Improved Chaikin Money FlowChaikin Money Flow is a well-known Indicator for gauging buying/selling pressure. Marc Chaikin intended this to be used on the daily timeframe to capture the behavior of price action at or near the daily close when larger-scale actors influence the market. The calculation is straight forward as described within the built-in TradingView "CMF" indicator:

1. Period Money Flow Multiplier = ((Close - Low) - (High - Close)) /(High - Low)

2. Period Money Flow Volume = Period Money Flow Multiplier x Volume for the Period

3. Chaikin Money Flow = 21 Period Sum of Money Flow Volume / 21 Period Sum of Volume

There is, however, a problem with this algorithm: it does not account for daily gaps in price action. This leads to the indicator sometimes moving out-of-sync with price action and/or an under-emphasis of the magnitude change of the indicator relative to the change in price action. This is a significant problem for someone trying to read divergences against an underlying.

Note: I have never seen a published attempt to improve this indicator which is why I decided that there had to be a way to do it.

In order to mitigate this issue, I have taken the basic script provided by TradingView and made a key modification. If the open of a candle is outside the range of the previous candle, then the close of the previous candle is used as the "high" for the current candle (in the case of a gap down) or the "low" for the current candle (in the case of a gap up). However, if the close of the current candle exceeds the previous close, highs and lows for the current candle are calculated as normal. I believe this accounts for gaps in price action without significantly altering the original intent of the indicator.

I have made four other minor tweaks:

1. Default style is color coded area above and below the Zero Line

2. Range scaled to +/-100 instead of +/-1 (displays better on graph)

3. Set timeframe to Daily (as that is the timeframe for which this indicator was intended by Chaikin)

4. Length defaults to 21 (which is what Chaikin uses)

Cari dalam skrip untuk "gaps"

Bodies X Wix Version of Smart Money Tools by makuchaku & eFeThis is the same Script as Super Fair Value Gaps / FVG /BoS / by makuchaku & eFe. Mine Should Default to Large Text instead of small. The Super Order Blocks I believe was meant to for you to find one of the many Smart Money tools such as turn on the Fair Value gap but leave the others off, or Turn on where the Break of Structure and leave the others off. The reason I believe this is because the default values for each of the structures were default colored (green for positive and red for negative) for all.

Mine has a different Color for every possible structure. As long as you can read with the larger text that I added, then you can create your own boxes positive for break of structure, rejection block, order blocks and fair value gaps for any time frame. The reason I did that is because There's only certain things I believe I will need to mark for myself in each time frame, and then from there You can stretch iyour own box out further in time because if price touches a fair value gap for example, the fair value gap should conyinue in time until at least 2 candles have filed the Fair valu gap going both directions. That's truly when the fair value gap should is mitigated and will from off the chart. However, If I knew How to add the code for that, I would.

Additionally, I have the Max Boxes per chart, so you should have the ability to see every OB, FVG,RJB, & BoS on the chart

I tried my hardest to create a colored border that was different from the box. But the way the original was coded was almost impossible to do. Because they defined each of the structures (FVG, OB, BoS, RJB) outer levels, when the outer levels connect via math in the code, then it joins all the outside lines for a rectangle. When creating a box, the coloe will always be the same as the border unfortunately. (Unless I replan this from the beginning)

I also Changed the default labels for reach structure from a hard to read gray to a white that pops out.

Also, chart indicators are a little large as well. Such as the cross, sideways cross, The green Triangle, and the white Diamond. You'll get used to it or you can change it as well.

Creating videos for students, you need something they can see.

So, I just wanted to ensure everything was a little more unique and easily usable when showing this to my students when I send them private videos for our weekly lessons. I'm trying to learn how to use the IPFS for THAT, (which i see has invaded PineScript) Hope this indicator helps.

If you're to borrow this, Just make sure you keep the authors in the name makuchaku & efe

PivotsSimply plots pivots found on any timeframe based on length specified.

Supports other timeframes, you choose to display gaps or not, with gaps on the labels may disappear so keep that in mind.

Gapgap indicator

True type:

The gap formed between the closing price of the last bar on Friday of the "current" chart period and the opening price of Monday of the "current" chart period

Fix type :

Displays the "daily" gap between Friday's close and Monday's open in "any" chart period

Intution type :

Any gaps are marked

(Not recommended to use in small cycles. There will be a lot of gaps due to the small transaction volume)

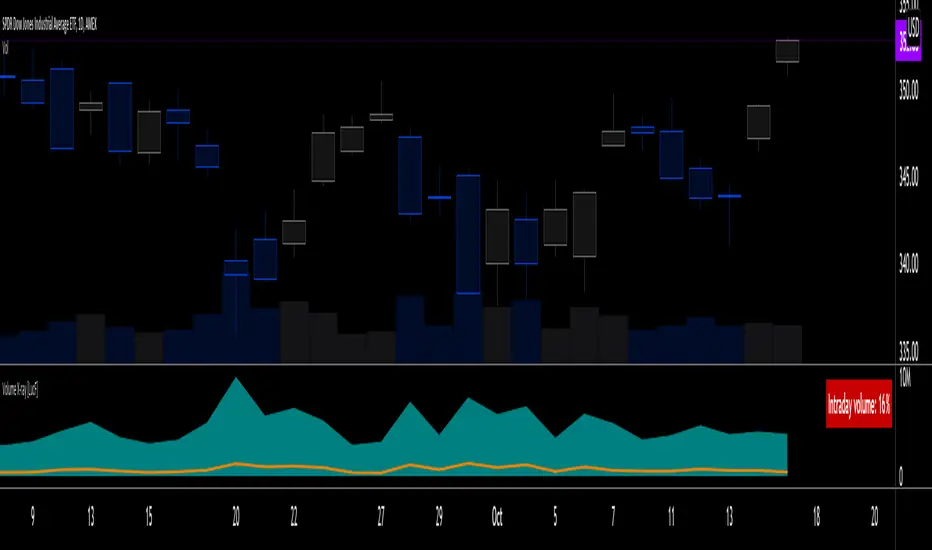

Volume X-ray [LucF]█ OVERVIEW

This tool analyzes the relative size of volume reported on intraday vs EOD (end of day) data feeds on historical bars. If you use volume data to make trading decisions, it can help you improve your understanding of its nature and quality, which is especially important if you trade on intraday timeframes.

I often mention, when discussing volume analysis, how it's important for traders to understand the volume data they are using: where it originates, what it includes and does not include. By helping you spot sizeable differences between volume reported on intraday and EOD data feeds for any given instrument, "Volume X-ray" can point you to instruments where you might want to research the causes of the difference.

█ CONCEPTS

The information used to build a chart's historical bars originates from data providers (exchanges, brokers, etc.) who often maintain distinct historical feeds for intraday and EOD timeframes. How volume data is assembled for intraday and EOD feeds varies with instruments, brokers and exchanges. Variations between the two feeds — or their absence — can be due to how instruments are traded in a particular sector and/or the volume reporting policy for the feeds you are using. Instruments from crypto and forex markets, for example, will often display similar volume on both feeds. Stocks will often display variations because block trades or other types of trades may not be included in their intraday volume data. Futures will also typically display variations. It is even possible that volume from different feeds may not be of the same nature, as you can get trade volume (market volume) on one feed and tick volume (transaction counts) on another. You will sometimes be able to find the details of what different feeds contain from the technical information provided by exchanges/brokers on their feeds. This is an example for the NASDAQ feeds . Once you determine which feeds you are using, you can look for the reporting specs for that feed. This is all research you will need to do on your own; "Volume X-ray" will not help you with that part.

You may elect to forego the deep dive in feed information and simply rely on the figure the indicator will calculate for the instruments you trade. One simple — and unproven — way to interpret "Volume X-ray" values is to infer that instruments with larger percentages of intraday/EOD volume ratios are more "democratic" because at intraday timeframes, you are seeing a greater proportion of the actual traded volume for the instrument. This could conceivably lead one to conclude that such volume data is more reliable than on an instrument where intraday volume accounts for only 3% of EOD volume, let's say.

Note that as intraday vs EOD variations exist for historical bars on some instruments, there will typically also be differences between the realtime feeds used on intraday vs 1D or greater timeframes for those same assets. Realtime reporting rules will often be different from historical feed reporting rules, so variations between realtime feeds will often be different from the variations between historical feeds for the same instrument. A deep dive in reporting rules will quickly reveal what a jungle they are for some instruments, yet it is the only way to really understand the volume information our charts display.

█ HOW TO USE IT

The script is very simple and has no inputs. Just add it to 1D charts and it will calculate the proportion of volume reported on the intraday feed over the EOD volume. The plots show the daily values for both volumes: the teal area is the EOD volume, the orange line is the intraday volume. A value representing the average, cumulative intraday/EOD volume percentage for the chart is displayed in the upper-right corner. Its background color changes with the percentage, with brightness levels proportional to the percentage for both the bull color (% >= 50) or the bear color (% < 50). When abnormal conditions are detected, such as missing volume of one kind or the other, a yellow background is used.

Daily and cumulative values are displayed in indicator values and the Data Window.

The indicator loads in a pane, but you can also use it in overlay mode by moving it on the chart with "Move to" in the script's "More" menu, and disabling the plot display from the "Settings/Style" tab.

█ LIMITATIONS

• The script will not run on timeframes >1D because it cannot produce useful values on them.

• The calculation of the cumulative average will vary on different intraday timeframes because of the varying number of days covered by the dataset.

Variations can also occur because of irregularities in reported volume data. That is the reason I recommend using it on 1D charts.

• The script only calculates on historical bars because in real time there is no distinction between intraday and EOD feeds.

• You will see plenty of special cases if you use the indicator on a variety of instruments:

• Some instruments have no intraday volume, while on others it's the opposite.

• Missing information will sometimes appear here and there on datasets.

• Some instruments have higher intraday than EOD volume.

Please do not ask me the reasons for these anomalies; it's your responsibility to find them. I supply a tool that will spot the anomalies for you — nothing more.

█ FOR PINE CODERS

• This script uses a little-known feature of request.security() , which allows us to specify `"1440"` for the `timeframe` argument.

When you do, data from the 1min intrabars of the historical intraday feed is aggregated over one day, as opposed to the usual EOD feed used with `"D"`.

• I use gaps on my request.security() calls. This is useful because at intraday timeframes I can cumulate non- na values only.

• I use fixnan() on some values. For those who don't know about it yet, it eliminates na values from a series, just like not using gaps will do in a request.security() call.

• I like how the new switch structure makes for more readable code than equivalent if structures.

• I wrote my script using the revised recommendations in the Style Guide from the Pine v5 User Manual.

• I use the new runtime.error() to throw an error when the script user tries to use a timeframe >1D.

Why? Because then, my request.security() calls would be returning values from the last 1D intrabar of the dilation of the, let's say, 1W chart bar.

This of course would be of no use whatsoever — and misleading. I encourage all Pine coders fetching HTF data to protect their script users in the same way.

As tool builders, it is our responsibility to shield unsuspecting users of our scripts from contexts where our calcs produce invalid results.

• While we're on the subject of accessing intrabar timeframes, I will add this to the intention of coders falling victim to what appears to be

a new misconception where the mere fact of using intrabar timeframes with request.security() is believed to provide some sort of edge.

This is a fallacy unless you are sending down functions specifically designed to mine values from request.security() 's intrabar context.

These coders do not seem to realize that:

• They are only retrieving information from the last intrabar of the chart bar.

• The already flawed behavior of their scripts on historical bars will not improve on realtime bars. It will actually worsen because in real time,

intrabars are not yet ordered sequentially as they are on historical bars.

• Alerts or strategy orders using intrabar information acquired through request.security() will be using flawed logic and data most of the time.

The situation reminds me of the mania where using Heikin-Ashi charts to backtest was all the rage because it produced magnificent — and flawed — results.

Trading is difficult enough when doing the right things; I hate to see traders infected by lethal beliefs.

Strive to sharpen your "herd immunity", as Lionel Shriver calls it. She also writes: "Be leery of orthodoxy. Hold back from shared cultural enthusiasms."

Be your own trader.

█ THANKS

This indicator would not exist without the invaluable insights from Tim, a member of the Pine team. Thanks Tim!

Gap RiderThis Indicator allows you to make statistics on the performance of any underlying on the days in which an opening gap occurs.

Specifically, the indicator was designed for "0 dte" options trades. In fact, it is possible to find parameters that give a good statistical advantage by opening a spread in the direction of the gap, creating a trade that has a risk-return ratio of 1: 1.

The indicator shows flags on the graph (green in case of gap up, red in case of gap down) and colored boxes (green in case the stock closed in the direction of the gap, red in case the stock closed in the opposite direction to the gap, yellow in the event that the stock closed at a distance that did not allow the spread in options to close in maximum loss or maximum profit, and therefore in breakeven)

The statistics panel, on the other hand, contains all the information necessary to search for parameters that give the trader a good statistical advantage.

In the settings you can filter the days of the week, only gap up or only gap down, ATR thresholds (volatility), points or minimum percentage for which a gap is taken into account, measure of the breakeven (which for options traders should represent the half the width of the spread to open), large gaps filter that takes into consideration only gaps that open out of range compared to the previous session. The Lookback parameter of course is used to set how many bars to take into account for the statistics.

Parameters and recommended strategy:

TODAY 31/08/2021 - Lookback 500 bars (2 years)

UNDERLYING: SPX

FILTERS: only Monday and Wednesday, only gap up, only gap> 0.01%

STRATEGY: exactly at opening, cover an ATM spread in the direction of the gap (example: gap up, I open a long call spread) that has the opening price as a break even, with a risk-return ratio of 1: 1 and leave it open until closing session, or set take profit at 90-95%. It is advisable to take into consideration the SPX statistics but to operate on the ES future so as to be able to open the spread a couple of minutes before the opening of the cash session and prevent the trade from "running away" due to too sudden movements of the opening. .

RESULTS:

124 Trade

70% profitable trades

30% losing trades

Max drawdown 3 trades

So assuming a spread on ES 10 points wide, each trade would gain or lose $ 250, applying the described strategy we would have in two years, investing only $ 250, a profit of $ 12500, with a max drawdown of $ 750. We would therefore have a profit of 5000%, or rather 2500% per year on the invested capital, with a drawdown of a much lower proportion of the profit ($ 750 compared to $ 6250 of annual profit).

The strategy is infinitely scalable by increasing the options contracts used and the impact of the commissions is almost zero.

MONEY MANAGEMENT: Example on a 50K account, with a spread that earns or loses $ 500, in two years it earns $ 25,000, therefore about 12500 per year, with a max drawdown of $ 1500, therefore 25% per year on the ENTIRE ACCOUNT with a maximum drawdown of 3%.

Note: the test was performed without a break even parameter, so the actual result will be more moderate, but of the same explosive nature.

** BUG STILL LOOKING FOR SOLUTION **

only in case the filters are set to take into account ONLY the gap down, the drawdown count in the statistics panel shows an incorrect result "

Repeated Median Regression ChannelThis script uses the Repeated Median (RM) estimator to construct a linear regression channel and thus offers an alternative to the available codes based on ordinary least squares.

The RM estimator is a robust linear regression algorithm. It was proposed by Siegel in 1982 (1) and has since found many applications in science and engineering for linear trend estimation and data filtering.

The key difference between RM and ordinary least squares methods is that the slope of the RM line is significantly less affected by data points that deviate strongly from the established trend. In statistics, these points are usually called outliers, while in the context of price data, they are associated with gaps, reversals, breaks from the trading range. Thus, robustness to outlier means that the nascent deviation from a predetermined trend will be more clearly seen in the RM regression compared to the least-squares estimate. For the same reason, the RM model is expected to better depict gaps and trend changes (2).

Input Description

Length : Determines the length of the regression line.

Channel Multiplier : Determines the channel width in units of root-mean-square deviation.

Show Channel : If switched off , only the (central) regression line is displayed.

Show Historical Broken Channel : If switched on , the channels that were broken in the past are displayed. Note that a certain historical broken channel is shown only when at least Length / 2 bars have passed since the last historical broken channel.

Print Slope : Displays the value of the current RM slope on the graph.

Method

Calculation of the RM regression line is done as follows (1,3):

For each sample point ( t (i), y (i)) with i = 1.. Length , the algorithm calculates the median of all the slopes of the lines connecting this point to the other Length -1 points.

The regression slope is defined as the median of the set of these median slopes.

The regression intercept is defined as the median of the set { y (i) – m * t (i)}.

Computational Time

The present implementation utilizes a brute-force algorithm for computing the RM-slope that takes O ( Length ^2) time. Therefore, the calculation of the historical broken channels might take a relatively long time (depending on the Length parameter). However, when the Show Historical Broken Channel option is off, only the real-time RM channel is calculated, and this is done quite fast.

References

1. A. F. Siegel (1982), Robust regression using repeated medians, Biometrika, 69 , 242–244.

2. P. L. Davies, R. Fried, and U. Gather (2004), Robust signal extraction for on-line monitoring data, Journal of Statistical Planning and Inference 122 , 65-78.

3. en.wikipedia.org

[BMAX] Averan BB(ENGLISH)

Averan is an indicator based on ADR, which shows the volatility of the market based on high-low prices on the selected timeframe. The difference between Averan and ATR is that Averan does not consider GAPs, so it basically consider the actual size of the candles.

This indicator also includes a standard deviation representation, the same as the top portion of the bollinger bands to present the variance of the volatility.

(PORTUGUÊS)

Averan é um indicador baseado no ADR, que apresenta a volatilidade do mercado baseado em máximas e mínimas do tempo gráfico escolhido. A diferença do Averan para o ATR é que o Averan não considera GAPs, portanto é basicamente calculado pelo real tamanho dos candles.

Este indicador também inclui a representação do desvio padrão, representado da mesma maneira que a banda superior do Bollinger Bands, apresentando portanto a variância da volatilidade.

scaled.orders [highwater]FOR EDUCATIONAL PURPOSES

There are multiple tools that allow you to place "scaled orders" on your exchange, namely Alertatron and Bybit Tools. This script is based on some Alertatron features, but you can use it for any grid like order placing strategy. Even if thats not your thing it's an example of how to use arrays in pinescript.

FROM PRICE - is the price to start your orders.

TO PRICE - is the price your orders will end.

SCALED TYPES :

LINEAR - will distribute orders evenly between from and to price.

EASE IN - will cluster orders closer to from price, then start to widen the gaps as you move closer to to price.

EASE OUT - will have wider gaps near from price, and start to cluster near to price.

EASE IN OUT - will cluster orders near both from price and to price.

COUNT - number of orders in each scaled order.

Awesome Oscillator_VTX

Abbreviations:

AO - Awesome Oscillator

AC - Accelerator Oscillator

TP - TimePeriod (1m,2m,5m,1h....)

TP Steps - 1m,3m,12m,1h,5h,D (This steps i use)

Use-case:

Awesome Oscillator best used to find Divergence/Convergence what results in Weakening of Momentum and Price reversals.

This script calculates and plots AO/AC with minute precision, removing GAPS when projecting Higher Period AO/AC.

So you can accommodate all important information on one chart with best precision.

Made for Intraday Perioads.

Best used for DayTrading, when you need to make quick and efficient decisions.

Calculation = Preferred resolution * Length / Present resolution.

As Additional Function, this Awesome Oscillator has AC built in.

Settings:

Resolution - Most used TP included, plus some exclusive paid plans (1m, 2m, 3m, 5m, 12m, 15m, 1h, 4h, 5h, Daily). Default set to 1h

Use AO - You can switch between EMA and SMA for FastMA/SlowMA calculation. Default set to EMA

FastMA - standard function. Default set to 5

SlowMA - standard function. Default set to 34

Signal Line - Plots MA to show Momentum. Uses EMA/SMA based on "Use AO" selection. Default set to 5

Use AC - You can switch between EMA and SMA for AC calculation. Default set to SMA

Offset - standard function. Default set to 0

Accelerator - AC length. Default set to 5

Source - standard function. Default set to hlc3

Why to use it ?

Yes, i know that variable TP is standard now in TradingView. But there are some limitations, especially for DayTraders.

Problem:

Imagine you are trading/scalping on 1m.. 5m.. 15.. charts and you want to see where are your on Higher TP.

-- You can change to 1h and check it, but you will loose the picture from smaller TP.

-- You can use Standard TP function, but your data will update every 15m, 1h (depends on TP). And in result you have Gaps between bars.

Solution:

This script help to solve this problem, by breaking information down to 1m and building from there.

So whatever Intraday TP you choose to trade, your AO/AC will be updated with minute precision.

Limitations:

Sadly nothing without limitations.

1. For Best performance use only Higher TP dividable By Yours (ex. You use 3m chart, then you can plot 12m, 15m, 1h / You use 5m chart, then you can plot 15m, 1h. 12m will already have 3m of information lost using 5m Chart )

Kicker ScannerThe kicker pattern is deemed to be one of the most reliable reversal patterns and usually signifies a dramatic change in the fundamentals of the company in question.

It is a 2-candle pattern, whereby there is a significant gap between the body of the most recent candle and the previous candle.

A bullish kicker is one in which the most recent candle is bullish, and the previous candle is bearish.

A bearish kicker is one in which the most recent candle is bearish, and the previous candle is bullish.

I notice this works best for stocks, as there are many gaps in a stock chart. Currencies have few gaps, and thus few kickers.

From within the settings, you can set the minimum permitted gap between the two candles, specified in price, accurate to 6 decimal places; 0.000001.

Line breakI decided to help TradingView programmers and wrote code that converts a standard candles / bars to a line break chart. The built-in linebreak() and security() functions for constructing a Linear Break chart are bad, the chart is not built correctly, and does not correspond to the Line Breakout chart built into TradingView. I’m talking about simulating the Linear Break lines using the plotcandle() annotation, because these are the same candles without shadows. When you try to use the market simulator, when the gaps are turned on in the security() function, nothing is added to the chart, and when turned off, a completely different line break chart is drawn. Do not try to write strategies based on the built-in linebreak() function! The developers write in the manual: "Please note that you cannot plot Line Break boxes from Pine script exactly as they look. You can only get a series of numbers similar to OHLC values for Line Break charts and use them in your algorithms." However, it is possible to build a “Linear Breakthrough” chart exactly like the “Linear Breakthrough" chart built into TradingView. Personally, I had enough Pine Script functionality.

For a complete understanding of how such a graph is built, you can refer to Steve Nison's book “BEYOND JAPANESE CANDLES” and see the instructions for creating a “Three-Line Breakthrough” chart (the number of lines for a breakthrough is three):

Rule 1: if today's price is above the base price (closing the first candle), draw a white line from the base price to the new maximum price (before closing).

or Rule 2: if today's price is below the base price, draw a black line from the base price to the new low of prices (before closing).

Rule 3: if today's price is no different from the base, do not draw any line.

Rule 4: if today's price rises above the maximum of the first line, shift to the column to the right and draw a new white line from the previous maximum to the new maximum of prices.

Rule 5: if the price is below the low of the first line, move one column to the right and draw a new black line down from the previous low to the new low of prices.

Rule 6: if the price is kept in the range of the first line, nothing is applied to the chart.

Rule 7: if the market reaches a new maximum, surpassing the maximum of previous lines, move to the column to the right and draw a new white line up to a new maximum.

Rule 8: if today's price is below the low of previous lines (i.e. there is a new low), move to the right column and draw a new black line down to a new low.

Rule 9: if the price is in the range of the first two lines, nothing is applied to the chart.

Rule 10: if there is a series of three white lines, a new white line is drawn when a new maximum is reached (even if it is only one tick higher than the old one). Under the same conditions, for drawing a black reversal line, the price should fall below the minimum of the series of the last three white lines. Such a black line is called a black reversal line. It runs from the base of the highest white line to a new low of price.

Rule 11: if there is a series of three black lines, a new black line is drawn when a new minimum is reached. Under the same conditions, for drawing a white line, called a white reversal line, the price must exceed the maximum of the previous three black lines. This line is drawn from the top of the lowest black line to a new high of the price.

So, the script was not small, but the idea is extremely simple: if you need to break n lines to build a line, then among these n lines (or less, if this is the beginning of the chart), the maximum or minimum of closures and openings will be searched. If the current candles closed above or below these highs or lows, then a new line is added to the chart on the current candles (trend or breakout). According to my observations, this script draws a chart that is completely identical to the Line Breakout chart built into TradingView, but of course with gaps, as there is time in the candles / bar chart. I stuffed all the logic into a wrapper in the form of the get_linebreak() function, which returns a tuple of OHLC values. And these series with the help of the plotcandle() annotation can be converted to the "Linear Breakthrough" chart. I also want to note that with a large number of candles on the chart, outrages about the buffer size uncertainty are heard from the TradingView black box. Because of this, in the annotation study() set the value to the max_bars_back parameter.

In general, use it (for example, to write strategies)!

GAP DETECTORGAP DETECTOR is an indicator displaying price gaps that have never been completely filled (only gaps >= 5 pips are considered).

Each gap is defined by two lines (the lower and upper bound of the gap), and a label giving information on its price range

#Parameters:

length: the number of candles being considered in the indicator (max is 3000).

width: the width of the gap lines.

[PX] VWAP Gap LevelHello guys,

another day, another method for detecting support and resistance level. This time it's all about the VWAP and daily gaps it might produce.

How does it work?

The indicator detects when a new daily candle begins and the VWAP makes a big move in either direction. Often it produces a gap and this is where the support or resistance level will be plotted. The idea behind it is, that those gaps get filled at some point in time. You can control how big a VWAP movement ("gap") has to be with the "VWAP Movement %" -setting. Also, you can adjust the style of the level.

If you find this indicator useful, please leave a "like" and hit that "follow" button :)

Have fun and happy trading :)))

Volume Profile Free Ultra SLI (100 Levels Value Area VWAP) - RRBVolume Profile Free Ultra SLI by RagingRocketBull 2019

Version 1.0

This indicator calculates Volume Profile for a given range and shows it as a histogram consisting of 100 horizontal bars.

This is basically the MAX SLI version with +50 more Pinescript v4 line objects added as levels.

It can also show Point of Control (POC), Developing POC, Value Area/VWAP StdDev High/Low as dynamically moving levels.

Free accounts can't access Standard TradingView Volume Profile, hence this indicator.

There are several versions: Free Pro, Free MAX SLI, Free Ultra SLI, Free History. This is the Free Ultra SLI version. The Differences are listed below:

- Free Pro: 25 levels, +Developing POC, Value Area/VWAP High/Low Levels, Above/Below Area Dimming

- Free MAX SLI: 50 levels, 2x SLI modes for Buy/Sell or even higher res 150 levels

- Free Ultra SLI: 100 levels, packed to the limit, 2x SLI modes for Buy/Sell or even higher res 300 levels

- Free History: auto highest/lowest, historic poc/va levels for each session

Features:

- High-Res Volume Profile with up to 100 levels (line implementation)

- 2x SLI modes for even higher res: 300 levels with 3x vertical SLI, 100 buy/sell levels with 2x horiz SLI

- Calculate Volume Profile on full history

- POC, Developing POC Levels

- Buy/Sell/Total volume modes

- Side Cover

- Value Area, VAH/VAL dynamic levels

- VWAP High/Low dynamic levels with Source, Length, StdDev as params

- Show/Hide all levels

- Dim Non Value Area Zones

- Custom Range with Highlighting

- 3 Anchor points for Volume Profile

- Flip Levels Horizontally

- Adjustable width, offset and spacing of levels

- Custom Color for POC/VA/VWAP levels, Transparency for buy/sell levels

WARNING:

- Compilation Time: 1 min 20 sec

Usage:

- specify max_level/min_level/spacing (required)

- select range (start_bar, range length), confirm with range highlighting

- select volume type: Buy/Sell/Total

- select mode Value Area/VWAP to show corresponding levels

- flip/select anchor point to position the buy/sell levels

- use Horiz Buy/Sell SLI mode with 100 or Vertical SLI with 300 levels if needed

- use POC/Developing POC/VA/VWAP High/Low as S/R levels. Usually daily values from 1-3 days back are used as levels for the current day.

SLI:

use SLI modes to extend the functionality of the indicator:

- Horiz Buy/Sell 2x SLI lets you view 100 Buy/Sell Levels at the same time

- Vertical Max_Vol 3x SLI lets you increase the resolution to 300 levels

- you need at least 2 instances of the indicator attached to the same chart for SLI to work

1) Enable Horiz SLI:

- attach 2 indicator instances to the chart

- make sure all instances have the same min_level/max_level/range/spacing settings

- select volume type for each instance: you can have a buy/sell or buy/total or sell/total SLI. Make sure your buy volume instance is the last attached to be displayed on top of sell/total instances without overlapping.

- set buy_sell_sli_mode to true for indicator instances with volume_type = buy/sell, for type total this is optional.

- this basically tells the script to calculate % lengths based on total volume instead of individual buy/sell volumes and use ext offset for sell levels

- Sell Offset is calculated relative to Buy Offset to stack/extend sell after buy. Buy Offset = Zero - Buy Length. Sell Offset = Buy Offset - Sell Length = Zero - Buy Length - Sell Length

- there are no master/slave instances in this mode, all indicators are equal, poc/va levels are not affected and can work independently, i.e. one instance can show va levels, another - vwap.

2) Enable Vertical SLI:

- attach the first instance and evaluate the full range to roughly determine where is the highest max_vol/poc level i.e. 0..20000, poc is in the bottom half (third, middle etc) or

- add more instances and split the full vertical range between them, i.e. set min_level/max_level of each corresponding instance to 0..10000, 10000..20000 etc

- make sure all instances have the same range/spacing settings

- an instance with a subrange containing the poc level of the full range is now your master instance (bottom half). All other instances are slaves, their levels will be calculated based on the max_vol/poc of the master instance instead of local values

- set show_max_vol_sli to true for the master instance. for slave instances this is optional and can be used to check if master/slave max_vol values match and slave can read the master's value. This simply plots the max_vol value

- you can also attach all instances and set show_max_vol_sli to true in all of them - the instance with the largest max_vol should become the master

Auto/Manual Ext Max_Vol Modes:

- for auto vertical max_vol SLI mode set max_vol_sli_src in all slave instances to the max_vol of the master indicator: "VolumeProfileFree_MAX_RRB: Max Volume for Vertical SLI Mode". It can be tricky with 2+ instances

- in case auto SLI mode doesn't work - assign max_vol_sli_ext in all slave instances the max_vol value of the master indicator manually and repeat on each change

- manual override max_vol_sli_ext has higher priority than auto max_vol_sli_src when both values are assigned, when they are 0 and close respectively - SLI is disabled

- master/slave max_vol values must match on each bar at all times to maintain proper level scale, otherwise slave's levels will look larger than they should relative to the master's levels.

- Max_vol (red) is the last param in the long list of indicator outputs

- the only true max_vol/poc in this SLI mode is the master's max_vol/poc. All poc/va levels in slaves will be irrelevant and are disabled automatically. Slaves can only show VWAP levels.

- VA Levels of the master instance in this SLI mode are calculated based on the subrange, not the whole range and may be inaccurate. Cross check with the full range.

WARNING!

- auto mode max_vol_sli_src is experimental and may not work as expected

- you can only assign auto mode max_vol_sli_src = max_vol once due to some bug with unhandled exception/buffer overflow in Tradingview. Seems that you can clear the value only by removing the indicator instance

- sometimes you may see a "study in error state" error when attempting to set it back to close. Remove indicator/Reload chart and start from scratch

- volume profile may not finish to redraw and freeze in an ugly shape after an UI parameter change when max_vol_sli_src is assigned a max_vol value. Assign it to close - VP should redraw properly, but it may not clear the assigned max_vol value

- you can't seem to be able to assign a proper auto max_vol value to the 3rd slave instance

- 2x Vertical SLI works and tested in both auto/manual, 3x SLI - only manual seems to work (you can have a mixed mode: 2nd instance - auto, 3rd - manual)

Notes:

- This code uses Pinescript v3 compatibility framework

- This code is 20x-30x faster (main for cycle is removed) especially on lower tfs with long history - only 4-5 sec load/redraw time vs 30-60 sec of the old Pro versions

- Instead of repeatedly calculating the total sum of volumes for the whole range on each bar, vol sums are now increased on each bar and passed to the next in the range making it a per range vs per bar calculation that reduces time dramatically

- 100 levels consist of 50 main plot levels and 50 line objects used as alternate levels, differences are:

- line objects are always shown on top of other objects, such as plot levels, zero line and side cover, it's not possible to cover/move them below.

- all line objects have variable lengths, use actual x,y coords and don't need side cover, while all plot levels have a fixed length of 100 bars, use offset and require cover.

- all key properties of line objects, such as x,y coords, color can be modified, objects can be moved/deleted, while this is not possible for static plot levels.

- large width values cause line objects to expand only up/down from center while their length remains the same and stays within the level's start/end points similar to an area style.

- large width values make plot levels expand in all directions (both h/v), beyond level start/end points, sometimes overlapping zero line, making them an inaccurate % length representation, as opposed to line objects/plot levels with area style.

- large width values translate into different widths on screen for line objects and plot levels.

- you can't compensate for this unwanted horiz width expansion of plot levels because width uses its own units, that don't translate into bars/pixels.

- line objects are visible only when num_levels > 50, plot levels are used otherwise

- Since line objects are lines, plot levels also use style line because other style implementations will break the symmetry/spacing between levels.

- if you don't see a volume profile check range settings: min_level/max_level and spacing, set spacing to 0 (or adjust accordingly based on the symbol's precision, i.e. 0.00001)

- you can view either of Buy/Sell/Total volumes, but you can't display Buy/Sell levels at the same time using a single instance (this would 2x reduce the number of levels). Use 2 indicator instances in horiz buy/sell sli mode for that.

- Volume Profile/Value Area are calculated for a given range and updated on each bar. Each level has a fixed length. Offsets control visible level parts. Side Cover hides the invisible parts.

- Custom Color for POC/VA/VWAP levels - UI Style color/transparency can only change shape's color and doesn't affect textcolor, hence this additional option

- Custom Width - UI Style supports only width <= 4, hence this additional option

- POC is visible in both modes. In VWAP mode Developing POC becomes VWAP, VA High and Low => VWAP High and Low correspondingly to minimize the number of plot outputs

- You can't change buy/sell level colors from input (only transparency) - this requires 2x plot outputs => 2x reduces the number of levels to fit the max 64 limit. That's why 2 additional plots are used to dim the non Value Area zones

- You can change level transparency of line objects. Due to Pinescript limitations, only discrete values are supported.

- Inverse transp correlation creates the necessary illusion of "covered" line objects, although they are shown on top of the cover all the time

- If custom lines_transp is set the illusion will break because transp range can't be skewed easily (i.e. transp 0..100 is always mapped to 100..0 and can't be mapped to 50..0)

- transparency can applied to lines dynamically but nva top zone can't be completely removed because plot/mixed type of levels are still used when num_levels < 50 and require cover

- transparency can't be applied to plot levels dynamically from script this can be done only once from UI, and you can't change plot color for the past length bars

- All buy/sell volume lengths are calculated as % of a fixed base width = 100 bars (100%). You can't set show_last from input to change it

- Range selection/Anchoring is not accurate on charts with time gaps since you can only anchor from a point in the future and measure distance in time periods, not actual bars, and there's no way of knowing the number of future gaps in advance.

- Adjust Width for Log Scale mode now also works on high precision charts with small prices (i.e. 0.00001)

- in Adjust Width for Log Scale mode Level1 width extremes can be capped using max deviation (when level1 = 0, shift = 0 width becomes infinite)

- There's no such thing as buy/sell volume, there's just volume, but for the purposes of the Volume Profile method, assume: bull candle = buy volume, bear candle = sell volume

P.S. I am your grandfather, Luke! Now, join the Dark Side in your father's steps or be destroyed! Once more the Sith will rule the Galaxy, and we shall have peace...

CME Gap Finder - BitcoinOnly for Bitcoin!

This indicator locates weekly gaps created by the CME Futures market for Bitcoin.

As you can see, Bitcoin tends to close the weekly gaps created in the futures market so I thought this could be a very useful tool.

Instead of having to look between multiple charts, this simply overlays the past weeks open and close should a gap appear.

I hope you find this indicator useful!

Cheers!

T2-%Use a superposition of 30 avarages to stress-out trend changes (points in time where all possible frequencies that create the movment change their phase from prositive to negetive or the opposite). The indicator has one paramater that should be adjusted: 'os'.

By defult the 30 avarages that are tested range from 7 to 63 in gaps of 2. increasing the 'os' parameter moves the ranges by multiplications of 65. therefore if you add 5 indicators ontop of eachother, each scaled to left and set the os of each to another value (0,1,2,3,4) you will have a full spectum of avarages ranging from 7 to 325 in gaps of 2.

GapologyThis indicator can be used as a simple measure of price action tradability. It's an alternative to volume that focuses on the gaps between close and open candle prices. The bigger the gaps, the more spread and slippage you'll get when trading.

Hersheys Volume Pressure v2Hersheys Volume Pressure gives you very nice confirmation of trend starts and stops using volume and price.

For up bars...

If you have a large price change with low volume , that's very bullish .

If you have a small price change with low volume , that's bullish .

For down bars...

If you have a large price change with low volume , that's very bearish .

If you have a small price change with low volume , that's bearish .

Look at the chart and you'll see how trends start and end with a PINCH and widen in the middle of the moves.

You can set the moving average period, 14 is the default.

Good trading!

Brian Hershey

v2 change log...

- issue with price gaps - gaps at the open were sometimes showing incorrect colors

- scaling issues - sometimes a change is so large it scales down all nearby data and renders it hard to view. Code was added to clip those huge values.

v3 what's coming next...

- better scaling - sometimes with thinly traded stocks there is too much clipping. For now increase the chart interval to correct.

True Gap Finder with Revisit DetectionTrue Gap Finder with Revisit Detection

This indicator is a powerful tool for intraday traders to identify and track price gaps. Unlike simple gap indicators, this script actively tracks the status of the gap, visualizing the void until it is filled (revisited) by price.

Key Features:

Active Gap Tracking: Finds gap-up and gap-down occurrences (where Low > Previous High or High < Previous Low) and actively tracks them.

Gap Zones (Clouds): Visually shades the empty "gap zone" (the void between the gap candles), making it instantly obvious where price needs to travel to fill the gap. The cloud disappears automatically once the gap is filled.

Dynamic Labels: automatically displays price labels at the origin of the gap, showing the specific price range (High-Low) that constitutes the gap. Labels are positioned intelligently to avoid cluttering current price action.

Alerts: Configurable alerts notify you the moment a gap is filled.

Customization: Full control over colors, clouds, labels, and alert settings to match your chart style.

How it works: The indicator tracks the most recent gap. If a new gap forms, it becomes the active focus. When price moves back to "close" or "fill" this gap area, the lines and clouds automatically stop plotting, giving you a clean chart that focuses only on open business.

Probability Cone█ Overview:

Probability Cone is based on the Expected Move . While Expected Move only shows the historical value band on every bar, probability panel extend the period in the future and plot a cone or curve shape of the probable range. It plots the range from bar 1 all the way to bar 31.

In this model, we assume asset price follows a log-normal distribution and the log return follows a normal distribution.

Note: Normal distribution is just an assumption; it's not the real distribution of return.

The area of probability range is based on an inverse normal cumulative distribution function. The inverse cumulative distribution gives the range of price for given input probability. People can adjust the range by adjusting the standard deviation in the settings. The probability of the entered standard deviation will be shown at the edges of the probability cone.

The shown 68% and 95% probabilities correspond to the full range between the two blue lines of the cone (68%) and the two purple lines of the cone (95%). The probabilities suggest the % of outcomes or data that are expected to lie within this range. It does not suggest the probability of reaching those price levels.

Note: All these probabilities are based on the normal distribution assumption for returns. It's the estimated probability, not the actual probability.

█ Volatility Models :

Sample SD : traditional sample standard deviation, most commonly used, use (n-1) period to adjust the bias

Parkinson : Uses High/ Low to estimate volatility, assumes continuous no gap, zero mean no drift, 5 times more efficient than Close to Close

Garman Klass : Uses OHLC volatility, zero drift, no jumps, about 7 times more efficient

Yangzhang Garman Klass Extension : Added jump calculation in Garman Klass, has the same value as Garman Klass on markets with no gaps.

about 8 x efficient

Rogers : Uses OHLC, Assume non-zero mean volatility, handles drift, does not handle jump 8 x efficient.

EWMA : Exponentially Weighted Volatility. Weight recently volatility more, more reactive volatility better in taking account of volatility autocorrelation and cluster.

YangZhang : Uses OHLC, combines Rogers and Garmand Klass, handles both drift and jump, 14 times efficient, alpha is the constant to weight rogers volatility to minimize variance.

Median absolute deviation : It's a more direct way of measuring volatility. It measures volatility without using Standard deviation. The MAD used here is adjusted to be an unbiased estimator.

You can learn more about each of the volatility models in out Historical Volatility Estimators indicator.

█ How to use

Volatility Period is the sample size for variance estimation. A longer period makes the estimation range more stable less reactive to recent price. Distribution is more significant on larger sample size. A short period makes the range more responsive to recent price. Might be better for high volatility clusters.

People usually assume the mean of returns to be zero. To be more accurate, we can consider the drift in price from calculating the geometric mean of returns. Drift happens in the long run, so short lookback periods are not recommended.

The shape of the cone will be skewed and have a directional bias when the length of mean is short. It might be more adaptive to the current price or trend, but more accurate estimation should use a longer period for the mean.

Using a short look back for mean will make the cone having a directional bias.

When we are estimating the future range for time > 1, we typically assume constant volatility and the returns to be independent and identically distributed. We scale the volatility in term of time to get future range. However, when there's autocorrelation in returns( when returns are not independent), the assumption fails to take account of this effect. Volatility scaled with autocorrelation is required when returns are not iid. We use an AR(1) model to scale the first-order autocorrelation to adjust the effect. Returns typically don't have significant autocorrelation. Adjustment for autocorrelation is not usually needed. A long length is recommended in Autocorrelation calculation.

Note: The significance of autocorrelation can be checked on an ACF indicator.

ACF

Time back settings shift the estimation period back by the input number. It's the origin of when the probability cone start to estimation it's range.

E.g., When time back = 5, the probability cone start its prediction interval estimation from 5 bars ago. So for time back = 5 , it estimates the probability range from 5 bars ago to X number of bars in the future, specified by the Forecast Period (max 1000).

█ Warnings:

People should not blindly trust the probability. They should be aware of the risk evolves by using the normal distribution assumption. The real return has skewness and high kurtosis. While skewness is not very significant, the high kurtosis should be noticed. The Real returns have much fatter tails than the normal distribution, which also makes the peak higher. This property makes the tail ranges such as range more than 2SD highly underestimate the actual range and the body such as 1 SD slightly overestimate the actual range. For ranges more than 2SD, people shouldn't trust them. They should beware of extreme events in the tails.

The uncertainty in future bars makes the range wider. The overestimate effect of the body is partly neutralized when it's extended to future bars. We encourage people who use this indicator to further investigate the Historical Volatility Estimators , Fast Autocorrelation Estimator , Expected Move and especially the Linear Moments Indicator .

The probability is only for the closing price, not wicks. It only estimates the probability of the price closing at this level, not in between.

SMC Statistical Liquidity Walls [PhenLabs]📊 SMC Statistical Liquidity Walls

Version: PineScript™ v6

📌 Description

The SMC Statistical Liquidity Walls indicator is designed to visualize market volatility and potential reversal zones using advanced statistical modeling. Unlike traditional Bollinger Bands that use simple lines, this script utilizes an “Inverted Sigmoid” opacity function to create a “fog of war” effect. This visualizes the density of liquidity: the further price moves from the equilibrium (mean), the “harder” the liquidity wall becomes.

This tool solves the problem of over-trading in low-probability areas. By automatically mapping “Premium” (Resistance) and “Discount” (Support) zones based on Standard Deviation (SD), traders can instantly see when price is overextended. The result is a clean, intuitive overlay that helps you identify high-probability mean reversion setups without cluttering your chart with manual drawings.

🚀 Points of Innovation

Inverted Sigmoid Logic: A custom mathematical function maps Standard Deviation to opacity, creating a realistic “wall” density effect rather than linear gradients.

Dynamic “Solidity”: The indicator is transparent at the center (Equilibrium) and becomes visually solid at the edges, mimicking physical resistance.

Separated Directional Bias: distinct Red (Premium) and Green (Discount) coding helps SMC traders instantly recognize expensive vs. cheap pricing.

Smart “Safe” Deviation: Includes fallback logic to handle calculation errors if deviation hits zero, ensuring the indicator never crashes during data gaps.

🔧 Core Components

Basis Calculation: Uses a Simple Moving Average (SMA) to determine the market’s equilibrium point.

Standard Deviation Zones: Calculates 1SD, 2SD, and 3SD levels to define the statistical extremes of price action.

Sigmoid Alpha Calculation: Converts the SD distance into a transparency value (0-100) to drive the visual gradient.

🔥 Key Features

Automated Premium/Discount Zones: Red zones indicate overbought (Premium) areas; Green zones indicate oversold (Discount) areas.

Customizable Density: Users can adjust the “Steepness” and “Midpoint” of the sigmoid curve to control how fast the walls become solid.

Integrated Alerts: Built-in alert conditions trigger when price hits the “Solid” wall (2SD or higher), perfect for automated trading or notifications.

Visual Clarity: The center of the chart remains clear (high transparency) to keep focus on price action where it matters most.

🎨 Visualization

Equilibrium Line: A gray line representing the mean price.

Gradient Fills: The space between bands fills with color that increases in opacity as it moves outward.

Premium Wall: Upper zones fade from transparent red to solid red.

Discount Wall: Lower zones fade from transparent green to solid green.

📖 Usage Guidelines

Range Period: Default 20. Controls the lookback period for the SMA and Standard Deviation calculation.

Source: Default Close. The price data used for calculations.

Center Transparency: Default 100 (Clear). Controls how transparent the middle of the chart is.

Edge Transparency: Default 45 (Solid). Controls the opacity of the outermost liquidity wall.

Wall Steepness: Default 2.5. Adjusts how aggressively the gradient transitions from clear to solid.

Wall Start Point: Default 1.5 SD. The deviation level where the gradient shift begins to accelerate.

✅ Best Use Cases

Mean Reversion Trading: Enter trades when price hits the solid 2SD or 3SD wall and shows rejection wicks.

Take Profit Targets: Use the Equilibrium (Gray Line) as a logical first target for reversal trades.

Trend Filtering: Do not initiate new long positions when price is deep inside the Red (Premium) wall.

⚠️ Limitations

Lagging Nature: As a statistical tool based on Moving Averages, the walls react to past price data and may lag during sudden volatility spikes.

Trending Markets: In strong parabolic trends, price can “ride” the bands for extended periods; mean reversion should be used with caution in these conditions.

💡 What Makes This Unique

Physics-Based Visualization: We treat liquidity as a physical barrier that gets denser the deeper you push, rather than just a static line on a chart.

🔬 How It Works

Step 1: The script calculates the mean (SMA) and the Standard Deviation (SD) of the source price.

Step 2: It defines three zones above and below the mean (1SD, 2SD, 3SD).

Step 3: The custom `get_inverted_sigmoid` function calculates an Alpha (transparency) value based on the SD distance.

Step 4: Plot fills are colored dynamically, creating a seamless gradient that hardens at the extremes to visualize the “Liquidity Wall.”

💡 Note

For best results, combine this indicator with Price Action confirmation (such as pin bars or engulfing candles) when price touches the solid walls.

Expected Move BandsExpected move is the amount that an asset is predicted to increase or decrease from its current price, based on the current levels of volatility.

In this model, we assume asset price follows a log-normal distribution and the log return follows a normal distribution.

Note: Normal distribution is just an assumption, it's not the real distribution of return

Settings:

"Estimation Period Selection" is for selecting the period we want to construct the prediction interval.

For "Current Bar", the interval is calculated based on the data of the previous bar close. Therefore changes in the current price will have little effect on the range. What current bar means is that the estimated range is for when this bar close. E.g., If the Timeframe on 4 hours and 1 hour has passed, the interval is for how much time this bar has left, in this case, 3 hours.

For "Future Bars", the interval is calculated based on the current close. Therefore the range will be very much affected by the change in the current price. If the current price moves up, the range will also move up, vice versa. Future Bars is estimating the range for the period at least one bar ahead.

There are also other source selections based on high low.

Time setting is used when "Future Bars" is chosen for the period. The value in time means how many bars ahead of the current bar the range is estimating. When time = 1, it means the interval is constructing for 1 bar head. E.g., If the timeframe is on 4 hours, then it's estimating the next 4 hours range no matter how much time has passed in the current bar.

Note: It's probably better to use "probability cone" for visual presentation when time > 1

Volatility Models :

Sample SD: traditional sample standard deviation, most commonly used, use (n-1) period to adjust the bias

Parkinson: Uses High/ Low to estimate volatility, assumes continuous no gap, zero mean no drift, 5 times more efficient than Close to Close

Garman Klass: Uses OHLC volatility, zero drift, no jumps, about 7 times more efficient

Yangzhang Garman Klass Extension: Added jump calculation in Garman Klass, has the same value as Garman Klass on markets with no gaps.

about 8 x efficient

Rogers: Uses OHLC, Assume non-zero mean volatility, handles drift, does not handle jump 8 x efficient

EWMA: Exponentially Weighted Volatility. Weight recently volatility more, more reactive volatility better in taking account of volatility autocorrelation and cluster.

YangZhang: Uses OHLC, combines Rogers and Garmand Klass, handles both drift and jump, 14 times efficient, alpha is the constant to weight rogers volatility to minimize variance.

Median absolute deviation: It's a more direct way of measuring volatility. It measures volatility without using Standard deviation. The MAD used here is adjusted to be an unbiased estimator.

Volatility Period is the sample size for variance estimation. A longer period makes the estimation range more stable less reactive to recent price. Distribution is more significant on a larger sample size. A short period makes the range more responsive to recent price. Might be better for high volatility clusters.

Standard deviations:

Standard Deviation One shows the estimated range where the closing price will be about 68% of the time.

Standard Deviation two shows the estimated range where the closing price will be about 95% of the time.

Standard Deviation three shows the estimated range where the closing price will be about 99.7% of the time.

Note: All these probabilities are based on the normal distribution assumption for returns. It's the estimated probability, not the actual probability.

Manually Entered Standard Deviation shows the range of any entered standard deviation. The probability of that range will be presented on the panel.

People usually assume the mean of returns to be zero. To be more accurate, we can consider the drift in price from calculating the geometric mean of returns. Drift happens in the long run, so short lookback periods are not recommended. Assuming zero mean is recommended when time is not greater than 1.

When we are estimating the future range for time > 1, we typically assume constant volatility and the returns to be independent and identically distributed. We scale the volatility in term of time to get future range. However, when there's autocorrelation in returns( when returns are not independent), the assumption fails to take account of this effect. Volatility scaled with autocorrelation is required when returns are not iid. We use an AR(1) model to scale the first-order autocorrelation to adjust the effect. Returns typically don't have significant autocorrelation. Adjustment for autocorrelation is not usually needed. A long length is recommended in Autocorrelation calculation.

Note: The significance of autocorrelation can be checked on an ACF indicator.

ACF

The multimeframe option enables people to use higher period expected move on the lower time frame. People should only use time frame higher than the current time frame for the input. An error warning will appear when input Tf is lower. The input format is multiplier * time unit. E.g. : 1D

Unit: M for months, W for Weeks, D for Days, integers with no unit for minutes (E.g. 240 = 240 minutes). S for Seconds.

Smoothing option is using a filter to smooth out the range. The filter used here is John Ehler's supersmoother. It's an advance smoothing technique that gets rid of aliasing noise. It affects is similar to a simple moving average with half the lookback length but smoother and has less lag.

Note: The range here after smooth no long represent the probability

Panel positions can be adjusted in the settings.

X position adjusts the horizontal position of the panel. Higher X moves panel to the right and lower X moves panel to the left.

Y position adjusts the vertical position of the panel. Higher Y moves panel up and lower Y moves panel down.

Step line display changes the style of the bands from line to step line. Step line is recommended because it gets rid of the directional bias of slope of expected move when displaying the bands.

Warnings:

People should not blindly trust the probability. They should be aware of the risk evolves by using the normal distribution assumption. The real return has skewness and high kurtosis. While skewness is not very significant, the high kurtosis should be noticed. The Real returns have much fatter tails than the normal distribution, which also makes the peak higher. This property makes the tail ranges such as range more than 2SD highly underestimate the actual range and the body such as 1 SD slightly overestimate the actual range. For ranges more than 2SD, people shouldn't trust them. They should beware of extreme events in the tails.

Different volatility models provide different properties if people are interested in the accuracy and the fit of expected move, they can try expected move occurrence indicator. (The result also demonstrate the previous point about the drawback of using normal distribution assumption).

Expected move Occurrence Test

The prediction interval is only for the closing price, not wicks. It only estimates the probability of the price closing at this level, not in between. E.g., If 1 SD range is 100 - 200, the price can go to 80 or 230 intrabar, but if the bar close within 100 - 200 in the end. It's still considered a 68% one standard deviation move.