Hash Ribbons Backtest - Bitcoin Beats YT

Hello Hello Hello and welcome back to Bitcoin Beats!

This is a script written by capriole_charles

Go check out the original!

I have added leverage and stoploss % but also made it a strategy so we can look back at past trades to see patterns and profit.

Personally I feel this is not enough data to trade off as BTC is such a young asset. However I have seen other models similar to this for other assets that hold strong.

Trade safe!

Good bye from bitcoin beats!

Not Meant For The 1H! My Bad! higher timeframes are better!

The "Spring" is the confirmed Miner capitulation period:

The 1st "gray" circle is the start of Capitulation (1 month Hash Rate crosses UNDER 2 month Hash Rate)

Last "green" circle is the end of Capitulation (1 month Hash Rate crosses OVER 2 month Hash Rate)

The "greener" the spring gets (up until blue) represents Hash Rate recovery (it is increasing)

The "blue" circle is the first instance of positive momentum following recovery of Hash Rate (1m HR > 2m HR). This is historically a rewarding place to buy with limited downside.

Cari dalam skrip untuk "bitcoin"

Strategy for The Bitcoin Buy/Sell IndicatorThis is the strategy for

Starting with a capital of $3,000 XBT , one might have $15,975 dollar worth of XBT plus whatever the bitcoin has appreciated over the years.

The Sharpe Ratio: 0.586, Net Profit is 532%, 57 closed trades from 2017 till today, Profit factor of 3.745 (aka for every dollar loss, there is 3.745 dollar profit) with 14% drawdown .

Let that sink in.

ATR and T3 strategyT3 Moving Average indicator was originally developed by Tim Tillson in 1998/99.

T3 Moving Average is considered as improved and better to traditional moving averages as it is smoother and performs better in trending market conditions.

It offers multiple opportunities when the price is in the state of retracement and therefore allows to minimize your exposed risk and allowing your profits run.

This strategy is for trend followers who are patient enough to have 6-10 trades per year.

What's included in strategy?

Two ATR (Code was taken from J.Dow and modified)

Tillson Moving average

Enter long signal:

When both ATR (Long and Short) are in uptrend and the bar closes above Upper Tillson's moving average band: Enter Long

Exit Long signal:

When hl2 is lower than Lower Tillson Moving Average band

Enter short signal:

When both ATR (Long and Short) are in downtrend and the bar closes below Lower Tillson's moving average band: Enter Short

Exit Shortsignal:

When hl2 is higher than Upper Tillson's Moving Average band

Best to use with Bitcoin on 12H TF

Can be used for different time frames as well but the settings must be adjusted accordingly

Remember, overtrading can be harmful to your trading account.

If this is helpful for you, consider a tip

BTC: 3FiBnveHo3YW6DSiPEmoCFCyCnsrWS3JBR

ETH: 0xac290B4A721f5ef75b0971F1102e01E1942A4578

Created by CryptoJoncis

Bitcoin 1H-15M Breakout StrategyKey Features

1H and 15M Timeframes:

The script uses the 1-hour timeframe for the range and 15-minute timeframe for breakout conditions.

request.security is used to fetch the higher timeframe data.

Risk Management:

Variables entry_price, sl_price, and tp_price are declared explicitly as float with na initialization to handle dynamic assignment.

Stop-loss and take-profit levels are calculated based on the specified Risk-Reward Ratio (RRR) and buffer (in pips).

Trade Logic:

Long trade triggered when the 15-minute candle closes above the 1-hour high.

Short trade triggered when the 15-minute candle closes below the 1-hour low.

Visualization:

The range_high and range_low (previous 1-hour high and low) are plotted on the chart using dashed lines.

Debugging:

Enabling the show_debug input displays labels showing stop-loss and take-profit values for easier troubleshooting.

ALT Risk Metric StrategyHere's a professional write-up for your ALT Risk Strategy script:

ALT/BTC Risk Strategy - Multi-Crypto DCA with Bitcoin Correlation Analysis

Overview

This strategy uses Bitcoin correlation as a risk indicator to time entries and exits for altcoins. By analyzing how your chosen altcoin performs relative to Bitcoin, the strategy identifies optimal accumulation periods (when alt/BTC is oversold) and profit-taking opportunities (when alt/BTC is overbought). Perfect for traders who want to outperform Bitcoin by strategically timing altcoin positions.

Key Innovation: Why Alt/BTC Matters

Most traders focus solely on USD price, but Alt/BTC ratios reveal true altcoin strength:

When Alt/BTC is low → Altcoin is undervalued relative to Bitcoin (buy opportunity)

When Alt/BTC is high → Altcoin has outperformed Bitcoin (take profits)

This approach captures the rotation between BTC and alts that drives crypto cycles

Key Features

📊 Advanced Technical Analysis

RSI (60% weight): Primary momentum indicator on weekly timeframe

Long-term MA Deviation (35% weight): Measures distance from 150-period baseline

MACD (5% weight): Minor confirmation signal

EMA Smoothing: Filters noise while maintaining responsiveness

All calculations performed on Alt/BTC pairs for superior market timing

💰 3-Tier DCA System

Level 1 (Risk ≤ 70): Conservative entry, base allocation

Level 2 (Risk ≤ 50): Increased allocation, strong opportunity

Level 3 (Risk ≤ 30): Maximum allocation, extreme undervaluation

Continuous buying: Executes every bar while below threshold for true DCA behavior

Cumulative sizing: L3 triggers = L1 + L2 + L3 amounts combined

📈 Smart Profit Management

Sequential selling: Must complete L1 before L2, L2 before L3

Percentage-based exits: Sell portions of position, not fixed amounts

Auto-reset on re-entry: New buy signals reset sell progression

Prevents premature full exits during volatile conditions

🤖 3Commas Automation

Pre-configured JSON webhooks for Custom Signal Bots

Multi-exchange support: Binance, Coinbase, Kraken, Bitfinex, Bybit

Flexible quote currency: USD, USDT, or BUSD

Dynamic order sizing: Automatically adjusts to your tier thresholds

Full webhook documentation compliance

🎨 Multi-Asset Support

Pre-configured for popular altcoins:

ETH (Ethereum)

SOL (Solana)

ADA (Cardano)

LINK (Chainlink)

UNI (Uniswap)

XRP (Ripple)

DOGE

RENDER

Custom option for any other crypto

How It Works

Risk Metric Calculation (0-100 scale):

Fetches weekly Alt/BTC price data for stability

Calculates RSI, MACD, and deviation from 150-period MA

Normalizes MACD to 0-100 range using 500-bar lookback

Combines weighted components: (MACD × 0.05) + (RSI × 0.60) + (Deviation × 0.35)

Applies 5-period EMA smoothing for cleaner signals

Color-Coded Risk Zones:

Green (0-30): Extreme buying opportunity - Alt heavily oversold vs BTC

Lime/Yellow (30-70): Accumulation range - favorable risk/reward

Orange (70-85): Caution zone - consider taking initial profits

Red/Maroon (85-100+): Euphoria zone - aggressive profit-taking

Entry Logic:

Buys execute every candle when risk is below threshold

As risk decreases, position sizing automatically scales up

Example: If risk drops from 60→25, you'll be buying at L1 rate until it hits 50, then L2 rate, then L3 rate

Exit Logic:

Sells only trigger when in profit AND risk exceeds thresholds

Sequential execution ensures partial profit-taking

If new buy signal occurs before all sells complete, sell levels reset to L1

Configuration Guide

Choosing Your Altcoin:

Select crypto from dropdown (or use CUSTOM for unlisted coins)

Pick your exchange

Choose quote currency (USD, USDT, BUSD)

Risk Metric Tuning:

Long Term MA (default 150): Higher = more extreme signals, Lower = more frequent

RSI Length (default 10): Lower = more volatile, Higher = smoother

Smoothing (default 5): Increase for less noise, decrease for faster reaction

Buy Settings (Aggressive DCA Example):

L1 Threshold: 70 | Amount: $5

L2 Threshold: 50 | Amount: $6

L3 Threshold: 30 | Amount: $7

Total L3 buy = $18 per candle when deeply oversold

Sell Settings (Balanced Exit Example):

L1: 70 threshold, 25% position

L2: 85 threshold, 35% position

L3: 100 threshold, 40% position (final exit)

3Commas Setup

Bot Configuration:

Create Custom Signal Bot in 3Commas

Set trading pair to your altcoin/USD (e.g., ETH/USD, SOL/USDT)

Order size: Select "Send in webhook, quote" to use strategy's dollar amounts

Copy Bot UUID and Secret Token

Script Configuration:

Paste credentials into 3Commas section inputs

Check "Enable 3Commas Alerts"

Save and apply to chart

TradingView Alert:

Create Alert → Condition: "alert() function calls only"

Webhook URL: api.3commas.io

Enable "Webhook URL" checkbox

Expiration: Open-ended

Strategy Advantages

✅ Outperform Bitcoin: Designed specifically to beat BTC by timing alt rotations

✅ Capture Alt Seasons: Automatically accumulates when alts lag, sells when they pump

✅ Risk-Adjusted Sizing: Buys more when cheaper (better risk/reward)

✅ Emotional Discipline: Systematic approach removes fear and FOMO

✅ Multi-Asset: Run same strategy across multiple altcoins simultaneously

✅ Proven Indicators: Combines RSI, MACD, and MA deviation - battle-tested tools

Backtesting Insights

Optimal Timeframes:

Daily chart: Best for backtesting and signal generation

Weekly data is fetched internally regardless of display timeframe

Historical Performance Characteristics:

Accumulates heavily during bear markets and BTC dominance periods

Captures explosive altcoin rallies when BTC stagnates

Sequential selling preserves capital during extended downtrends

Works best on established altcoins with multi-year history

Risk Considerations:

Requires capital reserves for extended accumulation periods

Some altcoins may never recover if fundamentals deteriorate

Past correlation patterns may not predict future performance

Always size positions according to personal risk tolerance

Visual Interface

Indicator Panel Displays:

Dynamic color line: Green→Lime→Yellow→Orange→Red as risk increases

Horizontal threshold lines: Dashed lines mark your buy/sell levels

Entry/Exit labels: Green labels for buys, Orange/Red/Maroon for sells

Real-time risk value: Numerical display on price scale

Customization:

All threshold lines are adjustable via inputs

Color scheme clearly differentiates buy zones (green spectrum) from sell zones (red spectrum)

Line weights emphasize most extreme thresholds (L3 buy and L3 sell)

Strategy Philosophy

This strategy is built on the principle that altcoins move in cycles relative to Bitcoin. During Bitcoin rallies, alts often bleed against BTC (high sell, accumulate). When Bitcoin consolidates, alts pump (take profits). By measuring risk on the Alt/BTC chart instead of USD price, we time these rotations with precision.

The 3-tier system ensures you're always averaging in at better prices and scaling out at better prices, maximizing your Bitcoin-denominated returns.

Advanced Tips

Multi-Bot Strategy:

Run this on 5-10 different altcoins simultaneously to:

Diversify correlation risk

Capture whichever alt is pumping

Smooth equity curve through rotation

Pairing with BTC Strategy:

Use alongside the BTC DCA Risk Strategy for complete portfolio coverage:

BTC strategy for core holdings

ALT strategies for alpha generation

Rebalance between them based on BTC dominance

Threshold Calibration:

Check 2-3 years of historical data for your chosen alt

Note where risk metric sat during major bottoms (set buy thresholds)

Note where it peaked during euphoria (set sell thresholds)

Adjust for your risk tolerance and holding period

Credits

Strategy Development & 3Commas Integration: Claude AI (Anthropic)

Technical Analysis Framework: RSI, MACD, Moving Average theory

Implementation: pommesUNDwurst

Disclaimer

This strategy is for educational purposes only. Cryptocurrency trading involves substantial risk of loss. Altcoins are especially volatile and many fail completely. The strategy assumes liquid markets and reliable Alt/BTC price data. Always do your own research, understand the fundamentals of any asset you trade, and never risk more than you can afford to lose. Past performance does not guarantee future results. The authors are not financial advisors and assume no liability for trading decisions.

Additional Warning: Using leverage or trading illiquid altcoins amplifies risk significantly. This strategy is designed for spot trading of established cryptocurrencies with deep liquidity.

Tags: Altcoin, Alt/BTC, DCA, Risk Metric, Dollar Cost Averaging, 3Commas, ETH, SOL, Crypto Rotation, Bitcoin Correlation, Automated Trading, Alt Season

Feel free to modify any sections to better match your style or add specific backtesting results you've observed! 🚀Claude is AI and can make mistakes. Please double-check responses. Sonnet 4.5

twisted SMA strategy [4h] Hello

I would like to introduce a very simple strategy that uses a combination of 3 simple moving averages ( SMA 4 , SMA 9 , SMA 18 )

this is a classic combination showing the most probable trend directions

Crosses were marked on the basis of the color of the candles (bulish cross - blue / bearish cross - maroon)

ma 100 was used to determine the main trend, which is one of the most popular 4-hour candles

We define main trend while price crosses SMA100 ( for bullish trend I use green candle color )

The long position strategy was created in combination of 3 moving averages with Kaufman's adaptive moving average by alexgrover

The strategy is very accurate and is easy to use indicators

the strategy uses only Buy (Long) signals in a combination of crossovers of the SMA 4, SMA 9, SMA 18 and the Kaufman Adaptive Moving Average.

As a signal to close a long position, only the opposite signal of the intersection of 3 different moving averages is used

the current strategy is recommended for higher time zones (4h +) due to the strength of the closing candles, which translates into signal strength

works fascinatingly well for long-term bullish market assets (for example 4h Apple, Tesla charts)

Enjoy and trade safe ;)

BTC Seasonality Strategy (Weekly)This strategy identifies potential weekend opportunities in Bitcoin (BTC) markets by leveraging the concept of seasonality, entering a position at a predefined time and day, and exiting at a specified time and day.

Key Features

Customizable Time and Day Selection:

Users can select the entry and exit days and corresponding times (in EST).

Directional Flexibility:

The strategy allows traders to choose between long or short positions.

TradingView Compliance:

The script adheres to TradingView's house rules, avoids overly complex conditions, and provides clear user-configurable inputs.

How It Works

The script determines the current weekday and hour in EST, converting TradingView's UTC time for accurate comparisons.

If the current day and hour match the selected entry conditions, a trade (long or short) is opened.

The position is closed when the current day and hour match the specified exit conditions.

Theoretical Basis

Market Seasonality:

The concept of seasonality in financial markets refers to predictable patterns based on time, such as weekends or specific days of the week. Studies have shown that cryptocurrency markets exhibit unique trading behaviors during weekends due to reduced institutional activity and higher retail participation behavioral Biases**:

Retail traders often dominate weekend markets, potentially causing predictable inefficiencies .

Reverences**

Baur, D. G., Hong, K., & Lee, A. D. (2018). Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money, 54, 177–189.

Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letters, 148, 80–82.

BTC Future Gamma-Weighted Momentum Model (BGMM)The BTC Future Gamma-Weighted Momentum Model (BGMM) is a quantitative trading strategy that utilizes the Gamma-weighted average price (GWAP) in conjunction with a momentum-based approach to predict price movements in the Bitcoin futures market. The model combines the concept of weighted price movements with trend identification, where the Gamma factor amplifies the weight assigned to recent prices. It leverages the idea that historical price trends and weighting mechanisms can be utilized to forecast future price behavior.

Theoretical Background:

1. Momentum in Financial Markets:

Momentum is a well-established concept in financial market theory, referring to the tendency of assets to continue moving in the same direction after initiating a trend. Any observed market return over a given time period is likely to continue in the same direction, a phenomenon known as the “momentum effect.” Deviations from a mean or trend provide potential trading opportunities, particularly in highly volatile assets like Bitcoin.

Numerous empirical studies have demonstrated that momentum strategies, based on price movements, especially those correlating long-term and short-term trends, can yield significant returns (Jegadeesh & Titman, 1993). Given Bitcoin’s volatile nature, it is an ideal candidate for momentum-based strategies.

2. Gamma-Weighted Price Strategies:

Gamma weighting is an advanced method of applying weights to price data, where past price movements are weighted by a Gamma factor. This weighting allows for the reinforcement or reduction of the influence of historical prices based on an exponential function. The Gamma factor (ranging from 0.5 to 1.5) controls how much emphasis is placed on recent data: a value closer to 1 applies an even weighting across periods, while a value closer to 0 diminishes the influence of past prices.

Gamma-based models are used in financial analysis and modeling to enhance a model’s adaptability to changing market dynamics. This weighting mechanism is particularly advantageous in volatile markets such as Bitcoin futures, as it facilitates quick adaptation to changing market conditions (Black-Scholes, 1973).

Strategy Mechanism:

The BTC Future Gamma-Weighted Momentum Model (BGMM) utilizes an adaptive weighting strategy, where the Bitcoin futures prices are weighted according to the Gamma factor to calculate the Gamma-Weighted Average Price (GWAP). The GWAP is derived as a weighted average of prices over a specific number of periods, with more weight assigned to recent periods. The calculated GWAP serves as a reference value, and trading decisions are based on whether the current market price is above or below this level.

1. Long Position Conditions:

A long position is initiated when the Bitcoin price is above the GWAP and a positive price movement is observed over the last three periods. This indicates that an upward trend is in place, and the market is likely to continue in the direction of the momentum.

2. Short Position Conditions:

A short position is initiated when the Bitcoin price is below the GWAP and a negative price movement is observed over the last three periods. This suggests that a downtrend is occurring, and a continuation of the negative price movement is expected.

Backtesting and Application to Bitcoin Futures:

The model has been tested exclusively on the Bitcoin futures market due to Bitcoin’s high volatility and strong trend behavior. These characteristics make the market particularly suitable for momentum strategies, as strong upward or downward movements are often followed by persistent trends that can be captured by a momentum-based approach.

Backtests of the BGMM on the Bitcoin futures market indicate that the model achieves above-average returns during periods of strong momentum, especially when the Gamma factor is optimized to suit the specific dynamics of the Bitcoin market. The high volatility of Bitcoin, combined with adaptive weighting, allows the model to respond quickly to price changes and maximize trading opportunities.

Scientific Citations and Sources:

• Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65–91.

• Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637–654.

• Fama, E. F., & French, K. R. (1992). The Cross-Section of Expected Stock Returns. The Journal of Finance, 47(2), 427–465.

Customizable BTC Seasonality StrategyThis strategy leverages intraday seasonality effects in Bitcoin, specifically targeting hours of statistically significant returns during periods when traditional financial markets are closed. Padysak and Vojtko (2022) demonstrate that Bitcoin exhibits higher-than-average returns from 21:00 UTC to 23:00 UTC, a period in which all major global exchanges, such as the New York Stock Exchange (NYSE), Tokyo Stock Exchange, and London Stock Exchange, are closed. The absence of competing trading activity from traditional markets during these hours appears to contribute to these statistically significant returns.

The strategy proceeds as follows:

Entry Time: A long position in Bitcoin is opened at a user-specified time, which defaults to 21:00 UTC, aligning with the beginning of the identified high-return window.

Holding Period: The position is held for two hours, capturing the positive returns typically observed during this period.

Exit Time: The position is closed at a user-defined time, defaulting to 23:00 UTC, allowing the strategy to exit as the favorable period concludes.

This simple seasonality strategy aims to achieve a 33% annualized return with a notably reduced volatility of 20.93% and maximum drawdown of -22.45%. The results suggest that investing only during these high-return hours is more stable and less risky than a passive holding strategy (Padysak & Vojtko, 2022).

References

Padysak, M., & Vojtko, R. (2022). Seasonality, Trend-following, and Mean reversion in Bitcoin.

HYE Combo Market [Strategy] (Vwap Mean Reversion + Trend Hunter)In this strategy, I used a combination of trend hunter and vwap mean reversion strategies that I published before.

Trend Hunter Strategy:

Mean Reversion Vwap Strategy:

The results are quite impressive, especially for bitcoin.

While the hodl return for bitcoin was 13419%, the strategy's return in the same period was about 5 times (65000%) of this.

s3.tradingview.com

In this combo strategy, I made some changes to the original settings of the strategies used together and added some more new features.

Trend Hunter Strategy Settings: (Original / Combo)

- Slow Tenkansen Period : 9 / 9

- Slow Kijunsen Period : 26 / 13

- Fast Tenkansen Period : 5 / 3

- Fast Kijunsen Period : 13 / 7

- BB Length : 20 / 20

- BB Stdev : 2 / 2

- TSV Length : 13 / 20

- TSV Ema Length : 7 / 7

* I also added a "vidya moving average" to be used as a confirmation tool to open a long position. (Candle close must be above the vidya line.)

Vwap Mean Reversion Strategy Settings: (Original / Combo)

- Small Vwap : 2 / 8

- Big Vwap : 5 / 10

- Percent Below to Buy : 3 / 2

- RSI Period : 2 / 2

- RSI Ema Period : 5 / 5

- Maximum RSI Level for Buy : 30

* I also added a "mean vwap line" to be used for exits in this part of the strategy. In the original version, when small vwap crossovers big vwap, we close the position, but in this strategy we will wait for the close above the mean vwap.

TIPS AND WARNINGS

1-) The standard settings of this combo strategy is designed and tested with daily timeframe. For lower timeframes, you should change the strategy settings and find the best value for yourself.

2-) Only the mean vwap line is displayed on the graph. For a detailed view, you can delete the "//" marks from the plot codes in the strategy code.

3-) This is a strategy for educational and experimental purposes. It cannot be considered as investment advice. You should be careful and make your own risk assessment when opening real market trades using this strategy.

________________________________________________________

Bu stratejide, daha önce yayınladığım trend avcısı ve vwap ortalamaya geri dönüş stratejilerinin bir kombinasyonunu kullandım.

Sonuçlar özellikle bitcoin için oldukça etkileyici.

Bitcoin için hodl getirisi %13419 iken, stratejinin aynı dönemdeki getirisi bunun yaklaşık 5 katı (%65000) idi.

Bu kombo stratejide, birlikte kullanılan stratejilerin orijinal ayarlarında bazı değişiklikler yaptım ve bazı yeni özellikler ekledim.

Trend Avcısı Strateji Ayarları: (Orijinal / Combo)

- Yavaş Tenkansen Periyodu : 9 / 9

- Yavaş Kijunsen Periyodu : 26 / 13

- Hızlı Tenkansen Periyodu : 5 / 3

- Hızlı Kijunsen Periyodu : 13 / 7

- BB Uzunluğu : 20 / 20

- BB Standart Sapması : 2 / 2

- TSV Uzunluğu : 13 / 20

- TSV Ema Uzunluğu : 7 / 7

* Ayrıca long pozisyon açmak için onay aracı olarak kullanılmak üzere "vidya hareketli ortalama" ekledim. (Mum kapanışı vidya çizgisinin üzerinde olmalıdır.)

Vwap Ortalamaya Dönüş Stratejisi Ayarları: (Orijinal / Combo)

- Küçük Vwap : 2 / 8

- Büyük Vwap : 5 / 10

- Alış İçin Gerekli Fark Oranı : 3 / 2

- RSI Periyodu : 2 / 2

- RSI Ema Periyodu: 5 / 5

- Alış için gerekli maksimum RSI seviyesi : 30

* Stratejinin bu bölümünde pozisyondan çıkışlar için kullanılacak bir "ortalama vwap çizgisi" de ekledim. Orijinal versiyonda, küçük vwap, büyük vwap'ı yukarı kestiğinde pozisyonu kapatıyoruz, ancak bu stratejide, ortalama vwap'ın üzerindeki kapanışı bekleyeceğiz.

İPUÇLARI VE UYARILAR

1-) Bu birleşik stratejinin standart ayarları, günlük zaman dilimi ile tasarlanmış ve test edilmiştir. Daha düşük zaman dilimleri için strateji ayarlarını değiştirmeli ve kendiniz için en iyi değeri bulmalısınız.

2-) Grafikte sadece ortalama vwap çizgisi görüntülenir. Ayrıntılı bir görünüm için strateji kodundaki "plot" ile başlayan satırlarda grafikte görünmesini istediğiniz özelliğin önündeki "//" işaretlerini silebilirsiniz.

3-) Eğitim ve deneysel amaçlı bir stratejidir. Yatırım tavsiyesi olarak değerlendirilemez. Bu stratejiyi kullanarak gerçek piyasa işlem açarken dikkatli olmalı ve kendi risk değerlendirmenizi yapmalısınız.

888 BOT #backtest█ 888 BOT #backtest (open source)

This is an Expert Advisor 'EA' or Automated trading script for ‘longs’ and ‘shorts’, which uses only a Take Profit or, in the worst case, a Stop Loss to close the trade.

It's a much improved version of the previous ‘Repanocha’. It doesn`t use 'Trailing Stop' or 'security()' functions (although using a security function doesn`t mean that the script repaints) and all signals are confirmed, therefore the script doesn`t repaint in alert mode and is accurate in backtest mode.

Apart from the previous indicators, some more and other functions have been added for Stop-Loss, re-entry and leverage.

It uses 8 indicators, (many of you already know what they are, but in case there is someone new), these are the following:

1. Jurik Moving Average

It's a moving average created by Mark Jurik for professionals which eliminates the 'lag' or delay of the signal. It's better than other moving averages like EMA , DEMA , AMA or T3.

There are two ways to decrease noise using JMA . Increasing the 'LENGTH' parameter will cause JMA to move more slowly and therefore reduce noise at the expense of adding 'lag'

The 'JMA LENGTH', 'PHASE' and 'POWER' parameters offer a way to select the optimal balance between 'lag' and over boost.

Green: Bullish , Red: Bearish .

2. Range filter

Created by Donovan Wall, its function is to filter or eliminate noise and to better determine the price trend in the short term.

First, a uniform average price range 'SAMPLING PERIOD' is calculated for the filter base and multiplied by a specific quantity 'RANGE MULTIPLIER'.

The filter is then calculated by adjusting price movements that do not exceed the specified range.

Finally, the target ranges are plotted to show the prices that will trigger the filter movement.

Green: Bullish , Red: Bearish .

3. Average Directional Index ( ADX Classic) and ( ADX Masanakamura)

It's an indicator designed by Welles Wilder to measure the strength and direction of the market trend. The price movement is strong when the ADX has a positive slope and is above a certain minimum level 'ADX THRESHOLD' and for a given period 'ADX LENGTH'.

The green color of the bars indicates that the trend is bullish and that the ADX is above the level established by the threshold.

The red color of the bars indicates that the trend is down and that the ADX is above the threshold level.

The orange color of the bars indicates that the price is not strong and will surely lateralize.

You can choose between the classic option and the one created by a certain 'Masanakamura'. The main difference between the two is that in the first it uses RMA () and in the second SMA () in its calculation.

4. Parabolic SAR

This indicator, also created by Welles Wilder, places points that help define a trend. The Parabolic SAR can follow the price above or below, the peculiarity that it offers is that when the price touches the indicator, it jumps to the other side of the price (if the Parabolic SAR was below the price it jumps up and vice versa) to a distance predetermined by the indicator. At this time the indicator continues to follow the price, reducing the distance with each candle until it is finally touched again by the price and the process starts again. This procedure explains the name of the indicator: the Parabolic SAR follows the price generating a characteristic parabolic shape, when the price touches it, stops and turns ( SAR is the acronym for 'stop and reverse'), giving rise to a new cycle. When the points are below the price, the trend is up, while the points above the price indicate a downward trend.

5. RSI with Volume

This indicator was created by LazyBear from the popular RSI .

The RSI is an oscillator-type indicator used in technical analysis and also created by Welles Wilder that shows the strength of the price by comparing individual movements up or down in successive closing prices.

LazyBear added a volume parameter that makes it more accurate to the market movement.

A good way to use RSI is by considering the 50 'RSI CENTER LINE' centerline. When the oscillator is above, the trend is bullish and when it is below, the trend is bearish .

6. Moving Average Convergence Divergence ( MACD ) and ( MAC-Z )

It was created by Gerald Appel. Subsequently, the histogram was added to anticipate the crossing of MA. Broadly speaking, we can say that the MACD is an oscillator consisting of two moving averages that rotate around the zero line. The MACD line is the difference between a short moving average 'MACD FAST MA LENGTH' and a long moving average 'MACD SLOW MA LENGTH'. It's an indicator that allows us to have a reference on the trend of the asset on which it is operating, thus generating market entry and exit signals.

We can talk about a bull market when the MACD histogram is above the zero line, along with the signal line, while we are talking about a bear market when the MACD histogram is below the zero line.

There is the option of using the MAC-Z indicator created by LazyBear, which according to its author is more effective, by using the parameter VWAP ( volume weighted average price ) 'Z-VWAP LENGTH' together with a standard deviation 'STDEV LENGTH' in its calculation.

7. Volume Condition

Volume indicates the number of participants in this war between bulls and bears, the more volume the more likely the price will move in favor of the trend. A low trading volume indicates a lower number of participants and interest in the instrument in question. Low volumes may reveal weakness behind a price movement.

With this condition, those signals whose volume is less than the volume SMA for a period 'SMA VOLUME LENGTH' multiplied by a factor 'VOLUME FACTOR' are filtered. In addition, it determines the leverage used, the more volume , the more participants, the more probability that the price will move in our favor, that is, we can use more leverage. The leverage in this script is determined by how many times the volume is above the SMA line.

The maximum leverage is 8.

8. Bollinger Bands

This indicator was created by John Bollinger and consists of three bands that are drawn superimposed on the price evolution graph.

The central band is a moving average, normally a simple moving average calculated with 20 periods is used. ('BB LENGTH' Number of periods of the moving average)

The upper band is calculated by adding the value of the simple moving average X times the standard deviation of the moving average. ('BB MULTIPLIER' Number of times the standard deviation of the moving average)

The lower band is calculated by subtracting the simple moving average X times the standard deviation of the moving average.

the band between the upper and lower bands contains, statistically, almost 90% of the possible price variations, which means that any movement of the price outside the bands has special relevance.

In practical terms, Bollinger bands behave as if they were an elastic band so that, if the price touches them, it has a high probability of bouncing.

Sometimes, after the entry order is filled, the price is returned to the opposite side. If price touch the Bollinger band in the same previous conditions, another order is filled in the same direction of the position to improve the average entry price, (% MINIMUM BETTER PRICE ': Minimum price for the re-entry to be executed and that is better than the price of the previous position in a given %) in this way we give the trade a chance that the Take Profit is executed before. The downside is that the position is doubled in size. 'ACTIVATE DIVIDE TP': Divide the size of the TP in half. More probability of the trade closing but less profit.

█ STOP LOSS and RISK MANAGEMENT.

A good risk management is what can make your equity go up or be liquidated.

The % risk is the percentage of our capital that we are willing to lose by operation. This is recommended to be between 1-5%.

% Risk: (% Stop Loss x % Equity per trade x Leverage) / 100

First the strategy is calculated with Stop Loss, then the risk per operation is determined and from there, the amount per operation is calculated and not vice versa.

In this script you can use a normal Stop Loss or one according to the ATR. Also activate the option to trigger it earlier if the risk percentage is reached. '% RISK ALLOWED'

'STOP LOSS CONFIRMED': The Stop Loss is only activated if the closing of the previous bar is in the loss limit condition. It's useful to prevent the SL from triggering when they do a ‘pump’ to sweep Stops and then return the price to the previous state.

█ BACKTEST

The objective of the Backtest is to evaluate the effectiveness of our strategy. A good Backtest is determined by some parameters such as:

- RECOVERY FACTOR: It consists of dividing the 'net profit' by the 'drawdown’. An excellent trading system has a recovery factor of 10 or more; that is, it generates 10 times more net profit than drawdown.

- PROFIT FACTOR: The ‘Profit Factor’ is another popular measure of system performance. It's as simple as dividing what win trades earn by what loser trades lose. If the strategy is profitable then by definition the 'Profit Factor' is going to be greater than 1. Strategies that are not profitable produce profit factors less than one. A good system has a profit factor of 2 or more. The good thing about the ‘Profit Factor’ is that it tells us what we are going to earn for each dollar we lose. A profit factor of 2.5 tells us that for every dollar we lose operating we will earn 2.5.

- SHARPE: (Return system - Return without risk) / Deviation of returns.

When the variations of gains and losses are very high, the deviation is very high and that leads to a very poor ‘Sharpe’ ratio. If the operations are very close to the average (little deviation) the result is a fairly high 'Sharpe' ratio. If a strategy has a 'Sharpe' ratio greater than 1 it is a good strategy. If it has a 'Sharpe' ratio greater than 2, it is excellent. If it has a ‘Sharpe’ ratio less than 1 then we don't know if it is good or bad, we have to look at other parameters.

- MATHEMATICAL EXPECTATION: (% winning trades X average profit) + (% losing trades X average loss).

To earn money with a Trading system, it is not necessary to win all the operations, what is really important is the final result of the operation. A Trading system has to have positive mathematical expectation as is the case with this script: ME = (0.87 x 30.74$) - (0.13 x 56.16$) = (26.74 - 7.30) = 19.44$ > 0

The game of roulette, for example, has negative mathematical expectation for the player, it can have positive winning streaks, but in the long term, if you continue playing you will end up losing, and casinos know this very well.

PARAMETERS

'BACKTEST DAYS': Number of days back of historical data for the calculation of the Backtest.

'ENTRY TYPE': For '% EQUITY' if you have $ 10,000 of capital and select 7.5%, for example, your entry would be $ 750 without leverage. If you select CONTRACTS for the 'BTCUSDT' pair, for example, it would be the amount in 'Bitcoins' and if you select 'CASH' it would be the amount in $ dollars.

'QUANTITY (LEVERAGE 1X)': The amount for an entry with X1 leverage according to the previous section.

'MAXIMUM LEVERAGE': It's the maximum allowed multiplier of the quantity entered in the previous section according to the volume condition.

The settings are for Bitcoin at Binance Futures (BTC: USDTPERP) in 15 minutes.

For other pairs and other timeframes, the settings have to be adjusted again. And within a month, the settings will be different because we all know the market and the trend are changing.

[Prod] SuperTrend with Stoploss+TrendZones - 1HHere, i'm using a SuperTrend (difference of moving averages) crossover strategy hybrid with stop-loss and trend-following to look at backtesting for the BCHUSD pair on the coinbase (GDAX) exchange.

Included in this script I've got some optimized parameters that seem to make a decent profit over ~35+ trades. The one thing that's bothering me here is that I get OCCASIONAL repaint issues with back-testing, but I can't figure out why for the life of me, because i'm using V3 in the start of the script. If someone could point out the mistake I may be making here , I feel like this could be a serious strategy to use against the BCHUSD pair on coinbase or other exchanges (with tuning of course).

I based this script off of with lots of modifications.

BTC Fear & Greed Incremental StrategyIMPORTANT: READ SETUP GUIDE BELOW OR IT WON'T WORK

# BTC Fear & Greed Incremental Strategy — TradeMaster AI (Pure BTC Stack)

## Strategy Overview

This advanced Bitcoin accumulation strategy is designed for long-term hodlers who want to systematically take profits during greed cycles and accumulate during fear periods, while preserving their core BTC position. Unlike traditional strategies that start with cash, this approach begins with a specified BTC allocation, making it perfect for existing Bitcoin holders who want to optimize their stack management.

## Key Features

### 🎯 **Pure BTC Stack Mode**

- Start with any amount of BTC (configurable)

- Strategy manages your existing stack, not new purchases

- Perfect for hodlers who want to optimize without timing markets

### 📊 **Fear & Greed Integration**

- Uses market sentiment data to drive buy/sell decisions

- Configurable thresholds for greed (selling) and fear (buying) triggers

- Automatic validation to ensure proper 0-100 scale data source

### 🐂 **Bull Year Optimization**

- Smart quarterly selling during bull market years (2017, 2021, 2025)

- Q1: 1% sells, Q2: 2% sells, Q3/Q4: 5% sells (configurable)

- **NO SELLING** during non-bull years - pure accumulation mode

- Preserves BTC during early bull phases, maximizes profits at peaks

### 🐻 **Bear Market Intelligence**

- Multi-regime detection: Bull, Early Bear, Deep Bear, Early Bull

- Different buying strategies based on market conditions

- Enhanced buying during deep bear markets with configurable multipliers

- Visual regime backgrounds for easy market condition identification

### 🛡️ **Risk Management**

- Minimum BTC allocation floor (prevents selling entire stack)

- Configurable position sizing for all trades

- Multiple safety checks and validation

### 📈 **Advanced Visualization**

- Clean 0-100 scale with 2 decimal precision

- Three main indicators: BTC Allocation %, Fear & Greed Index, BTC Holdings

- Real-time portfolio tracking with cash position display

- Enhanced info table showing all key metrics

## How to Use

### **Step 1: Setup**

1. Add the strategy to your BTC/USD chart (daily timeframe recommended)

2. **CRITICAL**: In settings, change the "Fear & Greed Source" from "close" to a proper 0-100 Fear & Greed indicator

---------------

I recommend Crypto Fear & Greed Index by TIA_Technology indicator

When selecting source with this indicator, look for "Crypto Fear and Greed Index:Index"

---------------

3. Set your "Starting BTC Quantity" to match your actual holdings

4. Configure your preferred "Start Date" (when you want the strategy to begin)

### **Step 2: Configure Bull Year Logic**

- Enable "Bull Year Logic" (default: enabled)

- Adjust quarterly sell percentages:

- Q1 (Jan-Mar): 1% (conservative early bull)

- Q2 (Apr-Jun): 2% (moderate mid bull)

- Q3/Q4 (Jul-Dec): 5% (aggressive peak targeting)

- Add future bull years to the list as needed

### **Step 3: Fine-tune Thresholds**

- **Greed Threshold**: 80 (sell when F&G > 80)

- **Fear Threshold**: 20 (buy when F&G < 20 in bull markets)

- **Deep Bear Fear Threshold**: 25 (enhanced buying in bear markets)

- Adjust based on your risk tolerance

### **Step 4: Risk Management**

- Set "Minimum BTC Allocation %" (default 20%) - prevents selling entire stack

- Configure sell/buy percentages based on your position size

- Enable bear market filters for enhanced timing

### **Step 5: Monitor Performance**

- **Orange Line**: Your BTC allocation percentage (target: fluctuate between 20-100%)

- **Blue Line**: Actual BTC holdings (should preserve core position)

- **Pink Line**: Fear & Greed Index (drives all decisions)

- **Table**: Real-time portfolio metrics including cash position

## Reading the Indicators

### **BTC Allocation Percentage (Orange Line)**

- **100%**: All portfolio in BTC, no cash available for buying

- **80%**: 80% BTC, 20% cash ready for fear buying

- **20%**: Minimum allocation, maximum cash position

### **Trading Signals**

- **Green Buy Signals**: Appear during fear periods with available cash

- **Red Sell Signals**: Appear during greed periods in bull years only

- **No Signals**: Either allocation limits reached or non-bull year

## Strategy Logic

### **Bull Years (2017, 2021, 2025)**

- Q1: Conservative 1% sells (preserve stack for later)

- Q2: Moderate 2% sells (gradual profit taking)

- Q3/Q4: Aggressive 5% sells (peak targeting)

- Fear buying active (accumulate on dips)

### **Non-Bull Years**

- **Zero selling** - pure accumulation mode

- Enhanced fear buying during bear markets

- Focus on rebuilding stack for next bull cycle

## Important Notes

- **This is not financial advice** - backtest thoroughly before use

- Designed for **long-term holders** (4+ year cycles)

- **Requires proper Fear & Greed data source** - validate in settings

- Best used on **daily timeframe** for major trend following

- **Cash calculations**: Use allocation % and BTC holdings to calculate available cash: `Cash = (Total Portfolio × (1 - Allocation%/100))`

## Risk Disclaimer

This strategy involves active trading and position management. Past performance does not guarantee future results. Always do your own research and never invest more than you can afford to lose. The strategy is designed for educational purposes and long-term Bitcoin accumulation thesis.

---

*Developed by Sol_Crypto for the Bitcoin community. Happy stacking! 🚀*

BTC EMA 5-9 Flip Strategy AutobotThis strategy is designed for fast and accurate trend-following trades on Bitcoin.

It uses a crossover between EMA 5 and EMA 9 to detect instant trend reversals and automatically flips between Long and Short positions.

How the strategy works

EMA 5 crossing above EMA 9 → Long

EMA 5 crossing below EMA 9 → Short

Automatically closes the opposite trade during a flip

Executes trades only on candle close

Prevents double entries with internal position-state logic

Fully compatible with automated trading via webhooks (Delta Exchange)

Why this strategy works

EMA 5–9 is extremely responsive for BTC’s volatility

Captures trend reversals early

Works best on 15-minute timeframe

Clean, simple logic without over-filtering reduces missed opportunities

Performs well in both uptrends and downtrends

Automation Ready

This strategy includes alert conditions and webhook-ready JSON for automated execution.

This is a fast-reacting BTC bot designed for intraday and swing crypto trend trading.

Quantum Reversal# 🧠 Quantum Reversal

## **Quantitative Mean Reversion Framework**

This algorithmic trading system employs **statistical mean reversion theory** combined with **adaptive volatility modeling** to capitalize on Bitcoin's inherent price oscillations around its statistical mean. The strategy integrates multiple technical indicators through a **multi-layered signal processing architecture**.

---

## ⚡ **Core Technical Architecture**

### 📊 **Statistical Foundation**

- **Bollinger Band Mean Reversion Model**: Utilizes 20-period moving average with 2.2 standard deviation bands for volatility-adjusted entry signals

- **Adaptive Volatility Threshold**: Dynamic standard deviation multiplier accounts for Bitcoin's heteroscedastic volatility patterns

- **Price Action Confluence**: Entry triggered when price breaches lower volatility band, indicating statistical oversold conditions

### 🔬 **Momentum Analysis Layer**

- **RSI Oscillator Integration**: 14-period Relative Strength Index with modified oversold threshold at 45

- **Signal Smoothing Algorithm**: 5-period simple moving average applied to RSI reduces noise and false signals

- **Momentum Divergence Detection**: Captures mean reversion opportunities when momentum indicators show oversold readings

### ⚙️ **Entry Logic Architecture**

```

Entry Condition = (Price ≤ Lower_BB) OR (Smoothed_RSI < 45)

```

- **Dual-Condition Framework**: Either statistical price deviation OR momentum oversold condition triggers entry

- **Boolean Logic Gate**: OR-based entry system increases signal frequency while maintaining statistical validity

- **Position Sizing**: Fixed 10% equity allocation per trade for consistent risk exposure

### 🎯 **Exit Strategy Optimization**

- **Profit-Lock Mechanism**: Positions only closed when showing positive unrealized P&L

- **Trend Continuation Logic**: Allows winning trades to run until momentum exhaustion

- **Dynamic Exit Timing**: No fixed profit targets - exits based on profitability state rather than arbitrary levels

---

## 📈 **Statistical Properties**

### **Risk Management Framework**

- **Long-Only Exposure**: Eliminates short-squeeze risk inherent in cryptocurrency markets

- **Mean Reversion Bias**: Exploits Bitcoin's tendency to revert to statistical mean after extreme moves

- **Position Management**: Single position limit prevents over-leveraging

### **Signal Processing Characteristics**

- **Noise Reduction**: SMA smoothing on RSI eliminates high-frequency oscillations

- **Volatility Adaptation**: Bollinger Bands automatically adjust to changing market volatility

- **Multi-Timeframe Coherence**: Indicators operate on consistent timeframe for signal alignment

---

## 🔧 **Parameter Configuration**

| Technical Parameter | Value | Statistical Significance |

|-------------------|-------|-------------------------|

| Bollinger Period | 20 | Standard statistical lookback for volatility calculation |

| Std Dev Multiplier | 2.2 | Optimized for Bitcoin's volatility distribution (95.4% confidence interval) |

| RSI Period | 14 | Traditional momentum oscillator period |

| RSI Threshold | 45 | Modified oversold level accounting for Bitcoin's momentum characteristics |

| Smoothing Period | 5 | Noise reduction filter for momentum signals |

---

## 📊 **Algorithmic Advantages**

✅ **Statistical Edge**: Exploits documented mean reversion tendency in Bitcoin markets

✅ **Volatility Adaptation**: Dynamic bands adjust to changing market conditions

✅ **Signal Confluence**: Multiple indicator confirmation reduces false positives

✅ **Momentum Integration**: RSI smoothing improves signal quality and timing

✅ **Risk-Controlled Exposure**: Systematic position sizing and long-only bias

---

## 🔬 **Mathematical Foundation**

The strategy leverages **Bollinger Band theory** (developed by John Bollinger) which assumes that prices tend to revert to the mean after extreme deviations. The RSI component adds **momentum confirmation** to the statistical price deviation signal.

**Statistical Basis:**

- Mean reversion follows the principle that extreme price deviations from the moving average are temporary

- The 2.2 standard deviation multiplier captures approximately 97.2% of price movements under normal distribution

- RSI momentum smoothing reduces noise inherent in oscillator calculations

---

## ⚠️ **Risk Considerations**

This algorithm is designed for traders with understanding of **quantitative finance principles** and **cryptocurrency market dynamics**. The strategy assumes mean-reverting behavior which may not persist during trending market phases. Proper risk management and position sizing are essential.

---

## 🎯 **Implementation Notes**

- **Market Regime Awareness**: Most effective in ranging/consolidating markets

- **Volatility Sensitivity**: Performance may vary during extreme volatility events

- **Backtesting Recommended**: Historical performance analysis advised before live implementation

- **Capital Allocation**: 10% per trade sizing assumes diversified portfolio approach

---

**Engineered for quantitative traders seeking systematic mean reversion exposure in Bitcoin markets through statistically-grounded technical analysis.**

Multi-EMA Crossover StrategyMulti-EMA Crossover Strategy

This strategy uses multiple exponential moving average (EMA) crossovers to identify bullish trends and execute long trades. The approach involves progressively stronger signals as different EMA pairs cross, indicating increasing bullish momentum. Each crossover triggers a long entry, and the intensity of bullish sentiment is reflected in the color of the bars on the chart. Conversely, bearish trends are represented by red bars.

Strategy Logic:

First Long Entry: When the 1-day EMA crosses above the 5-day EMA, it signals initial bullish momentum.

Second Long Entry: When the 3-day EMA crosses above the 10-day EMA, it confirms stronger bullish sentiment.

Third Long Entry: When the 5-day EMA crosses above the 20-day EMA, it indicates further trend strength.

Fourth Long Entry: When the 10-day EMA crosses above the 40-day EMA, it suggests robust long-term bullish momentum.

The bar colors reflect these conditions:

More blue bars indicate stronger bullish sentiment as more short-term EMAs are above their longer-term counterparts.

Red bars represent bearish conditions when short-term EMAs are below longer-term ones.

Example: Bitcoin Trading on a Daily Timeframe

Bullish Scenario:

Imagine Bitcoin is trading at $30,000 on March 31, 2025:

First Signal: The 1-day EMA crosses above the 5-day EMA at $30,000. This suggests initial upward momentum, prompting a small long entry.

Second Signal: A few days later, the 3-day EMA crosses above the 10-day EMA at $31,000. This confirms strengthening bullish sentiment; another long position is added.

Third Signal: The 5-day EMA crosses above the 20-day EMA at $32,500, indicating further upward trend development; a third long entry is executed.

Fourth Signal: Finally, the 10-day EMA crosses above the 40-day EMA at $34,000. This signals robust long-term bullish momentum; a fourth long position is entered.

Bearish Scenario:

Suppose Bitcoin reverses from $34,000 to $28,000:

The 1-day EMA crosses below the 5-day EMA at $33,500.

The 3-day EMA dips below the 10-day EMA at $32,000.

The 5-day EMA falls below the 20-day EMA at $30,000.

The final bearish signal occurs when the 10-day EMA drops below the 40-day EMA at $28,000.

The bars turn increasingly red as bearish conditions strengthen.

Advantages of This Strategy:

Progressive Confirmation: Multiple crossovers provide layered confirmation of trend strength.

Visual Feedback: Bar colors help traders quickly assess market sentiment and adjust positions accordingly.

Flexibility: Suitable for trending markets like Bitcoin during strong rallies or downturns.

Limitations:

Lagging Signals: EMAs are lagging indicators and may react slowly to sudden price changes.

False Breakouts: Crossovers in choppy markets can lead to whipsaws or false signals.

This strategy works best in trending markets and should be combined with additional risk management techniques, e.g., stop loss or optimal position sizes (Kelly Criterion).

Bot for Spot Market - Custom GridThis script is designed to create a trading bot for the spot market, specifically for buying and selling bitcoins profitably. Recommended for timeframes above two hours. Here are the main functions and features of the script:

Strategy Setup: The bot is set up with a custom grid strategy, defining parameters like pyramiding (allowed number of simultaneous trades), margin requirements, commission, and initial capital.

Order Requirements: It calculates the order price and amount based on the minimum requirements set by the exchange and rounds them appropriately.

Entry Conditions: The bot makes new entries if the closing price falls a certain percentage below the last entry price. It continues to make entries until the closing price rises a certain percentage above the average entry price.

Targets and Plots:

It calculates and plots the target profit level.

It plots the average entry price and the last entry price.

It plots the next entry price based on the defined conditions.

It plots the maximum number of orders allowed based on equity and the number of open orders.

Timerange: The bot can start trading from a specific date and time defined by the user.

Entries: It places orders if the timerange conditions are met. It also places new orders if the closing price is below the last entry price by a defined percentage.

Profit Calculation: The script calculates open profit or loss for the open positions.

Exit Conditions: It closes all positions if the open profit is positive and the closing price is above the target profit level.

Performance Table: The bot maintains and displays statistics like the number of open and closed trades, net profit, and equity in a table format.

The script is customizable, allowing users to adjust parameters like initial capital, commission, order values, and profit targets to fit their specific trading needs and exchange requirements.

Black-Scholes option price model & delta hedge strategyBlack-Scholes Option Pricing Model Strategy

The strategy is based on the Black-Scholes option pricing model and allows the calculation of option prices, various option metrics (the Greeks), and the creation of synthetic positions through delta hedging.

ATTENTION!

Trading derivative financial instruments involves high risks. The author of the strategy is not responsible for your financial results! The strategy is not self-sufficient for generating profit! It is created exclusively for constructing a synthetic derivative financial instrument. Also, there might be errors in the script, so use it at your own risk! I would appreciate it if you point out any mistakes in the comments! I would be even more grateful if you send the corrected code!

Application Scope

This strategy can be used for delta hedging short positions in sold options. For example, suppose you sold a call option on Bitcoin on the Deribit exchange with a strike price of $60,000 and an expiration date of September 27, 2024. Using this script, you can create a delta hedge to protect against the risk of loss in the option position if the price of Bitcoin rises.

Another example: Suppose you use staking of altcoins in your strategies, for which options are not available. By using this strategy, you can hedge the risk of a price drop (Put option). In this case, you won't lose money if the underlying asset price increases, unlike with a short futures position.

Another example: You received an airdrop, but your tokens will not be fully unlocked soon. Using this script, you can fully hedge your position and preserve their dollar value by the time the tokens are fully unlocked. And you won't fear the underlying asset price increasing, as the loss in the event of a price rise is limited to the option premium you will pay if you rebalance the portfolio.

Of course, this script can also be used for simple directional trading of momentum and mean reversion strategies!

Key Features and Input Parameters

1. Option settings:

- Style of option: "European vanilla", "Binary", "Asian geometric".

- Type of option: "Call" (bet on the rise) or "Put" (bet on the fall).

- Strike price: the option contract price.

- Expiration: the expiry date and time of the option contract.

2. Market statistic settings:

- Type of price source: open, high, low, close, hl2, hlc3, ohlc4, hlcc4 (using hl2, hlc3, ohlc4, hlcc4 allows smoothing the price in more volatile series).

- Risk-free return symbol: the risk-free rate for the market where the underlying asset is traded. For the cryptocurrency market, the return on the funding rate arbitrage strategy is accepted (a special function is written for its calculation based on the Premium Price).

- Volatility calculation model: realized (standard deviation over a moving period), implied (e.g., DVOL or VIX), or custom (you can specify a specific number in the field below). For the cryptocurrency market, the calculation of implied volatility is implemented based on the product of the realized volatility ratio of the considered asset and Bitcoin to the Bitcoin implied volatility index.

- User implied volatility: fixed implied volatility (used if "Custom" is selected in the "Volatility Calculation Method").

3. Display settings:

- Choose metric: what to display on the indicator scale – the price of the underlying asset, the option price, volatility, or Greeks (all are available).

- Measure: bps (basis points), percent. This parameter allows choosing the unit of measurement for the displayed metric (for all except the Greeks).

4. Trading settings:

- Hedge model: None (do not trade, default), Simple (just open a position for the full volume when the strike price is crossed), Synthetic option (creating a synthetic option based on the Black-Scholes model).

- Position side: Long, Short.

- Position size: the number of units of the underlying asset needed to create the option.

- Strategy start time: the moment in time after which the strategy will start working to create a synthetic option.

- Delta hedge interval: the interval in minutes for rebalancing the portfolio. For example, a value of 5 corresponds to rebalancing the portfolio every 5 minutes.

Post scriptum

My strategy based on the SegaRKO model. Many thanks to the author! Unfortunately, I don't have enough reputation points to include a link to the author in the description. You can find the original model via the link in the code, as well as through the search indicators on the charts by entering the name: "Black-Scholes Option Pricing Model". I have significantly improved the model: the calculation of volatility, risk-free rate and time value of the option have been reworked. The code performance has also been significantly optimized. And the most significant change is the execution, with which you can now trade using this script.

Innocent Heikin Ashi Ethereum StrategyHello there, im back!

If you are familiar with my previous scripts, this one will seem like the future's nostalgia!

Functionality:

As you can see, all candles are randomly colored. This has no deeper meaning, it should remind you to switch to Heikin Ashi. The Strategy works on standard candle stick charts, but should be used with Heikin Ashi to see the actual results. (Regular OHLC calculations are included.)

Same as in my previous scripts we import our PVSRA Data from @TradersReality open source Indicator.

With this data and the help of moving averages, we have got an edge in the market.

Signal Logic:

When a "violently green" candle appears (high buy volume + tick speed) above the 50 EMA indicates a change in trend and sudden higher prices. Depending on OHLC of the candle itself and volume, Take Profit and Stop Loss is calculated. (The price margin is the only adjustable setting). Additionally, to make this script as simple and easily useable as possible, all other adjustable variables have been already set to the best suitable value and the chart was kept plain, except for the actual entries and exits.

Basic Settings and Adjustables:

Main Input 1: TP and SL combined price range. (Double, Triple R:R equally.)

Trade Inputs: All standard trade size and contract settings for testing available.

Special Settings:

Checkbox 1: Calculate Signal in Heikin Ashi chart, including regular candle OHLC („Open, High, Low, Close“)

Checkbox 2/3: Calculate by order fill or every tick.

Checkbox 4: Possible to fill orders on bar close.

Timeframe and practical usage:

Made for the 5 Minute to 1 hour timeframe.

Literally ONLY works on Ethereum and more or less on Bitcoin.

EVERY other asset has absolute 0% profitability.

Have fun and share with your friends!

Thanks for using!

Example Chart:

YinYang RSI Volume Trend StrategyThere are many strategies that use RSI or Volume but very few that take advantage of how useful and important the two of them combined are. This strategy uses the Highs and Lows with Volume and RSI weighted calculations on top of them. You may be wondering how much of an impact Volume and RSI can have on the prices; the answer is a lot and we will discuss those with plenty of examples below, but first…

How does this strategy work?

It’s simple really, when the purchase source crosses above the inner low band (red) it creates a Buy or Long. This long has a Trailing Stop Loss band (the outer low band that's also red) that can be adjusted in the Settings. The Stop Loss is based on a % of the inner low band’s price and by default it is 0.1% lower than the inner band’s price. This Stop Loss is not only a stop loss but it can also act as a Purchase Available location.

You can get back into a trade after a stop loss / take profit has been hit when your Reset Purchase Availability After condition has been met. This can either be at Stop Loss, Entry or None.

It is advised to allow it to reset in case the stop loss was a fake out but the call was right. Sometimes it may trigger stop loss multiple times in a row, but you don’t lose much on stop loss and you gain lots when the call is right.

The Take Profit location is the basis line (white). Take Profit occurs when the Exit Source (close, open, high, low or other) crosses the basis line and then on a different bar the Exit Source crosses back over the basis line. For example, if it was a Long and the bar’s Exit Source closed above the basis line, and then 2 bars later its Exit Source closed below the basis line, Take Profit would occur. You can disable Take Profit in Settings, but it is very useful as many times the price will cross the Basis and then correct back rather than making it all the way to the opposing zone.

Longs:

If for instance your Long doesn’t need to Take Profit and instead reaches the top zone, it will close the position when it crosses above the inner top line (green).

Please note you can change the Exit Source too which is what source (close, open, high, low) it uses to end the trades.

The Shorts work the same way as the Long but just opposite, they start when the purchase source crosses under the inner upper band (green).

Shorts:

Shorts take profit when it crosses under the basis line and then crosses back.

Shorts will Stop loss when their outer upper band (green) is crossed with the Exit Source.

Short trades are completed and closed when its Exit Source crosses under the inner low red band.

So, now that you understand how the strategy works, let’s discuss why this strategy works and how it is profitable.

First we will discuss Volume as we deem it plays a much bigger role overall and in our strategy:

As I’m sure many of you know, Volume plays a huge factor in how much something moves, but it also plays a role in the strength of the movement. For instance, let’s look at two scenarios:

Bitcoin’s price goes up $1000 in 1 Day but the Volume was only 10 million

Bitcoin’s price goes up $200 in 1 Day but the Volume was 40 million

If you were to only look at the price, you’d say #1 was more important because the price moved x5 the amount as #2, but once you factor in the volume, you know this is not true. The reason why Volume plays such a huge role in Price movement is because it shows there is a large Limit Order battle going on. It means that both Bears and Bulls believe that price is a good time to Buy and Sell. This creates a strong Support and Resistance price point in this location. If we look at scenario #2, when there is high volume, especially if it is drastically larger than the average volume Bitcoin was displaying recently, what can we decipher from this? Well, the biggest take away is that the Bull’s won the battle, and that likely when that happens we will see bullish movement continuing to happen as most of the Bears Limit Orders have been fulfilled. Whereas with #2, when large price movement happens and Bitcoin goes up $1000 with low volume what can we deduce? The main takeaway is that Bull’s pressured the price up with Market Orders where they purchased the best available price, also what this means is there were very few people who were wanting to sell. This generally dictates that Whale Limit orders for Sells/Shorts are much higher up and theres room for movement, but it also means there is likely a whale that is ready to dump and crash it back down.

You may be wondering, what did this example have to do with YinYang RSI Volume Trend Strategy? Well the reason we’ve discussed this is because we use Volume multiple times to apply multiplications in our calculations to add large weight to the price when there is lots of volume (this is applied both positively and negatively). For instance, if the price drops a little and there is high volume, our strategy will move its bounds MUCH lower than the price actually dropped, and if there was low volume but the price dropped A LOT, our strategy will only move its bounds a little. We believe this reflects higher levels of price accuracy than just price alone based on the examples described above.

Don’t believe us?

Here is with Volume NOT factored in (VWMA = SMA and we remove our Volume Filter calculation):

Which produced -$2880 Profit

Here is with our Volume factored in:

Which produced $553,000 (55.3%)

As you can see, we wen’t from $-2800 profit with volume not factored to $553,000 with volume factored. That's quite a big difference! (Please note previous success does not predict future success we are simply displaying the $ amounts as example).

Now how about RSI and why does it matter in this strategy?

As I’m sure most of you are aware, RSI is one of the leading indicators used in trading. For this reason we figured it would only make sense to incorporate it into our calculations. We fiddled with RSI for quite awhile and sometimes what logically seems to be the right way to use it isn’t. Now, because of this, our RSI calculation is a little odd, but basically what we’re doing is we calculate the RSI, then turn it into a percentage (between 0-1) that can easily be multiplied to the price point we need. The price point we use is the difference between our high purchase zone and our low purchase zone. This allows us to see how much price movement there is between zones. We multiply our zone size with our RSI multiplication and we get the amount we will add +/- to our basis line (white line). This officially creates the NEW high and low purchase zones that we are actually using and displaying in our trades.

If you found that confusing, here are some examples to why it is an important calculation for this strategy:

Before RSI factored in:

Which produced 27.8% Profit

After RSI factored in:

Which produced 553% Profit

As you can see, the RSI makes not only the purchase zones more accurate, but it also greatly increases the profit the strategy is able to make. It also helps ensure an relatively linear profit slope so you know it is reliable with its trades.

This strategy can work on pretty much anything, but you should tweak the values a bit for each pair you are trading it with for best results.

We hope you can find some use out of this simple but effective strategy, if you have any questions, comments or concerns please let us know.

HAPPY TRADING!

Quantitative Trend Strategy- Uptrend longTrend Strategy #1

Indicators:

1. SMA

2. Pivot high/low functions derived from SMA

3. Step lines to plot support and resistance based on the pivot points

4. If the close is over the resistance line, green arrows plot above, and vice versa for red arrows below support.

Strategy:

1. Long Only

2. Mutable 2% TP/1.5% SL

3. 0.01% commission

4. When the close is greater than the pivot point of the sma pivot high, and the close is greater than the resistance step line, a long position is opened.

*At times, the 2% take profit may not trigger IF; the conditions for reentry are met at the time of candle closure + no exit conditions have been triggered.

5. If the position is in the green and the support step line crosses over the resistance step line, positions are exited.

How to use it and what makes it unique:

Use this strategy to trade an up-trending market using a simple moving average to determine the trend. This strategy is meant to capture a good risk/reward in a bullish market while staying active in an appropriate fashion. This strategy is unique due to it's inclusion of the step line function with statistics derived from myself.

This description tells the indicators combined to create a new strategy, with commissions and take profit/stop loss conditions included, and the process of strategy execution with a description on how to use it. If you have any questions feel free to PM me and boost if you enjoyed it. Thank you, pineUSERS!

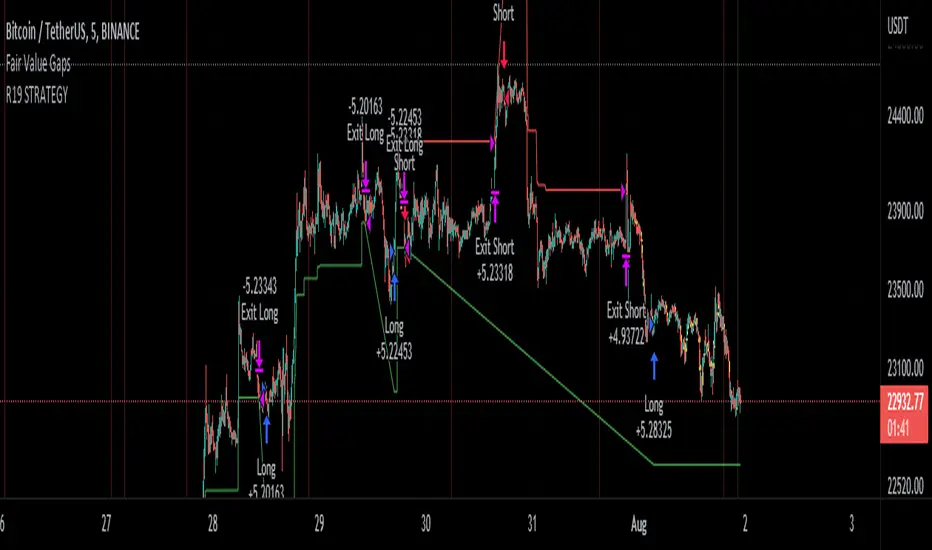

R19 STRATEGYHello again.

Let me introduce you R19 Strategy I wrote for mostly BTC long/short signals

This is an upgrated version of STRATEGY R18 F BTC strategy.

I checked this strategy on different timeframes and different assest and found it very usefull for BTC 1 Hour and 5 minutes chart.

Strategy is basically takes BTC/USDT as a main indicator, so you can apply this strategy to all cryptocurrencies as they mostly acts accordingly with BTC itself (Of course you can change main indicator to different assets if you think that there is a positive corelation with. i.e. for BTC signals you can sellect DXY index for main indicator to act for BTC long/short signals)

Default variables of the inticator is calibrated to BTC/USDT 5 minute chart. I gained above %77 success.

Strategy simply uses, ADX, MACD, SMA, Fibo, RSI combination and opens positions accordingly. Timeframe variable is very important that, strategy decides according the timeframe you've sellected but acts within the timeframe in the chart. For example, if you're on the 5 minutes chart, but you've selected 1 hour for the time frame variable, strategy looks for 1 hour MACD crossover for opening a position, but this happens in 5 minutes candle, It acts quickly and opens the position.

Strategy also uses a trailing stop loss feature. You can determine max stoploss, at which point trailing starts and at which distance trailing follows. The green and red lines will show your stoploss levels according to the position strategy enters (green for long, red for short stop loss levels). When price exceeds to the certaing levels of success, stop loss goes with the profitable price (this means, when strategy opens a position, you can put your stop loss to the green/red line in actual trading)

You can fine tune strategy to all assets.

Please write down your comments if you get more successfull about different time zones and different assets. And please tell me your fine tuning levels of this strategy as well.

See you all.

Cipher B divergencies for Crypto (Finandy support)Hello Traders!

In times of high volatility, it is important to follow a market-neutral strategy to protect your hard-earned assets. The simple script employs common buy/sell and/or divergencies signals from the VuManChu Cipher B indicator with fixed stop losses and takes profits. The signals are filtered by a local trend of a coin of interest and the global trend of Bitcoin. These trends-filtered signals demonstrated better performance on most of the back- and forward- tests for USDT cryptocurrency futures. The strategy is based on my real experience, it's a diamond I want to share with you.

In terms of visualization if the background is red and the price is below the yellow line then only a short position can be opened. Conversely, if the price is above the yellow line AND the background is green only a long position can be opened.

Inputs from VuManChu you can find on the top. Frankly, I do not know how they can help you to improve the performance of the strategy. My inputs of the script you can find in "Trend Settings" and "TP/SL Settings" at the bottom.

The checkbox "Only divergencies" lets to broadcast only more reliable buy/sell signals for a cost of rare deals.

The checkbox "Cancel all positions if price crosses local sma?" makes additional trailing stop loss. Usually, this function increases the win rate by "smoothing" the risk/reward ratio, as a usual stop loss does.

You can tune SL/TP based on backtesting.

To connect the script to Finandy just edit "name" and "secret" to connect your webhook (see the bottom of the script).

The rule of thumb for the strategy is "only divergencies" - ON, high reward/risk (TP/SL) ratio, 5 min timeframe on chart help with performance.

Finally, I am looking forward to feedback from you. If you have some cool features for my script in your mind, do not hesitate to leave them in the comments.

Good luck!