DAMMU AUTOMATICAL AI ENRTY AND TARGET AND EXITMain Components

Supertrend System –

Detects market trend direction (Buy/Sell zones).

→ Green = Uptrend (Buy)

→ Red = Downtrend (Sell)

SMA Filter –

Uses 50 & 200 moving averages to confirm overall trend.

→ Price above both → Bullish

→ Price below both → Bearish

Buy/Sell Signals –

Generated when Supertrend flips direction and SMA confirms.

→ Triangle up = Buy

→ Triangle down = Sell

Take Profit / Stop Loss Levels –

Automatically calculated after Buy/Sell entry.

→ TP1, TP2, SL shown on chart

ADX (Sideways Zone Filter) –

If ADX < 25 → Market sideways → Avoid trades

Shows “No Trade Zone” area

Smart Money Concepts (SMC) Tools –

🔹 Market structure (HH, HL, LH, LL)

🔹 Order blocks (OB)

🔹 Equal highs/lows

🔹 Fair Value Gaps (FVG)

🔹 Premium & Discount zones

Helps find institutional entry points

Visual Display –

Color-coded background (trend zones)

Labels for buy/sell/structure

Optional FVG and order block boxes

Risk Management –

Input-based position sizing, SL & TP management

(to calculate profit levels and minimize loss)

Cari dalam skrip untuk "gaps"

FX Sessions by m_cptForex Intraday Sessions Indicator, config time in UTC-4. Support 4 main sessions, smooth end-to-start candles mode, without gaps if your sessions has config like:

1) 19:00 - 03:00

2) 02:00 - 03:00

3) 03:00 -11:00

No excluded last candles issue on all TFs.

Working on LTF up to 1h TF since its intraday sessions indicator.

Stock Fundamental Overlay [DarwinDarma]Stock Fundamental Overlay

Stock Fundamental Overlay is a comprehensive valuation indicator that displays multiple fundamental analysis metrics directly on your price chart.

Key Features:

• Graham Number - Benjamin Graham's intrinsic value formula

• Book Value Per Share (BVPS) - Net asset value baseline

• DCF Valuation - Discounted Cash Flow analysis (non-financial stocks)

• DDM Valuation - Dividend Discount Model (dividend-paying stocks)

• Visual Value Zones - Color-coded undervalued/overvalued regions

• Real-time Fundamental Table - Live metrics and valuations

• Price vs Graham Comparison - Quick valuation assessment

• Built-in Alerts - Notification when price crosses key levels

Valuation Models:

• Graham Number: √(22.5 × EPS × BVPS)

• DCF: Customizable discount rate, growth rate, and forecast period

• DDM: Gordon Growth Model for dividend analysis

Visual Elements:

• Plot lines for BVPS, Graham Number, and DCF values

• Shaded value zone between BVPS and Graham Number

• Background coloring: Deep value (below BVPS), Undervalued (below Graham), Overvalued (>1.5x Graham)

• Dynamic table showing all metrics with theme-aware text colors

Special Handling:

• Financial sector detection - DCF disabled for banks/financials where FCF metrics are distorted

• Automatic light/dark theme adaptation

• TTM (Trailing Twelve Months) data for current metrics

How to Use - Value Investing Approach:

1. Identifying Undervalued Stocks:

• Look for price trading BELOW the Graham Number (green zone) - potential value opportunity

• Deep value: Price below BVPS indicates trading below net asset value

• Check "Price vs Graham" % in table - negative values suggest undervaluation

• Compare multiple models: When price is below Graham, DCF, and BVPS simultaneously, stronger buy signal

2. Margin of Safety:

• Benjamin Graham recommended buying at 2/3 of intrinsic value (33% margin of safety)

• Monitor the gap between current price and valuation lines

• Larger gaps = greater margin of safety = lower downside risk

• Use the shaded "Value Zone" as your target buying range

3. Setting Alerts:

• "Price Below Graham Number" - Notifies when stock enters value territory

• "Price Below Book Value" - Extreme value alert for deep value hunters

• "Price Below DCF Value" - Cash flow-based value signal

• Set alerts on watchlist stocks to catch value opportunities

4. Customizing for Your Strategy:

• Conservative investors: Use lower growth rates (3-4%) and higher discount rates (12-15%)

• Growth-value investors: Adjust growth rate (6-8%) for quality compounders

• Dividend investors: Focus on DDM value and Div/Share metrics

• Adjust forecast years based on business predictability (stable = 10 years, cyclical = 5 years)

5. Red Flags to Avoid:

• Negative EPS or FCF (red values in table) - proceed with caution

• Financial sector stocks - Use DDM and Graham, ignore DCF

• Price far above Graham (>1.5x) with red background = overvalued territory

• No fundamental data = "N/A" in table - stock may lack reporting or be too small

• Stock persistently below BVPS for extended periods - potential value trap or business in distress

• Price significantly above ALL models (BVPS, Graham, DCF) - sentiment-driven, lacks intrinsic value foundation (fragile)

⚠️ Important Value Investing Warnings:

• Value Trap Alert: A stock staying below BVPS for months/years may signal fundamental deterioration, asset impairments, or dying industry - not just "cheap." Investigate WHY it's cheap before buying

• Sentiment Bubble Risk: When price trades far above BVPS, Graham Number, AND DCF simultaneously, the stock has no intrinsic value basis. Examples: commodity stocks during boom cycles (gold miners in gold rallies), meme stocks, hype-driven sectors. These are highly fragile and vulnerable to mean reversion

• Cyclical Trap: Commodity/cyclical stocks can appear "cheap" at peak earnings (low P/E, high FCF) but are actually expensive. Normalize earnings across the cycle before valuing

• Quality Matters: Some excellent businesses (asset-light, high ROIC) naturally trade above book value. Don't avoid quality - adjust expectations for business model

6. Monitoring Positions:

• Watch for price approaching or exceeding Graham Number - consider taking profits

• Track EPS and FCF trends quarter-to-quarter in the table

• If fundamentals deteriorate (falling BVPS, negative FCF), reassess thesis

• Use background colors for quick visual check: green = hold/buy, red = overvalued

Perfect for:

Value investors seeking multi-model fundamental analysis, long-term investors comparing intrinsic value to market price, dividend investors evaluating yield stocks, and fundamental traders looking for entry/exit signals.

Note: Only works with stocks that have financial data available. Not applicable to crypto, forex, or futures. This indicator provides analysis tools; always conduct thorough research and due diligence before investing.

Liquidity Swap Detector Ultimate - Cedric JeanjeanAdvanced Smart Money Concepts indicator designed to detect high-probability liquidity sweeps and institutional order flow reversals. This professional-grade tool combines multiple ICT (Inner Circle Trader) strategies to identify optimal entry points.

═══════════════════════════════════════════════════════

📊 KEY FEATURES:

✅ Smart Swing Detection

- Identifies confirmed swing highs and lows using adaptive lookback periods

- Eliminates false signals through double-confirmation logic

- Detects liquidity grabs at key market structure points

✅ Fair Value Gap (FVG) Analysis

- Multi-timeframe FVG detection for enhanced accuracy

- Filters imbalances by minimum size threshold

- Combines current timeframe and higher timeframe FVGs

✅ Advanced Volatility Filter

- ATR-based volatility analysis to avoid low-quality setups

- Adjustable volatility threshold (default 0.35%)

- Ensures entries during optimal market conditions

✅ Precision Signal Generation

- LONG signals: Confirmed swing lows + FVG + volatility confirmation

- SHORT signals: Confirmed swing highs + FVG + volatility confirmation

- Clear visual markers with price labels

✅ Comprehensive Alert System

- Three alert types: Simple, Detailed, JSON (for webhooks)

- Separate LONG/SHORT alert controls

- Compatible with MT5 integration via webhooks

- TradingView native alertcondition support

✅ Professional Dashboard

- Real-time ATR monitoring

- Volatility percentage display

- FVG status indicator

- Alert status tracker

═══════════════════════════════════════════════════════

⚙️ CUSTOMIZABLE PARAMETERS:

🔹 Lookback Swing (1-50): Defines swing detection sensitivity

🔹 ATR Multiplier: Controls wick filter strength

🔹 Volatility Filter: Minimum required market volatility (%)

🔹 FVG Filter: Minimum fair value gap size (%)

🔹 FVG Timeframe: Higher timeframe for multi-TF analysis

🔹 Visual Options: Toggle swing marks, FVG zones, labels

🔹 Alert Controls: Enable/disable LONG/SHORT notifications

═══════════════════════════════════════════════════════

📈 HOW IT WORKS:

1. The indicator scans for confirmed swing points using a robust double-confirmation algorithm

2. Simultaneously analyzes Fair Value Gaps on both current and higher timeframes

3. Validates market volatility to ensure sufficient price movement

4. Generates precise entry signals when all conditions align

5. Triggers customizable alerts for instant notification

═══════════════════════════════════════════════════════

🎯 BEST PRACTICES:

- Use on liquid markets (Forex majors, indices, crypto)

- Recommended timeframes: 15m, 1H, 4H

- Combine with support/resistance for confirmation

- Adjust lookback period based on market volatility

- Test alert settings before live trading

- Use JSON alerts for automated trading integration

═══════════════════════════════════════════════════════

⚡ ALERT CONFIGURATION:

1. Click the Alert icon (bell) in TradingView

2. Select "Liquidity Swap Detector Ultimate - TITAN v6"

3. Choose your preferred alert condition:

- LONG Signal: Only bullish setups

- SHORT Signal: Only bearish setups

- ANY Signal: All trading opportunities

4. Set expiration and notification preferences

5. For MT5 integration: Select "JSON" message type and configure webhook URL

Pivot Regime Anchored VWAP [CHE] Pivot Regime Anchored VWAP — Detects body-based pivot regimes to classify swing highs and lows, anchoring volume-weighted average price lines directly at higher highs and lower lows for adaptive reference levels.

Summary

This indicator identifies shifts between top and bottom regimes through breakouts in candle body highs and lows, labeling swing points as higher highs, lower highs, lower lows, or higher lows. It then draws anchored volume-weighted average price lines starting from the most recent higher high and lower low, providing dynamic support and resistance that evolve with volume flow. These anchored lines differ from standard volume-weighted averages by resetting only at confirmed swing extremes, reducing noise in ranging markets while highlighting momentum shifts in trends.

Motivation: Why this design?

Traders often struggle with static reference lines that fail to adapt to changing market structures, leading to false breaks in volatile conditions or missed continuations in trends. By anchoring volume-weighted average price calculations to body pivot regimes—specifically at higher highs for resistance and lower lows for support—this design creates reference levels tied directly to price structure extremes. This approach addresses the problem of generic moving averages lagging behind swing confirmations, offering a more context-aware tool for intraday or swing trading.

What’s different vs. standard approaches?

- Baseline reference: Traditional volume-weighted average price indicators compute a running total from session start or fixed periods, often ignoring price structure.

- Architecture differences:

- Regime detection via body breakout logic switches between high and low focus dynamically.

- Anchoring limited to confirmed higher highs and lower lows, with historical recalculation for accurate line drawing.

- Polyline rendering rebuilds only on the last bar to manage performance.

- Practical effect: Charts show fewer, more meaningful lines that start at swing points, making it easier to spot confluences with structure breaks rather than cluttered overlays from continuous calculations.

How it works (technical)

The indicator first calculates the maximum and minimum of each candle's open and close to define body highs and lows. It then scans a lookback window for the highest body high and lowest body low. A top regime triggers when the body high from the lookback period exceeds the window's highest, and a bottom regime when the body low falls below the window's lowest. These regime shifts confirm pivots only when crossing from one state to the other.

For top pivots, it compares the new body high against the previous swing high: if greater, it marks a higher high and anchors a new line; otherwise, a lower high. The same logic applies inversely for bottom pivots. Anchored lines use cumulative price-volume products and volumes from the anchor bar onward, subtracting prior cumulatives to isolate the segment. On pivot confirmation, it loops backward from the current bar to the anchor, computing and storing points for the line. New points append as bars advance, ensuring the line reflects ongoing volume weighting.

Initialization uses persistent variables to track the last swing values and anchor bars, starting with neutral states. Data flows from regime detection to pivot classification, then to anchoring and point accumulation, with lines rendered globally on the final bar.

Parameter Guide

Pivot Length — Controls the lookback window for detecting body breakouts, influencing pivot frequency and sensitivity to recent action. Shorter values catch more pivots in choppy conditions; longer smooths for major swings. Default: 30 (bars). Trade-offs/Tips: Min 1; for intraday, try 10–20 to reduce lag but watch for noise; on daily, 50+ for stability.

Show Pivot Labels — Toggles display of text markers at swing points, aiding quick identification of higher highs, lower highs, lower lows, or higher lows. Default: true. Trade-offs/Tips: Disable in multi-indicator setups to declutter; useful for backtesting structure.

HH Color — Sets the line and label color for higher high anchored lines, distinguishing resistance levels. Default: Red (solid). Trade-offs/Tips: Choose contrasting hues for dark/light themes; pair with opacity for fills if added later.

LL Color — Sets the line and label color for lower low anchored lines, distinguishing support levels. Default: Lime (solid). Trade-offs/Tips: As above; green shades work well for bullish contexts without overpowering candles.

Reading & Interpretation

Higher high labels and red lines indicate potential resistance zones where volume weighting begins at a new swing top, suggesting sellers may defend prior highs. Lower low labels and lime lines mark support from a fresh swing bottom, with the line's slope reflecting buyer commitment via volume. Lower highs or higher lows appear as labels without new anchors, signaling possible range-bound action. Line proximity to price shows overextension; crosses may hint at regime shifts, but confirm with volume spikes.

Practical Workflows & Combinations

- Trend following: Enter longs above a rising lower low anchored line after higher low confirmation; filter with rising higher highs for uptrends. Use line breaks as trailing stops.

- Exits/Stops: In downtrends, exit shorts below a higher high line; set aggressive stops above it for scalps, conservative below for swings. Pair with momentum oscillators for divergence.

- Multi-asset/Multi-TF: Defaults suit forex/stocks on 1H–4H; on crypto 15M, shorten length to 15. Scale colors for dark themes; combine with higher timeframe anchors for confluence.

Behavior, Constraints & Performance

Closed-bar logic ensures pivots confirm after the lookback period, with no repainting on historical bars—live bars may adjust until regime shift. No higher timeframe calls, so minimal repaint risk beyond standard delays. Resources include a 2000-bar history limit, label/polyline caps at 200/50, and loops for historical point filling (up to current bar count from anchor, typically under 500 iterations). Known limits: In extreme gaps or low-volume periods, anchors may skew; lines absent until first pivots.

Sensible Defaults & Quick Tuning

Start with the 30-bar length for balanced pivot detection across most assets. For too-frequent pivots in ranges, increase to 50 for fewer signals. If lines lag in trends, reduce to 20 and enable labels for visual cues. In low-volatility assets, widen color contrasts; test on 100-bar history to verify stability.

What this indicator is—and isn’t

This is a structure-aware visualization layer for anchoring volume-weighted references at swing extremes, enhancing manual analysis of regimes and levels. It is not a standalone signal generator or predictive model—always integrate with broader context like order flow or news. Use alongside risk management and position sizing, not as isolated buy/sell triggers.

Many thanks to LuxAlgo for the original script "McDonald's Pattern ". The implementation for body pivots instead of wicks uses a = max(open, close), b = min(open, close) and then highest(a, length) / lowest(b, length). This filters noise from the wicks and detects breakouts over/under bodies. Unusual and targeted, super innovative.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Realtime RenkoI've been working on real-time renko for a while as a coding challenge. The interesting problem here is building renko bricks that form based on incoming tick data rather than waiting for bar closes. Every tick that comes through gets processed immediately, and when price moves enough to complete a brick, that brick closes and a new one opens right then. It's just neat because you can run it and it updates as you'd expect with renko, forming bricks based purely on price movement happening in real time rather than waiting for arbitrary time intervals to pass.

The three brick sizing methods give you flexibility in how you define "enough movement" to form a new brick. Traditional renko uses a fixed price range, so if you set it to 10 ticks, every brick represents exactly 10 ticks of movement. This works well for instruments with stable tick sizes and predictable volatility. ATR-based sizing calculates the average true range once at startup using a weighted average across all historical bars, then divides that by your brick value input. If you want bricks that are one full ATR in size, you'd use a brick value of 1. If you want half-ATR bricks, use 2. This inverted relationship exists because the calculation is ATR divided by your input, which lets you work with multiples and fractions intuitively. Percentage-based sizing makes each brick a fixed percentage move from the previous brick's close, which automatically scales with price level and works well for instruments that move proportionally rather than in absolute tick increments.

The best part about this implementation is how it uses varip for state management. When you first load the indicator, there's no history at all. Everything starts fresh from the moment you add it to your chart because varip variables only exist in real-time. This means you're watching actual renko bricks form from real tick data as it arrives. The indicator builds its own internal history as it runs, storing up to 250 completed bricks in memory, but that history only exists for the current session. Refresh the page or reload the indicator and it starts over from scratch.

The visual implementation uses boxes for brick bodies and lines for wicks, drawn at offset bar indices to create the appearance of a continuous renko chart in the indicator pane. Each brick occupies two bar index positions horizontally, which spaces them out and makes the chart readable. The current brick updates in real time as new ticks arrive, with its high, low, and close values adjusting continuously until it reaches the threshold to close and become finalized. Once a brick closes, it gets pushed into the history array and a new brick opens at the closing level of the previous one.

What makes this especially useful for debugging and analysis are the hover tooltips on each brick. Clicking on any brick brings up information showing when it opened with millisecond precision, how long it took to form from open to close, its internal bar index within the renko sequence, and the brick size being used. That time delta measurement is particularly valuable because it reveals the pace of price movement. A brick that forms in five seconds indicates very different market conditions than one that takes three minutes, even though both bricks represent the same amount of price movement. You can spot acceleration and deceleration in trend development by watching how quickly consecutive bricks form.

The pine logs that generate when bricks close serve as breadcrumbs back to the main chart. Every time a brick finalizes, the indicator writes a log entry with the same information shown in the tooltip. You can click that log entry and TradingView jumps your main chart to the exact timestamp when that brick closed. This lets you correlate renko brick formation with what was happening on the time-based chart, which is critical for understanding context. A brick that closed during a major news announcement or at a key support level tells a different story than one that closed during quiet drift, and the logs make it trivial to investigate those situations.

The internal bar indexing system maintains a separate count from the chart's bar_index, giving each renko brick its own sequential number starting from when the indicator begins running. This makes it easy to reference specific bricks in your analysis or when discussing patterns with others. The internal index increments only when a brick closes, so it's a pure measure of how many bricks have formed regardless of how much chart time has passed. You can match these indices between the visual bricks and the log entries, which helps when you're trying to track down the details of a specific brick that caught your attention.

Brick overshoot handling ensures that when price blows through the threshold level instead of just barely touching it, the brick closes at the threshold and the excess movement carries over to the next brick. This prevents gaps in the renko sequence and maintains the integrity of the brick sizing. If price shoots up through your bullish threshold and keeps going, the current brick closes at exactly the threshold level and the new brick opens there with the overshoot already baked into its initial high. Without this logic, you'd get renko bricks with irregular sizes whenever price moved aggressively, which would undermine the whole point of using fixed-range bricks.

The timezone setting lets you adjust timestamps to your local time or whatever reference you prefer, which matters when you're analyzing logs or comparing brick formation times across different sessions. The time delta formatter converts raw milliseconds into human-readable strings showing days, hours, minutes, and seconds with fractional precision. This makes it immediately clear whether a brick took 12.3 seconds or 2 minutes and 15 seconds to form, without having to parse millisecond values mentally.

This is the script version that will eventually be integrated into my real-time candles library. The library version had an issue with tooltips not displaying correctly, which this implementation fixes by using a different approach to label creation and positioning. Running it as a standalone indicator also gives you more control over the visual settings and makes it easier to experiment with different brick sizing methods without affecting other tools that might be using the library version.

What this really demonstrates is that real-time indicators in Pine Script require thinking about state management and tick processing differently than historical indicators. Most indicator code assumes bars are immutable once closed, so you can reference `close ` and know that value will never change. Real-time renko throws that assumption out because the current brick is constantly mutating with every tick until it closes. Using varip for state variables and carefully tracking what belongs to finalized bricks versus the developing brick makes it possible to maintain consistency while still updating smoothly in real-time. The fact that there's no historical reconstruction and everything starts fresh when you load it is actually a feature, not a limitation, because you're seeing genuine real-time brick formation rather than some approximation of what might have happened in the past.

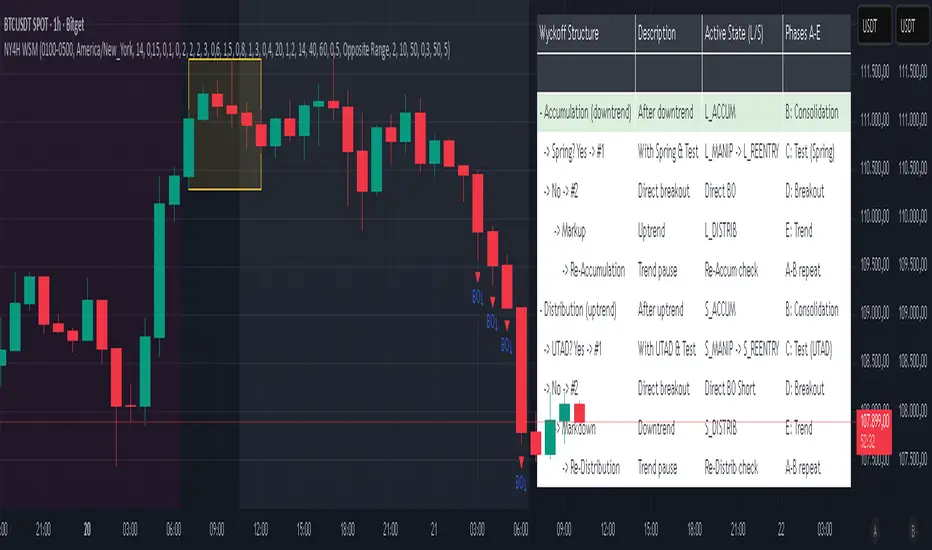

NY 4H Wyckoff State Machine [CHE] NY 4H Wyckoff State Machine — Full (Re-Entry, Breakout, Wick, Re-Accum/Distrib, Dynamic Table) — One-Candle Wyckoff Re-Entry (OCWR)

Summary

OCWR operationalizes a one-candle session workflow: mark the first four-hour New York candle, fix its high and low as the session range when the window closes, and drive entries through a Wyckoff-style state machine on intraday bars. The script adds an ATR-scaled buffer around the range and requires multi-bar acceptance before treating breaks or re-entries as valid. Optional wick-cluster evidence, a proximity retest, and simple volume or RSI gates increase selectivity. Background tints expose regimes, shapes mark events, a dynamic table explains the current state, and hidden plots supply alert payloads. The design reduces random flips and makes state transitions auditable without higher-timeframe calls.

Origin and name

Method name: One-Candle Wyckoff Re-Entry (OCWR)

Transcript origin: The source idea is a “stupid simple one-candle scalping” routine: mark the first New York four-hour candle (commonly between one and five in the morning New York time), drop to five minutes, observe accumulation inside, wait for a manipulation move outside, then trade the re-entry back inside. Stops go beyond the excursion extreme; targets are either a fixed reward multiple or the opposite side of the range. Preference is given to several manipulation candles. This indicator codifies that workflow with explicit states, acceptance counters, buffers, and optional quality filters. Any external performance claims are not part of the code.

Motivation: Why this design?

Session levels are widely respected, yet single-bar breaches around them are noisy. OCWR separates range discovery from trade logic. It locks the range at the end of the window, applies an ATR-scaled buffer to ignore marginal oversteps, and requires acceptance over several bars for breaks and re-entries. Wick evidence and optional retest proximity help confirm that an excursion likely cleared liquidity rather than launched a trend. This yields cleaner transitions from test to commitment.

What’s different vs. standard approaches?

Baseline: Static session lines or one-shot Wyckoff tags without process control.

Architecture: Dual long and short state machines; ATR-buffered edges; multi-bar acceptance for breaks and re-entries; optional wick dominance and cluster checks; optional retest tolerance; direct and opposite breakout paths; cooldown after fires; distribution timeout; dynamic table with highlighted row.

Practical effect: Fewer single-bar head-fakes, clearer hand-offs, and on-chart explanations of the machine’s view.

Wyckoff structure by example — OCWR on five minutes

One-candle setup:

On the four-hour chart, mark the first New York candle’s high and low, then switch to five minutes. Solid lines show the fixed range; dashed lines show ATR-buffered edges.

Long path (verbal mapping):

Phase A, Stopping Action: Price stabilizes inside the range.

Phase B, Consolidation: Sustained balance while the window is closed and after the range is fixed.

Phase C, Test (Spring): Excursion below the buffered low with preference for several outside bars and dominant lower wicks, then a return inside.

Re-entry acceptance: A required run of inside bars validates the test.

Phase D, Breakout to Markup: Long signal fires; stop beyond the excursion extreme; objective is the opposite range or a fixed reward multiple.

Phase E, Trend (Markup) and Re-Accumulation: Advance continues until target, stop, confirmation back against the box, or timeout. A pause inside trend may register as re-accumulation.

Short path mirrors the above: A UTAD-style move forms above the buffered high, then re-entry leads to Markdown and possible re-distribution.

Variant map (verbal):

Accumulation after a downtrend: with Spring and Test, or without Spring; both proceed to Markup and may pause in Re-Accumulation.

Distribution after an uptrend: with UTAD and Test, or without UTAD; both proceed to Markdown and may pause in Re-Distribution.

Note: Phases A through E occur within each variant and are not separate variants.

How it works (technical)

Session window: A configurable four-hour New York window records its high and low. At window end, the bounds are fixed for the session.

ATR buffer: A margin above and below the fixed range discourages triggers from tiny oversteps.

Inside and outside: Users choose close-based or wick-based detection. Overshoot requirements are expressed verbally as a fraction of the range with an optional absolute minimum.

Manipulation tracking: The machine counts bars spent outside and records the side extreme.

Re-entry acceptance: After a return inside, a specified number of inside bars must print before acceptance.

Direct and opposite breakouts: Direct breakouts from accumulation and opposite breakouts after manipulation are supported, subject to acceptance and optional filters.

Targets and exits: Choose the opposite boundary or a fixed reward multiple. Distribution ends on target, stop, confirmation back against the range, or timeout.

Context filters (optional): Volume above a scaled SMA, RSI thresholds, and a trend SMA for simple regime context.

Diagnostics: Background tints for regimes; arrows for re-entries; triangles for breakouts; table with row highlights; hidden plots for alert values.

Central table (Wyckoff console)

The table sits top-right and explains the machine’s stance. Columns: Structure label, plain-English description, active state pair for long and short, and human phase tags. Rows: Start and range building; accumulation branch with Spring and Test as well as direct breakout; Markup and re-accumulation; distribution branch with UTAD and Test as well as direct short breakout; Markdown and re-distribution. Only the active state cell is rewritten each last bar, for example “L_ACCUM slash S_ACCUM”. Row highlighting is context-aware: accumulation, Spring or UTAD, breakout, Markup or Markdown, and re-accumulation or re-distribution checks can highlight independently so users see simultaneous conditions. The table is created once, updated only on the last bar for efficiency, and functions as a read-only console to audit why a signal fired and where the path currently sits.

Parameter Guide

Session window and time zone: First four hours of New York by default; time zone “America/New_York”.

ATR length and buffer factor: Control buffer size; larger reduces sensitivity, smaller reacts faster.

Minimum overshoot (fraction and absolute): Demand meaningful extension beyond the buffer.

Break mode: Close-based is stricter; wick-based is more reactive.

Acceptance counts: Separate counts for break, re-entry, and opposite breakout; higher values reduce noise.

Minimum bars outside: Ensures manipulation is not a single spike.

Wick detection and clusters (optional): Dominance thresholds and cluster size within a short window.

Retest required and tolerance (optional): Gate re-entry by proximity to the buffered edge.

Volume and RSI filters (optional): Simple gates on activity and momentum.

TP mode and reward multiple: Opposite range or fixed multiple.

Cooldown and distribution timeout: Rate-limit signals and prevent endless distribution.

Visualization toggles: Background phases, labels, table, and helper lines.

Reading & Interpretation

Solid lines are the fixed session bounds; dashed lines are buffers. Backgrounds tint accumulation, manipulation, and distribution. Arrows show accepted re-entries; triangles show direct or opposite breakouts. Labels can summarize entry, stop, target, and risk. The table highlights the active row and the current state pair.

Practical Workflows & Combinations

OCWR baseline: Each morning, mark the New York four-hour candle, move to five minutes, prefer multi-bar manipulation outside, then wait for a qualified re-entry inside. Stop beyond the excursion extreme. Target the opposite range for conservative management or a fixed multiple for uniform sizing.

Trend following: Favor direct breakouts with trend alignment and no contradictory wick evidence.

Quality control: When noise rises, increase acceptance, raise the buffer factor, enable retest, and require wick clusters.

Discretionary confluences: Fair-value gaps and trend lines can be added by the user; they are not computed by this script.

Behavior, Constraints & Performance

Closed-bar confirmation is recommended when you require finality; live-bar conditions can change until close. The script does not call higher-timeframe data. It uses arrays, lines, labels, boxes, and a table; maximum bars back is five thousand; table updates are last-bar only. Known limits include compressed buffers in quiet sessions, unreliable wick evidence in thin markets, and session misalignment if the platform time zone is not New York.

Sensible Defaults & Quick Tuning

Start with ATR length fourteen, buffer factor near zero point fifteen, overshoot fraction near zero point ten, acceptance counts of two, minimum outside duration three, retest required on.

Too many flips: increase acceptance, raise buffer, enable retest, and tighten wick thresholds.

Too slow: reduce acceptance, lower buffer, switch to wick-based breaks, disable retest.

Noisy wicks: increase minimum wick ratio and cluster size, or disable wick detection.

What this indicator is—and isn’t

A session-anchored visualization and signal layer that formalizes a Wyckoff-style re-entry and breakout workflow derived from a single four-hour New York candle. It is not predictive and not a complete trading system. Use with structure analysis, risk controls, and position management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Smart Money Concepts Pro – OB, FVG, Liquidity + Trade SetupsThis script is a complete Smart Money Concepts (SMC) toolkit designed for traders who want clean and actionable charts without clutter.

It combines the most important institutional concepts into one indicator:

Order Blocks (OB): auto-detection of bullish and bearish order blocks with mitigation tracking, merging and TTL (time-to-live).

Fair Value Gaps (FVG): automatic gap recognition with size filters, mitigation tracking and lifetime control.

Liquidity Pools (EQH/EQL): equal highs and equal lows marked with tolerance (ATR-based or fixed).

Break of Structure (BOS): up/down structure shifts plotted directly on the chart.

Multi-Timeframe (HTF): option to use higher timeframe data (e.g. H4, Daily) for stronger zones.

Trend Filter: show zones only in the direction of market structure.

Trade Setups: automatic signals for OB Retest + Trend setups, with entry, stop-loss and take-profit levels (custom R-R).

Flexible Zone Extension: choose between extending zones to the live bar or fixed box width for a cleaner look when scrolling.

Features

Fully customizable (pivot length, ATR filters, box width, TTL, zone colors)

Separate presets for Scalping, Intraday, Swing trading styles

Visual trade planning with entry/SL/TP lines and optional labels

Works across all markets (crypto, forex, indices, stocks)

How to use

Bias: identify overall direction (BOS + HTF zones).

Wait: for price to return to an unmitigated OB or FVG.

Entry: take the setup signal (OB retest + trend filter).

Risk: stop-loss at opposite OB boundary.

Target: TP based on chosen R-R multiple (default 2R).

⚡ Whether you scalp short-term moves or swing trade HTF zones, this indicator gives you a clear institutional edge in spotting supply/demand imbalances and high-probability setups.

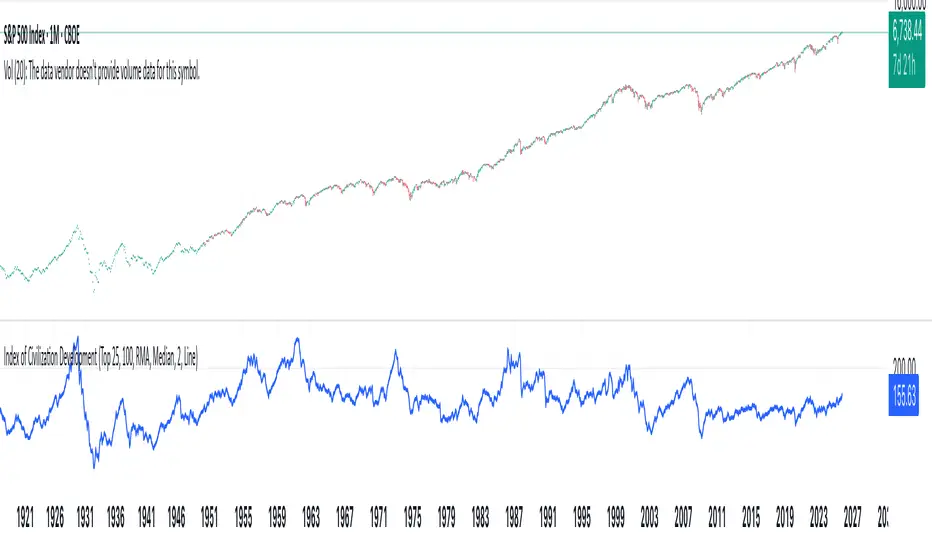

Index of Civilization DevelopmentIndex of Civilization Development Indicator

This Pine Script (version 6) creates a custom technical indicator for TradingView, titled Index of Civilization Development. It generates a composite index by averaging normalized stock market performances from a selection of global country indices. The normalization is relative to each index's 100-period simple moving average (SMA), scaled to a percentage (100% baseline). This allows for a comparable "development" or performance metric across diverse markets, potentially highlighting trends in global economic or "civilizational" progress based on equity markets.The indicator plots as a single line in a separate pane (non-overlay) and is designed to handle up to 40 symbols to respect TradingView's request.security() call limits.Key FeaturesComposite Index Calculation: Fetches the previous bar's close (close ) and its 100-period SMA for each selected symbol.

Normalizes each: (close / SMA(100)) * 100.

Averages the valid normalizations (ignores invalid/NA data) to produce a single "Index (%)" value.

Symbol Selection Modes:Top N Countries: Selects from a predefined list of the top 50 global stock indices (by market cap/importance, e.g., SPX for USA, SHCOMP for China). Options: Top 5, 15, 25, or 50.

Democratic Countries: ~38 symbols from democracies (e.g., SPX, NI225, NIFTY; based on democracy indices ≥6/10, including flawed/parliamentary systems).

Dictatorships: ~12 symbols from authoritarian/hybrid regimes (e.g., SHCOMP, TASI, IMOEX; scores <6/10).

Customization:Line color (default: blue).

Line width (1-5, default: 2).

Line style: Solid line (default), Stepline, or Circles.

Data Handling:Uses request.security() with lookahead enabled for real-time accuracy, gaps off, and invalid symbol ignoring.

Runs calculations on every bar, with max_bars_back=2000 for historical depth.

Arrays are populated only on the first bar (barstate.isfirst) for efficiency.

Predefined Symbol Lists (Examples)Top 50: SPX (USA), SHCOMP (China), NI225 (Japan), ..., BAX (Bahrain).

Democratic: Focuses on free-market democracies like USA, Japan, UK, Canada, EU nations, Australia, etc.

Dictatorships: Authoritarian markets like China, Saudi Arabia, Russia, Turkey, etc.

Usage TipsAdd to any chart (e.g., daily/weekly timeframe) to view the composite line.

Ideal for macro analysis: Compare democratic vs. authoritarian performance, or track "top world" equity health.

Potential Limitations: Relies on TradingView's symbol availability; some exotic indices (e.g., KWSEIDX) may fail if not supported. The 40-symbol cap prevents errors.

Interpretation: Values >100 indicate above-trend performance; <100 suggest underperformance relative to recent averages.

This script blends financial data with geopolitical categorization for a unique "civilization index" perspective on global markets. For modifications, ensure symbol tickers match TradingView's format.

Swing Points LiquiditySwing Points Liquidity

Unlock advanced swing detection and liquidity zone marking for smarter trading decisions.

Overview:

Swing Points Liquidity automatically identifies key swing highs and swing lows using a five-candle “palm” structure, marking each significant price turn with precise labels: “BSL swing high” for potential bearish liquidity and “SSL swing low” for potential bullish liquidity. This transparent swing logic provides a robust way to highlight areas where price is most likely to react—making it an invaluable tool for traders applying Smart Money Concepts, supply and demand, or liquidity-based strategies.

How It Works:

The indicator scans every candle on your chart to detect and label swing highs and lows.

A swing high (“BSL swing high”) is identified when a central candle’s high is greater than the highs of the previous two and next two candles.

A swing low (“SSL swing low”) is identified when a central candle’s low is lower than the lows of the previous two and next two candles.

Labels are plotted for every detected swing point, providing clear visualization of important market liquidity levels on any symbol and timeframe.

How to Use:

Liquidity levels marked by the indicator are potential price reversal zones. To optimize your entries, combine these levels with confirmation signals such as reversal candlestick patterns, order blocks, or fair value gaps (FVGs).

When you see a “BSL swing high” or “SSL swing low” label, observe the price action at that area—if a reliable reversal pattern or order block/FVG forms, it can signal a high-probability trade opportunity.

These marked liquidity swings are also excellent for locating confluence zones, setting stop losses, and identifying where institutional activity or smart money may trigger significant moves. Always use market structure and price action in conjunction with these levels for greater consistency and confidence in your trading.

Features:

Customizable label display for swing highs (BSL) and swing lows (SSL)

Automatic detection using robust 5-candle palm logic

Works with all symbols and chart timeframes

Lightweight, clear visual style—easy for manual and algorithmic traders

Notes:

The indicator requires at least two candles both before and after each swing point, so labels will start appearing after enough historical data is loaded.

For deeper historical analysis, simply scroll left or zoom out on your chart to load more candles—the indicator will automatically process and display swing points on all available data.

Outside Candle Session Breakout [CHE]Outside Candle Session Breakout

Session - anchored HTF levels for clear market-structure and precise breakout context

Summary

This indicator is a relevant market-structure tool. It anchors the session to the first higher-timeframe bar, then activates only when the second bar forms an outside condition. Price frequently reacts around these anchors, which provides precise breakout context and a clear overview on both lower and higher timeframes. Robustness comes from close-based validation, an adaptive volatility and tick buffer, first-touch enforcement, optional retest, one-signal-per-session, cooldown, and an optional trend filter.

Pine version: v6. Overlay: true.

Motivation: Why this design?

Short-term breakout tools often trigger during noise, duplicate within the same session, or drift when volatility shifts. The core idea is to gate signals behind a meaningful structure event: a first-bar anchor and a subsequent outside bar on the session timeframe. This narrows attention to structurally important breaks while adaptive buffering and debouncing reduce false or mid-run triggers.

What’s different vs. standard approaches?

Baseline: Simple high-low breaks or fixed buffers without session context.

Architecture: Session-anchored first-bar high/low; outside-bar gate; close-based confirmation with an adaptive ATR and tick buffer; first-touch enforcement; optional retest window; one-signal-per-session and cooldown; optional EMA trend and slope filter; higher-timeframe aggregation with lookahead disabled; themeable visuals and a range fill between levels.

Practical effect: Cleaner timing at structurally relevant levels, fewer redundant or late triggers, and better multi-timeframe situational awareness.

How it works (technical)

The chart timeframe is mapped to an analysis timeframe and a session timeframe.

The first session bar defines the anchor high and low. The setup becomes active only after the next bar forms an outside range relative to that first bar.

While active, the script tracks these anchors and checks for a breakout beyond a buffered threshold, using closing prices or wicks by preference.

The buffer scales with volatility and is limited by a minimum tick floor. First-touch enforcement avoids mid-run confirmations.

Optional retest requires a pullback to the raw anchor followed by a new close beyond the buffered level within a user window.

Optional trend gating uses an EMA on the analysis timeframe, including an optional slope requirement and price-location check.

Higher-timeframe data is requested with lookahead disabled. Values can update during a forming higher-timeframe bar; waiting and confirmation mitigate timing shifts.

Parameter Guide

Enable Long / Enable Short — Direction toggles. Default: true / true. Reduces unwanted side.

Wait Candles — Minimum bars after outside confirmation before entries. Default: five. More waiting increases stability.

Close-based Breakout — Confirm on candle close beyond buffer. Default: true. For wick sensitivity, disable.

ATR Buffer — Enables adaptive volatility buffer. Default: true.

ATR Multiplier — Buffer scaling. Default: zero point two. Increase to reduce noise.

Ticks Buffer — Minimum buffer in ticks. Default: two. Protects in quiet markets.

Cooldown Bars — Blocks new signals after a trigger. Default: three.

One Signal per Session — Prevents duplicates within a session. Default: true.

Require Retest — Pullback to raw anchor before confirming. Default: false.

Retest Window — Bars allowed for retest completion. Default: five.

HTF Trend Filter — EMA-based gating. Default: false.

EMA Length — EMA period. Default: two hundred.

Slope — Require EMA slope direction. Default: true.

Price Above/Below EMA — Require price location relative to EMA. Default: true.

Show Levels / Highlight Session / Show Signals — Visual controls. Default: true.

Color Theme — “Blue-Green” (default), “Monochrome”, “Earth Tones”, “Classic”, “Dark”.

Time Period Box — Visibility, size, position, and colors for the info box. (Optional)

Reading & Interpretation

The two level lines represent the session’s first-bar high and low. The filled band illustrates the active session range.

“OUT” marks that the outside condition is confirmed and the setup is live.

“LONG” or “SHORT” appears only when the breakout clears buffer, debounce, and optional gates.

Background tint indicates sessions where the setup is valid.

Alerts fire on confirmed long or short breakout events.

Practical Workflows & Combinations

Trend-following: Keep close-based validation, ATR buffer near the default, one-signal-per-session enabled; add EMA trend and slope for directional bias.

Retest confirmation: Enable retest with a short window to prioritize cleaner continuation after a pullback.

Lower-timeframe scalping: Reduce waiting and cooldown slightly; keep a small tick buffer to filter micro-whips.

Swing and position context: Increase ATR multiplier and waiting; maintain once-per-session to limit duplicates.

Timeframe Tiers and Trader Profiles

The script adapts its internal mapping based on the chart timeframe:

Under fifteen minutes → Analysis: one minute; Session: sixty minutes. Useful for scalpers and high-frequency intraday reads.

Between fifteen and under sixty minutes → Analysis: fifteen minutes; Session: one day. Suits day traders who need intraday alignment to the daily session.

Between sixty minutes and under one day → Analysis: sixty minutes; Session: one week. Serves intraday-to-swing transitions and end-of-day planning.

Between one day and under one week → Analysis: two hundred forty minutes; Session: two weeks. Fits swing traders who monitor multi-day structure.

Between one week and under thirty days → Analysis: one day; Session: three months. Supports position traders seeking quarterly context.

Thirty days and above → Analysis: one day; Session: twelve months. Provides a broad annual anchor for macro context.

These tiers are designed to keep anchors meaningful across regimes while preserving responsiveness appropriate to the trader profile.

Behavior, Constraints & Performance

Signals can be validated on closed bars through close-based logic; enabling this reduces intrabar flicker.

Higher-timeframe values may evolve during a forming bar; waiting parameters and the outside-bar gate reduce, but do not remove, this effect.

Resource footprint is light; the script uses standard indicators and a single higher-timeframe request per stream.

Known limits: rare setups during very quiet periods, sensitivity to gaps, and reduced reliability on illiquid symbols.

Sensible Defaults & Quick Tuning

Start with close-based validation on, ATR buffer on with a multiplier near zero point two, tick buffer two, cooldown three, once-per-session on.

Too many flips: increase the ATR multiplier and cooldown; consider enabling the EMA filter and slope.

Too sluggish: reduce the ATR multiplier and waiting; disable retest.

Choppy conditions: keep close-based validation, increase tick buffer, shorten the retest window.

What this indicator is—and isn’t

This is a visualization and signal layer for session-anchored breakouts with stability gates. It is not a complete trading system, risk framework, or predictive engine. Combine it with structured analysis, position sizing, and disciplined risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Fair Value Gap ZonesDescription

This script automatically detects and highlights Fair Value Gaps (FVGs) on any chart and timeframe.

It identifies bullish and bearish imbalance zones using candle-to-candle price displacement and shades them visually on the chart for easy reference.

Bullish FVGs are marked with dark green zones, showing areas where price may later return before continuing upward.

Bearish FVGs are shaded in light red, indicating potential retracement zones in downtrends.

All zones extend forward automatically, updating dynamically as new candles form.

Designed for traders who use Smart Money Concepts (SMC) or ICT-style analysis, this tool helps visualize market inefficiencies and potential reaction points with clear, minimal visuals.

ALISH WEEK LABELS THE ALISH WEEK LABELS

Overview

This indicator programmatically delineates each trading week and encapsulates its realized price range in a live-updating, filled rectangle. A week is defined in America/Toronto time from Monday 00:00 to Friday 16:00. Weekly market open to market close, For every week, the script draws:

a vertical start line at the first bar of Monday 00:00,

a vertical end line at the first bar at/after Friday 16:00, and

a white, semi-transparent box whose top tracks the highest price and whose bottom tracks the lowest price observed between those two temporal boundaries.

The drawing is timeframe-agnostic (M1 → 1D): the box expands in real time while the week is open and freezes at the close boundary.

Time Reference and Session Boundaries

All scheduling decisions are computed with time functions called using the fixed timezone string "America/Toronto", ensuring correct behavior across DST transitions without relying on chart timezone. The start condition is met at the first bar where (dayofweek == Monday && hour == 0 && minute == 0); on higher timeframes where an exact 00:00 bar may not exist, a fallback checks for the first Monday bar using ta.change(dayofweek). The close condition is met on the first bar at or after Friday 16:00 (Toronto), which guarantees deterministic closure on intraday and higher timeframes.

State Model

The indicator maintains minimal persistent state using var globals:

week_open (bool): whether the current weekly session is active.

wk_hi / wk_lo (float): rolling extrema for the active week.

wk_box (box): the graphical rectangle spanning × .

wk_start_line and a transient wk_end_line (line): vertical delimiters at the week’s start and end.

Two dynamic arrays (boxes, vlines) store object handles to support bounded history and deterministic garbage collection.

Update Cycle (Per Bar)

On each bar the script executes the following pipeline:

Start Check: If no week is open and the start condition is satisfied, instantiate wk_box anchored at the current bar_index, prime wk_hi/wk_lo with the bar’s high/low, create the start line, and push both handles to their arrays.

Accrual (while week_open): Update wk_hi/wk_lo using math.max/min with current bar extremes. Propagate those values to the active wk_box via box.set_top/bottom and slide box.set_right to the current bar_index to keep the box flush with live price.

Close Check: If at/after Friday 16:00, finalize the week by freezing the right edge (box.set_right), drawing the end line, pushing its handle, and flipping week_open false.

Retention Pruning: Enforce a hard cap on historical elements by deleting the oldest objects when counts exceed configured limits.

Drawing Semantics

The range container is a filled white rectangle (bgcolor = color.new(color.white, 100 − opacity)), with a solid white border for clear contrast on dark or light themes. Start/end boundaries are full-height vertical white lines (y1=+1e10, y2=−1e10) to guarantee visibility across auto-scaled y-axes. This approach avoids reliance on price-dependent anchors for the lines and is robust to large volatility spikes.

Multi-Timeframe Behavior

Because session logic is driven by wall-clock time in the Toronto zone, the indicator remains consistent across chart resolutions. On coarse timeframes where an exact boundary bar might not exist, the script legally approximates by triggering on the first available bar within or immediately after the boundary (e.g., Friday 16:00 occurs between two 4-hour bars). The box therefore represents the true realized high/low of the bars present in that timeframe, which is the correct visual for that resolution.

Inputs and Defaults

Weeks to keep (show_weeks_back): integer, default 40. Controls retention of historical boxes/lines to avoid UI clutter and resource overhead.

Fill opacity (fill_opacity): integer 0–100, default 88. Controls how solid the white fill appears; border color is fixed pure white for crisp edges.

Time zone is intentionally fixed to "America/Toronto" to match the strategy definition and maintain consistent historical backtesting.

Performance and Limits

Objects are reused only within a week; upon closure, handles are stored and later purged when history limits are exceeded. The script sets generous but safe caps (max_boxes_count/max_lines_count) to accommodate 40 weeks while preserving Editor constraints. Per-bar work is O(1), and pruning loops are bounded by the configured history length, keeping runtime predictable on long histories.

Edge Cases and Guarantees

DST Transitions: Using a fixed IANA time zone ensures Friday 16:00 and Monday 00:00 boundaries shift correctly when DST changes in Toronto.

Weekend Gaps/Holidays: If the market lacks bars exactly at boundaries, the nearest subsequent bar triggers the start/close logic; range statistics still reflect observed prices.

Live vs Historical: During live sessions the box edge advances every bar; when replaying history or backtesting, the same rules apply deterministically.

Scope (Intentional Simplicity)

This tool is strictly a visual framing indicator. It does not compute labels, statistics, alerts, or extended S/R projections. Its single responsibility is to clearly present the week’s realized range in the Toronto session window so you can layer your own execution or analytics on top.

Anchored VWAP Polyline [CHE] Anchored VWAP Polyline — Anchored VWAP drawn as a polyline from a user-defined bar count with last-bar updates and optional labels

Summary

This indicator renders an anchored Volume-Weighted Average Price as a continuous polyline starting from a user-selected anchor point a specified number of bars back. It accumulates price multiplied by volume only from the anchor forward and resets cleanly when the anchor moves. Drawing is object-based (polyline and labels) and updated on the most recent bar only, which reduces flicker and avoids excessive redraws. Optional labels mark the anchor and, conditionally, a delta label when the current close is below the historical close at the anchor offset.

Motivation: Why this design?

Anchored VWAP is often used to track fair value after a specific event such as a swing, breakout, or session start. Traditional plot-based lines can repaint during live updates or incur overhead when frequently redrawn. This implementation focuses on explicit state management, last-bar rendering, and object recycling so the line stays stable while remaining responsive when the anchor changes. The design emphasizes deterministic updates and simple session gating from the anchor.

What’s different vs. standard approaches?

Baseline: Classic VWAP lines plotted from session open or full history.

Architecture differences:

Anchor defined by a fixed bar offset rather than session or day boundaries.

Object-centric drawing via `polyline` with an array of `chart.point` objects.

Last-bar update pattern with deletion and replacement of the polyline to apply all points cleanly.

Conditional labels: an anchor marker and an optional delta label only when the current close is below the historical close at the offset.

Practical effect: You get a visually continuous anchored VWAP that resets when the anchor shifts and remains clean on chart refreshes. The labels act as lightweight diagnostics without clutter.

How it works (technical)

The anchor index is computed as the latest bar index minus the user-defined bar count.

A session flag turns true from the anchor forward; prior bars are excluded.

Two persistent accumulators track the running sum of price multiplied by volume and the running sum of volume; they reset when the session flag turns from false to true.

The anchored VWAP is the running sum divided by the running volume whenever both are valid and the volume is not zero.

Points are appended to an array only when the anchored VWAP is valid. On the most recent bar, any existing polyline is deleted and replaced with a new one built from the point array.

Labels are refreshed on the most recent bar:

A yellow warning label appears when there are not enough bars to compute the reference values.

The anchor label marks the anchor bar.

The delta label appears only when the current close is below the close at the anchor offset; otherwise it is suppressed.

No higher-timeframe requests are used; repaint is limited to normal live-bar behavior.

Parameter Guide

Bars back — Sets the anchor offset in bars; default two hundred thirty-three; minimum one. Larger values extend the anchored period and increase stability but respond more slowly to regime changes.

Labels — Toggles all labels; default enabled. Disable to keep the chart clean when using multiple instances.

Reading & Interpretation

The polyline represents the anchored VWAP from the chosen anchor to the current bar. Price above the line suggests strength relative to the anchored baseline; price below suggests weakness.

The anchor label shows where the accumulation starts.

The delta label appears only when today’s close is below the historical close at the offset; it provides a quick context for negative drift relative to that reference.

A yellow message at the current bar indicates the chart does not have enough history to compute the reference comparison yet.

Practical Workflows & Combinations

Trend following: Anchor after a breakout bar or a swing confirmation. Use the anchored VWAP as dynamic support or resistance; look for clean retests and holds for continuation.

Mean reversion: Anchor at a local extreme and watch for approaches back toward the line; require structure confirmation to avoid early entries.

Session or event studies: Re-set the anchor around earnings, macro releases, or session opens by adjusting the bar offset.

Combinations: Pair with structure tools such as swing highs and lows, or with volatility measures to filter chop. The labels can be disabled when combining multiple instances to maintain chart clarity.

Behavior, Constraints & Performance

Repaint and confirmation: The line is updated on the most recent bar only; historical values do not rely on future bars. Normal live-bar movement applies until the bar closes.

No higher timeframe: There is no `security` call; repaint paths related to higher-timeframe lookahead do not apply here.

Resources: Uses one polyline object that is rebuilt on the most recent bar, plus two labels when conditions are met. `max_bars_back` is two thousand. Arrays store points from the anchor forward; extremely long anchors or very long charts increase memory usage.

Known limits: With very thin volume, the VWAP can be unavailable for some bars. Very large anchors reduce responsiveness. Labels use ATR for vertical placement; extreme gaps can place them close to extremes.

Sensible Defaults & Quick Tuning

Starting point: Bars back two hundred thirty-three with Labels enabled works well on many assets and timeframes.

Too noisy around the line: Increase Bars back to extend the accumulation window.

Too sluggish after regime changes: Decrease Bars back to focus on a shorter anchored period.

Chart clutter with multiple instances: Disable Labels while keeping the polyline visible.

What this indicator is—and isn’t

This is a visualization of an anchored VWAP with optional diagnostics. It is not a full trading system and does not include entries, exits, or position management. Use it alongside clear market structure, risk controls, and a plan for trade management. It does not predict future prices.

Inputs with defaults

Bars back: two hundred thirty-three bars, minimum one.

Labels: enabled or disabled toggle, default enabled.

Pine version: v6

Overlay: true

Primary outputs: one polyline, optional labels (anchor, conditional delta, and a warning when insufficient bars).

Metrics and functions: volume, ATR for label offset, object drawing via polyline and chart points, last-bar update pattern.

Special techniques: session gating from the anchor, persistent state, object recycling, explicit guards against unavailable values and zero volume.

Compatibility and assets: Designed for standard candlestick or bar charts across liquid assets and common timeframes.

Diagnostics: Yellow warning label when history is insufficient.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

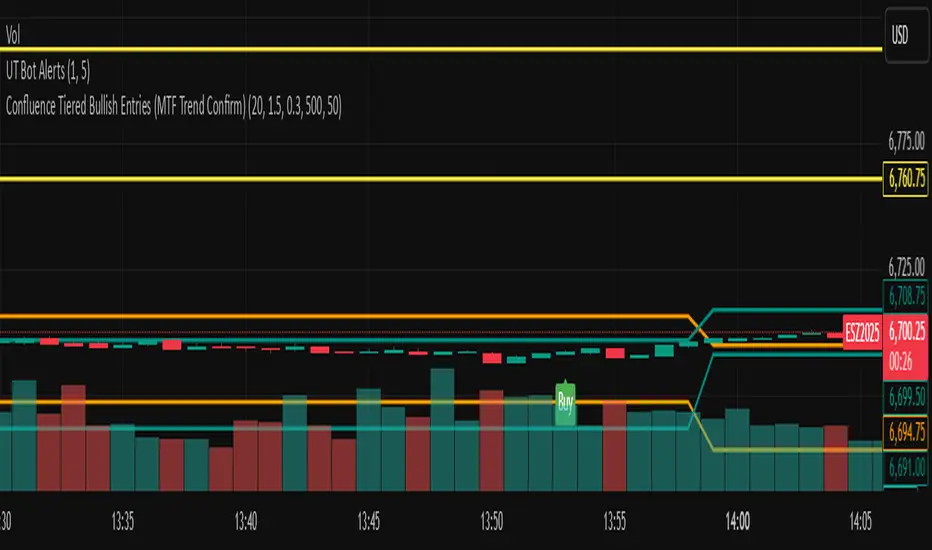

HTF Cross Breakout [CHE] HTF Cross Breakout — Detects higher timeframe close crossovers for breakout signals, anchors VWAP for trend validation, and flags continuations or traps with visual extensions for delta percent and stop levels.

Summary

This indicator spots moments when the current chart's close price crosses a higher timeframe close, marking potential breakouts only when the current bar shows directional strength. It anchors a volume-weighted average price line from the breakout point to track trend health, updating labels to show if the move continues or reverses into a trap. Extensions add a dotted line linking the breakout level to the current close with percent change display, plus a stop-loss marker at the VWAP end. Signals gain robustness from higher timeframe confirmation and anti-repainting options, reducing noise in live bars compared to simple crossover tools.

Motivation: Why this design?

Traders often face false breakouts from intrabar wiggles on lower timeframes, especially without higher timeframe alignment, leading to whipsaws in volatile sessions. This design uses higher timeframe close as a stable reference for crossover detection, combined with anchored volume weighting to gauge sustained momentum. It addresses these by enforcing bar confirmation and directional filters, providing clearer entry validation and risk points without overcomplicating the chart.

What’s different vs. standard approaches?

Reference baseline

Standard crossover indicators like moving average crosses operate solely on the chart timeframe, ignoring higher timeframe context and lacking volume anchoring.

Architecture differences

- Higher timeframe data pulls via security calls with optional repainting control for stability.

- Anchored VWAP resets at each signal, accumulating from the breakout bar only.

- Label dynamics update in real-time for continuation checks, with extensions for visual delta and stop computation.

- Event-driven line finalization prunes old elements after a set bar extension.

Practical effect

Charts show persistent lines and labels that extend live but finalize cleanly on new events, avoiding clutter. This matters for spotting trap reversals early via label color shifts, and extensions provide quick risk visuals without manual calculations, improving decision speed in trend trades.

How it works (technical)

The indicator first determines a higher timeframe based on user selection, pulling its close price securely. It checks for crossovers or crossunders of the current close against this higher close, but only triggers on confirmed bars with matching directional opens and closes. On a valid event, a horizontal line and label mark the higher close level, while a dashed VWAP line starts accumulating typical price times volume from that bar onward. During the active phase, the breakout line extends to the current bar, the label repositions and updates text based on whether the current close holds above or below the level for bulls or bears. A background tint warns if the close deviates adversely from the current VWAP. Extensions draw a vertical dotted line at the last bar between the breakout level and close, placing a midpoint label with percent difference; separately, a label at the VWAP end shows a computed stop price. Persistent variables track the active state and accumulators, resetting on new events after briefly extending old elements. Repaint risk from security calls is mitigated by confirmed bar gating or user opt-in.

Parameter Guide

Plateau Length (reserved for future, currently unused): Sets a length for potential plateau detection in extensions; default 3, minimum 1. Higher values would increase stability but are not active yet—leave at default to avoid tuning.

Line Width: Controls thickness of breakout, VWAP, and extension lines; default 2, range 1 to 5. Thicker lines improve visibility on busy charts but may obscure price action—use 1 for clean views, 3 or more for emphasis.

+Bars after next HTF event (finalize old, then delete): Extends old lines and labels by this many bars before deletion on new signals; default 20, minimum 0. Shorter extensions keep charts tidy but risk cutting visuals prematurely; longer aids review but builds clutter over time.

Evaluate label only on HTF close (prevents gray traps intrabar): When true, label updates wait for higher timeframe confirmation; default true. Enabling reduces intrabar flips for stabler signals, though it may delay feedback—disable for faster live trading at repaint cost.

Allow Repainting: Permits real-time security data without confirmation offset; default false. False ensures historical accuracy but lags live bars; true speeds updates but can repaint on HTF closes.

Timeframe Type: Chooses HTF method—Auto Timeframe (dynamic steps up), Multiplier (chart multiple), or Manual (fixed string); default Auto Timeframe. Auto adapts to chart scale for convenience; Multiplier suits custom scaling like 5 times current; Manual for precise like 1D on any chart.

Multiplier for Alternate Resolution: Scales chart timeframe when Multiplier type selected; default 5, minimum 1. Values near 1 mimic current resolution for subtle shifts; higher like 10 jumps to broader context, increasing signal rarity.

Manual Resolution: Direct timeframe string like 60 for 1H when Manual type; default 60. Match to trading horizon—shorter for swing, longer for positional—to balance frequency and reliability.

Show Extension 1: Toggles dotted line and delta percent label between breakout level and current close; default true. Disable to simplify for basic use, enable for precise momentum tracking.

Dotted Line Width: Thickness for Extension 1 line; default 2, range 1 to 5. Align with main Line Width for consistency.

Text Size: Size for delta percent label; options tiny, small, normal, large; default normal. Smaller reduces overlap on dense charts; larger aids glance reads.

Decimals for Δ%: Precision in percent change display; default 2, range 0 to 6. Fewer decimals speed reading; more suit low-volatility assets.

Positive Δ Color: Hue for upward percent changes; default lime. Choose contrasting for visibility.

Negative Δ Color: Hue for downward percent changes; default red. Pair with positive for quick polarity scan.

Dotted Line Color: Color for Extension 1 line; default gray. Neutral tones blend well; brighter for emphasis.

Background Transparency (0..100): Opacity for delta label background; default 90. Higher values fade for subtlety; lower solidifies for readability.

Show Extension 2: Toggles stop-loss label at VWAP end; default true. Turn off for entry focus only.

Stop Method: Percent from VWAP end or fixed ticks; options Percent, Ticks; default Percent. Percent scales with price levels; Ticks suits tick-based instruments.

Stop %: Distance as fraction of VWAP for Percent method; default 1.0, step 0.05, minimum 0.0. Tighter like 0.5 reduces risk but increases stops; wider like 2.0 allows breathing room.

Stop Ticks: Tick count offset for Ticks method; default 20, minimum 0. Adjust per asset volatility—fewer for tight control.

Price Decimals: Rounding for stop price text; default 4, range 0 to 10. Match syminfo.precision for clean display.

Text Size: Size for stop label; options tiny, small, normal, large; default normal. Scale to chart zoom.

Text Color: Foreground for stop text; default white. Ensure contrast with background.

Inherit VWAP Color (BG tint): Bases stop label background on VWAP hue; default true. True maintains theme; false allows custom black base.

BG Transparency (0..100): Opacity for stop label background; default 0. Zero for no tint; up to 100 for full fade.

Reading & Interpretation

Breakout lines appear green for bullish crosses or red for bearish, extending live until a new event finalizes them briefly then deletes. Labels start blank, updating to Bull Cont. or Bear Cont. in matching colors if holding the level, or gray Bull Trap/Bear Trap on reversal. VWAP dashes yellow for bulls, orange for bears, sloping with accumulated volume weight—deviations trigger faint red background warnings. Extension 1's dotted vertical shows at the last bar, with midpoint label green/red for positive/negative percent from breakout to close. Extension 2 places a left-aligned label at VWAP end with stop price and method note, tinted to VWAP for context.

Practical Workflows & Combinations

For trend following, enter long on green Bull Cont. labels above VWAP with higher highs confirmation, filtering via rising structure; short on red Bear Cont. below. Pair with volume surges or RSI above 50 for bulls to avoid traps. For exits, trail stops using the Extension 2 level, tightening on warnings or gray labels—aggressive on continuations, conservative post-trap. In multi-timeframe setups, use default Auto on 15m charts for 1H signals, scaling multiplier to 4 for daily context on hourly; test on forex/stocks where volume is reliable, avoiding low-liquidity assets.

Behavior, Constraints & Performance

Signals confirm on bar close with HTF gating when strict mode active, but live bars may update if repainting enabled—opt false for backtest fidelity, true for intraday speed. Security calls risk minor repaints on HTF closes, mitigated by confirmation offsets. Resources cap at 1000 bars back, 50 lines/labels total, with event prunes to stay under budgets—no loops, minimal arrays. Limits include VWAP lag in low-volume periods and dependency on accurate HTF data; gaps or holidays may skew anchors.

Sensible Defaults & Quick Tuning

Defaults suit 5m-1H charts on liquid assets: Auto HTF, no repaint, 1% stops. For choppy markets with excess signals, enable strict eval and bump multiplier to 10 for rarer triggers. If sluggish in trends, shorten extend bars to 10 and allow repainting for quicker visuals. On high-vol like crypto, widen stop % to 2.0 and use Ticks method; for stables like indices, tighten to 0.5% and keep Percent.

What this indicator is—and isn’t