VQI Z-Score Pro Suite [MTF + Divs]Description:

The VQI Z-Score Pro Suite is a premium-grade volatility oscillator designed to filter market noise and identify high-probability reversal or continuation points. It evolves the classic Volatility Quality Index (VQI) by applying advanced smoothing and statistical normalization (Z-Score).

Unlike standard indicators that lag significantly, this suite uses advanced moving averages (JMA, FRAMA, ALMA) to remain responsive while filtering out "bad volatility" (choppy markets).

🚀 Key Features:

Advanced MA Engine: Choose from over 20 smoothing methods, including Jurik (JMA), ALMA, and Kaufman (KAMA), to perfectly tune the indicator to your asset.

Statistical Thresholds: Uses Z-Score standard deviations to objectively identify market extremes:

> 1.64: Start of Momentum (90% Probability)

> 1.96: Strong Trend (95% Probability)

> 2.58: Extreme / Exhaustion (99% Probability)

Auto-Adaptive Length: Optional feature that adjusts the Z-Score lookback period dynamically based on market volatility (ATR).

Smart Divergences: Automatically detects Regular (Reversal) and Hidden (Continuation) divergences between Price and Volatility.

📊 Pro Dashboard: Includes a glass-morphism information panel that displays:

Current Trend Status (with Unicode arrows)

Z-Score Value (Color coded)

Active Divergences

Timeframe & Settings

🛠 How to use:

Trend Trading: Look for the Z-Score to cross 1.64 (Yellow) to confirm a breakout.

Reversals: Watch for the Z-Score hitting Extreme levels (>2.58) combined with a Regular Divergence label (R+ / R-).

Multi-Timeframe: Enable MTF in settings to view higher timeframe volatility trends while trading on lower timeframes.

📘 Operating Manual: VQI Z-Score Pro Suite

1. Introduction & Philosophy

The VQI Z-Score Pro is not just a simple oscillator. It is an advanced statistical tool designed to solve the main problem traders face: distinguishing "good" volatility (Trend) from "bad" volatility (Noise).

The indicator leverages two powerful mathematical concepts:

VQI (Volatility Quality Index): An algorithm that measures the quality of price movement (how "clean" the trend is).

Z-Score (Statistical Normalization): Transforms raw VQI values into Standard Deviations. This allows us to objectively know if a movement is statistically significant or extreme.

2. Visual Interpretation (Chart & Dashboard)

The Chart (Histogram)

The indicator displays bars (columns) oscillating around a zero line.

Gray Zone (-1.64 to +1.64): Market noise or consolidation. No statistical edge.

Yellow Zone (> 1.64): Momentum Start. Price has broken statistical normality (90% confidence).

Orange Zone (> 1.96): Strong Trend. Healthy directional movement (95% confidence).

Green/Red Zone (> 2.58): Extreme/Climatic. Exceptional movement (99% confidence). This may indicate a violent pump/dump or imminent exhaustion (top/bottom).

The "Glass" Dashboard (Info Panel)

Located in the top right, it provides an instant snapshot:

Mode: The Moving Average type and Timeframe currently in use.

Z-Score: The exact numerical value.

Status: Indicates current sentiment with arrows (e.g., ▲ STRONG BULL).

Divergence: Signals if a divergence is active (REG = Reversal, HID = Continuation).

Settings: Displays the calculation length (useful if using Auto-Adaptive mode).

3. Parameters Guide (Inputs)

⚙️ General Settings

Price Smoothing Length: (Default: 15). Determines how much the price is "smoothed" before calculation. Low values (5-10) for reactive scalping, high values (20-30) for clean swing trading.

MA Mode: The core of the system. Choose the smoothing algorithm:

Recommended: JMA (Jurik - Perfect balance), ALMA (Arnaud Legoux - Great for reducing lag), KAMA (Kaufman - Adaptive).

Classic: EMA, SMA, RMA.

📊 Z-Score Settings (Auto-Tuning)

Auto-Adaptive Length? (Default: False).

OFF: Uses a fixed length (Default 100). Ideal for standard analysis.

ON: The indicator adapts the Z-Score length based on volatility (ATR). If the market is frantic, it shortens the period to be more reactive; if calm, it lengthens it to filter false signals.

🎯 Signal Thresholds

These levels are derived from the Normal Distribution (Gaussian):

1.64: 90% Threshold. Filters baseline noise.

1.96: 95% Threshold. Confirms the trend.

2.58: 99% Threshold. Rare event (Black Swan or Exhaustion).

💎 Divergences (Premium)

The system automatically detects discrepancies between Price and Oscillator:

Regular (R+ / R-): Solid Lines. Indicate a possible Reversal. (e.g., Price makes lower lows, but the oscillator makes higher lows).

Hidden (H+ / H-): Dashed Lines. Indicate trend Continuation. (e.g., Price makes higher lows, oscillator unloads making lower lows).

4. Technical Trading Strategies

Strategy A: Trend Following (Breakout)

Ideal for catching the start of a movement.

Setup: Wait for the histogram to be gray (consolidation).

Trigger: The histogram breaks the 1.64 threshold and becomes colored (Yellow/Orange).

Confirmation: The Dashboard reads "BULLISH" or "STRONG BULL".

Exit: When the histogram falls back below 1.64 or changes to the opposite color.

Strategy B: Mean Reversion (Contrarian)

Ideal for catching tops and bottoms (Top/Bottom fishing).

Setup: The histogram reaches extreme levels > 2.58 (Bright Green or Bright Red).

Trigger: A Regular Divergence (R+ or R-) appears. This indicates that momentum is exhausted even if the price is still moving.

Entry: At the close of the candle with the Divergence Label.

Strategy C: Multi-Timeframe (MTF)

To filter false signals on lower timeframes (e.g., 5 min).

Go to Settings > Multi-Timeframe.

Check "Enable MTF" and set "Higher Timeframe" to 1 Hour or 4 Hours.

Rule: Trade on your 5-min chart ONLY in the direction indicated by the higher timeframe Z-Score (e.g., if MTF is Green/Bullish, only take long positions).

5. Technical Notes & Troubleshooting

Repainting: The indicator does NOT repaint on the current timeframe. In MTF mode, historical bars may update until the higher timeframe candle closes (standard TradingView behavior).

Performance: If the chart appears slow on very low timeframes (1 second), disable "Divergences" to lighten the calculation load.

Chart Hygiene: The system includes a "Garbage Collector" that automatically deletes old divergence lines to keep the chart clean (max 30 visible objects).

Disclaimer: This tool provides statistical analysis and does not constitute financial advice. Always use stop losses and proper risk management.

Zscore

ZenAlgo - Coin XA multi input Z Score framework that compares the behavior of a selected symbol against several market wide aggregates: total crypto market metrics, alternative asset baskets, stablecoin dominance, Bitcoin, and risk composites. The script processes each data stream into comparable normalized values, evaluates their relationships, and derives a set of bias states, alerts, and real time conditions.

Data Preparation and Normalization

The indicator starts by gathering multiple reference series:

The chart ticker.

A basket representing non Bitcoin crypto assets.

Bitcoin market data.

Several total market variations (full, without Bitcoin, and additional categories).

A stablecoin dominance series.

A macro risk composite.

A daily anchored average used for context.

Each series is transformed into a normalized value using a lookback window. This produces multiple comparable Z Scores that reflect how far each series currently sits from its typical range. Smoothing is optionally applied to macro based values to reduce noise. These normalized values allow consistent comparisons across unrelated instruments.

This works because Z Score based normalization removes scale differences and makes directional deviations directly comparable across many independent metrics, which is necessary when the script later evaluates their relationships.

Cross and Momentum Detection

The script then evaluates structural interactions between the normalized series:

Whether one group rises above or falls below another.

Whether any of the series crosses over or under another.

Whether each series is currently advancing or declining.

Whether price is above or below the daily anchored average.

Whether stablecoin dominance is rising or falling.

Whether a sharp directional change occurs within a single bar.

Whether a multi threshold movement happens within a defined number of bars.

These checks capture relative strength shifts across the market. For example, an increase in the ticker combined with a decline in dominance suggests capital rotation toward the ticker, while the opposite suggests defensive flows. Using normalized changes allows these comparisons to be scale independent.

Combined Bias Logic

The indicator then evaluates a hierarchy of conditions that combine normalized relationships, momentum, and sharp movement checks. Each condition corresponds to a specific market state. The script tests the conditions in a defined order because later conditions depend on earlier structural checks.

Examples of combined evaluations include:

Cases where the ticker and alternative asset basket rise together while dominance declines.

Cases where both the ticker and alternatives fall together under a rising dominance series.

Conditions where several aggregates cross above or below dominance simultaneously.

Cases where multiple aggregates show coordinated sharp rises or sharp declines.

Situations where stablecoin dominance rises during weakness of other groups.

Situations where stablecoins fall while the ticker strengthens.

Conditions where the ticker rapidly moves through several thresholds in a short period.

The script assigns a bias label that corresponds to the earliest satisfied condition. This design ensures that highly distinctive and rare states take priority over broader or more common states. The reasoning behind this is that specific coordinated market moves provide clearer view than general divergence or simple momentum alone.

Crash and Pump Amplification

The script includes a section that detects extreme scenarios by combining several coordinated factors:

Very negative or very positive normalized values across multiple aggregates.

Sharp bar by bar declines or rises across key series.

Simultaneous movement in the risk composite and dominance.

These checks amplify certain bias states when market conditions show synchronized extreme movement. This provides additional clarity when multiple parts of the market behave in the same direction beyond typical deviation. The logic relies only on the relationships of the normalized values and their changes.

Fast Movement Detection

Two additional mechanisms evaluate movements over a short multi bar window.

A fast ticker move is detected when the current normalized ticker value differs from one several bars ago by multiple threshold increments.

A fast stablecoin rise or fall is detected using a step based method. The script checks for progression through sequential levels across the window while verifying whether the ticker moves in agreement or disagreement with the direction.

These mechanisms are intended to identify sudden acceleration or deceleration that standard normalized changes may not fully capture.

Season Scale

The script calculates a quantitative scale from minus 100 to plus 100 by evaluating several binary conditions:

Whether the ticker is above or below the alternative basket.

Whether the alternative basket is above or below dominance.

Whether the ticker and alternative basket are rising or falling.

Whether dominance is rising or falling.

Optionally whether price is above or below the anchored average.

Each condition contributes positively or negatively. The weighted combination produces the season value which is rounded. The naming of the state (Full Bull, Neutral, Full Bear etc.) is derived from where the score falls on the range.

This works because combining several directional tests across related groups provides a compressed singular measure of market structure.

Divergence Detection

The script includes divergence logic for Bitcoin, the alternative asset basket, and the chart ticker. It evaluates pivot highs and lows in price and compares them with pivot highs and lows in their respective normalized values. The script checks for pairs of pivot points where price moves in one direction while the normalized oscillator moves in the opposite. Both regular and hidden forms are evaluated.

This works because divergences highlight points where price and its normalized deviation disagree which often marks a structural imbalance.

Table Output

If enabled, the indicator displays a table showing the current normalized values of all monitored series along with color backgrounds reflecting structural relationships identified earlier. This supports interpretation without opening additional charts.

Visual Lines and Background

The script draws horizontal reference lines for several normalized levels using a fading mechanism if ghost mode is enabled. The background color changes according to the main season logic and intensifies with market wide deviations. Optional pulse effects are triggered when the bias state changes.

This works because visual context helps understand how extreme the current market state is relative to its typical historical range.

Alerts

The indicator creates alerts for all important structural states:

Bias state changes.

Fast ticker moves.

Fast stablecoin rises or falls.

Divergence based triggers.

Cross conditions corresponding to notable structural transitions.

These alerts correspond exactly to the logical conditions already described.

Added Value Compared to Free Alternatives

It evaluates many separate market wide aggregates simultaneously rather than relying on a single comparison.

It uses a consistent normalized framework so unrelated metrics become comparable.

It identifies multi series coordinated shifts which many simpler indicators cannot detect.

It provides a full deterministic bias state hierarchy that removes interpretation ambiguity.

It includes fast movement evaluation through multi level and multi bar logic.

It combines multiple categories of divergences with normalized values rather than only price based oscillators.

It provides a unified season value derived from several independent binary conditions.

Limitations and Situations Where It May Fall Short

Normalized values depend on the chosen lookback window and may behave differently under unusual volatility regimes.

If reference data feeds are incomplete or delayed the relationships may briefly reflect distorted values.

Extreme single bar events can cause temporary exaggeration of normalized values before stabilization.

Divergence detection depends on identifying pivots which may repaint until the pivot is confirmed.

Bias states rely on hierarchical evaluation so rare but extreme conditions will override more common states by design.

Sudden changes in stablecoin supply or methodology on the data source may influence stable dominance readings.

How to Interpret the Values

Positive normalized values indicate movement above the typical range while negative values indicate movement below the typical range.

The relationships between the ticker, the alternative asset basket, dominance, and the risk composite define the structural meaning of each bias.

The season value near plus 100 means most bull related conditions are simultaneously satisfied while near minus 100 means most bear related conditions are satisfied.

Sharp rise or fall conditions indicate abrupt movement beyond the usual deviation.

Cross conditions indicate structural transitions such as the ticker moving above or below another aggregate.

Divergences indicate inconsistency between price action and normalized deviation.

Best Practices for Practical Use

Use the bias state as a structural context rather than a direct entry or exit trigger.

Observe whether multiple aggregates align in the same direction since the script is designed around confirming coordinated behavior.

Combine the season value with the main bias state to evaluate whether short term view agree with broader conditions.

Use fast movement alerts for monitoring sudden volatility or intraday acceleration.

Use divergence conditions to identify potential exhaustion points when the main bias does not align with price behavior.

Reference the table and background colors for a quick visual overview of how several groups relate in the current moment.

RunRox - Pairs Screener📊 Pairs Screener is part of our premium suite for pair trading.

This indicator is designed to scan and rank the most profitable and optimal pairs for the Pairs Strategy. The screener can backtest multiple metrics on deep historical data and display results for many pairs against one base asset at the same time.

This allows you to quickly detect market inefficiencies and select the most promising pairs for live trading.

HOW DOES THIS STRATEGY WORK⁉️

The core idea of the strategy is described in detail in our main indicator Pairs Strategy from the same product line.

There you can find a full explanation of the concept, the math behind pair trading, and the internal logic of the engine.

The Pairs Screener is built on top of the same core technology as the main indicator and uses the same internal logic and calculations.

It is designed as a key companion tool to the main strategy: it helps you find tradeable pairs, evaluate current deviations, sort and filter lists of candidates, and much more. All of these features will be described in this post.

✅ KEY FEATURES

More than 400+ assets available for scanning

Forex assets

Crypto assets

Lower Timeframe Backtester Strategy support

Invert signals mode

Hedge Coefficient (position size balancing between both legs)

6 hedge modes

Stop Loss support

Take Profit support

Whitelist with your own custom asset list

Blacklist to exclude unwanted assets

Custom filters

12 tracking metrics for pair evaluation

Customizable alerts

And many other tools for fine-tuning your search

The screener runs backtests simultaneously across a large number of assets and calculates metrics automatically.

This helps you very quickly find pairs with strong structural relationships or current inefficiencies that can be used as the basis for your pair trading strategies.

⚙️ MAIN SETTINGS

The first section controls the core parameters of the screener: Score, correlation, asset groups for scanning, and other base settings. All major crypto and forex symbols are embedded directly into the screener.

Since there are more than 400 assets, it is technically impossible to analyze everything at once, so we grouped them into batches of 40 assets per group.

The workflow is simple:

Open the chart of the asset you want to use as the base ticker.

In the screener settings choose the market (Crypto or Forex).

Select a Group (for example, Group 1) and the indicator will scan all assets inside that group against your base ticker.

Then you switch to Group 2, Group 3, etc., and repeat the scan.

Embedded universe:

400+ assets total

350+ Crypto – split into 10 groups

70+ Forex – split into 3 groups

Below is a description of each setting.

🔸 Exclude Dates

Allows you to specify a period that should be excluded from analysis.

Useful for removing abnormal spikes, news events, or any non-typical segments that distort the statistics for your pairs.

🔸 Market

Defines which universe will be used to build pairs with the current main asset:

Crypto – 350+ crypto symbols

Forex – 70+ FX symbols

Whitelist – your own custom list of assets

🔸 Group

Selects the asset group to scan.

As mentioned above, assets are split into groups of about 40 instruments:

350+ Crypto → 10 groups

70+ Forex → 3 groups

The screener will calculate all metrics only for the group you select.

🔸 Lower Timeframe

This option enables deep history analysis.

Each TradingView plan has a limit on the number of visible bars (for example, 5,000 bars on the basic plan). In standard mode you would only get statistics for the last 5,000 bars of your current timeframe.

If you want a deeper backtest on a lower timeframe, you can do the following:

Suppose your target timeframe for analysis is 5 minutes.

Switch your chart to a 30-minute timeframe.

Enable Lower Timeframe in the indicator.

Select 5 minutes as the lower timeframe inside the screener.

In this mode the screener can reconstruct and analyze up to 99,000 bars of data for your assets. This allows you to evaluate pairs on a much deeper history and see whether the results are stable over a larger sample.

🔸 Method

Here you choose the deviation model:

preferred Z-Score or S-Score for your analysis,

plus you can enable Invert to search for negatively correlated pairs and calculate their profit correctly.

🔸 Period

This is the lookback period for Z/S Score.

It defines how many bars are used to calculate the deviation metric for each pair.

🔸 Correlation Period

This is the number of bars used to calculate correlation between the base asset and each candidate in the group.

The resulting correlation value is also displayed in the results table.

🔀 HEDGE COEFFICIENT

The next block of settings is related to the hedge coefficient.

This defines how much margin is allocated to each leg of the pair.

The classic approach in pair trading is to split the position equally between both assets.

For example, if you allocate 100 USD to a trade , the standard model would open 50 USD long on one asset and 50 USD short on the other.

This works well for pairs with similar volatility , such as BTCUSDT / ETHUSDT

However, if you use a pair like BTCUSDT / DOGEUSDT , the volatility of these assets is very different.

They can still be correlated, but their amplitude is not the same. While Bitcoin might move 2% , Dogecoin can move 10% over the same period.

Because of that, for pairs with strongly different volatility, we can use a hedge coefficient and, for example, enter with 30 USD on one leg and 70 USD on the other, taking the volatility difference into account.

This is the main idea behind the Hedge Coefficient section and its primary use.

The indicator includes 6 methods of calculating the coefficient:

Cumulative RMA

Beta OLS

Beta TLS

Beta EMA

RMA Range

RMA Delta

Each method uses a different formula to compute the hedge coefficient and to size the position based on different metrics of the assets.

We leave it to the trader to decide which algorithm works best for their specific pair and style.

Below are the settings inside this section:

🔹 Method

When Auto Hedge is enabled, you can select which method to use from the list above.

The chosen method will automatically calculate the hedge coefficient between the two legs.

🔹 Hedge Coefficient

This is the manual hedge ratio per trade when Auto Hedge is disabled.

By default it is set to 1, which means the position is opened 50/50 between the two assets.

🔹 Min Allowed Hedge Coef.

This is the minimum allowed hedge coefficient.

By default it is 0.2, which means the model will not go below a 20% / 80% split between the legs.

🔹 MA Length

For methods that use moving averages (for example Beta EMA), this parameter sets the period used to calculate the hedge coefficient.

💰 STRATEGY SETTINGS

This section defines the base backtesting settings for all assets in the screener.

Here you configure entries, exits, Stop Loss, and other parameters used to find the most optimal pairs for your strategy. 🔸 Commission %

In this field you set your broker’s fee percentage per trade.

The indicator automatically calculates the correct commission for each leg of every trade. You only need to input the real commission rate that your broker charges for volume. No additional manual calculations are required.

🔸 Qty $

The margin amount used for backtesting across all assets in the screener.

This margin is split between both legs of the pair either equally or according to the selected hedge coefficient.

🔸 Entry

The Z/S Score deviation level at which the backtest opens a trade for each pair.

🔸 Exit

The Z/S Score level at which the backtest closes trades for the tested assets.

🔸 Stop Loss

PnL threshold at which a trade is force-closed during the historical test.

🔸 Cooldown

Number of bars the strategy will wait after a Stop Loss before opening the next trade.

This block gives you flexible control over how your strategy is tested on 400+ assets, helping you standardize the rules and compare pairs under the exact same conditions.

🗒️ WHITELIST

In this section you can define your own custom list of assets for monitoring and backtesting.

This is useful if you want to work with symbols that are not included in the built-in lists, such as exotic crypto from smaller exchanges, specific stocks, or any custom universe 🔹 Exchange Prefix

Enter the exchange prefix used for your tickers.

Example: BINANCE, OANDA, etc.

🔹 Ticker Postfix

Enable this option if the tickers require a postfix.

Example 1: .P for Binance Futures perpetual contracts.

Example 2: USDT if you only provide the base asset in the ticker list.

🔹 Ticker List

Enter a comma-separated list of tickers to analyze.

Example 1: BTCUSDT, ETHUSDT, BNBUSDT (when the exchange prefix is set).

Example 2: BTC, ETH, BNB (when using postfix USDT).

Example 3: BINANCE:BTCUSDT.P, OANDA:EURUSD (when different exchanges are used and the prefix option is disabled).

This gives you full flexibility to build a screener universe that matches exactly the assets you trade.

⛔ BLACKLIST

In this section you can enable a blacklist of unwanted assets that should be skipped during analysis. Enter a comma-separated list of tickers to exclude from the screener:

Example 1: BTCUSDT, ETHUSDT

Example 2: BTC, ETH (all tickers that contain these symbols will be excluded)

This helps you quickly remove illiquid, noisy, or unwanted instruments from the results without changing your main groups or whitelist.

📈 DASHBOARD

This section controls the results dashboard: table position, style, and sorting logic.

Here is what you can configure:

Result Table – position of the results table on the chart.

Background / Text – colors and opacity for the table background and text.

Table Size – overall size of the results table (from 0 to 30).

Show Results – how many rows (pairs) to display in the table.

Sort by (stat) – which metric to use for sorting the results.

Available options: Profit Factor, Profit, Winrate, Correlation, Score.

This lets you quickly focus on the most interesting pairs according to the exact metric that matters most for your strategy.

📎 FILTER SETTINGS

This section lets you filter the results table by metric values.

For example, you can show only pairs with a minimum correlation of 0.8 to focus on more stable relationships. 🔸 Min Correlation

Minimum allowed correlation between the two assets over the selected lookback period.

🔸 Min Score

Minimum absolute Score (Z-Score or S-Score) required to include a pair in the results.

For example, 2.0 means only pairs with Score >= 2.0 or <= -2.0 will be displayed.

🔸 Min Winrate

Minimum win rate percentage for a pair to be included in the table.

🔸 Min Profit Factor

Minimum profit factor required for a pair to stay in the results. These filters help you quickly narrow the list down to pairs that meet your quality criteria and match your risk profile.

📌 COLUMN SELECTION

This section lets you fully customize which metrics are displayed in the results table.

You can enable or hide any column to focus only on the data you need to identify the best pairs for trading. The screener allows you to show up to 12 metrics at the same time, which gives a detailed view of pair quality. Available columns:

🔹 Exchange Prefix

Show the exchange prefix in the ticker.

🔹 Correlation

Correlation between the two assets’ prices over the lookback period.

🔹 Score

Current Score value (Z-Score or S-Score).

On lower timeframe research, Score is not displayed.

🔹 Spread

Shows spread as % change since entry.

Positive value = profit on the main position.

🔹 Unrealized PnL

Shows unrealized PnL as a $ value based on current prices.

🔹 Profit

Total profit from all trades: Gross Profit − Gross Loss.

🔹 Winrate

Percentage of profitable trades out of all executed trades.

🔹 Profit Factor

Gross Profit / Gross Loss.

🔹 Trades

Total number of trades.

🔹 Max Drawdown

Maximum observed loss from peak to trough before a new peak is made.

🔹 Max Loss

Largest loss recorded on a single trade.

🔹 Long/Short Profit

Separate profit/loss for long trades and short trades.

🔹 Avg. Trade Time

Average duration of trades.

All these metrics are designed to help you quickly identify the strongest pairs for your strategy.

You can change colors, opacity, and hide any columns that are not relevant to your workflow.

🔔 ALERT

The alert system in this screener works in a specific way.

Alerts are tied directly to the filters you set in the Filter Settings section:

Minimum Correlation

Minimum Score

Minimum Winrate

Minimum Profit Factor

You can configure alerts to trigger when a new pair appears that matches all your filter conditions. 💡 Example

You set:

Minimum Score = 3

Then you create an alert based on the screener.

When any pair reaches a Score greater than +3 or less than −3, you will receive a notification.

This is how alerts work in this screener.

The idea is to deliver the most relevant information about the current market situation without forcing you to watch the screener all the time.

Supported placeholders for alert messages: {{ticker_1}} – main ticker (the one on the chart).

{{ticker_2}} – the paired ticker listed in the table.

{{corr}} – correlation value.

{{score}} – Score value (Z-Score or S-Score).

{{time}} – bar open time (UTC).

{{timenow}} – alert trigger time (UTC). You can use these placeholders to build alert text or JSON payloads in any format required by your tools.

The screener is designed to significantly enhance your pair trading workflow: it helps you quickly identify working pairs and current market inefficiencies, and with the alert system you can react to opportunities without constantly sitting in front of the screen.

Always remember that past performance does not guarantee future results.

Use the screener data within a risk-controlled trading system and adjust position sizing according to your own risk management rules.

RunRox - Pairs Strategy🧬 Pairs Strategy is a new indicator by RunRox included in our premium subscription.

It is a specialized tool for trading pairs, built around working with two correlated instruments at the same time.

The indicator is designed specifically for pair trading logic: it helps track the relationship between two assets, identify statistical deviations, and generate signals for opening and managing long/short combinations on both legs of the pair.

Below in this description I will go through the core functions of the indicator and the main concepts behind the strategy so you can clearly understand how to apply it in your trading.

📌 CONCEPT

The core idea of pair trading is to find and trade correlated instruments that usually move in a similar way.

When these two assets temporarily diverge from each other, a trading opportunity appears.

In such moments, the relatively overvalued asset is sold (short leg), and the relatively undervalued asset is bought (long leg).

When the spread between them narrows and both instruments revert back toward their typical relationship (mean), the position is closed and the trader captures the profit from this convergence.

In practice, one leg of the pair can end up in a loss while the other generates a larger profit.

Due to the difference in performance between the two assets, the combined result of the pair trade can still be positive.

✅ KEY FEATURES:

2 deviation types (Z-Score and S-Score)

Invert signals mode

Hedge Coefficient (position size balancing between both legs)

6 hedge modes

Entries based on Score or RSI

Extra entries based on Score or Spread

Stop Loss

Take Profit

RSI Filter

RSI Pivot Mode

Built-in Backtester Strategy

Lower Timeframe Backtester Strategy

Live trade panel for current position

Equity curve chart

21 performance metrics in the backtester

2 alert types

*And many more fine-tuning options for pair trading

🔗 SCORE

Score is the core deviation metric between the two assets in the pair.

For example, if you are trading ETHUSDT/BTCUSDT, the indicator analyzes the relationship ETH/BTC, and when one leg temporarily diverges from the other, this difference is reflected in the Score value.

In other words, Score shows how much the current spread between the two instruments deviates from its typical state and is used as the main signal source for pair entries and exits.

In the screenshot above you can see how Score looks in our indicator.

Depending on how large the difference is between the two assets, the Score value can move in a range from −N to +N

When Score is in the −N zone, this is a 🟢 long zone for the first asset and a short zone for the second.

Using the ETH/BTC example: when Score is deeply negative, you open a long on ETH and a short on BTC at the same time, then close both legs when Score returns back to the 0 zone (balance between the two assets).

When Score is in the +N zone, this is a 🔴 short zone for the first asset and a long zone for the second.

In the same ETH/BTC example: when Score is strongly positive, you short ETH and long BTC, and again close both positions when Score comes back to the neutral 0 zone.

☯️ Z/S SCORE

Inside the indicator we added two different formulas for calculating the spread between the two legs of the pair: Z-Score and S-Score.

These approaches measure deviation in different ways and can produce slightly different signals depending on the chosen pair and its behavior.

This allows you to switch between Z-Score and S-Score and choose the method that gives more stable and cleaner signals for your specific instruments.

As you can see in the screenshot above, we used the same pair but applied different Score types to measure the spread and deviation from the norm.

🟣 Z-Score – generated 9 entry signals .

It reacts to price fluctuations more smoothly and usually stays within a range of approximately −8 to +8 .

🟠 S-Score – generated 5 entry signals .

It reacts to price changes more aggressively and produces wider deviations, often reaching −15 to +15 .

This gives traders the choice between a more sensitive but smoother model (Z-Score) and a more selective, stronger-deviation model (S-Score)

⁉️ HOW DOES THE STRATEGY WORK

Here is a basic example of how you can trade this pair trading strategy using our indicator and its signals.

In the classic approach the trade consists of one initial entry and several scale-ins (averaging) if the spread continues to move against the position.

The first entry is opened when Score reaches a standard deviation of −2 or +2.

If price does not revert to the mean and moves further against the position so that Score expands to −3 or +3, the strategy performs the first scale-in.

If Score extends to −4 or +4, a second scale-in is added.

If the spread grows even more and Score reaches −5 or +5, a third scale-in is executed.

In our indicator the number of averaging steps can be up to 4 scale-ins .

After that the position waits until Score returns back to the 0 level , where the whole pair position is closed.

This is the standard model of classical pair trading.

However there are many variations:

using Stop Loss and Take Profit,

exiting earlier or later than the 0 zone,

scaling in not by Score but by Spread, since Score is not linear while Spread is linear,

entering when RSI on both tickers shows opposite extremes, for example RSI 20 on one asset and RSI 80 on the other, and so on.

The number of possible trading styles for this strategy is very large.

We designed the indicator to cover as many of these variations as possible and added flexible tools so you can build your own pair trading logic on top of it.

Below is an example of a classic pair trade with two entries: one main entry and one extra entry (scale-in) .

The pair SUIUSDT / PENGUUSDT shows a high correlation, and on one of the trades the sequence looked like this:

A −2 Score deviation occurred into the long zone and triggered the Main Entry .

🔹 Main Entry

Long SUIUSDT – Margin: 5,000 USD, Entry price: 1.5708

Short PENGUUSDT – Margin: 5,000 USD, Entry price: 0.011793

Price then moved further against the position, Score went deeper into deviation, and the strategy added one extra entry.

🔸 Extra Entry

Long SUIUSDT – Margin: 5,000 USD, Entry price: 1.5938

Short PENGUUSDT – Margin: 5,000 USD, Entry price: 0.012173

The trade was closed when Score reverted back toward the 0 zone (mean reversion of the spread):

❎ Exit

SUIUSDT P&L: −403.34 USD, Exit price: 1.5184

PENGUUSDT P&L: +743.73 USD, Exit price: 0.011089

✅ Total P&L: +340.39 USD

With a total margin of 10,000 USD used per side (20,000 USD combined), this trade yielded around +1.7% on the deployed margin.

On different assets the size and speed of the spread movement will vary, but the principle remains the same.

This is just one example to illustrate how the strategy works in practice using simplified theoretical balances.

⚙️ MAIN SETTINGS

After explaining how the strategy works, we can move to the indicator settings and their logic.

The first block is Main Settings, which controls how the pair is built, how the spread is calculated, and how the backtest is performed.

The core idea of the indicator is to backtest historical data, generate entry signals, show open-position parameters, and provide all necessary metrics for both discretionary and algorithmic trading.

This is a complete framework for analyzing a pair of assets and building a trading system around them. Below I will go through the main parameters one by one.

🔹 Exclude Dates

Allows you to exclude abnormal periods in the pair’s history to remove outlier trades from the backtest.

This is useful when the market experienced extreme news events, listing spikes, or other non-typical situations that distort statistics.

🔹 Pair

Here you select the second asset for your pair.

For example, if your main chart is BTCUSDT, in this field you choose a correlated asset such as ETHUSDT, and the working pair becomes BTCUSDT / ETHUSDT.

The indicator then calculates spread, Score, and all related metrics based on this asset combination.

🔹 Lower Timeframe

This is a special mode for backtesting on a lower timeframe while using a higher timeframe chart to extend the history limit.

For example, if your TradingView plan provides only 5,000 bars of history on the current timeframe, you can switch your chart to a higher timeframe and select a lower timeframe in this setting.

The indicator will then reconstruct the pair logic using up to 99,000 bars of lower timeframe data for backtesting.

This allows you to test the pair on a much longer historical period and find more stable combinations of assets.

🔹 Method

Here you choose which deviation model you want to use: Z-Score or S-Score.

Both methods calculate spread deviation but use different formulas, which can give different signal behavior depending on the pair.

Examples of these two methods are shown earlier in this description.

🔹 Period

This parameter defines how many bars are used to calculate the average deviation for the pair.

If you set Period = 300, the indicator looks back 300 bars and calculates the typical spread deviation over that window.

For example, if the average deviation over 300 bars is around 1%, then a move to 2% or more will push Z/S Score closer to its boundary levels, since such a deviation is considered abnormal for that lookback period.

A larger Period means that only bigger deviations will be treated as anomalies.

A smaller Period makes the model more sensitive and treats smaller deviations as anomalies.

This allows you to tune how aggressive or conservative your pair trading signals should be.

🔹 Invert

This setting is used for negatively correlated pairs.

Some instruments have a positive correlation in the range from +0.8 to +1.0 (strong positive correlation), while others show a negative correlation from −0.8 to −1.0, meaning they usually move in opposite directions.

A classic example is the pair EURUSD and DXY.

As shown in the screenshot above, these instruments often have strong negative correlation due to macro factors and typically move in opposite directions: when EURUSD is rising, DXY is falling, and vice versa.

Such pairs can also be traded with our indicator.

To do this, we use the Invert option, which effectively flips one of the assets (as shown in the screenshot below). After inversion, both instruments are brought to a “same-direction” behavior from the model’s point of view.

From there, you trade the pair in the same way as a positively correlated one:

you open both legs in the same direction (both long or both short) depending on the spread and Score, and then wait for the spread between the inverted pair to converge back toward its mean.

🔀 HEDGE COEFFICIENT

The next block of settings is related to the hedge coefficient.

This defines how much margin is allocated to each leg of the pair.

The classic approach in pair trading is to split the position equally between both assets.

For example, if you allocate 100 USD to a trade , the standard model would open 50 USD long on one asset and 50 USD short on the other.

This works well for pairs with similar volatility , such as BTCUSDT / ETHUSDT

However, if you use a pair like BTCUSDT / DOGEUSDT , the volatility of these assets is very different.

They can still be correlated, but their amplitude is not the same. While Bitcoin might move 2% , Dogecoin can move 10% over the same period.

Because of that, for pairs with strongly different volatility, we can use a hedge coefficient and, for example, enter with 30 USD on one leg and 70 USD on the other, taking the volatility difference into account.

This is the main idea behind the Hedge Coefficient section and its primary use.

The indicator includes 6 methods of calculating the coefficient:

Cumulative RMA

Beta OLS

Beta TLS

Beta EMA

RMA Range

RMA Delta

Each method uses a different formula to compute the hedge coefficient and to size the position based on different metrics of the assets.

We leave it to the trader to decide which algorithm works best for their specific pair and style.

Below are the settings inside this section:

🔹 Method

When Auto Hedge is enabled, you can select which method to use from the list above.

The chosen method will automatically calculate the hedge coefficient between the two legs.

🔹 Hedge Coefficient

This is the manual hedge ratio per trade when Auto Hedge is disabled.

By default it is set to 1, which means the position is opened 50/50 between the two assets.

🔹 Min Allowed Hedge Coef.

This is the minimum allowed hedge coefficient.

By default it is 0.2, which means the model will not go below a 20% / 80% split between the legs.

🔹 MA Length

For methods that use moving averages (for example Beta EMA), this parameter sets the period used to calculate the hedge coefficient.

🛠️ STRATEGY SETTINGS

The next important block is Strategy Settings .

Here you define the core parameters used for backtesting: trading commission, position size, entry / exit logic, Stop Loss, Take Profit, and other rules that describe how you want the strategy to operate.

Below are all parameters with a detailed explanation.

🔸 Commission %

In this field you set your broker’s fee percentage per trade .

The indicator automatically calculates the correct commission for each leg of every trade. You only need to input the real commission rate that your broker charges for volume. No additional manual calculations are required.

🔸 Main Entry Mode

There are two options for the main entry:

Score - This is the primary entry method based on Z/S Score.

When Score reaches the deviation level defined in the settings below, the strategy opens the first position.

For example, if you set “Entry at 2 deviations”, the trade will be opened when Score hits ±2.

RSI Only - Alternative entry method based on RSI divergence between the two assets.

The exact RSI levels are defined in the RSI settings section below.

For example, if you set the entry threshold at 30, then when one asset has RSI below 30 and the second one has RSI above 70, the first entry will be triggered.

🔸 Extra Entries Mode

This defines how scale-ins (averaging) are executed. There are two modes:

Score - Works the same way as the main entry, but for additional entries.

For example, the main entry can be at 2 deviations, the first scale-in at 3, the second at 4, etc.

Spread - This mode uses the Spread (difference between the two assets) starting from the main entry moment.

As the spread continues to widen, the strategy can add extra entries based on spread growth rather than Score.

Since Score is a non-linear metric and Spread is linear, in some configurations averaging by Spread can produce better results than averaging by Score. This is pair- and strategy-dependent. 🔸 Entry parameters

Deviation / Spread threshold

Entry size

Main Entry – first field (deviation / spread), second field (position size)

Entry 2 – first field (deviation / spread), second field (position size)

Entry 3 – first field (deviation / spread), second field (position size)

Entry 4 – first field (deviation / spread), second field (position size)

This allows you to define up to four scaling steps with different triggers and different sizing.

🔸 Exit Level

This parameter defines at what Score level you want to exit the trade.

By default it is 0, which means the backtester closes the position when Score returns to the neutral (0) zone.

You can also use positive or negative values. Example:

Assume your main entry is configured at a 3 deviation.

You can exit at the 0 level, or you can set Exit Level = 2.

If your initial entry was at −3, the position will be closed when Score reaches +2.

If your initial entry was at +3, the position will be closed when Score reaches −2.

This approach can increase the profit per trade due to a larger captured spread, but it may also increase the holding time of the position.

🔸 Stop Loss

Here you define the maximum loss per trade in PnL units.

If a trade reaches the negative PnL value specified in this field and the Stop Loss option is enabled, the indicator will close the trade at a loss.

The Cooldown parameter sets a pause after a losing trade:

the strategy will wait a specified number of bars before opening the next trade.

🔸 Take Profit

Works similar to Stop Loss but for profit targets.

You set the desired PnL value you want to reach.

The trade will be closed when either the Take Profit target is hit or when Score reaches the exit level defined in the settings, whichever occurs first (depending on your configuration).

🔸 Show Qty in currency

When enabled, trade size is displayed in currency (USD) instead of token quantity.

This is useful for quickly understanding position size in monetary terms.

You will see this in the Current Trade panel, which is described later.

🔸 Size Rounding

Controls how many decimal places are used when rounding position size (from 0 to 10 digits after the decimal).

This is also used for the Current Trade panel so you can adjust how detailed or compact the size display should be.

📊 RSI FILTERS

This section is used for additional trade filtering.

RSI can be used in two ways:

as a primary entry signal,

or as an extra filter for entries based on Z/S Score.

If in the Strategy Settings the Main Entry Mode is set to RSI, then RSI becomes the main trigger for opening a position.

In this case a trade is opened when the RSI of the two assets reaches opposite zones.

Example:

If the threshold is set to 30, then:

when one asset has RSI below 30, and

the second asset has RSI above 70 (100 − 30),

the strategy opens the first entry.

All extra entries after that will be executed either by Spread or by Z/S Score, depending on your Extra Entries Mode.

Below are the parameters in this block:

RSI Length – standard RSI period setting.

RSI Pivot Mode – when enabled, RSI is used as an additional filter together with Z/S Score. The indicator looks for a reversal pattern on RSI (pivot behavior). If RSI forms a reversal structure, the trade is allowed to open. If not, the signal is skipped until a proper RSI pivot is formed.

Entry RSI Filter – here you define the RSI thresholds used for RSI-based entries. These are the same boundary levels described in the example above.

Overall, this section helps filter out lower-quality trades using additional RSI conditions or lets you build RSI-only entry logic based on extreme levels.

🎨 MAIN CHART STYLING

This section controls the visual appearance of trades on the main chart.

You can customize how the second asset line is drawn, as well as the icons for entries, scale-ins, and exits, including their size and style.

▫️ Price Line

This is the line that shows the price of the second asset and the relative difference between the two instruments.

You can adjust the line thickness and color to make it more readable on your chart.

▫️ Adjust Price Line by Hedge Coefficient

When this option is enabled, the second asset’s line is normalized by the hedge coefficient.

If you turn it off, the hedge coefficient will not be applied to the second asset’s line, and it will be displayed in raw form.

▫️ Entry Label

Here you can customize how the entry markers look:

choose the color, icon style, and size of the label that marks each trade entry and scale-in on the chart.

▫️ Exit Label

Similarly, you can define the color, icon style, and size of the label used for exits.

This helps visually separate entries and exits and makes it easier to read the trade history directly from the chart.

🎯 INDICATOR PANEL

This section controls the settings of the indicator panel, which works like an oscillator and allows you to visualize multiple metrics in one place.

You can flexibly enable, style, and scale each parameter.

🔹 Score

Displays the main deviation metric between the two assets.

You can customize the color and line thickness of the Score plot.

🔹 Spread

Shows the spread between the two assets.

It starts calculating from the moment the trade is opened.

You can adjust its color and thickness for better visibility.

🔹 Total Profit

Displays the cumulative profit for this pair and strategy as a line that grows (or falls) over time.

Color, opacity, and line thickness can be customized.

🔹 Unrealized PNL

Once a trade is opened, this line shows the current PnL of the active position.

It also lets you see historical drawdowns on the pair.

Color and thickness can be adjusted.

🔹 Released PNL

Shows the realized PnL of each closed trade as bars.

Useful for quickly evaluating the result of every individual trade in the backtest.

🔹 Correlation

Plots the correlation coefficient between the two assets as a graph, so you can visually track how stable or unstable the relationship between them is over time.

🔹 Hedge Coefficient

Shows the hedge coefficient as a line, which helps understand how the model is rebalancing exposure between the two legs depending on their behavior.

For each metric there is also a 📎 Stretch option.

Stretch allows you to compress or expand the scale of a specific line to visually align metrics with different ranges on the same panel and make the chart easier to read.

📈 PROFIT CHART

Since TradingView does not natively support proper backtesting for pair trading, this indicator includes its own profit curve for the pair.

You can visually see how the strategy performed over historical data: whether there were deep drawdowns, abnormal profit spikes, or stable equity growth over time. This makes it much easier to evaluate the quality of the pair and the strategy on history.

In the settings of this section you can flexibly customize how the profit chart is displayed:

labels, position of the panel, padding, and other visual details.

Everything depends on your personal preferences, so we give full control over styling:

you can adjust the look of the profit chart to match your layout or completely hide it from the chart if you do not need it.

📌 CURRENT TRADE

This section controls the current trade table.

When there is an active trade on the chart, the panel displays all key information for the open position:

direction for each ticker (long or short),

required position size for each leg,

entry price for both assets,

and real-time PnL for each leg separately,

so you always have a clear view of the current situation.

The main thing you can do with this table is customize its appearance:

you can change the size, position on the chart, background and text colors, as well as separate coloring for positive / negative PnL and different colors for long and short positions.

📅 BACKTEST RESULTS

The next key block is Backtest Results.

This results table with detailed metrics gives you an extended view of how the pair and strategy perform: win rate, profit factor, long/short breakdown, and more than 20 additional stats that help you evaluate the potential of your setup.

⚠️ First of all, it is important to note ⚠️

past performance does not guarantee future results.

Every trader must keep this in mind and factor these risks into their strategy.

The table shows metrics in three cuts:

All Entries

Main Entries

Extra Entries (scale-ins)

Core metrics:

Profit – total profit for each entry type.

Winrate – win rate for this pair.

Profit Factor – ratio of gross profit to gross loss for the strategy.

Trades – number of trades in the backtest.

Wins – number of winning trades.

Losses – number of losing trades.

Long Profit – profit generated by long positions.

Short Profit – profit generated by short positions.

Longs – total number of long trades.

Shorts – total number of short trades.

Avg. Time – average time spent in a trade.

Additional metrics for a deeper evaluation of the pair:

Correlation – current correlation between the two assets in the pair.

Bars Processed – number of bars used in the analysis.

Max Drawdown – maximum historical drawdown of the strategy.

Biggest Loss – the largest single losing trade in the backtest.

Recommended Hedge – recommended hedge coefficient based on historical behavior.

Max Spread – maximum positive spread observed in history.

Min Spread – maximum negative spread observed in history.

Avg. Max Spread – average of positive extreme spread values (above 0).

Avg. Min Spread – average of negative extreme spread values (below 0).

Avg Positive Spread – average positive spread across all trades (only values above 0).

Avg Negative Spread – average negative spread across all trades (only values below 0).

Current Spread – current spread between the assets when a trade is open.

These metrics together allow you to quickly assess how stable the pair is, how the risk/return profile looks, and whether the strategy parameters are suitable for live trading. You can fully customize this results table to fit your workflow:

hide metrics you don’t need, change colors, opacity, and other visual styles, and reorder the focus of the stats according to your trading style.

This way the backtest block can show only the metrics that matter to you most and remain clean and readable during analysis.

📣 ALERTS

The next section is dedicated to alerts.

Here you can configure all signals you need, both for manual trading and for full automation of this pair trading strategy. This block is designed to cover most practical use cases. The indicator supports two alert modes:

Single Alert – one universal custom alert for all events.

Two Alerts – separate alerts for each ticker so you can receive different messages per asset.

Available alert events:

Main Entry – when the main entry is triggered.

Entry 2 – when the first scale-in is executed.

Entry 3 – when the second scale-in is executed.

Entry 4 – when the third scale-in is executed.

Exit Alert – when the position is closed.

StopLoss Alert – when Stop Loss is hit.

TakeProfit Alert – when Take Profit is hit.

All alerts are fully customizable and support a set of placeholders for building structured messages or JSON payloads.

🔹1 Alert Type

List of supported placeholders: {{event}} – trigger name ('Entry 1', 'Exit').

{{dir_1}} – 'Long' or 'Short' for the main ticker.

{{dir_2}} – 'Long' or 'Short' for the other ticker.

{{action_1}} – 'Buy', 'Sell' or 'Close' for the main ticker.

{{action_2}} – 'Buy', 'Sell' or 'Close' for the other ticker.

{{price_1}} – price for the main ticker.

{{price_2}} – price for the other ticker.

{{qty_1}} – order size for the main ticker.

{{qty_2}} – order size for the other ticker.

{{ticker_1}} – main ticker (e.g. 'BTCUSD').

{{ticker_2}} – other ticker (e.g. 'ETHUSD').

{{time}} – candle open time in UTC.

{{timenow}} – signal time in UTC.

🔹2 Alert Type

List of supported placeholders: {{event}} – trigger name ('Entry 1', 'Exit', 'SL', 'TP').

{{action}} – 'Buy', 'Sell' or 'Close'.

{{price}} – order price.

{{qty}} – order size.

{{ticker}} – ticker (e.g. 'BTCUSD').

{{time}} – candle open time in UTC.

{{timenow}} – signal time in UTC. You can use these placeholders to build any JSON structure or custom alert text required by your trading bot, exchange API, or automation service.

In this post I’ve explained how the indicator works, the core concept behind this pair trading strategy, and shown practical examples of trades together with a detailed breakdown of each unique feature inside the tool.

We have invested a lot of work into building this indicator and we truly hope it will help you trade pair strategies more efficiently and more profitably by giving you structured, strategy-specific information that is difficult to obtain in any other way.

⚠️ Please also remember that past performance does not guarantee future results.

Always evaluate the risks, the robustness of your setup, and your own risk tolerance before entering any position, and make independent, well-considered decisions when using this or any other strategy.

Pair Correlation Master [Macro]The Main Idea

Trading represents a constant battle between Systemic Flows (the whole market moving together) and Idiosyncratic Moves (one specific asset moving on its own).

This tool allows you to monitor a "basket" of 4 assets simultaneously (e.g., the major USD pairs). It answers the most important question in forex and multi-asset trading: "Is this move happening because the Dollar is weak, or because the Euro is strong?"

It separates the "Signal" (the unique move) from the "Noise" (the herd movement).

1. The Chart Lines: The "Race" (Macro Trend)

Think of the lines on your chart as a long-distance race. They visualize the performance of all 4 assets over the last 200 candles (adjustable).

- Bunched Together: If all lines are moving in the same direction, the market is highly correlated. (e.g., "The Dollar is selling off everywhere").

- Fanning Out: If the lines are spreading apart, specific currencies are outperforming others.

- The Zero Line: This is the starting line.

--- Above 0: The pair is in a macro uptrend.

--- Below 0: The pair is in a macro downtrend.

2. The Dashboard: The "Health Check" (Micro Data)

The table in the top right gives you the immediate statistics for right now.

- A. The Z-Score (The Rubber Band)

This measures how "stretched" price is compared to its normal behavior.

- White (< 2.0): Normal trading activity.

- Orange (> 2.0): The price is stretching. Warning sign.

- Red (> 3.0): Critical Stretch. The rubber band is pulled to its limit. Statistically, a pullback or pause is highly likely.

B. The Star (★)

The script automatically calculates the average behavior of your group. If one asset is behaving completely differently from the rest, it marks it with a Star (★).

- Example: EURUSD, GBPUSD, and NZDUSD are flat, but AUDUSD is rallying hard. AUDUSD gets the ★. This is where the unique opportunity lies.

🎯 Best Uses: 4H & Daily Timeframes

This indicator is tuned for "Macro" analysis. It works best on the "4-Hour" and "Daily" charts to filter out intraday noise and capture swing trading moves.

- Strategy 1: The "Rubber Band" Snap (Mean Reversion)

- Setup: Look for a Z-Score in the RED (> 3.0) on the Daily timeframe.

- Action: This indicates an unsustainable move. Look for reversals or exhaustion patterns to trade against the trend back toward the mean.

- Strategy 2: The "Lone Wolf" (Trend Following)

- Setup: Look for the asset with the Star (★).

- Action: If the whole basket is flat (Balanced), but the Star asset is breaking out, that creates a high-quality trend trade because that specific currency has its own catalyst (News/Earnings).

- Strategy 3: Systemic Flows (Basket Trading)

- Setup: The dashboard footer says "⚠️ SYSTEMIC MOVE."

- Action: This means everything is moving together (e.g., a massive USD crash). Don't look for unique setups; just join the trend on the strongest pair.

Dashboard Footer Key

The bottom of the table summarizes the current state of the market for you:

- Balanced / Rangebound: The market is quiet. Good for range trading.

- Focus: : Trade this specific pair. It is moving independently.

- Systemic Move: The whole basket is moving violently. Trade the momentum.

p.s. Suggestion - apply and use on the chart rather than an oscillator.

ZScore SemiConductoresZ-Score of Semiconductor Sector Volume

This custom Pine Script indicator applies a Z-Score calculation to the aggregated trading volume of leading semiconductor companies. The goal is to highlight statistical extremes in sector activity that may signal unusual market behavior.

🔧 How it works

- Fixed ticker list: NVDA, AVGO, TSM, AMD, ASML, MU, ARM, ON, TXN, QCOM, INTC.

- Aggregate volume: The script sums the trading volume of all tickers in the list for the selected timeframe.

- Z-Score calculation:

- Moving average and standard deviation are computed over a configurable window (default = 50 bars).

- Formula:

Z= (Current Volume - Mean) / Standard Deviation

Visualization:

- Z-Score plotted in green.

- Reference lines at 0, ±1σ, ±2σ.

- Labels (triangles) mark critical signals when Z > +2 or Z < -2.

📈 Why it matters

- Detects abnormal surges or drops in sector-wide volume.

- Highlights potential euphoria (+2σ) or panic (-2σ) moments.

- Useful as a filter for trading strategies or as a sector-level alert system.

⚠️ Disclaimer: This script is for educational purposes only and not financial advice

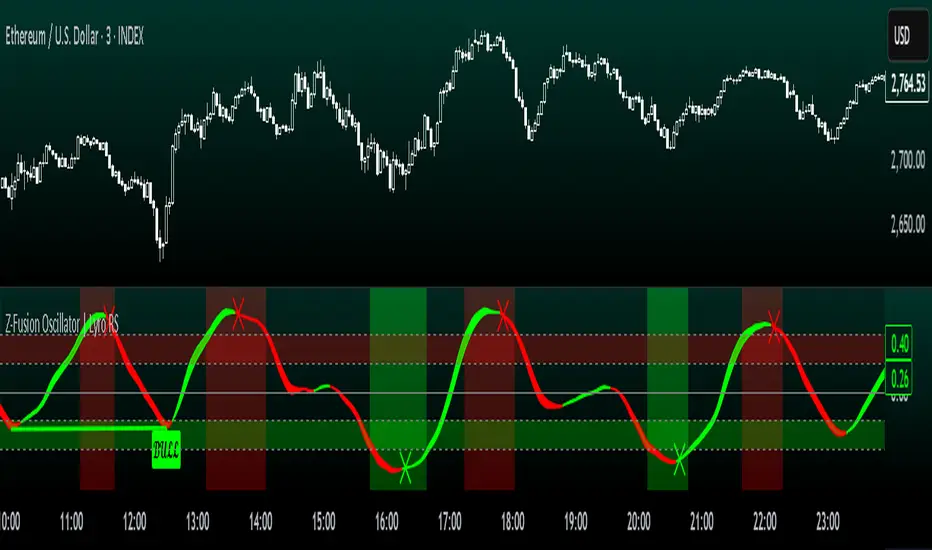

Z-Fusion Oscillator | Lyro RSThe Z-Fusion Oscillator converts five momentum indicators into Z-scores and blends them into one normalized signal that adapts across markets.

By combining normalization, smoothing, and divergence detection, users can easily identify when momentum is accelerating, weakening, reversing, or entering extreme zones

🔶 USAGE

The Z-Fusion Oscillator is designed to give traders a unified reading of market momentum—removing the noise of comparing tools that normally run on different scales.

By transforming RSI, MACD histogram, Stochastic, Momentum, and Rate of Change into Z-scores, this tool standardizes all inputs, making trend strength and shifts easier to interpret.

A dual-line system (fast Z-fusion line + slower baseline) highlights turning points, while overbought/oversold bands and “X-marks” help traders spot exhaustion and potential reversals.

🔹 Unified Momentum Structure

The indicator’s core strength comes from combining five Z-scored signals into one average.

Which makes momentum behavior more consistent across assets, reduces false extremes, and highlights true shifts in trend conviction.

🔹 Divergence Detection

The tool includes fully integrated divergence detection:

Regular Bullish Divergence: Price makes a lower low while Z-Fusion forms a higher low.

Regular Bearish Divergence: Price makes a higher high while Z-Fusion forms a lower high

Bullish and bearish divergences are marked directly on the oscillator with labels and colored pivot connections, making hidden momentum shifts obvious.

🔹 Visual Extremes

Two sets of upper and lower Z-score thresholds help identify:

Extreme overbought surges

Extreme oversold drops

Reversal zones

Potential exhaustion conditions

Background coloring reinforces when the oscillator moves beyond major levels, helping traders quickly assess momentum pressure.

🔹 Detecting Momentum Anomalies

Z-scores allow the oscillator to highlight when market momentum behaves abnormally relative to its own recent history.

For example:

The oscillator reaching +1 or –1 after an extended trend may indicate a climax.

A sharp Z-score reversal within an extreme zone can signal a trend exhaustion or a corrective move.

Divergences often appear earlier due to normalization smoothing out indicator noise.

This makes the Z-Fusion Oscillator particularly useful for spotting subtle shifts in trend direction that traditional indicators may miss.

🔶 DETAILS

🔹 Composite Z-Score Framework

Each momentum tool is smoothed, normalized, and transformed:

RSI → EMA-smoothed, Z-scored

MACD histogram → Z-scored

Stochastic → EMA + SMA smoothing, then Z-scored

Momentum → EMA-smoothed, Z-scored

Rate of Change → EMA-smoothed, Z-scored

These are averaged into one composite Z-score to provide a consistent reading across assets and market conditions.

🔹 Fusion Trend Lines

Two lines serve as the core signal:

Fast Line (savg) – reacts quicker to trend changes

Slow Line (savg2) – acts as a baseline filter

Crossovers between these lines highlight momentum shifts, while their color reflects trend bias.

🔹 Overbought/Oversold Zones

Two upper and two lower Z-score thresholds define “zones”:

Upper zones highlight overheated momentum or potential bearish reversals

Lower zones highlight depressed momentum or potential bullish reversals

Filled regions and background colors help visually confirm extreme conditions.

🔹 Pivot-Based Divergence Engine

The script includes filtered pivot detection with customizable look-backs and range limits to ensure divergences are meaningful, not noise-driven.

🔶 SETTINGS

🔹 Indicator Settings

Source — Price series used for all calculations.

Z-Score Length — Lookback period for Z-score normalization.

Z-Score MA Length — Smoothing length for the fusion signal lines.

Overbought/Oversold Levels — Four customizable threshold lines.

Color Palette — Choose from preset themes or define custom colors.

🔹 RSI

Length — RSI calculation period.

EMA Smoothing Length — Smooths RSI before Z-score conversion.

🔹 MACD

Fast Length — Fast EMA length.

Slow Length — Slow EMA length.

Signal Line Length — MACD signal smoothing.

🔹 Stochastic

%K Length — Main stochastic length.

EMA Smoothing — Smooths %K for stability.

%D Length — Smoothing for the signal line.

🔹 Momentum

Length — Momentum lookback.

EMA Smoothing — Smooths momentum before Z-scoring.

🔹 Rate of Change

Length — ROC lookback.

EMA Smoothing — Smooths ROC values.

🔹 Divergence

Enable/Disable Divergence Detection — Toggle divergence engine.

Pivot Left/Right Lookback — Defines pivot detection sensitivity.

Detection Range Limits — Controls allowable range for divergence.

Bull/Bear Colors & Styling — Customize divergence visualization.

🔶 SUMMARY

The Z-Fusion Oscillator combines multiple momentum signatures into a single normalized signal, enabling traders to:

Identify reversals early

Detect momentum exhaustion

Spot bullish and bearish divergences

Track overbought/oversold conditions

Visualize trend strength with clarity

Whether you're a swing trader, intraday analyst, or trend-reversal hunter, the Z-Fusion Oscillator provides a powerful and adaptive way to read momentum.

Uptrick: Dynamic Z-Score DivergenceIntroduction

Uptrick: Dynamic Z-Score Divergence is an oscillator that combines multiple momentum sources within a Z-Score framework, allowing for the detection of statistically significant mean-reversion setups, directional shifts, and divergence signals. It integrates a multi-source normalized oscillator, a slope-based signal engine, structured divergence logic, a slope-adaptive EMA with dynamic bands, and a modular bar coloring system. This script is designed to help traders identify statistically stretched conditions, evolving trend dynamics, and classical divergence behavior using a unified statistical approach.

Overview

At its core, this script calculates the Z-Score of three momentum sources—RSI, Stochastic RSI, and MACD—using a user-defined lookback period. These are averaged and smoothed to form the main oscillator line. This normalized oscillator reflects how far short-term momentum deviates from its mean, highlighting statistically extreme areas.

Signals are triggered when the oscillator reverses slope within defined inner zones, indicating a shift in direction while the signal remains in a statistically stretched state. These mean-reversion flips (referred to as TP signals) help identify turning points when price momentum begins to revert from extended zones.

In addition, the script includes a divergence detection engine that compares oscillator pivot points with price pivot points. It confirms regular bullish and bearish divergence by validating spacing between pivots and visualizes both the oscillator-side and chart-side divergences clearly.

A dynamic trend overlay system is included using a Slope Adaptive EMA (SA-EMA). This trend line becomes more responsive when Z-Score deviation increases, allowing the trend line to adapt to market conditions. It is paired with ATR-based bands that are slope-sensitive and selectively visible—offering context for dynamic support and resistance.

The script includes configurable bar coloring logic, allowing users to color candles based on oscillator slope, last confirmed divergence, or the most recent signal of any type. A full alert system is also built-in for key signals.

Originality

The script is based on the well-known concept of Z-Score valuation, which is a standard statistical method for identifying how far a signal deviates from its mean. This foundation—normalizing momentum values such as RSI or MACD to measure relative strength or weakness—is not unique to this script and is widely used in quantitative analysis.

What makes this implementation original is how it expands the Z-Score foundation into a fully featured, signal-producing system. First, it introduces a multi-source composite oscillator by combining three momentum inputs—RSI, Stochastic RSI, and MACD—into a unified Z-Score stream. Second, it builds on that stream with a directional slope logic that identifies turning points inside statistical zones.

The most distinctive additions are the layered features placed on top of this normalized oscillator:

A structured divergence detection engine that compares oscillator pivots with price pivots to validate regular bullish and bearish divergence using precise spacing and timing filters.

A fully integrated slope-adaptive EMA overlay, where the smoothing dynamically adjusts based on real-time Z-Score movement of RSI, allowing the trend line to become more reactive during high-momentum environments and slower during consolidation.

ATR-based dynamic bands that adapt to slope direction and offer real-time visual zones for support and resistance within trend structures.

These features are not typically found in standard Z-Score indicators and collectively provide a unique approach that bridges statistical normalization, structure detection, and adaptive trend modeling within one script.

Features

Z-Score-based oscillator combining RSI, StochRSI, and MACD

Configurable smoothing for stable composite signal output

Buy/Sell TP signals based on slope flips in defined zones

Background highlighting for extreme outer bands

Inner and outer zones with fill logic for statistical context

Pivot-based divergence detection (regular bullish/bearish)

Divergence markers on oscillator and price chart

Slope-Adaptive EMA (SA-EMA) with real-time adaptivity based on RSI Z-Score

ATR-based upper and lower bands around the SA-EMA, visibility tied to slope direction

Configurable bar coloring (oscillator slope, divergence, or most recent signal)

Alerts for TP signals and confirmed divergences

Optional fixed Y-axis scaling for consistent oscillator view

The full setup mode can be seen below:

Input Parameters

General Settings

Full Setup: Enables rendering of the full visual system (lines, bands, signals)

Z-Score Lookback: Lookback period for normalization (mean and standard deviation)

Main Line Smoothing: EMA length applied to the averaged Z-Score

Slope Detection Index: Used to calculate directional flips for signal logic

Enable Background Highlighting: Enables visual region coloring in

overbought/oversold areas

Force Visible Y-Axis Scale: Forces max/min bounds for a consistent oscillator range

Divergence Settings

Enable Divergence Detection: Toggles divergence logic

Pivot Lookback Left / Right: Defines the structure of oscillator pivot points

Minimum / Maximum Bars Between Pivots: Controls the allowed spacing range for divergence validation

Bar Coloring Settings

Bar Coloring Mode:

➜ Line Color: Colors bars based on oscillator slope

➜ Latest Confirmed Signal: Colors bars based on the most recent confirmed divergence

➜ Any Latest Signal: Colors based on the most recent signal (TP or divergence)

SA-EMA Settings

RSI Length: RSI period used to determine adaptivity

Z-Score Length: Lookback for normalizing RSI in adaptive logic

Base EMA Length: Base length for smoothing before adaptivity

Adaptivity Intensity: Scales the smoothing responsiveness based on RSI deviation

Slope Index: Determines slope direction for coloring and band logic

Band ATR Length / Band Multiplier: Controls the width and responsiveness of the trend-following bands

Alerts

The script includes the following alert conditions:

Buy Signal (TP reversal detected in oversold zone)

Sell Signal (TP reversal detected in overbought zone)

Confirmed Bullish Divergence (oscillator HL, price LL)

Confirmed Bearish Divergence (oscillator LH, price HH)

These alerts allow integration into automation systems or signal monitoring setups.

Summary