Top-Down Analysis - Multi-Timeframe AlignmentThis indicator implements a Top-Down Multi-Timeframe Trading Analysis System. Here's what it does:

Core Functionality

1. Multi-Timeframe Bias Detection

Monitors three timeframes: Daily, 4-Hour, and 1-Hour

Determines if each timeframe is bullish, bearish, or neutral based on two EMAs (9 and 21 period by default)

A timeframe is bullish when: Fast EMA > Slow EMA AND price is above Fast EMA

A timeframe is bearish when: Fast EMA < Slow EMA AND price is below Fast EMA

2. Alignment Tier System

Tier 1 (Full Alignment): All three timeframes agree (Daily = 4H = 1H direction)

Tier 2 (Partial Alignment): Daily and 1H agree, but 4H differs

No Alignment: Timeframes disagree

3. Previous Day Support & Resistance Levels

Automatically plots key levels from the previous day:

Previous Day High (PDH) - resistance

Previous Day Low (PDL) - support

Previous Day Close (PDC)

Previous Day Midpoint (PDM)

4. Execution Zone (15-Minute Window)

Highlights the first 15 minutes after each new 4H candle opens

This is the optimal entry window when alignment conditions are met

5. Pattern Recognition

Detects trading setups:

Double tops/bottoms

Long wicks at support/resistance

Bullish/bearish closes aligned with bias

6. Trade Signals

Generates entry signals when:

There's Tier 1 or Tier 2 alignment

Price is in the 15-minute execution zone

A valid pattern forms (double top/bottom or wick rejection)

7. Visual Dashboard

Shows a real-time table with:

Each timeframe's current bias

Alignment status

Next 4H prediction

Whether price is at a key support/resistance level

Trading Strategy

The indicator helps traders follow the principle of "trade with the higher timeframe trend" by only taking trades when multiple timeframes agree, focusing entries during specific windows, and respecting previous day's key price levels as potential reaction zones.

Cari dalam skrip untuk "如何用wind搜索股票的发行价和份数"

Forex Session TrackerForex Session Tracker - Professional Trading Session Indicator

The Forex Session Tracker is a comprehensive and visually intuitive indicator designed specifically for forex traders who need precise tracking of major global trading sessions. This powerful tool helps traders identify active market sessions, monitor session-specific price ranges, and capitalize on volatility patterns unique to each trading period.

Understanding when major financial centers are active is crucial for forex trading success. This indicator provides real-time visualization of the Tokyo, London, New York, and Sydney trading sessions, allowing traders to align their strategies with peak liquidity periods and avoid low-volatility trading windows.

---

Key Features

📊 Four Major Global Trading Sessions

The indicator tracks all four primary forex trading sessions with precision:

- Tokyo Session (Asian Market) - Captures the Asian trading hours, ideal for JPY, AUD, and NZD pairs

- London Session (European Market) - Monitors the most liquid trading period, perfect for EUR, GBP pairs

- New York Session (American Market) - Tracks US market hours, essential for USD-based currency pairs

- Sydney Session (Pacific Market) - Identifies the opening of the trading week and AUD/NZD activity

Each session is fully customizable with individual color schemes, making it easy to distinguish between different market periods at a glance.

🎯 Session Range Visualization

For each active trading session, the indicator automatically:

- Draws rectangular boxes that highlight the session's time period

- Tracks and displays session HIGH and LOW price levels in real-time

- Creates horizontal lines at session extremes for easy reference

- Positions session labels at the center of each trading period

- Updates dynamically as new highs or lows are formed within the session

This visual approach helps traders quickly identify:

- Session breakout opportunities

- Support and resistance zones formed during specific sessions

- Range-bound vs. trending session behavior

- Key price levels that institutional traders are watching

📱 Live Information Dashboard

A sleek, professional information panel displays:

- Real-time session status - Instantly see which sessions are currently active

- Color-coded indicators - Green dots for active sessions, gray for closed sessions

- Timezone information - Confirms your current timezone settings

- Customizable positioning - Place the dashboard anywhere on your chart (Top Left, Top Right, Bottom Left, Bottom Right)

- Adjustable size - Choose from Tiny, Small, Normal, or Large text sizes for optimal visibility

The dashboard provides at-a-glance awareness of market conditions without cluttering your chart analysis.

⚙️ Extensive Customization Options

Every aspect of the indicator can be tailored to your trading preferences:

Session-Specific Controls:

- Enable/disable individual sessions

- Customize colors for each trading period

- Adjust session times to match your broker's server time

- Toggle background highlighting on/off

- Show/hide session high/low lines independently

General Settings:

- UTC Offset Control - Adjust timezone from UTC-12 to UTC+14

- Exchange Timezone Option - Automatically use your chart's exchange timezone

- Background Transparency - Fine-tune the opacity of session highlighting (0-100%)

- Session Labels - Show or hide session name labels

- Information Panel - Toggle the live status dashboard on/off

Style Settings:

- Turn session backgrounds ON/OFF directly from the Style tab

- Maintain clean charts while keeping all analytical features active

🔔 Built-in Alert System

Stay informed about session openings with customizable alerts:

- Tokyo Session Started

- London Session Started

- New York Session Started

- Sydney Session Started

Set up notifications to never miss important market opening periods, even when you're away from your charts.

---

How to Use This Indicator

For Day Traders:

1. Identify High-Volatility Periods - Focus your trading during London and New York session overlaps for maximum liquidity

2. Monitor Session Breakouts - Watch for price breaks above/below session highs and lows

3. Avoid Low-Volume Periods - Recognize when major sessions are closed to avoid false signals

For Swing Traders:

1. Mark Key Levels - Use session highs and lows as support/resistance zones

2. Track Multi-Session Patterns - Observe how price behaves across different trading sessions

3. Plan Entry/Exit Points - Time your trades around session openings for better execution

For Currency-Specific Traders:

1. JPY Pairs - Focus on Tokyo session movements

2. EUR/GBP Pairs - Monitor London session activity

3. USD Pairs - Track New York session volatility

4. AUD/NZD Pairs - Watch Sydney and Tokyo sessions

---

Technical Specifications

- Pine Script Version: 5

- Overlay Indicator: Yes (displays directly on price chart)

- Maximum Bars Back: 500

- Drawing Objects: Up to 500 lines, boxes, and labels

- Performance: Optimized for real-time data processing

- Compatibility: Works on all timeframes (recommended: 5m to 1H for session tracking)

---

Installation & Setup

1. Add to Chart - Click "Add to Chart" after copying the script to Pine Editor

2. Configure Timezone - Set your UTC offset or enable "Use Exchange Timezone"

3. Customize Colors - Choose your preferred color scheme for each session

4. Adjust Display - Enable/disable features based on your trading style

5. Set Alerts - Create alert notifications for session starts

---

Best Practices

✅ Combine with Price Action - Use session ranges alongside candlestick patterns for confirmation

✅ Watch Session Overlaps - The London-New York overlap (1300-1600 UTC) typically shows highest volatility

✅ Respect Session Highs/Lows - These levels often act as intraday support and resistance

✅ Adjust for Your Broker - Verify session times match your broker's server clock

✅ Use Multiple Timeframes - View sessions on both lower (15m) and higher (1H) timeframes for context

---

Why Choose Forex Session Tracker Pro?

✨ Professional Grade Tool - Built with clean, efficient code following TradingView best practices

✨ Beginner Friendly - Intuitive design with clear visual cues

✨ Highly Customizable - Adapt every feature to match your trading style

✨ Performance Optimized - Lightweight code that won't slow down your charts

✨ Actively Maintained - Regular updates and improvements

✨ No Repainting - All visual elements are fixed once the session completes

---

Support & Updates

This indicator is designed to provide reliable, accurate session tracking for forex traders of all experience levels. Whether you're a scalper looking for high-volatility windows or a position trader marking key institutional levels, the Forex Session Tracker Pro delivers the insights you need to make informed trading decisions.

Happy Trading! 📈

---

Disclaimer

This indicator is a tool for technical analysis and should be used as part of a comprehensive trading strategy. Past performance does not guarantee future results. Always practice proper risk management and never risk more than you can afford to lose. Trading forex carries a high level of risk and may not be suitable for all investors.

[Statistics] killzone SFPSFP Statistics (ICT Sessions)

This indicator automatically finds and draws the high and low of the Asia, London, and New York trading sessions. It then hunts for Swing Failure Patterns (SFPs) that sweep these key session levels.

The main purpose of this script is to gather statistics on when these high-probability SFPs occur, allowing you to map out and identify the times of day when they are most frequent.

How to Use This Indicator

Set Your SFP Timeframe: In the settings, choose the timeframe you want to hunt for SFPs on (e.g., 1H, 15m). Important: You must also set your main chart to this exact same timeframe for the statistics to be collected correctly.

Define Your Sessions: Go to the "Session Definitions" tab.

Set the Global Timezone to your preferred trading timezone (e.g., "America/New_York"). This controls all session times and table times.

Adjust the start and end times for Asia, London, and NY AM sessions.

You can turn off sessions you don't want to track (like NY Lunch or NY PM).

You can also change the colors and text style for the session boxes here.

Set Confirmation Bars: In "SFP Engine Settings," the "Confirmation Bars" (default is 2) defines how many bars must close after the SFP bar without invalidating the level. An SFP is only "confirmed" and drawn after this period.

0 = Confirms immediately on the SFP candle's close.

2 = Confirms 2 bars after the SFP candle's close.

Read the Statistics: The "Custom SFP Statistics" table will appear on your chart. This table logs every confirmed SFP and tells you:

Which time of day they happen most.

How many were Bearish (swept a high) vs. Bullish (swept a low).

It's set by default to show the "Top 20" most frequent times, sorted chronologically.

Filter Your Chart (Optional): If your chart feels cluttered, go to "Visual Time Filter" and turn it ON.

Set a time window (e.g., "09:30-11:00").

The indicator will now only draw SFP signals that occurred within that specific time window. This is perfect for focusing on a single killzone.

How to Set Up Alerts

You can set up server-side alerts to be notified every time a new SFP is confirmed.

Check the "Enable SFP Alerts" box at the top of the indicator's settings.

Click the "Alert" button (alarm clock icon) on the TradingView toolbar.

In the "Condition" dropdown, select "SFP Statistics (ICT Sessions)".

In the second dropdown, choose "Any alert() function call".

Most Important Step: In the "Message" box, delete any default text and type in this exact placeholder:

{{alert_message}}

Set the trigger to "Once Per Bar Close".

Click "Create".

How Alerts Work (Triggers & Filtering)

Trigger: Alerts are tied to the confirmed signal. An alert will only fire after your "Confirmation Bars" have passed and the SFP is locked in. This prevents you from getting alerts on fake-outs.

Alert Filtering: The alerts are linked to the "Visual Time Filter". If you turn on the Visual Time Filter (e.g., to 09:30-11:00), you will only receive alerts for SFPs that are confirmed within that time window. If an SFP happens at 14:00, the script will ignore it, it will not be drawn, and it will not send you an alert. This allows you to get alerts only for the session you are actively trading.

Note: This is a first draft of this indicator. I will continue to work on it and improve it over time, as it may still contain small bugs.

Acknowledgements:

A big thank you to TFO (tradeforopp). The session detection logic and the visual style for the session boxes were adapted from his excellent "ICT Killzones & Pivots " indicator.

US/SPY- Financial Regime Index Swing Strategy Credits: concept inspired by EdgeTools Bloomberg Financial Conditions Index (Proxy)

Improvements: eight component basket, inverse volatility weights, winsorization option( statistical technique used to limit the influence of outliers in a dataset by replacing extreme values with less extreme ones, rather than removing them entirely), slope and price gates, exit guards, table and gradients.

Summary in one paragraph

A macro regime swing strategy for index ETFs, futures, FX majors, and large cap equities on daily calculation with optional lower time execution. It acts only when a composite Financial Conditions proxy plus slope and an optional price filter align. Originality comes from an eight component macro basket with inverse volatility weights and winsorized return z scores that produce a portable yardstick.

Scope and intent

Markets: SPY and peers, ES futures, ACWI, liquid FX majors, BTC, large cap equities.

Timeframes: calculation daily by default, trade on any chart.

Default demo: SPY on Daily.

Purpose: convert broad financial conditions into clear swing bias and exits.

Originality and usefulness

Unique fusion: return z scores for eight liquid proxies with inverse volatility weighting and optional winsorization, then slope and price gates.

Failure mode addressed: false starts in chop and early shorts during easy liquidity.

Testability: all knobs are inputs and the table shows components and weights.

Portable yardstick: z scores center at zero so thresholds transfer across symbols.

Method overview in plain language

Base measures

Return basis: natural log return over a configurable window, standardized to a z score. Winsorization optional to cap extremes.

Components

EQ US and EQ GLB measure equity tone.

CREDIT uses LQD over HYG. Higher credit quality outperformance is risk off so sign is flipped after z score.

RATES2Y uses two year yield, sign flipped.

SLOPE uses ten minus two year yield spread.

USD uses DXY, sign flipped.

VOL uses VIX, sign flipped.

LIQ uses BIL over SPY, sign flipped.

Each component is smoothed by the composite EMA.

Fusion rule

Weighted sum where weights are equal or inverse volatility with exponent gamma, normalized to percent so they sum to one.

Signal rule

Long when composite crosses up the long threshold and its slope is positive and price is above the SMA filter, or when composite is above the configured always long floor.

Short when composite crosses down the short threshold and its slope is negative and price is below the SMA filter.

Long exit on cross down of the long exit line or on a fresh short signal.

Short exit on cross up of the short exit line or on a fresh long signal, or when composite falls below the force short exit guard.

What you will see on the chart

Markers on suggestion bars: L for long, S for short, LX and SX for exits.

Reference lines at zero and soft regime bands at plus one and minus one.

Optional background gradient by regime intensity.

Compact table with component z, weight percent, and composite readout.

Table fields and quick reading guide

Component: EQ US, EQ GLB, CREDIT, RATES2Y, SLOPE, USD, VOL, LIQ.

Z: current standardized value, green for positive risk tone where applicable.

Weight: contribution percent after normalization.

Composite: current index value.

Reading tip: a broadly green Z column with slope positive often precedes better long context.

Inputs with guidance

Setup

Calc timeframe: default Daily. Leave blank to inherit chart.

Lookback: 50 to 1500. Larger length stabilizes regimes and delays turns.

EMA smoothing: 1 to 200. Higher smooths noise and delays signals.

Normalization

Winsorize z at ±3: caps extremes to reduce one off shocks.

Return window for equities: 5 to 260. Shorter reacts faster.

Weighting

Weight lookback: 20 to 520.

Weight mode: Equal or InvVol.

InvVol exponent gamma: 0.1 to 3. Higher compresses noisy components more.

Signals

Trade side: Long Short or Both.

Entry threshold long and short: portable z thresholds.

Exit line long and short: soft exits that give back less.

Slope lookback bars: 1 to 20.

Always long floor bfci ≥ X: macro easy mode keep long.

Force short exit when bfci < Y: macro stress guard.

Confirm

Use price trend filter and Price SMA length.

View

Glow line and Show component table.

Symbols

SPY ACWI HYG LQD VIX DXY US02Y US10Y BIL are defaults and can be changed.

Realism and responsible publication

No performance claims. Past is not future.

Shapes can move intrabar and settle on close.

Execution is on standard candles only.

Honest limitations and failure modes

Major economic releases and illiquid sessions can break assumptions.

Very quiet regimes reduce contrast. Use longer windows or higher thresholds.

Component proxies are ETFs and indexes and cannot match a proprietary FCI exactly.

Strategy notice

Orders are simulated on standard candles. All security calls use lookahead off. Nonstandard chart types are not supported for strategies.

Entries and exits

Long rule: bfci cross above long threshold with positive slope and optional price filter OR bfci above the always long floor.

Short rule: bfci cross below short threshold with negative slope and optional price filter.

Exit rules: long exit on bfci cross below long exit or on a short signal. Short exit on bfci cross above short exit or on a long signal or on force close guard.

Position sizing

Percent of equity by default. Keep target risk per trade low. One percent is a sensible starting point. For this example we used 3% of the total capital

Commisions

We used a 0.05% comission and 5 tick slippage

Legal

Education and research only. Not investment advice. Test in simulation first. Use realistic costs.

Cora Combined Suite v1 [JopAlgo]Cora Combined Suite v1 (CCSV1)

This is an 2 in 1 indicator (Overlay & Oscillator) the Cora Combined Suite v1 .

CCSV1 combines a price-pane Overlay for structure/trend with a compact Oscillator for timing/pressure. It’s designed to be clear, beginner-friendly, and largely automatic: you pick a profile (Scalp / Intraday / Swing), choose whether to run as Overlay or Oscillator, and CCSV1 tunes itself in the background.

What’s inside — at a glance

1) Overlay (price pane)

CoRa Wave: a smooth trend line based on a compound-ratio WMA (CRWMA).

Green when the slope rises (bull bias), Red when it falls (bear bias).

Asymmetric ATR Cloud around the CoRa Wave

Width expands more up when buyer pressure dominates and more down when seller pressure dominates.

Fill is intentionally light, so candlesticks remain readable.

Chop Guard (Range-Lock Gate)

When the cloud stays very narrow versus ATR (classic “dead water”), pullback alerts are muted to avoid noise.

Visuals don’t change—only the alerting logic goes quiet.

Typical Overlay reads

Trend: Follow the CoRa color; green favors long setups, red favors shorts.

Value: Pullbacks into/through the cloud in trend direction are higher-quality than chasing breaks far outside it.

Dominance: A visibly asymmetric cloud hints which side is funding the move (buyers vs sellers).

2) Oscillator (subpane or inline preview)

Stretch-Z (columns): how far price is from the CoRa mean (mean-reversion context), clipped to ±clip.

Near 0 = equilibrium; > +2 / < −2 = stretched/extended.

Slope-Z (line): z-score of CoRa’s slope (momentum of the trend line).

Crossing 0 upward = potential bullish impulse; downward = potential bearish impulse.

VPO (stepline): a normalized Volume-Pressure read (positive = buyers funding, negative = sellers).

Rendered as a clean stepline to emphasize state changes.

Event Bands ±2 (subpane): thin reference lines to spot extension/exhaustion zones fast.

Floor/Ceiling lines (optional): quiet boundaries so the panel doesn’t feel “bottomless.”

Inline vs Subpane

Inline (overlay): the oscillator auto-anchors and scales beneath price, so it never crushes the price scale.

Subpane (raw): move to a new pane for the classic ±clip view (with ±2 bands). Recommended for systematic use.

Why traders like it

Two in one: Structure on the chart, timing in the panel—built to complement each other.

Retail-first automation: Choose Scalp / Intraday / Swing and let CCSV1 auto-tune lengths, clips, and pressure windows.

Robust statistics: On fast, spiky markets/timeframes, it prefers outlier-resistant math automatically for steadier signals.

Optional HTF gate: You can require higher-timeframe agreement for oscillator alerts without changing visuals.

Quick start (simple playbook)

Run As

Overlay for structure: assess trend direction, where value is (the cloud), and whether chop guard is active.

Oscillator for timing: move to a subpane to see Stretch-Z, Slope-Z, VPO, and ±2 bands clearly.

Profile

Scalp (1–5m), Intraday (15–60m), or Swing (4H–1D). CCSV1 adjusts length/clip/pressure windows accordingly.

Overlay entries

Trade with CoRa color.

Prefer pullbacks into/through the cloud (trend direction).

If chop guard is active, wait; let the market “breathe” before engaging.

Oscillator timing

Look for Funded Flips: Slope-Z crossing 0 in the direction of VPO (i.e., momentum + funded pressure).

Use ±2 bands to manage risk: stretched conditions can stall or revert—better to scale or wait for a clean reset.

Optional HTF gate

Enable to green-light only those oscillator alerts that align with your chosen higher timeframe.

What each signal means (plain language)

CoRa turns green/red (Overlay): trend bias shift on your chart.

Cloud width tilts asymmetrically: one side (buyers/sellers) is dominating; extensions on that side are more likely.

Stretch-Z near 0: fair value around CoRa; pullback timing zone.

Stretch-Z > +2 / < −2: extended; watch for slowing momentum or scale decisions.

Slope-Z cross up/down: new impulse starting; combine with VPO sign to avoid unfunded crosses.

VPO positive/negative: net buying/selling pressure funding the move.

Alerts included

Overlay

Pullback Long OK

Pullback Short OK

Oscillator

Funded Flip Up / Funded Flip Down (Slope-Z crosses 0 with VPO agreement)

Pullback Long Ready / Pullback Short Ready (near equilibrium with aligned momentum and pressure)

Exhaustion Risk (Long/Short) (Stretch-Z beyond ±2 with weakening momentum or pressure)

Tip: Keep chart alerts concise and use strategy rules (TP/SL/filters) in your trade plan.

Best practices

One glance workflow

Read Overlay for direction + value.

Use Oscillator for trigger + confirmation.

Pairing

Combine with S/R or your preferred execution framework (e.g., your JopAlgo setups).

The suite is neutral: it won’t force trades; it highlights context and quality.

Markets

Works on crypto, indices, FX, and commodities.

Where real volume is available, VPO is strongest; on synthetic volume, treat VPO as a soft filter.

Timeframes

Use the Profile preset closest to your style; feel free to fine-tune later.

For multi-TF trading, enable the HTF gate on the oscillator alerts only.

Inputs you’ll actually use (the rest can stay on Auto)

Run As: Overlay or Oscillator.

Profile: Scalp / Intraday / Swing.

Oscillator Render: “Subpane (raw)” for a classic panel; “Inline (overlay)” only for a quick preview.

HTF gate (optional): require higher-timeframe Slope-Z agreement for oscillator alerts.

Everything else ships with sensible defaults and auto-logic.

Limitations & tips

Not a strategy: CCSV1 is a decision support tool; you still need your entry/exit rules and risk management.

Non-repainting design: Signals finalize on bar close; intrabar graphics can adjust during the bar (Pine standard).

Very flat sessions: If price and volume are extremely quiet, expect fewer alerts; that restraint is intentional.

Who is this for?

Beginners who want one clean overlay for structure and one simple oscillator for timing—without wrestling settings.

Intermediates seeking a coherent trend/pressure framework with HTF confirmation.

Advanced users who appreciate robust stats and clean engineering behind the visuals.

Disclaimer: Educational purposes only. Not financial advice. Trading involves risk. Use at your own discretion.

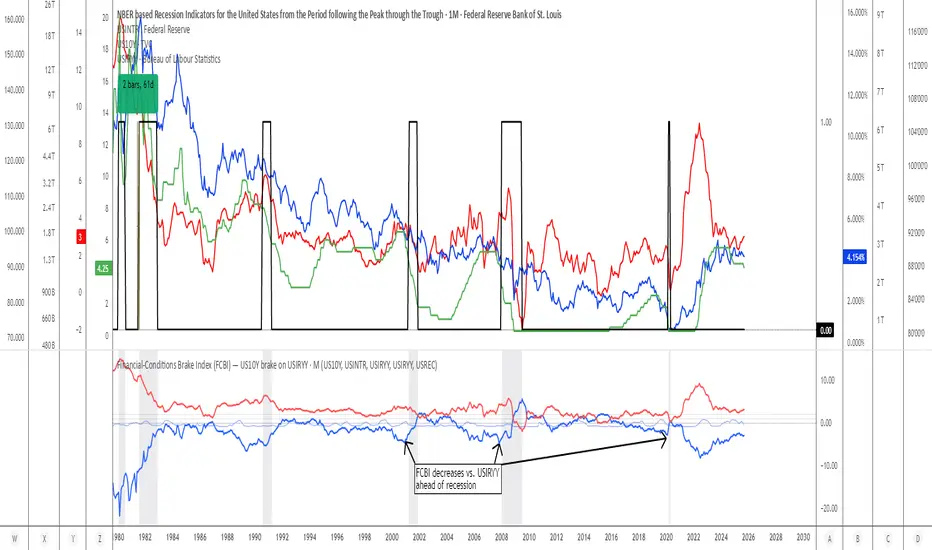

Financial-Conditions Brake Index (FCBI) — US10Y brake on USIRYYFinancial-Conditions Brake Index (FCBI) – US10Y Brake on USIRYY

Concept

The Financial-Conditions Brake Index (FCBI) measures how U.S. long-term yields (US10Y) interact with the Federal Funds Rate (USINTR) and inflation (CPI YoY) to shape real-rate conditions (USIRYY).

It visualizes whether the bond market is tightening or loosening overall financial conditions relative to the Federal Reserve’s policy stance.

Formula

FCBI = (US10Y) − (USINTR) − (CPI YoY)

How It Works

The FCBI expresses the difference between the long-term yield curve and short-term policy rates, adjusted for inflation. It shows whether the long end of the curve is amplifying or counteracting the Fed’s stance.

FCBI > +2 → Strong brake → Long yields remain elevated despite easing → tight conditions → recession delayed.

FCBI +1 to +2 → Mild brake → Financial transmission slower; lag ≈ 12–18 months.

FCBI 0 to +1 → Neutral → Typical early post-cut environment.

FCBI < 0 → Accelerator → Long yields and inflation expectations falling → liquidity flows freely → recession often follows within 6–14 months.

How to Read the Chart

Blue line (FCBI) shows the strength of the financial brake.

Red line (USIRYY) represents the real yield baseline.

Recession shading (gray) marks NBER recessions for comparison.

FCBI < USIRYY → Brake engaged → financial conditions tighter than real-rate baseline.

FCBI > USIRYY → Brake released → long end easing faster than policy → liquidity surge → late-cycle setup.

Historically, U.S. recessions begin on average about 14 months after the first Fed rate cut, and a decline of the FCBI below zero often precedes that window.

Practical Use

Use the FCBI to identify when policy transmission is blocked (brake engaged) or flowing (brake released).

Cross-check with yield-curve inversions, Fed policy shifts, and inflation expectations to estimate macro timing windows.

Current Example (Oct 2025)

FCBI ≈ −3.1, USIRYY ≈ +3.0 → Brake still engaged.

Once FCBI rises above USIRYY and crosses positive, it signals the “brake released” phase — historically the final liquidity surge before a U.S. recession.

Summary

FCBI shows how tight the brake is.

USIRYY shows how fast the car is moving.

When FCBI rises above USIRYY, the brake is released — liquidity accelerates and the historical recession countdown begins.

Asia & London Session High/Low – EOD Segments (v4.5)What it does

Plots the Asia and London session high & low each day.

When a session ends, its high/low are locked (non-repainting) and drawn as horizontal segments that auto-extend to the end of that same day (no infinite rays).

Optional labels show the exact level at session close.

Toggle whether to keep prior days on the chart or auto-clear them on the first bar of a new day.

Why traders use it

Quickly see overnight liquidity levels that often act as magnets or barriers during the U.S. session.

Map session range extremes for breakout/reversal planning, partials, and invalidation.

Works great alongside VWAP, 8/20/200 MAs, or your NY session tools to build confluence.

How it works

You define the session windows (defaults: Asia 00:00–06:00, London 07:00–11:00).

While a session is active, the script tracks running high/low.

On the bar after the session ends, the level is finalized and drawn; the segment’s right edge updates each bar until EOD, then stops automatically.

Inputs

Session Timezone: “Exchange”, UTC, or a specific region (set this to match your venue).

Asia / London Session: editable HHMM-HHMM windows.

Show Asia / Show London: enable either/both sessions.

Keep history: keep or auto-delete previous days.

Show labels: price labels at session close.

Colors & width: customize high/low colors and line width.

Best practices

Use on intraday timeframes (1–60m).

For equities/futures, set timezone to your exchange (e.g., America/New_York). For FX/crypto, pick what matches your workflow.

Common tweak: London 08:00–12:00 local; Asia 00:00–05:00 or your broker’s definition.

Notes

Non-repainting: levels only print once the session is complete.

Designed to be light and reliable—no boxes, just clean lines and labels.

If you want NY session levels, midlines (50%), anchored stop-time, or alerts on touches, this script can be extended.

For educational use only. Not financial advice.

Custom Net ATR Mapping - NateThis indicator measures how much an asset actually moves — both on average and across full periods — so traders can compare short-term volatility with longer-term net momentum.

It displays four key metrics in a simple color-coded table:

Standard ATR – the average daily (or per-bar) range, showing typical volatility.

Net ATR – the average open-to-close move, revealing how much price tends to travel directionally within each bar.

Total Net Move – the total distance price has moved from the start to the end of the most recent measurement window.

Average Net Move – the typical size of that full-period move, averaged across multiple recent windows.

Together these readings help you see whether recent price action is choppy but contained (high ATR, low net move) or sustained and directional (high net move relative to ATR) — useful for spotting trend strength, breakout potential, or range-bound conditions.

Jensen Alpha RS🧠 Jensen Alpha RS (J-Alpha RS)

Jensen Alpha RS is a quantitative performance evaluation tool designed to compare multiple assets against a benchmark using Jensen’s Alpha — a classic risk-adjusted return metric from modern portfolio theory.

It helps identify which assets have outperformed their benchmark on a risk-adjusted basis and ranks them in real time, with optional gating and visual tools. 📊

✨ Key Features

• 🧩 Multi-Asset Comparison: Evaluate up to four assets simultaneously.

• 🔀 Adaptive Benchmarking: TOTALES mode uses CRYPTOCAP:TOTALES (total crypto market cap ex-stablecoins). Dynamic mode automatically selects the strongest benchmark among BTC, ETH, and TOTALES based on rolling momentum.

• 📐 Jensen’s Alpha Calculation: Uses rolling covariance, variance, and beta to estimate α, showing how much each asset outperformed its benchmark.

• 📈 Z-Score & Consistency Metrics: Z-Score highlights statistical deviations in alpha; Consistency % shows how often α has been positive over a chosen window.

• 🚦 Trend & Zero Gates: Optional filters that require assets to be above EMA (trend) and/or have α > 0 for confirmation.

• 🏆 Leaders Board Table: Displays α, Z, Rank, Consistency %, and Gate ✓/✗ for all assets in a clear visual layout.

• 🔔 Dynamic Alerts: Get notified whenever the top alpha leader changes on confirmed (non-repainting) data.

• 🎨 Visual Enhancements: Smooth α with an SMA or color bars by the current top-performing asset.

🧭 Typical Use Cases

• 🔄 Portfolio Rotation & Relative Strength: Identify which assets consistently outperform their benchmark to optimize capital allocation.

• 🧮 Alpha Persistence Analysis: Gauge whether a trend’s performance advantage is statistically sustainable.

• 🌐 Market Regime Insight: Observe how asset leadership rotates as benchmarks shift across market cycles.

⚙️ Inputs Overview

• 📝 Assets (1–4): Select up to four tickers for evaluation.

• 🧭 Benchmark Mode: Choose between static TOTALES or Dynamic auto-selection.

• 📏 Alpha Settings: Adjustable lookback, smoothing, and consistency windows.

• 🚦 Gates: Optional trend and alpha filters to refine results.

• 🖥️ Display: Enable/disable table and customize colors.

• 🔔 Alerts: Toggle notifications on leadership changes.

🔎 Formula Basis

Jensen’s Alpha (α) is estimated as:

α = E − β × E

where β = Cov(Ra, Rb) / Var(Rb), and Ra/Rb represent asset and benchmark returns, respectively.

A positive α indicates outperformance relative to the risk-adjusted benchmark expectation. ✅

⚠️ Disclaimer

This script is for educational and analytical purposes only.

It is NOT a signal. 🚫📉

It does not constitute financial advice, trading signals, or investment recommendations. 💬

The author is not responsible for any financial losses or trading decisions made based on this indicator. 🙏

Always perform your own analysis and use proper risk management. 🛡️

Session Volume Spike DetectorSession Volume Spike Detector (Buy/Sell, Dual Windows, MTF + Edge/Cooldown)

What it does

Detects statistically significant buy/sell volume spikes inside two DST-aware Mountain Time sessions and projects 1m / 5m / 10m signals onto any chart timeframe (even 1s). Spikes are confirmed at the close of their native bar and are edge-triggered with optional cooldowns to prevent duplicate alerts.

How spikes are detected

Volume ≥ SMA × multiplier

Optional jump vs recent highest volume

Optional Z-Score gate for significance

Separate Buy/Sell logic using your Direction Mode (Prev Close or Candle Body)

Multi-Timeframe (MTF) display

Shows 1m, 5m, 10m arrows on your current chart

Each HTF fires once on its bar close (no repaint after close)

Sessions (DST-aware, MT)

Morning: 05:30–08:30

Midday: 11:00–13:30

Spikes only count inside these windows.

Inputs & styling

Thresholds: SMA length, multipliers, recent lookback, Z-Score toggle/level

Toggles for which TFs to display (chart TF, 1m, 5m, 10m)

Per-TF colors + cooldowns (seconds) for Any TF, 1m, 5m, 10m

Alerts (edge + cooldown)

MTF Volume Spike (Any TF) — fires on the first qualifying spike across enabled TFs

1m / 5m / 10m Volume Spike — per-TF alerts, Buy or Sell

Recommended: set alert Trigger = Once per bar close. Cooldowns tame “triggered too often” warnings.

Great with

FVG zones, bank/insto levels, session range breaks, and trend filters. Use the MTF arrows as a participation/pressure tell to confirm or fade moves.

Notes

Works on any symbol/timeframe; best viewed on 1m or sub-minute charts.

HTF spikes appear on the bar close of 1m/5m/10m respectively.

No dynamic plot titles; Pine v6-safe.

Short summary (≤250 chars):

MTF volume-spike detector for intraday sessions (DST-aware, MT). Projects 1m/5m/10m buy/sell spikes onto any chart, with edge-triggered alerts and per-TF cooldowns to prevent duplicates. Ideal for spotting institutional participation.

ORB 15m + MAs (v4.1)Session ORB Live Pro — Pre-Market Boxes & MA Suite (v4.1)

What it is

A precision Opening Range Breakout (ORB) tool that anchors every session to one specific 15-minute candle—then projects that same high/low onto lower timeframes so your 1m/5m levels always match the source 15m bar. Perfect for scalpers who want session structure without drift.

What it draws

Asia, Pre-London, London, Pre-New York, New York session boxes.

On 15m: only the high/low of the first 15-minute bar of each window (optionally persists for extra bars).

On 5m: mirrors the same 15m range, visible up to 10 bars.

On 1m: mirrors the same 15m range, visible up to 15 bars.

Levels update live while the 15m candle is forming, then lock.

Fully editable windows (easy UX)

Change session times with TradingView’s native input.session fields using the familiar format HHMM-HHMM:1234567. You can tweak each window independently:

Asia

Pre-London

London

Pre-New York

New York

Multi-TF logic (no guesswork)

Designed to show only on 1m, 5m, 15m (by default).

15m = ground truth. Lower timeframes never “recalculate a different range”—they mirror the 15m bar for that session, exactly.

Alerts

Optional breakout alerts when price closes above/below the session range.

Clean visuals

Per-session color controls (box + lines). Boxes extend only for the configured number of bars per timeframe, keeping charts uncluttered.

Built-in MA suite

SMA 50 and RMA 200.

Three extra MAs (SMA/EMA/RMA/WMA/HMA) with selectable color, width, and style (line, stepline, circles).

Why traders like it

Consistency: Lower-TF ranges always match the 15m source bar.

Speed: You see structure immediately—no waiting for N bars.

Control: Edit session times directly; tune how long boxes stay on chart per TF.

Clarity: Minimal, purposeful plotting with alerts when it matters.

Quick start

Set your session times via the five input.session fields.

Choose how long boxes persist on 1m/5m/15m.

Enable alerts if you want instant breakout notifications.

(Optional) Configure the MA suite for trend/bias context.

Best for

Intraday traders and scalpers who rely on repeatable session behavior and demand exact cross-TF alignment of ORB levels.

Small Business Economic Conditions - Statistical Analysis ModelThe Small Business Economic Conditions Statistical Analysis Model (SBO-SAM) represents an econometric approach to measuring and analyzing the economic health of small business enterprises through multi-dimensional factor analysis and statistical methodologies. This indicator synthesizes eight fundamental economic components into a composite index that provides real-time assessment of small business operating conditions with statistical rigor. The model employs Z-score standardization, variance-weighted aggregation, higher-order moment analysis, and regime-switching detection to deliver comprehensive insights into small business economic conditions with statistical confidence intervals and multi-language accessibility.

1. Introduction and Theoretical Foundation

The development of quantitative models for assessing small business economic conditions has gained significant importance in contemporary financial analysis, particularly given the critical role small enterprises play in economic development and employment generation. Small businesses, typically defined as enterprises with fewer than 500 employees according to the U.S. Small Business Administration, constitute approximately 99.9% of all businesses in the United States and employ nearly half of the private workforce (U.S. Small Business Administration, 2024).

The theoretical framework underlying the SBO-SAM model draws extensively from established academic research in small business economics and quantitative finance. The foundational understanding of key drivers affecting small business performance builds upon the seminal work of Dunkelberg and Wade (2023) in their analysis of small business economic trends through the National Federation of Independent Business (NFIB) Small Business Economic Trends survey. Their research established the critical importance of optimism, hiring plans, capital expenditure intentions, and credit availability as primary determinants of small business performance.

The model incorporates insights from Federal Reserve Board research, particularly the Senior Loan Officer Opinion Survey (Federal Reserve Board, 2024), which demonstrates the critical importance of credit market conditions in small business operations. This research consistently shows that small businesses face disproportionate challenges during periods of credit tightening, as they typically lack access to capital markets and rely heavily on bank financing.

The statistical methodology employed in this model follows the econometric principles established by Hamilton (1989) in his work on regime-switching models and time series analysis. Hamilton's framework provides the theoretical foundation for identifying different economic regimes and understanding how economic relationships may vary across different market conditions. The variance-weighted aggregation technique draws from modern portfolio theory as developed by Markowitz (1952) and later refined by Sharpe (1964), applying these concepts to economic indicator construction rather than traditional asset allocation.

Additional theoretical support comes from the work of Engle and Granger (1987) on cointegration analysis, which provides the statistical framework for combining multiple time series while maintaining long-term equilibrium relationships. The model also incorporates insights from behavioral economics research by Kahneman and Tversky (1979) on prospect theory, recognizing that small business decision-making may exhibit systematic biases that affect economic outcomes.

2. Model Architecture and Component Structure

The SBO-SAM model employs eight orthogonalized economic factors that collectively capture the multifaceted nature of small business operating conditions. Each component is normalized using Z-score standardization with a rolling 252-day window, representing approximately one business year of trading data. This approach ensures statistical consistency across different market regimes and economic cycles, following the methodology established by Tsay (2010) in his treatment of financial time series analysis.

2.1 Small Cap Relative Performance Component

The first component measures the performance of the Russell 2000 index relative to the S&P 500, capturing the market-based assessment of small business equity valuations. This component reflects investor sentiment toward smaller enterprises and provides a forward-looking perspective on small business prospects. The theoretical justification for this component stems from the efficient market hypothesis as formulated by Fama (1970), which suggests that stock prices incorporate all available information about future prospects.

The calculation employs a 20-day rate of change with exponential smoothing to reduce noise while preserving signal integrity. The mathematical formulation is:

Small_Cap_Performance = (Russell_2000_t / S&P_500_t) / (Russell_2000_{t-20} / S&P_500_{t-20}) - 1

This relative performance measure eliminates market-wide effects and isolates the specific performance differential between small and large capitalization stocks, providing a pure measure of small business market sentiment.

2.2 Credit Market Conditions Component

Credit Market Conditions constitute the second component, incorporating commercial lending volumes and credit spread dynamics. This factor recognizes that small businesses are particularly sensitive to credit availability and borrowing costs, as established in numerous Federal Reserve studies (Bernanke and Gertler, 1995). Small businesses typically face higher borrowing costs and more stringent lending standards compared to larger enterprises, making credit conditions a critical determinant of their operating environment.

The model calculates credit spreads using high-yield bond ETFs relative to Treasury securities, providing a market-based measure of credit risk premiums that directly affect small business borrowing costs. The component also incorporates commercial and industrial loan growth data from the Federal Reserve's H.8 statistical release, which provides direct evidence of lending activity to businesses.

The mathematical specification combines these elements as:

Credit_Conditions = α₁ × (HYG_t / TLT_t) + α₂ × C&I_Loan_Growth_t

where HYG represents high-yield corporate bond ETF prices, TLT represents long-term Treasury ETF prices, and C&I_Loan_Growth represents the rate of change in commercial and industrial loans outstanding.

2.3 Labor Market Dynamics Component

The Labor Market Dynamics component captures employment cost pressures and labor availability metrics through the relationship between job openings and unemployment claims. This factor acknowledges that labor market tightness significantly impacts small business operations, as these enterprises typically have less flexibility in wage negotiations and face greater challenges in attracting and retaining talent during periods of low unemployment.

The theoretical foundation for this component draws from search and matching theory as developed by Mortensen and Pissarides (1994), which explains how labor market frictions affect employment dynamics. Small businesses often face higher search costs and longer hiring processes, making them particularly sensitive to labor market conditions.

The component is calculated as:

Labor_Tightness = Job_Openings_t / (Unemployment_Claims_t × 52)

This ratio provides a measure of labor market tightness, with higher values indicating greater difficulty in finding workers and potential wage pressures.

2.4 Consumer Demand Strength Component

Consumer Demand Strength represents the fourth component, combining consumer sentiment data with retail sales growth rates. Small businesses are disproportionately affected by consumer spending patterns, making this component crucial for assessing their operating environment. The theoretical justification comes from the permanent income hypothesis developed by Friedman (1957), which explains how consumer spending responds to both current conditions and future expectations.

The model weights consumer confidence and actual spending data to provide both forward-looking sentiment and contemporaneous demand indicators. The specification is:

Demand_Strength = β₁ × Consumer_Sentiment_t + β₂ × Retail_Sales_Growth_t

where β₁ and β₂ are determined through principal component analysis to maximize the explanatory power of the combined measure.

2.5 Input Cost Pressures Component

Input Cost Pressures form the fifth component, utilizing producer price index data to capture inflationary pressures on small business operations. This component is inversely weighted, recognizing that rising input costs negatively impact small business profitability and operating conditions. Small businesses typically have limited pricing power and face challenges in passing through cost increases to customers, making them particularly vulnerable to input cost inflation.

The theoretical foundation draws from cost-push inflation theory as described by Gordon (1988), which explains how supply-side price pressures affect business operations. The model employs a 90-day rate of change to capture medium-term cost trends while filtering out short-term volatility:

Cost_Pressure = -1 × (PPI_t / PPI_{t-90} - 1)

The negative weighting reflects the inverse relationship between input costs and business conditions.

2.6 Monetary Policy Impact Component

Monetary Policy Impact represents the sixth component, incorporating federal funds rates and yield curve dynamics. Small businesses are particularly sensitive to interest rate changes due to their higher reliance on variable-rate financing and limited access to capital markets. The theoretical foundation comes from monetary transmission mechanism theory as developed by Bernanke and Blinder (1992), which explains how monetary policy affects different segments of the economy.

The model calculates the absolute deviation of federal funds rates from a neutral 2% level, recognizing that both extremely low and high rates can create operational challenges for small enterprises. The yield curve component captures the shape of the term structure, which affects both borrowing costs and economic expectations:

Monetary_Impact = γ₁ × |Fed_Funds_Rate_t - 2.0| + γ₂ × (10Y_Yield_t - 2Y_Yield_t)

2.7 Currency Valuation Effects Component

Currency Valuation Effects constitute the seventh component, measuring the impact of US Dollar strength on small business competitiveness. A stronger dollar can benefit businesses with significant import components while disadvantaging exporters. The model employs Dollar Index volatility as a proxy for currency-related uncertainty that affects small business planning and operations.

The theoretical foundation draws from international trade theory and the work of Krugman (1987) on exchange rate effects on different business segments. Small businesses often lack hedging capabilities, making them more vulnerable to currency fluctuations:

Currency_Impact = -1 × DXY_Volatility_t

2.8 Regional Banking Health Component

The eighth and final component, Regional Banking Health, assesses the relative performance of regional banks compared to large financial institutions. Regional banks traditionally serve as primary lenders to small businesses, making their health a critical factor in small business credit availability and overall operating conditions.

This component draws from the literature on relationship banking as developed by Boot (2000), which demonstrates the importance of bank-borrower relationships, particularly for small enterprises. The calculation compares regional bank performance to large financial institutions:

Banking_Health = (Regional_Banks_Index_t / Large_Banks_Index_t) - 1

3. Statistical Methodology and Advanced Analytics

The model employs statistical techniques to ensure robustness and reliability. Z-score normalization is applied to each component using rolling 252-day windows, providing standardized measures that remain consistent across different time periods and market conditions. This approach follows the methodology established by Engle and Granger (1987) in their cointegration analysis framework.

3.1 Variance-Weighted Aggregation

The composite index calculation utilizes variance-weighted aggregation, where component weights are determined by the inverse of their historical variance. This approach, derived from modern portfolio theory, ensures that more stable components receive higher weights while reducing the impact of highly volatile factors. The mathematical formulation follows the principle that optimal weights are inversely proportional to variance, maximizing the signal-to-noise ratio of the composite indicator.

The weight for component i is calculated as:

w_i = (1/σᵢ²) / Σⱼ(1/σⱼ²)

where σᵢ² represents the variance of component i over the lookback period.

3.2 Higher-Order Moment Analysis

Higher-order moment analysis extends beyond traditional mean and variance calculations to include skewness and kurtosis measurements. Skewness provides insight into the asymmetry of the sentiment distribution, while kurtosis measures the tail behavior and potential for extreme events. These metrics offer valuable information about the underlying distribution characteristics and potential regime changes.

Skewness is calculated as:

Skewness = E / σ³

Kurtosis is calculated as:

Kurtosis = E / σ⁴ - 3

where μ represents the mean and σ represents the standard deviation of the distribution.

3.3 Regime-Switching Detection

The model incorporates regime-switching detection capabilities based on the Hamilton (1989) framework. This allows for identification of different economic regimes characterized by distinct statistical properties. The regime classification employs percentile-based thresholds:

- Regime 3 (Very High): Percentile rank > 80

- Regime 2 (High): Percentile rank 60-80

- Regime 1 (Moderate High): Percentile rank 50-60

- Regime 0 (Neutral): Percentile rank 40-50

- Regime -1 (Moderate Low): Percentile rank 30-40

- Regime -2 (Low): Percentile rank 20-30

- Regime -3 (Very Low): Percentile rank < 20

3.4 Information Theory Applications

The model incorporates information theory concepts, specifically Shannon entropy measurement, to assess the information content of the sentiment distribution. Shannon entropy, as developed by Shannon (1948), provides a measure of the uncertainty or information content in a probability distribution:

H(X) = -Σᵢ p(xᵢ) log₂ p(xᵢ)

Higher entropy values indicate greater unpredictability and information content in the sentiment series.

3.5 Long-Term Memory Analysis

The Hurst exponent calculation provides insight into the long-term memory characteristics of the sentiment series. Originally developed by Hurst (1951) for analyzing Nile River flow patterns, this measure has found extensive application in financial time series analysis. The Hurst exponent H is calculated using the rescaled range statistic:

H = log(R/S) / log(T)

where R/S represents the rescaled range and T represents the time period. Values of H > 0.5 indicate long-term positive autocorrelation (persistence), while H < 0.5 indicates mean-reverting behavior.

3.6 Structural Break Detection

The model employs Chow test approximation for structural break detection, based on the methodology developed by Chow (1960). This technique identifies potential structural changes in the underlying relationships by comparing the stability of regression parameters across different time periods:

Chow_Statistic = (RSS_restricted - RSS_unrestricted) / RSS_unrestricted × (n-2k)/k

where RSS represents residual sum of squares, n represents sample size, and k represents the number of parameters.

4. Implementation Parameters and Configuration

4.1 Language Selection Parameters

The model provides comprehensive multi-language support across five languages: English, German (Deutsch), Spanish (Español), French (Français), and Japanese (日本語). This feature enhances accessibility for international users and ensures cultural appropriateness in terminology usage. The language selection affects all internal displays, statistical classifications, and alert messages while maintaining consistency in underlying calculations.

4.2 Model Configuration Parameters

Calculation Method: Users can select from four aggregation methodologies:

- Equal-Weighted: All components receive identical weights

- Variance-Weighted: Components weighted inversely to their historical variance

- Principal Component: Weights determined through principal component analysis

- Dynamic: Adaptive weighting based on recent performance

Sector Specification: The model allows for sector-specific calibration:

- General: Broad-based small business assessment

- Retail: Emphasis on consumer demand and seasonal factors

- Manufacturing: Enhanced weighting of input costs and currency effects

- Services: Focus on labor market dynamics and consumer demand

- Construction: Emphasis on credit conditions and monetary policy

Lookback Period: Statistical analysis window ranging from 126 to 504 trading days, with 252 days (one business year) as the optimal default based on academic research.

Smoothing Period: Exponential moving average period from 1 to 21 days, with 5 days providing optimal noise reduction while preserving signal integrity.

4.3 Statistical Threshold Parameters

Upper Statistical Boundary: Configurable threshold between 60-80 (default 70) representing the upper significance level for regime classification.

Lower Statistical Boundary: Configurable threshold between 20-40 (default 30) representing the lower significance level for regime classification.

Statistical Significance Level (α): Alpha level for statistical tests, configurable between 0.01-0.10 with 0.05 as the standard academic default.

4.4 Display and Visualization Parameters

Color Theme Selection: Eight professional color schemes optimized for different user preferences and accessibility requirements:

- Gold: Traditional financial industry colors

- EdgeTools: Professional blue-gray scheme

- Behavioral: Psychology-based color mapping

- Quant: Value-based quantitative color scheme

- Ocean: Blue-green maritime theme

- Fire: Warm red-orange theme

- Matrix: Green-black technology theme

- Arctic: Cool blue-white theme

Dark Mode Optimization: Automatic color adjustment for dark chart backgrounds, ensuring optimal readability across different viewing conditions.

Line Width Configuration: Main index line thickness adjustable from 1-5 pixels for optimal visibility.

Background Intensity: Transparency control for statistical regime backgrounds, adjustable from 90-99% for subtle visual enhancement without distraction.

4.5 Alert System Configuration

Alert Frequency Options: Three frequency settings to match different trading styles:

- Once Per Bar: Single alert per bar formation

- Once Per Bar Close: Alert only on confirmed bar close

- All: Continuous alerts for real-time monitoring

Statistical Extreme Alerts: Notifications when the index reaches 99% confidence levels (Z-score > 2.576 or < -2.576).

Regime Transition Alerts: Notifications when statistical boundaries are crossed, indicating potential regime changes.

5. Practical Application and Interpretation Guidelines

5.1 Index Interpretation Framework

The SBO-SAM index operates on a 0-100 scale with statistical normalization ensuring consistent interpretation across different time periods and market conditions. Values above 70 indicate statistically elevated small business conditions, suggesting favorable operating environment with potential for expansion and growth. Values below 30 indicate statistically reduced conditions, suggesting challenging operating environment with potential constraints on business activity.

The median reference line at 50 represents the long-term equilibrium level, with deviations providing insight into cyclical conditions relative to historical norms. The statistical confidence bands at 95% levels (approximately ±2 standard deviations) help identify when conditions reach statistically significant extremes.

5.2 Regime Classification System

The model employs a seven-level regime classification system based on percentile rankings:

Very High Regime (P80+): Exceptional small business conditions, typically associated with strong economic growth, easy credit availability, and favorable regulatory environment. Historical analysis suggests these periods often precede economic peaks and may warrant caution regarding sustainability.

High Regime (P60-80): Above-average conditions supporting business expansion and investment. These periods typically feature moderate growth, stable credit conditions, and positive consumer sentiment.

Moderate High Regime (P50-60): Slightly above-normal conditions with mixed signals. Careful monitoring of individual components helps identify emerging trends.

Neutral Regime (P40-50): Balanced conditions near long-term equilibrium. These periods often represent transition phases between different economic cycles.

Moderate Low Regime (P30-40): Slightly below-normal conditions with emerging headwinds. Early warning signals may appear in credit conditions or consumer demand.

Low Regime (P20-30): Below-average conditions suggesting challenging operating environment. Businesses may face constraints on growth and expansion.

Very Low Regime (P0-20): Severely constrained conditions, typically associated with economic recessions or financial crises. These periods often present opportunities for contrarian positioning.

5.3 Component Analysis and Diagnostics

Individual component analysis provides valuable diagnostic information about the underlying drivers of overall conditions. Divergences between components can signal emerging trends or structural changes in the economy.

Credit-Labor Divergence: When credit conditions improve while labor markets tighten, this may indicate early-stage economic acceleration with potential wage pressures.

Demand-Cost Divergence: Strong consumer demand coupled with rising input costs suggests inflationary pressures that may constrain small business margins.

Market-Fundamental Divergence: Disconnection between small-cap equity performance and fundamental conditions may indicate market inefficiencies or changing investor sentiment.

5.4 Temporal Analysis and Trend Identification

The model provides multiple temporal perspectives through momentum analysis, rate of change calculations, and trend decomposition. The 20-day momentum indicator helps identify short-term directional changes, while the Hodrick-Prescott filter approximation separates cyclical components from long-term trends.

Acceleration analysis through second-order momentum calculations provides early warning signals for potential trend reversals. Positive acceleration during declining conditions may indicate approaching inflection points, while negative acceleration during improving conditions may suggest momentum loss.

5.5 Statistical Confidence and Uncertainty Quantification

The model provides comprehensive uncertainty quantification through confidence intervals, volatility measures, and regime stability analysis. The 95% confidence bands help users understand the statistical significance of current readings and identify when conditions reach historically extreme levels.

Volatility analysis provides insight into the stability of current conditions, with higher volatility indicating greater uncertainty and potential for rapid changes. The regime stability measure, calculated as the inverse of volatility, helps assess the sustainability of current conditions.

6. Risk Management and Limitations

6.1 Model Limitations and Assumptions

The SBO-SAM model operates under several important assumptions that users must understand for proper interpretation. The model assumes that historical relationships between economic variables remain stable over time, though the regime-switching framework helps accommodate some structural changes. The 252-day lookback period provides reasonable statistical power while maintaining sensitivity to changing conditions, but may not capture longer-term structural shifts.

The model's reliance on publicly available economic data introduces inherent lags in some components, particularly those based on government statistics. Users should consider these timing differences when interpreting real-time conditions. Additionally, the model's focus on quantitative factors may not fully capture qualitative factors such as regulatory changes, geopolitical events, or technological disruptions that could significantly impact small business conditions.

The model's timeframe restrictions ensure statistical validity by preventing application to intraday periods where the underlying economic relationships may be distorted by market microstructure effects, trading noise, and temporal misalignment with the fundamental data sources. Users must utilize daily or longer timeframes to ensure the model's statistical foundations remain valid and interpretable.

6.2 Data Quality and Reliability Considerations

The model's accuracy depends heavily on the quality and availability of underlying economic data. Market-based components such as equity indices and bond prices provide real-time information but may be subject to short-term volatility unrelated to fundamental conditions. Economic statistics provide more stable fundamental information but may be subject to revisions and reporting delays.

Users should be aware that extreme market conditions may temporarily distort some components, particularly those based on financial market data. The model's statistical normalization helps mitigate these effects, but users should exercise additional caution during periods of market stress or unusual volatility.

6.3 Interpretation Caveats and Best Practices

The SBO-SAM model provides statistical analysis and should not be interpreted as investment advice or predictive forecasting. The model's output represents an assessment of current conditions based on historical relationships and may not accurately predict future outcomes. Users should combine the model's insights with other analytical tools and fundamental analysis for comprehensive decision-making.

The model's regime classifications are based on historical percentile rankings and may not fully capture the unique characteristics of current economic conditions. Users should consider the broader economic context and potential structural changes when interpreting regime classifications.

7. Academic References and Bibliography

Bernanke, B. S., & Blinder, A. S. (1992). The Federal Funds Rate and the Channels of Monetary Transmission. American Economic Review, 82(4), 901-921.

Bernanke, B. S., & Gertler, M. (1995). Inside the Black Box: The Credit Channel of Monetary Policy Transmission. Journal of Economic Perspectives, 9(4), 27-48.

Boot, A. W. A. (2000). Relationship Banking: What Do We Know? Journal of Financial Intermediation, 9(1), 7-25.

Chow, G. C. (1960). Tests of Equality Between Sets of Coefficients in Two Linear Regressions. Econometrica, 28(3), 591-605.

Dunkelberg, W. C., & Wade, H. (2023). NFIB Small Business Economic Trends. National Federation of Independent Business Research Foundation, Washington, D.C.

Engle, R. F., & Granger, C. W. J. (1987). Co-integration and Error Correction: Representation, Estimation, and Testing. Econometrica, 55(2), 251-276.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, 25(2), 383-417.

Federal Reserve Board. (2024). Senior Loan Officer Opinion Survey on Bank Lending Practices. Board of Governors of the Federal Reserve System, Washington, D.C.

Friedman, M. (1957). A Theory of the Consumption Function. Princeton University Press, Princeton, NJ.

Gordon, R. J. (1988). The Role of Wages in the Inflation Process. American Economic Review, 78(2), 276-283.

Hamilton, J. D. (1989). A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle. Econometrica, 57(2), 357-384.

Hurst, H. E. (1951). Long-term Storage Capacity of Reservoirs. Transactions of the American Society of Civil Engineers, 116(1), 770-799.

Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263-291.

Krugman, P. (1987). Pricing to Market When the Exchange Rate Changes. In S. W. Arndt & J. D. Richardson (Eds.), Real-Financial Linkages among Open Economies (pp. 49-70). MIT Press, Cambridge, MA.

Markowitz, H. (1952). Portfolio Selection. Journal of Finance, 7(1), 77-91.

Mortensen, D. T., & Pissarides, C. A. (1994). Job Creation and Job Destruction in the Theory of Unemployment. Review of Economic Studies, 61(3), 397-415.

Shannon, C. E. (1948). A Mathematical Theory of Communication. Bell System Technical Journal, 27(3), 379-423.

Sharpe, W. F. (1964). Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk. Journal of Finance, 19(3), 425-442.

Tsay, R. S. (2010). Analysis of Financial Time Series (3rd ed.). John Wiley & Sons, Hoboken, NJ.

U.S. Small Business Administration. (2024). Small Business Profile. Office of Advocacy, Washington, D.C.

8. Technical Implementation Notes

The SBO-SAM model is implemented in Pine Script version 6 for the TradingView platform, ensuring compatibility with modern charting and analysis tools. The implementation follows best practices for financial indicator development, including proper error handling, data validation, and performance optimization.

The model includes comprehensive timeframe validation to ensure statistical accuracy and reliability. The indicator operates exclusively on daily (1D) timeframes or higher, including weekly (1W), monthly (1M), and longer periods. This restriction ensures that the statistical analysis maintains appropriate temporal resolution for the underlying economic data sources, which are primarily reported on daily or longer intervals.

When users attempt to apply the model to intraday timeframes (such as 1-minute, 5-minute, 15-minute, 30-minute, 1-hour, 2-hour, 4-hour, 6-hour, 8-hour, or 12-hour charts), the system displays a comprehensive error message in the user's selected language and prevents execution. This safeguard protects users from potentially misleading results that could occur when applying daily-based economic analysis to shorter timeframes where the underlying data relationships may not hold.

The model's statistical calculations are performed using vectorized operations where possible to ensure computational efficiency. The multi-language support system employs Unicode character encoding to ensure proper display of international characters across different platforms and devices.

The alert system utilizes TradingView's native alert functionality, providing users with flexible notification options including email, SMS, and webhook integrations. The alert messages include comprehensive statistical information to support informed decision-making.

The model's visualization system employs professional color schemes designed for optimal readability across different chart backgrounds and display devices. The system includes dynamic color transitions based on momentum and volatility, professional glow effects for enhanced line visibility, and transparency controls that allow users to customize the visual intensity to match their preferences and analytical requirements. The clean confidence band implementation provides clear statistical boundaries without visual distractions, maintaining focus on the analytical content.

Hazel nut BB Strategy, volume base- lite versionHazel nut BB Strategy, volume base — lite version

Having knowledge and information in financial markets is only useful when a trader operates with a well-defined trading strategy. Trading strategies assist in capital management, profit-taking, and reducing potential losses.

This strategy is built upon the core principle of supply and demand dynamics. Alongside this foundation, one of the widely used technical tools — the Bollinger Bands — is employed to structure a framework for profit management and risk control.

In this strategy, the interaction of these tools is explained in detail. A key point to note is that for calculating buy and sell volumes, a lower timeframe function is used. When applied with a tick-level resolution, this provides the most precise measurement of buyer/seller flows. However, this comes with a limitation of reduced historical depth. Users should be aware of this trade-off: if precise tick-level data is required, shorter timeframes should be considered to extend historical coverage .

The strategy offers multiple configuration options. Nevertheless, it should be treated strictly as a supportive tool rather than a standalone trading system. Decisions must integrate personal analysis and other instruments. For example, in highly volatile assets with narrow ranges, it is recommended to adjust profit-taking and stop-loss percentages to smaller values.

◉ Volume Settings

• Buyer and seller volume (up/down volume) are requested from a lower timeframe, with an option to override the automatic resolution.

• A global lookback period is applied to calculate moving averages and cumulative sums of buy/sell/delta volumes.

• Ratios of buyers/sellers to total volume are derived both on the current bar and across the lookback window.

◉ Bollinger Band

• Bands are computed using configurable moving averages (SMA, EMA, RMA, WMA, VWMA).

• Inputs allow control of length, standard deviation multiplier, and offset.

• The basis, upper, and lower bands are plotted, with a shaded background between them.

◉ Progress & Proximity

• Relative position of the price to the Bollinger basis is expressed as percentages (qPlus/qMinus).

• “Near band” conditions are triggered when price progress toward the upper or lower band exceeds a user-defined threshold (%).

• A signed score (sScore) represents how far the close has moved above or below the basis relative to band width.

◉ Info Table

• Optional compact table summarizing:

• - Upper/lower band margins

• - Buyer/seller volumes with moving averages

• - Delta and cumulative delta

• - Buyer/seller ratios per bar and across the window

• - Money flow values (buy/sell/delta × price) for bar-level and summed periods

• The table is neutral-colored and resizable for different chart layouts.

◉ Zone Event Gate

• Tracks entry into and exit from “near band” zones.

• Arming logic: a side is armed when price enters a band proximity zone.

• Trigger logic: on exit, a trade event is generated if cumulative buyer or seller volume dominates over a configurable window.

◉ Trading Logic

• Orders are placed only on zone-exit events, conditional on volume dominance.

• Position sizing is defined as a fixed percentage of strategy equity.

• Long entries occur when leaving the lower zone with buyer dominance; short entries occur when leaving the upper zone with seller dominance.

◉ Exit Rules

• Open positions are managed by a strict priority sequence:

• 1. Stop-loss (% of entry price)

• 2. Take-profit (% of entry price)

• 3. Opposite-side event (zone exit with dominance in the other direction)

• Stop-loss and take-profit levels are configurable

◉ Notes

• This lite version is intended to demonstrate the interaction of Bollinger Bands and volume-based dominance logic.

• It provides a framework to observe how price reacts at band boundaries under varying buy/sell pressure, and how zone exits can be systematically converted into entry/exit signals.

When configuring this strategy, it is essential to carefully review the settings within the Strategy Tester. Ensure that the chosen parameters and historical data options are correctly aligned with the intended use. Accurate back testing depends on applying proper configurations for historical reference. The figure below illustrates sample result and configuration type.

QZ Trend (Crypto Edition) v1.1a: Donchian, EMA, ATR, Liquidity/FThe "QZ Trend (Crypto Edition)" is a rules-based trend-following breakout strategy for crypto spot or perpetual contracts, focusing on following trends, prioritizing risk control, seeking small losses and big wins, and trading only when advantageous.

Key mechanisms include:

- Market filters: Screen favorable conditions via ADX (trend strength), dollar volume (liquidity), funding fee windows, session/weekend restrictions, and spot-long-only settings.

- Signals & entries: Based on price position relative to EMA and EMA trends, combined with breaking Donchian channel extremes (with ATR ratio confirmation), plus single-position rules and post-exit cooldowns.

- Position sizing: Calculate positions by fixed risk percentage; initial stop-loss is ATR-based, complying with exchange min/max lot requirements.

- Exits & risk management: Include initial stop-loss, trailing stop (tightens only), break-even rule (stop moves to entry when target floating profit is hit), time-based exit, and post-exit cooldowns.

- Pyramiding: Add positions only when profitable with favorable momentum, requiring ATR-based spacing; add size is a fraction of the base position, with layers sharing stop logic but having unique order IDs.

Charts display EMA, Donchian channels, current stop lines, and highlight low ADX, avoidable funding windows, and low-liquidity periods.

Recommend starting with 4H or 1D timeframes, with typical parameters varying by cycle. Liquidity settings differ by token; perpetuals should enable funding window filters, while spot requires "long-only" and matching fees. The strategy performs well in trends with quick stop-losses but faces whipsaws in ranges (filters mitigate but don’t eliminate noise). Share your symbol and timeframe for tailored parameters.

Rolling Range Bands by tvigRolling Range Bands

Plots two dynamic price envelopes that track the highest and lowest prices over a Short and Long lookback. Use them to see near-term vs. broader market structure, evolving support/resistance, and volatility changes at a glance.

What it shows

• Short Bands: recent trading range (fast, more reactive).

• Long Bands: broader range (slow, structural).

• Optional step-line style and shaded zones for clarity.

• Option to use completed bar values to avoid intrabar jitter (no repaint).

How to read

• Price pressing the short high while the long band rises → short-term momentum in a larger uptrend.