Risk Management Tool [LuxAlgo]Good money management is one of the fundamental pillars of successful trading. With this indicator, we propose a simple way to manage trading positions. This tool shows Profit & Loss (P&L), suggests position size given a certain risk, sets stop losses and take profit levels using fixed price value/percentage/ATR/Range, and can also determine entries from crosses with technical indicators which is particularly handy if you don't want to set an entry manually.

1. Settings

Position Type: Determines if the position should be a "Long" or "Short".

Account Size: Determines the total capital of the trading account.

Risk: The maximum risk amount for a trade. Can be set as a percentage of the account size or as a fixed amount.

Entry Price: Determines the entry price of the position.

Entry From Cross: When enabled, allows to set the entry price where a cross with an external source was produced.

1.1 Stop Loss/Take Profit

Take Profit: Determines the take profit level, which can be determined by a value or percentage.

Stop Loss: Determines the stop loss level, which can be determined by a value or percentage.

2. Usage

One of the main usages of position management tools is to determine the position size to allocate given a specific risk amount and stop-loss. 2% of your capital is often recommended as a risk amount.

Our tool allows setting stop losses and take profits with different methods.

The ATR method sets the stop loss/take profit one ATR away from the entry price, with the ATR period being determined in the drop-down menu next to the selected methods. The range method works similarly but instead of using the ATR, we use a rolling range with a period determined in the drop-down menu next to the selected methods as well.

Unlike the available position management tool on TradingView, the entry can be determined from a cross between the price an an external source. The image above shows entries from the Volatility Stop indicator. This is particularly useful if you set positions based on trailing stops.

Risk

Portfolio Tracker [Anan]█ OVERVIEW

A simple Portfolio Tracker to track your Profit/Loss for any ticker in any market (stock, futures, index, forex, crypto, fund, dr.).

You just need to input (Asset / Quantity / Avg. Buy/Sell Price) and the script will calculate everything.

Also, you can use it for paper trading, or even what-if cases..

█ FEATURES

- Up to 10 positions

- Track your position real-time price and 24H change %

- Calculate your position current value

- Calculate your position cost value

- Calculate Profit/Loss

- Calculate Profit/Loss %

- Change every color in the table as you like.

Pot SizeA little FREE script - which may help people set their trade size and stop levels for bitcoin trades.

NOTE :- This script conveys information that requires "indicator arguments" to be turned on.

TO USE :- To adjust to your requirements, click the cog wheel next to the indicator, and adjust "POT SIZE" (how much dollar you have), "RISK %" (the percentage of your dollar portfolio you would like to risk on this trade) and "BITCOIN AMOUNT" - until the short and long 'stop' lines are in the right place in your estimation, for a stop loss that represents the risk you want in relation to the current price for this trade.

The script takes its reference from the closing price; and doesn't include calculations for spread, fees, true range, and volatility etc. That is left open for anyone to add that if they wish. Anyone using this has to make their own adjustments for such considerations not being in this script and therefore make their own compensations.

Anyone wanting to change anything (because values don't go far enough for you) but doesn't know pinescript, can change the numbers next to "defval", "minval", "maxval", and "step" to their suiting in the script itself.

If you use this, you have to work out for yourself if it is useful for you or not. If you depend on it, you must have your own confidence that the calculations in it are acceptable and correct for your use, and you should check yourself and seek advice before trusting it. I convey no confidence in these calculations or this script, and they must be assumed to be acceptable by you if you use it.

Thanks

M

money managementthis indicator has been designed to make your calculations easier and faster.

you can use this indicator to set tp and sl prices based on your entry price, balance,risk and leverage.

it has been designed only for cryptocurrency market and it is not recommended to use it in other markets!

1- enter your balance in the setting of the indicator.

2- enter risk percentage of your balance.

3- enter your sl percentage.

4- enter your tp percentage.

5- set your leverage if you are trading in futures market.

6- and at last set your entry price.

your position size both in spot market and futures market and the exact price of tp and sl , will be shown top right of the screen.

caution: before using this indicator in real market, please make sure that you understand this indicator's behavior and test it.

--------------------------------------------------------------------

این اندیکاتور برای تسریع محاسبات مدیریت سرمایه و سهولت رعایت آن طراحی شده است.

شما میتوانید با وارد کردن پارامترهاقیمت ورودی، سرمایه کل، ریسک و اهرم، قیمت حد سود و ضرر خود را محاسبه کنید.

همچنین اندازه حجم معاملات شما توسط این اندیکاتور محاسبه خواهد شد.

این اندیکاتور برای بازار کریپتوکارنسی طراحی شده است و استفاده از آن در سایر بازارها پیشنهاد نمیشود.

از بخش تنظیمات اندیکاتورمراحل زیر را انجام دهید:

1- میزان سرمایه خود را در قسمت بالانس وارد کنید

2- میزان ریسک سرمایه در هر معامله را مشخص کنید (به درصد)

3- میزان حد ضرر خود را مشخص کنید (به درصد)

4- میزان حد سود خود را مشخص کنید (به درصد)

5- عدد اهرم خود را وارد کنید

6- قیمت ورود به معامله را وارد کنید

توجه: قبل از استفاده این اندیکاتور در بازار لایو لطفا آن را تست کنید و از کارکرد صحیح آن با مدیریت سرمایه خود اطمینان حاصل فرمایید.

Position Tracker by KrisWatersPosition tracker helps you to know "Stop" and "Take Profit" prices with provided "Entry Price" data. You can use on Long and Short setups.

Position calcCurrent script was created to help faster calculate possible gain or loss from a furure trade. Making money management a bit simpler, by changing values you can adjust proper trade leverage and see possible target values

Heisenberg's Uncertainty BandsHeisenberg's Uncertainty Bands:

This is a volatility indicator to determine and visualize the uncertainty in a securities' price.

In quantum mechanics, the uncertainty principle (also known as Heisenberg's uncertainty principle) is any of a variety of mathematical inequalities asserting a fundamental limit to the accuracy with which the values for certain pairs of physical quantities of a particle, such as position, x, and momentum, p, can be predicted from initial conditions.

It plots a Kalman filter average of the bars inside a higher timeframe bar, to attempt to find the most frequent price in that bar's timespan. To plot what is effectively a MA using POC (IvanLabrie's code, credits to the author).

It derives momentum from relative momentum, yielding results more sensitive to changes.

Then it uses Heisenberg's uncertainty principle to find an uncertainty range, and uses it as the channel distance from the POC MA, meaning price is likely to fluctuate within that range.

Since uncertainty must be greater than h/2, adding fib levels will make it a useful indicator. Essentially they are pseudo-Fibonacci Bollinger Bands, which uses a different calculation.

Benefits:

Prices fluctuate, and it can be helpful to visualize price as a range, rather than a single point or line. This visualization can help in managing risk, determining entries and exits, and prevent losing one's position due to price fluctuations during a trend.

If we use a particle model, the uncertainty principle dictates that it is impossible to predict the price within a range. This is a good model for risk management!

Usage:

There are 5 Fibonacci ratio outer bands that can be turned on or off according to user's preference.

Recommended that the length inputs should be increased in higher timeframes, to visualize trends, shorter timeframes should have lower lengths.

GLHF

- DPT

Annualised Price Volatility %Annualised Price Volatility in percent, also called Instrument Risk, as outlined by Rob Carver in his excellent books, 'Systematic Trading' and 'Leveraged Trading'.

This is written for those who have read one of his books and want to use this tool on TradingView.

Trend strength, oscillators, and volume indicators are all the rage. Finding a great setup is, of course, key. You've decided to go long. Great!

But how much is your capital at risk?

How does that compare with your level of risk tolerance?

When trading, it's key to understand just how risky a certain instrument is. An uptrend is an uptrend, but is it at an annualised volatility of 2% per year or 500% per year? If it's the former, I know I can put a good chunk of capital into trading it. But if its the latter, I don't want to put so much money at risk. Volatility is rarely in a straight line. It's usually up and down.

I won't give the whole game away. To find out more about how to use this concept of risk, I'd highly recommend the books 'Leveraged Trading' and 'Systematic Trading' by Rob Carver.

Do you have any thoughts, ideas, or questions? Let me know in the comments or send me a message! I'd be glad to help you out.

Risk/Reward CalculatorJust a simple risk reward calculator to help indicate the R:R levels of your risk on a trade. The drawing tool doesn't have multiple R capabilities.

Equity Risk PremiumInspired by the article "2020's Best Performing Hedge Fund Warns Of 'Incredible Move' Around The Election" from ZeroHedge:

This script explores the relationship and attempts to find dislocation between equity risk (VIX) and high-yield corporate debt risk (VXHYG, The Cboe VXHYG Index is an estimate of the expected 30-day volatility of the return on iShares' High Yield Grade ETF (HYG). VXHYG is derived by applying the VIX algorithm to options on HYG).

The basic logic is (closing price of VIX / closing price of VXHYG) - 1. When equity risk is high and credit risk is low, the value of premium will be high, and vice-versa.

“'Equity volatility is almost inescapably high. Is that a good form of insurance? The payoff profiles are nothing like they were back in January. Whereas in credit, we’re almost back to where we were in January.

I find today the risk-reward profile of credit to be basically among the worst, relative to other things, I’ve seen in my career,' Weinstein said. 'A VIX at 20 used to be quite a feat. Here we are at 30, and the credit market hasn’t blinked.'

As a result of the gaping divergence between the VIX and credit spreads - the two had moved in tandem for years, but in August the two series blew out as the VIX started rising as spreads kept falling - Weinstein has pounced on the trade, betting on vol compression."

When equity risk premium is high, the market may be forming a local top.

When equity risk premium is low, the market may be forming a local bottom.

Make sure to select your current timeframe on the dropdown menu.

[blackcat] L1 Trading Risk Assessment Indicator Level: 1

Background

Risk assessment is a general term used in many industries to determine the likelihood of losing an asset, loan, or investment. Risk assessment is important in determining how profitable a particular investment is and which techniques are best for risk mitigation. It shows the upward reward versus the risk profile. Risk assessment is important in determining the rate of return an investor would need to earn in order to consider an investment as worth the potential risk.

Function

L1 Trading Risk Assessment Indicator provides a trading risk evaluation mechanism that follows the megatrend. By defining transaction risk as 4 levels: highly risky, risky, safe, and highly safe, the current bar’s evaluation value can be compared with historical bar data to understand the current level of trading risk and the level of trading risk Trend.

Key Signal

h1~h5 --> trading risk level threshold, which can be adjusted according different markets.

currentsafetylevel --> it indicates current bar risk assessment result

Pros and Cons

Pros:

1. according risk level, proper position size can be adjusted

2. know global trend and select propoer time to exit

Cons:

1. no exact long and short entry are disclosed

2. different markets require different thresholds

Remarks

An improved version of KDJ with less satration observed.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

Position Size CalculatorThis is a script to make calculating position size easier. It calculates position size as a percentage of account balance and Risk/Reward based on input values of entry, exit, stoploss and shows the R/R box similar to tradingview's R/R tool. There is an option to toggle showing label and choosing of label text color.

Have to enter the following inputs in order for it to work properly

1. Account Balance : Account balance in either whatever is base currency of account

2. Risk % : Percentage of account balance to lose if stop is hit.

3. Entry

4. Stoploss

5. Target Price

Notes:

- Target Price is required for calculating R/R but is not necessary to calculate position size.

- Formula to calculate position size is : Balance * Risk % / SL %

- Formula to calculate R/R is : TP % / SL %

- SL % = ( Entry - SL ) / Entry * 100

- TP % = (TP - Entry ) / Entry * 100

Thanks to u/Chonky_ for help with feedback.

Risk RangeThis indicator creates risk ranges using implied volatility (VIX) or historical volatility, skewness ( Cboe SKEW or estimate ) and kurtosis.

Daily Risk RangesThis indictor creates daily Risk Ranges using historical volatility, volatility skew and vol-of-vol.

Simple and efficient swing RSI systemHello there,

I am glad to bring you another simple and efficient algorithm.

Its made purely from RSI which can be used directly or inversed. Its suited for swing trading 15 min chart or more minimum.

Can be adapted to all types of financial markets.

Rules for entry are easy : First we have the stop loss and take profits levels. Based on SL , we have the risk % of our equity, where the minimum lot we can trade its setted on 0.1 lots , can be modified tho.

For entries, we have the overbought and oversold levels.

Whenever we cross one of them we enter the trade . We close the trade whenever we reach sl/tp or inverse crosses.

Although its has a low win rate, its a very good system to catch big trends, so there you can recover all the small losses that you had in a untrend market .

Aswell it requires a lot of patience, since a position can be kept for weeks, even months.

Hope you enjoyed it .

Risk Metrics: Crypto VersionRisk Metrics for Crypto.

Market can be set to BTCUSD, BTCEUR, BTCCHF, BTCGBP, BTC1!, BTC2!, SPX, and DTB3

Beta

Correlation

Standard Deviation

Variance

R-squared

Risk Metrics: beta 'β', correl 'ρxy', stdev 'σ', variance 'σ²'Portfolio Risk Metrics (Part I):

beta 'β'

The beta coefficient can be interpreted as follows:

β =1 exactly as volatile as the market

β >1 more volatile than the market

β <1>0 less volatile than the market

β =0 uncorrelated to the market

β <0 negatively correlated to the market

excerpt from the Corporate Finance Institute

correlation coefficient 'ρxy'

The correlation coefficient is a value that indicates the strength of the relationship between variables.

The coefficient can take any values from -1 to 1. The interpretations of the values are:

-1: Perfect negative correlation. The variables tend to move in opposite directions

(i.e., when one variable increases, the other variable decreases).

0: No correlation. The variables do not have a relationship with each other.

1: Perfect positive correlation. The variables tend to move in the same direction

(i.e., when one variable increases, the other variable also increases).

excerpt from the Corporate Finance Institute

standard deviation 'σ'

68% of returns will fall within 1 standard deviation of the arithmetic mean

95% of returns will fall within 2 standard deviations of the arithmetic mean

99% of returns will fall within 3 standard deviations of the arithmetic mean

excerpt from Corporate Finance Institute

variance 'σ²'

In investing, variance is used to compare the relative performance of each asset in a portfolio.

Because the results can be difficult to analyze, standard deviation is often used instead of variance.

In either case, the goal for the investor is to improve asset allocation.

excerpt from Investopedia

Portfolio Metrics = α(Jensen's), β, CAPM(Ra), Sharpe, TreynorPortfolio Metrics...

Standard Deviation

Jensen's Alpha

Beta

Expected Return (CAPM, Ra)

Sharpe Ratio

Treynor Ratio

Trading Psychology - Fear & Greed Index by DGTPsychology of a Market Cycle - Where are we in the cycle?

Before proceeding with the question "where", let's first have a quick look at "What is market psychology?"

Market psychology is the idea that the movements of a market reflect the emotional state of its participants. It is one of the main topics of behavioral economics - an interdisciplinary field that investigates the various factors that precede economic decisions. Many believe that emotions are the main driving force behind the shifts of financial markets and that the overall fluctuating investor sentiment is what creates the so-called psychological market cycles - which is also dynamic.

Stages of Investor Emotions:

* Optimism – A positive outlook encourages us about the future, leading us to buy stocks.

* Excitement – Having seen some of our initial ideas work, we begin considering what our market success could allow us to accomplish.

* Thrill – At this point we investors cannot believe our success and begin to comment on how smart we are.

* Euphoria – This marks the point of maximum financial risk. Having seen every decision result in quick, easy profits, we begin to ignore risk and expect every trade to become profitable.

* Anxiety – For the first time the market moves against us. Having never stared at unrealized losses, we tell ourselves we are long-term investors and that all our ideas will eventually work.

* Denial – When markets have not rebounded, yet we do not know how to respond, we begin denying either that we made poor choices or that things will not improve shortly.

* Fear – The market realities become confusing. We believe the stocks we own will never move in our favor.

* Desperation – Not knowing how to act, we grasp at any idea that will allow us to get back to breakeven.

* Panic – Having exhausted all ideas, we are at a loss for what to do next.

* Capitulation – Deciding our portfolio will never increase again, we sell all our stocks to avoid any future losses.

* Despondency – After exiting the markets we do not want to buy stocks ever again. This often marks the moment of greatest financial opportunity.

* Depression – Not knowing how we could be so foolish, we are left trying to understand our actions.

* Hope – Eventually we return to the realization that markets move in cycles, and we begin looking for our next opportunity.

* Relief – Having bought a stock that turned profitable, we renew our faith that there is a future in investing.

It's hard to predict with certainty where we exactly are in the market cycle, we can only make an educated guess as to the rough stage based on data available. And here comes the study "Trading Psychology - Fear & Greed Index"

Factors taken into account in this study include:

1-Price Momentum : Price Divergence/Convergence versus its Slow Moving Average

2-Strenght : Rate of Return (RoR) also called Return on Investment (ROI) is a performance measure used to evaluate the efficiency of an investment, net gain or loss of an investment over a specified time period, the rate of change in price movement over a period of time to help investors determine the strength

3-Money Flow : Chaikin Money Flow (CMF) is a technical analysis indicator used to measure Money Flow Volume over a set period of time. CMF can be used as a way to further quantify changes in buying and selling pressure and can help to anticipate future changes and therefore trading opportunities. CMF calculations is based on Accumulation/Distribution

4-Market Volatility : CBOE Volatility Index (VIX), the Volatility Index, or VIX, is a real-time market index that represents the market's expectation of 30-day forward-looking volatility. Derived from the price inputs of the S&P 500 index options, it provides a measure of market risk and investors' sentiments. It is also known by other names like "Fear Gauge" or "Fear Index." Investors, research analysts and portfolio managers look to VIX values as a way to measure market risk, fear and stress before they take investment decisions

5-Safe Haven Demand : in this study GOLD demand is assumed

What to look for :

*Fear and Greed Index as explained above,

*Divergencies

Tool tip of the label displayed provides details of references

Conclusion:

As investors, we always get caught up in the day to day price movements, and lose sight of the bigger picture. The biggest crashes happen not when investors are cautious and fearful, it's when they're euphoric and expecting financial instruments to continue going higher. So as we continue investing, don’t forget to stop and ask yourself, where in the chart do you think we are right now? The Market Psychology Cycle shines light on how emotions evolve, fear and greed index can come in handy, provided that it is not the only tool used to make investment decisions. It is easy to look back at market cycles and recognize how the overall psychology changed. Analyzing previous data makes it obvious what actions and decisions would have been the most profitable. However, it is much harder to understand how the market is changing as it goes - and even harder to predict what comes next. Many investors use technical analysis (TA) to attempt to anticipate where the market is likely to go. Investors are advised to keep tabs on fear for potential buying the dips opportunities and view periods of greed as a potential indicator that financial instruments might be overvalued.

Warren Buffett's quote, buy when others are fearful, and sell when others are greedy

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

Disclaimer : The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

Trend Risk Indicator (TRI)The Trend Risk Indicator is a simple bands indicator made of 2 custom averages of candlesticks ranges calculated within the variable “ BandBars ” period.

Upper and lower channel bands width can be adjusted with the “ Deviation ” variable, which act as a simple factor to enlarge the spread between them.

When Close crosses over the upper band, it is a bearish signal and candlesticks are painted in Red.

When Close crosses under the lower band, it’s a bullish signal and candlesticks are painted in Green.

One of the most interesting indicators for 1 minute scalping. Recommended to use on Renko bars.

*drag to chart and pin to scale, also remove borders from candlesticks.

Drawdown SimulatorDrawdown Simulator.

Will simulate a series of percent based stop losses being triggered in a row if you risked x% of capital per trade.

Also simulates what the capital outcome would be if you were in a leveraged position.

Default settings simulate the use of $3000 starting capital balance , 1% Risk per trade and 5 Losing trades in a row with no leverage (1x).

This will not account of commission fees.

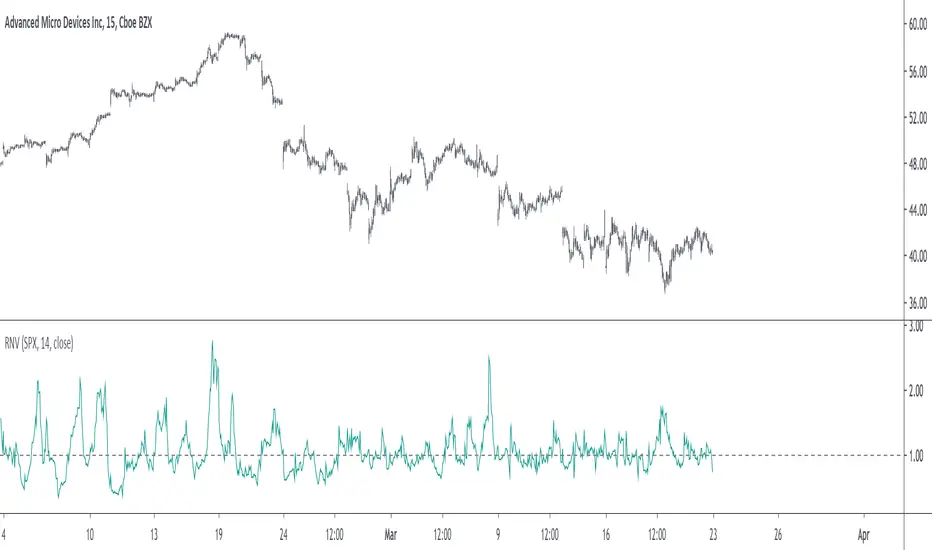

Relative Normalized VolatilityThere are plenty of indicators that aim to measure the volatility (degree of variation) in the price of an instrument, the most well known being the average true range and the rolling standard deviation. Volatility indicators form the key components of most bands and trailing stops indicators, but can also be used to normalize oscillators, they are therefore extremely versatile.

Today proposed indicator aim to compare the estimated volatility of two instruments in order to provide various informations to the user, especially about risk and profitability.

CALCULATION

The relative normalized volatility (RNV) indicator is the ratio between the moving average of the absolute normalized price changes value of two securities, that is:

SMA(|Δ(a)/σ(a)|)

―――――――――――

SMA(|Δ(b)/σ(b)|)

Where a and b are two different securities (note that notation "Δ(x)" refer to the 1st difference of x, and the "||" notation is used to indicate absolute value, for example "|x|" means absolute value of x) .

INTERPRETATION

The indicator aim tell us which security is more volatile between a and b , with a value of the indicator greater than 1 indicating that a is on average more volatile than b over the last length period, while a value lower than 1 indicating that the security b is more on average volatile than a .

The indicator use the current symbol as a , while the second security b must be defined in the setting window (by default the S&P500). Risk and profitability are closely related to volatility, as larger price variations could potentially mean larger losses (but also larger gains), therefore a value of the indicator greater than 1 can indicate that it could be more risked (and profitable) to trade security a .

RNV using AMD (top) volatility against Intel (bottom) volatility.

RNV using EURUSD (top) volatility against USDJPY (bottom) volatility.

Larger values of length will make the indicator fluctuate less often around 1. You can also plot the logarithm of the ratio instead in order to have the indicator centered around 0, it will also help make values originally below 1 have more importance in the scale.

POSSIBLE ERRORS

If you compare different types of markets the indicator might return NaN values, this is because one market might be closed, for example if you compare AMD against BTCUSD with the indicator you will get NaN values. If you really need to compare two markets then increase your time frame, else use an histogram or area plot in order to have a cleaner plot.

CONCLUSION

An original indicator comparing the volatility between two securities has been presented. The choice of posting a volatility indicator has been made by my twitter followers, so if you want to decide which type of indicator i should do next make sure to check my twitter to see if there are polls available (i should do one after every posted indicator).