Opening Range Breakout with VWAP & RSI ConfirmationThis indicator identifies breakout trading opportunities based on the Opening Range Breakout (ORB) strategy combined with intraday VWAP and higher timeframe RSI confirmation.

Opening Range: Calculates the high, low, and midpoint of the first 15 or 30 minutes (configurable) after your specified market open time.

Intraday VWAP: A volume-weighted average price calculated manually and reset daily, tracking price action throughout the trading day.

RSI Confirmation: Uses RSI from a user-selected higher timeframe (1H, 4H, or Daily) to confirm signals.

Buy Signal: Triggered when VWAP breaks above the Opening Range High AND the RSI is below or equal to the buy threshold (default 30).

Sell Signal: Triggered when VWAP breaks below the Opening Range Low AND the RSI is above or equal to the sell threshold (default 70).

Visuals: Plots Opening Range levels and VWAP on the chart with clear buy/sell markers and optional labels showing RSI values.

Alerts: Provides alert conditions for buy and sell signals to facilitate timely trading decisions.

This tool helps traders capture momentum breakouts while filtering trades based on momentum strength indicated by RSI.

Cari dalam skrip untuk "港股央企红利etf"

LSTM-Inspired BB Mean Reversion// ============================================================================

// BOLLINGER BANDS MEAN REVERSION STRATEGY

// Based on LSTM Model True Positive Signal Characteristics

// ============================================================================

// Model learned to identify:

// 1. Price at/below Lower Bollinger Band (100% of TP signals)

// 2. RSI < 30 (Oversold) (75% of TP signals)

// 3. High volatility (wide BB bands)

// 4. Below average volume (contrarian)

// ============================================================================

Dual Pivot StructureDual Pivot Structure: Speed vs. Stability

Overview

This script is an experimental prototype designed to solve the most common frustration with Market Structure indicators: The Trade-off between Lag and Noise.

In traditional Price Action analysis, verifying a Pivot High or Low requires waiting for X number of candles to close.

High Lookback (e.g., 5 bars): Reliable structure, but the signal appears too late to trade.

Low Lookback (e.g., 1 bar): Fast signals, but prone to "fake-outs" and noise.

This indicator runs both logic systems simultaneously, allowing traders to see the "True" market structure while receiving "Early Warning" signals for potential entries.

How It Works

The script calculates two parallel layers of market data:

1. The "Structure" Layer (Slow & Reliable)

Uses a standard, higher lookback period (Default: 5 Left / 5 Right).

Purpose: Defines the macro trend. It labels confirmed Higher Highs (HH), Lower Lows (LL), etc.

Visual: Solid colored labels. These confirm the trend bias.

2. The "Signal" Layer (Fast & Actionable)

Uses a rapid, minimal lookback period (Default: 1 Left / 1 Right).

Purpose: Hunts for potential reversals within the macro trend.

Logic: If the Macro Trend is bullish, but price pulls back, this layer looks for a "Micro Pivot" that is higher than the previous Macro Low.

Visual: Orange "⚠ HL?" or "⚠ LH?" text.

How to Use This Script

This tool is best used to time entries within an established trend.

Identify the Trend: Look at the Solid Labels (Green/Red). Are we making HHs and HLs? The trend is Up.

Wait for the Pullback: Allow price to retrace.

Watch for the Early Warning: Look for the orange "⚠ HL?" text.

This appears bars before the structural pivot is confirmed.

The Signal: This is your aggressive entry trigger or alert to watch for a lower timeframe change of character.

Confirmation: If price continues in your direction, the script will eventually print a solid HL label, confirming your early entry was correct.

Settings

Structure Settings: Controls the sensitivity of the main trend (Default: 5/5). Increase this for higher timeframes to filter noise.

Signal Settings: Controls the sensitivity of the early warnings (Default: 1/1). Keep this low for maximum speed.

Visuals: Toggle the "Early Warning" labels on/off and customize colors to fit your chart theme.

Disclaimer

This script is a prototype for educational purposes. The "Early Warning" signals are, by definition, unconfirmed and carry higher risk. Always manage risk accordingly.

MACD X SignalsThis is a fundamental signal indicator based on MACD crossovers. It enhances the standard MACD by adding visual labels that classify signals based on their location relative to the Zero Line. This helps identify whether a trend is reversing, continuing, or potentially overextended.

Signal Legend:

B (Reversal): Bullish crossover in the Negative Zone .

B+ (Neutral): Bullish crossover in the Middle Zone .

B- (Trend): Bullish crossover in the Positive Zone

S : MACD crossing down (Bearish signal).

SMC IndicatorTitle: Smart Money Concepts Market Structure

Description: This is a technical analysis tool designed to map Market Structure using Smart Money Concepts (SMC) logic. Unlike standard ZigZag indicators that often clutter the chart with repainting lines, this script focuses on delivering a clean, objective view of Trend Structure (Highs/Lows) and Structural Breaks.

The Problem It Solves: Traders often struggle to identify the valid "Swing High" or "Swing Low" in real-time. This indicator automates that process using a non-repainting detection engine, helping traders objectively spot Trend Continuations (BoS) and Potential Reversals (CHoCH).

How It Works:

1. Pivot Detection (The ZigZag Engine): The script identifies Swing Points based on a user-defined Depth and Deviation %.

High (H): A peak is confirmed when price retraces by the deviation percentage.

Low (L): A trough is confirmed when price rallies by the deviation percentage.

Ghost Line: A dotted line connects the last confirmed pivot to the current live price, allowing you to visualize the developing structure before it locks in.

2. Structure Mapping: Once pivots are confirmed, the script analyzes price action relative to those points:

BoS (Break of Structure): Trend Continuation. Triggered when price breaks a confirmed pivot in the direction of the trend (e.g., breaking a Higher High in an uptrend).

CHoCH (Change of Character): Trend Reversal. Triggered when price breaks a major pivot in the opposite direction (e.g., breaking a Higher Low in an uptrend).

Visual Features:

Minimalist Design: Uses floating text labels (no background boxes) to keep price action visible.

Color Coded: Blue/Maroon for Continuation (BoS), Aqua/Orange for Reversal (CHoCH).

Settings Guide:

ZigZag Deviation %: Set this to 5.0 for Higher Timeframes (Daily/4H) or lower it to 0.2 - 0.5 for Intraday Scalping (1m/5m).

Ghost Line: Toggle on/off to see the real-time projection.

Alerts: Full alert support included for Bullish/Bearish BoS and CHoCH signals.

Credits: Logic based on standard Price Action and Market Structure theory.

Squeeze Momentum OscillatorTitle: Squeeze Momentum Oscillator

Description: This indicator is a panel-based oscillator designed to visualize the relationship between market volatility and momentum. Based on the classic TTM Squeeze concept, it helps traders identify periods of consolidation ("The Squeeze") and the subsequent release of energy ("The Breakout").

Originality & Enhancements: Standard squeeze oscillators only show when a squeeze fires (turning from red to green). This enhanced version adds a specific Breakout Validation layer. It changes the center-line dot color to Fuchsia or Blue only if the squeeze release is confirmed by the slope of the 20-period Moving Average, filtering out weak or false fires.

How It Works:

1. The Center Line (Volatility State): The dots along the zero line tell you the current volatility condition:

🔴 Red Dot: Squeeze ON. Bollinger Bands are inside Keltner Channels. Volatility is compressed. The market is charging up.

🟣 Fuchsia Dot: Bullish Breakout. The squeeze has fired upward, and the underlying trend (20 SMA slope) is positive.

🔵 Blue Dot: Bearish Breakout. The squeeze has fired downward, and the underlying trend (20 SMA slope) is negative.

🟢 Green Dot: Squeeze OFF. Normal volatility conditions.

2. The Histogram (Momentum): The bars indicate the strength and direction of the price movement using Linear Regression logic:

Cyan/Green: Bullish momentum. (Darker = weakening).

Red/Maroon: Bearish momentum. (Darker = weakening).

Visual Guide:

Setup: Wait for a series of Red Dots.

Trigger: Look for the first Fuchsia (Bullish) or Blue (Bearish) dot accompanied by an expanding Histogram in the same direction.

Settings:

Feature Toggle: You can turn the "Breakout Colors" (Fuchsia/Blue) on or off if you prefer the classic look.

Sensitivity: Fully customizable lengths and multipliers for Bollinger Bands and Keltner Channels.

Credits: Based on the foundational TTM Squeeze oscillator logic. Linear regression momentum calculation adapted from standard open-source methods. Breakout validation logic added for enhanced reliability.

Ultimate Squeeze & BreakoutTitle: Ultimate Squeeze & Breakout

Description: This indicator is a volatility analysis tool designed to identify periods of market compression ("The Squeeze") and validate subsequent breakouts using momentum logic. It builds upon the classic relation between Bollinger Bands and Keltner Channels but adds a directional filter to reduce false signals.

The Problem It Solves: Standard squeeze indicators often signal a breakout the moment price exits the bands, even if the underlying trend is weak or flat. This can lead to entering "wicks" or fakeouts. This script solves this by requiring the Basis Line Slope to align with the breakout direction before generating a signal.

How It Works:

1. Compression (The Setup) The script monitors the relationship between Bollinger Bands (Standard Deviation) and Keltner Channels (ATR).

Red Cloud: When the Bollinger Bands contract completely inside the Keltner Channels, it indicates a critical drop in volatility. The market is coiling and storing energy.

2. The Momentum Filter (The Validation) Unlike basic squeeze indicators, a breakout is not signaled solely by price closing outside the bands.

Logic: The script calculates the slope of the 20-period Basis Line (Simple Moving Average).

Bullish Validation: Price > Upper Band AND Basis Line is sloping UP.

Bearish Validation: Price < Lower Band AND Basis Line is sloping DOWN.

Visual Guide:

🟥 Red Cloud: Squeeze ON. Volatility is compressed. Do not trade; wait for expansion.

🟣 Fuchsia Cloud: Bullish Breakout (Price released upward + Positive Momentum).

🔵 Blue Cloud: Bearish Breakout (Price released downward + Negative Momentum).

⬜ Gray/Green Cloud: Standard Trending phase (Volatility is normal).

Features:

Precision Inputs: Multipliers for Standard Deviation and ATR can be adjusted in 0.01 increments for fine-tuning sensitivity.

Visual Toggles: Option to color the neutral trending cloud Green or Gray based on preference.

Alerts: Built-in alerts for "Squeeze Started" and validated "Bullish/Bearish Breakouts."

Credits: Core mechanics based on the TTM Squeeze concept popularized by John Carter. Momentum filtering logic added for enhanced signal reliability.

Simple Gap IndicatorTitle: Simple Gap Indicator

Description: This is a utility script designed to automate the tracking and management of price gaps (also known as "Windows") on the chart. Unlike static drawings, this indicator dynamically monitors open gaps and automatically "closes" them (stops drawing) once price has filled the area, keeping your chart clean and focused on active levels only.

Why Use This Tool? Traders often mark gaps manually, but charts quickly become cluttered with old, invalid levels. This script solves that problem by using an array-based management system to track every open gap in real-time and remove it the moment it is invalidated by price action.

Technical Methodology:

Gap Detection: The script identifies "Full Gaps" where the Low of the current candle is higher than the High of the previous candle (Bullish), or vice versa (Bearish). This indicates a total disconnect in price delivery.

Dynamic Filtering:

ATR Filter: Users can filter out insignificant "noise" gaps by setting a minimum size threshold based on the Average True Range (ATR).

Time Filter: Option to restrict gap detection to specific session hours (e.g., ignoring overnight gaps on 24h charts).

Auto-Closure: The script loops through all active gaps on every new bar. If the current price wick touches an open gap, the box is visually terminated at that specific bar index and removed from the tracking array.

Visuals:

Green Box: Bullish Gap (Support Zone).

Red Box: Bearish Gap (Resistance Zone).

Labels: Optional text displaying the precise Top/Bottom price coordinates of the gap.

How to Use:

Enable "Auto-Close Gap on Retest" to keep your chart clean.

Use the ATR Filter if you are getting too many signals on lower timeframes (e.g., set to 0.5x ATR).

Set alerts for "New Gap" or "Gap Filled" to automate your workflow.

Credits: Calculations based on standard Gap/Window price action theory. Array management logic custom-coded for Pine Script v6.

WOLFGATEWOLFGATE is a clean, session-aware market structure and regime framework designed to help traders contextualize price action using widely accepted institutional references. The indicator focuses on structure, momentum alignment, and mean interaction, without generating trade signals or predictions.

This script is built for clarity and decision support. It provides a consistent way to evaluate market conditions across different environments while remaining flexible to individual trading styles.

What This Indicator Displays

Momentum & Structure Averages

9 EMA — Short-term momentum driver

21 EMA — Structural control and trend confirmation

200 SMA — Primary regime boundary

400 SMA (optional) — Deep regime / macro bias reference

These averages are intended to help assess directional alignment, trend strength, and structural consistency.

Session VWAP (Institutional Mean)

Session-based VWAP with a clean daily reset

Default session: 09:30–16:00 ET

Uses HLC3 as the VWAP source for balanced price input

Rendered in a high-contrast institutional blue for visibility

VWAP can be used to evaluate mean interaction, acceptance, or rejection during the active session.

How to Use WOLFGATE

This framework is designed for context, not signals.

Traders may use WOLFGATE to:

Identify bullish or bearish market regimes

Evaluate momentum alignment across multiple time horizons

Observe price behavior relative to VWAP

Maintain directional bias during trending conditions

Avoid low-quality conditions when structure is misaligned

The indicator does not generate buy or sell signals and does not include alerts or automated execution logic.

Important Notes

Volume must be added separately using TradingView’s built-in Volume indicator

(Volume cannot be embedded directly into this script due to platform limitations.)

This script is intended for educational and analytical purposes only

No financial advice is provided

Users are responsible for their own risk management and trade decisions

Optimal Daily MA Suite [MTF]Title: Optimal Daily MA Suite

Description: This is a comprehensive Multi-Timeframe (MTF) analysis suite designed to streamline chart layouts. Instead of loading multiple separate indicators to track various trend lines, this single tool allows traders to overlay higher-timeframe Moving Averages and key support/resistance levels directly onto their intraday charts.

Utility & Workflow: Swing traders and day traders often need to monitor "Big Picture" Daily Moving Averages (like the Daily 200 SMA or Daily 50 EMA) while executing trades on lower timeframes like the 15m or 1H. This tool automates that process, ensuring the major trend context is always visible without cluttering the indicator list.

Key Features:

Multi-Timeframe Engine: By default, all MAs are calculated on the Daily ("D") timeframe, regardless of the chart's current timeframe. This creates a stable "anchor" for trend analysis. The timeframe is fully customizable in the settings (e.g., set to "W" for Weekly analysis).

10 Customizable Slots: Toggle up to 10 different Moving Averages on/off individually.

Flexible Calculation Types: Supports SMA, EMA, WMA, VWMA, RMA (SMMA), and SWMA for every single line.

Trend Cloud Crossovers: Includes two dedicated "Cloud" setups to visualize crossovers (e.g., Golden Cross or Death Cross) with fill shading between the fast and slow lines.

Price Action Crossovers: Optional markers to highlight when the closing price crosses specific MAs.

Contextual Levels: Includes Previous Day High (PDH) and Previous Day Low (PDL) markers for immediate intraday support/resistance context.

How to Use:

Settings: Open the settings menu to select your "Indicator Timeframe" (Default: Daily).

Customization: Enable only the MAs relevant to your strategy (e.g., Enable MA 8 for the 50 SMA and MA 10 for the 200 SMA).

Clouds: Use the "Crossover Set" inputs to define a Bullish/Bearish trend cloud between two moving averages of your choice.

Technical Note: This script uses request.security with lookahead=barmerge.lookahead_off to ensure no repainting of historical data while providing accurate higher-timeframe values on closed bars.

Credits: Standard Moving Average calculations based on TradingView built-in functions.

ORB + FVG A+ PRO (All-in-One) [QQQ]Configurable ORB + FVG + filters (VIX, ORB range, relative volume) + A+ PRO (retest at the FVG edge + rejection) + anti-fakeout + orange reminder “CONFIRM POC/HVN (Volume Profile)” right when the A+ signal appears

Alertes Trading Manuel//@version=6

indicator("Signal simple +0.5% LONG", overlay = true)

// --- Paramètres ---

tpPctInput = input.float(0.5, "TP (%)", step = 0.1) // objectif pour toi : 0.5%

slPctInput = input.float(0.3, "SL (%)", step = 0.1) // SL indicatif : 0.3%

tpPct = tpPctInput / 100.0

slPct = slPctInput / 100.0

emaLenFast = input.int(50, "EMA rapide (intraday)", minval = 1)

emaLenSlow = input.int(200, "EMA lente (intraday)", minval = 1)

volLen = input.int(20, "Période moyenne Volume", minval = 1)

// --- Tendance daily : MA200 jours ---

ma200D = request.security(syminfo.tickerid, "D", ta.sma(close, 200))

above200D = close > ma200D

// --- Tendance intraday ---

emaFast = ta.ema(close, emaLenFast)

emaSlow = ta.ema(close, emaLenSlow)

upTrendIntraday = close > emaFast and emaFast > emaSlow

// --- MACD & RSI ---

= ta.macd(close, 12, 26, 9)

rsi = ta.rsi(close, 14)

macdOK = macdLine > macdSignal

rsiOK = rsi > 49 and rsi < 75

// --- Volume ---

volMa = ta.sma(volume, volLen)

volOK = volume > volume and volume > volMa

// --- Signal LONG simple ---

longSignal = above200D and upTrendIntraday and macdOK and rsiOK and volOK

// --- Affichage du signal ---

plotshape(

longSignal,

title = "Signal LONG",

location = location.belowbar,

style = shape.triangleup,

color = color.lime,

size = size.small,

text = "LONG"

)

// --- Lignes TP / SL indicatives basées sur le dernier signal ---

var float tpLine = na

var float slLine = na

if longSignal

tpLine := close * (1 + tpPct)

slLine := close * (1 - slPct)

// Les lignes restent jusqu'au prochain signal

plot(tpLine, "TP indicatif", color = color.new(color.green, 50), style = plot.style_linebr)

plot(slLine, "SL indicatif", color = color.new(color.red, 50), style = plot.style_linebr)

// --- Affichage des moyennes ---

plot(emaFast, "EMA rapide", color = color.new(color.blue, 40))

plot(emaSlow, "EMA lente", color = color.new(color.orange, 40))

plot(ma200D, "MA200 jours (daily)", color = color.new(color.fuchsia, 0), linewidth = 2)

DR/IDR fractals break candle (ChadAnt)This indicator is an Opening Range Breakout (ORB) tool. It identifies the high and low price range established during a specific time window (e.g., the first hour of trading, 9:30–10:30 AM NY time). Once that time window closes, it watches for the price to "break out" of that range and projects profit targets based on the size of the initial range.

Key Features & How They Work

1. The Opening Range (The Box)

Time Window: The indicator waits for your specific start time (default 9:30 AM NY). It does not draw anything before this time.

The "Wicks": It tracks the absolute highest and lowest prices reached during this time (the Wicks). These act as your Breakout Triggers.

The "Body": It tracks the highest and lowest candle closes/opens during this time. This creates a shaded "zone" on your chart, representing the core area where most trading occurred.

Shading: To keep your chart clean, the background shading only appears during the forming time window.

2. Breakout Signals

Once the time window ends (e.g., 10:30 AM), the indicator "locks" the levels.

It then waits for a candle to move above the Wick High or below the Wick Low.

The Signal: When this happens, a label ("BREAK") appears on the chart.

Green Label: Bullish breakout (price went above the range).

Red Label: Bearish breakout (price went below the range).

Note: It only signals the first breakout of the day to avoid false alarms during choppy markets.

3. Extension Targets (Profit Levels)

When a breakout signal occurs, the indicator automatically draws target lines (extensions).

Calculation: These targets are based on the height of the "Body" zone (the shaded area).

Example: If your setting is 1.0, the indicator measures the height of the shaded body range and projects that exact distance above the breakout point. This is often used as a "Measured Move" target.

You can customize how many lines appear and how far apart they are (e.g., 0.5, 1.0, 1.5 times the range size).

4. Williams Fractals

During the opening range time, the indicator looks for specific price patterns called "Williams Fractals" (a 5-candle pattern that highlights potential turning points).

If a fractal peak or valley occurs inside your opening range, it marks it with a small triangle (▲ or ▼). Traders often use these as early signs of support or resistance forming inside the range.

5. Clean Visuals

Line Cutoff: You can set a "Stop Time" (e.g., 16:00 or 4:00 PM). The lines will stop drawing at that time so they don't clutter your chart overnight.

Gap Handling: The lines are programmed to break cleanly between days, so you don't see messy diagonal lines connecting yesterday's close to today's open.

Summary of Settings You Can Change

Session Time: When the range starts and ends.

Line Stop Time: When the lines should disappear for the day.

Visuals: Colors, line width, and style (solid, dotted, dashed).

Extensions: How many target lines to draw and the step size (e.g., 0.5x, 1.0x).

Fractals: Toggle the triangle icons on/off.

NQ Futures VWAP on QQQOverlay NQ1 vwap for QQQ

Track NQ future's vwap on your QQQ chart to scale with optional bands

Custom Timeframe SMAsThis indicator plots up to three Simple Moving Averages (SMAs), each calculated from a user-selected timeframe and displayed on the current chart. This allows you to visualize higher- or lower-timeframe SMAs without switching charts.

Features

Three fully customizable SMAs with alerts

Each SMA has its own:

Length

Timeframe

Color

Line thickness

On/Off toggle

Use Cases

View higher timeframe SMAs (e.g., 1-hour 50 SMA on a 5-minute chart)

Combine trend signals across multiple timeframes

Track dynamic support/resistance from different timeframes

Enhance scalping, day trading, or swing trading setups

ADR% / ATR / Dynamic LoD–HoD TableThis indicator displays a clean data table showing ADR%, ATR, and a dynamic LoD/HoD distance value based on daily trend conditions.

When price is above the 21-day or 50-day moving average, the indicator shows the distance from the Low of Day.

When price is below BOTH daily moving averages, it automatically switches to showing distance from the High of Day.

The table updates in real-time and gives a fast, volatility-based view of where price sits inside the day’s range.

Features

• ADR% (Average Daily Range Percentage)

• ATR (Average True Range)

• Automatic LoD → HoD switching based on daily trend

• Customizable colors and layout

• Clean, space-efficient table format

• Designed for intraday and volatility-focused traders

market condition by moving averagewhen the 10ma and 20ma of S&P is sloping up, the indicator will show a green background, which means breakout trade has a higher chance of working out.

ART MACRO PEEK 2025-Info v2 With this indicator you will be able to understand what the (vix, btc, triple aaa, dxy) looks like before entering market in one glance, it will act more like market thermometer.

RV − IV Spread Alert (SPY vs VIX)Realized vs Implied Volatility Spread (RV − IV) for the S&P 500 / SPY.

Plots the daily difference between 30-day realized volatility (SPY) and implied volatility (VIX) in basis points.

Key insight from the research: when the spread turns and stays above ≈ +50 bps, forward returns historically degrade and volatility of returns rises sharply — a useful early-warning regime flag.

Features:

- Clean daily plot of RV − IV in bps

- Horizontal lines at 0, −50 bps and +50 bps

- Red background when spread > +50 bps

- Built-in alert condition that fires once per bar close when spread closes above +50 bps

- Optional “all-clear” alert when it drops back below

Use on SPY or ES1! daily chart. Perfect for anyone wanting a simple notification when the market enters the “risk-on” volatility regime highlighted by Machina Quanta and the original Bali & Hovakimian (2007) paper.

CCI by DioAdded background color to entry points of the channel for easy observation to levels I am looking at.

Dynamic 15-Ticker Multi-Symbol Table 2025 EditionTitle:

Dynamic 15-Ticker Multi-Symbol Table 2025 Edition

Description:

This script provides a multi-ticker table for TradingView charts. It is fully open-source and free to use. The table displays up to 15 tickers, including SPY as the baseline symbol. The script updates in real-time on any timeframe.

Features:

SPY baseline: The first row always shows SPY for reference.

Custom tickers: Add up to 14 additional tickers via the input settings. Rows without tickers remain hidden.

Price and direction: Each ticker row displays the current price and an indicator of direction based on recent price movement.

RSI (14) indicator: Shows the current relative strength index value with a simple directional marker.

Volume formatting: Displays volume values in thousands, millions, or billions automatically. Volume change is indicated with directional markers.

Stable layout: The table uses alternating row colors for readability and maintains consistent row count without collapsing or disappearing rows.

Real-time updates: All displayed values refresh automatically on any chart timeframe.

How to use:

Add the script to your chart.

Enter your chosen tickers in the input settings. SPY will remain as the first ticker automatically.

Tickers not entered will remain hidden. When a ticker is removed, the row will be removed-dynamically.

Observe live prices, RSI values, and volume changes directly on your chart without switching symbols.

Additional notes:

The script is fully open-source; users are encouraged to modify or improve it.

No external links or references are required to understand its function.

This script does not repaint and does not require additional requests to update values.

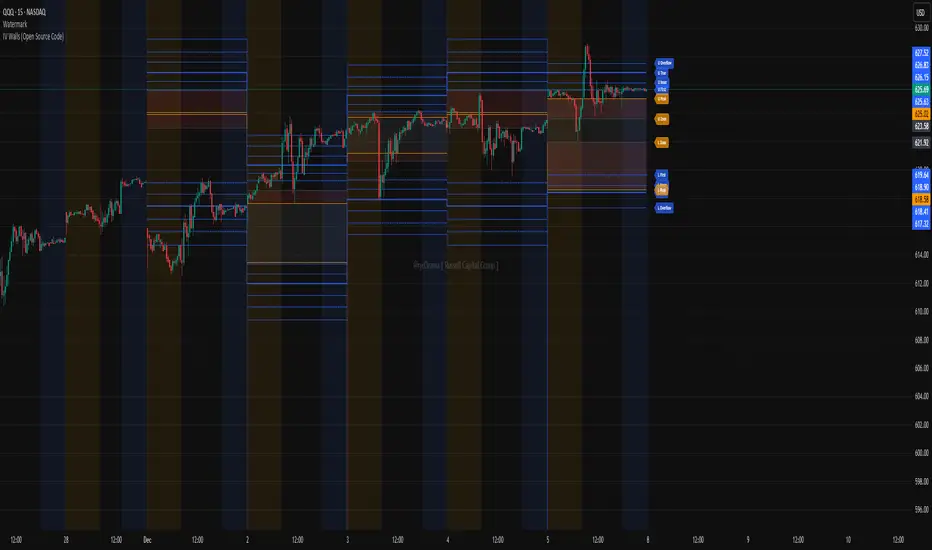

IV Walls (Open Source Code)Russell Capital Group

Code is completely open source. You are encouraged to make a copy as it is necessary for applying the indicator to multiple symbols. Each day's derived data must be plotted by code. Data is derived from the Fractal X software.

Message @ryd3rama on discord for more information or help.

Chaos Volatility Breakout (ATR + Breakout)-VMThis indicator is a volatility-based breakout trading tool inspired by principles from Chaos Theory, where small changes in momentum during high-energy market conditions can lead to large price movements.

Instead of predicting the market, it focuses on identifying “high-probability expansion zones”—moments when the market is under stress (high volatility) and price is breaking out of a recent range.