Kitaran

US Elections Democrate-Republicain (1920-2025)This script shows the different U.S. presidents and indicates whether each was Democratic or Republican. It allows users to analyze the market based on the president in office.

15-Min EMA CrossoverVery useful swing setup indicator that can be used in different styles of trading

Works on any timeframe but calculates EMA and cross signals based on 15-minute candles.

Plots the EMA line.

Shows green triangle for bullish crossover and red triangle for bearish crossunder.

Session Levels [odnac]This indicator plots the high and low levels of the three main trading sessions—Asia, Europe, and New York—along with the previous day’s high, low, and open. Each session’s time range can be customized using a UTC offset, and the indicator automatically tracks session highs and lows as price develops.

Functions:

Plots session highs and lows for Asia, Europe, and New York.

Shows previous day’s high, low, and open as reference levels.

Session times are fully configurable with hour and minute precision, including UTC offset adjustment.

Each session level is marked with both a line and a label for clarity.

Color customization for each session and previous day levels.

Designed for intraday timeframes (1–60 minutes).

Filter Condition:

When the filter option is enabled, the indicator adjusts how levels are drawn:

A session high above the current close is displayed as a solid line with a visible label.

Once price closes above that high, the line becomes dotted and dimmed, and the label also becomes less emphasized.

Similarly, a session low below the current close is displayed as a solid line and label.

If price closes below that low, the line switches to dotted and dimmed, with the label adjusted accordingly.

This behavior highlights only the most relevant levels for the current market position while still keeping breached levels visible in a subdued style, making it easier to spot active breakout or liquidity zones.

Sunset Zones by PDVDescription

Sunset Zones by PDV is an intraday reference indicator that plots key horizontal levels based on selected “root candles” throughout the trading day. At each programmed time, the indicator identifies the high and low of the corresponding candle and projects those levels forward with extended lines, providing traders with a clean visual framework of potential intraday reaction zones.

These zones serve as reference levels for support, resistance, liquidity grabs, and session context, allowing traders to analyze how price reacts around time-specific structures. Unlike lagging indicators, Sunset Zones gives traders real-time, rule-based levels tied directly to the price action of specific moments in the session.

Key Features

Predefined Time Codes

The script comes with a curated list of intraday timestamps (in HHMM format). Each represents a “root candle” from which levels are generated. Examples include 03:12, 06:47, 07:41, 08:51, etc. These time codes can reflect historically important market moments such as session opens, liquidity sweeps, or volatility inflection points.

Automatic Zone Plotting

At each root time, the script captures the candle’s high and low and instantly extends those levels forward across the chart. This provides consistent, objective reference points for intraday trading.

Extended Lines

Levels are projected far into the future (default: 500 bars) so traders can easily track how price interacts with those zones throughout the day.

Color-Coded Levels

Each root time is assigned a distinct color for fast identification. For example:

03:12 → Fuchsia

06:47 → Purple

07:41 → Teal

08:51 → White

09:53 → White

10:20 → Orange

11:10 → Green

11:49 → Red

12:05 → White

13:05 → Teal

14:09 → Aqua

This helps traders quickly recognize which time-of-day level price is interacting with.

Lightweight & Visual

The indicator focuses purely on price and time, avoiding complexity or lagging signals. It can be layered with other analysis tools, order flow charts, or session-based studies.

Practical Use Cases

Intraday Bias:

Observe whether price respects, rejects, or consolidates around these reference levels to form a bias.

Liquidity Zones:

High/low sweeps of the root candle can act as liquidity pools where institutions might trigger stops or reversals.

Support & Resistance:

Extended lines create intraday S/R zones without the need to manually draw levels.

Confluence Finder:

Combine Sunset Zones with VWAP, session ranges, Fibonacci levels, or higher-timeframe structure for layered confluence.

Important Notes

This is a visual reference tool only. It does not generate buy or sell signals.

Default times are provided, but the concept is flexible — traders can adapt it by modifying or expanding the list of time codes.

Works best on intraday timeframes where session structure is most relevant (e.g., 1-minute to 15-minute charts).

✅ In short: Sunset Zones by PDV gives intraday traders a systematic way to anchor their charts to important time-based highs and lows, creating a consistent framework for analyzing price reactions across the day.

Gronk-Style Lunar Cycle Projection (fixed 30m base)Based on the lunar cycle timing provided by Gronko Polo - A Bromance in Finance

FVG & SMA @danciFVG zones with 200 SMA & daily dividers for intraday analysis, customizable and clear.

DCA Anchor (Weekly/Monthly/N Bars) [CHE] What is Dollar-Cost Averaging (DCA)?

DCA is a position-building method where you invest a fixed amount at fixed intervals (e.g., weekly or monthly) regardless of price. Over time, this:

reduces timing risk (you don’t need to guess tops/bottoms),

smooths entry price by buying more units when price is low and fewer when price is high,

keeps decisions simple and repeatable.

Trade-offs:

You’ll never catch the exact bottom.

In strong uptrends, lump-sum can outperform.

Fees matter if you buy very frequently.

Simple math:

Qty bought at time t = `amount / price_t` (net of fees if fees are not “on top”).

Total qty = sum of all buys.

Average price (cost basis) = `total invested / total qty`.

Equity = `total qty last price`.

P\&L = `equity − total invested` (and `%` = `P&L / total invested`).

DCA Anchor (Weekly/Monthly/N Bars)

Purpose: automate scheduled DCA buys on chart data, optionally add extra buys on drawdowns, track stats, and fire alerts.

Core features

Schedules:

1. Every N bars,

2. Weekly (first bar of a new week),

3. Monthly (first bar of a new month).

A Start time input gates when the logic begins.

Fees model:

Fee on top: you pay `amount + fee` in cash; quantity = `amount / close`.

Fee from amount: fee is deducted from the amount; quantity is smaller, cash outlay equals `amount`.

Optional drawdown buys:

Trigger when `close ≤ avgCost (1 − ddPct/100)`.

Controls: drawdown % threshold, multiplier (extra size vs. base amount), and cooldown in bars.

State & metrics: tracks total invested, total quantity, average price, equity, P\&L (abs/%).

Visuals:

Line plot of Average Price.

Buy labels at execution bars (plan and drawdown).

Compact table (positionable) with key stats (trades, invested, qty, avg price, equity, P\&L).

Alerts:

Plan Buy (Bar Close) and Drawdown Buy (Bar Close) — robust, non-repainting.

Optional Intrabar Preview alerts for early heads-up (can fire before bar close).

How to use it (quick start)

1. Add to chart → Inputs:

Buy frequency: pick Every N bars, Weekly, or Monthly.

Start time: date from which buys may begin.

Buy amount: fixed cash per planned buy.

Fees % and Fee on top? to match your broker/exchange model.

(Optional) Enable drawdown buy, set threshold %, multiplier, and cooldown.

Toggle Show buy labels and Show stats table.

2. Alerts (recommended):

Use “DCA Plan Buy (Bar Close)” and/or “DCA Drawdown Buy (Bar Close)” with Once per bar close.

If you need early signals, enable Intrabar pre-alerts and add the two Intrabar Preview alerts with Once per bar.

3. Interpretation:

The yellow line is your average price.

Green/orange markers show plan buys and drawdown buys.

The table summarizes total trades, invested capital, quantity, average price, current equity, and P\&L.

Practical notes

All executions occur at bar close by default to avoid intrabar repainting.

Weekly/monthly roll depends on the symbol’s exchange calendar.

Backtest realism: no slippage, no partial fills. Fees are modeled as configured.

If you buy very frequently, consider higher “N” or weekly/monthly to keep fees under control.

If you want, I can tailor the defaults (amount, fee model, drawdown rules) to your typical markets and timeframes.

Disclaimer

No indicator guarantees profits. DCA Anchor (Weekly/Monthly/N Bars) is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Best regards

Chervolino

SESSIONS Golden Team SESSIONS — Multi-Session Forex Box & Range Analysis

This indicator displays the major Forex market sessions — London, New York, Tokyo, Sydney, and Frankfurt — directly on the chart. Each session is shown as a customizable colored box with optional Fibonacci levels and opening range markers.

It also calculates and displays the average pip range of each session over a user-defined number of past days, allowing traders to analyze volatility patterns for each trading period.

Key Features:

Configurable session times and time zones

Individual on/off toggle for each session

Custom colors, box transparency, and border styles

Optional Opening Range and Fibonacci retracement levels for each session

Average pip range table for quick volatility reference

Works on any intraday timeframe

How It Works:

The script identifies the start and end times of each session based on user settings.

A box is drawn around the high/low of the session period.

At the end of each session, the pip range is recorded, and an average is calculated over the last N sessions (default: 20).

The results are displayed in a statistics table showing average pips and whether the session is currently active.

Suggested Use:

Identify high-volatility sessions for breakout trading

Filter trades to active trading hours

Study historical volatility to refine entry timing

FX Market Sessions serkanMarket stock market opening and closing indicators

Opening and closing time ranges

Frankfurt

London

CM

New York opening and closing time ranges

VWAP MTF Scalping ModuleThe VWAP MTF indicator allows you to visualize anchored VWAP across multiple timeframes, while maintaining a clean and responsive display.

Designed for intraday traders, scalpers, and swing traders, this module offers a clear view of volume-weighted average price zones across key timeframes (1m, 5m, 15m, 1h... customizable).

Multi-Timeframe HTS Retest Strategy v6Multi-Timeframe HTS Retest Strategy v6 is a trend-following tool designed to detect high-probability retest entries aligned with higher timeframe direction. The indicator applies HTS bands (short & long) on both the current and higher timeframe (4x–8x multiplier) to confirm market bias.

A strong trend is validated when HTS bands separate on the higher timeframe. On the lower timeframe, the strategy tracks price behavior relative to the bands: after breaking outside, price must retest either the fast (blue) or slow (red) band, confirmed by a rejection candle. This generates precise BUY or SELL retest signals.

Features include flexible average methods (RMA, EMA, SMA, etc.), customizable cross detection (final cross, 4 crosses, or both), volume-based retest conditions, and clear visual signals (dots for trend start, triangles for retests). Alerts are integrated for automation.

This strategy is suitable for forex, crypto, indices, and stocks, supporting both scalping and swing trading.

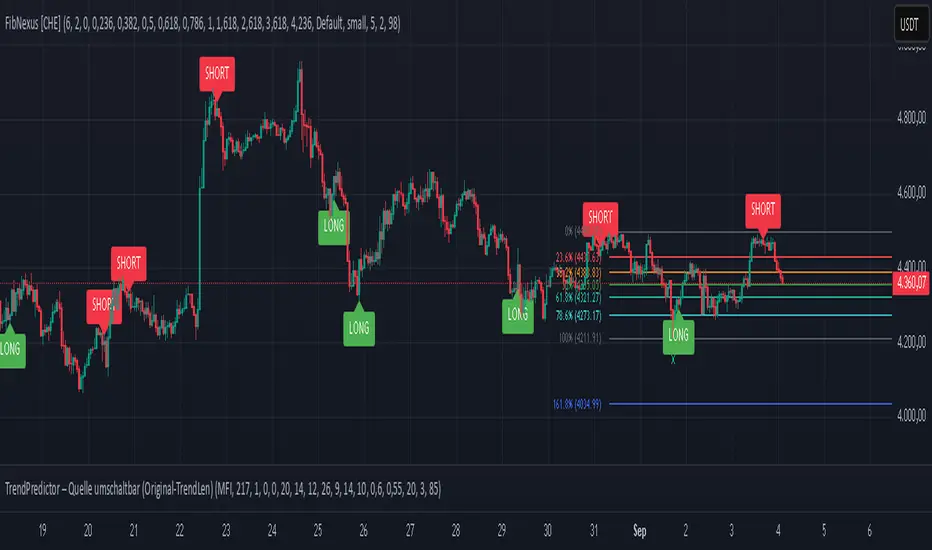

FibNexus [CHE]FibNexus — Auto-Fibonacci with Adaptive TrendLen + TFRSI Triggers

What it is.

FibNexus is a chart overlay that auto-anchors Fibonacci levels to the most relevant swing range without any manual timeframe picking. It does this by computing an adaptive trend length (“TrendLen”) from recent price behavior, then drawing retracements/extensions from the detected swing High/Low. A built-in TFRSI module adds LONG/SHORT triggers and ready-made alerts.

What makes FibNexus different (the TrendLen edge)

Most Fibonacci tools either (a) use fixed lookbacks or (b) force you to choose a higher reference timeframe (or a multiplier of it) and then place Fibs on those higher-TF swings. Your earlier Ultimate Fibonacci Trading Tool \ follows that higher-reference approach (auto TF, multiplier, or manual) and emphasizes custom level/label options. ( )

FibNexus flips that workflow:

* It doesn’t rely on a higher timeframe or a static lookback.

* Instead, it measures multiple window lengths inside the current chart timeframe and selects the one that best fits the data right now.

* From that data-driven window, it automatically finds the most recent swing high & low and draws the entire Fib stack from there.

* When the statistically “best” window changes, anchors update once, labels refresh cleanly, and then lines just extend to the right on each new bar.

Result: No more guesswork about “which timeframe or lookback should I use?”—FibNexus adapts the anchors to market conditions and keeps the drawing noise low.

How TrendLen works (transparent, deterministic)

1. Scan windows: The script evaluates a series of lookbacks (10, 20, …, 500 bars).

2. Score by correlation: For each window, it computes the correlation between price and its lagged version and picks the window with the highest correlation (the strongest, most self-consistent trend segment).

3. Anchor the swing: On a confirmed bar and only when TrendLen changes, it scans the last `TrendLen` bars to capture the highest high and lowest low and marks them with “X”.

4. Draw once, extend later: It deletes the old Fib objects, redraws the active levels from those anchors, and from then on extends the lines to the right as new bars print (no redraw spam).

This makes FibNexus responsive (it adapts when the structure shifts) and quiet (it doesn’t constantly repaint Fibs).

Fibonacci engine (levels, labels, direction)

* Retracements: 0.000 · 0.236 · 0.382 · 0.500 · 0.618 · 0.786 · 1.000

* Extensions: 1.618 · 2.618 · 3.618 · 4.236

* Label styles: *Default* (percent + price), *None*, *Percentage*, *Price*

* Label sizing: *tiny → huge*

* Bull/Bear context: Direction is inferred from mid-range positioning; prices are projected accordingly (retracement vs. extension math is handled for both cases).

* Selective toggles: You can show/hide any level and color it independently.

Momentum & signals (TFRSI module)

FibNexus embeds your TFRSI (“The Forbidden RSI \ ”) as the momentum/trigger layer. TFRSI is your open-source oscillator published on TradingView and designed for fast, normalized momentum readouts with customizable length/smoothing. ( )

* Defaults: `TFRSI length = 6`, `signal smoothing = 2`

* Triggers:

* LONG when TFRSI crosses up through the Long level (default 2.0)

* SHORT when TFRSI crosses down through the Short level (default 98.0)

* On-chart labels: Green LONG under the bar, red SHORT above the bar.

* Spam control: Keep only the N most recent labels to avoid clutter.

* Confirmed bars only: Signals/labels finalize at bar close to reduce flicker.

Alerts (ready for TradingView)

* LONG signal (TFRSI crossover)

* SHORT signal (TFRSI crossunder)

* TrendLen changed (anchors/Fibs recalculated)

* Price crossed a Fib level (any active level)

Use the provided `alertcondition(...)` entries in the TV dialog. Optionally enable instant `alert()` calls with verbose text (avoid duplicates if you also add alertconditions).

Typical use-cases & playbook

* Level reaction trading: In trends, watch 0.382 / 0.5 / 0.618 for reaction. A TFRSI up-cross near a retracement in an uptrend is a straightforward continuation setup; the opposite applies in downtrends.

* Breakout objectives: After clearing the 1.000 line (old swing), 1.618 is a common first extension target; beyond that, 2.618/3.618/4.236 map stretch objectives.

* Chop control: In range conditions, keep signals conservative (e.g., stick with the tight defaults 2.0/98.0 or raise thresholds). Always seek confluence (candlesticks, volume, HTF bias).

* Less micromanagement: You don’t need to babysit timeframe selection or anchors—TrendLen recomputes only when the data say so.

Inputs (by group)

* Core: TFRSI length & smoothing.

* Fibonacci Levels: Per-level toggles, numeric values, colors.

* Fibonacci Labels: Style (percentage/price/both/none) and size.

* Signals: Max number of visible LONG/SHORT labels (or 0 = off).

* TFRSI Trigger: Long/Short thresholds (defaults 2.0 / 98.0).

* Alerts: Master enable, per-event toggles, optional instant `alert()`.

Performance & UX

* Overlay indicator; efficient object handling.

* Clean redraw policy: Full re-draw only when TrendLen changes; otherwise Fibs extend horizontally.

* Clarity: Auto-marked swing anchors (“X”), configurable labels/colors.

Credits & references

* TFRSI – “The Forbidden RSI \ ” (open-source publication and description on TradingView). Used here as the momentum basis.

* “Ultimate Fibonacci Trading Tool \ ” (your earlier open-source tool on TradingView). Focuses on higher-reference timeframe selection (auto/multiplier/manual) and rich labeling controls; FibNexus replaces the fixed/higher-TF anchor logic with adaptive TrendLen in the current timeframe.

Risk disclaimer

This indicator is for educational/information purposes only and is not financial advice. No performance guarantees; past behavior does not predict future results. Trading involves substantial risk (including total loss). Always do your own research, test on demo, use risk management, and consult a licensed advisor where appropriate. Use at your own risk.

Disclaimer:

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence with FibNexus ! 🚀

Happy trading

Chervolino

Stacey Burke Signal Day LTE“Previously published as ‘Day Zero Fakeout Detector MTF’”

Stacey Burke Signal Day LTE

Automatic detection of Day Zero, Inside Days, and Outside Days for Stacey Burke’s intraday playbook

🔎 Stacey Burke’s Signal Days

This indicator highlights the key daily patterns that often lead to high-probability intraday setups in Stacey Burke’s methodology:

1️⃣ Day Zero

The reset days within a 3-day cycle (e.g. breakout → continuation → exhaustion/reversal).

Can mark the beginning of a new directional phase.

Trades back inside the prior range after a Peak Formation High (PFH) or Peak Formation Low (PFL).

Bias: Look for measured parabolic session moves. When combined with trend following indicators, these signal days can be very powerful.

2️⃣ Inside Day

A day where the entire range is contained within the prior day’s range.

Signals consolidation and energy build-up.

Often leads to explosive breakouts in the next session.

Bias: Trade breakouts of the inside day’s high/low or breakout reversal in the session at key timings in the direction of higher timeframe bias. When combined with trend following indicators, these signal days can be very powerful.

3️⃣ Outside Day (Engulfing Day)

`

A day where the range is larger than the prior day’s range, engulfing both high and low.

Marks trapped traders and fakeouts on both sides.

Often precedes strong continuations or sharp reversals from outside of the ranges.

Bias: Align trades with the true continuation move. When combined with trend following indicators, these signal days can be very powerful.

📌 How They Work Together

Day Zero → Signals the new cycle after PFH/PFL.

Inside Day → Signals compression → expect breakout setups.

Outside Day → Signals exhaustion/fakeouts → expect reversals or continuations.

Together, they give traders a clear daily roadmap for where liquidity sits and when to expect the highest-probability setups.

✅ Example in Practice

Market rallies for 3 days → PFH forms → Day Zero short bias.

Next day prints an Inside Day → watch for breakout continuation short, and breakout reversals.

Later, an Outside Day traps both longs and shorts → the following session offers a clean intraday reversal or continuation trade in line with the underlying MTF trend/bias.

⚙️ Features of This Indicator

Automatic detection of Day Zero, Inside Days, and Outside Days

Multi-Timeframe (MTF) support for cycle alignment

Visual markers for PFH/PFL and consolidation zones

Measured move projections for breakout targets

👉 Stacey Burke Signal Day LTE gives traders just a few of the most important signal days — Day Zero, Inside Day, and Outside Day — to structure their intraday trades around fake outs, breakouts, and reversals within the daily cycles of the week. (This is work in progress: Next up, FRD/FGD's, 3-day cycle detecting, 3DLs, 3DSs).

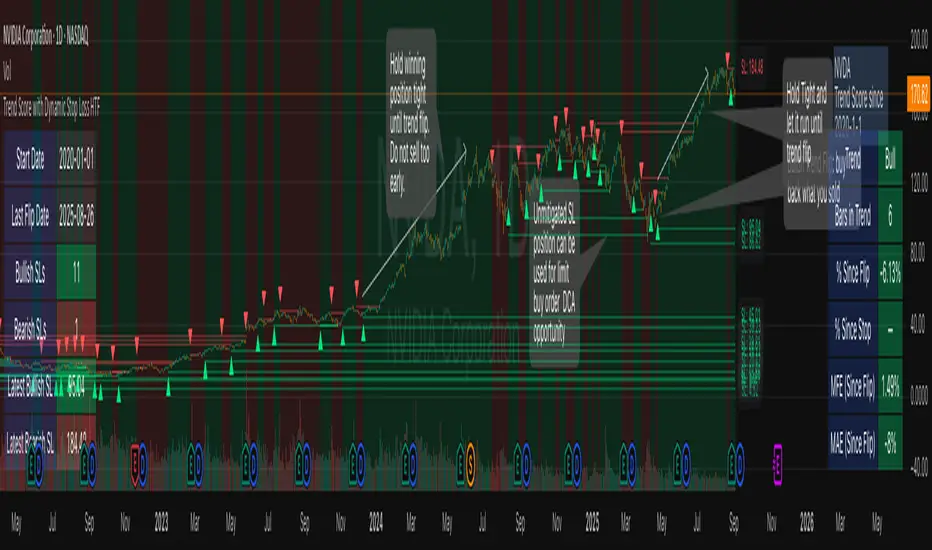

Trend Score with Dynamic Stop Loss HTF

How the Trend Score System Works

This indicator uses a Trend Score (TS) to measure price momentum over time. It tracks whether price is breaking higher or lower, then sums these moves into a cumulative score to define trend direction.

⸻

1. Trend Score (+1 / -1 Mechanism)

On each new bar:

• +1 point: if the current bar breaks the previous bar’s high.

• −1 point: if the current bar breaks the previous bar’s low.

• If both happen in the same bar, they cancel each other out.

• If neither happens, the score does not change.

This creates a simple running measure of bullish vs bearish pressure.

⸻

2. Cumulative Trend Score

The Trend Score is cumulative, meaning each new +1 or -1 is added to the total score, building a continuous count.

• Rising scores = buyers are consistently pushing price to higher highs.

• Falling scores = sellers are consistently pushing price to lower lows.

This smooths out noise and helps identify persistent momentum rather than single-bar spikes.

⸻

3. Trend Flip Trigger (default = 3)

A trend flip occurs when the cumulative Trend Score changes by 3 points (default setting) in the opposite direction of the current trend.

• Bullish Flip:

• Cumulative TS rises 3 points from its most recent low pivot.

• Marks a potential start of a new uptrend.

• A bullish stop-loss (SL) is set at the most recent swing low.

• Bearish Flip:

• Cumulative TS falls 3 points from its most recent high pivot.

• Marks a potential start of a new downtrend.

• A bearish SL is set at the most recent swing high.

Example:

• TS is at -2, then climbs to +1.

• That’s a +3 change, triggering a bullish flip.

⸻

4. Visual Summary

• Green background: Active bullish trend.

• Red background: Active bearish trend.

• ▲ Triangle Up: A bullish flip occurred this bar.

• Stop Loss Line: Shows the structural low used for risk management.

⸻

Why This Matters

The Trend Score measures trend pressure simply and objectively:

• +1 / -1 mechanics track real price behavior (breakouts of highs and lows).

• Cumulative changes of 3 points act like a momentum filter, ignoring small reversals.

• This helps you see true regime shifts on higher timeframes, which is especially useful for swing trades and investing decisions.

⸻

Key Takeaways

• Only flips after meaningful swings: prevents overreacting to single-bar noise.

• SL shows invalidation point: helps you know where a trend thesis fails.

• Works best on Daily or Weekly charts: for smoother, more reliable signals. Using Trend Score for Long-Term Investing

This indicator is designed to support decision-making for higher timeframe investing, such as swing trades, multi-month positions, or even multi-year holds.

It helps you:

• Identify major bullish regimes.

• Decide when to add to winning positions (DCA up).

• Know when to pause buying or consider trimming during weak periods.

• Stay disciplined while holding long-term winners.

Important Note:

These are suggestions for context. Always combine them with your own analysis, portfolio allocation rules, and risk tolerance.

⸻

1. Start With the Higher Timeframe

• Use Weekly charts for a broad investing view.

• Use Daily charts only for fine-tuning entry points or deciding when to add.

• A Bullish Flip on Weekly suggests the market may be entering a major uptrend.

• If Weekly is bullish and Daily also turns bullish, it’s extra confirmation of strength.

⸻

2. Building a Position with DCA

Goal: Grow your position gradually during strong bullish regimes while staying aware of risk.

A. Initial Buy

• Start with a small initial allocation when a Bullish Flip appears on Weekly or Daily.

• This is just a starter position to get exposure while the new trend develops.

B. Adding Through Strength (DCA Up)

• Consider adding during pullbacks, as long as price stays above the active SL line.

• Each add should be smaller or equal to your first buy.

• Spread out adds over time or price levels, instead of going all-in at once.

C. Pause Buying When:

• Price approaches or touches the SL level (trend invalidation).

• A Bearish Flip appears on Weekly or Daily — this signals potential weakness.

• Your total position size reaches your maximum allocation limit for that asset.

⸻

3. Holding Winners

When a position grows in profit:

• Stay in the trend as long as the Weekly regime remains bullish.

• The indicator’s green background acts as a reminder to hold, not panic sell.

• Use the SL bubble to monitor where the trend could potentially break.

• Avoid selling just because of small pullbacks — focus on big-picture trend health.

⸻

4. Taking Partial Profits

While this tool is designed to help hold long-term winners, there may be times to lighten risk:

• After large, rapid moves far above the SL, consider trimming a small portion of your position.

• When MFE (Maximum Favorable Excursion) in the table reaches unusually high levels, it may signal overextension.

• If the Weekly chart turns Neutral or Bearish, you can gradually reduce exposure while waiting for the next Bullish Flip.

⸻

5. Using the Stop Loss Line for Awareness

The Dynamic SL line represents a structural level that, if broken, may suggest the bullish trend is weakening.

How to think about it:

• Above SL: Market remains structurally healthy — continue holding or adding gradually.

• Close to SL: Pause adds. Be cautious and consider tightening your risk.

• Below SL: Treat this as a potential signal to reassess your position, especially if the break is confirmed on Weekly.

The SL is not a hard stop — it’s a visual guide to help you manage expectations.

⸻

6. Example Use Case

Imagine you are investing in a growth stock:

• Weekly Bullish Flip: You open a small starter position.

• Price pulls back slightly but stays above SL: You add a second, smaller tranche.

• Trend continues up for months: You hold and stop adding once your desired allocation is reached.

• Price doubles: You trim 10–20% to lock some profits, but continue holding the majority.

• Price later dips below SL: You slow down, reassess, and decide whether to reduce exposure.

This keeps you:

• Participating in major uptrends.

• Avoiding overcommitment during weak phases.

• Making adjustments gradually, not emotionally.

⸻

7. Suggested Workflow

1. Check Weekly chart → is it Bullish?

2. If yes, review Daily chart to fine-tune entry or adds.

3. Build exposure gradually while Weekly remains bullish.

4. Watch SL bubbles as awareness points for risk management.

5. Use partial trims during big rallies, but avoid exiting entirely too soon.

6. Reassess if Weekly turns Neutral or Bearish.

⸻

Key Takeaways

• Use this as a compass, not a command system.

• Weekly flips = big picture direction.

• Daily flips = timing and precision.

• Add gradually (DCA) while above SL, pause near SL, reassess below SL.

• Hold winners as long as Weekly remains bullish.

Trend Score with Dynamic Stop Loss RTH

📘 Trend Score with Dynamic Stop Loss (RTH) — Guide

🔎 Overview

This indicator tracks intraday momentum during Regular Trading Hours and flags trend flips using a cumulative TrendScore. It also draws dynamic stop-loss levels and shows a live stats table for quick decision-making and journaling.

⸻

⚙️ Core Concepts

1) TrendScore (per bar)

• +1 if the current bar makes a higher high than the previous bar (counted once per bar).

• –1 if the current bar makes a lower low than the previous bar (counted once per bar).

• If a bar takes both the prior high and low, the net contribution can cancel out within that bar.

2) Cumulative TrendScore (running total)

• The per-bar TrendScore accumulates across the session to form the cumulative TrendScore (TS).

• TS resets to 0 at session open and is cleared at session close.

• Rising TS = persistent upside pressure; falling TS = persistent downside pressure.

⸻

🔄 Flip Rules (3-point reversal of the cumulative TrendScore)

A flip occurs when the cumulative TrendScore reverses by 3 points in the opposite direction of the current trend.

• Bullish Flip

• Trigger: After a decline, the cumulative TrendScore rises by +3 from its down-leg.

• Interpretation: Bulls have taken control.

• Stop-loss: the lowest price of the prior (down) leg.

• Bearish Flip

• Trigger: After a rise, the cumulative TrendScore falls by –3 from its up-leg.

• Interpretation: Bears have taken control.

• Stop-loss: the highest price of the prior (up) leg.

Flip bars are marked with ▲ (lime) for bullish and ▼ (red) for bearish.

Note: If you prefer a different reversal distance, adjust the flip distance setting in the script’s inputs (default is 3).

⸻

📏 Stop-Loss Lines

• A dotted line is drawn at the prior leg’s extreme:

Green (below price) after a bullish flip.

Red (above price) after a bearish flip.

• Options:

Remove on touch for a clean chart.

Freeze on touch to keep a visual record for journaling.

• All stop lines are cleared at session end.

⸻

🧮 Stats Table (what you see)

• Trend: Bull / Bear / Neutral

• Bars in Trend: Count since the flip bar

• Since Flip: Current close minus flip bar close

• Since SL: Current close minus active stop level

• MFE-Maximum Favorable Excursion: Highest favorable move since flip

• MAE-Maximum Adverse Excursion: Largest adverse move since flip

Table colors reflect the current trend (green for bull, red for bear).

⸻

📊 Trading Playbook

Entries

• Aggressive: Enter immediately on a flip marker.

• Conservative: Wait for a small pullback that doesn’t violate the stop.

Stops

• Place the stop at the script’s flip stop-loss line (the prior leg extreme).

Exits

Choose one style and stick with it:

• Stop-only: Exit when the stop is hit.

• Time-based: Flatten at session close.

• Targets: Scale/close at 1R, 2R.

• Trailing: Trail behind minor swings once MFE > 1R.

Ultimately Exit choice is your own edge, so you must decide for yourself.

💡 Best Practices

• Skip the first few bars after the open (gap noise).

• Use regular candles (Heikin-Ashi will distort highs/lows).

• If you want fewer flips, increase the flip distance (e.g., 4 or 5). For more

responsiveness, use 2. Otherwise, increase your time frame to 5m, 10m, 15m.

• Keep SL lines frozen (not auto-removed) if you’re journaling.

Elliott Wave Rule EngineWhat this tool does

The indicator scans price for two concurrent swing structures—a Small (shorter-degree) and a Large (higher-degree) set—then applies an Elliott/NeoWave rule engine to the most recent 5-swing motive (1-2-3-4-5) or 3-swing corrective (A-B-C). It produces:

Blue lines for Small swings and Orange lines for Large swings.

A rule dashboard (optional) showing PASS/FAIL/WARN for core rules & guidelines.

Buy/Sell labels when (a) a valid motive completes and (b) loop “consensus,” alignment, and scoring gates are satisfied.

Reading the chart

Small swings: thin blue segments, built from your Small settings.

Large swings: thicker orange segments, from your Large settings.

Background tint: faint green when a motive (impulse/diagonal) is valid right now on Small.

Labels (if enabled):

“1…5” or “A-B-C” markers on the latest detected structure.

Buy/Sell label at the last pivot when all gates pass; text may include a score %.

How it works

For both Small and Large degrees the script:

- Loops over all (left, right) combinations you specify (e.g., Small Left = 3..6, Right = 0..0) and calls ta.pivothigh/low.

- Aggregates the results:

- Keeps the most extreme pivot found in the loop (highest high or lowest low) that’s newer than the last accepted swing.

- Gates acceptance by minimum % change versus the last opposite swing (inside the loop) and a post-aggregation filter (Small Minimum swing %, Large Minimum swing %).

- Merges back-to-back same-type swings (HH or LL) by keeping only the more extreme one.

- Keeps only the last N=lookbackWaves swings (default 100).

- Consensus (used for signals) comes from the loop counts:

- sBuyConsensus = small L-count / total-combos (bullish bias)

- sSellConsensus = small H-count / total-combos (bearish bias)

(and the same for Large). This is a data-driven “how many combos agreed” measure.

2) Rule engine (Impulse/Diagonal vs. Corrective)

When there are at least 6 Small swings, the engine tests 1-2-3-4-5:

Hard rules (must pass for an Impulse):

- Wave-2 not > 100% of Wave-1 (no retrace beyond start of W1).

- Wave-3 not the shortest among 1,3,5.

- Wave-4 doesn’t overlap Wave-1 (if it does, structure may be a Diagonal).

- Diagonal eligibility: Rules 1 & 2 pass but Rule 3 fails ⇒ eligible as a Diagonal (

Guidelines (7 checks, count toward a threshold you set):

- W2 retraces a Fib level (within ±fibTol).

- W4 retraces a Fib level (within ±fibTol).

- W3 strongest momentum (speed = |Δprice| / bars).

- Alternation: W2 vs W4 have meaningfully different “sharpness” (price per bar), threshold altSlopeThr.

- Proportion (Price): |W1| and |W3| within propTolP× each other.

- Proportion (Time): W1W3 and W2W4 durations within propTolT×.

- W5 weaker than W3 (momentum divergence proxy).

A Motive is valid if:

- Impulse: all 3 hard rules pass and guideline passes ≥ Min guideline passes.

- Diagonal: diagonal-eligible and guideline passes ≥ Min guideline passes.

- if motive fails, the engine still evaluates ABC as Zigzag and Flat to populate the table:

- Zigzag: B shallower than ~0.618A; C ≈ A or 1.618A (±fibTol).

- Flat: B ≥ ~0.9A; expanded flat if B > 1.0A and C in *A; “running” note if C < A.

3) Signal logic (consensus-gated & scored)

Signals fire only on new Small pivots and only if a Small motive just validated:Direction comes from the motive’s W1 (up = bull, down = bear).

Consensus checks (from the loop):

Use Sell consensus if the last pivot is a High, or Buy consensus if it’s a Low.Require it ≥ Min SMALL loop consensus and ahead of the opposite side by at least Min consensus margin.If you also require Large quality: check the corresponding Large consensus ≥ Min LARGE loop consensus.

Alignment: If Require small/large directional alignment is ON, Small and Large directions must match (or the Large motive must be complete).

Score:

- If Large not required: finalScore = smallConsensus × smallQuality.

- If Large required: finalScore = smallConsensus × smallQuality × largeQuality.

- Need finalScore ≥ Min final score.

When all gates pass, you’ll see “Buy xx%” or “Sell xx%” at the pivot.

Inputs (explained):

- Smaller Wave Swing Detection (Looped)

- Small Left Min / Max (default 3..6): ta.pivot* left widths to scan.

- Small Right Min / Max (default 0..0): right widths to scan (0 = earliest confirmation).

- Small Minimum swing % (post-aggregation) (0.3%): filters out tiny swings after the loop.

- Larger Wave Swing Detection (Looped)

- Large Left Min / Max (100..200) and Right Min/Max (0..0): higher-degree scan (defaults are big; adjust for intraday).

- Large Minimum swing % (post-aggregation) (1.5%).

- Loop Filters (inside the loop)

- Small loop min % change (0.20%): a candidate pivot counts only if move vs. last opposite Small swing ≥ this.

- Large loop min % change (1.50%): same idea for Large.

Rule Engine Tolerances

- Fibonacci tolerance (±%) (0.05 = 5%): closeness to Fib levels.

-Same-degree TIME proportion max (x) (2.00×) and PRICE proportion max (x) (3.00×).

- Alternation slope ratio threshold (0.10): higher = stricter alternation.

- Min guideline passes (0–7) (5): threshold for motive validity.

- Signal Probability (Loop Consensus)

- Min SMALL loop consensus (0.60).

- Min LARGE loop consensus (0.50) (used only if Large validation matters).

- Min consensus margin vs opposite (0.10): e.g., 0.60 vs 0.45 fails (margin 0.15 passes).

Require LARGE 1–5 valid (or diagonal) for signal (off by default).

Min final score (0.20): gate on the composite score.

Annotate label with score % (on).

WARN (orange): guideline not met—pattern can still be valid if total passes ≥ Min guideline passes.

FAQ

Q: Why did I get a diagonal instead of an impulse?

A: Wave-4 overlapped Wave-1 (Rule 3). If Rules 1 & 2 pass and guidelines meet your minimum, it’s eligible as a Diagonal.

Q: Where do Buy/Sell labels come from?

A: Only after a valid Small motive at a new pivot, and only if consensus, alignment, and final score gates pass (per your settings).

Q: It “missed” a wave in hindsight.

A: Pivots require right bars to confirm; extremely tight settings can filter that swing; adjust Small min % or ranges.

Q: Are there repaints?

A: No, It uses standard pivot confirmation; until a pivot is confirmed, recent swings can evolve. After confirmation, lines/labels are stable.

Limitations & disclaimers

Elliott/NeoWave rules are heuristics; markets are messy. Treat outputs as structured context, not certainty.

Consensus is pattern-scan agreement, not probability of profit Not investment advice; always couple with risk management.

XAU 0/5 GridThis indicator draws horizontal price grids for XAUUSD. It anchors the grid to a base price that ends with 0 or 5, then plots equally spaced levels every 5 price units above and below that base. It’s a clean way to eyeball fixed-interval structure for rough support/resistance zones and simple TP/SL planning.

How it works

Base (0/5):

base = floor(close / 5) × 5 → forces the base to always end with 0/5.

Grid levels:

level_i = base + i × 5, where i is any integer (positive/negative).

The script updates positions only when the base changes to avoid flicker and reduce chart load.

It uses a persistent line array to manage the line objects efficiently.

Usage

Add the indicator to an XAUUSD chart on any timeframe.

Configure in the panel:

Show Lines – toggle visibility

Lines each side – number of lines above/below the base

Line Color / Line Width – appearance

Use the grid as fixed reference levels (e.g., 3490, 3495, 3500, 3505, …) for planning TP/SL or observing grid breaks.

Highlights

Strict 0/5 anchoring keeps levels evenly spaced and easy to read on gold.

Auto-reanchors when price moves to a new 0/5 zone, maintaining a steady view.

Lightweight design: lines are created once and then updated, minimizing overhead.

Limitations

Visualization only — not a buy/sell signal.

Spacing is fixed at 5 price units, optimized for XAUUSD. If used on other symbols/brokers with different tick scales, adjust the logic accordingly.

Grid lines do not guarantee support/resistance; always combine with broader market context.

BTC Power-Law Decay Channel Oscillator (0–100)🟠 BTC Power-Law Decay Channel Oscillator (0–100)

This indicator calculates Bitcoin’s position inside its long-term power-law decay channel and normalizes it into an easy-to-read 0–100 oscillator.

🔎 Concept

Bitcoin’s long-term price trajectory can be modeled by a log-log power-law channel.

A baseline is fitted, then an upper band (excess/euphoria) and a lower band (capitulation/fear).

The oscillator shows where the current price sits between those bands:

0 = near the lower band (historical bottoms)

100 = near the upper band (historical tops)

📊 How to Read

Oscillator > 80 → euphoric excess, often cycle tops

Oscillator < 20 → capitulation, often cycle bottoms

Works best on weekly or bi-weekly timeframes.

⚙️ Adjustable Parameters

Anchor date: starting point for the power-law fit (default: 2011).

Smoothing days: moving average applied to log-price (default: 365 days).

Upper / Lower multipliers: scale the bands to align with historical highs and lows.

✅ Best Use

Combine with other cycle signals (dominance ratios, macro indicators, sentiment).

Designed for long-term cycle analysis, not intraday trading.

PnL Bubble [%] | Fractalyst1. What's the indicator purpose?

The PnL Bubble indicator transforms your strategy's trade PnL percentages into an interactive bubble chart with professional-grade statistics and performance analytics. It helps traders quickly assess system profitability, understand win/loss distribution patterns, identify outliers, and make data-driven strategy improvements.

How does it work?

Think of this indicator as a visual report card for your trading performance. Here's what it does:

What You See

Colorful Bubbles: Each bubble represents one of your trades

Blue/Cyan bubbles = Winning trades (you made money)

Red bubbles = Losing trades (you lost money)

Bigger bubbles = Bigger wins or losses

Smaller bubbles = Smaller wins or losses

How It Organizes Your Trades:

Like a Photo Album: Instead of showing all your trades at once (which would be messy), it shows them in "pages" of 500 trades each:

Page 1: Your first 500 trades

Page 2: Trades 501-1000

Page 3: Trades 1001-1500, etc.

What the Numbers Tell You:

Average Win: How much money you typically make on winning trades

Average Loss: How much money you typically lose on losing trades

Expected Value (EV): Whether your trading system makes money over time

Positive EV = Your system is profitable long-term

Negative EV = Your system loses money long-term

Payoff Ratio (R): How your average win compares to your average loss

R > 1 = Your wins are bigger than your losses

R < 1 = Your losses are bigger than your wins

Why This Matters:

At a Glance: You can instantly see if you're a profitable trader or not

Pattern Recognition: Spot if you have more big wins than big losses

Performance Tracking: Watch how your trading improves over time

Realistic Expectations: Understand what "average" performance looks like for your system

The Cool Visual Effects:

Animation: The bubbles glow and shimmer to make the chart more engaging

Highlighting: Your biggest wins and losses get extra attention with special effects

Tooltips: hover any bubble to see details about that specific trade.

What are the underlying calculations?

The indicator processes trade PnL data using a dual-matrix architecture for optimal performance:

Dual-Matrix System:

• Display Matrix (display_matrix): Bounded to 500 trades for rendering performance

• Statistics Matrix (stats_matrix): Unbounded storage for complete statistical accuracy

Trade Classification & Aggregation:

// Separate wins, losses, and break-even trades

if val > 0.0

pos_sum += val // Sum winning trades

pos_count += 1 // Count winning trades

else if val < 0.0

neg_sum += val // Sum losing trades

neg_count += 1 // Count losing trades

else

zero_count += 1 // Count break-even trades

Statistical Averages:

avg_win = pos_count > 0 ? pos_sum / pos_count : na

avg_loss = neg_count > 0 ? math.abs(neg_sum) / neg_count : na

Win/Loss Rates:

total_obs = pos_count + neg_count + zero_count

win_rate = pos_count / total_obs

loss_rate = neg_count / total_obs

Expected Value (EV):

ev_value = (avg_win × win_rate) - (avg_loss × loss_rate)

Payoff Ratio (R):

R = avg_win ÷ |avg_loss|

Contribution Analysis:

ev_pos_contrib = avg_win × win_rate // Positive EV contribution

ev_neg_contrib = avg_loss × loss_rate // Negative EV contribution

How to integrate with any trading strategy?

Equity Change Tracking Method:

//@version=6

strategy("Your Strategy with Equity Change Export", overlay=true)

float prev_trade_equity = na

float equity_change_pct = na

if barstate.isconfirmed and na(prev_trade_equity)

prev_trade_equity := strategy.equity

trade_just_closed = strategy.closedtrades != strategy.closedtrades

if trade_just_closed and not na(prev_trade_equity)

current_equity = strategy.equity

equity_change_pct := ((current_equity - prev_trade_equity) / prev_trade_equity) * 100

prev_trade_equity := current_equity

else

equity_change_pct := na

plot(equity_change_pct, "Equity Change %", display=display.data_window)

Integration Steps:

1. Add equity tracking code to your strategy

2. Load both strategy and PnL Bubble indicator on the same chart

3. In bubble indicator settings, select your strategy's equity tracking output as data source

4. Configure visualization preferences (colors, effects, page navigation)

How does the pagination system work?

The indicator uses an intelligent pagination system to handle large trade datasets efficiently:

Page Organization:

• Page 1: Trades 1-500 (most recent)

• Page 2: Trades 501-1000

• Page 3: Trades 1001-1500

• Page N: Trades to

Example: With 1,500 trades total (3 pages available):

• User selects Page 1: Shows trades 1-500

• User selects Page 4: Automatically falls back to Page 3 (trades 1001-1500)

5. Understanding the Visual Elements

Bubble Visualization:

• Color Coding: Cyan/blue gradients for wins, red gradients for losses

• Size Mapping: Bubble size proportional to trade magnitude (larger = bigger P&L)

• Priority Rendering: Largest trades displayed first to ensure visibility

• Gradient Effects: Color intensity increases with trade magnitude within each category

Interactive Tooltips:

Each bubble displays quantitative trade information:

tooltip_text = outcome + " | PnL: " + pnl_str +

" Date: " + date_str + " " + time_str +

" Trade #" + str.tostring(trade_number) + " (Page " + str.tostring(active_page) + ")" +

" Rank: " + str.tostring(rank) + " of " + str.tostring(n_display_rows) +

" Percentile: " + str.tostring(percentile, "#.#") + "%" +

" Magnitude: " + str.tostring(magnitude_pct, "#.#") + "%"

Example Tooltip:

Win | PnL: +2.45%

Date: 2024.03.15 14:30

Trade #1,247 (Page 3)

Rank: 5 of 347

Percentile: 98.6%

Magnitude: 85.2%

Reference Lines & Statistics:

• Average Win Line: Horizontal reference showing typical winning trade size

• Average Loss Line: Horizontal reference showing typical losing trade size

• Zero Line: Threshold separating wins from losses

• Statistical Labels: EV, R-Ratio, and contribution analysis displayed on chart

What do the statistical metrics mean?

Expected Value (EV):

Represents the mathematical expectation per trade in percentage terms

EV = (Average Win × Win Rate) - (Average Loss × Loss Rate)

Interpretation:

• EV > 0: Profitable system with positive mathematical expectation

• EV = 0: Break-even system, profitability depends on execution

• EV < 0: Unprofitable system with negative mathematical expectation

Example: EV = +0.34% means you expect +0.34% profit per trade on average

Payoff Ratio (R):

Quantifies the risk-reward relationship of your trading system

R = Average Win ÷ |Average Loss|

Interpretation:

• R > 1.0: Wins are larger than losses on average (favorable risk-reward)

• R = 1.0: Wins and losses are equal in magnitude

• R < 1.0: Losses are larger than wins on average (unfavorable risk-reward)

Example: R = 1.5 means your average win is 50% larger than your average loss

Contribution Analysis (Σ):

Breaks down the components of expected value

Positive Contribution (Σ+) = Average Win × Win Rate

Negative Contribution (Σ-) = Average Loss × Loss Rate

Purpose:

• Shows how much wins contribute to overall expectancy

• Shows how much losses detract from overall expectancy

• Net EV = Σ+ - Σ- (Expected Value per trade)

Example: Σ+: 1.23% means wins contribute +1.23% to expectancy

Example: Σ-: -0.89% means losses drag expectancy by -0.89%

Win/Loss Rates:

Win Rate = Count(Wins) ÷ Total Trades

Loss Rate = Count(Losses) ÷ Total Trades

Shows the probability of winning vs losing trades

Higher win rates don't guarantee profitability if average losses exceed average wins

7. Demo Mode & Synthetic Data Generation

When using built-in sources (close, open, etc.), the indicator generates realistic demo trades for testing:

if isBuiltInSource(source_data)

// Generate random trade outcomes with realistic distribution

u_sign = prand(float(time), float(bar_index))

if u_sign < 0.5

v_push := -1.0 // Loss trade

else

// Skewed distribution favoring smaller wins (realistic)

u_mag = prand(float(time) + 9876.543, float(bar_index) + 321.0)

k = 8.0 // Skewness factor

t = math.pow(u_mag, k)

v_push := 2.5 + t * 8.0 // Win trade

Demo Characteristics:

• Realistic win/loss distribution mimicking actual trading patterns

• Skewed distribution favoring smaller wins over large wins

• Deterministic randomness for consistent demo results

• Includes jitter effects to prevent visual overlap

8. Performance Limitations & Optimizations

Display Constraints:

points_count = 500 // Maximum 500 dots per page for optimal performance

Pine Script v6 Limits:

• Label Count: Maximum 500 labels per indicator

• Line Count: Maximum 100 lines per indicator

• Box Count: Maximum 50 boxes per indicator

• Matrix Size: Efficient memory management with dual-matrix system

Optimization Strategies:

• Pagination System: Handle unlimited trades through 500-trade pages

• Priority Rendering: Largest trades displayed first for maximum visibility

• Dual-Matrix Architecture: Separate display (bounded) from statistics (unbounded)

• Smart Fallback: Automatic page clamping prevents empty displays

Impact & Workarounds:

• Visual Limitation: Only 500 trades visible per page

• Statistical Accuracy: Complete dataset used for all calculations

• Navigation: Use page input to browse through entire trade history

• Performance: Smooth operation even with thousands of trades

9. Statistical Accuracy Guarantees

Data Integrity:

• Complete Dataset: Statistics matrix stores ALL trades without limit

• Proper Aggregation: Separate tracking of wins, losses, and break-even trades

• Mathematical Precision: Pine Script v6's enhanced floating-point calculations

• Dual-Matrix System: Display limitations don't affect statistical accuracy

Calculation Validation:

// Verified formulas match standard trading mathematics

avg_win = pos_sum / pos_count // Standard average calculation

win_rate = pos_count / total_obs // Standard probability calculation

ev_value = (avg_win * win_rate) - (avg_loss * loss_rate) // Standard EV formula

Accuracy Features:

• Mathematical Correctness: Formulas follow established trading statistics

• Data Preservation: Complete dataset maintained for all calculations

• Precision Handling: Proper rounding and boundary condition management

• Real-Time Updates: Statistics recalculated on every new trade

10. Advanced Technical Features

Real-Time Animation Engine:

// Shimmer effects with sine wave modulation

offset = math.sin(shimmer_t + phase) * amp

// Dynamic transparency with organic flicker

new_transp = math.min(flicker_limit, math.max(-flicker_limit, cur_transp + dir * flicker_step))

• Sine Wave Shimmer: Dynamic glowing effects on bubbles

• Organic Flicker: Random transparency variations for natural feel

• Extreme Value Highlighting: Special visual treatment for outliers

• Smooth Animations: Tick-based updates for fluid motion

Magnitude-Based Priority Rendering:

// Sort trades by magnitude for optimal visual hierarchy

sort_indices_by_magnitude(values_mat)

• Largest First: Most important trades always visible

• Intelligent Sorting: Custom bubble sort algorithm for trade prioritization

• Performance Optimized: Efficient sorting for real-time updates

• Visual Hierarchy: Ensures critical trades never get hidden

Professional Tooltip System:

• Quantitative Data: Pure numerical information without interpretative language

• Contextual Ranking: Shows trade position within page dataset

• Percentile Analysis: Performance ranking as percentage

• Magnitude Scaling: Relative size compared to page maximum

• Professional Format: Clean, data-focused presentation

11. Quick Start Guide

Step 1: Add Indicator

• Search for "PnL Bubble | Fractalyst" in TradingView indicators

• Add to your chart (works on any timeframe)

Step 2: Configure Data Source

• Demo Mode: Leave source as "close" to see synthetic trading data

• Strategy Mode: Select your strategy's PnL% output as data source

Step 3: Customize Visualization

• Colors: Set positive (cyan), negative (red), and neutral colors

• Page Navigation: Use "Trade Page" input to browse trade history

• Visual Effects: Built-in shimmer and animation effects are enabled by default

Step 4: Analyze Performance

• Study bubble patterns for win/loss distribution

• Review statistical metrics: EV, R-Ratio, Win Rate

• Use tooltips for detailed trade analysis

• Navigate pages to explore full trade history

Step 5: Optimize Strategy

• Identify outlier trades (largest bubbles)

• Analyze risk-reward profile through R-Ratio

• Monitor Expected Value for system profitability

• Use contribution analysis to understand win/loss impact

12. Why Choose PnL Bubble Indicator?

Unique Advantages:

• Advanced Pagination: Handle unlimited trades with smart fallback system

• Dual-Matrix Architecture: Perfect balance of performance and accuracy

• Professional Statistics: Institution-grade metrics with complete data integrity

• Real-Time Animation: Dynamic visual effects for engaging analysis

• Quantitative Tooltips: Pure numerical data without subjective interpretations

• Priority Rendering: Intelligent magnitude-based display ensures critical trades are always visible

Technical Excellence:

• Built with Pine Script v6 for maximum performance and modern features

• Optimized algorithms for smooth operation with large datasets

• Complete statistical accuracy despite display optimizations

• Professional-grade calculations matching institutional trading analytics

Practical Benefits:

• Instantly identify system profitability through visual patterns

• Spot outlier trades and risk management issues

• Understand true risk-reward profile of your strategies

• Make data-driven decisions for strategy optimization

• Professional presentation suitable for performance reporting

Disclaimer & Risk Considerations:

Important: Historical performance metrics, including positive Expected Value (EV), do not guarantee future trading success. Statistical measures are derived from finite sample data and subject to inherent limitations:

• Sample Bias: Historical data may not represent future market conditions or regime changes

• Ergodicity Assumption: Markets are non-stationary; past statistical relationships may break down

• Survivorship Bias: Strategies showing positive historical EV may fail during different market cycles

• Parameter Instability: Optimal parameters identified in backtesting often degrade in forward testing

• Transaction Cost Evolution: Slippage, spreads, and commission structures change over time

• Behavioral Factors: Live trading introduces psychological elements absent in backtesting

• Black Swan Events: Extreme market events can invalidate statistical assumptions instantaneously

Indicator 102#M3indicator based on Daily and weekly fib Level. Initial Breakout and breakdowns have been denoted as well

[GrandAlgo] Moving Averages Cross LevelsMoving Averages Cross Levels

Many traders watch for moving average crossovers – such as the golden cross (50 MA crossing above 200 MA) or death cross – as signals of changing trends. However, once a crossover happens, the exact price level where it occurred often fades from view, even though that level can be an important reference point. Moving Averages Cross Levels is an indicator that keeps those crossover price levels visible on your chart, helping you track where momentum shifts occurred and how price behaves relative to those key levels.

This tool plots horizontal line segments at the price where each pair of selected moving averages crossed within a recent window of bars. Each level is labeled with the moving average lengths (for example, “21×50” for a 21/50 MA cross) and is color-coded – green for bullish crossovers (short-term MA crossing above long-term MA) and red for bearish crossunders (short-term crossing below). By visualizing these crossover levels, you can quickly identify past trend change points and use them as potential support/resistance or decision levels in your trading. Importantly, this indicator is non-repainting – once a crossover level is plotted, it remains fixed at the historical price where the cross occurred, allowing you to continually monitor that level going forward. (As with any moving average-based analysis, crossover signals are lagging, so use these levels in conjunction with other tools for confirmation.)

Key Features:

✅ Multiple Moving Averages: Track up to 7 different MAs (e.g. 5, 8, 21, 50, 64, 83, 200 by default) simultaneously. You can enable/disable each MA and set its length, allowing flexible combinations of short-term and long-term averages.

✅ Selectable MA Type: Each average can be calculated as a Simple (SMA), Exponential (EMA), Volume-Weighted (VWMA), or Smoothed (RMA) moving average, giving you flexibility to match your preferred method.

✅ Auto Crossover Detection: The script automatically detects all crosses between any enabled MA pairs, so you don’t have to specify pairs manually. Whether it’s a fast cross (5×8) or a long-term cross (50×200), every crossover within the lookback period will be identified and marked.

✅ Horizontal Level Markers: For each detected crossover, a horizontal line segment is drawn at the exact price where the crossover occurred. This makes it easy to glance at your chart and see precisely where two moving averages intersected in the recent past.

✅ Labeled and Color-Coded: Each crossover line is labeled with the two MA lengths that crossed (e.g. “50×200”) for clear identification. Colors indicate crossover direction – by default green for bullish (positive) crossovers and red for bearish (negative) crossovers – so you can tell at a glance which way the trend shifted. (You can customize these colors in the settings.)

✅ Adjustable Lookback: A “Crosses with X candles” input lets you control how far back the script looks for crossovers to plot. This prevents your chart from getting cluttered with too many old levels – for example, set X = 100 to show crossovers from roughly the last 100 bars. Older crossover lines beyond this lookback window will automatically clear off the chart.

✅ Optional MA Plots: You can toggle the display of each moving average line on the chart. This means you can either view just the crossover levels alone for a clean look, or also overlay the MA curves themselves for additional context (to see how price and MAs were moving around the crossover).

✅ No Repainting or Hindsight Bias: Once a crossover level is plotted, it stays at that fixed price. The indicator doesn’t move levels around after the fact – each line is a true historical event marker. This allows you to backtest visually: see how price acted after the crossover by observing if it retested or respected that level later.

How It Works:

1️⃣ Add to Chart & Configure – Simply add the indicator to your chart. In the settings, choose which moving averages you want to include and set their lengths. For example, you might enable 21, 50, 200 to focus on medium and long-term crosses (including the golden cross), or turn on shorter MAs like 5 and 8 for quick momentum shifts. Adjust the lookback (number of bars to scan for crosses) if needed.

2️⃣ Visualization – The script continuously checks the latest X bars for any points where one MA crossed above or below another. Whenever a crossover is found, it calculates the exact price level at which the two moving averages intersected. On the last bar of your chart, it will draw a horizontal line segment extending from the crossover bar to the current bar at that price level, and place a label to the right of the line with the MA lengths. Green lines/labels signify bullish crossovers (where the first MA crossed above the second), and red lines indicate bearish crossunders.

3️⃣ On Your Chart – You will see these labeled levels aligned with the price scale. For example, if a 50 MA crossed above a 200 MA (bullish) 50 bars ago at price $100, there will be a green “50×200” line at $100 extending to the present, showing you exactly where that golden cross happened. You might notice price pulling back near that level and bouncing, or if price falls back through it, it could signal a failed crossover. The indicator updates in real-time: if a new crossover happens on the latest bar, a new line and label will instantly appear, and if any old cross moves out of the lookback range, its line is removed to keep the chart focused.

4️⃣ Customization – You can fine-tune the appearance: toggle any MA’s visibility, change line colors or label styles, and modify the lookback length to suit different timeframes. For instance, on a 1-hour chart you might use a lookback of 500 bars to see a few weeks of cross history, whereas on a daily chart 100 bars (about 4–5 months) may be sufficient. Adjust these settings based on how many crossover levels you find useful to display.

Ideal for Traders Who:

Use MA Crossovers in Strategy: If your strategy involves moving average crossovers (for trend confirmation or entry/exit signals), this indicator provides an extra layer of insight by keeping the price of those crossover events in sight. For example, trend-followers can watch if price stays above a bullish crossover level as a sign of trend strength, or falls below it as a sign of weakness.

Identify Support/Resistance from MA Events: Crossover levels often coincide with pivot points in market sentiment. A crossover can act like a regime change – the level where it happened may turn into support or resistance. This tool helps you mark those potential S/R levels automatically. Rather than manually noting where a golden cross occurred, you’ll have it highlighted, which can be useful for setting stop-losses (e.g. below the crossover price in a bullish scenario) or profit targets.

Track Multiple Averages at Once: Instead of focusing on just one pair of moving averages, you might be interested in the interaction of several (short, medium, and long-term trends). This indicator caters to that by plotting all relevant crossovers among your chosen MAs. It’s great for multi-timeframe thinkers as well – e.g. you could apply it on a higher timeframe chart to mark major cross levels, then drill down to lower timeframes knowing those key prices.

Value Clean Visualization: There are no flashing signals or arrows – just simple lines and labels that enhance your chart’s storytelling. It’s ideal if you prefer to make trading decisions based on understanding price interaction with technical levels rather than following automatic trade calls. Moving Averages Cross Levels gives you information to act on, without imposing any bias or strategy – you interpret the crossover levels in the context of your own trading system.

MomentumScriptThis is Momentum Tracker based on Richard Driehaus' research:

1) 12–1 momentum (return from t-12 months to t-1 month

2) FIP / path efficiency (many small up days > one big gap)

3) Proximity to 52-week high/low