KalmanfilterLibrary "Kalmanfilter"

A sophisticated Kalman Filter implementation for financial time series analysis

@author Rocky-Studio

@version 1.0

initialize(initial_value, process_noise, measurement_noise)

Initializes Kalman Filter parameters

Parameters:

initial_value (float) : (float) The initial state estimate

process_noise (float) : (float) The process noise coefficient (Q)

measurement_noise (float) : (float) The measurement noise coefficient (R)

Returns: A tuple containing

update(prev_state, prev_covariance, measurement, process_noise, measurement_noise)

Update Kalman Filter state

Parameters:

prev_state (float)

prev_covariance (float)

measurement (float)

process_noise (float)

measurement_noise (float)

calculate_measurement_noise(price_series, length)

Adaptive measurement noise calculation

Parameters:

price_series (array)

length (int)

calculate_measurement_noise_simple(price_series)

Parameters:

price_series (array)

update_trading(prev_state, prev_velocity, prev_covariance, measurement, volatility_window)

Enhanced trading update with velocity

Parameters:

prev_state (float)

prev_velocity (float)

prev_covariance (float)

measurement (float)

volatility_window (int)

model4_update(prev_mean, prev_speed, prev_covariance, price, process_noise, measurement_noise)

Kalman Filter Model 4 implementation (Benhamou 2018)

Parameters:

prev_mean (float)

prev_speed (float)

prev_covariance (array)

price (float)

process_noise (array)

measurement_noise (float)

model4_initialize(initial_price)

Initialize Model 4 parameters

Parameters:

initial_price (float)

model4_default_process_noise()

Create default process noise matrix for Model 4

model4_calculate_measurement_noise(price_series, length)

Adaptive measurement noise calculation for Model 4

Parameters:

price_series (array)

length (int)

Statistics

Request█ OVERVIEW

This library is a tool for Pine Script™ programmers that consolidates access to a wide range of lesser-known data feeds available on TradingView, including metrics from the FRED database, FINRA short sale volume, open interest, and COT data. The functions in this library simplify requests for these data feeds, making them easier to retrieve and use in custom scripts.

█ CONCEPTS

Federal Reserve Economic Data (FRED)

FRED (Federal Reserve Economic Data) is a comprehensive online database curated by the Federal Reserve Bank of St. Louis. It provides free access to extensive economic and financial data from U.S. and international sources. FRED includes numerous economic indicators such as GDP, inflation, employment, and interest rates. Additionally, it provides financial market data, regional statistics, and international metrics such as exchange rates and trade balances.

Sourced from reputable organizations, including U.S. government agencies, international institutions, and other public and private entities, FRED enables users to analyze over 825,000 time series, download their data in various formats, and integrate their information into analytical tools and programming workflows.

On TradingView, FRED data is available from ticker identifiers with the "FRED:" prefix. Users can search for FRED symbols in the "Symbol Search" window, and Pine scripts can retrieve data for these symbols via `request.*()` function calls.

FINRA Short Sale Volume

FINRA (the Financial Industry Regulatory Authority) is a non-governmental organization that supervises and regulates U.S. broker-dealers and securities professionals. Its primary aim is to protect investors and ensure integrity and transparency in financial markets.

FINRA's Short Sale Volume data provides detailed information about daily short-selling activity across U.S. equity markets. This data tracks the volume of short sales reported to FINRA's trade reporting facilities (TRFs), including shares sold on FINRA-regulated Alternative Trading Systems (ATSs) and over-the-counter (OTC) markets, offering transparent access to short-selling information not typically available from exchanges. This data helps market participants, researchers, and regulators monitor trends in short-selling and gain insights into bearish sentiment, hedging strategies, and potential market manipulation. Investors often use this data alongside other metrics to assess stock performance, liquidity, and overall trading activity.

It is important to note that FINRA's Short Sale Volume data does not consolidate short sale information from public exchanges and excludes trading activity that is not publicly disseminated.

TradingView provides ticker identifiers for requesting Short Sale Volume data with the format "FINRA:_SHORT_VOLUME", where "" is a supported U.S. equities symbol (e.g., "AAPL").

Open Interest (OI)

Open interest is a cornerstone indicator of market activity and sentiment in derivatives markets such as options or futures. In contrast to volume, which measures the number of contracts opened or closed within a period, OI measures the number of outstanding contracts that are not yet settled. This distinction makes OI a more robust indicator of how money flows through derivatives, offering meaningful insights into liquidity, market interest, and trends. Many traders and investors analyze OI alongside volume and price action to gain an enhanced perspective on market dynamics and reinforce trading decisions.

TradingView offers many ticker identifiers for requesting OI data with the format "_OI", where "" represents a derivative instrument's ticker ID (e.g., "COMEX:GC1!").

Commitment of Traders (COT)

Commitment of Traders data provides an informative weekly breakdown of the aggregate positions held by various market participants, including commercial hedgers, non-commercial speculators, and small traders, in the U.S. derivative markets. Tallied and managed by the Commodity Futures Trading Commission (CFTC) , these reports provide traders and analysts with detailed insight into an asset's open interest and help them assess the actions of various market players. COT data is valuable for gaining a deeper understanding of market dynamics, sentiment, trends, and liquidity, which helps traders develop informed trading strategies.

TradingView has numerous ticker identifiers that provide access to time series containing data for various COT metrics. To learn about COT ticker IDs and how they work, see our LibraryCOT publication.

█ USING THE LIBRARY

Common function characteristics

• This library's functions construct ticker IDs with valid formats based on their specified parameters, then use them as the `symbol` argument in request.security() to retrieve data from the specified context.

• Most of these functions automatically select the timeframe of a data request because the data feeds are not available for all timeframes.

• All the functions have two overloads. The first overload of each function uses values with the "simple" qualifier to define the requested context, meaning the context does not change after the first script execution. The second accepts "series" values, meaning it can request data from different contexts across executions.

• The `gaps` parameter in most of these functions specifies whether the returned data is `na` when a new value is unavailable for request. By default, its value is `false`, meaning the call returns the last retrieved data when no new data is available.

• The `repaint` parameter in applicable functions determines whether the request can fetch the latest unconfirmed values from a higher timeframe on realtime bars, which might repaint after the script restarts. If `false`, the function only returns confirmed higher-timeframe values to avoid repainting. The default value is `true`.

`fred()`

The `fred()` function retrieves the most recent value of a specified series from the Federal Reserve Economic Data (FRED) database. With this function, programmers can easily fetch macroeconomic indicators, such as GDP and unemployment rates, and use them directly in their scripts.

How it works

The function's `fredCode` parameter accepts a "string" representing the unique identifier of a specific FRED series. Examples include "GDP" for the "Gross Domestic Product" series and "UNRATE" for the "Unemployment Rate" series. Over 825,000 codes are available. To access codes for available series, search the FRED website .

The function adds the "FRED:" prefix to the specified `fredCode` to construct a valid FRED ticker ID (e.g., "FRED:GDP"), which it uses in request.security() to retrieve the series data.

Example Usage

This line of code requests the latest value from the Gross Domestic Product series and assigns the returned value to a `gdpValue` variable:

float gdpValue = fred("GDP")

`finraShortSaleVolume()`

The `finraShortSaleVolume()` function retrieves EOD data from a FINRA Short Sale Volume series. Programmers can call this function to retrieve short-selling information for equities listed on supported exchanges, namely NASDAQ, NYSE, and NYSE ARCA.

How it works

The `symbol` parameter determines which symbol's short sale volume information is retrieved by the function. If the value is na , the function requests short sale volume data for the chart's symbol. The argument can be the name of the symbol from a supported exchange (e.g., "AAPL") or a ticker ID with an exchange prefix ("NASDAQ:AAPL"). If the `symbol` contains an exchange prefix, it must be one of the following: "NASDAQ", "NYSE", "AMEX", or "BATS".

The function constructs a ticker ID in the format "FINRA:ticker_SHORT_VOLUME", where "ticker" is the symbol name without the exchange prefix (e.g., "AAPL"). It then uses the ticker ID in request.security() to retrieve the available data.

Example Usage

This line of code retrieves short sale volume for the chart's symbol and assigns the result to a `shortVolume` variable:

float shortVolume = finraShortSaleVolume(syminfo.tickerid)

This example requests short sale volume for the "NASDAQ:AAPL" symbol, irrespective of the current chart:

float shortVolume = finraShortSaleVolume("NASDAQ:AAPL")

`openInterestFutures()` and `openInterestCrypto()`

The `openInterestFutures()` function retrieves EOD open interest (OI) data for futures contracts. The `openInterestCrypto()` function provides more granular OI data for cryptocurrency contracts.

How they work

The `openInterestFutures()` function retrieves EOD closing OI information. Its design is focused primarily on retrieving OI data for futures, as only EOD OI data is available for these instruments. If the chart uses an intraday timeframe, the function requests data from the "1D" timeframe. Otherwise, it uses the chart's timeframe.

The `openInterestCrypto()` function retrieves opening, high, low, and closing OI data for a cryptocurrency contract on a specified timeframe. Unlike `openInterest()`, this function can also retrieve granular data from intraday timeframes.

Both functions contain a `symbol` parameter that determines the symbol for which the calls request OI data. The functions construct a valid OI ticker ID from the chosen symbol by appending "_OI" to the end (e.g., "CME:ES1!_OI").

The `openInterestFutures()` function requests and returns a two-element tuple containing the futures instrument's EOD closing OI and a "bool" condition indicating whether OI is rising.

The `openInterestCrypto()` function requests and returns a five-element tuple containing the cryptocurrency contract's opening, high, low, and closing OI, and a "bool" condition indicating whether OI is rising.

Example usage

This code line calls `openInterest()` to retrieve EOD OI and the OI rising condition for a futures symbol on the chart, assigning the values to two variables in a tuple:

= openInterestFutures(syminfo.tickerid)

This line retrieves the EOD OI data for "CME:ES1!", irrespective of the current chart's symbol:

= openInterestFutures("CME:ES1!")

This example uses `openInterestCrypto()` to retrieve OHLC OI data and the OI rising condition for a cryptocurrency contract on the chart, sampled at the chart's timeframe. It assigns the returned values to five variables in a tuple:

= openInterestCrypto(syminfo.tickerid, timeframe.period)

This call retrieves OI OHLC and rising information for "BINANCE:BTCUSDT.P" on the "1D" timeframe:

= openInterestCrypto("BINANCE:BTCUSDT.P", "1D")

`commitmentOfTraders()`

The `commitmentOfTraders()` function retrieves data from the Commitment of Traders (COT) reports published by the Commodity Futures Trading Commission (CFTC). This function significantly simplifies the COT request process, making it easier for programmers to access and utilize the available data.

How It Works

This function's parameters determine different parts of a valid ticker ID for retrieving COT data, offering a streamlined alternative to constructing complex COT ticker IDs manually. The `metricName`, `metricDirection`, and `includeOptions` parameters are required. They specify the name of the reported metric, the direction, and whether it includes information from options contracts.

The function also includes several optional parameters. The `CFTCCode` parameter allows programmers to request data for a specific report code. If unspecified, the function requests data based on the chart symbol's root prefix, base currency, or quoted currency, depending on the `mode` argument. The call can specify the report type ("Legacy", "Disaggregated", or "Financial") and metric type ("All", "Old", or "Other") with the `typeCOT` and `metricType` parameters.

Explore the CFTC website to find valid report codes for specific assets. To find detailed information about the metrics included in the reports and their meanings, see the CFTC's Explanatory Notes .

View the function's documentation below for detailed explanations of its parameters. For in-depth information about COT ticker IDs and more advanced functionality, refer to our previously published COT library .

Available metrics

Different COT report types provide different metrics . The tables below list all available metrics for each type and their applicable directions:

+------------------------------+------------------------+

| Legacy (COT) Metric Names | Directions |

+------------------------------+------------------------+

| Open Interest | No direction |

| Noncommercial Positions | Long, Short, Spreading |

| Commercial Positions | Long, Short |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No direction |

| Traders Noncommercial | Long, Short, Spreading |

| Traders Commercial | Long, Short |

| Traders Total Reportable | Long, Short |

| Concentration Gross LT 4 TDR | Long, Short |

| Concentration Gross LT 8 TDR | Long, Short |

| Concentration Net LT 4 TDR | Long, Short |

| Concentration Net LT 8 TDR | Long, Short |

+------------------------------+------------------------+

+-----------------------------------+------------------------+

| Disaggregated (COT2) Metric Names | Directions |

+-----------------------------------+------------------------+

| Open Interest | No Direction |

| Producer Merchant Positions | Long, Short |

| Swap Positions | Long, Short, Spreading |

| Managed Money Positions | Long, Short, Spreading |

| Other Reportable Positions | Long, Short, Spreading |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No Direction |

| Traders Producer Merchant | Long, Short |

| Traders Swap | Long, Short, Spreading |

| Traders Managed Money | Long, Short, Spreading |

| Traders Other Reportable | Long, Short, Spreading |

| Traders Total Reportable | Long, Short |

| Concentration Gross LE 4 TDR | Long, Short |

| Concentration Gross LE 8 TDR | Long, Short |

| Concentration Net LE 4 TDR | Long, Short |

| Concentration Net LE 8 TDR | Long, Short |

+-----------------------------------+------------------------+

+-------------------------------+------------------------+

| Financial (COT3) Metric Names | Directions |

+-------------------------------+------------------------+

| Open Interest | No Direction |

| Dealer Positions | Long, Short, Spreading |

| Asset Manager Positions | Long, Short, Spreading |

| Leveraged Funds Positions | Long, Short, Spreading |

| Other Reportable Positions | Long, Short, Spreading |

| Total Reportable Positions | Long, Short |

| Nonreportable Positions | Long, Short |

| Traders Total | No Direction |

| Traders Dealer | Long, Short, Spreading |

| Traders Asset Manager | Long, Short, Spreading |

| Traders Leveraged Funds | Long, Short, Spreading |

| Traders Other Reportable | Long, Short, Spreading |

| Traders Total Reportable | Long, Short |

| Concentration Gross LE 4 TDR | Long, Short |

| Concentration Gross LE 8 TDR | Long, Short |

| Concentration Net LE 4 TDR | Long, Short |

| Concentration Net LE 8 TDR | Long, Short |

+-------------------------------+------------------------+

Example usage

This code line retrieves "Noncommercial Positions (Long)" data, without options information, from the "Legacy" report for the chart symbol's root, base currency, or quote currency:

float nonCommercialLong = commitmentOfTraders("Noncommercial Positions", "Long", false)

This example retrieves "Managed Money Positions (Short)" data, with options included, from the "Disaggregated" report:

float disaggregatedData = commitmentOfTraders("Managed Money Positions", "Short", true, "", "Disaggregated")

█ NOTES

• This library uses dynamic requests , allowing dynamic ("series") arguments for the parameters defining the context (ticker ID, timeframe, etc.) of a `request.*()` function call. With this feature, a single `request.*()` call instance can flexibly retrieve data from different feeds across historical executions. Additionally, scripts can use such calls in the local scopes of loops, conditional structures, and even exported library functions, as demonstrated in this script. All scripts coded in Pine Script™ v6 have dynamic requests enabled by default. To learn more about the behaviors and limitations of this feature, see the Dynamic requests section of the Pine Script™ User Manual.

• The library's example code offers a simple demonstration of the exported functions. The script retrieves available data using the function specified by the "Series type" input. The code requests a FRED series or COT (Legacy), FINRA Short Sale Volume, or Open Interest series for the chart's symbol with specific parameters, then plots the retrieved data as a step-line with diamond markers.

Look first. Then leap.

█ EXPORTED FUNCTIONS

This library exports the following functions:

fred(fredCode, gaps)

Requests a value from a specified Federal Reserve Economic Data (FRED) series. FRED is a comprehensive source that hosts numerous U.S. economic datasets. To explore available FRED datasets and codes, search for specific categories or keywords at fred.stlouisfed.org Calls to this function count toward a script's `request.*()` call limit.

Parameters:

fredCode (series string) : The unique identifier of the FRED series. The function uses the value to create a valid ticker ID for retrieving FRED data in the format `"FRED:fredCode"`. For example, `"GDP"` refers to the "Gross Domestic Product" series ("FRED:GDP"), and `"GFDEBTN"` refers to the "Federal Debt: Total Public Debt" series ("FRED:GFDEBTN").

gaps (simple bool) : Optional. If `true`, the function returns a non-na value only when a new value is available from the requested context. If `false`, the function returns the latest retrieved value when new data is unavailable. The default is `false`.

Returns: (float) The value from the requested FRED series.

finraShortSaleVolume(symbol, gaps, repaint)

Requests FINRA daily short sale volume data for a specified symbol from one of the following exchanges: NASDAQ, NYSE, NYSE ARCA. If the chart uses an intraday timeframe, the function requests data from the "1D" timeframe. Otherwise, it uses the chart's timeframe. Calls to this function count toward a script's `request.*()` call limit.

Parameters:

symbol (series string) : The symbol for which to request short sale volume data. If the specified value contains an exchange prefix, it must be one of the following: "NASDAQ", "NYSE", "AMEX", "BATS".

gaps (simple bool) : Optional. If `true`, the function returns a non-na value only when a new value is available from the requested context. If `false`, the function returns the latest retrieved value when new data is unavailable. The default is `false`.

repaint (simple bool) : Optional. If `true` and the chart's timeframe is intraday, the value requested on realtime bars may change its time offset after the script restarts its executions. If `false`, the function returns the last confirmed period's values to avoid repainting. The default is `true`.

Returns: (float) The short sale volume for the specified symbol or the chart's symbol.

openInterestFutures(symbol, gaps, repaint)

Requests EOD open interest (OI) and OI rising information for a valid futures symbol. If the chart uses an intraday timeframe, the function requests data from the "1D" timeframe. Otherwise, it uses the chart's timeframe. Calls to this function count toward a script's `request.*()` call limit.

Parameters:

symbol (series string) : The symbol for which to request open interest data.

gaps (simple bool) : Optional. If `true`, the function returns non-na values only when new values are available from the requested context. If `false`, the function returns the latest retrieved values when new data is unavailable. The default is `false`.

repaint (simple bool) : Optional. If `true` and the chart's timeframe is intraday, the value requested on realtime bars may change its time offset after the script restarts its executions. If `false`, the function returns the last confirmed period's values to avoid repainting. The default is `true`.

Returns: ( ) A tuple containing the following values:

- The closing OI value for the symbol.

- `true` if the closing OI is above the previous period's value, `false` otherwise.

openInterestCrypto(symbol, timeframe, gaps, repaint)

Requests opening, high, low, and closing open interest (OI) data and OI rising information for a valid cryptocurrency contract on a specified timeframe. Calls to this function count toward a script's `request.*()` call limit.

Parameters:

symbol (series string) : The symbol for which to request open interest data.

timeframe (series string) : The timeframe of the data request. If the timeframe is lower than the chart's timeframe, it causes a runtime error.

gaps (simple bool) : Optional. If `true`, the function returns non-na values only when new values are available from the requested context. If `false`, the function returns the latest retrieved values when new data is unavailable. The default is `false`.

repaint (simple bool) : Optional. If `true` and the `timeframe` represents a higher timeframe, the function returns unconfirmed values from the timeframe on realtime bars, which repaint when the script restarts its executions. If `false`, it returns only confirmed higher-timeframe values to avoid repainting. The default is `true`.

Returns: ( ) A tuple containing the following values:

- The opening, high, low, and closing OI values for the symbol, respectively.

- `true` if the closing OI is above the previous period's value, `false` otherwise.

commitmentOfTraders(metricName, metricDirection, includeOptions, CFTCCode, typeCOT, mode, metricType)

Requests Commitment of Traders (COT) data with specified parameters. This function provides a simplified way to access CFTC COT data available on TradingView. Calls to this function count toward a script's `request.*()` call limit. For more advanced tools and detailed information about COT data, see TradingView's LibraryCOT library.

Parameters:

metricName (series string) : One of the valid metric names listed in the library's documentation and source code.

metricDirection (series string) : Metric direction. Possible values are: "Long", "Short", "Spreading", and "No direction". Consult the library's documentation or code to see which direction values apply to the specified metric.

includeOptions (series bool) : If `true`, the COT symbol includes options information. Otherwise, it does not.

CFTCCode (series string) : Optional. The CFTC code for the asset. For example, wheat futures (root "ZW") have the code "001602". If one is not specified, the function will attempt to get a valid code for the chart symbol's root, base currency, or main currency.

typeCOT (series string) : Optional. The type of report to request. Possible values are: "Legacy", "Disaggregated", "Financial". The default is "Legacy".

mode (series string) : Optional. Specifies the information the function extracts from a symbol. Possible modes are:

- "Root": The function extracts the futures symbol's root prefix information (e.g., "ES" for "ESH2020").

- "Base currency": The function extracts the first currency from a currency pair (e.g., "EUR" for "EURUSD").

- "Currency": The function extracts the currency of the symbol's quoted values (e.g., "JPY" for "TSE:9984" or "USDJPY").

- "Auto": The function tries the first three modes (Root -> Base currency -> Currency) until it finds a match.

The default is "Auto". If the specified mode is not available for the symbol, it causes a runtime error.

metricType (series string) : Optional. The metric type. Possible values are: "All", "Old", "Other". The default is "All".

Returns: (float) The specified Commitment of Traders data series. If no data is available, it causes a runtime error.

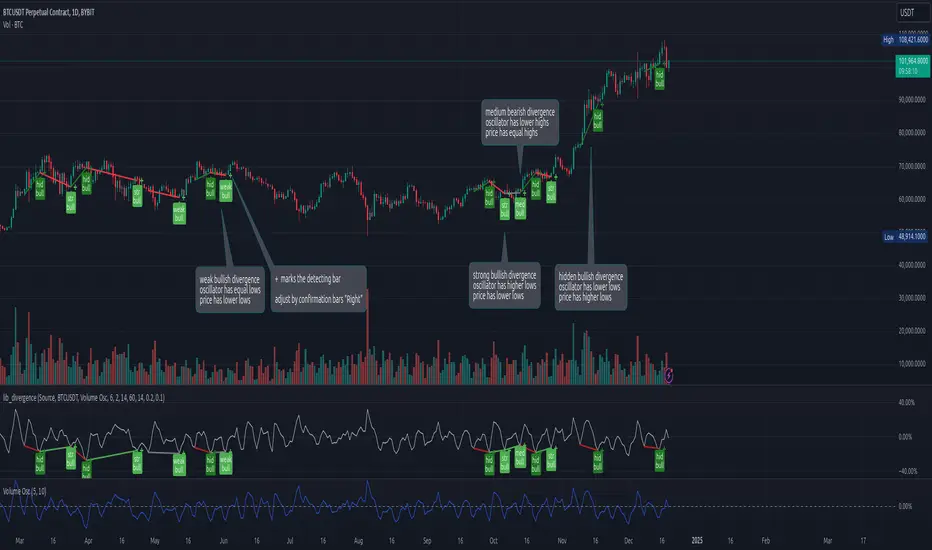

lib_divergenceLibrary "lib_divergence"

offers a commonly usable function to detect divergences. This will take the default RSI or other symbols / indicators / oscillators as source data.

divergence(osc, pivot_left_bars, pivot_right_bars, div_min_range, div_max_range, ref_low, ref_high, min_divergence_offset_fraction, min_divergence_offset_dev_len, min_divergence_offset_atr_mul)

Detects Divergences between Price and Oscillator action. For bullish divergences, look at trend lines between lows. For bearish divergences, look at trend lines between highs. (strong) oscillator trending, price opposing it | (medium) oscillator trending, price trend flat | (weak) price opposite trending, oscillator trend flat | (hidden) price trending, oscillator opposing it. Pivot detection is only properly done in oscillator data, reference price data is only compared at the oscillator pivot (speed optimization)

Parameters:

osc (float) : (series float) oscillator data (can be anything, even another instrument price)

pivot_left_bars (simple int) : (simple int) optional number of bars left of a confirmed pivot point, confirming it is the highest/lowest in the range before and up to the pivot (default: 5)

pivot_right_bars (simple int) : (simple int) optional number of bars right of a confirmed pivot point, confirming it is the highest/lowest in the range from and after the pivot (default: 5)

div_min_range (simple int) : (simple int) optional minimum distance to the pivot point creating a divergence (default: 5)

div_max_range (simple int) : (simple int) optional maximum amount of bars in a divergence (default: 50)

ref_low (float) : (series float) optional reference range to compare the oscillator pivot points to. (default: low)

ref_high (float) : (series float) optional reference range to compare the oscillator pivot points to. (default: high)

min_divergence_offset_fraction (simple float) : (simple float) optional scaling factor for the offset zone (xDeviation) around the last oscillator H/L detecting following equal H/Ls (default: 0.01)

min_divergence_offset_dev_len (simple int) : (simple int) optional lookback distance for the deviation detection for the offset zone around the last oscillator H/L detecting following equal H/Ls. Used as well for the ATR that does the equal H/L detection for the reference price. (default: 14)

min_divergence_offset_atr_mul (simple float) : (simple float) optional scaling factor for the offset zone (xATR) around the last price H/L detecting following equal H/Ls (default: 1)

@return A tuple of deviation flags.

QTALibrary "QTA"

This is simple library for basic Quantitative Technical Analysis for retail investors. One example of it being used can be seen here ().

calculateKellyRatio(returns)

Parameters:

returns (array) : An array of floats representing the returns from bets.

Returns: The calculated Kelly Ratio, which indicates the optimal bet size based on winning and losing probabilities.

calculateAdjustedKellyFraction(kellyRatio, riskTolerance, fedStance)

Parameters:

kellyRatio (float) : The calculated Kelly Ratio.

riskTolerance (float) : A float representing the risk tolerance level.

fedStance (string) : A string indicating the Federal Reserve's stance ("dovish", "hawkish", or neutral).

Returns: The adjusted Kelly Fraction, constrained within the bounds of .

calculateStdDev(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The standard deviation of the returns, or 0 if insufficient data.

calculateMaxDrawdown(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The maximum drawdown as a percentage.

calculateEV(avgWinReturn, winProb, avgLossReturn)

Parameters:

avgWinReturn (float) : The average return from winning bets.

winProb (float) : The probability of winning a bet.

avgLossReturn (float) : The average return from losing bets.

Returns: The calculated Expected Value of the bet.

calculateTailRatio(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The Tail Ratio, or na if the 5th percentile is zero to avoid division by zero.

calculateSharpeRatio(avgReturn, riskFreeRate, stdDev)

Parameters:

avgReturn (float) : The average return of the investment.

riskFreeRate (float) : The risk-free rate of return.

stdDev (float) : The standard deviation of the investment's returns.

Returns: The calculated Sharpe Ratio, or na if standard deviation is zero.

calculateDownsideDeviation(returns)

Parameters:

returns (array) : An array of floats representing the returns.

Returns: The standard deviation of the downside returns, or 0 if no downside returns exist.

calculateSortinoRatio(avgReturn, downsideDeviation)

Parameters:

avgReturn (float) : The average return of the investment.

downsideDeviation (float) : The standard deviation of the downside returns.

Returns: The calculated Sortino Ratio, or na if downside deviation is zero.

calculateVaR(returns, confidenceLevel)

Parameters:

returns (array) : An array of floats representing the returns.

confidenceLevel (float) : A float representing the confidence level (e.g., 0.95 for 95% confidence).

Returns: The Value at Risk at the specified confidence level.

calculateCVaR(returns, varValue)

Parameters:

returns (array) : An array of floats representing the returns.

varValue (float) : The Value at Risk threshold.

Returns: The average Conditional Value at Risk, or na if no returns are below the threshold.

calculateExpectedPriceRange(currentPrice, ev, stdDev, confidenceLevel)

Parameters:

currentPrice (float) : The current price of the asset.

ev (float) : The expected value (in percentage terms).

stdDev (float) : The standard deviation (in percentage terms).

confidenceLevel (float) : The confidence level for the price range (e.g., 1.96 for 95% confidence).

Returns: A tuple containing the minimum and maximum expected prices.

calculateRollingStdDev(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling standard deviation of returns.

calculateRollingVariance(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling variance of returns.

calculateRollingMean(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling mean of returns.

calculateRollingCoefficientOfVariation(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling coefficient of variation of returns.

calculateRollingSumOfPercentReturns(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling sum of percent returns.

calculateRollingCumulativeProduct(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling cumulative product of returns.

calculateRollingCorrelation(priceReturns, volumeReturns, window)

Parameters:

priceReturns (array) : An array of floats representing the price returns.

volumeReturns (array) : An array of floats representing the volume returns.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling correlation.

calculateRollingPercentile(returns, window, percentile)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

percentile (int) : An integer representing the desired percentile (0-100).

Returns: An array of floats representing the rolling percentile of returns.

calculateRollingMaxMinPercentReturns(returns, window)

Parameters:

returns (array) : An array of floats representing the returns.

window (int) : An integer representing the rolling window size.

Returns: A tuple containing two arrays: rolling max and rolling min percent returns.

calculateRollingPriceToVolumeRatio(price, volData, window)

Parameters:

price (array) : An array of floats representing the price data.

volData (array) : An array of floats representing the volume data.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the rolling price-to-volume ratio.

determineMarketRegime(priceChanges)

Parameters:

priceChanges (array) : An array of floats representing the price changes.

Returns: A string indicating the market regime ("Bull", "Bear", or "Neutral").

determineVolatilityRegime(price, window)

Parameters:

price (array) : An array of floats representing the price data.

window (int) : An integer representing the rolling window size.

Returns: An array of floats representing the calculated volatility.

classifyVolatilityRegime(volatility)

Parameters:

volatility (array) : An array of floats representing the calculated volatility.

Returns: A string indicating the volatility regime ("Low" or "High").

method percentPositive(thisArray)

Returns the percentage of positive non-na values in this array.

This method calculates the percentage of positive values in the provided array, ignoring NA values.

Namespace types: array

Parameters:

thisArray (array)

_candleRange()

_PreviousCandleRange(barsback)

Parameters:

barsback (int) : An integer representing how far back you want to get a range

redCandle()

greenCandle()

_WhiteBody()

_BlackBody()

HighOpenDiff()

OpenLowDiff()

_isCloseAbovePreviousOpen(length)

Parameters:

length (int)

_isCloseBelowPrevious()

_isOpenGreaterThanPrevious()

_isOpenLessThanPrevious()

BodyHigh()

BodyLow()

_candleBody()

_BodyAvg(length)

_BodyAvg function.

Parameters:

length (simple int) : Required (recommended is 6).

_SmallBody(length)

Parameters:

length (simple int) : Length of the slow EMA

Returns: a series of bools, after checking if the candle body was less than body average.

_LongBody(length)

Parameters:

length (simple int)

bearWick()

bearWick() function.

Returns: a SERIES of FLOATS, checks if it's a blackBody(open > close), if it is, than check the difference between the high and open, else checks the difference between high and close.

bullWick()

barlength()

sumbarlength()

sumbull()

sumbear()

bull_vol()

bear_vol()

volumeFightMA()

volumeFightDelta()

weightedAVG_BullVolume()

weightedAVG_BearVolume()

VolumeFightDiff()

VolumeFightFlatFilter()

avg_bull_vol(userMA)

avg_bull_vol(int) function.

Parameters:

userMA (int)

avg_bear_vol(userMA)

avg_bear_vol(int) function.

Parameters:

userMA (int)

diff_vol(userMA)

diff_vol(int) function.

Parameters:

userMA (int)

vol_flat(userMA)

vol_flat(int) function.

Parameters:

userMA (int)

_isEngulfingBullish()

_isEngulfingBearish()

dojiup()

dojidown()

EveningStar()

MorningStar()

ShootingStar()

Hammer()

InvertedHammer()

BearishHarami()

BullishHarami()

BullishBelt()

BullishKicker()

BearishKicker()

HangingMan()

DarkCloudCover()

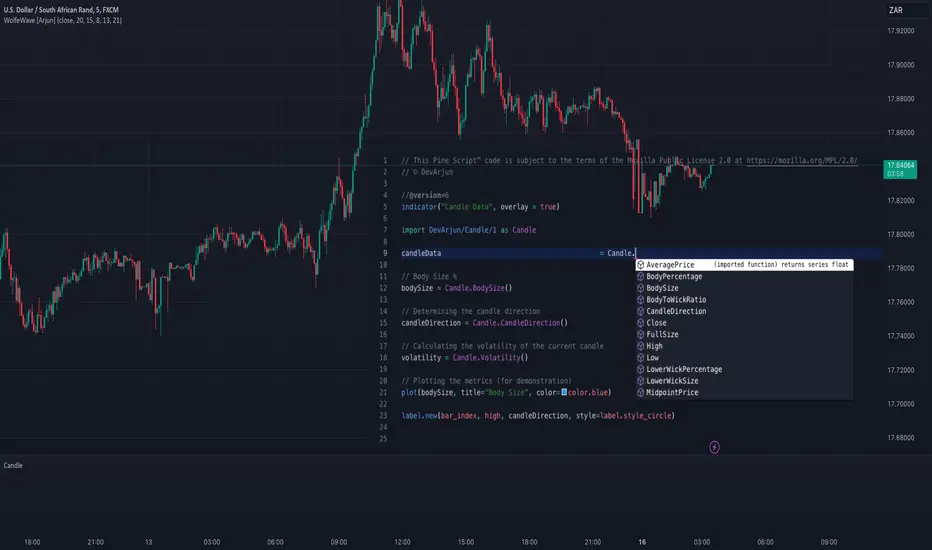

CandleCandle: A Comprehensive Pine Script™ Library for Candlestick Analysis

Overview

The Candle library, developed in Pine Script™, provides traders and developers with a robust toolkit for analyzing candlestick data. By offering easy access to fundamental candlestick components like open, high, low, and close prices, along with advanced derived metrics such as body-to-wick ratios, percentage calculations, and volatility analysis, this library enables detailed insights into market behavior.

This library is ideal for creating custom indicators, trading strategies, and backtesting frameworks, making it a powerful resource for any Pine Script™ developer.

Key Features

1. Core Candlestick Data

• Open : Access the opening price of the current candle.

• High : Retrieve the highest price.

• Low : Retrieve the lowest price.

• Close : Access the closing price.

2. Candle Metrics

• Full Size : Calculates the total range of the candle (high - low).

• Body Size : Computes the size of the candle’s body (open - close).

• Wick Size : Provides the combined size of the upper and lower wicks.

3. Wick and Body Ratios

• Upper Wick Size and Lower Wick Size .

• Body-to-Wick Ratio and Wick-to-Body Ratio .

4. Percentage Calculations

• Upper Wick Percentage : The proportion of the upper wick size relative to the full candle size.

• Lower Wick Percentage : The proportion of the lower wick size relative to the full candle size.

• Body Percentage and Wick Percentage relative to the candle’s range.

5. Candle Direction Analysis

• Determines if a candle is "Bullish" or "Bearish" based on its closing and opening prices.

6. Price Metrics

• Average Price : The mean of the open, high, low, and close prices.

• Midpoint Price : The midpoint between the high and low prices.

7. Volatility Measurement

• Calculates the standard deviation of the OHLC prices, providing a volatility metric for the current candle.

Code Architecture

Example Functionality

The library employs a modular structure, exporting various functions that can be used independently or in combination. For instance:

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © DevArjun

//@version=6

indicator("Candle Data", overlay = true)

import DevArjun/Candle/1 as Candle

// Body Size %

bodySize = Candle.BodySize()

// Determining the candle direction

candleDirection = Candle.CandleDirection()

// Calculating the volatility of the current candle

volatility = Candle.Volatility()

// Plotting the metrics (for demonstration)

plot(bodySize, title="Body Size", color=color.blue)

label.new(bar_index, high, candleDirection, style=label.style_circle)

Scalability

The modularity of the Candle library allows seamless integration into more extensive trading systems. Functions can be mixed and matched to suit specific analytical or strategic needs.

Use Cases

Trading Strategies

Developers can use the library to create strategies based on candle properties such as:

• Identifying long-bodied candles (momentum signals).

• Detecting wicks as potential reversal zones.

• Filtering trades based on candle ratios.

Visualization

Plotting components like body size, wick size, and directional labels helps visualize market behavior and identify patterns.

Backtesting

By incorporating volatility and ratio metrics, traders can design and test strategies on historical data, ensuring robust performance before live trading.

Education

This library is a great tool for teaching candlestick analysis and how each component contributes to market behavior.

Portfolio Highlights

Project Objective

To create a Pine Script™ library that simplifies candlestick analysis by providing comprehensive metrics and insights, empowering traders and developers with advanced tools for market analysis.

Development Challenges and Solutions

• Challenge : Achieving high precision in calculating ratios and percentages.

• Solution : Implemented robust mathematical operations and safeguarded against division-by-zero errors.

• Challenge : Ensuring modularity and scalability.

• Solution : Designed functions as independent modules, allowing flexible integration.

Impact

• Efficiency : The library reduces the time required to calculate complex candlestick metrics.

• Versatility : Supports various trading styles, from scalping to swing trading.

• Clarity : Clean code and detailed documentation ensure usability for developers of all levels.

Conclusion

The Candle library exemplifies the power of Pine Script™ in simplifying and enhancing candlestick analysis. By including this project in your portfolio, you showcase your expertise in:

• Financial data analysis.

• Pine Script™ development.

• Creating tools that solve real-world trading challenges.

This project demonstrates both technical proficiency and a keen understanding of market analysis, making it an excellent addition to your professional portfolio.

Library "Candle"

A comprehensive library to access and analyze the basic components of a candlestick, including open, high, low, close prices, and various derived metrics such as full size, body size, wick sizes, ratios, percentages, and additional analysis metrics.

Open()

Open

@description Returns the opening price of the current candle.

Returns: float - The opening price of the current candle.

High()

High

@description Returns the highest price of the current candle.

Returns: float - The highest price of the current candle.

Low()

Low

@description Returns the lowest price of the current candle.

Returns: float - The lowest price of the current candle.

Close()

Close

@description Returns the closing price of the current candle.

Returns: float - The closing price of the current candle.

FullSize()

FullSize

@description Returns the full size (range) of the current candle (high - low).

Returns: float - The full size of the current candle.

BodySize()

BodySize

@description Returns the body size of the current candle (open - close).

Returns: float - The body size of the current candle.

WickSize()

WickSize

@description Returns the size of the wicks of the current candle (full size - body size).

Returns: float - The size of the wicks of the current candle.

UpperWickSize()

UpperWickSize

@description Returns the size of the upper wick of the current candle.

Returns: float - The size of the upper wick of the current candle.

LowerWickSize()

LowerWickSize

@description Returns the size of the lower wick of the current candle.

Returns: float - The size of the lower wick of the current candle.

BodyToWickRatio()

BodyToWickRatio

@description Returns the ratio of the body size to the wick size of the current candle.

Returns: float - The body to wick ratio of the current candle.

UpperWickPercentage()

UpperWickPercentage

@description Returns the percentage of the upper wick size relative to the full size of the current candle.

Returns: float - The percentage of the upper wick size relative to the full size of the current candle.

LowerWickPercentage()

LowerWickPercentage

@description Returns the percentage of the lower wick size relative to the full size of the current candle.

Returns: float - The percentage of the lower wick size relative to the full size of the current candle.

WickToBodyRatio()

WickToBodyRatio

@description Returns the ratio of the wick size to the body size of the current candle.

Returns: float - The wick to body ratio of the current candle.

BodyPercentage()

BodyPercentage

@description Returns the percentage of the body size relative to the full size of the current candle.

Returns: float - The percentage of the body size relative to the full size of the current candle.

WickPercentage()

WickPercentage

@description Returns the percentage of the wick size relative to the full size of the current candle.

Returns: float - The percentage of the wick size relative to the full size of the current candle.

CandleDirection()

CandleDirection

@description Returns the direction of the current candle.

Returns: string - "Bullish" if the candle is bullish, "Bearish" if the candle is bearish.

AveragePrice()

AveragePrice

@description Returns the average price of the current candle (mean of open, high, low, and close).

Returns: float - The average price of the current candle.

MidpointPrice()

MidpointPrice

@description Returns the midpoint price of the current candle (mean of high and low).

Returns: float - The midpoint price of the current candle.

Volatility()

Volatility

@description Returns the standard deviation of the OHLC prices of the current candle.

Returns: float - The volatility of the current candle.

DynamicPeriodPublicDynamic Period Calculation Library

This library provides tools for adaptive period determination, useful for creating indicators or strategies that automatically adjust to market conditions.

Overview

The Dynamic Period Library calculates adaptive periods based on pivot points, enabling the creation of responsive indicators and strategies that adjust to market volatility.

Key Features

Dynamic Periods: Computes periods using distances between pivot highs and lows.

Customizable Parameters: Users can adjust detection settings and period constraints.

Robust Handling: Includes fallback mechanisms for cases with insufficient pivot data.

Use Cases

Adaptive Indicators: Build tools that respond to market volatility by adjusting their periods dynamically.

Dynamic Strategies: Enhance trading strategies by integrating pivot-based period adjustments.

Function: `dynamic_period`

Description

Calculates a dynamic period based on the average distances between pivot highs and lows.

Parameters

`left` (default: 5): Number of left-hand bars for pivot detection.

`right` (default: 5): Number of right-hand bars for pivot detection.

`numPivots` (default: 5): Minimum pivots required for calculation.

`minPeriod` (default: 2): Minimum allowed period.

`maxPeriod` (default: 50): Maximum allowed period.

`defaultPeriod` (default: 14): Fallback period if no pivots are found.

Returns

A dynamic period calculated based on pivot distances, constrained by `minPeriod` and `maxPeriod`.

Example

//@version=6

import CrimsonVault/DynamicPeriodPublic/1

left = input.int(5, "Left bars", minval = 1)

right = input.int(5, "Right bars", minval = 1)

numPivots = input.int(5, "Number of Pivots", minval = 2)

period = DynamicPeriodPublic.dynamic_period(left, right, numPivots)

plot(period, title = "Dynamic Period", color = color.blue)

Implementation Notes

Pivot Detection: Requires sufficient historical data to identify pivots accurately.

Edge Cases: Ensures a default period is applied when pivots are insufficient.

Constraints: Limits period values to a user-defined range for stability.

lib_kernelLibrary "lib_kernel"

Library "lib_kernel"

This is a tool / library for developers, that contains several common and adapted kernel functions as well as a kernel regression function and enum to easily select and embed a list into the settings dialog.

How to Choose and Modify Kernels in Practice

Compact Support Kernels (e.g., Epanechnikov, Triangular): Use for localized smoothing and emphasizing nearby data.

Oscillatory Kernels (e.g., Wave, Cosine): Ideal for detecting periodic patterns or mean-reverting behavior.

Smooth Tapering Kernels (e.g., Gaussian, Logistic): Use for smoothing long-term trends or identifying global price behavior.

kernel_Epanechnikov(u)

Parameters:

u (float)

kernel_Epanechnikov_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Triangular(u)

Parameters:

u (float)

kernel_Triangular_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Rectangular(u)

Parameters:

u (float)

kernel_Uniform(u)

Parameters:

u (float)

kernel_Uniform_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Logistic(u)

Parameters:

u (float)

kernel_Logistic_alt(u)

Parameters:

u (float)

kernel_Logistic_alt2(u, sigmoid_steepness)

Parameters:

u (float)

sigmoid_steepness (float)

kernel_Gaussian(u)

Parameters:

u (float)

kernel_Gaussian_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Silverman(u)

Parameters:

u (float)

kernel_Quartic(u)

Parameters:

u (float)

kernel_Quartic_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel_Biweight(u)

Parameters:

u (float)

kernel_Triweight(u)

Parameters:

u (float)

kernel_Sinc(u)

Parameters:

u (float)

kernel_Wave(u)

Parameters:

u (float)

kernel_Wave_alt(u)

Parameters:

u (float)

kernel_Cosine(u)

Parameters:

u (float)

kernel_Cosine_alt(u, sensitivity)

Parameters:

u (float)

sensitivity (float)

kernel(u, select, alt_modificator)

wrapper for all standard kernel functions, see enum Kernel comments and function descriptions for usage szenarios and parameters

Parameters:

u (float)

select (series Kernel)

alt_modificator (float)

kernel_regression(src, bandwidth, kernel, exponential_distance, alt_modificator)

wrapper for kernel regression with all standard kernel functions, see enum Kernel comments for usage szenarios. performance optimized version using fixed bandwidth and target

Parameters:

src (float) : input data series

bandwidth (simple int) : sample window of nearest neighbours for the kernel to process

kernel (simple Kernel) : type of Kernel to use for processing, see Kernel enum or respective functions for more details

exponential_distance (simple bool) : if true this puts more emphasis on local / more recent values

alt_modificator (float) : see kernel functions for parameter descriptions. Mostly used to pronounce emphasis on local values or introduce a decay/dampening to the kernel output

GapDetectGap Severity Analysis Library

This library, GapDetect , simplifies the identification and evaluation of overnight gaps by leveraging statistical metrics such as standard deviation and percentage moves. It is ideal for detecting large abnormal gaps which may be used to modify how strategies may decide to enter or exit.

Key Features:

Overnight Gap Detection

Provides two core functions:

today : Computes the value of today's overnight gap.

todayPercent : Computes the percentage change for today's overnight gap.

Volatility Analysis

Includes functions for statistical gap analysis:

normal : Calculates the normal daily standard deviation of the overnight gap, filtering outliers using customizable thresholds.

normalPercent : Similar to normal , but for percentage-based gap moves.

Gap Severity Metric

severity : a positive or negative value that represents the ratio of the current overnight move compared to the standard deviation of previous ones.

Customizable Parameters

Supports custom session specifications, resolutions, and outlier thresholds.

lib_smcLibrary "lib_smc"

This is an adaptation of LuxAlgo's Smart Money Concepts indicator with numerous changes. Main changes include integration of object based plotting, plenty of performance improvements, live tracking of Order Blocks, integration of volume profiles to refine Order Blocks, and many more.

This is a library for developers, if you want this converted into a working strategy, let me know.

buffer(item, len, force_rotate)

Parameters:

item (float)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (int)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (Profile type from robbatt/lib_profile/32)

len (int)

force_rotate (bool)

swings(len)

INTERNAL: detect swing points (HH and LL) in given range

Parameters:

len (simple int) : range to check for new swing points

Returns: values are the price level where and if a new HH or LL was detected, else na

method init(this)

Namespace types: OrderBlockConfig

Parameters:

this (OrderBlockConfig)

method delete(this)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

method clear_broken(this, broken_buffer)

INTERNAL: delete internal order blocks box coordinates if top/bottom is broken

Namespace types: map

Parameters:

this (map)

broken_buffer (map)

Returns: any_bull_ob_broken, any_bear_ob_broken, broken signals are true if an according order block was broken/mitigated, broken contains the broken block(s)

create_ob(id, mode, start_t, start_i, top, end_t, end_i, bottom, break_price, early_confirmation_price, config, init_plot, force_overlay)

INTERNAL: set internal order block coordinates

Parameters:

id (int)

mode (int) : 1: bullish, -1 bearish block

start_t (int)

start_i (int)

top (float)

end_t (int)

end_i (int)

bottom (float)

break_price (float)

early_confirmation_price (float)

config (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

Returns: signals are true if an according order block was broken/mitigated

method align_to_profile(block, align_edge, align_break_price)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

align_edge (bool)

align_break_price (bool)

method create_profile(block, opens, tops, bottoms, closes, values, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

opens (array)

tops (array)

bottoms (array)

closes (array)

values (array)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

method create_profile(block, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

track_obs(swing_len, hh, ll, top, btm, bull_bos_alert, bull_choch_alert, bear_bos_alert, bear_choch_alert, min_block_size, max_block_size, config_bull, config_bear, init_plot, force_overlay, enabled, extend_blocks, clear_broken_buffer_before, align_edge_to_value_area, align_break_price_to_poc, profile_args_bull, profile_args_bear, use_soft_confirm, soft_confirm_offset, use_retracements_with_FVG_out)

Parameters:

swing_len (int)

hh (float)

ll (float)

top (float)

btm (float)

bull_bos_alert (bool)

bull_choch_alert (bool)

bear_bos_alert (bool)

bear_choch_alert (bool)

min_block_size (float)

max_block_size (float)

config_bull (OrderBlockConfig)

config_bear (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

enabled (bool)

extend_blocks (simple bool)

clear_broken_buffer_before (simple bool)

align_edge_to_value_area (simple bool)

align_break_price_to_poc (simple bool)

profile_args_bull (ProfileArgs type from robbatt/lib_profile/32)

profile_args_bear (ProfileArgs type from robbatt/lib_profile/32)

use_soft_confirm (simple bool)

soft_confirm_offset (float)

use_retracements_with_FVG_out (simple bool)

method draw(this, config, extend_only)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

config (OrderBlockConfig)

extend_only (bool)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: array

Parameters:

blocks (array)

config (OrderBlockConfig)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: map

Parameters:

blocks (map)

config (OrderBlockConfig)

method cleanup(this, ob_bull, ob_bear)

removes all Profiles that are older than the latest OrderBlock from this profile buffer

Namespace types: array

Parameters:

this (array type from robbatt/lib_profile/32)

ob_bull (OrderBlock)

ob_bear (OrderBlock)

_plot_swing_points(mode, x, y, show_swing_points, linecolor_swings, keep_history, show_latest_swings_levels, trail_x, trail_y, trend)

INTERNAL: plot swing points

Parameters:

mode (int) : 1: bullish, -1 bearish block

x (int) : x-coordingate of swing point to plot (bar_index)

y (float) : y-coordingate of swing point to plot (price)

show_swing_points (bool) : switch to enable/disable plotting of swing point labels

linecolor_swings (color) : color for swing point labels and lates level lines

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

show_latest_swings_levels (bool)

trail_x (int) : x-coordinate for latest swing point (bar_index)

trail_y (float) : y-coordinate for latest swing point (price)

trend (int) : the current trend 1: bullish, -1: bearish, to determine Strong/Weak Low/Highs

_pivot_lvl(mode, trend, hhll_x, hhll, super_hhll, filter_insignificant_internal_breaks)

INTERNAL: detect whether a structural level has been broken and if it was in trend direction (BoS) or against trend direction (ChoCh), also track the latest high and low swing points

Parameters:

mode (simple int) : detect 1: bullish, -1 bearish pivot points

trend (int) : current trend direction

hhll_x (int) : x-coordinate of newly detected hh/ll (bar_index)

hhll (float) : y-coordinate of newly detected hh/ll (price)

super_hhll (float) : level/y-coordinate of superior hhll (if this is an internal structure pivot level)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: coordinates of internal structure that has been broken (x,y): start of structure, (trail_x, trail_y): tracking hh/ll after structure break, (bos_alert, choch_alert): signal whether a structural level has been broken

_plot_structure(x, y, is_bos, is_choch, line_color, line_style, label_style, label_size, keep_history)

INTERNAL: plot structural breaks (BoS/ChoCh)

Parameters:

x (int) : x-coordinate of newly broken structure (bar_index)

y (float) : y-coordinate of newly broken structure (price)

is_bos (bool) : whether this structural break was in trend direction

is_choch (bool) : whether this structural break was against trend direction

line_color (color) : color for the line connecting the structural level and the breaking candle

line_style (string) : style (line.style_dashed/solid) for the line connecting the structural level and the breaking candle

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the structural level and the breaking candle

label_size (string) : size (size.small/tiny) for the label above/below the line connecting the structural level and the breaking candle

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure_values(length, super_hh, super_ll, filter_insignificant_internal_breaks)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: trend: direction 1:bullish -1:bearish, (bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up): whether and which level broke in a bullish direction, trailing high, (bbear_bos_alert, bear_choch_alert, tm_x, btm_y, trail_dn_x, trail_dn): same in bearish direction

structure_plot(trend, bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up, hh, bear_bos_alert, bear_choch_alert, btm_x, btm_y, trail_dn_x, trail_dn, ll, color_bull, color_bear, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history)

detect (and plot) structural breaks and the resulting new trend

Parameters:

trend (int) : crrent trend 1: bullish, -1: bearish

bull_bos_alert (bool) : if there was a bullish bos alert -> plot it

bull_choch_alert (bool) : if there was a bullish choch alert -> plot it

top_x (int) : latest shwing high x

top_y (float) : latest swing high y

trail_up_x (int) : trailing high x

trail_up (float) : trailing high y

hh (float) : if there was a higher high

bear_bos_alert (bool) : if there was a bearish bos alert -> plot it

bear_choch_alert (bool) : if there was a bearish chock alert -> plot it

btm_x (int) : latest swing low x

btm_y (float) : latest swing low y

trail_dn_x (int) : trailing low x

trail_dn (float) : trailing low y

ll (float) : if there was a lower low

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure(length, color_bull, color_bear, super_hh, super_ll, filter_insignificant_internal_breaks, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history, enabled)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

enabled (bool)

_check_equal_level(mode, len, eq_threshold, enabled)

INTERNAL: detect equal levels (double top/bottom)

Parameters:

mode (int) : detect 1: bullish/high, -1 bearish/low pivot points

len (int) : lookback period for equal level (swing point) detection

eq_threshold (float) : maximum price offset for a level to be considered equal

enabled (bool)

Returns: eq_alert whether an equal level was detected and coordinates of the first and the second level/swing point

_plot_equal_level(show_eq, x1, y1, x2, y2, label_txt, label_style, label_size, line_color, line_style, keep_history)

INTERNAL: plot equal levels (double top/bottom)

Parameters:

show_eq (bool) : whether to plot the level or not

x1 (int) : x-coordinate of the first level / swing point

y1 (float) : y-coordinate of the first level / swing point

x2 (int) : x-coordinate of the second level / swing point

y2 (float) : y-coordinate of the second level / swing point

label_txt (string) : text for the label above/below the line connecting the equal levels

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the equal levels

label_size (string) : size (size.tiny) for the label above/below the line connecting the equal levels

line_color (color) : color for the line connecting the equal levels (and it's label)

line_style (string) : style (line.style_dotted) for the line connecting the equal levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

equal_levels_values(len, threshold, enabled)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

enabled (bool) : whether detection is enabled

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels_plot(eqh_x1, eqh_y1, eqh_x2, eqh_y2, eql_x1, eql_y1, eql_x2, eql_y2, color_eqh, color_eql, show, keep_history)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

eqh_x1 (int) : coordinates of first point of equal high

eqh_y1 (float) : coordinates of first point of equal high

eqh_x2 (int) : coordinates of second point of equal high

eqh_y2 (float) : coordinates of second point of equal high

eql_x1 (int) : coordinates of first point of equal low

eql_y1 (float) : coordinates of first point of equal low

eql_x2 (int) : coordinates of second point of equal low

eql_y2 (float) : coordinates of second point of equal low

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels(len, threshold, color_eqh, color_eql, enabled, show, keep_history)

detect (and plot) equal levels (double top/bottom)

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

enabled (bool) : whether detection is enabled

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert) whether an equal high was detected, (eql_alert) same for equal lows

_detect_fvg(mode, enabled, o, h, l, c, filter_insignificant_fvgs, change_tf)

INTERNAL: detect FVG (fair value gap)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

enabled (bool) : whether detection is enabled

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

Returns: whether a new FVG was detected and its top/mid/bottom levels

_clear_broken_fvg(mode, upper_boxes, lower_boxes)

INTERNAL: clear mitigated FVGs (fair value gaps)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

upper_boxes (array) : array that stores the upper parts of the FVG boxes

lower_boxes (array) : array that stores the lower parts of the FVG boxes

_plot_fvg(mode, show, top, mid, btm, border_color, extend_box)

INTERNAL: plot (and clear broken) FVG (fair value gap)

Parameters:

mode (int) : plot 1: bullish, -1 bearish gap

show (bool) : whether plotting is enabled

top (float) : top level of fvg

mid (float) : center level of fvg

btm (float) : bottom level of fvg

border_color (color) : color for the FVG box

extend_box (int) : how many bars into the future the FVG box should be extended after detection

fvgs_values(o, h, l, c, filter_insignificant_fvgs, change_tf, enabled)

detect (and plot / clear broken) FVGs (fair value gaps), and return alerts and level values

Parameters:

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

enabled (bool) : whether detection is enabled

Returns: (bullish_fvg_alert, bull_top, bull_mid, bull_btm): whether a new bullish FVG was detected and its top/mid/bottom levels, (bearish_fvg_alert, bear_top, bear_mid, bear_btm): same for bearish FVGs

fvgs_plot(bullish_fvg_alert, bull_top, bull_mid, bull_btm, bearish_fvg_alert, bear_top, bear_mid, bear_btm, color_bull, color_bear, extend_box, show)

Parameters:

bullish_fvg_alert (bool)

bull_top (float)

bull_mid (float)

bull_btm (float)

bearish_fvg_alert (bool)

bear_top (float)

bear_mid (float)

bear_btm (float)

color_bull (color) : color for bullish FVG boxes

color_bear (color) : color for bearish FVG boxes

extend_box (int) : how many bars into the future the FVG box should be extended after detection

show (bool) : whether plotting is enabled

Returns: (bullish_fvg_alert, bull_top, bull_mid, bull_btm): whether a new bullish FVG was detected and its top/mid/bottom levels, (bearish_fvg_alert, bear_top, bear_mid, bear_btm): same for bearish FVGs

fvgs(o, h, l, c, filter_insignificant_fvgs, change_tf, color_bull, color_bear, extend_box, enabled, show)

detect (and plot / clear broken) FVGs (fair value gaps)

Parameters:

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

color_bull (color) : color for bullish FVG boxes

color_bear (color) : color for bearish FVG boxes

extend_box (int) : how many bars into the future the FVG box should be extended after detection

enabled (bool) : whether detection is enabled

show (bool) : whether plotting is enabled

Returns: (bullish_fvg_alert): whether a new bullish FVG was detected, (bearish_fvg_alert): same for bearish FVGs

OrderBlock

Fields:

id (series int)

dir (series int)

left_top (chart.point)

right_bottom (chart.point)

break_price (series float)

early_confirmation_price (series float)

ltf_high (array)

ltf_low (array)

ltf_volume (array)

plot (Box type from robbatt/lib_plot_objects/49)

profile (Profile type from robbatt/lib_profile/32)

trailing (series bool)

extending (series bool)

awaiting_confirmation (series bool)

touched_break_price_before_confirmation (series bool)

soft_confirmed (series bool)

has_fvg_out (series bool)

hidden (series bool)

broken (series bool)

OrderBlockConfig

Fields:

show (series bool)

show_last (series int)

show_id (series bool)

show_profile (series bool)

args (BoxArgs type from robbatt/lib_plot_objects/49)

txt (series string)

txt_args (BoxTextArgs type from robbatt/lib_plot_objects/49)

delete_when_broken (series bool)

broken_args (BoxArgs type from robbatt/lib_plot_objects/49)

broken_txt (series string)

broken_txt_args (BoxTextArgs type from robbatt/lib_plot_objects/49)

broken_profile_args (ProfileArgs type from robbatt/lib_profile/32)

use_profile (series bool)

profile_args (ProfileArgs type from robbatt/lib_profile/32)

BacktestLibraryLibrary "BacktestLibrary"

A library providing functions for equity calculation and performance metrics.

since(date, active)

: Calculates the number of candles since a specified date.

Parameters:

date (simple float) : (simple float): The starting date in timestamp format (e.g., input.time(timestamp()))

active (simple bool) : (simple bool): If true, counts the number of candles since the date; if false, returns 0.

Returns: (int): The number of candles since the specified date.

buy_and_hold(r, startDate)

: Calculates the Buy and Hold Equity from a specified date.

Parameters:

r (float) : (series float): Daily returns of the asset (e.g., 0.02 for 2% move).

startDate (simple float) : (simple float): Timestamp of the starting date for the equity calculation.

Returns: (float): Buy and Hold Equity of the asset from the specified date.

equity(sig, threshold, r, startDate, signals)

: Calculates the strategy's equity on a candle-by-candle basis.

Parameters:

sig (float) : (series float): Signal values; positive for long, negative for short.

threshold (simple float) : (simple float): Signal threshold for entering trades.

r (float) : (series float): Daily returns of the asset (e.g., 0.02 for 2% move).