OKXJsonLibrary "OKXJson"

f_buildId(prefix, instrument)

Parameters:

prefix (string)

instrument (string)

f_utcTimestamp()

f_investmentType(internalAction, entryType, closeType)

Parameters:

internalAction (string)

entryType (string)

closeType (string)

f_build(id, okxAction, marketPosition, prevMarketPosition, instrument, signalToken, timestampUtc, investmentType, amount, maxLagSeconds)

Parameters:

id (string)

okxAction (string)

marketPosition (string)

prevMarketPosition (string)

instrument (string)

signalToken (string)

timestampUtc (string)

investmentType (string)

amount (string)

maxLagSeconds (string)

Penunjuk dan strategi

Candle Pattern Library [1CG]Candle Pattern Library

A comprehensive and easy-to-use Pine Script™ library for detecting single, two, and three-candle patterns. This library provides detailed pattern analysis including size classification, direction validation, and specific pattern identification.

Quick Start

1. Import the Library

import OneCleverGuy/CandlePatternLibrary/1 as CPL

2. Analyze Candles

Use the main analysis functions to detect patterns. You can analyze the current forming candle or confirmed historical candles.

// 1. Analyze candles (Current , Previous , and the one before )

// Note: We use full variable names for clarity.

CandleData candleNewest = CPL.analyzeCandle(open, high, low, close, 250, 50, 10, 50, 85)

CandleData candleMiddle = CPL.analyzeCandle(open , high , low , close , 250, 50, 10, 50, 85)

CandleData candleOldest = CPL.analyzeCandle(open , high , low , close , 250, 50, 10, 50, 85)

// 2. Analyze multi-candle patterns

// Pass candles in chronological order: Oldest -> Newest

var twoCandleData = CPL.analyzeTwoCandlePattern(candleMiddle, candleNewest, 10, 85)

var threeCandleData = CPL.analyzeThreeCandlePattern(candleOldest, candleMiddle, candleNewest)

Enums Reference

These are the Enum Types exported by the library. When checking results, use the pattern Alias.EnumType.Value (e.g., CPL.CandlePattern.Hammer).

CandlePattern

Enum Type for single-candle formations.

Usage: CPL.CandlePattern.

Values:

Unknown : No specific pattern detected.

RegularBullish : A standard bullish candle.

RegularBearish : A standard bearish candle.

BullishMarubozu : Bullish candle with little to no wicks.

BearishMarubozu : Bearish candle with little to no wicks.

Hammer : Small body at the top of the range (bullish reversal).

ShootingStar : Small body at the bottom of the range (bearish reversal).

SpinningTop : Small body centered in the range.

Doji : Open and close are effectively equal.

LongLeggedDoji : Doji with long upper and lower wicks.

CrossDoji : Doji with the body in the upper section.

DragonflyDoji : Doji where open/close are at the high.

InvertedCrossDoji : Doji with the body in the lower section.

GravestoneDoji : Doji where open/close are at the low.

FourPriceDoji : Open, High, Low, and Close are all equal.

TwoCandlePattern

Enum Type for two-candle formations.

Usage: CPL.TwoCandlePattern.

Values:

None : No two-candle pattern detected.

BullishEngulfingWeak : Bullish candle engulfs the previous body (close does not engulf range).

BullishEngulfingStrong : Bullish candle completely engulfs the previous body close outside range.

BearishEngulfingWeak : Bearish candle engulfs the previous body.

BearishEngulfingStrong : Bearish candle completely engulfs the previous body.

InsideBar : The second candle is completely contained within the first.

TweezerTop : Two candles with matching highs (bearish reversal).

TweezerBottom : Two candles with matching lows (bullish reversal).

BullishRailRoad : Two opposite Marubozus (Down -> Up).

BearishRailRoad : Two opposite Marubozus (Up -> Down).

ThreeCandlePattern

Enum Type for three-candle formations.

Usage: CPL.ThreeCandlePattern.

Values:

None : No three-candle pattern detected.

ThreeWhiteSoldiers : Three consecutive bullish candles.

ThreeBlackCrows : Three consecutive bearish candles.

ThreeWhiteSoldiersWithBullishFVG : Three White Soldiers containing a Bullish FVG.

ThreeWhiteSoldiersWithBearishFVG : Three White Soldiers containing a Bearish FVG.

ThreeBlackCrowsWithBullishFVG : Three Black Crows containing a Bullish FVG.

ThreeBlackCrowsWithBearishFVG : Three Black Crows containing a Bearish FVG.

MorningStar : Bearish -> Small/Doji -> Bullish (Bullish Reversal).

EveningStar : Bullish -> Small/Doji -> Bearish (Bearish Reversal).

BullishAbandonedBaby : Morning Star with gaps between all candles.

BearishAbandonedBaby : Evening Star with gaps between all candles.

EngulfingSandwich : Bearish -> Bullish (Engulfing) -> Bearish (Inside).

BullishFairValueGap : A gap between Candle 1 High and Candle 3 Low.

BearishFairValueGap : A gap between Candle 1 Low and Candle 3 High.

CandleSize

Enum Type for candle size classification.

Usage: CPL.CandleSize.

Values:

Short

Normal

Long

CandleDirection

Enum Type for candle direction classification.

Usage: CPL.CandleDirection.

Values:

Bearish

Neutral

Bullish

Function Reference

Analysis Functions

analyzeCandle(_open, _high, _low, _close, _avgSize, _sizeThresholdPct, _equivTolerance, _bodyTolerance, _positionThreshold)

analyzeCandle - Analyzes a single candle's OHLC data to determine its size, direction, and single-candle pattern.

Parameters:

_open (float) : (float) - Candle open price.

_high (float) : (float) - Candle high price.

_low (float) : (float) - Candle low price.

_close (float) : (float) - Candle close price.

_avgSize (float) : (float) - Baseline size (wick range) to compare against.

_sizeThresholdPct (float) : (float) - % difference from average to be considered Long/Short (e.g., 50.0).

_equivTolerance (float) : (float) - Absolute price diff for Close to equal Open (Doji checks).

_bodyTolerance (float) : (float) - Absolute price diff for "Small Body" checks.

_positionThreshold (int) : (int) - Int (0-100) determining valid wick ratios for Hammers/Shooting Stars (e.g., 85).

Returns: (CandleData) - CandleData object containing CandlePattern, CandleSize, CandleDirection.

analyzeTwoCandlePattern(_candle1, _candle2, _equivTolerance, _positionThreshold)

analyzeTwoCandlePattern - Analyzes two consecutive candles to find pairs like Engulfing, Tweezers, or Inside Bars.

Parameters:

_candle1 (CandleData) : (CandleData) - The first (older) candle data (previous).

_candle2 (CandleData) : (CandleData) - The second (newer) candle data (current).

_equivTolerance (float) : (float) - Price tolerance for matching highs/lows (Tweezers).

_positionThreshold (int) : (int) - Threshold for wick validations.

Returns: (TwoCandleData) - TwoCandleData object containing TwoCandlePattern.

analyzeThreeCandlePattern(_candle1, _candle2, _candle3)

analyzeThreeCandlePattern - Analyzes three consecutive candles to find complex patterns like Morning Stars, Abandoned Babies, or Three White Soldiers.

Parameters:

_candle1 (CandleData) : (CandleData) - The first (oldest) candle data.

_candle2 (CandleData) : (CandleData) - The second (middle) candle data.

_candle3 (CandleData) : (CandleData) - The third (newest) candle data.

Returns: (ThreeCandleData) - ThreeCandleData object containing ThreeCandlePattern.

Naming Utilities

getPatternName(_pattern)

getPatternName - Returns the string name of a candle pattern.

Parameters:

_pattern (CandlePattern) : (CandlePattern) - The candle pattern enum value.

Returns: (string) - Human-readable pattern name (e.g., "Hammer").

getTwoCandlePatternName(_pattern)

getTwoCandlePatternName - Returns the string name of a two-candle pattern.

Parameters:

_pattern (TwoCandlePattern) : (TwoCandlePattern) - The two-candle pattern enum value.

Returns: (string) - Human-readable pattern name (e.g., "Bullish Engulfing").

getThreeCandlePatternName(_pattern)

getThreeCandlePatternName - Returns the string name of a three-candle pattern.

Parameters:

_pattern (ThreeCandlePattern) : (ThreeCandlePattern) - The three-candle pattern enum value.

Returns: (string) - Human-readable pattern name (e.g., "Morning Star").

getSizeName(_size)

getSizeName - Returns the string name of a candle size.

Parameters:

_size (CandleSize) : (CandleSize) - The candle size enum value.

Returns: (string) - Human-readable size name ("Short", "Normal", or "Long").

getDirectionName(_direction)

getDirectionName - Returns the string name of a candle direction.

Parameters:

_direction (CandleDirection) : (CandleDirection) - The candle direction enum value.

Returns: (string) - Human-readable direction name ("Bullish", "Bearish", or "Neutral").

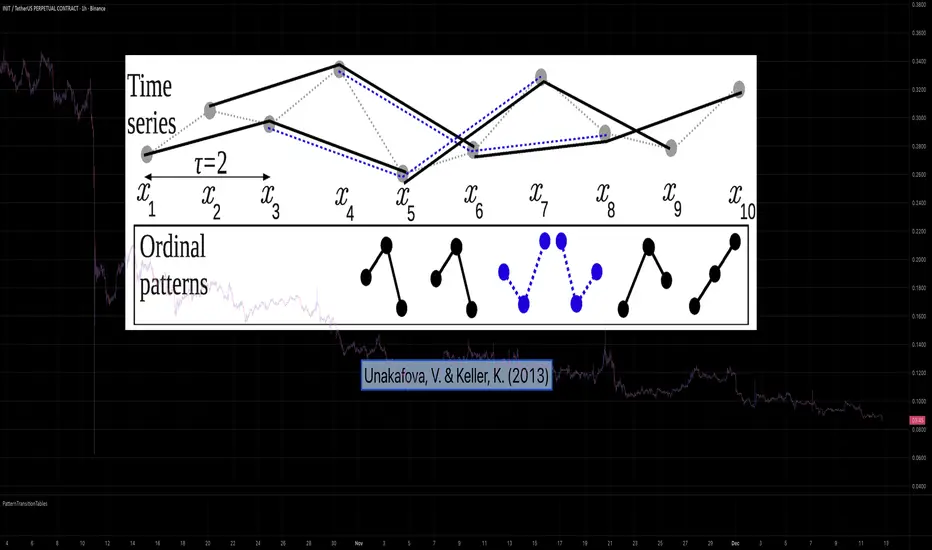

PatternTransitionTablesPatternTransitionTables Library

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- 1. INTRODUCTION --------- 🌸

💮 Overview

This library provides precomputed state transition tables to enable ultra-efficient, O(1) computation of Ordinal Patterns. It is designed specifically to support high-performance indicators calculating Permutation Entropy and related complexity measures.

💮 The Problem & Solution

Calculating Permutation Entropy, as introduced by Bandt and Pompe (2002), typically requires computing ordinal patterns within a sliding window at every time step. The standard successive-pattern method (Equations 2+3 in the paper) requires ≤ 4d-1 operations per update.

Unakafova and Keller (2013) demonstrated that successive ordinal patterns "overlap" significantly. By knowing the current pattern index and the relative rank (position l) of just the single new data point, the next pattern index can be determined via a precomputed look-up table. Computing l still requires d comparisons, but the table lookup itself is O(1), eliminating the need for d multiplications and d additions. This reduces total operations from ≤ 4d-1 to ≤ 2d per update (Table 4). This library contains these precomputed tables for orders d = 2 through d = 5.

🌸 --------- 2. THEORETICAL BACKGROUND --------- 🌸

💮 Permutation Entropy

Bandt, C., & Pompe, B. (2002). Permutation entropy: A natural complexity measure for time series.

doi.org

This concept quantifies the complexity of a system by comparing the order of neighbouring values rather than their magnitudes. It is robust against noise and non-linear distortions, making it ideal for financial time series analysis.

💮 Efficient Computation

Unakafova, V. A., & Keller, K. (2013). Efficiently Measuring Complexity on the Basis of Real-World Data.

doi.org

This library implements the transition function φ_d(n, l) described in Equation 5 of the paper. It maps a current pattern index (n) and the position of the new value (l) to the successor pattern, reducing the complexity of updates to constant time O(1).

🌸 --------- 3. LIBRARY FUNCTIONALITY --------- 🌸

💮 Data Structure

The library stores transition matrices as flattened 1D integer arrays. These tables are mathematically rigorous representations of the factorial number system used to enumerate permutations.

💮 Core Function: get_successor()

This is the primary interface for the library for direct pattern updates.

• Input: The current pattern index and the rank position of the incoming price data.

• Process: Routes the request to the specific transition table for the chosen order (d=2 to d=5).

• Output: The integer index of the next ordinal pattern.

💮 Table Access: get_table()

This function returns the entire flattened transition table for a specified dimension. This enables local caching of the table (e.g. in an indicator's init() method), avoiding the overhead of repeated library calls during the calculation loop.

💮 Supported Orders & Terminology

The parameter d is the order of ordinal patterns (following Bandt & Pompe 2002). Each pattern of order d contains (d+1) data points, yielding (d+1)! unique patterns:

• d=2: 3 points → 6 unique patterns, 3 successor positions

• d=3: 4 points → 24 unique patterns, 4 successor positions

• d=4: 5 points → 120 unique patterns, 5 successor positions

• d=5: 6 points → 720 unique patterns, 6 successor positions

Note: d=6 is not implemented. The resulting code size (approx. 191k tokens) exceeds the Pine Script limit of 100k tokens (as of 2025-12).

SharelineUI_LibraryLibrary "SharelineUI_Library"

get_text_size(opt)

Parameters:

opt (string)

status_color(val)

Parameters:

val (float)

trend_color(trend_cat)

Parameters:

trend_cat (string)

momentum_color(score, bullTh, bearTh)

Parameters:

score (float)

bullTh (float)

bearTh (float)

create_standard_hud(pos, cols, rows)

Parameters:

pos (string)

cols (int)

rows (int)

SharelineCore_LibraryLibrary "SharelineCore_Library"

funding_premium(premiumSym, funding_period, plot_type, interest_rate, fundScale)

Parameters:

premiumSym (string)

funding_period (string)

plot_type (string)

interest_rate (float)

fundScale (float)

cvd_vwap_delta(spotSym, perpSym, normLen, resetCVD)

Parameters:

spotSym (string)

perpSym (string)

normLen (int)

resetCVD (bool)

cvd_trend_norm(spotSymbol, perpSymbol, normLen, resetOnSession)

Parameters:

spotSymbol (string)

perpSymbol (string)

normLen (int)

resetOnSession (bool)

trend_strength_engine(cvdSpot, cvdPerp)

Parameters:

cvdSpot (float)

cvdPerp (float)

bias_engine(plot_value, spotTrendVal, perpTrendVal, spotStrength, perpStrength)

Parameters:

plot_value (float)

spotTrendVal (float)

perpTrendVal (float)

spotStrength (float)

perpStrength (float)

smc_engine(h, l, c, v, ms_len, bos_len, vol_filter, scale_factor, smooth_len, signal_len)

Parameters:

h (float)

l (float)

c (float)

v (float)

ms_len (int)

bos_len (int)

vol_filter (bool)

scale_factor (float)

smooth_len (simple int)

signal_len (simple int)

momentum_engine(o, c, v, fast, slow, signal, rsiLen, normLen, smaShort, smaLong, wMacd, wRsi, wCvd, wVpi)

Parameters:

o (float)

c (float)

v (float)

fast (simple int)

slow (simple int)

signal (simple int)

rsiLen (simple int)

normLen (int)

smaShort (int)

smaLong (int)

wMacd (float)

wRsi (float)

wCvd (float)

wVpi (float)

oi_engine(quotecur, useBinance, useBinance2, useBinance3, useBitmex, useBitmex2, useKraken, d_mult, strength1_mult, strength2_mult)

Parameters:

quotecur (string)

useBinance (bool)

useBinance2 (bool)

useBinance3 (bool)

useBitmex (bool)

useBitmex2 (bool)

useKraken (bool)

d_mult (float)

strength1_mult (float)

strength2_mult (float)

TRZigZagLibLibrary "TRZigZagLib"

method directionName(this)

Gets pivot direction as string

Namespace types: Pivot

Parameters:

this (Pivot) : Pivot instance

Returns: "HIGH" or "LOW"

method isHigh(this)

Checks if pivot is a high

Namespace types: Pivot

Parameters:

this (Pivot) : Pivot instance

Returns: true if pivot is a high

method isLow(this)

Checks if pivot is a low

Namespace types: Pivot

Parameters:

this (Pivot) : Pivot instance

Returns: true if pivot is a low

method newSettings(minLength, minBarSize, maxBarSize)

Creates default ZigZag settings

Namespace types: series int, simple int, input int, const int

Parameters:

minLength (int) : Minimum pivot length (default: 10)

minBarSize (int) : Minimum bars between pivots (default: 5)

maxBarSize (int) : Maximum bars to lookback (default: 300)

Returns: New ZigZagSettings instance

method setLineStyle(this, lineColor, lineWidth, lineStyle)

Sets line appearance

Namespace types: ZigZagSettings

Parameters:

this (ZigZagSettings) : Settings instance

lineColor (color)

lineWidth (int)

lineStyle (string)

Returns: Modified settings instance

method newZigZag(settings, depth)

Creates a new ZigZag instance

Namespace types: ZigZagSettings

Parameters:

settings (ZigZagSettings) : ZigZag settings

depth (int) : Depth value for this ZigZag

Returns: New ZigZag instance

method calculate(this)

Calculates ZigZag using LuxAlgo-style pivot detection

Namespace types: ZigZag

Parameters:

this (ZigZag) : ZigZag instance

method getLastPivots(this, count)

Gets the last N pivots

Namespace types: ZigZag

Parameters:

this (ZigZag) : ZigZag instance

count (int) : Number of pivots to get (default: 5)

Returns: Array of pivots

method getPivot(this, index)

Gets pivot at index

Namespace types: ZigZag

Parameters:

this (ZigZag) : ZigZag instance

index (int) : Index (0 = most recent)

Returns: Pivot or na

method truncate(this, maxBars)

Truncates old pivots beyond lookback window

Namespace types: ZigZag

Parameters:

this (ZigZag) : ZigZag instance

maxBars (int) : Maximum bars to keep

method newMultiZigZag(settings, minDepth, maxDepth, count)

Creates a new MultiZigZag manager

Namespace types: ZigZagSettings

Parameters:

settings (ZigZagSettings) : Base settings for all ZigZags

minDepth (int) : Minimum depth value

maxDepth (int) : Maximum depth value

count (int) : Number of ZigZag instances (max 11)

Returns: New MultiZigZag instance

method calculateAll(this)

Updates all ZigZag instances

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

method getZigZag(this, index)

Gets ZigZag at index

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

index (int) : Index (0 to count-1)

Returns: ZigZag instance or na

method getDepth(this, index)

Gets depth value at index

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

index (int) : Index (0 to count-1)

Returns: Depth value

method size(this)

Gets total number of ZigZag instances

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

Returns: Count of ZigZag instances

method truncateAll(this, maxBars)

Truncates all ZigZag instances

Namespace types: MultiZigZag

Parameters:

this (MultiZigZag) : MultiZigZag instance

maxBars (int) : Maximum bars to keep

method distance(p1, p2)

Calculates distance between two pivots

Namespace types: Pivot

Parameters:

p1 (Pivot) : First pivot

p2 (Pivot) : Second pivot

Returns: Price distance (absolute)

method barSpan(p1, p2)

Calculates bar span between two pivots

Namespace types: Pivot

Parameters:

p1 (Pivot) : First pivot

p2 (Pivot) : Second pivot

Returns: Bar span (absolute)

method isAlternating(pivots)

Checks if pivots are alternating (high-low-high or low-high-low)

Namespace types: array

Parameters:

pivots (array) : Array of pivots

Returns: true if alternating pattern exists

Pivot

Pivot point in the chart

Fields:

d (series int) : Direction: 1=high, -1=low

x (series int) : Bar index

y (series float) : Price

confirmed (series bool) : Pivot confirmation flag

ZigZagSettings

ZigZag configuration settings

Fields:

minLength (series int) : Minimum pivot detection length

minBarSize (series int) : Minimum bars between pivots

maxBarSize (series int) : Maximum bars to lookback

lineColor (series color) : ZigZag line color

lineWidth (series int) : ZigZag line width

lineStyle (series string) : ZigZag line style

ZigZag

Single ZigZag instance

Fields:

settings (ZigZagSettings) : Configuration settings

pivots (array) : Array of pivot points (max 25 for patterns)

lastUpdateBar (series int) : Last bar index when updated

depth (series int) : Current depth value

MultiZigZag

Multi-depth ZigZag manager

Fields:

zigzags (array) : Array of ZigZag instances (max 11)

depthValues (array) : Array of depth values being used

currentBar (series int) : Current bar index being processed

LuxyEnergyIndexThe Luxy Energy Index (LEI) library provides functions to measure price movement exhaustion by analyzing three dimensions: Extension (distance from fair value), Velocity (speed of movement), and Volume (confirmation level).

LEI answers a different question than traditional momentum indicators: instead of "how far has price gone?" (like RSI), LEI asks "how tired is this move?"

This library allows Pine Script developers to integrate LEI calculations into their own indicators and strategies.

How to Import

//@version=6

indicator("My Indicator")

import OrenLuxy/LuxyEnergyIndex/1 as LEI

Main Functions

`lei(src)` → float

Returns the LEI value on a 0-100 scale.

src (optional): Price source, default is `close`

Returns : LEI value (0-100) or `na` if insufficient data (first 50 bars)

leiValue = LEI.lei()

leiValue = LEI.lei(hlc3) // custom source

`leiDetailed(src)` → tuple

Returns LEI with all component values for detailed analysis.

= LEI.leiDetailed()

Returns:

`lei` - Final LEI value (0-100)

`extension` - Distance from VWAP in ATR units

`velocity` - 5-bar price change in ATR units

`volumeZ` - Volume Z-Score

`volumeModifier` - Applied modifier (1.0 = neutral)

`vwap` - VWAP value used

Component Functions

| Function | Description | Returns |

|-----------------------------------|---------------------------------|---------------|

| `calcExtension(src, vwap)` | Distance from VWAP / ATR | float |

| `calcVelocity(src)` | 5-bar price change / ATR | float |

| `calcVolumeZ()` | Volume Z-Score | float |

| `calcVolumeModifier(volZ)` | Volume modifier | float (≥1.0) |

| `getVWAP()` | Auto-detects asset type | float |

Signal Functions

| Function | Description | Returns |

|---------------------------------------------|----------------------------------|-----------|

| `isExhausted(lei, threshold)` | LEI ≥ threshold (default 70) | bool |

| `isSafe(lei, threshold)` | LEI ≤ threshold (default 30) | bool |

| `crossedExhaustion(lei, threshold)` | Crossed into exhaustion | bool |

| `crossedSafe(lei, threshold)` | Crossed into safe zone | bool |

Utility Functions

| Function | Description | Returns |

|----------------------------|-------------------------|-----------|

| `getZone(lei)` | Zone name | string |

| `getColor(lei)` | Recommended color | color |

| `hasEnoughHistory()` | Data check | bool |

| `minBarsRequired()` | Required bars | int (50) |

| `version()` | Library version | string |

Interpretation Guide

| LEI Range | Zone | Meaning |

|-------------|--------------|--------------------------------------------------|

| 0-30 | Safe | Low exhaustion, move may continue |

| 30-50 | Caution | Moderate exhaustion |

| 50-70 | Warning | Elevated exhaustion |

| 70-100 | Exhaustion | High exhaustion, increased reversal risk |

Example: Basic Usage

//@version=6

indicator("LEI Example", overlay=false)

import OrenLuxy/LuxyEnergyIndex/1 as LEI

// Get LEI value

leiValue = LEI.lei()

// Plot with dynamic color

plot(leiValue, "LEI", LEI.getColor(leiValue), 2)

// Reference lines

hline(70, "High", color.red)

hline(30, "Low", color.green)

// Alert on exhaustion

if LEI.crossedExhaustion(leiValue) and barstate.isconfirmed

alert("LEI crossed into exhaustion zone")

Technical Details

Fixed Parameters (by design):

Velocity Period: 5 bars

Volume Period: 20 bars

Z-Score Period: 50 bars

ATR Period: 14

Extension/Velocity Weights: 50/50

Asset Support:

Stocks/Forex: Uses Session VWAP (daily reset)

Crypto: Uses Rolling VWAP (50-bar window) - auto-detected

Edge Cases:

Returns `na` until 50 bars of history

Zero volume: Volume modifier defaults to 1.0 (neutral)

Credits and Acknowledgments

This library builds upon established technical analysis concepts:

VWAP - Industry standard volume-weighted price measure

ATR by J. Welles Wilder Jr. (1978) - Volatility normalization

Z-Score - Statistical normalization method

Volume analysis principles from Volume Spread Analysis (VSA) methodology

Disclaimer

This library is provided for **educational and informational purposes only**. It does not constitute financial advice. Past performance does not guarantee future results. The exhaustion readings are probabilistic indicators, not guarantees of price reversal. Always conduct your own research and use proper risk management when trading.

Mirpapa_Lib_StructLibrary "Mirpapa_Lib_Struct"

ICT 구조 변화 감지 라이브러리 (BOS, CHoCH, MSS, Sweep)

initStructState()

StructState 초기화

checkBOS(_trend, _currentClose, _lastHHPrice, _lastLLPrice)

BOS 체크 (추세 지속) - 종가 기준

Parameters:

_trend (string) : 현재 추세

_currentClose (float) : 현재 종가

_lastHHPrice (float) : 마지막 HH 가격

_lastLLPrice (float) : 마지막 LL 가격

Returns:

checkCHoCH(_trend, _currentClose, _lastHHPrice, _lastLLPrice)

CHoCH 체크 (추세 전환) - 종가 기준

Parameters:

_trend (string) : 현재 추세

_currentClose (float) : 현재 종가

_lastHHPrice (float) : 마지막 HH 가격

_lastLLPrice (float) : 마지막 LL 가격

Returns:

checkSweep(_currentHigh, _currentLow, _currentClose, _lastHHPrice, _lastLLPrice)

Sweep 체크 (유동성 수집) 설명

Parameters:

_currentHigh (float) : 현재 고가

_currentLow (float) : 현재 저가

_currentClose (float) : 현재 종가

_lastHHPrice (float) : 마지막 HH 가격

_lastLLPrice (float) : 마지막 LL 가격

Returns:

checkMSS(_hadCHoCH, _chochDir, _currentHigh, _currentLow, _chochPrice)

MSS 체크 (CHoCH + 리테스트 확인)

Parameters:

_hadCHoCH (bool) : CHoCH 발생 여부

_chochDir (string) : CHoCH 방향

_currentHigh (float) : 현재 고가

_currentLow (float) : 현재 저가

_chochPrice (float) : CHoCH 발생 가격

Returns:

drawStructLabel(_price, _time, _type, _dir, _lblColor)

구조 변화 라벨 그리기

Parameters:

_price (float) : 가격

_time (int) : 시간

_type (string) : 구조 타입

_dir (string) : 방향

_lblColor (color) : 라벨 색상

drawStructLine(_price, _startTime, _endTime, _lineColor, _lineWidth)

구조 변화 라인 그리기

Parameters:

_price (float) : 가격

_startTime (int) : 시작 시간

_endTime (int) : 끝 시간

_lineColor (color) : 라인 색상

_lineWidth (int) : 라인 두께

StructType

구조 타입 상수

Fields:

BOS (series string)

CHOCH (series string)

MSS (series string)

SWEEP (series string)

TrendDir

추세 방향 상수

Fields:

UP (series string)

DOWN (series string)

NONE (series string)

StructState

구조 변화 상태

Fields:

_trend (series string) : 현재 추세 방향

_lastHHPrice (series float) : 마지막 HH 가격

_lastHHTime (series int) : 마지막 HH 시간

_lastLLPrice (series float) : 마지막 LL 가격

_lastLLTime (series int) : 마지막 LL 시간

_peakHHPrice (series float) : 최고 HH 가격 (BOS 레벨용)

_peakHHTime (series int) : 최고 HH 시간

_peakLLPrice (series float) : 최저 LL 가격 (BOS 레벨용)

_peakLLTime (series int) : 최저 LL 시간

_bosLevelHH (series float) : BOS 체크용 HH 레벨 (확정된 최고 HH)

_bosLevelHHTime (series int) : BOS 체크용 HH 시간

_bosLevelLL (series float) : BOS 체크용 LL 레벨 (확정된 최저 LL)

_bosLevelLLTime (series int) : BOS 체크용 LL 시간

KernelFunctionsLibrary "KernelFunctions"

This library provides non-repainting kernel functions for Nadaraya-Watson estimator implementations. This allows for easy substition/comparison of different kernel functions for one another in indicators. Furthermore, kernels can easily be combined with other kernels to create newer, more customized kernels.

rationalQuadratic(_src, _lookback, _relativeWeight, startAtBar)

Rational Quadratic Kernel - An infinite sum of Gaussian Kernels of different length scales.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_relativeWeight (simple float) : Relative weighting of time frames. Smaller values resut in a more stretched out curve and larger values will result in a more wiggly curve. As this value approaches zero, the longer time frames will exert more influence on the estimation. As this value approaches infinity, the behavior of the Rational Quadratic Kernel will become identical to the Gaussian kernel.

startAtBar (simple int)

Returns: yhat The estimated values according to the Rational Quadratic Kernel.

gaussian(_src, _lookback, startAtBar)

Gaussian Kernel - A weighted average of the source series. The weights are determined by the Radial Basis Function (RBF).

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

startAtBar (simple int)

Returns: yhat The estimated values according to the Gaussian Kernel.

periodic(_src, _lookback, _period, startAtBar)

Periodic Kernel - The periodic kernel (derived by David Mackay) allows one to model functions which repeat themselves exactly.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period (simple int) : The distance between repititions of the function.

startAtBar (simple int)

Returns: yhat The estimated values according to the Periodic Kernel.

locallyPeriodic(_src, _lookback, _period, startAtBar)

Locally Periodic Kernel - The locally periodic kernel is a periodic function that slowly varies with time. It is the product of the Periodic Kernel and the Gaussian Kernel.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period (simple int) : The distance between repititions of the function.

startAtBar (simple int)

Returns: yhat The estimated values according to the Locally Periodic Kernel.

MLExtensionsLibrary "MLExtensions"

A set of extension methods for a novel implementation of a Approximate Nearest Neighbors (ANN) algorithm in Lorentzian space.

normalizeDeriv(src, quadraticMeanLength)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src (float) : The input series (i.e., the first-order derivative for price).

quadraticMeanLength (int) : The length of the quadratic mean (RMS).

Returns: nDeriv The normalized derivative of the input series.

normalize(src, min, max)

Rescales a source value with an unbounded range to a target range.

Parameters:

src (float) : The input series

min (float) : The minimum value of the unbounded range

max (float) : The maximum value of the unbounded range

Returns: The normalized series

rescale(src, oldMin, oldMax, newMin, newMax)

Rescales a source value with a bounded range to anther bounded range

Parameters:

src (float) : The input series

oldMin (float) : The minimum value of the range to rescale from

oldMax (float) : The maximum value of the range to rescale from

newMin (float) : The minimum value of the range to rescale to

newMax (float) : The maximum value of the range to rescale to

Returns: The rescaled series

getColorShades(color)

Creates an array of colors with varying shades of the input color

Parameters:

color (color) : The color to create shades of

Returns: An array of colors with varying shades of the input color

getPredictionColor(prediction, neighborsCount, shadesArr)

Determines the color shade based on prediction percentile

Parameters:

prediction (float) : Value of the prediction

neighborsCount (int) : The number of neighbors used in a nearest neighbors classification

shadesArr (array) : An array of colors with varying shades of the input color

Returns: shade Color shade based on prediction percentile

color_green(prediction)

Assigns varying shades of the color green based on the KNN classification

Parameters:

prediction (float) : Value (int|float) of the prediction

Returns: color

color_red(prediction)

Assigns varying shades of the color red based on the KNN classification

Parameters:

prediction (float) : Value of the prediction

Returns: color

tanh(src)

Returns the the hyperbolic tangent of the input series. The sigmoid-like hyperbolic tangent function is used to compress the input to a value between -1 and 1.

Parameters:

src (float) : The input series (i.e., the normalized derivative).

Returns: tanh The hyperbolic tangent of the input series.

dualPoleFilter(src, lookback)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src (float) : The input series (i.e., the hyperbolic tangent).

lookback (int) : The lookback window for the smoothing.

Returns: filter The smoothed hyperbolic tangent of the input series.

tanhTransform(src, smoothingFrequency, quadraticMeanLength)

Returns the tanh transform of the input series.

Parameters:

src (float) : The input series (i.e., the result of the tanh calculation).

smoothingFrequency (int)

quadraticMeanLength (int)

Returns: signal The smoothed hyperbolic tangent transform of the input series.

n_rsi(src, n1, n2)

Returns the normalized RSI ideal for use in ML algorithms.

Parameters:

src (float) : The input series (i.e., the result of the RSI calculation).

n1 (simple int) : The length of the RSI.

n2 (simple int) : The smoothing length of the RSI.

Returns: signal The normalized RSI.

n_cci(src, n1, n2)

Returns the normalized CCI ideal for use in ML algorithms.

Parameters:

src (float) : The input series (i.e., the result of the CCI calculation).

n1 (simple int) : The length of the CCI.

n2 (simple int) : The smoothing length of the CCI.

Returns: signal The normalized CCI.

n_wt(src, n1, n2)

Returns the normalized WaveTrend Classic series ideal for use in ML algorithms.

Parameters:

src (float) : The input series (i.e., the result of the WaveTrend Classic calculation).

n1 (simple int)

n2 (simple int)

Returns: signal The normalized WaveTrend Classic series.

n_adx(highSrc, lowSrc, closeSrc, n1)

Returns the normalized ADX ideal for use in ML algorithms.

Parameters:

highSrc (float) : The input series for the high price.

lowSrc (float) : The input series for the low price.

closeSrc (float) : The input series for the close price.

n1 (simple int) : The length of the ADX.

regime_filter(src, threshold, useRegimeFilter)

Parameters:

src (float)

threshold (float)

useRegimeFilter (bool)

filter_adx(src, length, adxThreshold, useAdxFilter)

filter_adx

Parameters:

src (float) : The source series.

length (simple int) : The length of the ADX.

adxThreshold (int) : The ADX threshold.

useAdxFilter (bool) : Whether to use the ADX filter.

Returns: The ADX.

filter_volatility(minLength, maxLength, useVolatilityFilter)

filter_volatility

Parameters:

minLength (simple int) : The minimum length of the ATR.

maxLength (simple int) : The maximum length of the ATR.

useVolatilityFilter (bool) : Whether to use the volatility filter.

Returns: Boolean indicating whether or not to let the signal pass through the filter.

backtest(high, low, open, startLongTrade, endLongTrade, startShortTrade, endShortTrade, isEarlySignalFlip, maxBarsBackIndex, thisBarIndex, src, useWorstCase)

Performs a basic backtest using the specified parameters and conditions.

Parameters:

high (float) : The input series for the high price.

low (float) : The input series for the low price.

open (float) : The input series for the open price.

startLongTrade (bool) : The series of conditions that indicate the start of a long trade.

endLongTrade (bool) : The series of conditions that indicate the end of a long trade.

startShortTrade (bool) : The series of conditions that indicate the start of a short trade.

endShortTrade (bool) : The series of conditions that indicate the end of a short trade.

isEarlySignalFlip (bool) : Whether or not the signal flip is early.

maxBarsBackIndex (int) : The maximum number of bars to go back in the backtest.

thisBarIndex (int) : The current bar index.

src (float) : The source series.

useWorstCase (bool) : Whether to use the worst case scenario for the backtest.

Returns: A tuple containing backtest values

init_table()

init_table()

Returns: tbl The backtest results.

update_table(tbl, tradeStatsHeader, totalTrades, totalWins, totalLosses, winLossRatio, winrate, earlySignalFlips)

update_table(tbl, tradeStats)

Parameters:

tbl (table) : The backtest results table.

tradeStatsHeader (string) : The trade stats header.

totalTrades (float) : The total number of trades.

totalWins (float) : The total number of wins.

totalLosses (float) : The total number of losses.

winLossRatio (float) : The win loss ratio.

winrate (float) : The winrate.

earlySignalFlips (float) : The total number of early signal flips.

Returns: Updated backtest results table.

Mirpapa_Lib_UnicornLibrary "Mirpapa_Lib_Unicorn"

유니콘 패턴 라이브러리 (Unicorn Pattern Library)

유니콘 모델 전략 로직, 데이터 구조체 및 상태 관리를 구현합니다.

initUnicornData(_isBull, _createTime, _createBar, _timeframe)

UnicornData 초기화

@description 새로운 UnicornData 객체를 생성하고 초기화합니다.

Parameters:

_isBull (bool) : 방향 (True: 상승, False: 하락)

_createTime (int) : 생성 시간

_createBar (int) : 생성 Bar Index

_timeframe (string) : 시간대

calculateOverlap(_obTop, _obBot, _fvgTop, _fvgBot)

중첩 영역(Overlap Zone) 계산

@description OB와 FVG 사이의 겹치는 영역을 계산합니다.

Parameters:

_obTop (float) : OB 상단

_obBot (float) : OB 하단

_fvgTop (float) : FVG 상단

_fvgBot (float) : FVG 하단

Returns: 겹침 영역 상단, 하단, 겹침 여부

updateUnicornStatus(_data, _currentHigh, _currentLow, _time)

유니콘 상태 업데이트

@description 가격 움직임에 따라 유니콘 패턴의 상태를 업데이트합니다.

active: 진입 대기 (리테스트 대기) -> triggered: 진입 (TP/SL 대기) -> win/loss: 결과 확정

Parameters:

_data (UnicornData) : UnicornData 객체

_currentHigh (float) : 현재 고가

_currentLow (float) : 현재 저가

_time (int) : 현재 시간

Returns: UnicornData 업데이트된 객체

activateUnicorn(_data)

유니콘 활성화 (Active 전환)

@description Pending 상태인 유니콘 데이터를 Active 상태로 전환합니다. (보통 CHoCH 발생 시 호출)

Parameters:

_data (UnicornData) : UnicornData 객체

setTradeLevels(_data, _entry, _stop, _target)

트레이딩 레벨 설정

@description 진입가, 목표가, 손절가를 설정합니다.

Parameters:

_data (UnicornData) : UnicornData 객체

_entry (float) : 진입가

_stop (float) : 손절가

_target (float) : 목표가

UnicornData

유니콘 데이터 (UnicornData)

Fields:

_isBull (series bool) : // 상승/하락 방향 (True: Long, False: Short)

_status (series string) : // "pending", "active", "triggered", "win", "loss", "cancelled"

_createTime (series int) : // 생성 시간

_createBar (series int) : // 생성 bar_index

_obTop (series float) : // OB 상단

_obBot (series float) : // OB 하단

_obTime (series int) : // OB 캔들 시간

_obBox (series box) : // OB 박스 객체

_fvgTop (series float) : // FVG 상단

_fvgBot (series float) : // FVG 하단

_fvgTime (series int) : // FVG 시간

_fvgBox (series box) : // FVG 박스 객체

_zoneTop (series float) : // 겹침 영역 상단 (Unicorn Zone)

_zoneBot (series float) : // 겹침 영역 하단 (Unicorn Zone)

_zoneBox (series box) : // Unicorn Zone 박스 객체

_chochConfirmed (series bool) : // CHoCH 확정 여부

_chochTime (series int) : // CHoCH 발생 시간

_chochPrice (series float) : // CHoCH 돌파 가격

_entryPrice (series float) : // 진입가

_targetPrice (series float) : // 목표가 (다음 유동성 레벨)

_stopPrice (series float) : // 손절가 (Zone 반대편)

_result (series string) : // "none", "win", "loss"

_resultTime (series int) : // 결과 확정 시간

_resultPrice (series float) : // 결과 확정 가격

_profitPips (series float) : // 수익 pips (양수)

_lossPips (series float) : // 손실 pips (음수)

_profitPercent (series float) : // 수익 %

_lossPercent (series float) : // 손실 %

_rrRatio (series float) : // Risk:Reward 비율

_timeframe (series string) : // 시간대 (HTF/MTF/CTF)

_triggerTime (series int) : // 진입 트리거 시간 (리테스트)

_triggerPrice (series float) : // 진입 트리거 가격

_isRetested (series bool) : // 리테스트 여부

_retestCount (series int) : // 리테스트 횟수

_maxDrawdown (series float) : // 최대 손실폭 (진입 후)

_maxProfit (series float) : // 최대 수익폭 (진입 후)

machine_learningLibrary "machine_learning"

euclidean(a, b)

Parameters:

a (array)

b (array)

manhattan(a, b)

Parameters:

a (array)

b (array)

cosine_similarity(a, b)

Parameters:

a (array)

b (array)

cosine_distance(a, b)

Parameters:

a (array)

b (array)

chebyshev(a, b)

Parameters:

a (array)

b (array)

minkowski(a, b, p)

Parameters:

a (array)

b (array)

p (float)

dot_product(a, b)

Parameters:

a (array)

b (array)

vector_norm(arr, p)

Parameters:

arr (array)

p (float)

sigmoid(x)

Parameters:

x (float)

sigmoid_derivative(x)

Parameters:

x (float)

tanh_derivative(x)

Parameters:

x (float)

relu(x)

Parameters:

x (float)

relu_derivative(x)

Parameters:

x (float)

leaky_relu(x, alpha)

Parameters:

x (float)

alpha (float)

leaky_relu_derivative(x, alpha)

Parameters:

x (float)

alpha (float)

elu(x, alpha)

Parameters:

x (float)

alpha (float)

gelu(x)

Parameters:

x (float)

swish(x, beta)

Parameters:

x (float)

beta (float)

softmax(arr)

Parameters:

arr (array)

apply_activation(arr, activation_type, alpha)

Parameters:

arr (array)

activation_type (string)

alpha (float)

normalize_minmax(arr, min_val, max_val)

Parameters:

arr (array)

min_val (float)

max_val (float)

normalize_zscore(arr, mean_val, std_val)

Parameters:

arr (array)

mean_val (float)

std_val (float)

normalize_matrix_cols(m)

Parameters:

m (matrix)

scaler_fit(arr, method)

Parameters:

arr (array)

method (string)

scaler_fit_matrix(m, method)

Parameters:

m (matrix)

method (string)

scaler_transform(scaler, arr)

Parameters:

scaler (ml_scaler)

arr (array)

scaler_transform_matrix(scaler, m)

Parameters:

scaler (ml_scaler)

m (matrix)

clip(x, lo, hi)

Parameters:

x (float)

lo (float)

hi (float)

clip_array(arr, lo, hi)

Parameters:

arr (array)

lo (float)

hi (float)

loss_mse(predicted, actual)

Parameters:

predicted (array)

actual (array)

loss_rmse(predicted, actual)

Parameters:

predicted (array)

actual (array)

loss_mae(predicted, actual)

Parameters:

predicted (array)

actual (array)

loss_binary_crossentropy(predicted, actual)

Parameters:

predicted (array)

actual (array)

loss_huber(predicted, actual, delta)

Parameters:

predicted (array)

actual (array)

delta (float)

gradient_step(weights, gradients, lr)

Parameters:

weights (array)

gradients (array)

lr (float)

adam_step(weights, gradients, m, v, lr, beta1, beta2, t, epsilon)

Parameters:

weights (array)

gradients (array)

m (array)

v (array)

lr (float)

beta1 (float)

beta2 (float)

t (int)

epsilon (float)

clip_gradients(gradients, max_norm)

Parameters:

gradients (array)

max_norm (float)

lr_decay(initial_lr, decay_rate, step)

Parameters:

initial_lr (float)

decay_rate (float)

step (int)

lr_cosine_annealing(initial_lr, min_lr, step, total_steps)

Parameters:

initial_lr (float)

min_lr (float)

step (int)

total_steps (int)

knn_create(k, distance_type)

Parameters:

k (int)

distance_type (string)

knn_fit(model, X, y)

Parameters:

model (ml_knn)

X (matrix)

y (array)

knn_predict(model, x)

Parameters:

model (ml_knn)

x (array)

knn_predict_proba(model, x)

Parameters:

model (ml_knn)

x (array)

knn_batch_predict(model, X)

Parameters:

model (ml_knn)

X (matrix)

linreg_fit(X, y)

Parameters:

X (matrix)

y (array)

ridge_fit(X, y, lambda)

Parameters:

X (matrix)

y (array)

lambda (float)

linreg_predict(model, x)

Parameters:

model (ml_linreg)

x (array)

linreg_predict_batch(model, X)

Parameters:

model (ml_linreg)

X (matrix)

linreg_score(model, X, y)

Parameters:

model (ml_linreg)

X (matrix)

y (array)

logreg_create(n_features, learning_rate, iterations)

Parameters:

n_features (int)

learning_rate (float)

iterations (int)

logreg_fit(model, X, y)

Parameters:

model (ml_logreg)

X (matrix)

y (array)

logreg_predict_proba(model, x)

Parameters:

model (ml_logreg)

x (array)

logreg_predict(model, x, threshold)

Parameters:

model (ml_logreg)

x (array)

threshold (float)

logreg_batch_predict(model, X, threshold)

Parameters:

model (ml_logreg)

X (matrix)

threshold (float)

nb_create(n_classes)

Parameters:

n_classes (int)

nb_fit(model, X, y)

Parameters:

model (ml_nb)

X (matrix)

y (array)

nb_predict_proba(model, x)

Parameters:

model (ml_nb)

x (array)

nb_predict(model, x)

Parameters:

model (ml_nb)

x (array)

nn_create(layers, activation)

Parameters:

layers (array)

activation (string)

nn_forward(model, x)

Parameters:

model (ml_nn)

x (array)

nn_predict_class(model, x)

Parameters:

model (ml_nn)

x (array)

accuracy(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

precision(y_true, y_pred, positive_class)

Parameters:

y_true (array)

y_pred (array)

positive_class (int)

recall(y_true, y_pred, positive_class)

Parameters:

y_true (array)

y_pred (array)

positive_class (int)

f1_score(y_true, y_pred, positive_class)

Parameters:

y_true (array)

y_pred (array)

positive_class (int)

r_squared(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

mse(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

rmse(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

mae(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

confusion_matrix(y_true, y_pred, n_classes)

Parameters:

y_true (array)

y_pred (array)

n_classes (int)

sliding_window(data, window_size)

Parameters:

data (array)

window_size (int)

train_test_split(X, y, test_ratio)

Parameters:

X (matrix)

y (array)

test_ratio (float)

create_binary_labels(data, threshold)

Parameters:

data (array)

threshold (float)

lag_matrix(data, n_lags)

Parameters:

data (array)

n_lags (int)

signal_to_position(prediction, threshold_long, threshold_short)

Parameters:

prediction (float)

threshold_long (float)

threshold_short (float)

confidence_sizing(probability, max_size, min_confidence)

Parameters:

probability (float)

max_size (float)

min_confidence (float)

kelly_sizing(win_rate, avg_win, avg_loss, max_fraction)

Parameters:

win_rate (float)

avg_win (float)

avg_loss (float)

max_fraction (float)

sharpe_ratio(returns, risk_free_rate)

Parameters:

returns (array)

risk_free_rate (float)

sortino_ratio(returns, risk_free_rate)

Parameters:

returns (array)

risk_free_rate (float)

max_drawdown(equity)

Parameters:

equity (array)

atr_stop_loss(entry_price, atr, multiplier, is_long)

Parameters:

entry_price (float)

atr (float)

multiplier (float)

is_long (bool)

risk_reward_take_profit(entry_price, stop_loss, ratio)

Parameters:

entry_price (float)

stop_loss (float)

ratio (float)

ensemble_vote(predictions)

Parameters:

predictions (array)

ensemble_weighted_average(predictions, weights)

Parameters:

predictions (array)

weights (array)

smooth_prediction(current, previous, alpha)

Parameters:

current (float)

previous (float)

alpha (float)

regime_classifier(volatility, trend_strength, vol_threshold, trend_threshold)

Parameters:

volatility (float)

trend_strength (float)

vol_threshold (float)

trend_threshold (float)

ml_knn

Fields:

k (series int)

distance_type (series string)

X_train (matrix)

y_train (array)

ml_linreg

Fields:

coefficients (array)

intercept (series float)

lambda (series float)

ml_logreg

Fields:

weights (array)

bias (series float)

learning_rate (series float)

iterations (series int)

ml_nn

Fields:

layers (array)

weights (matrix)

biases (array)

weight_offsets (array)

bias_offsets (array)

activation (series string)

ml_nb

Fields:

class_priors (array)

means (matrix)

variances (matrix)

n_classes (series int)

ml_scaler

Fields:

min_vals (array)

max_vals (array)

means (array)

stds (array)

method (series string)

ml_train_result

Fields:

loss_history (array)

final_loss (series float)

converged (series bool)

iterations_run (series int)

ml_prediction

Fields:

class_label (series int)

probability (series float)

probabilities (array)

value (series float)

Mirpapa_Lib_StructsLibrary "Mirpapa_Lib_Structs"

ICT 구조 변화 감지 라이브러리 (BOS, CHoCH, MSS, Sweep)

initStructState()

StructState 초기화

checkBOS(_trend, _currentClose, _lastHHPrice, _lastLLPrice)

BOS 체크 (추세 지속) - 종가 기준

Parameters:

_trend (string) : 현재 추세

_currentClose (float) : 현재 종가

_lastHHPrice (float) : 마지막 HH 가격

_lastLLPrice (float) : 마지막 LL 가격

Returns:

checkCHoCH(_trend, _currentClose, _lastHHPrice, _lastLLPrice)

CHoCH 체크 (추세 전환) - 종가 기준

Parameters:

_trend (string) : 현재 추세

_currentClose (float) : 현재 종가

_lastHHPrice (float) : 마지막 HH 가격

_lastLLPrice (float) : 마지막 LL 가격

Returns:

checkSweep(_currentHigh, _currentLow, _currentClose, _lastHHPrice, _lastLLPrice)

Sweep 체크 (유동성 수집)

Parameters:

_currentHigh (float) : 현재 고가

_currentLow (float) : 현재 저가

_currentClose (float) : 현재 종가

_lastHHPrice (float) : 마지막 HH 가격

_lastLLPrice (float) : 마지막 LL 가격

Returns:

checkMSS(_hadCHoCH, _chochDir, _currentHigh, _currentLow, _chochPrice)

MSS 체크 (CHoCH + 리테스트 확인)

Parameters:

_hadCHoCH (bool) : CHoCH 발생 여부

_chochDir (string) : CHoCH 방향

_currentHigh (float) : 현재 고가

_currentLow (float) : 현재 저가

_chochPrice (float) : CHoCH 발생 가격

Returns:

drawStructLabel(_price, _time, _type, _dir, _lblColor)

구조 변화 라벨 그리기

Parameters:

_price (float) : 가격

_time (int) : 시간

_type (string) : 구조 타입

_dir (string) : 방향

_lblColor (color) : 라벨 색상

drawStructLine(_price, _startTime, _endTime, _lineColor, _lineWidth)

구조 변화 라인 그리기

Parameters:

_price (float) : 가격

_startTime (int) : 시작 시간

_endTime (int) : 끝 시간

_lineColor (color) : 라인 색상

_lineWidth (int) : 라인 두께

StructType

구조 타입 상수

Fields:

BOS (series string)

CHOCH (series string)

MSS (series string)

SWEEP (series string)

TrendDir

추세 방향 상수

Fields:

UP (series string)

DOWN (series string)

NONE (series string)

StructState

구조 변화 상태

Fields:

_trend (series string) : 현재 추세 방향

_lastHHPrice (series float) : 마지막 HH 가격

_lastHHTime (series int) : 마지막 HH 시간

_lastLLPrice (series float) : 마지막 LL 가격

_lastLLTime (series int) : 마지막 LL 시간

CEDEARDataLibrary "CEDEARData"

getUnderlying(cedearTicker)

Parameters:

cedearTicker (simple string)

getRatio(cedearTicker)

Parameters:

cedearTicker (simple string)

getCurrency(cedearTicker)

Parameters:

cedearTicker (simple string)

isValidCedear(cedearTicker)

Parameters:

cedearTicker (simple string)

ZigZagCoreZigZagCore

ZigZagCore is a generic ZigZag engine that works with any user-defined threshold (ATR-based, volatility-based, fixed ticks, etc.).

API

import ReflexSignals/ZigZagCore/ as zz

var zz.ZzState state = zz.zz_new()

float thr = ... // your threshold in price units

state := zz.zz_update(state, thr)

zz_update(state, thr)

Parameters:

state (ZzState)

thr (float)

ZzState

Fields:

dir (series int)

highSinceLow (series float)

lowSinceHigh (series float)

lastHighLevel (series float)

lastLowLevel (series float)

lastHighIndex (series int)

lastLowIndex (series int)

highSinceLowIndex (series int)

lowSinceHighIndex (series int)

isNewHigh (series bool)

isNewLow (series bool)

Directional State

dir = 1 → market is in an upswing

dir = -1 → market is in a downswing

dir = na → initial undecided state

Live Swing Tracking (Unconfirmed Leg)

Continuously updated swing extremes:

highSinceLow — highest price since the last confirmed low

lowSinceHigh — lowest price since the last confirmed high

Their corresponding bar indices

These fields describe the current active swing leg, which updates every bar until a pivot is confirmed.

Pivot Detection

A pivot confirms only when price moves beyond the prior swing extreme by more than threshold. When this occurs, the library sets:

isNewHigh = true (on the detection bar only) and updates lastHighLevel, lastHighIndex

isNewLow = true and updates lastLowLevel, lastLowIndex

Mirpapa_Lib_LineLibrary "Mirpapa_Lib_Line"

CreateLine(_breachMode, _isBull, _leftTime, _rightTime, _price, _lineColor, _lineWidth, _lineStyle, _text)

CreateLine

@description 라인 생성 (값 전달 방식 - 모든 좌표 직접 지정).\

호출자가 모든 좌표와 시간을 계산하여 전달.\

breachMode: "price"(고가/저가 돌파) 또는 "close"(종가 돌파).\

Parameters:

_breachMode (string) : 돌파 처리 방식: "price" 또는 "close"

_isBull (bool) : 상승(true) 또는 하락(false)

_leftTime (int) : 라인 시작 시간

_rightTime (int) : 라인 종료 시간

_price (float) : 라인 가격

_lineColor (color) : 라인 색상

_lineWidth (int) : 라인 두께

_lineStyle (string) : 라인 스타일 (line.style_solid, line.style_dashed 등)

_text (string) : 라인 텍스트

Returns: 성공 여부와 라인 데이터

ProcessLineDatas(_openLines, _closedLines, _closeCount, _colorClose, _currentBarIndex, _currentLow, _currentHigh, _currentTime)

ProcessLineDatas

@description 라인 확장 및 돌파 처리.\

열린 라인들을 현재 bar까지 확장하고, 돌파 조건 체크.\

_closeCount: 돌파 횟수 (이 횟수만큼 돌파 시 라인 종료).\

breachMode에 따라 돌파 체크 방식 다름 (price/close).\

종료된 라인은 _closedLines로 이동하고 _colorClose 색상 적용.\

barstate.islast와 barstate.isconfirmed에서 호출 권장.

Parameters:

_openLines (array) : 열린 라인 배열

_closedLines (array) : 닫힌 라인 배열

_closeCount (int) : 돌파 카운트 (이 횟수만큼 돌파 시 종료)

_colorClose (color) : 종료된 라인 색상

_currentBarIndex (int) : 현재 bar_index

_currentLow (float) : 현재 low

_currentHigh (float) : 현재 high

_currentTime (int) : 현재 time

Returns: bool 항상 true

BreachMode

BreachMode

Fields:

PRICE (series string)

CLOSE (series string)

LineData

LineData

Fields:

_breachMode (series string) : 돌파 처리 방식

_isBull (series bool) : 상승(true) 또는 하락(false) 방향

_line (series line) : 라인 객체

_price (series float) : 라인 가격

_text (series string) : 라인 텍스트

_breached (series bool) : 돌파 여부

_breakCount (series int) : 돌파 카운트

M20M60_win10_libLibrary "M20M60_win10_lib"

f_m20m60_win10_features(srcOpen, srcHigh, srcLow, srcClose, bandCenter, bandWidth)

Parameters:

srcOpen (float)

srcHigh (float)

srcLow (float)

srcClose (float)

bandCenter (float)

bandWidth (float)

f_m20m60_win10_is_cluster5(bodyMean, rangeMean, cBandDiff, insideRatio, maxAbove)

Parameters:

bodyMean (float)

rangeMean (float)

cBandDiff (float)

insideRatio (float)

maxAbove (float)

f_m20m60_win10_is_cluster1(bodyMean, rangeMean, cBandDiff, insideRatio, maxAbove)

Parameters:

bodyMean (float)

rangeMean (float)

cBandDiff (float)

insideRatio (float)

maxAbove (float)

LibBarLibBar is a lightweight and practical Pine Script library designed to simplify candlestick analysis.

It provides a set of helper functions for identifying candle type, measuring body and wick sizes, and evaluating candle structure.

Perfect for building indicators, pattern detectors, or any script that relies on detailed bar-level analysis.

Available Functions

isBull(index) - Returns true if the bar is bullish.

isBear(index) - Returns true if the bar is bearish.

getBody(index) - Returns the candle’s body size.

getUpperWick(index) - Returns the size of the upper wick.

getLowerWick(index) - Returns the size of the lower wick.

getSize(index) - Returns the total candle size (high − low).

getBodyPercentage(index) - Returns the body size as a percentage of total candle size.

getUpperWickPercentage(index) - Returns the upper wick size as a percentage of the candle.

getLowerWickPercentage(index) - Returns the lower wick size as a percentage of the candle.

Mirpapa_Lib_HTFLibrary "Mirpapa_Lib_HTF"

High Time Frame Handler Library:

Provides utilities for working with High Time Frame (HTF) and chart (LTF) conversions and data retrieval.

IsChartTFcomparisonHTF(_chartTf, _htfTf)

IsChartTFcomparisonHTF

@description

Determine whether the given High Time Frame (HTF) is greater than or equal to the current chart timeframe.

Parameters:

_chartTf (string) : The current chart’s timeframe string (examples: "5", "15", "1D").

_htfTf (string) : The High Time Frame string to compare (examples: "60", "1D").

@return

Returns true if HTF minutes ≥ chart minutes, false otherwise or na if conversion fails.

GetHTFrevised(_tf)

GetHTFrevised

@description

Retrieve a specific bar value from a Higher Time Frame (HTF) series.

Supports current and historical OHLC values, based on a case identifier.

Parameters:

_tf (string) : The target HTF string (examples: "60", "1D").

GetHTFrevised(_tf, _case)

Parameters:

_tf (string)

_case (string)

GetHTFfromLabel(_label)

GetHTFfromLabel

@description

Convert a Korean HTF label into a Pine Script-recognizable timeframe string.

Examples:

"5분" → "5"

"1시간" → "60"

"일봉" → "1D"

"주봉" → "1W"

"월봉" → "1M"

"연봉" → "12M"

Parameters:

_label (string) : The Korean HTF label string (examples: "5분", "1시간", "일봉").

@return

Returns the Pine Script timeframe string corresponding to the label, or "1W" if no match is found.

GetHTFoffsetToLTFoffset(_offset, _chartTf, _htfTf)

GetHTFoffsetToLTFoffset

@description

Adjust an HTF bar index and offset so that it aligns with the current chart’s bar index.

Useful for retrieving historical HTF data on an LTF chart.

Parameters:

_offset (int) : The HTF bar offset (0 means current HTF bar, 1 means one bar ago, etc.).

_chartTf (string) : The current chart’s timeframe string (examples: "5", "15", "1D").

_htfTf (string) : The High Time Frame string to align (examples: "60", "1D").

@return

Returns the corresponding LTF bar index after applying HTF offset. If result is negative, returns 0.

UpdateHTFCache(_cache, _tf)

UpdateHTFCache

@description HTF 데이터 캐싱 (성능 최적화).\

HTF의 OHLC 데이터를 캐싱하여 매 틱마다 request.security 호출 방지.\

_cache: 기존 캐시 (없으면 na, 첫 호출 시).\

_tf: 캐싱할 시간대 (예: "60", "1D").\

새 bar 또는 bar_index 변경 시에만 업데이트, 그 외에는 기존 캐시 반환.\

Parameters:

_cache (HTFCache) : 기존 캐시 데이터 (없으면 na)

_tf (string) : 시간대

Returns: HTFCache 업데이트된 캐시 데이터

GetTimeframeSettings(_currentTF, _midTF1m, _highTF1m, _midTF5m, _highTF5m, _midTF15m, _highTF15m, _midTF30m, _highTF30m, _midTF60m, _highTF60m, _midTF240m, _highTF240m, _midTF1D, _highTF1D, _midTF1W, _highTF1W, _midTF1M, _highTF1M)

GetTimeframeSettings

@description 현재 차트 시간대에 맞는 중위/상위 시간대 자동 선택.\

_currentTF: 현재 차트 시간대 (timeframe.period).\

1분~1월 차트별로 적절한 중위/상위 시간대 매핑.\

예: 5분 차트 → 중위 15분, 상위 60분.\

반환: .\

Parameters:

_currentTF (string) : 현재 차트 시간대

_midTF1m (string)

_highTF1m (string)

_midTF5m (string)

_highTF5m (string)

_midTF15m (string)

_highTF15m (string)

_midTF30m (string)

_highTF30m (string)

_midTF60m (string)

_highTF60m (string)

_midTF240m (string)

_highTF240m (string)

_midTF1D (string)

_highTF1D (string)

_midTF1W (string)

_highTF1W (string)

_midTF1M (string)

_highTF1M (string)

Returns:

HTFCache

Fields:

_timeframe (series string)

_lastBarIndex (series int)

_isNewBar (series bool)

_barIndex (series int)

_open (series float)

_high (series float)

_low (series float)

_close (series float)

_open1 (series float)

_close1 (series float)

_high1 (series float)

_low1 (series float)

_open2 (series float)

_close2 (series float)

_high2 (series float)

_low2 (series float)

_high3 (series float)

_low3 (series float)

_time1 (series int)

_time2 (series int)

MirPapa_Lib_BoxLibrary "MirPapa_Lib_Box"

GetHTFrevised(_tf, _case)

GetHTFrevised

@description Retrieve a specific bar value from a Higher Time Frame (HTF) series.

Parameters:

_tf (string) : string The target HTF string (examples: "60", "1D").

_case (string) : string Case string determining which OHLC value to request.

@return float Returns the requested HTF value or na if _case does not match.

GetHTFrevised(_tf)

Parameters:

_tf (string)

GetHTFoffsetToLTFoffset(_offset, _chartTf, _htfTf)

GetHTFoffsetToLTFoffset

@description Adjust an HTF offset to an LTF offset by calculating the ratio of timeframes.

Parameters:

_offset (int) : int The HTF bar offset (0 means current HTF bar).

_chartTf (string) : string The current chart's timeframe (e.g., "5", "15", "1D").

_htfTf (string) : string The High Time Frame string (e.g., "60", "1D").

@return int The corresponding LTF bar index. Returns 0 if the result is negative.

GetHtfFromLabel(_label)

GetHtfFromLabel

@description Convert a Korean HTF label into a Pine Script timeframe string.

Parameters:

_label (string) : string The Korean label (e.g., "5분", "1시간").

@return string Returns the corresponding Pine Script timeframe (e.g., "5", "60").

IsChartTFcomparisonHTF(_chartTf, _htfTf)

IsChartTFcomparisonHTF

@description Determine whether a given HTF is greater than or equal to the current chart timeframe.

Parameters:

_chartTf (string) : string Current chart timeframe (e.g., "5", "15", "1D").

_htfTf (string) : string HTF timeframe (e.g., "60", "1D").

@return bool True if HTF ≥ chartTF, false otherwise.

IsCondition(_boxType, _isBull, _pricePrev, _priceNow)

IsCondition

@description FOB, FVG 조건 체크.\

_boxType: "fob"(Fair Order Block) 또는 "fvg"(Fair Value Gap).\

_isBull: true(상승 패턴), false(하락 패턴).\

상승 시 현재 가격이 이전 가격보다 높으면 true, 하락 시 이전 가격이 현재 가격보다 높으면 true 반환.

Parameters:

_boxType (string) : 박스 타입 ("fob", "fvg")

_isBull (bool) : 상승(true) 또는 하락(false)

_pricePrev (float) : 이전 가격

_priceNow (float) : 현재 가격

Returns: bool 조건 만족 여부

IsCondition(_boxType, _high2, _high1, _high0, _low2, _low1, _low0)

IsCondition

@description Sweep 조건 체크 (Swing High/Low 동시 발생).\

_boxType: "sweep" 또는 "breachBoth".\

조건: high2 < high1 > high0 (Swing High) AND low2 > low1 < low0 (Swing Low).\

중간 캔들이 양쪽보다 높고 낮은 지점을 동시에 형성할 때 true 반환.

Parameters:

_boxType (string) : 박스 타입 ("sweep", "breachBoth")

_high2 (float)

_high1 (float)

_high0 (float)

_low2 (float)

_low1 (float)

_low0 (float)

Returns: bool 조건 만족 여부

IsCondition(_boxType, _isBull, _open1, _close1, _high1, _low1, _open0, _close0, _low2, _low3, _high2, _high3)

IsCondition

@description RB (Rejection Block) 조건 체크.\

_boxType: "rb" (Rejection Block).\

상승 RB: candle1=음봉, candle0=양봉, low3>low1 AND low2>low1, close1*1.001>open0, open1close0.\

이전 캔들의 거부 후 현재 캔들이 반대 방향으로 전환될 때 true 반환.

Parameters:

_boxType (string) : 박스 타입 ("rb")

_isBull (bool) : 상승(true) 또는 하락(false)

_open1 (float)

_close1 (float)

_high1 (float)

_low1 (float)

_open0 (float)

_close0 (float)

_low2 (float)

_low3 (float)

_high2 (float)

_high3 (float)

Returns: bool 조건 만족 여부

IsCondition(_boxType, _isBull, _open2, _close1, _open1, _close0)

IsCondition

@description SOB (Strong Order Block) 조건 체크.\

_boxType: "sob" (Strong Order Block).\

상승 SOB: 양봉2 => 음봉1 => 양봉0, open2 > close1 AND open1 < close0.\

하락 SOB: 음봉2 => 양봉1 => 음봉0, open2 < close1 AND open1 > close0.\

3개 캔들 패턴으로 강한 주문 블록 형성 시 true 반환.

Parameters:

_boxType (string) : 박스 타입 ("sob")

_isBull (bool) : 상승(true) 또는 하락(false)

_open2 (float) : 2개 이전 캔들 open

_close1 (float) : 1개 이전 캔들 close

_open1 (float) : 1개 이전 캔들 open

_close0 (float) : 현재 캔들 close

Returns: bool 조건 만족 여부

CreateBox(_boxType, _tf, _isBull, _useLine, _colorBG, _colorBD, _colorText, _cache)

CreateBox

@description 박스 생성 (breachMode 자동 결정).\

_boxType: "fob", "rb", "custom" → directionalHighLow, 나머지 → both.\

_tf: 시간대 (timeframe.period 또는 HTF).\

_isBull: true(상승 박스), false(하락 박스).\

_cache: HTF 사용 시 필수, CurrentTF는 na.\

반환: .

Parameters:

_boxType (string) : 박스 타입

_tf (string) : 시간대

_isBull (bool) : 상승(true) 또는 하락(false)

_useLine (bool) : 중간선 표시 여부

_colorBG (color) : 박스 배경색

_colorBD (color) : 박스 테두리색

_colorText (color) : 텍스트 색상

_cache (HTFCache) : HTF 캐시 데이터

Returns: 성공 여부와 박스 데이터

CreateBox(_boxType, _tf, _isBull, _useLine, _colorBG, _colorBD, _colorText, _cache, _customText)

CreateBox

@description 박스 생성 (커스텀 텍스트 지원, breachMode 자동 결정).\

_boxType: "fob", "rb", "custom" → directionalHighLow, 나머지 → both.\

_customText: 박스에 표시할 텍스트 (비어있으면 "시간대 박스타입" 형식으로 자동 생성).\

_isBull: true(상승 박스), false(하락 박스).\

반환: .

Parameters:

_boxType (string) : 박스 타입

_tf (string) : 시간대

_isBull (bool) : 상승(true) 또는 하락(false)

_useLine (bool) : 중간선 표시 여부

_colorBG (color) : 박스 배경색

_colorBD (color) : 박스 테두리색

_colorText (color) : 텍스트 색상

_cache (HTFCache) : HTF 캐시 데이터

_customText (string) : 커스텀 텍스트

Returns: 성공 여부와 박스 데이터

CreateBox(_boxType, _breachMode, _tf, _isBull, _useLine, _colorBG, _colorBD, _colorText, _cache, _customText)

CreateBox

@description 박스 생성 (breachMode 명시적 지정).\

_breachMode: "both"(양쪽 모두 돌파), "directionalHighLow"(방향성 high/low 돌파), "directionalClose"(방향성 close 돌파).\

_isBull: true(상승 박스), false(하락 박스).\

_customText: 박스에 표시할 텍스트 (비어있으면 "시간대 박스타입" 형식으로 자동 생성).\

반환: .

Parameters:

_boxType (string) : 박스 타입 (fob, fvg, sweep, rb, custom 등)

_breachMode (string) : 돌파 처리 방식: "both" (양쪽 모두), "directionalHighLow" (방향성 high/low), "directionalClose" (방향성 close)

_tf (string) : 시간대

_isBull (bool) : 상승(true) 또는 하락(false) 방향

_useLine (bool) : 중간선 표시 여부

_colorBG (color) : 박스 배경색

_colorBD (color) : 박스 테두리색

_colorText (color) : 텍스트 색상

_cache (HTFCache) : HTF 캐시 데이터 (CurrentTF는 na)

_customText (string) : 커스텀 텍스트 (비어있으면 자동 생성)

Returns: 성공 여부와 박스 데이터

CreateCustomBox(_boxType, _breachMode, _isBull, _top, _bottom, _left, _right, _useLine, _colorBG, _colorBD, _colorText, _text)

CreateCustomBox

@description 완전히 유연한 커스텀 박스 생성.\

사용자가 박스 위치(top, bottom, left, right), breach mode, 모든 파라미터를 직접 지정.\

조건 체크는 사용자 스크립트에서 수행하고, 이 함수는 박스 생성만 담당.\

새로운 박스 타입 추가 시 라이브러리 수정 없이 사용 가능.

Parameters:

_boxType (string) : 박스 타입 (사용자 정의 문자열)

_breachMode (string) : 돌파 처리 방식: "both", "directionalHighLow", "directionalClose", "sobClose"

_isBull (bool) : 상승(true) 또는 하락(false) 방향

_top (float) : 박스 상단 가격

_bottom (float) : 박스 하단 가격

_left (int) : 박스 시작 시간 (xloc.bar_time 사용)

_right (int) : 박스 종료 시간 (xloc.bar_time 사용)

_useLine (bool) : 중간선 표시 여부

_colorBG (color) : 박스 배경색

_colorBD (color) : 박스 테두리색

_colorText (color) : 텍스트 색상

_text (string) : 박스에 표시할 텍스트

Returns: 성공 여부와 박스 데이터

ProcessBoxDatas(_openBoxes, _closedBoxes, _useMidLine, _closeCount, _colorClose, _currentBarIndex, _currentLow, _currentHigh, _currentTime)

ProcessBoxDatas

@description 박스 확장 및 돌파 처리.\

열린 박스들을 현재 bar까지 확장하고, 돌파 조건 체크.\

_closeCount: 돌파 횟수 (이 횟수만큼 돌파 시 박스 종료).\

breachMode에 따라 돌파 체크 방식 다름 (both/directionalHighLow/directionalClose).\

종료된 박스는 _closedBoxes로 이동하고 _colorClose 색상 적용.\

barstate.islast와 barstate.isconfirmed에서 호출 권장.

Parameters:

_openBoxes (array) : 열린 박스 배열

_closedBoxes (array) : 닫힌 박스 배열

_useMidLine (bool) : 중간선 표시 여부

_closeCount (int) : 돌파 카운트 (이 횟수만큼 돌파 시 종료)

_colorClose (color) : 종료된 박스 색상

_currentBarIndex (int) : 현재 bar_index

_currentLow (float) : 현재 low

_currentHigh (float) : 현재 high

_currentTime (int) : 현재 time

Returns: bool 항상 true

UpdateHTFCache(_cache, _tf)

UpdateHTFCache

@description HTF 데이터 캐싱 (성능 최적화).\

HTF의 OHLC 데이터를 캐싱하여 매 틱마다 request.security 호출 방지.\

_cache: 기존 캐시 (없으면 na, 첫 호출 시).\

_tf: 캐싱할 시간대 (예: "60", "1D").\

새 bar 또는 bar_index 변경 시에만 업데이트, 그 외에는 기존 캐시 반환.\

Parameters:

_cache (HTFCache) : 기존 캐시 데이터 (없으면 na)

_tf (string) : 시간대

Returns: HTFCache 업데이트된 캐시 데이터

GetTimeframeSettings(_currentTF, _midTF1m, _highTF1m, _midTF5m, _highTF5m, _midTF15m, _highTF15m, _midTF30m, _highTF30m, _midTF60m, _highTF60m, _midTF240m, _highTF240m, _midTF1D, _highTF1D, _midTF1W, _highTF1W, _midTF1M, _highTF1M)

GetTimeframeSettings

@description 현재 차트 시간대에 맞는 중위/상위 시간대 자동 선택.\

_currentTF: 현재 차트 시간대 (timeframe.period).\

1분~1월 차트별로 적절한 중위/상위 시간대 매핑.\

예: 5분 차트 → 중위 15분, 상위 60분.\

반환: .\

Parameters:

_currentTF (string) : 현재 차트 시간대

_midTF1m (string)

_highTF1m (string)

_midTF5m (string)

_highTF5m (string)

_midTF15m (string)

_highTF15m (string)

_midTF30m (string)

_highTF30m (string)

_midTF60m (string)

_highTF60m (string)

_midTF240m (string)

_highTF240m (string)

_midTF1D (string)

_highTF1D (string)

_midTF1W (string)

_highTF1W (string)

_midTF1M (string)

_highTF1M (string)

Returns:

BoxData

BoxData

Fields:

_type (series string) : 박스 타입 (fob, fvg, sweep, rb, custom 등)

_breachMode (series string) : 돌파 처리 방식

_isBull (series bool) : 상승(true) 또는 하락(false) 방향

_box (series box)

_line (series line)

_boxTop (series float)

_boxBot (series float)

_boxMid (series float)

_topBreached (series bool)

_bottomBreached (series bool)

_breakCount (series int)

_createdBar (series int)

HTFCache

Fields:

_timeframe (series string)

_lastBarIndex (series int)

_isNewBar (series bool)

_barIndex (series int)

_open (series float)

_high (series float)

_low (series float)

_close (series float)

_open1 (series float)

_close1 (series float)

_high1 (series float)

_low1 (series float)

_open2 (series float)

_close2 (series float)

_high2 (series float)

_low2 (series float)

_high3 (series float)

_low3 (series float)

_time1 (series int)

_time2 (series int)

tgpFibonacciLib_v2Library "tgpFibonacciLib_v2"

getFib(tf, ratio)

Parameters:

tf (string)

ratio (float)

getGoldenPocket(tf)

Parameters:

tf (string)

getMonthlyFib(ratio)

Parameters:

ratio (float)

getWeeklyFib(ratio)

Parameters:

ratio (float)

getYestFib(ratio)

Parameters:

ratio (float)

AssetCorrelationLibraryLibrary "AssetCorrelationLibrary™"

detectIndicesFutures(ticker)

Detects Index Futures (NQ/ES/YM/RTY + micro variants)

Parameters:

ticker (string) : The ticker string to check (typically syminfo.ticker)

Returns: AssetPairing with secondary and tertiary assets configured

detectMetalsFutures(ticker)

Detects Metal Futures (GC/SI/HG + micro variants)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectForexFutures(ticker)

Detects Forex Futures (6E/6B + micro variants)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectEnergyFutures(ticker)

Detects Energy Futures (CL/RB/HO + micro variants)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectTreasuryFutures(ticker)

Detects Treasury Futures (ZB/ZF/ZN)

Parameters:

ticker (string) : The ticker string to check

Returns: AssetPairing with secondary and tertiary assets configured

detectForexCFD(ticker, tickerId)

Detects Forex CFD pairs (EUR/GBP/DXY, USD/JPY/CHF triads)

Parameters:

ticker (string) : The ticker string to check

tickerId (string) : The full ticker ID (syminfo.tickerid) for primary asset

Returns: AssetPairing with secondary and tertiary assets configured

detectCrypto(ticker, tickerId)

Detects major Crypto assets (BTC, ETH, SOL, XRP, alts)

Parameters:

ticker (string) : The ticker string to check

tickerId (string) : The full ticker ID for primary asset

Returns: AssetPairing with secondary and tertiary assets configured

detectMetalsCFD(ticker, tickerId)

Detects Metals CFD (XAU/XAG/Copper)

Parameters:

ticker (string) : The ticker string to check

tickerId (string) : The full ticker ID for primary asset

Returns: AssetPairing with secondary and tertiary assets configured

detectIndicesCFD(ticker, tickerId)

Detects Indices CFD (NAS100/SP500/DJ30)

Parameters:

ticker (string) : The ticker string to check

tickerId (string) : The full ticker ID for primary asset