TradeUniv.com Expected MovesTradeUniv.com Expected Moves

See where the market expects stocks to move based on options pricing data. This indicator shows you upper and lower price levels that help identify potential support, resistance, and overextended moves.

What Are Expected Moves?

Expected moves are calculated from option prices and show where the market thinks a stock is likely to trade by the end of the day or week. Think of them as probability zones - when price reaches or crosses these levels, it may signal an unusual

move or potential reversal opportunity.

What You'll See on Your Chart:

• Upper Level (Green) - Expected high for the period

• Lower Level (Red) - Expected low for the period• Midpoint (Gray) - Previous day's closing price (your reference point)

• Shaded Area - The expected trading range between levels

How to Use:

1. Visit www.tradeuniv.com

2. Select your favorite tickers

3. Click "Generate Script" and copy the TradingView input

4. Paste it into this indicator's settings

5. The indicator automatically shows the expected moves for whatever chart you're viewing

Perfect For:

• Day traders planning entry and exit zones

• Identifying when price has moved "too far too fast"

• Spotting potential reversal areas

• Understanding daily volatility expectations

• Planning option strategies around expected ranges

Features:

• Automatically detects daily vs weekly expirations (SPY, IWM, QQQ use daily; others use weekly)

• Customizable colors and line styles

• Price crossing alerts (get notified when price breaks above/below expected levels)

• Works on any timeframe

• Clean, minimal chart display

Important:

• Requires TradeUniv.com free account to generate data

• Refresh your data daily for accurate calculations

• Only shows levels for tickers you selected when generating

Expectedmove

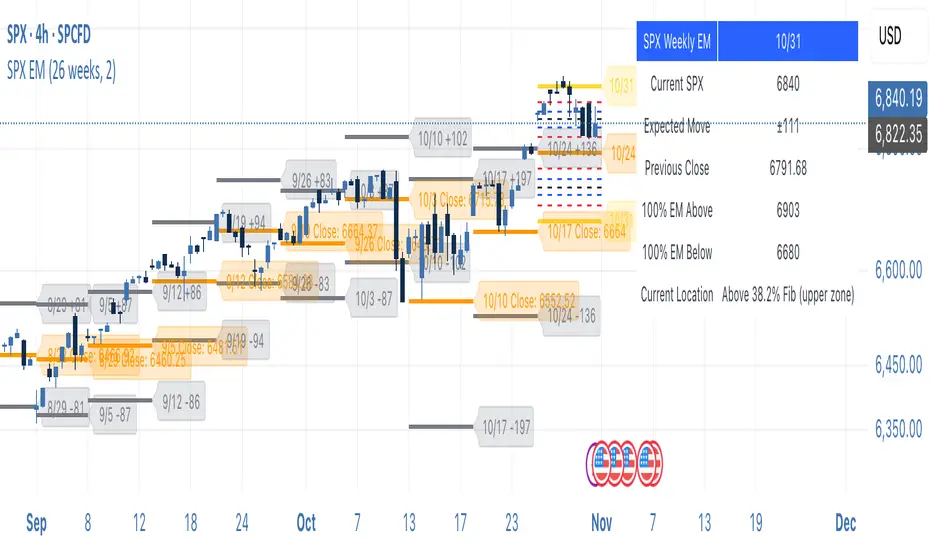

SPX Weekly Expected Moves# SPX Weekly Expected Moves Indicator

A professional Pine Script indicator for TradingView that displays weekly expected move levels for SPX based on real options data, with integrated Fibonacci retracement analysis and intelligent alerting system.

## Overview

This indicator helps options and equity traders visualize weekly expected move ranges for the S&P 500 Index (SPX) by plotting historical and current week expected move boundaries derived from weekly options pricing. Unlike theoretical volatility calculations, this indicator uses actual market-based expected move data that you provide from options platforms.

## Key Features

### 📈 **Expected Move Visualization**

- **Historical Lines**: Display past weeks' expected moves with configurable history (10, 26, or 52 weeks)

- **Current Week Focus**: Highlighted current week with extended lines to present time

- **Friday Close Reference**: Orange baseline showing the previous Friday's close price

- **Timeframe Independent**: Works consistently across all chart timeframes (1m to 1D)

### 🎯 **Fibonacci Integration**

- **Five Fibonacci Levels**: 23.6%, 38.2%, 50%, 61.8%, 76.4% between Friday close and expected move boundaries

- **Color-Coded Levels**:

- Red: 23.6% & 76.4% (outer levels)

- Blue: 38.2% & 61.8% (golden ratio levels)

- Black: 50% (midpoint - most critical level)

- **Current Week Only**: Fibonacci levels shown only for active trading week to reduce clutter

### 📊 **Real-Time Information Table**

- **Current SPX Price**: Live market price

- **Expected Move**: ±EM value for current week

- **Previous Close**: Friday close price (baseline for calculations)

- **100% EM Levels**: Exact upper and lower boundary prices

- **Current Location**: Real-time position within the EM structure (e.g., "Above 38.2% Fib (upper zone)")

### 🚨 **Intelligent Alert System**

- **Zone-Aware Alerts**: Separate alerts for upper and lower zones

- **Key Level Breaches**: Alerts for 23.6% and 76.4% Fibonacci level crossings

- **Bar Close Based**: Alerts trigger on confirmed bar closes, not tick-by-tick

- **Customizable**: Enable/disable alerts through settings

## How It Works

### Data Input Method

The indicator uses a **manual data entry approach** where you input actual expected move values obtained from options platforms:

```pinescript

// Add entries using the options expiration Friday date

map.put(expected_moves, 20250613, 91.244) // Week ending June 13, 2025

map.put(expected_moves, 20250620, 95.150) // Week ending June 20, 2025

```

### Weekly Structure

- **Monday 9:30 AM ET**: Week begins

- **Friday 4:00 PM ET**: Week ends

- **Lines Extend**: From Monday open to Friday close (historical) or current time + 5 bars (current week)

- **Timezone Handling**: Uses "America/New_York" for proper DST handling

### Calculation Logic

1. **Base Price**: Previous Friday's SPX close price

2. **Expected Move**: Market-derived ±EM value from weekly options

3. **Upper Boundary**: Friday Close + Expected Move

4. **Lower Boundary**: Friday Close - Expected Move

5. **Fibonacci Levels**: Proportional levels between Friday close and EM boundaries

## Setup Instructions

### 1. Data Collection

Obtain weekly expected move values from options platforms such as:

- **ThinkOrSwim**: Use thinkBack feature to look up weekly expected moves

- **Tastyworks**: Check weekly options expected move data

- **CBOE**: Reference SPX weekly options data

- **Manual Calculation**: (ATM Call Premium + ATM Put Premium) × 0.85

### 2. Data Entry

After each Friday close, update the indicator with the next week's expected move:

```pinescript

// Example: On Friday June 7, 2025, add data for week ending June 13

map.put(expected_moves, 20250613, 91.244) // Actual EM value from your platform

```

### 3. Configuration

Customize the indicator through the settings panel:

#### Visual Settings

- **Show Current Week EM**: Toggle current week display

- **Show Past Weeks**: Toggle historical weeks display

- **Max Weeks History**: Choose 10, 26, or 52 weeks of history

- **Show Fibonacci Levels**: Toggle Fibonacci retracement levels

- **Label Controls**: Customize which labels to display

#### Colors

- **Current Week EM**: Default yellow for active week

- **Past Weeks EM**: Default gray for historical weeks

- **Friday Close**: Default orange for baseline

- **Fibonacci Levels**: Customizable colors for each level type

#### Alerts

- **Enable EM Breach Alerts**: Master toggle for all alerts

- **Specific Alerts**: Four alert types for Fibonacci level breaches

## Trading Applications

### Options Trading

- **Straddle/Strangle Positioning**: Visualize breakeven levels for neutral strategies

- **Directional Plays**: Assess probability of reaching target levels

- **Earnings Plays**: Compare actual vs. expected move outcomes

### Equity Trading

- **Support/Resistance**: Use EM boundaries and Fibonacci levels as key levels

- **Breakout Trading**: Monitor for moves beyond expected ranges

- **Mean Reversion**: Look for reversals at extreme Fibonacci levels

### Risk Management

- **Position Sizing**: Gauge likely price ranges for the week

- **Stop Placement**: Use Fibonacci levels for logical stop locations

- **Profit Targets**: Set targets based on EM structure probabilities

## Technical Implementation

### Performance Features

- **Memory Managed**: Configurable history limits prevent memory issues

- **Timeframe Independent**: Uses timestamp-based calculations for consistency

- **Object Management**: Automatic cleanup of drawing objects prevents duplicates

- **Error Handling**: Robust bounds checking and NA value handling

### Pine Script Best Practices

- **v6 Compliance**: Uses latest Pine Script version features

- **User Defined Types**: Structured data management with WeeklyEM type

- **Efficient Drawing**: Smart line/label creation and deletion

- **Professional Standards**: Clean code organization and comprehensive documentation

## Customization Guide

### Adding New Weeks

```pinescript

// Add after market close each Friday

map.put(expected_moves, YYYYMMDD, EM_VALUE)

```

### Color Schemes

Customize colors for different trading styles:

- **Dark Theme**: Use bright colors for visibility

- **Light Theme**: Use contrasting dark colors

- **Minimalist**: Use single color with transparency

### Label Management

Control label density:

- **Show Current Week Labels Only**: Reduce clutter for active trading

- **Show All Labels**: Full information for analysis

- **Selective Display**: Choose specific label types

## Troubleshooting

### Common Issues

1. **No Lines Appearing**: Check that expected move data is entered for current/recent weeks

2. **Wrong Time Display**: Ensure "America/New_York" timezone is properly handled

3. **Duplicate Lines**: Restart indicator if drawing objects appear duplicated

4. **Missing Fibonacci Levels**: Verify "Show Fibonacci Levels" is enabled

### Data Validation

- **Expected Move Format**: Use positive numbers (e.g., 91.244, not ±91.244)

- **Date Format**: Use YYYYMMDD format (e.g., 20250613)

- **Reasonable Values**: Verify EM values are realistic (typically 50-200 for SPX)

## Version History

### Current Version

- **Pine Script v6**: Latest version compatibility

- **Fibonacci Integration**: Five-level retracement analysis

- **Zone-Aware Alerts**: Upper/lower zone differentiation

- **Dynamic Line Management**: Smart current week extension

- **Professional UI**: Comprehensive information table

### Future Enhancements

- **Multiple Symbols**: Extend beyond SPX to other indices

- **Automated Data**: Integration with options data APIs

- **Statistical Analysis**: Success rate tracking for EM predictions

- **Additional Levels**: Custom percentage levels beyond Fibonacci

## License & Usage

This indicator is designed for educational and trading purposes. Users are responsible for:

- **Data Accuracy**: Ensuring correct expected move values

- **Risk Management**: Proper position sizing and risk controls

- **Market Understanding**: Comprehending options-based expected move concepts

## Support

For questions, issues, or feature requests related to this indicator, please refer to the code comments and documentation within the Pine Script file.

---

**Disclaimer**: This indicator is for informational purposes only. Trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results.

DAILY ATR LEVELS AND EXPECTED MOVE LEVELSThis Pine Script code is designed to visualize ATR (Average True Range) levels and expected move levels on a chart. It provides useful inputs for customizing how these levels are displayed, such as line width, style, and color. The script is divided into several sections, each focused on a different feature:

1. User Inputs for Customization:

- Line Width and Style: Users can customize the line width, style (solid, dotted, or dashed), and color for various levels.

- Offset for Line Placement: The rightOffset input controls how far in the future the lines extend (measured in minutes).

- Show Labels: Labels can be toggled on/off for ATR levels and expected move lines, with customizable text colors.

2. ATR Levels and ATR Settings:

- The ATR length (atrLength) and the multiplier (atrMultiplier) control the calculation of ATR levels.

- The script plots ATR levels based on the daily open price, including key levels like ATR +25%, ATR +50%, etc., for both positive and negative movements.

- Line Drawing: The script dynamically creates lines for each ATR level, and the lines are customized according to the user's inputs. For each level, the line.new function is used to plot a line from the start of the day (daily open) to a point offset in the future.

- Labels: Labels are added near each ATR level to make them more identifiable, such as "ATR +25%" or "Daily Open."

3. Expected Move Calculation and Logic:

- The script calculates the expected move for the next trading session based on the previous close price and the volatility derived from the VIX (Volatility Index).

- The expected move is calculated as a percentage of the previous close and is added and subtracted from the previous close price to generate upper and lower levels.

- Volatility Adjustment: The VIX value is adjusted by the square root of 252 (the number of average trading days in a year) to calculate the daily volatility.

- Upper and Lower Lines: Lines are drawn for the expected move's upper and lower bounds, showing the potential price movement based on volatility.

4. Customizable Expected Move Lines:

- Line Style and Color: The upper and lower expected move lines can be customized in terms of width, style, and color, as specified by the user.

- Labels for Expected Move Levels: Labels are added for the upper and lower expected move lines, such as "Expected Move Upper" and "Expected Move Lower."

5. Logic for Drawing Lines:

- The script continuously evaluates whether the levels should be displayed based on the user's preferences.

- If showATRLevels or showLineEM is enabled, the script will draw the respective lines and labels on the chart.

- It uses line.new to draw the lines and label.new to position the labels at the correct levels on the chart.

6. Handling Time and Line Deletion:

- The script handles the dynamic nature of the chart by deleting previous lines (using line.delete) to avoid cluttering the chart with outdated lines.

- The time for the lines is set dynamically using the startTime and endTime variables, ensuring that lines are drawn within the correct timeframe.

Summary of Key Features:

- ATR Levels: Plots key levels of ATR, such as daily open, ATR +25%, ATR -25%, etc., with customizable colors and line styles.

- Expected Move Levels: Calculates and plots the upper and lower bounds of the expected move based on the VIX and previous close price.

- Customization Options: Users can control the appearance (line width, style, color) and whether to show labels for the ATR and expected move levels.

- Dynamic Updates: The lines and labels update dynamically throughout the trading day, adjusting based on market conditions.

Overall, this script is designed to help traders visualize volatility and potential price movement on a daily chart by providing ATR-based levels and expected move projections. It offers a high degree of customization to suit different charting preferences.

Options Overlay [Pro] IVR IV Skew Delta Exp.mv MurreyMath Expiry

𝗧𝗵𝗲 𝗳𝗶𝗿𝘀𝘁 𝗿𝗲𝗮𝗹 𝗼𝗽𝘁𝗶𝗼𝗻𝘀 𝗱𝗮𝘁𝗮 𝗶𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿 𝗼𝗻 𝗧𝗿𝗮𝗱𝗶𝗻𝗴𝗩𝗶𝗲𝘄, 𝗮𝘃𝗮𝗶𝗹𝗮𝗯𝗹𝗲 𝗳𝗼𝗿 𝗼𝘃𝗲𝗿 𝟭𝟱𝟬+ 𝗹𝗶𝗾𝘂𝗶𝗱 𝗨𝗦 𝗺𝗮𝗿𝗸𝗲𝘁 𝘀𝘆𝗺𝗯𝗼𝗹𝘀.

🔃 Auto-Updating Option Metrics without refresh!

🍒 Developed and maintained by option traders for option traders.

📈 Specifically designed for TradingView users who trade options.

Our indicator provides essential key metrics such as:

✅ IVRank

✅ IVx

✅ 5-Day IVx Change

✅ Delta curves and interpolated distances

✅ Expected move curve

✅ Standard deviation (STD1) curve

✅ Vertical Pricing Skew

✅ Horizontal IVx Skew

✅ Delta Skew

like TastyTrade, TOS, IBKR etc, but in a much more visually intuitive way. See detailed descriptions below.

If this isn't enough, we also include a unique grid system designed specifically for options traders. This package features our innovative dynamic grid system:

✅ Enhanced Murrey Math levels (horizontal scale)

✅ Options expirations (vertical scale)

Designed to help you assess market conditions and make well-informed trading decisions, this tool is an essential addition for every serious options trader!

Ticker Information:

This indicator is currently implemented for more than 150 liquid US market tickers and we are continuously expanding the list:

SP:SPX AMEX:SPY NASDAQ:QQQ NASDAQ:TLT AMEX:GLD

NYSE:AA NASDAQ:AAL NASDAQ:AAPL NYSE:ABBV NASDAQ:ABNB NASDAQ:AMD NASDAQ:AMZN AMEX:ARKK NASDAQ:AVGO NYSE:AXP NYSE:BA NYSE:BABA NYSE:BAC NASDAQ:BIDU AMEX:BITO NYSE:BMY NYSE:BP NASDAQ:BYND NYSE:C NYSE:CAT NYSE:CCJ NYSE:CCL NASDAQ:COIN NYSE:COP NASDAQ:COST NYSE:CRM NASDAQ:CRWD NASDAQ:CSCO NYSE:CVNA NYSE:CVS NYSE:CVX NYSE:DAL NASDAQ:DBX AMEX:DIA NYSE:DIS NASDAQ:DKNG NASDAQ:EBAY NASDAQ:ETSY NASDAQ:EXPE NYSE:F NYSE:FCX NYSE:FDX AMEX:FXI AMEX:GDX AMEX:GDXJ NYSE:GE NYSE:GM NYSE:GME NYSE:GOLD NASDAQ:GOOG NASDAQ:GOOGL NYSE:GPS NYSE:GS NASDAQ:HOOD NYSE:IBM NASDAQ:IEF NASDAQ:INTC AMEX:IWM NASDAQ:JD NYSE:JNJ NYSE:JPM NYSE:JWN NYSE:KO NYSE:LLY NYSE:LOW NYSE:LVS NYSE:MA NASDAQ:MARA NYSE:MCD NYSE:MET NASDAQ:META NYSE:MGM NYSE:MMM NYSE:MPC NYSE:MRK NASDAQ:MRNA NYSE:MRO NASDAQ:MRVL NYSE:MS NASDAQ:MSFT AMEX:MSOS NYSE:NCLH NASDAQ:NDX NYSE:NET NASDAQ:NFLX NYSE:NIO NYSE:NKE NASDAQ:NVDA NASDAQ:ON NYSE:ORCL NYSE:OXY NASDAQ:PEP NYSE:PFE NYSE:PINS NYSE:PLTR NASDAQ:PTON NASDAQ:PYPL NASDAQ:QCOM NYSE:RBLX NYSE:RCL NASDAQ:RIOT NASDAQ:RIVN NASDAQ:ROKU NASDAQ:SBUX NYSE:SHOP AMEX:SLV NASDAQ:SMCI NASDAQ:SMH NYSE:SNAP NYSE:SQ NYSE:T NYSE:TGT NASDAQ:TQQQ NASDAQ:TSLA NYSE:TSM NASDAQ:TTD NASDAQ:TXN NYSE:U NASDAQ:UAL NYSE:UBER AMEX:UNG NYSE:UPS NASDAQ:UPST AMEX:USO NYSE:V AMEX:VXX NYSE:VZ NASDAQ:WBA NYSE:WFC NYSE:WMT NASDAQ:WYNN NYSE:X AMEX:XHB AMEX:XLE AMEX:XLF AMEX:XLI AMEX:XLK AMEX:XLP AMEX:XLU AMEX:XLV AMEX:XLY NYSE:XOM NYSE:XPEV CBOE:XSP NASDAQ:ZM

How does the indicator work and why is it unique?

This Pine Script indicator is a complex tool designed to provide various option metrics and visualization tools for options market traders. The indicator extracts raw options data from an external data provider (ORATS), processes and refines the delayed data package using pineseed, and sends it to TradingView, visualizing the data using specific formulas (see detailed below) or interpolated values (e.g., delta distances). This method of incorporating options data into a visualization framework is unique and entirely innovative on TradingView.

The indicator aims to offer a comprehensive view of the current state of options for the implemented instruments, including implied volatility (IV), IV rank (IVR), options skew, and expected market movements, which are objectively measured as detailed below.

The options metrics we display may be familiar to options traders from various major brokerage platforms such as TastyTrade, IBKR, TOS, Tradier, TD Ameritrade, Schwab, etc.

🟨 𝗗𝗘𝗧𝗔𝗜𝗟𝗘𝗗 𝗗𝗢𝗖𝗨𝗠𝗘𝗡𝗧𝗔𝗧𝗜𝗢𝗡 🟨

🔶 Auto-Updating Option Metrics and Curved Lines

🔹 Interpolated DELTA Curves (16,20,25,30,40)

In our indicator, the curve layer settings allow you to choose the delta value for displaying the delta curve: 16, 20, 25, 30, or even 40. The color of the curve can be customized, and you can also hide the delta curve by selecting the "-" option.

It's important to mention that we display interpolated deltas from the actual option chain of the underlying asset using the Black-Scholes model. This ensures that the 16 delta truly reflects the theoretical, but accurate, 16 delta distance. (For example, deltas shown by brokerages for individual strikes are rounded; a 0.16 delta might actually be 0.1625.)

🔹 Expected Move Curve (Exp.mv)

The expected move is the predicted dollar change in the underlying stock's price by a given option's expiration date, with 68% certainty. It is calculated using the expiration's pricing and implied volatility levels. We chose the TastyTrade method for calculating expected move, as we found it to be the most expressive.

Expected Move Calculation

Expected Move = (ATM straddle price x 0.6) + (1st OTM strangle price x 0.3) + (2nd OTM strangle price x 0.1)

For example , if stock XYZ is trading at 121 and the ATM straddle is 4.40, the 120/122 strangle is 3.46, and the 119/123 strangle is 2.66, the expected move is calculated as follows: 4.40 x 0.60 = 2.64; 3.46 x 0.30 = 1.04; 2.66 x 0.10 = 0.27; Expected move = 2.64 + 1.04 + 0.27 = ±3.9

In this example below, the TastyTrade platform indicates the expected move on the option chain with a brown color, and the exact value is displayed behind the ± symbol for each expiration. By default, we also use brown for this indication, but this can be changed or the curve display can be turned off.

🔹 Standard Deviation Curve (1 STD)

One standard deviation of a stock encompasses approximately 68.2% of outcomes in a distribution of occurrences based on current implied volatility.

We use the expected move formula to calculate the one standard deviation range of a stock. This calculation is based on the days-to-expiration (DTE) of our option contract, the stock price, and the implied volatility of a stock:

Calculation:

Standard Deviation = Closing Price * Implied Volatility * sqrt(Days to Expiration / 365)

According to options literature, there is a 68% probability that the underlying asset will fall within this one standard deviation range at expiration.

If the 1 STD and Exp.mv displays are both enabled, the indicator fills the area between them with a light gray color. This is because both represent probability distributions that appear as a "bell curve" when graphed, making it visually appealing.

Tip and Note:

The 1 STD line might appear jagged at times , which does not indicate a problem with the indicator. This is normal immediately after market open (e.g., during the first data refresh of the day) or if the expirations are illiquid (e.g., weekly expirations). The 1 STD value is calculated based on the aggregated IVx for the expirations, and the aggregated IVx value for weekly expirations updates less frequently due to lower trading volume. In such cases, we recommend enabling the "Only Monthly Expirations" option to smooth out the bell curve.

∑ Quant Observation:

The values of the expected move and the 1st standard deviation (1STD) will not match because they use different calculation methods, even though both are referred to as representing 68% of the underlying asset's movement in options literature. The expected move is based on direct market pricing of ATM options. The 1STD, on the other hand, uses the averaged implied volatility (IVX) for the given expiration to determine its value. Based on our experience, it is better to consider the area between the expected move and the 1STD as the true representation of the original 68% rule.

🔶 IVR Dashboard Panel Rows

🔹 IVR (IV Rank)

The Implied Volatility Rank (IVR) indicator helps options traders assess the current level of implied volatility (IV) in comparison to the past 52 weeks. IVR is a useful metric to determine whether options are relatively cheap or expensive. This can guide traders on whether to buy or sell options. We calculate IVrank, like TastyTrade does.

IVR Calculation:

IV Rank = (current IV - 52 week IV low) / (52 week IV high - 52 week IV low)

IVR Levels and Interpretations:

IVR 0-10 (Green): Very low implied volatility rank. Options might be "cheap," potentially a good time to buy options.

IVR 10-35 (White): Normal implied volatility rank. Options pricing is relatively standard.

IVR 35-50 (Orange): Almost high implied volatility rank.

IVR 50-75 (Red): Definitely high implied volatility rank. Options might be "expensive," potentially a good time to sell options for higher premiums.

IVR above 75 (Highlighted Red): Ultra high implied volatility rank. Indicates very high levels, suggesting a favorable time for selling options.

The panel refreshes automatically if the symbol is implemented. You can hide the panel or change the position and size.

🔹IVx (Implied Volatility Index)

The Implied Volatility Index (IVx) displayed in the option chain is calculated similarly to the VIX. The Cboe uses standard and weekly SPX options to measure the expected volatility of the S&P 500. A similar method is utilized to calculate IVx for each option expiration cycle.

For our purposes on the IVR Panel, we aggregate the IVx values specifically for the 35-70 day monthly expiration cycle . This aggregated value is then presented in the screener and info panel, providing a clear and concise measure of implied volatility over this period.

IVx Color coding:

IVx above 30 is displayed in orange.

IVx above 60 is displayed in red

IVx on curve:

The IVx values for each expiration can be viewed by hovering the mouse over the colored tooltip labels above the Curve.

IVx avg on IVR panel :

If the option is checked in the IVR panel settings, the IVR panel will display the average IVx values up to the optimal expiration.

Important Note:

The IVx value alone does not provide sufficient context. There are stocks that inherently exhibit high IVx values. Therefore, it is crucial to consider IVx in conjunction with the Implied Volatility Rank (IVR), which measures the IVx relative to its own historical values. This combined view helps in accurately assessing the significance of the IVx in relation to the specific stock's typical volatility behavior.

This indicator offers traders a comprehensive view of implied volatility, assisting them in making informed decisions by highlighting both the absolute and relative volatility measures.

🔹IVx 5 days change %

We are displaying the five-day change of the IV Index (IVx value). The IV Index 5-Day Change column provides quick insight into recent expansions or decreases in implied volatility over the last five trading days.

Traders who expect the value of options to decrease might view a decrease in IVX as a positive signal. Strategies such as Strangle and Ratio Spread can benefit from this decrease.

On the other hand, traders anticipating further increases in IVX will focus on the rising IVX values. Strategies like Calendar Spread or Diagonal Spread can take advantage of increasing implied volatility.

This indicator helps traders quickly assess changes in implied volatility, enabling them to make informed decisions based on their trading strategies and market expectations.

🔹 Vertical Pricing Skew

At TanukiTrade, Vertical Pricing Skew refers to the difference in pricing between put and call options with the same expiration date at the same distance (at expected move). We analyze this skew to understand market sentiment. This is the same formula used by TastyTrade for calculations.

We calculate the interpolated strike price based on the expected move , taking into account the neighboring option prices and their distances. This allows us to accurately determine whether the CALL or PUT options are more expensive.

PUT Skew (red): Put options are more expensive than call options, indicating the market expects a downward move (▽). If put options are more expensive by more than 20% at the same expected move distance, we color it lighter red.

CALL Skew (green): Call options are more expensive than put options, indicating the market expects an upward move (△). If call options are priced more than 30% higher at the examined expiration, we color it lighter green.

Vertical Skew on Curve:

The degree of vertical pricing skew for each expiration can be viewed by hovering over the points above the curve. Hover with mouse for more information.

Vertical Skew on IVR panel:

We focus on options with 35-70 days to expiration (DTE) for optimal analysis in case of vertical skew. Hover with mouse for more information.

This approach helps us gauge market expectations accurately, providing insights into potential price movements. Remember, we always evaluate the skew at the expected move using linear interpolation to determine the theoretical pricing of options.

🔹 Delta Skew 🌪️ (Twist)

We have a new metric that examines which monthly expiration indicates a "Delta Skew Twist" where the 16 delta deviates from the monthly STD. This is important because, under normal circumstances, the 16 delta is positioned between the expected move and the standard deviation (STD1) line (see Exp.mv & 1STD exact definitions above). However, if the interpolated 16 delta line exceeds the STD1 line either upwards or downwards, it represents a special case of vertical skew on the option chain.

Normal case : exp.move < delta16 < std1

Delta Skew Twist: exp.move < std1 < delta16

We indicate this with direction-specific colors (red/green) on the delta line. We also color the section of the delta curve affected by the delta skew in this case, even if you choose to display a lower delta, such as 30, instead of 16.

If "Colored Labels with Tooltips" is enabled, we also display a 🌪️ symbol in the tooltip for the expirations affected by Delta Skew.

If you have enabled the display of 'Vertical Pricing Skew' on the IVR Panel, a 🌪️ symbol will also appear next to the value of the vertical skew, and the tooltip will indicate from which expiration Delta Skew is observed.

🔹 Horizontal IVx Skew

In options pricing, it is typically expected that the implied volatility (IVx) increases for options with later expiration dates. This means that options further out in time are generally more expensive. At TanukiTrade, we refer to the phenomenon where this expectation is reversed—when the IVx decreases between two consecutive expirations—as Horizontal Skew or IVx Skew.

Horizontal IVx Skew occurs when: Front Expiry IVx < Back Expiry IVx

This scenario can create opportunities for traders who prefer diagonal or calendar strategies . Based on our experience, we categorize Horizontal Skew into two types:

Weekly Horizontal Skew:

When IVx skew is observed between two consecutive non-monthly expirations, the displayed value is the rounded-up percentage difference. On hover, the approximate location of this skew is also displayed. The precise location can be seen on this indicator.

Monthly Horizontal Skew:

When IVx skew is observed between two consecutive monthly expirations , the displayed value is the rounded-up percentage difference. On hover, the approximate location of this skew is also displayed. The precise location can be seen on our Overlay indicator.

The Monthly Vertical IVx skew is consistently more liquid than the weekly vertical IVx skew. Weekly Horizontal IVx Skew may not carry relevant information for symbols not included in the 'Weeklies & Volume Masters' preset in our Options Screener indicator.

If the options chain follows the normal IVx pattern, no skew value is displayed.

Color codes or tooltip labels above curve:

Gray - No horizontal skew;

Purple - Weekly horizontal skew;

BigBlue - Monthly horizontal skew

The display of monthly and weekly IVx skew can be toggled on or off on the IVR panel. However, if you want to disable the colored tooltips above the curve, this can only be done using the "Colored labels with tooltips" switch.

We indicate this range with colorful information bubbles above the upper STD line.

🔶 The Option Trader’s GRID System: Adaptive MurreyMath + Expiry Lines

At TanukiTrade, we utilize Enhanced MurreyMath and Expiry lines to create a dynamic grid system, unlike the basic built-in vertical grids in TradingView, which provide no insight into specific price levels or option expirations.

These grids are beneficial because they provide a structured layout, making important price levels visible on the chart. The grid automatically resizes as the underlying asset's volatility changes, helping traders identify expected movements for various option expirations.

The Option Trader’s GRID System part of this indicator can be used without limitations for all instruments . There are no type or other restrictions, and it automatically scales to fit every asset. Even if we haven't implemented the option metrics for a particular underlying asset, the GRID system will still function!

🔹 SETUP OF YOUR OPTIONS GRID SYSTEM

You can setup your new grid system in 3 easy steps!

STEP1: Hide default horizontal grid lines in TradingView

Right-click on an empty area of your chart, then select “Settings.” In the Chart settings -> Canvas -> Grid lines section, disable the display of horizontal lines to avoid distraction.

SETUP STEP2: Scaling fix

Right-click on the price scale on the right side, then select "Scale price chart only" to prevent the chart from scaling to the new horizontal lines!

STEP3: Enable Tanuki Options Grid

As a final step, make sure that both the vertical (MurreyMath) and horizontal (Expiry) lines are enabled in the Grid section of our indicator.

You are done, enjoy the new grid system!

🔹 HORIZONTAL: Enhanced MurreyMath Lines

Murrey Math lines are based on the principles observed by William Gann, renowned for his market symmetry forecasts. Gann's techniques, such as Gann Angles, have been adapted by Murrey to make them more accessible to ordinary investors. According to Murrey, markets often correct at specific price levels, and breakouts or returns to these levels can signal good entry points for trades.

At TanukiTrade, we enhance these price levels based on our experience , ensuring a clear display. We acknowledge that while MurreyMath lines aren't infallible predictions, they are useful for identifying likely price movements over a given period (e.g., one month) if the market trend aligns.

Our opinion: MurreyMath lines are not crystal balls (like no other tool). They should be used to identify that if we are trading in the right direction, the price is likely to reach the next unit step within a unit time (e.g. monthly expiration).

One unit step is the distance between Murrey Math lines, such as between the 0/8 and 1/8 lines. This interval helps identify different quadrants and is crucial for recognizing support and resistance levels.

Some option traders use Murrey Math lines to gauge the movement speed of an instrument over a unit time. A quadrant encompasses 4 unit steps.

Key levels, according to TanukiTrade, include:

Of course, the lines can be toggled on or off, and their default color can also be changed.

🔹 VERTICAL: Expiry Lines

The indicator can display monthly and weekly expirations as dashed lines, with customizable colors. Weekly expirations will always appear in a lighter shade compared to monthly expirations.

Monthly Expiry Lines:

You can turn off the lines indicating monthly expirations, or set the direction (past/future/both) and the number of lines to be drawn.

Weekly Expiry Lines:

You can display weekly expirations pointing to the future. You can also turn them off or specify how many weeks ahead the lines should be drawn.

Of course, the lines can be toggled on or off, and their default color can also be changed.

TIP: Hide default vertical grid lines in TradingView

Right-click on an empty area of your chart, then select “Settings.” In the Chart settings -> Canvas -> Grid lines section, disable the display of vertical lines to avoid distraction. Same, like steps above at MurreyMath lines.

🔶 ADDITIONAL IMPORTANT COMMENTS

- U.S. market only:

Since we only deal with liquid option chains: this option indicator only works for the USA options market and do not include future contracts; we have implemented each selected symbol individually.

- Why is there a slight difference between the displayed data and my live brokerage data? There are two reasons for this, and one is beyond our control.

- Brokerage Calculation Differences:

Every brokerage has slight differences in how they calculate metrics like IV and IVx. If you open three windows for TOS, TastyTrade, and IBKR side by side, you will notice that the values are minimally different. We had to choose a standard, so we use the formulas and mathematical models described by TastyTrade when analyzing the options chain and drawing conclusions.

- Option-data update frequency:

According to TradingView's regulations and guidelines, we can update external data a maximum of 5 times per day. We strive to use these updates in the most optimal way:

(1st update) 15 minutes after U.S. market open

(2nd, 3rd, 4th updates) 1.5–3 hours during U.S. market open hours

(5th update) 10 minutes before market close.

You don’t need to refresh your window, our last refreshed data-pack is always automatically applied to your indicator , and you can see the time elapsed since the last update at the bottom of your indicator.

- Skewed Curves:

The delta, expected move, and standard deviation curves also appear relevantly on a daily or intraday timeframe. Data loss is experienced above a daily timeframe: this is a TradingView limitation.

- Weekly illiquid expiries:

Especially for instruments where weekly options are illiquid: the weekly expiration STD1 data is not relevant. In these cases, we recommend checking in the "Display only Monthly labels" checkbox to avoid displaying not relevant weekly options expirations.

-Timeframe Issues:

Our option indicator visualizes relevant data on a daily resolution. If you see strange or incorrect data (e.g., when the options data was last updated), always switch to a daily (1D) timeframe. If you still see strange data, please contact us.

Disclaimer:

Our option indicator uses approximately 15min-3 hour delayed option market snapshot data to calculate the main option metrics. Exact realtime option contract prices are never displayed; only derived metrics and interpolated delta are shown to ensure accurate and consistent visualization. Due to the above, this indicator can only be used for decision support; exclusive decisions cannot be made based on this indicator . We reserve the right to make errors.This indicator is designed for options traders who understand what they are doing. It assumes that they are familiar with options and can make well-informed, independent decisions. We work with public data and are not a data provider; therefore, we do not bear any financial or other liability.

Options Overlay [Lite] IVR IV Skew Delta Expmv MurreyMath Expiry𝗡𝗼𝗻-𝗼𝗳𝗳𝗶𝗰𝗶𝗮𝗹 𝗧𝗢𝗦 𝗮𝗻𝗱 𝗧𝗮𝘀𝘁𝘆𝗧𝗿𝗮𝗱𝗲 𝗹𝗶𝗸𝗲 𝗜𝗩𝗥 𝗢𝗽𝘁𝗶𝗼𝗻𝘀 𝘃𝗶𝘀𝘂𝗮𝗹𝗶𝘇𝗮𝘁𝗶𝗼𝗻 𝘁𝗼𝗼𝗹 𝘄𝗶𝘁𝗵 𝗱𝗲𝗹𝗮𝘆𝗲𝗱 𝗼𝗽𝘁𝗶𝗼𝗻 𝗰𝗵𝗮𝗶𝗻 𝗱𝗮𝘁𝗮

Are you an options trader who uses TradingView for technical analysis for the US market?

➡️ Do you want to see the IV Rank of an instrument on TradingView?

➡️ Can’t you check the key options metrics while charting?

➡️ Have you never visualized the options chain before?

➡️ Would you like to see how the IVx has changed for a specific ticker?

If you answered "yes" to any of these questions, then we have the solution for you!

🔃 Auto-Updating Option Metrics without refresh!

🍒 Developed and maintained by option traders for option traders.

📈 Specifically designed for TradingView users who trade options.

Our indicator provides essential key metrics such as:

✅ IVRank

✅ IVx

✅ 5-Day IVx Change

✅ Delta curves and interpolated distances

✅ Expected move curve

✅ Standard deviation (STD1) curve

✅ Vertical Pricing Skew

✅ Horizontal IVx Skew

✅ Delta Skew

like TastyTrade, TOS, IBKR etc, but in a much more visually intuitive way. See detailed descriptions below.

If this isn't enough, we also include a unique grid system designed specifically for options traders. This package features our innovative dynamic grid system:

✅ Enhanced Murrey Math levels (horizontal scale)

✅ Options expirations (vertical scale)

Designed to help you assess market conditions and make well-informed trading decisions, this tool is an essential addition for every serious options trader!

Ticker Information:

This indicator is currently implemented for 5 liquid tickers: NASDAQ:AAPL NASDAQ:AMZN AMEX:DIA NYSE:ORCL and NASDAQ:TSLA

How does the indicator work and why is it unique?

This Pine Script indicator is a complex tool designed to provide various option metrics and visualization tools for options market traders. The indicator extracts raw options data from an external data provider (ORATS), processes and refines the delayed data package using pineseed, and sends it to TradingView, visualizing the data using specific formulas (see detailed below) or interpolated values (e.g., delta distances). This method of incorporating options data into a visualization framework is unique and entirely innovative on TradingView.

The indicator aims to offer a comprehensive view of the current state of options for the implemented instruments, including implied volatility (IV), IV rank (IVR), options skew, and expected market movements, which are objectively measured as detailed below.

The options metrics we display may be familiar to options traders from various major brokerage platforms such as TastyTrade, IBKR, TOS, Tradier, TD Ameritrade, Schwab, etc.

Key Features:

IV Rank (IVR) : The implied volatility rank compares the current IV to the lowest and highest values over the past 52 weeks. The IVR indicator helps determine whether options are relatively cheap or expensive.

IV Average (IVx) : The implied volatility displayed in the options chain, calculated similarly to the VIX. IVx values are aggregated within the 35-70 day expiration cycle.

IV Change (5 days) : The change in implied volatility over the past five trading days. This indicator provides a quick insight into the recent changes in IV.

Expected Move (Exp. Move) : The expected movement for the options expiration cycle, calculated using the price of the ATM (at-the-money) straddle, the first OTM (out-of-the-money) strangle, and the second OTM strangle.

Options Skew : The price difference between put and call options with the same expiration date. Vertical and horizontal skew indicators help understand market sentiment and potential price movements.

Visualization Tools:

Informational IVR Panel : A tabular display mode that presents the selected indicators on the chart. The panel’s placement, size, and content are customizable, including color and tooltip settings.

1 STD, Delta, and Expected Move : Visualization of fundamental classic options metrics corresponding to expirations with bell curves.

Colored Label Tooltips : Detailed tooltips above the bell curves showing options metrics for each expiration.

Adaptive Murrey Math Lines : A horizontal line system based on the principles of Murrey Math Lines, helping identify important price levels and market structures.

Expiration Lines : Displays both monthly and weekly options expirations. The indicator supports various color and style settings, as well as the regulation of the number of expirations displayed.

🟨 𝗗𝗘𝗧𝗔𝗜𝗟𝗘𝗗 𝗗𝗢𝗖𝗨𝗠𝗘𝗡𝗧𝗔𝗧𝗜𝗢𝗡 🟨

🔶 Auto-Updating Option Metrics and Curved Lines

🔹 Interpolated DELTA Curves (16,20,25,30,40)

In our indicator, the curve layer settings allow you to choose the delta value for displaying the delta curve: 16, 20, 25, 30, or even 40. The color of the curve can be customized, and you can also hide the delta curve by selecting the "-" option.

It's important to mention that we display interpolated deltas from the actual option chain of the underlying asset using the Black-Scholes model. This ensures that the 16 delta truly reflects the theoretical, but accurate, 16 delta distance. (For example, deltas shown by brokerages for individual strikes are rounded; a 0.16 delta might actually be 0.1625.)

🔹 Expected Move Curve (Exp.mv)

The expected move is the predicted dollar change in the underlying stock's price by a given option's expiration date, with 68% certainty. It is calculated using the expiration's pricing and implied volatility levels. We chose the TastyTrade method for calculating expected move, as we found it to be the most expressive.

Expected Move Calculation

Expected Move = (ATM straddle price x 0.6) + (1st OTM strangle price x 0.3) + (2nd OTM strangle price x 0.1)

For example , if stock XYZ is trading at 121 and the ATM straddle is 4.40, the 120/122 strangle is 3.46, and the 119/123 strangle is 2.66, the expected move is calculated as follows: 4.40 x 0.60 = 2.64; 3.46 x 0.30 = 1.04; 2.66 x 0.10 = 0.27; Expected move = 2.64 + 1.04 + 0.27 = ±3.9

In this example below, the TastyTrade platform indicates the expected move on the option chain with a brown color, and the exact value is displayed behind the ± symbol for each expiration. By default, we also use brown for this indication, but this can be changed or the curve display can be turned off.

🔹 Standard Deviation Curve (1 STD)

One standard deviation of a stock encompasses approximately 68.2% of outcomes in a distribution of occurrences based on current implied volatility.

We use the expected move formula to calculate the one standard deviation range of a stock. This calculation is based on the days-to-expiration (DTE) of our option contract, the stock price, and the implied volatility of a stock:

Calculation:

Standard Deviation = Closing Price * Implied Volatility * sqrt(Days to Expiration / 365)

According to options literature, there is a 68% probability that the underlying asset will fall within this one standard deviation range at expiration.

If the 1 STD and Exp.mv displays are both enabled, the indicator fills the area between them with a light gray color. This is because both represent probability distributions that appear as a "bell curve" when graphed, making it visually appealing.

Tip and Note:

The 1 STD line might appear jagged at times , which does not indicate a problem with the indicator. This is normal immediately after market open (e.g., during the first data refresh of the day) or if the expirations are illiquid (e.g., weekly expirations). The 1 STD value is calculated based on the aggregated IVx for the expirations, and the aggregated IVx value for weekly expirations updates less frequently due to lower trading volume. In such cases, we recommend enabling the "Only Monthly Expirations" option to smooth out the bell curve.

∑ Quant Observation:

The values of the expected move and the 1st standard deviation (1STD) will not match because they use different calculation methods, even though both are referred to as representing 68% of the underlying asset's movement in options literature. The expected move is based on direct market pricing of ATM options. The 1STD, on the other hand, uses the averaged implied volatility (IVX) for the given expiration to determine its value. Based on our experience, it is better to consider the area between the expected move and the 1STD as the true representation of the original 68% rule.

🔶 IVR Dashboard Panel Rows

🔹 IVR (IV Rank)

The Implied Volatility Rank (IVR) indicator helps options traders assess the current level of implied volatility (IV) in comparison to the past 52 weeks. IVR is a useful metric to determine whether options are relatively cheap or expensive. This can guide traders on whether to buy or sell options. We calculate IVrank, like TastyTrade does.

IVR Calculation:

IV Rank = (current IV - 52 week IV low) / (52 week IV high - 52 week IV low)

IVR Levels and Interpretations:

IVR 0-10 (Green): Very low implied volatility rank. Options might be "cheap," potentially a good time to buy options.

IVR 10-35 (White): Normal implied volatility rank. Options pricing is relatively standard.

IVR 35-50 (Orange): Almost high implied volatility rank.

IVR 50-75 (Red): Definitely high implied volatility rank. Options might be "expensive," potentially a good time to sell options for higher premiums.

IVR above 75 (Highlighted Red): Ultra high implied volatility rank. Indicates very high levels, suggesting a favorable time for selling options.

The panel refreshes automatically if the symbol is implemented. You can hide the panel or change the position and size.

🔹IVx (Implied Volatility Index)

The Implied Volatility Index (IVx) displayed in the option chain is calculated similarly to the VIX. The Cboe uses standard and weekly SPX options to measure the expected volatility of the S&P 500. A similar method is utilized to calculate IVx for each option expiration cycle.

For our purposes on the IVR Panel, we aggregate the IVx values specifically for the 35-70 day monthly expiration cycle . This aggregated value is then presented in the screener and info panel, providing a clear and concise measure of implied volatility over this period.

IVx Color coding:

IVx above 30 is displayed in orange.

IVx above 60 is displayed in red

IVx on curve:

The IVx values for each expiration can be viewed by hovering the mouse over the colored tooltip labels above the Curve.

IVx avg on IVR panel :

If the option is checked in the IVR panel settings, the IVR panel will display the average IVx values up to the optimal expiration.

Important Note:

The IVx value alone does not provide sufficient context. There are stocks that inherently exhibit high IVx values. Therefore, it is crucial to consider IVx in conjunction with the Implied Volatility Rank (IVR), which measures the IVx relative to its own historical values. This combined view helps in accurately assessing the significance of the IVx in relation to the specific stock's typical volatility behavior.

This indicator offers traders a comprehensive view of implied volatility, assisting them in making informed decisions by highlighting both the absolute and relative volatility measures.

🔹IVx 5 days change %

We are displaying the five-day change of the IV Index (IVx value). The IV Index 5-Day Change column provides quick insight into recent expansions or decreases in implied volatility over the last five trading days.

Traders who expect the value of options to decrease might view a decrease in IVX as a positive signal. Strategies such as Strangle and Ratio Spread can benefit from this decrease.

On the other hand, traders anticipating further increases in IVX will focus on the rising IVX values. Strategies like Calendar Spread or Diagonal Spread can take advantage of increasing implied volatility.

This indicator helps traders quickly assess changes in implied volatility, enabling them to make informed decisions based on their trading strategies and market expectations.

🔹 Vertical Pricing Skew

At TanukiTrade, Vertical Pricing Skew refers to the difference in pricing between put and call options with the same expiration date at the same distance (at expected move). We analyze this skew to understand market sentiment. This is the same formula used by TastyTrade for calculations.

We calculate the interpolated strike price based on the expected move , taking into account the neighboring option prices and their distances. This allows us to accurately determine whether the CALL or PUT options are more expensive.

PUT Skew (red): Put options are more expensive than call options, indicating the market expects a downward move (▽). If put options are more expensive by more than 20% at the same expected move distance, we color it lighter red.

CALL Skew (green): Call options are more expensive than put options, indicating the market expects an upward move (△). If call options are priced more than 30% higher at the examined expiration, we color it lighter green.

Vertical Skew on Curve:

The degree of vertical pricing skew for each expiration can be viewed by hovering over the points above the curve. Hover with mouse for more information.

Vertical Skew on IVR panel:

We focus on options with 35-70 days to expiration (DTE) for optimal analysis in case of vertical skew. Hover with mouse for more information.

This approach helps us gauge market expectations accurately, providing insights into potential price movements. Remember, we always evaluate the skew at the expected move using linear interpolation to determine the theoretical pricing of options.

🔹 Delta Skew 🌪️ (Twist)

We have a new metric that examines which monthly expiration indicates a "Delta Skew Twist" where the 16 delta deviates from the monthly STD. This is important because, under normal circumstances, the 16 delta is positioned between the expected move and the standard deviation (STD1) line (see Exp.mv & 1STD exact definitions above). However, if the interpolated 16 delta line exceeds the STD1 line either upwards or downwards, it represents a special case of vertical skew on the option chain.

Normal case : exp.move < delta16 < std1

Delta Skew Twist: exp.move < std1 < delta16

We indicate this with direction-specific colors (red/green) on the delta line. We also color the section of the delta curve affected by the delta skew in this case, even if you choose to display a lower delta, such as 30, instead of 16.

If "Colored Labels with Tooltips" is enabled, we also display a 🌪️ symbol in the tooltip for the expirations affected by Delta Skew.

If you have enabled the display of 'Vertical Pricing Skew' on the IVR Panel, a 🌪️ symbol will also appear next to the value of the vertical skew, and the tooltip will indicate from which expiration Delta Skew is observed.

🔹 Horizontal IVx Skew

In options pricing, it is typically expected that the implied volatility (IVx) increases for options with later expiration dates. This means that options further out in time are generally more expensive. At TanukiTrade, we refer to the phenomenon where this expectation is reversed—when the IVx decreases between two consecutive expirations—as Horizontal Skew or IVx Skew.

Horizontal IVx Skew occurs when: Front Expiry IVx < Back Expiry IVx

This scenario can create opportunities for traders who prefer diagonal or calendar strategies . Based on our experience, we categorize Horizontal Skew into two types:

Weekly Horizontal Skew:

When IVx skew is observed between two consecutive non-monthly expirations, the displayed value is the rounded-up percentage difference. On hover, the approximate location of this skew is also displayed. The precise location can be seen on this indicator.

Monthly Horizontal Skew:

When IVx skew is observed between two consecutive monthly expirations , the displayed value is the rounded-up percentage difference. On hover, the approximate location of this skew is also displayed. The precise location can be seen on our Overlay indicator.

The Monthly Vertical IVx skew is consistently more liquid than the weekly vertical IVx skew. Weekly Horizontal IVx Skew may not carry relevant information for symbols not included in the 'Weeklies & Volume Masters' preset in our Options Screener indicator.

If the options chain follows the normal IVx pattern, no skew value is displayed.

Color codes or tooltip labels above curve:

Gray - No horizontal skew;

Purple - Weekly horizontal skew;

BigBlue - Monthly horizontal skew

The display of monthly and weekly IVx skew can be toggled on or off on the IVR panel. However, if you want to disable the colored tooltips above the curve, this can only be done using the "Colored labels with tooltips" switch.

We indicate this range with colorful information bubbles above the upper STD line.

🔶 The Option Trader’s GRID System: Adaptive MurreyMath + Expiry Lines

At TanukiTrade, we utilize Enhanced MurreyMath and Expiry lines to create a dynamic grid system, unlike the basic built-in vertical grids in TradingView, which provide no insight into specific price levels or option expirations.

These grids are beneficial because they provide a structured layout, making important price levels visible on the chart. The grid automatically resizes as the underlying asset's volatility changes, helping traders identify expected movements for various option expirations.

The Option Trader’s GRID System part of this indicator can be used without limitations for all instruments . There are no type or other restrictions, and it automatically scales to fit every asset. Even if we haven't implemented the option metrics for a particular underlying asset, the GRID system will still function!

🔹 SETUP OF YOUR OPTIONS GRID SYSTEM

You can setup your new grid system in 3 easy steps!

STEP1: Hide default horizontal grid lines in TradingView

Right-click on an empty area of your chart, then select “Settings.” In the Chart settings -> Canvas -> Grid lines section, disable the display of horizontal lines to avoid distraction.

SETUP STEP2: Scaling fix

Right-click on the price scale on the right side, then select "Scale price chart only" to prevent the chart from scaling to the new horizontal lines!

STEP3: Enable Tanuki Options Grid

As a final step, make sure that both the vertical (MurreyMath) and horizontal (Expiry) lines are enabled in the Grid section of our indicator.

You are done, enjoy the new grid system!

🔹 HORIZONTAL: Enhanced MurreyMath Lines

Murrey Math lines are based on the principles observed by William Gann, renowned for his market symmetry forecasts. Gann's techniques, such as Gann Angles, have been adapted by Murrey to make them more accessible to ordinary investors. According to Murrey, markets often correct at specific price levels, and breakouts or returns to these levels can signal good entry points for trades.

At TanukiTrade, we enhance these price levels based on our experience , ensuring a clear display. We acknowledge that while MurreyMath lines aren't infallible predictions, they are useful for identifying likely price movements over a given period (e.g., one month) if the market trend aligns.

Our opinion: MurreyMath lines are not crystal balls (like no other tool). They should be used to identify that if we are trading in the right direction, the price is likely to reach the next unit step within a unit time (e.g. monthly expiration).

One unit step is the distance between Murrey Math lines, such as between the 0/8 and 1/8 lines. This interval helps identify different quadrants and is crucial for recognizing support and resistance levels.

Some option traders use Murrey Math lines to gauge the movement speed of an instrument over a unit time. A quadrant encompasses 4 unit steps.

Key levels, according to TanukiTrade, include:

Of course, the lines can be toggled on or off, and their default color can also be changed.

🔹 VERTICAL: Expiry Lines

The indicator can display monthly and weekly expirations as dashed lines, with customizable colors. Weekly expirations will always appear in a lighter shade compared to monthly expirations.

Monthly Expiry Lines:

You can turn off the lines indicating monthly expirations, or set the direction (past/future/both) and the number of lines to be drawn.

Weekly Expiry Lines:

You can display weekly expirations pointing to the future. You can also turn them off or specify how many weeks ahead the lines should be drawn.

Of course, the lines can be toggled on or off, and their default color can also be changed.

TIP: Hide default vertical grid lines in TradingView

Right-click on an empty area of your chart, then select “Settings.” In the Chart settings -> Canvas -> Grid lines section, disable the display of vertical lines to avoid distraction. Same, like steps above at MurreyMath lines.

🔶 ADDITIONAL IMPORTANT COMMENTS

- U.S. market only:

Since we only deal with liquid option chains: this option indicator only works for the USA options market and do not include future contracts; we have implemented each selected symbol individually.

- Why is there a slight difference between the displayed data and my live brokerage data? There are two reasons for this, and one is beyond our control.

- Brokerage Calculation Differences:

Every brokerage has slight differences in how they calculate metrics like IV and IVx. If you open three windows for TOS, TastyTrade, and IBKR side by side, you will notice that the values are minimally different. We had to choose a standard, so we use the formulas and mathematical models described by TastyTrade when analyzing the options chain and drawing conclusions.

- Option-data update frequency:

According to TradingView's regulations and guidelines, we can update external data a maximum of 5 times per day. We strive to use these updates in the most optimal way:

(1st update) 15 minutes after U.S. market open

(2nd, 3rd, 4th updates) 1.5–3 hours during U.S. market open hours

(5th update) 10 minutes before market close.

You don’t need to refresh your window, our last refreshed data-pack is always automatically applied to your indicator , and you can see the time elapsed since the last update at the bottom of your indicator.

- Skewed Curves:

The delta, expected move, and standard deviation curves also appear relevantly on a daily or intraday timeframe. Data loss is experienced above a daily timeframe: this is a TradingView limitation.

- Weekly illiquid expiries:

Especially for instruments where weekly options are illiquid: the weekly expiration STD1 data is not relevant. In these cases, we recommend checking in the "Display only Monthly labels" checkbox to avoid displaying not relevant weekly options expirations.

-Timeframe Issues:

Our option indicator visualizes relevant data on a daily resolution. If you see strange or incorrect data (e.g., when the options data was last updated), always switch to a daily (1D) timeframe. If you still see strange data, please contact us.

Disclaimer:

Our option indicator uses approximately 15min-3 hour delayed option market snapshot data to calculate the main option metrics. Exact realtime option contract prices are never displayed; only derived metrics and interpolated delta are shown to ensure accurate and consistent visualization. Due to the above, this indicator can only be used for decision support; exclusive decisions cannot be made based on this indicator . We reserve the right to make errors.This indicator is designed for options traders who understand what they are doing. It assumes that they are familiar with options and can make well-informed, independent decisions. We work with public data and are not a data provider; therefore, we do not bear any financial or other liability.

Expected Move BandsExpected Moves

The Expected Move of a security shows the amount that a stock is expected to rise or fall from its current market price based on its level of volatility or implied volatility. The expected move of a stock is usually measured with standard deviations.

An Expected Move Range of 1 SD shows that price will be near the 1 SD range 68% of the time given enough samples.

Expected Move Bands

This indicator gets the Expected Move for 1-4 Standard Deviation Ranges using Historical Volatility. Then it displays it on price as bands.

The Expected Move indicator also allows you to see MTF Expected Moves if you want to.

This indicator calculates the expected price movements by analyzing the historical volatility of an asset. Volatility is the measure of fluctuation.

This script uses log returns for the historical volatility calculation which can be modelled as a normal distribution most of the time meaning it is symmetrical and stationary unlike other scripts that use bands to find "reversals". They are fundamentally incorrect.

What these ranges tell you is basically the odds of the price movement being between these levels.

If you take enough samples, 95.5% of the them will be near the 2nd Standard Deviation. And so on. (The 3rd Standard deviation is 99.7%)

For higher timeframes you might need a smaller sample size.

Features

MTF Option

Parameter customization

[BCT] Option Pricing via Markov Chain Monte Carlo SimulationOverview:

This script offers a toolkit for quantitative options trading, using Monte Carlo simulations based on actual historical returns to model potential future price paths for underlying assets. A range of metrics related to options trading are also provided.

Monte Carlo Simulations:

The script employs Monte Carlo simulations to model future price paths based on the historical returns of the underlying asset. These simulated paths are represented as parabolas at the 2-sigma, 25th percentile, and median levels for quick reference.

Methodologies:

For calculating options prices at At-the-Money (or any user-selected strike), two methodologies are used:

Simple Averaging: Takes the mean of the simulated asset price paths.

Kernel Density Estimation (KDE): Applied to the simulated asset price paths to produce a smoothed estimate of its probability density function, thereby aiding in a more nuanced option price calculation.

Bootstrap Resampling:

Bootstrap resampling is specifically applied to the simulated asset price paths to generate an estimate of the standard deviation of the options prices. Note that while bootstrap methods are employed, they serve as statistical tools and do not guarantee statistical reliability.

Metrics Displayed:

Model-Estimated At-the-Money (or selected strike) Straddle Price

Model-Estimated At-the-Money (or selected strike) Call Price

Model-Estimated At-the-Money (or selected strike) Put Price

Model-Estimated Standard deviation for Option Prices from simulated price paths

Underlying Monte Carlo Simulation Results (represented as parabolas at the 2 sigma, 25 percentile and median)

This is not financial advice. Use at your own risk.

Disclaimer: Options trading carries a high level of risk and may not be suitable for all investors. This script is intended to serve as an educational tool and should not be considered financial advice. While designed to aid in decision-making, the script's indicators are not guarantees of performance or outcomes. Always conduct your own due diligence before making trading decisions.

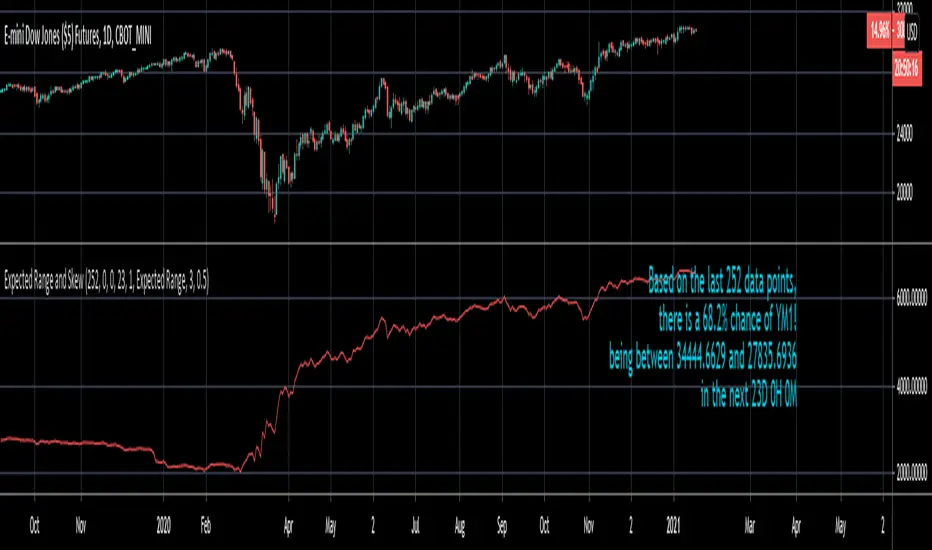

True Range/Expected MoveThis indicator plots the ratio of True Range/Expected Move of SPX. True Range is simple the high-low range of any period. Expected move is the amount that SPX is predicted to increase or decrease from its current price based on the current level of implied volatility. There are several choices of volatility indexes to choose from. The shift in color from red to green is set by default to 1 but can be adjusted in the settings.

Red bars indicate the true range was below the expected move and green bars indicate it was above. Because markets tend to overprice volatility it is expected that there would be more red bars than green. If you sell SPX or SPY option premium red days tend to be successful while green days tend to get stopped out. On a 1D chart it is interesting to look at the clusters of bar colors.

Supply and Demand Deluxe (Stock Justice)Introducing " Supply and Demand Deluxe (Stock Justice) " - the ultimate TradingView indicator that revolutionizes how traders identify crucial supply and demand levels. With its unrivaled capabilities across multiple timeframes, this indicator offers a comprehensive toolkit for traders seeking an edge in the market.

To fully harness the power of "Supply and Demand Deluxe," traders can fine-tune the indicator's input parameters to suit their preferences and trading strategies. Let's delve into the key components and functionalities that make this indicator truly exceptional:

Daily and Weekly Pivots :

The indicator empowers you to plot vital reference points, including the previous week's high and low, yesterday's high and low, and the midpoint of yesterday's range. These plots provide invaluable insights into market sentiment and potential turning points.

Weekly Supply and Demand Levels :

Regardless of what timeframe you are looking at, this indicator allows you to unlock the ability to plot weekly supply and demand levels directly on your chart. Enjoy the freedom to customize the number of levels to plot, choose line colors and styles, and decide whether to extend the lines. For a more comprehensive analysis, enable the "Show Price" option to view the associated prices.

Daily Supply and Demand Levels :

Similar to the weekly levels, this feature allows you to plot daily supply and demand levels with ease. Tailor the number of levels, line colors, and styles to your preferences. The "Extend Left" and "Extend Right" options provide flexibility in determining whether the lines extend to the left, right, or both. Enable the "Show Price" option to display the corresponding prices, enhancing your decision-making process.

Hourly Supply and Demand Levels :

Effortlessly plot hourly supply and demand levels on your chart. The indicator automatically identifies these levels based on the highest and lowest values of previous ranges. Customize the number of levels, line colors, and styles to match your visual preferences. As with the previous features, you can display prices associated with these levels, amplifying your trading insights.

ATR Expected Moves :

Gain a deeper understanding of potential price moves with the ATR Expected Moves feature. Based on the Average True Range (ATR), this functionality allows you to plot expected price ranges. Adjust the lookback length and multipliers to fine-tune the calculation according to your trading style. With the flexibility to extend lines, choose colors and line styles, and display prices, you can adapt the indicator to your specific needs.

Futures Levels :

For futures traders, "Supply and Demand Deluxe" provides specific levels for the Midnight Open, London Open, Asian Open, and the 8:30am EST level. These pre-defined levels act as valuable reference points, enabling you to navigate futures markets with confidence.

By incorporating these cutting-edge features, the Supply and Demand Deluxe indicator by Stock Justice empowers traders to identify key supply and demand levels across various timeframes. Its customizable visual elements and adaptable parameters allow traders to align the indicator with their unique trading strategies, amplifying their potential for success.

////////////////////////

UNIQUENESS

////////////////////////

This one-of-a-kind indicator stands out from existing tools in the market due to its unparalleled combination of features and customization options. While other indicators may focus on specific aspects of supply and demand analysis, "Supply and Demand Deluxe (Stock Justice)" brings together a comprehensive suite of tools that cater to traders across various timeframes. From daily and weekly pivots to hourly supply and demand levels, this indicator covers a wide range of trading scenarios, allowing users to gain a holistic view of market dynamics.

What truly sets "Supply and Demand Deluxe" apart is the fact that it is its emphasis on customization. Traders have the freedom to fine-tune every aspect of the indicator, from the number of plotted levels to the colors, line styles, and extension options. By providing such extensive customization capabilities, this indicator enables traders to align it precisely with their unique trading strategies and preferences. Whether you're an aggressive short-term trader or a patient long-term investor, "Supply and Demand Deluxe" adapts to your individual style, empowering you to make well-informed trading decisions.

Furthermore, the incorporation of the ATR Expected Moves feature adds an extra layer of sophistication to this indicator. By leveraging the Average True Range, traders can gain insights into expected price ranges, enhancing their risk management and trade planning. The ability to adjust the lookback length and multipliers ensures that traders can adapt the ATR calculations to suit their desired level of precision. This feature, combined with the indicator's visual plots and customizable elements, sets "Supply and Demand Deluxe (Stock Justice)" in a league of its own, providing traders with an edge in understanding and navigating the market.

In summary, the uniqueness of "Supply and Demand Deluxe (Stock Justice)" lies in its comprehensive approach to supply and demand analysis, its extensive customization options, and the incorporation of the ATR Expected Moves feature. With its ability to cater to traders across various timeframes and adapt to individual trading styles, this indicator empowers users to unlock the full potential of supply and demand analysis and make informed trading decisions with confidence.

////////////////////////

Embrace the future of trading with "Supply and Demand Deluxe (Stock Justice)" and unleash the full potential of supply and demand analysis in your trading endeavors. Elevate your trading journey with this game-changing indicator.

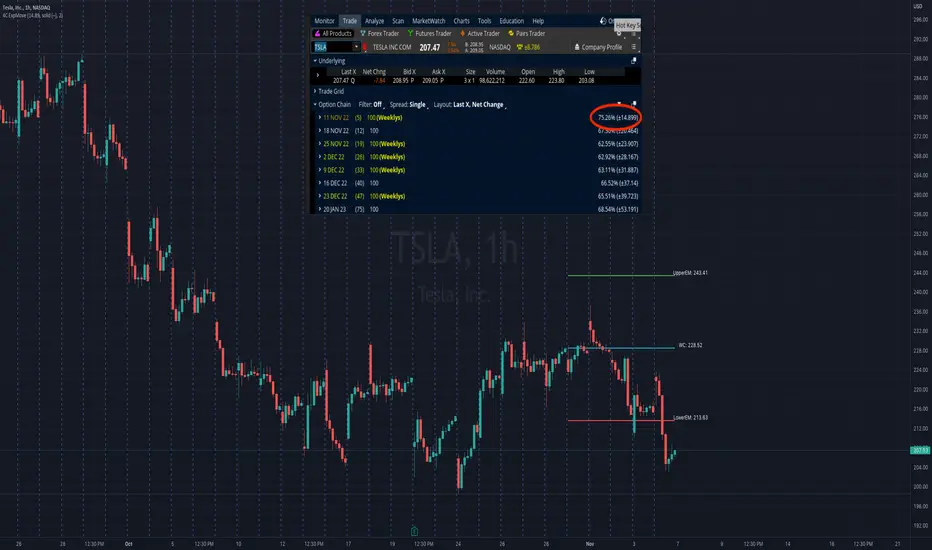

4C Options Expected Move (Weekly + 0DTE)This indicator plots the calculated Expected Move for BOTH Weekly and Zero Dated Expiration (0DTE) Daily options, for a quick visual reference.

Please Note: This indicator is different from our original "4C Expected Move (Weekly Options)" indicator, as it now packages the ability to ALSO plot 0DTE options expected moves along with Weekly expected moves. Many other newer features have also been implemented.

Background Information

The Expected Move (EM) is the amount that a stock is predicted to increase or decrease from its current price, based on the current level of options pricing and implied volatility.

This range can be viewed as possible support and resistance, or, once price gets outside of the range, institutional hedging actions can accelerate the move in that direction.

It can be useful to know what the weekly EM range is for a stock to understand the probabilities of the overall distance, direction and volatility for the week.

About the Indicator

This indicator plots the calculated Expected Move for BOTH Weekly and Zero Dated Expiration (0DTE) options, for a quick visual reference.

For the weekly EM, the range is based on the Weekly close of the prior week.

For the Daily EM based on 0DTE options, the range is based on the Daily close of the prior day.

The indicator will automatically start a new weekly EM plot at the beginning of the week, and a new daily EM at the beginning of each day.

The EM values must be updated weekly and/or daily.

Features

Plots the EM for the week

Plots the EM for the day, for symbols that offer daily expiration options

Plots the 2 Standard Deviation EM for both the weekly and daily EM

Labels with calculated values are plotted near the levels for quick visual aid

Settings

Can toggle weekly EM on/off

Can toggle Daily EM on/off

Can toggle 2 Standard Deviation lines on/off

Can toggle labels for all EM on/off

Robust line settings

Can adjust label location left/right based on personal preference

Can enter symbol into settings as a reference

Handy instructions in the settings

How To Set Up The Indicator

To use this indicator you must have access to a broker with options data (not available on Tradingview).

Usually, you can look at the stock's option chain to find the weekly expected move.

You will have to do your own research to find where this information is displayed depending on your broker. You may also need to find the information elsewhere if your broker does not have this information.

You can also do your calculation of the EM using the following formula (please do your own research):

Expected Move = Option Price x Implied Volatility x Square Root of Time

See screenshot example below

This is the Thinkorswim platform's option chain, and the Implied Volatility % and the calculated EM are on the right side of the option chain.

The Expected Move is circled in blue. Use the +- number in parentheses, NOT the % value.

For the weekly EM, input the number that corresponds to the weekly option into the indicator. This must be done on a weekly basis, and It is typically best to use the EM for the next week expiration that is generated AFTER the Friday close and/or before the Monday open of the upcoming week.

For the daily EM, input the number that corresponds to the daily 0DTE option into the indicator. This must be done on a daily basis, and it is typically best to use the EM value for the 0DTE option that is generated the night before (after market close), or before the market opens for that 0DTE. .

SPX Implied Probability of closing above/belowThis is a recreation of the work done by Michael Rechenthin aka "Dr.Data" from Tastytrade back in 2016 (this indicator is for SP:SPX only)

You can watch the episode where "Dr.Data", Tom and Tony go over this concept on the following link:

www.tastytrade.com

The following are my personal additions:

- ability to choose between TVC:VIX and NASDAQ:VOLI as the IV input

- ability to choose between 252 and 365 for the number of days

Note that I’m displaying 4 decimal places (#.####) to be as accurate as possible but sometimes you will see 0% or 100% displayed which means that more decimal places are needed (0% could be 0.00005% or 100% could be 99.99995%).

4C Expected Move (Weekly Options)This indicator plots the Expected Move (EM) calculated from weekly options pricing, for a quick visual reference.

The EM is the amount that a stock is predicted to increase or decrease from its current price, based on the current level of implied volatility.

This range can be viewed as support and resistance, or once price gets outside of the range, institutional hedging actions can accelerate the move in that direction.

The EM range is based on the Weekly close of the prior week.

It can be useful to know what the weekly EM range is for a stock to understand the probabilities of the overall distance, direction and volatility for the week.

To use this indicator you must have access to a broker with options data (not available on Tradingview).

Look at the stock's option chain and find the weekly expected move. You will have to do your own research to find where this information is displayed depending on your broker.