Low Volatility Breakout + TP/SL Levels█ OVERVIEW

"Low Volatility Breakout + TP/SL Levels" is a breakout indicator designed to detect and trade breakouts from periods of low volatility (consolidation). Unlike classic strategies based on fixed support/resistance levels, this indicator dynamically identifies consolidations characterized by small candle bodies and only generates a signal when the breakout occurs with a large, decisive candle. It also automatically plots 3 Take Profit levels and a Stop Loss (with two calculation modes), making it a complete breakout trading tool.

█ CONCEPTS

The strongest market moves most often start after a prolonged period of very low volatility — when candles become small and the market "falls asleep". The indicator first detects such consolidations (small bodies for at least X bars), draws a box around them, and then waits for a breakout with a candle significantly larger than the average. Additional filters (e.g., the box height cannot exceed the average candle body by too much) eliminate false consolidations and volatility traps. Immediately after the breakout, TP1, TP2, TP3, and SL levels are plotted.

█ FEATURES

Dynamic detection of low-volatility consolidations

- candles with small bodies (< average body × consolidationMultiplier)

- minimum number of bars in consolidation: confirmBars (default 5)

Automatic drawing of consolidation boxes

- green (bullish) or red (bearish) with transparent background (85)

- adjustable border thickness (border_width 1–5)

- box height filter (boxHeightMultiplier, default 6.0 × average body) – removes overly stretched/false consolidations

Breakout conditions

- current candle must be larger than average body × threshold (default 1.5)

- must be the largest candle in the entire consolidation

- must close above the highest high (long) or below the lowest low (short)

Breakout signals

- small green triangles below the bar (long)

- small red triangles above the bar (short)

Automatic Take Profit and Stop Loss levels (drawn 5 bars forward)

- two calculation modes:

• Candle Multiplier – based on average true range (high-low) over tp_sl_length period

• Percentage – fixed percentage from breakout close price (percentages must be manually adjusted to the asset and timeframe)

- 3 TP levels (default 2×, 3×, 4× or 2%, 3%, 4%)

- 1 SL level (default 2× or 1.5%)

Live TP/SL price table (top-right corner)

- displays exact current values of SL, TP1, TP2, TP3 immediately after each new signal

- colors identical to drawn lines (red background for SL, green for TP levels)

- updates automatically with every new breakout

Built-in alerts

- “Bullish Breakout Alert” and “Bearish Breakout Alert”

█ HOW TO USE

Add the indicator to your TradingView chart → Indicators → search “Low Volatility Breakout + TP/SL Levels”.

After each valid breakout you will immediately see:

- the colored box

- signal triangle

- horizontal TP/SL lines

- updated table in the top-right corner showing precise price levels for the current trade

Key settings to adjust:

Consolidation Settings

- Volatility Window (length) – period for average body calculation (default 20)

- Consolidation Multiplier – how small bodies must be to count as consolidation (default 2.0)

- Breakout Multiplier – minimum size of breakout candle (default 1.5)

- Box Height Multiplier – maximum allowed box height (default 6.0)

- Min Consolidation Bars – minimum bars required (default 5)

Risk Management Settings

- Choose TP/SL mode: Candle Multiplier or Percentage

- Adjust TP1–3 and SL multipliers/percentages to match your risk management style

Signal interpretation:

- Green triangle below bar + green box + green TP levels in table = long signal

- Red triangle above bar + red box + red SL level in table = short signal

- Boxes remain on chart until broken — they highlight accumulation/distribution zones

█ APPLICATIONS

- Trading breakouts from consolidation on all markets and timeframes

- Recommended to trade in the direction of the higher-timeframe trend or with additional confirmations (e.g., key level breaks). Aggressive mode (trading both directions) is also possible — provided box and TP/SL settings are properly optimized

- Experiment with different TP/SL ratios — higher reward-to-risk setups (e.g., SL 1×, TP3 6–8×) with lower win rate are often more profitable in the long run

- Strongly encourage testing various box parameters (consolidationMultiplier, boxHeightMultiplier, confirmBars) — small changes can dramatically affect signal frequency and quality

█ NOTES

Always test and optimize parameters for the specific instrument and timeframe.

Ketidakstabilan

Multi Condition Stock Screener & Alert SystemMulti Condition Stock Screener & Strategy Builder

This script is a comprehensive Stock Screener and Strategy Builder designed to scan predefined groups of stocks (specifically focused on BIST/Istanbul Stock Exchange symbols) or a custom list of symbols based on user-defined technical conditions.

It allows users to combine multiple technical indicators to create complex entry or exit conditions without writing code. The script iterates through a list of symbols and triggers alerts when the conditions are met.

Key Features

• Custom Strategy Building: Users can define up to 6 separate conditions. • Logical Operators: Conditions can be linked using logical operators (AND / OR) to create flexible strategies. • Predefined Groups: Includes 14 groups of stocks (covering BIST symbols) for quick scanning. • Custom Scanner: Users can select the "SPECIAL" group to manually input up to 40 custom symbols to scan. • Directional Scanning: Capable of scanning for both Buy/Long and Sell/Short signals. • Alert Integration: Generates JSON-formatted alert messages suitable for webhook integrations (e.g., sending notifications to Telegram bots).

Supported Indicators for Conditions

The script utilizes built-in ta.* functions to calculate the following indicators:

• MA (Moving Average): Supports EMA, SMA, RMA, and WMA. • RSI (Relative Strength Index) • CCI (Commodity Channel Index) • ATR (Average True Range) • BBW (Bollinger Bands Width) • ADX (Average Directional Index) • MFI (Money Flow Index) • MOM (Momentum)

How it Works

The script uses request.security() to fetch data for the selected group of symbols based on the current timeframe. It evaluates the user-defined logic (Condition 1 to 6) for each symbol.

• Comparison Logic: You can compare an indicator against a value (e.g., RSI > 50 ) or against another indicator (e.g., MA1 CrossOver MA2 ). • Signal Generation: If the logical result is TRUE based on the "AND/OR" settings, a visual label is plotted on the chart, and an alert condition is triggered.

Alert Configuration

The script produces a JSON output containing the Ticker, Signal Type, Period, and Price. This is optimized for users who want to parse alerts programmatically or send them to external messaging apps via webhooks.

Disclaimer This tool is for informational purposes only and does not constitute financial advice. Since it uses request.security across multiple symbols, please allow time for the script to load data on the chart.

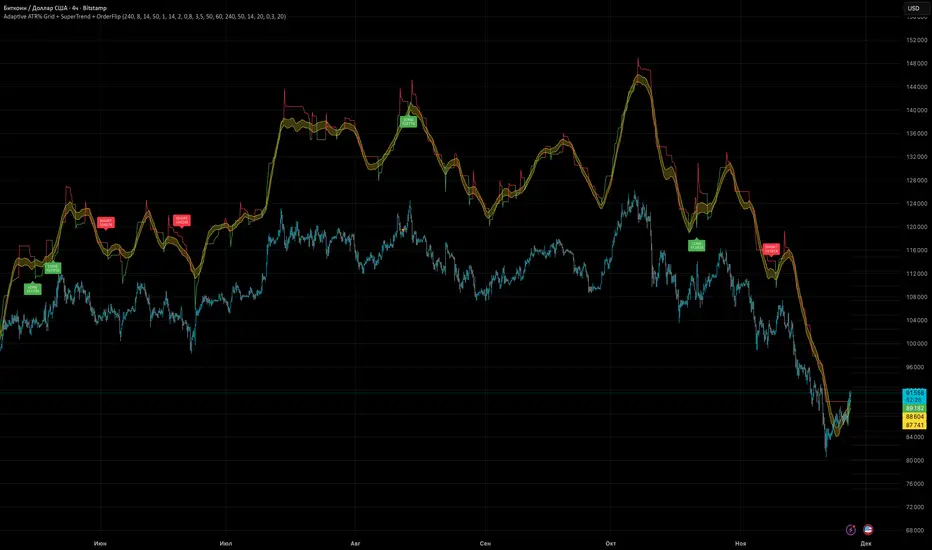

Adaptive ATR% Grid + SuperTrend + OrderFlipDescription:

This indicator combines multiple technical analysis tools to identify key price levels and trading signals:

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

OrderFlip – identifies price reversal points relative to a moving average with ATR-based sensitivity, optionally filtered by OBV and DMI.

MTF Confirmation – multi-timeframe trend verification using EMA to reduce false signals.

Signal Labels – "LONG" and "SHORT" labels appear on the chart with an offset from the price for better visibility.

JSON Alerts – ready-to-use format for automated alerts, including price, SuperTrend direction, Fair Zone, and ATR%.

Features:

Fully compatible with Pine Script v6

Lines and signals are fixed on the chart, do not shift with new bars

Configurable grid, ATR, SuperTrend, and filter parameters

Works with MTF analysis and classic indicators (OBV/DMI)

Usage:

Best used with additional indicators and risk management strategies. ATR% Grid is ideal for both positional trading and intraday setups.

перевод на русский

Описание:

Этот индикатор объединяет несколько методов технического анализа для выявления ключевых уровней цены и сигналов на покупку/продажу:

Сетка ATR% (ATR% Grid) – автоматическое построение уровней поддержки и сопротивления на основе текущей цены и волатильности (ATR). Позволяет видеть потенциальные цели и зоны входа/выхода.

SuperTrend – классический трендовый индикатор с адаптивным множителем ATR, который корректируется на основе средней волатильности.

OrderFlip – определение моментов разворота цены относительно скользящей средней с учетом ATR, с возможностью фильтрации по OBV и DMI.

MTF-подтверждение – проверка направления тренда на нескольких таймфреймах с помощью EMA, чтобы снизить ложные сигналы.

Сигнальные метки – на графике появляются "LONG" и "SHORT" с отступом от цены для наглядности.

JSON Alerts – готовый формат для автоматических уведомлений, включающий цену, направление SuperTrend, Fair Zone и ATR%.

Особенности:

Поддержка Pine Script v6

Линии и сигналы закреплены на графике, не двигаются при обновлении свечей

Настраиваемые параметры сетки, ATR, SuperTrend и фильтров

Совместимость с MTF-анализом и классическими индикаторами OBV/DMI

Рекомендации:

Используйте в сочетании с другими индикаторами и стратегиями управления риском. Сетка ATR% отлично подходит для позиционной торговли и интрадей.

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

Adaptive MACD PROAdaptive MACD PRO

Highlights structural momentum changes using dynamic normalization of MACD and Signal.

Phase Momentum Core

Adds directional confirmation based on short-term phase behavior.

Visual Output

• MACD & Signal lines with trend-based coloring

• Adaptive histogram reflecting momentum strength

• Fixed-position Buy/Sell dots at predefined levels

• AutoCalib dots on MACD_z threshold crossings

• Optional HUD panel displaying calibration levels and MACD_z

Features

• Selectable MA types (EMA, SMA, KAMA)

• Z-score normalization

• ATR-based volatility weighting

• Higher timeframe alignment

• Auto-calibration with SAFE / AGGRESSIVE modes

• Unified long/short triggers

• Full bar-coloring control

• Works on all assets and timeframes

The full source code is visible and may be modified or extended.

This script is intended for technical analysis and research only.

This indicator is published as a free, open-source script with full visible code.

QLC - Gibaum 1.0 QLC - Gibaum 1.0

Good for Leverage AND Short - 5 to 20 minutes >70%.

Gibaum The Beast

Little Black Guy suffers in america

Monitor Posición Bollinger Multi-TFThis indicator provides a comprehensive dashboard that allows you to monitor the price position relative to Bollinger Bands across 7 different timeframes simultaneously, without the need to switch charts.

It uses the %B (Percent B) logic to normalize the price position, giving you an instant "Heatmap" view of the market state (Overbought/Oversold) from the 1-minute chart up to the Weekly chart.

Key Features:

Multi-Timeframe Monitoring: Watch 1m, 5m, 15m, 1h, 4h, Daily, and Weekly timeframes in a single panel.

Dynamic Color Coding:

Dark Red: Price breaking above the Upper Band (>100%).

Light Red: Price near the Upper Band (Resistance zone).

Gray: Price in the neutral middle zone.

Light Green: Price near the Lower Band (Support zone).

Dark Green: Price breaking below the Lower Band (<0%).

Trend Arrows: Indicates momentum (▲ or ▼) based on the previous candle's position.

Current Timeframe Highlight: Automatically highlights the row corresponding to your current chart view in orange.

Fully Customizable: Adjust Bollinger settings (Length, Mult), choose your preferred timeframes, and change the table position/size.

Movable Panel: Includes X/Y offset settings to prevent the table from blocking price action or menu buttons.

How to Use:

Add the indicator to your chart.

Use the dashboard to spot confluence across timeframes.

Example: If 15m, 1H, and 4H are all showing Red, the asset is likely overextended to the upside.

Example: If the lower timeframes are turning Green while the higher timeframes remain Gray/Bullish, it might indicate a pullback opportunity.

Settings:

Bollinger Config: Length (20) and Multiplier (2.0) by default.

Timeframes: Select the 7 specific TFs you want to track.

Visuals: Change table position, text size, and offset coordinates.

This tool is essential for scalpers and day traders who need situational awareness across multiple fractals instantly.

Institutional Valuation SuiteStandard volatility indicators often fail on long-term growth charts because they measure volatility in dollars rather than percentages. This causes bands to break or become irrelevant during exponential price moves (e.g., Bitcoin going from $1,000 to $100,000).

The Institutional Valuation Suite solves this by utilising Geometric (Log-Normal) Standard Deviation. This allows the model to adapt to the asset's price scale, providing accurate valuation zones regardless of price magnitude.

The model functions as a mean-reversion tool, visualizing price as an elastic band anchored to a "Fair Value" baseline. It identifies when the asset is statistically overextended (Bubble/FOMO) or undervalued (Deep Discount).

Key Features

1. Log-Normal Math Engine

Geometric Mode (Default): Calculates volatility in percentage terms. Essential for Crypto and Growth Stocks.

Arithmetic Mode: Available for Forex or range-bound assets where linear standard deviation is preferred.

2. Sentiment Heat map

Visualises valuation directly on the candles to remove interpretation bias.

GREEN: Deep Value / Accumulation Zone (< -0.5σ).

ORANGE: Overvalued / FOMO Zone (> 2.0σ).

RED: Speculative Bubble Zone (> 3.0σ).

3. Reversion Signals

"VALUE RECLAIM": Triggers when price re-enters the bottom band from below, filtering out "falling knife" scenarios.

"TOP EXIT": Triggers when price breaks down from the speculative top zone.

4. Statistical Dashboard

Displays the real-time Z-Score to quantify how "stretched" the price is relative to its baseline.

> 3.0: Statistical Anomaly (Top).

< -0.5: Statistical Discount (Bottom).

Optimisation Cheat Sheet

The "Cycle Length" input determines the lookback period for the baseline. Recommended settings:

Crypto Macro: 200 (Approx. 4 Years).

Altcoins: 100 (Approx. 2 Years).

Stocks (S&P 500): 50 (1 Year Trend).

Day Trading: Set "Timeframe Lock" to "Chart".

Technical Note

This indicator uses strict offset logic (`barmerge.lookahead_on`) to ensure historical consistency. The signals displayed on historical bars match exactly what would have appeared in real-time.

*Disclaimer: This script provides statistical analysis based on historical volatility and does not constitute financial advice.*

Compression Breakout [30min 65+33 EMA]Compression Breakout

by GhostMMXM (inspired by Chris Cady & Steidlmayer Market Profile principles)

This indicator automates the exact compression-to-displacement setup that veteran CBOT floor trader and Market Profile pioneer Chris Cady describes in interviews and his work with Peter Steidlmayer.

Core idea

Chris Cady uses two simple moving averages on the 30-minute chart — a 33-period and a 65-period — to visually detect when the market falls into “balance” (compression). When both lines go almost perfectly flat for several bars, the market is in a low-volatility, high-consensus state — the calm before a violent vertical breakout.

What this script does

• Detects when both the 33 EMA and 65 EMA are virtually flat (user-adjustable sensitivity)

• Requires a minimum of 6 consecutive flat bars (adjustable) before declaring compression

• Draws a light-grey background + live-updating box showing the detecting compression

• Triggers only on the first strong displacing bar that:

– closes entirely above the compression high OR entirely below the compression low

– has a range ≥ 1.5× the average bar range inside the compression zone (adjustable)

• Plots a clear “LONG Cady Break” or “SHORT Cady Break” label on the breakout bar

• Fires a clean alert instantly usable on entire watchlists:

BTC → Compression LONG breakout!

ES1! → Compression SHORT breakout!

Designed for 30-minute charts (BTC, ETH, SOL, NQ, CL, GC, etc.) but works on any timeframe.

Perfect for traders who want to catch the highest-conviction vertical moves that Chris Cady has traded for decades with only a few contracts scaled in aggressively on the break.

Settings

• Minimum flat bars for compression (default 6)

• Max % slope to be considered flat (default 0.08 %)

• Minimum range multiplier vs compression average (default 1.5×)

Enjoy the cleanest, most mechanical version of Chris Cady’s famous compression breakout strategy available on TradingView.

Happy trading!

able MACD Overview

Purpose: The indicator combines the traditional MACD (Moving Average Convergence Divergence) with a short-term “forecast” (projection) of MACD/histogram values to give early warning of momentum changes.

Typical outputs:

MACD line (fastEMA − slowEMA)

Signal line (EMA of MACD)

Histogram (MACD − signal)

Forecasted MACD or histogram projected N bars ahead

Optional buy/sell markers and alert conditions

Add the indicator to TradingView (Installation)

Open TradingView and the chart you want to apply the indicator to.

Click “Pine Editor” at the bottom of the chart.

Copy the contents of able_macd_forecast.pine into the Pine Editor window.

Click “Add to chart” (or Save then Add to chart). If it’s a study, it will appear on the chart below price.

If you plan to re-use the script, click Save and give it a meaningful name.

Inputs / Parameters (typical) Note: exact input names may differ in your script. Replace the names below with the script’s input labels when you inspect it.

Source: price source for calculations (close, hl2, etc.).

Fast Length: length for the fast EMA (commonly 12).

Slow Length: length for the slow EMA (commonly 26).

Signal Length: length for the MACD signal EMA (commonly 9).

Forecast Length / Horizon: how many bars ahead the script projects the MACD/histogram (e.g., 1–5).

Forecast Method / Smoothing: choice of projection method (linear regression, EMA extrapolation, simple slope * N, etc.) if available.

Histogram Thresholds: numeric thresholds to emphasize significant momentum (optional).

Show Forecast: toggle on/off the forecast plot.

Alerts On/Off toggles: enable or disable alert conditions baked into the indicator.

Visual / Style settings: colors, plot thickness, histogram style (columns/areas), show labels, show buy/sell arrows.

How the indicator is typically calculated (summary)

MACD line = EMA(source, fast) − EMA(source, slow)

Signal line = EMA(MACD line, signal length)

Histogram = MACD − Signal

Forecast = method-specific short-term projection of MACD or histogram (for example: extend the last slope forward, apply linear regression to MACD values and extrapolate N bars, or apply an additional smoothing and extend that value) Note: For exact math, I need to inspect the script; this is the typical approach.

How to read the indicator (signals & interpretation)

Bullish signal:

MACD line crossing above the signal line (MACD cross up).

Histogram turns positive (cross above zero).

Forecast shows MACD/histogram moving higher in the next N bars (if forecast is positive or trending up).

Bearish signal:

MACD line crossing below the signal line (MACD cross down).

Histogram turns negative (cross below zero).

Forecast shows MACD/histogram moving lower ahead.

Confirmations:

Use price action (higher highs/lows for bullish, lower highs/lows for bearish).

Volume or other momentum/confluence indicators (RSI, ADX).

Divergences:

Bullish divergence: price makes lower low while MACD histogram makes higher low.

Bearish divergence: price makes higher high while MACD histogram makes lower high.

Forecast behavior:

If the forecast leads the MACD cross (forecast crosses before the current MACD does), it’s an early warning.

Use caution: forecasts are prone to false signals; always confirm.

Common trading setups using this indicator

Conservative:

Wait for MACD to cross signal + histogram above zero + forecast already trending same direction.

Use stop below recent swing low (for long) or above recent swing high (for short).

Aggressive (early entry):

Enter when forecast turns positive while MACD still below signal (anticipating cross).

Use tighter stops and smaller position sizes.

Exit rules:

Opposite MACD cross, histogram flipping sign, or a target based on risk-reward.

Use trailing stop based on ATR or structure.

Example settings for different timeframes (starting points)

Scalping / 5–15 min:

Fast 8, Slow 21, Signal 5, Forecast 1–2

Intraday / 1H:

Fast 12, Slow 26, Signal 9, Forecast 2–3

Swing / 4H–Daily:

Fast 12, Slow 26, Signal 9, Forecast 3–5 Adjust based on the asset volatility and backtests.

Adding alerts (TradingView)

Click the “Alerts” button (clock icon) or press Alt + A.

In the Condition dropdown, select the indicator name (able_macd_forecast) and choose a plotted series or built-in alert condition (if the script uses alertcondition).

Common alert types:

MACD crosses Signal (Crossing)

Histogram crosses 0 (Crossing)

Forecast crosses 0 or Forecast trend change (if provided)

Message templates:

“{{ticker}}: MACD crossed above signal on {{interval}}”

“{{ticker}} Forecast positive: MACD forecast shows upward momentum”

Customize the message for your trade automation or notifications.

Configure frequency (Only once, Once per bar, or Once per bar close) — for signals like crossovers, “Once per bar close” is usually safer to avoid repainting issues. Note: If the script includes alertcondition() calls with explicit IDs/messages, use those directly — they are the most reliable for automation.

Backtesting / Strategy conversion

If this script is a study (indicator), you can:

Convert it to a strategy by adding strategy.* order calls (strategy.entry, strategy.close) using the entry/exit logic you prefer, or

Use TradingView’s “Bar Replay” to manually test signals across different markets/timeframes.

If you want, I can help convert or write a strategy wrapper that uses the indicator’s signals to place backtest trades (I’ll need the code).

Practical tips & best practices

Use higher timeframe confirmation for lower-timeframe entries (e.g., check daily MACD momentum before trading 15m signals).

Beware of choppy markets; MACD / forecast may produce whipsaws. Combine with trend filters (moving average direction, ADX).

If you rely on forecasted values, prefer alerts “on bar close” when possible to reduce false alerts from intra-bar noise.

Tune parameters for the specific asset (FX, crypto, stocks have different behavior).

Record each signal and outcome for a sample period (20–100 trades) to evaluate performance.

Troubleshooting

Indicator won’t add: verify Pine version in script header (//@version=4 or //@version=5). TradingView may reject scripts with unsupported version syntax.

Plots missing: check script inputs (Some scripts hide plots if toggles are off).

Alerts firing too often: change alert frequency to “Once per bar close” or adjust threshold values.

Forecast seems to repaint: some forecast methods can repaint (use “bar_index” or store values only on closed bars, or use non-repainting forecast methods). Ask me to inspect the script for repainting logic.

What I can do next (recommended)

If you paste the content of able_macd_forecast.pine here, I will:

Produce a precise, line-by-line usage guide mapping to the exact input names and default values.

Show the exact plotted series names and how to reference them for alerts.

Point out any repainting risks and suggest fixes.

Provide example alert messages that match the script’s alertcondition IDs (if any).

Optionally convert it into a strategy for backtesting, or add non-repainting forecast logic if needed.

Daily RDR (Prev Day H/L, Intraday)This indicator identifies intraday Range-Deviation Reversal (RDR) signals using the previous day’s high and low. At each new session, it stores yesterday’s levels and resets today’s range tracking. During the day, it detects when price first breaks above the prior high or below the prior low, then waits for a reversal: a bearish RDR triggers when price exceeds yesterday’s high and then closes back below it, while a bullish RDR triggers when price undercuts yesterday’s low and then closes back above it. The script plots the previous day’s levels and marks RDR reversals with small up/down triangles.

Global Liquidity Score

Global Liquidity Score – Simple Risk-On / Risk-Off Gauge

This indicator measures overall market liquidity conditions using a single, normalized score.

It takes several macro and crypto variables, standardizes each one (z-score), and combines them into one clear Liquidity Score Line.

You only follow one line (your pink/white line).

The background color shows the current liquidity regime.

⸻

What the indicator measures

The algorithm looks at four major liquidity sources:

1. USD Liquidity (tightening or easing)

• DXY (strong dollar = tighter global liquidity)

• US10Y yield (higher yields = liquidity drain)

2. Risk Sentiment (risk-on vs risk-off)

• VIX index (volatility)

• S&P 500 index (SPX)

3. Credit Market Strength

• High-yield ETFs: HYG, JNK

• Investment-grade corporate credit: LQD

Stronger credit = easier liquidity.

Weaker credit = tightening risk.

4. Internal Crypto Liquidity

• USDT dominance (higher = risk-off in crypto)

• Bitcoin price

• TOTAL2 (crypto market cap excluding BTC)

These are all converted into z-scores and combined into one metric:

Total Liquidity Score =

USD Block + Risk Block − Credit Block − 0.5 × Crypto Block

⸻

How to read the colors

The indicator uses background colors to show the liquidity regime:

Color Meaning

Dark Red Severe liquidity tightening / strong risk-off

Red Mild-to-moderate tightening

Green Liquidity easing / soft risk-on

Dark Green Strong easing, high liquidity / risk-on

Your pink/white line = the final liquidity score.

You only need to follow that single line.

⸻

How to interpret the score

📉 Positive score → Liquidity Tightening (Risk-Off)

• USD stronger

• Yields rising

• Volatility rising

• Credit markets weakening

• Crypto rotating to stablecoins

📈 Negative score → Liquidity Easing (Risk-On)

• USD weakening

• Yields falling

• Stocks rising

• Volatility low

• Credit markets strong

• Crypto beta assets outperform

⸻

What this indicator is NOT

This is not a price predictor.

It does not follow BTC directly.

It tells you liquidity conditions, not immediate price direction.

It answers the macro question:

“Is liquidity flowing INTO the market or OUT of the market?”

If liquidity is tightening (red), crypto rallies are harder to sustain.

If liquidity is easing (green), crypto rallies have more fuel.

CVD [able0.1]# CVD Overlay iOS Style - Complete User Guide

## 📖 Table of Contents

1. (#what-is-cvd)

2. (#installation-guide)

3. (#understanding-the-display)

4. (#reading-the-info-table)

5. (#settings--customization)

6. (#trading-strategies)

7. (#common-mistakes-to-avoid)

---

## 🎯 What is CVD?

**CVD (Cumulative Volume Delta)** tracks the **difference between buying and selling pressure** over time.

### Simple Explanation:

- **Positive CVD** (Orange) = More buying than selling = Bulls winning

- **Negative CVD** (Gray) = More selling than buying = Bears winning

- **Rising CVD** = Increasing buying pressure = Potential uptrend

- **Falling CVD** = Increasing selling pressure = Potential downtrend

### Why It Matters:

CVD helps you see **who's really in control** of the market - not just price movement, but actual buying/selling volume.

---

## 🚀 Installation Guide

### Step 1: Open Pine Editor

1. Go to TradingView

2. Click the **"Pine Editor"** tab at the bottom of the screen

3. Click **"New"** or open an existing script

### Step 2: Copy & Paste the Code

1. Select all existing code (Ctrl+A / Cmd+A)

2. Delete it

3. Copy the entire CVD iOS Style code

4. Paste it into Pine Editor

### Step 3: Add to Chart

1. Click **"Save"** button (or Ctrl+S / Cmd+S)

2. Click **"Add to Chart"** button

3. The indicator will appear on your chart!

### Step 4: Initial Setup

- The indicator appears as an **overlay** on your price chart

- You'll see an **orange/gray line** following price

- An **info table** appears in the top-right corner

---

## 📊 Understanding the Display

### Main Chart Elements:

#### 1. **CVD Line** (Orange/Gray)

- **Orange Line** = Positive CVD (buying pressure)

- **Gray Line** = Negative CVD (selling pressure)

- This line moves with your price chart but shows volume delta

#### 2. **CVD Zone** (Shaded Area)

- Light shaded box around the CVD line

- Shows the "range" of CVD movement

- Helps visualize CVD boundaries

#### 3. **Center Line** (Dotted)

- Gray dotted line in the middle of the zone

- Represents the "neutral" point

- CVD crossing this = shift in market control

#### 4. **Reference Asset Line** (Light Gray)

- Shows Bitcoin (BTC) price movement for comparison

- Helps you see if your asset moves with or against BTC

- Can be changed to any asset you want

#### 5. **CVD Label**

- Shows current CVD value

- Positioned above/below zone to avoid overlap

- Updates in real-time

#### 6. **Reset Background** (Very Light Gray)

- Appears when CVD resets

- Indicates a new calculation period

---

## 📋 Reading the Info Table

The info table (top-right) shows **8 key metrics**:

### Row 1: **Header**

```

╔═ CVD able ═╗ | 15m | ████████ | able

```

- **CVD able** = Indicator name + creator

- **15m** = Current timeframe

- **████████** = Visual decoration

- **able** = Creator signature

### Row 2: **CVD Value**

```

CVD▲ | 7.39K | ████████ | █

█

█

```

- **CVD▲** = CVD with trend arrow

- ▲ = CVD increasing

- ▼ = CVD decreasing

- ► = CVD unchanged

- **7.39K** = Actual CVD number

- **Progress Bar** = Visual strength (darker = stronger)

- **Vertical Bars** = Height shows intensity

### Row 3: **Delta**

```

◆DELTA | -1.274K | ████░░░░ | ░

░

```

- **Delta** = Volume change THIS BAR ONLY

- **Negative** = More selling this bar

- **Positive** = More buying this bar

- Shows **immediate** pressure (not cumulative)

### Row 4: **UP Volume**

```

UP↑ | -1.263K | ████████ | █

█

█

```

- Total **buying volume** this bar

- Higher = Stronger buying pressure

- Green/Orange vertical bars = Bullish strength

### Row 5: **DOWN Volume**

```

DN↓ | 2.643K | ████████ | ░

░

░

```

- Total **selling volume** this bar

- Higher = Stronger selling pressure

- Gray vertical bars = Bearish strength

### Row 6-7: **Reference Asset** (if enabled)

```

══ REF ══ | ══════ | ████████ | █

█

PRICE▲ | 4130.300 | ████████ | █

█

```

- **REF** = Reference asset header

- **PRICE▲** = Reference price with trend

- Shows if BTC (or chosen asset) is rising/falling

- Compare with your chart to see correlation

### Row 8: **Market Status**

```

◄STATUS► | NEUT | ████░░░░ | ▒

▒

```

- **BULL** = CVD positive + Delta positive = Strong buying

- **BEAR** = CVD negative + Delta negative = Strong selling

- **NEUT** = Mixed signals = Wait for clarity

**Status Colors:**

- **Orange background** = Bullish (good for long)

- **Gray background** = Bearish (good for short)

- **White background** = Neutral (no clear signal)

---

## ⚙️ Settings & Customization

### Main Settings (⚙️)

#### **CVD Reset**

- **None** = CVD never resets (from beginning of data)

- **On Higher Timeframe** = Resets when HTF candle closes

- 15m chart → Resets hourly

- 1h chart → Resets daily

- Recommended for most traders

- **On Session Start** = Resets at market open

- **On Visible Chart** = Resets from leftmost visible bar

#### **Precision**

- **Low (Fast)** = Uses 1m data, faster but less accurate

- **Medium** = Uses 5m data, balanced (recommended)

- **High** = Uses 15m data, most accurate but slower

#### **Cumulative**

- ✅ On = CVD accumulates over time (recommended)

- ❌ Off = Shows only current bar delta

#### **Show Labels**

- ✅ On = Shows CVD value label on chart

- ❌ Off = Cleaner chart, no label

#### **Show Info Table**

- ✅ On = Shows info table (recommended for beginners)

- ❌ Off = Hide table for minimalist view

---

### 🎨 iOS Style Colors

You can customize **every color** to match your chart theme:

#### **Primary Colors**

- **Primary (Orange)** = Main bullish color (#FF9500)

- **Secondary (Gray)** = Main bearish color (#8E8E93)

- **Background** = Table background (#FFFFFF)

- **Text** = Text color (#1C1C1E)

#### **Bullish/Bearish**

- **Bullish (Orange)** = Positive CVD color

- **Bearish (Gray)** = Negative CVD color

- **Opacity** = Zone transparency (0-100%)

- **Show Zone** = Enable/disable shaded area

#### **Table Colors** (📋)

- **Header Background** = Top row background

- **Header Text** = Top row text color

- **Cell Background** = Data cells background

- **Cell Text** = Data cells text color

- **Border** = Table border color

- **Accent Background** = Special rows background

- **Alert Background** = Warning/status background

---

### 📊 Reference Asset Settings

#### **Enable**

- ✅ On = Shows reference asset line

- ❌ Off = Hide reference asset

#### **Symbol**

- Default: `BINANCE:BTCUSDT`

- Can change to any asset:

- `BINANCE:ETHUSDT` (Ethereum)

- `SPX` (S&P 500)

- `DXY` (US Dollar Index)

- Any ticker symbol

#### **Color & Width**

- Customize line appearance

- Width: 1-4 (thickness)

---

## 💡 Trading Strategies

### Strategy 1: CVD Divergence (Beginner-Friendly)

**What to Look For:**

- Price making **higher highs** but CVD making **lower highs** = Bearish divergence

- Price making **lower lows** but CVD making **higher lows** = Bullish divergence

**How to Trade:**

1. Wait for divergence to form

2. Look for confirmation (price reversal, candlestick pattern)

3. Enter trade in divergence direction

4. Stop loss beyond recent high/low

**Example:**

```

Price: /\ /\ /\ (higher highs)

CVD: /\ / \/ (lower highs) = Bearish signal

```

### Strategy 2: CVD Trend Following (Intermediate)

**What to Look For:**

- **Strongly rising CVD** + **rising price** = Strong uptrend

- **Strongly falling CVD** + **falling price** = Strong downtrend

**How to Trade:**

1. Wait for CVD and price moving in same direction

2. Enter on pullbacks to support/resistance

3. Stay in trade while CVD trend continues

4. Exit when CVD trend breaks

**Signals:**

- CVD ▲▲▲ + Price ↑ = Go LONG

- CVD ▼▼▼ + Price ↓ = Go SHORT

### Strategy 3: CVD + Reference Asset (Advanced)

**What to Look For:**

- Your asset **rising** but BTC (reference) **falling** = Relative strength

- Your asset **falling** but BTC (reference) **rising** = Relative weakness

**How to Trade:**

1. Compare CVD movement with BTC

2. If your CVD rises faster than BTC = Buy signal

3. If your CVD falls faster than BTC = Sell signal

4. Use for **pair trading** or **asset selection**

### Strategy 4: Volume Delta Confirmation

**What to Look For:**

- **Large positive Delta** = Strong buying this bar

- **Large negative Delta** = Strong selling this bar

**How to Trade:**

1. Price breaks resistance + Large positive Delta = Confirmed breakout

2. Price breaks support + Large negative Delta = Confirmed breakdown

3. Use Delta to **confirm** price moves, not predict them

**Rules:**

- Delta > 2x average = Very strong pressure

- Delta near zero at key level = Weak move, likely false breakout

---

## 🎓 Reading Real Scenarios

### Scenario 1: Strong Buying Pressure

```

Table Shows:

CVD▲ | 12.5K | ████████ | ████ (CVD rising)

◆DELTA | +2.8K | ████████ | ▲ (Positive delta)

UP↑ | 3.1K | ████████ | ████ (High buy volume)

DN↓ | 0.3K | ██░░░░░░ | ░ (Low sell volume)

◄STATUS► | BULL | ████████ | ████ (Orange background)

```

**Interpretation:** Strong buying, good for LONG trades

### Scenario 2: Distribution (Hidden Selling)

```

Table Shows:

CVD► | 8.2K | ████░░░░ | ▒▒ (CVD flat)

◆DELTA | -1.5K | ████████ | ▼ (Negative delta)

UP↑ | 0.8K | ███░░░░░ | ░ (Low buy volume)

DN↓ | 2.3K | ████████ | ████ (High sell volume)

◄STATUS► | BEAR | ████████ | ░░░░ (Gray background)

```

**Interpretation:** Price may look stable, but selling increasing = Prepare for drop

### Scenario 3: Neutral/Choppy Market

```

Table Shows:

CVD► | 5.1K | ████░░░░ | ▒ (CVD sideways)

◆DELTA | +0.2K | ██░░░░░░ | ─ (Small delta)

UP↑ | 1.2K | ████░░░░ | ▒ (Medium buy)

DN↓ | 1.0K | ████░░░░ | ▒ (Medium sell)

◄STATUS► | NEUT | ████░░░░ | ▒▒ (White background)

```

**Interpretation:** No clear direction = Stay out or reduce position size

---

## ⚠️ Common Mistakes to Avoid

### Mistake 1: Trading on CVD Alone

- ❌ **Wrong:** "CVD is rising, I'll buy immediately"

- ✅ **Right:** "CVD is rising, let me check price structure, support/resistance, and wait for confirmation"

### Mistake 2: Ignoring Delta

- ❌ **Wrong:** Looking only at cumulative CVD

- ✅ **Right:** Watch both CVD (trend) and Delta (momentum)

- Delta shows **immediate** pressure changes

### Mistake 3: Wrong Timeframe

- ❌ **Wrong:** Using 1m chart with High Precision (too slow)

- ✅ **Right:** Match precision to timeframe:

- 1m-5m → Low Precision

- 15m-1h → Medium Precision

- 4h+ → High Precision

### Mistake 4: Not Using Reset

- ❌ **Wrong:** Using "None" reset for intraday trading

- ✅ **Right:** Use "On Higher Timeframe" to see fresh CVD each session

### Mistake 5: Overtrading Neutral Status

- ❌ **Wrong:** Forcing trades when STATUS = NEUT

- ✅ **Right:** Only trade clear BULL or BEAR status

### Mistake 6: Ignoring Reference Asset

- ❌ **Wrong:** Trading altcoin without checking BTC

- ✅ **Right:** Always check if BTC CVD agrees with your asset

---

## 🔥 Pro Tips

### Tip 1: Multi-Timeframe Analysis

- Check CVD on **3 timeframes**:

- Lower TF (15m) = Entry timing

- Current TF (1h) = Trade direction

- Higher TF (4h) = Overall trend

### Tip 2: Volume Confirmation

- Big price move + Small Delta = **Weak move** (likely reversal)

- Small price move + Big Delta = **Strong accumulation** (continuation)

### Tip 3: CVD Reset Zones

- Pay attention to **reset backgrounds** (light gray)

- Often marks **session starts** = High volatility periods

### Tip 4: Divergence + Status

- Bearish divergence + STATUS = BEAR = **Strongest short signal**

- Bullish divergence + STATUS = BULL = **Strongest long signal**

### Tip 5: Color Psychology

- **Orange** (Bullish) is **warm** = Buying energy

- **Gray** (Bearish) is **cool** = Selling pressure

- Train your eye to read colors instantly

### Tip 6: Table as Quick Scan

- Glance at table without reading numbers:

- **All orange** = Bullish

- **All gray** = Bearish

- **Mixed** = Wait

---

## 📱 Quick Reference Card

| Signal | CVD | Delta | Status | Action |

|--------|-----|-------|--------|--------|

| **Strong Buy** | ▲▲ High | ++ Positive | BULL | Long Entry |

| **Strong Sell** | ▼▼ Low | -- Negative | BEAR | Short Entry |

| **Divergence Buy** | ▲ Rising | Price ▼ | → BULL | Long Setup |

| **Divergence Sell** | ▼ Falling | Price ▲ | → BEAR | Short Setup |

| **Neutral** | → Flat | ~0 Near Zero | NEUT | Stay Out |

| **Accumulation** | → Flat | ++ Positive | NEUT→BULL | Watch for Breakout |

| **Distribution** | → Flat | -- Negative | NEUT→BEAR | Watch for Breakdown |

---

## 🆘 Troubleshooting

### Issue: "Indicator not showing"

- **Solution:** Make sure overlay=true in code, re-add to chart

### Issue: "Table overlaps with price"

- **Solution:** Change table position in code or use TradingView's "Move" feature

### Issue: "CVD line too far from price"

- **Solution:** This is normal! CVD is volume-based, not price-based. Focus on CVD direction, not position

### Issue: "Too many lines on chart"

- **Solution:** Disable "Show Zone" and "Show Labels" in settings for cleaner view

### Issue: "Calculations too slow"

- **Solution:** Change Precision to "Low (Fast)" or use higher timeframe

### Issue: "Reference asset not showing"

- **Solution:** Check if "Enable" is ON and symbol is valid (e.g., BINANCE:BTCUSDT)

---

## 🎬 Getting Started Checklist

- Install indicator on TradingView

- Set precision to "Medium"

- Set reset to "On Higher Timeframe"

- Enable info table

- Add reference asset (BTC)

- Practice reading the table on demo account

- Test on different timeframes (15m, 1h, 4h)

- Compare CVD with your current strategy

- Paper trade for 1 week before going live

- Keep a trading journal of CVD signals

---

## 📚 Summary

**CVD shows WHO is winning: Buyers or Sellers**

**Key Points:**

1. **Orange/Rising CVD** = Buying pressure = Bullish

2. **Gray/Falling CVD** = Selling pressure = Bearish

3. **Delta** = Immediate momentum THIS BAR

4. **Status** = Overall market condition

5. **Always confirm** with price action & other indicators

**Remember:**

- CVD is a **tool**, not a crystal ball

- Use with proper risk management

- Practice makes perfect

- Stay disciplined!

---

**Created by: able**

**Version:** iOS Style v1.0

**Contact:** For questions, refer to TradingView community

Happy Trading! 🚀📈

[CT] ATR Chart Levels From Open ATR Chart Levels From Open is a volatility mapping tool that projects ATR based price levels directly from a user defined center price, most commonly the current session open, and displays them as clean horizontal levels across your chart. The script pulls an Average True Range from a higher timeframe, by default the daily, using a user selectable moving average type such as SMA, EMA, WMA, RMA or VWMA. That ATR value is then used as the unit of measure for all projected levels. You can choose the ATR length and timeframe so the bands can represent anything from a fast intraday volatility regime to a smoother multi week average range.

The core of the tool is the center line, which is treated as zero ATR. By default this center is the current session open, but you can instead anchor it to the previous close, previous open, previous high or low, or several blended prices such as HLC3, HL2, HLCC4 and OHLC4, including options that use the minimum or maximum of the previous close and current open. From this center, the indicator builds a symmetric grid of ATR based levels above and below the zero line. The grid size input controls the spacing in ATR units, for example a value of 0.25 produces levels at plus or minus 25, 50, 75, 100 percent of ATR and so on, while the number of grids each side determines how far out the bands extend. You can restrict levels to only the upper side, only the lower side, or draw both, which is useful when you want to focus on upside targets or downside expansion separately.

The levels themselves are drawn as horizontal lines on the main price chart, with configurable line style and width. Color handling is flexible. You can assign separate colors to the upper and lower levels, keep the center line in a neutral color, and choose how the colors are applied. The “Cool Towards Center” and “Cool Towards Outermost” modes apply smooth gradients that either intensify toward the middle or toward the outer bands, giving an immediate visual sense of how extended price is relative to its average range. Alternatively, the “Candle’s Close” mode dynamically colors levels based on whether the current close is above or below a given band, which can help highlight zones that are acting as resistance or support in real time.

Each level is optionally labeled at its right endpoint so you always know exactly what you are looking at. The center line label shows “Daily Open”, or more generally the chosen center, along with the exact price. All other bands show the percentage of ATR and the corresponding price, for example “+25% ATR 25999.90”. The label offset input lets you push those tags a user defined number of bars to the right of the current price action so the chart remains clean while still keeping the information visible. As new bars print, both the lines and their labels automatically extend and slide to maintain that fixed offset into the future.

To give additional context about current volatility, the script includes an optional table in the upper right corner of the chart. This table shows the latest single period ATR value on the chosen higher timeframe alongside the smoothed ATR used for the bands, clearly labeled with the timeframe and ATR length. When enabled, a highlight color marks the table cells whenever the most recent ATR reading exceeds the average, making it easy to see when the market is operating in an elevated volatility environment compared to its recent history.

In practical trading terms, ATR Chart Levels From Open turns the abstract concept of “average daily range” into specific, actionable intraday structure. The bands can be used to frame opening range breakouts, define realistic intraday profit targets, establish volatility aware stop placement, or identify areas where price has moved an unusually high percentage of its average range and may be vulnerable to mean reversion or responsive flow. Because the ATR is computed on a higher timeframe yet projected on whatever chart you are trading, you can sit on a one minute or five minute chart and still see the full higher timeframe volatility envelope anchored from your chosen center price for the session.

ORB 15min: Break & ConfirmUsing the 15-minute opening candle range, this generates an alert when a 5-minute candle breaks the range and another 5-minute candle closes above the breakout candle's high or the high of any other candle that attempted to break the range.

Predictive Analysis Engine — Adaptive MACD Forecasting with R² SProfessional and Rule-Compliant Description (Ready for Publishing)

This description explains every component of the script in detail, highlights its originality, and provides traders with clear usage instructions — exactly what TradingView expects.

Predictive Analysis Engine (PAE)

This script is a predictive analysis model that combines trend filtering, linear forecasting, stability analysis (R²), and outlier filtering using ATR to produce an advanced, leading-style version of MACD rather than a traditional lagging one.

The indicator does not rely on random elements; it is built on four core components that work together:

1. Stability Measurement Using R²

The coefficient of determination (R²) is calculated based on the correlation between price and time, then normalized to a 0–1 scale.

A higher R² indicates more stable price movement, allowing the script to increase forecast accuracy.

Here, R² acts as a primary component of the Confidence Filter.

2. Forecasted Price Using Linear Regression

Instead of relying solely on the current price, the script uses:

Linear Regression

Weighted blending between the forecasted price and actual price

This enables the script to build a Leading MACD based on an “advanced” price that anticipates probable movement.

3. Advanced MACD With Adaptive Smoothing

MACD is applied to the blended (real + forecasted) price using:

Fast EMA

Slow EMA

MACD base

Optional TEMA for reducing signal lag

Adjustable histogram smoothing

This process makes MACD more responsive with significantly less lag, reacting faster to predicted movements.

4. Predictive MACD (Projected MACD)

Linear Regression is applied again — but this time to:

MACD

Signal

Histogram

to generate projected versions of each line (proj_macd, proj_signal), while proj_hist is used to produce early signals before the actual crossover occurs.

5. Volatility Filtering Using ATR & Volatility Ratio

ATR is used to evaluate:

Strength of movement

Overextension levels

Signal quality

ATR is combined with R² to compute:

Confidence = R² × Volatility Ratio

This suppresses weak signals and boosts high-quality, reliable ones.

6. Predictive Signals + Safety Filters

A signal is triggered when:

proj_hist crosses the 0 level

Confidence exceeds the required threshold

The real histogram is not excessively stretched (extra safety)

The script includes:

BUY / SELL

BUY_STRONG / SELL_STRONG

based on the smoothed histogram trend.

7. Coloring, Background & Visual Enhancements

The script colors:

The histogram

Chart background

Signal lines

to clearly highlight momentum direction and confidence conditions.

8. Built-In Alerts

The script provides ready-to-use alerts:

BUY Alert

SELL Alert

Both based on the predictive MACD model.

How to Use the Script

Add it to any timeframe and any market.

BUY/SELL signals are generated from the projected histogram crossover.

Higher Confidence = stronger signal.

Background colors help visualize trend transitions instantly.

Recommended to combine with support/resistance or price action.

Indicator Objective

This script is designed to deliver early insight into momentum shifts using a blend of:

Linear forecasting

Trend stability via R²

Signal quality filtering via ATR

A fast and adaptive advanced MACD

HVPro Style IndicatorHVPro Style Indicator – Historical Volatility + Volume

HVPro Style Indicator is a combined volatility-and-volume tool designed to help traders visualize market expansion and contraction phases.

It calculates Historical Volatility (HV) using log-returns and a customizable lookback period, then smooths the result for a cleaner trend signal.

The script also includes a volume histogram, scaled by a multiplier, with bar colors changing based on whether volatility is rising or falling.

This makes it easy to spot moments when both volume and volatility align, often signaling trend transitions, breakouts, or exhaustion.

Features

✔ Historical Volatility calculation (annualized)

✔ Smoothed HV for cleaner visual trends

✔ Volume histogram with customizable multiplier

✔ Volume bar color shifts based on HV direction

✔ User-controlled visibility for both HV and volume

✔ Lightweight and optimized for all timeframes

How to Use

Rising HV (green volume bars) can indicate trend expansion or breakout momentum.

Falling HV (red bars) suggests contraction, ranging conditions, or volatility cooldown.

Watch for volatility shifts combined with volume spikes for potential trade entries.

GK BOS ultimateGK BOS ultimate is a structured Break of Structure tool designed to highlight major shifts in the market structure.

The script identifies when price breaks above a significant previous high or below a significant low, using a defined lookback period and a ATR filter to reduce weak or minor breakouts

When a major bullish or bearish structure breaks occurs, the indicator marks the chart with a GK BUY or GK SELL label.

It also plots a TP1 level based on ATR(14) multiplied by a user-selected factor.

This provides a consistent volatility-based reference point that helps traders analyse potential follow-through areas after a structure break.

HOW IT WORKS

the script calculates the highest high and lowest low over the chosen lookback period

A break of structure is confirmed only if the close moves beyond these levels with enough strength relative to ATR, When this happens the indicator

Prints GK BUY for bullish structure breaks

Prints GK SELL for bearish structure breaks

Plots a corresponding TP1 PRINT derived from recent volatility

no repainting occurs because calculations are based on confirmed closes

this TOOL is intended for educational and analytical purposes only

Sniper BB + VWAP System (with SMT Divergence Arrows)STEP 1: Load two correlated futures charts.

Example: CL + RB/SI+GC/ NQ+ES

STEP 2: Add Bollinger Bands (20, 2.0) on both.

Optional add (20, 3.0).

STEP 3: Watch for a BB tag on one chart but not the other.

STEP 4: Wait for a reclaim candle back inside the band.

STEP 5: Enter with stop below/above the wick + 3.0 BB.

STEP 6: Scale out midline, then opposite band.

STEP 7: Hold partials when both pairs confirm trend.

*You can take the vwap bands off the chart if it is too cluttered.

The 'Qualified' POI Scorer [PhenLabs]📊 The “Qualified” POI Scorer (Q-POI)

Version: PineScript™ v6

📌 Description

The “Qualified” POI Scorer helps intermediate traders overcome "analysis paralysis" by filtering Smart Money Concepts (SMC) structures based on their probability. Instead of flooding your chart with every possible Order Block, this script assigns a proprietary “Quality Score” (0-100) to each zone. It analyzes the strength of the displacement, the presence of imbalances (FVG), and liquidity mechanics to determine which zones are worth your attention. It is designed to clean up your charts and enforce discipline by visually fading out low-quality setups.

🚀 Points of Innovation

Dynamic “Glass UI” Transparency that automatically fades weak zones based on their score.

Proprietary Scoring Algorithm (0-100) based on three distinct institutional factors.

Visual Icon System that prints analytical context (💧— 🚀/🐌—🧱) directly on the chart.

Automated Mitigation Tracking that changes the visual state of zones after they are tested.

Displacement Velocity calculation using ATR to verify institutional intent.

🔧 Core Components

Liquidity Sweep Engine: Detects if a pivot point grabbed liquidity from the previous X bars before reversing.

FVG Validator: Checks if the move away from the zone created a valid Fair Value Gap.

Momentum Scorer: Calculates the size of the displacement candle relative to the Average True Range (ATR).

🔥 Key Features

Quality Filtering: Automatically hides or dims zones that score below 50 (user configurable).

State Management: Zones turn grey when mitigated and delete themselves when invalidated.

Visual Scorecard: Displays the exact numeric score on the zone for quick decision-making.

Time-Decay Logic: Keeps the chart clean by managing the lifespan of old zones.

🎨 Visualization

High Score Zones (80-100): Display as bright, semi-solid boxes indicating high probability.

Medium Score Zones (50-79): Display as translucent “glass” boxes.

Low Score Zones (<50): Display as faint “ghost” boxes or are completely hidden.

Rocket Icon (🚀): Indicates high momentum displacement.

Snail Icon (🐌): Indicates low momentum displacement.

Drop Icon (💧): Indicates the zone swept liquidity.

Brick Icon (🧱): Indicates the zone is supported by an FVG.

📖 Usage Guidelines

Swing Structure Length (Default: 5): Controls the sensitivity of the pivot detection; lower numbers create more zones, higher numbers find major swing points.

ATR Length (Default: 14): Determines the lookback period for calculating relative momentum.

Minimum Quality Score (Default: 50): The threshold for which zones are considered “valid” enough to be fully visible.

Bullish/Bearish Colors: Fully customizable colors that adapt their own transparency based on the score.

Show Weak Zones (Default: False): Toggles the visibility of zones that failed the quality check.

✅ Best Use Cases

Filtering noise during high-volatility sessions by focusing only on Score 80+ zones.

Confirming trend continuation entries by looking for the Rocket (🚀) momentum icon.

Avoiding “stale” zones by ignoring any box that has turned grey (Mitigated).

⚠️ Limitations

The indicator is reactive to closed candles and cannot predict news-driven spikes.

Scoring is based on technical structure and does not account for fundamental drivers.

In extremely choppy markets, the ATR filter may produce lower scores due to lack of displacement.

💡 What Makes This Unique

It transforms subjective SMC analysis into an objective, quantifiable score.

The visual hierarchy allows traders to assess chart quality in milliseconds without reading data.

It integrates three separate SMC concepts (Liquidity, Imbalance, Structure) into a single tool.

🔬 How It Works

Step 1: The script identifies a Swing High or Low based on your length input.

Step 2: It looks backward to see if that swing swept liquidity, and looks forward to check for an FVG and displacement.

Step 3: It calculates a weighted score (30pts for Sweep, 30pts for FVG, 40pts for Momentum).

Step 4: It draws the zone with a transparency level designated by the score and appends the relevant icons.

💡 Note:

For the best results, use this indicator on the timeframe you execute trades on (e.g., 15m or 1h). Do not use it to find entries on the 1m chart if your analysis is based on the 4h chart.

MAHI Indicator v9.5 - Smart Momentum HUD + IntradayMAHI Indicator v9.5 — Smart Momentum HUD (Multi-Framework + Intraday Engine)

A Complete Momentum, Trend, and Setup Framework for Swing, Position & Intraday Traders

MAHI v9.5 is the most advanced version yet — a highly optimized, visual, multi-framework trading system that blends momentum, trend alignment, adaptive setup detection, and now Auto-Intraday Mode for short-term traders.

This indicator acts like a Heads-Up Display (HUD) on your chart: it shows trend strength, squeeze zones, dynamic support/resistance, EMAs, setup validation, and early reversal signals in one clean interface — without clutter.

✔ Core Features

📌 1. Smart Momentum Ribbon

A dynamic EMA-based momentum band that visually shifts as trend strength changes.

Helps identify strong vs. weak momentum zones

Adapts to volatility & trend slope

Works on all timeframes (1m to 1M)

📌 2. EMA 9 → 21 Flip System

A precision trend-switching signal:

EMA 9 → 21 BULL = early bullish momentum

EMA 9 → 21 BEAR = early bearish momentum

More reliable than stand-alone MA crossovers

📌 3. Bullish Setup Engine (Standard + Weak)

Automatically identifies when price is entering a reversal-ready state based on:

Position relative to the ribbon

Candle structure

Momentum compression

Slope + exhaustion conditions

Includes:

Bull Setup (Standard) — Higher probability setup

Bull Setup (Weak) — Early or less developed setup

Setup Invalidated — Confirms that the pattern failed

This prevents false confidence & keeps traders disciplined.

📌 4. Strong Buy / Strong Sell Signals

Only appear when multiple confirmations align:

Ribbon bias

EMA slope

Momentum compression

Trend alignment

Filtered to remove noise — especially in lower timeframes.

📌 5. Multi-Timeframe Trend HUD

Top-right panel summarizing:

Overall Trend (Bullish, Bearish, Neutral)

RSI Condition

Daily vs Weekly Alignment

Trading Mode Suggestions (Buy / Sell / LEAPS / Neutral)

This gives instant context.

📌 6. Auto Intraday Engine (NEW in v9.5)

Automatically switches internal logic when you move into intraday timeframes (1m–30m):

Intraday Enhancements:

Adaptive setup detection

Faster momentum sensitivity

EMAs tuned for scalp/swing precision

Tighter invalidation logic

Reduced false positives

Optional strict filtering

Perfect for scalping, day trading & micro-trends

Works instantly — no settings needed.

Just change the chart timeframe and MAHI adjusts.

📌 7. Dynamic High-Timeframe Support (W & M)

Auto-layers weekly & monthly levels:

Helps identify strong bounce zones

Extremely useful for swing & LEAPS traders

📌 8. Weekly Volume Shelf Projection

Lightweight VWAP-style level based on weekly volume aggregation.

Shows probable bottoming areas during pullbacks.

✔ Who This Indicator Is For

Perfect for:

Day traders

Swing traders

Momentum riders

LEAPS & long-term investors

Beginner traders needing a structured system

MAHI adapts to your timeframe and trading style.

✔ Why MAHI Works

MAHI isn’t a single-signal indicator — it’s a framework.

It combines:

Trend

Momentum

Volatility

Setup pattern detection

Validation & invalidation

Multi-timeframe alignment

Dynamic zones

Intraday optimization

This eliminates guesswork and helps traders avoid the emotional traps that cause most losses.

You don’t just get a signal — you get context.

✔ How to Use It

Follow the ribbon bias

Use EMA 9→21 flips as trend confirmation

Look for Bull Setup tags during pullbacks

Avoid trades when you see Setup Invalidated

Respect weekly/monthly HTF support levels

On intraday charts — rely on auto-optimized mode

For swing entries, combine setups with HTF trend HUD

MAHI gives the map. You choose the path.

✔ Final Notes

This version is heavily optimized for performance, clarity, and high-probability signals.

MAHI does not repaint, and works on all assets including:

Stocks

Crypto

ETFs

Forex

Futures

Orbital Barycenter Matrix @darshaksscThe Orbital Barycenter Matrix is a visual, informational-only tool that models how price behaves around a dynamically calculated barycenter —a type of moving equilibrium derived entirely from historical price data.

Instead of focusing on signals, this indicator focuses on market structure symmetry, distance, compression, expansion, and volatility-adjusted movement.

This script does not predict future price and does not provide buy/sell signals .

All values and visuals come solely from confirmed historical data , in full compliance with TradingView policy.

📘 How the Indicator Works

1. Dynamic Barycenter (Core Mean Line)

The barycenter is calculated from a smoothed blend of historical price components.

It represents the center of mass around which price tends to oscillate.

This is not a forecast line—only a representation of historical average behavior.

2. Orbital Rings (Distance Zones)

Around the barycenter, the indicator draws several “orbital rings.”

Each ring shows a volatility-scaled distance from the barycenter using ATR-based calculations.

These rings help visualize:

How far price has drifted from its historical center

Whether price is moving in an inner, mid, or outer region

How volatility influences the spacing of the rings

Rings do not imply future targets and are informational only.

3. Orbital Extension Range

Beyond the outermost ring, a wider band (extension range) shows a high-volatility reference distance.

It represents extended displacement relative to past price behavior—not a projected target.

4. Orbit Trail (Motion Trace)

The Orbit Trail plots small circles behind price, helping visualize how price has moved through the orbital regions over time.

Colors adjust with “pressure” (distance from center), making compression and expansion easy to observe.

5. Satellite Nodes (Swing Markers)

Confirmed swing highs and lows (using fixed pivots) are marked as small dots.

Their color reflects the orbital zone they formed in, giving context to how significant or extended each pivot was.

These swing markers do not repaint because they use confirmed pivots.

6. Pressure & Distance Calculations

The indicator converts price displacement away from the barycenter into a pressure metric, scaled between 0%–100%.

Higher pressure means price is further from its historical center relative to volatility.

The dashboard displays:

Zone classification

ATR-based distance

Pressure level

A small intensity gauge

All are informational readings—no direction or forecast.

📊 Key Features

✔ Dynamic barycenter core

✔ Up to four orbital rings

✔ Informational orbital extension band

✔ Visual orbit trail showing recent movement

✔ Non-repainting satellite swing nodes

✔ Distance & pressure analytics

✔ Fully adjustable HUD

✔ Always-visible floating dashboard (screen-anchored)

✔ Zero repainting on confirmed elements

✔ 100% sourced from historical data only

✔ Policy-safe: no predictions, no signals, no targets

🎯 What to Look For

1. How close price is to the barycenter

This can reveal whether price is in:

The inner region

The mid zone

The outer region

The extended field

2. Pressure level

Shows how “stretched” price is relative to its past behavior.

3. Satellite nodes

Indicate where confirmed pivots formed and in which orbital band.

4. Ring interactions

Observe how price moves between rings—inside, outside, or oscillating around them.

5. Color changes in the orbit trail

These show changes in market compression/expansion.

🧭 How to Read the Indicator

Inner Orbit

Price close to its historical equilibrium.

Mid Orbit

Moderate displacement from typical range.

Outer Orbit

Historically extended movement.

Beyond Extension Field

Price has moved further than usual relative to historical volatility.

These are descriptive conditions only , not trade recommendations.

🛠 How to Apply It on the Chart

Use the barycenter to understand where price has historically balanced.

Observe how volatility changes the spacing between rings.

Use pressure readings to identify when price is compressed, neutral, or extended.

Use swing nodes to contextualize historical pivot formation.

Watch how price interacts with rings to better understand rhythm, velocity, and structural behavior.

This tool is meant to enhance visual understanding—not to generate trade entries or exits.

⚠️ Important Disclosure

This indicator is strictly informational.

It does not predict or project future price movement.

It does not provide buy/sell/long/short signals.

All lines, zones, and values are derived solely from past market data.

Any interpretation is at the user’s discretion.

Silent 60pt Volatility Trigger (60pt Range in 5min)This alert triggers when a 5 minute candle reaches a range of 60pts in a 5 min candle /MNQ. Good for a mid day vol alert