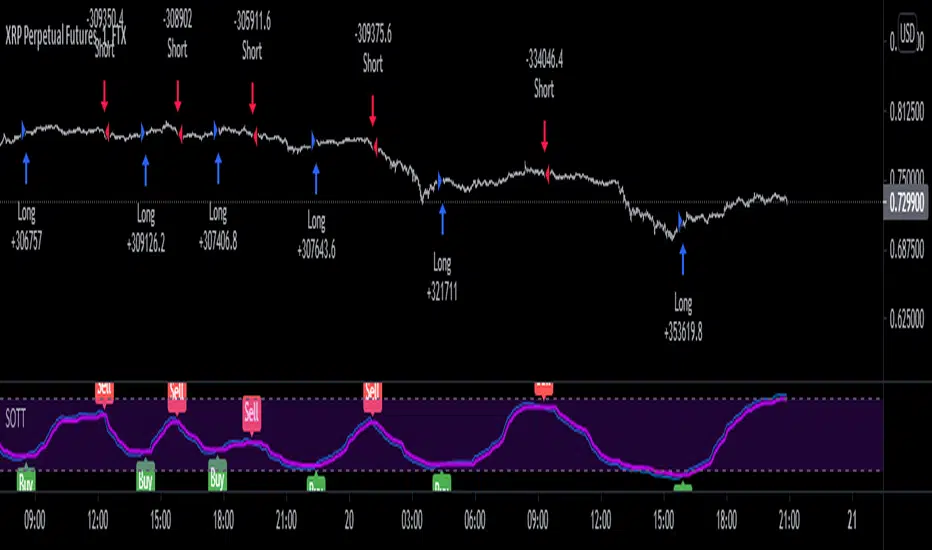

Ichimoku + RSI Crypto trending strategyThis is a crypto trending strategy designed for big timeframes such as 3-4h+.

Its components are:

RSI

ICHIMOKU full pack

Heikin Ashi candles for logic calculation inside

Rules for entry.

For long : we have a long cross condition on ichimoku and price is above the ichimoku lines, and at the same time RSI value is > 50.

For long : we have a short cross condition on ichimoku and price is below the ichimoku lines, and at the same time RSI value is < 50.

Rules for exit

We exit whenever we receive an opposite signal of the initial entry.

SInce this strategy is using no risk management inside, I recommend to be careful with it .

If you have any questions, let me know !

Strategi Pine Script®