Dr.ManiaTemel olarak teknik analizlerde kullanılabilecek en yaygın komutların hepsinin bir arada olduğu (Ichimoku, MavilimW, Bollinger, Oklar, Hareketli Ortalamaları) komuttur.

Ichimoku+MavilimW+BB+Arrow+MAVCOMBO

Cari dalam skrip untuk "ichimoku"

Cloud, MA & BB Signal ConvergenceA combination of 3 popular lagging indicators (Ichimoku Cloud, Moving Average and Bollinger Bands) that generates a signal when all 3 of those lagging indicators are bullish or bearish.

Bullish is represented with a green dot above price. Bearish is represented with a red dot below price.

PARAMETERS:

1) Ichimoku Cloud

-Bullish Kumo

-Price above Kumo

-Chikou span above price

-Tenkan-sen and Kijun-sen above Kumo

-Tenkan-sen above Kijun-sen

-Price above Tenkan-sen

*opposite for bearish

Note: cloud settings is the popular settings for cryptocurrency advocated by @CarpeNoctom.

2) Moving Average

-MA1 greater than MA2

-MA2 greater than MA3

-MA3 greater than MA4

-MA4 greater than MA5

*opposite for bearish

Note: Put your MA setting from lowest to highest on MA1-MA5 respectively to generate more accurate signals.

3) Bollinger Bands

-price closed above upper band at least once

*opposite for bearish

Note: Put your MA setting from lowest to highest on MA1-MA5 respectively to generate more accurate signals.

P.S. Still on early alpha stage.

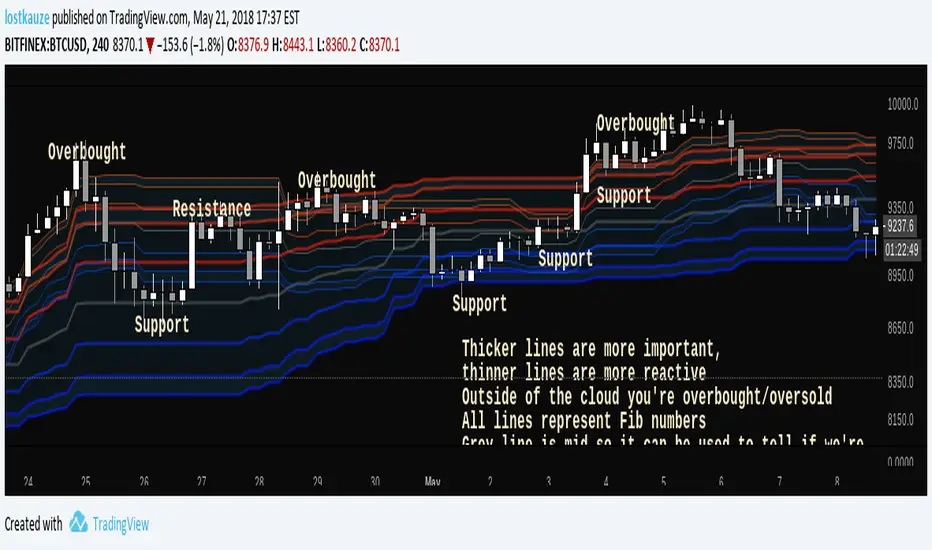

Fibonacci CloudInspired by Ichimoku Fibonacci Hybrid , this indicator is for those who don't mind a lot of lines. All lines represent Fib ratios: thicker lines are fibs for a longer period, while thinner lines are fibs for a shorter period.

- Dynamic S/R

- Overbought/Oversold zones

- Trend indicator

- Customisable periods

- Fast/Slow crossovers

See what works for you!

Gyspy Bot Trade Engine - V1.2B - Alerts - 12-7-25 - SignalLynxGypsy Bot Trade Engine (MK6 V1.2B) - Alerts & Visualization

Brought to you by Signal Lynx | Automation for the Night-Shift Nation 🌙

1. Executive Summary & Architecture

Gypsy Bot (MK6 V1.2B) is not merely a strategy; it is a massive, modular Trade Engine built specifically for the TradingView Pine Script V6 environment. While most tools rely on a single dominant indicator to generate signals, Gypsy Bot functions as a sophisticated Consensus Algorithm.

Note: This is the Indicator / Alerts version of the engine. It is designed for visual analysis and generating live alert signals for automation. If you wish to see Backtest data (Equity Curves, Drawdown, Profit Factors), please use the Strategy version of this script.

The engine calculates data from up to 12 distinct Technical Analysis Modules simultaneously on every bar closing. It aggregates these signals into a "Vote Count" and only fires a signal plot when a user-defined threshold of concurring signals is met. This "Voting System" acts as a noise filter, requiring multiple independent mathematical models—ranging from volume flow and momentum to cyclical harmonics and trend strength—to agree on market direction.

Beyond entries, Gypsy Bot features a proprietary Risk Management suite called the Dump Protection Team (DPT). This logic layer operates independently of the entry modules, specifically scanning for "Moon" (Parabolic) or "Nuke" (Crash) volatility events to signal forced exits, preserving capital during Black Swan events.

2. ⚠️ The Philosophy of "Curve Fitting" (Must Read)

One must be careful when applying Gypsy Bot to new pairs or charts.

To be fully transparent: Gypsy Bot is, by definition, a very advanced curve-fitting engine. Because it grants the user granular control over 12 modules, dozens of thresholds, and specific voting requirements, it is extremely easy to "over-fit" the data. You can easily toggle switches until the charts look perfect in hindsight, only to have the signals fail in live markets because they were tuned to historical noise rather than market structure.

To use this engine successfully:

Visual Verification: Do not just look for "green arrows." Look for signals that occur at logical market structure points.

Stability: Ensure signals are not flickering. This script uses closed-candle logic for key decisions to ensure that once a signal plots, it remains painted.

Regular Maintenance is Mandatory: Markets shift regimes (e.g., from Bull Trend to Crab Range). Gypsy Bot settings should be reviewed and adjusted at regular intervals to ensure the voting logic remains aligned with current market volatility.

Timeframe Recommendations:

Gypsy Bot is optimized for High Time Frame (HTF) trend following. It generally produces the most reliable results on charts ranging from 1-Hour to 12-Hours, with the 4-Hour timeframe historically serving as the "sweet spot" for most major cryptocurrency assets.

3. The Voting Mechanism: How Entries Are Generated

The heart of the Gypsy Bot engine is the ActivateOrders input (found in the "Order Signal Modifier" settings).

The engine constantly monitors the output of all enabled Modules.

Long Votes: GoLongCount

Short Votes: GoShortCount

If you have 10 Modules enabled, and you set ActivateOrders to 7:

The engine will ONLY plot a Buy Signal if 7 or more modules return a valid "Buy" signal on the same closed candle.

If only 6 modules agree, the signal is rejected.

4. Technical Deep Dive: The 12 Modules

Gypsy Bot allows you to toggle the following modules On/Off individually to suit the asset you are trading.

Module 1: Modified Slope Angle (MSA)

Logic: Calculates the geometric angle of a moving average relative to the timeline.

Function: Filters out "lazy" trends. A trend is only considered valid if the slope exceeds a specific steepness threshold.

Module 2: Correlation Trend Indicator (CTI)

Logic: Measures how closely the current price action correlates to a straight line (a perfect trend).

Function: Ensures that we are moving up with high statistical correlation, reducing fake-outs.

Module 3: Ehlers Roofing Filter

Logic: A spectral filter combining High-Pass (trend removal) and Super Smoother (noise removal).

Function: Isolates the "Roof" of price action to catch cyclical turning points before standard moving averages.

Module 4: Forecast Oscillator

Logic: Uses Linear Regression forecasting to predict where price "should" be relative to where it is.

Function: Signals when the regression trend flips. Offers "Aggressive" and "Conservative" calculation modes.

Module 5: Chandelier ATR Stop

Logic: A volatility-based trend follower that hangs a "leash" (ATR multiple) from extremes.

Function: Used as an entry filter. If price is above the Chandelier line, the trend is Bullish.

Module 6: Crypto Market Breadth (CMB)

Logic: Pulls data from multiple major tickers (BTC, ETH, and Perpetual Contracts).

Function: Calculates "Market Health." If Bitcoin is rising but the rest of the market is dumping, this module can veto a trade.

Module 7: Directional Index Convergence (DIC)

Logic: Analyzes the convergence/divergence between Fast and Slow Directional Movement indices.

Function: Identifies when trend strength is expanding.

Module 8: Market Thrust Indicator (MTI)

Logic: A volume-weighted breadth indicator using Advance/Decline and Volume data.

Function: One of the most powerful modules. Confirms that price movement is supported by actual volume flow. Recommended setting: "SSMA" (Super Smoother).

Module 9: Simple Ichimoku Cloud

Logic: Traditional Japanese trend analysis.

Function: Checks for a "Kumo Breakout." Price must be fully above/below the Cloud to confirm entry.

Module 10: Simple Harmonic Oscillator

Logic: Analyzes harmonic wave properties to detect cyclical tops and bottoms.

Function: Serves as a counter-trend or early-reversal detector.

Module 11: HSRS Compression / Super AO

Logic: Detects volatility compression (HSRS) or Momentum/Trend confluence (Super AO).

Function: Great for catching explosive moves resulting from consolidation.

Module 12: Fisher Transform (MTF)

Logic: Converts price data into a Gaussian normal distribution.

Function: Identifies extreme price deviations. Uses Multi-Timeframe (MTF) logic to ensure you aren't trading against the major trend.

5. Global Inhibitors (The Veto Power)

Even if 12 out of 12 modules vote "Buy," Gypsy Bot performs a final safety check using Global Inhibitors.

Bitcoin Halving Logic: Prevents trading during chaotic weeks surrounding Halving events (dates projected through 2040).

Miner Capitulation: Uses Hash Rate Ribbons to identify bearish regimes when miners are shutting down.

ADX Filter: Prevents trading in "Flat/Choppy" markets (Low ADX).

CryptoCap Trend: Checks the total Crypto Market Cap chart for broad market alignment.

6. Risk Management & The Dump Protection Team (DPT)

Even in this Indicator version, the RM logic runs to generate Exit Signals.

Dump Protection Team (DPT): Detects "Nuke" (Crash) or "Moon" (Pump) volatility signatures. If triggered, it plots an immediate Exit Signal (Yellow Plot).

Advanced Adaptive Trailing Stop (AATS): Dynamically tightens stops in low volatility ("Dungeon") and loosens them in high volatility ("Penthouse").

Staged Take Profits: Plots TP1, TP2, and TP3 events on the chart for visual confirmation or partial exit alerts.

7. Recommended Setup Guide

When applying Gypsy Bot to a new chart, follow this sequence:

Set Timeframe: 4 Hours (4H).

Tune DPT: Adjust "Dump/Moon Protection" inputs first. These filter out bad signals during high volatility.

Tune Module 8 (MTI): Experiment with the MA Type (SSMA is recommended).

Select Modules: Enable/Disable modules based on the asset's personality (Trending vs. Ranging).

Voting Threshold: Adjust ActivateOrders to filter out noise.

Alert Setup: Once visually satisfied, use the "Any Alert Function Call" option when creating an alert in TradingView to capture all Buy/Sell/Close events generated by the engine.

8. Technical Specs

Engine Version: Pine Script V6

Repainting: This indicator uses Closed Candle data for all Risk Management and Entry decisions. This ensures that signals do not vanish after the candle closes.

Visuals:

Blue Plot: Buy/Sell Signal.

Yellow Plot: Risk Management (RM) / DPT Close Signal.

Green/Lime/Olive Plots: Take Profit hits.

Disclaimer:

This script is a complex algorithmic tool for market analysis. Past performance is not indicative of future results. Cryptocurrency trading involves substantial risk of loss. Use this tool to assist your own decision-making, not to replace it.

9. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

Enhanced Ichimoku CloudDYNAMIC INDICATOR... im a beginer at this so i like to enhance my indicator by adding Visual Elements so that its easier to read for me... here is a visual representation of trend changes.

Relative Volume EMA (RVOL)Relative Volume EMA (RVOL) measures the current bar’s volume relative to its typical volume over a selected lookback period.

It helps traders identify whether a price move is supported by real participation or if it’s occurring on weak, low-quality volume.

This version uses:

RVOL = Current Volume ÷ Volume EMA

Volume EMA Length: adjustable

Signal Threshold: a customizable horizontal line (default = 1.2)

How to Use

1. RVOL > 1.2 → High-Quality Momentum

A value above 1.2 indicates that the current bar has at least 20% more volume than normal, suggesting:

Strong conviction

Algorithmic activity

Momentum-backed breakout or breakdown

Higher probability trend continuation

These bars are ideal for confirming entries after a technical setup (e.g., pullback, engulfing pattern, Ichimoku trend confirmation, etc.).

2. RVOL < 1.0 → Weak or Low-Quality Move

When RVOL is below 1.0:

Volume is below average

Moves are more likely to fail or reverse

Breakouts are unreliable

Triggers lack institutional participation

These bars are best avoided for trade entries.

Why This Indicator Is Useful

In many strategies, price alone is not enough.

RVOL acts as a filter to ensure that your signals occur during times when the market is actually active and committed.

Typical use cases:

Confirm trend-following entries

Validate pullbacks and breakout candles

Filter out low-volume chop

Identify session-based volume surges

Improve risk-to-reward quality by entering only during true momentum

Recommended Settings

EMA Length: 20

Threshold Line: 1.2

Works well on Forex, Crypto, and Indices

Best used on 15m, 30m, 1H, and 4H charts

Super momentum DBSISuper momentum DBSI: The Ultimate Guide

1. What is this Indicator?

The Super momentum DBSI is a "Consensus Engine." Instead of relying on a single line (like an RSI) to tell you where the market is going, this tool calculates 33 distinct technical indicators simultaneously for every single candle.

It treats the market like a democracy. It asks 33 mathematical "voters" (Momentum, Trend, Volume, Volatility) if they are Bullish or Bearish.

If 30 out of 33 say "Buy," the score is high (Yellow), and the trend is extremely strong.

If only 15 say "Buy," the score is low (Teal), and the trend is weak or choppy.

2. Visual Guide: How to Read the Numbers

The Scores

Top Number (Bears): Represents Selling Pressure.

Bottom Number (Bulls): Represents Buying Pressure.

The Colors (The Traffic Lights)

The colors are your primary signal. They tell you who is currently winning the war.

🟡 YELLOW (Dominance):

This indicates the Winning Side.

If the Bottom Number is Yellow, Bulls are in control.

If the Top Number is Yellow, Bears are in control.

🔴 RED (Weakness):

This appears on the Top. It means Bears are present but losing.

🔵 TEAL (Weakness):

This appears on the Bottom. It means Bulls are present but losing.

3. Trading Strategy

Scenario A: The "Strong Buy" (Long Entry)

The Setup: You are looking for a shift in momentum where Buyers overwhelm Sellers.

Watch the Bottom Number: Wait for it to turn Yellow.

Confirm Strength: Ensure the score is above 15 and rising (e.g., 12 → 18 → 22).

Check the Top: The Top Number should be Red and low (below 10).

Trigger: Enter on the candle close.

Scenario B: The "Strong Sell" (Short Entry)

The Setup: You are looking for Sellers to crush the Buyers.

Watch the Top Number: Wait for it to turn Yellow.

Confirm Strength: Ensure the score is above 15 and rising.

Check the Bottom: The Bottom Number should be Teal and low.

Trigger: Enter on the candle close.

Scenario C: The "No Trade Zone" (Choppy Market)

The Setup: The market is confused.

Visual: Top is Red, Bottom is Teal.

Meaning: NOBODY IS WINNING. There is no Yellow number.

Action: Do not trade. This usually happens during lunch hours, weekends, or right before big news. This filter alone will save you from many false breakouts.

4. What is Inside? (The 33 Indicators)

To give you confidence in the signals, here is exactly what the script is checking:

Group 1: Momentum (Oscillators)

Detects if price is moving fast.

RSI (Relative Strength Index)

CCI (Commodity Channel Index)

Stochastic

Williams %R

Momentum

Rate of Change (ROC)

Ultimate Oscillator

Awesome Oscillator

True Strength Index (TSI)

Stoch RSI

TRIX

Chande Momentum Oscillator

Group 2: Trend Direction

Detects the general path of the market.

13. MACD

14. Parabolic SAR

15. SuperTrend

16. ALMA (Moving Average)

17. Aroon

18. ADX (Directional Movement)

19. Coppock Curve

20. Ichimoku Conversion Line

21. Hull Moving Average

Group 3: Price Action

Detects where price is relative to averages.

22. Price vs EMA 20

23. Price vs EMA 50

24. Price vs EMA 200

Group 4: Volume & Force

Detects if there is money behind the move.

25. Money Flow Index (MFI)

26. On Balance Volume (OBV)

27. Chaikin Money Flow (CMF)

28. VWAP (Intraday)

29. Elder Force Index

30. Ease of Movement

Group 5: Volatility

Detects if price is pushing the outer limits.

31. Bollinger Bands

32. Keltner Channels

33. Donchian Channels

5. Pro Tips for Success

Don't Catch Knives: If the Bear score (Top) is Yellow and 25+, do not try to buy the dip. Wait for the Yellow score to break.

Exit Early: If you are Long and the Yellow Bull score drops from 28 to 15 in one candle, TAKE PROFIT. The momentum has died.

Use Higher Timeframes: This indicator works best on 15m, 1H, and 4H charts. On the 1m chart, it may be too volatile.

Ansupublicly-usable Pine Script that implements the same concepts described on that page (Ichimoku, McGinley, multiple moving averages, RSI, MACD, Stochastic, Bollinger Bands, and composite buy/sell signals). Below is a solid Pine-Script v5 implementation you can add to TradingView and tweak

Lynie's V9 SELL🟢🔴 Lynie’s V8 — BUY & SELL (Mirrored, Interlocking System)

Lynie’s V8 is a paired long/short engine built as two mirrored scripts—Lynie’s V8 BUY and Lynie’s V8 SELL—that read price the same way, flip conditions symmetrically, and manage trades with the exact logic on opposite sides. Use either one standalone or run both together for full two-sided automation of entries, re-entries, caution states, and adaptive SL/TP.

✳️ What “mirrored” means here

Supertrend Tri-Stack (10/11/12):

BUY: ST10 primary pierce; ST12 fallback; “PAG Buy” when price pierces any ST while above the other two.

SELL: Exact inverse—ST10 primary pierce down; ST12 fallback; “PAG Sell” when price pierces any ST while below the other two.

Re-Enter Clusters:

BUY: Ratcheted up (Heikin-Ashi green holds/tightens).

SELL: Ratcheted down (Heikin-Ashi red holds/tightens).

Both sides use the same cluster age/decay math, care penalties, session awareness, and fast-candle tightening.

Care Flags (context risk):

Ichimoku, MACD, RSI combine into single and paired flags that tighten or widen offsets on both sides with the same scoring.

VWAP–EMA50 (5m) cluster gate:

Identical distance checks for BUY/SELL. When the mean cluster is present, offsets and labels adapt (tighter/“riskier scalp” messaging).

Golden Pocket A/B/C (prev-day):

Same fib boxes & labeling (gold tone) on both sides to call out TP-friendly zones.

SL/TP Envelope:

Shared dynamic engine: per-bar decay, fast-candle expansion, and care-based compress/relax—all mirrored for up/down.

Caution Labels:

BUY side prints CAUTION SELL if HA flips red inside an active long cluster.

SELL side prints CAUTION BUY if HA flips green inside an active short cluster.

Same latching & auto-release behavior.

🧠 Core workflow (both sides)

Primary trigger via ST10 pierce (structure shift) with an ST12 fallback when ST10 didn’t qualify.

PAG Mode when price is already on the right side of the other two STs—strongest conviction.

Cluster phase begins after a signal: ratcheted re-entry level, session-aware offsets, dynamic tightening on fast bars.

Care system shapes every re-entry & SL/TP label (Ichi/MACD/RSI combos + VWAP/EMA gate + QQE).

Protective layer: SL-wick and SL-body logic, caution flips, and “hold 1 bar” cluster carry after SL to avoid whipsaw spam.

🔎 Labels & messages (shared vocabulary)

Lynie’s / Lynie’s+ / Lynie’s++ — strength tiers (ST12 involvement & clean context).

Re-Enter / Excellent Re-Enter — cluster pullback quality; ratchet shows the “must-hold” zone.

SL&TP (n) — live offset multiplier the engine is using right now.

CAUTION BUY / CAUTION SELL — HA flip against the active side inside the cluster.

Restart Next Candle — visual cue to re-arm after a confirmed signal bar.

⚡ Why run both together

Continuity: When a long cycle ends (SL or caution degradation), the SELL engine is already tracking the inverse without re-tuning.

Symmetry: Same math, same signals, opposite direction—no hidden biases.

Coverage: Trend hand-offs are cleaner; you don’t miss early shorts after a long fade (and vice versa).

🔧 Recommended usage

Intraday futures (ES/NQ) or any liquid market.

Keep the VWAP–EMA cluster ON; it filters FOMO chases.

Honor Caution flips inside cluster—scale down or wait for the next clean re-enter.

Treat Golden Zones as TP magnets, not guaranteed reversals.

📌 Notes

Both scripts are Pine v6 and independent. Load BUY and SELL together for the full experience.

All offsets (re-enter & SL/TP) are visible in labels—so you always know why a zone is where it is.

Alerts are provided for signals, re-enter hits, caution, and SL events on both sides.

Summary: Lynie’s V8 BUY & SELL are vice-versa twins—one framework, two directions—delivering consistent entries, adaptive re-entries, and contextual risk management whether the market is pressing up or breaking down.

Advanced Multi-Timeframe Trend & Signal System═══════════════════════════════════════════════════════════════

ADVANCED MULTI-TIMEFRAME TREND & SIGNAL SYSTEM v1.0

═══════════════════════════════════════════════════════════════

Created by: Zakaria Safri

License: Mozilla Public License 2.0

A comprehensive technical analysis tool designed for traders seeking

multi-dimensional market insights. This indicator combines proven

technical analysis methods with modern visualization techniques.

═══════════════════════════════════════════════════════════════

KEY FEATURES

═══════════════════════════════════════════════════════════════

✓ SUPERTREND SIGNAL GENERATION

- Customizable sensitivity settings

- Clear long/short entry signals

- Automatic trend direction detection

- ATR-based dynamic calculations

✓ MULTI-TIMEFRAME DASHBOARD

- Real-time trend analysis across 6 timeframes

- Synchronized trend confirmation

- Customizable table position and size

- Current: 1M, 5M, 15M, 1H, 1D coverage

✓ QQE REVERSAL DETECTION

- Quantitative Qualitative Estimation algorithm

- Early reversal signal identification

- Adjustable RSI and smoothing parameters

- Confirmation-based plotting

✓ DYNAMIC SUPPORT & RESISTANCE

- Pivot-based level calculation

- Quick and standard pivot detection

- Color-coded zones (8 levels)

- Automatic level updates

✓ MOMENTUM BREAKOUT SIGNALS

- Ichimoku-inspired calculations

- Bullish and bearish breakout detection

- Visual zone highlighting

- Trend confirmation filters

✓ RISK MANAGEMENT SYSTEM

- ATR-based stop loss calculation

- Multiple take profit targets (TP1, TP2, TP3)

- Customizable risk-to-reward ratios

- Dynamic price level tracking

- Hit detection markers

✓ VOLATILITY BANDS

- Keltner Channel implementation

- Multiple band layers (3 levels)

- EMA-based calculations

- Adaptive to market conditions

✓ TREND CLOUD VISUALIZATION

- Dual moving average cloud

- Clear trend direction indication

- Customizable color scheme

- Trend bar coloring

═══════════════════════════════════════════════════════════════

HOW TO USE

═══════════════════════════════════════════════════════════════

SETUP:

1. Add indicator to your chart

2. Configure sensitivity in Core Signals section

3. Enable desired features (signals, reversals, breakouts)

4. Set up risk management levels if trading

5. Position MTF dashboard to preference

SIGNAL INTERPRETATION:

• LONG Signal: Price crosses above Supertrend

• SHORT Signal: Price crosses below Supertrend

• REV (Reversal): QQE indicates potential trend change

• Diamond Breakouts: Momentum shift confirmation

• T1/T2/T3: Take profit level hits

MULTI-TIMEFRAME ANALYSIS:

• Green (BULL): Higher timeframe supports uptrend

• Red (BEAR): Higher timeframe supports downtrend

• Use for trend alignment and confirmation

• Best results when multiple timeframes align

RISK MANAGEMENT:

• Enable Stop Loss for automatic SL calculation

• Activate TP levels based on trading style

• Adjust Risk-to-Reward ratio (1:1 to 1:10)

• Monitor hit detection circles for exits

═══════════════════════════════════════════════════════════════

TECHNICAL SPECIFICATIONS

═══════════════════════════════════════════════════════════════

CALCULATIONS:

• Supertrend: ATR-based with customizable multiplier

• QQE: Modified RSI with Wilders smoothing

• Keltner Channels: EMA basis with ATR bands

• Pivots: Standard left/right bar methodology

• Support/Resistance: Multi-level pivot analysis

PARAMETERS:

• Supertrend Sensitivity: 0.5 to 10.0 (default: 2.0)

• RSI Period: 5 to 50 (default: 14)

• QQE Multiplier: 1.0 to 10.0 (default: 4.238)

• Risk-to-Reward: 1 to 10 (default: 4)

TIMEFRAMES:

Compatible with all timeframes. MTF dashboard displays:

• 1 Minute (1M)

• 5 Minutes (5M)

• 15 Minutes (15M)

• 1 Hour (1H)

• 1 Day (1D)

• Current chart timeframe

═══════════════════════════════════════════════════════════════

CUSTOMIZATION OPTIONS

═══════════════════════════════════════════════════════════════

VISUAL:

• Professional color scheme (Cyan/Orange)

• Adjustable table position (9 positions)

• Table size options (tiny/small/normal/large)

• Transparent zone highlighting

• Clean, modern label design

TOGGLES:

• Enable/disable any feature independently

• Show/hide signals, reversals, breakouts

• Toggle S/R levels and zones

• Control trend cloud and bands

• Master trend line optional

ALERTS:

The indicator provides visual signals that can be used with

TradingView's alert system by setting alerts on the indicator.

═══════════════════════════════════════════════════════════════

BEST PRACTICES

═══════════════════════════════════════════════════════════════

✓ Combine signals for higher probability setups

✓ Use MTF dashboard for trend confirmation

✓ Respect S/R levels for entry/exit planning

✓ Monitor QQE reversals at key price levels

✓ Adjust sensitivity based on asset volatility

✓ Test on demo/paper trading first

✓ Use proper risk management always

═══════════════════════════════════════════════════════════════

IMPORTANT DISCLAIMER

═══════════════════════════════════════════════════════════════

This indicator is a technical analysis tool and does NOT:

• Guarantee profitable trades

• Provide financial advice

• Predict future price movements with certainty

• Replace proper risk management

• Substitute for personal due diligence

Past performance does not indicate future results. All trading

involves risk. Users should:

- Understand the indicator's logic

- Test thoroughly before live trading

- Use appropriate position sizing

- Never risk more than they can afford to lose

- Consult financial advisors if needed

═══════════════════════════════════════════════════════════════

CODING STANDARDS

═══════════════════════════════════════════════════════════════

This indicator follows PineCoders Coding Conventions:

✓ Proper variable naming (prefixes: i_, f_, c_)

✓ Clear function documentation

✓ Organized code structure

✓ Type declarations

✓ Efficient calculations

✓ No repainting (confirmed signals)

✓ Proper use of request.security

═══════════════════════════════════════════════════════════════

SUPPORT & UPDATES

═══════════════════════════════════════════════════════════════

Version: 1.0

Author: Zakaria Safri

License: MPL 2.0

Last Updated: 2024

For questions, feedback, or suggestions, please comment below.

═══════════════════════════════════════════════════════════════

#trading #signals #supertrend #multiTimeframe #QQE #reversals

#supportResistance #riskManagement #trendAnalysis #momentum

Forecast PriceTime Oracle [CHE] Forecast PriceTime Oracle — Prioritizes quality over quantity by using Power Pivots via RSI %B metric to forecast future pivot highs/lows in price and time

Summary

This indicator identifies potential pivot highs and lows based on out-of-bounds conditions in a modified RSI %B metric, then projects future occurrences by estimating time intervals and price changes from historical medians. It provides visual forecasts via diagonal and horizontal lines, tracks achievement with color changes and symbols, and displays a dashboard for statistical overview including hit rates. Signals are robust due to median-based aggregation, which reduces outlier influence, and optional tolerance settings for near-misses, making it suitable for anticipating reversals in ranging or trending markets.

Motivation: Why this design?

Standard pivot detection often lags or generates false signals in volatile conditions, missing the timing of true extrema. This design leverages out-of-bounds excursions in RSI %B to capture "Power Pivots" early—focusing on quality over quantity by prioritizing significant extrema rather than every minor swing—then uses historical deltas in time and price to forecast the next ones, addressing the need for proactive rather than reactive analysis. It assumes that pivot spacing follows statistical patterns, allowing users to prepare entries or exits ahead of confirmation.

What’s different vs. standard approaches?

- Reference baseline: Diverges from traditional ta.pivothigh/low, which require fixed left/right lengths and confirm only after bars close, often too late for dynamic markets.

- Architecture differences:

- Detects extrema during OOB runs rather than post-bar symmetry.

- Aggregates deltas via medians (or alternatives) over a user-defined history, capping arrays to manage resources.

- Applies tolerance thresholds for hit detection, with options for percentage, absolute, or volatility-adjusted (ATR) flexibility.

- Freezes achieved forecasts with visual states to avoid clutter.

- Practical effect: Charts show proactive dashed projections instead of retrospective dots; the dashboard reveals evolving hit rates, helping users gauge reliability over time without manual calculation.

How it works (technical)

The indicator first computes a smoothed RSI over a specified length, then applies Bollinger Bands to derive %B, flagging out-of-bounds below zero or above one hundred as potential run starts. During these runs, it tracks the extreme high or low price and bar index. Upon exit from the OOB state, it confirms the Power Pivot at that extreme and records the time delta (bars since prior) and price change percentage to rolling arrays.

For forecasts, it calculates the median (or selected statistic) of recent deltas, subtracts the confirmation delay (bars from apex to exit), and projects ahead by that adjusted amount. Price targets use the median change applied to the origin pivot value. Lines are drawn from the apex to the target bar and price, with a short horizontal at the endpoint. Arrays store up to five active forecasts, pruning oldest on overflow.

Tolerance adjusts hit checks: for highs, if the high reaches or exceeds the target (adjusted by tolerance); for lows, if the low drops to or below. Once hit, the forecast freezes, changing colors and symbols, and extends the horizontal to the hit bar. Persistent variables maintain last pivot states across bars; arrays initialize empty and grow until capped at history length.

Parameter Guide

Source: Specifies the data input for the RSI computation, influencing how price action is captured. Default is close. For conservative signals in noisy environments, switch to high; using low boosts responsiveness but may increase false positives.

RSI Length: Sets the smoothing period for the RSI calculation, with longer values helping to filter out whipsaws. Default is 32. Opt for shorter lengths like 14 to 21 on faster timeframes for quicker reactions, or extend to 50 or more in strong trends to enhance stability at the cost of some lag.

BB Length: Defines the period for the Bollinger Bands applied to %B, directly affecting how often out-of-bounds conditions are triggered. Default is 20. Align it with the RSI length: shorter periods detect more potential runs but risk added noise, while longer ones provide better filtering yet might overlook emerging extrema.

BB StdDev: Controls the multiplier for the standard deviation in the bands, where wider settings reduce false out-of-bounds alerts. Default is 2.0. Narrow it to 1.5 for highly volatile assets to catch more signals, or broaden to 2.5 or higher to emphasize only major movements.

Show Price Forecast: Enables or disables the display of diagonal and target lines along with their updates. Default is true. Turn it off for simpler chart views, or keep it on to aid in trade planning.

History Length: Determines the number of recent pivot samples used for median-based statistics, where more history leads to smoother but potentially less current estimates. Default is 50. Start with a minimum of 5 to build data; limit to 100 to 200 to prevent outdated regimes from skewing results.

Max Lookahead: Limits the number of bars projected forward to avoid overly extended lines. Default is 500. Reduce to 100 to 200 for intraday focus, or increase for longer swing horizons.

Stat Method: Selects the aggregation technique for time and price deltas: Median for robustness against outliers, Trimmed Mean (20%) for a balanced trim of extremes, or 75th Percentile for a conservative upward tilt. Default is Median. Use Median for even distributions; switch to Percentile when emphasizing potential upside in trending conditions.

Tolerance Type: Chooses the approach for flexible hit detection: None for exact matches, Percentage for relative adjustments, Absolute for fixed point offsets, or ATR for scaling with volatility. Default is None. Begin with Percentage at 0.5 percent for currency pairs, or ATR for adapting to cryptocurrency swings.

Tolerance %: Provides the relative buffer when using Percentage mode, forgiving small deviations. Default is 0.5. Set between 0.2 and 1.0 percent; higher values accommodate gaps but can overstate hit counts.

Tolerance Points: Establishes a fixed offset in price units for Absolute mode. Default is 0.0010. Tailor to the asset, such as 0.0001 for forex pairs, and validate against past wick behavior.

ATR Length: Specifies the period for the Average True Range in dynamic tolerance calculations. Default is 14. This is the standard setting; shorten to 10 to reflect more recent volatility.

ATR Multiplier: Adjusts the ATR scale for tolerance width in ATR mode. Default is 0.5. Range from 0.3 for tighter precision to 0.8 for greater leniency.

Dashboard Location: Positions the summary table on the chart. Default is Bottom Right. Consider Top Left for better visibility on mobile devices.

Dashboard Size: Controls the text scaling for dashboard readability. Default is Normal. Choose Tiny for dense overlays or Large for detailed review sessions.

Text/Frame Color: Sets the color scheme for dashboard text and borders. Default is gray. Align with your chart theme, opting for lighter shades on dark backgrounds.

Reading & Interpretation

Forecast lines appear as dashed diagonals from confirmed pivots to projected targets, with solid horizontals at endpoints marking price levels. Open targets show a target symbol (🎯); achieved ones switch to a trophy symbol (🏆) in gray, with lines fading to gray. The dashboard summarizes median time/price deltas, sample counts, and hit rates—rising rates indicate improving forecast alignment. Colors differentiate highs (red) from lows (lime); frozen states signal validated projections.

Practical Workflows & Combinations

- Trend following: Enter long on low forecast hits during uptrends (higher highs/lower lows structure); filter with EMA crossovers to ignore counter-trend signals.

- Reversal setups: Short above high projections in overextended rallies; use volume spikes as confirmation to reduce false breaks.

- Exits/Stops: Trail stops to prior pivot lows; conservative on low hit rates (below 50%), aggressive above 70% with tight tolerance.

- Multi-TF: Apply on 1H for entries, 4H for time projections; combine with Ichimoku clouds for confluence on targets.

- Risk management: Position size inversely to delta uncertainty (wider history = smaller bets); avoid low-liquidity sessions.

Behavior, Constraints & Performance

Confirmation occurs on OOB exit, so live-bar pivots may adjust until close, but projections update only on events to minimize repaint. No security or HTF calls, so no external lookahead issues. Arrays cap at history length with shifts; forecasts limited to five active, pruning FIFO. Loops iterate over small fixed sizes (e.g., up to 50 for stats), efficient on most hardware. Max lines/labels at 500 prevent overflow.

Known limits: Sensitive to OOB parameter tuning—too tight misses runs; assumes stationary pivot stats, which may shift in regime changes like low vol. Gaps or holidays distort time deltas.

Sensible Defaults & Quick Tuning

Defaults suit forex/crypto on 1H–4H: RSI 32/BB 20 for balanced detection, Median stats over 50 samples, None tolerance for exactness.

- Too many false runs: Increase BB StdDev to 2.5 or RSI Length to 50 for filtering.

- Lagging forecasts: Shorten History Length to 20; switch to 75th Percentile for forward bias.

- Missed near-hits: Enable Percentage tolerance at 0.3% to capture wicks without overcounting.

- Cluttered charts: Reduce Max Lookahead to 200; disable dashboard on lower TFs.

What this indicator is—and isn’t

This is a forecasting visualization layer for pivot-based analysis, highlighting statistical projections from historical patterns. It is not a standalone system—pair with price action, volume, and risk rules. Not predictive of all turns; focuses on OOB-derived extrema, ignoring volume or news impacts.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

[ZP] Fixed v6 testDISCLAIMER:

This indicator in Pine V6 as my first ever Tradingview indicator, has been developed for my personal trading analysis, consolidating various powerful indicators that I frequently use. A number of the embedded indicators within this tool are the creations of esteemed Pine Script developers from the TradingView community. In recognition of their contributions, the names of these developers will be prominently displayed alongside the respective indicator names. My selection of these indicators is rooted in my own experience and reflects those that have proven most effective for me. Please note that the past performance of any trading system or methodology is not necessarily indicative of future results. Always conduct your own research and due diligence before using any indicator or tool.

===========================================================================

Introducing the ultimate all-in-one DIY strategy builder indicator, With over 30+ famous indicators (some with custom configuration/settings) indicators included, you now have the power to mix and match to create your own custom strategy for shorter time or longer time frames depending on your trading style. Say goodbye to cluttered charts and manual/visual confirmation of multiple indicators and hello to endless possibilities with this indicator.

Available indicators that you can choose to build your strategy, are coded to seamlessly print the BUY and SELL signal upon confirmation of all selected indicators:

EMA Filter

2 EMA Cross

3 EMA Cross

Range Filter (Guikroth)

SuperTrend

Ichimoku Cloud

SuperIchi (LuxAlgo)

B-Xtrender (QuantTherapy)

Bull Bear Power Trend (Dreadblitz)

VWAP

BB Oscillator (Veryfid)

Trend Meter (Lij_MC)

Chandelier Exit (Everget)

CCI

Awesome Oscillator

DMI ( Adx )

Parabolic SAR

Waddah Attar Explosion (Shayankm)

Volatility Oscillator (Veryfid)

Damiani Volatility ( DV ) (RichardoSantos)

Stochastic

RSI

MACD

SSL Channel (ErwinBeckers)

Schaff Trend Cycle ( STC ) (LazyBear)

Chaikin Money Flow

Volume

Wolfpack Id (Darrellfischer1)

QQE Mod (Mihkhel00)

Hull Suite (Insilico)

Vortex Indicator

Trend Bars with Okuninushi Line Filter# Trend Bars with Okuninushi Line Filter: A Powerful Trading Indicator

## Introduction

The **Trend Bars with Okuninushi Line Filter** is an innovative technical indicator that combines two powerful concepts: trend bar analysis and the Okuninushi Line filter. This indicator helps traders identify high-quality trending moves by analyzing candle body strength relative to the overall price range while ensuring the price action aligns with the dominant market structure.

## What Are Trend Bars?

Trend bars are candles where the body (distance between open and close) represents a significant portion of the total price range (high to low). These bars indicate strong directional momentum with minimal indecision, making them valuable signals for trend continuation.

### Key Characteristics:

- **Strong directional movement**: Large body relative to total range

- **Minimal upper/lower shadows**: Shows sustained pressure in one direction

- **High conviction**: Represents decisive market action

## The Okuninushi Line Filter

The Okuninushi Line, also known as the Kijun Line in Ichimoku analysis, is calculated as the midpoint of the highest high and lowest low over a specified period (default: 52 periods).

**Formula**: `(Highest High + Lowest Low) / 2`

This line acts as a dynamic support/resistance level and trend filter, helping to:

- Identify the overall market bias

- Filter out counter-trend signals

- Provide confluence for trade entries

## How the Indicator Works

The indicator combines these two concepts with the following logic:

### Bull Trend Bars (Green)

A candle is colored **green** when ALL conditions are met:

1. **Bullish candle**: Close > Open

2. **Strong body**: |Close - Open| ≥ Threshold × (High - Low)

3. **Above trend filter**: Close > Okuninushi Line

### Bear Trend Bars (Red)

A candle is colored **red** when ALL conditions are met:

1. **Bearish candle**: Close < Open

2. **Strong body**: |Close - Open| ≥ Threshold × (High - Low)

3. **Below trend filter**: Close < Okuninushi Line

### Neutral Bars (Gray)

All other candles that don't meet the complete criteria are colored **gray**.

## Customizable Parameters

### Trend Bar Threshold

- **Range**: 10% to 100%

- **Default**: 75%

- **Purpose**: Controls how "strong" a candle must be to qualify as a trend bar

**Threshold Effects:**

- **Low (10-30%)**: More sensitive, catches smaller trending moves

- **Medium (50-75%)**: Balanced approach, filters out most noise

- **High (80-100%)**: Very selective, only captures the strongest moves

### Okuninushi Line Length

- **Default**: 52 periods

- **Purpose**: Determines the lookback period for calculating the midpoint

- **Common Settings**:

- 26 periods: More responsive to recent price action

- 52 periods: Standard setting, good balance

- 104 periods: Longer-term trend perspective

## Trading Applications

### 1. Trend Continuation Signals

- **Green bars**: Look for bullish continuation opportunities

- **Red bars**: Consider bearish continuation setups

- **Gray bars**: Exercise caution, mixed signals

### 2. Market Structure Analysis

- Clusters of same-colored bars indicate strong trends

- Alternating colors suggest choppy, indecisive markets

- Transition from red to green (or vice versa) may signal trend changes

### 3. Entry Timing

- Use colored bars as confirmation for existing trade setups

- Wait for color alignment with your market bias

- Avoid trading during predominantly gray periods

### 4. Risk Management

- Gray bars can serve as early warning signs of weakening trends

- Color changes might indicate appropriate exit points

- Use in conjunction with other risk management tools

## Advantages

1. **Dual Filtering**: Combines momentum (trend bars) with trend direction (Okuninushi Line)

2. **Visual Clarity**: Immediate visual feedback through candle coloring

3. **Customizable**: Adjustable parameters for different trading styles

4. **Versatile**: Works across multiple timeframes and instruments

5. **Objective**: Rule-based system reduces subjective interpretation

## Limitations

1. **Lagging Nature**: Based on historical price data

2. **False Signals**: Can produce whipsaws in choppy markets

3. **Parameter Sensitivity**: Requires optimization for different instruments

4. **Market Conditions**: May be less effective in ranging markets

## Best Practices

### Optimization Tips:

- **Volatile Markets**: Use higher thresholds (80-90%)

- **Steady Trends**: Use moderate thresholds (60-75%)

- **Short-term Trading**: Shorter Okuninushi Line periods (26)

- **Long-term Analysis**: Longer Okuninushi Line periods (104+)

### Combination Strategies:

- Pair with volume indicators for confirmation

- Use alongside support/resistance levels

- Combine with other trend-following indicators

- Consider market context and overall trend direction

## Conclusion

The Trend Bars with Okuninushi Line Filter offers traders a sophisticated yet intuitive way to identify high-quality trending moves. By combining the momentum characteristics of trend bars with the directional filter of the Okuninushi Line, this indicator helps traders focus on the most promising opportunities while avoiding low-probability setups.

Remember that no single indicator should be used in isolation. Always consider market context, risk management, and other technical factors when making trading decisions. The true power of this indicator lies in its ability to quickly highlight periods of strong, aligned price action – exactly what trend traders are looking for.

---

*Disclaimer: This article is for educational purposes only and should not be considered as financial advice. Always conduct your own research and consider your risk tolerance before making any trading decisions.*

Swing Guardrail — 30-sec Midterm Check (EBITDA Margin & EV/EBITDWhat it does

Before a short-term swing entry, this indicator right-sizes positions by a quick midterm (3–12m) durability screen using two fundamentals:

EBITDA Margin (TTM) → earning power / operational resilience

EV/EBITDA (TTM) → price tag vs earning capacity (payback feel)

A high-contrast table (top-right) shows both metrics and a verdict:

PASS — both meet thresholds → normal size

HALF — only one meets → reduce size

FAIL — neither meets → avoid

Why check “midterm” for a short-term trade?

Short swings still face earnings/news gaps, failed breakouts, and regime shifts. Names with weak margins or stretched valuation tend to break faster and deeper. A 30-sec durability check helps you:

Filter fragile setups (avoid expensive + weakening names)

Stabilize drawdowns (size down when quality/price don’t align)

Keep timing unchanged while improving risk-adjusted returns

Inputs (defaults)

Min EBITDA Margin % (TTM): 8%

Max EV/EBITDA (TTM): 12

Dark chart? High-contrast colors

How to use with a swing system

Get your entry from price/volume (e.g., Ichimoku cloud break, Kijun reclaim, Tenkan>Kijun; or your A/B/C rules).

Run this check only to set size (not timing).

Optional alerts: Once per bar close for PASS / HALF / FAIL.

Size mapping & event guard

PASS → 100% of your planned size

HALF → ~50% size / tighter stops

FAIL → watchlist only

If earnings < ~10 JP business days, drop one tier; ≤3 days → avoid.

Sector guides (tweak as needed)

Software/Internet: Margin ≥ 15%, EV/EBITDA ≤ 18

Industrials/Consumer: Margin ≥ 8%, EV/EBITDA ≤ 12

Retail: Margin ≥ 5–7%, EV/EBITDA ≤ 10–12

Edge cases / substitutions

Banks/Insurers/REITs or net-cash/negative EBITDA: EV/EBITDA may mislead → consider Net Debt/EBITDA or sector metrics (CET1/LTV/DSCR).

Sparse data / fresh listings: numbers may be NA until updates.

Notes & limitations

Data via request.financial() (TTM/most-recent). Some tickers/regions can show NA until fundamentals refresh.

This is a risk-screen / sizing tool, not a buy/sell signal.

Disclaimer

Educational use only. Not investment advice.

日本語

タイトル

スイング用ガードレール―中期“壊れにくさ”30秒チェック(EBITDAマージン & EV/EBITDA, TTM)

概要

短期スイングのエントリー前に、中期(3〜12か月)の耐久性を2指標で素早く確認し、ポジションサイズを決めるためのツールです。

EBITDAマージン(TTM):事業の稼ぐ力・体力

EV/EBITDA(TTM):その体力に対する“値札”(回収年数の感覚)

右上の高コントラスト表に数値と判定を表示:

PASS:両方クリア → 通常サイズ

HALF:片方のみ → サイズ半分

FAIL:両方NG → 見送り

なぜ短期でも“中期”を確認?

短期でも決算・ニュースのギャップ、ブレイク失敗、地合い転換は起きます。マージンが弱い/割高すぎる銘柄は崩れやすく、戻りも鈍い傾向。30秒の耐久性チェックで

脆いセットアップを回避

ドローダウンを平準化(サイズで吸収)

タイミングは変えずに、リスク調整後リターンの改善を狙えます。

入力(既定)

最低EBITDAマージン:8%

最大EV/EBITDA:12

黒背景向け:高コントラスト表示

使い方(スイング手法と併用)

まずは価格シグナル(一目の雲上抜け/基準線回復/転換線>基準線、またはA/B/Cルール)。

本インジの判定でサイズのみ決定(エントリーのタイミングは出しません)。

任意でバー確定アラート(PASS/HALF/FAIL)を設定。

サイズ目安 & イベント抑制

PASS:計画サイズ100%

HALF:約50%(ストップもタイトに)

FAIL:見送り

決算まで≦10営業日なら1段階サイズダウン、≦3営業日は原則見送り。

セクター目安(調整推奨)

ソフト/ネット:マージン 15%以上、EV/EBITDA 18以下

工業/一般消費:マージン 8%以上、EV/EBITDA 12以下

小売:マージン 5〜7%以上、EV/EBITDA 10〜12以下

例外・代替

銀行・保険・REIT/ネットキャッシュ・EBITDAマイナス:EV/EBITDAは適さない場合 → Net Debt/EBITDAやCET1/LTV/DSCR等で補助。

新規上場・データ薄:更新までNAのことあり。

注意

データは request.financial() を使用。更新前はNAの可能性。

本ツールはリスク確認/サイズ調整用で、売買シグナルではありません。

免責

情報提供のみ。投資判断は自己責任で。

Trend Continuation Filter - 🚀 Trend Continuation Filter — Multi-Factor Overlay

This overlay plots bullish / bearish continuation labels & arrows only when the market has enough confluence behind the move. Think of it as your “trend gatekeeper” — cutting out weak setups and highlighting only those with real momentum + structure.

🔍 Built-in Filters

✔ Ichimoku Cloud → trend bias + Tenkan/Kijun confirmation

✔ MACD (12/26/9) → acceleration via histogram slope

✔ RSI / MFI (14) → momentum quality (≥60 bullish / ≤40 bearish)

✔ ADX (14) → strength check (≥20 and rising)

➕ EMA Alignment (9/21/55/233) (optional)

➕ ATR Slope (14) (optional)

🎯 How it works

✅ Prints a Bull Continuation label/arrow when ≥4 filters align to the upside

✅ Prints a Bear Continuation label/arrow when ≥4 filters align to the downside

⚙️ minChecks input lets you adjust the strictness:

• Normal Days → set to 4 (more frequent, flexible)

• Trend Days → raise to 5–6 (fewer, high-conviction setups)

📈 Best Practices

⏰ Focus on London & New York sessions for clean expectancy

🧩 Pair with a HUD/Dashboard panel to see exactly which filters are active

T-Virus Sentiment [hapharmonic]🧬 T-Virus Sentiment: Visualize the Market's DNA

Remember the iconic T-Virus vial from the first Resident Evil? That powerful, swirling helix of potential has always fascinated me. It sparked an idea: what if we could visualize the market's underlying health in a similar way? What if we could capture the "genetic code" of market sentiment and contain it within a dynamic, 3D indicator? This project is the result of that idea, brought to life with Pine Script.

The indicator's main goal is to measure the strength and direction of market sentiment by analyzing the "genetic code" of price action through a variety of trusted indicators. The result is displayed as a liquid level within a DNA helix, a bubble density representing buying pressure, and a T-Virus mascot that reflects the overall mood.

🧐 Core Concept: How It Works

The primary output of the indicator is the "Active %" gauge you see on the right side of the vial. This percentage represents the overall sentiment score, calculated as an average from 7 different technical analysis tools. Each tool is analyzed on every bar and assigned a score from 1 (strong bearish pressure) to 5 (strong bullish potential).

In this indicator, we re-imagine market dynamics through the lens of a viral outbreak. A strong bear market is like a virus taking hold, pulling all technical signals down into a state of weakness. Conversely, a powerful bull market is like an antiviral serum ; positive signals rise and spread toward the top of the vial, indicating that the system is being injected with strength.

This is not just another line on a chart. It's a comprehensive sentiment dashboard designed to give an immediate, at-a-glance understanding of the confluence between 7 classic technical indicators. The incredible 3D model of the vial itself was inspired by a design concept found here .

⚛️ The 4 Core Elements of T-Virus Sentiment

These four elements work in harmony to give a complete, multi-faceted picture of market sentiment. Each component tells a different part of the story.

The Virus Mascot: An instant emotional cue. This character provides the quickest possible read on the overall market mood, combining sentiment with volume pressure.

The Antiviral Serum Level: The main quantitative output. This is the liquid level in the DNA helix and the percentage gauge on the right, representing the average sentiment score from all 7 indicators.

Buy Pressure & Bubble Density: This visualizes volume flow. The density of bubbles represents the intensity of accumulation (buying) versus distribution (selling). It's the "power" behind the move.

The Signal Distribution: This shows the confluence (or dispersion) of sentiment. Are all signals bullish and clustered at the top, or are they scattered, indicating a conflicted market? The position of the indicator labels is crucial, as each is assigned to one of five distinct zones:

Base Bottom: The market is at its weakest. Signals here suggest strong bearish control and distribution.

Lower Zone: The market is still bearish, but signals may be showing early signs of accumulation or bottoming.

Neutral Core (Center): A state of balance or sideways consolidation. The market is waiting for a new direction.

Upper Zone: Bullish momentum is becoming clear. Signals are strengthening and showing bullish control.

Top Cap: The market is "heating up" with strong bullish sentiment, potentially nearing overbought conditions.

🐂🐻 The Virus Mascot: The At-a-Glance Indicator

This character acts as a shortcut to confirm market health. It combines the sentiment score with volume, preventing false confidence in a low-volume rally.

Its state is determined by a dual-check: the overall "Antiviral Serum Level" and the "Buy Pressure" must both be above 50%.

Green & Smiling: The 'all clear' signal. This means that not only is the overall technical sentiment bullish, but it's also being supported by real buying pressure. This is a sign of a healthy bull market.

Red & Angry: A warning sign. This appears if either the sentiment is weak, or a bullish sentiment is not being confirmed by buying volume. The latter could indicate a potential "bull trap" or an exhaustive move.

This mascot can be disabled from the settings page under "Virus Mascot Styling" if a cleaner look is preferred.

🫧 Bubble Density: Gauging Buy vs. Sell Pressure

The bubbles visualize the battle between buyers and sellers. There are two modes to control how this is calculated:

Mode 1: Visible Range (The 'Big Picture' View)

This default mode is best for getting a broad, contextual understanding of the current session. It dynamically analyzes the volume of every single candlestick currently visible on the screen to calculate the buy/sell pressure ratio. It answers the question: "Over the entire period I'm looking at, who is in control?" As you zoom in or out, the calculation adapts.

Mode 2: Custom Lookback (The 'Precision' View)

This mode is for traders who need to analyze short-term pressure. You can define a fixed number of recent bars to analyze, which is perfect for scalping or understanding the volume dynamics leading into a key level. It answers the question: "What is happening right now ?" In the example above, a lookback of 2 focuses only on the most recent action, clearly showing intense, immediate selling pressure (few bubbles) and a corresponding drop in the sentiment score to 29%.

ℹ️ Interactive Tooltips: Dive Deeper

We believe in transparency, not 'black box' indicators. This feature transforms the indicator from a visual aid into an active learning tool.

Simply hover the mouse over any indicator label (like EMA, OBV, etc.) to get a detailed tooltip. It will explain the specific data points and thresholds that signal met to be placed in its current zone. This helps build trust in the signals and allows users to fine-tune the indicator settings to better match their own trading style.

🎯 The Scoring Logic Breakdown

The "Antiviral Serum Level" gauge is the average score from 7 technical analysis tools. Each is graded on a 5-point scale (1=Strong Bearish to 5=Strong Bullish). Here’s a detailed, transparent look at how each "gene" is evaluated:

Relative Strength Index (RSI)

Measures momentum and overbought/oversold conditions.

Group 1 (Strong Bearish): RSI > 80 (Extreme Overbought)

Group 2 (Bearish): 70 < RSI ≤ 80 (Overbought)

Group 3 (Neutral): 30 ≤ RSI ≤ 70

Group 4 (Bullish): 20 ≤ RSI < 30 (Oversold)

Group 5 (Strong Bullish): RSI < 20 (Extreme Oversold)

Exponential Moving Averages (EMA)

Evaluates the trend's strength and structure based on the alignment of multiple EMAs (9, 21, 50, 100, 200, 250).

Group 1 (Strong Bearish): A perfect bearish sequence (9 < 21 < 50 < ...)

Group 2 (Bearish Transition): Early signs of a potential reversal (e.g., 9 > 21 but still below 50)

Group 3 (Neutral / Mixed): MAs are intertwined or showing a partial bullish sequence.

Group 4 (Bullish): A strong bullish sequence is forming (e.g., 9 > 21 > 50 > 100)

Group 5 (Strong Bullish): A perfect bullish sequence (9 > 21 > 50 > 100 > 200 > 250)

Moving Average Convergence Divergence (MACD)

Analyzes the relationship between two moving averages to gauge momentum.

Group 1 (Strong Bearish): MACD & Histogram are negative and momentum is falling.

Group 2 (Weakening Bearish): MACD is negative but the histogram is rising or positive.

Group 3 (Neutral / Crossover): A crossover event is occurring near the zero line.

Group 4 (Bullish): MACD & Histogram are positive.

Group 5 (Strong Bullish): MACD & Histogram are positive, rising strongly, and accelerating.

Average Directional Index (ADX)

Measures trend strength, not direction. The score is based on both ADX value and the dominance of DI+ vs DI-.

Group 1 (Bearish / No Trend): ADX < 20 and DI- is dominant.

Group 2 (Developing Bearish Trend): 20 ≤ ADX < 25 and DI- is dominant.

Group 3 (Neutral / Indecision): Trend is weak or DI+ and DI- are nearly equal.

Group 4 (Developing Bullish Trend): 25 ≤ ADX ≤ 40 and DI+ is dominant.

Group 5 (Strong Bullish Trend): ADX > 40 and DI+ is dominant.

Ichimoku Cloud (IKH)

A comprehensive indicator that defines support/resistance, momentum, and trend direction.

Group 1 (Strong Bearish): Price is below the Kumo, Tenkan < Kijun, and Chikou is below price.

Group 2 (Bearish): Price is inside or below the Kumo, with mixed secondary signals.

Group 3 (Neutral / Ranging): Price is inside the Kumo, often with a Tenkan/Kijun cross.

Group 4 (Bullish): Price is above the Kumo with strong primary signals.

Group 5 (Strong Bullish): All signals are aligned bullishly: price above Kumo, bullish Tenkan/Kijun cross, bullish future Kumo, and Chikou above price.

Bollinger Bands (BB)

Measures volatility and relative price levels.

Group 1 (Strong Bearish): Price is below the lower band.

Group 2 (Bearish Territory): Price is between the lower band and the basis line.

Group 3 (Neutral): Price is hovering around the basis line.

Group 4 (Bullish Territory): Price is between the basis line and the upper band.

Group 5 (Strong Bullish): Price is above the upper band.

On-Balance Volume (OBV)

Uses volume flow to predict price changes. The score is based on OBV's trend and its position relative to its moving average.

Group 1 (Strong Bearish): OBV is below its MA and falling.

Group 2 (Weakening Bearish): OBV is below its MA but showing signs of rising.

Group 3 (Neutral): OBV is very close to its MA.

Group 4 (Bullish): OBV is above its MA and rising.

Group 5 (Strong Bullish): OBV is above its MA, rising strongly, and showing signs of a volume spike.

🧭 How to Use the T-Virus Sentiment Indicator

IMPORTANT: This indicator is a sentiment dashboard , not a direct buy/sell signal generator. Its strength lies in showing confluence and providing a quick, holistic view of the market's technical health.

Confirmation Tool: Use the "Active %" gauge to confirm a trade setup from your primary strategy. For example, if you see a bullish chart pattern, a high and rising sentiment score can add confidence to your trade.

Momentum & Trend Gauge: A consistently high score (e.g., > 75%) suggests strong, established bullish momentum. A consistently low score (< 25%) suggests strong bearish control. A score hovering around 50% often indicates a ranging or indecisive market.

Divergence & Warning System: Pay attention to divergences. If the price is making new highs but the sentiment score is failing to follow or is actively decreasing, it could be an early warning sign that the underlying momentum is weakening.

⚙️ Settings & Customization

The indicator is highly customizable to fit any trading style.

Position & Anchor: Control where the vial appears on the chart.

Styling (Vial, Helix, etc.): Nearly every visual element can be color-customized.

Signals: This is where the real power is. All underlying indicator parameters (RSI length, MACD settings, etc.) can be fine-tuned to match a personal strategy. The text labels can also be disabled if the chart feels cluttered.

Enjoy visualizing the market's DNA with the T-Virus Sentiment indicator

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25