LAX Murray Math LevelsLAX Murrey Math Levels

Specify a starting price, then an interval and Lookback window.

The indicator will then plot a moving window of murray math levels.

Cari dalam skrip untuk "如何用wind搜索股票的发行价和份数"

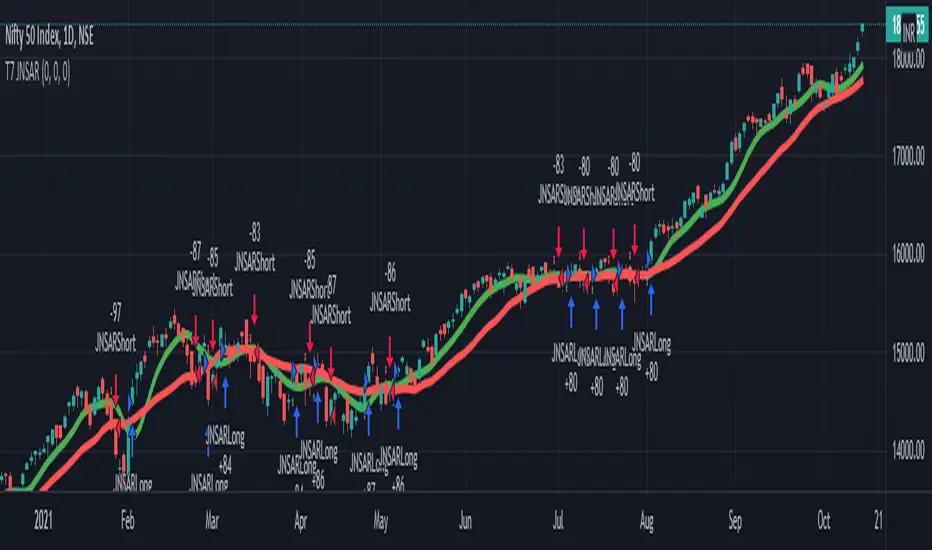

T7 JNSARJNSAR stands for Just Nifty -0.14% Stop & Reverse. This is a Trend Following Daily Bar Trading System for NIFTY -0.14% . Original idea belongs to ILLANGO @ I coded the pine version of this system based on a request from @stocksonfire. Use it at your own risk after validation at your end. Neither me or my company is responsible for any losses you may incur using this system. Hope you like this system and enjoy trading it !!!

Updated V3 code for the T7 JNSAR system earlier published here V2 and here V1

Following updates made to the code

1. Added a 22 Period Simple moving average filter over and above the standard JNSAR value for generating trading signals. This simple filter reduces the whipsaw trades drastically along with similar improvements in the max draw down and overall profitability of the system. The SMA filter is turned ON by default but can be turned OFF by user through the settings window.

2. Backtest option is now turned ON by default.

Also am republishing the trading rules here again with some modification

1. Go Long when the daily close is above the JNSAR line. Go Short when the daily close is below the JNSAR line. JNSAR line is the varying green line overlayed over the price chart. Once a signal comes at market close enter in the direction of the signal @ market price @ next day market open.

2. Trade only Nifty -0.14% Index. This system was developed and backtested only for NIFTY -0.14% Index. So trade in its Futures or Options, as you may deem fit. My recommendation is to choose futures for simplicity. If you want to reduce the trading cost and go with options, trade with deep in the money options, preferably 2 strikes far from the spot price.

3. Trade all signals. Markets trend only 30-35% of the time and hence the system is only accurate to that extend. But system tends to make enough money, in this small trending window, to keep the overall profitability in good health. But one never knows when a big trend may come and when it comes its absolutely imperative that you take it. To ensure that, trade all signals and don't be choosy about what signals you are going to trade. Also I wouldn't recommend using your own analysis to trade this system. Too many drivers will crash the car.

4. Like all trend following systems, this system will have many whipsaws during flat markets along with large trade and account drawdowns. Also some months and even years may not be profitable. But to trade this system profitably, it is necessary to take these in one's stride and keep trading. As the backtester results from 1990 to 2017 proves, this system is profitable overall thus far. Take confidence from that objective fact.

5. Trade with only that amount of money you can afford to loose. Initial capital that you need to have to trade one lot of NIFTY -0.14% should be atleast - (Margin Money required to take and hold 1 lot position + maximum drawdown amount per lot)*1.2. Be prepared to add more if need be, but the above formula will give a rough idea of what you need to have to start trading and be in the game always.

6. Place an After Market Order @ Market Price with your broker after market close so that you get to execute the trade next trading day @ Market open to capture near similar price as the daily open price seen on the chart. This execution mode will give you the best chance to minimize the slippage and mimic the backtester results as closely as practically possible.

7. Follow all the 6 rules above religiously, as if your life depends on it. If you cant, then don't trade this system; You will certainly loose money.

Happy Trading !!! As always am looking out for your valuable feedback.

QTALibrary "QTA"

This is simple library for basic Quantitative Technical Analysis for retail investors. One example of it being used can be seen here ().

calculateKellyRatio(returns)

Parameters:

returns (array) : An array of floats representing the returns from bets.

Returns: The calculated Kelly Ratio, which indicates the optimal bet size based on winning and losing probabilities.

calculateAdjustedKellyFraction(kellyRatio, riskTolerance, fedStance)

Parameters:

kellyRatio (float) : The calculated Kelly Ratio.

riskTolerance (float) : A float representing the risk tolerance level.

fedStance (string) : A string indicating the Federal Reserve's stance ("dovish", "hawkish", or neutral).

Returns: The adjusted Kelly Fraction, constrained within the bounds of .

calculateStdDev(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The standard deviation of the returns, or 0 if insufficient data.

calculateMaxDrawdown(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The maximum drawdown as a percentage.

calculateEV(avgWinReturn, winProb, avgLossReturn)

Parameters:

avgWinReturn (float) : The average return from winning bets.

winProb (float) : The probability of winning a bet.

avgLossReturn (float) : The average return from losing bets.

Returns: The calculated Expected Value of the bet.

calculateTailRatio(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The Tail Ratio, or na if the 5th percentile is zero to avoid division by zero.

calculateSharpeRatio(avgReturn, riskFreeRate, stdDev)

Parameters:

avgReturn (float) : The average return of the investment.

riskFreeRate (float) : The risk-free rate of return.

stdDev (float) : The standard deviation of the investment's returns.

Returns: The calculated Sharpe Ratio, or na if standard deviation is zero.

calculateDownsideDeviation(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The standard deviation of the downside returns, or 0 if no downside returns exist.

calculateSortinoRatio(avgReturn, downsideDeviation)

Parameters:

avgReturn (float) : The average return of the investment.

downsideDeviation (float) : The standard deviation of the downside returns.

Returns: The calculated Sortino Ratio, or na if downside deviation is zero.

calculateVaR(returns, confidenceLevel)

Parameters:

returns (array) : An array of floats representing the returns.

confidenceLevel (float) : A float representing the confidence level (e.g., 0.95 for 95% confidence).

Returns: The Value at Risk at the specified confidence level.

calculateCVaR(returns, varValue)

Parameters:

returns (array) : An array of floats representing the returns.

varValue (float) : The Value at Risk threshold.

Returns: The average Conditional Value at Risk, or na if no returns are below the threshold.

calculateExpectedPriceRange(currentPrice, ev, stdDev, confidenceLevel)

Parameters:

currentPrice (float) : The current price of the asset.

ev (float) : The expected value (in percentage terms).

stdDev (float) : The standard deviation (in percentage terms).

confidenceLevel (float) : The confidence level for the price range (e.g., 1.96 for 95% confidence).

Returns: A tuple containing the minimum and maximum expected prices.

calculateRollingStdDev(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling standard deviation of returns.

calculateRollingVariance(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling variance of returns.

calculateRollingMean(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling mean of returns.

calculateRollingCoefficientOfVariation(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling coefficient of variation of returns.

calculateRollingSumOfPercentReturns(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling sum of percent returns.

calculateRollingCumulativeProduct(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling cumulative product of returns.

calculateRollingCorrelation(priceReturns, volumeReturns, window)

Parameters:

priceReturns (array) : An array of floats representing the price returns.

volumeReturns (array) : An array of floats representing the volume returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling correlation.

calculateRollingPercentile(returns, window, percentile)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

percentile (int) : An integer representing the desired percentile (0-100).

Returns: An array of floats representing the rolling percentile of returns.

calculateRollingMaxMinPercentReturns(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: A tuple containing two arrays: rolling max and rolling min percent returns.

calculateRollingPriceToVolumeRatio(price, volData, window)

Parameters:

price (array) : An array of floats representing the price data.

volData (array) : An array of floats representing the volume data.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling price-to-volume ratio.

determineMarketRegime(priceChanges)

Parameters:

priceChanges (array) : An array of floats representing the price changes.

Returns: A string indicating the market regime ("Bull", "Bear", or "Neutral").

determineVolatilityRegime(price, window)

Parameters:

price (array) : An array of floats representing the price data.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the calculated volatility.

classifyVolatilityRegime(volatility)

Parameters:

volatility (array) : An array of floats representing the calculated volatility.

Returns: A string indicating the volatility regime ("Low" or "High").

method percentPositive(thisArray)

Returns the percentage of positive non-na values in this array.

This method calculates the percentage of positive values in the provided array, ignoring NA values.

Namespace types: array

Parameters:

thisArray (array)

_candleRange()

_PreviousCandleRange(barsback)

Parameters:

barsback (int) : An integer representing how far back you want to get a range

redCandle()

greenCandle()

_WhiteBody()

_BlackBody()

HighOpenDiff()

OpenLowDiff()

_isCloseAbovePreviousOpen(length)

Parameters:

length (int)

_isCloseBelowPrevious()

_isOpenGreaterThanPrevious()

_isOpenLessThanPrevious()

BodyHigh()

BodyLow()

_candleBody()

_BodyAvg(length)

_BodyAvg function.

Parameters:

length (simple int) : Required (recommended is 6).

_SmallBody(length)

Parameters:

length (simple int) : Length of the slow EMA

Returns: a series of bools, after checking if the candle body was less than body average.

_LongBody(length)

Parameters:

length (simple int)

bearWick()

bearWick() function.

Returns: a SERIES of FLOATS, checks if it's a blackBody(open > close), if it is, than check the difference between the high and open, else checks the difference between high and close.

bullWick()

barlength()

sumbarlength()

sumbull()

sumbear()

bull_vol()

bear_vol()

volumeFightMA()

volumeFightDelta()

weightedAVG_BullVolume()

weightedAVG_BearVolume()

VolumeFightDiff()

VolumeFightFlatFilter()

avg_bull_vol(userMA)

avg_bull_vol(int) function.

Parameters:

userMA (int)

avg_bear_vol(userMA)

avg_bear_vol(int) function.

Parameters:

userMA (int)

diff_vol(userMA)

diff_vol(int) function.

Parameters:

userMA (int)

vol_flat(userMA)

vol_flat(int) function.

Parameters:

userMA (int)

_isEngulfingBullish()

_isEngulfingBearish()

dojiup()

dojidown()

EveningStar()

MorningStar()

ShootingStar()

Hammer()

InvertedHammer()

BearishHarami()

BullishHarami()

BullishBelt()

BullishKicker()

BearishKicker()

HangingMan()

DarkCloudCover()

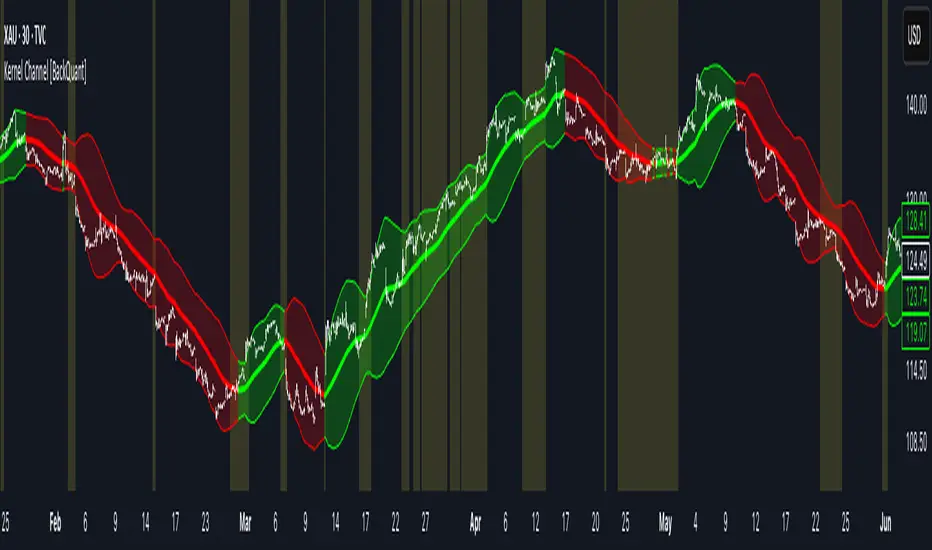

Kernel Channel [BackQuant]Kernel Channel

A non-parametric, kernel-weighted trend channel that adapts to local structure, smooths noise without lagging like moving averages, and highlights volatility compressions, expansions, and directional bias through a flexible choice of kernels, band types, and squeeze logic.

What this is

This indicator builds a full trend channel using kernel regression rather than classical averaging. Instead of a simple moving average or exponential weighting, the midline is computed as a kernel-weighted expectation of past values. This allows it to adapt to local shape, give more weight to nearby bars, and reduce distortion from outliers.

You can think of it as a sliding local smoother where you define both the “window” of influence (Window Length) and the “locality strength” (Bandwidth). The result is a flexible midline with optional upper and lower bands derived from kernel-weighted ATR or kernel-weighted standard deviation, letting you visualize volatility in a structurally consistent way.

Three plotting modes help demonstrate this difference:

When the midline is shown alone, you get a smooth, adaptive baseline that behaves almost like a regression moving average, as shown in this view:

When full channels are enabled, you see how standard deviation reacts to local structure with dynamically widening and tightening bands, a mode illustrated here:

When ATR mode is chosen instead of StdDev, band width reflects breadth of movement rather than variance, creating a volatility-aware envelope like the example here:

Why kernels

Classical moving averages allocate fixed weights. Kernels let the user define weighting shape:

Epanechnikov — emphasizes bars near the current bar, fades fast, stable and smooth.

Triangular — linear decay, simple and responsive.

Laplacian — exponential decay from the current point, sharper reactivity.

Cosine — gentle periodic decay, balanced smoothness for trend filters.

Using these in combination with a bandwidth parameter gives fine control over smoothness vs responsiveness. Smaller bandwidths give sharper local sensitivity, larger bandwidths give smoother curvature.

How it works (core logic)

The indicator computes three building blocks:

1) Kernel-weighted midline

For every bar, a sliding window looks back Window Length bars. Each bar in this window receives a kernel weight depending on:

its index distance from the present

the chosen kernel shape

the bandwidth parameter (locality)

Weights form the denominator, weighted values form the numerator, and the resulting ratio is the kernel regression mean. This midline is the central trend.

2) Kernel-based width

You choose one of two band types:

Kernel ATR — ATR values are kernel-averaged, producing a smooth, volatility-based width that is not dependent on variance. Ideal for directional trend channels and regime separation.

Kernel StdDev — local variance around the midline is computed through kernel weighting. This produces a true statistical envelope that narrows in quiet periods and widens in noisy areas.

Width is scaled using Band Multiplier , controlling how far the envelope extends.

3) Upper and lower channels

Provided midline and width exist, the channel edges are:

Upper = midline + bandMult × width

Lower = midline − bandMult × width

These create smooth structures around price that adapt continuously.

Plotting modes

The indicator supports multiple visual styles depending on what you want to emphasize.

When only the midline is displayed, you get a pure kernel trend: a smooth regression-like curve that reacts to local structure while filtering noise, demonstrated here: This provides a clean read on direction and slope.

With full channels enabled, the behavior of the bands becomes visible. Standard deviation mode creates elastic boundaries that tighten during compressions and widen during turbulence, which you can see in the band-focused demonstration: This helps identify expansion events, volatility clusters, and breakouts.

ATR mode shifts interpretation from statistical variance to raw movement amplitude. This makes channels less sensitive to outliers and more consistent across trend phases, as shown in this ATR variation example: This mode is particularly useful for breakout systems and bar-range regimes.

Regime detection and bar coloring

The slope of the midline defines directional bias:

Up-slope → green

Down-slope → red

Flat → gray

A secondary regime filter compares close to the channel:

Trend Up Strong — close above upper band and midline rising.

Trend Down Strong — close below lower band and midline falling.

Trend Up Weak — close between midline and upper band with rising slope.

Trend Down Weak — close between lower band and midline with falling slope.

Compression mode — squeeze conditions.

Bar coloring is optional and can be toggled for cleaner charts.

Squeeze logic

The indicator includes non-standard squeeze detection based on relative width , defined as:

width / |midline|

This gives a dimensionless measure of how “tight” or “loose” the channel is, normalized for trend level.

A rolling window evaluates the percentile rank of current width relative to past behavior. If the width is in the lowest X% of its last N observations, the script flags a squeeze environment. This highlights compression regions that may precede breakouts or regime shifts.

Deviation highlighting

When using Kernel StdDev mode, you may enable deviation flags that highlight bars where price moves outside the channel:

Above upper band → bullish momentum overextension

Below lower band → bearish momentum overextension

This is turned off in ATR mode because ATR widths do not represent distributional variance.

Alerts included

Kernel Channel Long — midline turns up.

Kernel Channel Short — midline turns down.

Price Crossed Midline — crossover or crossunder of the midline.

Price Above Upper — early momentum expansion.

Price Below Lower — downward volatility expansion.

These help automate regime changes and breakout detection.

How to use it

Trend identification

The midline acts as a bias filter. Rising midline means trend strength upward, falling midline means downward behavior. The channel width contextualizes confidence.

Breakout anticipation

Kernel StdDev compressions highlight areas where price is coiling. Breakouts often follow narrow relative width. ATR mode provides structural expansion cues that are smooth and robust.

Mean reversion

StdDev mode is suitable for fade setups. Moves to outer bands during low volatility often revert to the midline.

Continuation logic

If price breaks above the upper band while midline is rising, the indicator flags strong directional expansion. Same logic for breakdowns on the lower band.

Volatility characterization

Kernel ATR maps raw bar movements and is excellent for identifying regime shifts in markets where variance is unstable.

Tuning guidance

For smoother long-term trend tracking

Larger window (150–300).

Moderate bandwidth (1.0–2.0).

Epanechnikov or Cosine kernel.

ATR mode for stable envelopes.

For swing trading / short-term structure

Window length around 50–100.

Bandwidth 0.6–1.2.

Triangular for speed, Laplacian for sharper reactions.

StdDev bands for precise volatility compression.

For breakout systems

Smaller bandwidth for sharp local detection.

ATR mode for stable envelopes.

Enable squeeze highlighting for identifying setups early.

For mean-reversion systems

Use StdDev bands.

Moderate window length.

Highlight deviations to locate overextended bars.

Settings overview

Kernel Settings

Source

Window Length

Bandwidth

Kernel Type (Epanechnikov, Triangular, Laplacian, Cosine)

Channel Width

Band Type (Kernel ATR or Kernel StdDev)

Band Multiplier

Visuals

Show Bands

Color Bars By Regime

Highlight Squeeze Periods

Highlight Deviation

Lookback and Percentile settings

Colors for uptrend, downtrend, squeeze, flat

Trading applications

Trend filtering — trade only in direction of the midline slope.

Breakout confirmation — expansion outside the bands while slope agrees.

Squeeze timing — compression periods often precede the next directional leg.

Volatility-aware stops — ATR mode makes channel edges suitable for adaptive stop placement.

Structural swing mapping — StdDev bands help locate midline pullbacks vs distributional extremes.

Bias rotation — bar coloring highlights when regime shifts occur.

Notes

The Kernel Channel is not a signal generator by itself, but a structural map. It helps classify trend direction, volatility environment, distribution shape, and compression cycles. Combine it with your entry and exit framework, risk parameters, and higher-timeframe confirmation.

It is designed to behave consistently across markets, to avoid the bluntness of classical averages, and to reveal subtle curvature in price that traditional channels miss. Adjust kernel type, bandwidth, and band source to match the noise profile of your instrument, then use squeeze logic and deviation highlighting to guide timing.

Savitzky-Golay Filter (SGF)The Savitzky-Golay Filter (SGF) is a digital filter that performs local polynomial regression on a series of values to determine the smoothed value for each point. Developed by Abraham Savitzky and Marcel Golay in 1964, it is particularly effective at preserving higher moments of the data while reducing noise. This implementation provides a practical adaptation for financial time series, offering superior preservation of peaks, valleys, and other important market structures that might be distorted by simpler moving averages.

## Core Concepts

* **Local polynomial fitting:** Fits a polynomial of specified order to a sliding window of data points

* **Moment preservation:** Maintains higher statistical moments (peaks, valleys, inflection points)

* **Optimized coefficients:** Uses pre-computed coefficients for common polynomial orders

* **Adaptive weighting:** Weight distribution varies based on polynomial order and window size

* **Market application:** Particularly effective for preserving significant price movements while filtering noise

The core innovation of the Savitzky-Golay filter is its ability to smooth data while preserving important features that are often flattened by other filtering methods. This makes it especially valuable for technical analysis where maintaining the shape of price patterns is crucial.

## Common Settings and Parameters

| Parameter | Default | Function | When to Adjust |

|-----------|---------|----------|---------------|

| Window Size | 11 | Number of points used in local fitting (must be odd) | Increase for smoother output, decrease for better feature preservation |

| Polynomial Order | 2 | Order of fitting polynomial (2 or 4) | Use 2 for general smoothing, 4 for better peak preservation |

| Source | close | Price data used for calculation | Consider using hlc3 for more stable fitting |

**Pro Tip:** A window size of 11 with polynomial order 2 provides a good balance between smoothing and feature preservation. For sharper peaks and valleys, use order 4 with a smaller window size.

## Calculation and Mathematical Foundation

**Simplified explanation:**

The filter fits a polynomial of specified order to a moving window of price data. The smoothed value at each point is computed from this local fit, effectively removing noise while preserving the underlying shape of the data.

**Technical formula:**

For a window of size N and polynomial order M, the filtered value is:

y = Σ(c_i × x )

Where:

- c_i are the pre-computed filter coefficients

- x are the input values in the window

- Coefficients depend on window size N and polynomial order M

> 🔍 **Technical Note:** The implementation uses optimized coefficient calculations for orders 2 and 4, which cover most practical applications while maintaining computational efficiency.

## Interpretation Details

The Savitzky-Golay filter can be used in various trading strategies:

* **Pattern recognition:** Preserves chart patterns while removing noise

* **Peak detection:** Maintains amplitude and width of significant peaks

* **Trend analysis:** Smooths price movement without distorting important transitions

* **Divergence trading:** Better preservation of local maxima and minima

* **Volatility analysis:** Accurate representation of price movement dynamics

## Limitations and Considerations

* **Computational complexity:** More intensive than simple moving averages

* **Edge effects:** First and last few points may show end effects

* **Parameter sensitivity:** Performance depends on appropriate window size and order selection

* **Data requirements:** Needs sufficient points for polynomial fitting

* **Complementary tools:** Best used with volume analysis and momentum indicators

## References

* Savitzky, A., Golay, M.J.E. "Smoothing and Differentiation of Data by Simplified Least Squares Procedures," Analytical Chemistry, 1964

* Press, W.H. et al. "Numerical Recipes: The Art of Scientific Computing," Chapter 14

* Schafer, R.W. "What Is a Savitzky-Golay Filter?" IEEE Signal Processing Magazine, 2011

TimeSeriesBenchmarkMeasuresLibrary "TimeSeriesBenchmarkMeasures"

Time Series Benchmark Metrics. \

Provides a comprehensive set of functions for benchmarking time series data, allowing you to evaluate the accuracy, stability, and risk characteristics of various models or strategies. The functions cover a wide range of statistical measures, including accuracy metrics (MAE, MSE, RMSE, NRMSE, MAPE, SMAPE), autocorrelation analysis (ACF, ADF), and risk measures (Theils Inequality, Sharpness, Resolution, Coverage, and Pinball).

___

Reference:

- github.com .

- medium.com .

- www.salesforce.com .

- towardsdatascience.com .

- github.com .

mae(actual, forecasts)

In statistics, mean absolute error (MAE) is a measure of errors between paired observations expressing the same phenomenon. Examples of Y versus X include comparisons of predicted versus observed, subsequent time versus initial time, and one technique of measurement versus an alternative technique of measurement.

Parameters:

actual (array) : List of actual values.

forecasts (array) : List of forecasts values.

Returns: - Mean Absolute Error (MAE).

___

Reference:

- en.wikipedia.org .

- The Orange Book of Machine Learning - Carl McBride Ellis .

mse(actual, forecasts)

The Mean Squared Error (MSE) is a measure of the quality of an estimator. As it is derived from the square of Euclidean distance, it is always a positive value that decreases as the error approaches zero.

Parameters:

actual (array) : List of actual values.

forecasts (array) : List of forecasts values.

Returns: - Mean Squared Error (MSE).

___

Reference:

- en.wikipedia.org .

rmse(targets, forecasts, order, offset)

Calculates the Root Mean Squared Error (RMSE) between target observations and forecasts. RMSE is a standard measure of the differences between values predicted by a model and the values actually observed.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

order (int) : Model order parameter that determines the starting position in the targets array, `default=0`.

offset (int) : Forecast offset related to target, `default=0`.

Returns: - RMSE value.

nmrse(targets, forecasts, order, offset)

Normalised Root Mean Squared Error.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

order (int) : Model order parameter that determines the starting position in the targets array, `default=0`.

offset (int) : Forecast offset related to target, `default=0`.

Returns: - NRMSE value.

rmse_interval(targets, forecasts)

Root Mean Squared Error for a set of interval windows. Computes RMSE by converting interval forecasts (with min/max bounds) into point forecasts using the mean of the interval bounds, then compares against actual target values.

Parameters:

targets (array) : List of target observations.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - RMSE value for the combined interval list.

mape(targets, forecasts)

Mean Average Percentual Error.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

Returns: - MAPE value.

smape(targets, forecasts, mode)

Symmetric Mean Average Percentual Error. Calculates the Mean Absolute Percentage Error (MAPE) between actual targets and forecasts. MAPE is a common metric for evaluating forecast accuracy, expressed as a percentage, lower values indicate a better forecast accuracy.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

mode (int) : Type of method: default=0:`sum(abs(Fi-Ti)) / sum(Fi+Ti)` , 1:`mean(abs(Fi-Ti) / ((Fi + Ti) / 2))` , 2:`mean(abs(Fi-Ti) / (abs(Fi) + abs(Ti))) * 100`

Returns: - SMAPE value.

mape_interval(targets, forecasts)

Mean Average Percentual Error for a set of interval windows.

Parameters:

targets (array) : List of target observations.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - MAPE value for the combined interval list.

acf(data, k)

Autocorrelation Function (ACF) for a time series at a specified lag.

Parameters:

data (array) : Sample data of the observations.

k (int) : The lag period for which to calculate the autocorrelation. Must be a non-negative integer.

Returns: - The autocorrelation value at the specified lag, ranging from -1 to 1.

___

The autocorrelation function measures the linear dependence between observations in a time series

at different time lags. It quantifies how well the series correlates with itself at different

time intervals, which is useful for identifying patterns, seasonality, and the appropriate

lag structure for time series models.

ACF values close to 1 indicate strong positive correlation, values close to -1 indicate

strong negative correlation, and values near 0 indicate no linear correlation.

___

Reference:

- statisticsbyjim.com

acf_multiple(data, k)

Autocorrelation function (ACF) for a time series at a set of specified lags.

Parameters:

data (array) : Sample data of the observations.

k (array) : List of lag periods for which to calculate the autocorrelation. Must be a non-negative integer.

Returns: - List of ACF values for provided lags.

___

The autocorrelation function measures the linear dependence between observations in a time series

at different time lags. It quantifies how well the series correlates with itself at different

time intervals, which is useful for identifying patterns, seasonality, and the appropriate

lag structure for time series models.

ACF values close to 1 indicate strong positive correlation, values close to -1 indicate

strong negative correlation, and values near 0 indicate no linear correlation.

___

Reference:

- statisticsbyjim.com

adfuller(data, n_lag, conf)

: Augmented Dickey-Fuller test for stationarity.

Parameters:

data (array) : Data series.

n_lag (int) : Maximum lag.

conf (string) : Confidence Probability level used to test for critical value, (`90%`, `95%`, `99%`).

Returns: - `adf` The test statistic.

- `crit` Critical value for the test statistic at the 10 % levels.

- `nobs` Number of observations used for the ADF regression and calculation of the critical values.

___

The Augmented Dickey-Fuller test is used to determine whether a time series is stationary

or contains a unit root (non-stationary). The null hypothesis is that the series has a unit root

(is non-stationary), while the alternative hypothesis is that the series is stationary.

A stationary time series has statistical properties that do not change over time, making it

suitable for many time series forecasting models. If the test statistic is less than the

critical value, we reject the null hypothesis and conclude the series is stationary.

___

Reference:

- www.jstor.org

- en.wikipedia.org

theils_inequality(targets, forecasts)

Calculates Theil's Inequality Coefficient, a measure of forecast accuracy that quantifies the relative difference between actual and predicted values.

Parameters:

targets (array) : List of target observations.

forecasts (array) : Matrix with list of forecasts, ordered column wise.

Returns: - Theil's Inequality Coefficient value, value closer to 0 is better.

___

Theil's Inequality Coefficient is calculated as: `sqrt(Sum((y_i - f_i)^2)) / (sqrt(Sum(y_i^2)) + sqrt(Sum(f_i^2)))`

where `y_i` represents actual values and `f_i` represents forecast values.

This metric ranges from 0 to infinity, with 0 indicating perfect forecast accuracy.

___

Reference:

- en.wikipedia.org

sharpness(forecasts)

The average width of the forecast intervals across all observations, representing the sharpness or precision of the predictive intervals.

Parameters:

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - Sharpness The sharpness level, which is the average width of all prediction intervals across the forecast horizon.

___

Sharpness is an important metric for evaluating forecast quality. It measures how narrow or wide the

prediction intervals are. Higher sharpness (narrower intervals) indicates greater precision in the

forecast intervals, while lower sharpness (wider intervals) suggests less precision.

The sharpness metric is calculated as the mean of the interval widths across all observations, where

each interval width is the difference between the upper and lower bounds of the prediction interval.

Note: This function assumes that the forecasts matrix has at least 2 columns, with the first column

representing the lower bounds and the second column representing the upper bounds of prediction intervals.

___

Reference:

- Hyndman, R. J., & Athanasopoulos, G. (2018). Forecasting: principles and practice. OTexts. otexts.com

resolution(forecasts)

Calculates the resolution of forecast intervals, measuring the average absolute difference between individual forecast interval widths and the overall sharpness measure.

Parameters:

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - The average absolute difference between individual forecast interval widths and the overall sharpness measure, representing the resolution of the forecasts.

___

Resolution is a key metric for evaluating forecast quality that measures the consistency of prediction

interval widths. It quantifies how much the individual forecast intervals vary from the average interval

width (sharpness). High resolution indicates that the forecast intervals are relatively consistent

across observations, while low resolution suggests significant variation in interval widths.

The resolution is calculated as the mean absolute deviation of individual interval widths from the

overall sharpness value. This provides insight into the uniformity of the forecast uncertainty

estimates across the forecast horizon.

Note: This function requires the forecasts matrix to have at least 2 columns (min, max) representing

the lower and upper bounds of prediction intervals.

___

Reference:

- (sites.stat.washington.edu)

- (www.jstor.org)

coverage(targets, forecasts)

Calculates the coverage probability, which is the percentage of target values that fall within the corresponding forecasted prediction intervals.

Parameters:

targets (array) : List of target values.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - Percent of target values that fall within their corresponding forecast intervals, expressed as a decimal value between 0 and 1 (or 0% and 100%).

___

Coverage probability is a crucial metric for evaluating the reliability of prediction intervals.

It measures how well the forecast intervals capture the actual observed values. An ideal forecast

should have a coverage probability close to the nominal confidence level (e.g., 90%, 95%, or 99%).

For example, if a 95% prediction interval is used, we expect approximately 95% of the actual

target values to fall within those intervals. If the coverage is significantly lower than the

nominal level, the intervals may be too narrow; if it's significantly higher, the intervals may

be too wide.

Note: This function requires the targets array and forecasts matrix to have the same number of

observations, and the forecasts matrix must have at least 2 columns (min, max) representing

the lower and upper bounds of prediction intervals.

___

Reference:

- (www.jstor.org)

pinball(tau, target, forecast)

Pinball loss function, measures the asymmetric loss for quantile forecasts.

Parameters:

tau (float) : The quantile level (between 0 and 1), where 0.5 represents the median.

target (float) : The actual observed value to compare against.

forecast (float) : The forecasted value.

Returns: - The Pinball loss value, which quantifies the distance between the forecast and target relative to the specified quantile level.

___

The Pinball loss function is specifically designed for evaluating quantile forecasts. It is

asymmetric, meaning it penalizes underestimates and overestimates differently depending on the

quantile level being evaluated.

For a given quantile τ, the loss function is defined as:

- If target >= forecast: (target - forecast) * τ

- If target < forecast: (forecast - target) * (1 - τ)

This loss function is commonly used in quantile regression and probabilistic forecasting

to evaluate how well forecasts capture specific quantiles of the target distribution.

___

Reference:

- (www.otexts.com)

pinball_mean(tau, targets, forecasts)

Calculates the mean pinball loss for quantile regression.

Parameters:

tau (float) : The quantile level (between 0 and 1), where 0.5 represents the median.

targets (array) : The actual observed values to compare against.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - The mean pinball loss value across all observations.

___

The pinball_mean() function computes the average Pinball loss across multiple observations,

making it suitable for evaluating overall forecast performance in quantile regression tasks.

This function leverages the asymmetric Pinball loss function to evaluate how well forecasts

capture specific quantiles of the target distribution. The choice of which column from the

forecasts matrix to use depends on the quantile level:

- For τ ≤ 0.5: Uses the first column (min) of forecasts

- For τ > 0.5: Uses the second column (max) of forecasts

This loss function is commonly used in quantile regression and probabilistic forecasting

to evaluate how well forecasts capture specific quantiles of the target distribution.

___

Reference:

- (www.otexts.com)

GaussianDistributionLibrary "GaussianDistribution"

This library defines a custom type `distr` representing a Gaussian (or other statistical) distribution.

It provides methods to calculate key statistical moments and scores, including mean, median, mode, standard deviation, variance, skewness, kurtosis, and Z-scores.

This library is useful for analyzing probability distributions in financial data.

Disclaimer:

I am not a mathematician, but I have implemented this library to the best of my understanding and capacity. Please be indulgent as I tried to translate statistical concepts into code as accurately as possible. Feedback, suggestions, and corrections are welcome to improve the reliability and robustness of this library.

mean(source, length)

Calculate the mean (average) of the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

Returns: Mean (μ)

stdev(source, length)

Calculate the standard deviation (σ) of the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

Returns: Standard deviation (σ)

skewness(source, length, mean, stdev)

Calculate the skewness (γ₁) of the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

@return Skewness (γ₁)

skewness(source, length)

Overloaded skewness to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Skewness (γ₁)

mode(mean, stdev, skewness)

Estimate mode - Most frequent value in the distribution (approximation based on skewness)

Parameters:

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

skewness (float) : the skewness (γ₁) of the distribution

@return Mode

mode(source, length)

Overloaded mode to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Mode

median(mean, stdev, skewness)

Estimate median - Middle value of the distribution (approximation)

Parameters:

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

skewness (float) : the skewness (γ₁) of the distribution

@return Median

median(source, length)

Overloaded median to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Median

variance(stdev)

Calculate variance (σ²) - Square of the standard deviation

Parameters:

stdev (float) : the standard deviation (σ) of the distribution

@return Variance (σ²)

variance(source, length)

Overloaded variance to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Variance (σ²)

kurtosis(source, length, mean, stdev)

Calculate kurtosis (γ₂) - Degree of "tailedness" in the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

@return Kurtosis (γ₂)

kurtosis(source, length)

Overloaded kurtosis to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Kurtosis (γ₂)

normal_score(source, mean, stdev)

Calculate Z-score (standard score) assuming a normal distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

@return Z-Score

normal_score(source, length)

Overloaded normal_score to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Z-Score

non_normal_score(source, mean, stdev, skewness, kurtosis)

Calculate adjusted Z-score considering skewness and kurtosis

Parameters:

source (float) : Distribution source (typically a price or indicator series)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

skewness (float) : the skewness (γ₁) of the distribution

kurtosis (float) : the "tailedness" in the distribution

@return Z-Score

non_normal_score(source, length)

Overloaded non_normal_score to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Z-Score

method init(this)

Initialize all statistical fields of the `distr` type

Namespace types: distr

Parameters:

this (distr)

method init(this, source, length)

Overloaded initializer to set source and length

Namespace types: distr

Parameters:

this (distr)

source (float)

length (int)

distr

Custom type to represent a Gaussian distribution

Fields:

source (series float) : Distribution source (typically a price or indicator series)

length (series int) : Window length for the distribution (must be >= 30 for meaningful statistics)

mode (series float) : Most frequent value in the distribution

median (series float) : Middle value separating the greater and lesser halves of the distribution

mean (series float) : μ (1st central moment) - Average of the distribution

stdev (series float) : σ or standard deviation (square root of the variance) - Measure of dispersion

variance (series float) : σ² (2nd central moment) - Squared standard deviation

skewness (series float) : γ₁ (3rd central moment) - Asymmetry of the distribution

kurtosis (series float) : γ₂ (4th central moment) - Degree of "tailedness" relative to a normal distribution

normal_score (series float) : Z-score assuming normal distribution

non_normal_score (series float) : Adjusted Z-score considering skewness and kurtosis

FunctionDiscreteCosineTransformLibrary "FunctionDiscreteCosineTransform"

Discrete Cosine Transform (DCT)

The Discrete Cosine Transform (DCT) is a mathematical algorithm that converts a series of samples of a signal, typically in the time domain, into another domain called the frequency or spectral domain. It's commonly used for data compression and image/video coding applications such as JPEG and MPEG standards.

The DCT works by multiplying the input sequence with specific cosine functions that are pre-defined and then summing up these products to obtain a new series of values, which represent the frequency components of the original signal. The main advantage of the DCT over other transforms like Fourier Transform is its ability to handle non-stationary signals (i.e., signals with varying statistical properties) more effectively due to its localized basis functions.

In simple terms, the DCT can be thought of as a way to break down an image or video into different frequency components and then compress them without losing too much information. This compression technique is essential for efficient transmission and storage of digital media files over the internet or on devices with limited memory capacity.

~Mixtral4x7b

___

Reference:

lcamtuf.substack.com

dct(data, len)

Discrete Cosine Transform.

Parameters:

data (array) : Data source.

len (int) : Length of the sampling window.

Returns: List with frequency domain transformed information.

dct(data, len)

Discrete Cosine Transform.

Parameters:

data (float) : Data source.

len (int) : Length of the sampling window.

Returns: List with frequency domain transformed information.

idct(data, len)

Inverse Discrete Cosine Transform.

Parameters:

data (array) : Data source.

len (int) : Length of the sampling window.

Returns: List with time domain transformed information.

idct(data, len)

Inverse Discrete Cosine Transform.

Parameters:

data (float) : Data source.

len (int) : Length of the sampling window.

Returns: List with time domain transformed information.

Supertrend Advance Pullback StrategyHandbook for the Supertrend Advance Strategy

1. Introduction

Purpose of the Handbook:

The main purpose of this handbook is to serve as a comprehensive guide for traders and investors who are looking to explore and harness the potential of the Supertrend Advance Strategy. In the rapidly changing financial market, having the right tools and strategies at one's disposal is crucial. Whether you're a beginner hoping to dive into the world of trading or a seasoned investor aiming to optimize and diversify your portfolio, this handbook offers the insights and methodologies you need. By the end of this guide, readers should have a clear understanding of how the Supertrend Advance Strategy works, its benefits, potential pitfalls, and practical application in various trading scenarios.

Overview of the Supertrend Advance Pullback Strategy:

At its core, the Supertrend Advance Strategy is an evolution of the popular Supertrend Indicator. Designed to generate buy and sell signals in trending markets, the Supertrend Indicator has been a favorite tool for many traders around the world. The Advance Strategy, however, builds upon this foundation by introducing enhanced mechanisms, filters, and methodologies to increase precision and reduce false signals.

1. Basic Concept:

The Supertrend Advance Strategy relies on a combination of price action and volatility to determine the potential trend direction. By assessing the average true range (ATR) in conjunction with specific price points, this strategy aims to highlight the potential starting and ending points of market trends.

2. Methodology:

Unlike the traditional Supertrend Indicator, which primarily focuses on closing prices and ATR, the Advance Strategy integrates other critical market variables, such as volume, momentum oscillators, and perhaps even fundamental data, to validate its signals. This multidimensional approach ensures that the generated signals are more reliable and are less prone to market noise.

3. Benefits:

One of the main benefits of the Supertrend Advance Strategy is its ability to filter out false breakouts and minor price fluctuations, which can often lead to premature exits or entries in the market. By waiting for a confluence of factors to align, traders using this advanced strategy can increase their chances of entering or exiting trades at optimal points.

4. Practical Applications:

The Supertrend Advance Strategy can be applied across various timeframes, from intraday trading to swing trading and even long-term investment scenarios. Furthermore, its flexible nature allows it to be tailored to different asset classes, be it stocks, commodities, forex, or cryptocurrencies.

In the subsequent sections of this handbook, we will delve deeper into the intricacies of this strategy, offering step-by-step guidelines on its application, case studies, and tips for maximizing its efficacy in the volatile world of trading.

As you journey through this handbook, we encourage you to approach the Supertrend Advance Strategy with an open mind, testing and tweaking it as per your personal trading style and risk appetite. The ultimate goal is not just to provide you with a new tool but to empower you with a holistic strategy that can enhance your trading endeavors.

2. Getting Started

Navigating the financial markets can be a daunting task without the right tools. This section is dedicated to helping you set up the Supertrend Advance Strategy on one of the most popular charting platforms, TradingView. By following the steps below, you'll be able to integrate this strategy into your charts and start leveraging its insights in no time.

Setting up on TradingView:

TradingView is a web-based platform that offers a wide range of charting tools, social networking, and market data. Before you can apply the Supertrend Advance Strategy, you'll first need a TradingView account. If you haven't set one up yet, here's how:

1. Account Creation:

• Visit TradingView's official website.

• Click on the "Join for free" or "Sign up" button.

• Follow the registration process, providing the necessary details and setting up your login credentials.

2. Navigating the Dashboard:

• Once logged in, you'll be taken to your dashboard. Here, you'll see a variety of tools, including watchlists, alerts, and the main charting window.

• To begin charting, type in the name or ticker of the asset you're interested in the search bar at the top.

3. Configuring Chart Settings:

• Before integrating the Supertrend Advance Strategy, familiarize yourself with the chart settings. This can be accessed by clicking the 'gear' icon on the top right of the chart window.

• Adjust the chart type, time intervals, and other display settings to your preference.

Integrating the Strategy into a Chart:

Now that you're set up on TradingView, it's time to integrate the Supertrend Advance Strategy.

1. Accessing the Pine Script Editor:

• Located at the top-center of your screen, you'll find the "Pine Editor" tab. Click on it.

• This is where custom strategies and indicators are scripted or imported.

2. Loading the Supertrend Advance Strategy Script:

• Depending on whether you have the script or need to find it, there are two paths:

• If you have the script: Copy the Supertrend Advance Strategy script, and then paste it into the Pine Editor.

• If searching for the script: Click on the “Indicators” icon (looks like a flame) at the top of your screen, and then type “Supertrend Advance Strategy” in the search bar. If available, it will show up in the list. Simply click to add it to your chart.

3. Applying the Strategy:

• After pasting or selecting the Supertrend Advance Strategy in the Pine Editor, click on the “Add to Chart” button located at the top of the editor. This will overlay the strategy onto your main chart window.

4. Configuring Strategy Settings:

• Once the strategy is on your chart, you'll notice a small settings ('gear') icon next to its name in the top-left of the chart window. Click on this to access settings.

• Here, you can adjust various parameters of the Supertrend Advance Strategy to better fit your trading style or the specific asset you're analyzing.

5. Interpreting Signals:

• With the strategy applied, you'll now see buy/sell signals represented on your chart. Take time to familiarize yourself with how these look and behave over various timeframes and market conditions.

3. Strategy Overview

What is the Supertrend Advance Strategy?

The Supertrend Advance Strategy is a refined version of the classic Supertrend Indicator, which was developed to aid traders in spotting market trends. The strategy utilizes a combination of data points, including average true range (ATR) and price momentum, to generate buy and sell signals.

In essence, the Supertrend Advance Strategy can be visualized as a line that moves with the price. When the price is above the Supertrend line, it indicates an uptrend and suggests a potential buy position. Conversely, when the price is below the Supertrend line, it hints at a downtrend, suggesting a potential selling point.

Strategy Goals and Objectives:

1. Trend Identification: At the core of the Supertrend Advance Strategy is the goal to efficiently and consistently identify prevailing market trends. By recognizing these trends, traders can position themselves to capitalize on price movements in their favor.

2. Reducing Noise: Financial markets are often inundated with 'noise' - short-term price fluctuations that can mislead traders. The Supertrend Advance Strategy aims to filter out this noise, allowing for clearer decision-making.

3. Enhancing Risk Management: With clear buy and sell signals, traders can set more precise stop-loss and take-profit points. This leads to better risk management and potentially improved profitability.

4. Versatility: While primarily used for trend identification, the strategy can be integrated with other technical tools and indicators to create a comprehensive trading system.

Type of Assets/Markets to Apply the Strategy:

1. Equities: The Supertrend Advance Strategy is highly popular among stock traders. Its ability to capture long-term trends makes it particularly useful for those trading individual stocks or equity indices.

2. Forex: Given the 24-hour nature of the Forex market and its propensity for trends, the Supertrend Advance Strategy is a valuable tool for currency traders.

3. Commodities: Whether it's gold, oil, or agricultural products, commodities often move in extended trends. The strategy can help in identifying and capitalizing on these movements.

4. Cryptocurrencies: The volatile nature of cryptocurrencies means they can have pronounced trends. The Supertrend Advance Strategy can aid crypto traders in navigating these often tumultuous waters.

5. Futures & Options: Traders and investors in derivative markets can utilize the strategy to make more informed decisions about contract entries and exits.

It's important to note that while the Supertrend Advance Strategy can be applied across various assets and markets, its effectiveness might vary based on market conditions, timeframe, and the specific characteristics of the asset in question. As always, it's recommended to use the strategy in conjunction with other analytical tools and to backtest its effectiveness in specific scenarios before committing to trades.

4. Input Settings

Understanding and correctly configuring input settings is crucial for optimizing the Supertrend Advance Strategy for any specific market or asset. These settings, when tweaked correctly, can drastically impact the strategy's performance.

Grouping Inputs:

Before diving into individual input settings, it's important to group similar inputs. Grouping can simplify the user interface, making it easier to adjust settings related to a specific function or indicator.

Strategy Choice:

This input allows traders to select from various strategies that incorporate the Supertrend indicator. Options might include "Supertrend with RSI," "Supertrend with MACD," etc. By choosing a strategy, the associated input settings for that strategy become available.

Supertrend Settings:

1. Multiplier: Typically, a default value of 3 is used. This multiplier is used in the ATR calculation. Increasing it makes the Supertrend line further from prices, while decreasing it brings the line closer.

2. Period: The number of bars used in the ATR calculation. A common default is 7.

EMA Settings (Exponential Moving Average):

1. Period: Defines the number of previous bars used to calculate the EMA. Common periods are 9, 21, 50, and 200.

2. Source: Allows traders to choose which price (Open, Close, High, Low) to use in the EMA calculation.

RSI Settings (Relative Strength Index):

1. Length: Determines how many periods are used for RSI calculation. The standard setting is 14.

2. Overbought Level: The threshold at which the asset is considered overbought, typically set at 70.

3. Oversold Level: The threshold at which the asset is considered oversold, often at 30.

MACD Settings (Moving Average Convergence Divergence):

1. Short Period: The shorter EMA, usually set to 12.

2. Long Period: The longer EMA, commonly set to 26.

3. Signal Period: Defines the EMA of the MACD line, typically set at 9.

CCI Settings (Commodity Channel Index):

1. Period: The number of bars used in the CCI calculation, often set to 20.

2. Overbought Level: Typically set at +100, denoting overbought conditions.

3. Oversold Level: Usually set at -100, indicating oversold conditions.

SL/TP Settings (Stop Loss/Take Profit):

1. SL Multiplier: Defines the multiplier for the average true range (ATR) to set the stop loss.

2. TP Multiplier: Defines the multiplier for the average true range (ATR) to set the take profit.

Filtering Conditions:

This section allows traders to set conditions to filter out certain signals. For example, one might only want to take buy signals when the RSI is below 30, ensuring they buy during oversold conditions.

Trade Direction and Backtest Period:

1. Trade Direction: Allows traders to specify whether they want to take long trades, short trades, or both.

2. Backtest Period: Specifies the time range for backtesting the strategy. Traders can choose from options like 'Last 6 months,' 'Last 1 year,' etc.

It's essential to remember that while default settings are provided for many of these tools, optimal settings can vary based on the market, timeframe, and trading style. Always backtest new settings on historical data to gauge their potential efficacy.

5. Understanding Strategy Conditions

Developing an understanding of the conditions set within a trading strategy is essential for traders to maximize its potential. Here, we delve deep into the logic behind these conditions, using the Supertrend Advance Strategy as our focal point.

Basic Logic Behind Conditions:

Every strategy is built around a set of conditions that provide buy or sell signals. The conditions are based on mathematical or statistical methods and are rooted in the study of historical price data. The fundamental idea is to recognize patterns or behaviors that have been profitable in the past and might be profitable in the future.

Buy and Sell Conditions:

1. Buy Conditions: Usually formulated around bullish signals or indicators suggesting upward price momentum.

2. Sell Conditions: Centered on bearish signals or indicators indicating downward price momentum.

Simple Strategy:

The simple strategy could involve using just the Supertrend indicator. Here:

• Buy: When price closes above the Supertrend line.

• Sell: When price closes below the Supertrend line.

Pullback Strategy:

This strategy capitalizes on price retracements:

• Buy: When the price retraces to the Supertrend line after a bullish signal and is supported by another bullish indicator.

• Sell: When the price retraces to the Supertrend line after a bearish signal and is confirmed by another bearish indicator.

Indicators Used:

EMA (Exponential Moving Average):

• Logic: EMA gives more weight to recent prices, making it more responsive to current price movements. A shorter-period EMA crossing above a longer-period EMA can be a bullish sign, while the opposite is bearish.

RSI (Relative Strength Index):

• Logic: RSI measures the magnitude of recent price changes to analyze overbought or oversold conditions. Values above 70 are typically considered overbought, and values below 30 are considered oversold.

MACD (Moving Average Convergence Divergence):

• Logic: MACD assesses the relationship between two EMAs of a security’s price. The MACD line crossing above the signal line can be a bullish signal, while crossing below can be bearish.

CCI (Commodity Channel Index):

• Logic: CCI compares a security's average price change with its average price variation. A CCI value above +100 may mean the price is overbought, while below -100 might signify an oversold condition.

And others...

As the strategy expands or contracts, more indicators might be added or removed. The crucial point is to understand the core logic behind each, ensuring they align with the strategy's objectives.

Logic Behind Each Indicator:

1. EMA: Emphasizes recent price movements; provides dynamic support and resistance levels.

2. RSI: Indicates overbought and oversold conditions based on recent price changes.

3. MACD: Showcases momentum and direction of a trend by comparing two EMAs.

4. CCI: Measures the difference between a security's price change and its average price change.

Understanding strategy conditions is not just about knowing when to buy or sell but also about comprehending the underlying market dynamics that those conditions represent. As you familiarize yourself with each condition and indicator, you'll be better prepared to adapt and evolve with the ever-changing financial markets.

6. Trade Execution and Management

Trade execution and management are crucial aspects of any trading strategy. Efficient execution can significantly impact profitability, while effective management can preserve capital during adverse market conditions. In this section, we'll explore the nuances of position entry, exit strategies, and various Stop Loss (SL) and Take Profit (TP) methodologies within the Supertrend Advance Strategy.

Position Entry:

Effective trade entry revolves around:

1. Timing: Enter at a point where the risk-reward ratio is favorable. This often corresponds to confirmatory signals from multiple indicators.

2. Volume Analysis: Ensure there's adequate volume to support the movement. Volume can validate the strength of a signal.

3. Confirmation: Use multiple indicators or chart patterns to confirm the entry point. For instance, a buy signal from the Supertrend indicator can be confirmed with a bullish MACD crossover.

Position Exit Strategies:

A successful exit strategy will lock in profits and minimize losses. Here are some strategies:

1. Fixed Time Exit: Exiting after a predetermined period.

2. Percentage-based Profit Target: Exiting after a certain percentage gain.

3. Indicator-based Exit: Exiting when an indicator gives an opposing signal.

Percentage-based SL/TP:

• Stop Loss (SL): Set a fixed percentage below the entry price to limit potential losses.

• Example: A 2% SL on an entry at $100 would trigger a sell at $98.

• Take Profit (TP): Set a fixed percentage above the entry price to lock in gains.

• Example: A 5% TP on an entry at $100 would trigger a sell at $105.

Supertrend-based SL/TP:

• Stop Loss (SL): Position the SL at the Supertrend line. If the price breaches this line, it could indicate a trend reversal.

• Take Profit (TP): One could set the TP at a point where the Supertrend line flattens or turns, indicating a possible slowdown in momentum.

Swing high/low-based SL/TP:

• Stop Loss (SL): For a long position, set the SL just below the recent swing low. For a short position, set it just above the recent swing high.

• Take Profit (TP): For a long position, set the TP near a recent swing high or resistance. For a short position, near a swing low or support.

And other methods...

1. Trailing Stop Loss: This dynamic SL adjusts with the price movement, locking in profits as the trade moves in your favor.

2. Multiple Take Profits: Divide the position into segments and set multiple TP levels, securing profits in stages.

3. Opposite Signal Exit: Exit when another reliable indicator gives an opposite signal.

Trade execution and management are as much an art as they are a science. They require a blend of analytical skill, discipline, and intuition. Regularly reviewing and refining your strategies, especially in light of changing market conditions, is crucial to maintaining consistent trading performance.

7. Visual Representations

Visual tools are essential for traders, as they simplify complex data into an easily interpretable format. Properly analyzing and understanding the plots on a chart can provide actionable insights and a more intuitive grasp of market conditions. In this section, we’ll delve into various visual representations used in the Supertrend Advance Strategy and their significance.

Understanding Plots on the Chart:

Charts are the primary visual aids for traders. The arrangement of data points, lines, and colors on them tell a story about the market's past, present, and potential future moves.

1. Data Points: These represent individual price actions over a specific timeframe. For instance, a daily chart will have data points showing the opening, closing, high, and low prices for each day.

2. Colors: Used to indicate the nature of price movement. Commonly, green is used for bullish (upward) moves and red for bearish (downward) moves.

Trend Lines:

Trend lines are straight lines drawn on a chart that connect a series of price points. Their significance:

1. Uptrend Line: Drawn along the lows, representing support. A break below might indicate a trend reversal.

2. Downtrend Line: Drawn along the highs, indicating resistance. A break above might suggest the start of a bullish trend.

Filled Areas:

These represent a range between two values on a chart, usually shaded or colored. For instance:

1. Bollinger Bands: The area between the upper and lower band is filled, giving a visual representation of volatility.

2. Volume Profile: Can show a filled area representing the amount of trading activity at different price levels.

Stop Loss and Take Profit Lines:

These are horizontal lines representing pre-determined exit points for trades.

1. Stop Loss Line: Indicates the level at which a trade will be automatically closed to limit losses. Positioned according to the trader's risk tolerance.

2. Take Profit Line: Denotes the target level to lock in profits. Set according to potential resistance (for long trades) or support (for short trades) or other technical factors.

Trailing Stop Lines:

A trailing stop is a dynamic form of stop loss that moves with the price. On a chart:

1. For Long Trades: Starts below the entry price and moves up with the price but remains static if the price falls, ensuring profits are locked in.

2. For Short Trades: Starts above the entry price and moves down with the price but remains static if the price rises.

Visual representations offer traders a clear, organized view of market dynamics. Familiarity with these tools ensures that traders can quickly and accurately interpret chart data, leading to more informed decision-making. Always ensure that the visual aids used resonate with your trading style and strategy for the best results.

8. Backtesting

Backtesting is a fundamental process in strategy development, enabling traders to evaluate the efficacy of their strategy using historical data. It provides a snapshot of how the strategy would have performed in past market conditions, offering insights into its potential strengths and vulnerabilities. In this section, we'll explore the intricacies of setting up and analyzing backtest results and the caveats one must be aware of.

Setting Up Backtest Period:

1. Duration: Determine the timeframe for the backtest. It should be long enough to capture various market conditions (bullish, bearish, sideways). For instance, if you're testing a daily strategy, consider a period of several years.

2. Data Quality: Ensure the data source is reliable, offering high-resolution and clean data. This is vital to get accurate backtest results.

3. Segmentation: Instead of a continuous period, sometimes it's helpful to backtest over distinct market phases, like a particular bear or bull market, to see how the strategy holds up in different environments.

Analyzing Backtest Results:

1. Performance Metrics: Examine metrics like the total return, annualized return, maximum drawdown, Sharpe ratio, and others to gauge the strategy's efficiency.

2. Win Rate: It's the ratio of winning trades to total trades. A high win rate doesn't always signify a good strategy; it should be evaluated in conjunction with other metrics.

3. Risk/Reward: Understand the average profit versus the average loss per trade. A strategy might have a low win rate but still be profitable if the average gain far exceeds the average loss.

4. Drawdown Analysis: Review the periods of losses the strategy could incur and how long it takes, on average, to recover.

9. Tips and Best Practices

Successful trading requires more than just knowing how a strategy works. It necessitates an understanding of when to apply it, how to adjust it to varying market conditions, and the wisdom to recognize and avoid common pitfalls. This section offers insightful tips and best practices to enhance the application of the Supertrend Advance Strategy.

When to Use the Strategy:

1. Market Conditions: Ideally, employ the Supertrend Advance Strategy during trending market conditions. This strategy thrives when there are clear upward or downward trends. It might be less effective during consolidative or sideways markets.

2. News Events: Be cautious around significant news events, as they can cause extreme volatility. It might be wise to avoid trading immediately before and after high-impact news.

3. Liquidity: Ensure you are trading in assets/markets with sufficient liquidity. High liquidity ensures that the price movements are more reflective of genuine market sentiment and not due to thin volume.

Adjusting Settings for Different Markets/Timeframes:

1. Markets: Each market (stocks, forex, commodities) has its own characteristics. It's essential to adjust the strategy's parameters to align with the market's volatility and liquidity.

2. Timeframes: Shorter timeframes (like 1-minute or 5-minute charts) tend to have more noise. You might need to adjust the settings to filter out false signals. Conversely, for longer timeframes (like daily or weekly charts), you might need to be more responsive to genuine trend changes.

3. Customization: Regularly review and tweak the strategy's settings. Periodic adjustments can ensure the strategy remains optimized for the current market conditions.

10. Frequently Asked Questions (FAQs)

Given the complexities and nuances of the Supertrend Advance Strategy, it's only natural for traders, both new and seasoned, to have questions. This section addresses some of the most commonly asked questions regarding the strategy.

1. What exactly is the Supertrend Advance Strategy?

The Supertrend Advance Strategy is an evolved version of the traditional Supertrend indicator. It's designed to provide clearer buy and sell signals by incorporating additional indicators like EMA, RSI, MACD, CCI, etc. The strategy aims to capitalize on market trends while minimizing false signals.

2. Can I use the Supertrend Advance Strategy for all asset types?