SuperZweig thrust (<= 30 dias)SuperZweig Thrust (≤ 30-day breadth trigger)

This study tracks the classic Zweig Breadth Thrust pattern, but restricts valid signals to a 30-bar (≈ 30-trading-day) window.

---

What it plots

| Plot | Meaning |

|------|---------|

| **Blue line** – `EMA10` | 10-bar exponential moving average of the _breadth ratio_:`advancing issues / (advancing + declining)` |

| **Red h-line 0.35** | Oversold threshold ( < 0.35 ) |

| **Green h-line 0.64** | Overbought threshold ( > 0.64 ) |

| **Red “×”** | The moment EMA10 crosses **down** through 0.35 |

| **Green “●”** | The moment EMA10 crosses **up** through 0.64 |

| **Green “BUY” label** | Complete Super-Zweig thrust: red × followed by green ● **within 30 daily bars** |

Signal logic

1. **Trigger phase** – when EMA10 drops below 0.35

*Script starts a 30-bar countdown.*

2. **Confirmation phase** – if, while the countdown is active, EMA10 rises above 0.64:

*A single “BUY” label is plotted beneath that bar.*

3. **Expiry** – if 30 bars elapse without the 0.64 cross, the cycle resets; no signal is produced.

4. After any valid “BUY” the cycle also resets, so a new signal requires a fresh cross < 0.35.

Inputs

* **EMA length** – default 10.

* **Advancing / Declining symbols** – default `ADVS` / `DECS` (NYSE issues); can be pointed to any Exchange-specific or custom breadth tickers.

Typical use

Apply on a **daily chart** of a broad index (e.g., S&P; 500).

A printed “BUY” indicates a historically rare surge in market breadth often associated with durable rallies. Combine with other risk-management and trend filters before trading.

Cari dalam skrip untuk "港股央企红利etf"

Stochastics + CM Williams VixFix (Simple Buy Signal)📈 Stochastics + CM Williams VixFix (Simple Buy Signal)

This indicator combines two powerful tools to detect potential bottoming opportunities:

✅ Stochastics: Looks for momentum reversals. A signal is triggered when both %K and %D are below the oversold threshold (default: 20), suggesting the asset is deeply oversold.

✅ CM Williams Vix Fix: A volatility-based fear detector. When it spikes above its dynamic threshold, it indicates potential panic selling — often preceding a market bounce.

💡 Buy Signal is generated when:

%K and %D are both below 20

VixFix shows a volatility spike (green condition)

Use this script to identify high-probability reversal setups, especially during market corrections or panic phases.

SPY 0DTE Scalper - Auto AlertsTimeframes:

Main chart: 1-minute (for precision entries)

Confirmations: 3-minute or 5-minute (to avoid fakeouts)

Indicators I Use:

VWAP – Orange line → Institutional fair value

EMA 9 – Green line → Short-term momentum

EMA 21 – Red line → Trend filter

Custom Pullback Signal Script – Marks buy/sell/pullback signals with labels (triangles)

Above VWAP = Bullish Bias

Below VWAP = Bearish Bias

Institutions treat this as the "fair price" — so I do too.

EMA 9 (Green):

If price hugs or bounces off EMA 9 = 🔥 strong continuation move.

I use this as my guide for momentum.

EMA 21 (Red):

Great for trend confirmation.

Above EMA 21 = Trend building to the upside.

Below EMA 21 = Weakness or possible reversal.

💸 Step 3: How I Read the Signals

✅ BUY Signal:

Price breaks above VWAP with volume 1.5x+ average

Candle must close strong (not a wickfest)

EMA 9 becomes my trailing stop for the move

🚨 SELL Signal:

Price breaks below VWAP with strong volume

Clean body close below → momentum shift to the downside

EMA 9 again = trailing resistance guide

🔵 Pullback Long (Blue Triangle Under Candle):

Bullish continuation entry

Price pulls back to EMA 9 or 21, but stays above VWAP

Low-risk re-entry after a breakout

🟣 Pullback Short (Purple Triangle Above Candle):

Bearish continuation entry

Price retraces into EMA 9, but stays below VWAP & EMA 21

Ideal for catching second legs after breakdowns

Easy MA SignalsEasy MA Signals

Overview

Easy MA Signals is a versatile Pine Script indicator designed to help traders visualize moving average (MA) trends, generate buy/sell signals based on crossovers or custom price levels, and enhance chart analysis with volume-based candlestick coloring. Built with flexibility in mind, it supports multiple MA types, crossover options, and customizable signal appearances, making it suitable for traders of all levels. Whether you're a day trader, swing trader, or long-term investor, this indicator provides actionable insights while keeping your charts clean and intuitive.

Configure the Settings

The indicator is divided into three input groups for ease of use:

General Settings:

Candlestick Color Scheme: Choose from 10 volume-based color schemes (e.g., Sapphire Pulse, Emerald Spark) to highlight high/low volume candles. Select “None” for TradingView’s default colors.

Moving Average Length: Set the MA period (default: 20). Adjust for faster (lower values) or slower (higher values) signals.

Moving Average Type: Choose between SMA, EMA, or WMA (default: EMA).

Show Buy/Sell Signals: Enable/disable signal plotting (default: enabled).

Moving Average Crossover: Select a crossover type (e.g., MA vs VWAP, MA vs SMA50) for signals or “None” to disable.

Volume Influence: Adjust how volume impacts candlestick colors (default: 1.2). Higher values make thresholds stricter.

Signal Appearance Settings:

Buy/Sell Signal Shape: Choose shapes like triangles, arrows, or labels for signals.

Buy/Sell Signal Position: Place signals above or below bars.

Buy/Sell Signal Color: Customize colors for better visibility (default: green for buy, red for sell).

Custom Price Alerts:

Custom Buy/Sell Alert Price: Set specific price levels for alerts (default: 0, disabled). Enter a non-zero value to enable.

Set Up Alerts

To receive notifications (e.g., sound, popup, email) when signals or custom price levels are hit:

Click the Alert button (alarm clock icon) in TradingView.

Select Easy MA Signals as the condition and choose one of the four alert types:

MA Crossover Buy Alert: Triggers on MA crossover buy signals.

MA Crossover Sell Alert: Triggers on MA crossover sell signals.

Custom Buy Alert: Triggers when price crosses above the custom buy price.

Custom Sell Alert: Triggers when price crosses below the custom sell price.

Enable Play Sound and select a sound (e.g., “Bell”).

Set the frequency (e.g., Once Per Bar Close for confirmed signals) and create the alert.

Analyze the Chart

Moving Average Line: Displays the selected MA with color changes (green for bullish, red for bearish, gray for neutral) based on price position relative to the MA.

Buy/Sell Signals: Appear as shapes or labels when crossovers or custom price levels are hit.

Candlestick Colors: If a color scheme is selected, candles change color based on volume strength (high, low, or neutral), aiding in trend confirmation.

Why Use Easy MA Signals?

Easy MA Signals is designed to simplify technical analysis while offering advanced customization. It’s ideal for traders who want:

A clear visualization of MA trends and crossovers.

Flexible signal generation based on MA crossovers or custom price levels.

Volume-enhanced candlestick coloring to identify market strength.

Easy-to-use settings with tooltips for beginners and pros alike.

This script is particularly valuable because it combines multiple features into one indicator, reducing chart clutter and providing actionable insights without overwhelming the user.

Benefits of Easy MA Signals

Highly Customizable: Supports SMA, EMA, and WMA with adjustable lengths.

Offers multiple crossover options (VWAP, SMA10, SMA20, etc.) for tailored strategies.

Custom price alerts allow precise targeting of key levels.

Volume-Based Candlestick Coloring: 10 unique color schemes highlight volume strength, helping traders confirm trends.

Adjustable volume influence ensures adaptability to different markets.

Flexible Signal Visualization: Choose from various signal shapes (triangles, arrows, labels) and positions (above/below bars).

Customizable colors improve visibility on any chart background.

Alert Integration: Built-in alert conditions for crossovers and custom prices support sound, email, and app notifications.

Easy setup for real-time trading decisions.

User-Friendly Design: Organized input groups with clear tooltips make configuration intuitive.

Suitable for beginners and advanced traders alike.

Example Use Cases

Swing Trading with MA Crossovers:

Scenario: A trader wants to trade Bitcoin (BTC/USD) on a 4-hour chart using an EMA crossover strategy.

Setup:

Set Moving Average Type to EMA, Length to 20.

Set Moving Average Crossover to “MA vs SMA50”.

Enable Show Buy/Sell Signals and choose “arrowup” for buy, “arrowdown” for sell.

Select “Emerald Spark” for candlestick colors to highlight volume surges.

Usage: Buy when the EMA20 crosses above the SMA50 (green arrow appears) and volume is high (dark green candles). Sell when the EMA20 crosses below the SMA50 (red arrow). Set alerts for real-time notifications.

Scalping with Custom Price Alerts:

Scenario: A day trader monitors Tesla (TSLA) on a 5-minute chart and wants alerts at specific support/resistance levels.

Setup:

Set Custom Buy Alert Price to 150.00 (support) and Custom Sell Alert Price to 160.00 (resistance).

Use “labelup” for buy signals and “labeldown” for sell signals.

Keep Moving Average Crossover as “None” to focus on price alerts.

Usage: Receive a sound alert and label when TSLA crosses 150.00 (buy) or 160.00 (sell). Use volume-colored candles to confirm momentum before entering trades.

When NOT to Use Easy MA Signals

High-Frequency Trading: Reason: The indicator relies on moving averages and volume, which may lag in ultra-fast markets (e.g., sub-second trades). High-frequency traders may need specialized tools with real-time tick data.

Alternative: Use order book or market depth indicators for faster execution.

Low-Volatility or Sideways Markets:

Reason: MA crossovers and custom price alerts can generate false signals in choppy, range-bound markets, leading to whipsaws.

Alternative: Use oscillators like RSI or Bollinger Bands to trade within ranges.

This indicator is tailored more towards less experienced traders. And as always, paper trade until you are comfortable with how this works if you're unfamiliar with trading! We hope you enjoy this and have great success. Thanks for your interested in Easy MA Signals!

Polygot Moving AveragesDescription

This is essentially a source merger of Bollinger Bands by Trading View and Simple Moving Averages by stoxxinbox. My additions and subtractions are minimal. There is the BB MA, which I default at 5d, and the other 4 averages are the standard 21, 50, 100, 200, day moving averages. I default the averaging method to WMA (Weighted Moving Average). The method of averaging can be changed as also can the lengths of the inputs to match user preferences. This is what I wanted for an indicator and didn't find.

Usage

The same as you would use any other BB or MA indicator. The benefit of this one is that it has 4 MAs, one MA with the Bollinger Bands attached, and the colours adjusted to be easy on the eyes when using high contrast themes, to be discernible yet sit quietly in the background with lines and candle sticks everywhere shouting for attention. I use it as a base first indicator which I can hide easily (imagine hiding five MA indicators individually constantly) when the more serious indicators come into play.

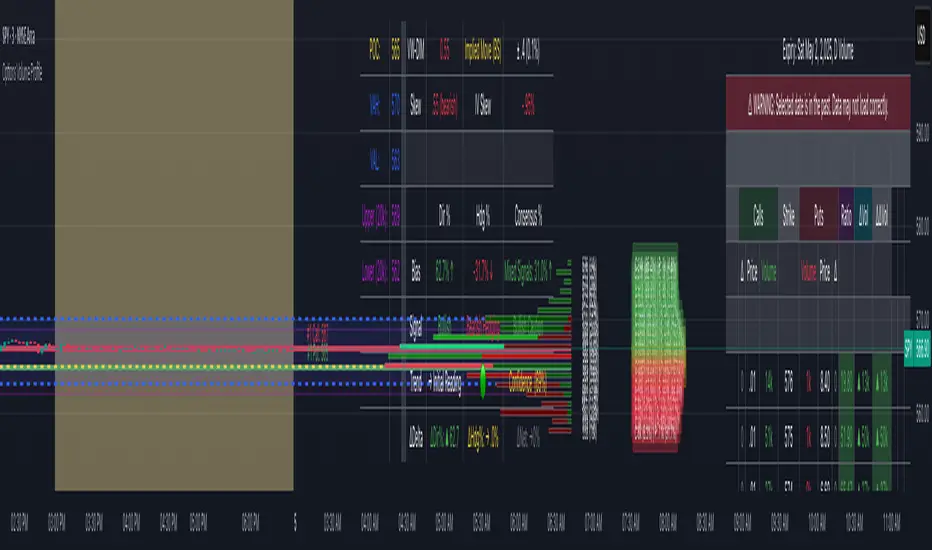

Options Volume ProfileOptions Volume Profile

Introduction

Unlock institutional-level options analysis directly on your charts with Options Volume Profile - a powerful tool designed to visualize and analyze options market activity with precision and clarity. This indicator bridges the gap between technical price action and options flow, giving you a comprehensive view of market sentiment through the lens of options activity.

What Is Options Volume Profile?

Options Volume Profile is an advanced indicator that analyzes call and put option volumes across multiple strikes for any symbol and expiration date available on TradingView. It provides a real-time visual representation of where money is flowing in the options market, helping identify potential support/resistance levels, market sentiment, and possible price targets.

Key Features

Comprehensive Options Data Visualization

Dynamic strike-by-strike volume profile displayed directly on your chart

Real-time tracking of call and put volumes with custom visual styling

Clear display of important value areas including POC (Point of Control)

Value Area High/Low visualization with customizable line styles and colors

BK Daily Range Identification

Secondary lines marking significant volume thresholds

Visual identification of key strike prices with substantial options activity

Value Area Cloud Visualization

Configurable cloud overlays for value areas

Enhanced visual identification of high-volume price zones

Detailed Summary Table

Complete breakdown of call and put volumes per strike

Percentage analysis of call vs put activity for sentiment analysis

Color-coded volume data for instant pattern recognition

Price data for both calls and puts at each strike

Custom Strike Selection

Configure strikes above and below ATM (At The Money)

Flexible strike spacing and rounding options

Custom base symbol support for various options markets

Use Cases

1. Identifying Key Support & Resistance

Visualize where major options activity is concentrated to spot potential support and resistance zones. The POC and Value Area lines often act as magnets for price.

2. Analyzing Market Sentiment

Compare call versus put volume distribution to gauge directional bias. Heavy call volume suggests bullish sentiment, while heavy put volume indicates bearish positioning.

3. Planning Around Institutional Activity

Volume profile analysis reveals where professional traders are positioning themselves, allowing you to align with or trade against smart money.

4. Setting Precise Targets

Use the POC and Value Area High/Low lines as potential profit targets when planning your trades.

5. Spotting Unusual Options Activity

The color-coded volume table instantly highlights anomalies in options flow that may signal upcoming price movements.

Customization Options

The indicator offers extensive customization capabilities:

Symbol & Data Settings : Configure base symbol and data aggregation

Strike Selection : Define number of strikes above/below ATM

Expiration Date Settings : Set specific expiry dates for analysis

Strike Configuration : Customize strike spacing and rounding

Profile Visualization : Adjust offset, width, opacity, and height

Labels & Line Styles : Fully configurable text and visual elements

Value Area Settings : Customize POC and Value Area visualization

Secondary Line Settings : Configure the BK Daily Range appearance

Cloud Visualization : Add colored overlays for enhanced visibility

How to Use

Apply the indicator to your chart

Configure the expiration date to match your trading timeframe

Adjust strike selection and spacing to match your instrument

Use the volume profile and summary table to identify key levels

Trade with confidence knowing where the real money is positioned

Perfect for options traders, futures traders, and anyone who wants to incorporate institutional-level options analysis into their trading strategy.

Take your trading to the next level with Options Volume Profile - where price meets institutional positioning.

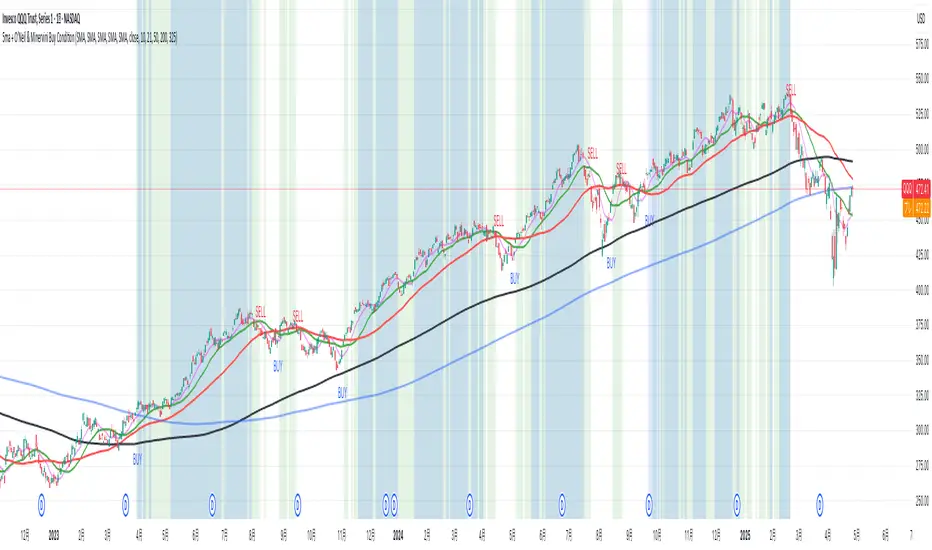

5ma + O’Neil & Minervini Buy ConditionIndicator Overview

5ma + O’Neil & Minervini Buy Condition is an original TradingView indicator that extends beyond a simple collection of standard moving averages by offering:

- Five Fully Independent Lines : Each of MA1–MA5 can be configured as SMA, EMA, WMA, or VWMA with its own period and data source. This level of customization unlocks unique combinations no existing script provides.

- Synergy of Multiple Timeframes : Default settings (10, 21, 50, 200, 325) reflect ultra‑short, short, medium, long, and volume‑weighted long‑term perspectives. The layered structure functions as a multi‑filter, sharpening entry signals and trend confirmation beyond any single MA.

- Integrated Buy Conditions : Built‑in O’Neil and Minervini buy filters use fixed SMA‑based rules (50 & 200 SMA rising within 15% of 52‑week high; 10 > 21 > 50 SMA rising within high/low thresholds), plus a combined condition highlighting when both methods align.

- Clean Visualization & Style Controls : Background coloring for each buy condition appears only in the Style tab under clearly named parameters (O’Neil Buy Condition, Minervini Buy Condition, Both Conditions). MA lines support transparent default colors and customizable line width for optimal readability without clutter.

Calculation & Logic

SMA: (P₁ + P₂ + … + Pₙ) ÷ N

EMA: α = 2 ÷ (N + 1)

EMA_today = (Price_today – EMA_yesterday) × α + EMA_yesterday

WMA: (P₁×N + P₂×(N–1) + … + Pₙ×1) ÷

VWMA: Σ(Pᵢ×Vᵢ) ÷ Σ(Vᵢ) for i = 1…N

```

Buy Condition Logic

- O’Neil: Price > 50 SMA & 200 SMA (both rising) **and** within 15% of the 52‑week high.

- Minervini : 10 SMA > 21 SMA > 50 SMA (both short‑term SMAs rising) **and** within 25% of the 52‑week high **and** at least 25% above the 52‑week low.

- Combined : Both O’Neil and Minervini conditions true.

Usage Examples

1. Short‑Mid Cross : Observe MA1/MA2 crossover while MA3/MA4 confirm trend strength.

2. Volume‑Weighted Long‑Term : Use VWMA as MA5 to filter institutional‑strength pullbacks.

3. Multi‑Filter Entry : Look for purple background (Both Conditions) on daily chart as high‑confidence entry.

Why It’s Unique

- Not a Mash‑Up : Though built on standard MA formulas, the customizable layering and built‑in buy filters create a novel multi‑dimensional analysis tool.

- Trader‑Friendly : Detailed comments in the code explain parameter choices, calculation methods, and practical entry scenarios so that even Pine novices can understand the underlying mechanics.

- Publication‑Ready : Description and code demonstrate originality, add clear value, and comply with house‑rule requirements by explaining why and how components interact, not just listing features.

- Combined Custom MA & Buy Conditions : By integrating customizable moving averages with built-in buy filters, users can easily recognize O’Neil and Minervini recommended setups.

Midnight (Daily) OpenMidnight (Daily) Open v1.0

Overview

Plots a real‑time horizontal line at the U.S. session “midnight” open (i.e. the daily candle’s open price) on any intraday chart. Optionally displays a label with the exact price, making it easy to see how price reacts to the session open.

Key Benefits

Immediate Context: See at a glance where today’s session began, helping identify support/resistance.

Consistent Reference: Works on any symbol or intraday timeframe.

Customizable Styling: Tweak colors, line thickness, and label appearance to match your chart theme.

Features

Retrieves the daily open via request.security() (Pine v6).

Draws or updates a single horizontal line that extends into the future.

Optional price label on the last bar, with user‑defined text and background colors.

Zero repainting—always shows the true daily open.

Moving Average Trend ToolsI. How M.A.T.T. Adds Value to the TradingView Community:

The "Moving Average Trend Tools" (M.A.T.T.) is a versatile Pine Script v6 indicator that empowers traders with clear trend analysis, reliable trade signals, and real-time insights. Its intuitive design and robust features make it a valuable addition to the TradingView Community Scripts by catering to traders of all levels. Here’s why it stands out:

Clear Trend Visualization: M.A.T.T. plots a moving average (MA) with dynamic coloring—green for rising, red for falling, and gray for flat—based on a user-defined lookback period. This simplifies trend interpretation, helping traders quickly assess market momentum.

Reliable Trade Signals : The script identifies price crossovers above or below the MA, plotting green circles for bullish crosses and red for bearish, confirmed on closed bars to prevent repainting. These signals guide entry and exit points for trend-following or reversal strategies.

Real-Time Extension Detection : M.A.T.T. calculates percentage price deviations from the MA, displaying real-time labels when thresholds (e.g., 6%) are exceeded. This highlights overextended moves, ideal for spotting reversals or pullbacks, with alerts to keep traders informed.

Extensive Customization : Traders can tailor the MA type (SMA, EMA, WMA, HMA), length, colors, line width, and label sizes. This flexibility supports diverse strategies across markets like stocks, forex, and crypto, from scalping to swing trading.

Automated Alerts : Alert conditions for crossovers and extensions integrate seamlessly with TradingView’s system, enabling traders to stay updated without constant chart monitoring.

M.A.T.T. combines trend analysis, signal generation, and overextension detection into a single, user-friendly tool. Its accessibility, reliability, and educational value for Pine Script learners make it a compelling contribution to the community.

II. What M.A.T.T. Does, How It Works, and Its Originality:

What It Does :

M.A.T.T. enhances trend analysis and trade decision-making through three core features:

Dynamic MA Visualization: Plots a customizable MA (SMA, EMA, WMA, or HMA) with trend-based coloring to reflect rising, falling, or flat market conditions.

Price Crossover Signals : Marks bullish (green circles) and bearish (red circles) crossovers, confirmed on closed bars, with alerts for trade opportunities.

Price Extension Labels : Displays real-time percentage deviations of price from the MA, with alerts when user-defined thresholds are breached, signaling potential reversals.

How It Works :

M.A.T.T. leverages Pine Script v6 for precise calculations and user-friendly outputs:

Inputs: Users select MA type, length, lookback period, colors, and thresholds for extensions, plus label styles and sizes for customization.

MA Calculation : A switch function computes the chosen MA (e.g., ta.ema(close, 21) for EMA). Trend direction is determined using ta.rising or ta.falling over the lookback period, coloring the MA accordingly.

Crossover Logic : Bullish crossovers (close > ma and close < ma ) and bearish crossovers (close < ma and close > ma ) are plotted as circles on confirmed bars (barstate.isconfirmed) to ensure reliability. Alerts trigger only on the first bar of a crossover.

Extension Logic : Percentage deviations are calculated as ((price - ma) / ma) * 100, using the high for above-MA extensions and low for below. Labels appear in real-time when thresholds are exceeded, with alerts on transitions to avoid noise.

Why It’s Original

M.A.T.T. distinguishes itself through a unique blend of features and thoughtful design:

All-in-One Design : It integrates dynamic MA coloring, non-repainting crossover signals, and real-time extension detection, addressing trend identification, trade signals, and overextension warnings in one tool—unlike most MA indicators that focus on a single aspect.

Real-Time Extension Labels : Displaying percentage deviations with customizable thresholds is a rare feature, ideal for volatile markets and not commonly found in standard scripts.

Non-Repainting Signals : Confirmed crossover signals enhance reliability for live trading, setting M.A.T.T. apart from less rigorous indicators.

Optimized Alert Condtions : Alerts trigger only on transitions (e.g., first bar of a crossover or extension), reducing noise and improving usability.

Visual and Functional Flexibility : Support for four MA types, extensive customization, and a clean interface (dynamic colors, tiny circles, clear labels) make it adaptable and user-friendly.

While MA plotting or crossovers exist elsewhere, M.A.T.T.’s seamless integration, real-time extension detection, alert conditions, and focus on reliability and customization create a distinctive, practical tool. Its balance of simplicity and sophistication makes it a unique asset for the TradingView community.

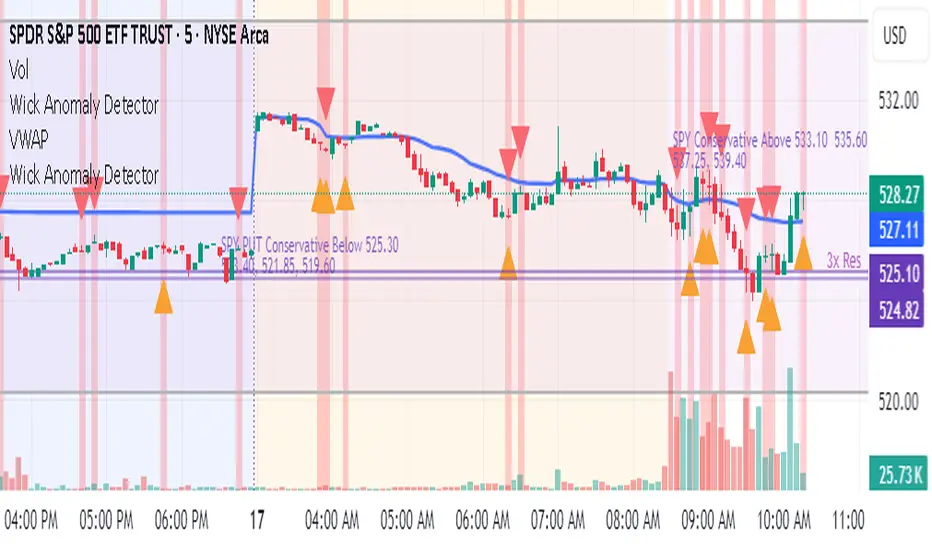

Wick Anomaly DetectorWick Anomaly Detector

This script helps identify candles with unusually large wicks compared to their body size — a common sign of price anomalies, false prints, or low-liquidity moves.

🔍 What it does:

Flags candles with upper or lower wicks that exceed a user-defined ratio (default: 3x the body size)

Helps traders spot suspicious spikes or “bad ticks,” especially in pre-market or illiquid stocks

📈 Use it to:

Avoid fake breakouts

Confirm real price action

Clean up your technical analysis

Customize the wick-to-body threshold as needed. Add volume filters or time filters for more precision.

Created for educational purposes — use with proper risk management!

TASC 2025.05 Trading The Channel█ OVERVIEW

This script implements channel-based trading strategies based on the concepts explained by Perry J. Kaufman in the article "A Test Of Three Approaches: Trading The Channel" from the May 2025 edition of TASC's Traders' Tips . The script explores three distinct trading methods for equities and futures using information from a linear regression channel. Each rule set corresponds to different market behaviors, offering flexibility for trend-following, breakout, and mean-reversion trading styles.

█ CONCEPTS

Linear regression

Linear regression is a model that estimates the relationship between a dependent variable and one or more independent variables by fitting a straight line to the observed data. In the context of financial time series, traders often use linear regression to estimate trends in price movements over time.

The slope of the linear regression line indicates the strength and direction of the price trend. For example, a larger positive slope indicates a stronger upward trend, and a larger negative slope indicates the opposite. Traders can look for shifts in the direction of a linear regression slope to identify potential trend trading signals, and they can analyze the magnitude of the slope to support trading decisions.

One caveat to linear regression is that most financial time series data does not follow a straight line, meaning a regression line cannot perfectly describe the relationships between values. Prices typically fluctuate around a regression line to some degree. As such, analysts often project ranges above and below regression lines, creating channels to model the expected extent of the data's variability. This strategy constructs a channel based on the method used in Kaufman's article. It measures the maximum distances from points on the linear regression line to historical price values, then adds those distances and the current slope to the regression points.

Depending on the trading style, traders might look for prices to move outside an established channel for breakout signals, or they might look for price action to reach extremes within the channel for potential mean reversion opportunities.

█ STRATEGY CALCULATIONS

Primary trade rules

This strategy implements three distinct sets of rules for trend, breakout, and mean-reversion trades based on the methods Kaufman describes in his article:

Trade the trend (Rule 1) : Open new positions when the sign of the slope changes, indicating a potential trend reversal. Close short trades and enter a long trade when the slope changes from negative to positive, and do the opposite when the slope changes from positive to negative.

Trade channel breakouts (Rule 2) : Open new positions when prices cross outside the linear regression channel for the current sample. Close short trades and enter a long trade when the price moves above the channel, and do the opposite when the price moves below the channel.

Trade within the channel (Rule 3) : Open new positions based on price values within the channel's range. Close short trades and enter a long trade when the price is near the channel's low, within a specified percentage of the channel's range, and do the opposite when the price is near the channel's high. With this rule, users can also filter the trades based on the channel's slope. When the filter is active, long positions are allowed only when the slope is positive, and short positions are allowed only when it is negative.

Position sizing

Kaufman's strategy uses specific trade sizes for equities and futures markets:

For an equities symbol, the number of shares traded is $10,000 divided by the current price.

For a futures symbol, the number of contracts traded is based on a volatility-adjusted formula that divides $25,000 by the product of the 20-bar average true range and the instrument's point value.

By default, this script automatically uses these sizes for its trade simulation on equities and futures symbols and does not simulate trading on other symbols. However, users can control position sizes from the "Settings/Properties" tab and enable trade simulation on other symbol types by selecting the "Manual" option in the script's "Position sizing" input.

Stop-loss

This strategy includes the option to place an accompanying stop-loss order for each trade, which users can enable from the "SL %" input in the "Settings/Inputs" tab. When enabled, the strategy places a stop-loss order at a specified percentage distance from the closing price where the entry order occurs, allowing users to compare how the strategy performs with added loss protection.

█ USAGE

This strategy adapts its display logic for the three trading approaches based on the rule selected in the "Trade rule" input:

For all rules, the script plots the linear regression slope in a separate pane. The plot is color-coded to indicate whether the current slope is positive or negative.

When the selected rule is "Trade the trend", the script plots triangles in the separate pane to indicate when the slope's direction changes from positive to negative or vice versa. Additionally, it plots a color-coded SMA on the main chart pane, allowing visual comparison of the slope to directional changes in a moving average.

When the rule is "Trade channel breakouts" or "Trade within the channel", the script draws the current period's linear regression channel on the main chart pane, and it plots bands representing the history of the channel values from the specified start time onward.

When the rule is "Trade within the channel", the script plots overbought and oversold zones between the bands based on a user-specified percentage of the channel range to indicate the value ranges where new trades are allowed.

Users can customize the strategy's calculations with the following additional inputs in the "Settings/Inputs" tab:

Start date : Sets the date and time when the strategy begins simulating trades. The script marks the specified point on the chart with a gray vertical line. The plots for rules 2 and 3 display the bands and trading zones from this point onward.

Period : Specifies the number of bars in the linear regression channel calculation. The default is 40.

Linreg source : Specifies the source series from which to calculate the linear regression values. The default is "close".

Range source : Specifies whether the script uses the distances from the linear regression line to closing prices or high and low prices to determine the channel's upper and lower ranges for rules 2 and 3. The default is "close".

Zone % : The percentage of the channel's overall range to use for trading zones with rule 3. The default is 20, meaning the width of the upper and lower zones is 20% of the range.

SL% : If the checkbox is selected, the strategy adds a stop-loss to each trade at the specified percentage distance away from the closing price where the entry order occurs. The checkbox is deselected by default, and the default percentage value is 5.

Position sizing : Determines whether the strategy uses Kaufman's predefined trade sizes ("Auto") or allows user-defined sizes from the "Settings/Properties" tab ("Manual"). The default is "Auto".

Long trades only : If selected, the strategy does not allow short positions. It is deselected by default.

Trend filter : If selected, the strategy filters positions for rule 3 based on the linear regression slope, allowing long positions only when the slope is positive and short positions only when the slope is negative. It is deselected by default.

NOTE: Because of this strategy's trading rules, the simulated results for a specific symbol or channel configuration might have significantly fewer than 100 trades. For meaningful results, we recommend adjusting the start date and other parameters to achieve a reasonable number of closed trades for analysis.

Additionally, this strategy does not specify commission and slippage amounts by default, because these values can vary across market types. Therefore, we recommend setting realistic values for these properties in the "Cost simulation" section of the "Settings/Properties" tab.

Fractal Wave MarkerFractal Wave Marker is an indicator that processes relative extremes of fluctuating prices within 2 periodical aspects. The special labeling system detects and visually marks multi-scale turning points, letting you visualize fractal echoes within unfolding cycles dynamically.

What This Indicator Does

Identifies major and minor swing highs/lows based on adjustable period.

Uses Phi in power exponent to compute a higher-degree swing filter.

Labels of higher degree appear only after confirmed base swings — no phantom levels, no hindsight bias. What you see is what the market has validated.

Swing points unfold in a structured, alternating rhythm . No two consecutive pivots share the same hierarchical degree!

Inspired by the Fractal Market Hypothesis, this script visualizes the principle that market behavior repeats across time scales, revealing structured narrative of "random walk". This inherent sequencing ensures fractal consistency across timeframes. "Fractal echoes" demonstrate how smaller price swings can proportionally mirror larger ones in both structure and timing, allowing traders to anticipate movements by recursive patterns. Cycle Transitions highlight critical inflection points where minor pivots flip polarity such as a series of lower highs progress into higher highs—signaling the birth of a new macro trend. A dense dense clusters of swing points can indicate Liquidity Zones, acting as footprints of institutional accumulation or distribution where price action validates supply and demand imbalances.

Visualization of nested cycles within macro trend anchors - a main feature specifically designed for the chartists who prioritize working with complex wave oscillations their analysis.

FeraTrading Relative Volume IndicatorThis FeraTrading Relative Volume Indicator measures relative volume pressure by comparing buying and selling activity, smoothed using a configurable average. It helps traders identify volume-driven momentum shifts, offering dynamic buy and sell signals based on weighted pressure values.

Key Features:

📈 Relative Volume (RV) Line: Measures net buying/selling pressure using volume-weighted price action.

🟢 Buy Signals: Triggered when RV crosses above a smoothed moving average (SMA 1).

🔴 Sell Signals (optional): Triggered when RV crosses below a separate SMA (SMA 2).

🔍 Customizable Inputs: Adjust smoothing length, weight, and signal sensitivity.

🕯️ Weighted Candles (optional): Visualizes custom OHLC based on volume-weighted volatility.

📊 Two SMAs: Use separate or combined moving averages to analyze trends in pressure.

🎨 Flexible Styling: Customize line and signal colors to match your chart setup.

Use Cases:

Spotting accumulation/distribution phases

Timing entries during volume surges

Confirming breakout momentum with underlying volume pressure

This indicator was developed by FeraTrading to visualize relative volume pressure.

Buffett Indicator (Wilshire 5000 / GDP)The Buffett Indicator (Wilshire 5000 / GDP) is a macroeconomic metric used to assess whether the U.S. stock market is overvalued or undervalued. It is calculated by dividing the total market capitalization (represented by the Wilshire 5000 Index) by the U.S. Gross Domestic Product (GDP). A value above 1 (or 100%) may indicate an overvalued market, while a value below 1 suggests potential undervaluation. This indicator is best suited for long-term investment analysis.

RSI in pane and 3 EMAs on chartCustom RSI in Pane + 3 EMAs on Chart — with Optional RSI Divergence Detection

Combines RSI in a separate pane with 3 EMAs on the chart and optional RSI-based divergence detection. Useful for analyzing both momentum and trend structure.

Features

RSI Pane

Custom RSI calculation (not built-in ta.rsi) with adjustable source and length

Overlay optional moving average (SMA, EMA, SMMA/RMA, WMA, VWMA, or Bollinger Bands) Overbought/oversold gradient fill for visual clarity (70 / 30 zones)

Midline (50) for neutral RSI territory

RSI Divergence Detection

Optional: toggle on/off with one input

Regular Bullish Divergence : Price makes a lower low, RSI makes a higher low

Regular Bearish Divergence : Price makes a higher high, RSI makes a lower high

Customizable lookback for pivot detection

Visual markers and labels plotted on RSI

Built-in alert conditions for both divergence types

3 EMA Trend Indicators on Price Chart

Three customizable EMAs (default: 20, 50, 200)

Color-coded and clearly plotted on main chart

Use to determine short/mid/long-term trend bias

No repainting or smoothing artifacts

Why use this script?

Gives a full view of trend + momentum without cluttering the main price chart, and it helps confirm entries and exits by observing RSI behavior alongside EMAs. The optional divergence detection can act as a signal for potential exhaustion or reversal (not entry signals on their own). It is a Good fit for traders who use RSI zones, divergences, and EMA structure in their decision-making, both for intra-day and swing trades (where it performs best).

How to use

Add this script to your chart. EMAs will appear on the main price chart; RSI and divergence will appear in a separate pane.

Adjust RSI and MA settings to fit your trading style (e.g., fast RSI for scalping, slower for swing)

Enable "Show Divergence" if you want visual alerts and markers

Use alerts to get notified when a divergence occurs without watching the chart

Always check the divergences on different time frames to validate the setup, and do not consider them valid on small time frames (<15 minutes).

Built for traders who want both momentum and trend context in a single tool — without clutter, repainting, or noise. I created this script to streamline my own analysis and avoid switching between multiple indicators. It's not meant to be a "signal generator" but a visual assistant for making better decisions. If you find it useful or have feedback, feel free to reach out.

Scalper's Fractal Cloud with RSI + VWAP + MACD (Fixed)Scalper’s Fractal Confluence Dashboard

1. Purpose of the Indicator

This TradingView indicator script provides a high-confluence setup for scalping and day trading. It blends momentum indicators (RSI, MACD), trend bias tools (EMA Cloud, VWAP), and structure (fractal swings, gap zones) to help confirm precise entries and exits.

2. Components of the Indicator

- EMA Cloud (50 & 200 EMA): Trend bias – green means bullish, red means bearish. Avoid longs under red cloud.

- VWAP: Institutional volume anchor. Ideal entries are pullbacks to VWAP in direction of trend.

- Gap Zones: Shows open-air zones (white space) where price can move fast. Used to anticipate momentum moves.

- ZigZag Swings: Marks structural pivots (highs/lows) – useful for stop placement and range anticipation.

- MACD Histogram: Shows bullish or bearish momentum via background color.

- RSI: Overbought (>70) or oversold (<30) warnings. Good for exits or countertrend reversion plays.

- EMA Spread Label: Quick view of momentum strength. Wide spread = strong trend.

3. Scalping Entry Checklist

Before entering a trade, confirm these conditions:

• • Bias: EMA cloud color supports trade direction

• • Price is above/below VWAP (confirming institutional flow)

• • MACD histogram matches direction (green for long, red for short)

• • RSI not at extreme (unless you’re fading trend)

• • If entering gap zone, expect fast move

• • Recent swing high/low nearby for target or stop

4. Risk & Sizing Guidelines

Risk 1–2% of account per trade. Place stop below recent swing low (for longs) or high (for shorts). Use fractional sizing near VWAP or white space zones for scalping reversals.

5. Daily Trade Journal Template

- Date:

- Ticker:

- Setup Type (VWAP pullback, Gap Break, EMA reversion):

- Entry Time:

- Bias (Green/Red Cloud):

- RSI Level / MACD Reading:

- Stop Loss:

- Target:

- Result (P/L):

- What I Did Well:

- What Needs Work:

Webby's Market OrderThis is visual representation of Webby's Market Order.

When three consecutive lows are above 21 EMA, Uptrend expectation is natural.

When three highs are below 21 EMA, Downtrend expectation is natural.

Alert Conditions can be set when uptrend and down trend are expected.

Use this indicator with IXIC or SPY or major indices.

This is set at three lows/Highs above 21 EMA as looked by Mike Webster.

FT-RSISummary of the Custom RSI Indicator Script (For Futu Niuniu Platform):

This Pine Script code implements a triple-period RSI indicator with horizontal reference lines (70, 50, 30) for technical analysis on the Futu Niuniu trading platform.

Key Features:

Multi-period RSI Calculation:

Computes three RSI values using 9, 14, and 22-period lengths to capture short-term, standard, and smoothed momentum signals.

Utilizes the Relative Moving Average (RMA) method for RSI calculation (ta.rma function).

Horizontal Reference Bands:

Upper Band (70): Red dotted line (semi-transparent) to identify overbought conditions.

Middle Band (50): Green dotted line as the neutral equilibrium level.

Lower Band (30): Blue dotted line (semi-transparent) to highlight oversold zones.

Visual Customization:

Distinct colors for each RSI line:

RSI (9): Orange (#F79A00)

RSI (14): Green (#49B50D)

RSI (22): Blue (#5188FF)

All lines have a thickness of 2 pixels for clear visibility.

Platform Compatibility:

This script is designed for Futu Niuniu’s charting system, leveraging Pine Script syntax adaptations supported by the platform. The horizontal bands and multi-period RSI logic help traders analyze trend strength and potential reversal points efficiently.

Note: Ensure Futu Niuniu’s scripting environment supports ta.rma and hline functions for proper execution.

StonkGame Major Market Open/ClosePlots vertical lines for Tokyo, London, and New York session opens and closes — auto-adjusted to your chart's timezone.

Open lines = lighter, dashed style.

Close lines = solid, full-color style.

Helps identify key liquidity windows, session-driven volatility, and clean market structure — without chart clutter.

Fully customizable colors and line styles for a professional, minimal look.

Leavitt Convolution ProbabilityTechnical Analysis of Markets with Leavitt Market Projections and Associated Convolution Probability

The aim of this study is to present an innovative approach to market analysis based on the research "Leavitt Market Projections." This technical tool combines one indicator and a probability function to enhance the accuracy and speed of market forecasts.

Key Features

Advanced Indicators : the script includes the Convolution line and a probability oscillator, designed to anticipate market changes. These indicators provide timely signals and offer a clear view of price dynamics.

Convolution Probability Function : The Convolution Probability (CP) is a key element of the script. A significant increase in this probability often precedes a market decline, while a decrease in probability can signal a bullish move. The Convolution Probability Function:

At each bar, i, the linear regression routine finds the two parameters for the straight line: y=mix+bi.

Standard deviations can be calculated from the sequence of slopes, {mi}, and intercepts, {bi}.

Each standard deviation has a corresponding probability.

Their adjusted product is the Convolution Probability, CP. The construction of the Convolution Probability is straightforward. The adjusted product is the probability of one times 1− the probability of the other.

Customizable Settings : Users can define oversold and overbought levels, as well as set an offset for the linear regression calculation. These options allow for tailoring the script to individual trading strategies and market conditions.

Statistical Analysis : Each analyzed bar generates regression parameters that allow for the calculation of standard deviations and associated probabilities, providing an in-depth view of market dynamics.

The results from applying this technical tool show increased accuracy and speed in market forecasts. The combination of Convolution indicator and the probability function enables the identification of turning points and the anticipation of market changes.

Additional information:

Leavitt, in his study, considers the SPY chart.

When the Convolution Probability (CP) is high, it indicates that the probability P1 (related to the slope) is high, and conversely, when CP is low, P1 is low and P2 is high.

For the calculation of probability, an approximate formula of the Cumulative Distribution Function (CDF) has been used, which is given by: CDF(x)=21(1+erf(σ2x−μ)) where μ is the mean and σ is the standard deviation.

For the calculation of probability, the formula used in this script is: 0.5 * (1 + (math.sign(zSlope) * math.sqrt(1 - math.exp(-0.5 * zSlope * zSlope))))

Conclusions

This study presents the approach to market analysis based on the research "Leavitt Market Projections." The script combines Convolution indicator and a Probability function to provide more precise trading signals. The results demonstrate greater accuracy and speed in market forecasts, making this technical tool a valuable asset for market participants.

OverUnder Yield Spread🗺️ OverUnder is a structural regime visualizer , engineered to diagnose the shape, tone, and trajectory of the yield curve. Rather than signaling trades directly, it informs traders of the world they’re operating in. Yield curve steepening or flattening, normalizing or inverting — each regime reflects a macro pressure zone that impacts duration demand, liquidity conditions, and systemic risk appetite. OverUnder abstracts that complexity into a color-coded compression map, helping traders orient themselves before making risk decisions. Whether you’re in bonds, currencies, crypto, or equities, the regime matters — and OverUnder makes it visible.

🧠 Core Logic

Built to show the slope and intent of a selected rate pair, the OverUnder Yield Spread defaults to 🇺🇸US10Y-US2Y, but can just as easily compare global sovereign curves or even dislocated monetary systems. This value is continuously monitored and passed through a debounce filter to determine whether the curve is:

• Inverted, or

• Steepening

If the curve is flattening below zero: the world is bracing for contraction. Policy lags. Risk appetite deteriorates. Duration gets bid, but only as protection. Stocks and speculative assets suffer, regardless of positioning.

📍 Curve Regimes in Bull and Bear Contexts

• Flattening occurs when the short and long ends compress . In a bull regime, flattening may reflect long-end demand or fading growth expectations. In a bear regime, flattening often precedes or confirms central bank tightening.

• Steepening indicates expanding spread . In a bull context, this may signal healthy risk appetite or early expansion. In a bear or crisis context, it may reflect aggressive front-end cuts and dislocation between short- and long-term expectations.

• If the curve is steepening above zero: the world is rotating into early expansion. Risk assets behave constructively. Bond traders position for normalization. Equities and crypto begin trending higher on rising forward expectations.

🖐️ Dynamically Colored Spread Line Reflects 1 of 4 Regime States

• 🟢 Normal / Steepening — early expansion or reflation

• 🔵 Normal / Flattening — late-cycle or neutral slowdown

• 🟠 Inverted / Steepening — policy reversal or soft landing attempt

• 🔴 Inverted / Flattening — hard contraction, credit stress, policy lag

🍋 The Lemon Label

At every bar, an anchored label floats directly on the spread line. It displays the active regime (in plain English) and the precise spread in percent (or basis points, depending on resolution). Colored lemon yellow, neither green nor red, the label is always legible — a design choice to de-emphasize bias and center the data .

🎨 Fill Zones

These bands offer spatial, persistent views of macro compression or inversion depth.

• Blue fill appears above the zero line in normal (non-inverted) conditions

• Red fill appears below the zero line during inversion

🧪 Sample Reading: 1W chart of TLT

OverUnder reveals a multi-year arc of structural inversion and regime transition. From mid-2021 through late 2023, the spread remains decisively inverted, signaling persistent flattening and credit stress as bond prices trended sharply lower. This prolonged inversion aligns with a high-volatility phase in TLT, marked by lower highs and an accelerating downtrend, confirming policy lag and macro tightening conditions.

As of early 2025, the spread has crossed back above the zero baseline into a “Normal / Steepening” regime (annotated at +0.56%), suggesting a macro inflection point. Price action remains subdued, but the shift in yield structure may foreshadow a change in trend context — particularly if follow-through in steepening persists.

🎭 Different Traders Respond Differently:

• Bond traders monitor slope change to anticipate policy pivots or recession signals.

• Equity traders use regime shifts to time rotations, from growth into defense, or from contraction into reflation.

• Currency traders interpret curve steepening as yield compression or divergence depending on region.

• Crypto traders treat inversion as a liquidity vacuum — and steepening as an early-phase risk unlock.

🛡️ Can It Compare Different Bond Markets?

Yes — with caveats. The indicator can be used to compare distinct sovereign yield instruments, for example:

• 🇫🇷FR10Y vs 🇩🇪DE10Y - France vs Germany

• 🇯🇵JP10Y vs 🇺🇸US10Y - BoJ vs Fed policy curves

However:

🙈 This no longer visualizes the domestic yield curve, but rather the differential between rate expectations across regions

🙉 The interpretation of “inversion” changes — it reflects spread compression across nations , not within a domestic yield structure

🙊 Color regimes should then be viewed as relative rate positioning , not absolute curve health

🙋🏻 Example: OverUnder compares French vs German 10Y yields

1. 🇫🇷 Change the long-duration ticker to FR10Y

2. 🇩🇪 Set the short-duration ticker to DE10Y

3. 🤔 Interpret the result as: “How much higher is France’s long-term borrowing cost vs Germany’s?”

You’ll see steepening when the spread rises (France decoupling), flattening when the spread compresses (convergence), and inversions when Germany yields rise above France’s — historically rare and meaningful.

🧐 Suggested Use

OverUnder is not a signal engine — it’s a context map. Its value comes from situating any trade idea within the prevailing yield regime. Use it before entries, not after them.

• On the 1W timeframe, OverUnder excels as a macro overlay. Yield regime shifts unfold over quarters, not days. Weekly structure smooths out rate volatility and reveals the true curvature of policy response and liquidity pressure. Use this view to orient your portfolio, define directional bias, or confirm long-duration trend turns in assets like TLT, SPX, or BTC.

• On the 1D timeframe, the indicator becomes tactically useful — especially when aligning breakout setups or trend continuations with steepening or flattening transitions. Daily views can also identify early-stage regime cracks that may not yet be visible on the weekly.

• Avoid sub-daily use unless you’re anchoring a thesis already built on higher timeframe structure. The yield curve is a macro construct — it doesn’t oscillate cleanly at intraday speeds. Shorter views may offer clarity during event-driven spikes (like FOMC reactions), but they do not replace weekly context.

Ultimately, OverUnder helps you decide: What kind of world am I trading in? Use it to confirm macro context, avoid fighting the curve, and lean into trades aligned with the broader pressure regime.

Stoch_RSI_ChartEnhanced Stochastic RSI Divergence Indicator with VWAP Filter for Charts

This custom indicator builds upon the classic Stochastic RSI to automatically detect both regular and hidden divergences. It’s designed to help traders spot potential market reversals or continuations using two methods for divergence detection (fractal‑ and pivot‑based) while offering optional VWAP filtering for confirmation.

Key Features

Stoch RSI Calculation

The indicator computes a smoothed Stoch RSI using configurable parameters for RSI length, stochastic length, and smoothing periods. An option to average the K and D lines provides a cleaner momentum view.

Divergence Detection via Fractals & Pivots

Fractal-Based Divergences:

Looks for 4-candle patterns to identify higher-highs or lower-lows in the price that are not confirmed by the oscillator, signaling potential reversals.

Pivot-Based Divergences:

Utilizes TradingView’s built-in pivot functions to find divergence conditions over adjustable pivot ranges.

Regular vs. Hidden Divergences:

Regular Divergence: Occurs when price makes a new extreme (higher high or lower low) while the Stoch RSI fails to follow suit.

Hidden Divergence: Indicates potential trend continuations when the oscillator diverges against the established price trend.

Optional VWAP Filtering

The script includes two optional VWAP filters that work as follows:

VWAP Filter on Regular Divergences:

Only confirms regular divergence signals if the current price satisfies the VWAP condition (e.g., price is above VWAP for bullish signals, below VWAP for bearish signals).

VWAP Filter on Hidden Divergences:

Similarly, hidden divergence signals are validated only when the price meets specific VWAP conditions, adding an extra layer of trend confirmation.

Customizable Alerts and Visual Labels

Easily configure divergence labels (“B” for bullish, “S” for bearish) and enable up to four alert conditions for real‑time notifications when a divergence occurs.

Credits & History:

Log RSI by @fskrypt

Divergence Detection originally by @RicardoSantos (with edits from @JustUncleL)

Further Edits by @NeoButane on August 8, 2018

Latest Edits by @FYMD on June 1, 2024

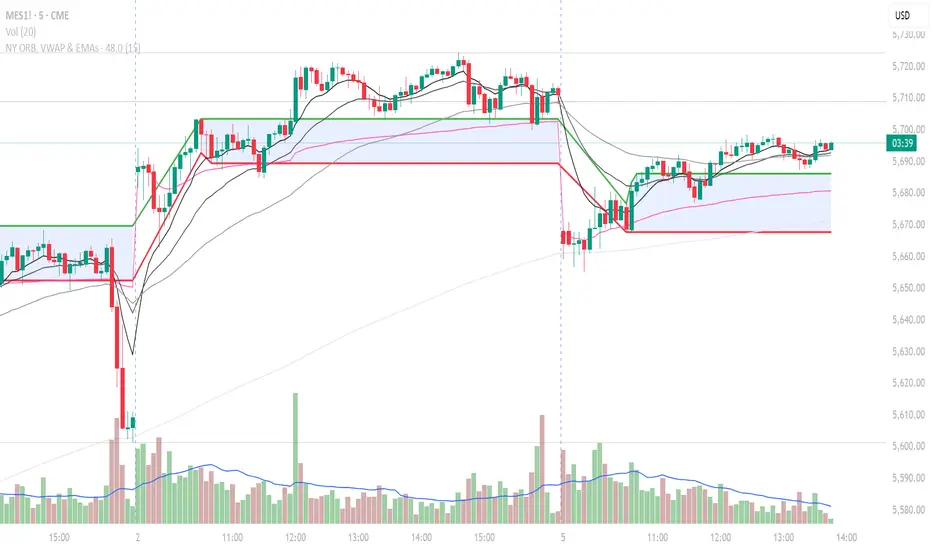

NY ORB, VWAP & EMAsIndicator is designed to display key technical analysis tools on your Trading View chart. It includes:

One of the key benefits of this indicator is that it allows Basic Trading View users to set VWAP, EMAs, and ORB in a single indicator. This is particularly useful for users who are limited to a single indicator on their Basic plan, as it provides a comprehensive view of market sentiment, trend, and potential breakouts without the need for multiple indicators.

Features

New York Opening Range Breakout (ORB): Plots the high and low of the first 15 minutes (configurable) of the New York trading session.

Volume Weighted Average Price (VWAP): Displays the VWAP line, which can be toggled on or off.

Exponential Moving Averages (EMAs): Plots four EMAs (9, 21, 50, and 200 periods), which can also be toggled on or off.

Customization

ORB Length: Choose from 5 or 15 minutes for the ORB calculation.

Show VWAP and EMAs: Toggle the visibility of the VWAP and EMA lines on or off.

Usage

This indicator is designed to help traders identify key market levels, trends, and potential breakouts during the New York trading session. The ORB can be used to gauge market sentiment, while the VWAP provides a benchmark for average price action. The EMAs offer additional trend analysis and can be used to identify potential support and resistance levels.