Real Relative Strength Indicator### What is RRS (Real Relative Strength)?

RRS is a volatility-normalized relative strength indicator that shows you – in real time – whether your stock, crypto, or any asset is genuinely beating or lagging the broader market after adjusting for risk and volatility. Unlike the classic “price ÷ SPY” line that gets completely fooled by volatility regimes, RRS answers the only question that actually matters to professional traders:

“Is this ticker moving better (or worse) than the market on a risk-adjusted basis right now?”

It does this by measuring the excess momentum of your ticker versus a benchmark (SPY, QQQ, BTC, etc.) and then dividing that excess by the average volatility (ATR) of both instruments. The result is a clean, centered-around-zero oscillator that works the same way in calm markets, crash markets, or parabolic bull runs.

### How to Use the RRS Indicator (Aqua/Purple Area Version) in Practice

The indicator is deliberately simple to read once you know the rules:

Positive area (aqua) means genuine outperformance.

Negative area (purple) means genuine underperformance.

The farther from zero, the stronger the leadership or weakness.

#### Core Signals and How to Trade Them

- RRS crossing above zero → one of the highest-probability long signals in existence. The asset has just started outperforming the market on a risk-adjusted basis. Enter or add aggressively if price structure agrees.

- RRS crossing below zero → leadership is ending. Tighten stops, take partial or full profits, or flip short if you trade both sides.

- RRS above +2 (bright aqua area) → clear leadership. This is where the real money is made in bull markets. Trail stops, add on pullbacks, let winners run.

- RRS below –2 (bright purple area) → clear distribution or capitulation. Avoid new longs, consider short entries or protective puts.

- Extreme readings above +4 or below –4 (background tint appears) → rare, very high-conviction moves. Treat these like once-a-month opportunities.

- Divergence (not plotted here, but easy to spot visually): price making new highs while the aqua area is shrinking → distribution. Price making new lows while the purple area is shrinking → hidden buying and coming reversal.

#### Best Settings by Style and Asset Class

For stocks and ETFs: keep benchmark as SPY (or QQQ for tech-heavy names) and length 14–20 on daily/4H charts.

For crypto: change the benchmark to BTCUSD (or ETHUSD) immediately — otherwise the reading is meaningless. Length 10–14 works best on 1H–4H crypto charts because volatility is higher.

For day trading: drop length to 10–12 and use 15-minute or 5-minute charts. Signals are faster and still extremely clean.

#### Highest-Edge Setups (What Actually Prints Money)

- RRS crosses above zero while price is still below a major moving average (50 EMA, 200 SMA, etc.) → early leadership, often catches the exact bottom of a new leg up.

- RRS already deep aqua (+3 or higher) and price pulls back to support without RRS dropping below +1 → textbook add-on or re-entry zone.

- RRS deep purple and suddenly turns flat or starts curling up while price is still falling → hidden accumulation, usually the exact low tick.

That’s it. Master these few rules and the RRS becomes one of the most powerful edge tools you will ever use for rotation trading...

Average True Range (ATR)

Hash SupertrendHash Supertrend is a visually enhanced Supertrend-based indicator designed by Hash Capital Research, tuned specifically for crypto trend trading on Solana (SOL) and Bitcoin (BTC). It combines institutional-style color coding, an optional session time filter, and production-ready alerts for systematic and discretionary traders alike.

What This Indicator Is

Hash Supertrend is a trend-following volatility band indicator built on TradingView’s native ta.supertrend() function.

It’s optimized and visually styled for:

High-volatility crypto pairs (especially SOL/USDT, SOL/USD, BTC/USDT, BTC/USD)

Timeframes typically used by crypto traders (from 5m scalping to 4H swing and 1D trend following)

The script is an indicator, not a strategy:

It does not place trades or show backtest results.

It provides clear trend states, flips, and alerts that you can plug into your own execution stack or manual trading.

Key Features

✅ Tuned for Crypto (Solana & Bitcoin)

Parameters are chosen to respond well to the volatility profile of SOL and BTC, reducing noise while still catching strong moves.

✅ Non-repainting Supertrend Core

Uses TradingView’s built-in ta.supertrend — values may move intrabar as the bar forms, but once a bar closes, the historical line and signals do not repaint.

✅ Fluorescent Trend Visualization

Bright green for bullish phases

Bright red for bearish phases

Adaptive color intensity based on user setting

✅ Glow Layer & Trend Zones

Glow effect around the Supertrend line for instant visual recognition

Optional filled zones between price and line for “trend cloud” style visualization

✅ Time Filter (Session Control)

Option to only mark signals during specific hours for those wanting to integrate with webhooks

Designed for traders who avoid certain sessions (e.g., low-liquidity hours)

✅ Signal Dots & Alerts

Tiny green dots for bullish flips

Tiny red dots for bearish flips

Professional, preconfigured alerts for:

Long Entry

Short Entry

Any Trend Change

Filtered signals outside trading hours (for monitoring only)

The core logic is built on:

ATR Length (ATR Length) Default: 16

Lower values (7–10): more sensitive, more signals, more noise

Higher values (12–20): smoother, fewer but stronger trend signals

Factor (Factor) Default: 3.11

Lower values (1.5–2.5): tighter bands, earlier entries, higher whipsaws

Higher values (3.0–4.0+): wider bands, later entries, stronger trend confirmation

The indicator reads direction from ta.supertrend and classifies:

Bullish Trend: direction < 0

Bearish Trend: direction > 0

A trend flip happens when direction changes sign:

longSignal: Supertrend flips from above price to below price (bearish → bullish)

shortSignal: Supertrend flips from below price to above price (bullish → bearish)

[CT] ATR Ratio MTFThis indicator is an enhanced, multi-timeframe version of the original “ATR ratio” by RafaelZioni. Huge thanks to RafaelZioni for the core concept and base logic. The script still combines an ATR-based ratio (Z-score style reading of where price sits within its recent ATR envelope) with an ATR Supertrend, but expands it into a more flexible trade-decision and visual context tool.

The ATR ratio is normalized so you can quickly see when price is pressing into extended bullish or bearish territory, while the Supertrend defines directional bias and a dynamic support-resistance trail. You can choose any higher timeframe in the settings, allowing you to run the ATR ratio and Supertrend from a larger anchor timeframe while trading on a lower chart.

Upgrades include a full Pine Script v6 rewrite, multi-timeframe support for both the ATR ratio and Supertrend, user-controlled colors for the Supertrend in bull and bear modes, and optional bar coloring so price bars automatically reflect Supertrend direction. Entry, pyramiding and take-profit logic from the original script are preserved, giving you a familiar framework with more control over timeframe, visuals and trend bias.

This indicator is designed to give you a clean directional framework that blends volatility, trend, and timing into one view. The ATR ratio side of the script shows you where price sits inside a recent ATR-based envelope. When the ATR ratio pushes up and sustains above the bullish threshold, it signals that price is trading in an extended, momentum-driven zone relative to recent volatility. When it drops and holds below the bearish threshold, it shows the opposite: sellers have pushed price down into an extended bearish zone. The optional background coloring simply makes these bullish and bearish environments easier to see at a glance.

On top of that, the Supertrend and bar colors tell you what side of the market to favor. The Supertrend is calculated from ATR on whatever timeframe you choose in the settings. If you set the MTF input to a higher timeframe, the Supertrend and ATR ratio become your higher time frame bias while you trade on a lower chart. When price is above the MTF Supertrend, the line uses your bullish color and, if bar coloring is enabled, candles adopt your bullish bar color. That is your “long only” environment: you generally look for buys when price is above the Supertrend and the ATR ratio is either turning up from neutral or already in a bullish zone. When price is below the MTF Supertrend, the line uses your bearish color and candles can shift to your bearish bar color; that is where you focus on shorts, especially when the ATR ratio is rolling over or holding in the bearish zone.

The built-in long and short conditions are meant as signal prompts, not rigid rules. Long signals fire when the ATR ratio crosses up through a positive level while the Supertrend is bullish. Short signals fire when the ATR ratio crosses down through a negative level while the Supertrend is bearish. The script tracks how many longs or shorts have been taken in sequence (pyramiding) and will only allow a new signal up to the limit you set, so you can control how aggressively you stack positions in a trend. The take-profit logic then watches the percentage move from your last entry and flags “TP” when that move has reached your take-profit percent, helping you standardize exits instead of eyeballing them bar by bar.

In practice you typically start by choosing your anchor timeframe for the MTF setting, for example a 1-hour or 4-hour Supertrend and ATR ratio while watching a 5-minute or 15-minute chart. You then use the Supertrend direction and bar colors as your bias filter, only taking signals in the direction of the trend, and you use the ATR ratio behavior to judge whether you are entering into strength, fading an extreme, or trading inside a neutral consolidation. Over time this gives you a consistent way to answer three questions on every chart: which side am I allowed to trade, how extended is price within its recent volatility, and where are my structured entries and exits based on that framework.

ATR Chart Display (SEANTRADES)Simple indicator that displays the ATR for the chart session as a number on the chart.

OTA ATR Stop BufferOTA ATR indicator calculates and displays the Daily Average True Range (ATR), and two customizable ATR percentage values in a clean table format. It provides values in ticks and points, helping traders set stop-loss buffers based on market volatility.

2t's MA 50, MA 150, ATRThis indicator displays three key technical signals on the chart:

SMA 50 – Short-term trend direction

SMA 150 – Medium-term trend direction

ATR – Market volatility (Average True Range)

Line colors and lengths can be customized in the settings.

The ATR is plotted on the same chart for quick volatility reference without needing a separate panel.

This tool is designed for traders who want a clean, lightweight view of trend strength and volatility in a single indicator.

ADR / $Volume DashboardSee 5 / 20 days ADR / Volume and price %age from low of day on top of the chart

Position Sizing Calculator (Real-Time) - Futures Edition█ SUMMARY

The following indicator is a Position Sizing Calculator based on Average True Range (ATR), originally developed by market technician J. Welles Wilder Jr., intended for real-time trading.

This script utilizes the user's account size, acceptable risk percentage, and a stop-loss distance based on ATR to dynamically calculate the appropriate position size for each trade in real time.

█ BACKGROUND

Developed for use on the Micro E-mini Nasdaq-100 futures (MNQ), this script provides traders with continuously updated dynamic position sizes. It enables traders to instantly determine the exact number of contracts to use when entering a trade while staying within their acceptable risk tolerance.

This real-time position sizing tool helps traders make well-informed decisions when planning trade entries and calculating maximum stop-loss levels, ultimately enhancing risk management.

█ USER INPUTS

Trading Account Size: Total dollar value of the user's trading account.

Acceptable Risk (%): Maximum percentage of the trading account that the user is willing to risk per trade.

ATR Multiplier for Stop-Loss: Multiplier used to determine the distance of the stop-loss from the current price, based on the ATR value.

ATR Length: The length of the lookback period used to calculate the ATR value.

Show Target Risk Row: Toggle to hide/show the Target Risk Row

SL Levels Display: Option to see Both, Long Only, Short Only, or None of the Stop Loss Level Values.

Contract Point Value ($): Point value per contract. Tooltip highlights common values.

Tick Size: Minimum Price Movement (Default set to 0.25)

Minimum Contracts: Override the Minimum Contracts per trade to a user selected value.

(May Exceed User's Target Risk)

Displacement Intelligence Channel (DIC) @darshaksscThe Displacement Intelligence Channel (DIC) is a clean, minimal, non-repainting analytical tool designed to help traders observe how price behaves around its dynamic equilibrium.

It does not generate buy/sell signals, does not predict future price movement, and should not be interpreted as financial advice.

All calculations are based strictly on confirmed historical bars.

⭐ What This Indicator Does

Price constantly fluctuates between expansion (large moves) and compression (small moves).

The DIC analyzes these changes through:

Displacement (how far price moves per bar)

ATR response (how volatility reacts over time)

Dynamic width calculation (channel widens or tightens as volatility changes)

EMA-based core midline (a smooth equilibrium reference)

The result is a smart two-line channel that adapts to market conditions without cluttering the chart.

This is NOT a fair value gap, moving average ribbon, or premium/discount model.

It is a purely mathematical displacement-ATR engine.

⭐ How It Works

The indicator builds three elements:

1. Intelligence Midline

A smooth EMA that acts as the channel’s core “equilibrium.”

It gives a stable reference of where price is gravitating during the current session or trend.

2. Adaptive Upper Boundary

Calculated using displacement + ATR.

When volatility increases, the channel expands outward.

When volatility compresses, the channel tightens.

3. Adaptive Lower Boundary

Mirrors the upper boundary.

Also expands and contracts based on market conditions.

All lines update only on confirmed bar closes, keeping the script non-repainting.

⭐ What to Look For (Purely Analytical)

This indicator does not imply trend continuation, reversal, or breakout.

Instead, here’s what traders typically observe:

1. Price Reactions Around the Midline

Price often oscillates around the midline during equilibrium phases.

Strong deviation from the midline highlights expansion or momentum phases.

2. Channel Expansion / Contraction

Wider channel → increased volatility, displacement, and uncertainty

Tighter channel → compression and calm conditions

Traders may use this for context only — not for decision-making.

3. Respect of Channel Boundary

When market structure respects the upper/lower channel lines, it simply indicates volatility boundaries, not overbought/oversold conditions.

⭐ How to Add This Indicator

Open TradingView

Select any chart

Click Indicators → Invite-Only Scripts / My Scripts

Choose “Displacement Intelligence Channel (DIC)”

The channel will appear automatically on the chart

⭐ Recommended Settings (Optional)

These settings do not change signals (because the indicator has none).

They only adjust sensitivity:

Center EMA Length (default 34)

Smoother or faster midline

Displacement Lookback (default 21)

Controls how much recent displacement affects width

ATR Lookback (default 21)

Governs how volatility is interpreted

Min/Max Multipliers

Limits how tight or wide the channel can expand

Adjust them cautiously for different timeframes or asset classes.

⭐ Important Notes

This tool is non-repainting

It does not use future data

It does not repaint previous channel widths

It follows TradingView House Rules

It contains no signals, no alerts, and no predictions

The DIC is designed for visual context only and should be used as an analytical overlay, not as a stand-alone decision tool.

⭐ Disclaimer

This script is strictly for informational and educational purposes only.

It does not provide or imply any trading signals, financial advice, or expected outcomes.

Always do your own research and consult a licensed financial professional before making trading decisions.

TR-ATR-DATR+MAs shows the Range of selected Candle + 3 Moving Averages

True Range

Avg True Range

Daily Range

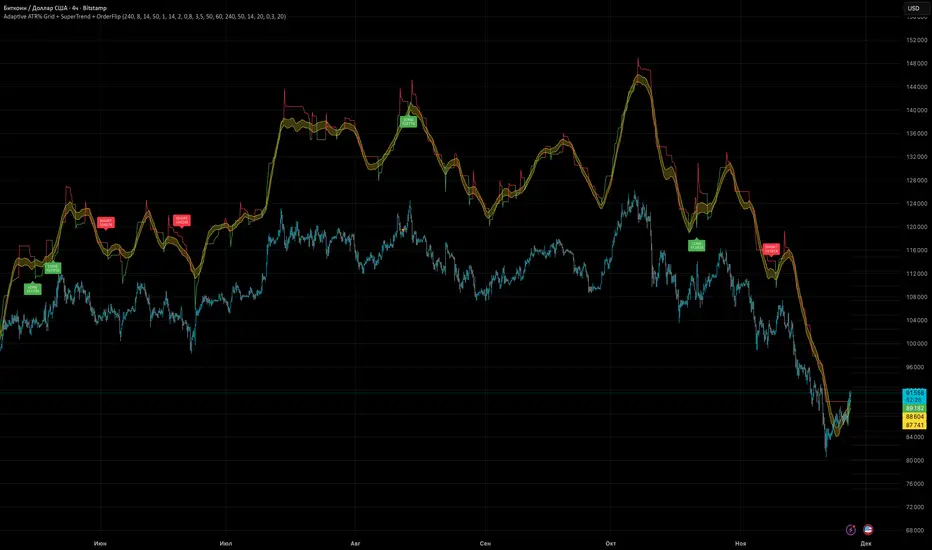

Adaptive ATR% Grid + SuperTrend + OrderFlipDescription:

This indicator combines multiple technical analysis tools to identify key price levels and trading signals:

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

OrderFlip – identifies price reversal points relative to a moving average with ATR-based sensitivity, optionally filtered by OBV and DMI.

MTF Confirmation – multi-timeframe trend verification using EMA to reduce false signals.

Signal Labels – "LONG" and "SHORT" labels appear on the chart with an offset from the price for better visibility.

JSON Alerts – ready-to-use format for automated alerts, including price, SuperTrend direction, Fair Zone, and ATR%.

Features:

Fully compatible with Pine Script v6

Lines and signals are fixed on the chart, do not shift with new bars

Configurable grid, ATR, SuperTrend, and filter parameters

Works with MTF analysis and classic indicators (OBV/DMI)

Usage:

Best used with additional indicators and risk management strategies. ATR% Grid is ideal for both positional trading and intraday setups.

перевод на русский

Описание:

Этот индикатор объединяет несколько методов технического анализа для выявления ключевых уровней цены и сигналов на покупку/продажу:

Сетка ATR% (ATR% Grid) – автоматическое построение уровней поддержки и сопротивления на основе текущей цены и волатильности (ATR). Позволяет видеть потенциальные цели и зоны входа/выхода.

SuperTrend – классический трендовый индикатор с адаптивным множителем ATR, который корректируется на основе средней волатильности.

OrderFlip – определение моментов разворота цены относительно скользящей средней с учетом ATR, с возможностью фильтрации по OBV и DMI.

MTF-подтверждение – проверка направления тренда на нескольких таймфреймах с помощью EMA, чтобы снизить ложные сигналы.

Сигнальные метки – на графике появляются "LONG" и "SHORT" с отступом от цены для наглядности.

JSON Alerts – готовый формат для автоматических уведомлений, включающий цену, направление SuperTrend, Fair Zone и ATR%.

Особенности:

Поддержка Pine Script v6

Линии и сигналы закреплены на графике, не двигаются при обновлении свечей

Настраиваемые параметры сетки, ATR, SuperTrend и фильтров

Совместимость с MTF-анализом и классическими индикаторами OBV/DMI

Рекомендации:

Используйте в сочетании с другими индикаторами и стратегиями управления риском. Сетка ATR% отлично подходит для позиционной торговли и интрадей.

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

[CT] ATR Chart Levels From Open ATR Chart Levels From Open is a volatility mapping tool that projects ATR based price levels directly from a user defined center price, most commonly the current session open, and displays them as clean horizontal levels across your chart. The script pulls an Average True Range from a higher timeframe, by default the daily, using a user selectable moving average type such as SMA, EMA, WMA, RMA or VWMA. That ATR value is then used as the unit of measure for all projected levels. You can choose the ATR length and timeframe so the bands can represent anything from a fast intraday volatility regime to a smoother multi week average range.

The core of the tool is the center line, which is treated as zero ATR. By default this center is the current session open, but you can instead anchor it to the previous close, previous open, previous high or low, or several blended prices such as HLC3, HL2, HLCC4 and OHLC4, including options that use the minimum or maximum of the previous close and current open. From this center, the indicator builds a symmetric grid of ATR based levels above and below the zero line. The grid size input controls the spacing in ATR units, for example a value of 0.25 produces levels at plus or minus 25, 50, 75, 100 percent of ATR and so on, while the number of grids each side determines how far out the bands extend. You can restrict levels to only the upper side, only the lower side, or draw both, which is useful when you want to focus on upside targets or downside expansion separately.

The levels themselves are drawn as horizontal lines on the main price chart, with configurable line style and width. Color handling is flexible. You can assign separate colors to the upper and lower levels, keep the center line in a neutral color, and choose how the colors are applied. The “Cool Towards Center” and “Cool Towards Outermost” modes apply smooth gradients that either intensify toward the middle or toward the outer bands, giving an immediate visual sense of how extended price is relative to its average range. Alternatively, the “Candle’s Close” mode dynamically colors levels based on whether the current close is above or below a given band, which can help highlight zones that are acting as resistance or support in real time.

Each level is optionally labeled at its right endpoint so you always know exactly what you are looking at. The center line label shows “Daily Open”, or more generally the chosen center, along with the exact price. All other bands show the percentage of ATR and the corresponding price, for example “+25% ATR 25999.90”. The label offset input lets you push those tags a user defined number of bars to the right of the current price action so the chart remains clean while still keeping the information visible. As new bars print, both the lines and their labels automatically extend and slide to maintain that fixed offset into the future.

To give additional context about current volatility, the script includes an optional table in the upper right corner of the chart. This table shows the latest single period ATR value on the chosen higher timeframe alongside the smoothed ATR used for the bands, clearly labeled with the timeframe and ATR length. When enabled, a highlight color marks the table cells whenever the most recent ATR reading exceeds the average, making it easy to see when the market is operating in an elevated volatility environment compared to its recent history.

In practical trading terms, ATR Chart Levels From Open turns the abstract concept of “average daily range” into specific, actionable intraday structure. The bands can be used to frame opening range breakouts, define realistic intraday profit targets, establish volatility aware stop placement, or identify areas where price has moved an unusually high percentage of its average range and may be vulnerable to mean reversion or responsive flow. Because the ATR is computed on a higher timeframe yet projected on whatever chart you are trading, you can sit on a one minute or five minute chart and still see the full higher timeframe volatility envelope anchored from your chosen center price for the session.

Orbital Barycenter Matrix @darshaksscThe Orbital Barycenter Matrix is a visual, informational-only tool that models how price behaves around a dynamically calculated barycenter —a type of moving equilibrium derived entirely from historical price data.

Instead of focusing on signals, this indicator focuses on market structure symmetry, distance, compression, expansion, and volatility-adjusted movement.

This script does not predict future price and does not provide buy/sell signals .

All values and visuals come solely from confirmed historical data , in full compliance with TradingView policy.

📘 How the Indicator Works

1. Dynamic Barycenter (Core Mean Line)

The barycenter is calculated from a smoothed blend of historical price components.

It represents the center of mass around which price tends to oscillate.

This is not a forecast line—only a representation of historical average behavior.

2. Orbital Rings (Distance Zones)

Around the barycenter, the indicator draws several “orbital rings.”

Each ring shows a volatility-scaled distance from the barycenter using ATR-based calculations.

These rings help visualize:

How far price has drifted from its historical center

Whether price is moving in an inner, mid, or outer region

How volatility influences the spacing of the rings

Rings do not imply future targets and are informational only.

3. Orbital Extension Range

Beyond the outermost ring, a wider band (extension range) shows a high-volatility reference distance.

It represents extended displacement relative to past price behavior—not a projected target.

4. Orbit Trail (Motion Trace)

The Orbit Trail plots small circles behind price, helping visualize how price has moved through the orbital regions over time.

Colors adjust with “pressure” (distance from center), making compression and expansion easy to observe.

5. Satellite Nodes (Swing Markers)

Confirmed swing highs and lows (using fixed pivots) are marked as small dots.

Their color reflects the orbital zone they formed in, giving context to how significant or extended each pivot was.

These swing markers do not repaint because they use confirmed pivots.

6. Pressure & Distance Calculations

The indicator converts price displacement away from the barycenter into a pressure metric, scaled between 0%–100%.

Higher pressure means price is further from its historical center relative to volatility.

The dashboard displays:

Zone classification

ATR-based distance

Pressure level

A small intensity gauge

All are informational readings—no direction or forecast.

📊 Key Features

✔ Dynamic barycenter core

✔ Up to four orbital rings

✔ Informational orbital extension band

✔ Visual orbit trail showing recent movement

✔ Non-repainting satellite swing nodes

✔ Distance & pressure analytics

✔ Fully adjustable HUD

✔ Always-visible floating dashboard (screen-anchored)

✔ Zero repainting on confirmed elements

✔ 100% sourced from historical data only

✔ Policy-safe: no predictions, no signals, no targets

🎯 What to Look For

1. How close price is to the barycenter

This can reveal whether price is in:

The inner region

The mid zone

The outer region

The extended field

2. Pressure level

Shows how “stretched” price is relative to its past behavior.

3. Satellite nodes

Indicate where confirmed pivots formed and in which orbital band.

4. Ring interactions

Observe how price moves between rings—inside, outside, or oscillating around them.

5. Color changes in the orbit trail

These show changes in market compression/expansion.

🧭 How to Read the Indicator

Inner Orbit

Price close to its historical equilibrium.

Mid Orbit

Moderate displacement from typical range.

Outer Orbit

Historically extended movement.

Beyond Extension Field

Price has moved further than usual relative to historical volatility.

These are descriptive conditions only , not trade recommendations.

🛠 How to Apply It on the Chart

Use the barycenter to understand where price has historically balanced.

Observe how volatility changes the spacing between rings.

Use pressure readings to identify when price is compressed, neutral, or extended.

Use swing nodes to contextualize historical pivot formation.

Watch how price interacts with rings to better understand rhythm, velocity, and structural behavior.

This tool is meant to enhance visual understanding—not to generate trade entries or exits.

⚠️ Important Disclosure

This indicator is strictly informational.

It does not predict or project future price movement.

It does not provide buy/sell/long/short signals.

All lines, zones, and values are derived solely from past market data.

Any interpretation is at the user’s discretion.

Dynamic Fair-Value Ribbon Pro @darshakssc1. What This Indicator Is (In Simple Terms)

The Dynamic Fair-Value Ribbon Pro is a visual tool that helps you see how price behaves around a statistically derived “fair-value zone”:

A colored ribbon/cloud marks a central “fair” area.

Areas above the ribbon are labeled as “Unfair High Zone”.

Areas below the ribbon are labeled as “Unfair Low Zone”.

A small state panel tells you where price currently sits relative to this ribbon.

All calculations are based only on historical price, volume, and volatility.

It does not predict future price, does not give buy/sell signals, and is not financial advice.

2. Adding the Indicator

Open a chart on TradingView.

Click on Indicators .

Search for “Dynamic Fair-Value Ribbon Pro” .

Click to add it to your chart.

You will see:

A cloud/ribbon around price.

Colored bars when price is outside the ribbon.

A panel in the top right describing the current state.

3. Core Concept: Fair vs Unfair Zones (Analytical Only)

The indicator tries to answer a descriptive question:

“Where is price trading relative to a historically derived central area?”

It does this by:

Calculating a central value (“fair mid”).

Building a band around that mid.

Coloring the chart depending on whether price is inside or outside that band.

It is not claiming that:

Price “must” return to the band.

Price is “overvalued” or “undervalued”.

Any state is good or bad.

It is simply a visual classification tool .

4. Engine Modes — How the Ribbon Is Calculated

Under “Fair-Value Engine” you can choose:

4.1 Mode 1: Range

Looks back over a chosen number of bars (default: 100).

Finds the highest high and lowest low in that window.

Defines a central “slice” of that range as the fair-value ribbon :

Range Mode: Lower Percent → bottom boundary of the slice (e.g., 30%).

Range Mode: Upper Percent → top boundary of the slice (e.g., 70%).

Effect:

The ribbon represents a middle portion of the historical range .

Above the ribbon = “Unfair High Zone” (analytical label only).

Below the ribbon = “Unfair Low Zone”.

This is purely statistical — it does not mean price is wrong or will revert.

4.2 Mode 2: VWAP + Stdev

In this mode, the central value is based on VWAP :

VWAP (Volume-Weighted Average Price) is used as the midline.

A standard deviation envelope is built around VWAP:

VWAP Mode: Stdev Multiplier controls how wide that envelope is.

Effect:

The ribbon shows where price is trading relative to a volume-weighted average .

Again, areas above and below are just described as “unfair” zones in a visual, analytical sense , not a predictive one.

5. ATR Adaptive Width — Making the Ribbon React to Volatility

Under “ATR Adaptive Width” :

Use ATR Adaptive Width:

On: the band width scales with volatility.

Off: band width stays fixed based on Range or VWAP settings.

ATR Length: how many bars to use for ATR.

Reference ATR (% of price): a reference level for normal volatility.

Min Width Scale / Max Width Scale: clamps the scaling so that the band doesn’t get too narrow or too wide.

What this does (analytically):

When volatility (ATR) is higher than the reference, the band can become wider .

When volatility is lower , the band can become narrower .

This is a mathematical rescaling only and does not imply any optimal levels or performance.

6. Visual Elements — What You See on the Chart

6.1 Fair-Value Ribbon (Cloud)

The cloud between Fair Ribbon Low and Fair Ribbon High is the fair zone .

Color can be changed via “Fair Ribbon Color” .

6.2 Midline

If “Show Center Line” is enabled:

A line runs through the middle of the ribbon.

In Range mode, this is the average of the upper and lower band.

In VWAP mode, it’s essentially the VWAP-based mid.

This line is for visual reference only and makes no claims about support, resistance, or reversion.

6.3 Bar Colors

Unfair High Zone: bars are colored with Unfair High Bar Color.

Unfair Low Zone: bars are colored with Unfair Low Bar Color.

Inside the ribbon:

If “Fade Bars Inside Fair Zone” is ON, bars may be more faded/neutral.

These colors are simply classification highlights ; they do not tell you what to do.

6.4 State Panel (Top Right)

If “Show State Panel” is enabled, you’ll see a small box that displays:

Current engine:

Range or VWAP+Stdev.

Current price state:

Inside Ribbon (Fair Zone)

Above Ribbon (Unfair High Zone)

Below Ribbon (Unfair Low Zone)

This is a quick summary of where price sits relative to the computed ribbon.

7. Typical Ways to Use It (Informational Only)

The indicator can help you visually:

See when price is spending time inside a historically defined central zone.

Notice when price is frequently trading outside that zone.

Compare different timeframes (e.g., 5m vs 1h vs 4h) to see how the fair zone shifts.

Experiment with:

Range length (shorter vs longer lookback).

VWAP vs Range mode.

ATR adaptation on/off.

Important:

Any interpretation of these visuals is entirely up to the user.

The script does not tell you to buy, sell, hold, or do anything specific.

8. Limitations and Important Notes

All calculations use past data only (price, volume, volatility).

The ribbon does not guarantee:

that price will revert,

that zones will hold,

or that any outcome will occur.

There are no built-in signals such as “long/short” or automatic entries/exits.

The script is best used as a supporting, visual layer alongside other tools or methods you choose.

9. Disclaimer

This indicator is:

Strictly informational and educational.

Not a trading system or strategy.

Not financial advice or a recommendation.

Not guaranteed to be accurate, complete, or suitable for any specific purpose.

Users should always perform their own research and due diligence.

Past behavior of any visual pattern or zone does not guarantee future behavior.

Average True Range % infoATR% is a modified version of the classic Average True Range indicator that displays price volatility as a percentage of the instrument's value, rather than in absolute values. This allows you to easily compare the volatility of different assets (e.g., Bitcoin vs Tesla stock) regardless of their price.

Main Features

1. ATR% Chart

The red line shows the average volatility from the last N candles (default 14), expressed as a percentage. For example:

ATR% = 2.5% means that the average daily move is approximately 2.5% of the asset's value

Higher values = greater volatility (higher profit potential, but also greater risk)

Lower values = lower volatility (calmer market)

2. Volatility Trend Analysis

The indicator automatically detects whether volatility is rising, falling, or stable:

Up arrow (↑) - volatility is rising (price becomes more "nervous")

Down arrow (↓) - volatility is falling (market is calming down)

Horizontal arrow (⮆) - volatility is stable (within ±3% of the moving average)

3. Information Table

In the upper right corner of the chart you will see Current ATR% value and Trend arrow with color coding:

- Green = rising volatility

- Red = falling volatility

- Gray = stable volatility

Parameters to Configure

Indicator Length (default: 14) - How many candles back to include in calculations:

Lower values (5-10): more sensitive to sudden changes, reacts faster

Higher values (20-30): more smoothed, shows long-term volatility picture

Trend Length (default: 10) - Period to analyze whether volatility is rising/falling:

Lower values: faster trend change signals

Higher values: more reliable, but slower signals

Sample Interpretations

ATR% Volatility Asset Type/Situation

< 1% Very low Stable blue-chip stocks, calm market

1-3% Low-medium Typical stocks, normal conditions

3-5% Medium-high Volatile stocks, cryptocurrencies at rest

5-10% High Cryptocurrencies, penny stocks

> 10% Extremely high Market panic, crash, pump & dump

ATR multiple from High & LowA simple numerical indicator measuring ATR multiple from recent 252 days high and low.

ATR multiples from high (and low) are used as a base in many systematic trading and trend following systems. As an example many systems buy after a 2.5–4 ATR multiple pullback in a strong stock if the regime allows it. This would then be paired with an entry tactic, for example buy as it recaptures the a pivot within the upper range, a MA or breaks out again after this mid term pullback/shakeout.

This indicator uses a function which captures the recent high and low no matter if we have 252 bars or not, which is not how standard high/low works in Tradingview. This means it also works with recent IPO:s.

I prefer to overlay the indicator in one of the lower panes, for example the volume pane and then right click on the indicator and select Pin to scale > No scale (fullscreen).

ATR Volatility AlertsOverview:

This is a dynamic alert tool based on the Average True Range (ATR), designed to help traders detect sudden price movements that exceed normal volatility levels. Whether you are trading breakouts or monitoring for abnormal spikes, this indicator visualizes these events on the chart and triggers system alerts when the price move exceeds your specified ATR multiplier.

Key Features:

Fully Customizable ATR Range:

You can adjust the ATR Length (Default: 14) and the Multiplier (Default: 1.5x).

Tip: Increase the multiplier (e.g., to 2.0 or 3.0) to catch only extreme volatility, or lower it for scalping smaller moves.

Visual Chart Signals:

Visual markers appear instantly when a bar's movement exceeds the ATR threshold.

Green Triangle: Indicates an Upward Spike.

Red Triangle: Indicates a Downward Spike.

Flexible System Alerts:

Designed to integrate seamlessly with TradingView's alert system. You can choose from three specific alert directions based on your strategy:

1.Price Spike Up: Triggers only on sharp upward moves.

2.Price Spike Down: Triggers only on sharp downward moves.

3.Bidirectional Volatility Alert: Triggers on BOTH huge pumps and dumps.

How to Set Alerts:

Click the "Create Alert" button in TradingView.

Select ATR Volatility Alerts in the "Condition" dropdown.

Choose the specific logic you need:

· Select Price Spike Up for bullish monitoring.

· Select Price Spike Down for bearish monitoring.

· Select Bidirectional Volatility Alert to watch for any volatility expansion.

Two Supertrend Crossover SignalThis indicator is designed to visualize trend shifts using two Supertrend lines and a crossover-based signal system.

It also colors the area between the two Supertrend lines based on the current trend direction, making trend changes easy to identify at a glance.

How It Works

The indicator plots:

Fast Supertrend (shorter ATR length, lower factor)

Slow Supertrend (longer ATR length, higher factor)

A crossover between these two Supertrend lines indicates a possible trend shift.

Buy Signal

A BUY signal occurs when: Fast Supertrend crosses ABOVE Slow Supertrend

This suggests bullish momentum strengthening.

Sell Signal

A SELL signal occurs when: Fast Supertrend crosses BELOW Slow Supertrend

This suggests bearish momentum increasing.

Buy/Sell Signal Labels

The chart displays clear BUY (green) and SELL (red) labels at every crossover.

These signals help traders quickly pinpoint potential entries or exits.

This indicator is ideal for:

✓ Trend trading

✓ Swing trading

✓ Identifying momentum shifts

✓ Visual confirmation of market direction

✓ Combining with price action or EMA filters

You may adjust ATR length and multiplier depending on the timeframe:

For Scalping (1–5 min):

Fast ATR: 5–7

Slow ATR: 10–14

For Intraday (5–15 min):

Fast ATR: 7

Slow ATR: 10–14

For Swing Trading (1h–4h):

Fast ATR: 10

Slow ATR: 20

Important Notes

This indicator does not repaint the Supertrend values.

Signals are based on confirmed crossovers.

Use stop-loss and risk management appropriate for your strategy.

Always combine with market context (support/resistance, volume, etc.)

The Bear & Bull TieWhat it does:

Bear & Bull Tie is a moving average crossover indicator that identifies trend reversals and generates entry/exit signals based on the relationship between price and three simple moving averages (SMA 21, SMA 55, SMA 89). The indicator combines these three MAs into an Average Moving Average (AMA) to confirm directional bias, then uses ATR (Average True Range) volatility measurement for dynamic position sizing and stop-loss placement.

How it works:

The indicator operates on a simple but effective principle: it enters a bullish trend when price closes above all three moving averages simultaneously, and enters a bearish trend when price closes below all three MAs simultaneously. This "three MA alignment" approach filters out noise and confirms genuine trend changes. The indicator then plots:

Entry levels at the highest MA during uptrends or lowest MA during downtrends

Stop-loss zones calculated using 2x ATR distance from entry prices

Trend confirmation fill between price and the Average Moving Average, color-coded blue for bullish and red for bearish

The ATR-based stop-loss sizing adapts to market volatility, making it suitable for different market conditions and timeframes.

How to use it:

Monitor the filled zones to visually confirm your trend bias

Watch for alerts when new long or short setups form; entry prices and ATR-based stops are displayed on the chart

Trade the zones between your entry level and stop-loss zone, adjusting position size based on your risk tolerance

Exit when colors reverse to indicate trend termination

The indicator works best on higher timeframes (1H and above) where trend clarity is stronger and false signals are reduced.

Alerts: FOR AUTOMATION / NOTIFICATION's (create an alert for B/B tie (2, 4) that uses Any Alert / Function Call )

Long Positions:

entries ---> "Bull Tie on NVDA | Entry : 100.5 | ATR Stop : 99.5"

exits ------> "Bull Tie on NVDA | Exit : 110.1"

Short Positions:

entries ---> "Bear Tie on NVDA | Entry : 120.05 | ATR Stop : 85.05"

exits -----> "Bear Tie on NVDA | Exit : 100"

Credits:

This script incorporates concepts and code portions from @LOKEN94 with his explicit permission. Special thanks for the foundational logic that inspired this development.

Disclaimer:

This indicator is for educational and analytical purposes. It is not financial advice. Past performance does not guarantee future results. Always manage risk properly and use stops. Test thoroughly on historical data before live trading.

Energy Meter (Candle Range/ATR Ratio)Purpose:

This indicator is a simple, intuitive way to visualize auction energy — the actual force behind a price move — rather than just its appearance on the chart. It’s built on a single idea:

If a bar travels farther than normal in its fixed amount of time, something pushed harder than usual.

That “push” is auction energy, and it’s the raw material of microstructure inference: reading intent and imbalance from nothing more than candles, tempo, and volatility.

Traditional indicators focus on price patterns or volume. This one focuses on pressure — the underlying imbalance driving each bar.

How It Works

Each bar’s True Range is divided by its ATR, producing a normalized ratio:

1.0 = Average energy

>1.2 (default) = Above-normal energy

<1.0 = Quiet, low-pressure bars

This ratio is plotted as a histogram to highlight bursts of force, with a smoothed line added to show the tempo of recent energy changes.

When the histogram spikes, you’re seeing the auction flash its teeth: aggression, initiative, failed absorption, breakout ignition, or the first punch of a reversal.

When the line rolls over, you’re seeing the engine lose torque.

It’s a minimalist tool for seeing who is actually winning the auction, even when price looks deceptively calm.

Why It Matters

Price moves because of imbalance, not geometry. Two candles that look identical can represent completely different internal dynamics.

This indicator helps you see:

Breakout strength vs. fakeouts

Acceleration vs. drift

Exhaustion after extended runs

Reversal attempts with real intent

Quiet absorption before explosive moves

Shifts in aggression hidden inside consolidation

For new traders, it’s a clean introduction to microstructure inference — extracting meaningful order-flow insights without needing L2, DOM, or volume profile.

For experienced traders, it's a compact impulse detector that complements trend, volatility, and liquidity models.

Summary

This is a lightweight, first-principles tool designed to expose the energy signature of the auction: how hard the market is trying to go somewhere.

It doesn’t predict direction — it reveals pressure, so you can judge the quality of the move you’re trading.

Energy beats geometry.

Intent beats patterns.

Microstructure is hiding in every candle; this indicator makes it visible.

ATRP & Volatility Table - AIMAN93The ATRP & Volatility Table is a simple yet powerful tool designed to quantify market volatility and help traders adapt their position sizing accordingly.

It calculates the Average True Range Percentage (ATRP) — the ATR value relative to current price — and classifies market conditions into three volatility levels: LOW, MEDIUM, or HIGH. Based on the volatility level, it suggests an indicative risk percentage to guide your trade management.

This visual tool displays real-time ATRP, volatility classification, and corresponding risk percentage in a compact on-chart table. Ideal for systematic traders who rely on volatility-based decision-making, position sizing, or risk management models.

Features:

- Dynamic ATRP calculation for any symbol or timeframe

- Customizable colors for text and background

- Automatic volatility classification (low / medium / high)

- Suggested risk percentage for each volatility level