VIPER DOPING - A Volume Profile to estimate trend probabilityDESCRIPTION :

VIPER DOPING uses volume analysis to help trader to understand trading keys below:

Support and Resistance

Profit and Loss

Estimate candle direction

Trend

Biggest Buy and Sell on level prices

HOW TO USE:

The volume bar will have buy and sell colors, by default the buy color is blue and the sell is red. The size of bar is important matter, the biggest bar size means that price level has strong volume or transaction and the smallest bar size indicates the lowest transaction or volume. How to read it?

The bar above the candle is the resistance

The bar below the candle is the support

If you want long the market, find the biggest or bigger support, which is below the candle

If you want short the market, find the biggest or bigger resistance which is above the candle

Trading style and the maximum range (total candle), default is 60. This setup to analyze volumes in specific candle range. Please check the following recommendation based on trading style:

Scalping: 30 - 60 candles, recommendation timeframe: 5m - 1h

Day Trading: 50 - 120 candles, recommendation timeframe: 30m - 4h

Swing Trading: 100- 240 candles, recommendation timeframe: 1h- 3D

The white box is to visualize trading area by total candle. Every line has the meaning:

The left line is the start candle

The right line is the end candle

The top line is the highest price of volume profile

The bottom line is the lowest price of volume profile

The fibonacci line will help you to confirm and compare of supports and resistances with the volume profile lines.

The TABLE CELLS

it contains information to help trader to understand the recent situation of market and to take strategy of trading:

Total Candle : the maximum candles are used to analyze the volume from previous active candle

Biggest Sell : the horizontal price area which has the largest of sell volume of the last total candle

Biggest Buy : the horizontal price area which has the largest of buy volume of the last total candle

Buy Rate : the ratio of buy and sell volume of the last total candle

Support: the closest price to be the support from the active candle, auto changed if support to be invalid

Resistance : the closest price to be the resistance from the active candle, auto changed if support to be invalid

PnL : the percentage profit if you trade using the support and resistance prices and it can be used for Risk Management. Wisely the risk is 50% of the profit, example if the profit 1% the your risk should be 0.5% from entry.

Estimate : to analize the next direction of candle or target, it will be changed automatically by volume condition.

CONFIGURATION:

Table Position : You can change the table position to top or bottom, to left, right or center

Calculation : You can include the active candle in volume calculation or you can choose the behind active candle. If you use active candle, there could be possible repainting.

The volume profile configuration is about appearance configuration, to setup the thickness, colors, position.

The fibonacci configuration is about appearance configuration, to setup the thickness, extend lines, label styles.

Probability

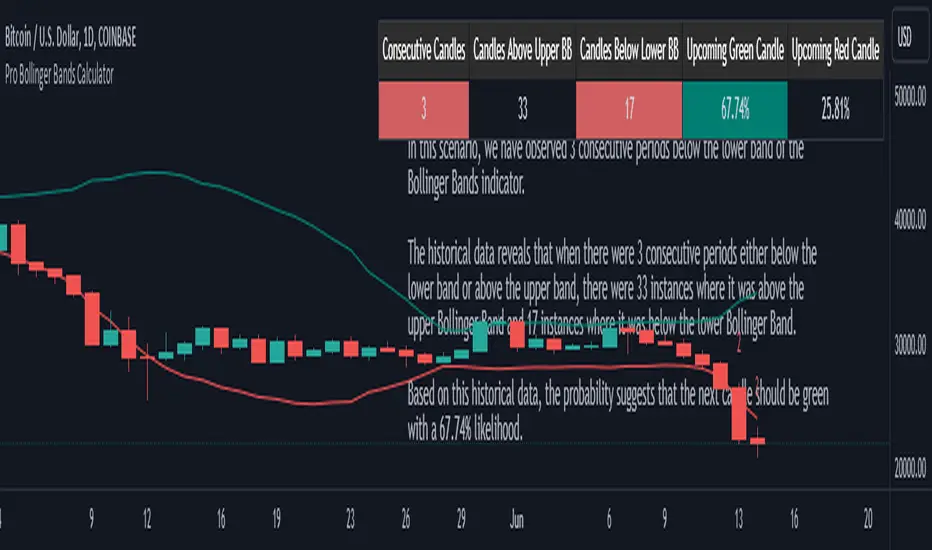

Pro Bollinger Bands CalculatorThe "Pro Bollinger Bands Calculator" indicator joins our suite of custom trading tools, which includes the "Pro Supertrend Calculator", the "Pro RSI Calculator" and the "Pro Momentum Calculator."

Expanding on this series, the "Pro Bollinger Bands Calculator" is tailored to offer traders deeper insights into market dynamics by harnessing the power of the Bollinger Bands indicator.

Its core mission remains unchanged: to scrutinize historical price data and provide informed predictions about future price movements, with a specific focus on detecting potential bullish (green) or bearish (red) candlestick patterns.

1. Bollinger Bands Calculation:

The indicator kicks off by computing the Bollinger Bands, a well-known volatility indicator. It calculates two pivotal Bollinger Bands parameters:

- Bollinger Bands Length: This parameter sets the lookback period for Bollinger Bands calculations.

- Bollinger Bands Deviation: It determines the deviation multiplier for the upper and lower bands, typically set at 2.0.

2. Visualizing Bollinger Bands:

The Bollinger Bands derived from the calculations are skillfully plotted on the price chart:

- Red Line: Represents the upper Bollinger Band during bearish trends, suggesting potential price declines.

- Teal Line: Represents the lower Bollinger Band in bullish market conditions, signaling the possibility of price increases.

3.Analyzing Consecutive Candlesticks:

The indicator's core functionality revolves around tracking consecutive candlestick patterns based on their relationship with the Bollinger Bands lines. To be considered for analysis, a candlestick must consistently close either above (green candles) or below (red candles) the Bollinger Bands lines for multiple consecutive periods.

4. Labeling and Enumeration:

To convey the count of consecutive candles displaying consistent trend behavior, the indicator meticulously assigns labels to the price chart. The position of these labels varies depending on the direction of the trend, appearing either below (for bullish patterns) or above (for bearish patterns) the candlesticks. The label colors match the candle colors: green labels for bullish candles and red labels for bearish ones.

5. Tabular Data Presentation:

The indicator complements its graphical analysis with a customizable table that prominently displays comprehensive statistical insights. Key data points within the table encompass:

- Consecutive Candles: The count of consecutive candles displaying consistent trend characteristics.

- Candles Above Upper BB: The number of candles closing above the upper Bollinger Band during the consecutive period.

- Candles Below Lower BB: The number of candles closing below the lower Bollinger Band during the consecutive period.

- Upcoming Green Candle: An estimated probability of the next candlestick being bullish, derived from historical data.

- Upcoming Red Candle: An estimated probability of the next candlestick being bearish, also based on historical data.

6. Custom Configuration:

To cater to diverse trading strategies and preferences, the indicator offers extensive customization options. Traders can fine-tune parameters such as Bollinger Bands length, upper and lower band deviations, label and table placement, and table size to align with their unique trading approaches.

SimilarityMeasuresLibrary "SimilarityMeasures"

Similarity measures are statistical methods used to quantify the distance between different data sets

or strings. There are various types of similarity measures, including those that compare:

- data points (SSD, Euclidean, Manhattan, Minkowski, Chebyshev, Correlation, Cosine, Camberra, MAE, MSE, Lorentzian, Intersection, Penrose Shape, Meehl),

- strings (Edit(Levenshtein), Lee, Hamming, Jaro),

- probability distributions (Mahalanobis, Fidelity, Bhattacharyya, Hellinger),

- sets (Kumar Hassebrook, Jaccard, Sorensen, Chi Square).

---

These measures are used in various fields such as data analysis, machine learning, and pattern recognition. They

help to compare and analyze similarities and differences between different data sets or strings, which

can be useful for making predictions, classifications, and decisions.

---

References:

en.wikipedia.org

cran.r-project.org

numerics.mathdotnet.com

github.com

github.com

github.com

Encyclopedia of Distances, doi.org

ssd(p, q)

Sum of squared difference for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of distance that calculates the squared euclidean distance.

euclidean(p, q)

Euclidean distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of distance that calculates the straight-line (or Euclidean).

manhattan(p, q)

Manhattan distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of absolute differences between both points.

minkowski(p, q, p_value)

Minkowsky Distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

p_value (float) : `float` P value, default=1.0(1: manhatan, 2: euclidean), does not support chebychev.

Returns: Measure of similarity in the normed vector space.

chebyshev(p, q)

Chebyshev distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of maximum absolute difference.

correlation(p, q)

Correlation distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of maximum absolute difference.

cosine(p, q)

Cosine distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Cosine distance between vectors `p` and `q`.

---

angiogenesis.dkfz.de

camberra(p, q)

Camberra distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Weighted measure of absolute differences between both points.

mae(p, q)

Mean absolute error is a normalized version of the sum of absolute difference (manhattan).

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Mean absolute error of vectors `p` and `q`.

mse(p, q)

Mean squared error is a normalized version of the sum of squared difference.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Mean squared error of vectors `p` and `q`.

lorentzian(p, q)

Lorentzian distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Lorentzian distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

intersection(p, q)

Intersection distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Intersection distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

penrose(p, q)

Penrose Shape distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Penrose shape distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

meehl(p, q)

Meehl distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Meehl distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

edit(x, y)

Edit (aka Levenshtein) distance for indexed strings.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

Returns: Number of deletions, insertions, or substitutions required to transform source string into target string.

---

generated description:

The Edit distance is a measure of similarity used to compare two strings. It is defined as the minimum number of

operations (insertions, deletions, or substitutions) required to transform one string into another. The operations

are performed on the characters of the strings, and the cost of each operation depends on the specific algorithm

used.

The Edit distance is widely used in various applications such as spell checking, text similarity, and machine

translation. It can also be used for other purposes like finding the closest match between two strings or

identifying the common prefixes or suffixes between them.

---

github.com

www.red-gate.com

planetcalc.com

lee(x, y, dsize)

Distance between two indexed strings of equal length.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

dsize (int) : `int` Dictionary size.

Returns: Distance between two strings by accounting for dictionary size.

---

www.johndcook.com

hamming(x, y)

Distance between two indexed strings of equal length.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

Returns: Length of different components on both sequences.

---

en.wikipedia.org

jaro(x, y)

Distance between two indexed strings.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

Returns: Measure of two strings' similarity: the higher the value, the more similar the strings are.

The score is normalized such that `0` equates to no similarities and `1` is an exact match.

---

rosettacode.org

mahalanobis(p, q, VI)

Mahalanobis distance between two vectors with population inverse covariance matrix.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

VI (matrix) : `matrix` Inverse of the covariance matrix.

Returns: The mahalanobis distance between vectors `p` and `q`.

---

people.revoledu.com

stat.ethz.ch

docs.scipy.org

fidelity(p, q)

Fidelity distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Bhattacharyya Coefficient between vectors `p` and `q`.

---

en.wikipedia.org

bhattacharyya(p, q)

Bhattacharyya distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Bhattacharyya distance between vectors `p` and `q`.

---

en.wikipedia.org

hellinger(p, q)

Hellinger distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The hellinger distance between vectors `p` and `q`.

---

en.wikipedia.org

jamesmccaffrey.wordpress.com

kumar_hassebrook(p, q)

Kumar Hassebrook distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Kumar Hassebrook distance between vectors `p` and `q`.

---

github.com

jaccard(p, q)

Jaccard distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Jaccard distance between vectors `p` and `q`.

---

github.com

sorensen(p, q)

Sorensen distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Sorensen distance between vectors `p` and `q`.

---

people.revoledu.com

chi_square(p, q, eps)

Chi Square distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

eps (float)

Returns: The Chi Square distance between vectors `p` and `q`.

---

uw.pressbooks.pub

stats.stackexchange.com

www.itl.nist.gov

kulczynsky(p, q, eps)

Kulczynsky distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

eps (float)

Returns: The Kulczynsky distance between vectors `p` and `q`.

---

github.com

FunctionMatrixCovarianceLibrary "FunctionMatrixCovariance"

In probability theory and statistics, a covariance matrix (also known as auto-covariance matrix, dispersion matrix, variance matrix, or variance–covariance matrix) is a square matrix giving the covariance between each pair of elements of a given random vector.

Intuitively, the covariance matrix generalizes the notion of variance to multiple dimensions. As an example, the variation in a collection of random points in two-dimensional space cannot be characterized fully by a single number, nor would the variances in the `x` and `y` directions contain all of the necessary information; a `2 × 2` matrix would be necessary to fully characterize the two-dimensional variation.

Any covariance matrix is symmetric and positive semi-definite and its main diagonal contains variances (i.e., the covariance of each element with itself).

The covariance matrix of a random vector `X` is typically denoted by `Kxx`, `Σ` or `S`.

~wikipedia.

method cov(M, bias)

Estimate Covariance matrix with provided data.

Namespace types: matrix

Parameters:

M (matrix) : `matrix` Matrix with vectors in column order.

bias (bool)

Returns: Covariance matrix of provided vectors.

---

en.wikipedia.org

numpy.org

Candles In Row (Expo)█ Overview

The Candles In Row (Expo) indicator is a powerful tool designed to track and visualize sequences of consecutive candlesticks in a price chart. Whether you're looking to gauge momentum or determine the prevailing trend, this indicator offers versatile functionality tailored to the needs of active traders. The Candles In Row indicator can be an integral part of a multi-timeframe trading strategy, allowing traders to understand market momentum, and set trading bias. By recognizing the patterns and likelihood of future price movements, traders can make more informed decisions and align their trades with the overall market direction.

█ How to use

The indicator enhances traders' understanding of the consecutive candle patterns, helping them to uncover trends and momentum. Consecutive candles in the same direction may indicate a strong trend. The Candles In Row indicator can be an essential tool for traders employing a multiple timeframes strategy.

Analyzing a Higher Timeframe:

Understanding Momentum: By analyzing consecutive green or red candles in a higher timeframe, traders can identify the prevailing momentum in the market. A series of green candles would suggest an upward trend, while a series of red candles would indicate a downward trend.

Predicting Next Candle: The indicator's predictive feature calculates the likelihood of the next candle being green or red based on historical patterns. This probability helps traders gauge the potential continuation of the trend.

Setting the Trading Bias: If the likelihood of the next candle being green is high, the trader may decide to focus on long (buy) opportunities. Conversely, if the likelihood of the next candle being red is high, the trader may look for short (sell) opportunities.

In this example, we are using the Heikin Ashi candles.

Moving to a Lower Timeframe:

Finding Entry Points: Once the trading bias is set based on the higher timeframe analysis, traders can switch to a lower timeframe to look for entry points in the direction of the bias. For example, if the higher timeframe suggests a high likelihood of a green candle, traders may look for buy opportunities in the lower timeframe.

Combining Timeframes for a Comprehensive Strategy:

Confirmation and Alignment: By analyzing the higher timeframe and confirming the direction in the lower timeframe, traders can ensure that they are trading in alignment with the broader trend.

Avoiding False Signals: By using a higher timeframe to set the trading bias and a lower timeframe to find entries, traders can avoid false signals and whipsaws that might be present in a single timeframe analysis.

█ Settings

Price Input Selection: Choose between regular open and close prices or Heikin Ashi candles as the basis for calculation.

Data Window Control: Decide between displaying the full data window or only the active data. You can also enable a counter that keeps track of the number of candles.

Alert Configuration: Set the desired number and color of consecutive candles that must occur in a row to trigger an alert.

Table Display Customization: Customize the location and size of the display table according to your preferences.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Normal Distribution CurveThis Normal Distribution Curve is designed to overlay a simple normal distribution curve on top of any TradingView indicator. This curve represents a probability distribution for a given dataset and can be used to gain insights into the likelihood of various data levels occurring within a specified range, providing traders and investors with a clear visualization of the distribution of values within a specific dataset. With the only inputs being the variable source and plot colour, I think this is by far the simplest and most intuitive iteration of any statistical analysis based indicator I've seen here!

Traders can quickly assess how data clusters around the mean in a bell curve and easily see the percentile frequency of the data; or perhaps with both and upper and lower peaks identify likely periods of upcoming volatility or mean reversion. Facilitating the identification of outliers was my main purpose when creating this tool, I believed fixed values for upper/lower bounds within most indicators are too static and do not dynamically fit the vastly different movements of all assets and timeframes - and being able to easily understand the spread of information simplifies the process of identifying key regions to take action.

The curve's tails, representing the extreme percentiles, can help identify outliers and potential areas of price reversal or trend acceleration. For example using the RSI which typically has static levels of 70 and 30, which will be breached considerably more on a less liquid or more volatile asset and therefore reduce the actionable effectiveness of the indicator, likewise for an asset with little to no directional volatility failing to ever reach this overbought/oversold areas. It makes considerably more sense to look for the top/bottom 5% or 10% levels of outlying data which are automatically calculated with this indicator, and may be a noticeable distance from the 70 and 30 values, as regions to be observing for your investing.

This normal distribution curve employs percentile linear interpolation to calculate the distribution. This interpolation technique considers the nearest data points and calculates the price values between them. This process ensures a smooth curve that accurately represents the probability distribution, even for percentiles not directly present in the original dataset; and applicable to any asset regardless of timeframe. The lookback period is set to a value of 5000 which should ensure ample data is taken into calculation and consideration without surpassing any TradingView constraints and limitations, for datasets smaller than this the indicator will adjust the length to just include all data. The labels providing the percentile and average levels can also be removed in the style tab if preferred.

Additionally, as an unplanned benefit is its applicability to the underlying price data as well as any derived indicators. Turning it into something comparable to a volume profile indicator but based on the time an assets price was within a specific range as opposed to the volume. This can therefore be used as a tool for identifying potential support and resistance zones, as well as areas that mark market inefficiencies as price rapidly accelerated through. This may then give a cleaner outlook as it eliminates the potential drawbacks of volume based profiles that maybe don't collate all exchange data or are misrepresented due to large unforeseen increases/decreases underlying capital inflows/outflows.

Thanks to @ALifeToMake, @Bjorgum, vgladkov on stackoverflow (and possibly some chatGPT!) for all the assistance in bringing this indicator to life. I really hope every user can find some use from this and help bring a unique and data driven perspective to their decision making. And make sure to please share any original implementaions of this tool too! If you've managed to apply this to the average price change once you've entered your position to better manage your trade management, or maybe overlaying on an implied volatility indicator to identify potential options arbitrage opportunities; let me know! And of course if anyone has any issues, questions, queries or requests please feel free to reach out! Thanks and enjoy.

Probability Box Rule of Thirds [PPI]█ Probability Box Rule of Thirds

The Probability Box Rule of Thirds , is a visual indicator that helps traders identify possible overbought and oversold conditions. It does this by dividing the price range – highest high minus the lowest low of a given lookback period or date range – into thirds. Each third has distinct probability characteristics and when combined represent a probability box.

We have spent years refining the probability box concept, and have previously published a How To on Trading View – "How to Trade Probability Ranges – The Critical Rule of 1/3" which can be found here:

To quickly summarize the How To – when using the Rule of Thirds , you are using a combination of statistics, probabilities of success, and prior price action to determine when to enter a trade. The visual range division helps remove subjectivity and clearly shows when the trading odds are stacked in your favor. By identifying and taking higher probability trades, you have a higher chance of success as trading is all about probability and risk management.

Implementing the Rule of Thirds starts with finding an instrument that is consolidating and identifying the nearest important support and resistance levels based on your targeted trading timeframe or lookback period.

The range between the support and resistance levels is divided into thirds to form three zones within the consolidation range.

When going LONG , you want to BUY in the bottom third of the range. Once you buy, your objective is to hold during the middle third and sell when the price enters the top third.

When you buy in the lower third, there's a 66.6% probability of success. If you buy in the middle third, you only have a 50% / 50% chance of success. Going long in the top third of the range gives you a 33.3% chance of success as you are already close to the identified resistance level.

When going SHORT , the sequence and odds are reversed. You want to SELL in the top third of the range, hold the middle third and exit in the bottom third of the range. This gives you a 66.6% chance of success when entering in the top third, a 50% / 50% chance when entering in the middle third, and a 33.3% chance in the bottom third given you are already close to the identified support level.

When the price lies in the middle third, the even 50% / 50% odds provide no probability edge and a trader is better off waiting until the price reaches the upper or lower thirds of the price range.

The Rule of Thirds allows us to quickly visually evaluate trades based on probabilities, selectively enter trades that have the highest odds of success, and avoid likely losing trades. The Rule of Thirds gives you confidence to hold trades based on prior trading ranges and provides clear levels where the prices are likely to either reverse or start trending.

The Probability Box Rule of Thirds automatically implements the first two steps of the Rule of Thirds by using the highest high and lowest low of a given lookback period to identify the support and resistance levels, and automatically divides the range into thirds. The rest of the Rule of Thirds rules remain the same.

Just having the price within the bottom thirds or top thirds, however, does not mean the price will immediately reverse. The GE chart below is an example of a stock that remained 'stuck' in the upper thirds of the price range for an extended amount of time:

And the CVS chart below is an example where the price is 'stuck' in the lower thirds of the price range:

While the price is in the upper or lower thirds, it is very important that the trader should use other indicators to identify when a significant trend reversal occurs. Once a trend reversal event happens, the trader either enters a trade AND/OR exits a trade if already in one.

When the price exceeds the bounds of the probability box, there are three possible outcomes – a strong continuation trend, the price consolidates around the probability box edge, or a trend reversal. Your favorite indicators will help determine which event is happening.

The CVS chart above is a good example of the probability box being exceeded with the last bar. The price exceeding the price range is temporary event as the price range will expand to encompass the revised price range on the next trading day.

█ Indicator Features

Each supported timeframe – Monthly, Weekly, and Daily – allows the selection of an appropriate lookback period for your trading style. The defaults are a good starting point for swing trading and long-term investing. You many need to experiment to find the optimal lookback period for your trading style.

Even if you only day trade, the Probability Box Rule of Thirds with the appropriate lookback periods can help you visualize the bigger picture of where the instrument is heading.

When viewing the charts, you can find the currently selected lookback period above the upper edge of the price range.

The indicator will display a dotted yellow line at 50% of the price range and show the line's value when requested.

The visibility of the actual thirds and border price values are controlled by the " Show Probability Box Values " checkbox. You may need to expand the chart's right margin to see the values.

The " Show Internal Labels " checkbox controls the display of the internal ⅓ Division labels and the percentage odds, along with the 50% label. This option by default is set to off.

The " Show Error Messages " checkbox controls the display of error messages and by default is turned on. Turn off to prevent error messages from being shown on intraday timeframes. Save as indicator default to prevent having to turn off this setting each time added to chart.

The color and transparency controls allow the user to modify the colors used for each third. The default settings are optimized for use with a DARK background.

█ Implementation Notes

IMPORTANT - the Probability Box Rule of Thirds is set up to only handle Monthly, Weekly and Daily charts. This is intentional as the indicator is designed to be used for safer multiple day and longer swing trades. When viewed on intraday charts, the indicator will be hidden.

The Probability Box Rule of Thirds uses a rolling window of the equivalent number of bars for the lookback period rather than relying on the bar starting and ending dates. This allows the use of a standard number of days in the selected lookback window across various instruments and ensures fast, efficient calculations.

The lookback periods are adjusted when non-standard timeframe multipliers are used – e.g., a 12M chart timeframe and a 3-year lookback period will result in a 3 bar lookback. Fractional bars in this calculation are rounded up and any incompatible lookback period and chart timeframe combination will generate a runtime error.

In summary, the Probability Box Rule of Thirds automates and visually identifies overbought and oversold areas, which combined with the Rule of Thirds probability risk profiles, increases your odds of success through better trade selections and higher confidence in your trades.

█ Disclaimer

There is substantial risk in trading. Losses incurred in trading can be significant. Only trade with money you can afford to lose. We make no claims whatsoever regarding the impact of past or future performance on your trading results.

Probability Trend IndicatorUnderstanding the Indicator:

The indicator calculates the probabilities of upward and downward trends based on the percentage change in price over a specified lookback period.

It displays these probabilities in a table and plots a histogram to represent the difference between the probabilities.

The colors of the histogram bars indicate the trend direction and whether the trend is increasing or decreasing.

Setting the Lookback Period:

The indicator allows you to specify the lookback period, which determines the number of bars to consider for calculating the probabilities.

By default, the lookback period is set to 50 bars. However, you can adjust it based on your trading preferences and the timeframe you're analyzing.

Analyzing the Probabilities:

The indicator calculates the probabilities of upward and downward trends and displays them in a table on the chart.

The probabilities are presented as percentages, representing the likelihood of each type of trend occurring.

You can use these probabilities to gain insights into the potential market direction and assess the strength of the prevailing trend.

Interpreting the Histogram:

The histogram is plotted based on the difference between the probabilities of upward and downward trends, known as the oscillator value.

The histogram bars are colored to provide visual cues about the trend direction and whether the trend is gaining or losing strength.

Green bars indicate upward trends, and red bars indicate downward trends.

Lighter shades of green or red suggest increasing trends, while darker shades suggest decreasing trends.

Making Trading Decisions:

The indicator serves as a tool for assessing the probabilities of trends and can be used alongside other technical analysis methods.

You can consider the probabilities, the histogram pattern, and the overall market context to make informed trading decisions.

It's important to remember that no indicator or tool can guarantee future market movements, so prudent risk management and additional analysis are essential.

BenfordsLawLibrary "BenfordsLaw"

Methods to deal with Benford's law which states that a distribution of first and higher order digits

of numerical strings has a characteristic pattern.

"Benford's law is an observation about the leading digits of the numbers found in real-world data sets.

Intuitively, one might expect that the leading digits of these numbers would be uniformly distributed so that

each of the digits from 1 to 9 is equally likely to appear. In fact, it is often the case that 1 occurs more

frequently than 2, 2 more frequently than 3, and so on. This observation is a simplified version of Benford's law.

More precisely, the law gives a prediction of the frequency of leading digits using base-10 logarithms that

predicts specific frequencies which decrease as the digits increase from 1 to 9." ~(2)

---

reference:

- 1: en.wikipedia.org

- 2: brilliant.org

- 4: github.com

cumsum_difference(a, b)

Calculate the cumulative sum difference of two arrays of same size.

Parameters:

a (float ) : `array` List of values.

b (float ) : `array` List of values.

Returns: List with CumSum Difference between arrays.

fractional_int(number)

Transform a floating number including its fractional part to integer form ex:. `1.2345 -> 12345`.

Parameters:

number (float) : `float` The number to transform.

Returns: Transformed number.

split_to_digits(number, reverse)

Transforms a integer number into a list of its digits.

Parameters:

number (int) : `int` Number to transform.

reverse (bool) : `bool` `default=true`, Reverse the order of the digits, if true, last will be first.

Returns: Transformed number digits list.

digit_in(number, digit)

Digit at index.

Parameters:

number (int) : `int` Number to parse.

digit (int) : `int` `default=0`, Index of digit.

Returns: Digit found at the index.

digits_from(data, dindex)

Process a list of `int` values and get the list of digits.

Parameters:

data (int ) : `array` List of numbers.

dindex (int) : `int` `default=0`, Index of digit.

Returns: List of digits at the index.

digit_counters(digits)

Score digits.

Parameters:

digits (int ) : `array` List of digits.

Returns: List of counters per digit (1-9).

digit_distribution(counters)

Calculates the frequency distribution based on counters provided.

Parameters:

counters (int ) : `array` List of counters, must have size(9).

Returns: Distribution of the frequency of the digits.

digit_p(digit)

Expected probability for digit according to Benford.

Parameters:

digit (int) : `int` Digit number reference in range `1 -> 9`.

Returns: Probability of digit according to Benford's law.

benfords_distribution()

Calculated Expected distribution per digit according to Benford's Law.

Returns: List with the expected distribution.

benfords_distribution_aprox()

Aproximate Expected distribution per digit according to Benford's Law.

Returns: List with the expected distribution.

test_benfords(digits, calculate_benfords)

Tests Benford's Law on provided list of digits.

Parameters:

digits (int ) : `array` List of digits.

calculate_benfords (bool)

Returns: Tuple with:

- Counters: Score of each digit.

- Sample distribution: Frequency for each digit.

- Expected distribution: Expected frequency according to Benford's.

- Cumulative Sum of difference:

to_table(digits, _text_color, _border_color, _frame_color)

Parameters:

digits (int )

_text_color (color)

_border_color (color)

_frame_color (color)

Trend Reversal Probability CalculatorThe "Trend Reversal Probability Calculator" is a TradingView indicator that calculates the probability of a trend reversal based on the crossover of multiple moving averages and the rate of change (ROC) of their slopes. This indicator is designed to help traders identify potential trend reversals by providing signals when the short-term moving averages start to slope in the opposite direction of the long-term moving average.

To use the indicator, simply add it to your TradingView chart and adjust the input parameters according to your preferences. The input parameters include the length of the moving averages, the ROC length (trend sensitivity), and the reversal sensitivity (signal percentage).

The indicator calculates the ROC of the moving averages and determines if the short-term moving averages are sloping in the opposite direction of the long-term moving average. The number of short-term moving averages that meet this condition is then counted, and the probability of a trend reversal is calculated based on the percentage of short-term moving averages that meet this condition.

When the probability of a trend reversal is high, a bullish or bearish signal is generated, depending on the direction of the reversal. The bullish signal is generated when the short-term moving averages start to slope upward, and the bearish signal is generated when the short-term moving averages start to slope downward.

Traders can use the "Trend Reversal Probability Calculator" to identify potential trend reversals and adjust their trading strategies accordingly. It is important to note that this indicator is not a guarantee of a trend reversal and should be used in conjunction with other technical analysis tools to make informed trading decisions.

Bayesian predictive leading indicator--------- ENGLISH ---------

This is a predictive indicator ( leading indicator ) that uses Bayes' formula to calculate the conditional probability of price increases given the angular coefficient. The indicator calculates the angular coefficient and its regression and uses it to predict prices.

Bayes' theorem is a fundamental result of probability theory and is used to calculate the probability of a cause causing the verified event. In other words, for our indicator, Bayes' theorem is used to calculate the conditional probability of one event (price event in this case) with respect to another event by calculating the probabilities of the two events (past price) and the conditional probability of the second event (future price) with respect to the first event.

The red line represents the angular coefficient. The blue line represents the normalized expected price. Finally, the yellow line represents the conditional probability that the price will increase or decrease.

How to use it. In addition to the convenient histogram, which follows the angular coefficient, another practical operational application might be to go long when the blue line is above the red and yellow lines. Conversely short when the blue is below the red and yellow.

When the yellow line passes above all others, a reversal in the long direction is imminent and vice versa.

The extent of the reversal depends on how far the yellow line will be away in price from the other 2 lines.

This indicator is in its embryonic state and updates will follow to make it more graphically readable, add alerts, etc.

Stay tuned! Leave a boost and comment or write to me if you wish.

--------- ITALIANO ---------

Questo è un indicatore predittivo ( leading indicator ) che utilizza la formula di Bayes per calcolare la probabilità condizionata che il prezzo aumenti dato il coefficiente angolare. L’indicatore calcola il coefficiente angolare e la sua regressione e lo utilizza per prevedere i prezzi.

Il teorema di Bayes è un risultato fondamentale della teoria della probabilità e viene impiegato per calcolare la probabilità di una causa che ha provocato l’evento verificato. In altre parole, per il nostro indicatore, il teorema di Bayes serve per calcolare la probabilità condizionata di un evento (di prezzo in questo caso) rispetto a un altro evento, calcolando le probabilità dei due eventi (prezzo passato) e la probabilità condizionata del secondo evento (prezzo futuro) rispetto al primo.

La linea rossa rappresenta il coefficiente angolare. La linea blu rappresenta il prezzo previsto normalizzato. Infine la linea gialla rappresenta la probabilità condizionata che il prezzo aumenti o diminuisca.

Come si usa? Oltre al comodo istogramma, che segue il coefficiente angolare, un'altra applicazione operativa pratica potrebbe essere di andare long quando la linea blu è sopra la linea rossa e gialla. Viceversa short quando la blu è sotto la rossa e la gialla.

Quando la linea gialla passa sopra tutte le altre è imminente un'inversione in direzione long e viceversa.

L'entità dell'inversione dipende da quanto la linea gialla sarà distante di prezzo dalle altre 2 linee.

Questo indicatore è al suo stato embrionale e seguiranno aggiornamenti per renderlo graficamente più leggibile, aggiungere alert, ecc.

Stay tuned! Lascia un boost e commenta o scrivimi se desideri.

MarkovChainLibrary "MarkovChain"

Generic Markov Chain type functions.

---

A Markov chain or Markov process is a stochastic model describing a sequence of possible events in which the

probability of each event depends only on the state attained in the previous event.

---

reference:

Understanding Markov Chains, Examples and Applications. Second Edition. Book by Nicolas Privault.

en.wikipedia.org

www.geeksforgeeks.org

towardsdatascience.com

github.com

stats.stackexchange.com

timeseriesreasoning.com

www.ris-ai.com

github.com

gist.github.com

github.com

gist.github.com

writings.stephenwolfram.com

kevingal.com

towardsdatascience.com

spedygiorgio.github.io

github.com

www.projectrhea.org

method to_string(this)

Translate a Markov Chain object to a string format.

Namespace types: MC

Parameters:

this (MC) : `MC` . Markov Chain object.

Returns: string

method to_table(this, position, text_color, text_size)

Namespace types: MC

Parameters:

this (MC)

position (string)

text_color (color)

text_size (string)

method create_transition_matrix(this)

Namespace types: MC

Parameters:

this (MC)

method generate_transition_matrix(this)

Namespace types: MC

Parameters:

this (MC)

new_chain(states, name)

Parameters:

states (state )

name (string)

from_data(data, name)

Parameters:

data (string )

name (string)

method probability_at_step(this, target_step)

Namespace types: MC

Parameters:

this (MC)

target_step (int)

method state_at_step(this, start_state, target_state, target_step)

Namespace types: MC

Parameters:

this (MC)

start_state (int)

target_state (int)

target_step (int)

method forward(this, obs)

Namespace types: HMC

Parameters:

this (HMC)

obs (int )

method backward(this, obs)

Namespace types: HMC

Parameters:

this (HMC)

obs (int )

method viterbi(this, observations)

Namespace types: HMC

Parameters:

this (HMC)

observations (int )

method baumwelch(this, observations)

Namespace types: HMC

Parameters:

this (HMC)

observations (int )

Node

Target node.

Fields:

index (series int) : . Key index of the node.

probability (series float) : . Probability rate of activation.

state

State reference.

Fields:

name (series string) : . Name of the state.

index (series int) : . Key index of the state.

target_nodes (Node ) : . List of index references and probabilities to target states.

MC

Markov Chain reference object.

Fields:

name (series string) : . Name of the chain.

states (state ) : . List of state nodes and its name, index, targets and transition probabilities.

size (series int) : . Number of unique states

transitions (matrix) : . Transition matrix

HMC

Hidden Markov Chain reference object.

Fields:

name (series string) : . Name of thehidden chain.

states_hidden (state ) : . List of state nodes and its name, index, targets and transition probabilities.

states_obs (state ) : . List of state nodes and its name, index, targets and transition probabilities.

transitions (matrix) : . Transition matrix

emissions (matrix) : . Emission matrix

initial_distribution (float )

FunctionProbabilityViterbiLibrary "FunctionProbabilityViterbi"

The Viterbi Algorithm calculates the most likely sequence of hidden states *(called Viterbi path)*

that results in a sequence of observed events.

viterbi(observations, transitions, emissions, initial_distribution)

Calculate most probable path in a Markov model.

Parameters:

observations (int ) : array . Observation states data.

transitions (matrix) : matrix . Transition probability table, (HxH, H:Hidden states).

emissions (matrix) : matrix . Emission probability table, (OxH, O:Observed states).

initial_distribution (float ) : array . Initial probability distribution for the hidden states.

Returns: array. Most probable path.

FunctionBaumWelchLibrary "FunctionBaumWelch"

Baum-Welch Algorithm, also known as Forward-Backward Algorithm, uses the well known EM algorithm

to find the maximum likelihood estimate of the parameters of a hidden Markov model given a set of observed

feature vectors.

---

### Function List:

> `forward (array pi, matrix a, matrix b, array obs)`

> `forward (array pi, matrix a, matrix b, array obs, bool scaling)`

> `backward (matrix a, matrix b, array obs)`

> `backward (matrix a, matrix b, array obs, array c)`

> `baumwelch (array observations, int nstates)`

> `baumwelch (array observations, array pi, matrix a, matrix b)`

---

### Reference:

> en.wikipedia.org

> github.com

> en.wikipedia.org

> www.rdocumentation.org

> www.rdocumentation.org

forward(pi, a, b, obs)

Computes forward probabilities for state `X` up to observation at time `k`, is defined as the

probability of observing sequence of observations `e_1 ... e_k` and that the state at time `k` is `X`.

Parameters:

pi (float ) : Initial probabilities.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing

states given a state matrix is size (M x M) where M is number of states.

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. Given

state matrix is size (M x O) where M is number of states and O is number of different

possible observations.

obs (int ) : List with actual state observation data.

Returns: - `matrix _alpha`: Forward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first

dimension refers to the state and the second dimension to time.

forward(pi, a, b, obs, scaling)

Computes forward probabilities for state `X` up to observation at time `k`, is defined as the

probability of observing sequence of observations `e_1 ... e_k` and that the state at time `k` is `X`.

Parameters:

pi (float ) : Initial probabilities.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing

states given a state matrix is size (M x M) where M is number of states.

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. Given

state matrix is size (M x O) where M is number of states and O is number of different

possible observations.

obs (int ) : List with actual state observation data.

scaling (bool) : Normalize `alpha` scale.

Returns: - #### Tuple with:

> - `matrix _alpha`: Forward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first

dimension refers to the state and the second dimension to time.

> - `array _c`: Array with normalization scale.

backward(a, b, obs)

Computes backward probabilities for state `X` and observation at time `k`, is defined as the probability of observing the sequence of observations `e_k+1, ... , e_n` under the condition that the state at time `k` is `X`.

Parameters:

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

obs (int ) : Array with actual state observation data.

Returns: - `matrix _beta`: Backward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first dimension refers to the state and the second dimension to time.

backward(a, b, obs, c)

Computes backward probabilities for state `X` and observation at time `k`, is defined as the probability of observing the sequence of observations `e_k+1, ... , e_n` under the condition that the state at time `k` is `X`.

Parameters:

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

obs (int ) : Array with actual state observation data.

c (float ) : Array with Normalization scaling coefficients.

Returns: - `matrix _beta`: Backward probabilities. The probabilities are given on a logarithmic scale (natural logarithm). The first dimension refers to the state and the second dimension to time.

baumwelch(observations, nstates)

**(Random Initialization)** Baum–Welch algorithm is a special case of the expectation–maximization algorithm used to find the

unknown parameters of a hidden Markov model (HMM). It makes use of the forward-backward algorithm

to compute the statistics for the expectation step.

Parameters:

observations (int ) : List of observed states.

nstates (int)

Returns: - #### Tuple with:

> - `array _pi`: Initial probability distribution.

> - `matrix _a`: Transition probability matrix.

> - `matrix _b`: Emission probability matrix.

---

requires: `import RicardoSantos/WIPTensor/2 as Tensor`

baumwelch(observations, pi, a, b)

Baum–Welch algorithm is a special case of the expectation–maximization algorithm used to find the

unknown parameters of a hidden Markov model (HMM). It makes use of the forward-backward algorithm

to compute the statistics for the expectation step.

Parameters:

observations (int ) : List of observed states.

pi (float ) : Initial probaility distribution.

a (matrix) : Transmissions, hidden transition matrix a or alpha = transition probability matrix of changing states

given a state matrix is size (M x M) where M is number of states

b (matrix) : Emissions, matrix of observation probabilities b or beta = observation probabilities. given state

matrix is size (M x O) where M is number of states and O is number of different possible observations

Returns: - #### Tuple with:

> - `array _pi`: Initial probability distribution.

> - `matrix _a`: Transition probability matrix.

> - `matrix _b`: Emission probability matrix.

---

requires: `import RicardoSantos/WIPTensor/2 as Tensor`

VS Score [SpiritualHealer117]An experimental indicator that uses historical prices and readings of technical indicators to give the probability that stock and crypto prices will be in a certain range on the next close. This indicator may be helpful for options traders or for traders who want to see the probability of a move.

It classifies returns into five categories:

Extreme Rise - Over 2 standard deviations above normal returns

Rise - Between 0.5 standard deviations and 2 standard deviations above normal returns

Flat - Falling in the range of +/- 0.5 standard deviations of normal returns

Fall - Between 0.5 standard deviations and 2 standard deviations below normal returns

Extreme Fall - Over 2 standard deviations below normal returns

It is an adaptive probability model, which trains on the previous 1000 data points, and is calculated by creating probability vectors for the current reading of the PPO, MA, volume histogram, and previous return, and combining them into one probability vector.

Quantitative Price Forecasting - The Quant ScienceThis script is a quantitative price forecasting indicator that forecasts price changes for a given asset.

The model aims to forecast future prices by analyzing past data within a selected time period. Mathematical probability is used to calculate whether starting from time X can lead to reaching prices Y1 and Y2. In this context, X represents the current selected time period, Y1 represents the selected percentage decrease, and Y2 represents the selected percentage increase. The probabilities are estimated using the simple average.

The simple average is displayed on the chart, showing in red the periods where the price is below the average and in green the periods where the price is above the average.

This powerful tool not only provides forecasts of future prices but also calculates the distribution of variations around the average. It then takes this information and creates an estimate of the average price variation around the simple average.

Using a mean-reverting logic, buying and selling opportunities are highlighted.

We recommend turning off the display of bars on your chart for a better experience when using this indicator.

Unlock the full potential of your trading strategy with our powerful indicator. By analyzing past price data, it provides accurate forecasts and calculates the probability of reaching specific price targets. Its mean-reverting logic highlights buying and selling opportunities, while the simple moving average displayed on the chart shows periods where the price is above or below the average. Additionally, it estimates the average variation of price around the simple average, giving you valuable insights into price movements. Don't miss out on this valuable tool that can take your trading to the next level

Triangulation : Statistically Approved ReversalsA lot of calculation, but a simple and effective result displayed on the chart.

It automatically identifies a very favorable period for a price reversal, by analyzing the daily and intraday price action statistics from the maximum of the most recent bars from the historical data. No repainting. Alerts can be set.

The statistical study is done in real time for each instrument. The probabilities therefore vary over time and adapt to the latest information collected by the indicator.

The time range of the data study can be changed by simply changing the UT :

- 30m = 3.5 last months feed statistics

- 15m = 52 last days feed statistics

- 5m = 17 last days feed statistics (recommanded)

HOW TO USE

This indicator informs when we are in a time period strongly favorable to reversal.

==> Crossing probabilities of different kinds, in price and in time => Triangulation of top and bottom !

HOW It WORK :

fractal statistics on high and low formation.

hour's probabilities of making the high/low of the day are crossed with day's probabilities of making the high/low of the week.

First for the day, we study:

- value of the probability compared to the average probabilities

- value of the coefficient between the high probability and the low probability

which we then refine for the hour, with the same calculation.

Result: bright color for a day + hour with high probability, weak color if the probability is low but remains the only possible bias. Between these two possibilities, intermediate colors are possible - just like looking for shorts if the day is bullish, if it is a high probability hour!

This color is displayed in the background, only if we are forming the high of the day for tops, and the low of the day for bottoms - detected with a stochastic.

All probabilities are studied in real time for the current asset.

We will call this signal "killstats", for "killzones statistics"

fractal statistics on the probability of closure under specific predefined levels according to 36 cycles.

the probabilities of several cycles are studied, for example:

NY session versus London and Asian sessions, London session compared to its opening, NY session compared to its opening, "algorithmic cycles" ( 1h30), Opening of NY compared to its intersection with London..

Each cycle producing a probability of closing with respect to the opening price of each period. The periods are : (Etc/UTC)

15-18h / 15-16h / 9-13h / 14-17h / 18-22h / 10-12h / 9-10h30 / 10h30-12h / 12-13h30 / 13h30-15h / 15h-16h30 / 16h30-18h

The cycles can be superimposed, which allows to support or attenuate a signal for the key periods of the day: 9am-12pm, and 3pm-6pm. The period of the day covered by the study of cycles is 9h-22h.

Result : ==> a straight line with a half bell. Colors = almost transparent for 53% probability (low), and very intense for a high probability (75%). The line displayed corresponds to the opening price, which we are supposed to close within the time limit - before the end of the period, where the line stops.

If the price goes in the opposite direction to the one predicted by the statistics, then a background connects the price to the close level to be respected.

if direction and close is respected, nothing is displayed : there is no opportunity, no divergence between statistics and actual price moves.

By unchecking the "light mode", you can see each close level displayed on the chart, with the corresponding probability and the number of times the cycle was detected. The color varies from intense for a high probability (75%), to light for a low probability (53%)

We will call this signal "cyclic anomalies"

By default, as shown in the indicator presentation image, the "intersection only" option is checked: only the intersection between 1) killstats and 2) cyclic anomalies is displayed. (filter +-30% of killstats signals)

MORE INFORMATIONS

/!\ : during a backtest, it is necessary to refresh the studied data to benefit from the real time signals, and for that you have to use the replay mode. if "Backtesting informations?"is checked, labels are displayed on the graph to warn of the % distortion of the signals. I recommend using the replay mode every 250 candles, and every 1000 candles for premium accounts, to have real signals.

- Alerts can be set for killzone, or intersections ( As in presentation picture)

- The ideal use is in m5. It can trigger several times a day, sometimes in opposite directions, and sometimes not trigger for several days.

- Premium account have 20k candles data, and not 5k => signals may vary depending on your tradingview subscription.

Chebyshevs BandsThis script calculates upper and lower bands using Chebyshev's inequality formula.

The main pros.: the band doesn't depend on particular distribution. It fits to any type of random variables. Also it allows to calculate bands for instruments with extremely high volatility.

Cons.: formula provides a rough estimation in some special cases like lognormal distribution.

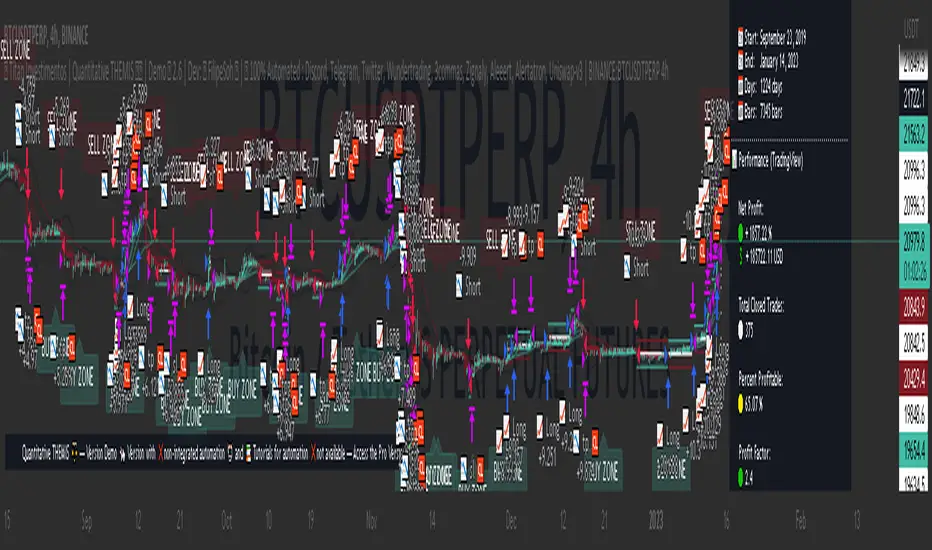

Titan Investments|Quantitative THEMIS|Pro|BINANCE:BTCUSDTP:4hInvestment Strategy (Quantitative Trading)

| 🛑 | Watch "LIVE" and 'COPY' this strategy in real time:

🔗 Link: www.tradingview.com

Hello, welcome, feel free 🌹💐

Since the stone age to the most technological age, one thing has not changed, that which continues impress human beings the most, is the other human being!

Deep down, it's all very simple or very complicated, depends on how you look at it.

I believe that everyone was born to do something very well in life.

But few are those who have, let's use the word 'luck' .

Few are those who have the 'luck' to discover this thing.

That is why few are happy and successful in their jobs and professions.

Thank God I had this 'luck' , and discovered what I was born to do well.

And I was born to program. 👨💻

📋 Summary : Project Titan

0️⃣ : 🦄 Project Titan

1️⃣ : ⚖️ Quantitative THEMIS

2️⃣ : 🏛️ Titan Community

3️⃣ : 👨💻 Who am I ❔

4️⃣ : ❓ What is Statistical/Probabilistic Trading ❓

5️⃣ : ❓ How Statistical/Probabilistic Trading works ❓

6️⃣ : ❓ Why use a Statistical/Probabilistic system ❓

7️⃣ : ❓ Why the human brain is not prepared to do Trading ❓

8️⃣ : ❓ What is Backtest ❓

9️⃣ : ❓ How to build a Consistent system ❓

🔟 : ❓ What is a Quantitative Trading system ❓

1️⃣1️⃣ : ❓ How to build a Quantitative Trading system ❓

1️⃣2️⃣ : ❓ How to Exploit Market Anomalies ❓

1️⃣3️⃣ : ❓ What Defines a Robust, Profitable and Consistent System ❓

1️⃣4️⃣ : 🔧 Fixed Technical

1️⃣5️⃣ : ❌ Fixed Outputs : 🎯 TP(%) & 🛑SL(%)

1️⃣6️⃣ : ⚠️ Risk Profile

1️⃣7️⃣ : ⭕ Moving Exits : (Indicators)

1️⃣8️⃣ : 💸 Initial Capital

1️⃣9️⃣ : ⚙️ Entry Options

2️⃣0️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Third-Party Services'

2️⃣1️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Exchanges

2️⃣2️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : 'Messaging Services'

2️⃣3️⃣ : ❓ How to Automate this Strategy ❓ : 🤖 Automation : '🧲🤖Copy-Trading'

2️⃣4️⃣ : ❔ Why be a Titan Pro 👽❔

2️⃣5️⃣ : ❔ Why be a Titan Aff 🛸❔

2️⃣6️⃣ : 📋 Summary : ⚖️ Strategy: Titan Investments|Quantitative THEMIS|Pro|BINANCE:BTCUSDTP:4h

2️⃣7️⃣ : 📊 PERFORMANCE : 🆑 Conservative

2️⃣8️⃣ : 📊 PERFORMANCE : Ⓜ️ Moderate

2️⃣9️⃣ : 📊 PERFORMANCE : 🅰 Aggressive

3️⃣0️⃣ : 🛠️ Roadmap

3️⃣1️⃣ : 🧻 Notes ❕

3️⃣2️⃣ : 🚨 Disclaimer ❕❗

3️⃣3️⃣ : ♻️ ® No Repaint

3️⃣4️⃣ : 🔒 Copyright ©️

3️⃣5️⃣ : 👏 Acknowledgments

3️⃣6️⃣ : 👮 House Rules : 📺 TradingView

3️⃣7️⃣ : 🏛️ Become a Titan Pro member 👽

3️⃣8️⃣ : 🏛️ Be a member Titan Aff 🛸

0️⃣ : 🦄 Project Titan

This is the first real, 100% automated Quantitative Strategy made available to the public and the pinescript community for TradingView.

You will be able to automate all signals of this strategy for your broker , centralized or decentralized and also for messaging services : Discord, Telegram or Twitter .

This is the first strategy of a larger project, in 2023, I will provide a total of 6 100% automated 'Quantitative' strategies to the pinescript community for TradingView.

The future strategies to be shared here will also be unique , never before seen, real 'Quantitative' bots with real, validated results in real operation.

Just like the 'Quantitative THEMIS' strategy, it will be something out of the loop throughout the pinescript/tradingview community, truly unique tools for building mutual wealth consistently and continuously for our community.

1️⃣ : ⚖️ Quantitative THEMIS : Titan Investments|Quantitative THEMIS|Pro|BINANCE:BTCUSDTP:4h

This is a truly unique and out of the curve strategy for BTC /USD .

A truly real strategy, with real, validated results and in real operation.

A unique tool for building mutual wealth, consistently and continuously for the members of the Titan community.

Initially we will operate on a monthly, quarterly, annual or biennial subscription service.

Our goal here is to build a great community, in exchange for an extremely fair value for the use of our truly unique tools, which bring and will bring real results to our community members.

With this business model it will be possible to provide all Titan users and community members with the purest and highest degree of sophistication in the market with pinescript for tradingview, providing unique and truly profitable strategies.

My goal here is to offer the best to our members!

The best 'pinescript' tradingview service in the world!

We are the only Start-Up in the world that will decentralize real and full access to truly real 'quantitative' tools that bring and will bring real results for mutual and ongoing wealth building for our community.

2️⃣ : 🏛️ Titan Community : 👽 Pro 🔁 Aff 🛸

Become a Titan Pro 👽

To get access to the strategy: "Quantitative THEMIS" , and future Titan strategies in a 100% automated way, along with all tutorials for automation.

Pro Plans: 30 Days, 90 Days, 12 Months, 24 Months.

👽 Pro 🅼 Monthly

👽 Pro 🆀 Quarterly

👽 Pro🅰 Annual

👽 Pro👾Two Years

You will have access to a truly unique system that is out of the curve .

A 100% real, 100% automated, tested, validated, profitable, and in real operation strategy.

Become a Titan Affiliate 🛸

By becoming a Titan Affiliate 🛸, you will automatically receive 50% of the value of each new subscription you refer .

You will receive 50% for any of the above plans that you refer .

This way we will encourage our community to grow in a fair and healthy way, because we know what we have in our hands and what we deliver real value to our users.

We are at the highest level of sophistication in the market, the consistency here and the results here speak for themselves.

So growing our community means growing mutual wealth and raising collective conscience.

Wealth must be created not divided.

And here we are creating mutual wealth on all ends and in all ways.

A non-zero sum system, where everybody wins.

3️⃣ : 👨💻 Who am I ❔

My name is FilipeSoh I am 26 years old, Technical Analyst, Trader, Computer Engineer, pinescript Specialist, with extensive experience in several languages and technologies.

For the last 4 years I have been focusing on developing, editing and creating pinescript indicators and strategies for Tradingview for people and myself.

Full-time passionate workaholic pinescript developer with over 10,000 hours of pinescript development.

• Pinescript expert ▬Tradingview.

• Specialist in Automated Trading

• Specialist in Quantitative Trading.

• Statistical/Probabilistic Trading Specialist - Mark Douglas Scholl.

• Inventor of the 'Classic Forecast' Indicators.

• Inventor of the 'Backtest Table'.

4️⃣ : ❓ What is Statistical/Probabilistic Trading ❓

Statistical/probabilistic trading is the only way to get a positive mathematical expectation regarding the market and consequently that is the only way to make money consistently from it.

I will present below some more details about the Quantitative THEMIS strategy, it is a real strategy, tested, validated and in real operation, 'Skin in the Game' , a consistent way to make money with statistical/probabilistic trading in a 100% automated.

I am a Technical Analyst , I used to be a Discretionary Trader , today I am 100% a Statistical Trader .

I've gotten rich and made a lot of money, and I've also lost a lot with 'leverage'.

That was a few years ago.

The book that changed everything for me was "Trading in The Zone" by Mark Douglas.

That's when I understood that the market is just a game of statistics and probability, like a casino!

It was then that I understood that the human brain is not prepared for trading, because it involves triggers and mental emotions.

And emotions in trading and in making trading decisions do not go well together, not in the long run, because you always have the burden of being wrong with the outcome of that particular position.

But remembering that the market is just a statistical game!

5️⃣ : ❓ How Statistical/Probabilistic Trading works ❓

Let's use a 'coin' as an example:

If we toss a 'coin' up 10 times.

Do you agree that it is impossible for us to know exactly the result of the 'plays' before they actually happen?

As in the example above, would you agree, that we cannot "guess" the outcome of a position before it actually happens?

As much as we cannot "guess" whether the coin will drop heads or tails on each flip.

We can analyze the "backtest" of the 10 moves made with that coin:

If we analyze the 10 moves and count the number of times the coin fell heads or tails in a specific sequence, we then have a percentage of times the coin fell heads or tails, so we have a 'backtest' of those moves.

Then on the next flip we can now assume a point or a favorable position for one side, the side with the highest probability .

In a nutshell, this is more or less how probabilistic statistical trading works.

As Statistical Traders we can never say whether such a Trader/Position we take will be a winner or a loser.

But still we can have a positive and consistent result in a "sequence" of trades, because before we even open a position, backtests have already been performed so we identify an anomaly and build a system that will have a positive statistical advantage in our favor over the market.

The advantage will not be in one trade itself, but in the "sequence" of trades as a whole!

Because our system will work like a casino, having a positive mathematical expectation relative to the players/market.

Design, develop, test models and systems that can take advantage of market anomalies, until they change.

Be the casino! - Mark Douglas

6️⃣ : ❓ Why use a Statistical/Probabilistic system ❓

In recent years I have focused and specialized in developing 100% automated trading systems, essentially for the cryptocurrency market.

I have developed many extremely robust and efficient systems, with positive mathematical expectation towards the market.

These are not complex systems per se , because here we want to avoid 'over-optimization' as much as possible.

As Da Vinci said: "Simplicity is the highest degree of sophistication".

I say this because I have tested, tried and developed hundreds of systems/strategies.

I believe I have programmed more than 10,000 unique indicators/strategies, because this is my passion and purpose in life.

I am passionate about what I do, completely!

I love statistical trading because it is the only way to get consistency in the long run!

This is why I have studied, applied, developed, and specialized in 100% automated cryptocurrency trading systems.

The reason why our systems are extremely "simple" is because, as I mentioned before, in statistical trading we want to exploit the market anomaly to the maximum, that is, this anomaly will change from time to time, usually we can exploit a trading system efficiently for about 6 to 12 months, or for a few years, that is; for fixed 'scalpers' systems.

Because at some point these anomalies will be identified , and from the moment they are identified they will be exploited and will stop being anomalies .

With the system presented here; you can even copy the indicators and input values shared here;

However; what I have to offer you is: it is me , our team , and our community !

That is, we will constantly monitor this system, for life , because our goal here is to create a unique , perpetual , profitable , and consistent system for our community.

Myself , our team and our community will keep this script periodically updated , to ensure the positive mathematical expectation of it.

So we don't mind sharing the current parameters and values , because the real value is also in the future updates that this system will receive from me and our team , guided by our culture and our community of real users !

As we are hosted on 'tradingview', all future updates for this strategy, will be implemented and updated automatically on your tradingview account.

What we want here is: to make sure you get gains from our system, because if you get gains , our ecosystem will grow as a whole in a healthy and scalable way, so we will be generating continuous mutual wealth and raising the collective consciousness .

People Need People: 3️⃣🅿

7️⃣ : ❓ Why the human brain is not prepared to do Trading ❓

Today my greatest skill is to develop statistically profitable and 100% automated strategies for 'pinescript' tradingview.

Note that I said: 'profitable' because in fact statistical trading is the only way to make money in a 'consistent' way from the market.

And consequently have a positive wealth curve every cycle, because we will be based on mathematics, not on feelings and news.

Because the human brain is not prepared to do trading.

Because trading is connected to the decision making of the cerebral cortex.

And the decision making is automatically linked to emotions, and emotions don't match with trading decision making, because in those moments, we can feel the best and also the worst sensations and emotions, and this certainly affects us and makes us commit grotesque mistakes!

That's why the human brain is not prepared to do trading.

If you want to participate in a fully automated, profitable and consistent trading system; be a Titan Pro 👽

I believe we are walking an extremely enriching path here, not only in terms of financial returns for our community, but also in terms of knowledge about probabilistic and automated statistical trading.

You will have access to an extremely robust system, which was built upon very strong concepts and foundations, and upon the world's main asset in a few years: Bitcoin .

We are the tip of the best that exists in the cryptocurrency market when it comes to probabilistic and automated statistical trading.

Result is result! Me being dressed or naked.

This is just the beginning!

But there is a way to consistently make money from the market.

Being the Casino! - Mark Douglas

8️⃣ : ❓ What is Backtest ❓

Imagine the market as a purely random system, but even in 'randomness' there are patterns.