LTP - Risk Ranges

This indicator shows volume and volatility adjusted risk ranges for the price.

Based on the previous volume in upside (downside) movements and the volatility of these upside (downside) movements a plausible range to the upside (downside) is calculated and drawn.

Cari dalam skrip untuk "range"

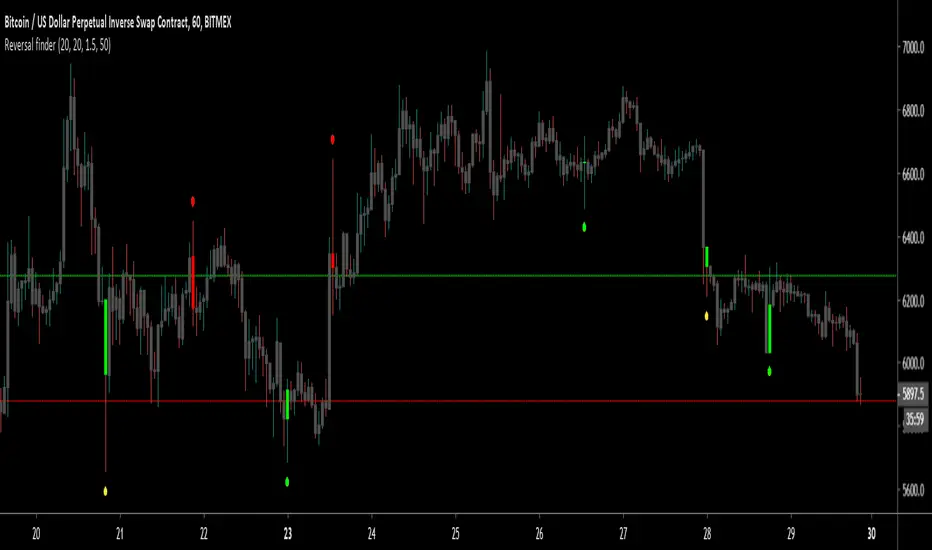

Reversal finderThis script is used to visually highlight candles which may signal a reversal following a false break of a support or resistance level.

Inputs are:

Lookback period: look for the highest high and the lowest low of the prior x bars.

SMA length: used for a simple moving average of the range (high minus low) of the prior x bars.

Range multiple: used to filter out signals for any bars with a range smaller than the average range of the preceding bars (determined by SMA length above) e.g. a range multiple of 2 will only show signals for bars with a range twice of that of the average range of the preceding bars.

Range threshold: used to filter signals for bars both the open and close of the bar are at the extreme end of the bar e.g. a threshold setting of 33% will only show buy signals for bars which open and close within the upper 1/3rd of the bar’s high/low range (vice versa for sell signals). This helps highlight, for example, bars with a high which exceeds resistance in a current range but which close back inside the range.

Highlight signal bars?: This will highlight bars with a buy signal in green, sell signal bars in red, and all other bars in grey. The script was designed for use with a dark background, so you will need to play around with the bar colours in the style settings to suit your preferences.

Settings used in the example chart are not the default – they are lookback: 5, SMA length: 20, range multiple: 1.2, range threshold: 33%.

Enjoy!

Volty Expan Close Strategy with Backtest Date RangeInput Information

Length Numeric 5 Number of bars used to determine the average true range.

NumATRs Numeric .75 Factor used to calculate a percentage of the average true range, used to

Long and short entry based on a percentage of price movement beyond the average range.

Profitable and simple strategy..

ADR - Average Daily Range [@treypeng] [v2]

This is an intraday indicator.

Average Daily Range provides an upper and lower level around the daily open. It is calculated by taking an EMA/SMA average of a given number of previous days' True Range.

It can be useful for helping guide support and resistance, for taking profits and for placing stops.

It's a similar idea to the ATR indicator, but calculated on a daily timeframe only.

Settings:

Length: number of days to take an average from

Offset: Set this to 0 to include today's range. Set to 1 to exclude today. Set to 2 to exclude today and yesterday.....and so on.

The other settings should be self explanatory :)

Securities day session - Opening-Range- Jayy Opening Range (OR) for regular daytime session eg NYSE 0 930hrs to 1600 hrs.

This is not for Forex sessions which is addressed in a separate script.

This script fixes two issues:

syntax error when code compiles

flaky plotting of the opening range and targets that required page reloading

Additions:

In this code there are more more opening range time period choices at the bottom of the format dialogue box

Opening Range Targets:

Opening Range Targets as per Leaf_West

Targets are set at 127% , 162%, 200 %, 262 %, 362%, 423%, 685%, 1109% and 1794% and this can be traded intraday using methods described at charts-by-leaf.com I also have some Leaf West PDFs that describe how the targets are set and how they are traded. There are others that use opening range.

See the notes in the script for more detail.

My first opening range script originated from work done by Chris Moody. This script has changed significantly but there are small remnants of Chris Moody's script lurking within.

This script is available to all.

Cheers Jayy

2% candlePart of my strategy involves entering a trade based on a candle on a 5-min chart being < 2% (ignoring major volatility).

I got tired of calculating the range of a single candle either in my head or on a calculator, so I wrote this up. Feel free to share it.

Shows the %move of any single candle, default horizontal lines are 1% & 2%, can be changed by clicking the gear icon next to the indicator after you have added the indicator to your chart. Works on any timeframe, 5m, 1h, 1d, etc , obviously

the higher the timeframe, the larger the move.

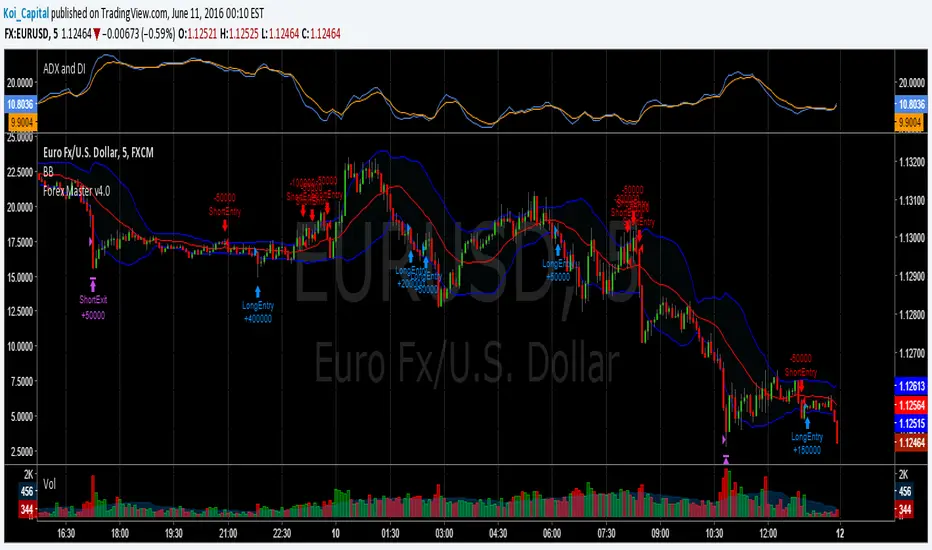

Forex Master v4.0 (EUR/USD Mean-Reversion Algorithm)DESCRIPTION

Forex Master v4.0 is a mean-reversion algorithm currently optimized for trading the EUR/USD pair on the 5M chart interval. All indicator inputs use the period's closing price and all trades are executed at the open of the period following the period where the trade signal was generated.

There are 3 main components that make up Forex Master v4.0:

I. Trend Filter

The algorithm uses a version of the ADX indicator as a trend filter to trade only in certain time periods where price is more likely to be range-bound (i.e., mean-reverting). This indicator is composed of a Fast ADX and a Slow ADX, both using the same look-back period of 50. However, the Fast ADX is smoothed with a 6-period EMA and the Slow ADX is smoothed with a 12-period EMA. When the Fast ADX is above the Slow ADX, the algorithm does not trade because this indicates that price is likelier to trend, which is bad for a mean-reversion system. Conversely, when the Fast ADX is below the Slow ADX, price is likelier to be ranging so this is the only time when the algorithm is allowed to trade.

II. Bollinger Bands

When allowed to trade by the Trend Filter, the algorithm uses the Bollinger Bands indicator to enter long and short positions. The Bolliger Bands indicator has a look-back period of 20 and a standard deviation of 1.5 for both upper and lower bands. When price crosses over the lower band, a Long Signal is generated and a long position is entered. When price crosses under the upper band, a Short Signal is generated and a short position is entered.

III. Money Management

Rule 1 - Each trade will use a limit order for a fixed quantity of 50,000 contracts (0.50 lot). The only exception is Rule

Rule 2 - Order pyramiding is enabled and up to 10 consecutive orders of the same signal can be executed (for example: 14 consecutive Long Signals are generated over 8 hours and the algorithm sends in 10 different buy orders at various prices for a total of 350,000 contracts).

Rule 3 - Every order will include a bracket with both TP and SL set at 50 pips (note: the algorithm only closes the current open position and does not enter the opposite trade once a TP or SL has been hit).

Rule 4 - When a new opposite trade signal is generated, the algorithm sends in a larger order to close the current open position as well as open a new one (for example: 14 consecutive Long Signals are generated over 8 hours and the algorithm sends in 10 different buy orders at various prices for a total of 350,000 contracts. A Short Signal is generated shortly after the 14th Long Signal. The algorithm then sends in a sell order for 400,000 contracts to close the 350,000 contracts long position and open a new short position of 50,000 contracts).

extended session - Regular Opening-Range- JayyOpening Range and some other scripts updated to plot correctly (see comments below.) There are three variations of the fibonacci expansion beyond the opening range and retracements within the opening range of the US Market session - I have not put in the script for the other markets yet.

The three scripts have different uses and strengths:

The extended session script (with the script here below) will plot the opening range whether you are using the extended session or the regular session. (that is to say whether "ext" in the lower right hand corner is highlighted or not.). While in the extended session the opening range has some plotting issues with periods like 13 minutes or any period that is not divisible into 330 mins with a round number outcome (eg 330/60 =5.5. Therefore an hour long opening range has problems in the extended session.

The pre session script is only for the premarket. You can select any opening range period you like. I have set the opening range to be the full premarket session. If you select a different session you will have to unselect "pre open to 9:30 EST for Opening Range?" in the format section. The script defaults to 15 minutes in the "period Of Pre Opening Range?". To go back to the 4 am to 9:30 pre opening range select "pre open to 9:30 EST for Opening Range?" there is no automatic 330 minute selection.

The past days offset script only works in 5 min or 15 minute period. It will show the opening range from up to 20 days past over the current days price action. Use this for the regular session only. 0 shows the current day's opening range. Use the positive integers for number of days back ie 1, 2, 3 etc not -1, -2, -3 etc. The script is preprogrammed to use the current day (0).

Scripts updated to plot correctly: One thing they all have in common is a way of they deal with a somewhat random problem that shifts the plots 4 hours in one direction or the other ie the plot started at 9:30 EST or 1:30PM EST. This issue started to occur approximately June 22, 2015 and impacts any script that tried to use "session" times to manage a plot in my scripts. The issue now seems to have been resolved during this past week.

Just in case the problem reoccurs I have added a "Switch session plot?" to each script. If the plot looks funny check or uncheck the "Switch session plot?" and see the difference. Of course if a new issue crops up it will likely require a different fix.

I have updated all of the scripts shown on this chart. If you are using a script of mine that suffers from the compiler issue then you will find an update on this chart. You can get any and all of the scripts by clicking on the small sideways wishbone on the left middle of the chart. You will see a dialogue box. Then click "make it mine". This will import all of the scripts to your computer and you can play around with them all to decide what you want and what you don't want. This is the easiest way to get all of the scripts in one fell swoop. It is also the easiest way for me to make all of the scripts available. I do not have all of the plots visible since it is too messy and one of the scripts (pre OR) is only for the regular session. To view the scripts click on the blue eye to the right of the script title to show it on this script. If you can only use the regular session. The scripts will all (with the exception of the pre OR) work fine.

If for any reason this script seems flakey refresh the page r try a slightly different period. I have noticed that sometimes randomly the script loves to return to the 5 min OR. This is a very new issue transient issue. As always if you see an issue please let me know.

Cheers Jayy

[RS]MTF CATR Stop Hunt Levels V0EXPERIMENTAL:

Adaptation from stop hunt levels:

Uses timeframe and atr to set ranges.

Opening Range Breakout with 2 Profit Targets.Opening Range Breakout with 2 Profit Targets.

Updated Indicator now works on all Symbols with Many Different Session Options.

***Known PineScript Issue…While the Opening Range is being Formed the lines only adjust for that individual bar. Just reset Indicator after Opening Range Completes.

***All Times are Based on New York Time

Session Options Forex U.S. Banks Open (8:00), Gold U.S. Open (8:20), Oil U.S. Open (9:00), U.S. Cash Session - Stocks (9:30), NY Forex Open (17:00) , Europe Open (02:00), or if you choose Setting 0 the Session Runs from 00:00 to 00:00 (Midnight to Midnight).

***Ability to use 60 minute Opening Range, 30 minute, 15 minute, and many other options.

***However you can manually change the times in the Inputs Tab to adjust for any session you prefer. This is useful for Day Light Savings Adjustments. Also the default times work if your charts are set to EST Time. If you use A different time zone in your settings you need to Adjust the times in the inputs tab.

Initially Opening Range High and Low plot as Yellow Lines. If Price Goes Above Opening Range then Line Turns Green. If Price Goes Below Opening Range Line Turns Red.

By default the First Profit Target is 1/2 the Width of the Opening Range and the 2nd Profit Target is 1 Times the Opening Range. However these are Adjustable in the Inputs Tab.

By Default the Opening Range Length is 1 Hour. However, you can Change the Opening Range Length to 15 min, 30 min, 2 hours etc. in the Inputs Tab.

Plots a 1 Above or Below Candle when 1st Profit Target is Achieved, and a 2 when 2nd Profit Target is Achieved.

Last Closed 4H Range + Fibs + Bias + CountdownLast Closed 4H Range + Fibs + Bias + Countdown

This indicator displays the most recent fully closed 4-hour (4H) candle range and projects it forward to provide a clear higher-timeframe framework for intraday trading.

🔹 Features

Last Closed 4H Range Box

Shows the high and low of the previous completed 4H candle (non-repainting).

Internal Fibonacci Levels

Automatically plots 25%, 50% (EQ), 75%, 61.8%, and 78.6% levels inside the 4H range.

4H Directional Bias

Bias is determined by the 4H close relative to the 50% equilibrium:

Above EQ → Bullish Bias

Below EQ → Bearish Bias

Bias Flip Alerts

Alerts trigger only when bias changes on a confirmed 4H candle close.

Live 4H Countdown Timer

Displays the remaining time until the current 4H candle closes, positioned below the range box.

SA Range Rank ALOG PRESSURE 1 AND 2This is a 4-candle market mechanic:

Bull pattern (orange)

Impulse up (strong bullish candle)

Stall / absorption (small candle; indecision)

Trap down (small bearish candle that fails to continue down)

Ignition up (bull candle breaks above the micro-range)

Bear pattern (yellow)

Impulse down

Stall / absorption

Trap up

Ignition down (bear candle breaks below micro-range)

Interpretation:

This is “pressure → absorption → reversal ignition.”

It’s meant to catch the moment where retail commits late and gets forced out.

How to Trade It on 15-Minute

15m is your structure execution timeframe: fewer signals, higher quality.

Recommended Indicator Settings (15m /NQ)

For CLEAN version (best baseline)

Sensitivity: BALANCED

Require VWAP bias: ON

Require EMA slope: ON

Targets: ON

Line extend bars: 40–60

For PRO (Looser) (more signals)

Keep defaults, then:

useVWAP: ON

useTrend: ON

useRetestHold: OFF (turn ON only if you want A+ only)

15m Entry Rules (Simple + Effective)

BULL (orange)

Enter on:

The close of the signal candle or

Next candle if it holds above the breakout area (safer)

BEAR (yellow)

Enter on:

The close of the signal candle or

Next candle if it holds below the breakdown area (safer)

15m Risk & Targets

STOP = the STOP line

PT1 = first scale / partial

PT2 = runner target

Suggested execution

Take 50–70% off at PT1

Move stop to breakeven after PT1 (optional)

Hold remainder to PT2 or trail

When to IGNORE a 15m signal

Skip it if:

Signal prints into a major level (prior day high/low, VWAP bands, overnight high/low)

You’re in the middle of chop and ATR is collapsing hard

The signal prints right before major news (CPI/FOMC)

How to Trade It on 1-Minute

1m is your execution / microstructure timeframe: more signals, faster decisions.

Recommended Indicator Settings (1m /NQ)

CLEAN version (to avoid spam)

Sensitivity: STRICT or BALANCED

VWAP: ON

EMA slope: ON

Targets: ON

PRO (Looser) (if you WANT frequent scalps)

Defaults are fine, but do:

useRetestHold: ON (recommended for 1m to avoid fake-outs)

Keep VWAP ON

1m Entry Rules (must be disciplined)

Best entry method (highest probability)

Wait for signal

Enter on the first retest/hold (if using retest hold)

If not using retest hold: enter only if next bar does not immediately reverse

1m Risk & Targets

PTs are ATR-based. On 1m, ATR is smaller, so targets are naturally tighter.

Use PT1 as a fast scalp, PT2 as stretch.

Suggested execution

Take 70–80% off at PT1

Very small runner to PT2

When to ignore 1m signals

Skip if:

It’s printing against the 15m direction

Price is whipping above/below VWAP repeatedly (chop)

ATR is extremely low (fake signals)

5) “Permission Layer” (15m → 1m workflow)

This is the cleanest way to combine both:

Step 1 (15m)

Use 15m signals as permission:

If 15m prints BULL, then you ONLY take 1m BULL signals for the next 30–90 minutes

If 15m prints BEAR, then you ONLY take 1m BEAR signals

Step 2 (1m)

Use 1m signals for entries and re-entries, with tighter targets.

This matches your framework:

15m = “structure gives permission”

1m = “execution extracts”

6) Ready-to-paste TradingView Descriptions

A) Description for SA 4-Candle Cycle — CLEAN (ATR Auto Targets)

Paste this into your TradingView script description:

SA 4-Candle Cycle (CLEAN) identifies a repeatable market mechanic: impulse → stall/absorption → trap → ignition.

Orange BULL signals print when a 4-candle bullish reversal/continuation cycle completes and price confirms by breaking above the micro-range. Yellow BEAR signals print on the inverse breakdown cycle.

This tool includes ATR-adaptive targets:

STOP = volatility-scaled invalidation level (optionally uses the swing reference candle)

PT1 / PT2 = first and second profit objectives scaled by ATR

Best use

15m: primary signal timeframe (higher quality, fewer signals). Enable VWAP and EMA slope filters for best results.

1m: execution timeframe for scalps and re-entries. Use STRICT/BALANCED sensitivity to reduce noise.

Risk note: This is not financial advice. Always manage risk and confirm with your larger structure levels.

B) Description for SA 4-Candle ATR-Adaptive Cycle — PRO (Looser) + Auto Targets

Paste this into your TradingView script description:

SA 4-Candle Cycle (PRO/Looser) is a higher-frequency variant of the 4-candle cycle model designed to print more signals while still respecting ATR-based structure. It detects impulse → absorption → trap → ignition sequences and plots ATR-scaled STOP, PT1, and PT2 levels automatically.

Best use

15m: use VWAP + EMA slope filters ON for higher probability.

1m: enable retest/hold if you want A+ entries only and fewer false breaks.

This version is ideal when you want earlier detection and more opportunities, while still keeping the risk framework systematic through ATR-adaptive targets.

Risk note: This is not financial advice. Use strict risk management.

Quick Recommendations (so you don’t get flooded)

If you want very high probability:

15m: CLEAN + BALANCED + VWAP ON + EMA slope ON

1m: PRO + VWAP ON + RetestHold ON + (optionally EMA slope ON)

Fibonacci Active Timeframe Range [UkutaLabs]█ OVERVIEW

Fibonacci Active Timeframe Range is a precision intraday structure tool that uses real-time price expansion combined with Fibonacci ratios to map dynamic support and resistance levels directly from the active timeframe.

Rather than relying on fixed historical averages, this indicator continuously builds a live range from current price action, projecting Fibonacci-derived levels that adapt to market conditions as they develop.

The goal is to give traders a clear structural framework for:

Intraday bias

Reaction zones

Volatility expansion

Pullback levels

Continuation targets

—all in a clean, visual format that integrates seamlessly into any strategy or system.

█ USAGE

The indicator calculates the current timeframe range in real time, anchoring from the active session’s open and projecting multiple Fibonacci levels within that range.

These levels act as dynamic support and resistance zones, updating as price evolves — allowing traders to:

Identify high-probability reaction areas

Define structure for entries and exits

Frame risk more precisely

Align trades with real-time volatility

Anticipate expansion and contraction phases

Each level is clearly labeled for instant recognition and can be used across scalping, intraday, and short-term swing strategies.

█ SETTINGS

Configuration

• Show Labels – Toggle labels on/off for a clean or informational view

• Display Mode – Control how much historical structure is visible

• Font Size – Adjust label size for readability

• Text Alignment – Align labels relative to each level

• Fibonacci Levels – Enable/disable specific ratios

• Range Mode – Select how the current timeframe range is calculated

Tokyo Sessions HighlighterOverview

This indicator provides a clean, visual representation of the Asian (Tokyo) trading session by highlighting its specific price range. It is designed to help traders identify the initial intraday range and key liquidity levels established during the Tokyo open.

Features

Dynamic Range Box: Automatically plots a box from the session's highest high to its lowest low.

Real-Time Updates: The box height and price labels update live as new session extremes are reached during the designated hours.

Professional Aesthetic: Features a minimalist gray fill, solid black borders, and black text for a clean, professional look on both light and dark chart themes.

Instant Data: Displays a label at the bottom of the box showing the exact price range in the format: Tokyo (Lowest Value - Highest Value).

How To Use

Settings: Adjust the Tokyo Session Time and Timezone in the indicator inputs to match your broker's server time or local requirements.

Strategy: Use the highlighted range to identify potential breakouts or to treat the session high and low as institutional liquidity zones for the London and New York sessions.

Customization: You can adjust the colors and transparency of the box through the script settings menu.

Open Range BreakoutOpen Range Breakout is a volatility harvesting tool designed to exploit directional expansion following major market opens. It isolates price action during initial liquidity injections to project institutional-grade zones that define a session's structural bias.

Core Methodology

The script uses a time-anchored engine to map critical supply and demand boundaries:

Anchor Identification: The algorithm captures the absolute High and Low within a user-defined window at the start of Tokyo, London, or New York sessions.

Structural Projection: It generates a Neutrality Box. A breach via candle close signals the transition from consolidation to expansion.

Mathematical Risk Modeling: Upon breakout, it calculates a 3:1 Risk-Reward framework based on fixed percentage volatility.

Session Dynamics

The system is optimized for the global liquidity cycle:

Session 1 (Asia): Maps early-day consolidation and range-bound liquidity.

Session 2 (Europe): Captures the London Move to identify the trend.

Session 3 (US): Analyzes high-volume New York opens for maximum momentum.

Key Features

Dynamic Price Mitigation: TP/SL zones stop extending the moment price touches the target or invalidation level to keep charts clean.

Volatility-Adjusted Levels: Stop Loss parameters are normalized to price percentage for consistency across Indices, Forex, or Crypto.

Minimalist Interface: Professional aesthetic with high-contrast visual cues for instant scannability.

Use Cases

Momentum Trading: Identifying the Origin of the Move post-open.

Mean Reversion: Recognizing failed breakouts when price returns inside the range.

Quantitative Backtesting: Benchmarking 3.0 RR targets across different session anchors.

HPDR Bands with projectionHPDR: Historical Price Delta Range

What is it? The HPDR indicator measures how much an asset’s price typically changes over a specific timeframe. It looks at historical price movements ("deltas") and organizes them into percentiles. These are then plotted on your chart as a median line surrounded by statistical bands.

This tool helps you understand an asset’s unique character and its typical price deviations.

Because the median is in this context a statistically relative stable value(if you add 7 values to 1000 it doesn't change much), it allows for high-probability projections of the future median.

For a clearer understanding of the indicator's logic, try setting the Range to 7 and the Offset to -7.

The 50% percentile Band signifies that in 50% of all bars, the price remained within this statistical range.

Session ATR Progression Tracker📊 Session ATR Progression Tracker - SIYL Regression Trading Tool

Track how much of your instrument's 7-day Average True Range (ATR) has been covered during the current trading session. This indicator is specifically designed for regression traders who follow the "Stay In Your Lane" (SIYL) methodology, helping you identify when the probability of mean reversion significantly increases. If you are interested in more on that check out Rod Casselli and tradersdevgroup.com.

🎯 Key Features:

• Real-time ATR Coverage Percentage - See at a glance what percentage of the 7-day ATR has been covered in the current session

• SIYL-Optimized Thresholds - See at a glance when the instrument has achieved 80% and 100% ATR coverage, the proven thresholds where mean reversion probability increases (customizable)

• Flexible Session Modes:

- Daily: Resets at calendar day change

- Session: Uses exchange-defined trading sessions

- Custom Session: Set your exact session start/end times (perfect for futures traders and international markets)

• Visual Alerts - Color-coded display (gray → orange → red) and optional background highlighting

• Repositionable Display - Choose from 9 screen positions to avoid chart clutter

• Session Markers - Green triangles mark the start of each new session

• Detailed Stats - View current range, ATR value, session high/low, and session status

💡 Why Use This Indicator?

This tool is built around a proven concept: regression trading becomes significantly more effective once a session has achieved at least 80% of its 7-day ATR. At this threshold, the probability of price reverting to mean increases substantially, creating higher-probability trade setups for SIYL practitioners.

Benefits for regression traders:

- Identify optimal entry points when mean reversion probability is highest (≥80% ATR coverage)

- Avoid premature regression entries before adequate range has been established

- Recognize when daily moves have "earned their range" and are ripe for reversal

- Time fade-the-move and counter-trend strategies with statistical backing

- Improve win rates by trading only after proven probability thresholds are met

⚙️ Setup Instructions:

1. Add the indicator to your chart

2. Select your preferred "Reset Mode" (recommend "Custom Session" for futures/international markets)

3. If using Custom Session, enter your session times in 24-hour format (e.g., 0930-1600 for US stocks, 1700-1600 for CME futures)

4. Adjust alert thresholds if desired (default: 80% and 100% - proven SIYL thresholds)

5. Position the display where it's most visible on your chart

📈 Works Across All Markets:

Stocks • Futures • Forex • Indices • Crypto • Commodities

Perfect for regression traders, mean reversion specialists, and SIYL practitioners who want to trade with probability on their side by entering only after the session has "earned its range."

---

Tip: For futures contracts with overnight sessions that span calendar days (like MES, MNQ, MYM), use "Custom Session" mode with your exchange's official session times for accurate tracking.

Day Range with OHLC LabelsThis indicator creates a synthetic daily candlestick that appears to the right of the chart, visually separated from real price bars.

It helps traders quickly view each day’s High, Low, Open, and Close without zooming, scrolling, or switching to higher timeframes.

What This Tool Does

✔ Draws a floating daily candle to the right of the current chart

✔ Displays the true Daily Open, High, Low, and Close

✔ Shows a center-aligned wick representing the full high-low range

✔ Shows a box-style candle body positioned using real OHLC values

✔ Labels the values (O, H, L, C) with large, clear fonts

✔ Automatically updates at each new day

✔ Works on any timeframe

✔ Helps intraday traders track daily structure visually

Why This Indicator Is Useful

This script is ideal for intraday traders who want instant awareness of the current day’s range.

Instead of guessing or drawing manual lines, you get a clean daily candlestick rendered off to the right side, avoiding chart clutter.

Great for:

Range traders

Breakout traders

Liquidity zone analysis

High/Low reference tracking

Traders who prefer non-intrusive visuals

Customization

Adjustable offset: position the candle further right

Configurable colors for wick + body

Large-font labels for easy reading

Automatically clears and redraws cleanly each day

Summary

This tool creates a clear, minimalistic, right-side daily candlestick complete with OHLC labels and centralized wick.

It’s designed to improve chart clarity and support quick decision-making without blocking price candles.

Daily Range Zones: PDH/PDL with SL/TPThis indicator automatically plots the previous day's High and Low levels and projects dynamic Stop Loss (SL) and Take Profit (TP) zones based on the daily range percentage.

It is designed for traders focusing on daily range breakouts or mean reversion strategies around the Previous Day High (PDH) and Previous Day Low (PDL).

Key Features:

Level 0 & 1: Visualizes the exact High and Low of the reference timeframe (Daily).

Inner Zone (Orange): Calculated inside the range. Acts as a buffer for Stop Loss placement or entry zones for mean reversion.

Outer Zone (Purple): Calculated outside the range (extension). Acts as a primary Take Profit target for breakout trades.

Settings:

Fully customizable percentages for inner and outer zones.

Option to toggle between current day or previous day data.

Works on any timeframe (intraday charts recommended).

Jace's Range DetectionAttempts to identify when an instrument is trading in a range. It uses Price Movement %, ATR and ADX. The following parameters are configurable: Range Detection Period, Range Threshold(%), ATR Period, ATR Range Multiplier.

Time Range HighlighterThis indicator highlights up to two custom time ranges on your chart with fully adjustable settings:

🔧 Features:

Define two separate time sessions

Set custom start and end times (in any time zone)

Choose unique highlight colors and opacity for each session

Toggle each range on or off independently

Timezone input allows syncing sessions to any global market hours (e.g., UTC, Asia/Tehran, New York)

🕒 Example Use Cases:

Highlight market opening hours (e.g. NYSE: 0930–1600)

Track your personal trading hours or peak volatility sessions

Visualize specific algorithm time filters

📌 Usage:

Enter your desired timezone string (e.g., "Asia/Tehran" or "Etc/UTC")

Customize session times like "0930-1200" and "1500-1700"

Adjust colors and visibility to fit your strategy

Ideal for traders who rely on time-based setups or session overlays.

ORB - Openning Range BreakoutORB - Opening Range Breakout (Indicator)

This indicator visualizes the Opening Range Breakout (ORB) for the New York market session (9:30 AM – 4:00 PM NY), highlighting the High and Low of the first 5 minutes of the session.

Key Features:

Automatically calculates the High and Low of the 9:30 AM candle and updates if subsequent candles expand the range within the first 5 minutes.

Plots invisible lines representing the High and Low of the opening range throughout the session.

Fills the area between High and Low with a semi-transparent background, clearly showing the opening range zone.

Works on any intraday timeframe and adapts automatically to the NY session.

Perfect for breakout strategies, visually marking early support and resistance zones.

How to Use:

The shaded area between High and Low indicates the opening range.

Traders can watch for breakouts above the High or breakdowns below the Low for potential entry signals.

Can be combined with trend or volume indicators for confirmation.

Notes:

The session is automatically calculated using New York time.

Background transparency can be adjusted to your preference.

Opening Range Gaps [TakingProphets]What is an Opening Range Gap (ORG)?

In ICT, the Opening Range Gap is defined as the price difference between the previous session’s close (e.g., 4:00 PM EST in U.S. indices) and the current day’s open (9:30 AM EST).

That gap is a liquidity void—an area where no trading occurred during regular hours.

Why ICT Traders Care About ORG

Liquidity Void (Gap Fill Logic)

-Because the gap is an untraded area, it naturally acts as a draw on liquidity.

-Price often seeks to rebalance by retracing into or fully filling this void.

Premium/Discount Sensitivity

-Once the ORG is defined, ICT treats it as a mini dealing range.

-Above EQ (Consequent Encroachment) = algorithmic premium (sell-sensitive).

-Below EQ = algorithmic discount (buy-sensitive).

-Price reaction at these levels gives a precise read on institutional intent intraday.

Support/Resistance from ORG

-If the session opens above prior close, the gap often acts as support until violated.

-If the session opens below prior close, the gap often acts as resistance until reclaimed.

Key ICT Concepts Anchored to ORG

Consequent Encroachment (CE): The midpoint of the gap. The algo is highly sensitive to CE as a decision point: reject → continuation; reclaim → reversal.

Draw on Liquidity (DoL): Price is algorithmically “pulled” toward gap fills, CE, or the opposite side of the ORG.

Order Flow Confirmation: If price ignores the gap and runs away from it, this signals strong institutional order flow in that direction.

Confluence with Other Tools: FVGs, OBs, and HTF PD arrays often overlap with ORG levels, strengthening setups.

Practical Application for Traders

Bias Formation:

Use ORG EQ as a line in the sand for intraday bias.

If price trades below ORG EQ after the open → look for short setups into the prior day’s low or external liquidity.

If price trades above ORG EQ → favor longs into highs/liquidity pools.

Execution Framework:

Wait for liquidity raids or market structure shifts at ORG edges (.00, .25, .50, .75).

Target: EQ, opposite quarter, or full gap fill.

Precision Reads:

ORG lines let traders anticipate where algorithms are likely to respond, providing mechanical invalidation and clear targets without clutter.