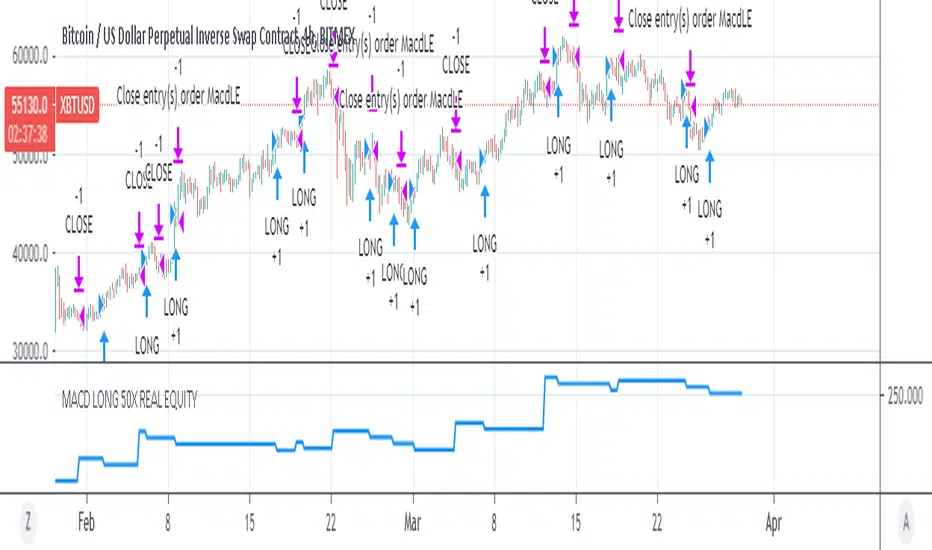

MACD 50x Leveraged Long Strategy Results with Real Equity Hello there.

I was looking for a way to simulate leveraged transactions in Tradingview and this script came out.

You can examine the equity graph without looking at the strategy results.

Thus, the facts will come to light.

Strategy parameters:

Adding margin: Forbidden or not specified. (Add Margin : No)

Position size: (for each trade) 1%

Stop-Loss: (2%)

Long: macd crossover

Exit: macd crossunder

Or ofc touching the stop-Loss value as predicted.

Warning: This strategy simulation is for Long direction only.

Regards.

Beyondtechnicalanalysis

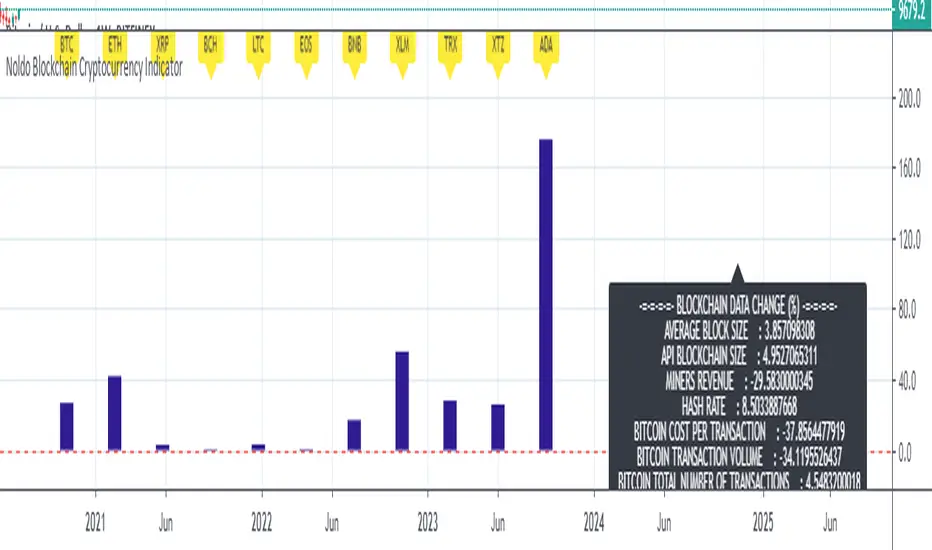

Noldo Blockchain Cryptocurrency Indicator

Hello, this script has the same logic as Noldo CFTC COT Forex Indicator :

And Noldo CFTC COT Commodities Indicator :

*

Script briefly calculates the period length between two signals of Pivot Reversal Strategy when new signal arrives and allows us to see relative Blockchain data and price changes of Major Cryptocurrencies over that automatic length.

This saves us from the hassle and time wasting of searching for a reference point.

Usage

This script works only on all Bitcoin / U.S Dollar pairs and futures.

It only works on 1W graphics.

ICOT data are pulled via Quandl

NOTE :

Since blockchain data is very votalile, 7-day ema values are adjusted to take into account.

Regards.

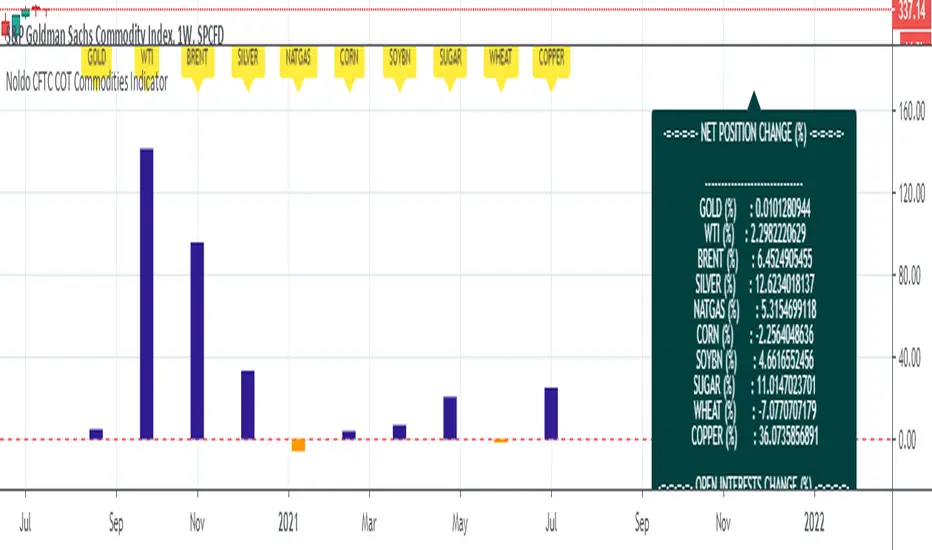

Noldo CFTC COT Commodities IndicatorHi.

Hello, this script has the same logic as Noldo CFTC COT Forex indicator :

It is the version for the future markets.

Major future assets are the subject.

Usage

This script works only on SPGSCI (S&P Goldman Sachs Commodity Index).

You must open SPGSCI :

www.tradingview.com

It only works on 1W graphics.

Because COT data is announced on Tuesday, it will cause repaint every Tuesday.

However, since it is a terminal, this factor is not strong enough to affect your decisions.

For use, you should open the bottom panel, go a little to the right in the history section and enlarge the panel you have opened.

The terminal will take its form in the presentation and provide analysis on the big screen.

COT data are pulled via Quandl.

Regards.

Funamental and financialsEarnings and Quarterly reporting and fundamental data at a glance.

A study of the financial data available by the "financial" functions in pinescript/tradingview

As far as I know, this script is unique. I found very few public examples of scripts using the fundamental data. and none that attempt to make the data available in a useful form

as an indicator / chart data. The only fitting category when publishing would be "trend analysis" We are going to look at the trend of the quarterly reports.

The intent is to create an indicator that instantly show the financial health of a company, and the trends in debt, cash and earnings

Normal settings displays all information on a per share basis, and should be viewed on a Daily chart

Percentage of market valuation can be used to compare fundamentals to current share price.

And actual to show the full numbers for verification with quarterly reporting and debuggging (actual is divided by 1.000.000 to keep numbers readable)

Credits to research study by Alex Orekhov (everget) for the Symbol Info Helper script

without it this would still be an unpublished mess, the use of textboxes allow me to remove many squiggly plot lines of fundamental data

Known problems and annoyances

1. Takes a long time to load. probably the amount of financial calls is the culprit. AFAIK not something i can to anything about in the script.

2. Textboxes crowd each other. dirty fix with hardcoded offsets. perhaps a few label offset options in the settings would do?

3. Only a faint idea of how to put text boxes on every quarter. Need time... (pun intended)

Have fun, and if you make significant improvements on this, please publish, or atleast leave a comment or message so I can consider adding it to this script.

© sjakk 2020-june-08

Macroeconomic Artificial Neural Networks

This script was created by training 20 selected macroeconomic data to construct artificial neural networks on the S&P 500 index.

No technical analysis data were used.

The average error rate is 0.01.

In this respect, there is a strong relationship between the index and macroeconomic data.

Although it affects the whole world,I personally recommend using it under the following conditions: S&P 500 and related ETFs in 1W time-frame (TF = 1W SPX500USD, SP1!, SPY, SPX etc. )

Macroeconomic Parameters

Effective Federal Funds Rate (FEDFUNDS)

Initial Claims (ICSA)

Civilian Unemployment Rate (UNRATE)

10 Year Treasury Constant Maturity Rate (DGS10)

Gross Domestic Product , 1 Decimal (GDP)

Trade Weighted US Dollar Index : Major Currencies (DTWEXM)

Consumer Price Index For All Urban Consumers (CPIAUCSL)

M1 Money Stock (M1)

M2 Money Stock (M2)

2 - Year Treasury Constant Maturity Rate (DGS2)

30 Year Treasury Constant Maturity Rate (DGS30)

Industrial Production Index (INDPRO)

5-Year Treasury Constant Maturity Rate (FRED : DGS5)

Light Weight Vehicle Sales: Autos and Light Trucks (ALTSALES)

Civilian Employment Population Ratio (EMRATIO)

Capacity Utilization (TOTAL INDUSTRY) (TCU)

Average (Mean) Duration Of Unemployment (UEMPMEAN)

Manufacturing Employment Index (MAN_EMPL)

Manufacturers' New Orders (NEWORDER)

ISM Manufacturing Index (MAN : PMI)

Artificial Neural Network (ANN) Training Details :

Learning cycles: 16231

AutoSave cycles: 100

Grid

Input columns: 19

Output columns: 1

Excluded columns: 0

Training example rows: 998

Validating example rows: 0

Querying example rows: 0

Excluded example rows: 0

Duplicated example rows: 0

Network

Input nodes connected: 19

Hidden layer 1 nodes: 2

Hidden layer 2 nodes: 0

Hidden layer 3 nodes: 0

Output nodes: 1

Controls

Learning rate: 0.1000

Momentum: 0.8000 (Optimized)

Target error: 0.0100

Training error: 0.010000

NOTE : Alerts added . The red histogram represents the bear market and the green histogram represents the bull market.

Bars subject to region changes are shown as background colors. (Teal = Bull , Maroon = Bear Market )

I hope it will be useful in your studies and analysis, regards.

Whale Trading SystemThis script is an advanced version of the distributional blocks script.

In distributional buys and sells:

I used a high - low cloud filter, which makes it more prudent to sell the next sell higher for sells and to buy the next purchase lower for buys.

I also used the Stochastic Money Flow Index function because it also uses volume to separate regions.

The long period is 52 weeks, which is equal to one year,

The short period is one-fourth of its value, which is equal to a financial quarter.

Then the values calculated with these periods are calculated by stochastic - rsi logic within the function, giving us two averages and separating the regions according to crossovers and crossunders .

In buys and sales, the higher your next distributional position size makes your profit more .

In the old system, there was a confusion as it was not divided into zones.

Because we divide into zones here, zone changes are the last stop to free up existing positions, and you must reopen each time you change zones.

And I changed standard distribution days, depending on the price change and the histogram, as StochMFI also took into account the volume.

In this way, there is sustainability.

I am also sharing my educational idea that explains the logic of this system in more detail :

Now that we have been divided into regions, a maximum of 10 pieces will suffice us.

And the regional shifts will allow us to sell and buy all of our position size, and now we will feel much more comfortable.

The most timeframe I find most accurate are the weekly bars.

Even in the example, we see how we have benefited from the sharp drop in bitcoin, while the price is falling, and we have lowered the average with higher-weight purchases than the previous one.

In both buys and sales here, both the histogram intensities and the average of the purchases you have reduced with the transactions, or the earnings you have increased with the sales, guide you.

In areas with high volatility ,if we adjust our positions properly, even if we follow the changes in the region, we will get rid of those situations with few wounds and we will surely catch the trend!

NOTE : Crossover/crossunder and distributional buy/sell alerts added.

Best regards , Noldo.

Customizable MACD (how to detect a strong convergence)Helloooo traders

I wondered once if a MACD was based on an EMA/EMA/SMA or SMA/SMA/EMA (or WHATEVA/WHATEVA/WHATEVA).

Seems they're so many alternatives out there.

I decided to empower my audience more by choosing the type of moving averages you want for your MACD.

More options doesn't always mean better performance - but who knows - some might find a config that they like with it for their favorite asset/timeframe.

I added also a multi-timeframe component because I'm a nice guy ^^

Convergence is my BEST friend

An oscillator (like MACD) is to measure how strong a momentum is - generally, traders use those indicators to confirm a trend.

So understand that a MACD (or any other indicator not based on convergence ) won't likely be sufficient for doing great on the market.

Combined with your favorite indicator, however, you may get great results.

My indicators fav cocktail is mixing :

1) an oscillator (momentum confirmation)

2) a trendline/key level break (momentum confirmation)

3) adding-up on a different trading method but still converging with the first entry.

The reason I'm deep with convergence detection is because I'm obsessed with removing those fakeout signals. You know which ones I'm talking about :)

Those trades when the market goes sideways but our capital goes South (pun 100% intended) - 2 days later, the price hasn't changed much but some lost some capital due to fees, being overexposed, buying the top/selling the bottom of a range they didn't identify.

It's publicly known that ranges are the worst traders' enemy. It's boring, not fun, and .... end up moving in the direction we expected when we go to sleep or outside.

NO ONE/BROKER/EX-GF is tracking your computer - I checked also for mine as it happened for me way too often in the past.

I surely preferred blaming a few external unknown conditions than improving my TA back in the days #bad #dave

But my backtest sir...

Our backtests show what they're being told to show . A backtest without a stop-loss/hard exit logic will show incredible results.

Then trying that backtest with live trading is like in the Matrix movie - discovering the real world is tough and we must choose between the blue pill (learning how to evaluate properly risk/opportunity caught) and the red pill (increasing the position sizing, not setting a stop loss, holding the positions hoping for the best)

Last few words

Convergences aren't invented because it's cool to mix indicators with others. (it is actually and even fun)

They're created to remove most of the fakeouts . For those that can't be removed - a strong risk management would cut most of the remaining potential big losses.

No system works 100% of the time - so a convergence system needs a back-up plan in case the converged signal is wrong (could be stop-loss, hard exit, reducing position sizing, ...)

Wishing you the BEST and happy beginning of your week

Daveatt

ANN GOLD WORLDWIDE This script consists of converting the value of 1 gram and / or 1 ounce of gold according to the national currencies into a system with artificial neural networks.

Why did I feel such a need?

Even though the printed products in the market are digitally circulated, only precious metals are available in full or near full.

Silver is difficult to carry because you have to buy too much because the unit price is low.

Platinum is very difficult to find and used in industry.

Gold is both practical and has less volatile movements, even more balanced than dollars, to preserve the value of money.

Uncertainty and tensions benefit gold.

Obviously this is my own opinion and is not worth the investment advice:

If there is to be an economic crisis, it is obvious that the dollar will rise against the emerging currencies, but I expect a crisis where gold and the dollar will rise together.

The world has been on a mercantilist line more than ever!

Spot gold can be bought from goldsmiths and banks.

I think this command will benefit people everywhere but in economies that are subject to developing currencies.

Now we can look at the details:

All you have to do is load the appropriate chart and select it from the menu.

Thus, the system will adjust itself to that instrument.

MENU and Tickers :

"GOLD" : XAUUSD or GC1! or GOLD (Average error = 0.0128)

"GOLDSILVER" : XAUXAG or GOLDSILVER (Gold Silver Ratio ) ( Average error : 0.01 )

"GOLD CZK " : XAUUSD/USDCZK ( 1 Ounce Gold Czech Koruna) ( Average error = 0.010879 )

"GOLD NZD " : XAUUSD/USDNZD ( 1 Ounce Gold New Zealand Dollar ) (Average error = 0.010736 )

"GOLD EURO" : XAUUSD/USDEUR ( 1 Ounce Gold Euro) ( Average error = 0.010000 )

"GOLD HUF " : XAUUSD/USDHUF ( 1 Ounce Gold Hungarian Forint ) ( Average error = 0.010000 )

"GOLD INR " : XAUUSD/USDINR (1 Ounce Gold Indian Rupee ) (Average error = 0.010458 )

"GOLD DKK" : XAUUSD/USDDKK (1 Ounce Gold Danish Krone) (Average error = 0.010671 )

"GOLD CHF" : XAUUSD/USDCHF (1 Ounce Gold Swiss Franc ) (Average error = 0.010967 )

"GOLD CNH" : XAUUSD/USDCNH(1 Ounce Gold Offshore RMB) (Average error = 0.012017 )

"GOLD MXN" : XAUUSD/USDMXN(1 Ounce Gold Mexican Peso) (Average error = 0.010000 )

"GOLD PLN" : XAUUSD/USDPLN (1 Ounce Gold Polish Zloty ) (Average error = 0.010173 )

"GOLD ZAR" : XAUUSD/USDZAR (1 Ounce Gold South African Rand (Average error = 0.010484 )

"GOLD NOK" : XAUUSD/USDNOK (1 Ounce Gold Norwegian Krone ) (Average error = 0.010842 )

"GOLD TRY" : XAUUSD/USDTRY (1 Ounce Gold Turkish Lira ) (Average error = 0.010000 )

"GOLD THB" : XAUUSD/USDTHB (1 Ounce Gold Thai Baht ) (Average error = 0.011747 )

Important note : XAUUSD/USDCUR = 1 Ounce Gold , XAUUSD/31.1*USDCUR = 1 gram Gold (CUR = Currency )

If you want to physically hold it, look gram value, because as far as I know, all goldsmiths and jewelleries in the world are selling gram gold.

I think that this command is the most useful and the concrete one that I have ever written.

I end my sentences with this anonymous proverb :

"Even if gold falls into the mud, it's still gold ! "

Distribution Position Size Panel

This panel is an example position size panel that I prepared and I consider the rates reasonable.

I have prepared this panel so that the money allocated to the investment ends 14 consecutive signals.

The sum of the ratios is 100 units.

You can adjust your positions according to this panel.

The first steps are low rates.

If the phrases are strong, you can specify a position size from the lower digits.

Likewise, when you make a big profit, you can empty your profits in the lower steps.

In the event of a color change, you can return to the beginning or lower limit.

NOTE: This script is an auxiliary command to the distribution blocks script,

if you want to use another script, you can add distribution days to yours.

14 th stake does not appear in the preview, you need to reduce the size of the distribution blocks indicator slightly.

Rafael Zioni's examples of the panels helped a lot, thanks to him.

Stay tuned ! Regards , Noldo.

Distribution BlocksThis idea has been created by the combination of the two existing systems as a result of my efforts to create a distributional buying and selling guide that has plagued my head for a long time.

1st idea is Accumulation / Distribution Line :

2nd idea is Distribution Day :

These two ideas, the intellectual assistance of professional brokers, and my observations of cot data played a role in the formation of this idea.

Let's start.

No matter how often we divide our risk, both our minds are not comfortable and our capital may end at any moment, and if we do not use professional systems, our chances of success are 50 percent.

If we take this system as an aid to our classic systems, we can determine the amount of risk with those predictions and gradually trade.

If we don't use leverage and we have a little predictive ability, our chances of success go above 50 percent.

But for the first time, we can keep our first lot very low and increase the number of positions in the same order of orders (example: buy and buy and buy).

If we keep the first amount low, the folds won't hurt us.

When we catch up with the trend, purchases with larger position sizes than lower prices lower our average price, so that we can make a good profit when the rising trend starts.

By accepting the zone changes as the reset point just like in the martingale system, we enter the folds in the new zone with our first lot weight.

Although we cannot catch the trend, we determine the stoploss level by adding the first point we entered or the first point we entered and the commission cost.

In fact, this method is the method of buying and selling very large traders and producers, banks, pro-brokers, hedge funds and in other words the new popular phrase "whales".

Because if he trades otherwise, he cannot find buyers because his goods are too big.

I like the comfort of mind in this way.

Finally, your methods separating the negative and positive regions (macd, rsi, interpretation observation etc.)

the stronger you are, the higher your success rate.

I think the Accumulation Distribution method is very successful, but it can be adjusted for the period.

I can't wait to integrate my relativity system on this.

And when my deep learning series is over, I will integrate them on ANN series and share them publicly.

To start with, I can say briefly.

If your capital is 100:

(first lot + (increase multiplier * first lot) + (increase multiplier * increase multiplier * first lot) + .....) = 100

I tell you that you can have the same position in this series 10 - 15 times,

this will help you decide how small a position size is to be used as the starting rate and choose a low increment multiplier!

I think that this idea cannot be converted into strategy, because when our expectations come true, we may want to free all positions and start again.And I think that's better.

And in sudden movements and developments we take action with different expectations.

I'm going to talk about this script's calculations and profits on educational ideas.

Regards , Noldo.

ANN MACD WTI (West Texas Intermediate) This script created by training WTI 4 hour data , 7 indicators and 12 Guppy Exponential Moving Averages.

Details :

Learning cycles: 1

AutoSave cycles: 100

Training error: 0.007593 ( Smaller than average target ! )

Input columns: 19

Output columns: 1

Excluded columns: 0

Training example rows: 300

Validating example rows: 0

Querying example rows: 0

Excluded example rows: 0

Duplicated example rows: 0

Input nodes connected: 19

Hidden layer 1 nodes: 2

Hidden layer 2 nodes: 6

Hidden layer 3 nodes: 0

Output nodes: 1

Learning rate: 0.7000

Momentum: 0.8000

Target error: 0.0100

Special thanks to wroclai for his great effort.

Deep learning series will continue. But I need to rest my eyes a little :)

Stay tuned ! Regards.

ANN MACD BRENT CRUDE OIL (UKOIL) This script trained with Brent Crude Oil data including 7 basic indicators and 12 Guppy Exponential Moving Averages .

Details :

Learning cycles: 1

Training error: 0.006591 ( Smaller than 0.01 ! )

AutoSave cycles: 100

Input columns: 19

Output columns: 1

Excluded columns: 0

Training example rows: 300

Validating example rows: 0

Querying example rows: 0

Excluded example rows: 0

Duplicated example rows: 0

Input nodes connected: 19

Hidden layer 1 nodes: 2

Hidden layer 2 nodes: 6

Hidden layer 3 nodes: 0

Output nodes: 1

Learning rate: 0.7000

Momentum: 0.8000

Target error: 0.0100

Note : Alerts added .

Special thanks to wroclai for his great effort.

Deep learning series will continue , stay tuned ! Regards.

ANN MACD GOLD (XAUUSD)This script aims to establish artificial neural networks with gold data.(4H)

Details :

Learning cycles: 329818

Training error: 0.012767 ( Slightly above average but negligible.)

Input columns: 19

Output columns: 1

Excluded columns: 0

Training example rows: 300

Validating example rows: 0

Querying example rows: 0

Excluded example rows: 0

Duplicated example rows: 0

Input nodes connected: 19

Hidden layer 1 nodes: 5

Hidden layer 2 nodes: 1

Hidden layer 3 nodes: 0

Output nodes: 1

Learning rate: 0.7000

Momentum: 0.8000

Target error: 0.0100

NOTE : Alarms added.

And special thanks to dear wroclai for his great effort.

Deep learning series will continue . Stay tuned! Regards.

ANN MACD S&P 500 This script is formed by training the S & P 500 Index with various indicators. Details :

Learning cycles: 78089

AutoSave cycles: 100

Training error: 0.011650 (Far less than the target, but acceptable.)

Input columns: 19

Output columns: 1

Excluded columns: 0

Training example rows: 300

Validating example rows: 0

Querying example rows: 0

Excluded example rows: 0

Duplicated example rows: 0

Input nodes connected: 19

Hidden layer 1 nodes: 2

Hidden layer 2 nodes: 1

Hidden layer 3 nodes: 0

Output nodes: 1

Learning rate: 0.7000

Momentum: 0.8000

Target error: 0.0100

Note : Thanks for dear wroclai for his great effort .

Deep learning series will continue . Stay tuned! Regards.

ANN MACD EURUSD (FX) Hello , this script is trained with eurusd 4-hour data. (550 columns) Details :

Learning cycles: 8327

AutoSave cycles: 100

Training error: 0.005500 ( That's a very good error coefficient.)

Input columns: 19

Output columns: 1

Excluded columns: 0

Training example rows: 550

Validating example rows: 0

Querying example rows: 0

Excluded example rows: 0

Duplicated example rows: 0

Input nodes connected: 19

Hidden layer 1 nodes: 2

Hidden layer 2 nodes: 5

Hidden layer 3 nodes: 0

Output nodes: 1

Learning rate: 0.6000

Momentum: 0.8000

Target error: 0.0055

NOTE : Use with EURUSD only.

Alarms added.

Thanks dear wroclai for his great effort.

Deep learning series will continue ! Stay tuned.

Regards , Noldo .

Dow Factor Stoch RSIThe indicator was generated by adding the Dow Factor to the Stochastic Relative Strength Index.( Stoch RSI )

The Dow factor is the effect of the correlation coefficient, which determines the relationship between volume and price, on the existing indicators.

With these codes we are able to integrate them numerically into the indicators.

For more information on the Dow factor, please see my indicator:

This code is open source under the MIT license. ( github.com )

My dow factor updates will continue.We adapted the indicators and saw successful results, now it is time to examine and develop the factor itself.

Stay tuned , best regards.

Dow Factor Relative Strength IndexThis script was written to create a new, rapid relative strength index inspired by the Dow Theory.

More info about Dow Theory : www.investopedia.com

According to the Dow Theory, volume should confirm market trends.

The correlation coefficient between prices and volume is negative in weakening trends and negative trends , positive in strengthening or positive trends.a factor was formed based on the correlation coefficient between volume and prices.

This factor was added to the relative strength index.

Period 5 is selected because the volume is very volatile and can be slow.

You can use the period you want, but I recommend the period as a minimum of 5.

It is suitable for all instruments and timeframes and thanks to its design, it provides control over gradual buying and selling points.

I haven't fully tested it, it's open to updates. For now, just use it to create ideas.

If I find it necessary,

I'll update after the tests.

If you have suggestions on these issues,

Leave your comments in the comment window.

This code is open source under the MIT license. If you have any improvements or corrections to suggest, please send me a pull request via the github repository github.com

Stay tuned , best regards.

CBOE PCR Factor Dependent Variable Odd Generator This script is the my Dependent Variable Odd Generator script :

with the Put / Call Ratio ( PCR ) appended, only for CBOE and the instruments connected to it.

For CBOE this script is more accurate and faster than Dependent Variable Odd Generator. And the stagnant market odds are better and more realistic.

Do not use for timeframe periods less than 1 day.

Because PCR data may give repaint error.

My advice is to use the 1-week bars to gain insight into your analysis.

This code is open source under the MIT license. If you have any improvements or corrections to suggest, please send me a pull request via the github repository github.com

I hope it will help your work.Best regards!

ANN MACD (BTC)

Logic is correct.

But I prefer to say experimental because the sample set is narrow. (300 columns)

Let's start:

6 inputs : Volume Change , Bollinger Low Band chg. , Bollinger Mid Band chg., Bollinger Up Band chg. , RSI change , MACD histogram change.

1 output : Future bar change (Historical)

Training timeframe : 15 mins (Analysis TF > 4 hours (My opinion))

Learning cycles : 337

Training error: 0.009999

Input columns: 6

Output columns: 1

Excluded columns: 0

Grid

Training example rows: 301

Validating example rows: 0

Querying example rows: 0

Excluded example rows: 0

Duplicated example rows: 0

Network

Input nodes connected: 6

Hidden layer 1 nodes: 8

Hidden layer 2 nodes: 0

Hidden layer 3 nodes: 0

Output nodes: 1

Learning rate : 0.6 Momentum : 0.8

More info :

EDIT : This code is open source under the MIT License. If you have any improvements or corrections to suggest, please send me a pull request via the github repository github.com

Dependent Variable Odd Generator For Machine Learning TechniquesCAUTION : Not suitable for strategy, open to development.

If can we separate the stagnant market from other markets, can we be so much more accurate?

This project was written to research it. It is just the tiny part of the begining.

And this is a very necessary but very small side function in the main function. Lets start :

Hi users, I had this idea in my mind for a long time but I had a hard time finding the parameters that would make the market stagnant. This idea is my first original command system. Although it is very difficult to make sense of the stagnant market, I think that this command system can achieve realistic proportions. With 's money flow index, I opened the track to determine the level. On the other hand, the prices were also using a money flow index, and it forced me to make the limitations between the levels in a logical way. But the good thing is that since the bollinger bandwidth uses a larger period, we are able to print normal values at extreme buy and sell values.

In terms of price, we can define excessive purchase and sale values as the period is smaller. I have repeatedly looked at the limit values that determine the bull, bear, and bollinger bandwidth (mfi), and I think this is the right one. Then I have included these values in the probability set.

The bull and bear market did not form the intersection of the cluster, and because there are connected events, the stagnant market, which is the intersection, will be added to the other markets with the same venn diagram logic and the sum of the probability set will be 1. is equal to. I hope that we can renew the number generators in the very important parameters of machine learning such as Markov Process with generators dependent on dependent variables, which bring us closer to reality. This function is open to development and can be made of various ideas on machine learning. Best wishes.

This code is open source under the MIT license. If you have any improvements or corrections to suggest, please send me a pull request via the github repository github.com