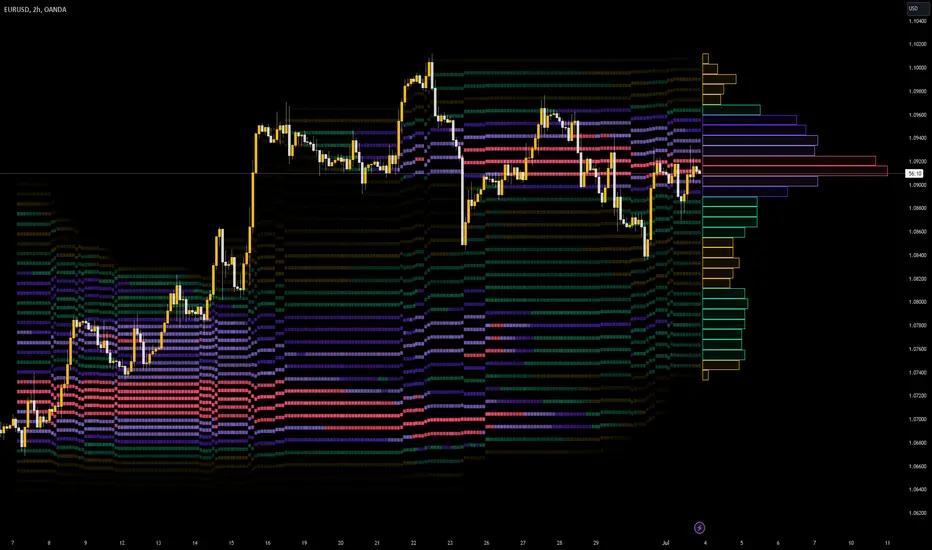

Market Generated InformationCredits

Original Author: mcthatsme

Remixed to add in London's High and Low

Overview

The Market Generated Information (MGI Levels v2) is a comprehensive technical analysis. It overlays key price levels from daily, weekly, and monthly timeframes on a chart, providing traders with critical market reference points such as Open, High, Low, Close, Volume Weighted Average Price (VWAP), and standard deviation bands. These levels help traders identify potential support, resistance, and pivot points for intraday and longer-term trading strategies. The indicator is highly customizable, allowing users to tailor the displayed levels, colors, line styles, and label settings to their preferences.

Features

Multi-Timeframe Levels: Displays key price levels from daily, weekly, and monthly sessions, including Open, High, Low, Close, VWAP, and VWAP standard deviation bands (SD1, SD2, SD3).

Session-Based Calculations: Supports Regular Trading Hours (RTH) and Extended Trading Hours (ETH) for stocks and futures, with specific session times for New York, London, and overnight sessions.

Customizable Display: Users can toggle the visibility of specific levels, adjust line styles (solid, dashed, dotted), colors, thicknesses, and label settings (size, offset, and price inclusion).

Opening Range and Initial Balance: Plots the Opening Range (default: 9:30–10:00 AM EST) and Initial Balance (default: 9:30–10:30 AM EST) for intraday traders.

Tested Level Tracking: Optionally tracks untested or tested levels, hiding or showing them based on user preferences.

Overnight and T+2 Levels: Includes overnight high/low and T+2 (two days prior) levels for additional context.

VWAP Calculations: Computes VWAP and its standard deviation bands for daily, weekly, and monthly periods.

Holiday and Session Filters: Adjusts for market-specific conditions, such as Good Friday or shortened trading sessions.

Inputs and Customization

The indicator is organized into three main groups: Daily Levels, Weekly Levels, and Monthly Levels. Each group allows users to configure the following:

Visibility: Toggle whether to show levels (e.g., Show Daily Levels, Show Weekly Levels).

Session Times: Define session ranges (e.g., New York RTH: 9:30 AM–4:00 PM EST, Opening Range: 9:30–10:00 AM EST).

Line and Label Settings: Customize line colors, styles (solid, dashed, dotted), thickness, label text size (Tiny, Small, Normal, Large, Huge), label offset, and whether to include price values in labels.

Number of Periods: Specify how many previous days (1–40), weeks (1–20), or months (1–12) to display.

Tested/Untested Levels: Choose to keep untested levels or show tested levels (Open, High, Low, Close).

Timeframe for Calculations: Option to use a 30-second or 1-minute timeframe for Opening Range and Initial Balance calculations to accommodate different TradingView plans.

Key Levels

Daily Levels: Includes Current Day High/Low, Previous Day High/Low, Opening Range High/Mid/Low, Initial Balance High/Mid/Low, Globex Open, RTH Open, Midnight Open, London Open/Close/High/Low, Previous Day 50% (HL2/OC2), T+2 Open/Close/High/Low, Overnight High/Low, RTH Close, 5 PM Close, and VWAP with standard deviation bands.

Weekly Levels: Previous Week High/Low, 50% (HL2/OC2), Current Week Open, Previous Week Close, and VWAP with standard deviation bands.

Monthly Levels: Previous Month High/Low, 50% (HL2/OC2), Current Month Open, Previous Month Close, and VWAP with standard deviation bands.

Troubleshooting

Levels Not Displaying: Check if the timeframe is ≤ 30 minutes for daily levels and ensure session times are correct for your market.

Incorrect Prices: Verify that extended hours are enabled for ETH charts or disabled for RTH-only charts.

Too Many Lines/Labels: Reduce the number of previous days/weeks/months or disable unneeded levels.

Session Errors: Ensure session times are in UTC-5 (New York time) and match your asset’s trading hours.

License

This script is licensed under the Mozilla Public License 2.0. See mozilla.org for details.

Marketprofile

Market Sessions Indicator by NomadTradesCustomisable Market session indicator

This indicator visually marks the high and low price levels for the Asia, London, and New York trading sessions directly on the chart, using distinct horizontal lines and color-coding for each session. Each session’s high and low are labelled for easy identification, allowing traders to quickly assess key support and resistance levels established during major global market hours. The indicator is designed for clear session demarcation, helping users identify price reactions at these significant levels and supporting multi-session analysis for intraday and swing trading strategies

PhenLabs - Market Fluid Dynamics📊 Market Fluid Dynamics -

Version: PineScript™ v6

📌 Description

The Market Fluid Dynamics - Phen indicator is a new thinking regarding market analysis by modeling price action, volume, and volatility using a fluid system. It attempts to offer traders control over more profound market forces, such as momentum (speed), resistance (thickness), and buying/selling pressure. By visualizing such dynamics, the script allows the traders to decide on the prevailing market flow, its power, likely continuations, and zones of calmness and chaos, and thereby allows improved decision-making.

This measure avoids the usual difficulty of reconciling multiple, often contradictory, market indications by including them within a single overarching model. It moves beyond traditional binary indicators by providing a multi-dimensional view of market behavior, employing fluid dynamic analogs to describe complex interactions in an accessible manner.

🚀 Points of Innovation

Integrated Fluid Dynamics Model: Combines velocity, viscosity, pressure, and turbulence into a single indicator.

Normalized Metrics: Uses ATR and other normalization techniques for consistent readings across different assets and timeframes.

Dynamic Flow Visualization: Main flow line changes color and intensity based on direction and strength.

Turbulence Background: Visually represents market stability with a gradient background, from calm to turbulent.

Comprehensive Dashboard: Provides an at-a-glance summary of key fluid dynamic metrics.

Multi-Layer Smoothing: Employs several layers of EMA smoothing for a clearer, more responsive main flow line.

🔧 Core Components

Velocity Component: Measures price momentum (first derivative of price), normalized by ATR. It indicates the speed and direction of price changes.

Viscosity Component: Represents market resistance to price changes, derived from ATR relative to its historical average. Higher viscosity suggests it’s harder for prices to move.

Pressure Component: Quantifies the force created by volume and price range (close - open), normalized by ATR. It reflects buying or selling pressure.

Turbulence Detection: Calculates a Reynolds number equivalent to identify market stability, ranging from laminar (stable) to turbulent (chaotic).

Main Flow Indicator: Combines the above components, applying sensitivity and smoothing, to generate a primary signal of market direction and strength.

🔥 Key Features

Advanced Smoothing Algorithm: Utilizes multiple EMA layers on the raw flow calculation for a fluid and responsive main flow line, reducing noise while maintaining sensitivity.

Gradient Flow Coloring: The main flow line dynamically changes color from light to deep blue for bullish flow and light to deep red for bearish flow, with intensity reflecting flow strength. This provides an immediate visual cue of market sentiment and momentum.

Turbulence Level Background: The chart background changes color based on calculated turbulence (from calm gray to vibrant orange), offering an intuitive understanding of market stability and potential for erratic price action.

Informative Dashboard: A customizable on-screen table displays critical metrics like Flow State, Flow Strength, Market Viscosity, Turbulence, Pressure Force, Flow Acceleration, and Flow Continuity, allowing traders to quickly assess current market conditions.

Configurable Lookback and Sensitivity: Users can adjust the base lookback period for calculations and the sensitivity of the flow to viscosity, tailoring the indicator to different trading styles and market conditions.

Alert Conditions: Pre-defined alerts for flow direction changes (positive/negative crossover of zero line) and detection of high turbulence states.

🎨 Visualization

Main Flow Line: A smoothed line plotted below the main chart, colored blue for bullish flow and red for bearish flow. The intensity of the color (light to dark) indicates the strength of the flow. This line crossing the zero line can signal a change in market direction.

Zero Line: A dotted horizontal line at the zero level, serving as a baseline to gauge whether the market flow is positive (bullish) or negative (bearish).

Turbulence Background: The indicator pane’s background color changes based on the calculated turbulence level. A calm, almost transparent gray indicates low turbulence (laminar flow), while a more vibrant, semi-transparent orange signifies high turbulence. This helps traders visually assess market stability.

Dashboard Table: An optional table displayed on the chart, showing key metrics like ‘Flow State’, ‘Flow Strength’, ‘Market Viscosity’, ‘Turbulence’, ‘Pressure Force’, ‘Flow Acceleration’, and ‘Flow Continuity’ with their current values and qualitative descriptions (e.g., ‘Bullish Flow’, ‘Laminar (Stable)’).

📖 Usage Guidelines

Setting Categories

Show Dashboard - Default: true; Range: true/false; Description: Toggles the visibility of the Market Fluid Dynamics dashboard on the chart. Enable to see key metrics at a glance.

Base Lookback Period - Default: 14; Range: 5 - (no upper limit, practical limits apply); Description: Sets the primary lookback period for core calculations like velocity, ATR, and volume SMA. Shorter periods make the indicator more sensitive to recent price action, while longer periods provide a smoother, slower signal.

Flow Sensitivity - Default: 0.5; Range: 0.1 - 1.0 (step 0.1); Description: Adjusts how much the market viscosity dampens the raw flow. A lower value means viscosity has less impact (flow is more sensitive to raw velocity/pressure), while a higher value means viscosity has a greater dampening effect.

Flow Smoothing - Default: 5; Range: 1 - 20; Description: Controls the length of the EMA smoothing applied to the main flow line. Higher values result in a smoother flow line but with more lag; lower values make it more responsive but potentially noisier.

Dashboard Position - Default: ‘Top Right’; Range: ‘Top Right’, ‘Top Left’, ‘Bottom Right’, ‘Bottom Left’, ‘Middle Right’, ‘Middle Left’; Description: Determines the placement of the dashboard on the chart.

Header Size - Default: ‘Normal’; Range: ‘Tiny’, ‘Small’, ‘Normal’, ‘Large’, ‘Huge’; Description: Sets the text size for the dashboard header.

Values Size - Default: ‘Small’; Range: ‘Tiny’, ‘Small’, ‘Normal’, ‘Large’; Description: Sets the text size for the metric values in the dashboard.

✅ Best Use Cases

Trend Identification: Identifying the dominant market flow (bullish or bearish) and its strength to trade in the direction of the prevailing trend.

Momentum Confirmation: Using the flow strength and acceleration to confirm the conviction behind price movements.

Volatility Assessment: Utilizing the turbulence metric to gauge market stability, helping to adjust position sizing or avoid choppy conditions.

Reversal Spotting: Watching for divergences between price and flow, or crossovers of the main flow line above/below the zero line, as potential reversal signals, especially when combined with changes in pressure or viscosity.

Swing Trading: Leveraging the smoothed flow line to capture medium-term market swings, entering when flow aligns with the desired trade direction and exiting when flow weakens or reverses.

Intraday Scalping: Using shorter lookback periods and higher sensitivity to identify quick shifts in flow and turbulence for short-term trading opportunities, particularly in liquid markets.

⚠️ Limitations

Lagging Nature: Like many indicators based on moving averages and lookback periods, the main flow line can lag behind rapid price changes, potentially leading to delayed signals.

Whipsaws in Ranging Markets: During periods of low volatility or sideways price action (high viscosity, low flow strength), the indicator might produce frequent buy/sell signals (whipsaws) as the flow oscillates around the zero line.

Not a Standalone System: While comprehensive, it should be used in conjunction with other forms of analysis (e.g., price action, support/resistance levels, other indicators) and not as a sole basis for trading decisions.

Subjectivity in Interpretation: While the dashboard provides quantitative values, the interpretation of “strong” flow, “high” turbulence, or “significant” acceleration can still have a subjective element depending on the trader’s strategy and risk tolerance.

💡 What Makes This Unique

Fluid Dynamics Analogy: Its core strength lies in translating complex market interactions into an intuitive fluid dynamics framework, making concepts like momentum, resistance, and pressure easier to visualize and understand.

Market View: Instead of focusing on a single aspect (like just momentum or just volatility), it integrates multiple factors (velocity, viscosity, pressure, turbulence) to provide a more comprehensive picture of market conditions.

Adaptive Visualization: The dynamic coloring of the flow line and the turbulence background provide immediate, adaptive visual feedback that changes with market conditions.

🔬 How It Works

Price Velocity Calculation: The indicator first calculates price velocity by measuring the rate of change of the closing price over a given ‘lookback’ period. The raw velocity is then normalized by the Average True Range (ATR) of the same lookback period. Normalization enables comparison of momentum between assets or timeframes by scaling for volatility. This is the direction and speed of initial price movement.

Viscosity Calculation: Market ‘viscosity’ or resistance to price movement is determined by looking at the current ATR relative to its longer-term average (SMA of ATR over lookback * 2). The further the current ATR is above its average, the lower the viscosity (less resistance to price movement), and vice-versa. The script inverts this relationship and bounds it so that rising viscosity means more resistance.

Pressure Force Measurement: A ‘pressure’ variable is calculated as a function of the ratio of current volume to its simple moving average, multiplied by the price range (close - open) and normalized by ATR. This is designed to measure the force behind price movement created by volume and intraday price thrusts. This pressure is smoothed by an EMA.

Turbulence State Evaluation: A equivalent ‘Reynolds number’ is calculated by dividing the absolute normalized velocity by the viscosity. This is the proclivity of the market to move in a chaotic or orderly fashion. This ‘reynoldsValue’ is smoothed with an EMA to get the ‘turbulenceState’, which indicates if the market is laminar (stable), transitional, or turbulent.

Main Flow Derivation: The ‘rawFlow’ is calculated by taking the normalized velocity, dampening its impact based on the ‘viscosity’ and user-input ‘sensitivity’, and orienting it by the sign of the smoothed ‘pressureSmooth’. The ‘rawFlow’ is then put through multiple layers of exponential moving average (EMA) smoothing (with ‘smoothingLength’ and derived values) to reach the final ‘mainFlow’ line. The extensive smoothing is designed to give a smooth and clear visualization of the overall market direction and magnitude.

Dashboard Metrics Compilation: Additional metrics like flow acceleration (derivative of mainFlow), and flow continuity (correlation between close and volume) are calculated. All primary components (Flow State, Strength, Viscosity, Turbulence, Pressure, Acceleration, Continuity) are then presented in a user-configurable dashboard for ease of monitoring.

💡 Note:

The “Market Fluid Dynamics - Phen” indicator is designed to offer a unique perspective on market behavior by applying principles from fluid dynamics. It’s most effective when used to understand the underlying forces driving price rather than as a direct buy/sell signal generator in isolation. Experiment with the settings, particularly the ‘Base Lookback Period’, ‘Flow Sensitivity’, and ‘Flow Smoothing’, to find what best suits your trading style and the specific asset you are analyzing. Always combine its insights with robust risk management practices.

Volume Profile PlusThis indicator provides a high-resolution and high-precision implementation of Volume Profile with flexible range settings. Its key features include:

1. Support for a high resolution of up to 2,500 rows.

2. Capability to examine lower timeframe bars (default 5,000 intra-bars) for enhanced precision.

3. Three range modes — "Visible Range", "Anchored Range", and "All Range".

4. Highlighting of Point of Control and Value Area.

5. Extensive customization options allowing users to configure dimensions, on-chart placements, and color schemes.

🔵 Settings

The settings screen, along with the explanations for each setting, is provided below:

🔵 High Resolution using Polyline

Inspired by @fikira, this indicator utilizes the newly introduced `polyline` type in PineScript to plot the volume profile. It employs a single polyline instance to represent the entire histogram. With each polyline instance supporting up to 10,000 points and each histogram row requiring 4 points, this indicator can accommodate 2500 rows, resulting in a significantly higher resolution compared to conventional volume profile indicators that use `line`s or `box`es to draw the histogram.

🔵 High Precision Data-binning using Lower Timeframe Data

Conventional volume profile indicators often face one or both of the following limitations:

1. They only consider volume within the chart's current timeframe.

2. They assign each bar's total volume to a single price bucket based on the bar's average price, rather than distributing volume across multiple price buckets.

As a result, when the number of bars in the chart is low, those indicators may provide imprecise results, making it difficult to accurately identify significant volume nodes and the point of control.

To address these limitations and enhance accuracy, this indicator examines data from lower timeframes and distributes the volume to fine-grained price buckets. It intelligently selects an appropriate lower timeframe to ensure precise output while complying with a maximum specified number of bars to maintain good performance.

🔵 Three Range Modes

This indicator offers users the flexibility to choose from three range modes:

1. Visible Range (Default Mode): In this mode, the volume profile calculation begins at the time of the left-most bar displayed in the current viewport. As the user scrolls through the viewport, the volume profile updates automatically.

2. Anchored Range: This mode allows the user to set the start time either by using the datetime input boxes or by dragging the anchor line on the chart.

3. All Range: In this mode, the volume profile calculation is based on all the historical bars available in the chart.

Market Sessions and TPO (+Forecast)This indicator "Market Sessions and TPO (+Forecast)" shows various market sessions alongside a TPO profile (presented as the traditional lettering system or as bars) and price forecast for the duration of the session.

Additionally, numerous statistics for the session are shown.

Features

Session open and close times presented in boxes

Session pre market and post market shown

TPO profile generated for each session (normal market hours only)

A forecast for the remained of the session is projected forward

Forecast can be augmented by ATR

Naked POCs remain on the chart until violated

Volume delta for the session shown

OI Change for the session shown (Binance sourced)

Total volume for the session shown

Price range for the session shown

The image above shows processes of the indicator.

Volume delta, OI change, total volume and session range are calculated and presented for each session.

Additionally, a TPO profile for the most recent session is shown, and a forecast for the remainder of the active session is shown.

The image above shows an alternative display method for the session forecast and TPO profile!

Additionally, the pre-market and post-market times are denoted by dashed boxes.

The image above exemplifies additional capabilities.

That's all for now; further updates to come and thank you for checking this out!

And a special thank you to @TradingView of course, for making all of this possible!

Historic Volume/Market ProfilesHistoric Volume/Market Profile is a Periodic Volume Profile with all of the improvements known in the original Volume/Market Profile.

VMP is a 2 in 1 Volume and Market Profile Indicator.

HVMP uses the base of VMP to offer a quick and simple view at multiple historic profiles at the same time.

This includes:

Cluster Identification for High Volume and Low Volume Areas.

Maximizing granularity by utilizing boxes and lines to get up to 1000 rows.

New Inclusions in HVMP vs VMP:

HVMP granularity is determined by the # of profiles on display. By doing this, each profile will get an even amount of allocated rows to use and granularity is scaled per-profile, to fit within the row allowance.

For Example: 1000/(# of profiles) = Maximum # of rows per profile.

HVMP introduces the "Auto-Scale" Option (on by Default), this automatically fits each profile within the defined timeframe period to provide a consistent display when switching timeframes.

Even with "Auto-Scale" enabled, "Display Size" dictates which direction the profile is displayed.

Below is a Negative Display Size (Displays from right to left, starting at the end of the period)

Below is a Positive Display Size (Displays from left to right, starting at the beginning of the period)

HVMP is only for historical data, you can get a live profile with the same Node Identification using VMP (Volume Market/Profile). The indicator that this one is based on.

Find it Here: Volume/Market Profile

Enjoy!

Developing Market Profile / TPO [Honestcowboy]The Developing Market Profile Indicator aims to broaden the horizon of Market Profile / TPO research and trading. While standard Market Profiles aim is to show where PRICE is in relation to TIME on a previous session (usually a day). Developing Market Profile will change bar by bar and display PRICE in relation to TIME for a user specified number of past bars.

What is a market profile?

"Market Profile is an intra-day charting technique (price vertical, time/activity horizontal) devised by J. Peter Steidlmayer. Steidlmayer was seeking a way to determine and to evaluate market value as it developed in the day time frame. The concept was to display price on a vertical axis against time on the horizontal, and the ensuing graphic generally is a bell shape--fatter at the middle prices, with activity trailing off and volume diminished at the extreme higher and lower prices."

For education on market profiles I recommend you search the net and study some profitable traders who use it.

Key Differences

Does not have a value area but distinguishes each column in relation to the biggest column in percentage terms.

Updates bar by bar

Does not take sessions into account

Shows historical values for each bar

While there is an entire education system build around Market Profiles they usually focus on a daily profile and in some cases how the value area develops during the day (there are indicators showing the developing value area).

The idea of trading based on a developing value area is what inspired me to build the Developing Market Profile.

🟦 CALCULATION

Think of this Developing Market Profile the same way as you would think of a moving average. On each bar it will lookback 200 bars (or as user specified) and calculate a Market Profile from those bars (range).

🔹Market Profile gets calculated using these steps:

Get the highest high and lowest low of the price range.

Separate that range into user specified amount of price zones (all spaced evenly)

Loop through the ranges bars and on each bar check in which price zones price was, then add +1 to the zones price was in (we do this using the OccurenceArray)

After it looped through all bars in the range it will draw columns for each price zone (using boxes) and make them as wide as the OccurenceArray dictates in number of bars

🔹Coloring each column:

The script will find the biggest column in the Profile and use that as a reference for all other columns. It will then decide for each column individually how big it is in % compared to the biggest column. It will use that percentage to decide which color to give it, top 20% will be red, top 40% purple, top 60% blue, top 80% green and all the rest yellow. The user is able to adjust these numbers for further customisation.

The historical display of the profiles uses plotchar() and will not only use the color of the column at that time but the % rating will also decide transparancy for further detail when analysing how the profiles developed over time. Each of those historical profiles is calculated using its own 200 past bars. This makes the script very heavy and that is why it includes optimisation settings, more info below.

🟦 USAGE

My general idea of the markets is that they are ever changing and that in studying that changing behaviour a good trader is able to distinguish new behaviour from old behaviour and adapt his approach before losing traders "weak hands" do.

A Market Profile can visually show a trader what kind of market environment we currently are in. In training this visual feedback helps traders remember past market environments and how the market behaved during these times.

Use the history shown using plotchars in colors to get an idea of how the Market Profile looked at each bar of the chart.

This history will help in studying how price moves at different stages of the Market Profile development.

I'm in no way an expert in trading Market Profiles so take this information with a grain of salt. Below an idea of how I would trade using this indicator:

🟦 SETTINGS

🔹MARKET PROFILING

Lookback: The amount of bars the Market Profile will look in the past to calculate where price has been the most in that range

Resolution: This is the amount of columns the Market Profile will have. These columns are calculated using the highest and lowest point price has been for the lookback period

Resolution is limited to a maximum of 32 because of pinescript plotting limits (64). Each plotchar() because of using variable colors takes up 2 of these slots

🔹VISUAL SETTINGS

Profile Distance From Chart: The amount of bars the market profile will be offset from the current bar

Border width (MP): The line thickness of the Market Profile column borders

Character: This is the character the history will use to show past profiles, default is a square.

Color theme: You can pick 5 colors from biggest column of the Profile to smallest column of the profile.

Numbers: these are for % to decide column color. So on default top 20% will be red, top 40% purple... Always use these in descending order

Show Market Profile: This setting will enable/disable the current Market Profile (columns on right side of current bar)

Show Profile History: This setting will enable/disable the Profile History which are the colored characters you see on each bar

🔹OPTIMISATION AND DEBUGGING

Calculate from here: The Market Profile will only start to calculate bar by bar from this point. Setting is needed to optimise loading time and quite frankly without it the script would probably exceed tradingview loading time limits.

Min Size: This setting is there to avoid visual bugs in the script. Scaling the chart there can be issues where the Market Profile extends all the way to 0. To avoid this use a minimum size bigger than the bugged bottom box

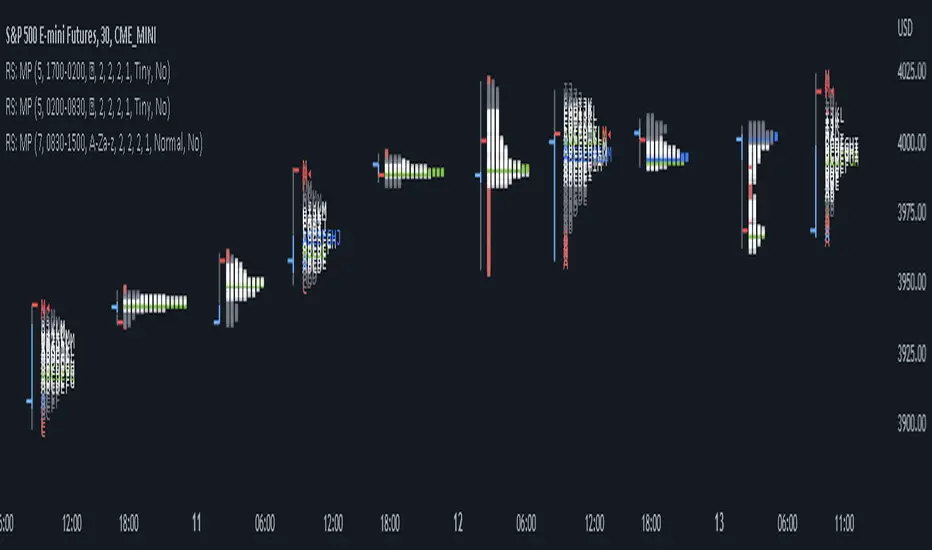

RS: Market ProfileA Market Profile (time price opportunity) implementation with an option to mark a point of control (POC) based on volume.

Config: Hide default candles. Select a session time using exchange timezone. Experiment with tick multiplier value to achieve desired level of detail. Choose the symbols of your choice, e.g. squares or A-Z chars. For multiple sessions you will have to add additional instances of this script with a different time configuration.

Limitations: TradingView has a hard limit for the number of characters (500), if it's reached, label rendering stops. Try increasing tick multiplier value to reduce the number of labels rendered or reduce the window size.

Features:

Use symbols or A-Z chars for TPOs

Mark POC

Calculate Value Area (volume or time based)

Highlight single prints (SP)

Highlight VWAP

Show daily bar

Highlight Open and Close

Highlight current price row (during live market)

Highlight initial balance (IB)

Open DriveOpen Drive is a market profile concept introduced by Jim Dalton. It occurs when the price moves directionally and persistently for the first 30 minutes from the cash market open.

It is necessary to use 30-minute bars as there needs to be enough time to measure an extreme move of the cash open. This means there will be fewer trades than other strategies using faster time periodicities.

The script finds open drives from these time points 0700/ 0800 and 1300/1430.

The entry signal also has a breakout threshold using the 5-bar high and 5-bar low to only take trades moving away from the prior 5-bar range. This weeds out most mid-range trades and small range expansion bars.

If the price has had a strong move from the open and has broken either below the prior 5-bar low or above the prior 5-bar high by an amount equal to the prior 5-bar range a trade is entered in the direction of the move.

The Exit criteria; exit after 3 bars which is 90mins when using a 30min periodicity.

Note, this script is shared to show that momentum generated on or around the cash open tends to persist. The entry and exits of this strategy are quite naive but there are plenty of ways to take more aggressive entries on faster time frames when an open drive occurs. The times chosen for this strategy will suit stock index futures mainly. The user can experiment with other futures products and their corresponding pit/ cash open hours.

Google "open drive market profile" for more information on open drives and market profile concepts.

Happy trading!

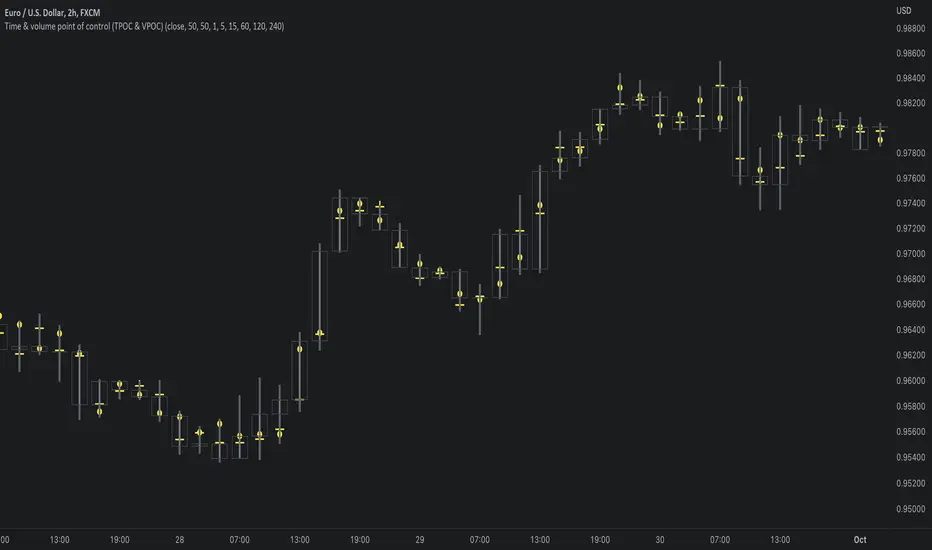

Time & volume point of control / quantifytoolsWhat are TPOC & VPOC?

TPOC (time point of control) and VPOC (volume point of control) are points in price where highest amount of time/volume was traded. This is considered key information in a market profile, as it shows where market participant interest was highest. Unlike full fledged market profile that shows total time/volume distribution, this script shows the points of control for each candle, plotted with a line (time) and a dot (volume). The script hides your candles/bars by default and forms a line in the middle representing candle range. In case of candles, borders will still be visible. This feature can be turned off in the settings.

Volume and time data are fetched from a lower timeframe that is automatically adjusted to fit the timeframe you're using. By default, the following settings are applied:

Charts <= 30 min: 1 minute timeframe

Charts > 30 min & <= 3 hours : 5 minute timeframe

Charts > 3 hours & <= 8 hours : 15 minute timeframe

Charts > 8 hours & <= 1D: 1 hour timeframe

Charts > 1D & <= 3D : 2 hour timeframe

Charts > 3D: 4 hour timeframe

Timeframe settings can be changed via input menu. The lower the timeframe, the more precision you get but with the cost of less historical data and slower loading time. Users can also choose which source to use for determining price for points of control, e.g. using close as source, the point of control is set to match the value of lower timeframe candle close. This could be replaced with OHLC4 for example, resulting in a point of control based on OHLC average.

To identify more profound points of market participant interest, TPOC & VPOC as percentage of total time/volume thresholds can be set via input menu. When a point of control is equal to or greater than the set percentage threshold, visual elements will be highlighted in a different color, e.g. 50% VPOC threshold will activate a highlight whenever volume traded at VPOC is equal to or greater than 50% of total volume. All colors are customizable.

VPOC is defined by fetching lower timeframe candle with the most amount of volume traded and using its close (by default) as a mark for point of control. For TPOC, each candle is divided into 10 lots which are used for calculating amount of closes taking place within the bracket values. The lot with highest amount of closes will be considered a point of control. This mark is displayed in the middle point of a lot:

How to utilize TPOC & VPOC

Example #1: Trapped market participants

One or both points of control at one end of candle range (wick tail) and candle close at the other end serves as an indication of market participants trapped in an awkward position. When price runs away further from these trapped participants, they are eventually forced to cover and drive price even further to the opposite direction:

Example #2: Trend initiation

A large move that leaves TPOC behind while VPOC is supportive serves as an indication of a trend initiation. Essentially, this is one way to identify an event where price traded sideways most of the time and suddenly moved away with volume:

Example #3: POC supported trend

A trend is healthy when it's supported by a point of control. Ideally you want to see either time or volume supporting a trend:

Average Volume ProfileAverage Volume Profile is an abstract based on a user suggestion.

The information displayed could be summed up as a volume profile divided by a market profile.

This indicator is a profile which displays the average volume of an area (of price).

It also calculates and displays the highest average volume point (HAV) and the relating value zones (calculated in the similar fashion to a volume profile).

Most of the code is directly from my "Volume/Market Profile" Indicator

I am not entirely sure of how to make use of the information displayed in this indicator or how useful it is.

However, I have added some things I figured would be useful to comprehend this information, such as:

- Read-out for highest average volume

- Read-out for current price average volume

- Read-out for current candle distributed volume (labeled as: "Vol")

- Floating line to visualize the current distributed volume in relation to the rest of the profile.

- Color changing labels for when the current distributed volume is higher than the current price avg volume.

Enjoy!

Volume/Market ProfileVolume/Market Profile is a 2 in 1 Volume Profile and Market Profile Indicator.

This indicator is my own calculations for compiling a volume profile and market profile.

The profile is progressively calculated live as the chart develops.

I have made use of both Boxes AND Lines to allow me to display a finer granularity profile by displaying up to twice the max amount of lines allowed in tradingview.

I have spent a lot of time to make sure the values are getting appended exactly as intended so that I can assure this profile is operating as precisely as possible within the limitations of the data available.

To make my calculations easier to use in other places, I have made my volume profile a function that can be extracted and used whenever you need values from a volume profile.

Feel free to read through the script if you don't understand how this profile is developed. I have made a commentary of my volume profile function to help you understand what exactly happens to compile the profiles.

As mentioned before, This indicator doubles as a market profile. To view both at the same time you will need to add the indicator on your chart twice.

I have built in comprehensive customizations to allow you to display your profiles however fits your needs.

Timeframe: The aggregation period for profiles, to see a 1 week profile, change the timeframe to 1 week.

Note: You can add custom timeframes by adding a custom timeframe in your chart timeframe dropdown menu. When you add timeframes in this area, they appear as options within indicators with the timeframe input.

Sensitivity: Allows for greater or less granularity changes. The calculation method for granularity automatically changes depending on the range of your chart.

Note: Multiply this value by 100 and that will be the max range (in ticks) of your price before the indicator automatically adjusts to make the profile less granular. (ex. If price ranges $1, and 1 tick is $0.01, granularity will be 0.01 with a sensitivity of 1+)

Value Area %: % of total volume to display as the value zone. (_% of total profile values are contained within the value zone)

Calculate as Market Profile: Uses a 1 Instead of the candle volume, to display a Market Profile. (If selected POC -> TPOC)

Display Size: Sets the # of bars from the profile axis to the profile's max value. If set negative, profile will be displayed left of axis, if positive, profile will be displayed to the right of the axis.

Display Offset: Sets the # of bars in front(or behind) the current chart bar to set the axis of the profile. If negative, the axis will be to the left of the current chart bar, if positive the axis will be right of the current chart bar.

Display Historical POC/VAH/VAL: Choose to display historical poc,vah,val lines.

Colors: I'm not explaining colors.

Enjoy!

TPO Market Profile [Kioseff Trading]REPOST; SCRIPT WORKS!!

Due to technical error, this script was republished! Thank you for your support (:

Hello!

This indicator comprises a real time TPO Market Profile!

The script works on any timeframe 1 second or greater - the script calculates relative to the timeframe selected for your chart.

The image above shows the 1-minute BTCUSD chart; 650 +/- tick levels are set.

To see the script in full functionality - try using bar replay on a cryptocurrency 1-minute chart (start at the beginning of a regular hours session). Be sure to adjust the tick spread if necessary (:

So far, the script's held up in real time - I've not had any array loop errors or timeouts. The TPO profile updates accordingly with changes in time / high and low prices. Letters are appended to the profile in real time.

The image above shows configurations for the indicator. I plan to update the indicator quite a bit over the coming days - more to come.

You can select the timeframe change the indicator accounts for. For instance, you can have set the indicator to reset every day, every 30 minutes, every 5 minutes, every week, month, etc.

In the image above, I configured the indicator to recalculate every 3 months. Consequently, the indicator will record a TPO profile for three consecutive, reset, then record a TPO profile for the next 3 months. This setting makes the indicator compatible with any timeframe greater than 1 minute.

You can also use a drag & drop time-start bar to modify the starting point for the market profile TPO calculation.

The indicator hosts an option to auto calculate the tick spread between levels. However, as you switch timeframes and assets, sometimes, you'll have to manually set the tick range (:

Thanks for checking it out; more to come!

Sep 4

Release Notes: UPDATE: The indicator can work on seconds-based charts.

The image above shows the indicator working on the 1-second chart.

(Screenshot is old; characters are now numbered instead of strange unicode)

Release Notes: Added value area + vah + val. Font update. Changed characters to numbered once the alphabet is exhausted. POC, VAH, and VAL label located left of the first bar of the interval. Initial balance range can be toggled. Spaced the characters (more legible). Quite a bit of aesthetic changes so check it out!

Soon, I'll release a version of the script that shows VAH, POC, VAL, and TPO letters from previous sessions. I coded this feature into this indicator; however, it was removed due to load time complications. This feature will be its own script (:

If the script has trouble loading please let me know (:

TPO Profile with Day StatFirst of all I want to Thank @noop42 for creating this wonderful Market Profile chart in Pine script

I have made some changes to this scripts

This Script can auto calculate the TPO Size for NSE Symbols and MCX Crude oil.

This Script Will only calculate the TPO's for visible range only so that the script use less heap size.

I have added some of the day Statistics to enhance your visualization.

Limitations of this Script

Currently This Script can Plot Market Profile Chart only for Historical Data.

It Can only Plot Market Profile Charts in 30-Mins Time Frame only so that you can't use it for Composite Profile Analysis.

To plot Market Profile Chart in Real Time and Historical please use "Market Profile With TPO by Drother"

Halfback + One-Time-Framing BarsThis indicator is designed to be used with Market Profile / Volume Profile trading techniques on a 30min chart.

The halfback of a candle is the mid point between the high and the low of the candle. A halfback trade can be taken once price retraces into this point as support/resistance using the prevailing trend as your trade direction.

One-Time-Framing is a fancy term for trending in one direction. One-Time-Framing happens when a candle breaks the previous candle's high without testing the low or when a candle breaks the low of the previous candle without testing the high. This indicates that the trend is one directional and opposing pressure is very weak. Taking trades in the opposing direction of multiple OTF bars is typically a bad trade setup.

Halfback and OTF setups are typically used on a 30min timeframe combined with Market or Volume Profile, but you can experiment with these setups on any timeframe if you wish.

I hope you all enjoy this indicator, comment below if you have any questions.

Rotation Factor: Buy/Sell Pressure for Market/Volume ProfileRotation Factor is a simple formula to figure out the buy and sell pressure of the overall day. Rotation Factor is usually combined with Market Profile or Volume Profile analysis. It is designed to be used on the 30min timeframe with a 1D interval reset. It can be used on other timeframes, but results will vary. Some Rotation Factor traders like to use it on a daily with a 1M interval reset for longer term trading.

The formula is very clean because it only focuses on price action, highs and lows. The formula is as follows:

Current Bar makes Higher High and Higher Low +2 points

Current Bar makes Lower High and Lower Low -2 Points

Current Bar makes Higher High and Lower Low 0 Points

Current Bar makes Lower High and Higher Low 0 Points

Current High and Previous High are Equal and Higher Low +1 Points

Current Bar makes Higher High but Current and Previous lows are equal +1 Points

Current Bar makes Lower High but Current and Previous lows are equal -1 Points

Current High and Previous High are Equal and Lower Low -1 Points

I hope you enjoy this indicator, if you have any questions let me know in the comments.

Market Profile Fixed ViewSome instruments does not provide any volume information, therefore, as a fixed volume profile user, I needed a fixed market profile indicator to use the same principles, regardless of whether the volumes are available or not.

This script draws a market profile histogram corresponding to price variations within a specific duration, you only need to specify Start and End date/time values to see the histogram on your chart.

Details

Two lines corresponding to highest/lowest prices are displayed around the histogram

The redline corresponds to the POC (point of control)

Options

Start calculation

End calculation

Bars number (histogram resolution, currently locked to a max value of 50 bars)

Display side/Width (allows to modify size of bars, to the left or to the right)

Bars/Borders/POC Color customization

Notes

This script will probably be updated (to add VAH/VAL zones, and maybe other options). However, some common market profile attributes have not been implemented yet since I don't really use them)

Market Profile with TPOThis is is Market Profile with TPO (the letters) on the current session. Due to pinescript limitations, we are limited to 500 TPOs, since this script uses 1 label per TPO. It is NOT volume profile, this is Time Profile (Time spent at a price).

Low Timeframe POCI have recently made a High Timeframe POC script (HFT POC) which is pretty popular. Thanks for this!

There are many requests to include lower timeframes in this script, that is why I created this script. I could have incorporated all the timeframe POC's into one indicator but I went this route to keep things more organized between all the different timeframes.

Currently included: Daily, 6H, 3H and 1H

/* DEFINITION */

Point Of Control (= POC) is a price level at which the heaviest volumes were traded.

/* HOW TO TRADE WITH THIS INDICATOR */

The basis for POC is determining bias on whichever timeframe you choose.

1. Identify a POC on the timeframe of your choosing.

/* If you choose the lowest timeframe (1H here) then always make sure to look at the higher timeframes to see how it is trading against a HTF POC.

2. When the price is moving away from the POC (either to the upside or downside) this can confirm or invalidate a trade.

3. You can now enter the trade on bias or wait for a retest of the same POC.

/* EXAMPLE TRADES /*

Here is a screenshot of some of the trades that are possible using these Low Timeframe POC's and some common sense.

s3.tradingview.com

High Timeframe POCBecause the big Bitcoin crash I have been looking a lot at high timeframe metrics. I never spent much time learning POC so I decided to create a little script for determining these on higher timeframes.

Currently included: Monthly, 3 months and 6 months.

/* DEFINITION */

Point Of Control (= POC) is a price level at which the heaviest volumes were traded.

Value Area High/Low (=VAH/VAL) is a range of prices where the majority of trading volume took place. Naturally, Value Area High being the top price level and Value Area Low being the lowest. POC always is between the two.

/* HOW TO TRADE WITH THIS INDICATOR */

The basis for POC is determining bias on whichever timeframe you choose.

1. Identify a POC on the timeframe of your choosing.

/* If you choose a "low" timeframe (monthly here) then make sure to look at the higher timeframes to see how it is playing against a higher timeframe POC.

2. When the price is moving away from the POC (either to the upside or downside) this will confirm or invalidate the trade.

3. You can now enter the trade on bias or wait for a retest of the same POC.

/* EXAMPLE TRADES /*

Here is a screenshot of some of the trades that are possible solely using the POC and some common sense.

s3.tradingview.com

Market ProfileHello All,

This is Market Profile script. "Market Profile is an intra-day charting technique (price vertical, time/activity horizontal) devised by J. Peter Steidlmayer. Steidlmayer was seeking a way to determine and to evaluate market value as it developed in the day time frame. The concept was to display price on a vertical axis against time on the horizontal, and the ensuing graphic generally is a bell shape--fatter at the middle prices, with activity trailing off and volume diminished at the extreme higher and lower prices." You better search it on the net for more information, you can find a lot of articles and books about the Market Profile.

You have option to see Value Area, All Channels or only POC line, you can set the colors as you wish.

Also you can choose the Higher Time Frame from the list or the script can choose the HTF for you automatically.

Enjoy!

[R&D] Moving CentroidThis script utilizes this concept. Instead of weighting by volume, it weights by amount of price action on every close price of the rolling window. I assume it can be used as an additional reference point for price mode and price antimode.

it is directly connected with Market (not volume) profile, or TPO charts.

The algorithm:

1) takes a rolling window of, for example, 50 data points of close prices:

2) for each of this closing prices, the algorithm will check how many bars touched this close price.

3) then: sum of datapoints * weights/sum of weights

Since the logic is implemented in pretty non-efficient way, the script sometimes can take time to make calculations. Moreover, it calculates the centroid taking into account only close prices, not every tick. of a given rolling window That's why it's still experimental.

Poor man's volume profileThis is an attempt to get something more or less similar to the volume profile for free.

The code is generated using a template. To change the settings, you may need to regenerate the code. The code has a link to the repository with the template.