Lorentzian Length Adaptive Moving Average [LLAMA] Adaptation of "Machine Learning: Lorentzian Classification" by

Gradient color by base on work by

LLAMA: A regime-aware adaptive moving average that bends with the market.

Start with a problem traders know:

Traditional moving averages are either too slow (EMA200) or too fast (EMA9)

Adaptive MAs exist, but they often hug price too tightly or smooth too much, failing to balance bias and tactics

LLAMA uses a Lorentzian distance function to adapt its length dynamically. Instead of a fixed smoothing window, it stretches or contracts depending on market conditions. This distortion reduces lag while still providing a clear bias line.

The indicator looks back at recent bars and measures how similar they are using a Lorentzian distance (a log‑scaled absolute difference). It keeps track of the “nearest neighbors” — bars that most resemble the current regime. Each neighbor carries a label (long, short, neutral) based on simple price comparisons. By averaging these labels, LLAMA predicts whether the market is leaning bullish or bearish. That prediction is then mapped into a dynamic length between and .

Bullish bias -> length stretches toward max (smoother, more stable).

Bearish bias -> length contracts toward min (snappier, more reactive).

During breakouts, LLAMA tightens and comes into contact with bars, giving actionable signals. During chop, it stretches to avoid false triggers. It covers both ends of the spectrum (bias and tactics) in one line, something static MA's can't do.

Think of LLAMA as a lens that bends with the market:

Wide lens (max length) for big picture bias.

Narrow lens (min length) for tactical precision.

The "Lorentzian Loop" is the math that decides when to widen or narrow.

Quant

Volatility-Targeted Momentum Portfolio [BackQuant]Volatility-Targeted Momentum Portfolio

A complete momentum portfolio engine that ranks assets, targets a user-defined volatility, builds long, short, or delta-neutral books, and reports performance with metrics, attribution, Monte Carlo scenarios, allocation pie, and efficiency scatter plots. This description explains the theory and the mechanics so you can configure, validate, and deploy it with intent.

Table of contents

What the script does at a glance

Momentum, what it is, how to know if it is present

Volatility targeting, why and how it is done here

Portfolio construction modes: Long Only, Short Only, Delta Neutral

Regime filter and when the strategy goes to cash

Transaction cost modelling in this script

Backtest metrics and definitions

Performance attribution chart

Monte Carlo simulation

Scatter plot analysis modes

Asset allocation pie chart

Inputs, presets, and deployment checklist

Suggested workflow

1) What the script does at a glance

Pulls a list of up to 15 tickers, computes a simple momentum score on each over a configurable lookback, then volatility-scales their bar-to-bar return stream to a target annualized volatility.

Ranks assets by raw momentum, selects the top 3 and bottom 3, builds positions according to the chosen mode, and gates exposure with a fast regime filter.

Accumulates a portfolio equity curve with risk and performance metrics, optional benchmark buy-and-hold for comparison, and a full alert suite.

Adds visual diagnostics: performance attribution bars, Monte Carlo forward paths, an allocation pie, and scatter plots for risk-return and factor views.

2) Momentum: definition, detection, and validation

Momentum is the tendency of assets that have performed well to continue to perform well, and of underperformers to continue underperforming, over a specific horizon. You operationalize it by selecting a horizon, defining a signal, ranking assets, and trading the leaders versus laggards subject to risk constraints.

Signal choices . Common signals include cumulative return over a lookback window, regression slope on log-price, or normalized rate-of-change. This script uses cumulative return over lookback bars for ranking (variable cr = price/price - 1). It keeps the ranking simple and lets volatility targeting handle risk normalization.

How to know momentum is present .

Leaders and laggards persist across adjacent windows rather than flipping every bar.

Spread between average momentum of leaders and laggards is materially positive in sample.

Cross-sectional dispersion is non-trivial. If everything is flat or highly correlated with no separation, momentum selection will be weak.

Your validation should include a diagnostic that measures whether returns are explained by a momentum regression on the timeseries.

Recommended diagnostic tool . Before running any momentum portfolio, verify that a timeseries exhibits stable directional drift. Use this indicator as a pre-check: It fits a regression to price, exposes slope and goodness-of-fit style context, and helps confirm if there is usable momentum before you force a ranking into a flat regime.

3) Volatility targeting: purpose and implementation here

Purpose . Volatility targeting seeks a more stable risk footprint. High-vol assets get sized down, low-vol assets get sized up, so each contributes more evenly to total risk.

Computation in this script (per asset, rolling):

Return series ret = log(price/price ).

Annualized volatility estimate vol = stdev(ret, lookback) * sqrt(tradingdays).

Leverage multiplier volMult = clamp(targetVol / vol, 0.1, 5.0).

This caps sizing so extremely low-vol assets don’t explode weight and extremely high-vol assets don’t go to zero.

Scaled return stream sr = ret * volMult. This is the per-bar, risk-adjusted building block used in the portfolio combinations.

Interpretation . You are not levering your account on the exchange, you are rescaling the contribution each asset’s daily move has on the modeled equity. In live trading you would reflect this with position sizing or notional exposure.

4) Portfolio construction modes

Cross-sectional ranking . Assets are sorted by cr over the chosen lookback. Top and bottom indices are extracted without ties.

Long Only . Averages the volatility-scaled returns of the top 3 assets: avgRet = mean(sr_top1, sr_top2, sr_top3). Position table shows per-asset leverages and weights proportional to their current volMult.

Short Only . Averages the negative of the volatility-scaled returns of the bottom 3: avgRet = mean(-sr_bot1, -sr_bot2, -sr_bot3). Position table shows short legs.

Delta Neutral . Long the top 3 and short the bottom 3 in equal book sizes. Each side is sized to 50 percent notional internally, with weights within each side proportional to volMult. The return stream mixes the two sides: avgRet = mean(sr_top1,sr_top2,sr_top3, -sr_bot1,-sr_bot2,-sr_bot3).

Notes .

The selection metric is raw momentum, the execution stream is volatility-scaled returns. This separation is deliberate. It avoids letting volatility dominate ranking while still enforcing risk parity at the return contribution stage.

If everything rallies together and dispersion collapses, Long Only may behave like a single beta. Delta Neutral is designed to extract cross-sectional momentum with low net beta.

5) Regime filter

A fast EMA(12) vs EMA(21) filter gates exposure.

Long Only active when EMA12 > EMA21. Otherwise the book is set to cash.

Short Only active when EMA12 < EMA21. Otherwise cash.

Delta Neutral is always active.

This prevents taking long momentum entries during obvious local downtrends and vice versa for shorts. When the filter is false, equity is held flat for that bar.

6) Transaction cost modelling

There are two cost touchpoints in the script.

Per-bar drag . When the regime filter is active, the per-bar return is reduced by fee_rate * avgRet inside netRet = avgRet - (fee_rate * avgRet). This models proportional friction relative to traded impact on that bar.

Turnover-linked fee . The script tracks changes in membership of the top and bottom baskets (top1..top3, bot1..bot3). The intent is to charge fees when composition changes. The template counts changes and scales a fee by change count divided by 6 for the six slots.

Use case: increase fee_rate to reflect taker fees and slippage if you rebalance every bar or trade illiquid assets. Reduce it if you rebalance less often or use maker orders.

Practical advice .

If you rebalance daily, start with 5–20 bps round-trip per switch on liquid futures and adjust per venue.

For crypto perp microcaps, stress higher cost assumptions and add slippage buffers.

If you only rotate on lookback boundaries or at signals, use alert-driven rebalances and lower per-bar drag.

7) Backtest metrics and definitions

The script computes a standard set of portfolio statistics once the start date is reached.

Net Profit percent over the full test.

Max Drawdown percent, tracked from running peaks.

Annualized Mean and Stdev using the chosen trading day count.

Variance is the square of annualized stdev.

Sharpe uses daily mean adjusted by risk-free rate and annualized.

Sortino uses downside stdev only.

Omega ratio of sum of gains to sum of losses.

Gain-to-Pain total gains divided by total losses absolute.

CAGR compounded annual growth from start date to now.

Alpha, Beta versus a user-selected benchmark. Beta from covariance of daily returns, Alpha from CAPM.

Skewness of daily returns.

VaR 95 linear-interpolated 5th percentile of daily returns.

CVaR average of the worst 5 percent of daily returns.

Benchmark Buy-and-Hold equity path for comparison.

8) Performance attribution

Cumulative contribution per asset, adjusted for whether it was held long or short and for its volatility multiplier, aggregated across the backtest. You can filter to winners only or show both sides. The panel is sorted by contribution and includes percent labels.

9) Monte Carlo simulation

The panel draws forward equity paths from either a Normal model parameterized by recent mean and stdev, or non-parametric bootstrap of recent daily returns. You control the sample length, number of simulations, forecast horizon, visibility of individual paths, confidence bands, and a reproducible seed.

Normal uses Box-Muller with your seed. Good for quick, smooth envelopes.

Bootstrap resamples realized returns, preserving fat tails and volatility clustering better than a Gaussian assumption.

Bands show 10th, 25th, 75th, 90th percentiles and the path mean.

10) Scatter plot analysis

Four point-cloud modes, each plotting all assets and a star for the current portfolio position, with quadrant guides and labels.

Risk-Return Efficiency . X is risk proxy from leverage, Y is expected return from annualized momentum. The star shows the current book’s composite.

Momentum vs Volatility . Visualizes whether leaders are also high vol, a cue for turnover and cost expectations.

Beta vs Alpha . X is a beta proxy, Y is risk-adjusted excess return proxy. Useful to see if leaders are just beta.

Leverage vs Momentum . X is volMult, Y is momentum. Shows how volatility targeting is redistributing risk.

11) Asset allocation pie chart

Builds a wheel of current allocations.

Long Only, weights are proportional to each long asset’s current volMult and sum to 100 percent.

Short Only, weights show the short book as positive slices that sum to 100 percent.

Delta Neutral, 50 percent long and 50 percent short books, each side leverage-proportional.

Labels can show asset, percent, and current leverage.

12) Inputs and quick presets

Core

Portfolio Strategy . Long Only, Short Only, Delta Neutral.

Initial Capital . For equity scaling in the panel.

Trading Days/Year . 252 for stocks, 365 for crypto.

Target Volatility . Annualized, drives volMult.

Transaction Fees . Per-bar drag and composition change penalty, see the modelling notes above.

Momentum Lookback . Ranking horizon. Shorter is more reactive, longer is steadier.

Start Date . Ensure every symbol has data back to this date to avoid bias.

Benchmark . Used for alpha, beta, and B&H line.

Diagnostics

Metrics, Equity, B&H, Curve labels, Daily return line, Rolling drawdown fill.

Attribution panel. Toggle winners only to focus on what matters.

Monte Carlo mode with Normal or Bootstrap and confidence bands.

Scatter plot type and styling, labels, and portfolio star.

Pie chart and labels for current allocation.

Presets

Crypto Daily, Long Only . Lookback 25, Target Vol 50 percent, Fees 10 bps, Regime filter on, Metrics and Drawdown on. Monte Carlo Bootstrap with Recent 200 bars for bands.

Crypto Daily, Delta Neutral . Lookback 25, Target Vol 50 percent, Fees 15–25 bps, Regime filter always active for this mode. Use Scatter Risk-Return to monitor efficiency and keep the star near upper left quadrants without drifting rightward.

Equities Daily, Long Only . Lookback 60–120, Target Vol 15–20 percent, Fees 5–10 bps, Regime filter on. Use Benchmark SPX and watch Alpha and Beta to keep the book from becoming index beta.

13) Suggested workflow

Universe sanity check . Pick liquid tickers with stable data. Thin assets distort vol estimates and fees.

Check momentum existence . Run on your timeframe. If slope and fit are weak, widen lookback or avoid that asset or timeframe.

Set risk budget . Choose a target volatility that matches your drawdown tolerance. Higher target increases turnover and cost sensitivity.

Pick mode . Long Only for bull regimes, Short Only for sustained downtrends, Delta Neutral for cross-sectional harvesting when index direction is unclear.

Tune lookback . If leaders rotate too often, lengthen it. If entries lag, shorten it.

Validate cost assumptions . Increase fee_rate and stress Monte Carlo. If the edge vanishes with modest friction, refine selection or lengthen rebalance cadence.

Run attribution . Confirm the strategy’s winners align with intuition and not one unstable outlier.

Use alerts . Enable position change, drawdown, volatility breach, regime, momentum shift, and crash alerts to supervise live runs.

Important implementation details mapped to code

Momentum measure . cr = price / price - 1 per symbol for ranking. Simplicity helps avoid overfitting.

Volatility targeting . vol = stdev(log returns, lookback) * sqrt(tradingdays), volMult = clamp(targetVol / vol, 0.1, 5), sr = ret * volMult.

Selection . Extract indices for top1..top3 and bot1..bot3. The arrays rets, scRets, lev_vals, and ticks_arr track momentum, scaled returns, leverage multipliers, and display tickers respectively.

Regime filter . EMA12 vs EMA21 switch determines if the strategy takes risk for Long or Short modes. Delta Neutral ignores the gate.

Equity update . Equity multiplies by 1 + netRet only when the regime was active in the prior bar. Buy-and-hold benchmark is computed separately for comparison.

Tables . Position tables show current top or bottom assets with leverage and weights. Metric table prints all risk and performance figures.

Visualization panels . Attribution, Monte Carlo, scatter, and pie use the last bars to draw overlays that update as the backtest proceeds.

Final notes

Momentum is a portfolio effect. The edge comes from cross-sectional dispersion, adequate risk normalization, and disciplined turnover control, not from a single best asset call.

Volatility targeting stabilizes path but does not fix selection. Use the momentum regression link above to confirm structure exists before you size into it.

Always test higher lag costs and slippage, then recheck metrics, attribution, and Monte Carlo envelopes. If the edge persists under stress, you have something robust.

Central Limit Theorem Reversion IndicatorDear TV community, let me introduce you to the first-ever Central Limit Theorem indicator on TradingView.

The Central Limit Theorem is used in statistics and it can be quite useful in quant trading and understanding market behaviors.

In short, the CLT states: "When you take repeated samples from any population and calculate their averages, those averages will form a normal (bell curve) distribution—no matter what the original data looks like."

In this CLT indicator, I use statistical theory to identify high-probability mean reversion opportunities in the markets. It calculates statistical confidence bands and z-scores to identify when price movements deviate significantly from their expected distribution, signaling potential reversion opportunities with quantifiable probability levels.

Mathematical Foundation

The Central Limit Theorem (CLT) says that when you average many data points together, those averages will form a predictable bell-curve pattern, even if the original data is completely random and unpredictable (which often is in the markets). This works no matter what you're measuring, and it gets more reliable as you use more data points.

Why using it for trading?

Individual price movements seem random and chaotic, but when we look at the average of many price movements, we can actually predict how they should behave statistically. This lets us spot when prices have moved "too far" from what's normal—and those extreme moves tend to snap back (mean reversion).

Key Formula:

Z = (X̄ - μ) / (σ / √n)

Where:

- X̄ = Sample mean (average return over n periods)

- μ = Population mean (long-term expected return)

- σ = Population standard deviation (volatility)

- n = Sample size

- σ/√n = Standard error of the mean

How I Apply CLT

Step 1: Calculate Returns

Measures how much price changed from one bar to the next (using logarithms for better statistical properties)

Step 2: Average Recent Returns

Takes the average of the last n returns (e.g., last 100 bars). This is your "sample mean."

Step 3: Find What's "Normal"

Looks at historical data to determine: a) What the typical average return should be (the long-term mean) and b) How volatile the market usually is (standard deviation)

Step 4: Calculate Standard Error

Determines how much sample averages naturally vary. Larger samples = smaller expected variation.

Step 5: Calculate Z-Score

Measures how unusual the current situation is.

Step 6: Draw Confidence Bands

Converts these statistical boundaries into actual price levels on your chart, showing where price is statistically expected to stay 95% and 99% of the time.

Interpretation & Usage

The Z-Score:

The z-score tells you how statistically unusual the current price deviation is:

|Z| < 1.0 → Normal behavior, no action

|Z| = 1.0 to 1.96 → Moderate deviation, watch closely

|Z| = 1.96 to 2.58 → Significant deviation (95%+), consider entry

|Z| > 2.58 → Extreme deviation (99%+), high probability setup

The Confidence Bands

- Upper Red Bands: 95% and 99% overbought zones → Expect mean reversion downward as the price is not likely to cross these lines.

- Center Gray Line: Statistical expectation (fair value)

- Lower Blue Bands: 95% and 99% oversold zones → Expect mean reversion upward

Trading Logic:

- When price exceeds the upper 95% band (z-score > +1.96), there's only a 5% probability this is random noise → Strong sell/short signal

- When price falls below the lower 95% band (z-score < -1.96), there's a 95% statistical expectation of upward reversion → Strong buy/long signal

Background Gradient

The background color provides real-time visual feedback:

- Blue shades: Oversold conditions, expect upward reversion

- Red shades: Overbought conditions, expect downward reversion

- Intensity: Darker colors indicate stronger statistical significance

Trading Strategy Examples

Hypothetically, this is how the indicator could be used:

- Long: Z-score < -1.96 (below 95% confidence band)

- Short: Z-score > +1.96 (above 95% confidence band)

- Take profit when price returns to center line (Z ≈ 0)

Input Parameters

Sample Size (n) - Default: 100

Lookback Period (m) - Default: 100

You can also create alerts based on the indicator.

Final notes:

- The indicator uses logarithmic returns for better statistical properties

- Converts statistical bands back to price space for practical use

- Adaptive volatility: Bands automatically widen in high volatility, narrow in low volatility

- No repainting: yay! All calculations use historical data only

Feedback is more than welcome!

Henri

Volume Sampled Supertrend [BackQuant]Volume Sampled Supertrend

A Supertrend that runs on a volume sampled price series instead of fixed time. New synthetic bars are only created after sufficient traded activity, which filters out low participation noise and makes the trend much easier to read and model.

Original Script Link

This indicator is built on top of my volume sampling engine. See the base implementation here:

Why Volume Sampling

Traditional charts print a bar every N minutes regardless of how active the tape is. During quiet periods you accumulate many small, low information bars that add noise and whipsaws to downstream signals.

Volume sampling replaces the clock with participation. A new synthetic bar is created only when a pre-set amount of volume accumulates (or, in Dollar Bars mode, when pricevolume reaches a dollar threshold). The result is a non-uniform time series that stretches in busy regimes and compresses in quiet regimes. This naturally:

filters dead time by skipping low volume chop;

standardizes the information content per bar, improving comparability across regimes;

stabilizes volatility estimates used inside banded indicators;

gives trend and breakout logic cleaner state transitions with fewer micro flips.

What this tool does

It builds a synthetic OHLCV stream from volume based buckets and then applies a Supertrend to that synthetic price. You are effectively running Supertrend on a participation clock rather than a wall clock.

Core Features

Sampling Engine - Choose Volume buckets or Dollar Bars . Thresholds can be dynamic from a rolling mean or median, or fixed by the user.

Synthetic Candles - Plots the volume sampled OHLC candles so you can visually compare against regular time candles.

Supertrend on Synthetic Price - ATR bands and direction are computed on the sampled series, not on time bars.

Adaptive Coloring - Candle colors can reflect side, intensity by volume, or a neutral scheme.

Research Panels - Table shows total samples, current bucket fill, threshold, bars-per-sample, and synthetic return stats.

Alerts - Long and Short triggers on Supertrend direction flips for the synthetic series.

How it works

Sampling

Pick Sampling Method = Volume or Dollar Bars.

Set the dynamic threshold via Rolling Lookback and Filter (Mean or Median), or enable Use Fixed and type a constant.

The script accumulates volume (or pricevolume) each time bar. When the bucket reaches the threshold, it finalizes one or more synthetic candles and resets accumulation.

Each synthetic candle stores its own OHLCV and is appended to the synthetic series used for all downstream logic.

Supertrend on the sampled stream

Choose Supertrend Source (Open, High, Low, Close, HLC3, HL2, OHLC4, HLCC4) derived from the synthetic candle.

Compute ATR over the synthetic series with ATR Period , then form upperBand = src + factorATR and lowerBand = src - factorATR .

Apply classic trailing band and direction rules to produce Supertrend and trend state.

Because bars only come when there is sufficient participation, band touches and flips tend to align with meaningful pushes, not idle prints.

Reading the display

Synthetic Volume Bars - The non-uniform candles that represent equal information buckets. Expect more candles during active sessions and fewer during lulls.

Volume Sampled Supertrend - The main line. Green when Trend is 1, red when Trend is -1.

Markers - Small dots appear when a new synthetic sample is created, useful for aligning activity cycles.

Time Bars Overlay (optional) - Plot regular time candles to compare how the synthetic stream compresses quiet chop.

Settings you will use most

Data Settings

Sampling Method - Volume or Dollar Bars.

Rolling Lookback and Filter - Controls the dynamic threshold. Median is robust to outliers, Mean is smoother.

Use Fixed and Fixed Threshold - Force a constant bucket size for consistent sampling across regimes.

Max Stored Samples - Ring buffer limit for performance.

Indicator Settings

SMA over last N samples - A moving average computed on the synthetic close series. Can be hidden for a cleaner layout.

Supertrend Source - Price field from the synthetic candle.

ATR Period and Factor - Standard Supertrend controls applied on the synthetic series.

Visuals and UI

Show Synthetic Bars - Turn synthetic candles on or off.

Candle Color Mode - Green/Red, Volume Intensity, Neutral, or Adaptive.

Mark new samples - Puts a dot when a bucket closes.

Show Time Bars - Overlay regular candles for comparison.

Paint candles according to Trend - Colors chart candles using current synthetic Supertrend direction.

Line Width , Colors , and Stats Table toggles.

Some workflow notes:

Trend Following

Set Sampling Method = Volume, Filter = Median, and a reasonable Rolling Lookback so busy regimes produce more samples.

Trade in the direction of the Volume Sampled Supertrend. Because flips require real participation, you tend to avoid micro whipsaws seen on time bars.

Use the synthetic SMA as a bias rail and trailing reference for partials or re-entries.

Breakout and Continuation

Watch for rapid clustering of new sample markers and a clean flip of the synthetic Supertrend.

The compression of quiet time and expansion in busy bursts often makes breakouts more legible than on uniform time charts.

Mean Reversion

In instruments that oscillate, faded moves against the synthetic Supertrend are easier to time when the bucket cadence slows and Supertrend flattens.

Combine with the synthetic SMA and return statistics in the table for sizing and expectation setting.

Stats table (top right)

Method and Total Samples - Sampling regime and current synthetic history length.

Current Vol or Dollar and Threshold - Live bucket fill versus the trigger.

Bars in Bucket and Avg Bars per Sample - How much time data each synthetic bar tends to compress.

Avg Return and Return StdDev - Simple research metrics over synthetic close-to-close changes.

Why this reduces noise

Time based bars treat a 5 minute print with 1 percent of average participation the same as one with 300 percent. Volume sampling equalizes bar information content. By advancing the bar only when sufficient activity occurs, you skip low quality intervals that add variance but little signal. For banded systems like Supertrend, this often means fewer false flips and cleaner runs.

Notes and tips

Use Dollar Bars on assets where nominal price varies widely over time or across symbols.

Median filter can resist single burst outliers when setting dynamic thresholds.

If you need a stable research baseline, set Use Fixed and keep the threshold constant across tests.

Enable Show Time Bars occasionally to sanity check what the synthetic stream is compressing or stretching.

Link again for reference

Original Volume Based Sampling engine:

Bottom line

When you let participation set the clock, your Supertrend reacts to meaningful flow instead of idle prints. The result is a cleaner state machine, fewer micro whipsaws, and a trend read that respects when the market is actually trading.

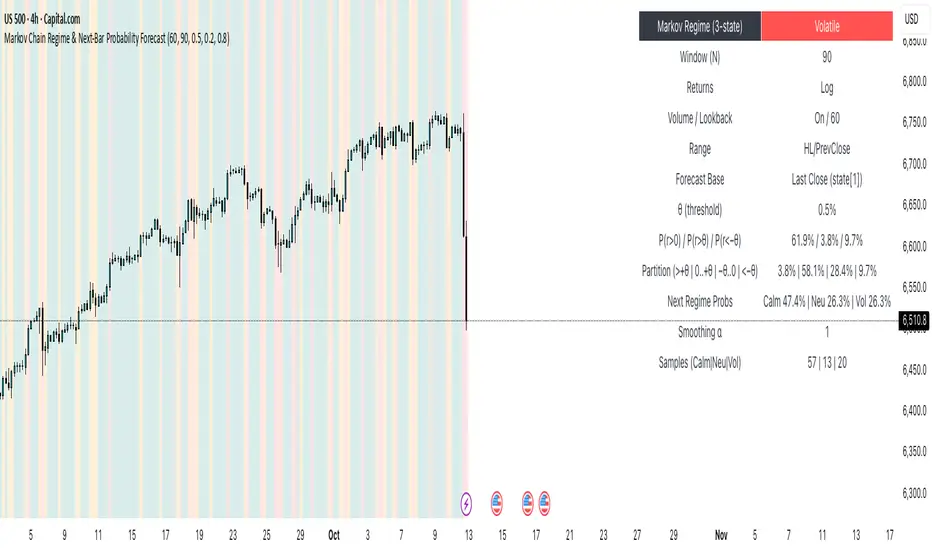

Markov Chain Regime & Next‑Bar Probability Forecast✨ What it is

A regime-aware, math-driven panel that forecasts the odds for the very next candle. It shows:

• P(next r > 0)

• P(next r > +θ)

• P(next r < −θ)

• A 4-bucket split of next-bar outcomes (>+θ | 0..+θ | −θ..0 | <−θ)

• Next-regime probabilities: Calm | Neutral | Volatile

🧠 Why the math is strong

• Markov regimes: Markets cluster in volatility “moods.” We learn a 3-state regime S∈{Calm, Neutral, Volatile} with a transition matrix A, where A = P(Sₜ₊₁=j | Sₜ=i).

• Condition on the future state: We estimate event odds given the next regime j—

q_pos(j)=P(rₜ₊₁>0 | Sₜ₊₁=j), q_gt(j)=P(rₜ₊₁>+θ | Sₜ₊₁=j), q_lt(j)=P(rₜ₊₁<−θ | Sₜ₊₁=j)—

and mix them with transitions from the current (or frozen) state sNow:

P(event) = Σⱼ A · q(event | j).

This mixture-of-regimes view (HMM-style one-step prediction) ties next-bar outcomes to where volatility is likely headed.

• Statistical hygiene: Laplace/Beta smoothing, minimum-sample gating, and unconditional fallbacks keep estimates stable. Heavy computations run on confirmed bars; “Freeze at close” avoids intrabar flicker.

📊 What each value means

• Regime label & background: 🟩 Calm, 🟧 Neutral, 🟥 Volatile — quick read of market context.

• P(next r > 0): Directional tilt for the very next bar.

• P(next r > +θ): Odds of an outsized positive move beyond θ.

• P(next r < −θ): Odds of an outsized negative move beyond −θ.

• Partition row: Distributes next-bar probability across four intuitive buckets; they ≈ sum to 100%.

• Next Regime Probs: Likelihood of switching to Calm/Neutral/Volatile on the next bar (row of A for the current/frozen state).

• Samples row: How many next-bar samples support each next-state estimate (a confidence cue).

• Smoothing α: The Laplace prior used to stabilize binary event rates.

⚙️ Inputs you control

• Returns: Log (default) or %

• Include Volume (z-score) + lookback

• Include Range (HL/PrevClose)

• Rolling window N (transitions & estimates)

• θ as percent (e.g., 0.5%)

• Freeze forecast at last close (recommended)

• Display toggles (plots, partition, samples)

🎯 How to use it

• Volatility awareness & sizing: Rising P(next regime = Volatile) → consider smaller size, wider stops, or skipping marginal entries.

• Breakout preparation: Elevated P(next r > +θ) highlights environments where range expansion is more likely; pair with your setup/trigger.

• Defense for mean-reversion: If P(next r < −θ) lifts while you’re late long (or P(next r > +θ) lifts while late short), tighten risk or wait for better context.

• Calibration tip: Start θ near your market’s typical bar size; adjust until “>+θ” flags truly meaningful moves for your timeframe.

📝 Method notes & limits

Activity features (|r|, volume z, range) are standardized; only positive z’s feed the composite activity score. Estimates adapt to instrument/timeframe; rare regimes or small windows increase variance (hence smoothing, sample gating, fallbacks). This is a context/forecast tool, not a standalone signal—combine with your entry/exit rules and risk management.

🧩 Strategies too

We also develop full strategy versions that use these probabilities for entries, filters, and position sizing. Like this publication if you’d like us to release the strategy edition next.

⚠️ Disclaimer

Educational use only. Not financial advice. Markets involve risk. Past performance does not guarantee future results.

Risk Recommender — (Heatmap)📊 Risk Recommender — Per-Trade & Annualized (Heatmap Columns)

Estimate the optimal risk percentage for any market regime.

This tool dynamically recommends how much of your account equity to risk — either per trade or at a portfolio (annualized) level — using volatility as the guide.

⚙️ How it works

Two distinct modes give you flexibility:

1️⃣ Per-Trade (ATR-based)

• Calculates the current Average True Range (ATR) compared to its long-term baseline.

• When volatility is high (ATR ↑), risk per trade decreases to maintain constant dollar risk.

• When volatility is low (ATR ↓), risk per trade increases within your defined floor and ceiling.

• The display is normalized by stop distance (× ATR) and smoothed to avoid noise.

2️⃣ Annualized (Volatility Targeting)

• Computes realized volatility (standard deviation of log returns) and an EWMA forecast of future volatility.

• Blends current and forecast volatilities to estimate “effective” volatility.

• Scales your base risk so that portfolio volatility converges toward your chosen annual target (e.g., 20%).

• Useful for portfolio-level or systematic strategies that maintain constant volatility exposure.

🎨 Heatmap Visualization

The vertical column graph acts like a thermometer:

• 🟥 Red → “Reduce risk” (volatility high).

• 🟩 Green → “Increase risk” (volatility low).

• Smoothed and bounded between your Floor and Ceiling risk levels.

• Optional dotted guides mark those bounds.

• Label shows the current mode, recommended risk %, and key metrics (ATR ratio or effective volatility).

🔧 Key Inputs

• Base max risk per trade (%) — your normal per-trade risk budget.

• ATR length / Baseline ATR length — control sensitivity to short- vs. long-term volatility.

• Target annualized volatility (%) — portfolio volatility target for quant mode.

• λ (lambda) — smoothing factor for the EWMA volatility forecast (0.90–0.99 typical).

• Floor & Ceiling — clamps the output to avoid extreme sizing.

• Smoothing & Hysteresis — prevent rapid changes in risk recommendations.

🧮 Interpreting the Output

• “Recommended Risk (%)” = suggested portion of equity to risk on the next trade (or current exposure).

• In Per-Trade mode: reflects current ATR ÷ baseline ATR .

• In Annualized mode: reflects target volatility ÷ effective volatility .

• Use the color and height of the column as a quick visual cue for aggressiveness.

💡 Typical Use Cases

• Position-sizing overlay for discretionary traders.

• Volatility-targeting component for algorithmic or multi-asset systems.

• Educational tool to understand how volatility governs prudent risk management.

📘 Notes

• This indicator provides risk suggestions only ; it does not place trades.

• Works on any symbol or timeframe.

• Combine with your own strategy or alerts for full automation.

• All calculations use built-in Pine functions; no proprietary logic.

Tags:

#RiskManagement #ATR #Volatility #Quant #PositionSizing #SystematicTrading #AlgorithmicTrading #Portfolio #TradingStrategy #Heatmap #EWMA #Risk

First Passage Time - Distribution AnalysisThe First Passage Time (FPT) Distribution Analysis indicator is a sophisticated probabilistic tool that answers one of the most critical questions in trading: "How long will it take for price to reach my target, and what are the odds of getting there first?"

Unlike traditional technical indicators that focus on what might happen, this indicator tells you when it's likely to happen.

Mathematical Foundation: First Passage Time Theory

What is First Passage Time?

First Passage Time (FPT) is a concept in stochastic processes that measures the time it takes for a random process to reach a specific threshold for the first time. Originally developed in physics and mathematics, FPT has applications in:

Quantitative Finance: Option pricing, risk management, and algorithmic trading

Neuroscience: Modeling neural firing patterns

Biology: Population dynamics and disease spread

Engineering: Reliability analysis and failure prediction

The Mathematics Behind It

This indicator uses Geometric Brownian Motion (GBM), the same stochastic model used in the Black-Scholes option pricing formula:

dS = μS dt + σS dW

Where:

S = Asset price

μ = Drift (trend component)

σ = Volatility (uncertainty component)

dW = Wiener process (random walk)

Through Monte Carlo simulation, the indicator runs 1,000+ price path simulations to statistically determine:

When each threshold (+X% or -X%) is likely to be hit

Which threshold is hit first (directional bias)

How often each scenario occurs (probability distribution)

🎯 How This Indicator Works

Core Algorithm Workflow:

Calculate Historical Statistics

Measures recent price volatility (standard deviation of log returns)

Calculates drift (average directional movement)

Annualizes these metrics for meaningful comparison

Run Monte Carlo Simulations

Generates 1,000+ random price paths based on historical behavior

Tracks when each path hits the upside (+X%) or downside (-X%) threshold

Records which threshold was hit first in each simulation

Aggregate Statistical Results

Calculates percentile distributions (10th, 25th, 50th, 75th, 90th)

Computes "first hit" probabilities (upside vs downside)

Determines average and median time-to-target

Visual Representation

Displays thresholds as horizontal lines

Shows gradient risk zones (purple-to-blue)

Provides comprehensive statistics table

📈 Use Cases

1. Options Trading

Selling Options: Determine if your strike price is likely to be hit before expiration

Buying Options: Estimate probability of reaching profit targets within your time window

Time Decay Management: Compare expected time-to-target vs theta decay

Example: You're considering selling a 30-day call option 5% out of the money. The indicator shows there's a 72% chance price hits +5% within 12 days. This tells you the trade has high assignment risk.

2. Swing Trading

Entry Timing: Wait for higher probability setups when directional bias is strong

Target Setting: Use median time-to-target to set realistic profit expectations

Stop Loss Placement: Understand probability of hitting your stop before target

Example: The indicator shows 85% upside probability with median time of 3.2 days. You can confidently enter long positions with appropriate position sizing.

3. Risk Management

Position Sizing: Larger positions when probability heavily favors one direction

Portfolio Allocation: Reduce exposure when probabilities are near 50/50 (high uncertainty)

Hedge Timing: Know when to add protective positions based on downside probability

Example: Indicator shows 55% upside vs 45% downside—nearly neutral. This signals high uncertainty, suggesting reduced position size or wait for better setup.

4. Market Regime Detection

Trending Markets: High directional bias (70%+ one direction)

Range-bound Markets: Balanced probabilities (45-55% both directions)

Volatility Regimes: Compare actual vs theoretical minimum time

Example: Consistent 90%+ bullish bias across multiple timeframes confirms strong uptrend—stay long and avoid counter-trend trades.

First Hit Rate (Most Important!)

Shows which threshold is likely to be hit FIRST:

Upside %: Probability of hitting upside target before downside

Downside %: Probability of hitting downside target before upside

These always sum to 100%

⚠️ Warning: If you see "Low Hit Rate" warning, increase this parameter!

Advanced Parameters

Drift Mode

Allows you to explore different scenarios:

Historical: Uses actual recent trend (default—most realistic)

Zero (Neutral): Assumes no trend, only volatility (symmetric probabilities)

50% Reduced: Dampens trend effect (conservative scenario)

Use Case: Switch to "Zero (Neutral)" to see what happens in a pure volatility environment, useful for range-bound markets.

Distribution Type

Percentile: Shows 10%, 25%, 50%, 75%, 90% levels (recommended for most users)

Sigma: Shows standard deviation levels (1σ, 2σ)—useful for statistical analysis

⚠️ Important Limitations & Best Practices

Limitations

Assumes GBM: Real markets have fat tails, jumps, and regime changes not captured by GBM

Historical Parameters: Uses recent volatility/drift—may not predict regime shifts

No Fundamental Events: Cannot predict earnings, news, or macro shocks

Computational: Runs only on last bar—doesn't give historical signals

Remember: Probabilities are not certainties. Use this indicator as part of a comprehensive trading plan with proper risk management.

Created by: Henrique Centieiro. feedback is more than welcome!

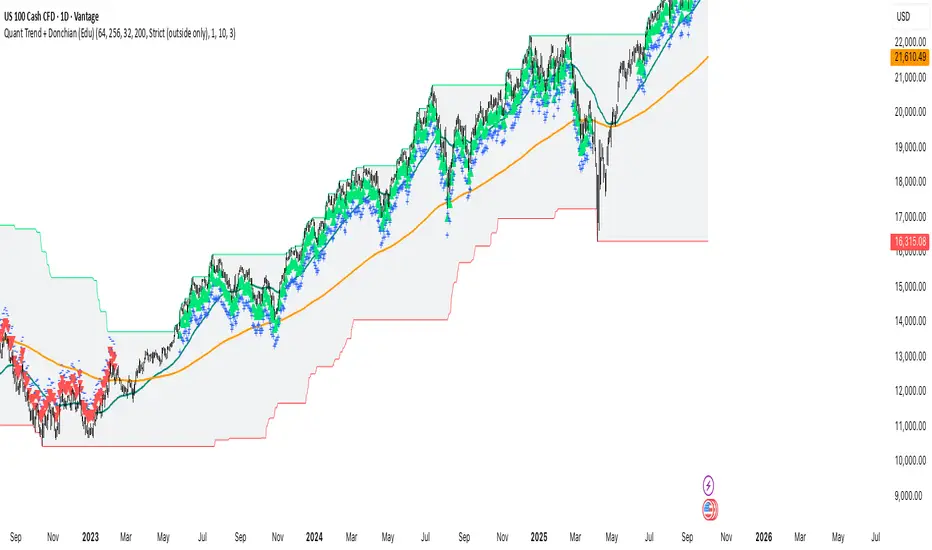

Quant Trend + Donchian (Educational, Public-Safe)What this does

Educational, public-safe visualization of a quant regime model:

• Trend : EMA(64) vs EMA(256) (EWMAC proxy)

• Breakout : Donchian channel (200)

• Volatility-awareness : internal z-scores (not plotted) for concept clarity

Why it’s useful

• Shows when trend & breakout align (clean regimes) vs conflict (chop)

• Helps explain why volatility-aware systems size up in smooth trends and scale down in noise

How to read it

• EMA64 above EMA256 with price near/above Donchian high → trend-following alignment

• EMA64 below EMA256 with price near/below Donchian low → bearish alignment

• Inside channel with EMAs tangled → range/chop risk

Notes

• Indicator is educational only (no orders).

• Built entirely with TradingView built-ins.

• For consistent visuals: enable “Indicator values on price scale” and disable “Scale price chart only” in Settings → Scales .

Trend-Following & Breakout — Index Quant Strategy (NASDAQ)📈 Trend-Following & Breakout — Index Quant Strategy (NASDAQ & S&P 500)

Type: Invite-only strategy

Markets: NASDAQ 100 (NAS100 / US100 / NQ), S&P 500 (US500 / SPX), and other major equity indices.

🧠 Concept: Continuous trend model combining EWMAC (trend-following) and Donchian (breakout) signals, scaled by forecast strength and portfolio risk.

⚙️ Execution: Rebalances only on decision-bar closes, using hysteresis and a no-trade band to reduce churn.

📊 Default bias: Long-only — aligned with equity index drift.

🧩 How it works

• EWMAC Trend: Difference between fast and slow EMAs, normalized by an EWMA of absolute returns.

• Donchian Breakout: Distance beyond a 200-bar channel (Strict mode) or relative z-score position within it.

• Forecast combination: Weighted sum of trend and breakout points, clamped to ± capPoints.

• Hysteresis: Prevents quick sign flips near zero forecast.

• Risk scaling: Maps forecast strength to position size using equity × risk budget × ATR-based stop distance.

• Rebalance: Executes only if the required quantity change exceeds the Δqty threshold; can optionally block increases on Sundays (for CFDs).

⚙️ Default parameters

Deployed on NQ / US100 / NAS100 on Daily Timeframe

• Decision timeframe = 360 min (other options from 1 min to 1 week).

• Trend (EWMAC): Fast = 64, Slow = 256, Vol Norm = 32, Weight = 0.8.

• Breakout (Donchian): Length = 200, Mode = Strict, Weight = 0.2.

• Forecast scaling: ptsPerSigma = 1.0, capPoints = 10.

• Risk % per rebalance = 4 % of equity.

• ATR stop: ATR(14) × 1.0.

• No-trade band (Δqty) = 4 units.

• Hysteresis = 2 forecast points.

• Bias = Long-only (Neutral / Long-bias 50 % optional).

• Skip Sunday increases = false (default).

📋 Backtest properties (documented)

• Initial capital = 100 000 USD.

• Commission = 0.20 % per trade.

• Pyramiding = 10.

• Calc on every tick = false.

• Point value = 1 (for NAS100 CFD).

• No financing or slippage modeled.

• If using CFDs, account for overnight funding.

• On futures (NQ / ES), carry is implicit.

📊 Typical behaviour

• Many small scratches, a few large winners.

• Performs best during multi-week / multi-month trends.

• Underperforms in tight or volatile ranges.

• Average hold ≈ 30 – 90 days in historical tests.

💡 Risk and performance guide (illustrative)

Sharpe ≈ 1.25

Sortino ≈ 1.10 – 1.30

Max drawdown ≈ –18 % to –25 %

Annual volatility ≈ 24 – 28 %

CAGR ≈ 50 – 60 % (at 4 % risk)

Edge ratio ≈ 5 (MFE / MAE)

Historical backtests only — past performance does not guarantee future results.

🌍 Intended markets and timeframes

Optimized for NASDAQ 100 and S&P 500; also effective on similar indices (DAX, Dow Jones, FTSE).

Best on Daily or higher timeframes.

Aligns with long-term index drift — suitable for long-bias systematic trend portfolios.

⚠️ Limitations

• Backtests exclude CFD funding costs.

• Trend models will have losing streaks in range-bound markets.

• Designed for experienced traders seeking systematic exposure.

🔑 Requesting access

Send a private TradingView message to with the text:

“Request access to Trend-Following & Breakout — Index Quant Strategy.”

Access is granted only on explicit request.

For further information, see my TradingView Signature.

🆕 Release notes (v1.0)

• Initial release (360 min TF): EWMAC 64/256 + Donchian 200 Strict.

• Risk 4 %, ATR × 1.0, Long-only bias, hysteresis 2 pts, Δqty ≥ 4.

• Developed for NASDAQ 100 and S&P 500 indices.

• Implements continuous risk-scaled positioning and no-trade band logic.

🧾 Originality statement

This strategy is original work built entirely from TradingView built-ins (EMA, ATR, Highest, Lowest).

It does not reuse open-source invite-only code.

Any future reuse of open scripts will be done with explicit permission and credit.

Volume Based Sampling [BackQuant]Volume Based Sampling

What this does

This indicator converts the usual time-based stream of candles into an event-based stream of “synthetic” bars that are created only when enough trading activity has occurred . You choose the activity definition:

Volume bars : create a new synthetic bar whenever the cumulative number of shares/contracts traded reaches a threshold.

Dollar bars : create a new synthetic bar whenever the cumulative traded dollar value (price × volume) reaches a threshold.

The script then keeps an internal ledger of these synthetic opens, highs, lows, closes, and volumes, and can display them as candles, plot a moving average calculated over the synthetic closes, mark each time a new sample is formed, and optionally overlay the native time-bars for comparison.

Why event-based sampling matters

Markets do not release information on a clock: activity clusters during news, opens/closes, and liquidity shocks. Event-based bars normalize for that heteroskedastic arrival of information: during active periods you get more bars (finer resolution); during quiet periods you get fewer bars (coarser resolution). Research shows this can reduce microstructure pathologies and produce series that are closer to i.i.d. and more suitable for statistical modeling and ML. In particular:

Volume and dollar bars are a common event-time alternative to time bars in quantitative research and are discussed extensively in Advances in Financial Machine Learning (AFML). These bars aim to homogenize information flow by sampling on traded size or value rather than elapsed seconds.

The Volume Clock perspective models market activity in “volume time,” showing that many intraday phenomena (volatility, liquidity shocks) are better explained when time is measured by traded volume instead of seconds.

Related market microstructure work on flow toxicity and liquidity highlights that the risk dealers face is tied to information intensity of order flow, again arguing for activity-based clocks.

How the indicator works (plain English)

Choose your bucket type

Volume : accumulate volume until it meets a threshold.

Dollar Bars : accumulate close × volume until it meets a dollar threshold.

Pick the threshold rule

Dynamic threshold : by default, the script computes a rolling statistic (mean or median) of recent activity to set the next bucket size. This adapts bar size to changing conditions (e.g., busier sessions produce more frequent synthetic bars).

Fixed threshold : optionally override with a constant target (e.g., exactly 100,000 contracts per synthetic bar, or $5,000,000 per dollar bar).

Build the synthetic bar

While a bucket fills, the script tracks:

o_s: first price of the bucket (synthetic open)

h_s: running maximum price (synthetic high)

l_s: running minimum price (synthetic low)

c_s: last price seen (synthetic close)

v_s: cumulative native volume inside the bucket

d_samples: number of native bars consumed to complete the bucket (a proxy for “how fast” the threshold filled)

Emit a new sample

Once the bucket meets/exceeds the threshold, a new synthetic bar is finalized and stored. If overflow occurs (e.g., a single native bar pushes you past the threshold by a lot), the code will emit multiple synthetic samples to account for the extra activity.

Maintain a rolling history efficiently

A ring buffer can overwrite the oldest samples when you hit your Max Stored Samples cap, keeping memory usage stable.

Compute synthetic-space statistics

The script computes an SMA over the last N synthetic closes and basic descriptors like average bars per synthetic sample, mean and standard deviation of synthetic returns, and more. These are all in event time , not clock time.

Inputs and options you will actually use

Data Settings

Sampling Method : Volume or Dollar Bars.

Rolling Lookback : window used to estimate the dynamic threshold from recent activity.

Filter : Mean or Median for the dynamic threshold. Median is more robust to spikes.

Use Fixed? / Fixed Threshold : override dynamic sizing with a constant target.

Max Stored Samples : cap on synthetic history to keep performance snappy.

Use Ring Buffer : turn on to recycle storage when at capacity.

Indicator Settings

SMA over last N samples : moving average in synthetic space . Because its index is sample count, not minutes, it adapts naturally: more updates in busy regimes, fewer in quiet regimes.

Visuals

Show Synthetic Bars : plot the synthetic OHLC candles.

Candle Color Mode :

Green/Red: directional close vs open

Volume Intensity: opacity scales with synthetic size

Neutral: single color

Adaptive: graded by how large the bucket was relative to threshold

Mark new samples : drop a small marker whenever a new synthetic bar prints.

Comparison & Research

Show Time Bars : overlay the native time-based candles to visually compare how the two sampling schemes differ.

How to read it, step by step

Turn on “Synthetic Bars” and optionally overlay “Time Bars.” You will see that during high-activity bursts, synthetic bars print much faster than time bars.

Watch the synthetic SMA . Crosses in synthetic space can be more meaningful because each update represents a roughly comparable amount of traded information.

Use the “Avg Bars per Sample” in the info table as a regime signal. Falling average bars per sample means activity is clustering, often coincident with higher realized volatility.

Try Dollar Bars when price varies a lot but share count does not; they normalize by dollar risk taken in each sample. Volume Bars are ideal when share count is a better proxy for information flow in your instrument.

Quant finance background and citations

Event time vs. clock time : Easley, López de Prado, and O’Hara advocate measuring intraday phenomena on a volume clock to better align sampling with information arrival. This framing helps explain volatility bursts and liquidity droughts and motivates volume-based bars.

Flow toxicity and dealer risk : The same authors show how adverse selection risk changes with the intensity and informativeness of order flow, further supporting activity-based clocks for modeling and risk management.

AFML framework : In Advances in Financial Machine Learning , event-driven bars such as volume, dollar, and imbalance bars are presented as superior sampling units for many ML tasks, yielding more stationary features and fewer microstructure distortions than fixed time bars. ( Alpaca )

Practical use cases

1) Regime-aware moving averages

The synthetic SMA in event time is not fooled by quiet periods: if nothing of consequence trades, it barely updates. This can make trend filters less sensitive to calendar drift and more sensitive to true participation.

2) Breakout logic on “equal-information” samples

The script exposes simple alerts such as breakout above/below the synthetic SMA . Because each bar approximates a constant amount of activity, breakouts are conditioned on comparable informational mass, not arbitrary time buckets.

3) Volatility-adaptive backtests

If you use synthetic bars as your base data stream, most signal rules become self-paced : entry and exit opportunities accelerate in fast markets and slow down in quiet regimes, which often improves the realism of slippage and fill modeling in research pipelines (pair this indicator with strategy code downstream).

4) Regime diagnostics

Avg Bars per Sample trending down: activity is dense; expect larger realized ranges.

Return StdDev (synthetic) rising: noise or trend acceleration in event time; re-tune risk.

Interpreting the info panel

Method : your sampling choice and current threshold.

Total Samples : how many synthetic bars have been formed.

Current Vol/Dollar : how much of the next bucket is already filled.

Bars in Bucket : native bars consumed so far in the current bucket.

Avg Bars/Sample : lower means higher trading intensity.

Avg Return / Return StdDev : return stats computed over synthetic closes .

Research directions you can build from here

Imbalance and run bars

Extend beyond pure volume or dollar thresholds to imbalance bars that trigger on directional order flow imbalance (e.g., buy volume minus sell volume), as discussed in the AFML ecosystem. These often further homogenize distributional properties used in ML. alpaca.markets

Volume-time indicators

Re-compute classical indicators (RSI, MACD, Bollinger) on the synthetic stream. The premise is that signals are updated by traded information , not seconds, which may stabilize indicator behavior in heteroskedastic regimes.

Liquidity and toxicity overlays

Combine synthetic bars with proxies of flow toxicity to anticipate spread widening or volatility clustering. For instance, tag synthetic bars that surpass multiples of the threshold and test whether subsequent realized volatility is elevated.

Dollar-risk parity sampling for portfolios

Use dollar bars to align samples across assets by notional risk, enabling cleaner cross-asset features and comparability in multi-asset models (e.g., correlation studies, regime clustering). AFML discusses the benefits of event-driven sampling for cross-sectional ML feature engineering.

Microstructure feature set

Compute duration in native bars per synthetic sample , range per sample , and volume multiple of threshold as inputs to state classifiers or regime HMMs . These features are inherently activity-aware and often predictive of short-horizon volatility and trend persistence per the event-time literature. ( Alpaca )

Tips for clean usage

Start with dynamic thresholds using Median over a sensible lookback to avoid outlier distortion, then move to Fixed thresholds when you know your instrument’s typical activity scale.

Compare time bars vs synthetic bars side by side to develop intuition for how your market “breathes” in activity time.

Keep Max Stored Samples reasonable for performance; the ring buffer avoids memory creep while preserving a rolling window of research-grade data.

Expected Value Monte CarloI created this indicator after noticing that there was no Expected Value indicator here on TradingView.

The EVMC provides statistical Expected Value to what might happen in the future regarding the asset you are analyzing.

It uses 2 quantitative methods:

Historical Backtest to ground your analysis in long-term, factual data.

Monte Carlo Simulation to project a cone of probable future outcomes based on recent market behavior.

This gives you a data-driven edge to quantify risk, and make more informed trading decisions.

The indicator includes:

Dual analysis: Combines historical probability with forward-looking simulation.

Quantified projections: Provides the Expected Value ($ and %), Win Rate, and Sharpe Ratio for both methods.

Asset-aware: Automatically adjusts its calculations for Stocks (252 trading days) and Crypto (365 days) for mathematical accuracy.

The projection cone shows the mean expected path and the +/- 1 standard deviation range of outcomes.

No repainting

Calculation:

1. Historical Expected Value:

This is a systematic backtest over thousands of bars. It calculates the return Rᵢ for N past trades (buy-and-hold). The Historical EV is the simple average of these returns, giving a baseline performance measure.

Historical EV % = (Σ Rᵢ) / N

2. Monte Carlo Projection:

This projection uses the Geometric Brownian Motion (GBM) model to simulate thousands of future price paths based on the market's recent behavior.

It first measures the drift (μ), or recent trend, and volatility (σ), or recent risk, from the Projection Lookback period. It then projects a final return for each simulation using the core GBM formula:

Projected Return = exp( (μ - σ²/2)T + σ√T * Z ) - 1

(Where T is the time horizon and Z is a random variable for the simulation.)

The purple line on the chart is the average of all simulated outcomes (the Monte Carlo EV). The cone represents one standard deviation of those outcomes.

The dashed lines represent one standard deviation (+/- 1σ) from the average, forming a cone of probable outcomes. Roughly 68% of the simulated paths ended within this cone.

This projection answers the question: "If the recent trend and volatility continue, where is the price most likely to go?"

Here's how to read the indicator

Expected Value ($/%): Is my average trade profitable?

Win Rate: How often can I expect to be right?

Sharpe Ratio: Am I being adequately compensated for the risk I'm taking?

User Guide

Max trade duration (bars): This is your analysis timeframe. Are you interested in the probable outcome over the next month (21 bars), quarter (63 bars), or year (252 bars)?

Position size ($): Set this to your typical trade size to see the Expected Value in real dollar terms.

Projection lookback (bars): This is the most important input for the Monte Carlo model. A short lookback (e.g., 50) makes the projection highly sensitive to recent momentum. Use this to identify potential recency bias. A long lookback (e.g., 252) provides a more stable, long-term projection of trend and volatility.

Historical Lookback (bars): For the historical backtest, more data is always better. Use the maximum that your TradingView plan allows for the most statistically significant results.

Use TP/SL for Historical EV: Check this box to see how the historical performance would have changed if you had used a simple Take Profit and Stop Loss, rather than just holding for the full duration.

I hope you find this indicator useful and please let me know if you have any suggestions. 😊

Mutanabby_AI | Ultimate Algo | Remastered+Overview

The Mutanabby_AI Ultimate Algo Remastered+ represents a sophisticated trend-following system that combines Supertrend analysis with multiple moving average confirmations. This comprehensive indicator is designed specifically for identifying high-probability trend continuation and reversal opportunities across various market conditions.

Core Algorithm Components

**Supertrend Foundation**: The primary signal generation relies on a customizable Supertrend indicator with adjustable sensitivity (1-20 range). This adaptive trend-following tool uses Average True Range calculations to establish dynamic support and resistance levels that respond to market volatility.

**SMA Confirmation Matrix**: Multiple Simple Moving Averages (SMA 4, 5, 9, 13) provide layered confirmation for signal strength. The algorithm distinguishes between regular signals and "Strong" signals based on SMA 4 vs SMA 5 relationship, offering traders different conviction levels for position sizing.

**Trend Ribbon Visualization**: SMA 21 and SMA 34 create a visual trend ribbon that changes color based on their relationship. Green ribbon indicates bullish momentum while red signals bearish conditions, providing immediate visual trend context.

**RSI-Based Candle Coloring**: Advanced 61-tier RSI system colors candles with gradient precision from deep red (RSI ≤20) through purple transitions to bright green (RSI ≥79). This visual enhancement helps traders instantly assess momentum strength and overbought/oversold conditions.

Signal Generation Logic

**Buy Signal Criteria**:

- Price crosses above Supertrend line

- Close price must be above SMA 9 (trend confirmation)

- Signal strength determined by SMA 4 vs SMA 5 relationship

- "Strong Buy" when SMA 4 ≥ SMA 5

- Regular "Buy" when SMA 4 < SMA 5

**Sell Signal Criteria**:

- Price crosses below Supertrend line

- Close price must be below SMA 9 (trend confirmation)

- Signal strength based on SMA relationship

- "Strong Sell" when SMA 4 ≤ SMA 5

- Regular "Sell" when SMA 4 > SMA 5

Advanced Risk Management System

**Automated TP/SL Calculation**: The indicator automatically calculates stop loss and take profit levels using ATR-based measurements. Risk percentage and ATR length are fully customizable, allowing traders to adapt to different market conditions and personal risk tolerance.

**Multiple Take Profit Targets**:

- 1:1 Risk-Reward ratio for conservative profit taking

- 2:1 Risk-Reward for balanced trade management

- 3:1 Risk-Reward for maximum profit potential

**Visual Risk Display**: All risk management levels appear as both labels and optional trend lines on the chart. Customizable line styles (solid, dashed, dotted) and positioning ensure clear visualization without chart clutter.

**Dynamic Level Updates**: Risk levels automatically recalculate with each new signal, maintaining current market relevance throughout position lifecycles.

Visual Enhancement Features

**Customizable Display Options**: Toggle trend ribbon, TP/SL levels, and risk lines independently. Decimal precision adjustments (1-8 decimal places) accommodate different instrument price formats and personal preferences.

**Professional Label System**: Clean, informative labels show entry points, stop losses, and take profit targets with precise price levels. Labels automatically position themselves for optimal chart readability.

**Color-Coded Momentum**: The gradient RSI candle coloring system provides instant visual feedback on momentum strength, helping traders assess market energy and potential reversal zones.

Implementation Strategy

**Timeframe Optimization**: The algorithm performs effectively across multiple timeframes, with higher timeframes (4H, Daily) providing more reliable signals for swing trading. Lower timeframes work well for day trading with appropriate risk adjustments.

**Sensitivity Adjustment**: Lower sensitivity values (1-5) generate fewer but higher-quality signals, ideal for conservative approaches. Higher sensitivity (15-20) increases signal frequency for active trading styles.

**Risk Management Integration**: Use the automated risk calculations as baseline parameters, adjusting risk percentage based on account size and market conditions. The 1:1, 2:1, 3:1 targets enable systematic profit-taking strategies.

Market Application

**Trend Following Excellence**: Primary strength lies in capturing significant trend movements through the Supertrend foundation with SMA confirmation. The dual-layer approach reduces false signals common in single-indicator systems.

**Momentum Assessment**: RSI-based candle coloring provides immediate momentum context, helping traders assess signal strength and potential continuation probability.

**Range Detection**: The trend ribbon helps identify ranging conditions when SMA 21 and SMA 34 converge, alerting traders to potential breakout opportunities.

Performance Optimization

**Signal Quality**: The requirement for both Supertrend crossover AND SMA 9 confirmation significantly improves signal reliability compared to basic trend-following approaches.

**Visual Clarity**: The comprehensive visual system enables rapid market assessment without complex calculations, ideal for traders managing multiple instruments.

**Adaptability**: Extensive customization options allow fine-tuning for specific markets, trading styles, and risk preferences while maintaining the core algorithm integrity.

## Non-Repainting Design

**Educational Note**: This indicator uses standard TradingView functions (Supertrend, SMA, RSI) with normal behavior patterns. Real-time updates on current candles are expected and standard across all technical indicators. Historical signals on closed candles remain fixed and unchanged, ensuring reliable backtesting and analysis.

**Signal Confirmation**: Final signals are confirmed only when candles close, following standard technical analysis principles. The algorithm provides clear distinction between developing signals and confirmed entries.

Technical Specifications

**Supertrend Parameters**: Default sensitivity of 4 with ATR length of 11 provides balanced signal generation. Sensitivity range from 1-20 allows adaptation to different market volatilities and trading preferences.

**Moving Average Configuration**: SMA periods of 8, 9, and 13 create multi-layered trend confirmation, while SMA 21 and 34 form the visual trend ribbon for broader market context.

**Risk Management**: ATR-based calculations with customizable risk percentage ensure dynamic adaptation to market volatility while maintaining consistent risk exposure principles.

Recommended Settings

**Conservative Approach**: Sensitivity 4-5, RSI length 14, higher timeframes (4H, Daily) for swing trading with maximum signal reliability.

**Active Trading**: Sensitivity 6-8, RSI length 8-10, intermediate timeframes (1H) for balanced signal frequency and quality.

**Scalping Setup**: Sensitivity 10-15, RSI length 5-8, lower timeframes (15-30min) with enhanced risk management protocols.

## Conclusion

The Mutanabby_AI Ultimate Algo Remastered+ combines proven trend-following principles with modern visual enhancements and comprehensive risk management. The algorithm's strength lies in its multi-layered confirmation approach and automated risk calculations, providing both novice and experienced traders with clear signals and systematic trade management.

Success with this system requires understanding the relationship between signal strength indicators and adapting sensitivity settings to match current market conditions. The comprehensive visual feedback system enables rapid decision-making while the automated risk management ensures consistent trade parameters.

Practice with different sensitivity settings and timeframes to optimize performance for your specific trading style and risk tolerance. The algorithm's systematic approach provides an excellent framework for disciplined trend-following strategies across various market environments.

Mutanabby_AI __ OSC+ST+SQZMOMMutanabby_AI OSC+ST+SQZMOM: Multi-Component Trading Analysis Tool

Overview

The Mutanabby_AI OSC+ST+SQZMOM indicator combines three proven technical analysis components into a unified trading system, providing comprehensive market analysis through integrated oscillator signals, trend identification, and volatility assessment.

Core Components

Wave Trend Oscillator (OSC): Identifies overbought and oversold market conditions using exponential moving average calculations. Key threshold levels include overbought zones at 60 and 53, with oversold areas marked at -60 and -53. Crossover signals between the two oscillator lines generate entry opportunities, displayed as colored circles on the chart for easy identification.

Supertrend Indicator (ST): Determines overall market direction using Average True Range calculations with a 2.5 factor and 10-period ATR configuration. Green lines indicate confirmed uptrends while red lines signal downtrend conditions. The indicator automatically adapts to market volatility changes, providing reliable trend identification across different market environments.

Squeeze Momentum (SQZMOM): Compares Bollinger Bands with Keltner Channels to identify consolidation periods and potential breakout scenarios. Black squares indicate squeeze conditions representing low volatility periods, green triangles signal confirmed upward breakouts, and red triangles mark downward breakout confirmations.

Signal Generation Logic

Long Entry Conditions:

Green triangles from Squeeze Momentum component

Supertrend line transitioning to green

Bullish crossovers in Wave Trend Oscillator from oversold territory

Short Entry Conditions:

Red triangles from Squeeze Momentum component

Supertrend line transitioning to red

Bearish crossovers in Wave Trend Oscillator from overbought territory

Automated Risk Management

The indicator incorporates comprehensive risk management through ATR-based calculations. Stop losses are automatically positioned at 3x ATR distance from entry points, while three progressive take profit targets are established at 1x, 2x, and 3x ATR multiples respectively. All risk management levels are clearly displayed on the chart using colored lines and informative labels.

When trend direction changes, the system automatically clears previous risk levels and generates new calculations, ensuring all risk parameters remain current and relevant to existing market conditions.

Alert and Notification System

Comprehensive alert framework includes trend change notifications with complete trade setup details, squeeze release alerts for breakout opportunity identification, and trend weakness warnings for active position management. Alert messages contain specific trading pair information, timeframe specifications, and all relevant entry and exit level data.

Implementation Guidelines

Timeframe Selection: Higher timeframes including 4-hour and daily charts provide the most reliable signals for position trading strategies. One-hour charts demonstrate good performance for day trading applications, while 15-30 minute timeframes enable scalping approaches with enhanced risk management requirements.

Risk Management Integration: Limit individual trade risk to 1-2% of total capital using the automatically calculated stop loss levels for precise position sizing. Implement systematic profit-taking at each target level while adjusting stop loss positions to protect accumulated gains.

Market Volatility Adaptation: The indicator's ATR-based calculations automatically adjust to changing market volatility conditions. During high volatility periods, risk management levels appropriately widen, while low volatility conditions result in tighter risk parameters.

Optimization Techniques

Combine indicator signals with fundamental support and resistance level analysis for enhanced signal validation. Monitor volume patterns to confirm breakout strength, particularly when Squeeze Momentum signals develop. Maintain awareness of scheduled economic events that may influence market behavior independent of technical indicator signals.

The multi-component design provides internal signal confirmation through multiple alignment requirements, significantly reducing false signal occurrence while maintaining reasonable trade frequency for active trading strategies.

Technical Specifications

The Wave Trend Oscillator utilizes customizable channel length (default 10) and average length (default 21) parameters for optimal market sensitivity. Supertrend calculations employ ATR period of 10 with factor multiplier of 2.5 for balanced signal quality. Squeeze Momentum analysis uses Bollinger Band length of 20 periods with 2.0 multiplication factor, combined with Keltner Channel length of 20 periods and 1.5 multiplication factor.

Conclusion

The Mutanabby_AI OSC+ST+SQZMOM indicator provides a systematic approach to technical market analysis through the integration of proven oscillator, trend, and momentum components. Success requires thorough understanding of each element's functionality and disciplined implementation of proper risk management principles.

Practice with demo trading accounts before live implementation to develop familiarity with signal interpretation and trade management procedures. The indicator's systematic approach effectively reduces emotional decision-making while providing clear, objective guidelines for trade entry, management, and exit strategies across various market conditions.

Momentum Regression [BackQuant]Momentum Regression

The Momentum Regression is an advanced statistical indicator built to empower quants, strategists, and technically inclined traders with a robust visual and quantitative framework for analyzing momentum effects in financial markets. Unlike traditional momentum indicators that rely on raw price movements or moving averages, this tool leverages a volatility-adjusted linear regression model (y ~ x) to uncover and validate momentum behavior over a user-defined lookback window.

Purpose & Design Philosophy

Momentum is a core anomaly in quantitative finance — an effect where assets that have performed well (or poorly) continue to do so over short to medium-term horizons. However, this effect can be noisy, regime-dependent, and sometimes spurious.

The Momentum Regression is designed as a pre-strategy analytical tool to help you filter and verify whether statistically meaningful and tradable momentum exists in a given asset. Its architecture includes:

Volatility normalization to account for differences in scale and distribution.

Regression analysis to model the relationship between past and present standardized returns.

Deviation bands to highlight overbought/oversold zones around the predicted trendline.

Statistical summary tables to assess the reliability of the detected momentum.

Core Concepts and Calculations

The model uses the following:

Independent variable (x): The volatility-adjusted return over the chosen momentum period.

Dependent variable (y): The 1-bar lagged log return, also adjusted for volatility.

A simple linear regression is performed over a large lookback window (default: 1000 bars), which reveals the slope and intercept of the momentum line. These values are then used to construct:

A predicted momentum trendline across time.

Upper and lower deviation bands , representing ±n standard deviations of the regression residuals (errors).

These visual elements help traders judge how far current returns deviate from the modeled momentum trend, similar to Bollinger Bands but derived from a regression model rather than a moving average.

Key Metrics Provided

On each update, the indicator dynamically displays:

Momentum Slope (β₁): Indicates trend direction and strength. A higher absolute value implies a stronger effect.

Intercept (β₀): The predicted return when x = 0.

Pearson’s R: Correlation coefficient between x and y.

R² (Coefficient of Determination): Indicates how well the regression line explains the variance in y.

Standard Error of Residuals: Measures dispersion around the trendline.

t-Statistic of β₁: Used to evaluate statistical significance of the momentum slope.

These statistics are presented in a top-right summary table for immediate interpretation. A bottom-right signal table also summarizes key takeaways with visual indicators.

Features and Inputs

✅ Volatility-Adjusted Momentum : Reduces distortions from noisy price spikes.

✅ Custom Lookback Control : Set the number of bars to analyze regression.

✅ Extendable Trendlines : For continuous visualization into the future.

✅ Deviation Bands : Optional ±σ multipliers to detect abnormal price action.

✅ Contextual Tables : Help determine strength, direction, and significance of momentum.

✅ Separate Pane Design : Cleanly isolates statistical momentum from price chart.

How It Helps Traders

📉 Quantitative Strategy Validation:

Use the regression results to confirm whether a momentum-based strategy is worth pursuing on a specific asset or timeframe.

🔍 Regime Detection:

Track when momentum breaks down or reverses. Slope changes, drops in R², or weak t-stats can signal regime shifts.

📊 Trade Filtering:

Avoid false positives by entering trades only when momentum is both statistically significant and directionally favorable.

📈 Backtest Preparation:

Before running costly simulations, use this tool to pre-screen assets for exploitable return structures.

When to Use It

Before building or deploying a momentum strategy : Test if momentum exists and is statistically reliable.

During market transitions : Detect early signs of fading strength or reversal.

As part of an edge-stacking framework : Combine with other filters such as volatility compression, volume surges, or macro filters.

Conclusion

The Momentum Regression indicator offers a powerful fusion of statistical analysis and visual interpretation. By combining volatility-adjusted returns with real-time linear regression modeling, it helps quantify and qualify one of the most studied and traded anomalies in finance: momentum.

Rolling Log Returns [BackQuant]Rolling Log Returns