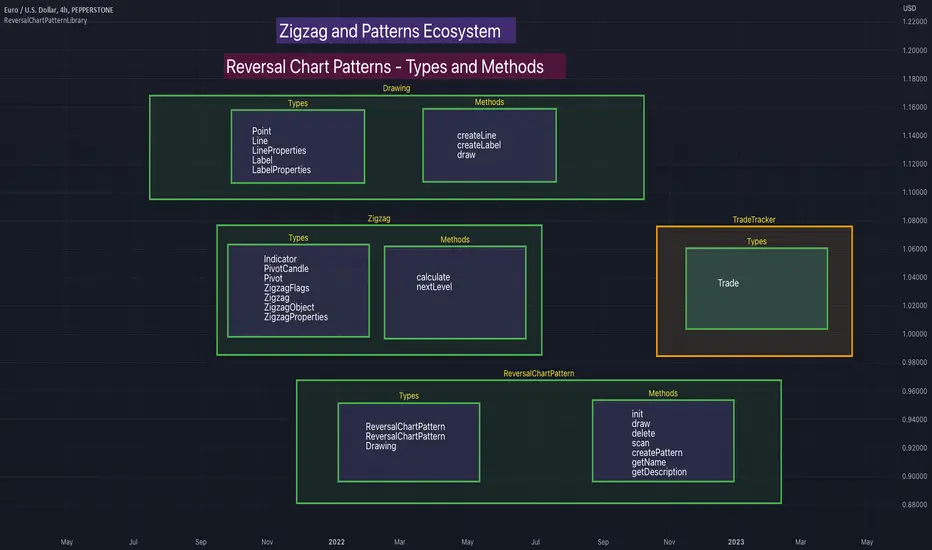

Vector3Library "Vector3"

Representation of 3D vectors and points.

This structure is used to pass 3D positions and directions around. It also contains functions for doing common vector operations.

Besides the functions listed below, other classes can be used to manipulate vectors and points as well.

For example the Quaternion and the Matrix4x4 classes are useful for rotating or transforming vectors and points.

___

**Reference:**

- github.com

- github.com

- github.com

- www.movable-type.co.uk

- docs.unity3d.com

- referencesource.microsoft.com

- github.com

\

new(x, y, z)

Create a new `Vector3`.

Parameters:

x (float) : `float` Property `x` value, (optional, default=na).

y (float) : `float` Property `y` value, (optional, default=na).

z (float) : `float` Property `z` value, (optional, default=na).

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.new(1.1, 1, 1)

```

from(value)

Create a new `Vector3` from a single value.

Parameters:

value (float) : `float` Properties positional value, (optional, default=na).

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.from(1.1)

```

from_Array(values, fill_na)

Create a new `Vector3` from a list of values, only reads up to the third item.

Parameters:

values (float ) : `array` Vector property values.

fill_na (float) : `float` Parameter value to replace missing indexes, (optional, defualt=na).

Returns: `Vector3` Generated new vector.

___

**Notes:**

- Supports any size of array, fills non available fields with `na`.

___

**Usage:**

```

.from_Array(array.from(1.1, fill_na=33))

.from_Array(array.from(1.1, 2, 3))

```

from_Vector2(values)

Create a new `Vector3` from a `Vector2`.

Parameters:

values (Vector2 type from RicardoSantos/CommonTypesMath/1) : `Vector2` Vector property values.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.from:Vector2(.Vector2.new(1, 2.0))

```

___

**Notes:**

- Type `Vector2` from CommonTypesMath library.

from_Quaternion(values)

Create a new `Vector3` from a `Quaternion`'s `x, y, z` properties.

Parameters:

values (Quaternion type from RicardoSantos/CommonTypesMath/1) : `Quaternion` Vector property values.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.from_Quaternion(.Quaternion.new(1, 2, 3, 4))

```

___

**Notes:**

- Type `Quaternion` from CommonTypesMath library.

from_String(expression, separator, fill_na)

Create a new `Vector3` from a list of values in a formated string.

Parameters:

expression (string) : `array` String with the list of vector properties.

separator (string) : `string` Separator between entries, (optional, default=`","`).

fill_na (float) : `float` Parameter value to replace missing indexes, (optional, defualt=na).

Returns: `Vector3` Generated new vector.

___

**Notes:**

- Supports any size of array, fills non available fields with `na`.

- `",,"` Empty fields will be ignored.

___

**Usage:**

```

.from_String("1.1", fill_na=33))

.from_String("(1.1,, 3)") // 1.1 , 3.0, NaN // empty field will be ignored!!

```

back()

Create a new `Vector3` object in the form `(0, 0, -1)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.back()

```

front()

Create a new `Vector3` object in the form `(0, 0, 1)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.front()

```

up()

Create a new `Vector3` object in the form `(0, 1, 0)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.up()

```

down()

Create a new `Vector3` object in the form `(0, -1, 0)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.down()

```

left()

Create a new `Vector3` object in the form `(-1, 0, 0)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.left()

```

right()

Create a new `Vector3` object in the form `(1, 0, 0)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.right()

```

zero()

Create a new `Vector3` object in the form `(0, 0, 0)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.zero()

```

one()

Create a new `Vector3` object in the form `(1, 1, 1)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.one()

```

minus_one()

Create a new `Vector3` object in the form `(-1, -1, -1)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.minus_one()

```

unit_x()

Create a new `Vector3` object in the form `(1, 0, 0)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.unit_x()

```

unit_y()

Create a new `Vector3` object in the form `(0, 1, 0)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.unit_y()

```

unit_z()

Create a new `Vector3` object in the form `(0, 0, 1)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.unit_z()

```

nan()

Create a new `Vector3` object in the form `(na, na, na)`.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.nan()

```

random(max, min)

Generate a vector with random properties.

Parameters:

max (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Maximum defined range of the vector properties.

min (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Minimum defined range of the vector properties.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.random(.from(math.pi), .from(-math.pi))

```

random(max)

Generate a vector with random properties (min set to 0.0).

Parameters:

max (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Maximum defined range of the vector properties.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

.random(.from(math.pi))

```

method copy(this)

Copy a existing `Vector3`

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .one().copy()

```

method i_add(this, other)

Modify a instance of a vector by adding a vector to it.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other Vector.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_add(.up())

```

method i_add(this, value)

Modify a instance of a vector by adding a vector to it.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` Value.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_add(3.2)

```

method i_subtract(this, other)

Modify a instance of a vector by subtracting a vector to it.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other Vector.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_subtract(.down())

```

method i_subtract(this, value)

Modify a instance of a vector by subtracting a vector to it.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` Value.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_subtract(3)

```

method i_multiply(this, other)

Modify a instance of a vector by multiplying a vector with it.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other Vector.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_multiply(.left())

```

method i_multiply(this, value)

Modify a instance of a vector by multiplying a vector with it.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` value.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_multiply(3)

```

method i_divide(this, other)

Modify a instance of a vector by dividing it by another vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other Vector.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_divide(.forward())

```

method i_divide(this, value)

Modify a instance of a vector by dividing it by another vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` Value.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_divide(3)

```

method i_mod(this, other)

Modify a instance of a vector by modulo assignment with another vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other Vector.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_mod(.back())

```

method i_mod(this, value)

Modify a instance of a vector by modulo assignment with another vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` Value.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_mod(3)

```

method i_pow(this, exponent)

Modify a instance of a vector by modulo assignment with another vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

exponent (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Exponent Vector.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_pow(.up())

```

method i_pow(this, exponent)

Modify a instance of a vector by modulo assignment with another vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

exponent (float) : `float` Exponent Value.

Returns: `Vector3` Updated source vector.

___

**Usage:**

```

a = .from(1) , a.i_pow(2)

```

method length_squared(this)

Squared length of the vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1)

Returns: `float` The squared length of this vector.

___

**Usage:**

```

a = .one().length_squared()

```

method magnitude_squared(this)

Squared magnitude of the vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `float` The length squared of this vector.

___

**Usage:**

```

a = .one().magnitude_squared()

```

method length(this)

Length of the vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `float` The length of this vector.

___

**Usage:**

```

a = .one().length()

```

method magnitude(this)

Magnitude of the vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `float` The Length of this vector.

___

**Usage:**

```

a = .one().magnitude()

```

method normalize(this, magnitude, eps)

Normalize a vector with a magnitude of 1(optional).

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

magnitude (float) : `float` Value to manipulate the magnitude of normalization, (optional, default=1.0).

eps (float)

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .new(33, 50, 100).normalize() // (x=0.283, y=0.429, z=0.858)

a = .new(33, 50, 100).normalize(2) // (x=0.142, y=0.214, z=0.429)

```

method to_String(this, precision)

Converts source vector to a string format, in the form `"(x, y, z)"`.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

precision (string) : `string` Precision format to apply to values (optional, default='').

Returns: `string` Formated string in a `"(x, y, z)"` format.

___

**Usage:**

```

a = .one().to_String("#.###")

```

method to_Array(this)

Converts source vector to a array format.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `array` List of the vector properties.

___

**Usage:**

```

a = .new(1, 2, 3).to_Array()

```

method to_Vector2(this)

Converts source vector to a Vector2 in the form `x, y`.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector2` Generated new vector.

___

**Usage:**

```

a = .from(1).to_Vector2()

```

method to_Quaternion(this, w)

Converts source vector to a Quaternion in the form `x, y, z, w`.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Sorce vector.

w (float) : `float` Property of `w` new value.

Returns: `Quaternion` Generated new vector.

___

**Usage:**

```

a = .from(1).to_Quaternion(w=1)

```

method add(this, other)

Add a vector to source vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).add(.unit_z())

```

method add(this, value)

Add a value to each property of the vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` Value.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).add(2.0)

```

add(value, other)

Add each property of a vector to a base value as a new vector.

Parameters:

value (float) : `float` Value.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(2) , b = .add(1.0, a)

```

method subtract(this, other)

Subtract vector from source vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).subtract(.left())

```

method subtract(this, value)

Subtract a value from each property in source vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` Value.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).subtract(2.0)

```

subtract(value, other)

Subtract each property in a vector from a base value and create a new vector.

Parameters:

value (float) : `float` Value.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .subtract(1.0, .right())

```

method multiply(this, other)

Multiply a vector by another.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).multiply(.up())

```

method multiply(this, value)

Multiply each element in source vector with a value.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` Value.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).multiply(2.0)

```

multiply(value, other)

Multiply a value with each property in a vector and create a new vector.

Parameters:

value (float) : `float` Value.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .multiply(1.0, .new(1, 2, 1))

```

method divide(this, other)

Divide a vector by another.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).divide(.from(2))

```

method divide(this, value)

Divide each property in a vector by a value.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` Value.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).divide(2.0)

```

divide(value, other)

Divide a base value by each property in a vector and create a new vector.

Parameters:

value (float) : `float` Value.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .divide(1.0, .from(2))

```

method mod(this, other)

Modulo a vector by another.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).mod(.from(2))

```

method mod(this, value)

Modulo each property in a vector by a value.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

value (float) : `float` Value.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).mod(2.0)

```

mod(value, other)

Modulo a base value by each property in a vector and create a new vector.

Parameters:

value (float) : `float` Value.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .mod(1.0, .from(2))

```

method negate(this)

Negate a vector in the form `(zero - this)`.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .one().negate()

```

method pow(this, other)

Modulo a vector by another.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(2).pow(.from(3))

```

method pow(this, exponent)

Raise the vector elements by a exponent.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

exponent (float) : `float` The exponent to raise the vector by.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).pow(2.0)

```

pow(value, exponent)

Raise value into a vector raised by the elements in exponent vector.

Parameters:

value (float) : `float` Base value.

exponent (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` The exponent to raise the vector of base value by.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .pow(1.0, .from(2))

```

method sqrt(this)

Square root of the elements in a vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).sqrt()

```

method abs(this)

Absolute properties of the vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).abs()

```

method max(this)

Highest property of the vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `float` Highest value amongst the vector properties.

___

**Usage:**

```

a = .new(1, 2, 3).max()

```

method min(this)

Lowest element of the vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `float` Lowest values amongst the vector properties.

___

**Usage:**

```

a = .new(1, 2, 3).min()

```

method floor(this)

Floor of vector a.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .new(1.33, 1.66, 1.99).floor()

```

method ceil(this)

Ceil of vector a.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .new(1.33, 1.66, 1.99).ceil()

```

method round(this)

Round of vector elements.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .new(1.33, 1.66, 1.99).round()

```

method round(this, precision)

Round of vector elements to n digits.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

precision (int) : `int` Number of digits to round the vector elements.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .new(1.33, 1.66, 1.99).round(1) // 1.3, 1.7, 2

```

method fractional(this)

Fractional parts of vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1.337).fractional() // 0.337

```

method dot_product(this, other)

Dot product of two vectors.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other vector.

Returns: `float` Dot product.

___

**Usage:**

```

a = .from(2).dot_product(.left())

```

method cross_product(this, other)

Cross product of two vectors.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).cross_produc(.right())

```

method scale(this, scalar)

Scale vector by a scalar value.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

scalar (float) : `float` Value to scale the the vector by.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).scale(2)

```

method rescale(this, magnitude)

Rescale a vector to a new magnitude.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

magnitude (float) : `float` Value to manipulate the magnitude of normalization.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(20).rescale(1)

```

method equals(this, other)

Compares two vectors.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

other (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Other vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).equals(.one())

```

method sin(this)

Sine of vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).sin()

```

method cos(this)

Cosine of vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).cos()

```

method tan(this)

Tangent of vector.

Namespace types: TMath.Vector3

Parameters:

this (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .from(1).tan()

```

vmax(a, b)

Highest elements of the properties from two vectors.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .vmax(.one(), .from(2))

```

vmax(a, b, c)

Highest elements of the properties from three vectors.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

c (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .vmax(.new(0.1, 2.5, 3.4), .from(2), .from(3))

```

vmin(a, b)

Lowest elements of the properties from two vectors.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .vmin(.one(), .from(2))

```

vmin(a, b, c)

Lowest elements of the properties from three vectors.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

c (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .vmin(.one(), .from(2), .new(3.3, 2.2, 0.5))

```

distance(a, b)

Distance between vector `a` and `b`.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Target vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = distance(.from(3), .unit_z())

```

clamp(a, min, max)

Restrict a vector between a min and max vector.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

min (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Minimum boundary vector.

max (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Maximum boundary vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .clamp(a=.new(2.9, 1.5, 3.9), min=.from(2), max=.new(2.5, 3.0, 3.5))

```

clamp_magnitude(a, radius)

Vector with its magnitude clamped to a radius.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.object, vector with properties that should be restricted to a radius.

radius (float) : `float` Maximum radius to restrict magnitude of vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .clamp_magnitude(.from(21), 7)

```

lerp_unclamped(a, b, rate)

`Unclamped` linearly interpolates between provided vectors by a rate.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Target vector.

rate (float) : `float` Rate of interpolation, range(0 > 1) where 0 == source vector and 1 == target vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .lerp_unclamped(.from(1), .from(2), 1.2)

```

lerp(a, b, rate)

Linearly interpolates between provided vectors by a rate.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Target vector.

rate (float) : `float` Rate of interpolation, range(0 > 1) where 0 == source vector and 1 == target vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = lerp(.one(), .from(2), 0.2)

```

herp(start, start_tangent, end, end_tangent, rate)

Hermite curve interpolation between provided vectors.

Parameters:

start (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Start vector.

start_tangent (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Start vector tangent.

end (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` End vector.

end_tangent (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` End vector tangent.

rate (int) : `float` Rate of the movement from `start` to `end` to get position, should be range(0 > 1).

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

s = .new(0, 0, 0) , st = .new(0, 1, 1)

e = .new(1, 2, 2) , et = .new(-1, -1, 3)

h = .herp(s, st, e, et, 0.3)

```

___

**Reference:** en.m.wikibooks.org

herp_2(a, b, rate)

Hermite curve interpolation between provided vectors.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Target vector.

rate (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Rate of the movement per component from `start` to `end` to get position, should be range(0 > 1).

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

h = .herp_2(.one(), .new(0.1, 3, 2), 0.6)

```

noise(a)

3D Noise based on Morgan McGuire @morgan3d

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = noise(.one())

```

___

**Reference:**

- thebookofshaders.com

- www.shadertoy.com

rotate(a, axis, angle)

Rotate a vector around a axis.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

axis (string) : `string` The plane to rotate around, `option="x", "y", "z"`.

angle (float) : `float` Angle in radians.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .rotate(.from(3), 'y', math.toradians(45.0))

```

rotate_x(a, angle)

Rotate a vector on a fixed `x`.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

angle (float) : `float` Angle in radians.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .rotate_x(.from(3), math.toradians(90.0))

```

rotate_y(a, angle)

Rotate a vector on a fixed `y`.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

angle (float) : `float` Angle in radians.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .rotate_y(.from(3), math.toradians(90.0))

```

rotate_yaw_pitch(a, yaw, pitch)

Rotate a vector by yaw and pitch values.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

yaw (float) : `float` Angle in radians.

pitch (float) : `float` Angle in radians.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .rotate_yaw_pitch(.from(3), math.toradians(90.0), math.toradians(45.0))

```

project(a, normal, eps)

Project a vector off a plane defined by a normal.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

normal (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` The normal of the surface being reflected off.

eps (float) : `float` Minimum resolution to void division by zero (default=0.000001).

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .project(.one(), .down())

```

project_on_plane(a, normal, eps)

Projects a vector onto a plane defined by a normal orthogonal to the plane.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

normal (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` The normal of the surface being reflected off.

eps (float) : `float` Minimum resolution to void division by zero (default=0.000001).

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .project_on_plane(.one(), .left())

```

project_to_2d(a, camera_position, camera_target)

Project a vector onto a two dimensions plane.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

camera_position (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Camera position.

camera_target (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Camera target plane position.

Returns: `Vector2` Generated new vector.

___

**Usage:**

```

a = .project_to_2d(.one(), .new(2, 2, 3), .zero())

```

reflect(a, normal)

Reflects a vector off a plane defined by a normal.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

normal (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` The normal of the surface being reflected off.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .reflect(.one(), .right())

```

angle(a, b, eps)

Angle in degrees between two vectors.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Target vector.

eps (float) : `float` Minimum resolution to void division by zero (default=1.0e-15).

Returns: `float` Angle value in degrees.

___

**Usage:**

```

a = .angle(.one(), .up())

```

angle_signed(a, b, axis)

Signed angle in degrees between two vectors.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Target vector.

axis (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Axis vector.

Returns: `float` Angle value in degrees.

___

**Usage:**

```

a = .angle_signed(.one(), .left(), .down())

```

___

**Notes:**

- The smaller of the two possible angles between the two vectors is returned, therefore the result will never

be greater than 180 degrees or smaller than -180 degrees.

- If you imagine the from and to vectors as lines on a piece of paper, both originating from the same point,

then the /axis/ vector would point up out of the paper.

- The measured angle between the two vectors would be positive in a clockwise direction and negative in an

anti-clockwise direction.

___

**Reference:**

- github.com

angle2d(a, b)

2D angle between two vectors.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

b (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Target vector.

Returns: `float` Angle value in degrees.

___

**Usage:**

```

a = .angle2d(.one(), .left())

```

transform_Matrix(a, M)

Transforms a vector by the given matrix.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

M (matrix) : `matrix` A 4x4 matrix. The transformation matrix.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

mat = matrix.new(4, 0)

mat.add_row(0, array.from(0.0, 0.0, 0.0, 1.0))

mat.add_row(1, array.from(0.0, 0.0, 1.0, 0.0))

mat.add_row(2, array.from(0.0, 1.0, 0.0, 0.0))

mat.add_row(3, array.from(1.0, 0.0, 0.0, 0.0))

b = .transform_Matrix(.one(), mat)

```

transform_M44(a, M)

Transforms a vector by the given matrix.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

M (M44 type from RicardoSantos/CommonTypesMath/1) : `M44` A 4x4 matrix. The transformation matrix.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .transform_M44(.one(), .M44.new(0,0,0,1,0,0,1,0,0,1,0,0,1,0,0,0))

```

___

**Notes:**

- Type `M44` from `CommonTypesMath` library.

transform_normal_Matrix(a, M)

Transforms a vector by the given matrix.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

M (matrix) : `matrix` A 4x4 matrix. The transformation matrix.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

mat = matrix.new(4, 0)

mat.add_row(0, array.from(0.0, 0.0, 0.0, 1.0))

mat.add_row(1, array.from(0.0, 0.0, 1.0, 0.0))

mat.add_row(2, array.from(0.0, 1.0, 0.0, 0.0))

mat.add_row(3, array.from(1.0, 0.0, 0.0, 0.0))

b = .transform_normal_Matrix(.one(), mat)

```

transform_normal_M44(a, M)

Transforms a vector by the given matrix.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector.

M (M44 type from RicardoSantos/CommonTypesMath/1) : `M44` A 4x4 matrix. The transformation matrix.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .transform_normal_M44(.one(), .M44.new(0,0,0,1,0,0,1,0,0,1,0,0,1,0,0,0))

```

___

**Notes:**

- Type `M44` from `CommonTypesMath` library.

transform_Array(a, rotation)

Transforms a vector by the given Quaternion rotation value.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector. The source vector to be rotated.

rotation (float ) : `array` A 4 element array. Quaternion. The rotation to apply.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .transform_Array(.one(), array.from(0.2, 0.2, 0.2, 1.0))

```

___

**Reference:**

- referencesource.microsoft.com

transform_Quaternion(a, rotation)

Transforms a vector by the given Quaternion rotation value.

Parameters:

a (Vector3 type from RicardoSantos/CommonTypesMath/1) : `Vector3` Source vector. The source vector to be rotated.

rotation (Quaternion type from RicardoSantos/CommonTypesMath/1) : `array` A 4 element array. Quaternion. The rotation to apply.

Returns: `Vector3` Generated new vector.

___

**Usage:**

```

a = .transform_Quaternion(.one(), .Quaternion.new(0.2, 0.2, 0.2, 1.0))

```

___

**Notes:**

- Type `Quaternion` from `CommonTypesMath` library.

___

**Reference:**

- referencesource.microsoft.com

Penunjuk dan strategi

Mad_MATHLibrary "MAD_MATH"

This is a mathematical library where I store useful kernels, filters and selectors for the different types of computations.

This library also contains opensource code from other scripters.

Future extensions are very likely, there are some functions I would like to add, but I have to wait for approvals so i can include them.

Ehlers_EMA(_src, _length)

Calculates the Ehlers Exponential Moving Average (Ehlers_EMA)

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers EMA

Returns: The Ehlers EMA value

Ehlers_Gaussian(_src, _length)

Calculates the Ehlers Gaussian Filter

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers Gaussian Filter

Returns: The Ehlers Gaussian Filter value

Ehlers_supersmoother(_src, _length)

Calculates the Ehlers Supersmoother

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers Supersmoother

Returns: The Ehlers Supersmoother value

Ehlers_SMA_fast(_src, _length)

Calculates the Ehlers Simple Moving Average (SMA) Fast

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers SMA Fast

Returns: The Ehlers SMA Fast value

Ehlers_EMA_fast(_src, _length)

Calculates the Ehlers Exponential Moving Average (EMA) Fast

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers EMA Fast

Returns: The Ehlers EMA Fast value

Ehlers_RSI_fast(_src, _length)

Calculates the Ehlers Relative Strength Index (RSI) Fast

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers RSI Fast

Returns: The Ehlers RSI Fast value

Ehlers_Band_Pass_Filter(_src, _length)

Calculates the Ehlers BandPass Filter

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers BandPass Filter

Returns: The Ehlers BandPass Filter value

Ehlers_Butterworth(_src, _length)

Calculates the Ehlers Butterworth Filter

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers Butterworth Filter

Returns: The Ehlers Butterworth Filter value

Ehlers_Two_Pole_Gaussian_Filter(_src, _length)

Calculates the Ehlers Two-Pole Gaussian Filter

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers Two-Pole Gaussian Filter

Returns: The Ehlers Two-Pole Gaussian Filter value

Ehlers_Two_Pole_Butterworth_Filter(_src, _length)

Calculates the Ehlers Two-Pole Butterworth Filter

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers Two-Pole Butterworth Filter

Returns: The Ehlers Two-Pole Butterworth Filter value

Ehlers_Band_Stop_Filter(_src, _length)

Calculates the Ehlers Band Stop Filter

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers Band Stop Filter

Returns: The Ehlers Band Stop Filter value

Ehlers_Smoother(_src)

Calculates the Ehlers Smoother

Parameters:

_src (float) : The source series for calculation

Returns: The Ehlers Smoother value

Ehlers_High_Pass_Filter(_src, _length)

Calculates the Ehlers High Pass Filter

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers High Pass Filter

Returns: The Ehlers High Pass Filter value

Ehlers_2_Pole_High_Pass_Filter(_src, _length)

Calculates the Ehlers Two-Pole High Pass Filter

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the Ehlers Two-Pole High Pass Filter

Returns: The Ehlers Two-Pole High Pass Filter value

pr(_src, _length)

pr Calculates the percentage rank (PR) of a value within a range.

Parameters:

_src (float) : The source value for which the percentage rank is calculated. It represents the value to be ranked within the range.

_length (simple int) : The _length of the range over which the percentage rank is calculated. It determines the number of bars considered for the calculation.

Returns: The percentage rank (PR) of the source value within the range, adjusted by adding 50 to the result.

smma(_src, _length)

Calculates the SMMA (Smoothed Moving Average)

Parameters:

_src (float) : The source series for calculation

_length (simple int)

Returns: The SMMA value

hullma(_src, _length)

Calculates the Hull Moving Average (HullMA)

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The _length of the HullMA

Returns: The HullMA value

tma(_src, _length)

Calculates the Triple Moving Average (TMA)

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The _length of the TMA

Returns: The TMA value

dema(_src, _length)

Calculates the Double Exponential Moving Average (DEMA)

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The _length of the DEMA

Returns: The DEMA value

tema(_src, _length)

Calculates the Triple Exponential Moving Average (TEMA)

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The _length of the TEMA

Returns: The TEMA value

w2ma(_src, _length)

Calculates the Normalized Double Moving Average (N2MA)

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The _length of the N2MA

Returns: The N2MA value

wma(_src, _length)

Calculates the Normalized Moving Average (NMA)

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The _length of the NMA

Returns: The NMA value

nma(_open, _close, _length)

Calculates the Normalized Moving Average (NMA)

Parameters:

_open (float) : The open price series

_close (float) : The close price series

_length (simple int) : The _length for finding the highest and lowest values

Returns: The NMA value

lma(_src, _length)

Parameters:

_src (float)

_length (simple int)

zero_lag(_src, _length, gamma1, zl)

Calculates the Zero Lag Moving Average (ZeroLag)

Parameters:

_src (float) : The source series for calculation

_length (simple int) : The length for the moving average

gamma1 (simple int) : The coefficient for calculating 'd'

zl (simple bool) : Boolean flag for applying Zero Lag

Returns: An array containing the ZeroLag Moving Average and a boolean flag indicating if it's flat

copyright HPotter, thanks for that great function

chebyshevI(src, len, ripple)

Calculates the Chebyshev Type I Filter

Parameters:

src (float) : The source series for calculation

len (int) : The length of the filter

ripple (float) : The ripple factor for the filter

Returns: The output of the Chebyshev Type I Filter

math from Pafnuti Lwowitsch Tschebyschow (1821–1894)

Thanks peacefulLizard50262 for the find and translation

chebyshevII(src, len, ripple)

Calculates the Chebyshev Type II Filter

Parameters:

src (float) : The source series for calculation

len (int) : The length of the filter

ripple (float) : The ripple factor for the filter

Returns: The output of the Chebyshev Type II Filter

math from Pafnuti Lwowitsch Tschebyschow (1821–1894)

Thanks peacefulLizard50262 for the find

wavetrend(_src, _n1, _n2)

Calculates the WaveTrend indicator

Parameters:

_src (float) : The source series for calculation

_n1 (simple int) : The period for the first EMA calculation

_n2 (simple int) : The period for the second EMA calculation

Returns: The WaveTrend value

f_getma(_type, _src, _length, ripple)

Calculates various types of moving averages

Parameters:

_type (simple string) : The type of indicator to calculate

_src (float) : The source series for calculation

_length (simple int) : The length for the moving average or indicator

ripple (simple float)

Returns: The calculated moving average or indicator value

f_getfilter(_type, _src, _length)

Calculates various types of filters

Parameters:

_type (simple string) : The type of indicator to calculate

_src (float) : The source series for calculation

_length (simple int) : The length for the moving average or indicator

Returns: The filtered value

f_getoszillator(_type, _src, _length)

Calculates various types of Deviations and other indicators

Parameters:

_type (simple string) : The type of indicator to calculate

_src (float) : The source series for calculation

_length (simple int) : The length for the moving average or indicator

Returns: The calculated moving average or indicator value

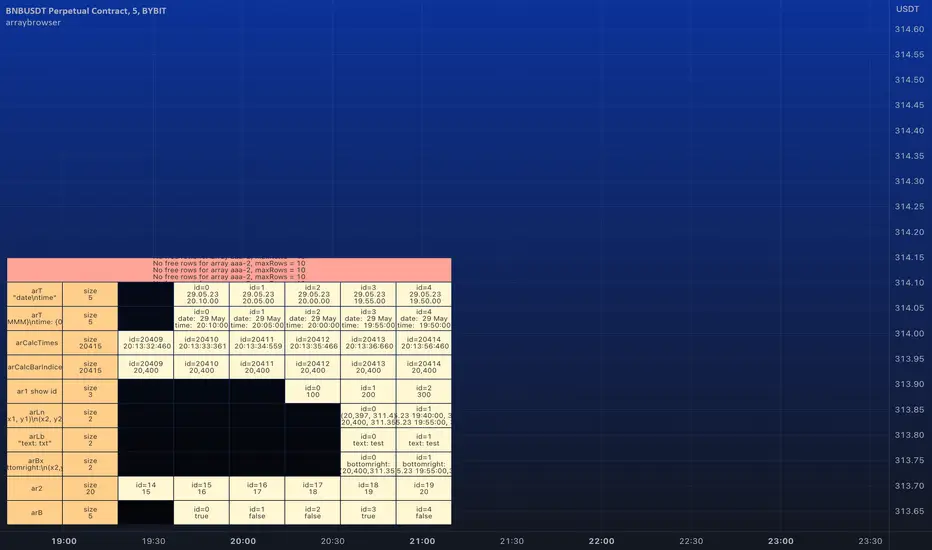

arraybrowser█ ARRAY BROWSER

Add you arrays to the array browser window and scroll them away left and right.

Flexible formatting options (see below).

Many thanks to @kaigouthro for his beautiful matrixautotable library. (import kaigouthro/matrixautotable/14)

How to use

Copy the "ARRAY BROWSER" commented code section below to your script and uncomment.

See DEMO section in the library for usage examples.

Basically: add() your arrays and draw() on barstate.islast.

If your script adds the arrays every calculation do not forget to clear() before adding.

Otherwise, since the arrays are added by reference, no need to add them on every bar, every time you draw() the actual values are retrieved.

Up to 10 arrays of each type (float/string/line/label/box) are supported (total 50 arrays).

Change offset in the input settings to scroll left/right.

Usage example:

import moebius1977/arraybrowser/1 as arraybrowser // this alias is used in the copied section, so better keep it

arbr.clear() // clears all rows and deletes the table

arbr.add(arrayFloat, format = "0.00") // adds an array with title

arbr.add(arrayInt) // adds an array without title

arbr.add(arrayTimes, "array of times 1", "date time") // format date and time so as to fit in the cell.

arbr.add(arrayTimes, "array of times 2", "{0, time, HH:mm}") // format date and time so as to fit in the cell.

arbr.add(arrayString) //

arbr.add(arrayLine, "arrayLines", "(x1, y1) (x2,y2)") // use your own format combining "x1", "y1", "x2", "y2"

arbr.add(arrayLabel, "arrayLabel", "txt") // only print label text, no coordinates

arbr.add(arrayBox, showIds = true) // show ID's for this array if input setting is "individually"

arbr.draw() // shows the table with arrays, use on barstate.islast

Formatting options

For float/int you can always use format string like "{0, time, HH:mm:ss}" or "{0.00}".

Additional options are

- --- Number formats ---

- "number"

- "0"

- "0.0"

- "0.00"

- "0.000"

- "0.0000"

- "0.00000"

- "0.000000"

- "0.0000000"

- --- Date formats ---

- "date"

- "date : time"

- "dd.MM"

- "dd"

- --- Time formats ---

- "time"

- "HH:mm"

- "mm:ss"

- "date time"

- "date, time"

- "date,time"

- "date\time"

For line and box : Empty `format` returns coordinates as "(x1, y1) - (x2, y2)". Otherwise "x1", "x2", "y1", "y2" in `format` string are replaced by values. (e.g. toS(line, "x1, x2") will only return x1 and x2 separated by comma).

For label : Empty `format` returns coordinates and text as "(x, y): text = text". Otherwise "x1", "y1", "txt" in `format` string are replaced by values. (e.g. toS(label, "txt") will only return text of the label)

JavaScript-style Debug ConsoleThis library provides a JavaScript-style debug console to Pine Coders. It supports the most commonly used utilities from the WHATWG Console Standard including the following:

• console.log

• console.debug

• console.info

• console.warn

• console.error

• console.assert

• console.count

• console.countReset

• console.group

• console.groupEnd

• console.clear

In addition to the WHATWG standard, this library also supports the following methods:

• console.show

• console.hide

FEATURES

• Follows the WHATWG Console Standard, which is widely adopted by all major JavaScript runtimes including browsers and Node.js.

• Provides an out-of-box UI with pre-configured theming, ensuring a clean and professional-looking console.

• Allows for easy UI customizations to fit your personal preferences.

• Has extremely simple import and initialization, making it easy to integrate with your existing codebase.

USAGE

1. Import this library:

import algotraderdev/Console/1

2. Initialize the console object:

var console = Console.new()

// You can also specify optional params to customize the look & feel.

var console = Console.new(

position = position.bottom_right,

max_rows = 50,

width = 0,

text_size = size.normal,

background_color = #000000CC,

timestamp_color = #AAAAAA,

info_message_color = #DDDDDD,

debug_message_color = #AAAAAA,

warn_message_color = #FFEB3B,

error_message_color = #ff3c00)

3. Use the console object to debug your code. Here are some examples:

// Basic logging

console.log('hello world!') // prints 'hello world'

console.warn('warn') // prints 'warn' in yellow

console.error('error') // prints 'error' in red

console.clear() // clears the console

// Assertion

console.assert(a.isEmpty(), 'array should be empty') // prints 'assertion failed: array should be empty' if the array is not empty

// Counter

console.count('fooFunction') // prints 'fooFunction: 1'

console.count('fooFunction') // prints 'fooFunction: 2'

console.countReset('fooFunction') // resets the counter

console.count('fooFunction') // prints 'fooFunction: 1'

// Group

console.log('A')

console.group()

console.log('B')

console.group()

console.log('C')

console.log('D')

console.groupEnd()

console.log('E')

console.groupEnd()

console.log('F')

// prints

// A

// B

// C

// D

// E

// F

// Hide and show

console.hide()

console.show()

biased_price_targetLibrary "biased_price_target"

Collection of functions that can be used for the calculation of biased price targets like stop loss and

take profit from a reference price using several methods that are already provided by the "distance_ratio" library plus

the 'HHLL'. Methods supported are percentagewise (PERC), atr-based (ATR), fixed profit (PROF), tick-based (TICKS),

risk reward ratio (RR), and highest high/lowest low (HHLL)

Position_controlLibrary "Position_control"

This is a library for defining positions and working with them.

f_calculateLeverage(_Leverage, _maintenance, _value, _direction)

Calculate the leverage used in a trade.

@description This function calculates the leverage used in a trade, based on the value of the trade, the maintenance margin, and the direction of the trade.

Parameters:

_Leverage (float) : The leverage used in the trade, as a floating point number.

_maintenance (float) : The maintenance margin percentage, as a floating point number.

_value (float) : The value of the trade, as a floating point number.

_direction (string) : The direction of the trade, either "long" or "short".

Returns: The leverage used in the trade, as a floating point number.

f_calculate_PL(_Position, _max_TP, _Position_index, _show_profit, _i_decimals_contracts, _i_decimals_prercent)

Calculate the profit or loss for a given trade.

@description This function calculates the profit or loss for a given trade, based on the position type, maximum take profit, position index, and whether to show the profit as a percentage or a value.

Parameters:

_Position (t_Position_type ) : An array of position types for the trade.

_max_TP (int) : The maximum take profit for the trade, as an integer value.

_Position_index (int) : The index of the position in the array, as an integer value.

_show_profit (bool) : A boolean value indicating whether to show the profit as a percentage or a value.

_i_decimals_contracts (int)

_i_decimals_prercent (int)

Returns: The profit or loss for the trade, as a floating point number.

f_drawposition(_Position, _Parameters, _Position_index)

draws a position on the chart

@description via sending in a typo of Position this function is able to drawout Stoploss, Entrybox, Takeprofits and the required labels with information

Parameters:

_Position (t_Position_type ) : array of type t_Position_type containing the position information.

_Parameters (t_drawing_parameters)

_Position_index (int) : the index of the current position.

Returns: None but boxes / lines / labels on the chart itself

t_TP_Variant

Fields:

TP_Type (series__string)

TP_Parameter_1 (series__integer)

TP_Parameter_2 (series__integer)

TP_Parameter_3 (series__float)

TP_Parameter_4 (series__float)

t_TPs

Fields:

TP_Price (series__float)

TP_Lot (series__float)

TP_Variant (|t_TP_Variant|#OBJ)

TP_Active (series__bool)

t_SLs

Fields:

SL_Price (series__float)

SL_Lot (series__float)

SL_Active (series__bool)

t_Position_type

Fields:

Lot (series__float)

Leverage (series__float)

Maintenance (series__float)

Starttime (series__integer)

Entry_Start (series__float)

Stoptime (series__integer)

Entry_Stop (series__float)

Entryprice (series__float)

TPs (array__|t_TPs|#OBJ)

SLs (array__|t_SLs|#OBJ)

t_drawing_parameters

Fields:

ShowPos (series__bool)

ShowLIQ (series__bool)

A_Colors (array__color)

Prolong_lines (series__bool)

Str_fontsize (series__string)

Textshift (series__integer)

Decimals_contracts (series__integer)

Decimals_price (series__integer)

Decimals_percent (series__integer)

bartime (series__integer)

Mad_StandardpartsLibrary "Mad_Standardparts"

This are my Standardparts used in upcoming scipts

roundTo(_value, _decimals)

Round a floating point value to a specified number of decimal places.

@description This function takes a floating point value and rounds it to a specified number of decimal places.

Parameters:

_value (float) : The floating point value to be rounded.

_decimals (int) : The number of decimal places to round to. Must be a non-negative integer.

Returns: The rounded value, as a floating point number.

clear_all()

Delete all drawings on the chart.

@description This function deletes all drawings on the chart, including lines, boxes, and labels.

Returns: None.

shifting(_value)

Create a string of spaces to shift text over by a specified amount.

@description This function takes an integer value and returns a string consisting of that many spaces, which can be used to shift text over in a PineScript chart.

Parameters:

_value (int) : The number of spaces to create in the output string.

Returns: A string consisting of the specified number of spaces.

fromLog(_value)

Convert a linear value to a logarithmic value.

@description This function takes a linear value and converts it to a logarithmic value, using the formula specified in the code.

Parameters:

_value (float)

Returns: The corresponding logarithmic value, as a floating point number.

toLog(_value)

Convert a logarithmic value to a linear value.

@description This function takes a logarithmic value and converts it to a linear value, using the formula specified in the code.

Parameters:

_value (float)

Returns: The corresponding linear value, as a floating point number.

f_getbartime()

Calculate the time per bar on the chart.

@description This function calculates the time per bar on the chart based on the first 100 bars.

Returns: The time per bar, as an integer value.

Metrics using Alternative Portfolio TheoryLibrary "APT_Metrics"

Portfolio metrics using alternative portfolio theory

metrics(init, cur, start, end, alpha)

Calculates APT metrics

Parameters:

init (float) : Starting Equity (strategy.initial)

cur (float)

start (int) : Start date (UNIX)

end (int) : End Date (UNIX)

alpha (float) : Confidence interval for DaR/CDaR. Defval = 0.05

Returns: Plots table with APT metrics

The metrics are shown in the bottom pane being applied to a buy-and-hold strategy.

PLEASE NOTE: This is the first draft of the library. Some calculations may be incorrect. If you spot any mistakes then please let me know and I will correct them as soon as possible. I am also open to suggestions on how to improve this.

At the moment this only works on the daily timeframe until I can find a way to universally calculate annualized volatility.

WebhookJsonMsgLibrary "WebhookJsonMsg"

This webhook json message library provides convenient functions for building JSON messages

Used to manage automatic transaction orders and positions

method buildWebhookJson(msg)

Builds the final JSON payload from a WebhookMessage type.

Namespace types: WebhookMessage

Parameters:

msg (WebhookMessage)

Returns: A JSON Payload.

Dict

Define some constant values

Fields:

OPEN_LONG (series string)

OPEN_SHORT (series string)

CLOSE_LONG (series string)

CLOSE_SHORT (series string)

LIMIT (series string)

MARKET (series string)

U_MARGIN (series string)

C_MARGIN (series string)

SPOT (series string)

WebhookMessage

Webhook message structure.

Fields:

strategyId (series string)

signalNo (series string)

symbol (series string)

symbolType (series string)

orderSide (series string)

price (series string)

orderType (series string)

takeProfitPrice (series string)

stopLossPrice (series string)

timestamp (series string)

accessKey (series string)

loggerLibrary "logger"

◼ Overview

A dual logging library for developers. Tradingview lacks logging capability. This library provides logging while developing your scripts and is to be used by developers when developing and debugging their scripts.

Using this library would potentially slow down you scripts. Hence, use this for debugging only. Once your code is as you would like it to be, remove the logging code.

◼︎ Usage (Console):

Console = A sleek single cell logging with a limit of 4096 characters. When you dont need a large logging capability.

//@version=5

indicator("demo.Console", overlay=true)

plot(na)

import GETpacman/logger/1 as logger

var console = logger.log.new()

console.init() // init() should be called as first line after variable declaration

console.FrameColor:=color.green

console.log(' ')

console.log(' ')

console.log('Hello World')

console.log(' ')

console.log(' ')

console.ShowStatusBar:=true

console.StatusBarAtBottom:=true

console.FrameColor:=color.blue //settings can be changed anytime before show method is called. Even twice. The last call will set the final value

console.ShowHeader:=false //this wont throw error but is not used for console

console.show(position=position.bottom_right) //this should be the last line of your code, after all methods and settings have been dealt with.

◼︎ Usage (Logx):

Logx = Multiple columns logging with a limit of 4096 characters each message. When you need to log large number of messages.

//@version=5

indicator("demo.Logx", overlay=true)

plot(na)

import GETpacman/logger/1 as logger

var logx = logger.log.new()

logx.init() // init() should be called as first line after variable declaration

logx.FrameColor:=color.green

logx.log(' ')

logx.log(' ')

logx.log('Hello World')

logx.log(' ')

logx.log(' ')

logx.ShowStatusBar:=true

logx.StatusBarAtBottom:=true

logx.ShowQ3:=false

logx.ShowQ4:=false

logx.ShowQ5:=false

logx.ShowQ6:=false

logx.FrameColor:=color.olive //settings can be changed anytime before show method is called. Even twice. The last call will set the final value

logx.show(position=position.top_right) //this should be the last line of your code, after all methods and settings have been dealt with.

◼︎ Fields (with default settings)

▶︎ IsConsole = True Log will act as Console if true, otherwise it will act as Logx

▶︎ ShowHeader = True (Log only) Will show a header at top or bottom of logx.

▶︎ HeaderAtTop = True (Log only) Will show the header at the top, or bottom if false, if ShowHeader is true.

▶︎ ShowStatusBar = True Will show a status bar at the bottom

▶︎ StatusBarAtBottom = True Will show the status bar at the bottom, or top if false, if ShowHeader is true.

▶︎ ShowMetaStatus = True Will show the meta info within status bar (Current Bar, characters left in console, Paging On Every Bar, Console dumped data etc)

▶︎ ShowBarIndex = True Logx will show column for Bar Index when the message was logged. Console will add Bar index at the front of logged messages

▶︎ ShowDateTime = True Logx will show column for Date/Time passed with the logged message logged. Console will add Date/Time at the front of logged messages

▶︎ ShowLogLevels = True Logx will show column for Log levels corresponding to error codes. Console will log levels in the status bar

▶︎ ReplaceWithErrorCodes = True (Log only) Logx will show error codes instead of log levels, if ShowLogLevels is switched on

▶︎ RestrictLevelsToKey7 = True Log levels will be restricted to Ley 7 codes - TRACE, DEBUG, INFO, WARNING, ERROR, CRITICAL, FATAL

▶︎ ShowQ1 = True (Log only) Show the column for Q1

▶︎ ShowQ2 = True (Log only) Show the column for Q2

▶︎ ShowQ3 = True (Log only) Show the column for Q3

▶︎ ShowQ4 = True (Log only) Show the column for Q4

▶︎ ShowQ5 = True (Log only) Show the column for Q5

▶︎ ShowQ6 = True (Log only) Show the column for Q6

▶︎ ColorText = True Log/Console will color text as per error codes

▶︎ HighlightText = True Log/Console will highlight text (like denoting) as per error codes

▶︎ AutoMerge = True (Log only) Merge the queues towards the right if there is no data in those queues.

▶︎ PageOnEveryBar = True Clear data from previous bars on each new bar, in conjuction with PageHistory setting.

▶︎ MoveLogUp = True Move log in up direction. Setting to false will push logs down.

▶︎ MarkNewBar = True On each change of bar, add a marker to show the bar has changed

▶︎ PrefixLogLevel = True (Console only) Prefix all messages with the log level corresponding to error code.

▶︎ MinWidth = 40 Set the minimum width needed to be seen. Prevents logx/console shrinking below these number of characters.

▶︎ TabSizeQ1 = 0 If set to more than one, the messages on Q1 or Console messages will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ2 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ3 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ4 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ5 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ6 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ PageHistory = 0 Used with PageOnEveryBar. Determines how many historial pages to keep.

▶︎ HeaderQbarIndex = 'Bar#' (Logx only) The header to show for Bar Index

▶︎ HeaderQdateTime = 'Date' (Logx only) The header to show for Date/Time

▶︎ HeaderQerrorCode = 'eCode' (Logx only) The header to show for Error Codes

▶︎ HeaderQlogLevel = 'State' (Logx only) The header to show for Log Level

▶︎ HeaderQ1 = 'h.Q1' (Logx only) The header to show for Q1

▶︎ HeaderQ2 = 'h.Q2' (Logx only) The header to show for Q2

▶︎ HeaderQ3 = 'h.Q3' (Logx only) The header to show for Q3

▶︎ HeaderQ4 = 'h.Q4' (Logx only) The header to show for Q4

▶︎ HeaderQ5 = 'h.Q5' (Logx only) The header to show for Q5

▶︎ HeaderQ6 = 'h.Q6' (Logx only) The header to show for Q6

▶︎ Status = '' Set the status to this text.

▶︎ HeaderColor Set the color for the header

▶︎ HeaderColorBG Set the background color for the header

▶︎ StatusColor Set the color for the status bar

▶︎ StatusColorBG Set the background color for the status bar

▶︎ TextColor Set the color for the text used without error code or code 0.

▶︎ TextColorBG Set the background color for the text used without error code or code 0.

▶︎ FrameColor Set the color for the frame around Logx/Console

▶︎ FrameSize = 1 Set the size of the frame around Logx/Console

▶︎ CellBorderSize = 0 Set the size of the border around cells.

▶︎ CellBorderColor Set the color for the border around cells within Logx/Console

▶︎ SeparatorColor = gray Set the color of separate in between Console/Logx Attachment

◼︎ Methods (summary)

● init ▶︎ Initialise the log

● log ▶︎ Log the messages. Use method show to display the messages

● page ▶︎ Clear messages from previous bar while logging messages on this bar.

● show ▶︎ Shows a table displaying the logged messages

● clear ▶︎ Clears the log of all messages

● resize ▶︎ Resizes the log. If size is for reduction then oldest messages are lost first.

● turnPage ▶︎ When called, all messages marked with previous page, or from start are cleared

● dateTimeFormat ▶︎ Sets the date time format to be used when displaying date/time info.

● resetTextColor ▶︎ Reset Text Color to library default

● resetTextBGcolor ▶︎ Reset Text BG Color to library default

● resetHeaderColor ▶︎ Reset Header Color to library default

● resetHeaderBGcolor ▶︎ Reset Header BG Color to library default

● resetStatusColor ▶︎ Reset Status Color to library default

● resetStatusBGcolor ▶︎ Reset Status BG Color to library default

● setColors ▶︎ Sets the colors to be used for corresponding error codes

● setColorsBG ▶︎ Sets the background colors to be used for corresponding error codes. If not match of error code, then text color used.

● setColorsHC ▶︎ Sets the highlight colors to be used for corresponding error codes.If not match of error code, then text bg color used.

● resetColors ▶︎ Reset the colors to library default (Total 36, not including error code 0)

● resetColorsBG ▶︎ Reset the background colors to library default

● resetColorsHC ▶︎ Reset the highlight colors to library default

● setLevelNames ▶︎ Set the log level names to be used for corresponding error codes. If not match of error code, then empty string used.

● resetLevelNames ▶︎ Reset the log level names to library default. (Total 36) 1=TRACE, 2=DEBUG, 3=INFO, 4=WARNING, 5=ERROR, 6=CRITICAL, 7=FATAL

● attach ▶︎ Attaches a console to an existing Logx, allowing to have dual logging system independent of each other

● detach ▶︎ Detaches an already attached console from Logx

method clear(this)

Clears all the queue, including bar_index and time queues, of existing messages

Namespace types: log

Parameters:

this (log)

method resize(this, rows)

Resizes the message queues. If size is decreased then removes the oldest messages

Namespace types: log

Parameters:

this (log)

rows (int) : The new size needed for the queues. Default value is 40.

method dateTimeFormat(this, format)

Re/set the date time format used for displaying date and time. Default resets to dd.MMM.yy HH:mm

Namespace types: log

Parameters:

this (log)

format (string)

method resetTextColor(this)

Resets the text color of the log to library default.

Namespace types: log

Parameters: