Axel AltsOverview

Axel Alts is a higher-timeframe-aware overlay that forms a two-line support band for altcoins using a sticky, threshold-and-step progression. It draws an Upper Support (mid) and a Lower Support (low) derived from evolving local lows, with smoothed transitions and an optional halving-cycle bear-window background.

The goal is disciplined context: identify controlled pullbacks into support in constructive regimes and avoid emotional chasing. All core settings are fixed for consistent behavior across symbols.

Core logic (concepts, not implementation)

• Two baseline levels are computed as fractional distances from the current base and then smoothed.

• A sticky mechanism advances each line toward its target only when deviation is material, and in capped steps. This reduces whipsaw and preserves structure.

• Visual easing smooths transitions so curves remain stable and readable.

• Rendering accounts for higher-timeframe structure and uses interpolation on lower timeframes for visual continuity; values do not look ahead and finalize on higher-timeframe closes.

• An optional bear-window background is derived from halving dates to flag a more cautious phase between the late part of one cycle and the run-up to the next.

Inputs

• Parameters are locked (lengths, fractions, sticky thresholds/steps, easing radii, bear-window bounds). No user-tweakable inputs—this prevents overfitting and improves repeatability.

How to read it

• The zone between Upper Support and Lower Support is the preferred “controlled pullback” area in constructive regimes.

• Persistent closes above Upper Support indicate strength; orderly reactions into the band can be constructive.

• Sustained closes below Lower Support warn of deterioration; be cautious with aggressive longs until recovery.

• The bear-window background suggests a more conservative stance on risk and size.

• Confirmations are best taken on daily/weekly closes; short-term pokes through the band are often noise.

Practical use cases

• Altcoin rotation: prioritize names holding the band; de-prioritize those persisting below it.

• Dollar-Cost Averaging (DCA) context: scale within the band during favorable regimes.

• Risk framing: tighten or reduce exposure on breaks below Lower Support or during the bear window.

• Confluence: combine with volume/volatility tools and market-wide risk gauges.

Best practices

• Rely on daily/weekly closes for confirmation.

• Pair with market structure (HH/HL vs. LH/LL) and higher-timeframe support/resistance.

• Consider broader cycle context (e.g., halving windows) before scaling risk.

Technical notes

• Non-repainting: values finalize on the close of the higher timeframe used by each calculation.

• Interpolation on lower timeframes is for continuity only; it is not forward-looking.

• Bear-window boundaries are fixed and derived from publicly known Bitcoin halving dates.

• The fill between lines is fixed in the current configuration.

Who it is for

• Traders who want a fixed-rules, repeatable context for alt pullbacks and trend health.

• Systematic users who prefer deterministic, non-tunable overlays for portfolio discipline.

Limitations & disclosures

• Closed-source; for educational and analytical use only.

• Not financial advice. Markets involve risk; past performance does not guarantee future results.

Release notes

• Includes sticky progression for both support lines with eased transitions.

• Improved visual continuity on lower timeframes while respecting higher-timeframe structure.

• Added halving-based bear-window highlighting (bounds are fixed).

Originality & why closed-source

This is not a reimplementation of public open-source scripts. Axel Alts integrates (1) sticky threshold-and-step progression, (2) dual support lines built from fractional levels off evolving lows with separate smoothing, (3) visual easing for stability, and (4) a halving-based bear window. The interaction of thresholds/steps, smoothing, and the regime window is proprietary and tuned to retain structure while limiting lag. The source is closed to protect this implementation.

Integration, not a mashup

Axel Alts is a single, self-contained framework. It does not merely merge indicators; its components are designed to work together to form a unified support band with a clear reading protocol (hold within the band, caution below, close-based confirmations, optional bear-window context).

Indicator, not a strategy

This publication is an indicator overlay, not a trading strategy. It includes no backtests, position logic, performance claims, or risk assumptions. Use it as analytical context within your own risk management.

Comparison to common tools

Compared to standard moving-average channels or volatility bands, Axel Alts emphasizes (1) structure retention via sticky thresholds/steps, (2) smoother visuals through eased transitions, and (3) explicit cycle context via the halving-based bear window.

Smoothing

Icy-Hot Visual Indicator [SciQua]🧊 Icy-Hot Visual Indicator

This indicator colors your price bars and/or chart background based on a normalized & smoothed transform of any price-based input (default: close). It gives you a quick “temperature map” of market momentum or volatility—cool blues for low readings, hot reds for high readings—without cluttering your chart.

🔍 Key Features

1. Dual Visual Layers

Candle Gradient: Applies a smooth, multi-color gradient to candle bodies and wicks based on normalized, smoothed input data

Background Gradient: Adds a semi-transparent gradient behind the candles to highlight broader trend zones or volatility regimes

2. Advanced Customization

Normalization Types: bounded, unbounded, z-score, MAD, percentile, sigmoid, tanh, rank, robust, and more

Smoothing Methods: EMA, SMA, WMA, RMA, HMA, TEMA, VWMA, Gaussian, LinReg, ExpReg, and others (12+ options)

3. Gradient Control: Choose 2–7 color stops, reverse direction, adjust display length

Flexible Source Inputs

Use any built-in price series (close, hl2, volume, etc.)

Feed outputs from external indicators (RSI, custom oscillators, moving averages) into either layer

❓How It Works

Inputs are normalized (z-score, bounded, etc.) then smoothed (EMA, LinReg, etc.) in the order you choose. The result is clamped to 0–1 and passed through a multi-stop gradient engine for precise color mapping.

✨ What Makes It Original

While many indicators apply colors or smoothing, this script combines multi-stage normalization, adaptive smoothing, and a modular gradient rendering engine in a highly customizable dual-layer system. It’s built using proprietary functions from the SciQua suite that are not available in public libraries and allow for advanced visual encoding without relying on alerts, signals, or extra panes.

This makes it original in both design and execution—offering a visual-first approach with unique depth, clarity, and flexibility.

🔐 Why This Script Is Closed-Source

While the underlying functions are published in the open-source SciQua library, this indicator’s specific implementation, configuration architecture, and visual behavior are proprietary. It combines multiple library utilities into a dual-layer adaptive system that handles advanced gradient rendering, multi-stage normalization, and smoothing pipelines in a unique way.

The source is closed to protect the design logic, interface abstraction, and fine-tuned behaviors that make this indicator commercially valuable. The building blocks are open to the Pine community, but this assembled product is not meant for replication or redistribution.

How to Use It

1. Highlight Trend Strength

Source: RSI percentile

Setup: 200-bar look-back, mild smoothing

Result: Warm tones when momentum is peaking; cool when it’s fading. Use as a quick filter for entries in the direction of the trend.

2. Visualize Volatility Regimes

Source: ATR or True Range

Setup: Bounded normalization with tighter smoothing bar color off, bg color on.

Result: Background bands that shade when volatility spikes. Helps you avoid low-volatility breakouts or throttle position sizing in choppy markets.

3. Combine with Other Indicators

Source: Output of your custom indicator (e.g., a Keltner Band width)

Setup: Match normalization period to your strategy’s timeframe

Result: Bars colored by your own logic—no extra panes, just enhanced candles.

4. Background Only Heatmap

Turn off bar coloring and dial in semi-transparent background shades—keeps candles crisp while still giving you a context heat-map behind price.

Dynamic Laguerre Filter Bands | OttoThis indicator combines trend-following and volatility analysis by enhancing the traditional Laguerre filter with a dynamic, volatility-adjusted band system. Instead of using fixed thresholds, the bands adapt in real-time to changing market conditions by applying smoothed standard deviation calculations. This design keeps the indicator responsive to significant price movements while effectively filtering out short-term market noise, resulting in more accurate trend identification and breakout signals.

Core Concept

The indicator is built around the following key components:

Laguerre Filter:

The Laguerre filter is designed to smooth out price data by reducing market noise while still being quick enough to detect real changes in price direction. Its goal is to create a clear, smooth trend line that helps traders/investors focus on the overall market trend without getting distracted by small, random price swings.

It uses a parameter called gamma to control how it balances smoothness and responsiveness:

A lower gamma gives more weight to recent price data, making the filter react faster to new price changes. This means the trend line is more sensitive but may also be less smooth and more prone to small fluctuations.

A higher gamma gives more weight to past price data, making the filter smoother and less sensitive to quick changes. This helps reduce noise and produces a steadier trend line, but it also introduces more lag, meaning the filter reacts slower to new price moves.

By adjusting gamma, the Laguerre filter lets you choose the balance between following price changes quickly and having a stable, noise-free trend signal.

Standard Deviation:

shows how much price varies from the mean. In this indicator, it’s used to measure market volatility.

Volatility Bands: The upper and lower bands are based on an EMA-smoothed standard deviation of price. The EMA reduces sudden jumps in volatility, creating smoother and more stable bands that still respond to changing market conditions. These bands are plotted around the Laguerre filter line, expanding and contracting in a controlled way to stay aligned with real market movement while avoiding short-term noise.

Signal Logic:

A long signal is triggered when the close price crosses above the upper band.

A short signal occurs when the close price falls below the lower band.

⚙️ Inputs

Source: Price source used in calculations

Gamma: Adjusts how much the Laguerre filter responds to price changes. Lower gamma values make the filter react more to recent prices, while higher values give more influence to older data, making the line smoother but slower to respond.

Volatility Length: Period used to calculate standard deviation

Volatility Smoothing Length: EMA smoothing length for standard deviation

Multiplier: Scales the width of the bands based on volatility

📈 Visual Output

Laguerre Filter Line: Plots the laguerre filter line, colored dynamically based on signal direction (green for bullish, purple for bearish)

Upper & Lower Bands: Volatility-based bands that adjust with market conditions. (green for bullish, purple for bearish)

Glow Effect: Optional glow layer to enhance visibility of the laguerre filter trend line (green for bullish, purple for bearish)

Bar Coloring: Candlesticks and bar colors reflect the active signal state for fast visual interpretation (green for bullish, purple for bearish)

How to Use

Apply the indicator to your chart and monitor for signal events:

Long Signal: When price closes above the upper band

Short Signal: When price closes below the lower band

🔔 Alerts

This indicator supports optional alert conditions you can enable for:

Long Signal: Close price crossing above the upper band

Short Signal: Close price crossing below the lower band

⚠️ Disclaimer:

This indicator is intended for educational and informational purposes only. Trading/investing involves risk, and past performance does not guarantee future results. Always test and evaluate indicators/strategies before applying them in live markets. Use at your own risk.

FVG Trailing Stop [LuxAlgo]The FVG Trailing Stop indicator tracks unmitigated Fair Value Gaps (FVG) data to produce a Trailing Stop indicator able to determine if the market is uptrending or downtrending easily.

🔶 USAGE

The FVG Trailing Stop is intended to identify trend directions through its position relative to the closing price:

Bullish: Price is located above the Trailing Stop, indicating that all Bearish FVGs have been mitigated and the trend is anticipated to continue upwards.

Bearish State: Price is located below the Trailing Stop, indicating that all Bullish FVGs have been mitigated and the trend is anticipated to continue downwards.

The Trailing Stop originates from two extremities obtained from the average of respective unmitigated FVGs. The specific directional average is also displayed as a more transparent secondary line, however, the trailing stop is derived from this value and a new trend will not be detected until the opposite directional average is crossed.

Price reaching the Trailing Stop is caused by retracements and can lead to the following scenarios:

Outcome 1: The directional average is crossed next, indicating a new trend direction.

Outcome 2: The directional average is held as support or resistance, leading to a new impulse and a continuation of the trend.

🔹 Reset on Cross

While price crossing the Trailing Stop should be considered as a sign of an upcoming trend change; it is possible for the price to still evolve outside it.

As a solution, we have included the "Reset on Cross" feature, which (as the name suggests) hides and resets the Trailing Stop each time it is crossed, leading to a "Neutral" state.

This opens the opportunity for the Trailing Stop to be displayed again once the price moves again in the direction of the pre-established trend. A trader might use this to accumulate positions within a specific trend.

🔶 DETAILS

The script uses a typical identification method for FVGs. Once identified, the script collects the point of the FVG farthest from the current price when formed.

For Upwards FVGs this is the bottom of the FVG.

For Downwards FVGs this is the top of the FVG.

The data is managed only to use the last input lookback of FVGs. If an FVG is mitigated, it frees up a spot in the memory for a new FVG, however, if the lookback is full, the oldest will be deleted.

From there, it uses a "trailing" logic only to move the Trailing Stop in one direction until the trailing stop resets or the direction flips.

The extremities used to calculate the Trailing Stop are created from 2 calculation steps, the first step involves taking the raw average of the FVG mitigation levels, and the second step applies a simple moving average (SMA) smoothing of the precedent-obtained averages.

🔶 SETTINGS

Unmitigated FVG Lookback: Sets the maximum number of Unmitigated FVGs that the script will use.

Smoothing Length: Sets the smoothing length for the Trailing Stop to reduce erratic results.

Reset on Cross: When enabled, hide and reset the Trailing Stop until the price starts moving in the pre-established trend direction again.

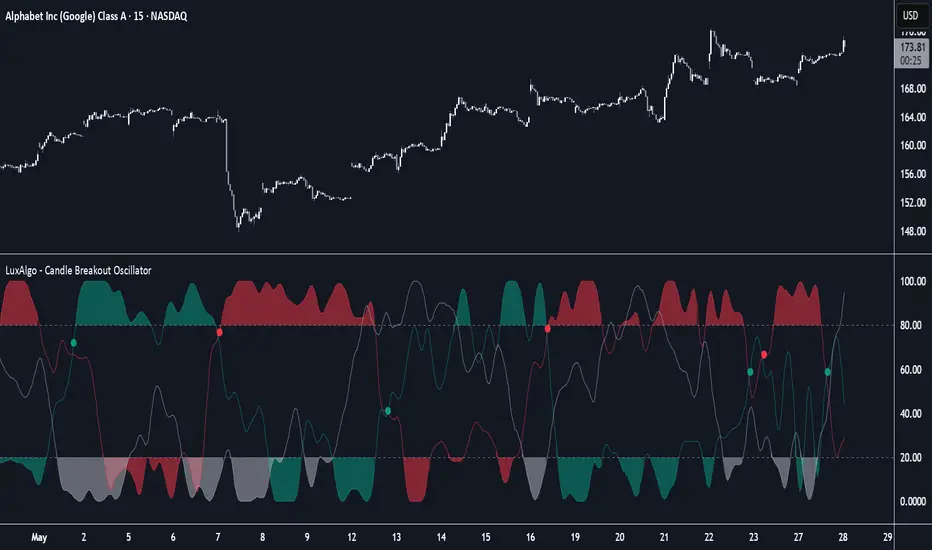

Candle Breakout Oscillator [LuxAlgo]The Candle Breakout Oscillator tool allows traders to identify the strength and weakness of the three main market states: bullish, bearish, and choppy.

Know who controls the market at any given moment with an oscillator display with values ranging from 0 to 100 for the three main plots and upper and lower thresholds of 80 and 20 by default.

🔶 USAGE

The Candle Breakout Oscillator represents the three main market states, with values ranging from 0 to 100. By default, the upper and lower thresholds are set at 80 and 20, and when a value exceeds these thresholds, a colored area is displayed for the trader's convenience.

This tool is based on pure price action breakouts. In this context, we understand a breakout as a close above the last candle's high or low, which is representative of market strength. All other close positions in relation to the last candle's limits are considered weakness.

So, when the bullish plot (in green) is at the top of the oscillator (values above 80), it means that the bullish breakouts (close below the last candle low) are at their maximum value over the calculation window, indicating an uptrend. The same interpretation can be made for the bearish plot (in red), indicating a downtrend when high.

On the other hand, weakness is indicated when values are below the lower threshold (20), indicating that breakouts are at their minimum over the last 100 candles. Below are some examples of the possible main interpretations:

There are three main things to look for in this oscillator:

Value reaches extreme

Value leaves extreme

Bullish/Bearish crossovers

As we can see on the chart, before the first crossover happens the bears come out of strength (top) and the bulls come out of weakness (bottom), then after the crossover the bulls reach strength (top) and the bears weakness (bottom), this process is repeated in reverse for the second crossover.

The other main feature of the oscillator is its ability to identify periods of sideways trends when the sideways values have upper readings above 80, and trending behavior when the sideways values have lower readings below 20. As we just saw in the case of bullish vs. bearish, sideways values signal a change in behavior when reaching or leaving the extremes of the oscillator.

🔶 DETAILS

🔹 Data Smoothing

The tool offers up to 10 different smoothing methods. In the chart above, we can see the raw data (smoothing: None) and the RMA, TEMA, or Hull moving averages.

🔹 Data Weighting

Users can add different weighting methods to the data. As we can see in the image above, users can choose between None, Volume, or Price (as in Price Delta for each breakout).

🔶 SETTINGS

Window: Execution window, 100 candles by default

🔹 Data

Smoothing Method: Choose between none or ten moving averages

Smoothing Length: Length for the moving average

Weighting Method: Choose between None, Volume, or Price

🔹 Thresholds

Top: 80 by default

Bottom: 20 by default

Half Causal EstimatorOverview

The Half Causal Estimator is a specialized filtering method that provides responsive averages of market variables (volume, true range, or price change) with significantly reduced time delay compared to traditional moving averages. It employs a hybrid approach that leverages both historical data and time-of-day patterns to create a timely representation of market activity while maintaining smooth output.

Core Concept

Traditional moving averages suffer from time lag, which can delay signals and reduce their effectiveness for real-time decision making. The Half Causal Estimator addresses this limitation by using a non-causal filtering method that incorporates recent historical data (the causal component) alongside expected future behavior based on time-of-day patterns (the non-causal component).

This dual approach allows the filter to respond more quickly to changing market conditions while maintaining smoothness. The name "Half Causal" refers to this hybrid methodology—half of the data window comes from actual historical observations, while the other half is derived from time-of-day patterns observed over multiple days. By incorporating these "future" values from past patterns, the estimator can reduce the inherent lag present in traditional moving averages.

How It Works

The indicator operates through several coordinated steps. First, it stores and organizes market data by specific times of day (minutes/hours). Then it builds a profile of typical behavior for each time period. For calculations, it creates a filtering window where half consists of recent actual data and half consists of expected future values based on historical time-of-day patterns. Finally, it applies a kernel-based smoothing function to weight the values in this composite window.

This approach is particularly effective because market variables like volume, true range, and price changes tend to follow recognizable intraday patterns (they are positive values without DC components). By leveraging these patterns, the indicator doesn't try to predict future values in the traditional sense, but rather incorporates the average historical behavior at those future times into the current estimate.

The benefit of using this "average future data" approach is that it counteracts the lag inherent in traditional moving averages. In a standard moving average, recent price action is underweighted because older data points hold equal influence. By incorporating time-of-day averages for future periods, the Half Causal Estimator essentially shifts the center of the filter window closer to the current bar, resulting in more timely outputs while maintaining smoothing benefits.

Understanding Kernel Smoothing

At the heart of the Half Causal Estimator is kernel smoothing, a statistical technique that creates weighted averages where points closer to the center receive higher weights. This approach offers several advantages over simple moving averages. Unlike simple moving averages that weight all points equally, kernel smoothing applies a mathematically defined weight distribution. The weighting function helps minimize the impact of outliers and random fluctuations. Additionally, by adjusting the kernel width parameter, users can fine-tune the balance between responsiveness and smoothness.

The indicator supports three kernel types. The Gaussian kernel uses a bell-shaped distribution that weights central points heavily while still considering distant points. The Epanechnikov kernel employs a parabolic function that provides efficient noise reduction with a finite support range. The Triangular kernel applies a linear weighting that decreases uniformly from center to edges. These kernel functions provide the mathematical foundation for how the filter processes the combined window of past and "future" data points.

Applicable Data Sources

The indicator can be applied to three different data sources: volume (the trading volume of the security), true range (expressed as a percentage, measuring volatility), and change (the absolute percentage change from one closing price to the next).

Each of these variables shares the characteristic of being consistently positive and exhibiting cyclical intraday patterns, making them ideal candidates for this filtering approach.

Practical Applications

The Half Causal Estimator excels in scenarios where timely information is crucial. It helps in identifying volume climaxes or diminishing volume trends earlier than conventional indicators. It can detect changes in volatility patterns with reduced lag. The indicator is also useful for recognizing shifts in price momentum before they become obvious in price action, and providing smoother data for algorithmic trading systems that require reduced noise without sacrificing timeliness.

When volatility or volume spikes occur, conventional moving averages typically lag behind, potentially causing missed opportunities or delayed responses. The Half Causal Estimator produces signals that align more closely with actual market turns.

Technical Implementation

The implementation of the Half Causal Estimator involves several technical components working together. Data collection and organization is the first step—the indicator maintains a data structure that organizes market data by specific times of day. This creates a historical record of how volume, true range, or price change typically behaves at each minute/hour of the trading day.

For each calculation, the indicator constructs a composite window consisting of recent actual data points from the current session (the causal half) and historical averages for upcoming time periods from previous sessions (the non-causal half). The selected kernel function is then applied to this composite window, creating a weighted average where points closer to the center receive higher weights according to the mathematical properties of the chosen kernel. Finally, the kernel weights are normalized to ensure the output maintains proper scaling regardless of the kernel type or width parameter.

This framework enables the indicator to leverage the predictable time-of-day components in market data without trying to predict specific future values. Instead, it uses average historical patterns to reduce lag while maintaining the statistical benefits of smoothing techniques.

Configuration Options

The indicator provides several customization options. The data period setting determines the number of days of observations to store (0 uses all available data). Filter length controls the number of historical data points for the filter (total window size is length × 2 - 1). Filter width adjusts the width of the kernel function. Users can also select between Gaussian, Epanechnikov, and Triangular kernel functions, and customize visual settings such as colors and line width.

These parameters allow for fine-tuning the balance between responsiveness and smoothness based on individual trading preferences and the specific characteristics of the traded instrument.

Limitations

The indicator requires minute-based intraday timeframes, securities with volume data (when using volume as the source), and sufficient historical data to establish time-of-day patterns.

Conclusion

The Half Causal Estimator represents an innovative approach to technical analysis that addresses one of the fundamental limitations of traditional indicators: time lag. By incorporating time-of-day patterns into its calculations, it provides a more timely representation of market variables while maintaining the noise-reduction benefits of smoothing. This makes it a valuable tool for traders who need to make decisions based on real-time information about volume, volatility, or price changes.

[GYTS] FiltersToolkit LibraryFiltersToolkit Library

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- 1. INTRODUCTION --------- 🌸

💮 What Does This Library Contain?

This library is a curated collection of high-performance digital signal processing (DSP) filters and auxiliary functions designed specifically for financial time series analysis. It includes a shortlist of our favourite and best performing filters — each rigorously tested and selected for their responsiveness, minimal lag and robustness in diverse market conditions. These tools form an integral part of the GoemonYae Trading System (GYTS), chosen for their unique characteristics in handling market data.

The library contains two main categories:

1. Smoothing filters (low-pass filters and moving averages) for e.g. denoising, trend following

2. Detrending tools (high-pass and band-pass filters, known as "oscillators") for e.g. mean reversion

This collection is finely tuned for practical trading applications and is therefore not meant to be exhaustive. However, will continue to expand as we discover and validate new filtering techniques. I welcome collaboration and suggestions for novel approaches.

🌸 ——— 2. ADDED VALUE ——— 🌸

💮 Unified syntax and comprehensive documentation

The FiltersToolkit Library brings together a wide array of valuable filters under a unified, intuitive syntax. Each function is thoroughly documented, with clear explanations and academic sources that underline the mathematical rigour behind the methods. This level of documentation not only facilitates integration into trading strategies but also helps underlying the underlying concepts and rationale.

💮 Optimised performance and readability

The code prioritizes computational efficiency while maintaining readability. Key optimizations include:

- Minimizing redundant calculations in recursive filters

- Smart coefficient caching

- Efficient state management

- Vectorized operations where applicable

💮 Enhanced functionality and flexibility

Some filters in this library introduce extended functionality beyond the original publications. For instance, the MESA Adaptive Moving Average (MAMA) and Ehlers’ Combined Bandpass Filter incorporate multiple variations found in the literature, thereby providing traders with flexible tools that can be fine-tuned to different market conditions.

🌸 ——— 3. THE FILTERS ——— 🌸

💮 Hilbert Transform Function

This function implements the Hilbert Transform as utilised by John Ehlers. It converts a real-valued time series into its analytic signal, enabling the extraction of instantaneous phase and frequency information—an essential step in adaptive filtering.

Source: John Ehlers - "Rocket Science for Traders" (2001), "TASC 2001 V. 19:9", "Cybernetic Analysis for Stocks and Futures" (2004)

💮 Homodyne Discriminator

By leveraging the Hilbert Transform, this function computes the dominant cycle period through a Homodyne Discriminator. It extracts the in-phase and quadrature components of the signal, facilitating a robust estimation of the underlying cycle characteristics.

Source: John Ehlers - "Rocket Science for Traders" (2001), "TASC 2001 V. 19:9", "Cybernetic Analysis for Stocks and Futures" (2004)

💮 MESA Adaptive Moving Average (MAMA)

An advanced dual-stage adaptive moving average, this function outputs both the MAMA and its companion FAMA. It combines adaptive alpha computation with elements from Kaufman’s Adaptive Moving Average (KAMA) to provide a responsive and reliable trend indicator.

Source: John Ehlers - "Rocket Science for Traders" (2001), "TASC 2001 V. 19:9", "Cybernetic Analysis for Stocks and Futures" (2004)

💮 BiQuad Filters

A family of second-order recursive filters offering exceptional control over frequency response:

- High-pass filter for detrending

- Low-pass filter for smooth trend following

- Band-pass filter for cycle isolation

The quality factor (Q) parameter allows fine-tuning of the resonance characteristics, making these filters highly adaptable to different market conditions.

Source: Robert Bristow-Johnson's Audio EQ Cookbook, implemented by @The_Peaceful_Lizard

💮 Relative Vigor Index (RVI)

This filter evaluates the strength of a trend by comparing the closing price to the trading range. Operating similarly to a band-pass filter, the RVI provides insights into market momentum and potential reversals.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 Cyber Cycle

The Cyber Cycle filter emphasises market cycles by smoothing out noise and highlighting the dominant cyclical behaviour. It is particularly useful for detecting trend reversals and cyclical patterns in the price data.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 Butterworth High Pass Filter

Inspired by the classical Butterworth design, this filter achieves a maximally flat magnitude response in the passband while effectively removing low-frequency trends. Its design minimises phase distortion, which is vital for accurate signal interpretation.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 2-Pole SuperSmoother

Employing a two-pole design, the SuperSmoother filter reduces high-frequency noise with minimal lag. It is engineered to preserve trend integrity while offering a smooth output even in noisy market conditions.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 3-Pole SuperSmoother

An extension of the 2-pole design, the 3-pole SuperSmoother further attenuates high-frequency noise. Its additional pole delivers enhanced smoothing at the cost of slightly increased lag.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 Adaptive Directional Volatility Moving Average (ADXVma)

This adaptive moving average adjusts its smoothing factor based on directional volatility. By combining true range and directional movement measurements, it remains exceptionally flat during ranging markets and responsive during directional moves.

Source: Various implementations across platforms, unified and optimized

💮 Ehlers Combined Bandpass Filter with Automated Gain Control (AGC)

This sophisticated filter merges a highpass pre-processing stage with a bandpass filter. An integrated Automated Gain Control normalises the output to a consistent range, while offering both regular and truncated recursive formulations to manage lag.

Source: John F. Ehlers – “Truncated Indicators” (2020), “Cycle Analytics for Traders” (2013)

💮 Voss Predictive Filter

A forward-looking filter that predicts future values of a band-limited signal in real time. By utilising multiple time-delayed feedback terms, it provides anticipatory coupling and delivers a short-term predictive signal.

Source: John Ehlers - "A Peek Into The Future" (TASC 2019-08)

💮 Adaptive Autonomous Recursive Moving Average (A2RMA)

This filter dynamically adjusts its smoothing through an adaptive mechanism based on an efficiency ratio and a dynamic threshold. A double application of an adaptive moving average ensures both responsiveness and stability in volatile and ranging markets alike. Very flat response when properly tuned.

Source: @alexgrover (2019)

💮 Ultimate Smoother (2-Pole)

The Ultimate Smoother filter is engineered to achieve near-zero lag in its passband by subtracting a high-pass response from an all-pass response. This creates a filter that maintains signal fidelity at low frequencies while effectively filtering higher frequencies at the expense of slight overshooting.

Source: John Ehlers - TASC 2024-04 "The Ultimate Smoother"

Note: This library is actively maintained and enhanced. Suggestions for additional filters or improvements are welcome through the usual channels. The source code contains a list of tested filters that did not make it into the curated collection.

Ehlers Maclaurin Ultimate Smoother [CT]Ehlers Maclaurin Ultimate Smoother

Introduction

The Ehlers Maclaurin Ultimate Smoother is an innovative enhancement of the classic Ehlers SuperSmoother. By leveraging advanced Maclaurin series approximations, this indicator offers superior market analysis and signal generation.

The indicator combines Ehlers' Ultimate Smoother with Maclaurin series approximations to create a more efficient and accurate smoothing mechanism:

Input price data passes through the initial smoothing phase

Maclaurin series approximates trigonometric functions

Enhanced high-pass filter removes market noise

Final smoothing phase produces the output signal

Why the Maclaurin Approach?

The Maclaurin series is a special form of the Taylor series, centered around 0. It provides an efficient way to approximate complex functions using polynomial terms. In this indicator, we use the Maclaurin approach to improve the sine and cosine functions, resulting in:

Faster Calculations: By using polynomial approximations, we significantly reduce computational complexity.

Improved Stability: The approximation provides a more stable numerical basis for calculations.

Preservation of Precision: Despite the approximation, we maintain the precision needed for price smoothing.

Calculations

The indicator employs several key mathematical components:

Maclaurin Series Approximation:

sin(x) ≈ x - x³/3! + x⁵/5! - x⁷/7! + x⁹/9!

cos(x) ≈ 1 - x²/2! + x⁴/4! - x⁶/6! + x⁸/8!

Smoothing Algorithm:

Uses exponential smoothing with optimized coefficients

Implements high-pass filtering for noise reduction

Applies dynamic weighting based on market conditions

Mathematical Foundation

Utilizes Maclaurin series for trigonometric approximation

Implements Ehlers' smoothing principles

Incorporates advanced filtering techniques

Technical Advantages

Signal Processing:

Lag Reduction: Faster signal detection with less delay.

Noise Filtration: Effective elimination of high-frequency noise.

Precision Enhancement: Preservation of critical price movements.

Adaptive Processing: Dynamic response to market volatility.

Visual Enhancements:

Smart color intensity mapping.

Real-time visualization of trend strength.

Adaptive opacity based on movement significance.

Implementation

Core Configuration:

Plot Type: Choose between the original and the Maclaurin enhanced version.

Length: Default set to 30, optimal for daily timeframes.

hpLength: Default set to 10 for enhanced noise reduction.

Advanced Parameters:

The indicator offers advanced control with:

Dual processing modes (Original/Maclaurin).

Dynamic color intensity system.

Customizable smoothing parameters.

Professional Analysis Tools:

Accurate trend reversal identification.

Advanced support/resistance detection.

Superior performance in volatile markets.

Technical Specifications

Maclaurin Series Implementation:

The indicator employs a 5-term Maclaurin series approximation for both sine and cosine, ensuring efficient and accurate computation.

Performance Metrics

Improved processing efficiency.

Reduced memory utilization.

Increased signal accuracy.

Licensing & Attribution

© 2024 Mupsje aka CasaTropical

Professional Credits

Original Ultimate and SuperSmoother concept: John F. Ehlers

Maclaurin enhancement: Casa Tropical (CT)

www.mathsisfun.com

RSI Team Synergy | JeffreyTimmermansRSI Team Synergy

The "RSI Team Synergy" indicator is an advanced and highly customizable tool that integrates a Double RSI (DRSI) approach for comprehensive trend and momentum analysis. It utilizes two layers of RSI calculations, along with optional smoothing and various moving average types, to enhance signal accuracy. The dynamic visuals and alerts make this indicator a valuable resource for traders aiming to optimize their strategies.

Key Features

Double RSI (DRSI) Calculation

First RSI (Primary Layer): Captures the core price momentum using a configurable period.

Second RSI (DRSI Layer): Applies a second RSI calculation to the smoothed first RSI, refining signals and amplifying trend accuracy.

Double RSI Formula: Combines the smoothed RSI layers into a single robust indicator that adapts to market conditions.

Smoothing and Advanced Moving Averages

Optional Smoothing: Enables users to reduce noise by applying smoothing to both RSI layers.

Advanced MA Options: Supports multiple MA types, including SMA, EMA, WMA, RMA, DEMA, TEMA, VWMA, ZLEMA, and HMA. These can be applied to tailor the indicator to specific trading conditions.

Separate Configurations: Independent smoothing lengths and types for each RSI layer provide unparalleled customization.

Threshold and Signal System

Long Threshold: Highlights bullish conditions when the Double RSI exceeds the threshold.

Short Threshold: Signals bearish conditions when the Double RSI falls below the threshold.

Directional State: Tracks the overall direction using a state-based signal system (bullish, bearish, or neutral).

Dynamic Visualization

Oscillator Color Coding: Green shades for bullish momentum. Red shades for bearish momentum. Dynamic gradients for smoother transitions.

Glow Effect: Optional glowing lines enhance the visual clarity of the oscillator.

Threshold Lines: Configurable dashed horizontal lines to mark critical levels for easy reference.

Bar Color Integration

Bar Coloring: Matches bar colors to the oscillator's direction for cohesive visualization.

Advanced Control: Toggle bar coloring on/off without affecting other plots.

Alerts

Bullish Signal Alert: Triggers when the Double RSI crosses above the long threshold.

Bearish Signal Alert: Triggers when the Double RSI crosses below the short threshold.

Custom Messages: Alerts are equipped with descriptive messages for actionable insights.

Signal Arrows

Bullish Arrow (↑): Marks upward trends directly on the chart.

Bearish Arrow (↓): Highlights downward trends, ensuring traders never miss an opportunity.

Improvements

Customizable Thresholds: Adjustable long and short thresholds allow traders to fine-tune sensitivity.

Enhanced Smoothing Control: Separate smoothing options for each RSI layer provide flexibility in noise reduction.

Multiple MA Types: Extensive support for advanced moving averages to suit diverse trading preferences.

Color-Coded Oscillator: Improves trend visibility with gradient-based coloring and optional glow effects.

Signal Detection: Clear and intuitive arrows directly on the chart for quick signal interpretation.

Alerts and Notifications: Comprehensive alert conditions keep traders informed in real-time.

Use Cases

Momentum Analysis: Identify sustained bullish or bearish trends using the Double RSI calculation.

Noise Reduction: Utilize smoothing and advanced MA options to remove market noise.

Reversal Detection: Spot potential trend reversals with threshold-based signals.

Customizable Strategies: Tailor the indicator for scalping, swing trading, or long-term analysis.

The RSI Team Synergy indicator combines precision, flexibility, and intuitive design, making it an essential tool for traders at all levels. With its innovative Double RSI approach and advanced customization options, it provides actionable insights for mastering market trends.

This script is inspired by "Clokivez" . However, it is more advanced and includes additional features and options.

-Jeffrey

Catalyst TrendCatalyst Trend – A Comprehensive Trend and Regime Analyzer

The Catalyst Trend indicator was designed to dynamically and intuitively merge various classic analytical techniques. The goal is to filter out short-term market noise and reveal reliable trend phases or potential turning points. Below is a detailed explanation of its core elements and practical usage.

1. Concept and Idea

Multidimensional Trend Detection

This indicator goes beyond a simple momentum or volatility focus. It factors in multiple measurements to provide a more well-rounded market perspective.

Versatile Indicator Fusion

Linear Regression (LinReg): Multiple LinReg calculations are combined to smooth out price fluctuations and produce a robust trendline—known here as the “Cycle Reduced Line.”

ADX (Average Directional Index): Measures trend strength.

RSI (Relative Strength Index): Flags potential overbought or oversold conditions, in both the current timeframe and a higher timeframe.

ATR (Average True Range): Assesses volatility; used to dynamically adjust calculation lengths.

By weaving these elements together, the indicator adds value beyond simply stacking multiple indicators. It adapts to real-time market conditions, aiming to highlight genuine trends and reduce false signals.

2. Key Functions and Calculations

Dynamic Length & Smoothing

A blend of volatility (ATR), ADX values, and RSI inputs determines how many candles are used in the LinReg calculations and how heavily the data is smoothed.

This allows the indicator to respond promptly during periods of high volatility, while automatically adjusting to filter out unnecessary noise in quieter phases.c

Cycle Reduced Line

The script averages several offset LinReg calculations to produce a cleaner overall signal. Random outliers are thus minimized, making the trend path more visually consistent.

An additional EMA smoothing (“Final Smoothing”) further stabilizes this trendline, reducing the impact of minor price fluctuations.

Channel Bands (Optional)

These bands are derived from the standard deviation of the price residual (the difference between the smoothed price and the trendline).

They highlight potential over-extension zones: the upper band can mark short-term overbought areas, while the lower band might indicate oversold conditions.

Trend and Sideways Determination

Slope Calculation: The slope of the trendline (comparing the current bar to the previous one) helps identify short-term directional shifts.

DX Threshold: Once the ADX surpasses a user-defined threshold and the slope is positive, it may indicate a developing uptrend. Similarly, if the slope is negative and ADX > threshold, it could signal a potential downtrend.

Multi-Level Color Coding

Original Mode: Interpolated colors reflect uptrends, downtrends, and sideways phases, factoring in metrics like ADX and RSI.

Single Color: For a neutral look, the indicator can be displayed in one uniform color.

HTF RSI: This mode uses the higher-timeframe RSI to color the trendline (Long/Short/Neutral), offering a quick gauge of overarching market pressure.

3. Use Cases and Interpretation

Timeframes & Markets

The indicator is versatile and adapts well to different intervals, from 5-minute charts to weekly views.

It can be applied to various markets—crypto, forex, stocks—since volatility and trend strength are universal concepts.

Signal Recognition

Color Swings into a more pronounced upward hue (e.g., green) may signal mounting strength.

Neutral or mixed tones often point to sideways phases, which breakout traders might watch for potential price surges.

A shift to downward colors (e.g., red) may indicate a growing bearish trend.

Channel Bands & Volatility

When the bands spread widely, it’s wise to proceed with caution: abrupt spikes above the upper band or below the lower band can flag rapid short-term extremes.

These bands are more of a reference for potential overextension than a strict buy or sell trigger.

Additional Confirmations

Not a standalone panacea: The Catalyst Trend indicator is an analytical tool, best used alongside other methods such as volume analysis or price action (candlestick patterns, support/resistance levels) to bolster confidence in trading decisions.

4. Practical Tips

Parameter Adjustments

Depending on the market—crypto vs. traditional currency pairs—different ADX, RSI, or smoothing periods may be more effective. Experiment with the settings to tailor the indicator to your preferred timeframe.

Strategic Integration

Trailing Stops: For those riding a trend, the trendline or the channel bands may serve as a reference to trail stop-loss orders.

Trend Confirmation: Using RSI and ADX filters can help traders avoid sideways markets or stay the course when the trend is strong.

5. Important Final Notes

No Guarantee of Profits

No indicator can predict the future. Markets are inherently volatile and often unpredictable.

Responsible Risk Management

Test the indicator in a demo environment or with smaller positions before committing to large trades.

Hybrid Triple Exponential Smoothing🙏🏻 TV, I present you HTES aka Hybrid Triple Exponential Smoothing, designed by Holt & Winters in the US, assembled by me in Saint P. I apply exponential smoothing individually to the data itself, then to residuals from the fitted values, and lastly to one-point forecast (OPF) errors, hence 'hybrid'. At the same time, the method is a closed-form solution and purely online, no need to make any recalculations & optimize anything, so the method is O(1).

^^ historical OPFs and one-point forecasting interval plotted instead of fitted values and prediction interval

Before the How-to, first let me tell you some non-obvious things about Triple Exponential smoothing (and about Exponential Smoothing in general) that not many catch. Expo smoothing seems very straightforward and obvious, but if you look deeper...

1) The whole point of exponential smoothing is its incremental/online nature, and its O(1) algorithm complexity, making it dope for high-frequency streaming data that is also univariate and has no weights. Consequently:

- Any hybrid models that involve expo smoothing and any type of ML models like gradient boosting applied to residuals rarely make much sense business-wise: if you have resources to boost the residuals, you prolly have resources to use something instead of expo smoothing;

- It also concerns the fashion of using optimizers to pick smoothing parameters; honestly, if you use this approach, you have to retrain on each datapoint, which is crazy in a streaming context. If you're not in a streaming context, why expo smoothing? What makes more sense is either picking smoothing parameters once, guided by exogenous info, or using dynamic ones calculated in a minimalistic and elegant way (more on that in further drops).

2) No matter how 'right' you choose the smoothing parameters, all the resulting components (level, trend, seasonal) are not pure; each of them contains a bit of info from the other components, this is just how non-sequential expo smoothing works. You gotta know this if you wanna use expo smoothing to decompose your time series into separate components. The only pure component there, lol, is the residuals;

3) Given what I've just said, treating the level (that does contain trend and seasonal components partially) as the resulting fit is a mistake. The resulting fit is level (l) + trend (b) + seasonal (s). And from this fit, you calculate residuals;

4) The residuals component is not some kind of bad thing; it is simply the component that contains info you consciously decide not to include in your model for whatever reason;

5) Forecasting Errors and Residuals from fitted values are 2 different things. The former are deltas between the forecasts you've made and actual values you've observed, the latter are simply differences between actual datapoints and in-sample fitted values;

6) Residuals are used for in-sample prediction intervals, errors for out-of-sample forecasting intervals;

7) Choosing between single, double, or triple expo smoothing should not be based exclusively on the nature of your data, but on what you need to do as well. For example:

- If you have trending seasonal data and you wanna do forecasting exclusively within the expo smoothing framework, then yes, you need Triple Exponential Smoothing;

- If you wanna use prediction intervals for generating trend-trading signals and you disregard seasonality, then you need single (simple) expo smoothing, even on trending data. Otherwise, the trend component will be included in your model's fitted values → prediction intervals.

8) Kind of not non-obvious, but when you put one smoothing parameter to zero, you basically disregard this component. E.g., in triple expo smoothing, when you put gamma and beta to zero, you basically end up with single exponential smoothing.

^^ data smoothing, beta and gamma zeroed out, forecasting steps = 0

About the implementation

* I use a simple power transform that results in a log transform with lambda = 0 instead of the mainstream-used transformers (if you put lambda on 2 in Box-Cox, you won't get a power of 2 transform)

* Separate set of smoothing parameters for data, residuals, and errors smoothing

* Separate band multipliers for residuals and errors

* Both typical error and typical residuals get multiplied by math.sqrt(math.pi / 2) in order to approach standard deviation so you can ~use Z values and get more or less corresponding probabilities

* In script settings → style, you can switch on/off plotting of many things that get calculated internally:

- You can visualize separate components (just remember they are not pure);

- You can switch off fit and switch on OPF plotting;

- You can plot residuals and their exponentially smoothed typical value to pick the smoothing parameters for both data and residuals;

- Or you might plot errors and play with data smoothing parameters to minimize them (consult SAE aka Sum of Absolute Errors plot);

^^ nuff said

More ideas on how to use the thing

1) Use Double Exponential Smoothing (data gamma = 0) to detrend your time series for further processing (Fourier likes at least weakly stationary data);

2) Put single expo smoothing on your strategy/subaccount equity chart (data alpha = data beta = 0), set prediction interval deviation multiplier to 1, run your strat live on simulator, start executing on real market when equity on simulator hits upper deviation (prediction interval), stop trading if equity hits lower deviation on simulator. Basically, let the strat always run on simulator, but send real orders to a real market when the strat is successful on your simulator;

3) Set up the model to minimize one-point forecasting errors, put error forecasting steps to 1, now you're doing nowcasting;

4) Forecast noisy trending sine waves for fun.

^^ nuff said 2

All Good TV ∞

Normalized Linear Regression (LSMA) OscillatorNormalized Linear Regression (LSMA) Oscillator

By Nathan Farmer

The Normalized LSMA Oscillator is a trend-following indicator that enhances the classic Linear Regression (LSMA) by applying a range of normalization techniques. This indicator allows traders to smooth out and normalize LSMA signals for better trend detection and dynamic market adaptation.

Key Features:

Configurable Normalization Methods:

This indicator offers several normalization techniques, such as Z-Score, Min-Max, Mean Normalization, Robust Scaler, Logistic Function, and Quantile Transformation. Each method helps in refining LSMA outputs to improve clarity in both trending and ranging market conditions.

Smoothing Options:

Smoothing can be applied after normalization, helping to reduce noise in the signals, thus making trend-following strategies that use this indicator more effective.

Recommended Settings:

Logistic Function Normalization: Recommended length of around 12, based on my preferred signal frequency.

Z-Score Normalization: Medium period (close to the default of 50), based on my preferred signal frequency.

Min-Max Normalization: Medium period, based on my preferred signal frequency.

Mean Normalization: Medium period, based on my preferred signal frequency.

Robust Scaler: Medium period, based on my preferred signal frequency.

Quantile Transformation: Medium period, based on my preferred signal frequency.

Usage:

Designed primarily for trend-following strategies, this indicator adapts well to varying market conditions. Traders can experiment with the various normalization and smoothing settings to match the indicator to their specific needs and market preferences.

Recommendation before usage:

Always backtest the indicator for yourself with respect to how you intend to use it. Modify the parameters to suit your needs, over your preferred time frame, on your preferred asset. My preferences are for the assets I happened to be looking at when I made this indicator. Odds are, you're looking at something else, over a different time frame, in a different market environment than what my settings are tailored for.

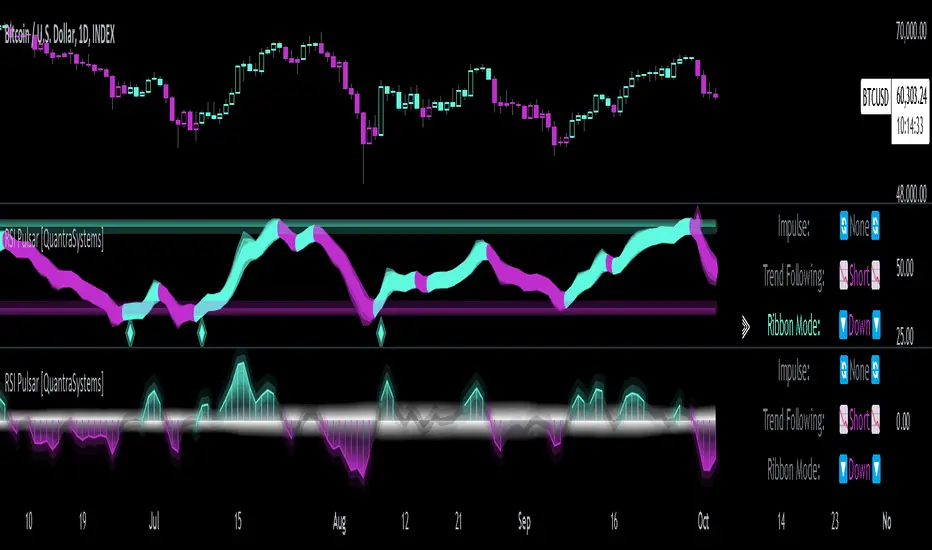

RSI Pulsar [QuantraSystems]RSI Pulsar

Introduction

The RSI Pulsar is an advanced and multifaceted tool designed to cater to the varying needs of traders, from long-term swing traders to higher-frequency day traders. This indicator takes the Relative Strength Index (RSI) to new heights by combining several unique methodologies to provide clear, actionable signals across different market conditions. With its ability to analyze impulsive trend strength, volatility, and binary market direction, the RSI Pulsar offers a holistic view of the market that assists traders in identifying robust signals and rotational opportunities within a volatile market.

The integration of dynamic color coding further aids in quick visual assessments, allowing traders to adapt swiftly to changing market conditions, making the RSI Pulsar an essential component in the arsenal of modern traders aiming for precision and adaptability in their trading endeavors.

Legend

The RSI Pulsar encapsulates various modes tailored to diverse trading strategies. The different modes are the:

Impulse Mode:

Focuses on strong outperformance, ideal for capturing movements in highly dynamic tokens.

Trend Following Mode:

A classical perpetual trend-following approach and provides binary long and short signal classifications ideal for medium term swing trading.

Ribbon Mode:

Offers quicker signals that are also binary in nature. Perfect for a confirmation signal when building higher frequency day trading systems.

Volatility Spectrum:

This feature projects a visual 'cloud' representing volatility, which helps traders spot emerging trends and potential breakouts or reversals.

Compressed Mode:

A condensed view that displays all signals in a clean and space-efficient manner. It provides a clear summary of market conditions, ideal for traders who prefer a simplified overview.

Methodology

The RSI Pulsar is built on a foundation of dynamic RSI analysis, where the traditional RSI is enhanced with advanced moving averages and standard deviation calculations. Each mode within the RSI Pulsar is designed to cater to specific aspects of the market's behavior, making it a versatile tool allowing traders to select different modes based on their trading style and market conditions.

Impulse Mode:

This mode identifies strong outperformance in assets, making it ideal for asset rotation systems. It uses a combination of RSI thresholds and dynamic moving averages to pinpoint when an asset is not just trending positively, but doing so with significant strength.

This is in contrast to typical usage of a base RSI, where elevated levels usually signal overbought and oversold periods. The RSI Pulsar flips this logic, where more extreme values are actually interpreted as a strong trend.

Trend Following Mode:

Here, the RSI is compared to the midline (the default is level 50, but a dynamic midline can also be set), to determine the prevailing trend. This mode simplifies the trend-following process, providing clear bullish or bearish signals based on whether the RSI is above or below the midline - whether a fixed or dynamic level.

Ribbon Mode:

This mode employs a series of calculated values derived from modified Heikin-Ashi smoothing to create a "ribbon" that smooths out price action and highlights underlying trends. The Ribbon Mode is particularly useful for traders who need quick confirmations of trend reversals or continuations.

Volatility Spectrum:

The Volatility Spectrum takes a unique approach to measuring market volatility by analyzing the size and direction of Heikin-Ashi candles. This data is used to create a volatility cloud that helps traders identify when volatility is rising, falling, or neutral - allowing them to adjust their strategies accordingly.

When the signal line breaks above the cloud, it signals increasing upwards volatility. When it breaks below it signifies increasing downwards volatility.

This can be used to help identify strengthening and weakening trends, as well as imminent volatile periods, allowing traders to position themselves and adapt their strategies accordingly. This mode also works as a great volatility filter for shorter term day trading strategies. It is incredibly sensitive to volatility divergences, and can give additional insights to larger market turning points.

Compressed Mode:

In Compressed Mode, all the signals from the various modes are displayed in a simplified format, making it easy for traders to quickly assess the market's overall condition without needing to delve into the details of each mode individually. Perfect for only viewing the exact data you need when live trading, or back testing.

Case Study I:

Utilizing ALMA Impulse Mode in High-Volatility Environments

Here, the RSI Pulsar is configured with an RSI length of 9 and an ALMA length of 2 in Impulse Mode. The chart example shows how this setup can identify significant price movements, allowing traders to enter positions early and capture substantial price moves. Despite the fast settings resulting in occasional false signals, the indicator's ability to catch and ride out major trends more than compensates, making it highly effective in volatile environments.

This configuration is suitable for traders seeking to trade quick, aggressive movements without enduring prolonged drawdowns. In Impulse Mode, the RSI Pulsar seeks strong trending zones, providing actionable signals that allow for timely entries and exits.

Case Study II:

SMMA Trend Following Mode for Ratio Analysis

The RSI Pulsar in Trend Following mode, configured with the SMMA with default length settings. This setup is ideal for analyzing longer-term trends, particularly useful in cryptocurrency pairs or ratio charts, where it’s crucial to identify robust directional moves. The chart showcases strong trends in the Solana/Ethereum pair. The RSI Pulsar’s ability to smooth out price action while remaining responsive to trend changes makes it an excellent tool for capturing extended price moves.

The image highlights how the RSI Pulsar efficiently tracks the strength of two tokens against each other, providing clear signals when one asset begins to outperform the other. Even in volatile markets, the SMMA ensures that the signals are reliable, filtering out noise and allowing traders to stay in the trend longer without being shaken out by minor corrections. This approach is particularly effective in ratio trading in order to inform a longer term swing trader of the strongest asset out of a customized pair.

Case Study III:

Monthly Analysis with RSI Pulsar in Ribbon Mode

This case study demonstrates the versatility and reliability of the RSI Pulsar in Ribbon mode, applied to a monthly chart of Bitcoin with an RSI length of 8 and a TEMA length of 14. This setup highlights the indicator’s robustness across multiple timeframes, extending even to long-term analysis. The RSI Pulsar effectively smooths out noise while capturing significant trends, as seen during Bitcoin bull markets. The Ribbon mode provides a clear visual representation of momentum shifts, making it easier for traders to identify trend continuations and reversals with confidence.

Case Study IV:

Divergences and Continuations with the Volatility Spectrum

Identifying harmony/divergences can be hit-or-miss at times, but this unique analysis method definitely has its merits at times. The RSI Pulsar, with its Volatility Spectrum feature, is used here to identify critical moments where price action either aligns with or diverges from the underlying volatility. As seen in the Bitcoin chart (using default settings), the indicator highlights areas where price trends either continue in harmony with volatility or diverge, signaling potential reversals. This method, while not always perfect, provides significant insight during key turning points in the market.

The Volatility Spectrum's visual representation of rising and falling volatility, combined with divergence and harmony analysis, enables traders to anticipate significant shifts in market dynamics. In this case, multiple divergences correctly identified early trend reversals, while periods of harmony indicated strong trend continuations. While this method requires careful interpretation, especially during complex market conditions, it offers valuable signals that can be pivotal in making informed trading decisions, especially if combined with other forms of analysis it can form a critical component of an investing system.

Kalman PSaR [BackQuant]Kalman PSaR

Overview and Innovation

The Kalman PSaR combines the well-known Parabolic SAR (PSaR) with the advanced smoothing capabilities of the Kalman Filter . This innovative tool aims to enhance the traditional PSaR by integrating Kalman filtering, which reduces noise and improves trend detection. The Kalman PSaR adapts dynamically to price movements, making it a highly effective indicator for spotting trend shifts while minimizing the impact of false signals caused by market volatility.

Please Find the Basic Kalman Here:

Kalman Filter Dynamics

The Kalman Filter is a powerful algorithm for estimating the true value of a system amidst noisy data. In the Kalman PSaR, this filter is applied to the high, low, and closing prices, resulting in a smoother and more accurate representation of price action. The filter’s parameters—process noise and measurement noise—are customizable, allowing traders to fine-tune the sensitivity of the indicator to market conditions. By reducing the impact of noise, the Kalman-filtered PSaR offers clearer signals for identifying trend reversals and continuations.

Enhanced PSaR Calculation

The traditional Parabolic SAR is a popular trend-following indicator that highlights potential entry and exit points based on price acceleration. In the Kalman PSaR, this calculation is enhanced by the Kalman-filtered prices, providing a smoother and more reliable signal. The indicator continuously updates based on the acceleration factor and max step values, while the Kalman filter ensures that sudden price spikes or market noise do not trigger false signals.

Min Step and Max Step: These settings control the sensitivity of the PSaR. The Min Step sets the initial acceleration factor, while the Max Step limits how fast the PSaR adapts to price changes, helping traders fine-tune the indicator’s responsiveness.

Optional Smoothing Techniques To further enhance the signal clarity, the Kalman PSaR includes an optional smoothing feature. Traders can choose from various smoothing methods, such as SMA, Hull, EMA, WMA, TEMA, and more, to reduce short-term fluctuations and emphasize the underlying trend. The smoothing period is customizable, allowing traders to adjust the indicator’s behavior according to their preferred trading style and timeframe.

Color-Coded Candle Painting The Kalman PSaR features color-coded candles that change according to the trend direction. When the price is above the PSaR, candles are painted green to indicate a long trend, and when the price is below the PSaR, candles are painted red to signal a short trend. This visual representation makes it easy to interpret market sentiment at a glance, improving decision-making speed during fast-moving markets.

Key Features and Customization

Kalman Filter Customization: The process noise and measurement noise parameters allow traders to adjust how aggressively the filter adapts to price changes, making it suitable for both volatile and stable markets.

Smoothing Options: A variety of moving average types, such as SMA, Hull, EMA, and more, can be applied to smooth the PSaR values, ensuring that the signal remains clear even in choppy markets.

Dynamic Trend Detection: The Kalman PSaR dynamically updates based on price movements, helping traders spot trend reversals early while filtering out false signals caused by short-term volatility.

Bar Coloring and PSaR Plotting: Traders can choose to color candles based on trend direction or plot the PSaR directly on the chart for additional visual clarity.

Practical Applications

Trend-Following Strategies: The Kalman PSaR excels in trend-following strategies by providing timely signals of trend changes. The dynamic nature of the indicator allows traders to capture significant price movements while avoiding market noise.

Reversal Identification: The indicator’s ability to filter out noise and provide smoother signals makes it ideal for identifying reversals in volatile markets.

Risk Management: By plotting clear stop levels based on the PSaR, traders can use this indicator to effectively manage risk, placing stop-loss orders at key points based on the trend direction.

Conclusion

The Kalman PSaR is a fusion of the classic Parabolic SAR and the Kalman filter, offering enhanced trend detection with reduced noise. Its customizable filtering and smoothing options, combined with dynamic trend-following capabilities, make it a versatile tool for traders seeking to improve their timing and signal accuracy. The adaptive nature of the Kalman filter, combined with the robust PSaR logic, helps traders stay on the right side of the market and manage risk more effectively.

ARIMA Indicator with Optional SmoothingOverview

The ARIMA (AutoRegressive Integrated Moving Average) Indicator is a powerful tool used to forecast future price movements by combining differencing, autoregressive, and moving average components. This indicator is designed to help traders identify trends and potential reversal points by analyzing the historical price data.

Key Features

AutoRegressive Component (AR): Utilizes past values to predict future prices.

Moving Average Component (MA): Averages past price differences to smooth out noise.

Differencing: Reduces non-stationarity in the time series data.

Optional Smoothing: Applies EMA to the ARIMA output for a smoother signal.

Customizable Parameters: Allows users to adjust AR and MA orders, differencing periods, and smoothing lengths.

Concepts Underlying the Calculations

Differencing: Subtracts previous prices from current prices to remove trends and seasonality, making the data stationary.

AutoRegressive Component (AR): Predicts future prices based on a linear combination of past values.

Moving Average Component (MA): Uses past forecast errors to refine future predictions.

Exponential Moving Average (EMA): Applies more weight to recent prices, providing a smoother and more responsive signal.

How It Works

The ARIMA Indicator first calculates the differenced series to achieve stationarity. Then, it computes the simple moving average (SMA) of this differenced series. The indicator uses the AR and MA components to adjust the SMA, creating an approximation of the ARIMA model. Finally, an optional smoothing step using EMA can be applied to the ARIMA approximation to produce a smoother signal.

How Traders Can Use It

Traders can use the ARIMA Indicator to:

Identify Trends: Detect emerging trends by observing the direction of the ARIMA line.

Spot Reversals: Look for divergences between the ARIMA line and the price to identify potential reversal points.

Generate Trading Signals: Use crossovers between the ARIMA line and the price to generate buy or sell signals.

Filter Noise: Enable the optional smoothing to filter out market noise and focus on significant price movements.

Example Usage Instructions

Add the ARIMA Indicator to your chart.

Adjust the input parameters to suit your trading strategy:

Set the SMA Length (e.g., 14).

Choose the Differencing Period (e.g., 1).

Define the AR Order (p) and MA Order (q) (e.g., 1).

Configure the Smoothing Length if smoothing is desired (e.g., 5).

Enable or disable smoothing as needed.

Observe the ARIMA line (blue) and compare it to the price chart.

Use the ARIMA line to identify trends and potential reversals.

Implement trading decisions based on the ARIMA line’s behavior relative to the price.

mathLibrary "math"

It's a library of discrete aproximations of a price or Series float it uses Fourier Discrete transform, Laplace Discrete Original and Modified transform and Euler's Theoreum for Homogenus White noice operations. Calling functions without source value it automatically take close as the default source value.

Here is a picture of Laplace and Fourier approximated close prices from this library:

Copy this indicator and try it yourself:

import AutomatedTradingAlgorithms/math/1 as math

//@version=5

indicator("Close Price with Aproximations", shorttitle="Close and Aproximations", overlay=false)

// Sample input data (replace this with your own data)

inputData = close

// Plot Close Price

plot(inputData, color=color.blue, title="Close Price")

ltf32_result = math.LTF32(a=0.01)

plot(ltf32_result, color=color.green, title="LTF32 Aproximation")

fft_result = math.FFT()

plot(fft_result, color=color.red, title="Fourier Aproximation")

wavelet_result = math.Wavelet()

plot(wavelet_result, color=color.orange, title="Wavelet Aproximation")

wavelet_std_result = math.Wavelet_std()

plot(wavelet_std_result, color=color.yellow, title="Wavelet_std Aproximation")

DFT3(xval, _dir)

Discrete Fourier Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

DFT2(xval, _dir)

Discrete Fourier Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

FFT(xval)

Fast Fourier Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DFT32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DTF32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

LFT3(xval, _dir, a)

Discrete Laplace Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT2(xval, _dir, a)

Discrete Laplace Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT(xval, a)

Fast Laplace Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LTF32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

whitenoise(indic_, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise, without extra aproximated src.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

whitenoise(indic_, dft1, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise and DFT1.

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

dft1 (float) : Aproximated src value for white noice calculation

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

smooth(dft1, indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series and aproximated source value

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

dft1 (float) : Value to be smoothed.

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed source (src) series

smooth(indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed src series

vzo_ema(src, len)