Linear % ST | QuantEdgeB🚀 Introducing Linear Percentile SuperTrend (Linear % ST) by QuantEdgeB

🛠️ Overview

Linear % SuperTrend (Linear % ST) by QuantEdgeB is a hybrid trend-following indicator that combines Linear Regression, Percentile Filters, and Volatility-Based SuperTrend Logic into one dynamic tool. This system is designed to identify trend shifts early while filtering out noise during choppy market conditions.

By utilizing percentile-based median smoothing and customized ATR multipliers, this tool captures both breakout momentum and pullback opportunities with precision.

✨ Key Features

🔹 Percentile-Based Median Filtering

Removes outliers and normalizes price movement for cleaner trend detection using the 50th percentile (median) of recent price action.

🔹 Linear Regression Smoothing

A smoothed baseline is computed with Linear Regression to detect the underlying trend while minimizing lag.

🔹 SuperTrend Structure with Adaptive Bands

The indicator implements an enhanced SuperTrend engine with custom ATR bands that adapt to trend direction. Bands tighten or loosen based on volatility and trend strength.

🔹 Dynamic Long/Short Conditions

Long and short signals are derived from the relationship between price and the SuperTrend threshold zones, clearly showing trend direction with optional "Long"/"Short" labels on the chart.

🔹 Multiple Visual Themes

Select from 6 built-in color palettes including Strategy, Solar, Warm, Cool, Classic, and Magic to match your personal style or strategy layout.

📊 How It Works

1️⃣ Percentile Filtering

The source price (default: close) is filtered using a nearest-rank 50th percentile over a custom lookback. This normalizes data to reflect the central tendency and removes noisy extremes.

2️⃣ Linear Regression Trend Base

A Linear Regression Moving Average (LSMA) is applied to the filtered median, forming the core trend line. This dynamic trendline provides a low-lag yet smooth view of market direction.

3️⃣ SuperTrend Engine

ATR is applied with custom multipliers (different for long and short) to create dynamic bands. The bands react to price movement and only shift direction after confirmation, preventing false flips.

4️⃣ Trend Signal Logic

• When price stays above the dynamic lower band → Bullish trend

• When price breaks below the upper band → Bearish trend

• Trend direction remains stable until violated by price.

⚙️ Custom Settings

• Percentile Length → Lookback for percentile smoothing (default: 35)

• LSMA Length → Determines the base trend via linear regression (default: 24)

• ATR Length → ATR period used in dynamic bands (default: 14)

• Long Multiplier → ATR multiplier for bullish thresholds (default: 0.8)

• Short Multiplier → ATR multiplier for bearish thresholds (default: 1.9)

✅ How to Use

1️⃣ Trend-Following Strategy

✔️ Go Long when price breaks above the lower ATR band, initiating an upward trend

✔️ Go Short when price falls below the upper ATR band, confirming bearish conditions

✔️ Remain in trend direction until the SuperTrend flips

2️⃣ Visual Confirmation

✔️ Use bar coloring and the dynamic bands to stay aligned with trend direction

✔️ Optional Long/Short labels highlight key signal flips

👥 Who Should Use Linear % ST?

✅ Swing & Position Traders → To ride trends confidently

✅ Trend Followers → As a primary directional filter

✅ Breakout Traders → For clean signal generation post-range break

✅ Quant/Systematic Traders → Integrate clean trend logic into algorithmic setups

📌 Conclusion

Linear % ST by QuantEdgeB blends percentile smoothing with linear regression and volatility bands to deliver a powerful, adaptive trend-following engine. Whether you're a discretionary trader seeking cleaner entries or a systems-based trader building logic for automation, Linear % ST offers clarity, adaptability, and precision in trend detection.

🔹 Key Takeaways:

1️⃣ Percentile + Regression = Noise-Reduced Core Trend

2️⃣ ATR-Based SuperTrend = Reliable Breakout Confirmation

3️⃣ Flexible Parameters + Color Modes = Custom Fit for Any Strategy

📈 Use it to spot emerging trends, filter false signals, and stay confidently aligned with market momentum.

📌 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

📌 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Cari dalam skrip untuk "豪24配债"

Strategy Stats [presentTrading]Hello! it's another weekend. This tool is a strategy performance analysis tool. Looking at the TradingView community, it seems few creators focus on this aspect. I've intentionally created a shared version. Welcome to share your idea or question on this.

█ Introduction and How it is Different

Strategy Stats is a comprehensive performance analytics framework designed specifically for trading strategies. Unlike standard strategy backtesting tools that simply show cumulative profits, this analytics suite provides real-time, multi-timeframe statistical analysis of your trading performance.

Multi-timeframe analysis: Automatically tracks performance metrics across the most recent time periods (last 7 days, 30 days, 90 days, 1 year, and 4 years)

Advanced statistical measures: Goes beyond basic metrics to include Information Coefficient (IC) and Sortino Ratio

Real-time feedback: Updates performance statistics with each new trade

Visual analytics: Color-coded performance table provides instant visual feedback on strategy health

Integrated risk management: Implements sophisticated take profit mechanisms with 3-step ATR and percentage-based exits

BTCUSD Performance

The table in the upper right corner is a comprehensive performance dashboard showing trading strategy statistics.

Note: While this presentation uses Vegas SuperTrend as the underlying strategy, this is merely an example. The Stats framework can be applied to any trading strategy. The Vegas SuperTrend implementation is included solely to demonstrate how the analytics module integrates with a trading strategy.

⚠️ Timeframe Limitations

Important: TradingView's backtesting engine has a maximum storage limit of 10,000 bars. When using this strategy stats framework on smaller timeframes such as 1-hour or 2-hour charts, you may encounter errors if your backtesting period is too long.

Recommended Timeframe Usage:

Ideal for: 4H, 6H, 8H, Daily charts and above

May cause errors on: 1H, 2H charts spanning multiple years

Not recommended for: Timeframes below 1H with long history

█ Strategy, How it Works: Detailed Explanation

The Strategy Stats framework consists of three primary components: statistical data collection, performance analysis, and visualization.

🔶 Statistical Data Collection

The system maintains several critical data arrays:

equityHistory: Tracks equity curve over time

tradeHistory: Records profit/loss of each trade

predictionSignals: Stores trade direction signals (1 for long, -1 for short)

actualReturns: Records corresponding actual returns from each trade

For each closed trade, the system captures:

float tradePnL = strategy.closedtrades.profit(tradeIndex)

float tradeReturn = strategy.closedtrades.profit_percent(tradeIndex)

int tradeType = entryPrice < exitPrice ? 1 : -1 // Direction

🔶 Performance Metrics Calculation

The framework calculates several key performance metrics:

Information Coefficient (IC):

The correlation between prediction signals and actual returns, measuring forecast skill.

IC = Correlation(predictionSignals, actualReturns)

Where Correlation is the Pearson correlation coefficient:

Correlation(X,Y) = (nΣXY - ΣXY) / √

Sortino Ratio:

Measures risk-adjusted return focusing only on downside risk:

Sortino = (Avg_Return - Risk_Free_Rate) / Downside_Deviation

Where Downside Deviation is:

Downside_Deviation = √

R_i represents individual returns, T is the target return (typically the risk-free rate), and n is the number of observations.

Maximum Drawdown:

Tracks the largest percentage drop from peak to trough:

DD = (Peak_Equity - Trough_Equity) / Peak_Equity * 100

🔶 Time Period Calculation

The system automatically determines the appropriate number of bars to analyze for each timeframe based on the current chart timeframe:

bars_7d = math.max(1, math.round(7 * barsPerDay))

bars_30d = math.max(1, math.round(30 * barsPerDay))

bars_90d = math.max(1, math.round(90 * barsPerDay))

bars_365d = math.max(1, math.round(365 * barsPerDay))

bars_4y = math.max(1, math.round(365 * 4 * barsPerDay))

Where barsPerDay is calculated based on the chart timeframe:

barsPerDay = timeframe.isintraday ?

24 * 60 / math.max(1, (timeframe.in_seconds() / 60)) :

timeframe.isdaily ? 1 :

timeframe.isweekly ? 1/7 :

timeframe.ismonthly ? 1/30 : 0.01

🔶 Visual Representation

The system presents performance data in a color-coded table with intuitive visual indicators:

Green: Excellent performance

Lime: Good performance

Gray: Neutral performance

Orange: Mediocre performance

Red: Poor performance

█ Trade Direction

The Strategy Stats framework supports three trading directions:

Long Only: Only takes long positions when entry conditions are met

Short Only: Only takes short positions when entry conditions are met

Both: Takes both long and short positions depending on market conditions

█ Usage

To effectively use the Strategy Stats framework:

Apply to existing strategies: Add the performance tracking code to any strategy to gain advanced analytics

Monitor multiple timeframes: Use the multi-timeframe analysis to identify performance trends

Evaluate strategy health: Review IC and Sortino ratios to assess predictive power and risk-adjusted returns

Optimize parameters: Use performance data to refine strategy parameters

Compare strategies: Apply the framework to multiple strategies to identify the most effective approach

For best results, allow the strategy to generate sufficient trade history for meaningful statistical analysis (at least 20-30 trades).

█ Default Settings

The default settings have been carefully calibrated for cryptocurrency markets:

Performance Tracking:

Time periods: 7D, 30D, 90D, 1Y, 4Y

Statistical measures: Return, Win%, MaxDD, IC, Sortino Ratio

IC color thresholds: >0.3 (green), >0.1 (lime), <-0.1 (orange), <-0.3 (red)

Sortino color thresholds: >1.0 (green), >0.5 (lime), <0 (red)

Multi-Step Take Profit:

ATR multipliers: 2.618, 5.0, 10.0

Percentage levels: 3%, 8%, 17%

Short multiplier: 1.5x (makes short take profits more aggressive)

Stop loss: 20%

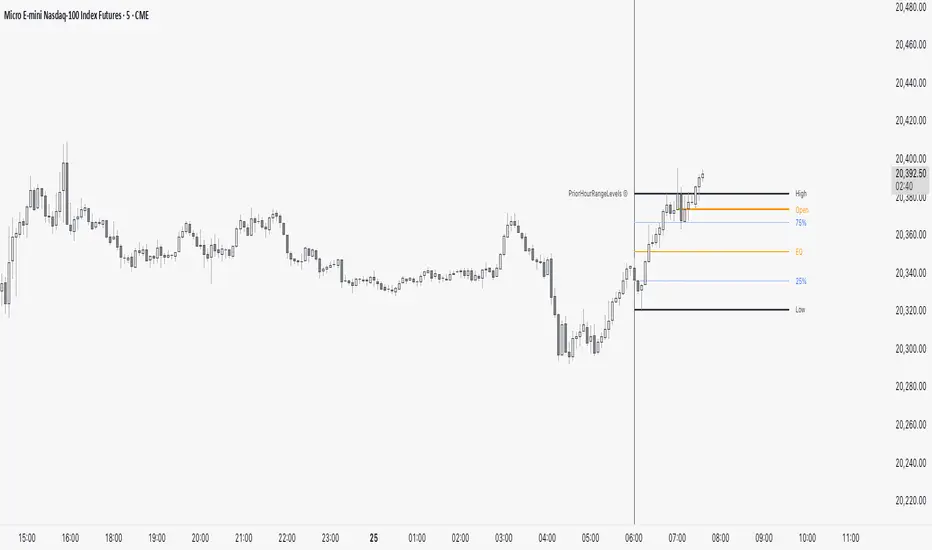

PriorHourRangeLevels_v0.1PriorHourRangeLevels_v0.1

Created by dc_77 | © 2025 | Mozilla Public License 2.0

Overview

"PriorHourRangeLevels_v0.1" is a versatile Pine Script™ indicator designed to help traders visualize and analyze price levels based on the prior hour’s range. It overlays key levels—High, Low, 75%, 50% (EQ), and 25%—from the previous hour onto the current price chart, alongside the current hour’s opening price. With customizable display options and time zone support, it’s ideal for intraday traders looking to identify support, resistance, and breakout zones.

How It Works

Hourly Reset: The indicator detects the start of each hour based on your chosen time zone (e.g., "America/New_York" by default).

Prior Hour Range: It calculates the High and Low of the previous hour, then derives three additional levels:

75%: 75% of the range above the Low.

EQ (50%): The midpoint of the range.

25%: 25% of the range above the Low.

Current Hour Open: Displays the opening price of the current hour.

Projection: Lines extend forward (default: 24 bars) to project these levels into the future, aiding in real-time analysis.

Alerts: Triggers alerts when the price crosses any of the prior hour’s levels (High, 75%, EQ, 25%, Low).

Key Features

Time Zone Flexibility: Choose from options like UTC, New York, Tokyo, or London to align with your trading session.

Visual Customization:

Toggle visibility for each level (High, Low, 75%, EQ, 25%, Open, and Anchor).

Adjust line styles (Solid, Dashed, Dotted), colors, and widths.

Show or hide labels with adjustable sizes (Tiny, Small, Normal, Large).

Anchor Line: A vertical line marks the start of the prior hour, with optional labeling.

Alert Conditions: Set up notifications for price crossings to catch key moments without watching the chart.

Usage Tips

Use the High and Low as potential breakout levels, while 75%, EQ, and 25% act as intermediate support/resistance zones.

Trend Confirmation: Watch how price interacts with the EQ (50%) level to gauge momentum.

Session Planning: Adjust the time zone to match your market (e.g., "Europe/London" for FTSE trading).

Projection Offset: Extend or shorten the lines (via "Projection Offset") based on your chart timeframe.

Inputs

Time Zone: Select your preferred market time zone.

Anchor Settings: Show/hide the prior hour start line, style, color, width, and label.

Level Settings: Customize visibility, style, color, width, and labels for Open, High, 75%, EQ, 25%, and Low.

Display: Set projection length and label size.

Golden Death Cross IndicatorThis indicator uses moving average to detect both a Golden Cross and Death Cross on any timeframe but is recommended for use on the daily and 24 hour timeframes only.

We have also provided instructions on how to create alerts for these indicators below.

Happy Trading!

Moving Averages: We’ll use Simple Moving Averages (SMA). The 50-day SMA looks at the average price over the last 50 periods, and the 200-day SMA does the same for 200 periods.

Crossovers: We’ll check when the 50-day SMA crosses above (Golden Cross) or below the 200-day SMA (Death Cross).

Set Up Alerts

Now, let’s make sure you get notified when a cross happens:

Open the Alerts Menu

On the chart, click the bell icon (top right of the screen) to create an alert.

Configure the Golden Cross Alert

In the “Condition” dropdown, select “Cross Alerts” (the name of your script).

Below that, select “Golden Cross.”

Set “Once Per Bar Close” in the next dropdown (this ensures it only triggers after the period ends, avoiding false signals mid-bar).

Choose how you want to be notified (e.g., popup, email, or phone app—set this under “Notifications”).

Name the alert (e.g., “Golden Cross Alert”) and click “Create.”

Configure the Death Cross Alert

Click the bell icon again to create a second alert.

Condition: “Cross Alerts” > “Death Cross.”

Set “Once Per Bar Close” again.

Choose your notification method.

Name it (e.g., “Death Cross Alert”) and click “Create.”

Rolling Pivot PointsThe "Rolling Pivot Points" indicator, built in Pine Script (version 6) for TradingView, overlays dynamic pivot levels on a price chart. It calculates a 24-hour lookback period (length = 1440 / (timeframe.in_seconds() / 60)) using the prior period’s high, low, and close to determine a Pivot Point (vPP) and three resistance (vR1, vR2, vR3) and support (vS1, vS2, vS3) levels. Plotted lines include vPP (yellow), vR1 (red), and vS1 (blue) in a cross style, with a customizable reset time (default: 8 AM) to refresh levels daily.

The indicator updates at the specified resetTime (minute = 0), otherwise retaining prior levels, making it ideal for intraday traders. The averageDays input (default: 5) is present but unclear in function. Suited for identifying key price zones, it adapts across timeframes, offering a concise, color-coded tool for technical analysis on TradingView.

ADX + DMI (HMA Version)📝 Description (What This Indicator Does)

🚀 ADX + DMI (HMA Version) is a trend strength oscillator that enhances the traditional ADX by using the Hull Moving Average (HMA) instead of EMA.

✅ This results in a much faster and more responsive trend detection while filtering out choppy price action.

🎯 What This Indicator Does:

1️⃣ Measures Trend Strength – ADX shows when a trend is strong or weak.

2️⃣ Identifies Trend Direction – DI+ (Green) shows bullish momentum, DI- (Red) shows bearish momentum.

3️⃣ Uses Hull Moving Average (HMA) for Faster Signals – Removes lag and reacts faster to trend changes.

4️⃣ Reduces False Signals – Traditional ADX lags behind, but this version reacts quickly to reversals.

5️⃣ Good for Scalping & Day Trading – Especially for BTC 5-min and lower timeframes.

⚙ Indicator Inputs (Customization)

Input Name Example Value Purpose

ADX Length 14 Defines the smoothing for the ADX value.

DI Length 14 Defines how DI+ and DI- are calculated.

HMA Length 24 Hull Moving Average smoothing for ADX & DI+.

Trend Threshold 25 The level above which ADX confirms a strong trend.

📌 You can adjust these settings to optimize for different assets and timeframes.

🎯 Trading Rules & How to Use It

✅ How to Identify a Strong Trend:

When ADX (Blue Line) is above 25→ A strong trend is in play.

When ADX is below 25 → The market is choppy or ranging.

✅ How to Use DI+ and DI- for Trend Direction:

If DI+ (Green) is above DI- (Red), the market is in an uptrend.

If DI- (Red) is above DI+ (Green), the market is in a downtrend.

✅ How to Confirm Entries & Exits:

1️⃣ Enter Long when DI+ crosses above DI- while ADX is rising above 25.

2️⃣ Enter Short when DI- crosses above DI+ while ADX is rising above 25.

3️⃣ Avoid trading when ADX is below 25 – the market is in a choppy range.

This should not be used as a stand alone oscillator. Trading takes skill and is risky. Use at your own risk.

This is not advise on how to trade, these are just examples of how I use the oscillator. Trade at your own risk.

You can put this on your chart versus the tradingview adx and you can adjust the settings to see the difference. This was optimized for btc on the 5 min chart. You can adjust for your trading strategy.

New York Open LinesThis indicator marks key New York trading session opens on the chart. It draws horizontal lines at the New York Midnight Open (00:00 NY time) and the New York Economic Open (08:30 NY time) prices.

Key Features:

1) Customizable Line Styles & Colors:

* Users can choose between solid, dotted, or dashed lines.

* Colors are customizable for each open level.

2) Timeframe-Based Logic:

* For timeframes above 30 minutes:

- It retrieves the midnight (NYMO) and 8:30 AM (ETO) open prices using request.security_lower_tf().

- The script ensures the price is stored only once per day.

* For 30-minute timeframes and below:

- The script draws lines at the exact open prices as bars appear.

3) Line Management:

* The lines extend for 24 hours from the open.

* The previous day's lines are removed to keep the chart clean.

4) Session Reset:

* At the start of a new trading day, the stored NYMO and ETO prices reset to na to prepare for the next session.

This helps traders quickly identify key New York session levels, often used for support, resistance, and breakout trading strategies.

Custom TABI Model with LayersCustom Top and Bottom Indicator (TABI) (Is a Trend Adaptive Blow-Off Indicator) -

User Guide & Description

Introduction

The TABI (Trend Adaptive Blow-Off Indicator) is a refined, multi-layered RSI tool designed to enhance trend analysis, detect momentum shifts, and highlight overbought/oversold conditions with a more nuanced, color-coded approach. This indicator is useful for traders seeking to identify key reversal points, confirm trend strength, and filter trade setups more effectively than traditional RSI.

By incorporating volume-based confirmation and divergence detection, TABI aims to reduce false signals and improve trade timing.

How It Works

TABI builds on the Relative Strength Index (RSI) by introducing:

A smoothed RSI calculation for better trend readability.

11 color-coded RSI levels, allowing traders to visually distinguish weak, neutral, and extreme conditions.

Volume-based confirmation to detect high-conviction moves.

Bearish & Bullish Divergence Detection, inspired by Market Cipher methods, to spot potential reversals early.

Overbought & Oversold alerts, with optional candlestick color changes to highlight trade signals.

Key Features

✅ Color-Coded RSI for Better Readability

The RSI is divided into multi-layered color zones:

🔵 Light Blue: Extremely oversold

🟢 Lime Green: Mild oversold, potential trend reversal

🟡 Yellow & Orange: Neutral, momentum consolidation

🟠 Dark Orange: Caution, overbought conditions developing

🔴 Red: Extreme overbought, possible exhaustion

✅ Divergence Detection

Bearish Divergence: Price makes higher highs, RSI makes lower highs → Potential top signal

Bullish Divergence: Price makes lower lows, RSI makes higher lows → Potential bottom signal

✅ Volume Confirmation Filter

Requires a 50% above-average volume spike for strong buy/sell signals, reducing false breakouts.

✅ Dynamic Labels & Alerts

🚨 Blow-Off Top Warning: If RSI is overbought + volume spikes + divergence detected

🟢 Oversold Bottom Alert: If RSI is oversold + bullish divergence

Candlestick color changes when extreme conditions are met.

How to Use

📌 Entry & Exit Signals

Buy Consideration:

RSI enters Green Zone (oversold)

Bullish divergence detected

Volume confirms the move

Sell Consideration:

RSI enters Red Zone (overbought)

Bearish divergence detected

Volume confirms exhaustion

📌 Trend Confirmation

Use the yellow/orange levels to confirm strong trends before entering counter-trend trades.

📌 Filtering Trade Noise

The RSI smoothing helps reduce false whipsaws, making it easier to read true momentum shifts.

Customization Options

🔧 User-Defined RSI Thresholds

Adjust the overbought/oversold levels to match your trading style.

🔧 Divergence Sensitivity

Modify the lookback period to fine-tune divergence detection accuracy.

🔧 Volume Thresholds

Set custom volume multipliers to control confirmation requirements.

Why This is Unique

🔹 Unlike traditional RSI, TABI visually maps RSI zones into layered gradients, making it easy to spot momentum shifts.

🔹 The multi-layered color scheme adds an intuitive, heatmap-like effect to RSI, helping traders quickly gauge conditions.

🔹 Incorporates CCF-inspired divergence detection and volume filtering, making signals more robust.

🔹 Dynamic labeling system ensures clarity without cluttering the chart.

Alerts & Notifications

🔔 TradingView Alerts Included

🚨 Blow-Off Top Detected → RSI overbought + volume spike + bearish divergence.

🟢 Oversold Bottom Detected → RSI oversold + bullish divergence.

Set alerts to receive notifications without watching the charts 24/7.

Final Thoughts

TABI is designed to simplify RSI analysis, provide better trade signals, and improve decision-making. Whether you're day trading, swing trading, or long-term investing, this tool helps you navigate market conditions with confidence.

🔥 Use it to detect high-probability reversals, confirm trends, and improve trade entries/exits! 🚀

Opening Lines (M15, H1 & H4) with Wickless Candle DetectorTailored for day traders, this technical analysis indicator serves as a multi-timeframe opening price visualization tool, displaying real-time and historical opening price levels across three distinct time intervals to enhance pattern identification and strategic decision-making. Additionally, the tool incorporates a ‘Wickless Candle Detector’ feature, which annotates candles that open without upper or lower wicks. Empirical observations suggest these wickless candles often act as future price magnets, particularly in index futures such as the Nasdaq and S&P500, making them critical reference points for market analysis.

Key Features:

1) Multi-Timeframe Opening Price Visualization:

◦ Plots horizontal reference lines for opening prices across:

✓ 15-minute (M15)

✓ 1-hour (H1)

✓ 4-hour (H4) timeframes

◦ Lines dynamically extend throughout their respective periods or can be configured to a fixed bar offset

2) Wickless Candle Detection:

◦ Automatically marks wickless candles with a discrete symbol at their opening price level

◦ Symbols are removed upon either:

✓ Price breaching the opening level by ≥1 tick

✓ A 24-hour expiration period (whichever occurs first)

3) Customization and Flexibility:

◦ Toggle visibility for individual timeframes, historical opening lines, and the Wickless Candle Detector

◦ Full customization of visual elements (colors, line styles, symbols) to align with user preferences or trading platform themes

TEMA OBOS Strategy PakunTEMA OBOS Strategy

Overview

This strategy combines a trend-following approach using the Triple Exponential Moving Average (TEMA) with Overbought/Oversold (OBOS) indicator filtering.

By utilizing TEMA crossovers to determine trend direction and OBOS as a filter, it aims to improve entry precision.

This strategy can be applied to markets such as Forex, Stocks, and Crypto, and is particularly designed for mid-term timeframes (5-minute to 1-hour charts).

Strategy Objectives

Identify trend direction using TEMA

Use OBOS to filter out overbought/oversold conditions

Implement ATR-based dynamic risk management

Key Features

1. Trend Analysis Using TEMA

Uses crossover of short-term EMA (ema3) and long-term EMA (ema4) to determine entries.

ema4 acts as the primary trend filter.

2. Overbought/Oversold (OBOS) Filtering

Long Entry Condition: up > down (bullish trend confirmed)

Short Entry Condition: up < down (bearish trend confirmed)

Reduces unnecessary trades by filtering extreme market conditions.

3. ATR-Based Take Profit (TP) & Stop Loss (SL)

Adjustable ATR multiplier for TP/SL

Default settings:

TP = ATR × 5

SL = ATR × 2

Fully customizable risk parameters.

4. Customizable Parameters

TEMA Length (for trend calculation)

OBOS Length (for overbought/oversold detection)

Take Profit Multiplier

Stop Loss Multiplier

EMA Display (Enable/Disable TEMA lines)

Bar Color Change (Enable/Disable candle coloring)

Trading Rules

Long Entry (Buy Entry)

ema3 crosses above ema4 (Golden Cross)

OBOS indicator confirms up > down (bullish trend)

Execute a buy position

Short Entry (Sell Entry)

ema3 crosses below ema4 (Death Cross)

OBOS indicator confirms up < down (bearish trend)

Execute a sell position

Take Profit (TP)

Entry Price + (ATR × TP Multiplier) (Default: 5)

Stop Loss (SL)

Entry Price - (ATR × SL Multiplier) (Default: 2)

TP/SL settings are fully customizable to fine-tune risk management.

Risk Management Parameters

This strategy emphasizes proper position sizing and risk control to balance risk and return.

Trading Parameters & Considerations

Initial Account Balance: $7,000 (adjustable)

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 128

Deep Test Results (2024/11/01 - 2025/02/24)BTCUSD-5M

Total P&L:+1638.20USD

Max equity drawdown:694.78USD

Total trades:128

Profitable trades:44.53

Profit factor:1.45

These settings aim to protect capital while maintaining a balanced risk-reward approach.

Visual Support

TEMA Lines (Three EMAs)

Trend direction is indicated by color changes (Blue/Orange)

ema3 (short-term) and ema4 (long-term) crossover signals potential entries

OBOS Histogram

Green → Strong buying pressure

Red → Strong selling pressure

Blue → Possible trend reversal

Entry & Exit Markers

Blue Arrow → Long Entry Signal

Red Arrow → Short Entry Signal

Take Profit / Stop Loss levels displayed

Strategy Improvements & Uniqueness

This strategy is based on indicators developed by "l_lonthoff" and "jdmonto0", but has been significantly optimized for better entry accuracy, visual clarity, and risk management.

Enhanced Trend Identification with TEMA

Detects early trend reversals using ema3 & ema4 crossover

Reduces market noise for a smoother trend-following approach

Improved OBOS Filtering

Prevents excessive trading

Reduces unnecessary risk exposure

Dynamic Risk Management with ATR-Based TP/SL

Not a fixed value → TP/SL adjusts to market volatility

Fully customizable ATR multiplier settings

(Default: TP = ATR × 5, SL = ATR × 2)

Summary

The TEMA + OBOS Strategy is a simple yet powerful trading method that integrates trend analysis and oscillators.

TEMA for trend identification

OBOS for noise reduction & overbought/oversold filtering

ATR-based TP/SL settings for dynamic risk management

Before using this strategy, ensure thorough backtesting and demo trading to fine-tune parameters according to your trading style.

ALN Sessions - for NQ2/24/25 - v1

This script does not calculate any stats.

It uses the sessions and stats from NQStats/ALNSessions

Option to draw boxes around the session times.

Options to adjust the table text/background colors/position.

The logic will determine how the Asia and London sessions interact.

Once the New York session starts (8am), it will then display the appropriate stats.

Script quirk...fyi. The script removes the stats table at 6PM.

That's just how it works. I used grok to assist with the code, and it got funky. It works, so I left it that way.

The appropriate stats table will then be displayed when the next New York session begins.

---

There is another table I used just for troubleshooting to show the values of the Asia/London session highs/lows. This can just be ignored.

3/3/25 - republished.

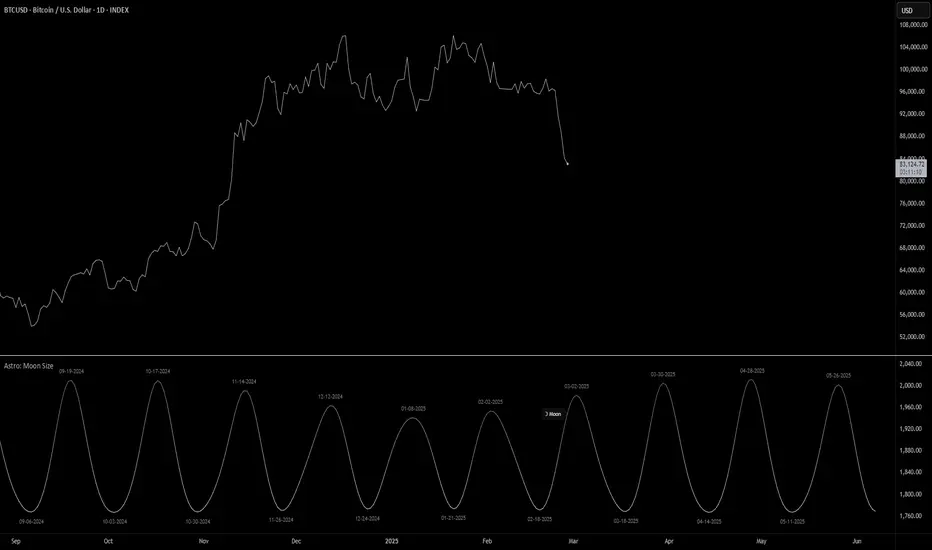

Astro: Moon SizeThe Astro: Moon Size indicator, built using AstroLib , calculates the distance and visualizes the apparent size of the Moon based on astronomical positioning. This script is tailored for the 1D timeframe and provides insights into lunar perigees (closest approach) and apogees (farthest distance), making it useful for astrologically-informed trading strategies.

New Astro Indicators Feature:

By setting the Julian Date to X number of days in the future, and offsetting the plot by X number of bars accordingly, it is now possible to visualize future projections of TradingView indicators that reference the AstroLib . This feature has been long requested and is far overdue, so thank you to everyone who pushed for this feature release. Enjoy, time travelers from the future!!

Key Features:

Moon Size Calculation: Uses Julian Date (J2000) conversion and AstroLib functions to determine the Moon's apparent distance.

Future Projection: Displays the Moon's distance from 28 up to 500 days ahead, with color gradients indicating proximity/size.

Pivot Identification: Marks local maxima (apogees) and minima (perigees) with labeled date stamps for easy reference.

Dynamic Labeling: Adapts label positioning and size based on the Moon's current trend and relative size.

Usage Notes:

⚠️ Timeframe Restriction: For now, the script only functions on the 1D timeframe and will prompt an error otherwise.

⚠️ Asset Restriction: This script is meant to be loaded on charts for assets that trade 24/7, like BTCUSD historical index.

PRC-ALMA | QuantEdgeBIntroducing PRC-ALMA by QuantEdgeB

Overview

The PRC-ALMA (Percentile Adaptive ALMA) is an advanced dynamic trend and volatility filtering indicator that leverages the Arnaud Legoux Moving Average (ALMA) combined with Percentile Rank Filtering and Median Absolute Deviation (MAD) Bands. It is designed to enhance market structure clarity, detect breakout zones, and provide trade signals by dynamically adjusting its filtering based on recent price action.

____

Key Features

1. 📈 Adaptive ALMA Smoothing:

- Uses ALMA for smoothing price action while reducing lag.

- Provides a more responsive moving average than traditional EMAs and SMAs.

2. 📊 Percentile Rank-Based Thresholds:

- Determines upper and lower regions using 75th and 25th percentile ranks.

- Allows for adaptive thresholding based on historical price movements.

3. 🎯 Median Absolute Deviation (MAD) Volatility Filtering:

- Filters out noise using robust statistical deviation measures.

- MAD Bands dynamically adjust based on volatility expansion and contraction.

4. 🔄 Dynamic Trade Signals:

- Generates long signals when price exceeds the upper threshold.

- Generates short signals when price drops below the lower threshold.

5. 🎨 Customizable Color Modes & Visual Enhancements:

- Choose between multiple color schemes to match trading preferences.

- Optional candlestick coloring to indicate market sentiment shifts.

____

How It Works

1. ALMA Calculation:

- The indicator starts by computing the ALMA (Arnaud Legoux Moving Average) with a customizable length, offset, and sigma.

2. Percentile Rank Filtering:

- It then calculates the 75th and 25th percentile ranks over a selected period, determining dynamic levels for trend identification.

3. Volatility Adjustment Using Median Absolute Deviation (MAD):

- MAD is applied to filter noise and adapt the upper/lower bands based on market volatility.

- The higher the MAD multiplier, the wider the bands, allowing more price fluctuations before a signal triggers.

4. Entry & Exit Conditions:

- Long Entry: When price crosses above the upper percentile band + MAD filter.

- Short Entry: When price crosses below the lower percentile band - MAD filter.

5. Visual Enhancements:

- Dynamic band plotting with shading between percentile ranks.

- Candlestick coloring to visually indicate long/short sentiment shifts.

____

Practical Applications

✅ Trend Following & Momentum Trading – Uses ALMA for trend smoothing and percentile-based breakouts.

✅ Mean Reversion Strategies – Adaptive MAD filtering ensures only significant deviations trigger signals.

✅ Multi-Timeframe Trading – Works on intraday, daily, and weekly timeframes based on user customization.

✅ Noise Reduction – Eliminates minor fluctuations while capturing meaningful market moves.

____

🛠 Settings

-ALMA Length: 24 – Defines the smoothing period for the Arnaud Legoux Moving Average.

-ALMA Offset: 0.7 – Adjusts the shift factor, controlling responsiveness.

-ALMA Sigma: 4 – Determines the smoothing strength, balancing trend-following and noise reduction.

-Percentile Length: 21 – Lookback period for calculating percentile rank levels.

-Median Period: 21 – The period used for the Median Absolute Deviation (MAD) filter.

-Median Multiplier: 1.8 – Adjusts the sensitivity of the MAD filter, impacting how signals are generated.

-Color Mode: Strategy – Various visual themes available for better chart readability.

-Signal Label: Off - If turned off the indicator produced a Long or Cash signal when the trend changes.

📌 Conclusion

The PRC-ALMA | QuantEdgeB is an advanced valuation and signal generation tool that dynamically adjusts based on market conditions. By combining ALMA for trend smoothing, percentile rank thresholds, and MAD-based volatility filtering, it provides traders with a versatile indicator for momentum, breakout, and mean reversion strategies.

Key Takeaways:

✔ Smooth & Adaptive – ALMA ensures minimal lag while maintaining trend responsiveness.

✔ Dynamic Overbought/Oversold Zones – Adjusts to real-time market conditions using percentile-based bands.

✔ Volatility-Aware Filtering – Uses MAD to eliminate market noise, making signals more reliable.

✔ Customizable & Multi-Timeframe Ready – Works on various asset classes and timeframes with adjustable settings.

🔹 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Crypto Scanner v4This guide explains a version 6 Pine Script that scans a user-provided list of cryptocurrency tokens to identify high probability tradable opportunities using several technical indicators. The script combines trend, momentum, and volume-based analyses to generate potential buying or selling signals, and it displays the results in a neatly formatted table with alerts for trading setups. Below is a detailed walkthrough of the script’s design, how traders can interpret its outputs, and recommendations for optimizing indicator inputs across different timeframes.

## Overview and Key Components

The script is designed to help traders assess multiple tokens by calculating several indicators for each one. The key components include:

- **Input Settings:**

- A comma-separated list of symbols to scan.

- Adjustable parameters for technical indicators such as ADX, RSI, MFI, and a custom Wave Trend indicator.

- Options to enable alerts and set update frequencies.

- **Indicator Calculations:**

- **ADX (Average Directional Index):** Measures trend strength. A value above the provided threshold indicates a strong trend, which is essential for validating momentum before entering a trade.

- **RSI (Relative Strength Index):** Helps determine overbought or oversold conditions. When the RSI is below the oversold level, it may present a buying opportunity, while an overbought condition (not explicitly part of this setup) could suggest selling.

- **MFI (Money Flow Index):** Similar in concept to RSI but incorporates volume, thus assessing buying and selling pressure. Values below the designated oversold threshold indicate potential undervaluation.

- **Wave Trend:** A custom indicator that calculates two components (WT1 and WT2); a crossover where WT1 moves from below to above WT2 (particularly near oversold levels) may signal a reversal and a potential entry point.

- **Scanning and Trading Zone:**

- The script identifies a *bullish setup* when the following conditions are met for a token:

- ADX exceeds the threshold (strong trend).

- Both RSI and MFI are below their oversold levels (indicating potential buying opportunities).

- A Wave Trend crossover confirms near-term reversal dynamics.

- A *trading zone* condition is also defined by specific ranges for ADX, RSI, MFI, and a limited difference between WT1 and WT2. This zone suggests that the token might be in a consolidation phase where even small moves may be significant.

- **Alerts and Table Reporting:**

- A table is generated, with each row corresponding to a token. The table contains columns for the symbol, ADX, RSI, MFI, WT1, WT2, and the trading zone status.

- Visual cues—such as different background colors—highlight tokens with a bullish setup or that are within the trading zone.

- Alerts are issued based on the detection of a bullish setup or entry into a trading zone. These alerts are limited per bar to avoid flooding the trader with notifications.

## How to Interpret the Indicator Outputs

Traders should use the indicator values as guidance, verifying them against their own analysis before making any trading decision. Here’s how to assess each output:

- **ADX:**

- **High values (above threshold):** Indicate strong trends. If other indicators confirm an oversold condition, a trader may consider a long position for a corrective reversal.

- **Low values:** Suggest that the market is not trending strongly, and caution should be taken when considering entry.

- **RSI and MFI:**

- **Below oversold levels:** These conditions are traditionally seen as signals that an asset is undervalued, potentially triggering a bounce.

- **Above typical resistance levels (not explicitly used here):** Would normally caution a trader against entering a long position.

- **Wave Trend (WT1 and WT2):**

- A crossover where WT1 moves upward above WT2 in an oversold environment can signal the beginning of a recovery or reversal, thereby reinforcing buy signals.

- **Trading Zone:**

- Being “in zone” means that the asset’s current values for ADX, RSI, MFI, and the closeness of the Wave Trend lines indicate a period of consolidation. This scenario might be suitable for both short-term scalping or as an early exit indicator, depending on further market analysis.

## Timeframe Optimization Input Table

Traders can optimize indicator inputs depending on the timeframe they use. The following table provides a set of recommended input values for various timeframes. These values are suggestions and should be adjusted based on market conditions and individual trading styles.

Timeframe ADX RSI MFI ADX RSI MFI WT Channel WT Average

5-min 10 10 10 20 30 20 7 15

15-min 12 12 12 22 30 20 9 18

1-hour 14 14 14 25 30 20 10 21

4-hour 16 16 16 27 30 20 12 24

1-day 18 18 18 30 30 20 14 28

Adjust these parameters directly in the script’s input settings to match the selected timeframe. For shorter timeframes (e.g., 5-min or 15-min), the shorter lengths help filter high-frequency noise. For longer timeframes (e.g., 1-day), longer input values may reduce false signals and capture more significant trends.

## Best Practices and Usage Tips

- **Token Limit:**

- Limit the number of tokens scanned to 10 per query line. If you need to scan more tokens, initiate a new query line. This helps manage screen real estate and ensures the table remains legible.

- **Confirming Signals:**

- Use this script as a starting point for identifying high potential trades. Each indicator’s output should be used to confirm your trading decision. Always cross-reference with additional technical analysis tools or market context.

- **Regular Review:**

- Since the script updates the table every few bars (as defined by the update frequency), review the table and alerts regularly. Market conditions change rapidly, so timely decisions are crucial.

## Conclusion

This Pine Script provides a comprehensive approach for scanning multiple cryptocurrencies using a combination of trend strength (ADX), momentum (RSI and MFI), and reversal signals (Wave Trend). By using the provided recommendation table for different timeframes and limiting the tokens to 20 per query line (with a maximum of four query lines), traders can streamline their scanning process and more effectively identify high probability tradable tokens. Ultimately, the outputs should be critically evaluated and combined with additional market research before executing any trades.

Timeframe Display + Countdown📘 Help Guide: Timeframe Display + Countdown + Alert

🔹 Overview

This indicator displays:

✅ The selected timeframe (e.g., 5min, 1H, 4H)

✅ A countdown timer showing minutes and seconds until the current candle closes

✅ An optional alert that plays a sound when 1 minute remains before the new candle starts

⚙️ How to Use

1️⃣ Add the Indicator

• Open TradingView

• Click on Pine Script Editor

• Copy and paste the script

• Click Add to Chart

2️⃣ Customize Settings

• Text Color: Choose a color for the displayed text

• Text Size: Adjust the font size (8–24)

• Transparency: Set how transparent the text is (0%–100%)

• Position: Choose where the text appears (Top Left, Top Right, Bottom Left, Bottom Right)

• Enable Audible Alert: Turn ON/OFF the alert when 1 minute remains

3️⃣ Set Up an Audible Alert in TradingView

🚨 Important: Pine Script cannot play sounds directly; you must set up a manual alert in TradingView.

Steps:

1. Click “Alerts” (🔔 icon in TradingView)

2. Click “Create Alert” (+ button)

3. In “Condition”, select this indicator (Timeframe Display + Countdown)

4. Under “Options”, choose:

• Trigger: “Once Per Bar”

• Expiration: Set a valid time range

• Alert Actions: Check “Play Sound” and choose a sound

5. Click “Create” ✅

🛠️ How It Works

• Countdown Timer:

• Updates in real time, displaying MM:SS until the candle closes

• Resets when a new candle starts

• Alert Trigger:

• When 1:00 minute remains, an alert is sent

• If properly configured in TradingView, it plays a sound

IB of New Hour (Customizable)Purpose: Tracks first x candles of each hour to define a price range

Customizable settings:

Border color of the IB box

Fill color of the IB box

Number of candles to define IB

Box width in hours (1-24)

Functionality:

Calculates highest high and lowest low for specified number of candles

Creates a rectangular box representing the initial balance

Adapts to different timeframes (1, 5, 15, 30, 60-minute charts)

Limits storage of boxes to prevent memory overload

Box Placement:

Starts at first candle of the hour

Width calculated based on current timeframe and user-specified hours

Maintains consistent visual representation across different chart timeframes

Indicator for helping you with bias

Hourly Market Movement Pattern Indicator# Hourly Market Movement Pattern Indicator

This versatile technical analysis tool identifies the most active hours for trading by analyzing historical price movements. While it can be viewed on any timeframe chart, the indicator specifically tracks and displays which hours of the day historically show the strongest upward or downward price movements, helping traders optimize their trading schedule around these recurring hourly patterns.

## Core Features

- Tracks the best performing hours for both upward and downward movements

- Viewable on any timeframe chart while maintaining hourly analysis

- Clear visual display through a color-coded table overlay

- Real-time updates with new market data

- Works with all trading instruments (stocks, crypto, forex, futures, etc.)

## Timeframe Applications

### Chart Viewing Options

- Can be viewed on any timeframe chart (1min to Monthly)

- Maintains hourly pattern analysis regardless of chart timeframe

- Helps correlate hourly patterns with your preferred trading timeframe

- Allows detailed visualization of hourly patterns within your analysis period

### Intraday Trading

- Identify the most profitable hours for trading

- Plan trading sessions around historically strong hours

- Optimize entry and exit timing based on hourly patterns

- Structure day trading schedules around peak movement hours

### Swing Trading

- Use hourly statistics to optimize entry/exit timing

- Plan trade executions during historically strong hours

- Time position entries based on hourly success rates

- Enhance swing trading decisions with hourly pattern data

## Practical Applications

### Pattern Recognition

- Track recurring hourly market movements

- Identify institutional trading hour patterns

- Detect regular market cycle hours

- Recognize changes in hourly market behavior

### Risk Management

- Adjust position sizing based on historical hourly patterns

- Plan entries during statistically favorable hours

- Time stop loss adjustments around known volatile hours

- Scale positions according to hourly success rates

### Trade Planning

- Schedule trading sessions during optimal hours

- Plan trade executions around strong movement periods

- Structure trading day around peak hours

- Time position adjustments to favorable hours

## Setup Options

- Timeframe: View on any chart timeframe while tracking hourly patterns

- Visual Display: Non-intrusive table overlay

- Color Coding: Green for upward movements, Red for downward movements

- Hour Display: 24-hour format for global market compatibility

## Trading Strategy Integration

The indicator enhances trading approaches through:

- Optimal hour identification for trade execution

- Historical hourly pattern analysis

- Day trading session optimization

- Position timing based on hourly statistics

## Notes

This indicator proves particularly valuable for:

- Traders seeking to optimize their daily trading schedule

- Day traders focusing on peak market hours

- Swing traders optimizing entry/exit timing

- Traders adapting strategies to specific market hours

- International traders tracking hour-specific patterns across sessions

The tool's hourly pattern analysis provides crucial timing information regardless of your preferred chart timeframe or trading style, helping optimize trade execution around the most statistically favorable hours of the day.

Thrax - Pullback based short side scalping⯁ This indicator is built for short trades only.

⤞ Pullback based scalping is a strategy where a trader anticipates a pullback and makes a quick scalp in this pullback. This strategy usually works in a ranging market as probability of pullbacks occurrence in ranging market is quite high.

⤞ The strategy is built by first determining a possible candidate price levels having high chance of pullbacks. This is determined by finding out multiple rejection point and creating a zone around this price. A rejection is considered to be valid only if it comes to this zone after going down by a minimum pullback percentage. Once the price has gone down by this minimum pullback percentage multiple times and reaches the zone again chances of pullback goes high and an indication on chart for the same is given.

⯁ Inputs

⤞ Zone-Top : This input parameter determines the upper range for the price zone.

⤞ Zone bottom : This input parameter determines the lower range for price zone.

⤞ Minimum Pullback : This input parameter determines the minimum pullback percentage required for valid rejection. Below is the recommended settings

⤞ Lookback : lookback period before resetting all the variables

⬦Below is the recommended settings across timeframes

⤞ 15-min : lookback – 24, Pullback – 2, Zone Top Size %– 0.4, Zone Bottom Size % – 0.2

⤞ 5-min : lookback – 50, pullback – 1% - 1.5%, Zone Top Size %– 0.4, Zone Bottom Size % – 0.2

⤞ 1-min : lookback – 100, pullback – 1%, Zone Top Size %– 0.4, Zone Bottom Size % – 0.2

⤞ Anything > 30-min : lookback – 11, pullback – 3%, Zone Top Size %– 0.4, Zone Bottom Size % – 0.2

✵ This indicator gives early pullback detection which can be used in below ways

1. To take short trades in the pullback.

2. To use this to exit an existing position in the next few candles as pullback may be incoming.

📌 Kindly note, it’s not necessary that pullback will happen at the exact point given on the chart. Instead, the indictor gives you early signals for the pullback

⯁ Trade Steup

1. Wait for pullback signal to occur on the chart.

2. Once the pullback warning has been displayed on the chart, you can either straight away enter the short position or wait for next 2-4 candles for initial sign of actual pullback to occurrence.

3. Once you have initiated short trade, since this is pullback-based strategy, a quick scalp should be made and closed as price may resume it’s original direction. If you have risk appetite you can stay in the trade longer and trial the stops if price keeps pulling back.

4. You can zone top as your stop, usually zone top + some% should be used as stop where ‘some %’ is based on your risk appetite.

5. It’s important to note that this indicator gives early sings of pullback so you may actually wait for 2-3 candles post ‘Pullback warning’ occurs on the chart before entering short trade.

Time-Based VWAP (TVWAP)(TVWAP) Indicator

The Time-Based Volume Weighted Average Price (TVWAP) indicator is a customized version of VWAP designed for intraday trading sessions with defined start and end times. Unlike the traditional VWAP, which calculates the volume-weighted average price over an entire trading day, this indicator allows you to focus on specific time periods, such as ICT kill zones (e.g., London Open, New York Open, Power Hour). It helps crypto scalpers and advanced traders identify price deviations relative to volume during key trading windows.

Key Features:

Custom Time Interval:

You can set the exact start and end times for the VWAP calculation using input settings for hours and minutes (24-hour format).

Ideal for analyzing short, high-liquidity periods.

Dynamic Accumulation of Price and Volume:

The indicator resets at the beginning of the specified session and accumulates price-volume data until the end of the session.

Ensures that the TVWAP reflects the weighted average price specific to the chosen session.

Visual Representation:

The indicator plots the TVWAP line only during the specified time window, providing a clear visual reference for price action during that period.

Outside the session, the TVWAP line is hidden (na).

Use Cases:

ICT Scalp Trading:

Monitor price rebalances or potential liquidity sweeps near TVWAP during important trading sessions.

Mean Reversion Strategies:

Detect pullbacks toward the session’s average price for potential entry points.

Breakout Confirmation:

Confirm price direction relative to TVWAP during kill zones or high-volume times to determine if a breakout is supported by volume.

Inputs:

Start Hour/Minute: The time when the TVWAP calculation starts.

End Hour/Minute: The time when the TVWAP calculation ends.

Technical Explanation:

The indicator uses the timestamp function to create time markers for the session start and end.

During the session, the price-volume (close * volume) is accumulated along with the total volume.

TVWAP is calculated as:

TVWAP = (Sum of (Price × Volume)) ÷ (Sum of Volume)

Once the session ends, the TVWAP resets for the next trading period.

Customization Ideas:

Alerts: Add notifications when the price touches or deviates significantly from TVWAP.

Different Colors: Use different line colors based on upward or downward trends.

Multiple Sessions: Add support for multiple TVWAP lines for different time periods (e.g., London + New York).

Comprehensive Trading Toolkit [BigBeluga]Trading Toolkit is a comprehensive indicator inspired by the trading strategies of the renowned crypto influencer Michaël van de Poppe . This tool combines RSI divergences, correction zones, and advanced support/resistance levels to provide traders with a robust framework for analyzing market movements.

🔵 Key Features:

RSI Divergences on Chart:

Automatically identifies and plots RSI divergences (bullish and bearish) directly on the main price chart.

Green lines indicate bullish divergences, suggesting potential upward reversals.

Red lines indicate bearish divergences, signaling possible downward movements.

Correction Boxes:

Traders typically define a correction as a drop in value of 10% or more. This drop can happen over a few hours or a few days. Also, it can last for less than 24 hours or many months.

This indicator visualizes corrections with blue shaded boxes, triggered by a percentage decline defined in the settings.

The boxes highlight sharp price drops, helping traders identify significant market movements quickly.

Advanced Support and Resistance Levels:

Dynamically detects key support and resistance levels based on price pivots.

When the price is above a level, it plots a green shaded area from the cross point, marking support.

When the price drops below a level, it plots a red shaded area, highlighting resistance.

Dashed lines indicate weaker levels, while solid lines represent stronger, more reliable levels.

🔵 Usage:

Identify Divergences: Use plotted RSI divergences to detect potential market reversals and align them with price action.

Analyze Correction Zones: Utilize correction boxes to evaluate significant price declines and find potential buying opportunities during these corrections.

Leverage Support and Resistance Levels: Confirm breakouts, reversals, or consolidation zones with the color-coded areas.

Enhance Risk Management: Combine divergences and correction zones to set informed stop-loss or take-profit levels.

Trading Toolkit empowers traders with actionable insights into market trends, corrections, and support/resistance dynamics, making it an invaluable tool for crypto and forex markets.

Volatility IndicatorThe volatility indicator presented here is based on multiple volatility indices that reflect the market’s expectation of future price fluctuations across different asset classes, including equities, commodities, and currencies. These indices serve as valuable tools for traders and analysts seeking to anticipate potential market movements, as volatility is a key factor influencing asset prices and market dynamics (Bollerslev, 1986).

Volatility, defined as the magnitude of price changes, is often regarded as a measure of market uncertainty or risk. Financial markets exhibit periods of heightened volatility that may precede significant price movements, whether upward or downward (Christoffersen, 1998). The indicator presented in this script tracks several key volatility indices, including the VIX (S&P 500), GVZ (Gold), OVX (Crude Oil), and others, to help identify periods of increased uncertainty that could signal potential market turning points.

Volatility Indices and Their Relevance

Volatility indices like the VIX are considered “fear gauges” as they reflect the market’s expectation of future volatility derived from the pricing of options. A rising VIX typically signals increasing investor uncertainty and fear, which often precedes market corrections or significant price movements. In contrast, a falling VIX may suggest complacency or confidence in continued market stability (Whaley, 2000).

The other volatility indices incorporated in the indicator script, such as the GVZ (Gold Volatility Index) and OVX (Oil Volatility Index), capture the market’s perception of volatility in specific asset classes. For instance, GVZ reflects market expectations for volatility in the gold market, which can be influenced by factors such as geopolitical instability, inflation expectations, and changes in investor sentiment toward safe-haven assets. Similarly, OVX tracks the implied volatility of crude oil options, which is a crucial factor for predicting price movements in energy markets, often driven by geopolitical events, OPEC decisions, and supply-demand imbalances (Pindyck, 2004).

Using the Indicator to Identify Market Movements

The volatility indicator alerts traders when specific volatility indices exceed a defined threshold, which may signal a change in market sentiment or an upcoming price movement. These thresholds, set by the user, are typically based on historical levels of volatility that have preceded significant market changes. When a volatility index exceeds this threshold, it suggests that market participants expect greater uncertainty, which often correlates with increased price volatility and the possibility of a trend reversal.

For example, if the VIX exceeds a pre-determined level (e.g., 30), it could indicate that investors are anticipating heightened volatility in the equity markets, potentially signaling a downturn or correction in the broader market. On the other hand, if the OVX rises significantly, it could point to an upcoming sharp movement in crude oil prices, driven by changing market expectations about supply, demand, or geopolitical risks (Geman, 2005).

Practical Application

To effectively use this volatility indicator in market analysis, traders should monitor the alert signals generated when any of the volatility indices surpass their thresholds. This can be used to identify periods of market uncertainty or potential market turning points across different sectors, including equities, commodities, and currencies. The indicator can help traders prepare for increased price movements, adjust their risk management strategies, or even take advantage of anticipated price swings through options trading or volatility-based strategies (Black & Scholes, 1973).

Traders may also use this indicator in conjunction with other technical analysis tools to validate the potential for significant market movements. For example, if the VIX exceeds its threshold and the market is simultaneously approaching a critical technical support or resistance level, the trader might consider entering a position that capitalizes on the anticipated price breakout or reversal.

Conclusion

This volatility indicator is a robust tool for identifying market conditions that are conducive to significant price movements. By tracking the behavior of key volatility indices, traders can gain insights into the market’s expectations of future price fluctuations, enabling them to make more informed decisions regarding market entries and exits. Understanding and monitoring volatility can be particularly valuable during times of heightened uncertainty, as changes in volatility often precede substantial shifts in market direction (French et al., 1987).

References

• Bollerslev, T. (1986). Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics, 31(3), 307-327.

• Christoffersen, P. F. (1998). Evaluating Interval Forecasts. International Economic Review, 39(4), 841-862.

• Whaley, R. E. (2000). Derivatives on Market Volatility. Journal of Derivatives, 7(4), 71-82.

• Pindyck, R. S. (2004). Volatility and the Pricing of Commodity Derivatives. Journal of Futures Markets, 24(11), 973-987.

• Geman, H. (2005). Commodities and Commodity Derivatives: Modeling and Pricing for Agriculturals, Metals and Energy. John Wiley & Sons.

• Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637-654.

• French, K. R., Schwert, G. W., & Stambaugh, R. F. (1987). Expected Stock Returns and Volatility. Journal of Financial Economics, 19(1), 3-29.

Anchored Geometric Brownian Motion Projections w/EVAnchored GBM (Geometric Brownian Motion) Projections + EV & Confidence Bands

Version: Pine Script v6

Overlay: Yes

Author:

Published On:

Overview

The Anchored GBM Projections + EV & Confidence Bands indicator leverages the Geometric Brownian Motion (GBM) model to project future price movements based on historical data. By simulating multiple potential future price paths, it provides traders with insights into possible price trajectories, their expected values, and confidence intervals. Additionally, it offers a "Mean of EV" (EV of EV) line, representing the running average of expected values across the projection period.

Key Features

Anchor Time Setup:

Define a specific point in time from which the projections commence.

By default, it uses the current bar's timestamp but can be customized.

Projection Parameters:

Projection Candles (Bars): Determines the number of future bars (time periods) to project.

Number of Simulations: Specifies how many GBM paths to simulate, ensuring statistical relevance via the Central Limit Theorem (CLT).

Display Toggles:

Simulation Lines: Visual representation of individual GBM simulation paths.

Expected Value (EV) Line: The average price across all simulations at each projection bar.

Upper & Lower Confidence Bands: 95% confidence intervals indicating potential price boundaries.

EV of EV Line: Running average of EV values, providing a smoothed central tendency across the projection period. Additionally, this line often acts as an indicator of trend direction.

Visualization:

Clear and distinguishable lines with customizable colors and styles.

Overlayed on the price chart for direct comparison with actual price movements.

Mathematical Foundation

Geometric Brownian Motion (GBM):

Definition: GBM is a continuous-time stochastic process used to model stock prices. It assumes that the logarithm of the stock price follows a Brownian motion with drift.

Equation:

S(t)=S0⋅e(μ−12σ2)t+σW(t)

S(t)=S0⋅e(μ−21σ2)t+σW(t) Where:

S(t)S(t) = Stock price at time tt

S0S0 = Initial stock price

μμ = Drift coefficient (average return)

σσ = Volatility coefficient (standard deviation of returns)

W(t)W(t) = Wiener process (standard Brownian motion)

Drift (μμ) and Volatility (σσ):

Drift (μμ) represents the expected return of the stock.

Volatility (σσ) measures the stock's price fluctuation intensity.

Central Limit Theorem (CLT):

Principle: With a sufficiently large number of independent simulations, the distribution of the sample mean (EV) approaches a normal distribution, regardless of the underlying distribution.

Application: Ensures that the EV and confidence bands are statistically reliable.

Expected Value (EV) and Confidence Bands:

EV: The mean price across all simulations at each projection bar.

Confidence Bands: Range within which the actual price is expected to lie with a specified probability (e.g., 95%).

EV of EV (Mean of Sample Means):

Definition: Represents the running average of EV values across the projection period, offering a smoothed central tendency.

Methodology

Anchor Time Setup:

The indicator starts projecting from a user-defined Anchor Time. If not customized, it defaults to the current bar's timestamp.

Purpose: Allows users to analyze projections from a specific historical point or the latest market data.

Calculating Drift and Volatility:

Returns Calculation: Computes the logarithmic returns from the Anchor Time to the current bar.

returns=ln(StSt−1)

returns=ln(St−1St)

Drift (μμ): Calculated as the simple moving average (SMA) of returns over the period since the Anchor Time.

Volatility (σσ): Determined using the standard deviation (stdev) of returns over the same period.

Simulation Generation:

Number of Simulations: The user defines how many GBM paths to simulate (e.g., 30).

Projection Candles: Determines the number of future bars to project (e.g., 12).

Process:

For each simulation:

Start from the current close price.

For each projection bar:

Generate a random number zz from a standard normal distribution.

Calculate the next price using the GBM formula:

St+1=St⋅e(μ−12σ2)+σz

St+1=St⋅e(μ−21σ2)+σz

Store the projected price in an array.

Expected Value (EV) and Confidence Bands Calculation:

EV Path: At each projection bar, compute the mean of all simulated prices.

Variance and Standard Deviation: Calculate the variance and standard deviation of simulated prices to determine the confidence intervals.

Confidence Bands: Using the standard normal z-score (1.96 for 95% confidence), establish upper and lower bounds:

Upper Band=EV+z⋅σEV

Upper Band=EV+z⋅σEV

Lower Band=EV−z⋅σEV

Lower Band=EV−z⋅σEV

EV of EV (Running Average of EV Values):

Calculation: For each projection bar, compute the average of all EV values up to that bar.

EV of EV =1j+1∑k=0jEV

EV of EV =j+11k=0∑jEV

Visualization: Plotted as a dynamic line reflecting the evolving average EV across the projection period.

Visualization Elements

Simulation Lines:

Appearance: Semi-transparent blue lines representing individual GBM simulation paths.

Purpose: Illustrate a range of possible future price trajectories based on current drift and volatility.

Expected Value (EV) Line:

Appearance: Solid orange line.

Purpose: Shows the average projected price at each future bar across all simulations.

Confidence Bands:

Upper Band: Dashed green line indicating the upper 95% confidence boundary.

Lower Band: Dashed red line indicating the lower 95% confidence boundary.

Purpose: Highlight the range within which the price is statistically expected to remain with 95% confidence.

EV of EV Line:

Appearance: Dashed purple line.

Purpose: Displays the running average of EV values, providing a smoothed trend of the central tendency across the projection period. As the mean of sample means it approximates the population mean (i.e. the trend since the anchor point.)

Current Price:

Appearance: Semi-transparent white line.

Purpose: Serves as a reference point for comparing actual price movements against projected paths.

Usage Instructions

Configuring User Inputs:

Anchor Time:

Set to a specific timestamp to start projections from a historical point or leave it as default to use the current bar's time.

Projection Candles (Bars):

Define the number of future bars to project (e.g., 12). Adjust based on your trading timeframe and analysis needs.

Number of Simulations:

Specify the number of GBM paths to simulate (e.g., 30). Higher numbers yield more accurate EV and confidence bands but may impact performance.

Display Toggles:

Show Simulation Lines: Toggle to display or hide individual GBM simulation paths.

Show Expected Value Line: Toggle to display or hide the EV path.

Show Upper Confidence Band: Toggle to display or hide the upper confidence boundary.

Show Lower Confidence Band: Toggle to display or hide the lower confidence boundary.

Show EV of EV Line: Toggle to display or hide the running average of EV values.

Managing TradingView's Object Limits:

Understanding Limits:

TradingView imposes a limit on the number of graphical objects (e.g., lines) that can be rendered. High values for projection candles and simulations can quickly consume these limits. TradingView appears to only allow a total of 55 candles to be projected, so if you want to see two complete lines, you would have to set the projection length to 27: since 27 * 2 = 54 and 54 < 55.

Optimizing Performance:

Use Toggles: Enable only the necessary visual elements. For instance, disable simulation lines and confidence bands when focusing on the EV and EV of EV lines. You can also use the maximum projection length of 55 with the lower limit confidence band as the only line, visualizing a long horizon for your risk.

Adjust Parameters: Lower the number of projection candles or simulations to stay within object limits without compromising essential insights.

Interpreting the Indicator:

Simulation Lines (Blue):

Represent individual potential future price paths based on GBM. A wider spread indicates higher volatility.

Expected Value (EV) Line (Goldenrod):

Shows the mean projected price at each future bar, providing a central trend.

Confidence Bands (Green & Red):

Indicate the statistical range (95% confidence) within which the price is expected to remain.

EV of EV Line (Dotted Line - Goldenrod):

Reflects the running average of EV values, offering a smoothed perspective of expected price trends over the projection period.

Current Price (White):

Serves as a benchmark for assessing how actual prices compare to projected paths.

Practical Applications

Risk Management:

Confidence Bands: Help in identifying potential support and resistance levels based on statistical confidence intervals.

EV Path: Assists in setting realistic target prices and stop-loss levels aligned with projected expectations.

Trend Analysis:

EV of EV Line: Offers a smoothed trendline, aiding in identifying overarching market directions amidst price volatility. Indicative of the population mean/overall trend of the data since your anchor point.

Scenario Planning:

Simulation Lines: Enable traders to visualize multiple potential outcomes, fostering better decision-making under uncertainty.

Performance Evaluation:

Comparing Actual vs. Projected Prices: Assess how actual price movements align with projected scenarios, refining trading strategies over time.

Mathematical and Statistical Insights

Simulation Integrity:

Independence: Each simulation path is generated independently, ensuring unbiased and diverse projections.

Randomness: Utilizes a Gaussian random number generator to introduce variability in diffusion terms, mimicking real market randomness.

Statistical Reliability:

Central Limit Theorem (CLT): By simulating a sufficient number of paths (e.g., 30), the sample mean (EV) converges to the population mean, ensuring reliable EV and confidence band calculations.

Variance Calculation: Accurate computation of variance from simulation data ensures precise confidence intervals.

Dynamic Projections:

Running Average (EV of EV): Provides a cumulative perspective, allowing traders to observe how the average expectation evolves as the projection progresses.

Customization and Enhancements

Adjustable Parameters:

Tailor the projection length and simulation count to match your trading style and analysis depth.

Visual Customization:

Modify line colors, styles, and transparency to enhance clarity and fit chart aesthetics.

Extended Statistical Metrics:

Future iterations can incorporate additional metrics like median projections, skewness, or alternative confidence intervals.

Dynamic Recalculation:

Implement logic to automatically update projections as new data becomes available, ensuring real-time relevance.

Performance Considerations

Object Count Management:

High simulation counts and extended projection periods can lead to a significant number of graphical objects, potentially slowing down chart performance.

Solution: Utilize display toggles effectively and optimize projection parameters to balance detail with performance.

Computational Efficiency:

The script employs efficient array handling and conditional plotting to minimize unnecessary computations and object creation.

Conclusion

The Anchored GBM Projections + EV & Confidence Bands indicator is a robust tool for traders seeking to forecast potential future price movements using statistical models. By integrating Geometric Brownian Motion simulations with expected value calculations and confidence intervals, it offers a comprehensive view of possible market scenarios. The addition of the "EV of EV" line further enhances analytical depth by providing a running average of expected values, aiding in trend identification and strategic decision-making.

Hope it helps!

TAPDA Hourly Open Lines (Candle Body Box)-What is TAPDA?

TAPDA (Time and Price Displacement Analysis) is based on the belief that markets are driven by algorithms that respond to key time-based price levels, such as session opens. Traders who follow TAPDA track these levels to anticipate price movements, reversals, and breakouts, aligning their strategies with the patterns left by these underlying algorithms. By plotting lines at specific hourly opens, the indicator allows traders to visualize where the market may react, providing a structured way to trade alongside the algorithmic flow.

***************

**Sauce Alert** "TAPDA levels essentially act like algorithmic support and resistance" By plotting these hourly opens, the TAPDA Hourly Open Lines indicator helps traders track where algorithms might engage with the market.

***************

-How It Works:

The indicator draws a "candle body box" at selected hours, marking the open and close prices to highlight price ranges at significant times. This creates dynamic zones that reflect market sentiment and structure throughout the day. TAPDA levels are commonly respected by price, making them useful for identifying potential entry points, stop placements, and trend reversals.

-Key Features:

Customizable Hour Levels – Enable or disable specific times to fit your trading approach.

Color & Label Control – Assign unique colors and labels to each hour for better visualization.

Line Extension – Project lines for up to 24 hours into the future to track key levels.

Dynamic Cleanup – Old lines automatically delete to maintain chart clarity.

Manual Time Offset – Adjust for broker or server time zone differences.

-Current Development:

This indicator is still in development, with further updates planned to enhance functionality and customization. If you find this script helpful, feel free to copy the code and stay tuned for new features and improvements!