Multi Volume Weighted Average Price1. Three independent VWAP configurations (VWAP 1, 2, and 3). Each can be set up separately

for periods such as: session, daily, weekly, monthly, etc.

2. Previous VWAP closing prices: Closed VWAPs from previous periods remain visible until the

price touches them. At that point, they are removed.

3. Bands: Based on standard deviation or a percentage of VWAP with an adjustable multiplier.

The bands can be turned on or off.

4. Source: OHLC4 is the default setting for an accurate approximation, but it is customizable

(e.g. HLC3).

5. Global Setting: Select 10,000 or 20,000 historical bars to prevent runtime errors for long

periods.

Usage tips:

1. Use VWAP 1 for daily sessions, VWAP 2 for weekly, and VWAP 3 for Monthly analysis to receive

multi-timeframe support.

2. Customize the labels to clearly distinguish them (e.g. D VWAP, W VWAP, M VWAP).

3. If you encounter errors with historical data (e.g. on the M1 chart), minimize the number of

historical bars displayed to 10,000.

Cari dalam skrip untuk "weekly"

Bitcoin Expectile Model [LuxAlgo]The Bitcoin Expectile Model is a novel approach to forecasting Bitcoin, inspired by the popular Bitcoin Quantile Model by PlanC. By fitting multiple Expectile regressions to the price, we highlight zones of corrections or accumulations throughout the Bitcoin price evolution.

While we strongly recommend using this model with the Bitcoin All Time History Index INDEX:BTCUSD on the 3 days or weekly timeframe using a logarithmic scale, this model can be applied to any asset using the daily timeframe or superior.

Please note that here on TradingView, this model was solely designed to be used on the Bitcoin 1W chart, however, it can be experimented on other assets or timeframes if of interest.

🔶 USAGE

The Bitcoin Expectile Model can be applied similarly to models used for Bitcoin, highlighting lower areas of possible accumulation (support) and higher areas that allow for the anticipation of potential corrections (resistance).

By default, this model fits 7 individual Expectiles Log-Log Regressions to the price, each with their respective expectile ( tau ) values (here multiplied by 100 for the user's convenience). Higher tau values will return a fit closer to the higher highs made by the price of the asset, while lower ones will return fits closer to the lower prices observed over time.

Each zone is color-coded and has a specific interpretation. The green zone is a buy zone for long-term investing, purple is an anomaly zone for market bottoms that over-extend, while red is considered the distribution zone.

The fits can be extrapolated, helping to chart a course for the possible evolution of Bitcoin prices. Users can select the end of the forecast as a date using the "Forecast End" setting.

While the model is made for Bitcoin using a log scale, other assets showing a tendency to have a trend evolving in a single direction can be used. See the chart above on QQQ weekly using a linear scale as an example.

The Start Date can also allow fitting the model more locally, rather than over a large range of prices. This can be useful to identify potential shorter-term support/resistance areas.

🔶 DETAILS

🔹 On Quantile and Expectile Regressions

Quantile and Expectile regressions are similar; both return extremities that can be used to locate and predict prices where tops/bottoms could be more likely to occur.

The main difference lies in what we are trying to minimize, which, for Quantile regression, is commonly known as Quantile loss (or pinball loss), and for Expectile regression, simply Expectile loss.

You may refer to external material to go more in-depth about these loss functions; however, while they are similar and involve weighting specific prices more than others relative to our parameter tau, Quantile regression involves minimizing a weighted mean absolute error, while Expectile regression minimizes a weighted squared error.

The squared error here allows us to compute Expectile regression more easily compared to Quantile regression, using Iteratively reweighted least squares. For Quantile regression, a more elaborate method is needed.

In terms of comparison, Quantile regression is more robust, and easier to interpret, with quantiles being related to specific probabilities involving the underlying cumulative distribution function of the dataset; on the other expectiles are harder to interpret.

🔹 Trimming & Alterations

It is common to observe certain models ignoring very early Bitcoin price ranges. By default, we start our fit at the date 2010-07-16 to align with existing models.

By default, the model uses the number of time units (days, weeks...etc) elapsed since the beginning of history + 1 (to avoid NaN with log) as independent variable, however the Bitcoin All Time History Index INDEX:BTCUSD do not include the genesis block, as such users can correct for this by enabling the "Correct for Genesis block" setting, which will add the amount of missed bars from the Genesis block to the start oh the chart history.

🔶 SETTINGS

Start Date: Starting interval of the dataset used for the fit.

Correct for genesis block: When enabled, offset the X axis by the number of bars between the Bitcoin genesis block time and the chart starting time.

🔹 Expectiles

Toggle: Enable fit for the specified expectile. Disabling one fit will make the script faster to compute.

Expectile: Expectile (tau) value multiplied by 100 used for the fit. Higher values will produce fits that are located near price tops.

🔹 Forecast

Forecast End: Time at which the forecast stops.

🔹 Model Fit

Iterations Number: Number of iterations performed during the reweighted least squares process, with lower values leading to less accurate fits, while higher values will take more time to compute.

Dynamic OHLC levels(Day/Week/Month/6M/Year)+Open MarkerThis indicator automatically displays the Open, High, Low, and Close (OHLC) levels from the previous trading period directly on your chart. It's a versatile tool for identifying key support and resistance zones based on historical price action. The indicator offers a unique "Auto" mode that intelligently selects the most relevant time frame (Daily, Weekly, Monthly, 6M, or Yearly) based on your current chart's time frame. Alternatively, you can choose a specific time frame in "Manual" mode.

The indicator is designed to provide traders with clear visual cues for important price levels, helping them make more informed trading decisions. It's a valuable resource for both intraday and swing traders, as these levels often act as significant psychological barriers and turning points in the market.

Key Benefits 🎯

Identifies Key Levels Instantly: Automatically plots crucial support and resistance levels from the previous session, saving you time and effort.

Adaptable & Versatile: The "Auto" mode intelligently adjusts to your chart's time frame, ensuring you always see the most relevant OHLC levels.

Customizable: You have full control over which levels to display (High, Low, Open, Close), their colors, line styles, and thickness.

Visual Clarity: The option to highlight the area between the previous high and low provides a clear visual representation of the past session's range.

Multi-Session Support: It supports both Regular Trading Hours (RTH) and Extended Trading Hours (ETH), with a configurable timezone, making it globally applicable.

Core Features ✨

Dynamic Timeframe Selection:

Auto Mode: Automatically displays previous Day OHLC on intraday charts (e.g., 1-hour), previous Week OHLC on daily charts, and so on.

Manual Mode: Allows you to explicitly choose between previous Day, Week, Month, 6-Month, or Year OHLC levels.

Customizable Visuals:

Show Previous High: Plots the highest price of the previous period.

Show Previous Low: Plots the lowest price of the previous period.

Show Previous Open: Plots the opening price of the previous period.

Show Previous Close: Plots the closing price of the previous period.

Show Current Open Marker Line: A separate line that marks the open of the current period.

Highlight Area: Fills the space between the previous high and low with a customizable color.

Global Trading Support:

Session Mode: Choose to display levels based on Regular Trading Hours, Extended Hours, or both.

Timezone Selection: Configure the session timezone to align with major markets like New York, London, Tokyo, or Kolkata.

Line Styling: Adjust the line thickness, style (Solid, Dashed, Dotted), and transparency for each level to match your chart's aesthetics.

Labels: Toggle on/off text labels that clearly identify each plotted level (e.g., "PDH" for Previous Day High).

Who is this indicator for? 👤

This indicator is a powerful tool for a wide range of traders looking to incorporate historical price action into their analysis.

Intraday Traders: Can use the previous Daily OHLC levels to identify potential support/resistance for breakouts and reversals during the trading day.

Swing Traders: Can leverage the previous Weekly, Monthly, or Yearly OHLC levels on higher time frames to spot long-term trend continuation or reversal points.

Day Traders: Use the Previous Daily High/Low to frame the day's trading range and identify key levels for potential mean-reversion trades.

Technical Analysts: Those who rely on key levels and price action will find this indicator invaluable for their analysis.

This indicator simplifies a crucial part of technical analysis, providing a clean, customizable, and adaptive way to visualize and trade off of historical price levels.

Dynamic 5DMA/EMA with Color for Multiple Products🔹 Dynamic 5DMA/EMA with Slope-Based Coloring (All Timeframes)

This indicator plots a dynamic 5-period moving average that adapts intelligently to your chart's timeframe and product type — giving you a clean, slope-sensitive visual edge across intraday, daily, and weekly views.

✅ Key Features:

📈 Dynamic MA Length Scaling:

On intraday timeframes, the MA adjusts for your selected market session (RTH, ETH, VIX, or Futures), calculating a true 5-day average based on actual session length — not just a flat bar count.

🔄 Automatic Timeframe Detection:

Daily Chart: Uses standard 5DMA or 5EMA.

Weekly Chart: Applies a true 5-week MA.

Intraday Charts: Converts 5 days into bar-length equivalent dynamically.

🎨 Color-Coded Slope Logic:

Green = Rising MA (bullish slope)

Red = Falling MA (bearish slope)

Neutral slope = previous color held for visual continuity

No more guessing — direction is instantly clear.

⚠️ Built-In Slope Flip Alerts:

Set alerts when the slope of the MA turns up or down. Ideal for timing pullback entries or exits across any product.

⚙️ Session Settings for Proper Scaling:

Choose your product's market structure to ensure accurate 5-day conversion on intraday charts:

Stocks - RTH: 390 mins/day

Stocks - ETH: 780 mins/day

VIX: 855 mins/day

Futures: 1440 mins/day

This ensures the MA reflects 5 full trading days, regardless of session irregularities or bar interval.

📌 Why Use This Indicator?

Most MAs misrepresent trend direction on intraday charts because they assume static daily bar counts. This tool corrects that, then adds slope-based coloring to give you a fast, visual read on short-term momentum. Whether you’re swing trading SPY, scalping VIX, or position trading futures, this indicator keeps your view aligned with how institutions see moving averages across timeframes.

🔧 Best For:

VIX & volatility traders

Short-term SPY/SPX traders

Swing traders who value clean setups

Anyone wanting a true 5-day trend anchor on any chart

Bitcoin Logarithmic Growth Curve 2025 Z-Score"The Bitcoin logarithmic growth curve is a concept used to analyze Bitcoin's price movements over time. The idea is based on the observation that Bitcoin's price tends to grow exponentially, particularly during bull markets. It attempts to give a long-term perspective on the Bitcoin price movements.

The curve includes an upper and lower band. These bands often represent zones where Bitcoin's price is overextended (upper band) or undervalued (lower band) relative to its historical growth trajectory. When the price touches or exceeds the upper band, it may indicate a speculative bubble, while prices near the lower band may suggest a buying opportunity.

Unlike most Bitcoin growth curve indicators, this one includes a logarithmic growth curve optimized using the latest 2024 price data, making it, in our view, superior to previous models. Additionally, it features statistical confidence intervals derived from linear regression, compatible across all timeframes, and extrapolates the data far into the future. Finally, this model allows users the flexibility to manually adjust the function parameters to suit their preferences.

The Bitcoin logarithmic growth curve has the following function:

y = 10^(a * log10(x) - b)

In the context of this formula, the y value represents the Bitcoin price, while the x value corresponds to the time, specifically indicated by the weekly bar number on the chart.

How is it made (You can skip this section if you’re not a fan of math):

To optimize the fit of this function and determine the optimal values of a and b, the previous weekly cycle peak values were analyzed. The corresponding x and y values were recorded as follows:

113, 18.55

240, 1004.42

451, 19128.27

655, 65502.47

The same process was applied to the bear market low values:

103, 2.48

267, 211.03

471, 3192.87

676, 16255.15

Next, these values were converted to their linear form by applying the base-10 logarithm. This transformation allows the function to be expressed in a linear state: y = a * x − b. This step is essential for enabling linear regression on these values.

For the cycle peak (x,y) values:

2.053, 1.268

2.380, 3.002

2.654, 4.282

2.816, 4.816

And for the bear market low (x,y) values:

2.013, 0.394

2.427, 2.324

2.673, 3.504

2.830, 4.211

Next, linear regression was performed on both these datasets. (Numerous tools are available online for linear regression calculations, making manual computations unnecessary).

Linear regression is a method used to find a straight line that best represents the relationship between two variables. It looks at how changes in one variable affect another and tries to predict values based on that relationship.

The goal is to minimize the differences between the actual data points and the points predicted by the line. Essentially, it aims to optimize for the highest R-Square value.

Below are the results:

snapshot

snapshot

It is important to note that both the slope (a-value) and the y-intercept (b-value) have associated standard errors. These standard errors can be used to calculate confidence intervals by multiplying them by the t-values (two degrees of freedom) from the linear regression.

These t-values can be found in a t-distribution table. For the top cycle confidence intervals, we used t10% (0.133), t25% (0.323), and t33% (0.414). For the bottom cycle confidence intervals, the t-values used were t10% (0.133), t25% (0.323), t33% (0.414), t50% (0.765), and t67% (1.063).

The final bull cycle function is:

y = 10^(4.058 ± 0.133 * log10(x) – 6.44 ± 0.324)

The final bear cycle function is:

y = 10^(4.684 ± 0.025 * log10(x) – -9.034 ± 0.063)

The main Criticisms of growth curve models:

The Bitcoin logarithmic growth curve model faces several general criticisms that we’d like to highlight briefly. The most significant, in our view, is its heavy reliance on past price data, which may not accurately forecast future trends. For instance, previous growth curve models from 2020 on TradingView were overly optimistic in predicting the last cycle’s peak.

This is why we aimed to present our process for deriving the final functions in a transparent, step-by-step scientific manner, including statistical confidence intervals. It's important to note that the bull cycle function is less reliable than the bear cycle function, as the top band is significantly wider than the bottom band.

Even so, we still believe that the Bitcoin logarithmic growth curve presented in this script is overly optimistic since it goes parly against the concept of diminishing returns which we discussed in this post:

This is why we also propose alternative parameter settings that align more closely with the theory of diminishing returns."

Now with Z-Score calculation for easy and constant valuation classification of Bitcoin according to this metric.

Created for TRW

Desempenho 4ªs (MA)This Pine Script v5 indicator calculates the performance from Wednesday to Wednesday at 10:30 AM for the charted instrument. Every Wednesday at that time, it records the closing price and computes the percentage change, assigning a signal: +1 for increases above 1 %, -1 for declines below -1 %, and 0 for intermediate movements. It plots a five-period simple moving average on the main chart, color-coded green, red, or gray based on the weekly signal. Vertical dotted lines mark each weekly separation, and two blue horizontal lines denote the ±1 % thresholds for the current week. A label displays the performance percentage and signal.

Period Highlighter ProPeriod Highlighter Pro is a versatile Pine Script indicator designed to visually highlight specific time periods on your TradingView charts, making it easier to analyze seasonal patterns, trading sessions, or specific weekdays. With customizable settings for months, weekdays, or intraday time ranges, this tool adapts to your trading strategy, allowing you to focus on key periods with precision.

Features

Flexible Highlight Modes: Choose from three modes to highlight:

Month Range: Highlight specific months or a range (e.g., March to June) for seasonal analysis.

Weekday Range: Highlight specific weekdays (e.g., Mondays or Monday to Wednesday) for weekly pattern analysis.

Time Range: Highlight daily time windows (e.g., 15:30–22:00) for intraday session analysis, restricted to weekdays.

Customizable Timezone: Set any IANA timezone (e.g., America/New_York, Europe/London) or UTC offset to align highlights with your preferred market hours.

Historical Range Control: Define how far back to apply highlights with options for years (Month Range), weeks (Weekday Range), or days (Time Range).

Visual Customization: Choose your highlight color to match your chart style.

User-Friendly Inputs: Intuitive dropdowns and tooltips guide you through configuring each mode, ensuring only relevant settings are adjusted.

How It Works

Select a highlight mode and configure the corresponding settings:

Month Range: Pick a start month and an optional end month (or "Disabled" for a single month) and set the number of years back.

Weekday Range: Choose a start weekday and an optional end weekday (or "Disabled" for a single day) and set the number of weeks back.

Time Range: Specify a start and end time (24-hour format) and the number of weekdays back. The indicator then applies a semi-transparent background color to chart bars that meet your criteria, making it easy to spot relevant periods.

Use Cases

Seasonal Traders: Highlight specific months to analyze recurring market patterns.

Day Traders: Focus on active trading sessions (e.g., New York open) with precise time range highlighting.

Weekly Pattern Analysts: Isolate specific weekdays to study price behavior.

Global Traders: Adjust for any timezone to align with your market of interest.

Why Use Period Highlighter Pro?

This indicator simplifies time-based analysis by providing a clear visual overlay for your chosen periods. Whether you're studying historical trends or focusing on specific trading hours, Period Highlighter Pro offers the flexibility and precision to enhance your chart analysis.

Licensed under the Mozilla Public License 2.0.

Advanced Forex Currency Strength Meter

# Advanced Forex Currency Strength Meter

🚀 The Ultimate Currency Strength Analysis Tool for Forex Traders

This sophisticated indicator measures and compares the relative strength of major currencies (EUR, GBP, USD, JPY, CHF, CAD, AUD, NZD) to help you identify the strongest and weakest currencies in real-time, providing clear trading signals based on currency strength differentials.

## 📊 What This Indicator Does

The Advanced Forex Currency Strength Meter analyzes currency relationships across 28+ major forex pairs and 8 currency indices to determine which currencies are gaining or losing strength. Instead of relying on individual pair analysis, this tool gives you a bird's-eye view of the entire forex market, helping you:

Identify the strongest and weakest currencies at any given time

Find high-probability trading opportunities by pairing strong vs weak currencies

Avoid ranging markets by detecting when currencies have similar strength

Get clear LONG/SHORT/NEUTRAL signals for your current trading pair

Optimize your trading strategy based on your preferred timeframe and holding period

## ⚙️ How The Indicator Works

### Dual Calculation Method

The indicator uses a sophisticated dual approach for maximum accuracy:

Pairs-Based Analysis: Calculates currency strength from 28+ major forex pairs (EURUSD, GBPUSD, USDJPY, etc.)

Index-Based Analysis: Incorporates official currency indices (DXY, EXY, BXY, JXY, CXY, AXY, SXY, ZXY)

Weighted Combination: Blends both methods using smart weighting for enhanced accuracy

### Smart Auto-Optimization System

The indicator automatically adjusts its parameters based on your chart timeframe and intended holding period:

The system recognizes that scalping requires different sensitivity than swing trading, automatically optimizing lookback periods, analysis timeframes, signal thresholds, and index weights.

### Strength Calculation Process

Fetches price data from multiple timeframes using optimized tuple requests

Calculates percentage change over the specified lookback period

Optionally normalizes by ATR (Average True Range) to account for volatility differences

Combines pair-based and index-based calculations using dynamic weighting

Generates relative strength by comparing base currency vs quote currency

Produces clear trading signals when strength differential exceeds threshold

## 🎯 How To Use The Indicator

### Quick Start

Add the indicator to any forex pair chart

Enable 🧠 Smart Auto-Optimization (recommended for beginners)

Watch for LONG 🚀 signals when the relative strength line is green and above threshold

Watch for SHORT 🐻 signals when the relative strength line is red and below threshold

Avoid trading during NEUTRAL ⚪ periods when currencies have similar strength

Note: This is highly recommended to couple this indicator with fundamental analysis and use it as an extra signal.

### 📋 Parameters Reference

#### 🤖 Smart Settings

🧠 Smart Auto-Optimization: (Default: Enabled) Automatically optimizes all parameters based on chart timeframe and trading style

#### ⚙️ Manual Override

These settings are only active when Smart Auto-Optimization is disabled:

Manual Lookback Period: (Default: 14) Number of periods to analyze for strength calculation

Manual ATR Period: (Default: 14) Period for ATR normalization calculation

Manual Analysis Timeframe: (Default: 240) Higher timeframe for strength analysis

Manual Index Weight: (Default: 0.5) Weight given to currency indices vs pairs (0.0 = pairs only, 1.0 = indices only)

Manual Signal Threshold: (Default: 0.5) Minimum strength differential required for trading signals

#### 📊 Display

Show Signal Markers: (Default: Enabled) Display triangle markers when signals change

Show Info Label: (Default: Enabled) Show comprehensive information label with current analysis

#### 🔍 Analysis

Use ATR Normalization: (Default: Enabled) Normalize strength calculations by volatility for fairer comparison

#### 💰 Currency Indices

💰 Use Currency Indices: (Default: Enabled) Include all 8 currency indices in strength calculation for enhanced accuracy

#### 🎨 Colors

Strong Currency Color: (Default: Green) Color for positive/strong signals

Weak Currency Color: (Default: Red) Color for negative/weak signals

Neutral Color: (Default: Gray) Color for neutral conditions

Strong/Weak Backgrounds: Background colors for clear signal visualization

### 🧠 Smart Optimization Profiles

The indicator automatically selects optimal parameters based on your chart timeframe:

#### ⚡ Scalping Profile (1M-5M Charts)

For positions held for a few minutes:

Lookback: 5 periods (fast/sensitive)

Analysis Timeframe: 15 minutes

Index Weight: 20% (favor pairs for speed)

Signal Threshold: 0.3% (sensitive triggers)

#### 📈 Intraday Profile (10M-1H Charts)

For positions held for a few hours:

Lookback: 12 periods (balanced sensitivity)

Analysis Timeframe: 4 hours

Index Weight: 40% (balanced approach)

Signal Threshold: 0.4% (moderate sensitivity)

#### 📊 Swing Profile (4H-Daily Charts)

For positions held for a few days:

Lookback: 21 periods (stable analysis)

Analysis Timeframe: Daily

Index Weight: 60% (favor indices for stability)

Signal Threshold: 0.5% (conservative triggers)

#### 📆 Position Profile (Weekly+ Charts)

For positions held for a few weeks:

Lookback: 30 periods (long-term view)

Analysis Timeframe: Weekly

Index Weight: 70% (heavily favor indices)

Signal Threshold: 0.6% (very conservative)

### Entry Timing

Wait for clear LONG 🚀 or SHORT 🐻 signals

Avoid trading during NEUTRAL ⚪ periods

Look for signal confirmations on multiple timeframes

### Risk Management

Stronger signals (higher relative strength values) suggest higher probability trades

Use appropriate position sizing based on signal strength

Consider the trading style profile when setting stop losses and take profits

💡 Pro Tip: The indicator works best when combined with your existing technical analysis. Use currency strength to identify which pairs to trade, then use your favorite technical indicators to determine when to enter and exit.

## 🔧 Key Features

28+ Forex Pairs Analysis: Comprehensive coverage of major currency relationships

8 Currency Indices Integration: DXY, EXY, BXY, JXY, CXY, AXY, SXY, ZXY for enhanced accuracy

Smart Auto-Optimization: Automatically adapts to your trading style and timeframe

ATR Normalization: Fair comparison across different currency pairs and volatility levels

Real-Time Signals: Clear LONG/SHORT/NEUTRAL signals with visual markers

Performance Optimized: Efficient tuple-based data requests minimize external calls

User-Friendly Interface: Simplified settings with comprehensive tooltips

Multi-Timeframe Support: Works on any timeframe from 1-minute to monthly charts

Transform your forex trading with the power of currency strength analysis! 🚀

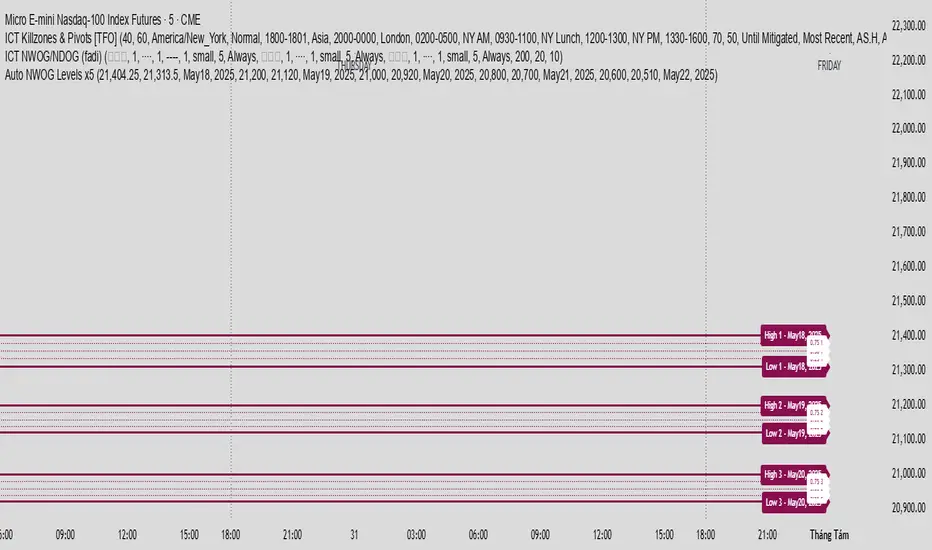

Auto NWOG Levels x5Indicator Name: Auto NWOG Levels with Labels

Description:

This indicator automatically plots the NWOG (Naked Weekly Open Gap) price levels on your chart. It includes:

NWOG High & Low: Solid maroon lines representing the high and low boundaries of the NWOG zone.

Intermediate Levels: Dotted maroon lines at 25%, 50%, and 75% levels within the NWOG range, providing visual guidance for possible support/resistance zones.

Labels: Each level is labeled on the right side of the chart, including a customizable date label for context.

Extendable Lines: All lines extend horizontally for a customizable number of bars (default: 500 bars) for better visibility over time.

Inputs:

NWOG High: Price level of the NWOG high.

NWOG Low: Price level of the NWOG low.

Date Label: Text to be displayed on the labels (e.g., the week of the NWOG).

This tool is useful for traders who monitor weekly price gaps and want clear, persistent levels drawn automatically on their charts.

Drawdown Distribution Analysis (DDA) ACADEMIC FOUNDATION AND RESEARCH BACKGROUND

The Drawdown Distribution Analysis indicator implements quantitative risk management principles, drawing upon decades of academic research in portfolio theory, behavioral finance, and statistical risk modeling. This tool provides risk assessment capabilities for traders and portfolio managers seeking to understand their current position within historical drawdown patterns.

The theoretical foundation of this indicator rests on modern portfolio theory as established by Markowitz (1952), who introduced the fundamental concepts of risk-return optimization that continue to underpin contemporary portfolio management. Sharpe (1966) later expanded this framework by developing risk-adjusted performance measures, most notably the Sharpe ratio, which remains a cornerstone of performance evaluation in financial markets.

The specific focus on drawdown analysis builds upon the work of Chekhlov, Uryasev and Zabarankin (2005), who provided the mathematical framework for incorporating drawdown measures into portfolio optimization. Their research demonstrated that traditional mean-variance optimization often fails to capture the full risk profile of investment strategies, particularly regarding sequential losses. More recent work by Goldberg and Mahmoud (2017) has brought these theoretical concepts into practical application within institutional risk management frameworks.

Value at Risk methodology, as comprehensively outlined by Jorion (2007), provides the statistical foundation for the risk measurement components of this indicator. The coherent risk measures framework developed by Artzner et al. (1999) ensures that the risk metrics employed satisfy the mathematical properties required for sound risk management decisions. Additionally, the focus on downside risk follows the framework established by Sortino and Price (1994), while the drawdown-adjusted performance measures implement concepts introduced by Young (1991).

MATHEMATICAL METHODOLOGY

The core calculation methodology centers on a peak-tracking algorithm that continuously monitors the maximum price level achieved and calculates the percentage decline from this peak. The drawdown at any time t is defined as DD(t) = (P(t) - Peak(t)) / Peak(t) × 100, where P(t) represents the asset price at time t and Peak(t) represents the running maximum price observed up to time t.

Statistical distribution analysis forms the analytical backbone of the indicator. The system calculates key percentiles using the ta.percentile_nearest_rank() function to establish the 5th, 10th, 25th, 50th, 75th, 90th, and 95th percentiles of the historical drawdown distribution. This approach provides a complete picture of how the current drawdown compares to historical patterns.

Statistical significance assessment employs standard deviation bands at one, two, and three standard deviations from the mean, following the conventional approach where the upper band equals μ + nσ and the lower band equals μ - nσ. The Z-score calculation, defined as Z = (DD - μ) / σ, enables the identification of statistically extreme events, with thresholds set at |Z| > 2.5 for extreme drawdowns and |Z| > 3.0 for severe drawdowns, corresponding to confidence levels exceeding 99.4% and 99.7% respectively.

ADVANCED RISK METRICS

The indicator incorporates several risk-adjusted performance measures that extend beyond basic drawdown analysis. The Sharpe ratio calculation follows the standard formula Sharpe = (R - Rf) / σ, where R represents the annualized return, Rf represents the risk-free rate, and σ represents the annualized volatility. The system supports dynamic sourcing of the risk-free rate from the US 10-year Treasury yield or allows for manual specification.

The Sortino ratio addresses the limitation of the Sharpe ratio by focusing exclusively on downside risk, calculated as Sortino = (R - Rf) / σd, where σd represents the downside deviation computed using only negative returns. This measure provides a more accurate assessment of risk-adjusted performance for strategies that exhibit asymmetric return distributions.

The Calmar ratio, defined as Annual Return divided by the absolute value of Maximum Drawdown, offers a direct measure of return per unit of drawdown risk. This metric proves particularly valuable for comparing strategies or assets with different risk profiles, as it directly relates performance to the maximum historical loss experienced.

Value at Risk calculations provide quantitative estimates of potential losses at specified confidence levels. The 95% VaR corresponds to the 5th percentile of the drawdown distribution, while the 99% VaR corresponds to the 1st percentile. Conditional VaR, also known as Expected Shortfall, estimates the average loss in the worst 5% of scenarios, providing insight into tail risk that standard VaR measures may not capture.

To enable fair comparison across assets with different volatility characteristics, the indicator calculates volatility-adjusted drawdowns using the formula Adjusted DD = Raw DD / (Volatility / 20%). This normalization allows for meaningful comparison between high-volatility assets like cryptocurrencies and lower-volatility instruments like government bonds.

The Risk Efficiency Score represents a composite measure ranging from 0 to 100 that combines the Sharpe ratio and current percentile rank to provide a single metric for quick asset assessment. Higher scores indicate superior risk-adjusted performance relative to historical patterns.

COLOR SCHEMES AND VISUALIZATION

The indicator implements eight distinct color themes designed to accommodate different analytical preferences and market contexts. The EdgeTools theme employs a corporate blue palette that matches the design system used throughout the edgetools.org platform, ensuring visual consistency across analytical tools.

The Gold theme specifically targets precious metals analysis with warm tones that complement gold chart analysis, while the Quant theme provides a grayscale scheme suitable for analytical environments that prioritize clarity over aesthetic appeal. The Behavioral theme incorporates psychology-based color coding, using green to represent greed-driven market conditions and red to indicate fear-driven environments.

Additional themes include Ocean, Fire, Matrix, and Arctic schemes, each designed for specific market conditions or user preferences. All themes function effectively with both dark and light mode trading platforms, ensuring accessibility across different user interface configurations.

PRACTICAL APPLICATIONS

Asset allocation and portfolio construction represent primary use cases for this analytical framework. When comparing multiple assets such as Bitcoin, gold, and the S&P 500, traders can examine Risk Efficiency Scores to identify instruments offering superior risk-adjusted performance. The 95% VaR provides worst-case scenario comparisons, while volatility-adjusted drawdowns enable fair comparison despite varying volatility profiles.

The practical decision framework suggests that assets with Risk Efficiency Scores above 70 may be suitable for aggressive portfolio allocations, scores between 40 and 70 indicate moderate allocation potential, and scores below 40 suggest defensive positioning or avoidance. These thresholds should be adjusted based on individual risk tolerance and market conditions.

Risk management and position sizing applications utilize the current percentile rank to guide allocation decisions. When the current drawdown ranks above the 75th percentile of historical data, indicating that current conditions are better than 75% of historical periods, position increases may be warranted. Conversely, when percentile rankings fall below the 25th percentile, indicating elevated risk conditions, position reductions become advisable.

Institutional portfolio monitoring applications include hedge fund risk dashboard implementations where multiple strategies can be monitored simultaneously. Sharpe ratio tracking identifies deteriorating risk-adjusted performance across strategies, VaR monitoring ensures portfolios remain within established risk limits, and drawdown duration tracking provides valuable information for investor reporting requirements.

Market timing applications combine the statistical analysis with trend identification techniques. Strong buy signals may emerge when risk levels register as "Low" in conjunction with established uptrends, while extreme risk levels combined with downtrends may indicate exit or hedging opportunities. Z-scores exceeding 3.0 often signal statistically oversold conditions that may precede trend reversals.

STATISTICAL SIGNIFICANCE AND VALIDATION

The indicator provides 95% confidence intervals around current drawdown levels using the standard formula CI = μ ± 1.96σ. This statistical framework enables users to assess whether current conditions fall within normal market variation or represent statistically significant departures from historical patterns.

Risk level classification employs a dynamic assessment system based on percentile ranking within the historical distribution. Low risk designation applies when current drawdowns perform better than 50% of historical data, moderate risk encompasses the 25th to 50th percentile range, high risk covers the 10th to 25th percentile range, and extreme risk applies to the worst 10% of historical drawdowns.

Sample size considerations play a crucial role in statistical reliability. For daily data, the system requires a minimum of 252 trading days (approximately one year) but performs better with 500 or more observations. Weekly data analysis benefits from at least 104 weeks (two years) of history, while monthly data requires a minimum of 60 months (five years) for reliable statistical inference.

IMPLEMENTATION BEST PRACTICES

Parameter optimization should consider the specific characteristics of different asset classes. Equity analysis typically benefits from 500-day lookback periods with 21-day smoothing, while cryptocurrency analysis may employ 365-day lookback periods with 14-day smoothing to account for higher volatility patterns. Fixed income analysis often requires longer lookback periods of 756 days with 34-day smoothing to capture the lower volatility environment.

Multi-timeframe analysis provides hierarchical risk assessment capabilities. Daily timeframe analysis supports tactical risk management decisions, weekly analysis informs strategic positioning choices, and monthly analysis guides long-term allocation decisions. This hierarchical approach ensures that risk assessment occurs at appropriate temporal scales for different investment objectives.

Integration with complementary indicators enhances the analytical framework. Trend indicators such as RSI and moving averages provide directional bias context, volume analysis helps confirm the severity of drawdown conditions, and volatility measures like VIX or ATR assist in market regime identification.

ALERT SYSTEM AND AUTOMATION

The automated alert system monitors five distinct categories of risk events. Risk level changes trigger notifications when drawdowns move between risk categories, enabling proactive risk management responses. Statistical significance alerts activate when Z-scores exceed established threshold levels of 2.5 or 3.0 standard deviations.

New maximum drawdown alerts notify users when historical maximum levels are exceeded, indicating entry into uncharted risk territory. Poor risk efficiency alerts trigger when the composite risk efficiency score falls below 30, suggesting deteriorating risk-adjusted performance. Sharpe ratio decline alerts activate when risk-adjusted performance turns negative, indicating that returns no longer compensate for the risk undertaken.

TRADING STRATEGIES

Conservative risk parity strategies can be implemented by monitoring Risk Efficiency Scores across a diversified asset portfolio. Monthly rebalancing maintains equal risk contribution from each asset, with allocation reductions triggered when risk levels reach "High" status and complete exits executed when "Extreme" risk levels emerge. This approach typically results in lower overall portfolio volatility, improved risk-adjusted returns, and reduced maximum drawdown periods.

Tactical asset rotation strategies compare Risk Efficiency Scores across different asset classes to guide allocation decisions. Assets with scores exceeding 60 receive overweight allocations, while assets scoring below 40 receive underweight positions. Percentile rankings provide timing guidance for allocation adjustments, creating a systematic approach to asset allocation that responds to changing risk-return profiles.

Market timing strategies with statistical edges can be constructed by entering positions when Z-scores fall below -2.5, indicating statistically oversold conditions, and scaling out when Z-scores exceed 2.5, suggesting overbought conditions. The 95% VaR serves as a stop-loss reference point, while trend confirmation indicators provide additional validation for position entry and exit decisions.

LIMITATIONS AND CONSIDERATIONS

Several statistical limitations affect the interpretation and application of these risk measures. Historical bias represents a fundamental challenge, as past drawdown patterns may not accurately predict future risk characteristics, particularly during structural market changes or regime shifts. Sample dependence means that results can be sensitive to the selected lookback period, with shorter periods providing more responsive but potentially less stable estimates.

Market regime changes can significantly alter the statistical parameters underlying the analysis. During periods of structural market evolution, historical distributions may provide poor guidance for future expectations. Additionally, many financial assets exhibit return distributions with fat tails that deviate from normal distribution assumptions, potentially leading to underestimation of extreme event probabilities.

Practical limitations include execution risk, where theoretical signals may not translate directly into actual trading results due to factors such as slippage, timing delays, and market impact. Liquidity constraints mean that risk metrics assume perfect liquidity, which may not hold during stressed market conditions when risk management becomes most critical.

Transaction costs are not incorporated into risk-adjusted return calculations, potentially overstating the attractiveness of strategies that require frequent trading. Behavioral factors represent another limitation, as human psychology may override statistical signals, particularly during periods of extreme market stress when disciplined risk management becomes most challenging.

TECHNICAL IMPLEMENTATION

Performance optimization ensures reliable operation across different market conditions and timeframes. All technical analysis functions are extracted from conditional statements to maintain Pine Script compliance and ensure consistent execution. Memory efficiency is achieved through optimized variable scoping and array usage, while computational speed benefits from vectorized calculations where possible.

Data quality requirements include clean price data without gaps or errors that could distort distribution analysis. Sufficient historical data is essential, with a minimum of 100 bars required and 500 or more preferred for reliable statistical inference. Time alignment across related assets ensures meaningful comparison when conducting multi-asset analysis.

The configuration parameters are organized into logical groups to enhance usability. Core settings include the Distribution Analysis Period (100-2000 bars), Drawdown Smoothing Period (1-50 bars), and Price Source selection. Advanced metrics settings control risk-free rate sourcing, either from live market data or fixed rate specification, along with toggles for various risk-adjusted metric calculations.

Display options provide flexibility in visual presentation, including color theme selection from eight available schemes, automatic dark mode optimization, and control over table display, position lines, percentile bands, and standard deviation overlays. These options ensure that the indicator can be adapted to different analytical workflows and visual preferences.

CONCLUSION

The Drawdown Distribution Analysis indicator provides risk management tools for traders seeking to understand their current position within historical risk patterns. By combining established statistical methodology with practical usability features, the tool enables evidence-based risk assessment and portfolio optimization decisions.

The implementation draws upon established academic research while providing practical features that address real-world trading requirements. Dynamic risk-free rate integration ensures accurate risk-adjusted performance calculations, while multiple color schemes accommodate different analytical preferences and use cases.

Academic compliance is maintained through transparent methodology and acknowledgment of limitations. The tool implements peer-reviewed statistical techniques while clearly communicating the constraints and assumptions underlying the analysis. This approach ensures that users can make informed decisions about the appropriate application of the risk assessment framework within their broader trading and investment processes.

BIBLIOGRAPHY

Artzner, P., Delbaen, F., Eber, J.M. and Heath, D. (1999) 'Coherent Measures of Risk', Mathematical Finance, 9(3), pp. 203-228.

Chekhlov, A., Uryasev, S. and Zabarankin, M. (2005) 'Drawdown Measure in Portfolio Optimization', International Journal of Theoretical and Applied Finance, 8(1), pp. 13-58.

Goldberg, L.R. and Mahmoud, O. (2017) 'Drawdown: From Practice to Theory and Back Again', Journal of Risk Management in Financial Institutions, 10(2), pp. 140-152.

Jorion, P. (2007) Value at Risk: The New Benchmark for Managing Financial Risk. 3rd edn. New York: McGraw-Hill.

Markowitz, H. (1952) 'Portfolio Selection', Journal of Finance, 7(1), pp. 77-91.

Sharpe, W.F. (1966) 'Mutual Fund Performance', Journal of Business, 39(1), pp. 119-138.

Sortino, F.A. and Price, L.N. (1994) 'Performance Measurement in a Downside Risk Framework', Journal of Investing, 3(3), pp. 59-64.

Young, T.W. (1991) 'Calmar Ratio: A Smoother Tool', Futures, 20(1), pp. 40-42.

HTF Current/Average RangeThe "HTF(Higher Timeframe) Current/Average Range" indicator calculates and displays the current and average price ranges across multiple timeframes, including daily, weekly, monthly, 4 hour, and user-defined custom timeframes.

Users can customize the lookback period, table size, timeframe, and font color; with the indicator efficiently updating on the final bar to optimize performance.

When the current range surpasses the average range for a given timeframe, the corresponding table cell is highlighted in green, indicating potential maximum price expansion and signaling the possibility of an impending retracement or consolidation.

For day trading strategies, the daily average range can serve as a guide, allowing traders to hold positions until the current daily range approaches or meets the average range, at which point exiting the trade may be considered.

For scalping strategies, the 15min and 5min average range can be utilized to determine optimal holding periods for fast trades.

Other strategies:

Intraday Trading - 1h and 4h Average Range

Swing Trading - Monthly Average Range

Short-term Trading - Weekly Average Range

Also using these statistics in accordance with Power 3 ICT concepts, will assist in holding trades to their statistical average range of the chosen HTF candle.

CODE

The core functionality lies in the data retrieval and table population sections.

The request.security function (e.g., = request.security(syminfo.tickerid, "D", , lookahead = barmerge.lookahead_off)) retrieves high and low prices from specified timeframes without lookahead bias, ensuring accurate historical data.

These values are used to compute current ranges and average ranges (ta.sma(high - low, avgLength)), which are then displayed in a dynamically generated table starting at (if barstate.islast) using table.new, with conditional green highlighting when the current range is greater than average range, providing a clear visual cue for volatility analysis.

Daily Performance Analysis [Mr_Rakun]The Daily Performance Analysis indicator is a comprehensive trading performance tracker that analyzes your strategy's success rate and profitability across different days of the week and month. This powerful tool provides detailed statistics to help traders identify patterns in their trading performance and optimize their strategies accordingly.

Weekly Performance Analysis:

Tracks wins/losses for each day of the week (Monday through Sunday)

Calculates net profit/loss for each trading day

Shows profit factor (gross profit ÷ gross loss) for each day

Displays win rate percentage for each day

Monthly Performance Analysis:

Monitors performance for each day of the month (1-31)

Provides the same detailed metrics as weekly analysis

Helps identify monthly patterns and trends

Add to Your Strategy:

Copy the performance analysis code and integrate it into your existing Pine Script strategy

Optimize Strategy: Use insights to refine entry/exit timing or avoid trading on poor-performing days

Pattern Recognition: Identify which days of the week/month work best for your strategy

Risk Management: Avoid trading on historically poor-performing days

Strategy Optimization: Fine-tune your approach based on empirical data

Performance Tracking: Monitor long-term trends in your trading success

Data-Driven Decisions: Make informed adjustments to your trading schedule

Multi-Timeframe RSI Table# Multi-Timeframe RSI Table

## Overview

This indicator displays RSI (Relative Strength Index) values across multiple timeframes in a convenient table format, allowing traders to quickly assess momentum conditions across different time horizons without switching charts.

## Features

• *7 Timeframes*: 5m, 15m, 1h, 4h, Daily, Weekly, Monthly

• *Color-coded RSI Values*:

- 🔴 Red: Overbought (≥70)

- 🟢 Green: Oversold (≤30)

- 🟠 Orange: Bullish momentum (50-70)

- 🟡 Yellow: Bearish momentum (30-50)

• *Clean Table Display*: Positioned in top-right corner for easy viewing

• *Customizable Settings*: Adjustable RSI length and overbought/oversold levels

## How to Use

1. Add the indicator to your chart

2. The table automatically displays current RSI values for all timeframes

3. Use color coding to quickly identify:

- *Buying opportunities* when multiple timeframes show green (oversold)

- *Selling opportunities* when multiple timeframes show red (overbought)

- *Trend alignment* when higher timeframes match your trading direction

## Trading Applications

• *Multi-timeframe analysis*: Confirm signals across different time horizons

• *Entry timing*: Find optimal entry points when shorter timeframes align with longer trends

• *Risk management*: Avoid trades when higher timeframes show opposite momentum

• *Swing trading*: Identify when daily/weekly RSI supports your position direction

## Settings

• *RSI Length*: Default 14 periods (standard RSI calculation)

• *Overbought Level*: Default 70 (customizable)

• *Oversold Level*: Default 30 (customizable)

## Best Practices

• Look for alignment across multiple timeframes for stronger signals

• Use higher timeframe RSI to determine overall trend direction

• Combine with price action and support/resistance levels

• Avoid trading against strong momentum shown in higher timeframes

Perfect for day traders, swing traders, and anyone who needs quick multi-timeframe RSI analysis without constantly switching chart timeframes.

Multi Pivot Point & Central Pivot Range - Nadeem Al-QahwiThis indicator combines four advanced trading modules into one flexible and easy-to-use script:

Traditional Pivot Points:

Calculates classic support and resistance levels (PP, R1–R5, S1–S5) based on previous session data. Ideal for identifying key turning points and mapping out the daily, weekly, or monthly structure.

Camarilla Levels:

Provides six upper and lower pivot levels (H1–H6, L1–L6) derived from volatility and closing price formulas. Especially effective for intraday reversal, mean reversion, and finding overbought/oversold extremes.

Central Pivot Range (CPR):

Plots the median, top, and bottom of the value area each session. CPR width instantly highlights whether the market is likely to trend (narrow CPR) or remain range-bound (wide CPR).

Developing CPR projects the evolving range for the current period—essential for real-time analysis and pre-market planning.

Dynamic Zone Levels (DZL):

Automatically detects and highlights clusters of pivots to reveal high-probability support/resistance zones, filtering out market “noise.”

DZL alerts notify you whenever price breaks or retests these key areas, making it easier to spot momentum trades and avoid false signals.

Key Features:

Multi-timeframe flexibility: Use with daily, weekly, monthly, yearly, or custom timeframes—even rare ones like biyearly and decennial.

Modular design: Activate or hide any system (Traditional, Camarilla, CPR, DZL) as you need.

Bilingual interface: Every setting and label is shown in both English and Arabic.

Full customization: Control visibility, color, style, and placement for every level and label.

Historical depth: Plot up to 5,000 pivot/zones back for deep analysis and backtesting.

Smart alerts: Get instant notifications on true S/R breakouts or retests (from DZL).

How to Use:

Trend Trading:

Watch for a very narrow CPR to identify potential trending days—trade in the breakout direction above/below the CPR.

Range Trading:

When CPR is wide, expect sideways movement. Fade reversals at R1/S1 or within the CPR boundaries.

Breakouts:

Use DZL alerts to capture momentum as price breaks or retests dynamic support/resistance zones.

Multi-Timeframe Confluence:

Combine CPR and pivot levels from multiple timeframes for higher-probability entries and exits.

All calculations and logic are fully open.

X Opens+Overview:

The X Opens+ indicator is a precision tool designed for traders seeking to analyze market structure and behavior around key timeframe opens. It highlights the open prices of custom-selected higher timeframes—such as daily, weekly, or monthly sessions—and visualizes them directly on lower timeframes. These open levels often coincide with high-volume zones, market imbalance, and institutional interest, making them powerful reference points for intraday and swing trading strategies.

Key Features:

Custom Timeframe Anchoring: Users can select any timeframe (e.g., daily, 4H, 1W) to display its current and previous session opens directly on their active chart. This allows for flexible multi-timeframe analysis within a single view.

Price Reaction Zones: Timeframe opens are frequently areas of heightened liquidity and directional bias. By identifying these opens and their relationship to current price action, traders can anticipate areas of support/resistance, trend continuation, or reversal.

Derived Midpoints and Ranges: The indicator also computes and displays the previous session’s range midpoint (EQ), as well as extension bands (e.g., ±1.0x or ±1.5x the prior range). These levels are useful for contextualizing volatility expansion and identifying breakout or fade setups around key open zones.

Historical Session Mapping: In addition to live opens, the tool optionally displays opens and range-based levels from previous sessions. This historical layering gives traders a broader context of how price has respected or rejected these levels over time.

Labeling and Customization: Each level can be labeled and color-coded to match user preferences. The visibility, size, and style of each element (e.g., lines, labels, bands) are fully configurable for visual clarity and user alignment.

Use Cases:

Confirming bias around daily or weekly opens, especially during market opens or key economic releases.

Identifying equilibrium levels for mean reversion or continuation setups.

Using ±1.0 and ±1.5 range projections as dynamic targets or invalidation zones.

Anchoring to key sessions for volume profile or order flow-based strategies.

Summary:

X Opens+ is a data-driven utility that transforms static session opens into dynamic market tools. By spotlighting where institutional interest likely concentrates—at the opens of significant timeframes—this indicator provides traders with a structural edge in identifying key zones that influence price behavior throughout the trading day or week

Info TableOverview

The Info Table V1 is a versatile TradingView indicator tailored for intraday futures traders, particularly those focusing on MESM2 (Micro E-mini S&P 500 futures) on 1-minute charts. It presents essential market insights through two customizable tables: the Main Table for predictive and macro metrics, and the New Metrics Table for momentum and volatility indicators. Designed for high-activity sessions like 9:30 AM–11:00 AM CDT, this tool helps traders assess price alignment, sentiment, and risk in real-time. Metrics update dynamically (except weekly COT data), with optional alerts for key conditions like volatility spikes or momentum shifts.

This indicator builds on foundational concepts like linear regression for predictions and adapts open-source elements for enhanced functionality. Gradient code is adapted from TradingView's Color Library. QQE logic is adapted from LuxAlgo's QQE Weighted Oscillator, licensed under CC BY-NC-SA 4.0. The script is released under the Mozilla Public License 2.0.

Key Features

Two Customizable Tables: Positioned independently (e.g., top-right for Main, bottom-right for New Metrics) with toggle options to show/hide for a clutter-free chart.

Gradient Coloring: User-defined high/low colors (default green/red) for quick visual interpretation of extremes, such as overbought/oversold or high volatility.

Arrows for Directional Bias: In the New Metrics Table, up (↑) or down (↓) arrows appear in value cells based on metric thresholds (top/bottom 25% of range), indicating bullish/high or bearish/low conditions.

Consensus Highlighting: The New Metrics Table's title cells ("Metric" and "Value") turn green if all arrows are ↑ (strong bullish consensus), red if all are ↓ (strong bearish consensus), or gray otherwise.

Predicted Price Plot: Optional line (default blue) overlaying the ML-predicted price for visual comparison with actual price action.

Alerts: Notifications for high/low Frahm Volatility (≥8 or ≤3) and QQE Bias crosses (bullish/bearish momentum shifts).

Main Table Metrics

This table focuses on predictive, positional, and macro insights:

ML-Predicted Price: A linear regression forecast using normalized price, volume, and RSI over a customizable lookback (default 500 bars). Gradient scales from low (red) to high (green) relative to the current price ± threshold (default 100 points).

Deviation %: Percentage difference between current price and predicted price. Gradient highlights extremes (±0.5% default threshold), signaling potential overextensions.

VWAP Deviation %: Percentage difference from Volume Weighted Average Price (VWAP). Gradient indicates if price is above (green) or below (red) fair value (±0.5% default).

FRED UNRATE % Change: Percentage change in U.S. unemployment rate (via FRED data). Cell turns red for increases (economic weakness), green for decreases (strength), gray if zero or disabled.

Open Interest: Total open MESM2 futures contracts. Gradient scales from low (red) to high (green) up to a hardcoded 300,000 threshold, reflecting market participation.

COT Commercial Long/Short: Weekly Commitment of Traders data for commercial positions. Long cell green if longs > shorts (bullish institutional sentiment); Short cell red if shorts > longs (bearish); gray otherwise.

New Metrics Table Metrics

This table emphasizes technical momentum and volatility, with arrows for quick bias assessment:

QQE Bias: Smoothed RSI vs. trailing stop (default length 14, factor 4.236, smooth 5). Green for bullish (RSI > stop, ↑ arrow), red for bearish (RSI < stop, ↓ arrow), gray for neutral.

RSI: Relative Strength Index (default period 14). Gradient from oversold (red, <30 + threshold offset, ↓ arrow if ≤40) to overbought (green, >70 - offset, ↑ arrow if ≥60).

ATR Volatility: Score (1–20) based on Average True Range (default period 14, lookback 50). High scores (green, ↑ if ≥15) signal swings; low (red, ↓ if ≤5) indicate calm.

ADX Trend: Average Directional Index (default period 14). Gradient from weak (red, ↓ if ≤0.25×25 threshold) to strong trends (green, ↑ if ≥0.75×25).

Volume Momentum: Score (1–20) comparing current to historical volume (lookback 50). High (green, ↑ if ≥15) suggests pressure; low (red, ↓ if ≤5) implies weakness.

Frahm Volatility: Score (1–20) from true range over a window (default 24 hours, multiplier 9). Dynamic gradient (green/red/yellow); ↑ if ≥7.5, ↓ if ≤2.5.

Frahm Avg Candle (Ticks): Average candle size in ticks over the window. Blue gradient (or dynamic green/red/yellow); ↑ if ≥0.75 percentile, ↓ if ≤0.25.

Arrows trigger on metric-specific logic (e.g., RSI ≥60 for ↑), providing directional cues without strict color ties.

Customization Options

Adapt the indicator to your strategy:

ML Inputs: Lookback (10–5000 bars) and RSI period (2+) for prediction sensitivity—shorter for volatility, longer for trends.

Timeframes: Individual per metric (e.g., 1H for QQE Bias to match higher frames; blank for chart timeframe).

Thresholds: Adjust gradients and arrows (e.g., Deviation 0.1–5%, ADX 0–100, RSI overbought/oversold).

QQE Settings: Length, factor, and smooth for fine-tuned momentum.

Data Toggles: Enable/disable FRED, Open Interest, COT for focus (e.g., disable macro for pure intraday).

Frahm Options: Window hours (1+), scale multiplier (1–10), dynamic colors for avg candle.

Plot/Table: Line color, positions, gradients, and visibility.

Ideal Use Case

Perfect for MESM2 scalpers and trend traders. Use the Main Table for entry confirmation via predicted deviations and institutional positioning. Leverage the New Metrics Table arrows for short-term signals—enter bullish on green consensus (all ↑), avoid chop on low volatility. Set alerts to catch shifts without constant monitoring.

Why It's Valuable

Info Table V1 consolidates diverse metrics into actionable visuals, answering critical questions: Is price mispriced? Is momentum aligning? Is volatility manageable? With real-time updates, consensus highlights, and extensive customization, it enhances precision in fast markets, reducing guesswork for confident trades.

Note: Optimized for futures; some metrics (OI, COT) unavailable on non-futures symbols. Test on demo accounts. No financial advice—use at your own risk.

The provided script reuses open-source elements from TradingView's Color Library and LuxAlgo's QQE Weighted Oscillator, as noted in the script comments and description. Credits are appropriately given in both the description and code comments, satisfying the requirement for attribution.

Regarding significant improvements and proportion:

The QQE logic comprises approximately 15 lines of code in a script exceeding 400 lines, representing a small proportion (<5%).

Adaptations include integration with multi-timeframe support via request.security, user-customizable inputs for length, factor, and smooth, and application within a broader table-based indicator for momentum bias display (with color gradients, arrows, and alerts). This extends the original QQE beyond standalone oscillator use, incorporating it as one of seven metrics in the New Metrics Table for confluence analysis (e.g., consensus highlighting when all metrics align). These are functional enhancements, not mere stylistic or variable changes.

The Color Library usage is via official import (import TradingView/Color/1 as Color), leveraging built-in gradient functions without copying code, and applied to enhance visual interpretation across multiple metrics.

The script complies with the rules: reused code is minimal, significantly improved through integration and expansion, and properly credited. It qualifies for open-source publication under the Mozilla Public License 2.0, as stated.

RSI Mansfield +RSI Mansfield+ – Adaptive Relative Strength Indicator with Divergences

Overview

RSI Mansfield+ is an advanced relative strength indicator that compares your instrument’s performance against a configurable benchmark index or asset (e.g., Bitcoin Dominance, S&P 500). It combines Mansfield normalization, adaptive smoothing techniques, and automatic detection of bullish and bearish divergences (regular and hidden), delivering a comprehensive tool for assessing relative strength across any market and timeframe.

Originality and Motivation

Unlike traditional relative strength scripts, this indicator introduces several distinctive improvements:

Mansfield Normalization: Scales the ratio between the asset and the benchmark relative to its moving average, transforming it into a normalized oscillator that fluctuates around zero, making it easier to spot outperformance or underperformance.

Adaptive Smoothing: Automatically selects whether to use EMA or SMA based on the market type (crypto or stocks) and timeframe (intraday, daily, weekly, monthly), avoiding manual configuration and providing more robust results under varying volatility conditions.

Divergence Detection: Identifies four types of divergences in the Mansfield oscillator to help anticipate potential reversal points or trend confirmations.

Multi-Market Support: Offers benchmark selection among major crypto and global stock indices from a single input.

These enhancements make RSI Mansfield+ more practical and powerful than conventional relative strength scripts with static benchmarks or without divergence capabilities.

Core Concepts

Relative Strength (RS): Compares price evolution between your asset and the selected benchmark.

Mansfield Normalization: Measures how much the RS deviates from its historical moving average, expressed as a scaled oscillator.

Divergences: Detects regular and hidden bullish or bearish divergences within the Mansfield oscillator.

Timeframe Adaptation: Dynamically adjusts moving average lengths based on timeframe and market type.

How It Works

Benchmark Selection

Choose among over 10 indices or market domains (BTC Dominance, ETH Dominance, S&P 500, European indices, etc.).

Ratio Calculation

Computes the price-to-benchmark ratio and smooths it with the adaptive moving average.

Normalization and Scaling

Transforms deviations into a Mansfield oscillator centered around zero.

Dynamic Coloring

Green indicates relative outperformance, red signals underperformance.

Divergence Detection

Automatically identifies bullish and bearish (regular and hidden) divergences by comparing oscillator pivots against price pivots.

Baseline Reference

A clear zero line helps interpret relative strength trends.

Usage Guidelines

Benchmark Comparison

Ideal for traders analyzing whether an asset is outperforming or lagging its sector or market.

Divergence Analysis

Helps detect potential reversal or continuation signals in relative strength.

Multi-Timeframe Compatibility

Can be applied to intraday, daily, weekly, or monthly charts.

Interpretation

Oscillator >0 and green: outperforming the benchmark.

Oscillator <0 and red: underperforming.

Bullish divergences: potential relative strength reversal to the upside.

Bearish divergences: possible loss of momentum or reversal to the downside.

Credits

The concept of Mansfield Relative Strength is based on Stan Weinstein’s original work on relative performance analysis. This script was built entirely from scratch in TradingView Pine Script v6, incorporating original logic for adaptive smoothing, normalized scaling, and divergence detection, without reusing any external open-source code.

Support Resistance with Order BlocksIndicator Description

Professional Price Level Detection for Smart Trading. Master the Markets with Precision Support/Resistance and Order Block Analysis . It provides traders with clear visual cues for potential reversal and breakout areas, combining both retail and institutional trading concepts into one powerful tool.

The Support & Resistance with Order Blocks indicator is a versatile Pine Script tool designed to empower traders with clear, actionable insights into key market levels. By combining advanced pivot-based support and resistance (S/R) detection with order block (OB) filtering, this indicator delivers clean, high-probability zones for entries, exits, and reversals. With customizable display options (boxes or lines) and intuitive settings, it’s perfect for traders of all styles—whether you’re scalping, swing trading, or investing long-term. Overlay it on your TradingView chart and elevate your trading strategy today!

________________________________________

Key Features

✅ Dynamic Support/Resistance - Auto-adjusting levels based on price action

✅ Smart Order Block Detection - Identifies institutional buying/selling zones

✅ Dual Display Modes - Choose between Boxes or Clean Lines for different chart styles

✅ Customizable Sensitivity - Adjust detection parameters for different markets

✅ Broken Level Markers - Clearly shows when key levels are breached

✅ Timeframe-Adaptive - Automatically adjusts for daily/weekly charts

1. Dynamic Support & Resistance Detection

Identifies critical S/R zones using pivot high/low calculations with adjustable look back periods.

Visualizes active S/R zones with distinct colors and labels ("Support" or "Resistance" for boxes, lines for cleaner charts).

Marks broken S/R levels as "Br S" (broken support) or "Br R" (broken resistance) when historical display is enabled, aiding in breakout and reversal analysis.

2. Smart Order Block Identification

Detects bullish and bearish order blocks based on significant price movements (default: ±0.3% over 5 candles).

Highlights institutional buying/selling zones with customizable colors, displayed as boxes or lines.

Filters out overlapping OB zones to keep your chart clutter-free.

3. Dual Display Options

Boxes or Lines: Choose to display S/R and OB as boxes for detailed zones or lines for a minimalist view.

Line Width Customization: Adjust line widths for S/R and OB (1–5 pixels) for optimal visibility.

Color Customization: Tailor colors for active/broken S/R and bullish/bearish OB zones.

4. Advanced Overlap Filtering

Ensures S/R zones don’t overlap with OB zones or other S/R levels, providing only the most relevant levels.

Limits the number of active zones (default: 10) to maintain chart clarity.

5. Historical S/R Visualization

Optionally display broken S/R levels with distinct colors and labels ("Br S" or "Br R") to track historical price reactions.

Broken levels are dynamically updated and removed (or retained) based on user settings.

6. Timeframe Adaptability

Automatically adjusts pivot detection for daily/weekly timeframes (40-candle look back) versus shorter timeframes (20-candle look back).

Works seamlessly across all asset classes (stocks, forex, crypto, etc.) and timeframes.

________________________________________

How It Works

• Support & Resistance:

Uses ta.pivothigh and ta.pivotlow to detect significant price pivots, with a user-defined look back (default: 5 candles post-pivot).

Plots S/R as boxes (with labels "Support" or "Resistance") or lines, extending to the current bar for real-time relevance.

Broken S/R levels are marked with adjusted colors and labels ("S" or "R" for boxes, "Br S" or "Br R" for lines when historical display is enabled).

• Order Blocks:

Identifies OB based on strong price movements over 4 candles, plotted as boxes or lines at the candle’s midpoint.

Validates OB to prevent overlap, ensuring only significant zones are displayed.

Removes OB zones when price breaks through, keeping the chart focused on active levels.

• Customization:

Toggle S/R and OB visibility, adjust detection sensitivity, and set maximum active zones (4–50).

Fine-tune line widths and colors for a personalized chart experience.

________________________________________

Why Use This Indicator?

• Precision Trading: Pinpoint high-probability entry/exit zones with filtered S/R and OB levels.

• Clean Charts: Overlap filtering and zone limits reduce clutter, focusing on key levels.

• Versatile Display: Switch between boxes for detailed zones or lines for simplicity, with adjustable line widths.

• Institutional Edge: Leverage OB detection to align with institutional activity for smarter trades.

• User-Friendly: Intuitive settings and clear visuals make it accessible for beginners and pros alike.

________________________________________

Settings Overview________________________________________

⚙ Input Parameters

Settings Overview

Display Options:

Display Type: Choose "Boxes" or "Lines" for S/R and OB visualization.

S/R Line Width: Set line thickness for S/R lines (1–5 pixels, default: 2).

OB Line Width: Set line thickness for OB lines (1–5 pixels, default: 2).

Order Block Options:

Show Order Block: Enable/disable OB display.

Bull/Bear OB Colors: Customise border and fill colors for bullish and bearish OB zones.

Support/Resistance Options:

Show S/R: Toggle active S/R zones.

Show Historical S/R: Display broken S/R levels, marked as "Br S" or "Br R" for lines.

Detection Period: Set candle lookback for pivot detection (4–50, default: 5).

Max Active Zones: Limit active S/R and OB zones (4–50, default: 10).

Colors: Customise active and broken S/R colors for clear differentiation.

________________________________________

How to Use

1. Add to Chart: Apply the indicator to your TradingView chart.

2. Customize Settings:

o Select "Boxes" or "Lines" for your preferred display style.

o Adjust line widths, colors, and detection parameters to suit your trading style.

o Enable "Show Historical S/R" to track broken levels with "Br S" and "Br R" labels.

3. Analyze Levels:

o Use support zones (green) for buy entries and resistance zones (red) for sell entries.

o Monitor OB zones for institutional activity, signaling potential reversals or continuations.

o Watch for "Br S" or "Br R" labels to identify breakout opportunities.

4. Combine with Other Tools: Pair with trend indicators, volume analysis, or price action for a robust strategy.

5. Monitor Breakouts: Trade breakouts when price breaches S/R or OB zones, with historical labels providing context.

________________________________________

Example Use Cases

• Swing Trading: Use S/R and OB zones to identify entry/exit points, with historical broken levels for context.

• Breakout Trading: Trade price breaks through S/R or OB, using "Br S" and "Br R" labels to confirm reversals.

• Scalping: Adjust detection period for faster S/R and OB identification on lower timeframes.

________________________________________

• Performance: Optimized for all timeframes, with best results on 5M, 15M, 30M, 1H, 4H, or daily charts for swing trading.

• Compatibility: Works with any asset class and TradingView chart.

________________________________________

Get Started

Transform your trading with Support & Resistance with Order Blocks! Add it to your chart, customize it to your style, and trade with confidence. For questions or feedback, drop a comment on TradingView or message the author. Happy trading! 🚀

________________________________________

Disclaimer: This indicator is for educational and informational purposes only. Always conduct your own analysis and practice proper risk management before trading.

X ORTX ORT — Opening Range & Time Reference Tool

Overview

The X ORT indicator is a precision tool designed for intraday traders seeking to anchor their trading decisions to high-probability price levels. It captures key market reference points including Opening Ranges, Settlement Prices, and Time-Specific Opens, all based on New York time, to help identify potential pivots and directional bias in the market.

Key Features & Usage

🔹 Opening Range Boxes (ORs)

The indicator defines up to two customizable Opening Ranges (e.g., 9:30–9:59 and 8:20–8:49 ET). Each range dynamically tracks the high, low, and midpoint price as the session unfolds, and continues to extend those levels forward throughout the day.