Enhanced Economic Composite with Dynamic WeightEnhanced Economic Composite with Dynamic Weight

Overview of the Indicator :

The "Enhanced Economic Composite with Dynamic Weight" is a comprehensive tool that combines multiple economic indicators, technical signals, and dynamic weighting to provide insights into market and economic health. It adjusts based on current volatility and recession risk, offering a detailed view of market conditions.

What This Indicator Does :

Tracks Economic Health: Uses key economic and market indicators to assess overall market conditions.

Dynamic Weighting: Adjusts the importance of components like stock indices, gold, and bonds based on volatility (VIX) and yield curve inversion.

Technical Signals: Identifies market momentum shifts through key crossovers like the Golden Cross, Death Cross, Silver Cross, and Hospice Cross.

Recession Shading: Marks known recessions for historical context.

Economic Factors Considered :

TIP (Treasury Inflation-Protected Securities): Reflects inflation expectations.

Gold: A safe-haven asset, increases in weight during volatility or rising momentum.

US Dollar Index (DXY): Measures USD strength, fixed weight of 10%, smoothed with EMA.

Commodities (DBC): Indicates global demand; weight increases with momentum or volatility.

Volatility Index (VIX): Reflects market risk, inversely related to market confidence.

Stock Indices (S&P 500, DJIA, NASDAQ, Russell 2000): Represent market performance, with weights reduced during high volatility or negative yield spread.

Yield Spread (10Y - 2Y Treasuries): Predicts recessions; negative spread reduces stock weighting.

Credit Spread (HYG - TLT): Indicates market risk through corporate vs. government bond yields.

How and Why Factors are Weighted:

Stock Indices get more weight in stable markets (low VIX, positive yield spread), while safe-haven assets like gold and bonds gain weight in volatile markets or during yield curve inversions. This dynamic adjustment ensures the composite reflects current market sentiment.

Technical Signals:

Golden Cross: 50 EMA crossing above 200 SMA, signaling bullish momentum.

Death Cross: 50 EMA below 200 SMA, indicating bearish momentum.

Silver Cross: 21 EMA crossing above 50 EMA, plotted only if below the 200-day SMA, signaling potential upside in downtrend conditions.

Hospice Cross: 50 EMA crosses below 21 EMA, plotted only if 21 EMA is below 200 SMA, a leading bearish signal.

Recession Shading:

Recession periods like the Great Recession, Early 2000s Recession, and COVID-19 Recession are shaded to provide historical context.

Benefits of Using This Indicator:

Comprehensive Analysis: Combines economic fundamentals and technical analysis for a full market view.

Dynamic Risk Adjustment: Weights shift between growth and safe-haven assets based on volatility and recession risk.

Early Signals: The Silver Cross and Hospice Cross provide early warnings of potential market shifts.

Recession Forecasting: Helps predict downturns through the yield curve and recession indicators.

Who Can Benefit:

Traders: Identify market momentum shifts early through crossovers.

Long-term Investors: Use recession warnings and dynamic adjustments to protect portfolios.

Analysts: A holistic tool for analyzing both economic trends and market movements.

This indicator helps users navigate varying market conditions by dynamically adjusting based on economic factors and providing early technical signals for market momentum shifts.

Cari dalam skrip untuk "美股科技股4月19日走势"

Nifty Dashboard//@version=5

//Author @GODvMarkets

indicator("GOD NSE Nifty Dashboard", "Nifty Dashboard")

i_timeframe = input.timeframe("D", "Timeframe")

// if not timeframe.isdaily

// runtime.error("Please switch timeframe to Daily")

i_text_size = input.string(size.auto, "Text Size", )

//-----------------------Functions-----------------------------------------------------

f_oi_buildup(price_chg_, oi_chg_) =>

switch

price_chg_ > 0 and oi_chg_ > 0 =>

price_chg_ > 0 and oi_chg_ < 0 =>

price_chg_ < 0 and oi_chg_ > 0 =>

price_chg_ < 0 and oi_chg_ < 0 =>

=>

f_color(val_) => val_ > 0 ? color.green : val_ < 0 ? color.red : color.gray

f_bg_color(val_) => val_ > 0 ? color.new(color.green,80) : val_ < 0 ? color.new(color.red,80) : color.new(color.black,80)

f_bg_color_price(val_) =>

fg_color_ = f_color(val_)

abs_val_ = math.abs(val_)

transp_ = switch

abs_val_ > .03 => 40

abs_val_ > .02 => 50

abs_val_ > .01 => 60

=> 80

color.new(fg_color_, transp_)

f_bg_color_oi(val_) =>

fg_color_ = f_color(val_)

abs_val_ = math.abs(val_)

transp_ = switch

abs_val_ > .10 => 40

abs_val_ > .05 => 50

abs_val_ > .025 => 60

=> 80

color.new(fg_color_, transp_)

f_day_of_week(time_=time) =>

switch dayofweek(time_)

1 => "Sun"

2 => "Mon"

3 => "Tue"

4 => "Wed"

5 => "Thu"

6 => "Fri"

7 => "Sat"

//-------------------------------------------------------------------------------------

var table table_ = table.new(position.middle_center, 22, 20, border_width = 1)

var cols_ = 0

var text_color_ = color.white

var bg_color_ = color.rgb(1, 5, 19)

f_symbol(idx_, symbol_) =>

symbol_nse_ = "NSE" + ":" + symbol_

fut_cur_ = "NSE" + ":" + symbol_ + "1!"

fut_next_ = "NSE" + ":" + symbol_ + "2!"

= request.security(symbol_nse_, i_timeframe, [close, close-close , close/close -1, volume], ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

= request.security(fut_cur_, i_timeframe, , ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

= request.security(fut_next_, i_timeframe, , ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

= request.security(fut_cur_ + "_OI", i_timeframe, [close, close-close ], ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

= request.security(fut_next_ + "_OI", i_timeframe, [close, close-close ], ignore_invalid_symbol = true, lookahead = barmerge.lookahead_on)

stk_vol_ = stk_vol_nse_

fut_vol_ = fut_cur_vol_ + fut_next_vol_

fut_oi_ = fut_cur_oi_ + fut_next_oi_

fut_oi_chg_ = fut_cur_oi_chg_ + fut_next_oi_chg_

fut_oi_chg_pct_ = fut_oi_chg_ / fut_oi_

fut_stk_vol_x_ = fut_vol_ / stk_vol_

fut_vol_oi_action_ = fut_vol_ / math.abs(fut_oi_chg_)

= f_oi_buildup(chg_pct_, fut_oi_chg_pct_)

close_color_ = fut_cur_close_ > fut_vwap_ ? color.green : fut_cur_close_ < fut_vwap_ ? color.red : text_color_

if barstate.isfirst

row_ = 0, col_ = 0

table.cell(table_, col_, row_, "Symbol", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Close", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "VWAP", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Pts", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Stk Vol", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Fut Vol", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Fut/Stk Vol", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Cur", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Next", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Cur Chg", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Next Chg", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "COI ", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "COI Chg", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Vol/OI Chg", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "COI Chg%", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "Pr.Chg%", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

table.cell(table_, col_, row_, "OI Buildup", text_color = text_color_, bgcolor = bg_color_, text_size = i_text_size), col_ += 1

cell_color_ = color.white

cell_bg_color_ = color.rgb(1, 7, 24)

if barstate.islast

row_ = idx_, col_ = 0

table.cell(table_, col_, row_, str.format("{0}", symbol_), text_color = f_color(chg_pct_), bgcolor = f_bg_color_price(chg_pct_), text_size = i_text_size, text_halign = text.align_left), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#.00}", fut_cur_close_), text_color = close_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#.00}", fut_vwap_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,0.00}", chg_pts_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", stk_vol_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_vol_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,0.00}", fut_stk_vol_x_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_cur_oi_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_next_oi_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_cur_oi_chg_), text_color = f_color(fut_cur_oi_chg_), bgcolor = f_bg_color(fut_cur_oi_chg_), text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_next_oi_chg_), text_color = f_color(fut_next_oi_chg_), bgcolor = f_bg_color(fut_next_oi_chg_), text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_oi_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,#,###}", fut_oi_chg_), text_color = f_color(fut_oi_chg_), bgcolor = f_bg_color(fut_oi_chg_), text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,0.00}", fut_vol_oi_action_), text_color = cell_color_, bgcolor = cell_bg_color_, text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,0.00%}", fut_oi_chg_pct_), text_color = f_color(fut_oi_chg_pct_), bgcolor = f_bg_color_oi(fut_oi_chg_pct_), text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0,number,0.00%}", chg_pct_), text_color = f_color(chg_pct_), bgcolor = f_bg_color_price(chg_pct_), text_size = i_text_size, text_halign = text.align_right), col_ += 1

table.cell(table_, col_, row_, str.format("{0}", oi_buildup_), text_color = oi_buildup_color_, bgcolor = color.new(oi_buildup_color_,80), text_size = i_text_size, text_halign = text.align_left), col_ += 1

idx_ = 1

f_symbol(idx_, "BANKNIFTY"), idx_ += 1

f_symbol(idx_, "NIFTY"), idx_ += 1

f_symbol(idx_, "CNXFINANCE"), idx_ += 1

f_symbol(idx_, "RELIANCE"), idx_ += 1

f_symbol(idx_, "HDFC"), idx_ += 1

f_symbol(idx_, "ITC"), idx_ += 1

f_symbol(idx_, "HINDUNILVR"), idx_ += 1

f_symbol(idx_, "INFY"), idx_ += 1

Interest Rate Trading (Manually Added Rate Decisions) [TANHEF]Interest Rate Trading: How Interest Rates Can Guide Your Next Move.

How were interest rate decisions added?

All interest rate decision dates were manually retrieved from the 'Record of Policy Actions' and 'Minutes of Actions' on the Federal Reserve's website due to inconsistent dates from other sources. These were manually added as Pine Script currently only identifies rate changes, not pauses.

█ Simple Explanation:

This script is designed for analyzing and backtesting trading strategies based on U.S. interest rate decisions which occur during Federal Open Market Committee (FOMC) meetings, to make trading decisions. No trading strategy is perfect, and it's important to understand that expectations won't always play out. The script leverages historical interest rate changes, including increases, decreases, and pauses, across multiple economic time periods from 1971 to the present. The tool integrates two key data sources for interest rates—USINTR and FEDFUNDS—to support decision-making around rate-based trades. The focus is on identifying opportunities and tracking trades driven by interest rate movements.

█ Interest Rate Decision Sources:

As noted above, each decision date has been manually added from the 'Record of Policy Actions' and 'Minutes of Actions' documents on the Federal Reserve's website. This includes +50 years of more than 600 rate decisions.

█ Interest Rate Data Sources:

USINTR: Reflects broader U.S. interest rate trends, including Treasury yields and various benchmarks. This is the preferred option as it corresponds well to the rate decision dates.

FEDFUNDS: Tracks the Federal Funds Rate, which is a more specific rate targeted by the Federal Reserve. This does not change on the exact same days as the rate decisions that occur at FOMC meetings.

█ Trade Criteria:

A variety of trading conditions are predefined to suit different trading strategies. These conditions include:

Increase/Decrease: Standard rate increases or decreases.

Double/Triple Increase/Decrease: A series of consecutive changes.

Aggressive Increase/Decrease: Rate changes that exceed recent movements.

Pause: Identification of no changes (pauses) between rate decisions, including double or triple pauses.

Complex Patterns: Combinations of pauses, increases, or decreases, such as "Pause after Increase" or "Pause or Increase."

█ Trade Execution and Exit:

The script allows automated trade execution based on selected criteria:

Auto-Entry: Option to enter trades automatically at the first valid period.

Max Trade Duration: Optional exit of trades after a specified number of bars (candles).

Pause Days: Minimum duration (in days) to validate rate pauses as entry conditions. This is especially useful for earlier periods (prior to the 2000s), where rate decisions often seemed random compared to the consistency we see today.

█ Visualization:

Several visual elements enhance the backtesting experience:

Time Period Highlighting: Economic time periods are visually segmented on the chart, each with a unique color. These periods include historical phases such as "Stagflation (1971-1982)" and "Post-Pandemic Recovery (2021-Present)".

Trade and Holding Results: Displays the profit and loss of trades and holding results directly on the chart.

Interest Rate Plot: Plots the interest rate movements on the chart, allowing for real-time tracking of rate changes.

Trade Status: Highlights active long or short positions on the chart.

█ Statistics and Criteria Display:

Stats Table: Summarizes trade results, including wins, losses, and draw percentages for both long and short trades.

Criteria Table: Lists the selected entry and exit criteria for both long and short positions.

█ Economic Time Periods:

The script organizes interest rate decisions into well-defined economic periods, allowing traders to backtest strategies specific to historical contexts like:

(1971-1982) Stagflation

(1983-1990) Reaganomics and Deregulation

(1991-1994) Early 1990s (Recession and Recovery)

(1995-2001) Dot-Com Bubble

(2001-2006) Housing Boom

(2007-2009) Global Financial Crisis

(2009-2015) Great Recession Recovery

(2015-2019) Normalization Period

(2019-2021) COVID-19 Pandemic

(2021-Present) Post-Pandemic Recovery

█ User-Configurable Inputs:

Rate Source Selection: Choose between USINTR or FEDFUNDS as the primary interest rate source.

Trade Criteria Customization: Users can select the criteria for long and short trades, specifying when to enter or exit based on changes in the interest rate.

Time Period: Select the time period that you want to isolate testing a strategy with.

Auto-Entry and Pause Settings: Options to automatically enter trades and specify the number of days to confirm a rate pause.

Max Trade Duration: Limits how long trades can remain open, defined by the number of bars.

█ Trade Logic:

The script manages entries and exits for both long and short trades. It calculates the profit or loss percentage based on the entry and exit prices. The script tracks ongoing trades, dynamically updating the profit or loss as price changes.

█ Examples:

One of the most popular opinions is that when rate starts begin you should sell, then buy back in when rate cuts stop dropping. However, this can be easily proven to be a difficult task. Predicting the end of a rate cut is very difficult to do with the the exception that assumes rates will not fall below 0.25%.

2001-2009

Trade Result: +29.85%

Holding Result: -27.74%

1971-2024

Trade Result: +533%

Holding Result: +5901%

█ Backtest and Real-Time Use:

This backtester is useful for historical analysis and real-time trading. By setting up various entry and exit rules tied to interest rate movements, traders can test and refine strategies based on real historical data and rate decision trends.

This powerful tool allows traders to customize strategies, backtest them through different economic periods, and get visual feedback on their trading performance, helping to make more informed decisions based on interest rate dynamics. The main goal of this indicator is to challenge the belief that future events must mirror the 2001 and 2007 rate cuts. If everyone expects something to happen, it usually doesn’t.

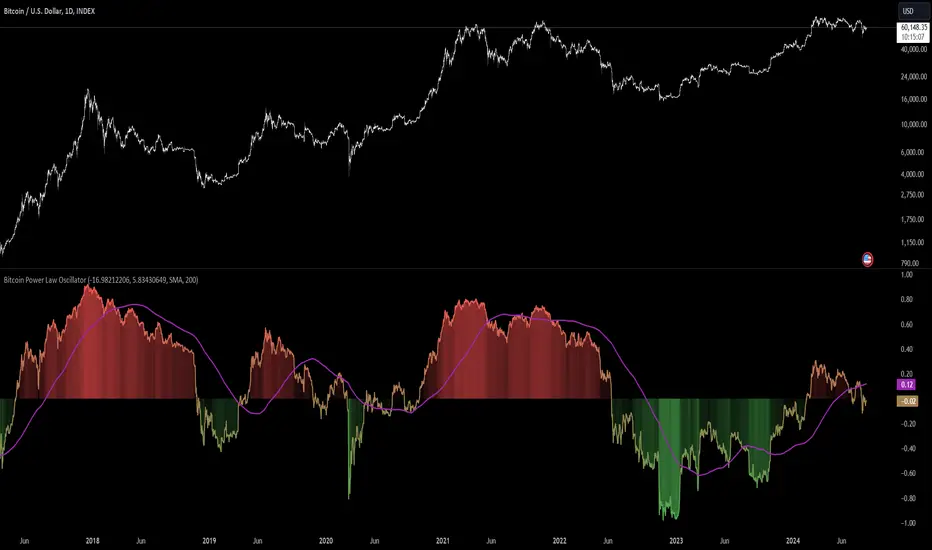

Bitcoin Power Law Oscillator [InvestorUnknown]The Bitcoin Power Law Oscillator is a specialized tool designed for long-term mean-reversion analysis of Bitcoin's price relative to a theoretical midline derived from the Bitcoin Power Law model (made by capriole_charles). This oscillator helps investors identify whether Bitcoin is currently overbought, oversold, or near its fair value according to this mathematical model.

Key Features:

Power Law Model Integration: The oscillator is based on the midline of the Bitcoin Power Law, which is calculated using regression coefficients (A and B) applied to the logarithm of the number of days since Bitcoin’s inception. This midline represents a theoretical fair value for Bitcoin over time.

Midline Distance Calculation: The distance between Bitcoin’s current price and the Power Law midline is computed as a percentage, indicating how far above or below the price is from this theoretical value.

float a = input.float (-16.98212206, 'Regression Coef. A', group = "Power Law Settings")

float b = input.float (5.83430649, 'Regression Coef. B', group = "Power Law Settings")

normalization_start_date = timestamp(2011,1,1)

calculation_start_date = time == timestamp(2010, 7, 19, 0, 0) // First BLX Bitcoin Date

int days_since = request.security('BNC:BLX', 'D', ta.barssince(calculation_start_date))

bar() =>

= request.security('BNC:BLX', 'D', bar())

int offset = 564 // days between 2009/1/1 and "calculation_start_date"

int days = days_since + offset

float e = a + b * math.log10(days)

float y = math.pow(10, e)

float midline_distance = math.round((y / btc_close - 1.0) * 100)

Oscillator Normalization: The raw distance is converted into a normalized oscillator, which fluctuates between -1 and 1. This normalization adjusts the oscillator to account for historical extremes, making it easier to compare current conditions with past market behavior.

float oscillator = -midline_distance

var float min = na

var float max = na

if (oscillator > max or na(max)) and time >= normalization_start_date

max := oscillator

if (min > oscillator or na(min)) and time >= normalization_start_date

min := oscillator

rescale(float value, float min, float max) =>

(2 * (value - min) / (max - min)) - 1

normalized_oscillator = rescale(oscillator, min, max)

Overbought/Oversold Identification: The oscillator provides a clear visual representation, where values near 1 suggest Bitcoin is overbought, and values near -1 indicate it is oversold. This can help identify potential reversal points or areas of significant market imbalance.

Optional Moving Average: Users can overlay a moving average (either SMA or EMA) on the oscillator to smooth out short-term fluctuations and focus on longer-term trends. This is particularly useful for confirming trend reversals or persistent overbought/oversold conditions.

This indicator is particularly useful for long-term Bitcoin investors who wish to gauge the market's mean-reversion tendencies based on a well-established theoretical model. By focusing on the Power Law’s midline, users can gain insights into whether Bitcoin’s current price deviates significantly from what historical trends would suggest as a fair value.

Multi-Step FlexiSuperTrend - Strategy [presentTrading]At the heart of this endeavor is a passion for continuous improvement in the art of trading

█ Introduction and How it is Different

The "Multi-Step FlexiSuperTrend - Strategy " is an advanced trading strategy that integrates the well-known SuperTrend indicator with a nuanced and dynamic approach to market trend analysis. Unlike conventional SuperTrend strategies that rely on static thresholds and fixed parameters, this strategy introduces multi-step take profit mechanisms that allow traders to capitalize on varying market conditions in a more controlled and systematic manner.

What sets this strategy apart is its ability to dynamically adjust to market volatility through the use of an incremental factor applied to the SuperTrend calculation. This adjustment ensures that the strategy remains responsive to both minor and major market shifts, providing a more accurate signal for entries and exits. Additionally, the integration of multi-step take profit levels offers traders the flexibility to scale out of positions, locking in profits progressively as the market moves in their favor.

BTC 6hr Long/Short Performance

█ Strategy, How it Works: Detailed Explanation

The Multi-Step FlexiSuperTrend strategy operates on the foundation of the SuperTrend indicator, but with several enhancements that make it more adaptable to varying market conditions. The key components of this strategy include the SuperTrend Polyfactor Oscillator, a dynamic normalization process, and multi-step take profit levels.

🔶 SuperTrend Polyfactor Oscillator

The SuperTrend Polyfactor Oscillator is the heart of this strategy. It is calculated by applying a series of SuperTrend calculations with varying factors, starting from a defined "Starting Factor" and incrementing by a specified "Increment Factor." The indicator length and the chosen price source (e.g., HLC3, HL2) are inputs to the oscillator.

The SuperTrend formula typically calculates an upper and lower band based on the average true range (ATR) and a multiplier (the factor). These bands determine the trend direction. In the FlexiSuperTrend strategy, the oscillator is enhanced by iteratively applying the SuperTrend calculation across different factors. The iterative process allows the strategy to capture both minor and significant trend changes.

For each iteration (indexed by `i`), the following calculations are performed:

1. ATR Calculation: The Average True Range (ATR) is calculated over the specified `indicatorLength`:

ATR_i = ATR(indicatorLength)

2. Upper and Lower Bands Calculation: The upper and lower bands are calculated using the ATR and the current factor:

Upper Band_i = hl2 + (ATR_i * Factor_i)

Lower Band_i = hl2 - (ATR_i * Factor_i)

Here, `Factor_i` starts from `startingFactor` and is incremented by `incrementFactor` in each iteration.

3. Trend Determination: The trend is determined by comparing the indicator source with the upper and lower bands:

Trend_i = 1 (uptrend) if IndicatorSource > Upper Band_i

Trend_i = 0 (downtrend) if IndicatorSource < Lower Band_i

Otherwise, the trend remains unchanged from the previous value.

4. Output Calculation: The output of each iteration is determined based on the trend:

Output_i = Lower Band_i if Trend_i = 1

Output_i = Upper Band_i if Trend_i = 0

This process is repeated for each iteration (from 0 to 19), creating a series of outputs that reflect different levels of trend sensitivity.

Local

🔶 Normalization Process

To make the oscillator values comparable across different market conditions, the deviations between the indicator source and the SuperTrend outputs are normalized. The normalization method can be one of the following:

1. Max-Min Normalization: The deviations are normalized based on the range of the deviations:

Normalized Value_i = (Deviation_i - Min Deviation) / (Max Deviation - Min Deviation)

2. Absolute Sum Normalization: The deviations are normalized based on the sum of absolute deviations:

Normalized Value_i = Deviation_i / Sum of Absolute Deviations

This normalization ensures that the oscillator values are within a consistent range, facilitating more reliable trend analysis.

For more details:

🔶 Multi-Step Take Profit Mechanism

One of the unique features of this strategy is the multi-step take profit mechanism. This allows traders to lock in profits at multiple levels as the market moves in their favor. The strategy uses three take profit levels, each defined as a percentage increase (for long trades) or decrease (for short trades) from the entry price.

1. First Take Profit Level: Calculated as a percentage increase/decrease from the entry price:

TP_Level1 = Entry Price * (1 + tp_level1 / 100) for long trades

TP_Level1 = Entry Price * (1 - tp_level1 / 100) for short trades

The strategy exits a portion of the position (defined by `tp_percent1`) when this level is reached.

2. Second Take Profit Level: Similar to the first level, but with a higher percentage:

TP_Level2 = Entry Price * (1 + tp_level2 / 100) for long trades

TP_Level2 = Entry Price * (1 - tp_level2 / 100) for short trades

The strategy exits another portion of the position (`tp_percent2`) at this level.

3. Third Take Profit Level: The final take profit level:

TP_Level3 = Entry Price * (1 + tp_level3 / 100) for long trades

TP_Level3 = Entry Price * (1 - tp_level3 / 100) for short trades

The remaining portion of the position (`tp_percent3`) is exited at this level.

This multi-step approach provides a balance between securing profits and allowing the remaining position to benefit from continued favorable market movement.

█ Trade Direction

The strategy allows traders to specify the trade direction through the `tradeDirection` input. The options are:

1. Both: The strategy will take both long and short positions based on the entry signals.

2. Long: The strategy will only take long positions.

3. Short: The strategy will only take short positions.

This flexibility enables traders to tailor the strategy to their market outlook or current trend analysis.

█ Usage

To use the Multi-Step FlexiSuperTrend strategy, traders need to set the input parameters according to their trading style and market conditions. The strategy is designed for versatility, allowing for various market environments, including trending and ranging markets.

Traders can also adjust the multi-step take profit levels and percentages to match their risk management and profit-taking preferences. For example, in highly volatile markets, traders might set wider take profit levels with smaller percentages at each level to capture larger price movements.

The normalization method and the incremental factor can be fine-tuned to adjust the sensitivity of the SuperTrend Polyfactor Oscillator, making the strategy more responsive to minor market shifts or more focused on significant trends.

█ Default Settings

The default settings of the strategy are carefully chosen to provide a balanced approach between risk management and profit potential. Here is a breakdown of the default settings and their effects on performance:

1. Indicator Length (10): This parameter controls the lookback period for the ATR calculation. A shorter length makes the strategy more sensitive to recent price movements, potentially generating more signals. A longer length smooths out the ATR, reducing sensitivity but filtering out noise.

2. Starting Factor (0.618): This is the initial multiplier used in the SuperTrend calculation. A lower starting factor makes the SuperTrend bands closer to the price, generating more frequent trend changes. A higher starting factor places the bands further away, filtering out minor fluctuations.

3. Increment Factor (0.382): This parameter controls how much the factor increases with each iteration of the SuperTrend calculation. A smaller increment factor results in more gradual changes in sensitivity, while a larger increment factor creates a wider range of sensitivity across the iterations.

4. Normalization Method (None): The default is no normalization, meaning the raw deviations are used. Normalization methods like Max-Min or Absolute Sum can make the deviations more consistent across different market conditions, improving the reliability of the oscillator.

5. Take Profit Levels (2%, 8%, 18%): These levels define the thresholds for exiting portions of the position. Lower levels (e.g., 2%) capture smaller profits quickly, while higher levels (e.g., 18%) allow positions to run longer for more significant gains.

6. Take Profit Percentages (30%, 20%, 15%): These percentages determine how much of the position is exited at each take profit level. A higher percentage at the first level locks in more profit early, reducing exposure to market reversals. Lower percentages at higher levels allow for a portion of the position to benefit from extended trends.

KillZones + ACD Fisher [TradingFinder] Sessions + Reversal Level🔵 Introduction

🟣 ACD Method

"The Logical Trader" opens with a thorough exploration of the ACD Methodology, which focuses on pinpointing particular price levels associated with the opening range.

This approach enables traders to establish reference points for their trades, using "A" and "C" points as entry markers. Additionally, the book covers the concept of the "Pivot Range" and how integrating it with the ACD method can help maximize position size while minimizing risk.

🟣 Session

The forex market is operational 24 hours a day, five days a week, closing only on Saturdays and Sundays. Typically, traders prefer to concentrate on one specific forex trading session rather than attempting to trade around the clock.

Trading sessions are defined time periods when a particular financial market is active, allowing for the execution of trades.

The most crucial trading sessions within the 24-hour cycle are the Asia, London, and New York sessions, as these are when substantial money flows and liquidity enter the market.

🟣 Kill Zone

Traders in financial markets earn profits by capitalizing on the difference between their buy/sell prices and the prevailing market prices.

Traders vary in their trading timelines.Some traders engage in daily or even hourly trading, necessitating activity during periods with optimal trading volumes and notable price movements.

Kill zones refer to parts of a session characterized by higher trading volumes and increased price volatility compared to the rest of the session.

🔵 How to Use

🟣 Session Times

The "Asia Session" comprises two parts: "Sydney" and "Tokyo." This session begins at 23:00 and ends at 06:00 UTC. The "Asia KillZone" starts at 23:00 and ends at 03:55 UTC.

The "London Session" includes "Frankfurt" and "London," starting at 07:00 and ending at 14:25 UTC. The "London KillZone" runs from 07:00 to 09:55 UTC.

The "New York" session starts at 14:30 and ends at 19:25 UTC, with the "New York am KillZone" beginning at 14:30 and ending at 22:55 UTC.

🟣 ACD Methodology

The ACD strategy is versatile, applicable to various markets such as stocks, commodities, and forex, providing clear buy and sell signals to set price targets and stop losses.

This strategy operates on the premise that the opening range of trades holds statistical significance daily, suggesting that initial market movements impact the market's behavior throughout the day.

Known as a breakout strategy, the ACD method thrives in volatile or strongly trending markets like crude oil and stocks.

Some key rules for employing the ACD strategy include :

Utilize points A and C as critical reference points, continually monitoring these during trades as they act as entry and exit markers.

Analyze daily and multi-day pivot ranges to understand market trends. Prices above the pivots indicate an upward trend, while prices below signal a downward trend.

In forex trading, the ACD strategy can be implemented using the ACD indicator, a technical tool that gauges the market's supply and demand balance. By evaluating trading volume and price, this indicator assists traders in identifying trend strength and optimal entry and exit points.

To effectively use the ACD indicator, consider the following :

Identifying robust trends: The ACD indicator can help pinpoint strong, consistent market trends.

Determining entry and exit points: ACD generates buy and sell signals to optimize trade timing.

Bullish Setup :

When the "A up" line is breached, it’s wise to wait briefly to confirm it’s not a "Fake Breakout" and that the price stabilizes above this line.

Upon entering the trade, the most effective stop loss is positioned below the "A down" line. It's advisable to backtest this to ensure the best outcomes. The recommended reward-to-risk ratio for this strategy is 1, which should also be verified through backtesting.

Bearish Setup :

When the "A down" line is breached, it’s prudent to wait briefly to ensure it’s not a "Fake Breakout" and that the price stabilizes below this line.

Upon entering the trade, the most effective stop loss is positioned above the "A up" line. Backtesting is recommended to confirm the best results. The recommended reward-to-risk ratio for this strategy is 1, which should also be validated through backtesting.

Advantages of Combining Kill Zone and ACD Method in Market Analysis :

Precise Trade Timing : Integrating the Kill Zone strategy with the ACD Method enhances precision in trade entries and exits. The ACD Method identifies key points for trading, while the Kill Zone focuses on high-activity periods, together ensuring optimal timing for trades.

Better Trend Identification : The ACD Method’s pivot ranges help spot market trends, and when combined with the Kill Zone’s emphasis on periods of significant price movement, traders can more effectively identify and follow strong market trends.

Maximized Profits and Minimized Risks : The ACD Method's structured approach to setting price targets and stop losses, coupled with the Kill Zone's high-volume trading periods, helps maximize profit potential while reducing risk.

Robust Risk Management : Combining these methods provides a comprehensive risk management strategy, strategically placing stop losses and protecting capital during volatile periods.

Versatility Across Markets : Both methods are applicable to various markets, including stocks, commodities, and forex, offering flexibility and adaptability in different trading environments.

Enhanced Confidence : Using the combined insights of the Kill Zone and ACD Method, traders gain confidence in their decision-making process, reducing emotional trading and improving consistency.

By merging the Kill Zone’s focus on trading volumes and the ACD Method’s structured breakout strategy, traders benefit from a synergistic approach that enhances precision, trend identification, and risk management across multiple markets.

ICT KillZones Hunt [TradingFinder] 4 Sessions + OB + FVG + Alert🔵 Introduction

🟣 ICT

The "ICT" style is a subset of "Price Action" technical analysis. The primary goal of the ICT trading strategy is to merge "Price Action" with the "Smart Money" concept to pinpoint optimal trade entry points.

However, this approach's strength extends beyond merely finding entry points. It also helps traders gain a deeper understanding of price behavior and adapt their trading strategies to the market structure.

The most important concepts of "ICT" :

Order Block

Fair Value Gap(FVG)

Liquidity

🟣 Session

Financial markets are divided into several time periods, each featuring distinct characteristics and levels of activity. These periods, known as sessions, are active at different times during the day.

The primary active sessions in financial markets include :

Asian Session

European Session

New York Session

Based on the UTC time zone, the schedule for these key sessions is :

Asian Session: 23:00 to 06:00

European Session: 07:00 to 16:30

New York Session: 13:00 to 22:00

Note

To avoid session overlap and minimize interference during kill zones, the session times have been modified as follows :

Asian Session: 23:00 to 06:00

European Session: 07:00 to 14:25

New York Session: 14:30 to 22:55

🟣 KillZone

Kill zones are periods within a session where trader activity spikes. During these times, trading volume surges, and price movements become more pronounced.

The major kill zones, according to the UTC time zone, are as follows :

Asian Kill Zone: 23:00 to 03:55

European Kill Zone: 07:00 to 09:55

New York Morning Kill Zone: 14:30 to 16:55

New York Evening Kill Zone: 19:30 to 20:55

🔵 How to Use

🟣 Order Block

Order blocks are a distinct category of "Supply and Demand" zones, formed when a series of orders are grouped together. These blocks are often created by banks or other significant market participants.

Banks typically execute large orders in blocks during their trading sessions. If they were to enter the market with small quantities, substantial price movements would occur before the orders were fully executed, reducing potential profit.

To mitigate this, they divide their orders into smaller, more manageable positions. Traders should seek "buy" opportunities in "demand order blocks" and "sell" opportunities in "supply order blocks."

🟣 Fair Value Gap (FVG)

To pinpoint the "Fair Value Gap" on the chart, meticulous candle-by-candle analysis is essential. Pay close attention to candles with significant bodies, examining each candle alongside the one preceding it.

The candles flanking this central candle should exhibit elongated shadows, with bodies that do not intersect the body of the central candle. The span between the shadows of the first and third candles is referred to as the FVG range.

Note :

The origin of all Order Blocks and FVGs starts from inside a kill zone and extends up to the end of the same session.

🟣 Kill Zone Hunt

Following this strategy, after the conclusion of the kill zone and the stabilization of its high and low lines, if the price touches either of these lines within the same session and encounters a robust rejection, it presents an opportunity to enter a trade.

🔵 Setting

🟣 Global Setting

Show All Order Block :

If it is turned off, only the last Order Block will be displayed.

Show All FVG :

If it is turned off, only the last FVG will be displayed.

Show More Info Session :

If it is turned on, more information about kill zones (Trade Volume, Time, Number of Candles) will be displayed.

🟣 Logic Parameter

Pivot Period of Order Blocks Detector :

Enter the desired pivot period to identify the Order Block.

Order Block Validity Period (Bar) :

You can specify the maximum time the Order Block remains valid based on the number of candles from the origin.

Mitigation Level Order Block :

Determining the basic level of a block order. When the price hits the basic level, the order block due to mitigation.

🟣 Order Blocks Display

Demand Order Block :

Show or not show and specify color.

Supply order Block :

Show or not show and specify color.

🟣 Order Block Refinement

Refine Demand OB :

Enable or disable the refinement feature. Mode selection.

Refine Supply OB :

Enable or disable the refinement feature. Mode selection.

🟣 FVG

FVG Validity Period (Bar) :

You can specify the maximum time the FVG remains valid based on the number of candles from the origin.

Mitigation Level FVG :

Determining the basic level of a FVG. When the price hits the basic level, the FVG due to mitigation.

Show Demand FVG :

Show or not show and specify color.

Show Supply FVG :

Show or not show and specify color.

FVG Filter :

Enable or disable filtering of FVGs. Select filter mode.

🟣 Session

Show More Info Session Color

Asia Session, London Sesseion, New York am Session & New York pm Session :

Show or not show session and kill zones. Change the display color.

🟣 Alert

Send Alert When Touched Session high & Low :

On / Off

Alert Demand OB Mitigation :

On / Off

Alert Supply OB Mitigation :

On / Off

Alert Demand FVG Mitigation :

On / Off

Alert Supply FVG Mitigation :

On / Off

Message Frequency :

This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Show Alert Time by Time Zone :

The date, hour, and minute you receive in alert messages can be based on any time zone you choose. For example, if you want New York time, you should enter "UTC-4". This input is set to the time zone "UTC" by default.

Display More Info :

Displays information about the price range of the order blocks (Zone Price) and the date, hour, and minute under "Display More Info". If you do not want this information to appear in the received message along with the alert, you should set it to "Off".

Intellect_city - Halvings Bitcoin CycleWhat is halving?

The halving timer shows when the next Bitcoin halving will occur, as well as the dates of past halvings. This event occurs every 210,000 blocks, which is approximately every 4 years. Halving reduces the emission reward by half. The original Bitcoin reward was 50 BTC per block found.

Why is halving necessary?

Halving allows you to maintain an algorithmically specified emission level. Anyone can verify that no more than 21 million bitcoins can be issued using this algorithm. Moreover, everyone can see how much was issued earlier, at what speed the emission is happening now, and how many bitcoins remain to be mined in the future. Even a sharp increase or decrease in mining capacity will not significantly affect this process. In this case, during the next difficulty recalculation, which occurs every 2014 blocks, the mining difficulty will be recalculated so that blocks are still found approximately once every ten minutes.

How does halving work in Bitcoin blocks?

The miner who collects the block adds a so-called coinbase transaction. This transaction has no entry, only exit with the receipt of emission coins to your address. If the miner's block wins, then the entire network will consider these coins to have been obtained through legitimate means. The maximum reward size is determined by the algorithm; the miner can specify the maximum reward size for the current period or less. If he puts the reward higher than possible, the network will reject such a block and the miner will not receive anything. After each halving, miners have to halve the reward they assign to themselves, otherwise their blocks will be rejected and will not make it to the main branch of the blockchain.

The impact of halving on the price of Bitcoin

It is believed that with constant demand, a halving of supply should double the value of the asset. In practice, the market knows when the halving will occur and prepares for this event in advance. Typically, the Bitcoin rate begins to rise about six months before the halving, and during the halving itself it does not change much. On average for past periods, the upper peak of the rate can be observed more than a year after the halving. It is almost impossible to predict future periods because, in addition to the reduction in emissions, many other factors influence the exchange rate. For example, major hacks or bankruptcies of crypto companies, the situation on the stock market, manipulation of “whales,” or changes in legislative regulation.

---------------------------------------------

Table - Past and future Bitcoin halvings:

---------------------------------------------

Date: Number of blocks: Award:

0 - 03-01-2009 - 0 block - 50 BTC

1 - 28-11-2012 - 210000 block - 25 BTC

2 - 09-07-2016 - 420000 block - 12.5 BTC

3 - 11-05-2020 - 630000 block - 6.25 BTC

4 - 20-04-2024 - 840000 block - 3.125 BTC

5 - 24-03-2028 - 1050000 block - 1.5625 BTC

6 - 26-02-2032 - 1260000 block - 0.78125 BTC

7 - 30-01-2036 - 1470000 block - 0.390625 BTC

8 - 03-01-2040 - 1680000 block - 0.1953125 BTC

9 - 07-12-2043 - 1890000 block - 0.09765625 BTC

10 - 10-11-2047 - 2100000 block - 0.04882813 BTC

11 - 14-10-2051 - 2310000 block - 0.02441406 BTC

12 - 17-09-2055 - 2520000 block - 0.01220703 BTC

13 - 21-08-2059 - 2730000 block - 0.00610352 BTC

14 - 25-07-2063 - 2940000 block - 0.00305176 BTC

15 - 28-06-2067 - 3150000 block - 0.00152588 BTC

16 - 01-06-2071 - 3360000 block - 0.00076294 BTC

17 - 05-05-2075 - 3570000 block - 0.00038147 BTC

18 - 08-04-2079 - 3780000 block - 0.00019073 BTC

19 - 12-03-2083 - 3990000 block - 0.00009537 BTC

20 - 13-02-2087 - 4200000 block - 0.00004768 BTC

21 - 17-01-2091 - 4410000 block - 0.00002384 BTC

22 - 21-12-2094 - 4620000 block - 0.00001192 BTC

23 - 24-11-2098 - 4830000 block - 0.00000596 BTC

24 - 29-10-2102 - 5040000 block - 0.00000298 BTC

25 - 02-10-2106 - 5250000 block - 0.00000149 BTC

26 - 05-09-2110 - 5460000 block - 0.00000075 BTC

27 - 09-08-2114 - 5670000 block - 0.00000037 BTC

28 - 13-07-2118 - 5880000 block - 0.00000019 BTC

29 - 16-06-2122 - 6090000 block - 0.00000009 BTC

30 - 20-05-2126 - 6300000 block - 0.00000005 BTC

31 - 23-04-2130 - 6510000 block - 0.00000002 BTC

32 - 27-03-2134 - 6720000 block - 0.00000001 BTC

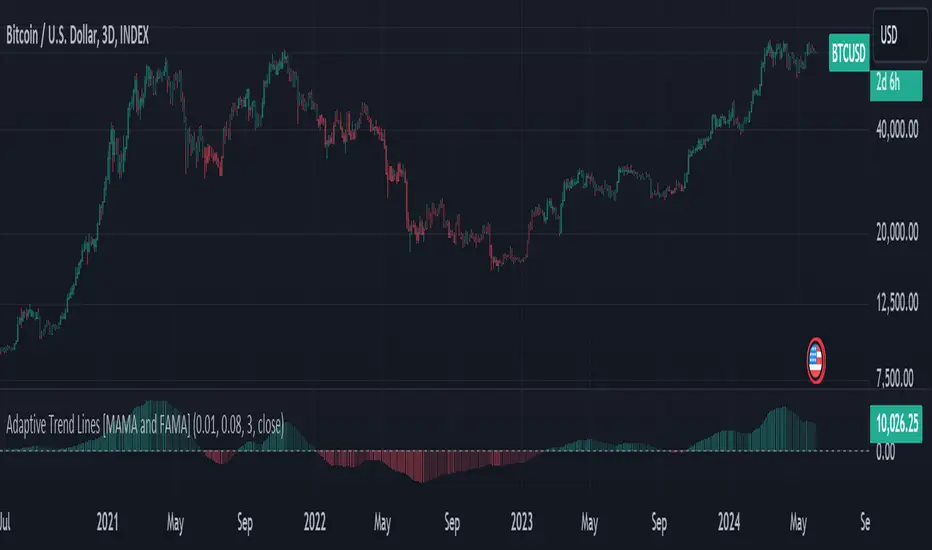

Adaptive Trend Lines [MAMA and FAMA]Updated my previous algo on the Adaptive Trend lines, however I have added new functionalities and sorted out the settings.

You can now switch between normalized and non-normalized settings, the colors have also been updated and look much better.

The MAMA and FAMA

These indicators was originally developed by John F. Ehlers (Stocks & Commodities V. 19:10: MESA Adaptive Moving Averages). Everget wrote the initial functions for these in pine script. I have simply normalized the indicators and chosen to use the Laplace transformation instead of the hilbert transformation

How the Indicator Works:

The indicator employs a series of complex calculations, but we'll break it down into key steps to understand its functionality:

LaplaceTransform: Calculates the Laplace distribution for the given src input. The Laplace distribution is a continuous probability distribution, also known as the double exponential distribution. I use this because of the assymetrical return profile

MESA Period: The indicator calculates a MESA period, which represents the dominant cycle length in the price data. This period is continuously adjusted to adapt to market changes.

InPhase and Quadrature Components: The InPhase and Quadrature components are derived from the Hilbert Transform output. These components represent different aspects of the price's cyclical behavior.

Homodyne Discriminator: The Homodyne Discriminator is a phase-sensitive technique used to determine the phase and amplitude of a signal. It helps in detecting trend changes.

Alpha Calculation: Alpha represents the adaptive factor that adjusts the sensitivity of the indicator. It is based on the MESA period and the phase of the InPhase component. Alpha helps in dynamically adjusting the indicator's responsiveness to changes in market conditions.

MAMA and FAMA Calculation: The MAMA and FAMA values are calculated using the adaptive factor (alpha) and the input price data. These values are essentially adaptive moving averages that aim to capture the current trend more effectively than traditional moving averages.

But Omar, why would anyone want to use this?

The MAMA and FAMA lines offer benefits:

The indicator offers a distinct advantage over conventional moving averages due to its adaptive nature, which allows it to adjust to changing market conditions. This adaptability ensures that investors can stay on the right side of the trend, as the indicator becomes more responsive during trending periods and less sensitive in choppy or sideways markets.

One of the key strengths of this indicator lies in its ability to identify trends effectively by combining the MESA and MAMA techniques. By doing so, it efficiently filters out market noise, making it highly valuable for trend-following strategies. Investors can rely on this feature to gain clearer insights into the prevailing trends and make well-informed trading decisions.

This indicator is primarily suppoest to be used on the big timeframes to see which trend is prevailing, however I am not against someone using it on a timeframe below the 1D, just be careful if you are using this for modern portfolio theory, this is not suppoest to be a mid-term component, but rather a long term component that works well with proper use of detrended fluctuation analysis.

Dont hesitate to ask me if you have any questions

Again, I want to give credit to Everget and ChartPrime!

Code explanation as required by House Rules:

fastLimit = input.float(title='Fast Limit', step=0.01, defval=0.01, group = "Indicator Settings")

slowLimit = input.float(title='Slow Limit', step=0.01, defval=0.08, group = "Indicator Settings")

src = input(title='Source', defval=close, group = "Indicator Settings")

input.float: Used to create input fields for the user to set the fastLimit and slowLimit values.

input: General function to get user inputs, like the data source (close price) used for calculations.

norm_period = input.int(3, 'Normalization Period', 1, group = "Normalized Settings")

norm = input.bool(defval = true, title = "Use normalization", group = "Normalized Settings")

input.int: Creates an input field for the normalization period.

input.bool: Allows the user to toggle normalization on or off.

Color settings in the code:

col_up = input.color(#22ab94, group = "Color Settings")

col_dn = input.color(#f7525f, group = "Color Settings")

Constants and functions

var float PI = math.pi

laplace(src) =>

(0.5) * math.exp(-math.abs(src))

_computeComponent(src, mesaPeriodMult) =>

out = laplace(src) * mesaPeriodMult

out

_smoothComponent(src) =>

out = 0.2 * src + 0.8 * nz(src )

out

math.pi: Represents the mathematical constant π (pi).

laplace: A function that applies the Laplace transform to the source data.

_computeComponent: Computes a component of the data using the Laplace transform.

_smoothComponent: Smooths data by averaging the current value with the previous one (nz function is used to handle null values).

Alpha function:

_computeAlpha(src, fastLimit, slowLimit) =>

mesaPeriod = 0.0

mesaPeriodMult = 0.075 * nz(mesaPeriod ) + 0.54

...

alpha = math.max(fastLimit / deltaPhase, slowLimit)

out = alpha

out

_computeAlpha: Calculates the adaptive alpha value based on the fastLimit and slowLimit. This value is crucial for determining the MAMA and FAMA lines.

Calculating MAMA and FAMA:

mama = 0.0

mama := alpha * src + (1 - alpha) * nz(mama )

fama = 0.0

fama := alpha2 * mama + (1 - alpha2) * nz(fama )

Normalization:

lowest = ta.lowest(mama_fama_diff, norm_period)

highest = ta.highest(mama_fama_diff, norm_period)

normalized = (mama_fama_diff - lowest) / (highest - lowest) - 0.5

ta.lowest and ta.highest: Find the lowest and highest values of mama_fama_diff over the normalization period.

The oscillator is normalized to a range, making it easier to compare over different periods.

And finally, the plotting:

plot(norm == true ? normalized : na, style=plot.style_columns, color=col_wn, title = "mama_fama_diff Oscillator Normalized")

plot(norm == false ? mama_fama_diff : na, style=plot.style_columns, color=col_wnS, title = "mama_fama_diff Oscillator")

Example of Normalized settings:

Example for setup:

Try to make sure the lower timeframe follows the higher timeframe if you take a trade based on this indicator!

KillZones Hunt + Sessions [TradingFinder] Alert & Volume Ranges🟣 Introduction

🔵 Session

Financial markets are divided into various time segments, each with its own characteristics and activity levels. These segments are called sessions, and they are active at different times of the day.

The most important active sessions in financial markets are :

1. Asian Session

2. European Session

3. New York Session

The timing of these major sessions based on the UTC time zone is as follows :

1. Asian Session: 23:00 to 06:00

2. European Session: 07:00 to 16:30

3. New York Session: 13:00 to 22:00

Note

To avoid overlap between sessions and interference in kill zones, we have adjusted the session timings as follows :

• Asian Session: 23:00 to 06:00

• European Session: 07:00 to 14:25

• New York Session: 14:30 to 22:55

🔵 Kill Zones

Kill zones are parts of a session where trader activity is higher than usual. During these periods, trading volume increases and price fluctuations are more intense.

The timing of the major kill zones based on the UTC time zone is as follows :

• Asian Kill Zone: 23:00 to 03:55

• European Kill Zone: 07:00 to 09:55

• New York Morning Kill Zone: 14:30 to 16:55

• New York Evening Kill Zone: 19:30 to 20:55

This indicator focuses on tracking the kill zone and its range. For example, once a kill zone ends, the high and low formed during it remain unchanged.

If the price reaches the high or low of the kill zone while the session is still active, the corresponding line is not drawn any further. Based on this information, various strategies can be developed, and the most important ones are discussed below.

🟣 How to Use

There are three main ways to trade based on the kill zone :

• Kill Zone Hunt

• Breakout and Pullback to Kill Zone

• Trading in the Trend of the Kill Zone

🔵 Kill Zone Hunt

According to this strategy, once the kill zone ends and its high and low lines no longer change, if the price reaches one of these lines within the same session and is strongly rejected, a trade can be entered.

🔵 Breakout and Pullback to Kill Zone

According to this strategy, once the kill zone ends and its high and low lines no longer change, if the price breaks one of these lines strongly within the same session, a trade can be entered on the pullback to that level.

Trading in the Trend of the Kill Zone

We know that kill zones are areas where high-volume trading occurs and powerful trends form. Therefore, trades can be made in the direction of the trend. For example, when an upward trend dominates this area, you can enter a buy trade when the price reaches a demand order block.

🟣 Features

🔵 Alerts

You can set alerts to be notified when the price hits the high or low lines of the kill zone.

🔵 More Information

By enabling this feature, you can view information such as the time and trading volume within the kill zone. This allows you to compare the trading volume with the same period on the previous day or other kill zones.

🟣 Settings

Through the settings, you have access to the following options :

• Show or hide additional information

• Enable or disable alerts

• Show or hide sessions

• Show or hide kill zones

• Set preferred colors for displaying sessions

• Customize the time range of sessions

• Customize the time range of kill zones

RSI Strategy with Manual TP and SL 19/03/2024This TradingView script implements a simple RSI (Relative Strength Index) strategy with manual take profit (TP) and stop-loss (SL) levels. Let's break down the script and analyze its components:

RSI Calculation: The script calculates the RSI using the specified length parameter. RSI is a momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and typically values above 70 indicate overbought conditions while values below 30 indicate oversold conditions.

Strategy Parameters:

length: Length of the RSI period.

overSold: Threshold for oversold condition.

overBought: Threshold for overbought condition.

trail_profit_pct: Percentage for trailing profit.

Entry Conditions:

For a long position: RSI crosses above 30 and the daily close is above 70% of the highest close in the last 50 bars.

For a short position: RSI crosses below 70 and the daily close is below 130% of the lowest close in the last 50 bars.

Entry Signals:

Long entry is signaled when both conditions for a long position are met.

Short entry is signaled when both conditions for a short position are met.

Manual TP and SL:

Take profit and stop-loss levels are calculated based on the entry price and the specified percentage.

For long positions, the take profit level is set above the entry price and the stop-loss level is set below the entry price.

For short positions, the take profit level is set below the entry price and the stop-loss level is set above the entry price.

Strategy Exits:

Exit conditions are defined for both long and short positions using the calculated take profit and stop-loss levels.

Chart Analysis:

This strategy aims to capitalize on short-term momentum shifts indicated by RSI crossings combined with daily price movements.

It utilizes manual TP and SL levels, providing traders with flexibility in managing their positions.

The strategy may perform well in ranging or oscillating markets where RSI signals are more reliable.

However, it may encounter challenges in trending markets where RSI can remain overbought or oversold for extended periods.

Traders should backtest this strategy thoroughly on historical data and consider optimizing parameters to suit different market conditions.

Risk management is crucial, so traders should carefully adjust TP and SL percentages based on their risk tolerance and market volatility.

Overall, this strategy provides a structured approach to trading based on RSI signals while allowing traders to customize their risk management. However, like any trading strategy, it should be used judiciously and in conjunction with other forms of analysis and risk management techniques.

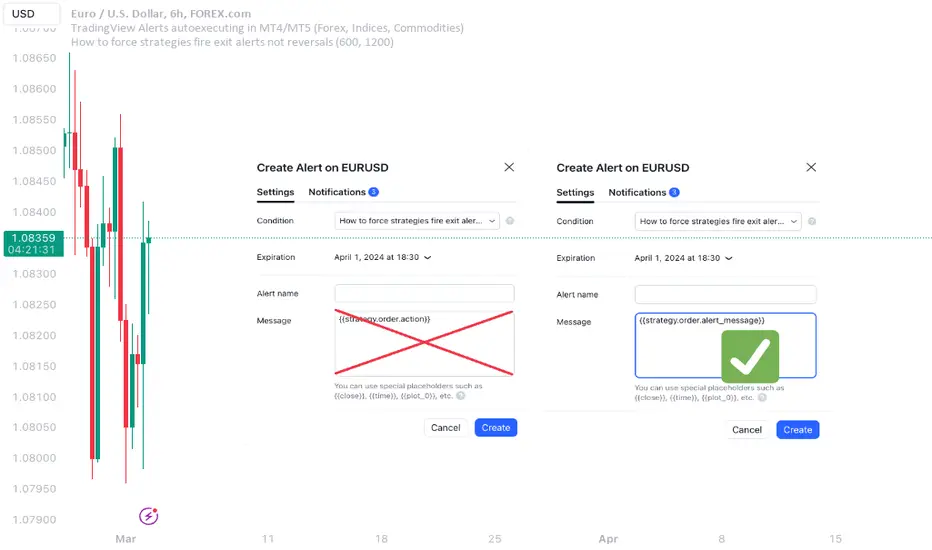

How to force strategies fire exit alerts not reversalsPineScript has gone a long way, from very simple and little-capable scripting language to a robust coding platform with reliable execution endpoints. However, this one small intuitivity glitch is still there and is likely to stay, because it is traditionally justified and quite intuitive for significant group of traders. I'm sharing this workaround in response to frequent inquiries about it.

What's the glitch? When setting alerts on strategies to be synchronized with TradingView's Strategy Tester events, using simple alert messages such as "buy" or "sell" based on entry direction seems straightforward by inserting {{strategy.order.action}} into the Create Alert's "Message" field. Because "buy" or "sell" are exactly the strings produced by {{strategy.order.action}} placeholder. However, complications arise when attempting to EXIT positions without reversing, whether triggered by price levels like Stop Loss or Take Profit, or logical conditions to close trades. Those bricks fall apart, because on such events {{strategy.order.action}} sends the same "sell" for exiting buy positions and "buy" for exiting sell positions, instead of something more differentiating like "closebuy" or "closesell". As a result reversal trades are opened, instead of simply closing the open ones.

This convention harkens back to traditional stock market practices, where traders either bought shares to enter positions or sold them to exit. However, modern trading encompasses diverse instruments like CFDs, indices, and Forex, alongside advanced features such as Stop Loss, reshaping the landscape. Despite these advancements, the traditional nomenclature persists.

And is poised to stay on TradingView as well, so we need a workaround to get a simple strategy going. Luckily it is here and is called alert_message . It is a parameter, which needs to be added into each strategy.entry() / strategy.exit() / strategy.close() function call - each call, which causes Strategy Tester to produce entry or exit orders. As in this example script:

line 12: strategy.entry(... alert_message ="buy")

line 14: strategy.entry(... alert_message ="sell")

line 19: strategy.exit(... alert_message ="closebuy")

line 20: strategy.exit(... alert_message ="closesell")

line 24: strategy.close(... alert_message ="closebuy")

line 26: strategy.close(... alert_message ="closesell")

These alert messages are compatible with the Alerts Syntax of TradingConnector - a tool facilitating auto-execution of TradingView alerts in MetaTrader 4 or 5. Yes, simple alert messages like "buy" / "sell" / "closebuy" / "closesell" suffice to carry the execution of simple strategy, without complex JSON files with multiple ids and such. Other parameters can be added (actually plenty), but they are only option and that's not a part of this story :)

Last thing left to do is to replace "Message" in Create Alert popup with {{strategy.order.alert_message}} . This placeholder transmits the string defined in the PineScript alert_message= parameter, as outlined in this publication. With this workaround, executing closing alerts becomes seamless within PineScript strategies on TradingView.

Disclaimer: this content is purely educational, especially please don't pay attention to backtest results on any timeframe/ticker.

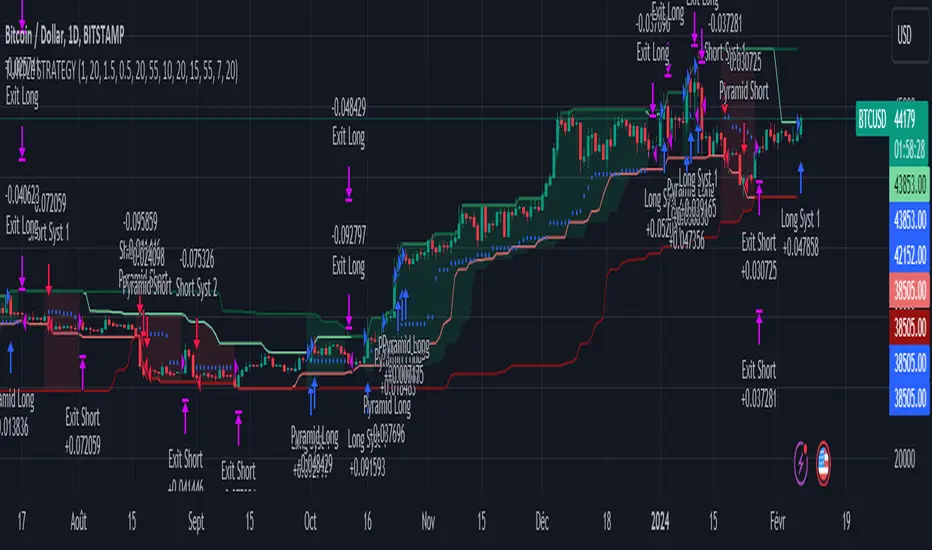

Turtle Trader StrategyTurtle Trader Strategy :

Introduction :

This strategy is based on the well known « Turtle Trader Strategy », that has proven itself over the years. It sends long and short signals with pyramid orders of up to 5, meaning that the strategy can trigger up to 5 orders in the same direction. Good risk and money management.

It's important to note that the strategy combines 2 systems working together (S1 and S2). Let’s describe the specific features of this strategy.

1/ Position size :

Position size is very important for turtle traders to manage risk properly. This position sizing strategy adapts to market volatility and to account (gains and losses). It’s based on ATR (Average True Range) which can also be called « N ». Its length is per default 20.

ATR(20) = (previous_atr(20)*19 + actual_true_range)/20

The number of units to buy is :

Unit = 1% * account/(ATR(20)*dollar_per_point)

where account is the actual account value and dollar_per_point is the variation in dollar of the asset with a 1 point move.

Depending on your risk aversion, you can increase the percentage of your account, but turtle traders default to 1%. If you trade contracts, units must be rounded down by default.

There is also an additional rule to reduce the risk if the value of the account falls below the initial capital : in this case and only in this case, account in the unit formula must be replace by :

account = actual_account*actual_account/initial capital

2/ Open a position :

2 systems are working together :

System 1 : Entering a new 20 day breakout

System 2 : Entering a new 55 day breakout

A breakout is a new high or new low. If it’s a new high, we open long position and vice versa if it’s a new low we enter in short position.

We add an additional rule :

System 1 : Breakout is ignored if last long/short position was a winner

System 2 : All signals are taken

This additional rule allows the trader to be in the major trends if the system 1 signal has been skipped. If a signal for system 1 has been skipped, and next candle is also a new 20 day breakout, S1 doesn’t give a signal. We have to wait S2 signal or wait for a candle that doesn’t make a new breakout to reactivate S1.

3/ Pyramid orders :

Turtle Strategy allows us to add extra units to the position if the price moves in our favor. I've configured the strategy to allow up to 5 orders to be added in the same direction. So if the price varies from 0.5*ATR(20) , we add units with the position size formula. Note that the value of account will be replaced by "remaining_account", i.e. the cash remaining in our account after subtracting the value of open positions.

4/ Stop Loss :

We set a stop loss at 1.5*ATR(20) below the entry price for longs and above the entry price for shorts. If pyramid units are added, the stop is increased/decreased by 0.5*ATR(20). Note that if SL is configured for a loss of more than 10%, we set the SL to 10% for the first entry order to avoid big losses. This configuration does not work for pyramid orders as SL moves by 0.5*ATR(20).

5/ Exit signals :

System 1 :

Exit long on a 10 day low

Exit short on a 10 day high

System 2 :

Exit long on a 20 day low

Exit short on a 20 day high

6/ What types of orders are placed ?

To enter in a position, stop orders are placed meaning that we place orders that will be automatically triggered by the signal at the exact breakout price. Stop loss and exit signals are also stop orders. Pyramid orders are market orders which will be triggered at the opening of the next candle to avoid repainting.

PARAMETERS :

Risk % of capital : Percentage used in the position size formula. Default is 1%

ATR period : ATR length used to calculate ATR. Default is 20

Stop ATR : Parameters used to fix stop loss. Default is 1.5 meaning that stop loss will be set at : buy_price - 1.5*ATR(20) for long and buy_price + 1.5*ATR(20) for short. Turtle traders default is 2 but 1.5 is better for cryptocurrency as there is a huge volatility.

S1 Long : System 1 breakout length for long. Default is 20

S2 Long : System 2 breakout length for long. Default is 55

S1 Long Exit : System 1 breakout length to exit long. Default is 10

S2 Long Exit : System 2 breakout length to exit long. Default is 20

S1 Short : System 1 breakout length for short. Default is 15

S2 Short : System 2 breakout length for short. Default is 55

S1 Short Exit : System 1 breakout length to exit short. Default is 7

S2 Short Exit : System 2 breakout length to exit short. Default is 20

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Pyramiding : Number of orders that can be passed in the same direction. Default is 5.

Important : Turtle traders don't trade crypto. For this specific asset type, I modify some parameters such as SL and Short S1 in order to maximize return while limiting drawdown. This strategy is the most optimal on BINANCE:BTCUSD in 1D timeframe with the parameters set per default. If you want to use this strategy for a different crypto please adapt parameters.

NOTE :

It's important to note that the first entry order (long or short) will be the largest. Subsequent pyramid orders will have fewer units than the first order. We've set a maximum SL for the first order of 10%, meaning that you won't lose more than 10% of the value of your first order. However, it is possible to lose more on your pyramid orders, as the SL is increased/decreased by 0.5*ATR(20), which does not secure a loss of more than 10% on your pyramid orders. The risk remains well managed because the value of these orders is less than the value of the first order. Remain vigilant to this small detail and adjust your risk according to your risk aversion.

Enjoy the strategy and don’t forget to take the trade :)

RSI & Backed-Weighted MA StrategyRSI & MA Strategy :

INTRODUCTION :

This strategy is based on two well-known indicators that work best together: the Relative Strength Index (RSI) and the Moving Average (MA). We're going to use the RSI as a trend-follower indicator, rather than a reversal indicator as most are used to. To the signals sent by the RSI, we'll add a condition on the chart's MA, filtering out irrelevant signals and considerably increasing our winning rate. This is a medium/long-term strategy. There's also a money management method enabling us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RSI :

The RSI is one of the best-known and most widely used indicators in trading. Its purpose is to warn traders when an asset is overbought or oversold. It was designed to send reversal signals, but we're going to use it as a trend indicator by increasing its length to 20. The RSI formula is as follows :

RSI (n) = 100 - (100 / (1 + (H (n)/L (n))))

With n the length of the RSI, H(n) the average of days closing above the open and L(n) the average of days closing below the open.

MA :

The Moving Average is also widely used in technical analysis, to smooth out variations in an asset. The SMA formula is as follows :

SMA (n) = (P1 + P2 + ... + Pn) / n

where n is the length of the MA.

However, an SMA does not weight any of its terms, which means that the price 10 days ago has the same importance as the price 2 days ago or today's price... That's why in this strategy we use a RWMA, i.e. a back-weighted moving average. It weights old prices more heavily than new ones. This will enable us to limit the impact of short-term variations and focus on the trend that was dominating. The RWMA used weights :

The 4 most recent terms by : 100 / (4+(n-4)*1.30)

The other oldest terms by : weight_4_first_term*1.30

So the older terms are weighted 1.30 more than the more recent ones. The moving average thus traces a trend that accentuates past values and limits the noise of short-term variations.

PARAMETERS :

RSI Length : Lenght of RSI. Default is 20.

MA Type : Choice between a SMA or a RWMA which permits to minimize the impact of short term reversal. Default is RWMA.

MA Length : Length of the selected MA. Default is 19.

RSI Long Signal : Minimum value of RSI to send a LONG signal. Default is 60.

RSI Short signal : Maximum value of RSI to send a SHORT signal. Default is 40.

ROC MA Long Signal : Maximum value of Rate of Change MA to send a LONG signal. Default is 0.

ROC MA Short signal : Minimum value of Rate of Change MA to send a SHORT signal. Default is 0.

TP activation in multiple of ATR : Threshold value to trigger trailing stop Take Profit. This threshold is calculated as multiple of the ATR (Average True Range). Default value is 5 meaning that to trigger the trailing TP the price need to move 5*ATR in the right direction.

Trailing TP in percentage : Percentage value of trailing Take Profit. This Trailing TP follows the profit if it increases, remaining selected percentage below it, but stops if the profit decreases. Default is 3%.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. Default is 400, which means that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:ETHUSD with a timeframe set to 6h. Parameters are set as follows :

MA type: RWMA

MA Length: 19

RSI Long Signal: >60

RSI Short Signal : <40

ROC MA Long Signal : <0

ROC MA Short Signal : >0

TP Activation in multiple ATR : 5

Trailing TP in percentage : 3

ENTER RULES :

The principle is very simple:

If the asset is overbought after a bear market, we are LONG.

If the asset is oversold after a bull market, we are SHORT.

We have defined a bear market as follows : Rate of Change (20) RWMA < 0

We have defined a bull market as follows : Rate of Change (20) RWMA > 0

The Rate of Change is calculated using this formula : (RWMA/RWMA(20) - 1)*100

Overbought is defined as follows : RSI > 60

Oversold is defined as follows : RSI < 40

LONG CONDITION :

RSI > 60 and (RWMA/RWMA(20) - 1)*100 < -1

SHORT CONDITION :

RSI < 40 and (RWMA/RWMA(20) - 1)*100 > 1

EXIT RULES FOR WINNING TRADE :

We have a trailing TP allowing us to exit once the price has reached the "TP Activation in multiple ATR" parameter, i.e. 5*ATR by default in the profit direction. TP trailing is triggered at this point, not limiting our gains, and securing our profits at 3% below this trigger threshold.

Remember that the True Range is : maximum(H-L, H-C(1), C-L(1))

with C : Close, H : High, L : Low

The Average True Range is therefore the average of these TRs over a length defined by default in the strategy, i.e. 20.

RISK MANAGEMENT :

This strategy may incur losses. The method for limiting losses is to set a Stop Loss equal to 3*ATR. This means that if the price moves against our position and reaches three times the ATR, we exit with a loss.

Sometimes the ATR can result in a SL set below 10% of the trade value, which is not acceptable. In this case, we set the SL at 10%, limiting losses to a maximum of 10%.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

Enjoy the strategy and don't forget to take the trade :)

Machine Learning: MFI Heat Map [YinYangAlgorithms]Overview:

MFI Heat Maps are a visually appealing way to display the values of 29 different MFIs at the same time while being able to make sense of it. Each plot within the Indicator represents a different MFI value. The higher you get up, the longer the length that was used for this MFI. This Indicator also features the use of Machine Learning to help balance the MFI levels. It doesn’t solely rely upon Machine Learning but instead incorporates a growing length MFI averaged with the Machine Learning MFI at any given index.

For instance, say we are calculating the 10th plot from the bottom, the MFI would be an average of: