yangwen1.0This script is an initial concept of mine. I attempted to use the 5-minute chart as ticks for catching bottoms and picking tops, but it's unable to avoid whipsaws. I've tested many methods to evade whipsaws, but they ultimately result in poor entry points, causing me to miss the bottoms and tops of price swings. I sincerely hope someone with better approaches can discuss this with me. Thank you.

Jalur dan Saluran

AkdakTrading1Script using M5 Order Blocks with an FVG and the first blocks of an impulse to take trades with a 1:1 risk-reward.

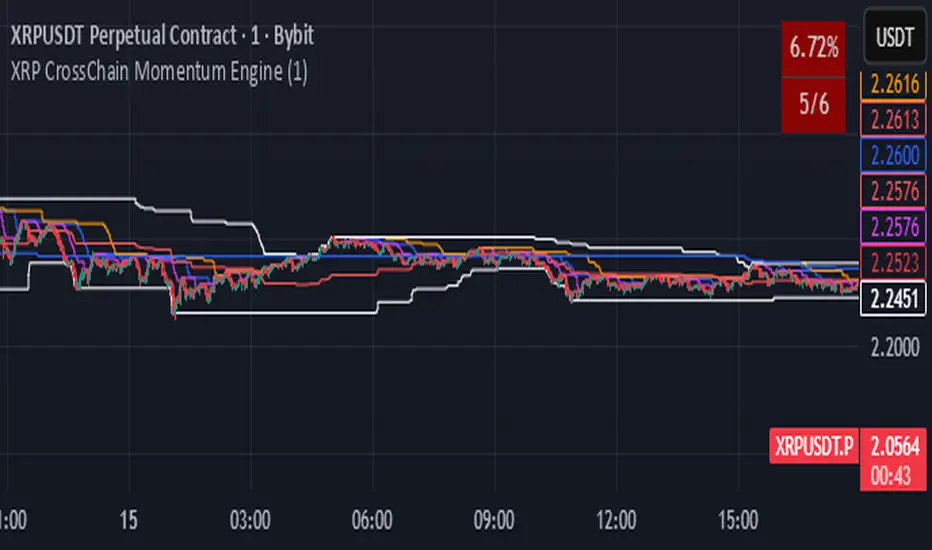

XRP CrossChain Momentum EngineThis is a strategy with stop loss 3% , leverage 4 and no pyramiding. It works great with XRP and other coins with similar price, but i suggest XRP. Profit in 1 year around 900% and profit in 2 years around 2000% as you can see in the pictures. I have initial capital 1000 but it can change.

盯盘-平均K线图This is a Pine Script v6 indicator/strategy designed to assist traders with clear, configurable trend and momentum signals. It combines adaptive filters and volatility-aware logic to highlight high‑quality entries and exits, includes optional multi‑timeframe confirmation, and supports risk controls such as stop loss/target levels. Signals are visualized directly on the chart with arrows/labels and can trigger TradingView alerts for real‑time notifications. The tool offers smoothing and sensitivity settings to tune responsiveness, overlay mode for price action, and strategy mode for backtesting performance. It’s built to be lightweight, transparent, and easy to adjust, helping traders streamline decision‑making while maintaining control over parameters and risk.

Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!

Fibo Tarayıcı + Mirror + Bot

KEY FEATURES:

1. Fibonacci Levels: Plots 23.6%, 38.2%, 50%, 61.8%, 78.6%, 88.6%, 100%, 127.2%, 141.4%, 161.8% levels

2. Mirror Fibonacci: Shows reverse extensions of main levels

3. Auto Trading System: Executes automatic trades at specified Fibonacci levels

4. Multi-Symbol Scanner: Scans 120+ crypto and stock symbols

5. Visual Alerts: Colored background and labels when price approaches Fibonacci levels

HOW IT WORKS:

1. Finds swing high/low points over 144 bars

2. Calculates Fibonacci levels between these points

3. Generates buy/sell signals when price approaches these levels

4. User can select which levels to trade

5. Scanner shows Fibonacci signals across multiple symbols

Kev's RSI2 SMA50 Strategy⭐ Kev’s RSI2 SMA50 Strategy — Institutional Edition (TSX Optimized + RR Filter)

A professional swing-trading system based on Larry Connors’ RSI(2) mean-reversion framework, optimized for TSX equities. Designed for Daily timeframe trading with institutional trend alignment, volatility filtering, and strict risk-reward controls.

📌 Overview

This strategy enhances the classic RSI(2) setup with:

• Strong trend confirmation (SMA50 + Weekly SMA50)

• Deep pullback detection (RSI2 < 3)

• Structural swing-based stop-loss

• Fixed 2R profit target (non-repainting)

• Optional Connors RSI (CRSI) confirmation

• Volatility filtering via ATR range

• Mechanical, deterministic, no-discretion rules

Works best on TSX large & mid-caps, ETFs, and liquid equities.

🔍 Core Philosophy

Buy strong stocks on pullbacks → Price must be above SMA50 + Weekly SMA50.

Pullback must be statistically meaningful → RSI(2) < 3.

R:R must justify the trade → Swing-low SL + 2R target with structural room to hit TP.

🧠 Entry Conditions (Non-Repainting)

• RSI(2) < 3 → Identifies extreme short-term oversold dips.

• SMA50 Filter → Ensures uptrend alignment.

• Weekly HTF Filter (Default = 1W) → Confirms broader trend direction.

• ATR Filter → Rejects volatile bars (range < ATR(14) × 2.2).

• Optional:

– SMA50 Slope (positive trend strength)

– Bullish Reversal Candle

– Connors RSI < 20 (deep pullback confirmation)

🎯 Risk Management

All levels are locked at entry and never repaint.

• Swing-Low SL (last 5 bars)

• 2R Profit Target = Entry + (Risk × 2)

• R:R Feasibility Filter → Only enters if recent swing high is above TP.

• Optional RSI Exit → Exit when RSI2 > 90 (enabled by default).

• Optional SMA Exit (disabled by default) → Conservative early exit.

📈 Visuals

The script plots:

• SMA50

• Weekly SMA50

• Swing-Low SL (fixed)

• 2R TP (fixed)

• Optional SMA exit line

All are non-repainting and update only on confirmed bars.

🔔 Alerts

Buy Signal → All entry filters aligned (RSI2, SMA50, HTF, ATR, RR check).

Exit Signal → 2R hit, SL hit, RSI exit, or SMA exit (if enabled).

🧭 Recommended Usage

• Timeframe: Daily

• HTF: Weekly (default)

• Best For: TSX equities, mid/large-cap stocks, ETFs

• Style: Short-term swing trading (1–10 bars)

• Avoid: Low-volume tickers, microcaps, crypto, biotech, news-driven spikes.

🛑 Notes

• All HTF data uses lookahead_off → non-repainting.

• Rules are fully mechanical and deterministic.

• Position sizing uses % equity by default.

• This script is for educational purposes only and not financial advice.

• Always forward-test before using live capital.

Semi-Martingala Sicura 1.20x PROIncrements or a maximum amount of 200. If the previous trade is profitable, the count is reset and the initial amount is resumed. Exit management uses fixed percentage stop loss and take profit, set relative to the entry price. In summary, this strategy aims to capitalize on trend and momentum signals, using a semi-martingale system to increase positions in case of losses, but with precise limits to contain risk. Note: This method aims to be "safer" than a classic martingale, respecting increment limits and a maximum amount.

Comment by saying what you think and what I could change.

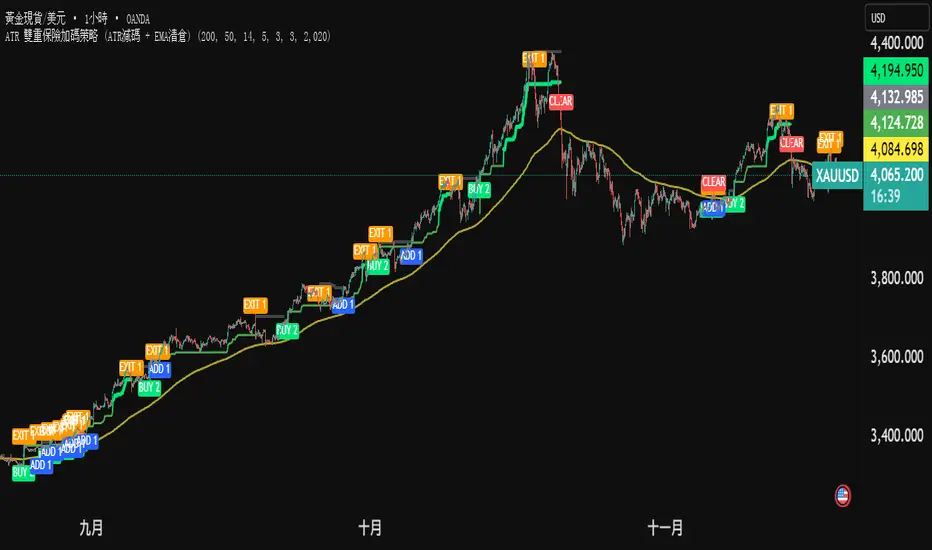

ATR 雙重保險加碼策略 (ATR減碼 + EMA清倉) (三寶爸黃金版)黃金雙保險戰法 (兩口單策略)

核心概念: 進場買兩口。一口賺了就跑(保本),一口死抱到底(拚大賺)。

1. 進場 (買 2 口):

只要價格站上黃線,而且突破前高。

別猶豫,直接買 2 口。

2. 減碼 (賣 1 口):

價格回檔碰到綠線。

代表短線轉弱,先賣掉 1 口。

好處: 錢先放口袋,心裡踏實。

3. 加碼 (買回 1 口):

如果你手上只剩 1 口,結果行情沒死,又創新高。

代表剛才賣錯了,趕快買回 1 口 (補回滿倉)。

好處: 繼續跟著趨勢賺錢。

4. 清倉 (全跑):

價格跌破黃線。

代表趨勢真的結束了,不管剩幾口,全部賣掉。

一句話總結: 「震盪時先賣一半保命,趨勢噴出時永遠滿倉在車上。」

Gold Dual-Insurance Tactic (2-Lot System)

Core Concept: Enter with 2 lots. Sell one early to lock in profits (Play Safe), and hold the other to catch the big wave (Go Big).

1. Entry (Buy 2 Lots):

When price is above the Yellow Line AND breaks the previous High.

Don't hesitate. Buy 2 lots immediately.

2. Scale Out (Sell 1 Lot):

When price pulls back and hits the Green Line.

This means short-term weakness. Sell 1 lot.

Benefit: Put money in your pocket. Peace of mind.

3. Add Position (Buy Back 1 Lot):

If you have only 1 lot left, but the market hits a New High.

It means the trend is alive. Quickly Buy back 1 lot (refill to full position).

Benefit: Continue maximizing profits with the trend.

4. Clear All (Exit Everything):

When price falls below the Yellow Line.

The trend is officially over. Sell everything, no matter what.

Faraz Perfect Structure XL / XS (Trend-Filtered)Faraz’s Perfect Structure XL/XS identifies premium trend continuation and reversal setups using a three-filter system:

structural breakouts using dynamic swing-based support/resistance,

trend confirmation via 200-EMA slope,

momentum validation through RSI and MACD.

Signals only trigger when all factors align, eliminating noise, chop, and false signals.

Designed for traders who want clean, high-probability long (XL) and short (XS) entries.

Intellect TBTS V02 [Strategy]📌 Intellect V01 TBO – Trend Breakout Options Strategy

Intellect V01 TBO is an intraday trend-breakout strategy designed for index traders who follow Nifty, BankNifty, and FinNifty.

It identifies trend shifts using structural pivots, adaptive trendlines, and volatility-adjusted breakout zones.

The strategy provides automatic Long/Short signals, optional stop-loss and target projections, and allows users to generate alert messages that include index-option strike information.

🔍 How the Strategy Works

1. Pivot-Based Structure

The script identifies short-term high and low pivots using a user-defined period.

These pivots become anchor points for constructing directional trendlines.

2. Dynamic Trendline Projection

For each pivot, the script builds:

A projected trendline

Two offset lines above/below

A volatility band based on ATR

These help detect potential breakout zones.

3. Breakout Signal Logic

A trade signal is generated when price crosses the projected trendline:

Long Signal – detected when price breaks above a pivot-derived trendline.

Short Signal – detected when price breaks below a pivot-derived trendline.

Users may optionally restrict entries to a specific time window.

🎯 Stop-Loss & Target Zones

When a trade is active:

SL and TP levels are set using ATR-based volatility distance

Levels appear visually on the chart if enabled

Exits occur automatically when TP/SL is hit

The strategy also closes open trades near the end of the session (default 3:10 PM)

These levels are for visual and backtesting support only.

📝 Index Option Strike Calculation (For Alert Text Only)

The strategy can dynamically compute:

ATM strike (with optional bias)

Correct expiry day for Nifty (weekly) and BankNifty/FinNifty (monthly Tuesday)

CE strike for Long signals

PE strike for Short signals

This strike information is only included in alert text for users who configure external automation.

It does not affect backtesting results inside TradingView.

⏱️ Time Window Filter (Optional)

Users may define:

Start time

End time

Outside this window, no new trades are generated.

🎛️ User Adjustable Inputs

Pivot lookback period

Trendline style and extension

Display of target/stop-loss

Expiry selection mode

Strike-bias

Lot size (for alert formatting only)

Time filter settings

🔔 Alert Messages

Alerts include:

Direction (Long/Short)

Strike details

Option type (CE/PE)

Quantity

A formatted JSON message

TradingView does not execute these orders.

Users are responsible for managing external automation independently.

⚠️ Important Notes

This script does not integrate with any broker by default.

It does not place trades automatically; alerts only send text.

Backtests simulate index movement, not live option pricing.

We recommend using realistic slippage and commission settings.

✔️ This strategy is intended for educational and analytical use. Adjust settings as needed.

✅ 2. CLEAN CHART BEFORE PUBLISHING

To avoid moderator flags:

Do This Before Publishing:

✔ Remove all manual drawings

✔ Hide any other indicators on the chart

✔ Use light or clean background

✔ Keep only signals/SL/TP from your script

If you leave extra drawings, moderators may hide the script again.

✅ 3. FINAL PUBLISHING CHECKLIST

Before you click Publish, verify:

✔ Description matches the one above

✔ No broker names anywhere

✔ No "algo trading" or "automation" advertising

✔ Backtest settings are realistic

Commission enabled

Slippage > 1

Reasonable lot assumption

✔ Chart is clean

✔ Script is set to “Strategy” and compiles without warnings

AutoTrader v3.0[by Irum]1. 스크립트 목적 / 정의

1-1. 한글 설명

이 스크립트의 목적

15분봉 BTC/USDT 같은 레버리지/선물 환경에서,

“EMA 재돌파 + BB 스퀴즈 국면”에서만 진입하고,

상위 추세(레짐 필터) + ATR 기반 리스크/수량 + ATR 트레일링 + 부분청산을 한 번에 관리하는 “올인원 자동 전략”입니다.

핵심 특징:

진입 로직

EMA(기본 9) 를 기준으로

종가가 EMA를 위로 돌파(골든크로스) & BB 폭이 좁을 때 → Long 진입 후보

종가가 EMA를 아래로 돌파(데드크로스) & BB 폭이 좁을 때 → Short 진입 후보

이걸 “Re-break + Squeeze” 구조로 설계해서,

변동성이 줄었다가 방향이 다시 나오려는 시점만 노립니다.

레짐 필터(Regime Filter)

상위 타임프레임(기본 1시간봉 HTF EMA 200)의 기울기와

ATR 빠른 선/느린 선으로

상승 추세 + 변동성 살아있는 구간만 Long 허용

하락 추세 + 변동성 살아있는 구간만 Short 허용

즉, 역추세 매매를 최대한 차단하고, 추세 방향만 따라갑니다.

Pivot 기반 손절 + ATR 리스크 기반 수량(ATR Sizing v2.1)

최근 swing low/high(피벗) 또는 일정 구간 fallback low/high를 기준으로 기술적 손절선을 잡고,

그 손절까지의 거리를 이용해,

“한 번의 손절 시 계좌의 riskPct%만 잃도록” 수량을 자동 계산합니다.

ATR 스파이크(갑작스러운 변동성 폭발) 구간은 진입 자체를 피하려고 합니다.

R-multiple 기반 TP + 부분 청산 + ATR Ladder 트레일링

진입 시점의 위험(R = Entry - SL) 을 기준으로

R 배수 기준 부분청산(예: 1R에서 50% 청산)

R 배수 기준 최종 TP(예: 2R)

포지션이 잘 가면 ATR 기반 트레일링 스탑(ATR Ladder) 을 적용해서,

이익 구간에서 손절선을 점점 끌어올려 BE(본전 이상) → 수익 보호 모드로 전환합니다.

세션 필터 / 뉴욕 뉴스피크 회피용 세션 회피

사용자가 정한 세션 안에서만 매매하거나,

특정 뉴스 타임(예: CPI, FOMC 근처 시간대)을 회피하도록 시간대를 차단할 수 있습니다.

1-2. English Description

Purpose

This strategy is an all-in-one auto-trading system designed mainly for leveraged/futures markets (e.g., BTC/USDT 15m) that:

Enters only on EMA re-break + Bollinger Band squeeze

Uses higher timeframe regime filter for trend direction

Sizes positions with ATR-based risk (v2.1)

Manages exits with R-multiple partial TP + final TP + ATR ladder trailing stop

Key points:

Entry Logic

Uses a fast EMA (default 9).

When price crosses above EMA and BB width is below threshold (squeeze) → Long signal.

When price crosses below EMA and BB width is below threshold → Short signal.

So it focuses on volatility contraction → re-expansion setups.

Regime Filter

Uses HTF EMA (default 200 EMA on 60m) slope + fast vs slow ATR:

Only allow long trades in uptrend + active volatility

Only allow short trades in downtrend + active volatility

This is to avoid counter-trend trading and align with macro trend.

Pivot-based SL + ATR Sizing v2.1

Sets SL using recent pivot highs/lows with a minimum buffer.

Computes risk per unit and chooses quantity so that riskPct % of equity is lost at SL.

Filters out trades during ATR spikes (abnormally large volatility).

R-multiple TP + Partial + ATR Ladder Trailing

Uses the initial risk (R) to:

Take partial profit at partialRR R (e.g., 1R at 50% size).

Set final TP at finalRR R or a fixed % TP.

Uses ATR ladder trailing to progressively tighten stops as price moves in favor.

Session / News Avoidance

Optionally trade only inside a custom session,

Or avoid specific time windows (e.g., high-impact news).

Seawolf Pivot Hunter [Strategy]Overview

Seawolf Pivot Hunter is a practical trading strategy that enhances the classic pivot-box breakout system with a structured risk-management framework. Using ATR-based stop loss and take-profit calculations, position sizing, multi-layer filtering, and daily loss-limit protection, it provides a stable and sustainable trading environment. It preserves the strengths of the original version while adding systems designed to manage real-market risks more effectively.

Core Philosophy

The most important element in trading is not generating profits but controlling losses. Even the best entry signals cannot compensate for a single large loss that wipes out accumulated gains. This strategy precisely calculates the risk exposure for every trade and includes multiple layers of protection to safeguard the account under worst-case scenarios.

Indicator Setup Link

kr.tradingview.com

Example of Optimal Parameter Settings

Asset (Exchange): ETH/USDT (Binance)

Timeframe: 15-minute chart

Pivot Detection Length: 5

Upper Box Width: 2

Lower Box Width: 2

Enable Risk Management: False

Use Trailing Stop: False

Use Volume Filter

-Min Buy Volume % for Long: 50

-Min Sell Volume % for Short: 50

Use Trend Filter (EMA): False

Enable Max Loss Protection

-Max Daily Loss ($): 200

-Max Trades Per Day: 10

Calculated Bars: 50,000

Risk-Management System

Every trade automatically receives a stop-loss level at the moment of entry. The stop is calculated using ATR, adjusting dynamically to market volatility. When volatility increases, the stop widens; in stable conditions, it tightens to reduce unnecessary exits. The default distance is set to twice the ATR.

The standard take-profit level is set to four times the ATR, providing a 1:2 risk-reward structure. With this ratio, even a 50 percent win rate can produce profitability—while the typical trade structure aims for small losses and larger gains to support long-term performance.

A trailing-stop option is also available. Once the trade moves into profit, the stop level automatically trails behind price action, protecting gains while allowing the position to expand when momentum continues.

Position size is calculated automatically based on the selected risk percentage. For example, with a 2 percent risk setting, each stop-loss hit would result in exactly 2 percent of the account balance being lost. This ensures a consistent risk profile regardless of account size.

The daily loss-limit function prevents excessive drawdown by halting new trades once a predefined loss threshold is reached. This helps avoid emotional decision-making after consecutive losses.

A daily trade-limit feature is included as well. The default is 10 trades per day, protecting traders from overtrading and unnecessary fees.

Filtering System

The volume filter analyzes buying and selling pressure within the pivot box. Long trades are allowed only when buy volume exceeds a specified percentage; shorts require sell-volume dominance. The default threshold is 55 percent.

The trend filter uses an EMA to determine market direction. When price is above the 200-EMA, only long signals are permitted; when below, only shorts are allowed. This ensures alignment with the broader trend and reduces counter-trend risk.

Each filter can be toggled independently. More filters generally reduce trade frequency but improve signal quality.

Real-Time Monitoring

A real-time statistics panel displays daily profit/loss, the number of trades taken, the maximum allowed trades, and whether new trades are currently permitted. When daily limits are reached, the panel provides clear visual warnings.

Entry Logic

A trade is validated only after a pivot-box breakout occurs and all active filters—volume, trend, daily loss limit, and daily trade limit—are satisfied. Position size, stop loss, and take-profit levels are then calculated automatically. Entry arrows and labels on the chart help with later review and analysis.

Setup Guide

Risk percentage is the most critical setting. Beginners should start at 1 percent. Anything above 3 percent becomes aggressive.

ATR stop-loss multipliers should reflect asset volatility.

ATR take-profit multipliers determine reward ratio; 4.0 is the standard.

Volume thresholds are typically set between 50–60 percent depending on market conditions.

Daily loss limits are typically 2–5 percent of the account.

Trading Strategy

This strategy performs best in trending environments and works especially well on the 4-hour and daily charts. New users should begin with all filters enabled and trade conservatively. A minimum of one month of paper trading is recommended before committing real capital.

Suitable Users

The strategy is ideal for beginners who lack risk-management experience as well as advanced traders seeking a customizable structure. It is particularly helpful for traders who struggle with emotional decision-making, as pre-defined limits and rules enforce discipline.

Backtesting Guide

Use at least 2–3 years of historical data that includes bullish, bearish, and sideways conditions.

Target metrics:

Sharpe ratio: 1.5 or higher

Maximum drawdown: below 25 percent

Win rate: 40 percent or higher

Total trades: at least 100 for statistical relevance

Optimization Precautions

Avoid over-fitting parameters. Always test values around the “best” setting to verify stability.

Out-of-sample testing is essential for confirming robustness.

Test across multiple assets and timeframes to ensure consistency.

Live Deployment Roadmap

After successful backtesting, follow a gradual rollout:

Paper trading for at least one month

Small-account live testing

Slow scaling as performance stabilizes

Continuous Improvement

Keep a detailed trading journal and evaluate performance each quarter using recent data.

Adapt settings as market conditions evolve.

Conclusion

Seawolf Pivot Hunter aims to provide more than simple trade signals—it is designed to create a stable and sustainable trading system built on disciplined risk management. No strategy is perfect, and long-term success depends on consistency, patience, and strict adherence to rules. Start small, verify results, and scale progressively.

Disclaimer

This strategy is for educational and research purposes only. Past performance does not guarantee future results. All trading decisions are the responsibility of the user.

개요

Seawolf Pivot Hunter는 기본 피봇 박스 브레이크아웃 전략에 전문적인 리스크 관리 시스템을 더한 실전형 트레이딩 전략입니다. ATR 기반의 손절매와 목표가 설정, 포지션 사이징, 다층 필터링 시스템, 일일 손실 제한 기능을 통해 안정적이고 지속 가능한 트레이딩 환경을 제공합니다. 기본 버전의 장점은 유지하면서 실제 시장에서 발생할 수 있는 위험을 체계적으로 관리할 수 있도록 설계되었습니다.

핵심 철학

트레이딩에서 가장 중요한 것은 수익이 아니라 손실 관리입니다. 아무리 훌륭한 진입 조건이 있어도 한 번의 큰 손실로 모든 수익이 사라질 수 있습니다. 이 전략은 각 거래마다 감수할 리스크를 명확히 계산하고, 최악의 상황에서도 계좌를 보호하기 위한 다양한 안전장치를 제공합니다.

지표 적용 링크 공유

kr.tradingview.com

최적 조건값 설정(예시)

"종목(거래소): ETH/USDT(Binance)", "15 분봉 기준"

-Pivot Detection Length: 5

-Upper Box width: 2

-Lower Box width: 2

-Enable Risk Management: False

-Use Trailing Stop: False

-Use Volume Filter

-Min Buy Volume % for Long: 50

-Min Buy Volume % for Long: 50

-Use Trend Filter(EMA): False

-Enable Max Loss Protection

-Max Daily Loss($): 200

-Max Trades Per Day: 10

-Calucated bars: 50000

리스크 관리 시스템

모든 거래는 진입과 동시에 손절매 주문이 자동 설정됩니다. 손절가는 ATR을 기준으로 계산되며, 시장의 변동성에 따라 자동으로 조정됩니다. 변동성이 큰 시장에서는 넓은 손절폭을, 안정적인 시장에서는 좁은 손절폭을 사용해 불필요한 청산을 줄입니다. 기본값은 ATR의 2배입니다.

목표가는 ATR의 4배를 기본값으로 설정하여 손익비 1:2 구조를 유지합니다. 승률이 50퍼센트만 되어도 수익성이 가능하며, 실제로는 손절은 짧고 이익은 길게 가져가는 방식으로 장기 성과를 확보합니다.

트레일링 스톱 기능도 제공됩니다. 포지션이 수익 구간에 들어서면 손절가가 자동으로 함께 움직이며 수익을 보호합니다. 이 기능은 사용자가 켜거나 끌 수 있습니다.

포지션 크기는 리스크 퍼센트 기반으로 자동 계산됩니다. 예를 들어 리스크를 2퍼센트로 설정하면 손절 시 계좌 자산의 2퍼센트만 잃도록 수량이 조절됩니다. 계좌 크기와 무관하게 항상 일정한 비율의 리스크만 감수하게 되는 방식입니다.

일일 손실 제한 기능은 하루에 허용 가능한 최대 손실을 초과하지 않도록 합니다. 지정 금액에 도달하면 당일 거래는 더 이상 실행되지 않습니다. 감정적 거래를 막고 일정한 규율을 유지하도록 돕습니다.

일일 거래 횟수 제한 기능도 제공됩니다. 기본값은 하루 10회로, 과매매와 수수료 증가를 방지합니다.

필터링 시스템

볼륨 필터는 박스 구간 내 매수·매도 압력을 분석해 진입 신호를 검증합니다. 롱은 매수 볼륨이 일정 비율 이상일 때, 숏은 매도 볼륨이 우세할 때만 진입합니다. 기본값은 55퍼센트입니다.

추세 필터는 EMA를 사용하며, 가격이 200EMA 위에 있을 때는 롱 신호만, 아래에서는 숏 신호만 허용합니다. 큰 추세 방향에만 거래하여 역추세 리스크를 줄입니다.

필터는 독립적으로 켜고 끌 수 있으며, 필터가 많을수록 거래 횟수는 줄지만 신호 품질은 향상됩니다.

실시간 모니터링

화면에 실시간 통계 테이블이 표시되며, 일일 손익, 거래 횟수, 최대 허용 횟수, 현재 거래 가능 여부가 즉시 확인됩니다. 손실 제한 또는 거래 제한 도달 시 시각적으로 표시됩니다.

진입 로직

피봇 박스 브레이크아웃 발생 후 볼륨 필터, 추세 필터, 일일 손실·거래 제한을 모두 통과하면 포지션 크기를 계산하고 손절·목표가를 설정한 뒤 진입합니다. 진입 지점에는 화살표와 레이블이 표시되어 분석에 도움을 줍니다.

설정 가이드

리스크 퍼센트는 가장 중요한 설정입니다. 초보자는 1퍼센트를 추천하며 3퍼센트 이상은 위험합니다.

손절 ATR 배수는 자산 특성에 맞게 조절합니다.

목표가 ATR 배수는 손익비를 결정하며 기본값은 4.0입니다.

볼륨 비율은 시장 상황에 따라 50~60퍼센트 내외로 조정합니다.

일일 손실 제한은 계좌의 2~5퍼센트 수준이 적절합니다.

사용 전략

추세가 명확한 시장에서 가장 효과적이며, 4시간봉 또는 일봉을 추천합니다. 초반에는 모든 필터를 켜고 보수적으로 시작하며, 최소 한 달간 페이퍼 트레이딩을 권장합니다.

적합한 사용자

리스크 관리 경험이 부족한 초보자부터, 커스터마이징을 원하는 경험자까지 폭넓게 적합합니다. 감정적 트레이딩을 억제하는 기능이 있어 규율 유지가 어렵던 트레이더에게 특히 유용합니다.

백테스트 가이드

최소 2~3년 데이터로 테스트하며, 상승·하락·횡보 모두 포함해야 합니다.

샤프비율 1.5 이상, 최대 낙폭 25퍼센트 이하를 목표로 합니다.

승률은 40퍼센트 이상이면 충분합니다.

최소 100회 이상 거래가 있어야 통계적으로 의미가 있습니다.

최적화 주의사항

과최적화를 피하고 주변 값도 테스트해야 합니다.

샘플 외 기간 검증은 필수입니다.

여러 자산·여러 시간대에서 테스트하여 일관성을 확인해야 합니다.

실전 적용 로드맵

백테스트 후 바로 실전 투입하지 말고, 한 달 이상의 페이퍼 트레이딩 → 소액 실전 → 점진적 확대 순으로 진행합니다.

지속적 개선

일지를 기록하고 분기마다 최신 데이터로 점검합니다.

시장 변화에 따라 유연하게 조정해야 합니다.

마치며

Seawolf Pivot Hunter는 단순 신호 제공을 넘어, 안전하고 지속 가능한 트레이딩 환경 구축을 목표로 합니다. 어떤 전략도 완벽할 수 없으며, 장기적 성공을 위해서는 규칙 준수와 인내가 가장 중요합니다. 충분한 검증을 거쳐 작은 금액으로 시작하고 점진적으로 확장해나가는 접근을 추천합니다.

면책 조항

이 전략은 교육 및 연구 목적이며, 과거 성과는 미래를 보장하지 않습니다. 모든 투자 결정은 본인의 판단과 책임 하에 이루어져야 합니다.

RSI BREAKOUT SIGNALSThis BB + RSI Breakout indicator is designed to help traders identify potential buy and sell opportunities based on price movements relative to the Donchian channel (or Bollinger-type channel) and momentum conditions. It calculates the highest high and lowest low over a user-defined length to form a dynamic channel, and then it checks whether the current price breaks above the upper band (for a buy signal) or below the lower band (for a sell signal). To avoid repeated signals in a row, the indicator uses a state system: after a buy signal occurs, it will not generate another buy until a sell occurs, and vice versa. When a buy signal is triggered, it automatically calculates a take-profit price a certain percentage above the buy candle and displays this price below the candle as a “TP” label. Sell signals are displayed above the candle, and any previous TP label is cleared. The indicator updates in real time, so the signals move with the chart, giving a clear and lag-free visualization of entry points and potential profit targets.

Cognex Fibonacci Breakout StrategyTHE COMPLETE TRADE LOGIC (What We Want):

Step 1: Morning Session (9:30-10:30)

Track session high and low

Step 2: After 10:30 - Wait for Breakout

Bullish: Close above session high

Bearish: Close below session low

Step 3: Track Extreme After Breakout

Keep updating highest_after_breakout or lowest_after_breakout

This continuously updates as price makes new extremes

Step 4: Detect 28% Retracement (THE LOCK)

When price retraces to 28%, set last_extreme_for_retracement to the current extreme

This LOCKS the extreme for fibonacci calculations

fib_100 should use this locked value

Step 5: Place Limit Order EARLY (at 20% retracement)

When price retraces to 20%, place limit order at 28% entry

This is so the order is ready when price hits 28%

Step 6: Cancel & Recalculate if New Extreme

If price makes a NEW extreme AFTER the order is placed

Cancel the old order

Wait for new 20% retracement to place new order

Step 7: One Trade Per Day

Only ONE order placement attempt per day

Even if cancelled, don't try again

TSI.LTA | Base BTC 1DTSI.LTA | Base BTC 1D is a closed‑source trend‑following strategy designed for BTC on the 1D timeframe .

It focuses on participating in the main directional moves of the market while avoiding as much short‑term noise as possible.

📊 The script:

Uses a combination of moving‑average–based filters and volatility bands to define the active trend.

Applies optional volume filters to avoid low‑participation or exhausted moves.

Includes risk‑management controls (Stop Loss, Take Profit, Trailing Stop) that work on a per‑trade basis.

All entries and exits are confirmed at bar close and the script does not repaint .

This makes it suitable for backtesting, alerts and external automation.

█ 💡 CONCEPTS

This strategy is built around a few simple ideas:

1 — Trend first.

Positions are only taken when a group of smoothed trend filters agree on direction.

The goal is to ride larger swings, not to scalp each fluctuation.

2 — Volatility awareness.

Standard‑deviation–based bands help avoid entries in abnormal spikes or during very compressed ranges.

3 — Participation filter.

Optional volume‑based conditions (VWMA, OBV slope, MFI, volume Z‑score) try to ensure that entries occur when the market shows enough activity, not during dead phases.

4 — Risk defined in advance.

Stop‑loss and trailing‑stop inputs are expressed as percentages relative to entry price, so users can align them with their own risk tolerance.

The logic is purposely conservative: it is expected to stay flat during parts of the market where the trend is unclear or participation is weak.

█ ⚙️ FEATURES & INPUTS

This section follows approximately the order of the script’s inputs, so users can read here and then match what they see in the “Inputs” tab.

1 — 📐 Trend filters

These inputs control how the strategy detects the underlying trend:

DEMA / Gaussian / SMMA lengths

Control how fast or slow the trend reacts to price changes.

Shorter lengths → more responsive, more trades, more noise.

Longer lengths → slower reaction, fewer trades, more filtering.

Volatility Bands (SD length & multipliers)

Standard‑deviation bands around the smoothed price series.

They are used to avoid entries during extreme moves or very narrow ranges where a breakout is not yet confirmed.

In practice, these settings let the user choose between a more “aggressive” trend follower (shorter lengths, smaller bands) or a more “patient” one.

2 — 📊 Volume filters (optional)

These filters are meant to restrict trades to periods where the market shows meaningful participation:

VWMA filter

Requires price to be aligned with a Volume‑Weighted Moving Average, which de‑emphasizes moves on very low volume.

OBV slope filter

Uses the slope of On‑Balance Volume to check that net volume flow supports the direction of the trade.

MFI band filter

Uses the Money Flow Index to avoid taking new entries in zones that often correspond to exhaustion (extreme values defined by the user).

Volume Z‑Score

Compares current volume to its recent history. Trades can be restricted when volume is unusually low or out of character for that period.

When any of these filters are turned off, the strategy relies only on price‑based trend and volatility logic.

When they are on, trades are more selective and may be fewer.

3 — 🛡️ Risk management

These inputs define how individual trades are managed once entered.

They do not change the trend logic itself:

Stop Loss (%)

A percentage move against the entry price that will close the position.

Typical values on BTC 1D remain in the single‑digit range so that no single trade risks an unrealistic portion of equity.

Take Profit (%)

An optional fixed target that closes the trade when price has moved a chosen percentage in favor.

This can be disabled if the user prefers to let the trend filters perform the exit.

Trailing Stop (%)

A stop that follows the most favorable price reached since entry.

When the “use lower timeframe peak” option is enabled, peaks can be detected on a lower timeframe for more granular trailing, while decisions still occur at the close of the 1D bar.

Fixed SL/TP Price and Activation Date

Allow defining absolute price levels and a date from which they start applying.

This is useful when the user wants structural protection around known price zones.

The combination of these controls determines how deep a pullback the user is willing to tolerate and how much profit they are prepared to give back in order to stay in trends.

4 — 🚫 Filter failure & cooldown

To avoid over‑trading in difficult environments, the script can:

Automatically exit when filters remain unfavorable for a configurable number of bars.

Enter a cooldown period, during which no new trades are taken, even if some conditions improve.

These mechanisms are intended to protect capital during choppy or low‑quality phases rather than force constant exposure.

█ 📚 HOW TO USE

A suggested process for using this strategy as a study tool:

1 — Start on BTC 1D.

Apply the script to BTCUSD or BTC/USDT on the 1D timeframe, with default inputs.

2 — Open the Strategy Tester.

Choose a time window (for example a full halving cycle, a crash + recovery period, or just the most recent bull leg).

3 — Compare with Buy & Hold.

For the same window, look at:

Net profit of the strategy vs Buy & Hold.

Max drawdown of the strategy vs Buy & Hold.

The goal is not to hit a particular number, but to see whether, in that window, the strategy manages to:

Provide a smoother equity curve (lower drawdown),

While still performing at least as well as, or better than, simply holding the asset.

4 — Experiment with risk inputs.

Vary Stop Loss, Trailing Stop and the volume filters.

After each change, re‑check the same two questions above. This should make clear how each input affects the trade‑off between participation and risk.

5 — Forward‑test.

Before using any configuration with real capital, let it run for a while in paper‑trading or demo conditions.

█ 🚧 LIMITATIONS

The strategy is built and tuned primarily for BTC on 1D.

It can be used on other symbols and timeframes, but behavior may differ and requires new testing.

In very tight ranges or during event‑driven gaps, trend logic may enter later than discretionary trading would. This is expected for a conservative trend‑following approach.

Results from historical backtests depend on data quality, broker settings, fees and slippage configured in the Strategy Tester.

█ 📝 NOTES

Signals are generated on bar close.

The script is closed‑source, but the description explains the main ideas so users and moderators can understand what it does and how to use it.

The HUD on the chart is meant as a compact summary of the same statistics available in the Strategy Tester; it simply makes comparisons quicker.

█ ⚠️ DISCLAIMER

This strategy is provided for educational and research purposes only .

It is not financial advice and does not recommend any specific trades, assets, position sizes, or risk levels.

Users are fully responsible for:

Choosing their own risk parameters (Stop Loss, Take Profit, Trailing Stop, position sizing, etc.).

Testing the script on the markets and timeframes they intend to trade.

Verifying that any configuration is appropriate for their capital, risk tolerance and jurisdiction.

Past performance in backtests or examples does not guarantee future results.

Always test carefully before considering any live deployment.

Moving Average Band StrategyOverview

The Moving Average Band Strategy is a fully customizable breakout and trend-continuation system designed for traders who need both simplicity and control.

The strategy creates adaptive bands around a user-selected moving average and executes trades when price breaks out of these bands, with advanced risk-management settings including optional Risk:Reward targets.

This script is suitable for intraday, swing, and positional traders across all markets — equities, futures, crypto, and forex.

Key Features

✔ Six Moving Average Types

Choose the MA that best matches your trading style:

SMA

EMA

WMA

HMA

VWMA

RMA

✔ Dynamic Bands

Upper Band built from MA of highs

Lower Band built from MA of lows

Adjustable band offset (%)

Color-coded band fill indicating price position

✔ Configurable Strategy Preferences

Toggle Long and/or Short trades

Toggle Risk:Reward Take-Profit

Adjustable Risk:Reward Ratio

Default position sizing: % of equity (configurable via strategy settings)

Entry Conditions

Long Entry

A long trade triggers when:

Price crosses above the Upper Band

Long trades are enabled

No existing long position is active

Short Entry

A short trade triggers when:

Price crosses below the Lower Band

Short trades are enabled

No existing short position is active

Clear entry markers and price labels appear on the chart.

Risk Management

This strategy includes a complete set of risk-controls:

Stop-Loss (Fixed at Entry)

Long SL: Lower Band

Short SL: Upper Band

These levels remain constant for the entire trade.

Optional Risk:Reward Take-Profit

Enabled/disabled using a toggle switch.

When enabled:

Long TP = Entry + (Risk × Risk:Reward Ratio)

Short TP = Entry – (Risk × Risk:Reward Ratio)

When disabled:

Exits are handled by reverse crossover signals.

Exit Conditions

Long Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Short Exit

Stop-Loss Hit (touch-based)

Take-Profit Hit (if enabled)

Reverse Band Crossover (if TP disabled)

Exit markers and price labels are plotted automatically.

Visual Tools

To improve clarity:

Upper & Lower Band (blue, adjustable width)

Middle Line

Dynamic band fill (green/red/yellow)

SL & TP line plotting when in position

Entry/Exit markers

Price labels for all executed trades

These are built to help users visually follow the strategy logic.

Alerts Included

Every trading event is covered:

Long Entry

Short Entry

Long SL / TP / Cross Exit

Short SL / TP / Cross Exit

Combined Alert for webhook/automation (JSON-formatted)

Perfect for algo trading, Discord bots, or automation platforms.

Best For

This strategy performs best in:

Trending markets

Breakout environments

High-momentum instruments

Clean intraday swings

Works seamlessly on:

Stocks

Index futures

Commodities

Crypto

Forex

⚠️ Important Disclaimer

This script is for educational purposes only.

Trading involves risk. Backtest results are not indicative of future performance.

Always validate settings and use proper position sizing.

EMA VIP STRThis strategy works on EMAS and standard deviation on both sides , the tp is decided on RSI levels. the strategy is a systematic trading setup

Fractional Candlestick Long Only Experimental V10Fractional Candlestick Long-Only Strategy – Technical Description

This document provides a professional English description of the "Fractional Candlestick Long Only Experimental V6" strategy using pure CF/AB fractional kernels and wavelet-based filtering.

1. Fractional Candlesticks (CF / AB)

The strategy computes two fractional representations of price using Caputo–Fabrizio (CF) and Atangana–Baleanu (AB) kernels. These provide long-memory filtering without EMA approximations. Both CF and AB versions are applied to O/H/L/C, producing fractional candlesticks and fractional Heikin-Ashi variants.

2. Trend Stack Logic

Trend confirmation is based on a 4-component stack:

- CF close > AB close

- HA_CF close > HA_AB close

- HA_CF bullish

- HA_AB bullish

The user selects how many components must align (4, 3, or any 2).

3. Wavelet Filtering

A wavelet transform (Haar, Daubechies-4, Mexican Hat) is applied to a chosen source (e.g., HA_CF close). The wavelet response is used as:

- entry filter (4 modes)

- exit filter (4 modes)

Wavelet modes: off, confirm, wavelet-only, block adverse signals.

4. Trailing System

Trailing stop uses fractional AB low × buffer, providing long-memory dynamic trailing behavior. A fractional trend channel (CF/AB lows vs HA highs) is also plotted.

5. Exit Framework

Exit options include: stack flip, CF

Трендовые линии с продвинутыми стопамиtrend analysis strategy can work in every trend on the market.

Fractional Candlestick Long Only Experimental V4 Another example of use an idea of Fractional Candlestick , based on mathematical rules of Fractional Calculus , typical kernel Caputo-Fabrizio ( CF ) and Atangana-Baleanu is used, alfa factor ( esential for calculation ) is in range 0,1-0.9.

Let's fun with this script .