License ID;

2. Fill out the Risk (trading volume) with the desired volume to be traded in each trade (the meaning of this value depends on the EA settings in Metatrader. Follow the detailed guide for additional information);

3. After filling out the fields, you need to enable the 'Use PineConnector Automation' option (check the box in the strategy settings);

4. Check if the chart has updated and you can see the appropriate order comments on your chart;

5. Create an alert with the strategy selected as Condition, and the Message as {{strategy.order.comment}} (should be there by default);

6. Enable the Webhook URL in the Notifications section, set it as the official PineConnector webhook address and enjoy your connection with MetaTrader.

License ID: 60123456789 by default

Risk (trading volume): 1 by default

NOTE! Fine-tuning/re-optimization is highly recommended when using other asset/timeframe combinations.

Luxy Momentum, Trend, Bias and Breakout Indicators V7

TABLE OF CONTENTS

This is Version 7 (V7) - the latest and most optimized release. If you are using any older versions (V6, V5, V4, V3, etc.), it is highly recommended to replace them with V7.

Why This Indicator is Different

Who Should Use This

Core Components Overview

The UT Bot Trading System

Understanding the Market Bias Table

Candlestick Pattern Recognition

Visual Tools and Features

How to Use the Indicator

Performance and Optimization

FAQ

---

### CREDITS & ATTRIBUTION

This indicator implements proven trading concepts using entirely original code developed specifically for this project.

### CONCEPTUAL FOUNDATIONS

• UT Bot ATR Trailing System

- Original concept by @QuantNomad: (search "UT-Bot-Strategy"

- Our version is a complete reimplementation with significant enhancements:

- Volume-weighted momentum adjustment

- Composite stop loss from multiple S/R layers

- Multi-filter confirmation system (swing, %, 2-bar, ZLSMA)

- Full integration with multi-timeframe bias table

- Visual audit trail with freeze-on-touch

- NOTE: No code was copied - this is a complete reimplementation with enhancements.

• Standard Technical Indicators (Public Domain Formulas):

- Supertrend: ATR-based trend calculation with custom gradient fills

- MACD: Gerald Appel's formula with separation filters

- RSI: J. Welles Wilder's formula with pullback zone logic

- ADX/DMI: Custom trend strength formula inspired by Wilder's directional movement concept, reimplemented with volume weighting and efficiency metrics

- ZLSMA: Zero-lag formula enhanced with Hull MA and momentum prediction

### Custom Implementations

- Trend Strength: Inspired by Wilder's ADX concept but using volume-weighted pressure calculation and efficiency metrics (not traditional +DI/-DI smoothing)

- All code implementations are original

### ORIGINAL FEATURES (70%+ of codebase)

- Multi-Timeframe Bias Table with live updates

- Risk Management System (R-multiple TPs, freeze-on-touch)

- Opening Range Breakout tracker with session management

- Composite Stop Loss calculator using 6+ S/R layers

- Performance optimization system (caching, conditional calcs)

- VIX Fear Index integration

- Previous Day High/Low auto-detection

- Candlestick pattern recognition with interactive tooltips

- Smart label and visual management

- All UI/UX design and table architecture

### DEVELOPMENT PROCESS

**AI Assistance:** This indicator was developed over 2+ months with AI assistance (ChatGPT/Claude) used for:

- Writing Pine Script code based on design specifications

- Optimizing performance and fixing bugs

- Ensuring Pine Script v6 compliance

- Generating documentation

**Author's Role:** All trading concepts, system design, feature selection, integration logic, and strategic decisions are original work by the author. The AI was a coding tool, not the system designer.

**Transparency:** We believe in full disclosure - this project demonstrates how AI can be used as a powerful development tool while maintaining creative and strategic ownership.

---

1. WHY THIS INDICATOR IS DIFFERENT

Most traders use multiple separate indicators on their charts, leading to cluttered screens, conflicting signals, and analysis paralysis. The Suite solves this by integrating proven technical tools into a single, cohesive system.

Key Advantages:

All-in-One Design: Instead of loading 5-10 separate indicators, you get everything in one optimized script. This reduces chart clutter and improves TradingView performance.

Multi-Timeframe Bias Table: Unlike standard indicators that only show the current timeframe, the Bias Table aggregates trend signals across multiple timeframes simultaneously. See at a glance whether 1m, 5m, 15m, 1h are aligned bullish or bearish - no more switching between charts.

Smart Confirmations: The indicator doesn't just give signals - it shows you WHY. Every entry has multiple layers of confirmation (MA cross, MACD momentum, ADX strength, RSI pullback, volume, etc.) that you can toggle on/off.

Dynamic Stop Loss System: Instead of static ATR stops, the SL is calculated from multiple support/resistance layers: UT trailing line, Supertrend, VWAP, swing structure, and MA levels. This creates more intelligent, price-action-aware stops.

R-Multiple Take Profits: Built-in TP system calculates targets based on your initial risk (1R, 1.5R, 2R, 3R). Lines freeze when touched with visual checkmarks, giving you a clean audit trail of partial exits.

Educational Tooltips Everywhere: Every single input has detailed tooltips explaining what it does, typical values, and how it impacts trading. You're not guessing - you're learning as you configure.

Performance Optimized: Smart caching, conditional calculations, and modular design mean the indicator runs fast despite having 15+ features. Turn off what you don't use for even better performance.

No Repainting: All signals respect bar close. Alerts fire correctly. What you see in history is what you would have gotten in real-time.

What Makes It Unique:

Integrated UT Bot + Bias Table: No other indicator combines UT Bot's ATR trailing system with a live multi-timeframe dashboard. You get precision entries with macro trend context.

Candlestick Pattern Recognition with Interactive Tooltips: Patterns aren't just marked - hover over any emoji for a full explanation of what the pattern means and how to trade it.

Opening Range Breakout Tracker: Built-in ORB system for intraday traders with customizable session times and real-time status updates in the Bias Table.

Previous Day High/Low Auto-Detection: Automatically plots PDH/PDL on intraday charts with theme-aware colors. Updates daily without manual input.

Dynamic Row Labels in Bias Table: The table shows your actual settings (e.g., "EMA 10 > SMA 20") not generic labels. You know exactly what's being evaluated.

Modular Filter System: Instead of forcing a fixed methodology, the indicator lets you build your own strategy. Start with just UT Bot, add filters one at a time, test what works for your style.

---

2. WHO WHOULD USE THIS

Designed For:

Intermediate to Advanced Traders: You understand basic technical analysis (MAs, RSI, MACD) and want to combine multiple confirmations efficiently. This isn't a "one-click profit" system - it's a professional toolkit.

Multi-Timeframe Traders: If you trade one asset but check multiple timeframes for confirmation (e.g., enter on 5m after checking 15m and 1h alignment), the Bias Table will save you hours every week.

Trend Followers: The indicator excels at identifying and following trends using UT Bot, Supertrend, and MA systems. If you trade breakouts and pullbacks in trending markets, this is built for you.

Intraday and Swing Traders: Works equally well on 5m-1h charts (day trading) and 4h-D charts (swing trading). Scalpers can use it too with appropriate settings adjustments.

Discretionary Traders: This isn't a black-box system. You see all the components, understand the logic, and make final decisions. Perfect for traders who want tools, not automation.

Works Across All Markets:

Stocks (US, international)

Cryptocurrency (24/7 markets supported)

Forex pairs

Indices (SPY, QQQ, etc.)

Commodities

NOT Ideal For :

Complete Beginners: If you don't know what a moving average or RSI is, start with basics first. This indicator assumes foundational knowledge.

Algo Traders Seeking Black Box: This is discretionary. Signals require context and confirmation. Not suitable for blind automated execution.

Mean-Reversion Only Traders: The indicator is trend-following at its core. While VWAP bands support mean-reversion, the primary methodology is trend continuation.

---

3. CORE COMPONENTS OVERVIEW

The indicator combines these proven systems:

Trend Analysis:

Moving Averages: Four customizable MAs (Fast, Medium, Medium-Long, Long) with six types to choose from (EMA, SMA, WMA, VWMA, RMA, HMA). Mix and match for your style.

Supertrend: ATR-based trend indicator with unique gradient fill showing trend strength. One-sided ribbon visualization makes it easier to see momentum building or fading.

ZLSMA : Zero-lag linear-regression smoothed moving average. Reduces lag compared to traditional MAs while maintaining smooth curves.

Momentum & Filters:

MACD: Standard MACD with separation filter to avoid weak crossovers.

RSI: Pullback zone detection - only enter longs when RSI is in your defined "buy zone" and shorts in "sell zone".

ADX/DMI: Trend strength measurement with directional filter. Ensures you only trade when there's actual momentum.

Volume Filter: Relative volume confirmation - require above-average volume for entries.

Donchian Breakout: Optional channel breakout requirement.

Signal Systems:

UT Bot: The primary signal generator. ATR trailing stop that adapts to volatility and gives clear entry/exit points.

Base Signals: MA cross system with all the above filters applied. More conservative than UT Bot alone.

Market Bias Table: Multi-timeframe dashboard showing trend alignment across 7 timeframes plus macro bias (3-day, weekly, monthly, quarterly, VIX).

Candlestick Patterns: Six major reversal patterns auto-detected with interactive tooltips.

ORB Tracker: Opening range high/low with breakout status (intraday only).

PDH/PDL: Previous day levels plotted automatically on intraday charts.

VWAP + Bands : Session-anchored VWAP with up to three standard deviation band pairs.

---

4. THE UT BOT TRADING SYSTEM

The UT Bot is the heart of the indicator's signal generation. It's an advanced ATR trailing stop that adapts to market volatility.

Why UT Bot is Superior to Fixed Stops:

Traditional ATR stops use a fixed multiplier (e.g., "stop = entry - 2×ATR"). UT Bot is smarter:

It TRAILS the stop as price moves in your favor

It WIDENS during high volatility to avoid premature stops

It TIGHTENS during consolidation to lock in profits

It FLIPS when price breaks the trailing line, signaling reversals

Visual Elements You'll See:

Orange Trailing Line: The actual UT stop level that adapts bar-by-bar

Buy/Sell Labels: Aqua triangle (long) or orange triangle (short) when the line flips

ENTRY Line: Horizontal line at your entry price (optional, can be turned off)

Suggested Stop Loss: A composite SL calculated from multiple support/resistance layers:

- UT trailing line

- Supertrend level

- VWAP

- Swing structure (recent lows/highs)

- Long-term MA (200)

- ATR-based floor

Take Profit Lines: TP1, TP1.5, TP2, TP3 based on R-multiples. When price touches a TP, it's marked with a checkmark and the line freezes for audit trail purposes.

Status Messages: "SL Touched ❌" or "SL Frozen" when the trade leg completes.

How UT Bot Differs from Other ATR Systems:

Multiple Filters Available: You can require 2-bar confirmation, minimum % price change, swing structure alignment, or ZLSMA directional filter. Most UT implementations have none of these.

Smart SL Calculation: Instead of just using the UT line as your stop, the indicator suggests a better SL based on actual support/resistance. This prevents getting stopped out by wicks while keeping risk controlled.

Visual Audit Trail: All SL/TP lines freeze when touched with clear markers. You can review your trades weeks later and see exactly where entries, stops, and targets were.

Performance Options: "Draw UT visuals only on bar close" lets you reduce rendering load without affecting logic or alerts - critical for slower machines or 1m charts.

Trading Logic:

UT Bot flips direction (Buy or Sell signal appears)

Check Bias Table for multi-timeframe confirmation

Optional: Wait for Base signal or candlestick pattern

Enter at signal bar close or next bar open

Place stop at "Suggested Stop Loss" line

Scale out at TP levels (TP1, TP2, TP3)

Exit remaining position on opposite UT signal or stop hit

---

5. UNDERSTANDING THE MARKET BIAS TABLE

This is the indicator's unique multi-timeframe intelligence layer. Instead of looking at one chart at a time, the table aggregates signals across seven timeframes plus macro trend bias.

Why Multi-Timeframe Analysis Matters:

Professional traders check higher and lower timeframes for context:

Is the 1h uptrend aligning with my 5m entry?

Are all short-term timeframes bullish or just one?

Is the daily trend supportive or fighting me?

Doing this manually means opening multiple charts, checking each indicator, and making mental notes. The Bias Table does it automatically in one glance.

Table Structure:

Header Row:

On intraday charts: 1m, 5m, 15m, 30m, 1h, 2h, 4h (toggle which ones you want)

On daily+ charts: D, W, M (automatic)

Green dot next to title = live updating

Headline Rows - Macro Bias:

These show broad market direction over longer periods:

3 Day Bias: Trend over last 3 trading sessions (uses 1h data)

Weekly Bias: Trend over last 5 trading sessions (uses 4h data)

Monthly Bias: Trend over last 30 daily bars

Quarterly Bias: Trend over last 13 weekly bars

VIX Fear Index: Market regime based on VIX level - bullish when low, bearish when high

Opening Range Breakout: Status of price vs. session open range (intraday only)

These rows show text: "BULLISH", "BEARISH", or "NEUTRAL"

Indicator Rows - Technical Signals:

These evaluate your configured indicators across all active timeframes:

Fast MA > Medium MA (shows your actual MA settings, e.g., "EMA 10 > SMA 20")

Price > Long MA (e.g., "Price > SMA 200")

Price > VWAP

MACD > Signal

Supertrend (up/down/neutral)

ZLSMA Rising

RSI In Zone

ADX ≥ Minimum

These rows show emojis: GREEB (bullish), RED (bearish), GRAY/YELLOW (neutral/NA)

AVG Column:

Shows percentage of active timeframes that are bullish for that row. This is the KEY metric:

AVG > 70% = strong multi-timeframe bullish alignment

AVG 40-60% = mixed/choppy, no clear trend

AVG < 30% = strong multi-timeframe bearish alignment

How to Use the Table:

For a long trade:

Check AVG column - want to see > 60% ideally

Check headline bias rows - want to see BULLISH, not BEARISH

Check VIX row - bullish market regime preferred

Check ORB row (intraday) - want ABOVE for longs

Scan indicator rows - more green = better confirmation

For a short trade:

Check AVG column - want to see < 40% ideally

Check headline bias rows - want to see BEARISH, not BULLISH

Check VIX row - bearish market regime preferred

Check ORB row (intraday) - want BELOW for shorts

Scan indicator rows - more red = better confirmation

When AVG is 40-60%:

Market is choppy, mixed signals. Either stay out or reduce position size significantly. These are low-probability environments.

Unique Features:

Dynamic Labels: Row names show your actual settings (e.g., "EMA 10 > SMA 20" not generic "Fast > Slow"). You know exactly what's being evaluated.

Customizable Rows: Turn off rows you don't care about. Only show what matters to your strategy.

Customizable Timeframes: On intraday charts, disable 1m or 4h if you don't trade them. Reduces calculation load by 20-40%.

Automatic HTF Handling: On Daily/Weekly/Monthly charts, the table automatically switches to D/W/M columns. No configuration needed.

Performance Smart: "Hide BIAS table on 1D or above" option completely skips all table calculations on higher timeframes if you only trade intraday.

---

6. CANDLESTICK PATTERN RECOGNITION

The indicator automatically detects six major reversal patterns and marks them with emojis at the relevant bars.

Why These Six Patterns:

These are the most statistically significant reversal patterns according to trading literature:

High win rate when appearing at support/resistance

Clear visual structure (not subjective)

Work across all timeframes and assets

Studied extensively by institutions

The Patterns:

Bullish Patterns (appear at bottoms):

Bullish Engulfing: Green candle completely engulfs prior red candle's body. Strong reversal signal.

Hammer: Small body with long lower wick (at least 2× body size). Shows rejection of lower prices by buyers.

Morning Star: Three-candle pattern (large red → small indecision → large green). Very strong bottom reversal.

Bearish Patterns (appear at tops):

Bearish Engulfing: Red candle completely engulfs prior green candle's body. Strong reversal signal.

Shooting Star: Small body with long upper wick (at least 2× body size). Shows rejection of higher prices by sellers.

Evening Star: Three-candle pattern (large green → small indecision → large red). Very strong top reversal.

Interactive Tooltips:

Unlike most pattern indicators that just draw shapes, this one is educational:

Hover your mouse over any pattern emoji

A tooltip appears explaining: what the pattern is, what it means, when it's most reliable, and how to trade it

No need to memorize - learn as you trade

Noise Filter:

"Min candle body % to filter noise" setting prevents false signals:

Patterns require minimum body size relative to price

Filters out tiny candles that don't represent real buying/selling pressure

Adjust based on asset volatility (higher % for crypto, lower for low-volatility stocks)

How to Trade Patterns:

Patterns are NOT standalone entry signals. Use them as:

Confirmation: UT Bot gives signal + pattern appears = stronger entry

Reversal Warning: In a trade, opposite pattern appears = consider tightening stop or taking profit

Support/Resistance Validation: Pattern at key level (PDH, VWAP, MA 200) = level is being respected

Best combined with:

UT Bot or Base signal in same direction

Bias Table alignment (AVG > 60% or < 40%)

Appearance at obvious support/resistance

---

7. VISUAL TOOLS AND FEATURES

VWAP (Volume Weighted Average Price):

Session-anchored VWAP with standard deviation bands. Shows institutional "fair value" for the trading session.

Anchor Options: Session, Day, Week, Month, Quarter, Year. Choose based on your trading timeframe.