Penunjuk dan strategi

4H Confirmation + 1H SFP BOS Retest4H Confirmation + 1H Entry (SFP + BOS + Retest)Run it on 1H

Uses 4H EMAs for higher-timeframe direction (confirmation)

Uses 1H SFP + BOS + retest + RSI for entries

This gives you more trades, still guided by the 4H trend

stormytrading orb botshows entries for 15m orb based on 5m break and retest made solely for mnq or nq, works good with smt

shows trades for ldn, nyc, nyc overlap and Asia session, pls follow stormy trading on insta for more

HMA+RVOL Strategy Hariss 369The Hull Moving Average (HMA) is a smooth, fast, and highly responsive moving average created by Alan Hull. It reduces lag significantly while still maintaining smoothness, making it one of the most popular tools for trend detection and entries. It is widely used for trend filter. Hull Moving Average(HMA) with RVOL strengthens the trend as volume is prime factor of price movement.

Trading with HMA: Simple method is buy when price closes above HMA , stop less below the low of last candle and target is 1.5 or 2 times of stop loss. The reverse is for sell. The HMA automatically turns to green on bull trend and red on bear trend for better visual confirmation.

Adding RVOL to HMA is better method of trading. Buy signal is initiated when price closes above HMA and RVOL is greater than 1.2. Sell signal is initiated when price closes below 89 HMA and rovl is greater than 1.2. One can change the value of RVOL according to trading style and type asset being traded.

It is a back tested strategy.

DEMA ATR Strategy [PrimeAutomation]⯁ OVERVIEW

The DEMA ATR Strategy combines trend-following logic with adaptive volatility filters to identify strong momentum phases and manage trades dynamically.

It uses a Double Exponential Moving Average (DEMA) anchored to ATR volatility bands, creating a self-adjusting trend baseline.

When the adjusted DEMA shifts direction, the strategy enters positions and scales out profit in phases based on ATR-driven targets.

This system adapts to volatility, filters noise, and seeks sustained directional moves.

⯁ KEY FEATURES

DEMA-Volatility Hybrid Filter

Uses Double EMA with ATR expansion/compression logic to form a dynamic trend baseline.

Directional Shift Entries

Entries occur when the adjusted DEMA flips trend (bullish crossover or bearish crossunder vs its past value).

Noise Reduction Mechanism

ATR range caps extreme moves and prevents false flips during choppy volatility spikes.

Multi-Level Take Profits

Targets scale out positions at 1×, 2×, and 3× ATR multiples in the trade direction.

Volatility-Adaptive Targets

ATR multiplier ensures profit targets expand/contract based on market conditions.

Single-Direction Exposure

No pyramiding; the strategy flips position only when trend shifts.

Automated Trade Finalization

When all profit targets trigger, the position is fully closed.

⯁ STRATEGY LOGIC

Trend Direction:

DEMA baseline is modified using ATR upper/lower envelopes.

• If the adjusted DEMA rises above previous value → Bullish

• If it falls below previous value → Bearish

Entry Rules:

• Enter Long when bullish shift occurs and no long position exists

• Enter Short when bearish shift occurs and no short position exists

Take Profit Logic:

3 partial exits for each trade based on ATR:

• TP1 = ±1× ATR

• TP2 = ±2× ATR

• TP3 = ±3× ATR

Profit distribution: 30% / 30% / 40%

Exit Conditions:

• Exit when all TPs hit (full scale-out if sum of all TPs 100%)

• Opposite trend signal closes current trade and opens new one

⯁ WHEN TO USE

Trending environments

Medium–high volatility phases

Swing trading and intraday trend plays

Markets that respect momentum continuation (crypto, indices, FX majors)

⯁ CONCLUSION

This strategy blends DEMA trend recognition with ATR-based volatility adaptation to generate cleaner directional entries and structured take-profit exits. It is designed to capture momentum phases while avoiding noise-driven false signals, delivering a disciplined and scalable trend-following approach.

BTC 30 m Long singal Asset: Bitcoin only

Timeframe: 30 minutes

Entry Conditions (Long):

MACD histogram turns from red to green (negative to positive)

Stochastic K line crosses above D line AND this crossover happens below the lower band (20)

RSI is above the middle band (50)

Crypto Grid 2025+ Long Only (Asym TP)Crypto Grid 2025+ Long Only (Asymmetric Take-Profit) is a long-only mean-reversion grid strategy designed for intraday cryptocurrency trading.

The core idea is to accumulate long positions as price moves downward within a locally defined price range and to exit positions on upward retracements.

The strategy automatically builds a multi-level grid between the highest and lowest price over a user-defined lookback period (“range length”). Each grid level acts as a potential entry point when price crosses it from above.

Key Features

1. Long-only grid logic

The strategy opens long positions only, progressively increasing exposure as price moves into lower grid levels.

2. Asymmetric take-profit mechanism

Instead of taking profit strictly at the next grid level, the strategy allows targeting multiple levels above the entry point. This increases the average profit per winning trade and shifts the reward-to-risk profile toward larger, less frequent wins.

3. Optional partial take-profit

A portion of each trade can be closed at the nearest grid level, while the remainder is held for a more distant asymmetric target. This balances consistency and profit potential.

4. Volume-based market filter

Entries can be restricted to periods of healthy market activity by requiring volume to exceed a moving-average baseline.

5. Capital-scaled position sizing

Position size is determined by risk percentage, grid spacing, and a dynamic sizing mode (original / conservative / aggressive).

6. Built-in risk controls

global stop below the lower boundary of the range,

global take-profit above the upper boundary,

automatic shutdown after a configurable loss-streak.

Market Philosophy

This strategy belongs to the mean-reversion family: it expects short-term overshoots to revert back toward mid-range liquidity zones.

It is not trend-following.

It performs best in choppy, range-bound, or slow-grinding markets — especially on liquid crypto pairs.

Recommended Use Cases

Short timeframes (1–15 minutes)

High-liquidity crypto pairs

Sideways or rotational price action

Exchanges with low fees (due to higher order count)

Not Intended For

Strong trending markets without pullbacks

Assets with thin order books

Use with leverage without additional risk controls

Summary

Crypto Grid 2025+ Long Only (Asymmetric TP) is a refined grid-based mean-reversion strategy optimized for modern crypto markets. Its asymmetric take-profit framework is specifically engineered to reduce the classical issue of “small wins and large occasional losses” found in traditional grid systems, giving it a more favorable long-term trade distribution.

CSS_LFU_v0.1Overview:

A multi-factor, market-adaptive swing strategy designed for intraday and short-term crypto trading. It synthesizes momentum, volatility, and trend signals into a unified composite score over a configurable lookback window. The strategy leverages a modular, signal-weighted approach to ensure robust entry timing while remaining compatible with human-in-the-loop validation and algorithmic execution.

Core Modules:

AJFFRSI (RSX-based Momentum): Measures smoothed price momentum with noise-reduction filters to detect crossovers relative to the QQE trailing stop.

QQE (Quantitative Qualitative Easing RSI): A modified RSI with a dynamic trailing stop that adapts to short-term volatility, identifying exhaustion and potential reversal points.

Keltner Channel Zones: Determines overextension relative to trend, providing buy/sell zones based on ATR-banded EMA.

WaveTrend Oscillator: Confirms short-term swings and market direction through smoothed oscillator cross signals.

Rolling Composite Score: Aggregates module signals over a unified lookback (e.g., 144 bars) to normalize noise and capture consistent trends.

Signal Logic:

Each module outputs a discrete score (+1 / 0 / -1).

The rolling composite score sums all module scores over the lookback period.

Long positions trigger when the rolling score meets or exceeds the long threshold.

Short positions trigger when the rolling score meets or falls below the short threshold.

Multi-dimensional signal aggregation reduces false positives from single indicators.

Rolling lookback ensures score normalization across different volatility regimes.

Highly modular: easy to adapt modules or weights to different instruments or timeframes.

Fully compatible with automated execution pipelines, including custom exchange screener bots.

Use Case:

Ideal for quant-driven altcoin or multi-asset strategies where high-frequency validation is critical and sequential module weighting enhances trend flip detection.

Inyerneck Sniper Engine v4.2 — FINAL WORKING 2025Aggressive momentum sniper for pennies. Fires on volume + EMA snaps. Use small size. Alerts ready.

Inyerneck Sniper Engine v4.2 — FINAL WORKING 2025yer momUltra-aggressive momentum sniper built for pennies & BTC.

Fires on every volume explosion + EMA snap. No mercy, no filters.

50+ trades per month. Use small size or die trying.

Private alpha —

Inyerneck Sniper Engine v4.2 — FINAL WORKING 2025Ultra-aggressive momentum sniper built for pennies & BTC.

Fires on every volume explosion + EMA snap. No mercy, no filters.

50+ trades per month. Use small size or die trying.

Private alpha — invite-only. do not change settings without first recording default settings, the default settings are great... usable on any time frame.. aaaaannd... yer mom!

EMA Trend Pro [Hedging & Fixed Risk]

This strategy is a comprehensive trend-following system designed to capture significant market movements while strictly managing risk. It combines multiple Exponential Moving Averages (EMAs) for trend identification, ADX for trend strength filtering, and Volume confirmation to reduce false signals.

Key Features:

Hedging Mode Compatible: The script is designed to handle Long and Short positions independently. This is ideal for markets where trends can reverse quickly or for traders who prefer hedging logic (requires hedging=true in strategy settings).

Professional Risk Management: Unlike standard strategies that use fixed contract sizes, this script calculates Position Size based on Risk. You can define a fixed risk per trade (e.g., 1% of equity or $100 fixed risk). The script automatically adjusts the lot size based on the Stop Loss distance (ATR).

Multi-Stage Take Profit: The strategy scales out positions at 3 different levels (TP1, TP2, TP3) to lock in profits while letting the remaining position ride the trend.

Strategy Logic:

Trend Identification:

Long Entry: EMA 7 > EMA 14 > EMA 21 > EMA 144 (Bullish Alignment).

Short Entry: EMA 7 < EMA 14 < EMA 21 < EMA 144 (Bearish Alignment).

Filters:

ADX Filter: Entries are only taken if ADX (14) > Threshold (default 20) to ensure the market is trending, avoiding chopping ranging markets.

Volume Filter: Current volume must exceed the 20-period SMA volume by 10% to confirm momentum.

Exits & Trade Management:

Stop Loss: Dynamic SL based on ATR (e.g., 1.8x ATR).

Breakeven: Once TP1 is hit, the Stop Loss is automatically moved to Breakeven to protect capital.

Take Profits:

TP1: 1x Risk Distance (30% pos)

TP2: 2x Risk Distance (50% pos)

TP3: 3x Risk Distance (Remaining pos)

Settings Guide:

Risk Type: Choose between "Percent" (of equity) or "Fixed Amount" (USD).

Risk Value: Input your desired risk (e.g., 1.0 for 1% risk).

Fee %: Set your exchange's Taker fee (e.g., 0.05 or 0.06) for accurate backtesting.

ADX Threshold: Adjust to filter out noise (Higher = Stricter trend requirement).

Disclaimer: This script is for educational and backtesting purposes only. Past performance does not guarantee future results. Please use proper risk management.

Volume weighted average price band strategy [Kevin-Patrick]VWAP Bands strategy, Credit

VWAP Machine Learning Bands is an advanced indicator designed to enhance trading analysis by integrating VWAP with a machine learning-inspired adaptive smoothing approach. This tool helps traders identify trend-based support and resistance zones, predict potential price movements, and generate dynamic trade signals.

Key Features

Adaptive ML VWAP Calculation: Uses a dynamically adjusted SMA-based VWAP model with volatility sensitivity for improved trend analysis.

Forecasting Mechanism: The 'Forecast' parameter shifts the ML output forward, providing predictive insights into potential price movements.

Volatility-Based Band Adjustments: The 'Sigma' parameter fine-tunes the impact of volatility on ML smoothing, adapting to market conditions.

Multi-Tier Standard Deviation Bands: Includes two levels of bands to define potential breakout or mean-reversion zones.

Dynamic Trend-Based Colouring: The VWAP and ML lines change colour based on their relative positions, visually indicating bullish and bearish conditions.

Custom Signal Detection Modes: Allows traders to choose between signals from Band 1, Band 2, or both, for more tailored trade setups.

+ Strategy setting by Kevin-Patrick

Stochastic Hash Strat [Hash Capital Research]# Stochastic Hash Strategy by Hash Capital Research

## 🎯 What Is This Strategy?

The **Stochastic Slow Strategy** is a momentum-based trading system that identifies oversold and overbought market conditions to capture mean-reversion opportunities. Think of it as a "buy low, sell high" approach with smart mathematical filters that remove emotion from your trading decisions.

Unlike fast-moving indicators that generate excessive noise, this strategy uses **smoothed stochastic oscillators** to identify only the highest-probability setups when momentum truly shifts.

---

## 💡 Why This Strategy Works

Most traders fail because they:

- **Chase prices** after big moves (buying high, selling low)

- **Overtrade** in choppy, directionless markets

- **Exit too early** or hold losses too long

This strategy solves all three problems:

1. **Entry Discipline**: Only trades when the stochastic oscillator crosses in extreme zones (oversold for longs, overbought for shorts)

2. **Cooldown Filter**: Prevents revenge trading by forcing a waiting period after each trade

3. **Fixed Risk/Reward**: Pre-defined stop-loss and take-profit levels ensure consistent risk management

**The Math Behind It**: The stochastic oscillator measures where the current price sits relative to its recent high-low range. When it's below 25, the market is oversold (time to buy). When above 70, it's overbought (time to sell). The crossover with its moving average confirms momentum is shifting.

---

## 📊 Best Markets & Timeframes

### ⭐ OPTIMAL PERFORMANCE:

**Crude Oil (WTI) - 12H Timeframe**

- **Why it works**: Oil markets have predictable volatility patterns and respect technical levels

**AAVE/USD - 4H to 12H Timeframe**

- **Why it works**: DeFi tokens exhibit strong momentum cycles with clear extremes

### ✅ Also Works Well On:

- **BTC/USD** (12H, Daily) - Lower frequency but high win rate

- **ETH/USD** (8H, 12H) - Balanced volatility and liquidity

- **Gold (XAU/USD)** (Daily) - Classic mean-reversion asset

- **EUR/USD** (4H, 8H) - Lower volatility, requires patience

### ❌ Avoid Using On:

- Timeframes below 4H (too much noise)

- Low-liquidity altcoins (wide spreads kill performance)

- Strongly trending markets without pullbacks (Bitcoin in 2021)

- News-driven instruments during major events

---

## 🎛️ Understanding The Settings

### Core Stochastic Parameters

**Stochastic Length (Default: 16)**

- Controls the lookback period for price comparison

- Lower = faster reactions, more signals (10-14 for volatile markets)

- Higher = smoother signals, fewer trades (16-21 for stable markets)

- **Pro tip**: Use 10 for crypto 4H, 16 for commodities 12H

**Overbought Level (Default: 70)**

- Threshold for short entries

- Lower values (65-70) = more trades, earlier entries

- Higher values (75-80) = fewer but higher-conviction trades

- **Sweet spot**: 70 works for most assets

**Oversold Level (Default: 25)**

- Threshold for long entries

- Higher values (25-30) = more trades, earlier entries

- Lower values (15-20) = fewer but stronger bounce setups

- **Sweet spot**: 20-25 depending on market conditions

**Smooth K & Smooth D (Default: 7 & 3)**

- Additional smoothing to filter out whipsaws

- K=7 makes the indicator slower and more reliable

- D=3 is the signal line that confirms the trend

- **Don't change these unless you know what you're doing**

---

### Risk Management

**Stop Loss % (Default: 2.2%)**

- Automatically exits losing trades

- Should be 1.5x to 2x your average market volatility

- Too tight = death by a thousand cuts

- Too wide = uncontrolled losses

- **Calibration**: Check ATR indicator and set SL slightly above it

**Take Profit % (Default: 7%)**

- Automatically exits winning trades

- Should be 2.5x to 3x your stop loss (reward-to-risk ratio)

- This default gives 7% / 2.2% = 3.18:1 R:R

- **The golden rule**: Never have R:R below 2:1

---

### Trade Filters

**Bar Cooldown Filter (Default: ON, 3 bars)**

- **What it does**: Forces you to wait X bars after closing a trade before entering a new one

- **Why it matters**: Prevents emotional revenge trading and overtrading in choppy markets

- **Settings guide**:

- 3 bars = Standard (good for most cases)

- 5-7 bars = Conservative (oil, slow-moving assets)

- 1-2 bars = Aggressive (only for experienced traders)

**Exit on Opposite Extreme (Default: ON)**

- Closes your long when stochastic hits overbought (and vice versa)

- Acts as an early profit-taking mechanism

- **Leave this ON** unless you're testing other exit strategies

**Divergence Filter (Default: OFF)**

- Looks for price/momentum divergences for additional confirmation

- **When to enable**: Trending markets where you want fewer but higher-quality trades

- **Keep OFF for**: Mean-reverting markets (oil, forex, most of the time)

---

## 🚀 Quick Start Guide

### Step 1: Set Up in TradingView

1. Open TradingView and navigate to your chart

2. Click "Pine Editor" at the bottom

3. Copy and paste the strategy code

4. Click "Add to Chart"

5. The strategy will appear in a separate pane below your price chart

### Step 2: Choose Your Market

**If you're trading Crude Oil:**

- Timeframe: 12H

- Keep all default settings

- Watch for signals during London/NY overlap (8am-11am EST)

**If you're trading AAVE or crypto:**

- Timeframe: 4H or 12H

- Consider these adjustments:

- Stochastic Length: 10-14 (faster)

- Oversold: 20 (more aggressive)

- Take Profit: 8-10% (higher targets)

### Step 3: Wait for Your First Signal

**LONG Entry** (Green circle appears):

- Stochastic crosses up below oversold level (25)

- Price likely near recent lows

- System places limit order at take profit and stop loss

**SHORT Entry** (Red circle appears):

- Stochastic crosses down above overbought level (70)

- Price likely near recent highs

- System places limit order at take profit and stop loss

**EXIT** (Orange circle):

- Position closes either at stop, target, or opposite extreme

- Cooldown period begins

### Step 4: Let It Run

The biggest mistake? **Interfering with the system.**

- Don't close trades early because you're scared

- Don't skip signals because you "have a feeling"

- Don't increase position size after a big win

- Don't revenge trade after a loss

**Follow the system or don't use it at all.**

---

### Important Risks:

1. **Drawdown Pain**: You WILL experience losing streaks of 5-7 trades. This is mathematically normal.

2. **Whipsaw Markets**: Choppy, range-bound conditions can trigger multiple small losses.

3. **Gap Risk**: Overnight gaps can cause your actual fill to be worse than the stop loss.

4. **Slippage**: Real execution prices differ from backtested prices (factor in 0.1-0.2% slippage).

---

## 🔧 Optimization Guide

### When to Adjust Settings:

**Market Volatility Increased?**

- Widen stop loss by 0.5-1%

- Increase take profit proportionally

- Consider increasing cooldown to 5-7 bars

**Getting Too Few Signals?**

- Decrease stochastic length to 10-12

- Increase oversold to 30, decrease overbought to 65

- Reduce cooldown to 2 bars

**Getting Too Many Losses?**

- Increase stochastic length to 18-21 (slower, smoother)

- Enable divergence filter

- Increase cooldown to 5+ bars

- Verify you're on the right timeframe

### A/B Testing Method:

1. **Run default settings for 50 trades** on your chosen market

2. Document: Win rate, profit factor, max drawdown, emotional tolerance

3. **Change ONE variable** (e.g., oversold from 25 to 20)

4. Run another 50 trades

5. Compare results

6. Keep the better version

**Never change multiple settings at once** or you won't know what worked.

---

## 📚 Educational Resources

### Key Concepts to Learn:

**Stochastic Oscillator**

- Developed by George Lane in the 1950s

- Measures momentum by comparing closing price to price range

- Formula: %K = (Close - Low) / (High - Low) × 100

- Similar to RSI but more sensitive to price movements

**Mean Reversion vs. Trend Following**

- This is a **mean reversion** strategy (price returns to average)

- Works best in ranging markets with defined support/resistance

- Fails in strong trending markets (2017 Bitcoin, 2020 Tech stocks)

- Complement with trend filters for better results

**Risk:Reward Ratio**

- The cornerstone of profitable trading

- Winning 40% of trades with 3:1 R:R = profitable

- Winning 60% of trades with 1:1 R:R = breakeven (after fees)

- **This strategy aims for 45% win rate with 2.5-3:1 R:R**

### Recommended Reading:

- *"Trading Systems and Methods"* by Perry Kaufman (Chapter on Oscillators)

- *"Mean Reversion Trading Systems"* by Howard Bandy

- *"The New Trading for a Living"* by Dr. Alexander Elder

---

## 🛠️ Troubleshooting

### "I'm not seeing any signals!"

**Check:**

- Is your timeframe 4H or higher?

- Is the stochastic actually reaching extreme levels (check if your asset is stuck in middle range)?

- Is cooldown still active from a previous trade?

- Are you on a low-liquidity pair?

**Solution**: Switch to a more volatile asset or lower the overbought/oversold thresholds.

---

### "The strategy keeps losing money!"

**Check:**

- What's your win rate? (Below 35% is concerning)

- What's your profit factor? (Below 0.8 means serious issues)

- Are you trading during major news events?

- Is the market in a strong trend?

**Solution**:

1. Verify you're using recommended markets/timeframes

2. Increase cooldown period to avoid choppy markets

3. Reduce position size to 5% while you diagnose

4. Consider switching to daily timeframe for less noise

---

### "My stop losses keep getting hit!"

**Check:**

- Is your stop loss tighter than the average ATR?

- Are you trading during high-volatility sessions?

- Is slippage eating into your buffer?

**Solution**:

1. Calculate the 14-period ATR

2. Set stop loss to 1.5x the ATR value

3. Avoid trading right after market open or major news

4. Factor in 0.2% slippage for crypto, 0.1% for oil

---

## 💪 Pro Tips from the Trenches

### Psychological Discipline

**The Three Deadly Sins:**

1. **Skipping signals** - "This one doesn't feel right"

2. **Early exits** - "I'll just take profit here to be safe"

3. **Revenge trading** - "I need to make back that loss NOW"

**The Solution:** Treat your strategy like a business system. Would McDonald's skip making fries because the cashier "doesn't feel like it today"? No. Systems work because of consistency.

---

### Position Management

**Scaling In/Out** (Advanced)

- Enter 50% position at signal

- Add 50% if stochastic reaches 10 (oversold) or 90 (overbought)

- Exit 50% at 1.5x take profit, let the rest run

**This is NOT for beginners.** Master the basic system first.

---

### Market Awareness

**Oil Traders:**

- OPEC meetings = volatility spikes (avoid or widen stops)

- US inventory reports (Wed 10:30am EST) = avoid trading 2 hours before/after

- Summer driving season = different patterns than winter

**Crypto Traders:**

- Monday-Tuesday = typically lower volatility (fewer signals)

- Thursday-Sunday = higher volatility (more signals)

- Avoid trading during exchange maintenance windows

---

## ⚖️ Legal Disclaimer

This trading strategy is provided for **educational purposes only**.

- Past performance does not guarantee future results

- Trading involves substantial risk of loss

- Only trade with capital you can afford to lose

- No one associated with this strategy is a licensed financial advisor

- You are solely responsible for your trading decisions

**By using this strategy, you acknowledge that you understand and accept these risks.**

---

## 🙏 Acknowledgments

Strategy development inspired by:

- George Lane's original Stochastic Oscillator work

- Modern quantitative trading research

- Community feedback from hundreds of backtests

Built with ❤️ for retail traders who want systematic, disciplined approaches to the markets.

---

**Good luck, stay disciplined, and trade the system, not your emotions.**

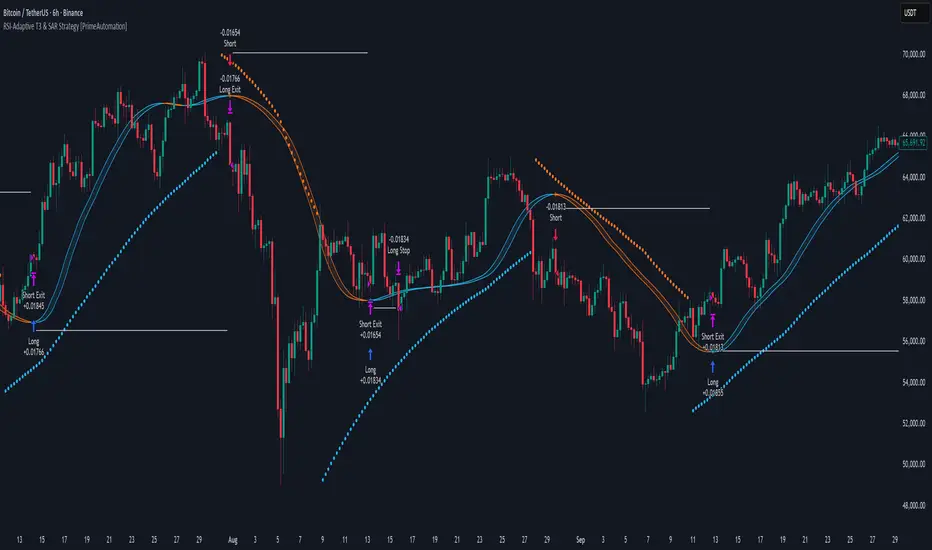

RSI-Adaptive T3 & SAR Strategy [PrimeAutomation]⯁ OVERVIEW

The RSI-Adaptive T3 and SAR Confluence Strategy combines adaptive smoothing with dynamic trend confirmation to identify precise trend reversals and continuation opportunities. It fuses the power of an RSI-based adaptive T3 moving average with the Parabolic SAR filter , aiming to trade in harmony with dominant momentum shifts while maintaining tight control through automatic stop-loss placement.

The RSI-Adaptive T3 is a precision trend-following tool built around the legendary T3 smoothing algorithm developed by Tim Tillson, designed to enhance responsiveness while reducing lag compared to traditional moving averages. Current implementation takes it a step further by dynamically adapting the smoothing length based on real-time RSI conditions — allowing the T3 to “breathe” with market volatility. This dynamic length makes the curve faster in trending moves and smoother during consolidations.

To help traders visualize volatility and directional momentum, adaptive volatility bands are plotted around the T3 line, with visual crossover markers and a dynamic info panel on the chart. It’s ideal for identifying trend shifts, spotting momentum surges, and adapting strategy execution to the pace of the market.

⯁ LOGIC

The T3 moving average length dynamically adjusts based on RSI values — when RSI is high, the smoothing period shortens to react faster; when RSI is low, the period increases for stability in slow markets.

A Parabolic SAR filter confirms directional bias, ensuring trades only occur in alignment with the broader market trend.

Long Entries: Trigger when the T3 curve crosses upward while the current price remains above the SAR — signaling bullish momentum alignment.

Short Entries: Trigger when the T3 crosses downward while the price remains below the SAR — confirming bearish trend alignment.

Stops: Dynamic stops are placed using the highest or lowest price over a set lookback period, adapting automatically to market volatility.

⯁ FEATURES

RSI-Adaptive T3 Filter: Adjusts smoothing in real time to market conditions, blending responsiveness with noise reduction.

SAR Confluence Check: Prevents counter-trend entries by confirming momentum direction via the Parabolic SAR.

Automatic Stop Placement: Uses recent highs or lows as stop-loss anchors, minimizing risk exposure.

Color-coded Visualization: The T3 line dynamically changes color based on slope direction, making momentum shifts visually intuitive.

Smoothed Trend Structure: Reduces market noise, allowing cleaner, more reliable trend recognition across different assets.

⯁ CONCLUSION

The RSI-Adaptive T3 and SAR Confluence Strategy delivers an advanced fusion of adaptive smoothing and structural confirmation. By combining RSI-driven reactivity with Parabolic SAR trend validation, this strategy offers a balanced approach to identifying sustainable momentum reversals while maintaining strong risk management through automatic stop levels. Ideal for traders who seek precision entries aligned with adaptive trend dynamics.

Recursive WMA Angle StrategyDescription: This strategy utilizes a recursive Weighted Moving Average (WMA) calculation to determine the trend direction and strength based on the slope (angle) of the curve. By calculating the angle of the smoothed moving average in degrees, the script filters out noise and aims to enter trades only during strong momentum phases.

How it Works:

Recursive WMA: The script calculates a series of nested WMAs (M1 to M5), creating a very smooth yet responsive curve.

Angle Calculation: It measures the rate of change of this curve over a user-defined lookback period and converts it into an angle (in degrees).

Entry Condition (Long): A long position is opened when the calculated angle exceeds the Min Angle for BUY threshold (default: 0.2), indicating a strong upward trend.

Exit Condition: The position is closed when the angle drops below the Min Angle for SELL threshold (default: -0.2), indicating a sharp trend reversal.

Settings:

MA Settings: Adjust the base lengths for the recursive calculation.

Angle Settings: Fine-tune the sensitivity by changing the Buy/Sell angle thresholds.

Date Filter: Restrict the backtest to a specific date range.

Note: This strategy is designed for Long-Only setups.

Super ORB v4 – 4 CONTRACTS – NUCLEAR FIXORB hands off printer, this is to gauge how few trades can happen off the ORB while not trading after hours either. Should be in the 5% a month range 4 contracts, no more than 5 trades a month.

Optimized EMA Ribbon Strategy v6 Based on EMA rotations, ADX we create a system of entering trades. Watch out for the sell and buy signals.

Hash Supertrend [Hash Capital Research]Hash Supertrend Strategy by Hash Capital Research

Overview

Hash Supertrend is a professional-grade trend-following strategy that combines the proven Supertrend indicator with institutional visual design and flexible time filtering.

The strategy uses ATR-based volatility bands to identify trend direction and executes position reversals when the trend flips.This implementation features a distinctive fluorescent color system with customizable glow effects, making trend changes immediately visible while maintaining the clean, professional aesthetic expected in quantitative trading environments.

Entry Signals:

Long Entry: Price crosses above the Supertrend line (trend flips bullish)

Short Entry: Price crosses below the Supertrend line (trend flips bearish)

Controls the lookback period for volatility calculation

Lower values (7-10): More sensitive to price changes, generates more signals

Higher values (12-14): Smoother response, fewer signals but potentially delayed entries

Recommended range: 7-14 depending on market volatility

Factor (Default: 3.0)

Restricts trading to specific hours

Useful for avoiding low-liquidity sessions, overnight gaps, or known choppy periods

When disabled, strategy trades 24/7

Start Hour (Default: 9) & Start Minute (Default: 30)

Define when the trading session begins

Uses exchange timezone in 24-hour format

Example: 9:30 = 9:30 AM

End Hour (Default: 16) & End Minute (Default: 0)

Controls the vibrancy of the fluorescent color system

1-3: Subtle, muted colors

4-6: Balanced, moderate saturation

7-10: Bright, highly saturated fluorescent appearance

Affects both the Supertrend line and trend zones

Glow Effect (Default: On)

Adds luminous halo around the Supertrend line

Creates a multi-layered visual with depth

Particularly effective during strong trends

Glow Intensity (Default: 5.0)

Displays tiny fluorescent dots at entry points

Green dot below bar: Long entry

Red dot above bar: Short entry

Provides clear visual confirmation of executed trades

Show Trend Zone (Default: On)

Strong trending markets (2020-style bull runs, sustained bear markets)

Markets with clear directional bias

Instruments with consistent volatility patterns

Timeframes: 15m to Daily (optimal on 1H-4H)

Challenging Conditions:

Choppy, range-bound markets

Low volatility consolidation periods

Highly news-driven instruments with frequent gaps

Very low timeframes (1m-5m) prone to noise

Recommended AssetsCryptocurrency:

Paulinho Signals – Cripto 5m/15m com Filtro de LateralidadeThis script is an automated Pine Script v6 strategy designed for short-term cryptocurrency trading, especially on 5-minute and 15-minute timeframes. It combines moving average crossovers, trend strength (ADX), volatility (ATR), and candlestick patterns to generate buy and sell signals with a fixed risk/reward management system.

How to Use:

- Apply to cryptocurrency charts on 5m or 15m timeframes.

- Adjust parameters to fit your preferences (EMA, RSI, ADX, ATR).

- Use for backtesting or as a decision-support tool.

Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Always test on demo accounts before applying to live trading.

Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!