Dual Keltner Channels Strategy [Eastgate3194]This strategy utilised 2 Keltner Channels to perform counter trade.

The strategy have 2 steps:

Long Position:

Step 1. Close price must cross under Outer Lower band of Keltner Channel.

Step 2. Close price cross over Inner Lower band of Keltner Channel.

Short Position:

Step 1. Close price must cross over Outer Upper band of Keltner Channel.

Step 2. Close price cross under Inner Upper band of Keltner Channel.

Ketidakstabilan

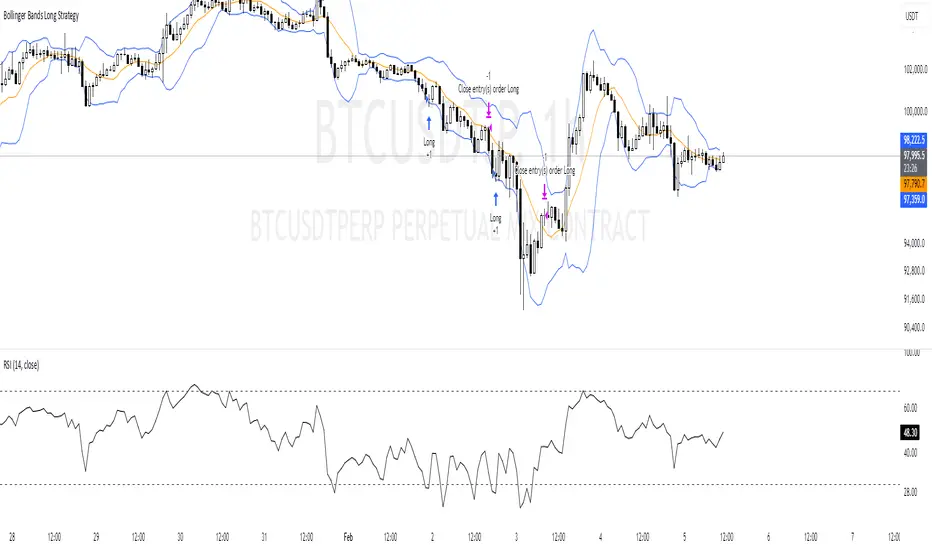

ThinkTech AI SignalsThink Tech AI Strategy

The Think Tech AI Strategy provides a structured approach to trading by integrating liquidity-based entries, ATR volatility thresholds, and dynamic risk management. This strategy generates buy and sell signals while automatically calculating take profit and stop loss levels, boasting a 64% win rate based on historical data.

Usage

The strategy can be used to identify key breakout and retest opportunities. Liquidity-based zones act as potential accumulation and distribution areas and may serve as future support or resistance levels. Buy and sell zones are identified using liquidity zones and ATR-based filters. Risk management is built-in, automatically calculating take profit and stop loss levels using ATR multipliers. Volume and trend filtering options help confirm directional bias using a 50 EMA and RSI filter. The strategy also allows for session-based trading, limiting trades to key market hours for higher probability setups.

Settings

The risk/reward ratio can be adjusted to define the desired stop loss and take profit calculations. The ATR length and threshold determine ATR-based breakout conditions for dynamic entries. Liquidity period settings allow for customized analysis of price structure for support and resistance zones. Additional trend and RSI filters can be enabled to refine trade signals based on moving averages and momentum conditions. A session filter is included to restrict trade signals to specific market hours.

Style

The strategy includes options to display liquidity lines, showing key support and resistance areas. The first 15-minute candle breakout zones can also be visualized to highlight critical market structure points. A win/loss statistics table is included to track trade performance directly on the chart.

This strategy is intended for descriptive analysis and should be used alongside other confluence factors. Optimize your trading process with Think Tech AI today!

DrNon Action Zone📈 Strategy Title:

DrNon Action Zone — EMA Cross with ATR Stop, % Take-Profit, Alerts & Date Range

⸻

🧠 Strategy Concept:

DrNon Action Zone is a long-only trend-following strategy that enters trades when momentum aligns with long-term trend confirmation. It uses:

• EMA Cross (Fast vs. Slow) to identify momentum shift

• Optional EMA Filter based on days to confirm that price is in a “trend zone”

• ATR-based trailing stop for adaptive risk management

• Percentage Take-Profit for reward targeting

• Date Range Filter for focused backtesting or event-based execution

It also includes alerts, visual signals, and full customization via inputs.

⸻

⚙️ Strategy Inputs Explained:

Input Name Description

Fast EMA Length Period of the short-term EMA used for crossover signals (default: 5)

Slow EMA Length Period of the long-term EMA used for crossover signals (default: 200)

ATR Period Period used to calculate the Average True Range (ATR)

ATR Multiplier Multiplies ATR value to calculate the trailing stop distance

Take-Profit % Percentage above entry price to exit the trade for profit

Use EMA Filter? If enabled, long entries require price to be above a customizable EMA filter

EMA Filter Days Number of days used for EMA filter (converted to bars based on chart timeframe)

Use Date Range? Enable or disable the date filter

Start Date / End Date Specify a custom range to apply the strategy

⸻

✅ Long Entry Conditions (The Action Zone):

A long trade is entered when:

1. EMA(Fast) crosses above EMA(Slow)

2. If EMA Filter is enabled, Close > EMA(Filter Days)

3. If Date Filter is enabled, current candle is within specified start and end dates

⸻

❌ Exit Conditions:

The strategy will close the position when either:

• Price drops to ATR-based trailing stop, OR

• Price reaches the Take-Profit % target

⸻

🛎️ Alerts:

Alert Name Trigger Condition

Long Entry Alert EMA cross and all filters passed (entry signal triggered)

Exit Alert Price hit ATR Stop or Take-Profit (exit signal triggered)

⸻

📊 Visual Elements:

• Yellow Line — Fast EMA

• Blue Line — Slow EMA

• Purple Line — EMA Filter (based on user-defined days)

• Red Line — ATR-based Trailing Stop

• Lime Line — Take-Profit Level

• Green Triangle — Long Entry Signal (on crossover)

⸻

🧪 Backtesting Tips:

• Adjust EMA Filter Days to simulate different trend conditions (e.g., 100d, 150d, 200d).

• Use ATR Multiplier to adapt the stop-loss to market volatility.

• Combine date filtering with known events (e.g., earnings, FOMC meetings).

• Test in multiple timeframes — 1H, 4H, or Daily for stronger signals.

FlexATRFlexATR: A Dynamic Multi-Timeframe Trading Strategy

Overview: FlexATR is a versatile trading strategy that dynamically adapts its key parameters based on the timeframe being used. It combines technical signals from exponential moving averages (EMAs) and the Relative Strength Index (RSI) with volatility-based risk management via the Average True Range (ATR). This approach helps filter out false signals while adjusting to varying market conditions — whether you’re trading on a daily chart, intraday charts (30m, 60m, or 5m), or even on higher timeframes like the 4-hour or weekly charts.

How It Works:

Multi-Timeframe Parameter Adaptation: FlexATR is designed to automatically adjust its indicator settings depending on the timeframe:

Daily and Weekly: On higher timeframes, the strategy uses longer periods for the fast and slow EMAs and standard periods for RSI and ATR to capture more meaningful trend confirmations while minimizing noise.

Intraday (e.g., 30m, 60m, 5m, 4h): The parameters are converted from “days” into the corresponding number of bars. For instance, on a 30-minute chart, a “day” might equal 48 bars. The preset values for a 30-minute chart have been slightly reduced (e.g., a fast EMA is set at 0.35 days instead of 0.4) to improve reactivity while maintaining robust filtering.

Signal Generation:

Entry Signals: The strategy enters long positions when the fast EMA crosses above the slow EMA and the RSI is above 50, and it enters short positions when the fast EMA crosses below the slow EMA with the RSI below 50. This dual confirmation helps ensure that signals are reliable.

Risk Management: The ATR is used to compute dynamic levels for stop loss and profit target:

Stop Loss: For a long position, the stop loss is placed at Price - (ATR × Stop Loss Multiplier). For a short position, it is at Price + (ATR × Stop Loss Multiplier).

Profit Target: The profit target is similarly set using the ATR multiplied by a designated profit multiplier.

Dynamic Trailing Stop: FlexATR further incorporates a dynamic trailing stop (if enabled) that adjusts according to the ATR. This trailing stop follows favorable price movements at a distance defined by a multiplier, locking in gains as the trend develops. The use of a trailing stop helps protect profits without requiring a fixed exit point.

Capital Allocation: Each trade is sized at 10% of the total equity. This percentage-based position sizing allows the strategy to scale with your account size. While the current setup assumes no leverage (a 1:1 exposure), the inherent design of the strategy means you can adjust the leverage externally if desired, with risk metrics scaling accordingly.

Visual Representation: For clarity and accessibility (especially for those with color vision deficiencies), FlexATR employs a color-blind friendly palette (the Okabe-Ito palette):

EMA Fast: Displayed in blue.

EMA Slow: Displayed in orange.

Stop Loss Levels: Rendered in vermilion.

Profit Target Levels: Shown in a distinct azzurro (light blue).

Benefits and Considerations:

Reliability: By requiring both EMA crossovers and an RSI confirmation, FlexATR filters out a significant amount of market noise, which reduces false signals at the expense of some delayed entries.

Adaptability: The automatic conversion of “day-based” parameters into bar counts for intraday charts means the strategy remains consistent across different timeframes.

Risk Management: Using the ATR for both fixed and trailing stops allows the strategy to adapt to changing market volatility, helping to protect your capital.

Flexibility: The strategy’s inputs are customizable via the input panel, allowing traders to fine-tune the parameters for different assets or market conditions.

Conclusion: FlexATR is designed as a balanced, adaptive strategy that emphasizes reliability and robust risk management across a variety of timeframes. While it may sometimes enter trades slightly later due to its filtering mechanism, its focus on confirming trends helps reduce the likelihood of false signals. This makes it particularly attractive for traders who prioritize a disciplined, multi-timeframe approach to capturing market trends.

ETH/USDT EMA Crossover Strategy - OptimizedStrategy Name: EMA Crossover Strategy for ETH/USDT

Description:

This trading strategy is designed for the ETH/USDT pair and is based on exponential moving average (EMA) crossovers combined with momentum and volatility indicators. The strategy uses multiple filters to identify high-probability signals in both bullish and bearish trends, making it suitable for traders looking to trade in trending markets.

Strategy Components

EMAs (Exponential Moving Averages):

EMA 200: Used to identify the primary trend. If the price is above the EMA 200, it is considered a bullish trend; if below, a bearish trend.

EMA 50: Acts as an additional filter to confirm the trend.

EMA 20 and EMA 50 Short: These short-term EMAs generate entry signals through crossovers. A bullish crossover (EMA 20 crosses above EMA 50 Short) is a buy signal, while a bearish crossover (EMA 20 crosses below EMA 50 Short) is a sell signal.

RSI (Relative Strength Index):

The RSI is used to avoid overbought or oversold conditions. Long trades are only taken when the RSI is above 30, and short trades when the RSI is below 70.

ATR (Average True Range):

The ATR is used as a volatility filter. Trades are only taken when there is sufficient volatility, helping to avoid false signals in quiet markets.

Volume:

A volume filter is used to confirm sufficient market participation in the price movement. Trades are only taken when volume is above average.

Strategy Logic

Long Trades:

The price must be above the EMA 200 (bullish trend).

The EMA 20 must cross above the EMA 50 Short.

The RSI must be above 30.

The ATR must indicate sufficient volatility.

Volume must be above average.

Short Trades:

The price must be below the EMA 200 (bearish trend).

The EMA 20 must cross below the EMA 50 Short.

The RSI must be below 70.

The ATR must indicate sufficient volatility.

Volume must be above average.

How to Use the Strategy

Setup:

Add the script to your ETH/USDT chart on TradingView.

Adjust the parameters according to your preferences (e.g., EMA periods, RSI, ATR, etc.).

Signals:

Buy and sell signals will be displayed directly on the chart.

Long trades are indicated with an upward arrow, and short trades with a downward arrow.

Risk Management:

Use stop-loss and take-profit orders in all trades.

Consider a risk-reward ratio of at least 1:2.

Backtesting:

Test the strategy on historical data to evaluate its performance before using it live.

Advantages of the Strategy

Trend-focused: The strategy is designed to trade in trending markets, increasing the probability of success.

Multiple filters: The use of RSI, ATR, and volume reduces false signals.

Adaptability: It can be adjusted for different timeframes, although it is recommended to test it on 5-minute and 15-minute charts for ETH/USDT.

Warnings

Sideways markets: The strategy may generate false signals in markets without a clear trend. It is recommended to avoid trading in such conditions.

Optimization: Make sure to optimize the parameters according to the market and timeframe you are using.

Risk management: Never trade without stop-loss and take-profit orders.

Author

Jose J. Sanchez Cuevas

Version

v1.0

iD EMARSI on ChartSCRIPT OVERVIEW

The EMARSI indicator is an advanced technical analysis tool that maps RSI values directly onto price charts. With adaptive scaling capabilities, it provides a unique visualization of momentum that flows naturally with price action, making it particularly valuable for FOREX and low-priced securities trading.

KEY FEATURES

1 PRICE MAPPED RSI VISUALIZATION

Unlike traditional RSI that displays in a separate window, EMARSI plots the RSI directly on the price chart, creating a flowing line that identifies momentum shifts within the context of price action:

// Map RSI to price chart with better scaling

mappedRsi = useAdaptiveScaling ?

median + ((rsi - 50) / 50 * (pQH - pQL) / 2 * math.min(1.0, 1/scalingFactor)) :

down == pQL ? pQH : up == pQL ? pQL : median - (median / (1 + up / down))

2 ADAPTIVE SCALING SYSTEM

The script features an intelligent scaling system that automatically adjusts to different market conditions and price levels:

// Calculate adaptive scaling factor based on selected method

scalingFactor = if scalingMethod == "ATR-Based"

math.min(maxScalingFactor, math.max(1.0, minTickSize / (atrValue/avgPrice)))

else if scalingMethod == "Price-Based"

math.min(maxScalingFactor, math.max(1.0, math.sqrt(100 / math.max(avgPrice, 0.01))))

else // Volume-Based

math.min(maxScalingFactor, math.max(1.0, math.sqrt(1000000 / math.max(volume, 100))))

3 MODIFIED RSI CALCULATION

EMARSI uses a specially formulated RSI calculation that works with an adaptive base value to maintain consistency across different price ranges:

// Adaptive RSI Base based on price levels to improve flow

adaptiveRsiBase = useAdaptiveScaling ? rsiBase * scalingFactor : rsiBase

// Calculate RSI components with adaptivity

up = ta.rma(math.max(ta.change(rsiSourceInput), adaptiveRsiBase), emaSlowLength)

down = ta.rma(-math.min(ta.change(rsiSourceInput), adaptiveRsiBase), rsiLengthInput)

// Improved RSI calculation with value constraint

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

4 MOVING AVERAGE CROSSOVER SYSTEM

The indicator creates a smooth moving average of the RSI line, enabling a crossover system that generates trading signals:

// Calculate MA of mapped RSI

rsiMA = ma(mappedRsi, emaSlowLength, maTypeInput)

// Strategy entries

if ta.crossover(mappedRsi, rsiMA)

strategy.entry("RSI Long", strategy.long)

if ta.crossunder(mappedRsi, rsiMA)

strategy.entry("RSI Short", strategy.short)

5 VISUAL REFERENCE FRAMEWORK

The script includes visual guides that help interpret the RSI movement within the context of recent price action:

// Calculate pivot high and low

pQH = ta.highest(high, hlLen)

pQL = ta.lowest(low, hlLen)

median = (pQH + pQL) / 2

// Plotting

plot(pQH, "Pivot High", color=color.rgb(82, 228, 102, 90))

plot(pQL, "Pivot Low", color=color.rgb(231, 65, 65, 90))

med = plot(median, style=plot.style_steplinebr, linewidth=1, color=color.rgb(238, 101, 59, 90))

6 DYNAMIC COLOR SYSTEM

The indicator uses color fills to clearly visualize the relationship between the RSI and its moving average:

// Color fills based on RSI vs MA

colUp = mappedRsi > rsiMA ? input.color(color.rgb(128, 255, 0), '', group= 'RSI > EMA', inline= 'up') :

input.color(color.rgb(240, 9, 9, 95), '', group= 'RSI < EMA', inline= 'dn')

colDn = mappedRsi > rsiMA ? input.color(color.rgb(0, 230, 35, 95), '', group= 'RSI > EMA', inline= 'up') :

input.color(color.rgb(255, 47, 0), '', group= 'RSI < EMA', inline= 'dn')

fill(rsiPlot, emarsi, mappedRsi > rsiMA ? pQH : rsiMA, mappedRsi > rsiMA ? rsiMA : pQL, colUp, colDn)

7 REAL TIME PARAMETER MONITORING

A transparent information panel provides real-time feedback on the adaptive parameters being applied:

// Information display

var table infoPanel = table.new(position.top_right, 2, 3, bgcolor=color.rgb(0, 0, 0, 80))

if barstate.islast

table.cell(infoPanel, 0, 0, "Current Scaling Factor", text_color=color.white)

table.cell(infoPanel, 1, 0, str.tostring(scalingFactor, "#.###"), text_color=color.white)

table.cell(infoPanel, 0, 1, "Adaptive RSI Base", text_color=color.white)

table.cell(infoPanel, 1, 1, str.tostring(adaptiveRsiBase, "#.####"), text_color=color.white)

BENEFITS FOR TRADERS

INTUITIVE MOMENTUM VISUALIZATION

By mapping RSI directly onto the price chart, traders can immediately see the relationship between momentum and price without switching between different indicator windows.

ADAPTIVE TO ANY MARKET CONDITION

The three scaling methods (ATR-Based, Price-Based, and Volume-Based) ensure the indicator performs consistently across different market conditions, volatility regimes, and price levels.

PREVENTS EXTREME VALUES

The adaptive scaling system prevents the RSI from generating extreme values that exceed chart boundaries when trading low-priced securities or during high volatility periods.

CLEAR TRADING SIGNALS

The RSI and moving average crossover system provides clear entry signals that are visually reinforced through color changes, making it easy to identify potential trading opportunities.

SUITABLE FOR MULTIPLE TIMEFRAMES

The indicator works effectively across multiple timeframes, from intraday to daily charts, making it versatile for different trading styles and strategies.

TRANSPARENT PARAMETER ADJUSTMENT

The information panel provides real-time feedback on how the adaptive system is adjusting to current market conditions, helping traders understand why the indicator is behaving as it is.

CUSTOMIZABLE VISUALIZATION

Multiple visualization options including Bollinger Bands, different moving average types, and customizable colors allow traders to adapt the indicator to their personal preferences.

CONCLUSION

The EMARSI indicator represents a significant advancement in RSI visualization by directly mapping momentum onto price charts with adaptive scaling. This approach makes momentum shifts more intuitive to identify and helps prevent the scaling issues that commonly affect RSI-based indicators when applied to low-priced securities or volatile markets.

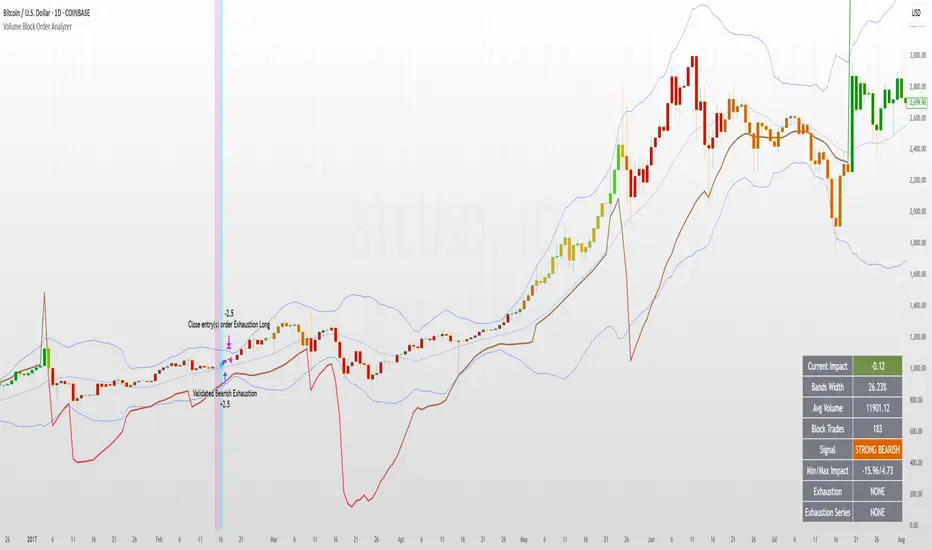

Volume Block Order AnalyzerCore Concept

The Volume Block Order Analyzer is a sophisticated Pine Script strategy designed to detect and analyze institutional money flow through large block trades. It identifies unusually high volume candles and evaluates their directional bias to provide clear visual signals of potential market movements.

How It Works: The Mathematical Model

1. Volume Anomaly Detection

The strategy first identifies "block trades" using a statistical approach:

```

avgVolume = ta.sma(volume, lookbackPeriod)

isHighVolume = volume > avgVolume * volumeThreshold

```

This means a candle must have volume exceeding the recent average by a user-defined multiplier (default 2.0x) to be considered a significant block trade.

2. Directional Impact Calculation

For each block trade identified, its price action determines direction:

- Bullish candle (close > open): Positive impact

- Bearish candle (close < open): Negative impact

The magnitude of impact is proportional to the volume size:

```

volumeWeight = volume / avgVolume // How many times larger than average

blockImpact = (isBullish ? 1.0 : -1.0) * (volumeWeight / 10)

```

This creates a normalized impact score typically ranging from -1.0 to 1.0, scaled by dividing by 10 to prevent excessive values.

3. Cumulative Impact with Time Decay

The key innovation is the cumulative impact calculation with decay:

```

cumulativeImpact := cumulativeImpact * impactDecay + blockImpact

```

This mathematical model has important properties:

- Recent block trades have stronger influence than older ones

- Impact gradually "fades" at rate determined by decay factor (default 0.95)

- Sustained directional pressure accumulates over time

- Opposing pressure gradually counteracts previous momentum

Trading Logic

Signal Generation

The strategy generates trading signals based on momentum shifts in institutional order flow:

1. Long Entry Signal: When cumulative impact crosses from negative to positive

```

if ta.crossover(cumulativeImpact, 0)

strategy.entry("Long", strategy.long)

```

*Logic: Institutional buying pressure has overcome selling pressure, indicating potential upward movement*

2. Short Entry Signal: When cumulative impact crosses from positive to negative

```

if ta.crossunder(cumulativeImpact, 0)

strategy.entry("Short", strategy.short)

```

*Logic: Institutional selling pressure has overcome buying pressure, indicating potential downward movement*

3. Exit Logic: Positions are closed when the cumulative impact moves against the position

```

if cumulativeImpact < 0

strategy.close("Long")

```

*Logic: The original signal is no longer valid as institutional flow has reversed*

Visual Interpretation System

The strategy employs multiple visualization techniques:

1. Color Gradient Bar System:

- Deep green: Strong buying pressure (impact > 0.5)

- Light green: Moderate buying pressure (0.1 < impact ≤ 0.5)

- Yellow-green: Mild buying pressure (0 < impact ≤ 0.1)

- Yellow: Neutral (impact = 0)

- Yellow-orange: Mild selling pressure (-0.1 < impact ≤ 0)

- Orange: Moderate selling pressure (-0.5 < impact ≤ -0.1)

- Red: Strong selling pressure (impact ≤ -0.5)

2. Dynamic Impact Line:

- Plots the cumulative impact as a line

- Line color shifts with impact value

- Line movement shows momentum and trend strength

3. Block Trade Labels:

- Marks significant block trades directly on the chart

- Shows direction and volume amount

- Helps identify key moments of institutional activity

4. Information Dashboard:

- Current impact value and signal direction

- Average volume benchmark

- Count of significant block trades

- Min/Max impact range

Benefits and Use Cases

This strategy provides several advantages:

1. Institutional Flow Detection: Identifies where large players are positioning themselves

2. Early Trend Identification: Often detects institutional accumulation/distribution before major price movements

3. Market Context Enhancement: Provides deeper insight than simple price action alone

4. Objective Decision Framework: Quantifies what might otherwise be subjective observations

5. Adaptive to Market Conditions: Works across different timeframes and instruments by using relative volume rather than absolute thresholds

Customization Options

The strategy allows users to fine-tune its behavior:

- Volume Threshold: How unusual a volume spike must be to qualify

- Lookback Period: How far back to measure average volume

- Impact Decay Factor: How quickly older trades lose influence

- Visual Settings: Labels and line width customization

This sophisticated yet intuitive strategy provides traders with a window into institutional activity, helping identify potential trend changes before they become obvious in price action alone.

Advanced Adaptive Grid Trading StrategyThis strategy employs an advanced grid trading approach that dynamically adapts to market conditions, including trend, volatility, and risk management considerations. The strategy aims to capitalize on price fluctuations in both rising (long) and falling (short) markets, as well as during sideways movements. It combines multiple indicators to determine the trend and automatically adjusts grid parameters for more efficient trading.

How it Works:

Trend Analysis:

Short, long, and super long Moving Averages (MA) to determine the trend direction.

RSI (Relative Strength Index) to identify overbought and oversold levels, and to confirm the trend.

MACD (Moving Average Convergence Divergence) to confirm momentum and trend direction.

Momentum indicator.

The strategy uses a weighted scoring system to assess trend strength (strong bullish, moderate bullish, strong bearish, moderate bearish, sideways).

Grid System:

The grid size (the distance between buy and sell levels) changes dynamically based on market volatility, using the ATR (Average True Range) indicator.

Grid density also adapts to the trend: in a strong trend, the grid is denser in the direction of the trend.

Grid levels are shifted depending on the trend direction (upwards in a bear market, downwards in a bull market).

Trading Logic:

The strategy opens long positions if the trend is bullish and the price reaches one of the lower grid levels.

It opens short positions if the trend is bearish and the price reaches one of the upper grid levels.

In a sideways market, it can open positions in both directions.

Risk Management:

Stop Loss for every position.

Take Profit for every position.

Trailing Stop Loss to protect profits.

Maximum daily loss limit.

Maximum number of positions limit.

Time-based exit (if the position is open for too long).

Risk-based position sizing (optional).

Input Options:

The strategy offers numerous settings that allow users to customize its operation:

Timeframe: The chart's timeframe (e.g., 1 minute, 5 minutes, 1 hour, 4 hours, 1 day, 1 week).

Base Grid Size (%): The base size of the grid, expressed as a percentage.

Max Positions: The maximum number of open positions allowed.

Use Volatility Grid: If enabled, the grid size changes dynamically based on the ATR indicator.

ATR Length: The period of the ATR indicator.

ATR Multiplier: The multiplier for the ATR to fine-tune the grid size.

RSI Length: The period of the RSI indicator.

RSI Overbought: The overbought level for the RSI.

RSI Oversold: The oversold level for the RSI.

Short MA Length: The period of the short moving average.

Long MA Length: The period of the long moving average.

Super Long MA Length: The period of the super long moving average.

MACD Fast Length: The fast period of the MACD.

MACD Slow Length: The slow period of the MACD.

MACD Signal Length: The period of the MACD signal line.

Stop Loss (%): The stop loss level, expressed as a percentage.

Take Profit (%): The take profit level, expressed as a percentage.

Use Trailing Stop: If enabled, the strategy uses a trailing stop loss.

Trailing Stop (%): The trailing stop loss level, expressed as a percentage.

Max Loss Per Day (%): The maximum daily loss, expressed as a percentage.

Time Based Exit: If enabled, the strategy exits the position after a certain amount of time.

Max Holding Period (hours): The maximum holding time in hours.

Use Risk Based Position: If enabled, the strategy calculates position size based on risk.

Risk Per Trade (%): The risk per trade, expressed as a percentage.

Max Leverage: The maximum leverage.

Important Notes:

This strategy does not guarantee profits. Cryptocurrency markets are volatile, and trading involves risk.

The strategy's effectiveness depends on market conditions and settings.

It is recommended to thoroughly backtest the strategy under various market conditions before using it live.

Past performance is not indicative of future results.

IU BBB(Big Body Bar) StrategyDESCRIPTION

The IU BBB (Big Body Bar) Strategy is a price action-based trading strategy that identifies high-momentum candles with significantly larger body sizes compared to the average. It enters trades when a strong bullish or bearish move occurs and manages risk using an ATR-based trailing stop-loss system.

USER INPUTS:

- Big Body Threshold – Defines how many times larger the candle body should be compared to the average body ( default is 4 ).

- ATR Length – The period for the Average True Range (ATR) used in the trailing stop-loss calculation ( default is 14 ).

- ATR Factor – Multiplier for ATR to determine the trailing stop distance ( default is 2 ).

LONG CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is higher than the opening price (bullish candle).

SHORT CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is lower than the opening price (bearish candle).

LONG EXIT:

- ATR-based trailing stop-loss dynamically adjusts, locking in profits as the price moves higher.

SHORT EXIT:

- ATR-based trailing stop-loss dynamically adjusts, securing profits as the price moves lower.

WHY IT IS UNIQUE:

- Unlike traditional momentum strategies, this system adapts to volatility by filtering trades based on relative candle size.

- It incorporates an ATR-based trailing stop-loss, ensuring risk management and profit protection.

- The strategy avoids choppy market conditions by only trading when significant momentum is present.

HOW USERS CAN BENEFIT FROM IT:

- Catch Strong Price Moves – The strategy helps traders enter trades when the market shows decisive momentum.

- Effective Risk Management – The ATR-based trailing stop ensures that winning trades remain profitable.

- Works Across Markets – Can be applied to stocks, forex, crypto, and indices with proper optimization.

- Fully Customizable – Users can adjust sensitivity settings to match their trading style and time frame.

IU Gap Fill StrategyThe IU Gap Fill Strategy is designed to capitalize on price gaps that occur between trading sessions. It identifies gaps based on a user-defined percentage threshold and executes trades when the price fills the gap within a day. This strategy is ideal for traders looking to take advantage of market inefficiencies that arise due to overnight or session-based price movements. An ATR-based trailing stop-loss is incorporated to dynamically manage risk and lock in profits.

USER INPUTS

Percentage Difference for Valid Gap - Defines the minimum gap size in percentage terms for a valid trade setup. ( Default is 0.2 )

ATR Length - Sets the lookback period for the Average True Range (ATR) calculation. (default is 14 )

ATR Factor - Determines the multiplier for the trailing stop-loss, helping in risk management. ( Default is 2.00 )

LONG CONDITION

A gap-up occurs, meaning the current session opens above the previous session’s close.

The price initially dips below the previous session's close but then recovers and closes above it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

SHORT CONDITION

A gap-down occurs, meaning the current session opens below the previous session’s close.

The price initially moves above the previous session’s close but then closes below it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

LONG EXIT

An ATR-based trailing stop-loss is set below the entry price and dynamically adjusts upwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

SHORT EXIT

An ATR-based trailing stop-loss is set above the entry price and dynamically adjusts downwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

WHY IT IS UNIQUE

Precision in Identifying Gaps - The strategy focuses on real price gaps rather than minor fluctuations.

Dynamic Risk Management - Uses ATR-based trailing stop-loss to secure profits while allowing the trade to run.

Versatility - Works on stocks, indices, forex, and any market that experiences session-based gaps.

Optimized Entry Conditions - Ensures entries are taken only when the price attempts to fill the gap, reducing false signals.

HOW USERS CAN BENEFIT FROM IT

Enhance Trade Timing - Captures high-probability trade setups based on market inefficiencies caused by gaps.

Minimize Risk - The ATR trailing stop-loss helps protect gains and limit losses.

Works in Different Market Conditions - Whether markets are trending or consolidating, the strategy adapts to potential gap fill opportunities.

Fully Customizable - Users can fine-tune gap percentage, ATR settings, and stop-loss parameters to match their trading style.

Dual SuperTrend w VIX Filter - Strategy [presentTrading]Hey everyone! Haven't been here for a long time. Been so busy again in the past 2 months. I recently started working on analyzing the combination of trend strategy and VIX, but didn't get outstanding results after a few tries. Sharing this tool with all of you in case you have better insights.

█ Introduction and How it is Different

The Dual SuperTrend with VIX Filter Strategy combines traditional trend following with market volatility analysis. Unlike conventional SuperTrend strategies that focus solely on price action, this experimental system incorporates VIX (Volatility Index) as an adaptive filter to create a more context-aware trading approach. By analyzing where current volatility stands relative to historical norms, the strategy adjusts to different market environments rather than applying uniform logic across all conditions.

BTCUSD 6hr Long Short Performance

█ Strategy, How it Works: Detailed Explanation

🔶 Dual SuperTrend Core

The strategy uses two SuperTrend indicators with different sensitivity settings:

- SuperTrend 1: Length = 13, Multiplier = 3.5

- SuperTrend 2: Length = 8, Multiplier = 5.0

The SuperTrend calculation follows this process:

1. ATR = Average of max(High-Low, |High-PreviousClose|, |Low-PreviousClose|) over 'length' periods

2. UpperBand = (High+Low)/2 - (Multiplier * ATR)

3. LowerBand = (High+Low)/2 + (Multiplier * ATR)

Trend direction is determined by:

- If Close > previous LowerBand, Trend = Bullish (1)

- If Close < previous UpperBand, Trend = Bearish (-1)

- Otherwise, Trend = previous Trend

🔶 VIX Analysis Framework

The core innovation lies in the VIX analysis system:

1. Statistical Analysis:

- VIX Mean = SMA(VIX, 252)

- VIX Standard Deviation = StdDev(VIX, 252)

- VIX Z-Score = (Current VIX - VIX Mean) / VIX StdDev

2. **Volatility Bands:

- Upper Band 1 = VIX Mean + (2 * VIX StdDev)

- Upper Band 2 = VIX Mean + (3 * VIX StdDev)

- Lower Band 1 = VIX Mean - (2 * VIX StdDev)

- Lower Band 2 = VIX Mean - (3 * VIX StdDev)

3. Volatility Regimes:

- "Very Low Volatility": VIX < Lower Band 1

- "Low Volatility": Lower Band 1 ≤ VIX < Mean

- "Normal Volatility": Mean ≤ VIX < Upper Band 1

- "High Volatility": Upper Band 1 ≤ VIX < Upper Band 2

- "Extreme Volatility": VIX ≥ Upper Band 2

4. VIX Trend Detection:

- VIX EMA = EMA(VIX, 10)

- VIX Rising = VIX > VIX EMA

- VIX Falling = VIX < VIX EMA

Local performance:

🔶 Entry Logic Integration

The strategy combines trend signals with volatility filtering:

Long Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bullish (trend = 1)

- AND selected VIX filter condition must be satisfied

Short Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bearish (trend = -1)

- AND selected VIX filter condition must be satisfied

Available VIX filter rules include:

- "Below Mean + SD": VIX < Lower Band 1

- "Below Mean": VIX < VIX Mean

- "Above Mean": VIX > VIX Mean

- "Above Mean + SD": VIX > Upper Band 1

- "Falling VIX": VIX < VIX EMA

- "Rising VIX": VIX > VIX EMA

- "Any": No VIX filtering

█ Trade Direction

The strategy allows testing in three modes:

1. **Long Only:** Test volatility effects on uptrends only

2. **Short Only:** Examine volatility's impact on downtrends only

3. **Both (Default):** Compare how volatility affects both trend directions

This enables comparative analysis of how volatility regimes impact bullish versus bearish markets differently.

█ Usage

Use this strategy as an experimental framework:

1. Form a hypothesis about how volatility affects trend reliability

2. Configure VIX filters to test your specific hypothesis

3. Analyze performance across different volatility regimes

4. Compare results between uptrends and downtrends

5. Refine your volatility filtering approach based on results

6. Share your findings with the trading community

This framework allows you to investigate questions like:

- Are uptrends more reliable during rising or falling volatility?

- Do downtrends perform better when volatility is above or below its historical average?

- Should different volatility filters be applied to long vs. short positions?

█ Default Settings

The default settings serve as a starting point for exploration:

SuperTrend Parameters:

- SuperTrend 1 (Length=13, Multiplier=3.5): More responsive to trend changes

- SuperTrend 2 (Length=8, Multiplier=5.0): More selective filter requiring stronger trends

VIX Analysis Settings:

- Lookback Period = 252: Establishes a full market cycle for volatility context

- Standard Deviation Bands = 2 and 3 SD: Creates statistically significant regime boundaries

- VIX Trend Period = 10: Balances responsiveness with noise reduction

Default VIX Filter Selection:

- Long Entry: "Above Mean" - Tests if uptrends perform better during above-average volatility

- Short Entry: "Rising VIX" - Tests if downtrends accelerate when volatility is increasing

Feel Free to share your insight below!!!

[3Commas] Turtle StrategyTurtle Strategy

🔷 What it does: This indicator implements a modernized version of the Turtle Trading Strategy, designed for trend-following and automated trading with webhook integration. It identifies breakout opportunities using Donchian channels, providing entry and exit signals.

Channel 1: Detects short-term breakouts using the highest highs and lowest lows over a set period (default 20).

Channel 2: Acts as a confirmation filter by applying an offset to the same period, reducing false signals.

Exit Channel: Functions as a dynamic stop-loss (wait for candle close), adjusting based on market structure (default 10 periods).

Additionally, traders can enable a fixed Take Profit level, ensuring a systematic approach to profit-taking.

🔷 Who is it for:

Trend Traders: Those looking to capture long-term market moves.

Bot Users: Traders seeking to automate entries and exits with bot integration.

Rule-Based Traders: Operators who prefer a structured, systematic trading approach.

🔷 How does it work: The strategy generates buy and sell signals using a dual-channel confirmation system.

Long Entry: A buy signal is generated when the close price crosses above the previous high of Channel 1 and is confirmed by Channel 2.

Short Entry: A sell signal occurs when the close price falls below the previous low of Channel 1, with confirmation from Channel 2.

Exit Management: The Exit Channel acts as a trailing stop, dynamically adjusting to price movements. To exit the trade, wait for a full bar close.

Optional Take Profit (%): Closes trades at a predefined %.

🔷 Why it’s unique:

Modern Adaptation: Updates the classic Turtle Trading Strategy, with the possibility of using a second channel with an offset to filter the signals.

Dynamic Risk Management: Utilizes a trailing Exit Channel to help protect gains as trades move favorably.

Bot Integration: Automates trade execution through direct JSON signal communication with your DCA Bots.

🔷 Considerations Before Using the Indicator:

Market & Timeframe: Best suited for trending markets; higher timeframes (e.g., H4, D1) are recommended to minimize noise.

Sideways Markets: In choppy conditions, breakouts may lead to false signals—consider using additional filters.

Backtesting & Demo Testing: It is crucial to thoroughly backtest the strategy and run it on a demo account before risking real capital.

Parameter Adjustments: Ensure that commissions, slippage, and position sizes are set accurately to reflect real trading conditions.

🔷 STRATEGY PROPERTIES

Symbol: BINANCE:ETHUSDT (Spot).

Timeframe: 4h.

Test Period: All historical data available.

Initial Capital: 10000 USDT.

Order Size per Trade: 1% of Capital, you can use a higher value e.g. 5%, be cautious that the Max Drawdown does not exceed 10%, as it would indicate a very risky trading approach.

Commission: Binance commission 0.1%, adjust according to the exchange being used, lower numbers will generate unrealistic results. By using low values e.g. 5%, it allows us to adapt over time and check the functioning of the strategy.

Slippage: 5 ticks, for pairs with low liquidity or very large orders, this number should be increased as the order may not be filled at the desired level.

Margin for Long and Short Positions: 100%.

Indicator Settings: Default Configuration.

Period Channel 1: 20.

Period Channel 2: 20.

Period Channel 2 Offset: 20.

Period Exit: 10.

Take Profit %: Disable.

Strategy: Long & Short.

🔷 STRATEGY RESULTS

⚠️Remember, past results do not guarantee future performance.

Net Profit: +516.87 USDT (+5.17%).

Max Drawdown: -100.28 USDT (-0.95%).

Total Closed Trades: 281.

Percent Profitable: 40.21%.

Profit Factor: 1.704.

Average Trade: +1.84 USDT (+1.80%).

Average # Bars in Trades: 29.

🔷 How to Use It:

🔸 Adjust Settings:

Select your asset and timeframe suited for trend trading.

Adjust the periods for Channel 1, Channel 2, and the Exit Channel to align with the asset’s historical behavior. You can visualize these channels by going to the Style tab and enabling them.

For example, if you set Channel 2 to 40 with an offset of 40, signals will take longer to appear but will aim for a more defined trend.

Experiment with different values, a possible exit configuration is using 20 as well. Compare the results and adjust accordingly.

Enable the Take Profit (%) option if needed.

🔸Results Review:

It is important to check the Max Drawdown. This value should ideally not exceed 10% of your capital. Consider adjusting the trade size to ensure this threshold is not surpassed.

Remember to include the correct values for commission and slippage according to the symbol and exchange where you are conducting the tests. Otherwise, the results will not be realistic.

If you are satisfied with the results, you may consider automating your trades. However, it is strongly recommended to use a small amount of capital or a demo account to test proper execution before committing real funds.

🔸Create alerts to trigger the DCA Bot:

Verify Messages: Ensure the message matches the one specified by the DCA Bot.

Multi-Pair Configuration: For multi-pair setups, enable the option to add the symbol in the correct format.

Signal Settings: Enable the option to receive long or short signals (Entry | TP | SL), copy and paste the messages for the DCA Bots configured.

Alert Setup:

When creating an alert, set the condition to the indicator and choose "alert() function call only".

Enter any desired Alert Name.

Open the Notifications tab, enable Webhook URL, and paste the Webhook URL.

For more details, refer to the section: "How to use TradingView Custom Signals".

Finalize Alerts: Click Create, you're done! Alerts will now be sent automatically in the correct format.

🔷 INDICATOR SETTINGS

Period Channel 1: Period of highs and lows to trigger signals

Period Channel 2: Period of highs and lows to filter signals

Offset: Move Channel 2 to the right x bars to try to filter out the favorable signals.

Period Exit: It is the period of the Donchian channel that is used as trailing for the exits.

Strategy: Order Type direction in which trades are executed.

Take Profit %: When activated, the entered value will be used as the Take Profit in percentage from the entry price level.

Use Custom Test Period: When enabled signals only works in the selected time window. If disabled it will use all historical data available on the chart.

Test Start and End: Once the Custom Test Period is enabled, here you select the start and end date that you want to analyze.

Check Messages: Check Messages: Enable this option to review the messages that will be sent to the bot.

Entry | TP | SL: Enable this options to send Buy Entry, Take Profit (TP), and Stop Loss (SL) signals.

Deal Entry and Deal Exit: Copy and paste the message for the deal start signal and close order at Market Price of the DCA Bot. This is the message that will be sent with the alert to the Bot, you must verify that it is the same as the bot so that it can process properly.

DCA Bot Multi-Pair: You must activate it if you want to use the signals in a DCA Bot Multi-pair in the text box you must enter (using the correct format) the symbol in which you are creating the alert, you can check the format of each symbol when you create the bot.

👨🏻💻💭 We hope this tool helps enhance your trading. Your feedback is invaluable, so feel free to share any suggestions for improvements or new features you'd like to see implemented.

__

The information and publications within the 3Commas TradingView account are not meant to be and do not constitute financial, investment, trading, or other types of advice or recommendations supplied or endorsed by 3Commas and any of the parties acting on behalf of 3Commas, including its employees, contractors, ambassadors, etc.

Bollinger Bands by Abu ElyasBollinger Bands with Adjustable Stop Loss (Long-Only)

This strategy uses a Bollinger Band breakout approach to enter long positions and incorporates an adjustable stop loss for risk management.

Below is an overview of the logic, parameters, and usage instructions.

1. Bollinger Bands Logic

Basis (Middle Band): A moving average (type selectable by the user) of the chosen source, typically the closing price.

Upper Band: The basis plus a specified number of standard deviations (user-defined multiplier).

Lower Band: The basis minus the same number of standard deviations.

2. Entry Triggers

The strategy enters a long position when the close price rises above the upper Bollinger Band , suggesting a potential bullish breakout.

This logic is only applied within a user-specified date range (adjustable in the strategy’s inputs).

3. Exit Triggers

1. Bollinger Band Exit:

If the close price drops below the lower Bollinger Band , the strategy closes the position, indicating a loss of bullish momentum.

2. Stop Loss Exit:

A default 8% stop loss is set, which automatically exits the trade if the close falls 8% below the entry price.

This stop-loss percentage is adjustable from the strategy’s settings, allowing users to tailor risk based on their preferences.

3. Date Range:

If the current bar is outside of the specified start/end dates, the strategy will also exit any open positions.

4. Position Sizing & Other Settings

1- Position Size:

By default, the script uses 100% of account equity for each trade.

2- Commissions & Slippage:

Commission is set to 0%, and slippage is set to 3 ticks.

3- Timeframe Handling:

You can select a custom timeframe or leave it blank to use the chart’s timeframe.

5. Customization

1. Bollinger Bands Parameters:

Length of the moving average, type of moving average (SMA, EMA, etc.), and the standard deviation multiplier can be adjusted.

2. Stop Loss (%)

The default stop loss of 8% can be changed in the script’s input settings to any percentage you prefer.

3. Date Filter:

Modify the start/end dates to control the historical period over which the strategy executes trades.

6. Notes & Best Practices

1- No Short Trades:

This is a long‐only strategy. It will either be in a long position or flat (no open position).

2- Risk Management:

An 8% stop loss may or may not align with your personal risk tolerance. Always adjust according to market conditions and your own trading style.

3- Market Gaps & Volatility:

In highly volatile markets, slippage or gaps can cause the actual exit price to be worse than the intended stop-loss level.

4- Test Thoroughly:

Backtest on different timeframes and market conditions. No single strategy works in all scenarios.

7. Disclaimer

Educational Use Only: This script is for informational and illustrative purposes and should not be considered financial advice.

No Guarantee of Profit: Past performance does not guarantee future results. Trading involves substantial risk, and it is possible to lose more than your initial investment.

Consult a Professional: Always consult a qualified financial advisor before making investment decisions.

Use this script as a foundation and personalize it based on your trading style, tolerance for drawdowns, and market conditions.

Enhanced BarUpDn StrategyEnhanced BarUpDn Strategy

The Enhanced BarUpDn Strategy is a refined price action-based trading approach that identifies market trends and reversals using bar formations. It focuses on detecting bullish and bearish momentum by analyzing consecutive price bars and key support/resistance levels.

Key Features:

✅ Trend Confirmation – Uses a combination of bar patterns and indicators (e.g., moving averages, RSI) to confirm momentum shifts.

✅ Entry Signals – A buy signal is triggered when an "Up Bar" (higher high, higher low) follows a bullish setup; a sell signal when a "Down Bar" (lower high, lower low) confirms bearish momentum.

✅ Enhanced Filters – Incorporates volume analysis and additional conditions to reduce false signals.

✅ Stop-Loss & Risk Management – Uses recent swing highs/lows for stop placement and dynamic trailing stops for maximizing gains.

IronBot v4IronBot v4 – Trading Strategy Overview

1. Quick Context

IronBot v4 is a trading strategy designed for users who want a simple yet effective approach to reading the markets. It uses a combination of Fibonacci retracement levels, custom logic triggers, and innovative modules (EMA validation, Iron Impulse Shield and Iron Auto Volume Detector) to identify potential entry and exit points, strengthening the strategy’s detection of sudden market volatility or shifts in trading volume.

2. Theoretical Details

Fibonacci Analysis

The script identifies recent market highs and lows, then calculates key Fibonacci levels (high- and low-based). These levels can help confirm potential reversals or trends.

EMA Option

When enabled, the exponential moving average (EMA) offers additional validation for trade entries. If the current price remains above a certain EMA threshold, long positions may be favored; conversely, if it stays below the EMA, short positions may be initiated.

IIS (Iron Impulse Shield)

IIS helps to filter out risky trades by measuring recent price shocks or surges. If an extreme movement is detected, the strategy may temporarily disable longs or shorts to avoid false signals.

IAVD (Iron Auto Volume Detector)

This functionality automatically detects the average market volume over a defined period (regardless of the market, since it relies on real data). When entering a position, it ensures that overall volume is high enough to confirm a genuinely active, robust market. By providing an additional filter, it can strengthen the decision-making process whenever the market’s participation level is in question.

Panel

IronBot v4 displays a real-time backtest panel that summarizes the selected configuration (including the current pair, analysis window, enabled filters), as well as showing net profit, applicable exchange fees, country taxes, and the final net balance. This gives traders an immediate overview of strategy performance and risk metrics.

What Pinescript Adds Visually

The script plots:

Fibonacci levels (highlighting potential reversal zones)

Trend lines indicating bullish (green) or bearish (red) lean

Optional EMA line

Optional Fibonacci forecast lines for anticipating future moves

Automatic labeling of entry, take-profit, and stop-loss levels, indicating the profit percentage of each trade.

3. Explanation of Inputs

The strategy exposes multiple inputs that can be toggled or configured by the user:

Analysis Window : Dictates how many bars to consider for high/low calculations and the fib retracement thresholds.

TRADES

Display TP/SL: For displaying Take profits and Stop loss.

Display Forecast: When enabled, this feature calculates and projects possible future Fibonacci retracements using historical data, helping traders anticipate potential upcoming trade setups.

Leverage: Only used for the Panel and not for trades. Lets you amplify your position size; higher leverage increases potential gains but also heightens risk. TradingView strategy is using properties for doing this.

Exchange Maker Fees & Exchange Taker Fees: Only used for the Panel and not for trades. Define the percentage cost applied by your exchange for maker and taker trades, respectively. These fees are accounted for in final profit calculations of the Panel.

Country Tax: Only used for the Panel and not for trades. Specifies a tax percentage to be deducted from net profits.

STOP LOSS and TAKE PROFITS

Stop-Loss & Take-Profit Parameters: Controls the percentage distances at which the strategy will exit positions. Additionally, you can configure up to four distinct take-profit levels (TP1 through TP4). Each level should be higher target than the previous one, and you can assign a specific percentage of the total position to close at each TP, ensuring the sum equals 100%. A break-even feature is also available when multiple TPs are used.

EMA

EMA (Exponential Moving Average) Option: When enabled, the strategy opens long trades only if the current price is above the specified EMA length, and opens short trades only if it is below that threshold.

PANELS

Show Panel: For displaying the backtest integrated panel.

IRON IMPULSE SHIELD (IIS)

IIS (Iron Impulse Shield) Option: When enabled, IIS continuously monitors recent price volatility depending on the analysis window set. If the market experiences an extreme surge or drop beyond a specified threshold, IIS temporarily blocks new long or short positions.

IRON AUTO VOLUME DETECTOR (IAVD)

IAVD (Iron Auto Volume Detector) Option: When enabled, it continuously measures the average market volume over a special period, irrespective of the specific trading pair. This ensures that IronBot v4 focuses on markets with robust participation, reducing the likelihood of entering trades during low-liquidity conditions.

By changing these values, IronBot v4 reacts differently to market structure and risk management requirements. Stop-loss and take-profit levels will adjust accordingly, while advanced filters (like EMA or IIS) influence when trades can open.

4. TradingView Strategy Properties

IronBot v4 uses the built-in TradingView “strategy” functionality. In particular:

Order Placement: The code calls strategy.entry() and strategy.close() for direct orders, ensuring signals are sent immediately (no limit orders are used). This helps connect with exchange signal bots for automated execution.

Initial Capital: The code uses initial capital defined in properties for calculating Net balance in the integrated panel.

On bar close: This strategy fill orders on bar close.

Pyramiding: This strategy can take only 1 successive trade in the same direction

Be careful to configure your leverage input depending on your strategy properties.

5. Visualization

5. Purpose & Disclaimer

This script is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Always confirm your own risk tolerance and consult a financial professional before placing live trades. Trading leveraged products can involve substantial risk of loss.

3 Red / 3 Green Strategy with Volatility CheckStrategy Name: 3 Red / 3 Green Strategy with Volatility Check by AlgoTradeKit

Overview

This long-only strategy is designed for daily bars on NASDAQ (or similar instruments) and combines simple price action with a volatility filter. It “tells it like it is” – enter when the market shows weakness, but only in sufficiently volatile conditions, and exit either on signs of a reversal or after a set number of days.

Entry Conditions

- Price Action :

Enter a long position when there are 3 consecutive red days (each day's close is below its open).

- Volatility Filter :

The entry is allowed only if the current ATR (Average True Range) calculated over the specified ATR Period (default 12) is greater than its 30-day simple moving average. This ensures the market has enough volatility to justify the trade.

Exit Conditions

- Reversal Signal :

Exit the long position when 3 consecutive green days occur (each day's close is above its open), signaling a potential reversal.

- Time Limit :

Regardless of market conditions, any open trade is closed if it reaches the Maximum Trade Duration (default 22 days). This helps limit exposure during stagnant or unfavorable market conditions.

- You can toggle the three-green-day exit if you want to isolate the time-based exit.

Input Parameters

- Maximum Trade Duration (days): Default is 22 days.

- ATR Period: Default is 12.

- Use 3 Green Days Exit: Toggle to enable or disable the three-green-day exit condition.

How It Works

1. Entry: The strategy monitors daily price action for 3 consecutive down days. When this occurs and if the market is volatile enough (current ATR > 30-day ATR average), it opens a long position.

2. Exit: The position is closed if the price action reverses with 3 consecutive up days or if the trade has been open for the maximum allowed duration - i.e. use it on daily chart.

Risk Management

- The built-in maximum trade duration prevents trades from lingering too long in a non-trending or consolidating market.

- The volatility filter helps ensure that trades are only taken when there is sufficient price movement, potentially increasing the odds of a meaningful move.

Disclaimer

This strategy is provided “as is” without any warranties. It is essential to backtest and validate the performance on your specific instrument and market conditions before deploying live capital. Trading involves significant risk, and you should adjust parameters to match your risk tolerance.

Test and tweak this strategy to see if it fits your trading style and market conditions. Happy trading!

Smart MA Crossover BacktesterSmart MA Crossover Backtester - Strategy Overview

Strategy Name: Smart MA Crossover Backtester

Published on: TradingView

Applicable Markets: Works well on crypto (tested profitably on ETH)

Strategy Concept

The Smart MA Crossover Backtester is an improved Moving Average (MA) crossover strategy that incorporates a trend filter and an ATR-based stop loss & take profit mechanism for better risk management. It aims to capture trends efficiently while reducing false signals by only trading in the direction of the long-term trend.

Core Components & Logic

Moving Averages (MA) for Entry Signals

Fast Moving Average (9-period SMA)

Slow Moving Average (21-period SMA)

A trade signal is generated when the fast MA crosses the slow MA.

Trend Filter (200-period SMA)

Only enters long positions if price is above the 200-period SMA (bullish trend).

Only enters short positions if price is below the 200-period SMA (bearish trend).

This helps in avoiding counter-trend trades, reducing whipsaws.

ATR-Based Stop Loss & Take Profit

Uses the Average True Range (ATR) with a multiplier of 2 to calculate stop loss.

Risk-Reward Ratio = 1:2 (Take profit is set at 2x ATR).

This ensures dynamic stop loss and take profit levels based on market volatility.

Trading Rules

✅ Long Entry (Buy Signal):

Fast MA (9) crosses above Slow MA (21)

Price is above the 200 MA (bullish trend filter active)

Stop Loss: Below entry price by 2× ATR

Take Profit: Above entry price by 4× ATR

✅ Short Entry (Sell Signal):

Fast MA (9) crosses below Slow MA (21)

Price is below the 200 MA (bearish trend filter active)

Stop Loss: Above entry price by 2× ATR

Take Profit: Below entry price by 4× ATR

Why This Strategy Works Well for Crypto (ETH)?

🔹 Crypto markets are highly volatile – ATR-based stop loss adapts dynamically to market conditions.

🔹 Long-term trend filter (200 MA) ensures trading in the dominant direction, reducing false signals.

🔹 Risk-reward ratio of 1:2 allows for profitable trades even with a lower win rate.

This strategy has been tested on Ethereum (ETH) and has shown profitable performance, making it a strong choice for crypto traders looking for trend-following setups with solid risk management. 🚀

Universal Strategy | QuantEdgeBIntroducing the Universal Strategy by QuantEdgeB

The Universal Strategy | QuantEdgeB is a dynamic, multi-indicator strategy designed to operate across various asset classes with precision and adaptability. This cutting-edge system utilizes four sophisticated methodologies, each integrating advanced trend-following, volatility filtering, and normalization techniques to provide robust signals. Its modular architecture and customizable features ensure suitability for diverse market conditions, empowering traders with data-driven decision-making tools. Its adaptability to different price behaviors and volatility levels makes it a robust and versatile tool, equipping traders with data-driven confidence in their market decisions.

_______

1. Core Methodologies and Features

1️⃣ DEMA ATR

Strength : Fast responsiveness to trend shifts.

The double exponential moving average is inherently aggressive, designed to reduce lag and quickly identify early signs of trend reversals or breakout opportunities. ATR bands add a volatility-sensitive layer, dynamically adjusting the breakout thresholds to match current market conditions, ensuring it remains responsive while filtering out noise

How It Fits :

This indicator is the first responder, providing early signals of potential trend shifts. While its aggressiveness can result in quick entries, it may occasionally overreact in noisy markets. This is where the smoother indicators step in to confirm signals.

2️⃣ Gaussian - VIDYA ATR (Variable Index Dynamic Average)

Strength : Smooth, adaptive trend identification.

Unlike DEMA, VIDYA adapts to market volatility through its standard deviation-based formula, making it smoother and less reactive to short-term fluctuations. ATR filtering ensures the indicator remains effective in volatile markets by dynamically adjusting its sensitivity.

How It Fits :

The smoother complement to DEMA ATR, VIDYA ATR filters out false signals from minor price movements. It provides confirmation for the trends identified by DEMA ATR, ensuring entries are based on robust, sustained price movements.

3️⃣ VIDYA Loop Trend Scoring

Strength : Historical trend scoring for consistent momentum detection.

This module evaluates the relative strength of trends by comparing the current VIDYA value to its historical values over a defined range. The loop mechanism provides a trend confidence score, quantifying the momentum behind price movements.

How It Fits :

VIDYA For-Loop adds a quantitative measure of trend strength, ensuring that trades are backed by sustained momentum. It balances the early signals from DEMA ATR and the smoothness of VIDYA ATR by providing a statistical check on the underlying trend.

4️⃣ Median SD with Normalization

Strength : Precision in breakout detection and market normalization.

The Median price serves as a robust baseline for detecting breakouts and reversals.

SD bands expand dynamically during periods of high volatility, making the indicator particularly effective for spotting strong trends or breakout opportunities. Normalization ensures the indicator adapts seamlessly across different assets and timeframes, providing consistent performance.

How It Fits :

The Median SD module provides final confirmation by focusing on price breakouts and market normalization. While the other indicators focus on momentum and trend strength, Median SD emphasizes precision, ensuring entries align with significant price movements rather than random fluctuations.

_______

2. How The Single Components Work Together

1️⃣ Balance of Speed and Smoothness :

The strategy blends quick responsiveness (DEMA ATR) with smooth and adaptive confirmation (VIDYA ATR & For-Loop), ensuring timely reactions without overreacting to market fluctuations. Median SD with Normalization refines breakout detection and stabilizes performance across assets using statistical anchors like price median and standard deviation.

Adaptability to Market Dynamics:

2️⃣ Adaptability to Market Dynamics :

The indicators complement each other seamlessly in trending markets, with the DEMA ATR and Median SD with Normalization quickly identifying shifts and confirming sustained momentum. In volatile or choppy markets, normalization and SD bands work together to filter out noise and reduce false signals, ensuring precise entries and exits. Meanwhile, the For-Loop scoring and Gaussian-Filtered VIDYA ATR focus on providing smoother, more reliable trend detection, offering consistent performance regardless of market conditions.

_______

3. Scoring and Signal Confirmation

The Universal Strategy consolidates signals from all four methodologies, calculating a Trend Probability Index (TPI). The four core indicators operate independently but contribute to a unified TPI, enabling highly adaptive behavior across asset classes.

- Each methodology generates a trend score: 1 for bullish trends, -1 for bearish trends.

- The TPI averages the scores, creating a unified signal.

- Long Position: Triggered when the TPI exceeds the long threshold (default: 0).

- Short Position: Triggered when the TPI falls below the short threshold (default: 0).

The strategy’s customizable settings allow traders to tailor its behavior to different market conditions—whether smoother trends in low-volatility assets or quick reaction to high-volatility breakouts. The long and short thresholds can be fine-tuned to match a trader’s risk tolerance and preferences.

_______

4. Use Cases:

The Universal Strategy | QuantEdgeB is designed to excel across a wide range of trading scenarios, thanks to its modular architecture and adaptability. Whether you're navigating trending, volatile, or range-bound markets, this strategy offers robust tools to enhance your decision-making. Below are the key use cases for its application:

1️⃣ Trend Trading

The strategy’s Gaussian-Filtered DEMA ATR and VIDYA ATR modules are perfect for identifying and riding sustained trends.

Ideal For: Traders looking to capture long-term momentum or position trades.

2️⃣ Breakout and Volatility-Based Strategies

With its Median SD with Normalization, the strategy excels in detecting volatility breakouts and significant price movements.

Ideal For: Traders aiming to capitalize on sudden market movements, especially in assets like cryptocurrencies and commodities.

3️⃣ Momentum and Strength Assessment

By generating a trend confidence score, the VIDYA For-Loop quantifies momentum strength—helping traders distinguish temporary spikes from sustainable trends.

Ideal For: Swing traders and those focusing on momentum-driven setups.

4️⃣ Adaptability Across Multiple Assets

The strategy’s robust framework ensures it performs consistently across different assets and timeframes.

Ideal For: Traders managing diverse portfolios or shifting between asset classes.

5️⃣ Backtesting and Optimization

Built-in backtesting and equity visualization tools make this strategy ideal for testing and refining parameters in real-world conditions.

• How It Helps: The strategy equity curve and metrics table offer a clear picture of performance, helping traders identify optimal settings for their chosen market and timeframe.

• Ideal For: Traders focused on rigorous testing and long-term optimization.

_______

5. Signal Composition Table:

This table presents a real-time breakdown of each indicator’s trend score (+1 bullish, -1 bearish) alongside the final aggregated signal. By visualizing the contribution of each methodology, traders gain greater transparency, confidence, and clarity in identifying long or short opportunities.

6. Customized Settings:

1️⃣ General Inputs

• Strategy Long Threshold (Lu): 0

• Strategy Short Threshold (Su): 0

2️⃣ Gaussian Filter

• Gaussian Length (len_FG): 4

• Gaussian Source (src_FG): close

• Gaussian Sigma (sigma_FG): 2.0

3️⃣ DEMA ATR

• DEMA Length (len_D): 30

• DEMA Source (src_D): close

• ATR Length (atr_D): 14

• ATR Multiplier (mult_D): 1.0

4️⃣ VIDYA ATR

• VIDYA Length (len_V1): 9

• SD Length (len_VHist1): 30

• ATR Length (atr_V): 14

• ATR Multiplier (mult_V): 1.7

5️⃣ VIDYA For-Loop

• VIDYA Length (len_V2): 2

• SD Length (len_VHist2): 5

• VIDYA Source (src_V2): close

• Start Loop (strat_loop): 1

• End Loop (end_loop): 60

• Long Threshold (long_t): 40

• Short Threshold (short_t): 8

6️⃣ Median SD

• Median Length (len_m): 24

• Normalized Median Length (len_msd): 50

• SD Length (SD_len): 32

• Long SD Weight (w1): 0.98

• Short SD Weight (w2): 1.02

• Long Normalized Smooth (smooth_long): 1

• Short Normalized Smooth (smooth_short): 1

Conclusion

The Universal Strategy | QuantEdgeB is a meticulously crafted, multi-dimensional trading system designed to thrive across diverse market conditions and asset classes. By combining Gaussian-Filtered DEMA ATR, VIDYA ATR, VIDYA For-Loop, and Median SD with Normalization, this strategy provides a seamless balance between speed, smoothness, and adaptability. Each component complements the others, ensuring traders benefit from early responsiveness, trend confirmation, momentum scoring, and breakout precision.

Its modular structure ensures versatility across trending, volatile, and consolidating markets. Whether applied to equities, forex, commodities, or crypto, it delivers data-driven precision while minimizing reliance on randomness, reinforcing confidence in decision-making.

With built-in backtesting tools, traders can rigorously evaluate performance under real-world conditions, while customization options allow fine-tuning for specific market dynamics and individual trading styles.

Why It Stands Out

The Universal Strategy | QuantEdgeB isn’t just a trading algorithm—it’s a comprehensive framework that empowers traders to make confident, informed decisions in the face of ever-changing market conditions. Its emphasis on precision, reliability, and transparency makes it a powerful tool for both professional and retail traders seeking consistent performance and enhanced risk management.

_______

🔹 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Stochastic-Dynamic Volatility Band ModelThe Stochastic-Dynamic Volatility Band Model is a quantitative trading approach that leverages statistical principles to model market volatility and generate buy and sell signals. The strategy is grounded in the concepts of volatility estimation and dynamic market regimes, where the core idea is to capture price fluctuations through stochastic models and trade around volatility bands.

Volatility Estimation and Band Construction

The volatility bands are constructed using a combination of historical price data and statistical measures, primarily the standard deviation (σ) of price returns, which quantifies the degree of variation in price movements over a specific period. This methodology is based on the classical works of Black-Scholes (1973), which laid the foundation for using volatility as a core component in financial models. Volatility is a crucial determinant of asset pricing and risk, and it plays a pivotal role in this strategy's design.

Entry and Exit Conditions

The entry conditions are based on the price’s relationship with the volatility bands. A long entry is triggered when the price crosses above the lower volatility band, indicating that the market may have been oversold or is experiencing a reversal to the upside. Conversely, a short entry is triggered when the price crosses below the upper volatility band, suggesting overbought conditions or a potential market downturn.

These entry signals are consistent with the mean reversion theory, which asserts that asset prices tend to revert to their long-term average after deviating from it. According to Poterba and Summers (1988), mean reversion occurs due to overreaction to news or temporary disturbances, leading to price corrections.

The exit condition is based on the number of bars that have elapsed since the entry signal. Specifically, positions are closed after a predefined number of bars, typically set to seven bars, reflecting a short-term trading horizon. This exit mechanism is in line with short-term momentum trading strategies discussed in literature, where traders capitalize on price movements within specific timeframes (Jegadeesh & Titman, 1993).

Market Adaptability

One of the key features of this strategy is its dynamic nature, as it adapts to the changing volatility environment. The volatility bands automatically adjust to market conditions, expanding in periods of high volatility and contracting when volatility decreases. This dynamic adjustment helps the strategy remain robust across different market regimes, as it is capable of identifying both trend-following and mean-reverting opportunities.

This dynamic adaptability is supported by the adaptive market hypothesis (Lo, 2004), which posits that market participants evolve their strategies in response to changing market conditions, akin to the adaptive nature of biological systems.

References:

Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637-654.

Bollinger, J. (1980). Bollinger on Bollinger Bands. Wiley.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Lo, A. W. (2004). The Adaptive Markets Hypothesis: Market Efficiency from an Evolutionary Perspective. Journal of Portfolio Management, 30(5), 15-29.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Volatility Arbitrage Spread Oscillator Model (VASOM)The Volatility Arbitrage Spread Oscillator Model (VASOM) is a systematic approach to capitalizing on price inefficiencies in the VIX futures term structure. By analyzing the differential between front-month and second-month VIX futures contracts, we employ a momentum-based oscillator (Relative Strength Index, RSI) to signal potential market reversion opportunities. Our research builds upon existing financial literature on volatility risk premia and contango/backwardation dynamics in the volatility markets (Zhang & Zhu, 2006; Alexander & Korovilas, 2012).

Volatility derivatives have become essential tools for managing risk and engaging in speculative trades (Whaley, 2009). The Chicago Board Options Exchange (CBOE) Volatility Index (VIX) measures the market’s expectation of 30-day forward-looking volatility derived from S&P 500 option prices (CBOE, 2018). Term structures in VIX futures often exhibit contango or backwardation, depending on macroeconomic and market conditions (Alexander & Korovilas, 2012).