AdaptivePNLLibrary "Adaptive Profit And Loss"

Provide Take profit and Stop loss values depending on source.

TakeProfitPriceTypes()

Provides supported Take profit sources

Returns: Supported Take profit sources

StopLossPriceTypes()

Provides supported Take profit sources

Returns: Supported Take profit sources

Price(type)

Get price value by selected price type

Parameters:

type (string) : price type from @TakeProfitPriceTypes() or @StopLossPriceTypes()

Returns: Required price value.

LinearProfit(initPerc, stepPerc)

Lineary changed profit

Parameters:

initPerc (float) : Initial profit value in percent unit

stepPerc (float) : Amount of change per every bar since last entry. Posiitive value will decrease profit in time.

Returns: Profit value lineary increased/decreased since last entry. If there is no opened trade, value is NaN

AdaptedProfit(initPerc, stepPerc, source)

Profit adapted to lowest/highest value of given source and lineary changes after it

Parameters:

initPerc (float) : Initial profit value in percent unit

stepPerc (float) : Amount of change per every bar since last entry. Posiitive value will decrease profit in time.

source (float) : Source according to is profit adapted. If it reach high, profit is increased for long positions, same for low and short positions.

Returns: Profit value lineary increased/decreased and adjusted since last entry. If there is no active trade, value is NaN

LinearStopLoss(initPerc, stepPerc)

Lineary changed stop loss

Parameters:

initPerc (float) : Initial stop loss value in percent unit

stepPerc (float) : Amount of change per every bar since last entry. Posiitive value will increase stop loss in time.

Returns: Stop loss value lineary increased/decreased since last entry. If there is no opened trade, value is NaN

AdaptedStopLoss(initPerc, stepPerc, source)

Stop loss adapted to highest/lowest value of given source and lineary changes after it

Parameters:

initPerc (float) : Initial stop loss value in percent unit

stepPerc (float) : Amount of change per every bar since last entry. Posiitive value will increase stop loss in time.

source (float) : Source according to is stop loss adapted. If it reach high, stop loss is increased for long positions, same for low and short positions.

Returns: Stop loss value lineary increased/decreased and adjusted since last entry. If there is no active trade, value is NaN

Strategies

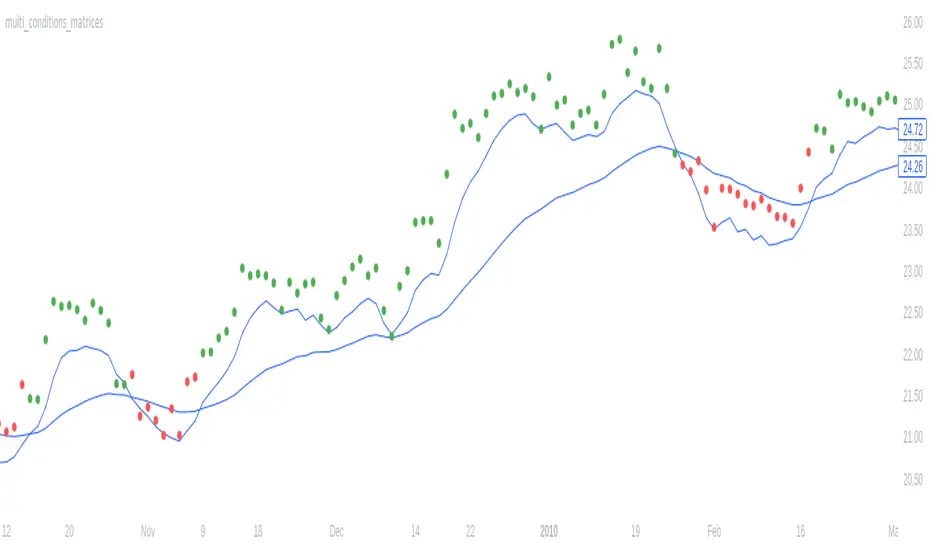

Multi conditions matricesLibrary "multi_conditions_matrices"

: facilitate including multiple AND / OR conditions to a script such as two entry / exit inputs groups.

method addConditions(conditions, conditionPair)

Helper to append conditions to a matrix condition array

Namespace types: matrix

Parameters:

conditions (matrix)

conditionPair (array) : array A condition pair , an input can be passed directly to enable

method check(conditions, operatorAnd)

check several condition within given operator

Namespace types: matrix

Parameters:

conditions (matrix)

operatorAnd (bool) : bool true if the operator between condition is AND (default OR)

Returns: bool Evaluates conditions

isWeekend()

isNightSignal(nightHour, morningHour, timezone)

Parameters:

nightHour (int)

morningHour (int)

timezone (string)

lib_risk_managementLibrary "lib_risk_management"

a lib to help with dynamic position sizing

position_size(risk, account_balance, entry_price, sl_price)

calculate the position size required to meet the account size based risk given when the stop loss is triggered

Parameters:

risk (float) : percentage of account balance to risk (1-100)

account_balance (float) : account balance in instrument currency

entry_price (float) : entry price

sl_price (float) : stop loss price

Returns: the position size in instrument currency that will loose the given risk percentage of the account balance when a stop loss is triggered

account_balance(to_currency, live)

converts the (current(default)/initial) account balance to the given currency at the daily rate

Parameters:

to_currency (simple string) The currency in which the account balance is to be converted. Possible values: a three-letter string with the currency code in the ISO 4217 format (e.g. "USD"), or one of the built-in variables that return currency codes, like syminfo.currency or currency.USD.

live (bool) converts the current account balance (strategy.equity) (default:true) or otherwise the initial capital (strategy.initial_capital)

Returns: the (current/initial) account balance converted to the given currency with at the current daily rate

simpletradeLibrary "simpletrade"

Library with Simple Trade types and tracking mechanism

method evaluate(this)

Evaluate current trade and update status

Namespace types: SimpleTrade

Parameters:

this (SimpleTrade) : SimpleTrade object that need to be evaluated

Returns: current SimpleTrade object

method erase(this)

Erase SimpleTrade drawings

Namespace types: SimpleTrade

Parameters:

this (SimpleTrade) : SimpleTrade object that needs to be erased

Returns: void

method draw(this, offset, gap)

Draw SimpleTrade drawings

Namespace types: SimpleTrade

Parameters:

this (SimpleTrade) : SimpleTrade object that needs to be drawn

offset (int) : offset distance at which the drawing needs to be drawn.

gap (int) : gap between start and end of the Simple trade drawings

Returns: updated offset

TradeDrawing

Object containing Trade drawings

Fields:

entryToStop (series box) : box showing entry to stop range

entryToTarget (series box) : box showing entry to target range

maxGain (series box) : box highlighting max gain of the Trade

maxLoss (series box) : box highlighting max lowss of the Trade

invalidationLine (series line) : line displaying trade invalidation price

invalidationLabel (series label) : label displaying trade invalidation price

stopLabel (series label) : label displaying trade stop price

entryLabel (series label) : label displaying trade entry price

targetLabel (series label) : label displaying trade target price

patternLabel (series label) : label displaying trade pattern details

SimpleTrade

Object containing Simple trade details for tracking

Fields:

id (series int) : Unique trade id

pid (series int) : parent id for trade. Multiple trades can have single parent id

dir (series int) : trade direction

tradeName (series string) : Trade name or description

tradeColor (series color) : color in which the trade needs to be drawn

entry (series float) : trade entry price

stop (series float) : trade stop price

invalidation (series float) : trade invalidation price

target (series float) : trade target price

maxGainPrice (series float) : price at which the trade attained max gain

maxLossPrice (series float) : price at which the trade attained max loss

drawing (TradeDrawing) : TradeDrawing object contianing drawing items

status (series int) : current status of the trade

maxStatus (series int) : max status attained by the trade

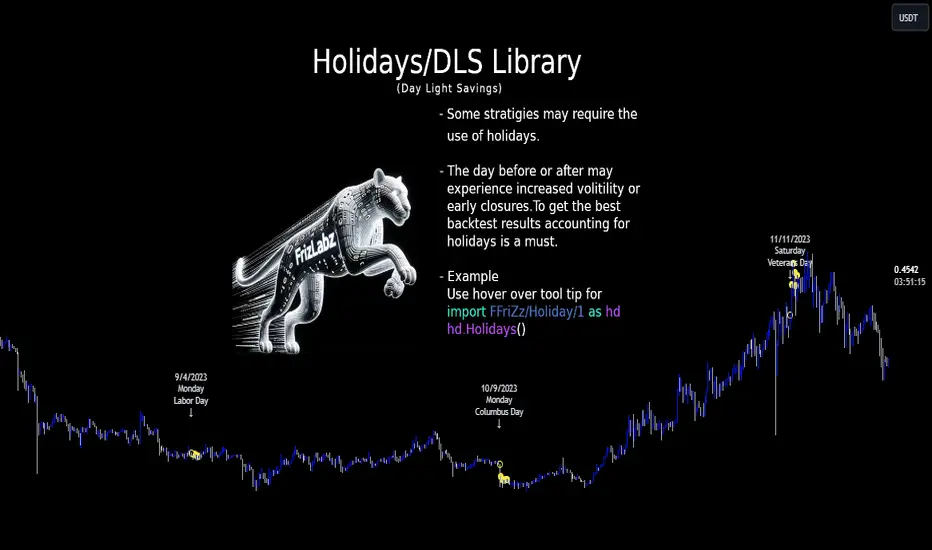

HolidayLibrary "Holiday"

- Full Control over Holidays and Daylight Savings Time (DLS)

The Holiday Library is an essential tool for traders and analysts who engage in backtesting and live trading . This comprehensive library enables the incorporation of crucial calendar elements - specifically Daylight Savings Time (DLS) adjustments and public holidays - into trading strategies and backtesting environments.

Key Features:

- DLS Adjustments: The library takes into account the shifts in time due to Daylight Savings. This feature is particularly vital for backtesting strategies, as DLS can impact trading hours, which in turn affects the volatility and liquidity in the market. Accurate DLS adjustments ensure that backtesting scenarios are as close to real-life conditions as possible.

- Comprehensive Holiday Metadata: The library includes a rich set of holiday metadata, allowing for the detailed scheduling of trading activities around public holidays. This feature is crucial for avoiding skewed results in backtesting, where holiday trading sessions might differ significantly in terms of volume and price movement.

- Customizable Holiday Schedules: Users can add or remove specific holidays, tailoring the library to fit various regional market schedules or specific trading requirements.

- Visualization Aids: The library supports on-chart labels, making it visually intuitive to identify holidays and DLS shifts directly on trading charts.

Use Cases:

1. Strategy Development: When developing trading strategies, it’s important to account for non-trading days and altered trading hours due to holidays and DLS. This library enables a realistic and accurate representation of these factors.

2. Risk Management: Trading around holidays can be riskier due to thinner liquidity and greater volatility. By integrating holiday data, traders can better manage their risk exposure.

3. Backtesting Accuracy: For backtesting to be effective, it must simulate the actual market conditions as closely as possible. Incorporating holidays and DLS adjustments contributes to more reliable and realistic backtesting results.

4. Global Trading: For traders active in multiple global markets, this library provides an easy way to handle different holiday schedules and DLS shifts across regions.

The Holiday Library is a versatile tool that enhances the precision and realism of trading simulations and strategy development . Its integration into the trading workflow is straightforward and beneficial for both novice and experienced traders.

EasterAlgo(_year)

Calculates the date of Easter Sunday for a given year using the Anonymous Gregorian algorithm.

`Gauss Algorithm for Easter Sunday` was developed by the mathematician Carl Friedrich Gauss

This algorithm is based on the cycles of the moon and the fact that Easter always falls on the first Sunday after the first ecclesiastical full moon that occurs on or after March 21.

While it's not considered to be 100% accurate due to rare exceptions, it does give the correct date in most cases.

It's important to note that Gauss's formula has been found to be inaccurate for some 21st-century years in the Gregorian calendar. Specifically, the next suggested failure years are 2038, 2051.

This function can be used for Good Friday (Friday before Easter), Easter Sunday, and Easter Monday (following Monday).

en.wikipedia.org

Parameters:

_year (int) : `int` - The year for which to calculate the date of Easter Sunday. This should be a four-digit year (YYYY).

Returns: tuple - The month (1-12) and day (1-31) of Easter Sunday for the given year.

easterInit()

Inits the date of Easter Sunday and Good Friday for a given year.

Returns: tuple - The month (1-12) and day (1-31) of Easter Sunday and Good Friday for the given year.

isLeapYear(_year)

Determine if a year is a leap year.

Parameters:

_year (int) : `int` - 4 digit year to check => YYYY

Returns: `bool` - true if input year is a leap year

method timezoneHelper(utc)

Helper function to convert UTC time.

Namespace types: series int, simple int, input int, const int

Parameters:

utc (int) : `int` - UTC time shift in hours.

Returns: `string`- UTC time string with shift applied.

weekofmonth()

Function to find the week of the month of a given Unix Time.

Returns: number - The week of the month of the specified UTC time.

dayLightSavingsAdjustedUTC(utc, adjustForDLS)

dayLightSavingsAdjustedUTC

Parameters:

utc (int) : `int` - The normal UTC timestamp to be used for reference.

adjustForDLS (bool) : `bool` - Flag indicating whether to adjust for daylight savings time (DLS).

Returns: `int` - The adjusted UTC timestamp for the given normal UTC timestamp.

getDayOfYear(monthOfYear, dayOfMonth, weekOfMonth, dayOfWeek, lastOccurrenceInMonth, holiday)

Function gets the day of the year of a given holiday (1-366)

Parameters:

monthOfYear (int)

dayOfMonth (int)

weekOfMonth (int)

dayOfWeek (int)

lastOccurrenceInMonth (bool)

holiday (string)

Returns: `int` - The day of the year of the holiday 1-366.

method buildMap(holidayMap, holiday, monthOfYear, weekOfMonth, dayOfWeek, dayOfMonth, lastOccurrenceInMonth, closingTime)

Function to build the `holidaysMap`.

Namespace types: map

Parameters:

holidayMap (map) : `map` - The map of holidays.

holiday (string) : `string` - The name of the holiday.

monthOfYear (int) : `int` - The month of the year of the holiday.

weekOfMonth (int) : `int` - The week of the month of the holiday.

dayOfWeek (int) : `int` - The day of the week of the holiday.

dayOfMonth (int) : `int` - The day of the month of the holiday.

lastOccurrenceInMonth (bool) : `bool` - Flag indicating whether the holiday is the last occurrence of the day in the month.

closingTime (int) : `int` - The closing time of the holiday.

Returns: `map` - The updated map of holidays

holidayInit(addHolidaysArray, removeHolidaysArray, defaultHolidays)

Initializes a HolidayStorage object with predefined US holidays.

Parameters:

addHolidaysArray (array) : `array` - The array of additional holidays to be added.

removeHolidaysArray (array) : `array` - The array of holidays to be removed.

defaultHolidays (bool) : `bool` - Flag indicating whether to include the default holidays.

Returns: `map` - The map of holidays.

Holidays(utc, addHolidaysArray, removeHolidaysArray, adjustForDLS, displayLabel, defaultHolidays)

Main function to build the holidays object, this is the only function from this library that should be needed. \

all functionality should be available through this function. \

With the exception of initializing a `HolidayMetaData` object to add a holiday or early close. \

\

**Default Holidays:** \

`DLS begin`, `DLS end`, `New Year's Day`, `MLK Jr. Day`, \

`Washington Day`, `Memorial Day`, `Independence Day`, `Labor Day`, \

`Columbus Day`, `Veterans Day`, `Thanksgiving Day`, `Christmas Day` \

\

**Example**

```

HolidayMetaData valentinesDay = HolidayMetaData.new(holiday="Valentine's Day", monthOfYear=2, dayOfMonth=14)

HolidayMetaData stPatricksDay = HolidayMetaData.new(holiday="St. Patrick's Day", monthOfYear=3, dayOfMonth=17)

HolidayMetaData addHolidaysArray = array.from(valentinesDay, stPatricksDay)

string removeHolidaysArray = array.from("DLS begin", "DLS end")

܂Holidays = Holidays(

܂ utc=-6,

܂ addHolidaysArray=addHolidaysArray,

܂ removeHolidaysArray=removeHolidaysArray,

܂ adjustForDLS=true,

܂ displayLabel=true,

܂ defaultHolidays=true,

܂ )

plot(Holidays.newHoliday ? open : na, title="newHoliday", color=color.red, linewidth=4, style=plot.style_circles)

```

Parameters:

utc (int) : `int` - The UTC time shift in hours

addHolidaysArray (array) : `array` - The array of additional holidays to be added

removeHolidaysArray (array) : `array` - The array of holidays to be removed

adjustForDLS (bool) : `bool` - Flag indicating whether to adjust for daylight savings time (DLS)

displayLabel (bool) : `bool` - Flag indicating whether to display a label on the chart

defaultHolidays (bool) : `bool` - Flag indicating whether to include the default holidays

Returns: `HolidayObject` - The holidays object | Holidays = (holidaysMap: map, newHoliday: bool, holiday: string, dayString: string)

HolidayMetaData

HolidayMetaData

Fields:

holiday (series string) : `string` - The name of the holiday.

dayOfYear (series int) : `int` - The day of the year of the holiday.

monthOfYear (series int) : `int` - The month of the year of the holiday.

dayOfMonth (series int) : `int` - The day of the month of the holiday.

weekOfMonth (series int) : `int` - The week of the month of the holiday.

dayOfWeek (series int) : `int` - The day of the week of the holiday.

lastOccurrenceInMonth (series bool)

closingTime (series int) : `int` - The closing time of the holiday.

utc (series int) : `int` - The UTC time shift in hours.

HolidayObject

HolidayObject

Fields:

holidaysMap (map) : `map` - The map of holidays.

newHoliday (series bool) : `bool` - Flag indicating whether today is a new holiday.

activeHoliday (series bool) : `bool` - Flag indicating whether today is an active holiday.

holiday (series string) : `string` - The name of the holiday.

dayString (series string) : `string` - The day of the week of the holiday.

Statistics TableStrategy Statistics

This library will add a table with statistics from your strategy. With this library, you won't have to switch to your strategy tester tab to view your results and positions.

Usage:

You can choose whether to set the table by input fields by adding the below code to your strategy or replace the parameters with the ones you would like to use manually.

// Statistics table options.

statistics_table_enabled = input.string(title='Show a table with statistics', defval='YES', options= , group='STATISTICS')

statistics_table_position = input.string(title='Position', defval='RIGHT', options= , group='STATISTICS')

statistics_table_margin = input.int(title='Table Margin', defval=10, minval=0, maxval=100, step=1, group='STATISTICS')

statistics_table_transparency = input.int(title='Cell Transparency', defval=20, minval=1, maxval=100, step=1, group='STATISTICS')

statistics_table_text_color = input.color(title='Text Color', defval=color.new(color.white, 0), group='STATISTICS')

statistics_table_title_cell_color = input.color(title='Title Cell Color', defval=color.new(color.gray, 80), group='STATISTICS')

statistics_table_cell_color = input.color(title='Cell Color', defval=color.new(color.purple, 0), group='STATISTICS')

// Statistics table init.

statistics.table(strategy.initial_capital, close, statistics_table_enabled, statistics_table_position, statistics_table_margin, statistics_table_transparency, statistics_table_text_color, statistics_table_title_cell_color, statistics_table_cell_color)

Sample:

If you are interested in the strategy used for this statistics table, you can browse the strategies on my profile.

two_ma_logicLibrary "two_ma_logic"

The core logic for the two moving average strategy that is used as an example for the internal logic of

the "Template Trailing Strategy" and the "Two MA Signal Indicator"

ma(source, maType, length)

ma - Calculate the moving average of the given source for the given length and type of the average

Parameters:

source (float) : - The source of the values

maType (simple string) : - The type of the moving average

length (simple int) : - The length of the moving average

Returns: - The resulted value of the calculations of the moving average

getDealConditions(drawings, longDealsEnabled, shortDealsEnabled, endDealsEnabled, cnlStartDealsEnabled, cnlEndDealsEnabled, emaFilterEnabled, emaAtrBandEnabled, adxFilterEnabled, adxSmoothing, diLength, adxThreshold)

Parameters:

drawings (TwoMaDrawings)

longDealsEnabled (simple bool)

shortDealsEnabled (simple bool)

endDealsEnabled (simple bool)

cnlStartDealsEnabled (simple bool)

cnlEndDealsEnabled (simple bool)

emaFilterEnabled (simple bool)

emaAtrBandEnabled (simple bool)

adxFilterEnabled (simple bool)

adxSmoothing (simple int)

diLength (simple int)

adxThreshold (simple float)

TwoMaDrawings

Fields:

fastMA (series__float)

slowMA (series__float)

emaLine (series__float)

emaUpperBand (series__float)

emaLowerBand (series__float)

TradeTrackerv2Library "TradeTrackerv2"

This library can be used to track (hypothetical) trades on the chart. Enter the Open, SL, and TP prices (or TP in R to have it calculated) and then call Trade.TrackTrade(barIndex). Keep track of your trades in an array and then simply call TradeTracker.UpdateAllTrades(close) to update all trades based on the current close price.

How to use:

1. Import the library, as always. I'm assuming the alias of "Tracker" below.

2. The Type Trade is exported, so generate a Trade object like newTrade = Tracker.Trade.new() .

3. Set the values for Open, SL, and TP. TP can be set either by price or by R, which will calculate the R based on the Open->SL range:

newTrade.priceOpen = 1.0

newTrade.priceSl = 0.5

newTrade.priceTp = 2.0

-- or in place of the third line above --

newTrade.rTp = 2

4. On each interval you want to update (whether that's per tick/close or on each bar), call trades.UpdateAllTrades(close) . This snippet assumes you have an array named trades (var trades = array.new()) .

In future updates, more customization options will be created. This is the initial prototype.

method MakeTradeLines(t, barIdx)

Namespace types: Trade

Parameters:

t (Trade)

barIdx (int)

method UpdateLabel(t)

Namespace types: Trade

Parameters:

t (Trade)

method MakeLabel(t, barIdx)

Namespace types: Trade

Parameters:

t (Trade)

barIdx (int)

method CloseTrade(t)

Namespace types: Trade

Parameters:

t (Trade)

method OpenTrade(t)

Namespace types: Trade

Parameters:

t (Trade)

method OpenCloseTrade(t, _close)

Namespace types: Trade

Parameters:

t (Trade)

_close (float)

method CalculateProfits(t, _close)

Calculates profits/losses for the Trade, given _close price

Namespace types: Trade

Parameters:

t (Trade)

_close (float)

method UpdateTrade(t, _close)

Namespace types: Trade

Parameters:

t (Trade)

_close (float)

method SetInitialValues(t, barIdx)

Namespace types: Trade

Parameters:

t (Trade)

barIdx (int)

method UpdateAllTrades(trades, _close)

Namespace types: Trade

Parameters:

trades (Trade )

_close (float)

method TrackTrade(t, barIdx)

Namespace types: Trade

Parameters:

t (Trade)

barIdx (int)

Trade

Fields:

id (series__integer)

isOpen (series__bool)

isClosed (series__bool)

isBuy (series__bool)

priceOpen (series__float)

priceTp (series__float)

priceSl (series__float)

rTP (series__float)

profit (series__float)

r (series__float)

resultR (series__float)

lineOpen (series__line)

lineTp (series__line)

lineSl (series__line)

labelStats (series__label)

TradingToolsLibraryLibrary "TradingToolsLibrary"

Easily create advanced entries, exits, filters and qualifiers to simulate strategies. Supports DCA (Dollar Cost Averaging) Lines, Stop Losses, Take Profits (with trailing or without) & ATR.

method deepCopy(this)

This creates a deep copy instead of a shallow copy of an entry_position. This does NOT deep copy the self_pyramiding_positions array reference, since only the master entry_position needs this to track the rest of its copies for efficiency reasons. This is to prevent a feedback loop.

Namespace types: entry_position

Parameters:

this (entry_position)

Returns: entry_position

method precision_fix(this, precision)

Convert a floating point number to a precise floating point number with digit precision to avoid floating point errors in quantity calculations.

Namespace types: series float, simple float, input float, const float

Parameters:

this (float)

precision (int)

Returns: float

xSellBuyMidInterpolation(_x, _high, _low, _sellRange, _buyRange)

Creates an interpolation for a sell range and buy range but with an emphasis on reaching the _low the closer to the middle of the _sell and _buy range you go.

Parameters:

_x (float) : is the value you want to use to control interpolation bewteen the _high and _low value. This will return the lowest percentage at the mid between high and low and highest percentage at the _high and _low.

_high (float)

_low (float)

_sellRange (float)

_buyRange (float)

Returns: an interpolated float between the _high and _low supplied.

xSellBuyInterpolation(_x, _high, _low, _sellRange, _buyRange)

Creates an interpolation a sell range and buy range

Parameters:

_x (float) : is the value you want to use to control interpolation bewteen the _high and _low value.

_high (float)

_low (float)

_sellRange (float)

_buyRange (float)

Returns: an interpolated float between the _high and _low supplied.

activate_entries_and_exits(_entries, _exits, _filters, _qualifiers, _equity)

Determines activation for entries or exits. Does not place the actual orders.

Parameters:

_entries (entry_position )

_exits (exit_position )

_filters (filter )

_qualifiers (qualifier )

_equity (equity_management)

Returns: void

create_entries_and_exits(_entries, _exits, _equity)

Creates actual entry and exit orders if activated

Parameters:

_entries (entry_position )

_exits (exit_position )

_equity (equity_management)

Returns: void

filter

Fields:

disabled (series__bool)

filter_for_entries_or_exits (series__string)

filter_for_groups (series__string)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

expire_condition_activate_value (series__string)

expire_condition_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_operator (series__string)

qualifier

Fields:

disabled (series__bool)

qualify_for_entries_or_exits (series__string)

qualify_for_groups (series__string)

disqualify (series__bool)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

expire_after_x_bars (series__integer)

use_expire_after_x_bars (series__bool)

use_expire_condition (series__bool)

use_override_expire_condition (series__bool)

expire_condition_operator (series__string)

expire_condition_source (series__float)

expire_compare_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_activate_value (series__string)

active (series__bool)

expire_after_bars_bar_index (series__integer)

expire_after_bars_bar_index_prior (series__integer)

expire_bar_count (series__integer)

expire_bar_changed (series__bool)

entry_position

Fields:

disabled (series__bool)

activate (series__bool)

active (series__bool)

override_occured (series__bool)

passDebug (array__bool)

initial_activation_price (series__float)

dca_done (series__bool)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

use_cash (series__bool)

use_percent_equity (series__bool)

percent_equity_amount (series__float)

cash_amount (series__float)

position_size (series__float)

total_position_size (series__float)

prior_total_position_size (series__float)

equity_remaining (series__float)

prior_equity_remaining (series__float)

initial_equity (series__float)

use_martingale (series__bool)

martingale_win_ratio (series__float)

martingale_lose_ratio (series__float)

martingale_win_limit (series__integer)

martingale_lose_limit (series__integer)

martingale_limit_reset_mode (series__string)

use_dynamic_percent_equity (series__bool)

dynamic_percent_equity_amount (series__float)

initial_dynamic_percent_equity_amount (series__float)

dynamic_percent_equity_source (series__float)

dynamic_percent_equity_min (series__float)

dynamic_percent_equity_max (series__float)

dynamic_percent_equity_source_sell_range (series__float)

dynamic_percent_equity_source_buy_range (series__float)

dynamic_equity_interpolation_method (series__string)

total_bars (series__integer)

bar_index_at_activate (series__integer)

bars_since_active (series__integer)

time_at_activate (series__integer)

time_since_active (series__integer)

bar_index_at_activated (series__integer)

bar_index_at_pyramid_change (series__integer)

name (series__string)

id (series__string)

group (series__string)

pyramiding_limit (series__integer)

self_pyramiding_limit (series__integer)

self_pyramiding_positions (array__|entry_position|#OBJ)

new_pyramid_cancels_dca (series__bool)

num_active_long_positions (series__integer)

num_active_short_positions (series__integer)

num_active_positions (series__integer)

position_remaining (series__float)

prior_position_remaining (series__float)

direction (series__string)

allow_flip_position (series__bool)

flip_occurred (series__bool)

ignore_flip (series__bool)

use_dca (series__bool)

dca_use_limit (series__bool)

dca_num_positions (series__integer)

dca_positions (array__float)

dca_deviation_percentage (series__float)

dca_scale (series__float)

dca_percentages (series__string)

dca_close_cancels (series__bool)

dca_active_positions (series__integer)

use_atr_deviation (series__bool)

dca_atr_length (series__integer)

dca_atr_mult (series__float)

dca_atr_updates_dca_positions (series__bool)

close_price_at_order (series__float)

dca_use_deviation_atr_min (series__bool)

dca_position_quantities (array__float)

use_dca_dynamic_percent_equity (series__bool)

dca_in_use (array__bool)

dca_activated (array__bool)

dca_money_used (array__float)

dca_lines (array__line)

dca_color (series__color)

show_dca_lines (series__bool)

atr_value (series__float)

atr_value_at_activation (series__float)

use_cooldown_bars (series__bool)

cooldown_bars (series__integer)

cooldown_bar_changed (series__bool)

cooldown_bar_index (series__integer)

cooldown_bar_index_prior (series__integer)

cooldown_bar_change_count (series__integer)

expire_condition_activate_value (series__string)

expire_condition_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_operator (series__string)

exit_position

Fields:

disabled (series__bool)

id (series__string)

group (series__string)

exit_for_entries (series__string)

exit_for_groups (series__string)

total_bars (series__integer)

name (series__string)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

activate (series__bool)

active (series__bool)

reset_equity (series__bool)

use_limit (series__bool)

use_alerts (series__bool)

reset_entry_cooldowns (series__bool)

prevent_new_entries_on_partial_close (series__bool)

show_activation_zone (series__bool)

use_average_position (series__bool)

source_value (series__float)

trigger_x_times (series__integer)

amount_of_times_triggered (series__integer)

quantity_percent (series__float)

trade_qty (series__float)

exit_amount (series__float)

entries_exiting_for (array__|entry_position|#OBJ)

atr_value (series__float)

update_atr (series__bool)

use_activate_after_bars (series__bool)

show_activate_after_bars (series__bool)

activate_after_bars (series__integer)

activate_after_bars_bar_changed (series__bool)

activate_after_bars_bar_index (series__integer)

activate_after_bars_bar_index_prior (series__integer)

activate_after_bars_bar_change_count (series__integer)

all_conditions_pass (series__bool)

use_close_if_profit_only (series__bool)

profit_value (series__float)

exit_type (series__string)

exit_modifier (series__string)

update_atr_with_new_pyramid (series__bool)

percentage (series__float)

activation_percentage (series__float)

atr_multiplier (series__float)

use_cancel_if_percent (series__bool)

cancel_if_percent (series__float)

activation_value (series__float)

activation_value_crossed (series__bool)

exit_value (series__float)

hypo_long_exit_value (series__float)

hypo_short_exit_value (series__float)

close_exit_value (series__float)

debug (series__float)

expire_condition_activate_value (series__string)

expire_condition_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_operator (series__string)

equity_management

Fields:

equity (series__float)

prior_equity (series__float)

position_used (series__float)

prior_position_used (series__float)

prevent_future_entries (series__bool)

minimum_order_size (series__float)

decimal_rounding_precision (series__integer)

direction (series__string)

show_order_info_in_comments (series__bool)

show_order_info_in_labels (series__bool)

allow_longs (series__bool)

allow_shorts (series__bool)

override_occured (series__bool)

flip_occured (series__bool)

num_concurrent_wins (series__integer)

num_concurrent_losses (series__integer)

first_entry (|entry_position|#OBJ)

num_win_trades (series__integer)

num_losing_trades (series__integer)

gFancyMALibrary "gFancyMA"

printLbl(y, x, c, m, b, s)

Parameters:

y (float)

x (int)

c (color)

m (string)

b (bool)

s (string)

lib_statemachineLibrary "lib_statemachine"

simple state machine that allows tracking a state an manipulating it with conditions

method step(this, before, after, condition)

will step the state of the state machine from one to the next in case of condition

Namespace types: StateMachine

Parameters:

this (StateMachine) : (StateMachine) the state machine to use

before (int) : (int) from state

after (int) : (int) to state

condition (bool) : (bool) if condition is true

Returns: true (bool) if the state of the statemachine changed

method step(this, after, condition)

will change the state of the state machine to the next in case of condition (not depending on previous state)

Namespace types: StateMachine

Parameters:

this (StateMachine) : (StateMachine) the state machine to use

after (int) : (int) to state

condition (bool) : (bool) if condition is true

Returns: true (bool) if the state of the statemachine changed

method changed(this, within_bars)

will return true if the state of the state machine was changed in this iteration

Namespace types: StateMachine

Parameters:

this (StateMachine) : (StateMachine) the state machine to use

within_bars (int)

Returns: true (bool) if the state of the statemachine changed

method reset(this, condition, min_occurrences)

will reset the state machine if a certain 'condition' appears 'min_occurrences' times

Namespace types: StateMachine

Parameters:

this (StateMachine) : (StateMachine) the state machine to use

condition (bool) : (bool) reset condition

min_occurrences (int) : (int) min times 'condition' must appear for the reset to happen

Returns: true (bool) if the state of the statemachine changed

StateMachine

Fields:

state (series__integer)

neutral (series__integer)

enabled (series__bool)

reset_counter (series__integer)

CNTLibraryLibrary "CNTLibrary"

Custom Functions To Help Code In Pinescript V5

Coded By Christian Nataliano

First Coded In 10/06/2023

Last Edited In 22/06/2023

Huge Shout Out To © ZenAndTheArtOfTrading and his ZenLibrary V5, Some Of The Custom Functions Were Heavily Inspired By Matt's Work & His Pine Script Mastery Course

Another Shout Out To The TradingView's Team Library ta V5

//====================================================================================================================================================

// Custom Indicator Functions

//====================================================================================================================================================

GetKAMA(KAMA_lenght, Fast_KAMA, Slow_KAMA)

Calculates An Adaptive Moving Average Based On Perry J Kaufman's Calculations

Parameters:

KAMA_lenght (int) : Is The KAMA Lenght

Fast_KAMA (int) : Is The KAMA's Fastes Moving Average

Slow_KAMA (int) : Is The KAMA's Slowest Moving Average

Returns: Float Of The KAMA's Current Calculations

GetMovingAverage(Source, Lenght, Type)

Get Custom Moving Averages Values

Parameters:

Source (float) : Of The Moving Average, Defval = close

Lenght (simple int) : Of The Moving Average, Defval = 50

Type (string) : Of The Moving Average, Defval = Exponential Moving Average

Returns: The Moving Average Calculation Based On Its Given Source, Lenght & Calculation Type (Please Call Function On Global Scope)

GetDecimals()

Calculates how many decimals are on the quote price of the current market © ZenAndTheArtOfTrading

Returns: The current decimal places on the market quote price

Truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places © ZenAndTheArtOfTrading

Parameters:

number (float)

decimalPlaces (simple float)

Returns: The given number truncated to the given decimalPlaces

ToWhole(number)

Converts pips into whole numbers © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

ToPips(number)

Converts whole numbers back into pips © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

GetPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period © ZenAndTheArtOfTrading

Parameters:

value1 (float)

value2 (float)

lookback (int)

BarsAboveMA(lookback, ma)

Counts how many candles are above the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are above the MA

BarsBelowMA(lookback, ma)

Counts how many candles are below the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are below the EMA

BarsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many times price recently crossed the EMA

GetPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count) © ZenAndTheArtOfTrading

Parameters:

lookback (int)

direction (int)

Returns: The bar count of how many candles have retraced over the given lookback & direction

GetSwingHigh(Lookback, SwingType)

Check If Price Has Made A Recent Swing High

Parameters:

Lookback (int) : Is For The Swing High Lookback Period, Defval = 7

SwingType (int) : Is For The Swing High Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing High

GetSwingLow(Lookback, SwingType)

Check If Price Has Made A Recent Swing Low

Parameters:

Lookback (int) : Is For The Swing Low Lookback Period, Defval = 7

SwingType (int) : Is For The Swing Low Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing Low

//====================================================================================================================================================

// Custom Risk Management Functions

//====================================================================================================================================================

CalculateStopLossLevel(OrderType, Entry, StopLoss)

Calculate StopLoss Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLoss (float) : Is The Custom StopLoss Distance, Defval = 2x ATR Below Close

Returns: Float - The StopLoss Level In Actual Price As A

CalculateStopLossDistance(OrderType, Entry, StopLoss)

Calculate StopLoss Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

StopLoss (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The StopLoss Value In Pips

CalculateTakeProfitLevel(OrderType, Entry, StopLossDistance, RiskReward)

Calculate TakeProfit Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLossDistance (float)

RiskReward (float)

Returns: Float - The TakeProfit Level In Actual Price

CalculateTakeProfitDistance(OrderType, Entry, TakeProfit)

Get TakeProfit Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

TakeProfit (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The TakeProfit Value In Pips

CalculateConversionCurrency(AccountCurrency, SymbolCurrency, BaseCurrency)

Get The Conversion Currecny Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

AccountCurrency (simple string) : Is For The Account Currency Used

SymbolCurrency (simple string) : Is For The Current Symbol Currency (Front Symbol)

BaseCurrency (simple string) : Is For The Current Symbol Base Currency (Back Symbol)

Returns: Tuple Of A Bollean (Convert The Currency ?) And A String (Converted Currency)

CalculateConversionRate(ConvertCurrency, ConversionRate)

Get The Conversion Rate Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

ConvertCurrency (bool) : Is To Check If The Current Symbol Needs To Be Converted Or Not

ConversionRate (float) : Is The Quoted Price Of The Conversion Currency (Input The request.security Function Here)

Returns: Float Price Of Conversion Rate (If In The Same Currency Than Return Value Will Be 1.0)

LotSize(LotSizeSimple, Balance, Risk, SLDistance, ConversionRate)

Get Current Lot Size

Parameters:

LotSizeSimple (bool) : Is To Toggle Lot Sizing Calculation (Simple Is Good Enough For Stocks & Crypto, Whilst Complex Is For Forex)

Balance (float) : Is For The Current Account Balance To Calculate The Lot Sizing Based Off

Risk (float) : Is For The Current Risk Per Trade To Calculate The Lot Sizing Based Off

SLDistance (float) : Is The Current Position StopLoss Distance From Its Entry Price

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - Position Size In Units

ToLots(Units)

Converts Units To Lots

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots

ToUnits(Lots)

Converts Lots To Units

Parameters:

Lots (float) : Is For How Many Lots Need To Be Converted Into Units (Minimun 0.01 Units)

Returns: Int - Position Size In Units

ToLotsInUnits(Units)

Converts Units To Lots Than Back To Units

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots That Were Rounded To Units

ATRTrail(OrderType, SourceType, ATRPeriod, ATRMultiplyer, SwingLookback)

Calculate ATR Trailing Stop

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

SourceType (int) : Is To Determine Where To Calculate The ATR Trailing From, Defval = close

ATRPeriod (simple int) : Is To Change Its ATR Period, Defval = 20

ATRMultiplyer (float) : Is To Change Its ATR Trailing Distance, Defval = 1

SwingLookback (int) : Is To Change Its Swing HiLo Lookback (Only From Source Type 5), Defval = 7

Returns: Float - Number Of The Current ATR Trailing

DangerZone(WinRate, AvgRRR, Filter)

Calculate Danger Zone Of A Given Strategy

Parameters:

WinRate (float) : Is The Strategy WinRate

AvgRRR (float) : Is The Strategy Avg RRR

Filter (float) : Is The Minimum Profit It Needs To Be Out Of BE Zone, Defval = 3

Returns: Int - Value, 1 If Out Of Danger Zone, 0 If BE, -1 If In Danger Zone

IsQuestionableTrades(TradeTP, TradeSL)

Checks For Questionable Trades (Which Are Trades That Its TP & SL Level Got Hit At The Same Candle)

Parameters:

TradeTP (float) : Is The Trade In Question Take Profit Level

TradeSL (float) : Is The Trade In Question Stop Loss Level

Returns: Bool - True If The Last Trade Was A "Questionable Trade"

//====================================================================================================================================================

// Custom Strategy Functions

//====================================================================================================================================================

OpenLong(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Long Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Long"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Long Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

OpenShort(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Short Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Short"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Short Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

TP_SLExit(FromID, TPLevel, SLLevel, PercentageClose, Comment, CommentValue)

Exits Based On Predetermined TP & SL Levels

Parameters:

FromID (string) : Is The Trade ID That The TP & SL Levels Be Palced

TPLevel (float) : Is The Take Profit Level

SLLevel (float) : Is The StopLoss Level

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

CloseLong(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Long Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Long"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

CloseShort(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Short Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Short"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

BrokerCheck(Broker)

Checks Traded Broker With Current Loaded Chart Broker

Parameters:

Broker (string) : Is The Current Broker That Is Traded

Returns: Bool - True If Current Traded Broker Is Same As Loaded Chart Broker

OpenPC(LicenseID, OrderType, UseLimit, LimitPrice, SymbolPrefix, Symbol, SymbolSuffix, Risk, SL, TP, OrderComment, Spread)

Compiles Given Parameters Into An Alert String Format To Open Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Open

UseLimit (bool) : Is If We Want To Enter The Position At Exactly The Previous Closing Price

LimitPrice (float) : Is The Limit Price Of The Trade (Only For Pending Orders)

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Risk (float) : Is The Trade Risk Per Trade / Fixed Lot Sizing

SL (float) : Is The Trade SL In Price / In Pips

TP (float) : Is The Trade TP In Price / In Pips

OrderComment (string) : Is The Executed Trade Comment

Spread (float) : is The Maximum Spread For Execution

Returns: String - Pine Connector Order Syntax Alert Message

ClosePC(LicenseID, OrderType, SymbolPrefix, Symbol, SymbolSuffix)

Compiles Given Parameters Into An Alert String Format To Close Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Close

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Returns: String - Pine Connector Order Syntax Alert Message

//====================================================================================================================================================

// Custom Backtesting Calculation Functions

//====================================================================================================================================================

CalculatePNL(EntryPrice, ExitPrice, LotSize, ConversionRate)

Calculates Trade PNL Based On Entry, Eixt & Lot Size

Parameters:

EntryPrice (float) : Is The Trade Entry

ExitPrice (float) : Is The Trade Exit

LotSize (float) : Is The Trade Sizing

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - The Current Trade PNL

UpdateBalance(PrevBalance, PNL)

Updates The Previous Ginve Balance To The Next PNL

Parameters:

PrevBalance (float) : Is The Previous Balance To Be Updated

PNL (float) : Is The Current Trade PNL To Be Added

Returns: Float - The Current Updated PNL

CalculateSlpComm(PNL, MaxRate)

Calculates Random Slippage & Commisions Fees Based On The Parameters

Parameters:

PNL (float) : Is The Current Trade PNL

MaxRate (float) : Is The Upper Limit (In Percentage) Of The Randomized Fee

Returns: Float - A Percentage Fee Of The Current Trade PNL

UpdateDD(MaxBalance, Balance)

Calculates & Updates The DD Based On Its Given Parameters

Parameters:

MaxBalance (float) : Is The Maximum Balance Ever Recorded

Balance (float) : Is The Current Account Balance

Returns: Float - The Current Strategy DD

CalculateWR(TotalTrades, LongID, ShortID)

Calculate The Total, Long & Short Trades Win Rate

Parameters:

TotalTrades (int) : Are The Current Total Trades That The Strategy Has Taken

LongID (string) : Is The Order ID Of The Long Trades Of The Strategy

ShortID (string) : Is The Order ID Of The Short Trades Of The Strategy

Returns: Tuple Of Long WR%, Short WR%, Total WR%, Total Winning Trades, Total Losing Trades, Total Long Trades & Total Short Trades

CalculateAvgRRR(WinTrades, LossTrades)

Calculates The Overall Strategy Avg Risk Reward Ratio

Parameters:

WinTrades (int) : Are The Strategy Winning Trades

LossTrades (int) : Are The Strategy Losing Trades

Returns: Float - The Average RRR Values

CAGR(StartTime, StartPrice, EndTime, EndPrice)

Calculates The CAGR Over The Given Time Period © TradingView

Parameters:

StartTime (int) : Is The Starting Time Of The Calculation

StartPrice (float) : Is The Starting Price Of The Calculation

EndTime (int) : Is The Ending Time Of The Calculation

EndPrice (float) : Is The Ending Price Of The Calculation

Returns: Float - The CAGR Values

//====================================================================================================================================================

// Custom Plot Functions

//====================================================================================================================================================

EditLabels(LabelID, X1, Y1, Text, Color, TextColor, EditCondition, DeleteCondition)

Edit / Delete Labels

Parameters:

LabelID (label) : Is The ID Of The Selected Label

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

Text (string) : Is The Text Than Wants To Be Written In The Label

Color (color) : Is The Color Value Change Of The Label Text

TextColor (color)

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

EditLine(LineID, X1, Y1, X2, Y2, Color, EditCondition, DeleteCondition)

Edit / Delete Lines

Parameters:

LineID (line) : Is The ID Of The Selected Line

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

X2 (int) : Is The X2 Coordinate IN BARINDEX Xloc

Y2 (float) : Is The Y2 Coordinate IN PRICE Yloc

Color (color) : Is The Color Value Change Of The Line

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

//====================================================================================================================================================

// Custom Display Functions (Using Tables)

//====================================================================================================================================================

FillTable(TableID, Column, Row, Title, Value, BgColor, TextColor, ToolTip)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

Column (int) : Is The Current Column Of The Table That Wants To Be Edited

Row (int) : Is The Current Row Of The Table That Wants To Be Edited

Title (string) : Is The String Title Of The Current Cell Table

Value (string) : Is The String Value Of The Current Cell Table

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

ToolTip (string) : Is The ToolTip Of The Current Cell In The Table

Returns: Void

DisplayBTResults(TableID, BgColor, TextColor, StartingBalance, Balance, DollarReturn, TotalPips, MaxDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

StartingBalance (float) : Is The Account Starting Balance

Balance (float)

DollarReturn (float) : Is The Account Dollar Reture

TotalPips (float) : Is The Total Pips Gained / loss

MaxDD (float) : Is The Maximum Drawdown Over The Backtesting Period

Returns: Void

DisplayBTResultsV2(TableID, BgColor, TextColor, TotalWR, QTCount, LongWR, ShortWR, InitialCapital, CumProfit, CumFee, AvgRRR, MaxDD, CAGR, MeanDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

TotalWR (float) : Is The Strategy Total WR In %

QTCount (int) : Is The Strategy Questionable Trades Count

LongWR (float) : Is The Strategy Total WR In %

ShortWR (float) : Is The Strategy Total WR In %

InitialCapital (float) : Is The Strategy Initial Starting Capital

CumProfit (float) : Is The Strategy Ending Cumulative Profit

CumFee (float) : Is The Strategy Ending Cumulative Fee (Based On Randomized Fee Assumptions)

AvgRRR (float) : Is The Strategy Average Risk Reward Ratio

MaxDD (float) : Is The Strategy Maximum DrawDown In Its Backtesting Period

CAGR (float) : Is The Strategy Compounded Average GRowth In %

MeanDD (float) : Is The Strategy Mean / Average Drawdown In The Backtesting Period

Returns: Void

//====================================================================================================================================================

// Custom Pattern Detection Functions

//====================================================================================================================================================

BullFib(priceLow, priceHigh, fibRatio)

Calculates A Bullish Fibonacci Value (From Swing Low To High) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

BearFib(priceLow, priceHigh, fibRatio)

Calculates A Bearish Fibonacci Value (From Swing High To Low) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

GetBodySize()

Gets The Current Candle Body Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN POINTS

GetTopWickSize()

Gets The Current Candle Top Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Top Wick Size IN POINTS

GetBottomWickSize()

Gets The Current Candle Bottom Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Bottom Wick Size IN POINTS

GetBodyPercent()

Gets The Current Candle Body Size As A Percentage Of Its Entire Size Including Its Wicks © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN PERCENTAGE

GetTopWickPercent()

Gets The Current Top Wick Size As A Percentage Of Its Entire Body Size

Returns: Float - The Current Candle Top Wick Size IN PERCENTAGE

GetBottomWickPercent()

Gets The Current Bottom Wick Size As A Percentage Of Its Entire Bodu Size

Returns: Float - The Current Candle Bottom Size IN PERCENTAGE

BullishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Engulfing Candle

BearishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bearish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Engulfing Candle

Hammer(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Star(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Doji(MaxWickSize, MaxBodySize, DojiType, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Doji Candle

Parameters:

MaxWickSize (float) : To Specify The Maximum Lenght Of Its Upper & Lower Wick, Defval = 2

MaxBodySize (float) : To Specify The Maximum Lenght Of Its Candle Body IN PERCENT, Defval = 0.05

DojiType (int)

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Doji Candle

BullishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Harami Candle

BearishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Harami Candle

//====================================================================================================================================================

// Custom Time Functions

//====================================================================================================================================================

BarInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls within the given time session

BarOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls outside the given time session

DateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range © ZenAndTheArtOfTrading

Parameters:

startTime (int)

endTime (int)

Returns: A boolean - true if the current bar falls within the given dates

DayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze © ZenAndTheArtOfTrading

Parameters:

monday (bool)

tuesday (bool)

wednesday (bool)

thursday (bool)

friday (bool)

saturday (bool)

sunday (bool)

Returns: A boolean - true if the current bar's day is one of the given days

AUSSess()

Checks If The Current Australian Forex Session In Running

Returns: Bool - True If Currently The Australian Session Is Running

ASIASess()

Checks If The Current Asian Forex Session In Running

Returns: Bool - True If Currently The Asian Session Is Running

EURSess()

Checks If The Current European Forex Session In Running

Returns: Bool - True If Currently The European Session Is Running

USSess()

Checks If The Current US Forex Session In Running

Returns: Bool - True If Currently The US Session Is Running

UNIXToDate(Time, ConversionType, TimeZone)

Converts UNIX Time To Datetime

Parameters:

Time (int) : Is The UNIX Time Input

ConversionType (int) : Is The Datetime Output Format, Defval = DD-MM-YYYY

TimeZone (string) : Is To Convert The Outputed Datetime Into The Specified Time Zone, Defval = Exchange Time Zone

Returns: String - String Of Datetime

Risk ManagementLibrary "RiskManagement"

This library keeps your money in check, and is used for testing and later on webhook-applications too. It has four volatility functions and two of them can be used to calculate a Stop-Loss, like Average True Range. It also can calculate Position Size, and the Risk Reward Ratio. But those calculations don't take leverage into account.

position_size(portfolio, risk, entry, stop_loss, use_leverage, qty_as_integer)

This function calculates the definite amount of contracts/shares/units you should use to buy or sell. This value can used by `strategy.entry(qty)` for example.

Parameters:

portfolio (float) : This is the total amount of the currency you own, and is also used by strategy.initial_capital, for example. The amount is needed to calculate the maximum risk you are willing to take per trade.

risk (float) : This is the percentage of your Portfolio you willing to loose on a single trade. Possible values are between 0.1 and 100%. Same usecase with strategy(default_qty_type=strategy.percent_of_equity,default_qty_value=100), except its calculation the risk only.

entry (float) : This is the limit-/market-price for the investment. In other words: The price per contract/share/unit you willing to buy or sell.

stop_loss (float) : This is the limit-/market-price when to exit the trade, to minimize your losses.

use_leverage (bool) : This value is optional. When not used or when set to false then this function will let you invest your portfolio at max.

qty_as_integer (bool) : This value is optional. When set to true this function will return a value used with integers. The largest integer less than or equal to the given number. Because some Broker/Exchanges let you trade hole contracts/shares/units only.

Returns: float

position_size_currency(portfolio, risk, entry, stop_loss)

This function calculates the definite amount of currency you should use when going long or short.

Parameters:

portfolio (float) : This is the total amount of the currency you own, and is also used by strategy.initial_capital, for example. The amount is needed to calculate the maximum risk you are willing to take per trade.

risk (float) : This is the percentage of your Portfolio you willing to loose on a single trade. For example: 1 is 100% and 0,01 is 1%. Default amount is 0.02 (2%).

entry (float) : This is the limit-/market-price for the current investment. In other words: The price per contract/share/units you willing to buy or sell.

stop_loss (float) : This is the limit-/market-price when to exit the trade, to minimize your losses.

Returns: float

rrr(entry, stop_loss, take_profit)

This function calculates the Risk Reward Ratio. Common values are between 1.5 and 2.0 and you should not go lower except for very few special cases.

Parameters:

entry (float) : This is the limit-/market-price for the investment. In other words: The price per contract/share/unit you willing to buy or sell.

stop_loss (float) : This is the limit-/market-price when to exit the trade, to minimize your losses.

take_profit (float) : This is the limit-/market-price when to take profits.

Returns: float

change_in_price(length)

This function calculates the difference between price now and close price of the candle 'n' bars before that. If prices are very volatile but closed where they began, then this method would show zero volatility. Over many calculations, this method returns a reasonable measure of volatility, but will always be lower than those using the highs and lows.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

maximum_price_fluctuation(length)

This function measures volatility over most recent candles, which could be used as an estimate of risk. It may also be effective as the basis for a stop-loss or take-profit, like the ATR but it ignores the frequency of directional changes within the time interval. In other words: The difference between the highest high and lowest low over 'n' bars.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

absolute_price_changes(length)

This function measures volatility over most recent close prices. This is excellent for comparing volatility. It includes both frequency and magnitude. In other words: Sum of differences between second to last close price and last close price as absolute value for 'n' bars.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

annualized_volatility(length)

This function measures volatility over most recent close prices. Its the standard deviation of close over the past 'n' periods, times the square root of the number of periods in a year.

Parameters:

length (int) : The length is needed to determine how many candles/bars back should take into account.

Returns: float

LYGLibraryLibrary "LYGLibrary"

A collection of custom tools & utility functions commonly used with my scripts

getDecimals()

Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places

Parameters:

number (float)

decimalPlaces (simple float)

Returns: The given number truncated to the given decimalPlaces

toWhole(number)

Converts pips into whole numbers

Parameters:

number (float)

Returns: The converted number

toPips(number)

Converts whole numbers back into pips

Parameters:

number (float)

Returns: The converted number

getPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period

Parameters:

value1 (float)

value2 (float)

lookback (int)

av_getPositionSize(balance, risk, stopPoints, conversionRate)

Calculates OANDA forex position size for AutoView based on the given parameters

Parameters:

balance (float)

risk (float)

stopPoints (float)

conversionRate (float)

Returns: The calculated position size (in units - only compatible with OANDA)

bullFib(priceLow, priceHigh, fibRatio)

Calculates a bullish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio)

Calculates a bearish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate