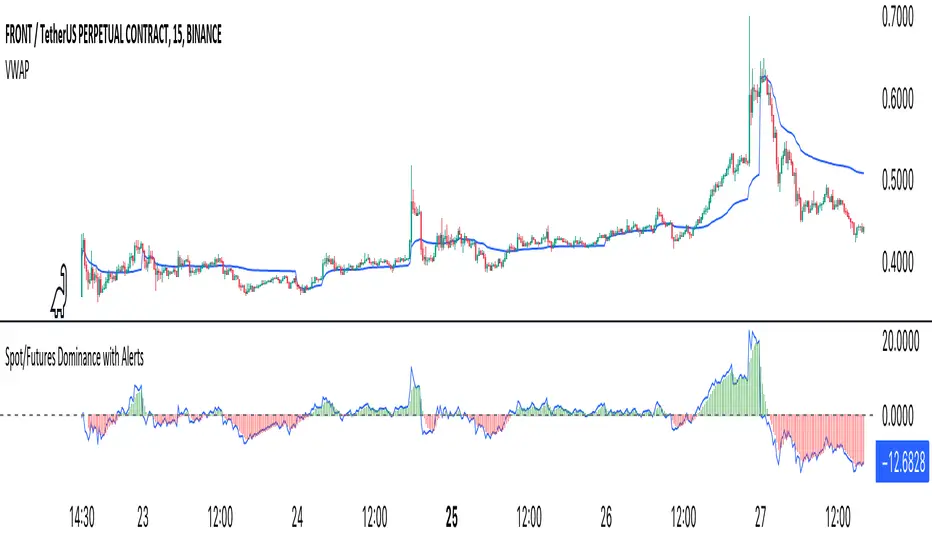

Crypto Spot/Futures Dominance Indicator with AlertsFutures/Spot Dominance Indicator:

Overview:

The futures/spot dominance indicator is a versatile tool used by traders and analysts to assess the relative strength or dominance of the futures market in relation to the spot (or cash) market for a specific asset. It offers insights into market sentiment, potential arbitrage opportunities, and risk management while incorporating the VWAP indicator for added context.

How It Works:

This indicator automatically detects and adapts to the futures symbol applied to the chart, simplifying the setup for traders. However, it still necessitates manual input of the corresponding spot pair to ensure accuracy.

Automatic Futures Symbol Detection: The indicator starts by automatically detecting the futures symbol on the trading chart, eliminating the need for manual configuration. This ensures that the indicator is applied to the correct futures contract.

Manual Spot Pair Entry: To provide a reliable reference point for the comparison, traders must manually input the corresponding spot symbol via the indicator's inputs. For instance, if the indicator detects the BTCUSDT.P futures symbol, traders would manually enter the BTCUSDT spot symbol.

Gathering Data: The indicator collects historical price data for both the detected futures contract and the manually specified spot symbol. This data includes open, high, low, and close prices, as well as trading volume.

VWAP Calculation: To gain a deeper understanding of price trends and market dynamics, the indicator calculates the VWAP (Volume Weighted Average Price) for both the futures and spot markets. The VWAP places more weight on prices with higher trading volume, offering a weighted average that reflects market consensus.

Premium/Discount Calculation: By subtracting the VWAP of the spot market from the VWAP of the futures market, the indicator quantifies the premium or discount of the futures price concerning the spot price. A positive value indicates a premium, while a negative value suggests a discount.

Plotting: The premium/discount value is displayed as a line on the chart, often alongside moving averages or other smoothing techniques for improved trend analysis.

Alerts: In addition to its analysis capabilities, this indicator now includes alerts to enhance your trading experience. It alerts you in the following scenarios:

Premium Above Average: Notifies you when the premium crosses above the average line.

Premium Below Average: Alerts you when the premium crosses below the average line.

Premium Above Zero: Provides an alert when the premium crosses above the zero line.

Premium Below Zero: Generates an alert when the premium crosses below the zero line.

Benefits of the Futures/Spot Dominance Indicator:

Sentiment Analysis: Traders use the indicator to assess market sentiment. A futures premium might signify bullish sentiment, while a discount could indicate bearish sentiment.

Arbitrage Opportunities: Identifying price discrepancies between futures and spot markets can help traders spot arbitrage opportunities, where they can profit from price differentials.

Risk Management: The indicator assists in evaluating risks associated with futures positions, helping traders manage their exposure effectively.

Trend Confirmation: When used in conjunction with other technical indicators, futures/spot dominance, along with VWAP, can provide additional confirmation of price trends.

Hedging: Investors and corporations use this tool to gauge the effectiveness of hedging strategies based on futures contracts.

Speculative Trading: Traders and investors use the indicator to inform speculative positions, aligning their trades with perceived market strength or weakness.

Insightful Analysis: Futures/spot dominance analysis, enriched by VWAP data, offers insights into market behavior during specific events or changes in economic conditions.

In summary, the futures/spot dominance indicator, with its integration of VWAP and automatic futures symbol detection, provides traders and investors with a comprehensive tool to assess market dynamics. It aids in sentiment analysis, risk management, and trend confirmation while offering potential arbitrage opportunities. The newly added alerts enhance the indicator's functionality, providing timely notifications of key market events. However, it relies on manual input of the corresponding spot pair to ensure precise comparisons between futures and spot markets. It should be used alongside other analysis techniques for a well-rounded view of the market.

Cari dalam skrip untuk "vwap"

VWAP y Standar DeviationThis script presents the real VWAP (Yellow line), in 50 period VWAP (Blue Line) and the 120 period VWAP (Red Line). Additionally, it presents the values of 1 and 1,618 standard deviations of the VWAP of 50 periods.

This confirmation allows to visualize the behavior of the price in realicon to the VWAP key indicator that represents the midpoint of the operating volumes in a period.

This script evaluates the deviation of the price in relation to the average of the volume traded in the different periods.

The indicator settings allow changing the length of the VWAP for custom settings. Standard deviations are determined based on VWAP 2. VWAP 1 is a reference for determining the global trend of movement in the established period.

The upper and lower limits of the representative Standard Deviation of 1.618 (Fibonacci Number) are used as confirmation of continuation of a trend once crossed by the price.

During the ranges the 1.618 limits of the Dev. Standard are used as entry and exit points of the operation (For this it is necessary to adjust the VWAP 2 to the studied temporality and the operated asset)

VWAP Pro v6 (Color + Bands)AI helped me code VWAP

When price goes above VWAP line, VWAP line will turn green to indicate buyers are in control.

When price goes below VWAP line, VWAP line will turn red to indicate sellers are in control.

VWAP line stays blue when price is considered fair value.

VWAP with period (rajib127)VWAP with Adjustable Period (rajib127)

This advanced VWAP (Volume Weighted Average Price) indicator offers enhanced functionality with customizable anchor periods and multiple standard deviation bands.

Key Features:

Adjustable Anchor Period: Unlike standard VWAP that resets daily, this indicator allows you to set custom anchor timeframes (Daily, Weekly, Monthly) to match your trading strategy

Multiple Deviation Bands: Display up to 3 sets of bands with customizable multipliers for better support/resistance identification

Dual Calculation Modes: Choose between Standard Deviation or Percentage-based band calculations

Flexible Price Sources: Select from 7 different price calculation methods (Typical, Close, High, Low, Median, Weighted, Open)

Timeframe Visibility Control: Option to hide VWAP on higher timeframes (Daily and above) for cleaner charts

Visual Enhancements: Color-coded bands with fill areas and real-time value display table

Trading Applications:

Identify dynamic support and resistance levels

Spot mean reversion opportunities when price deviates from bands

Use different anchor periods for swing trading vs day trading strategies

Combine with other indicators for confluence-based entries

Unique Advantage:

The ability to adjust the VWAP reset period makes this indicator versatile for various trading styles - from intraday scalping with hourly resets to swing trading with weekly anchors.

Perfect for traders who want more control over their VWAP analysis beyond the standard daily reset limitation.

SwingTrade ADX Strategy v6This is a swing trading strategy that combines VWAP (Volume Weighted Average Price), ADX (Average Directional Index) for trend strength, and volume ratios to generate long/short entry and exit signals. It's designed for daily charts but can be adapted.

#### Key Features:

- **Entries**: Based on VWAP crossovers, rising/falling delta (price deviation from VWAP), ADX trend confirmation, and volume ratios.

- **Exits**: Dynamic exits when VWAP delta reverses after a peak.

- **Filters**: Optional toggles for VWAP signals, ADX, and volume. Backtest date range for custom periods.

- **Visuals**: VWAP line, signal shapes/labels, and an info panel showing key metrics (VWAP Delta %, ADX, Volume Ratio).

- **Alerts**: Built-in alerts for buy/sell entries and exits.

#### How to Use:

1. Apply to your chart (e.g., stocks, forex, crypto).

2. Adjust parameters in the settings (e.g., ADX threshold, volume period).

3. Enable/disable indicators as needed.

4. Backtest using the date filters and review equity curve.

**Disclaimer**: This is for educational purposes only. Past performance is not indicative of future results. Not financial advice—trade at your own risk. Backtest thoroughly and use with proper risk management.

Feedback welcome! If you find it useful, give it a like.

Volume Zones IndicatorVolume Zones Indicator — VWAP with Dynamic Monthly Volume Zones

This indicator is an enhanced version of the classic VWAP (Volume Weighted Average Price), designed to create clear monthly zones around VWAP based on average price range (ATR) and volume activity.

The core idea is to highlight key zones where price is more likely to reverse or consolidate, based on where significant trading volume occurs.

How does it work?

VWAP is calculated over the last N days (set by the lookbackPeriod input).

Four zones are plotted above and below VWAP, spaced using a multiple of ATR.

Each zone has its own color for clarity:

Blue — closest to VWAP

Red — second band

Green — third band

Orange — outer band (potential breakout or exhaustion zone)

If the current volume exceeds the moving average of volume, it is highlighted directly on the chart. This helps detect accumulation or distribution moments more easily.

What does the trader see?

You see horizontal colored bands on the chart that update at the start of each new month. These zones:

Remain fixed throughout the month

Automatically adjust based on recent volume and volatility

Act as dynamic support/resistance levels

Best used for:

Mean reversion strategies — identifying pullbacks toward value areas

Support and resistance mapping — automatic SR zones based on price/volume behavior

Breakout filtering — when price reaches zone 3 or 4, trend continuation or reversal is likely

Adding volume context to price action — works well with candlestick and pattern analysis

Settings

Lookback Period (Days): VWAP and volume smoothing length

Volume Area Threshold %: Reserved for future functionality

Works on any timeframe; best suited for 4H timeframe.

Zones are calculated and fixed monthly for clean visual context

Combines price structure with actual volume flow for more reliable decision-making

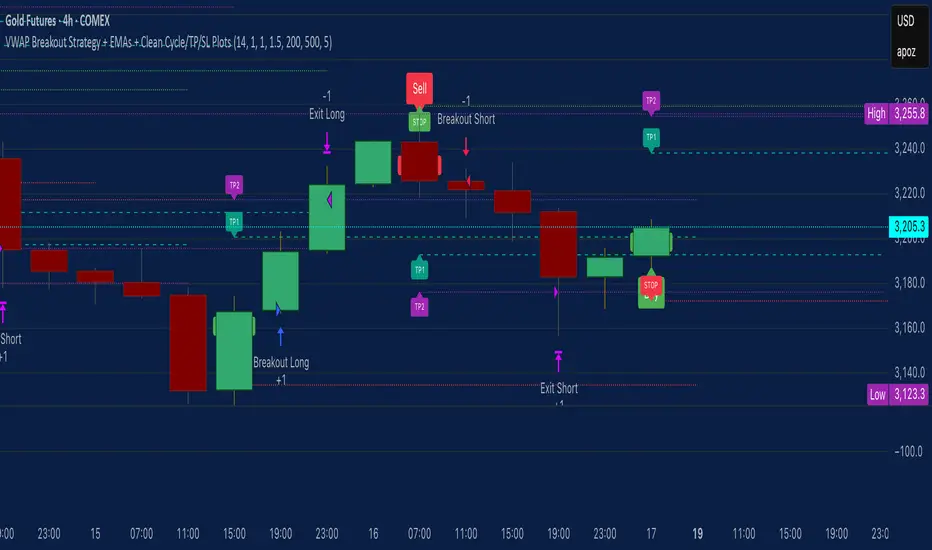

VWAP Breakout Strategy + EMAs + Clean Cycle/TP/SL PlotsHere’s a quick user-guide to get you up and running with your “VWAP Breakout Strategy + EMAs + Clean Cycle/TP/SL Plots” script in TradingView:

⸻

1. Installing the Script

1. Open TradingView, go to Pine Editor (bottom panel).

2. Paste in your full Pine-v6 code and hit Add to chart.

3. Save it (“Save as…”): give it a memorable name (e.g. “VWAP Breakout+EMAs”).

⸻

2. Configuring Your Inputs

Once it’s on the chart, click the ⚙️ Settings icon to tune:

Setting Default What it does

ATR Length 14 Period for average true range (volatility measure)

ATR Multiplier for Stop 1.5 How many ATRs away your stop-loss sits

TP1 / TP2 Multipliers (ATR) 1.0 / 2.0 Distance of TP1 and TP2 in ATR multiples

Show VWAP / EMAs On Toggles the blue VWAP line & EMAs (100/34/5)

Full Cycle Range Points 200 Height of the shaded “cycle zone”

Pivot Lookback 5 How many bars back to detect a pivot low

Round Number Step 500 Spacing of your dotted horizontal lines

Show TP/SL Labels On Toggles all the “ENTRY”, “TP1”, “TP2”, “STOP” tags

Feel free to adjust ATR multipliers and cycle-zone size based on the instrument’s typical range.

⸻

3. Reading the Signals

• Long Entry:

• Trigger: price crosses above VWAP

• You’ll see a green “Buy” tag at the low of the signal bar, plus an “ENTRY (Long)” label at the close.

• Stop is plotted as a red dashed line below (ATR × 1.5), and TP1/TP2 as teal and purple lines above.

• Short Entry:

• Trigger: price crosses below VWAP

• A red “Sell” tag appears at the high, with “ENTRY (Short)” at the close.

• Stop is the green line above; TP1/TP2 are dashed teal/purple lines below.

⸻

4. Full Cycle Zone

Whenever a new pivot low is detected (using your Pivot Lookback), the script deletes the old box and draws a shaded yellow rectangle from that low up by “Full Cycle Range Points.”

• Use this to visualize the “maximum expected swing” from your pivot.

• You can quickly see whether price is still traveling within a normal cycle or has overstretched.

⸻

5. Round-Number Levels

With Show Round Number Levels enabled, you’ll always get horizontal dotted lines at the nearest multiples of your “Round Number Step” (e.g. every 500 points).

• These often act as psychological support/resistance.

• Handy to see confluence with VWAP or cycle-zone edges.

⸻

6. Tips & Best-Practices

• Timeframes: Apply on any intraday chart (5 min, 15 min, H1…), but match your ATR length & cycle-points to the timeframe’s typical range.

• Backtest first: Use the Strategy Tester tab to review performance, tweak ATR multipliers or cycle size, then optimize.

• Combine with context: Don’t trade VWAP breakouts blindly—look for confluence (e.g. support/resistance zones, higher-timeframe trend).

• Label clutter: If too many labels build up, you can toggle Show TP/SL Labels off and rely just on the lines.

⸻

That’s it! Once you’ve added it to your chart and dialed in the inputs, your entries, exits, cycle ranges, and key levels will all be plotted automatically. Feel free to experiment with the ATR multipliers and cycle-zone size until it fits your instrument’s personality. Happy trading!

VWAP Predictive Breakout + RSI + OB + Trend/Chop📈 VWAP Predictive Breakout + RSI + Order Blocks + Trend/Chop Filter

This multi-layered day trading and scalping tool is designed to predict price direction after a VWAP breakout, rather than react to it. It combines volume, RSI, candlestick structure, order blocks, and trend/chop analysis to improve the accuracy of intraday signals.

🔍 Core Features

VWAP Predictive Breakout

Signals are generated when price breaks above/below VWAP with strength (volume spike + strong candle body), supported by trend confirmation.

RSI Momentum Filter

Uses RSI divergence behavior to validate breakouts, filtering out weak or exhausted moves.

Order Block Detection

Marks bullish and bearish engulfing patterns and checks for proximity to these zones as confirmation for breakouts.

Trend vs Chop Detection

Uses ADX, ATR, EMA distance, Bollinger Band width, and candlestick cleanliness to dynamically identify whether the market is trending or choppy.

Clean Candle Behavior

Filters out noisy or indecisive candles by analyzing wick-to-body ratio and ATR-based body size.

📌 Visual Markers

🟢 Buy Signal: Green triangle below bar

🔴 Sell Signal: Red triangle above bar

🟢⚪ Bullish Order Block: Green circle

🔴⚪ Bearish Order Block: Red circle

🟩 Trending Background: Light green

🟥 Choppy Background: Light red

🛎 Alerts Included

Long signal: VWAP breakout + RSI + Order Block + Clean Candle

Short signal: VWAP breakdown + RSI + Order Block + Clean Candle

🧠 Best Use Cases

Scalping high-probability VWAP reversals or continuations

Day trading in markets where trend clarity is critical

Filtering noise in sideways conditions using real-time chop detection

VWAP Double Touch Alert (Timeframe-Aware)📌 VWAP Double Touch Alert — Smart Re-entry Signal for Precision Traders

Take your VWAP trading to the next level with this intelligent indicator that filters out the noise and zeroes in on high-probability re-entry setups.

💡 How it works:

This script tracks every time price touches the VWAP line and alerts you when it happens twice within a defined window of time (adjustable per your timeframe). This is often a sign of smart money accumulation, potential reversals, or explosive breakouts.

🔍 Why Traders Love It:

✅ Filters out weak signals — only alerts on confirmed double touches

✅ Fully adjustable VWAP zone sensitivity

✅ Selectable timeframe profiles or custom window (1m, 5m, 15m, 30m, etc.)

✅ Clean visual cues with minimal chart clutter

✅ Perfect for scalping, intraday reversals, or VWAP mean-reversion strategies

⚙️ Customization:

VWAP zone width (in %)

Time window in bars or automatic based on timeframe

Custom alert messages

Alert only triggers once per double-touch event to avoid spamming

🎯 Best For:

Crypto scalpers & day traders

VWAP bounce and mean-reversion traders

Traders who want clean, conclusive entry alerts without lag

TLC sessionA Professional Intraday Session Tracker with VWAP and Economic Event Integration

Description

This indicator provides visual tracking of major trading sessions (Asian, London, New York) combined with VWAP calculations and macroeconomic event zones. It's designed for intraday traders who need to monitor session overlaps, liquidity periods, and high-impact news events.

The basic script of trading sessions was taken as a basis and refined for greater convenience.

Key Features:

Customizable Session Tracking: Visualize up to 3 trading sessions with adjustable time zones (supports IANA & GMT formats)

Dynamic VWAP Integration: Built-in Volume-Weighted Average Price calculation

Macro Event Zones: Highlights key economic announcement windows (adjustable for summer/winter time)

Price Action Visualization: Displays open/close prices, session ranges, and average price levels

Automatic DST Adjustment: Uses IANA timezone database for daylight savings awareness

How It Works

1. Trading Session Detection

Three fully configurable sessions (e.g., Asia, London, New York)

Each session displays:

Colored background zone

Opening price (dashed line)

Closing price (dashed line)

Average price (dotted line)

Optional label with session name

2. VWAP Calculation

Standard Volume-Weighted Average Price plotted as circled line

Helps identify fair value within each session

3. Macro Event Zones

Special highlighted period for economic news releases

Automatically adjusts for summer/winter time

Default set to 1000-1200 (summer) or 0900-1100 (winter) GMT-5 (US session open)

Why This Indicator is Unique

Multi-Session Awareness

Unlike simple session indicators, this tool:

Tracks price development within each session

Shows session overlaps (critical for volatility periods)

Maintains separate VWAP calculations across sessions

Professional-Grade Features

IANA timezone support (automatic DST handling)

Customizable visual elements (toggle labels, ranges, averages)

Object-based architecture (clean, efficient rendering)

News event integration (helps avoid trading during high-impact releases)

Usage Recommendations

Best Timeframes

1-minute to 1-hour charts (intraday focus)

Not recommended for daily+ timeframes

Trading Applications

1. Session Breakout Strategy: Trade breakouts when London/New York sessions open

2. VWAP Reversion: Fade moves that deviate too far from VWAP

3. News Avoidance: Reduce position sizing during macro event windows

Visual Example

Asian session (red)

London session (blue)

New York session (purple)

Macro event zone (white)

VWAP line (gold circles)

The basic script of trading sessions was taken as a basis and refined for greater convenience.

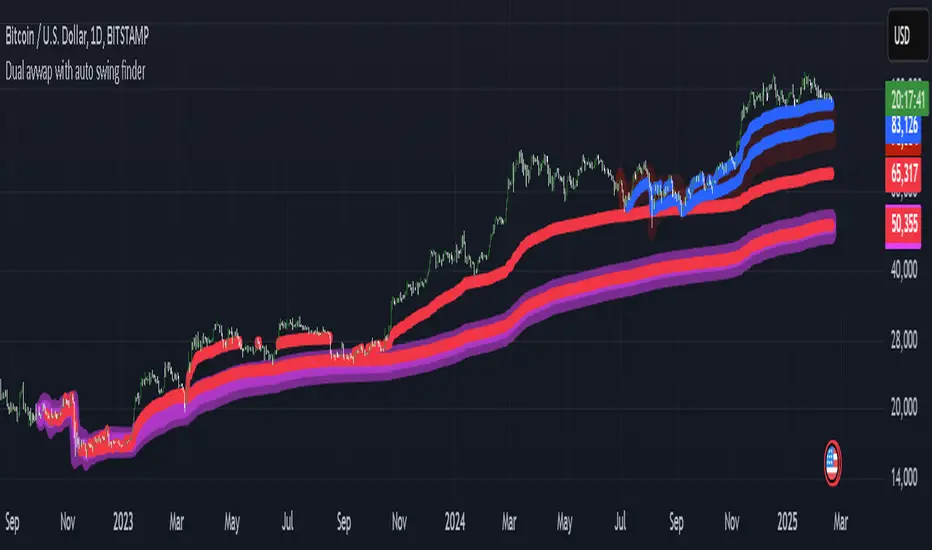

My auto dual avwap with Auto swing low/pivot low finderWelcome to My Auto Dual AVWAP with Auto Swing Low/Pivot Low Finder – an open-source TradingView indicator designed to enhance your technical analysis toolbox. This indicator is published under the Mozilla Public License 2.0 and is available for anyone to study, modify, and distribute.

Key Features

Auto Pivot/Swing Low Finder:

In addition to VWAP lines, the indicator incorporates an automatic detection mechanism for swing lows/pivot lows. This feature assists in identifying potential support areas and price reversals, further enhancing your trading strategy.

Dual VWAP Calculation with high/low range:

The indicator calculates two separate volume-weighted average price (VWAP) lines based on different price inputs (low and high prices) and defined time sessions. This allows traders to gain a more nuanced view of market activity during specific trading periods.

Customizable Time Sessions:

You can specify distinct start and end times for each VWAP calculation session. This flexibility helps you align the indicator with your preferred trading hours or market sessions, making it adaptable to various time zones and trading styles.

Easy to Customize:

With clear code structure and detailed comments, the script is designed to be accessible even for traders who want to customize or extend its functionality. Whether you're a seasoned coder or just starting out, the code is written with transparency in mind.

How It Works

Session Initialization:

The script sets up two distinct time sessions using user-defined start and end times. For each session, it detects the beginning of the trading period to reset cumulative values.

Cumulative Calculations:

During each session, the indicator accumulates the product of price and volume as well as the total volume. The VWAP is then computed as the ratio of these cumulative values.

Dual Data Sources:

Two separate data inputs (using low and high prices) are used to calculate two VWAP lines. This dual approach provides a broader perspective on market trends and can help in identifying dynamic support and resistance levels.

Visualization:

The calculated VWAP lines are plotted directly on your chart with distinct colors and thickness settings for easy visualization. This makes it simple to interpret the data at a glance.

Why Use This Indicator?

Whether you are a day trader, swing trader, or simply looking to refine your market analysis, My Auto Dual AVWAP with Auto Swing Low/Pivot Low Finder offers a robust set of features that can help you identify key price levels and improve your decision-making process. Its open-source nature invites collaboration and customization, ensuring that you can tailor it to fit your unique trading style.

Feel free to explore, modify, and share this indicator. Happy trading!

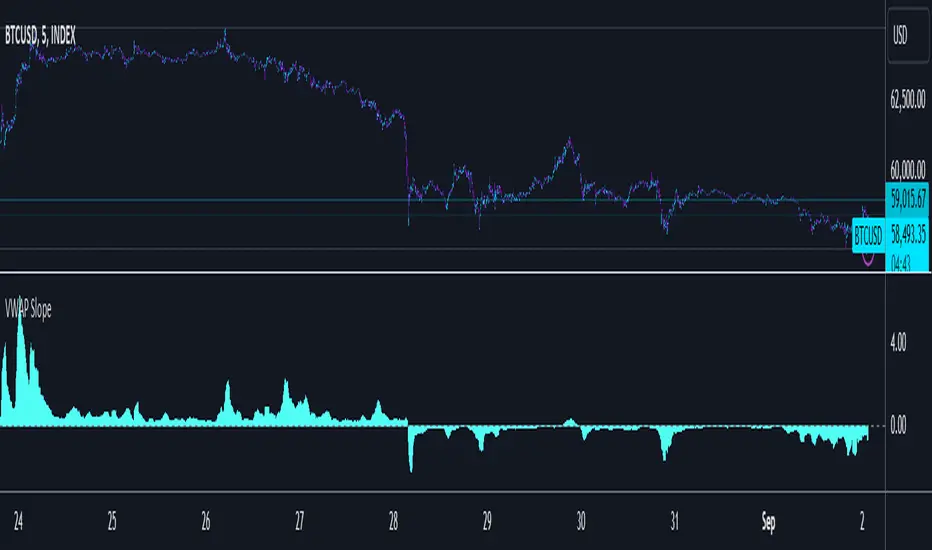

VWAP SlopeThis script calculates and displays the slope of the Volume Weighted Average Price (VWAP) . It compares the current VWAP with its value from a user-defined lookback period to determine the slope. The slope is color-coded: green for an upward trend (positive slope) and red for a downward trend (negative slope) .

Key Points:

VWAP Calculation: The script calculates the VWAP based on a user-defined timeframe (default: daily), which represents the average price weighted by volume.

Slope Determination: The slope is calculated by comparing the current VWAP to its value from a previous period, providing insight into market trends.

Color-Coding: The slope line is color-coded to visually indicate the market direction: green for uptrend and red for downtrend.

This script helps traders identify the direction of the market based on VWAP , offering a clear view of trends and potential turning points.

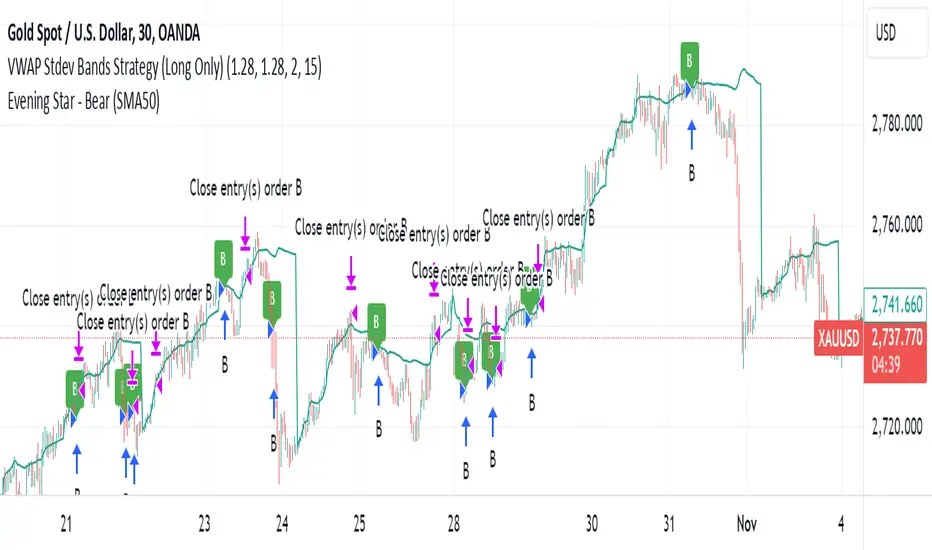

VWAP Stdev Bands Strategy (Long Only)The VWAP Stdev Bands Strategy (Long Only) is designed to identify potential long entry points in trending markets by utilizing the Volume Weighted Average Price (VWAP) and standard deviation bands. This strategy focuses on capturing upward price movements, leveraging statistical measures to determine optimal buy conditions.

Key Features:

VWAP Calculation: The strategy calculates the VWAP, which represents the average price a security has traded at throughout the day, weighted by volume. This is an essential indicator for determining the overall market trend.

Standard Deviation Bands: Two bands are created above and below the VWAP, calculated using specified standard deviations. These bands act as dynamic support and resistance levels, providing insight into price volatility and potential reversal points.

Trading Logic:

Long Entry Condition: A long position is triggered when the price crosses below the lower standard deviation band and then closes above it, signaling a potential price reversal to the upside.

Profit Target: The strategy allows users to set a predefined profit target, closing the long position once the specified target is reached.

Time Gap Between Orders: A customizable time gap can be specified to prevent multiple orders from being placed in quick succession, allowing for a more controlled trading approach.

Visualization: The VWAP and standard deviation bands are plotted on the chart with distinct colors, enabling traders to visually assess market conditions. The strategy also provides optional plotting of the previous day's VWAP for added context.

Use Cases:

Ideal for traders looking to engage in long-only positions within trending markets.

Suitable for intraday trading strategies or longer-term approaches based on market volatility.

Customization Options:

Users can adjust the standard deviation values, profit target, and time gap to tailor the strategy to their specific trading style and market conditions.

Note: As with any trading strategy, it is important to conduct thorough backtesting and analysis before live trading. Market conditions can change, and past performance does not guarantee future results.

Derivative Oscillator Cu [ID: AC-P]The "AC-P" version of the Derivative Oscillator is my personal customized version of Constance Brown's Derivative Oscillator (using Everget's implementation of it as the base), with the the following modifications and additions:

VWAP Indication - option to show whether the price input option is above or below the Daily VWAP (red triangles = price input is below vwap, green triangles = price input is above vwap)

Bullish and Bearish phases from shayankm's Waddah Attar Explosion V2 () is included as indication dots (bullish = blue dots, bearish = yellow dots) below/above the Derivative Oscillator histogram

Coral Trend from Lazybear () is included as indication dots (red/green dots below/above the Derivative Oscillator histogram

Input source options for vwap, Waddah components (MACD, Bollinger Upper/Lower)

Centerline option for Coral trend, and Horizontal center option for the Derivative Oscillator with circle indication (optional - provided as option for flexibility in use with overlaying with other indicators)

This indicator is a hybrid, with a combination of leading indicators and lagging trending indicators combined into one. Specifically, a few of the other indicators I use are lacking in the momentum and trend department, and this is one of the indicators I use to address that:

VWAP provides trend information on lower timeframes from a high timeframe interval (D)

Coral Trend provides additional confirmation to VWAP trend wise, and is adjustable

Waddah Attar Explosion provides a third level of confirmation for trending moves, taking into account shorter and longer timeframes (FastEMA and SlowEMA parameters).

Script base for the Derivative Oscillator is credited to Everget () and LazyBear ().

Source attribution to Constance Brown for the Derivative Oscillator formula/indicator:

// Brown, Constance.

// Reference 1: “The Derivative Oscillator: a New Approach to an Old Problem,” Journal of Technical Analysis (Winter-Spring 1994) 45–61.

// Reference 2: Technical Analysis for the Trading Professional. New York, NY: McGraw-Hill, 1999.

Information on the Derivative Oscillator:

www.investopedia.com

MNQ TopStep 50K | Ultra Quality v3.0MNQ TopStep 50K | Ultra Quality v3.0 - Publish Summary📊 OverviewA professional-grade trading indicator designed specifically for MNQ futures traders using TopStep funded accounts. Combines 7 technical confirmations with 5 advanced safety filters to deliver high-quality trade signals while managing drawdown risk.🎯 Key FeaturesCore Signal System

7-Point Confirmation: VWAP, EMA crossovers, 15-min HTF trend, MACD, RSI, ADX, and Volume

Signal Grading: Each signal is rated A+ through D based on 7 quality factors

Quality Threshold: Adjustable minimum grade requirement (A+, A, B, C, D)

Advanced Safety Filters (Customizable)

Mean Reversion Filter - Prevents chasing extended moves beyond VWAP bands

ATR Spike Filter - Avoids trading during extreme volatility events

EMA Spacing Filter - Ensures proper trend separation (optional)

Momentum Filter - Requires consecutive directional bars (optional)

Multi-Timeframe Confirmation - Aligns with 15-min trend (optional)

TopStep Risk Management

Real-time drawdown tracking

Position sizing calculator based on remaining cushion

Daily loss limit monitoring

Consecutive loss protection

Max trades per day limiter

Visual Components

VWAP with 1σ, 2σ, 3σ bands

EMA 9/21 with cloud fill

15-min EMA 50 for HTF trend

Comprehensive metrics dashboard

Risk management panel

Filter status panel

Detailed trade labels with entry, stops, and targets

⚙️ Default Settings (Balanced for Regular Signals)Technical Indicators

Fast EMA: 9 | Slow EMA: 21 | HTF EMA: 50 (15-min)

MACD: 10/22/9

RSI: 14 period | Thresholds: 52 (buy) / 48 (sell)

ADX: 14 period | Minimum: 20

ATR: 14 period | Stop: 2x | TP1: 2x | TP2: 3x

Volume: 1.2x average required

Session Settings

Default: 9:30 AM - 11:30 AM ET (adjustable)

Avoids first 15 minutes after market open

Customizable trading hours

Safety Filters (Default Configuration)

✅ Mean Reversion: Enabled (2.5σ max from VWAP)

✅ ATR Spike: Enabled (2.0x threshold)

❌ EMA Spacing: Disabled (can enable for quality)

❌ Momentum: Disabled (can enable for quality)

❌ MTF Confirmation: Disabled (can enable for quality)

Risk Controls

Minimum Signal Quality: C (adjustable to A+ for fewer/better signals)

Min Bars Between Signals: 10

Max Trades Per Day: 5

Stop After Consecutive Losses: 2

📈 Expected PerformanceWith Default Settings:

Signals per week: 10-15 trades

Estimated win rate: 55-60%

Risk-Reward: 1:2 (TP1) and 1:3 (TP2)

With Aggressive Settings (Min Quality = D, All Filters Off):

Signals per week: 20-25 trades

Estimated win rate: 50-55%

With Conservative Settings (Min Quality = A, All Filters On):

Signals per week: 3-5 trades

Estimated win rate: 65-70%

🚀 How to UseBasic Setup:

Add indicator to MNQ 5-minute chart

Adjust TopStep account settings in inputs

Set your risk per trade percentage (default: 0.5%)

Configure trading session hours

Set minimum signal quality (Start with C for balanced results)

Signal Interpretation:

Green Triangle (BUY): Long signal - all confirmations aligned

Red Triangle (SELL): Short signal - all confirmations aligned

Label Details: Shows entry, stop loss, take profit levels, position size, and signal grade

Signal Grade: A+ = Elite (6-7 points) | A = Strong (5) | B = Good (4) | C = Fair (3)

Dashboard Monitoring:

Top Right: Technical metrics and market conditions

Top Left: Filter status (which filters are passing/blocking)

Bottom Right: TopStep risk metrics and position sizing

⚡ Customization TipsFor More Signals:

Lower "Minimum Signal Quality" to D

Decrease ADX threshold to 18-20

Lower RSI thresholds to 50/50

Reduce Volume multiplier to 1.1x

Disable additional filters

For Higher Quality (Fewer Signals):

Raise "Minimum Signal Quality" to A or A+

Increase ADX threshold to 25-30

Enable all 5 advanced filters

Tighten VWAP distance to 2.0σ

Increase momentum requirement to 3-4 bars

For TopStep Compliance:

Adjust "Max Total Drawdown" and "Daily Loss Limit" to match your account

Update "Already Used Drawdown" daily

Monitor the Risk Panel for cushion remaining

Use recommended contract sizing

🛡️ Risk DisclaimerIMPORTANT: This indicator is for educational and informational purposes only.

Past performance does not guarantee future results

All trading involves substantial risk of loss

Use proper risk management and position sizing

Test thoroughly in paper trading before live use

The indicator does not guarantee profitable trades

Adjust settings based on your risk tolerance and trading style

Always comply with your broker's and TopStep's rules

TCLC - Multi TimeFrame VWAPVWAP :

VWAP, or Volume Weighted Average Price, is a trading indicator that represents the average price of a security over a specific period, weighted by the volume of trades at each price level. It is calculated by taking the sum of the product of price and volume and dividing it by the total volume for the period. Essentially, VWAP shows the average price at which most trades occurred, giving more weight to prices with higher trading volumes.

The Indicator Plots the VWAP in Daily, WEEKLY , MONTHLY , YEARLY which helps to gauage the trend where the Volume vs Price exists....

VWAP Filtrado con TendenciaThis indicator combines the classic VWAP with a trend EMA filtered by the TDFI oscillator to confirm market direction.

- VWAP is displayed in white as the fair value reference.

- The trend EMA dynamically changes color according to market condition: green (uptrend), red (downtrend), orange (range).

- Candles highlight in blue when a bullish VWAP crossover is confirmed, and in fuchsia when a bearish crossover is confirmed.

- Includes adjustable thresholds and a cooldown filter to reduce noise and improve reliability.

This approach allows traders to identify not only the relative position to VWAP but also the strength and clarity of the trend, enhancing decision-making across all timeframes.

VWAP Filtered with TrendThis indicator combines the classic **VWAP** with a trend EMA filtered by the TDFI oscillator to confirm market direction.

- VWAP is displayed in white as the fair value reference.

- The trend EMA dynamically changes color according to market condition: green (uptrend), red (downtrend), orange (range).

- Candles highlight in blue when a bullish VWAP crossover is confirmed, and in fuchsia when a bearish crossover is confirmed.

- Includes adjustable thresholds and a cooldown filter to reduce noise and improve reliability.

This approach allows traders to identify not only the relative position to VWAP but also the strength and clarity of the trend, enhancing decision-making across all timeframes.

VWAP-RSI Scalper FINAL v1Description

This script implements a robust, battle-tested intraday scalping strategy designed for prop firm challenges, funded trader programs, and serious futures scalpers.

It combines VWAP, RSI, EMA trend, and ATR-based risk management to capture high-probability mean reversion and momentum moves during the most liquid hours of the trading day.

Core Logic

RSI (Relative Strength Index):

Trades are triggered when the RSI is either oversold or overbought using a short lookback (default: 3). This ensures only the strongest intraday reversals or exhaustion moves are considered.

VWAP Filter:

Longs are only taken above VWAP, shorts only below VWAP, aligning trades with the session’s dominant bias.

EMA Filter:

Additional trend quality filter—longs require price above EMA, shorts below EMA.

Session Control:

Only trades between user-defined session hours (default: US cash session), eliminating overnight/illiquid action.

ATR-based Dynamic Stops & Targets:

Every trade uses a stop loss at 1x ATR and a take profit at 2x ATR for a positive risk/reward ratio.

Max Trades Per Day:

Prevents overtrading and controls risk exposure (default: 3).

Performance (Sample Backtest)

Profit Factor: 1.37+ (prop-firm quality)

Drawdown: <1% (very conservative risk)

Win Rate: 37–48% (RR > 1, so high edge)

Consistency: Smooth, steady equity curve over hundreds of trades.

Best For:

ES/NQ/CL/GC intraday traders

Prop firm evaluation challenges (Tradeify, Topstep, Apex, etc.)

Anyone needing robust, no-nonsense systematic edge for futures or indices.

How to Use & Tune

Apply to 3min, 5min, or 15min charts of liquid futures or indices.

Change parameters in the settings panel to suit your asset, volatility, or session hours.

Use “Strategy Tester” to validate P&L, win rate, and drawdown.

How to Optimize

Raise/lower RSI length or bands to make signals more/less frequent.

Adjust stop/target multiples for your preferred risk/reward profile.

Change session hours to match your broker or market.

Disclaimer

This is not financial advice. Use on a demo or sim account first. Results will vary by market, slippage, and execution speed. Past performance does not guarantee future results.

If you find this useful, please give it a like, follow for more strategies, and comment your results or questions!

Good luck and safe trading!

VWAP + KCVolume Weighted Average Price (VWAP) is a technical analysis tool used to measure the average price weighted by volume. VWAP is typically used with intraday charts as a way to determine the general direction of intraday prices. It's similar to a moving average in that when price is above VWAP, prices are rising and when price is below VWAP, prices are falling. VWAP is primarily used by technical analysts to identify market trend.

The Keltner Channels (KC) indicator is a banded indicator similar to Bollinger Bands and Moving Average Envelopes. They consist of an Upper Envelope above a Middle Line as well as a Lower Envelope below the Middle Line. The Middle Line is a moving average of price over a user-defined time period. Either a simple moving average or an exponential moving average are typically used. The Upper and Lower Envelopes are set a (user-defined multiple) of a range away from the Middle Line. This can be a multiple of the daily high/low range, or more commonly a multiple of the Average True Range.

VWAP Suite by Augur - Multi PeriodOverview

The Multi-Timeframe VWAP Suite revolutionizes price analysis by combining institutional-grade volume-weighted pricing with multi-period deviation analytics. This professional toolkit simultaneously tracks VWAP across 5 time horizons (Daily to Yearly) with smart deviation bands, offering traders unparalleled insight into market structure and volatility dynamics.

Key Features

Multi-Timeframe VWAP Matrix

Simultaneous Daily/Weekly/Monthly/Quarterly/Yearly VWAP tracking

Institutional-level volume-weighted calculations

Independent timeframe toggles for focused analysis

Smart Deviation Architecture

Dual-layer standard deviation bands (1σ & 2σ)

Separate colors for upper/lower deviation zones

Adaptive 95% transparency fills for layered visualization

Professional Visual Design

Strategic color coding per timeframe (FIXED palette)

Dark Blue/Yellow/Purple/Pink/Red VWAP hierarchy

Orange-Green-Red-Blue deviation band system

Advanced Calculation Engine

HLC3 price source integration

Cumulative volume-weighting algorithm

Real-time standard deviation updates

VWAP SlopePublishing one of the simplest yet one of my favorite concepts. Had to publish since I didn't really find any script for this on TV.

VWAP slope.

This is nothing fancy because it's just calculating "slope" with a very basic level formula

vwap_slope = (vwap - vwap ) / length

Above zero line, it's positive zone.

Below zero line, it's a negative zone.

The idea is to avoid choppy conditions and stay true to larger readings, sometimes when we have vwap directly on chart and when price interacts with it, we tend to take the lot of bad trades.

The intention here is to avoid just that.

This is also good at tracking failure of change in sentiments, this failure is very important, because one's failure occurs there is significant movement in the opposite direction of the failure.

Since there isn't much alteration to this idea, there is not much to talk about tbh.

Just remember, this is an educational idea and not assurance of future performance.

Regards.

VWAP Stdev BandsCurrent price always obeys VWAP and is very useful for intraday traders. The Price will never go beyond the second deviation of VWAP at any point of time. The deviation bands are also very useful in predicting the volatility of the script.

Breakout trades can be taken based on the previous day's VWAP and it's deviations.

One can say that the stock has experienced breakout if current price crosses the fourth deviation of the previous day's VWAP or price bounces off that level, the price movement will be rapid if this occurs providing a good trading opportunity with low risk-reward ratio.